Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - COMPUTER TASK GROUP INC | Financial_Report.xls |

| EX-32 - EX-32 - COMPUTER TASK GROUP INC | d261903dex32.htm |

| EX-23 - EX-23 - COMPUTER TASK GROUP INC | d261903dex23.htm |

| EX-21 - EX-21 - COMPUTER TASK GROUP INC | d261903dex21.htm |

| EX-10.L - EX-10.L - COMPUTER TASK GROUP INC | d261903dex10l.htm |

| EX-31.A - EX-31.A - COMPUTER TASK GROUP INC | d261903dex31a.htm |

| EX-31.B - EX-31.B - COMPUTER TASK GROUP INC | d261903dex31b.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition period from to

Commission File No. 1-9410

COMPUTER TASK GROUP, INCORPORATED

(Exact name of Registrant as specified in its charter)

| New York | 16-0912632 | |

| (State of incorporation) | (I.R.S. Employer Identification No.) | |

| 800 Delaware Avenue, Buffalo, New York | 14209 | |

| (Address of principal executive offices) | (Zip Code) | |

| Registrant’s telephone number, including area code: (716) 882-8000 | ||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $.01 par value |

The NASDAQ Stock Market LLC | |

| Rights to Purchase Series A Participating Preferred Stock |

The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ¨ NO x

The aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates, computed by reference to the price at which the common equity was last sold on the last business day of the registrant’s most recently completed second quarter was $174.3 million. Solely for the purposes of this calculation, all persons who are or may be executive officers or directors of the registrant have been deemed to be affiliates.

The total number of shares of Common Stock of the Registrant outstanding at February 8, 2012 was 18,534,614.

DOCUMENTS INCORPORATED BY REFERENCE

Certain sections of the Company’s definitive proxy statement to be filed with the Securities and Exchange Commission (SEC) within 120 days of the end of the Company’s fiscal year ended December 31, 2011, are incorporated by reference into Part III hereof. Except for those portions specifically incorporated by reference herein, such document shall not be deemed to be filed with the SEC as part of this annual report on Form 10-K.

Table of Contents

Table of Contents

As used in this annual report on Form 10-K, references to “CTG,” “the Company” or “the Registrant” refer to Computer Task Group, Incorporated and its subsidiaries, unless the context suggests otherwise.

PART I

Forward-Looking Statements

This annual report on Form 10-K contains forward-looking statements made by the management of Computer Task Group, Incorporated (“CTG,” “the Company” or “the Registrant”) that are subject to a number of risks and uncertainties. These forward-looking statements are based on information as of the date of this report. The Company assumes no obligation to update these statements based on information from and after the date of this report. Generally, forward-looking statements include words or phrases such as “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “projects,” “could,” “may,” “might,” “should,” “will” and words and phrases of similar impact. The forward-looking statements include, but are not limited to, statements regarding future operations, industry trends or conditions and the business environment, and statements regarding future levels of, or trends in, revenue, operating expenses, capital expenditures, and financing. The forward-looking statements are made pursuant to safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Numerous factors could cause actual results to differ materially from those in the forward-looking statements, including the following: (i) the availability to CTG of qualified professional staff, (ii) renegotiations, nullification, or breaches of contracts with customers, vendors, subcontractors or other parties, (iii) the partial or complete loss of the revenue the Company generates from International Business Machines Corporation (IBM), (iv) risks associated with operating in foreign jurisdictions, (v) the change in valuation of recorded goodwill balances, (vi) the impact of current and future laws and government regulation, as well as repeal or modification of such, affecting the IT solutions and staffing industry, taxes and the Company’s operations in particular, (vii) industry and economic conditions, including fluctuations in demand for information technology (IT) services, (viii) consolidation among the Company’s competitors or customers, (ix) domestic and foreign industry competition for customers and talent, (x) the need to supplement or change our IT services in response to new offerings in the industry, and (xi) the risks described in Item 1A of this annual report on Form 10-K and from time to time in the Company’s reports filed with the Securities and Exchange Commission (SEC).

| Item 1. | Business |

Overview

CTG was incorporated in Buffalo, New York on March 11, 1966, and its corporate headquarters are located at 800 Delaware Avenue, Buffalo, New York 14209 (716-882-8000). CTG is an information technology (IT) solutions and staffing company with operations in North America and Europe. CTG employs approximately 3,700 people worldwide. During 2011, the Company had six operating subsidiaries: Computer Task Group of Canada, Inc., providing services in Canada; and Computer Task Group Belgium N.V., CTG ITS S.A., Computer Task Group IT Solutions, S.A., Computer Task Group Luxembourg PSF, and Computer Task Group (U.K.) Ltd., each primarily providing services in Europe. Services provided in North America are performed by CTG.

Services

The Company operates in one industry segment, providing IT services to its clients. These services include IT Solutions and IT Staffing. CTG provides these primary services to all of the markets that it serves. The services provided typically encompass the IT business solution life cycle, including phases for planning, developing, implementing, managing, and ultimately maintaining the IT solution. A

1

Table of Contents

typical customer is an organization with large, complex information and data processing requirements. The Company’s IT Solutions and IT Staffing services are further described as follows:

| • | IT Solutions: CTG’s services in this area include helping clients assess their business needs and identifying the right IT solutions to meet these needs, the delivery of services that include the selection and implementation of packaged software and the design, development, testing, and integration of new systems, and the development and implementation of customized software and solutions designed to fit the needs of a specific client or vertical market. |

Generally, IT Solutions services include taking responsibility for the service related deliverables on a project and may include high-end consulting services. CTG has significant experience in implementing electronic medical records (EMR) systems in integrated delivery networks and other provider organizations. CTG’s experience in supporting EMR systems and the formation of Health Information Exchanges (HIEs) favorably positions the Company as demand for these services is expected to remain strong in future years. Additionally, the Company continued providing services to assist in the start-up and development of HIEs. HIEs are consortiums of providers, payers, and government agencies at the local level that are charged with implementing secure communitywide electronic medical records.

Also included in IT Solutions is Transitional Application Management (TAM). In 2011, the healthcare market accounted for most of CTG’s TAM business. In a TAM engagement, the client hires CTG to manage an application for an extended time period, typically ranging from one to three years, while its internal IT staff focuses on implementation of a new application replacing the application being phased out. Additionally, CTG’s services in this area could include outsourcing support of single or multiple applications and help desk functions. Depending on client needs, these engagements are performed at client or CTG sites.

In 2011, CTG continued to invest in new IT Solutions development, primarily targeted to the healthcare market, which support cost reductions and productivity improvements. In 2011, several healthcare solutions under development moved from the pilot stage of testing using live data into the sales process as completed tools. These solutions include medical fraud, waste, and abuse detection and reduction, medical care and disease management, and group insurance underwriting risk assessment. The Company has developed proprietary software to support these offerings which expands the potential market for sale and support of these solutions. These solutions support both the healthcare provider and payer markets.

| • | IT Staffing: CTG recruits, retains, and manages IT talent for its clients, which are primarily large technology service providers and companies with multiple locations and significant need for high-volume external IT resources. The Company also supports larger companies and organizations that need to augment their own IT staff on a flexible basis. Our clients may require the services of our IT talent on a temporary or long-term basis. Our IT professionals generally work with the client’s internal IT staff at client sites. Our recruiting organization works with customers to define their staffing requirements and develop competitive pricing to meet those requirements. |

The primary focus of the Company’s staffing business is a managed services model that provides large clients with higher value support through cost-effective supply models customized to client needs, resource management support, vendor management programs, and a highly automated recruiting process and system with global reach.

Independent software testing is a common practice in Western Europe and represents a significant portion of the IT staffing business of CTG’s European operations. This comprehensive testing offering supports IT environments across multiple industries.

A trend affecting the staffing industry in recent years is that large users of external technology support are reducing their number of approved suppliers to fewer firms with a preference for

2

Table of Contents

those firms able to fulfill high volume requirements at competitive rates and to locate resources with specialized skills on a national level. CTG’s staffing business model fits this profile and it has consistently remained a preferred provider with large technology services providers and users that have reduced their lists of approved IT staffing suppliers.

IT solutions and staffing revenue as a percentage of total revenue for the years ended December 31, 2011, 2010 and 2009 is as follows:

| 2011 | 2010 | 2009 | ||||||||||

| IT solutions |

37 | % | 34 | % | 33 | % | ||||||

| IT staffing |

63 | % | 66 | % | 67 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Total |

100 | % | 100 | % | 100 | % | ||||||

|

|

|

|

|

|

|

|||||||

In recent years, a major strategic focus of the Company has been to increase the amount of revenue from its IT solutions business, and the percentage of IT solutions revenue to total revenue, as operating margins generated by the IT solutions business are generally significantly higher than those of the IT staffing business. Overall, the Company’s revenue increased $64.9 million or 19.6% from 2010 to 2011 due to an overall strengthening of demand for both the Company’s IT solutions and IT staffing services. The higher margin IT solutions business increased $36.9 million or 33.1% from 2010 to 2011, while IT staffing services increased $28.0 million or 12.7% in the same period. The Company’s operating margin in 2011 was 4.9%, which was the highest level for the Company since 1999. The Company’s operating margin was 4.2% in 2010, and was 3.6% in 2009.

Vertical Markets

The Company promotes a majority of its services through four vertical market focus areas: Technology Service Providers, Healthcare (which includes services provided to healthcare providers, health insurers (payers), and life sciences companies), Energy, and Financial Services. The remainder of CTG’s revenue is derived from general markets.

CTG’s revenue by vertical market for the years ended December 31, 2011, 2010 and 2009 is as follows:

| 2011 | 2010 | 2009 | ||||||||||

| Technology service providers |

34 | % | 36 | % | 30 | % | ||||||

| Healthcare |

30 | % | 27 | % | 27 | % | ||||||

| Financial services |

7 | % | 6 | % | 8 | % | ||||||

| Energy |

6 | % | 7 | % | 9 | % | ||||||

| General markets |

23 | % | 24 | % | 26 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Total |

100 | % | 100 | % | 100 | % | ||||||

|

|

|

|

|

|

|

|||||||

The Company’s growth efforts are primarily focused in the healthcare market based on its leading position in serving the provider market, its expertise and experience serving all segments of this market (providers, payers and life sciences companies), higher demand for solutions offerings and support from healthcare companies, and the greater relative strength of this sector due to the higher demand compared with other sectors of the U.S. economy. The Company’s healthcare revenue increased $28.1 million or 31.5% from 2010 to 2011 primarily due to a significant increase in demand for new healthcare related solutions projects, including those related to EMR projects. Revenue from the provider market was strong in 2011 due to the U.S. Federal government legislation that provides funding for EMRs, and the continued improvement in the credit markets. Revenue from the payer market was consistent from 2010 to 2011, and

3

Table of Contents

revenue from the life sciences market decreased year-over-year as payers and life sciences companies in the U.S. continue to limit spending on discretionary IT projects due to the challenging economic environment. Accordingly, as revenue from the Company’s targeted EMR market was strong in 2011, this caused the overall percentage of revenue for the healthcare vertical market to increase from 27% in 2009 and 2010 to 30% in 2011.

Although the percentage of total revenue declined in 2011 as compared with 2010, the Company experienced growth in the technology service provider’s vertical market during 2011 due to continued strong demand for the Company’s services. The Company’s customers cut back significantly in 2009 due to the global economic recession, and we believe the growth experienced in 2010 and 2011 was much higher than normal due to customer’s efforts to backfill for those positions cut in 2009. Going forward, we do not expect the 2010 and 2011 growth rates we experienced in our technology service provider market to be sustainable, but do expect that the long-term growth should exceed the U.S. Gross Domestic Product rate, and be similar to that of the Company’s compound annual growth rate in revenue from 2004 to 2008 of approximately 8-10%.

During 2011, the percentage of the financial services market increased from the percentage in 2010 due to an increase in the work performed in our European operations for IT staffing services. The 2011 increase was a reverse of a trend in 2009 and 2010 as the financial services market to CTG’s total revenue declined in those years primarily as of result of greater use of offshore support and lower overall demand in this sector due to the global economic recession. In recent years, most of CTG’s revenue in the financial services market was generated by its European operations, totaling 94% of the Company’s overall 2011 revenue from the financial services market.

At December 31, 2011, CTG provided IT services to approximately 300 clients in North America and Europe. In North America, the Company operates in the United States and Canada, with greater than 99% of 2011 North American revenue generated in the United States. In Europe, the Company operates in Belgium, Luxembourg, and the United Kingdom. Of total 2011 consolidated revenue of $396.2 million, approximately 83% was generated in North America and 17% in Europe, and only one client, International Business Machines Corporation (“IBM”), accounted for greater than 10% of CTG’s consolidated revenue in 2011, 2010, and 2009.

Pricing and Backlog

The Company recognizes revenue when persuasive evidence of an arrangement exists, when the services have been rendered, when the price is determinable, and when collectibility of the amounts due is reasonably assured. For time-and-material contracts, revenue is recognized as hours are incurred and costs are expended. For contracts with periodic billing schedules, primarily monthly, revenue is recognized as services are rendered to the customer. Revenue for fixed-price contracts is recognized as per the proportional method of accounting using an input-based approach whereby salary and indirect labor costs incurred are measured and compared with the total estimate of costs at completion for a project. Revenue is recognized based upon the percentage-of-completion calculation of total incurred costs to total estimated costs. The Company infrequently works on fixed-price projects that include significant amounts of material or other non-labor related costs which could distort the percent complete within a percentage-of-completion calculation. The Company’s estimate of the total labor costs it expects to incur over the term of the contract is based on the nature of the project and its past experience on similar projects, and includes management judgments and estimates which affect the amount of revenue recognized on fixed-price contracts in any accounting period.

4

Table of Contents

The Company’s revenue from contracts accounted for under time-and-material, progress billing, and percentage-of-completion methods for the years ended December 31, 2011, 2010 and 2009 is as follows:

| 2011 | 2010 | 2009 | ||||||||||

| Time-and-material |

91 | % | 91 | % | 91 | % | ||||||

| Progress billing |

7 | % | 6 | % | 7 | % | ||||||

| Percentage-of-completion |

2 | % | 3 | % | 2 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Total |

100 | % | 100 | % | 100 | % | ||||||

|

|

|

|

|

|

|

|||||||

As of December 31, 2011 and 2010, the backlog for fixed-price and all managed-support contracts was approximately $34.4 million and $22.8 million, respectively. Approximately 72.1% or $24.8 million of the December 31, 2011 backlog is expected to be earned in 2012. Of the $22.8 million of backlog at December 31, 2010, approximately 81.9%, or $18.7 million was earned in 2011. Revenue is subject to seasonal variations, with a minor slowdown in months of high vacation and legal holidays (July, August, and December). Backlog does not tend to be seasonal; however, it does fluctuate based upon the timing of entry into long-term contracts.

Competition

The IT services market, for both IT solutions and IT staffing services, is highly competitive. The market is also highly fragmented with many providers with no single competitor maintaining clear market leadership. Competition varies by location, the type of service provided, and the customer to whom services are provided. The Company’s competition comes from four major channels: large national or international vendors, including major accounting and consulting firms; hardware vendors and suppliers of packaged software systems; small local firms or individuals specializing in specific programming services or applications; and a customer’s internal data processing staff. CTG competes against all four of these channels for its share of the market. The Company believes that to compete successfully it is necessary to have a local geographic presence, offer appropriate IT solutions, provide skilled professional resources, and price its services competitively.

CTG has implemented a Global Management System, with the goal to achieve continuous, measured improvements in services and deliverables. As part of this program, CTG has developed specific methodologies for providing high value services that result in unique solutions and specified deliverables for its clients. The Company believes these methodologies will enhance its ability to compete. CTG initially achieved worldwide ISO 9001:1994 certification in June 2000. CTG received its worldwide ISO 9001:2000 certification in January 2003. The Company believes it is the only IT services company with approximately $500 million in revenue to achieve worldwide certification.

Intellectual Property

The Company has registered its symbol and logo with the U.S. Patent and Trademark Office and has taken steps to preserve its rights in other countries where it operates. CTG has entered into agreements with various software and hardware vendors from time to time in the normal course of business, and has capitalized certain costs under software development projects.

Employees

CTG’s business depends on the Company’s ability to attract and retain qualified professional staff to provide services to its customers. The Company has a structured recruiting organization that works with its clients to meet their requirements by recruiting and providing high quality, motivated staff. The

5

Table of Contents

Company employs approximately 3,700 employees worldwide, with approximately 3,200 in the United States and Canada and 500 in Europe. Of these employees, approximately 3,300 are IT professionals and 400 are individuals who work in sales, recruiting, delivery, administrative and support positions. The Company believes that its relationship with its employees is good. No employees are covered by a collective bargaining agreement or are represented by a labor union. CTG is an equal opportunity employer.

Financial Information Relating to Foreign and Domestic Operations

The following table sets forth certain financial information relating to the performance of the Company for the years ended December 31, 2011, 2010, and 2009. This information should be read in conjunction with the audited consolidated financial statements and notes thereto included in Item 8, “Financial Statements and Supplementary Data” included in this report.

| 2011 | 2010 | 2009 | ||||||||||

| (amounts in thousands) | ||||||||||||

| Revenue from External Customers: |

||||||||||||

| United States |

$ | 328,422 | $ | 269,071 | $ | 211,265 | ||||||

|

Belgium(1) |

43,011 | 41,317 | 42,326 | |||||||||

| Other European countries |

23,969 | 19,396 | 20,418 | |||||||||

| Other country |

873 | 1,623 | 1,551 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total revenue |

$ | 396,275 | $ | 331,407 | $ | 275,560 | ||||||

|

|

|

|

|

|

|

|||||||

| Operating Income: |

||||||||||||

| United States |

$ | 16,508 | $ | 12,401 | $ | 8,342 | ||||||

| Europe |

2,729 | 1,465 | 1,527 | |||||||||

| Other country |

73 | 64 | 20 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total operating income |

$ | 19,310 | $ | 13,930 | $ | 9,889 | ||||||

|

|

|

|

|

|

|

|||||||

| Total Assets: |

||||||||||||

| United States |

$ | 119,912 | $ | 104,914 | $ | 89,015 | ||||||

|

Belgium(1) |

15,148 | 13,326 | 14,458 | |||||||||

| Other European countries |

12,133 | 11,575 | 10,549 | |||||||||

| Other country |

299 | 458 | 700 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total assets |

$ | 147,492 | $ | 130,273 | $ | 114,722 | ||||||

|

|

|

|

|

|

|

|||||||

| (1) | Revenue and total assets for Belgium have been disclosed separately as they exceed 10% of the consolidated balances for the years presented. |

6

Table of Contents

Executive Officers of the Company

As of December 31, 2011, the following individuals were executive officers of the Company:

| Name |

Age | Office |

Period During Which Served as Executive Officer |

Other Positions and Offices with Registrant | ||||

| James R. Boldt |

60 | Chairman, President and Chief Executive Officer | June 21, 2001 for President, July 16, 2001 for Chief Executive Officer, May 2002 for Chairman, all to date | Director | ||||

| Executive Vice President | February 2001 to June 2001 | |||||||

| Vice President, Strategic Staffing | December 2000 to September 2001 | |||||||

| Acting Chief Executive Officer | June 2000 to November 2000 | |||||||

| Vice President and Chief Financial Officer | February 12, 1996 to October 1, 2001 | |||||||

| Michael J. Colson |

49 | Senior Vice President | January 3, 2005 to date | None | ||||

| Arthur W. Crumlish |

57 | Senior Vice President | September 24, 2001 to date | None | ||||

| Filip J.L. Gyde |

51 | Senior Vice President | October 1, 2000 to date | None | ||||

| Brendan M. Harrington |

45 | Senior Vice President, Chief Financial Officer | September 13, 2006 to date | None | ||||

| Interim Chief Financial Officer | October 17, 2005 to September 12, 2006 | None | ||||||

| Peter P. Radetich |

57 | Senior Vice President, General Counsel | April 28, 1999 to date | Secretary | ||||

| Ted Reynolds |

56 | Vice President, Health Solutions | March 7, 2011 to date | None | ||||

Mr. Boldt was appointed President and joined CTG’s Board of Directors on June 21, 2001, and was appointed Chief Executive Officer on July 16, 2001. Mr. Boldt became the Company’s Chairman in May 2002. Mr. Boldt joined the Company as a Vice President and its Chief Financial Officer and Treasurer in February 1996.

Mr. Colson joined the Company as Senior Vice President of Solutions Development in January 2005. Prior to that, Mr. Colson was Chief Executive Officer of Manning and Napier Information Services, a software and venture capital firm from September 1998 until the time he joined CTG.

Mr. Crumlish was promoted to Senior Vice President in September 2001, and is currently responsible for the Company’s Strategic Staffing Services organization. Prior to that, Mr. Crumlish was Controller of the Company’s Strategic Staffing Services organization. Mr. Crumlish joined the Company in 1990.

Mr. Gyde was promoted to Senior Vice President in October 2000, at which time he assumed responsibility for all of the Company’s European operations. Prior to that, Mr. Gyde was Managing Director of the Company’s Belgium operation. Mr. Gyde has been with the Company since May 1987.

7

Table of Contents

Mr. Harrington was promoted to Senior Vice President and Chief Financial Officer on September 13, 2006. Previously he was Interim Chief Financial Officer and Treasurer from October 17, 2005 to September 12, 2006. Mr. Harrington joined the Company in February 1994 and served in a number of managerial financial positions in the Company’s corporate and European operations, including as the Director of Accounting since 2003, before being appointed Corporate Controller in May 2005.

Mr. Radetich joined the Company in June 1988 as Associate General Counsel, and was promoted to General Counsel and Secretary in April 1999.

Mr. Reynolds was promoted in to Vice President for CTG Health Solutions in March 2011 and is currently responsible for CTG’s entire provider and payer related services. Prior to that, Mr. Reynolds served as the Company’s Client Services Executive for our Epic practice. Mr. Reynolds joined CTG in 2006, and previously had approximately 30 years of experience in healthcare and IT.

Available Company Information

The Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (Exchange Act), and reports pertaining to the Company filed under Section 16 of the Exchange Act are available without charge on the Company’s website at www.ctg.com as soon as reasonably practicable after the Company electronically files the information with, or furnishes it to, the SEC. The Company’s code of ethics, committee charters and governance policies are also available without charge on the Company’s website at http://investors.ctg.com/governance.cfm.

8

Table of Contents

| Item 1A. | Risk Factors |

We operate in a dynamic and rapidly changing environment that involves numerous risks and uncertainties. The following section describes some, but not all, of the risks and uncertainties that could have a material adverse effect on our business, financial condition, results of operations and the market price of our common stock, and could cause our actual results to differ materially from those expressed or implied in our forward-looking statements.

Our business depends on the availability of a large number of highly qualified IT professionals and our ability to recruit and retain these professionals.

We actively compete with many other IT service providers for qualified professional staff. The availability of qualified professional staff may affect our ability to provide services and meet the needs of our customers in the future. An inability to fulfill customer requirements at agreed upon rates due to a lack of available qualified staff may adversely impact our revenue and operating results in the future.

Increased competition and the bargaining power of our large customers may cause our billing rates to decline, which would have an adverse effect on our revenue and, if we are unable to control our personnel costs accordingly, on our margins and operating results.

We have experienced reductions in the rates at which we bill some of our larger customers for services during previous highly competitive market conditions. Additionally, we actively compete against many other companies for business with new and existing clients. Bill rate reductions or competitive pressures, may lead to a decline in revenue or the rates we bill our customers for services. If we are unable to make commensurate reductions in our personnel costs, our margins and operating results in the future may be adversely affected.

Liability or damage to our reputation could arise if we fail to protect client and Company data or information systems as obligated by law or contract if our information systems are breached.

As a company operating in the IT and professional services industry, we are dependent on information technology networks and systems to process, transmit and store electronic information, and to communicate among our locations within the United States and around the world as well as with our clients and vendors. Although the Company has had no prior significant cyber incidents, and we believe the likelihood of the occurrence of such incidents is low, the breadth and complexity of our technological infrastructure increases the potential risk of security breaches. Such breaches could lead to shutdowns or disruptions of our systems and potential unauthorized disclosure of confidential information such as protected health information (PHI) protected under the Health Insurance Portability and Accountability Act of 1996 (HIPAA). The Company’s failure to protect PHI covered under HIPAA could result in fines and penalties which could have a material, adverse impact on us.

We derive a significant portion of our revenue from a single customer and a significant reduction in the amount of IT services requested by this customer would have an adverse effect on our revenue and operating results.

IBM is CTG’s largest customer. CTG provides services to various IBM divisions in many locations. During the 2011 fourth quarter, the National Technical Services Agreement (“NTS Agreement”) was renewed for three years until December 31, 2014. In 2011, 2010, and 2009, IBM accounted for $116.5 million or 29.4%, $102.3 million or 30.9%, and $71.2 million or 25.8% of the Company’s consolidated revenue, respectively. No other customer accounted for more than 10% of the Company’s revenue in 2011, 2010 or 2009. The Company’s accounts receivable from IBM at December 31, 2011 and 2010 amounted to $12.8 million and $13.1 million, respectively. If IBM were to significantly reduce the amount of IT services they purchase from the Company, our revenue and operating results would be adversely affected.

9

Table of Contents

The currency exchange, legislative, tax, regulatory and economic risks associated with international operations could have an adverse effect on our operating results if we are unable to mitigate or hedge these risks.

We have operations in the United States and Canada in North America, and in Belgium, Luxembourg, and the United Kingdom in Europe. Although our foreign operations conduct their business in their local currencies, these operations are subject to their own currency fluctuations, legislation, employment and tax law changes, and economic climates. These factors as they relate to our foreign operations are different than those of the United States. Although we actively manage these foreign operations with local management teams, our overall operating results may be negatively affected by local economic conditions, changes in foreign currency exchange rates, or tax, regulatory or other economic changes beyond our control.

Our customer contracts generally have a short term or are terminable on short notice and a significant number of failures to renew contracts, early terminations or renegotiations of our existing customer contracts could adversely affect our results of operations.

Our clients typically retain us on a non-exclusive, engagement-by-engagement basis, rather than under exclusive long-term contracts. We performed approximately 91% of our services on a time-and-materials basis during 2011. As such, our customers generally have the right to terminate a contract with us upon written notice without the payment of any financial penalty. Client projects may involve multiple engagements or stages, and there is a risk that a client may choose not to retain us for additional stages of a project, or that a client will cancel or delay additional planned engagements. These terminations, cancellations or delays could result from factors that are beyond our control and are unrelated to our work product or the progress of the project, but could be related to business or financial conditions of the client, changes in client strategies or the economy in general. When contracts are terminated, we lose the anticipated future revenue and we may not be able to eliminate the associated costs required to support those contracts in a timely manner. Consequently, our operating results in subsequent periods may be lower than expected. Our clients can cancel or reduce the scope of their engagements with us on short notice. If they do so, we may be unable to reassign our professionals to new engagements without delay. The cancellation or reduction in scope of an engagement could, therefore, reduce the utilization rate of our professionals, which would have a negative impact on our business, financial condition, and results of operations. As a result of these and other factors, our past financial performance should not be relied on as a guarantee of similar or better future performance. Due to these factors, we believe that our results of operations may fluctuate from period to period in the future.

A significant portion of our total assets consists of goodwill, which is subject to a periodic impairment analysis and a significant impairment determination in any future period could have an adverse effect on our results of operations even without a significant loss of revenue or increase in cash expenses attributable to such period.

We have goodwill recorded totaling approximately $35.7 million at December 31, 2011. At least annually, we evaluate this goodwill for impairment based on the fair value of the business operations to which this goodwill relates. This estimated fair value could change if there is a significant decrease in the enterprise value of CTG, if we are unable to achieve operating results at the levels that have been forecasted, the market valuation of such companies decreases based on transactions involving similar companies which could occur given the economic downturn in recent years in the countries in which the Company operates, or there is a permanent, negative change in the market demand for the services offered by this business unit. These changes could result in an impairment of the existing goodwill balance that could require a material non-cash charge which would have an adverse impact on our results of operations.

10

Table of Contents

Changes in government regulations and laws affecting the IT services industry, including accounting principles and interpretations and the taxation of domestic and foreign operations, could adversely affect our results of operations.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002, the Dodd-Frank Wall Street Reform and Consumer Protection Act, the Patient Protection and Affordable Care Act (PPACA), and new SEC regulations, create uncertainty for companies such as ours. These new or updated laws, regulations and standards are subject to varying interpretations which, in many instances, is due to their lack of specificity. As a result, the application of these new standards and regulations in practice may evolve over time as new guidance is provided by regulatory and governing bodies. This could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. We are committed to maintaining high standards of corporate governance and public disclosure. As a result, our efforts to comply with evolving laws, tax regulations and other standards have resulted in, and are likely to continue to result in, increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities. In particular, our continuing efforts to comply with Section 404 of the Sarbanes-Oxley Act of 2002 and the related regulations regarding our required assessment of our internal controls over financial reporting and our independent auditors’ audit of internal control require the commitment of significant internal, financial and managerial resources.

The Financial Accounting Standards Board (FASB), the SEC, and the Public Company Accounting Oversight Board (PCAOB) or other accounting rulemaking authorities may issue new accounting rules or auditing standards that are different than those that we presently apply to our financial results. Such new accounting rules or auditing standards could require significant changes from the way we currently report our financial condition, results of operations or cash flows.

U.S. generally accepted accounting principles have been the subject of frequent changes in interpretations. As a result of the enactment of the Sarbanes-Oxley Act of 2002 and the review of accounting policies by the SEC as well as by national and international accounting standards bodies, the frequency of future accounting policy changes may accelerate. Such future changes in financial accounting standards may have a significant effect on our reported results of operations, including results of transactions entered into before the effective date of the changes.

The Company does not currently offer healthcare coverage to its hourly employees, which includes approximately half of its total employees. Under recently issued legislation (PPACA), the Company will be required to offer healthcare coverage to those employees, or pay penalties currently totaling at least $2,000 per person. The Company may not be able to pass these costs to its customers, which could significantly negatively impact the Company’s operating results when the legislation goes into effect in 2014.

We are subject to income and other taxes in the United States (federal and state) and numerous foreign jurisdictions. Our provisions for income and other taxes and our tax liabilities in the future could be adversely affected by numerous factors. These factors include, but are not limited to, income before taxes being lower than anticipated in countries with lower statutory tax rates and higher than anticipated in countries with higher statutory tax rates, changes in the valuation of deferred tax assets and liabilities, and changes in various federal, state and international tax laws, regulations, accounting principles or interpretations thereof, which could adversely impact our financial condition, results of operations and cash flows in future periods.

During 2011, the Company experienced higher unemployment tax rates in many of the states in which we do business, which increased our direct costs and negatively impacted our profitability. Considering current economic conditions in the U.S., the Company expects these rates will continue to increase in 2012 and future years.

11

Table of Contents

Existing and potential customers may outsource or consider outsourcing their IT requirements to foreign countries in which we may not currently have operations, which could have an adverse effect on our ability to obtain new customers or retain existing customers.

In the past few years, more companies started using or are considering using low cost offshore outsourcing centers to perform technology-related work and complete projects. Currently, we have partnered with clients to perform services in Russia to mitigate and reduce this risk to our Company. However, the risk of additional increases in the future in the outsourcing of IT solutions overseas to countries where we do not have operations could have a material, negative impact on our future operations.

The introduction of new IT products or services may render our existing IT Solutions or IT Staffing offerings to be obsolete, which, if we are unable to keep pace with these corresponding changes, could have an adverse effect on our business.

Our success depends, in part, on our ability to implement and deliver IT Solutions or IT Staffing services that anticipate and keep pace with rapid and continuing changes in technology, industry standards and client preferences. We may not be successful in anticipating or responding to these developments on a timely basis, and our offerings may not be successful in the marketplace. Also, services, solutions and technologies developed by our competitors may make our solutions or staffing offerings uncompetitive or obsolete. Any one of these circumstances could have a material adverse effect on our ability to obtain and successfully complete client engagements.

Decreases in demand for information technology (IT) solutions and staffing services in the future would cause an adverse effect on our revenue and operating results.

The Company’s revenue and operating results are significantly affected by changes in demand for its services. In recent years, the U.S. economy, where the Company performs greater than 80% of its total business based upon revenue, significantly deteriorated primarily due to subprime mortgage issues, financial market conditions, and other economic concerns. In 2009, these economic pressures also extended to the European markets where the Company operates. These negative pressures on the economy led to a worldwide contraction of the credit markets, more severe recessionary conditions, and a decline in demand for the Company’s services which negatively affected the Company’s revenue and operating results in 2009 as compared with 2008. Economic pressures also led to customers’ reducing their spending on IT projects and external professional services. Economic conditions in 2010 and 2011 stabilized in the U.S., but continued to be challenging in Europe. Declines in spending for IT services in 2012 or future years may additionally adversely affect our operating results in the future as they have in the past.

The IT services industry is highly competitive and fragmented, which means that our customers have a number of choices for providers of IT services and we may not be able to compete effectively.

The market for our services is highly competitive. The market is fragmented, and no company holds a dominant position. Consequently, our competition for client requirements and experienced personnel varies significantly by geographic area and by the type of service provided. Some of our competitors are larger and have greater technical, financial, and marketing resources and greater name recognition than we have in the markets we collectively serve. In addition, clients may elect to increase their internal IT systems resources to satisfy their custom software development and integration needs. Finally, our industry is being impacted by the growing use of lower-cost offshore delivery capabilities (primarily India and other parts of Asia). There can be no assurance that we will be able to continue to compete successfully with existing or future competitors or that future competition will not have a material adverse effect on our results of operations and financial condition.

12

Table of Contents

Changing economic conditions and the affect of such changes on accounting estimates could have a material impact on our results of operations.

The Company has also made a number of estimates and assumptions relating to the reporting of its assets and liabilities and the disclosure of contingent assets and liabilities to prepare its consolidated financial statements pursuant to the rules and regulations of the SEC and other accounting rulemaking authorities. Such estimates primarily relate to the valuation of goodwill, the valuation of stock options for recording equity-based compensation expense, allowances for doubtful accounts receivable, investment valuation, legal matters, other contingencies and estimates of progress toward completion and direct profit or loss on contracts, as applicable. As future events and their effects cannot be determined with precision, actual results could differ from these estimates. Changes in the economic climates in which the Company operates may affect these estimates and will be reflected in the Company’s financial statements in the event they occur. Such changes could result in a material impact on the Company’s results of operations.

13

Table of Contents

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

The Company owns and occupies its headquarters building at 800 Delaware Avenue, and an office building at 700 Delaware Avenue, both located in Buffalo, New York. These buildings are operated by CTG of Buffalo, a subsidiary of the Company which is part of the Company’s North American operations. The corporate headquarters consists of approximately 48,000 square feet and is occupied by corporate administrative operations. The office building consists of approximately 42,000 square feet and is also occupied by corporate administrative operations. At December 31, 2011, these properties were not mortgaged as part of the Company’s existing revolving credit agreement.

All of the remaining Company locations, totaling approximately 20 sites, are leased facilities. Most of these facilities serve as sales and support offices and their size varies, generally in the range from 250 to 10,150 square feet, with the number of people employed at each office. The Company’s lease terms generally vary from periods of less than a year to five years and typically have flexible renewal options. The Company believes that its presently owned and leased facilities are adequate to support its current and anticipated future needs.

| Item 3. | Legal Proceedings |

The Company and its subsidiaries are involved from time to time in various legal proceedings arising in the ordinary course of business. Although the outcome of lawsuits or other proceedings involving the Company and its subsidiaries cannot be predicted with certainty and the amount of any liability that could arise with respect to such lawsuits or other proceedings cannot be predicted accurately, management does not expect these matters, if any, to have a material adverse effect on the financial position, results of operations, or cash flows of the Company.

| Item 4. | Mine Safety Disclosures |

Not applicable.

14

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Stock Market Information

The Company’s common stock is traded on The NASDAQ Stock Market LLC under the symbol CTGX. The following table sets forth the high and low sales prices for the Company’s common stock for each quarter of the previous two years.

| Stock Price | High | Low | ||||||

| Year ended December 31, 2011 |

||||||||

| Fourth Quarter |

$ | 14.50 | $ | 9.68 | ||||

| Third Quarter |

$ | 14.25 | $ | 9.47 | ||||

| Second Quarter |

$ | 15.00 | $ | 11.19 | ||||

| First Quarter |

$ | 13.58 | $ | 10.65 | ||||

| Year ended December 31, 2010 |

||||||||

| Fourth Quarter |

$ | 11.90 | $ | 7.72 | ||||

| Third Quarter |

$ | 8.64 | $ | 6.23 | ||||

| Second Quarter |

$ | 9.58 | $ | 6.26 | ||||

| First Quarter |

$ | 8.25 | $ | 6.86 | ||||

On February 8, 2012, there were 1,784 record holders of the Company’s common shares. The Company has not paid a dividend since 2000. The Company is required to meet certain financial covenants under its current revolving credit agreement in order to pay dividends. The Company was in compliance with these financial covenants at each of December 31, 2009, 2010 and 2011. The determination of the timing, amount and payment of dividends in the future on the Company’s common stock is at the discretion of the Board of Directors and will depend upon, among other things, the Company’s profitability, liquidity, financial condition, capital requirements and compliance with the aforementioned financial covenants.

For information concerning common stock issued in connection with the Company’s equity compensation plans, see Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Issuer Purchases of Equity Securities

The Company’s share repurchase program (originally announced on May 12, 2005) does not have an expiration date, nor was it terminated during the 2011 fourth quarter. During February 2011, the Company’s Board of Directors authorized the addition of one million shares to the repurchase program. The information in the table below does not include shares tendered to the Company either to satisfy the exercise cost for the cashless exercise of employee stock options, or tax withholding obligations associated with employee equity awards.

15

Table of Contents

Purchases by the Company of its common stock during the fourth quarter ended December 31, 2011 are as follows:

| Period |

Total Number of Shares Purchased |

Average Price Paid per Share* |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Maximum Number of Shares that May Yet be Purchased Under the Plans or Programs |

||||||||||||

| October 2 – October 31 |

18,949 | $ | 10.74 | 18,949 | 868,894 | |||||||||||

| November 1 – November 30 |

7,900 | $ | 11.90 | 7,900 | 860,994 | |||||||||||

| December 1 – December 31 |

— | $ | — | — | 860,994 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total |

26,849 | $ | 11.08 | 26,849 | ||||||||||||

|

|

|

|

|

|

|

|||||||||||

| * | Excludes broker commissions |

16

Table of Contents

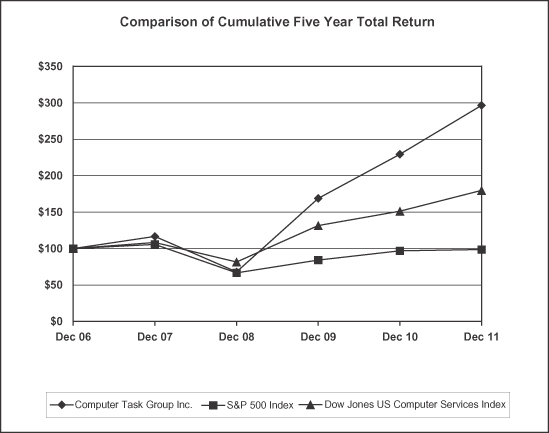

Company Performance Graph

The following graph displays a five-year comparison of cumulative total shareholder returns for the Company’s common stock, the S&P 500 Index, and the Dow Jones U.S. Computer Services Index, assuming a base index of $100 at the end of 2006. The cumulative total return for each annual period within the five years presented is measured by dividing (1) the sum of (A) the cumulative amount of dividends for the period, assuming dividend reinvestment, and (B) the difference between the Company’s share price at the end and the beginning of the period by (2) the share price at the beginning of the period. The calculations were made excluding trading commissions and taxes.

| Base Period |

Indexed Returns Years Ending |

|||||||||||||||||||||||

| Dec. 06 | Dec. 07 | Dec. 08 | Dec. 09 | Dec. 10 | Dec. 11 | |||||||||||||||||||

| Computer Task Group, Inc. |

$ | 100.00 | $ | 116.42 | $ | 67.79 | $ | 168.63 | $ | 229.05 | $ | 296.42 | ||||||||||||

| S&P 500 Index |

$ | 100.00 | $ | 105.49 | $ | 66.46 | $ | 84.05 | $ | 96.71 | $ | 98.76 | ||||||||||||

| Dow Jones U.S. Computer Services Index |

$ | 100.00 | $ | 108.42 | $ | 81.66 | $ | 131.31 | $ | 151.29 | $ | 179.54 | ||||||||||||

The information included under this section entitled “Company Performance Graph” is deemed not to be “soliciting material” or “filed” with the SEC, is not subject to the liabilities of Section 18 of the Exchange Act, and shall not be deemed incorporated by reference into any of the filings previously made or made in the future by the Company under the Exchange Act or the Securities Act of 1933, except to the extent the Company specifically incorporates any such information into a document that is filed.

17

Table of Contents

| Item 6. | Selected Financial Data |

Consolidated Summary—Five-Year Selected Financial Information

The selected operating data and financial position information set forth below for each of the years in the five-year period ended December 31, 2011 has been derived from the Company’s audited consolidated financial statements. This information should be read in conjunction with the audited consolidated financial statements and notes thereto included in Item 8, “Financial Statements and Supplementary Data” included in this report.

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (amounts in millions, except per-share data) |

(1 | ) | (1 | ) | ||||||||||||||||

| Operating Data |

||||||||||||||||||||

| Revenue |

$ | 396.3 | $ | 331.4 | $ | 275.6 | $ | 353.2 | $ | 325.3 | ||||||||||

| Operating Income |

$ | 19.3 | $ | 13.9 | $ | 9.9 | $ | 13.1 | $ | 6.5 | ||||||||||

| Net Income |

$ | 11.9 | $ | 8.4 | $ | 5.9 | $ | 7.8 | $ | 4.2 | ||||||||||

| Basic net income per share |

$ | 0.80 | $ | 0.57 | $ | 0.40 | $ | 0.51 | $ | 0.26 | ||||||||||

| Diluted net income per share |

$ | 0.71 | $ | 0.52 | $ | 0.38 | $ | 0.49 | $ | 0.25 | ||||||||||

| Cash dividend per share |

$ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Financial Position |

||||||||||||||||||||

| Working capital |

$ | 45.4 | $ | 33.0 | $ | 25.8 | $ | 24.8 | $ | 23.2 | ||||||||||

| Total assets |

$ | 147.5 | $ | 130.3 | $ | 114.7 | $ | 115.8 | $ | 112.5 | ||||||||||

| Long-term debt |

$ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Shareholders’ equity |

$ | 88.8 | $ | 77.9 | $ | 71.7 | $ | 67.6 | $ | 65.1 | ||||||||||

| (1) | During 2007, the Company received two unsolicited merger proposals from RCM Technologies, Inc. After consideration of the proposals, the Company’s Board of Directors unanimously determined that the proposals were inadequate and did not reflect the value inherent in CTG’s business and the Company’s potential growth opportunities. In 2008 and 2007, included in operating income, the Company recorded $0.2 million and $0.7 million, respectively, related to advisory fees incurred in conjunction with its consideration of the two unsolicited merger proposals. |

18

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Forward-Looking Statements

This management’s discussion and analysis of financial condition and results of operations contains forward-looking statements made by the management of CTG that are subject to a number of risks and uncertainties. These forward-looking statements are based on information as of the date of this report. The Company assumes no obligation to update these statements based on information from and after the date of this report. Generally, forward-looking statements include words or phrases such as “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “projects,” “could,” “may,” “might,” “should,” “will” and words and phrases of similar impact. The forward-looking statements include, but are not limited to, statements regarding future operations, industry trends or conditions and the business environment, and statements regarding future levels of, or trends in, revenue, operating expenses, capital expenditures, and financing. The forward-looking statements are made pursuant to safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Numerous factors could cause actual results to differ materially from those in the forward-looking statements, including the following: (i) the availability to CTG of qualified professional staff, (ii) renegotiations, nullification, or breaches of contracts with customers, vendors, subcontractors or other parties, (iii) the partial or complete loss of the revenue the Company generates from International Business Machines Corporation (IBM), (iv) risks associated with operating in foreign jurisdictions, (v) the change in valuation of recorded goodwill balances, (vi) the impact of current and future laws and government regulation, as well as repeal or modification of such, affecting the IT solutions and staffing industry, taxes and the Company’s operations in particular, (vii) industry and economic conditions, including fluctuations in demand for information technology (IT) services, (viii) consolidation among the Company’s competitors or customers, (ix) domestic and foreign industry competition for customers and talent, (x) the need to supplement or change our IT services in response to new offerings in the industry, and (xi) the risks described in Item 1A of this annual report on Form 10-K and from time to time in the Company’s reports filed with the Securities and Exchange Commission (SEC).

Industry Trends

The market demand for the Company’s services is heavily dependent on IT spending by major corporations, organizations and government entities in the markets and regions that we serve. The pace of technology advances and changes in business requirements and practices of our clients all have a significant impact on the demand for the services that we provide. Competition for new engagements and pricing pressure has been strong. Since August 2009, we have noticed an increase in demand for our services, primarily in the healthcare provider solution and general IT staffing businesses. We added new electronic medical records (EMR) projects throughout 2011 ranging from one to three years in duration, and have a total of 18 significant EMR engagements in process as of December 31, 2011. We anticipate a continuation of the strong demand for our EMR healthcare solutions services in 2012 due to the U.S. government funding, and the greater demand for healthcare services in the U.S. due to the aging population.

19

Table of Contents

We have two main services, which are providing IT solutions and IT staffing to our clients. With IT solutions, we generally take responsibility for the deliverables on a project and the services may include high-end consulting services. When providing IT staffing services, we typically supply personnel to our customers who then, in turn, take their direction from the client’s managers. IT solutions and IT staffing revenue as a percentage of total revenue for the years ended December 31, 2011, 2010 and 2009 is as follows:

| 2011 | 2010 | 2009 | ||||||||||

| IT solutions |

37 | % | 34 | % | 33 | % | ||||||

| IT staffing |

63 | % | 66 | % | 67 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Total |

100 | % | 100 | % | 100 | % | ||||||

|

|

|

|

|

|

|

|||||||

The Company promotes a majority of its services through four vertical market focus areas: Technology Service Providers, Healthcare (which includes services provided to healthcare providers, health insurers, and life sciences companies), Energy, and Financial Services. The remainder of CTG’s revenue is derived from general markets. CTG’s revenue by vertical market for the years ended December 31, 2011, 2010 and 2009 is as follows:

| 2011 | 2010 | 2009 | ||||||||||

| Technology service providers |

34 | % | 36 | % | 30 | % | ||||||

| Healthcare |

30 | % | 27 | % | 27 | % | ||||||

| Financial services |

7 | % | 6 | % | 8 | % | ||||||

| Energy |

6 | % | 7 | % | 9 | % | ||||||

| General markets |

23 | % | 24 | % | 26 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Total |

100 | % | 100 | % | 100 | % | ||||||

|

|

|

|

|

|

|

|||||||

The IT services industry is extremely competitive and characterized by continuous changes in customer requirements and improvements in technologies. Our competition varies significantly by geographic region, as well as by the type of service provided. Many of our competitors are larger than CTG, and have greater financial, technical, sales and marketing resources. In addition, the Company frequently competes with a client’s own internal IT staff. Our industry is being impacted by the growing use of lower-cost offshore delivery capabilities (primarily India and other parts of Asia). There can be no assurance that we will be able to continue to compete successfully with existing or future competitors or that future competition will not have a material adverse effect on our results of operations and financial condition.

Revenue Recognition

The Company recognizes revenue when persuasive evidence of an arrangement exists, when the services have been rendered, when the price is determinable, and when collectibility of the amounts due is reasonably assured. For time-and-material contracts, revenue is recognized as hours are incurred and costs are expended. For contracts with periodic billing schedules, primarily monthly, revenue is recognized as services are rendered to the customer. Revenue for fixed-price contracts is recognized as per the proportional method of accounting using an input-based approach whereby salary and indirect labor costs incurred are measured and compared with the total estimate of costs of such items at completion for a project. Revenue is recognized based upon the percentage-of-completion calculation of total incurred costs to total estimated costs. The Company infrequently works on fixed-price projects that include significant amounts of material or other non-labor related costs which could distort the percent completed within a percentage-of-completion calculation. The Company’s estimate of the total labor costs it expects to incur over the term of the contract is based on the nature of the project and our past experience on similar projects, and includes management judgments and estimates which affect the amount of revenue recognized on fixed-price contracts in any accounting period.

20

Table of Contents

The Company previously entered into a series of contracts with a customer that provides for application customization and integration services, as well as post contract support (PCS) services, specifically utilizing one of several of the software tools the Company has internally developed. These services are provided under a software-as-a-service model. As the contracts are closely interrelated and dependent on each other, for accounting purposes the contracts are considered to be one arrangement. Additionally, as the project includes significant modification and customization services to transform the previously developed software tool into an expanded tool that will meet the customer’s requirements, the percentage-of-completion method of contract accounting is being utilized for the project. Total revenue and costs were recognized equally until completion of the application customization and integration services portion of the project. The remaining unrecognized portion of the contract value was recognized on a straight-line basis over the term of the PCS period that ended December 31, 2011.

The Company’s revenue from contracts accounted for under time-and-material, progress billing, and percentage-of-completion methods for the years ended December 31, 2011, 2010 and 2009 is as follows:

| 2011 | 2010 | 2009 | ||||||||||

| Time-and-material |

91 | % | 91 | % | 91 | % | ||||||

| Progress billing |

7 | % | 6 | % | 7 | % | ||||||

| Percentage-of-completion |

2 | % | 3 | % | 2 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Total |

100 | % | 100 | % | 100 | % | ||||||

|

|

|

|

|

|

|

|||||||

Results of Operations

The table below sets forth percentage information calculated as a percentage of consolidated revenue as reported on the Company’s consolidated statements of income as included in Item 8, “Financial Statements and Supplementary Data” in this report.

| Year Ended December 31, | 2011 | 2010 | 2009 | |||||||||

| (percentage of revenue) | ||||||||||||

| Revenue |

100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Direct costs |

78.7 | % | 78.5 | % | 77.5 | % | ||||||

| Selling, general and administrative expenses |

16.4 | % | 17.3 | % | 18.9 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Operating income |

4.9 | % | 4.2 | % | 3.6 | % | ||||||

| Interest and other expense, net |

0.1 | % | 0.1 | % | 0.1 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Income before income taxes |

4.8 | % | 4.1 | % | 3.5 | % | ||||||

| Provision for income taxes |

1.8 | % | 1.6 | % | 1.4 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Net income |

3.0 | % | 2.5 | % | 2.1 | % | ||||||

|

|

|

|

|

|

|

|||||||

2011 as compared with 2010

In 2011, the Company recorded revenue of $396.3 million, an increase of 19.6% as compared with revenue of $331.4 million recorded in 2010. Revenue from the Company’s North American operations totaled $329.3 million in 2011, an increase of 21.6% when compared with revenue of $270.7 million in 2010. Revenue from the Company’s European operations totaled $67.0 million in 2011, an increase of 10.3% when compared with 2010 revenue of $60.7 million. The European revenue represented 16.9% and 18.3% of 2011 and 2010 consolidated revenue, respectively. The Company’s revenue includes reimbursable expenses billed to customers. These expenses totaled $12.7 million and $9.1 million in 2011 and 2010, respectively.

21

Table of Contents

In North America, the significant revenue increase in 2011 as compared with 2010 is due to strong demand for both the Company’s IT solutions and IT staffing services as general economic conditions continued to improve from those that existed during the recession in 2008/2009. IT solutions revenue increased 33.1% and IT staffing revenue increased 12.7% in 2011 as compared with 2010. The IT solutions revenue increase totaled $36.9 million and was primarily driven by an increase in the Company’s EMR work. The Company expects demand for its EMR solutions and other healthcare related services to remain strong in 2012. The IT staffing revenue increase totaled $28.0 million as the Company’s customers filled staffing requirements that had remained open from 2009 due to the economic recession in the United States. The Company expects the growth in IT staffing demand in 2012 to slow from that in 2011, however, and for the long-term growth rate to be similar to that of the Company’s compound annual growth rate in revenue from 2004 to 2008 of approximately 8-10%.

The Company’s European operations include Belgium, Luxembourg and the United Kingdom. The increase in year-over-year revenue in the Company’s European operations was primarily due to modest strength in the Company’s European IT staffing business, much of which is due to work with government ministries associated with the European Union. This revenue increase was supported by the strength relative to the U.S. dollar of the currencies of Belgium, Luxembourg, and the United Kingdom. In Belgium and Luxembourg, the functional currency is the Euro, while in the United Kingdom the functional currency is the British Pound. In 2011 as compared with 2010, the average value of the Euro increased 4.9%, while the average value of the British Pound increased 3.8%. Had there been no change in these exchange rates from 2010 to 2011, total European revenue would have been approximately $3.0 million lower, or $64.0 million as compared with the $67.0 million reported.

IBM is CTG’s largest customer. CTG provides services to various IBM divisions in many locations. During the 2011 fourth quarter, the NTS Agreement was renewed for three years until December 31, 2014. As part of the NTS Agreement, the Company also provides its services as a predominant supplier to IBM’s Integrated Technology Services unit and as the sole provider to the Systems and Technology Group business unit. These agreements accounted for approximately 94% of all of the services provided to IBM by the Company in 2011. In 2011, 2010, and 2009, IBM accounted for $116.5 million or 29.4%, $102.3 million or 30.9%, and $71.2 million or 25.8% of the Company’s consolidated revenue, respectively. We expect to continue to derive a significant portion of our revenue from IBM in future years. However, a significant decline or the loss of the revenue from IBM would have a significant negative effect on our operating results. The Company’s accounts receivable from IBM at December 31, 2011 and 2010 amounted to $12.8 million and $13.1 million, respectively. No other customer accounted for more than 10% of the Company’s revenue in 2011, 2010 or 2009.

Direct costs, defined as costs for billable staff including billable out-of-pocket expenses, were 78.7% of consolidated revenue in 2011 and 78.5% of consolidated revenue in 2010. The increase in direct costs as a percentage of revenue in 2011 compared with 2010 was due to an increase in employee benefit costs, primarily unemployment insurance, in 2011.

Selling, general and administrative (SG&A) expenses were 16.4% of revenue in 2011 as compared with 17.3% of revenue in 2010. The SG&A decrease as a percentage of revenue in 2011 as compared with 2010 is primarily due to disciplined cost management and the economies of scale, especially pertaining to fixed costs, associated with the revenue growth experienced in 2011 as compared with 2010.

Operating income was 4.9% of revenue in 2011 as compared with 4.2% of revenue in 2010. Operating income from North American operations was $16.6 million and $12.4 million in 2011 and 2010, respectively, while European operations generated operating income of $2.7 million and $1.5 million in 2011 and 2010, respectively. Operating income in the Company’s European operations increased by approximately $0.2 million due to the change in foreign currency exchange rates year-over-year.

22

Table of Contents

Interest and other expense, net was 0.1% of revenue in both 2011 and 2010. This balance primarily consists of interest expense on borrowings under the Company’s revolving line of credit, bank fees, and foreign exchange losses. The Company recorded a net exchange loss on intercompany balances totaling less than $0.1 million in both 2011 and 2010, resulting from balances settled during the year or those intended to be settled as of December 31, 2011. In 2011, partially offsetting the net interest and other expense balance was approximately $0.1 million resulting from a gain on a sale of property.

The Company’s effective tax rate (ETR) is calculated based upon the full years’ operating results, and various tax related items. The Company’s normal ETR ranges from 38% to 42%. The 2011 ETR was 37.6%, and the 2010 ETR was 39.2%. The ETR during 2011 was reduced as the Company recorded $0.3 million of tax credits related to research and development activities, and $0.3 million of federal tax credits related to the retention of certain individuals hired during 2010. The impact of these credits was partially offset by an increase in the valuation allowance of $0.2 million associated with net operating losses incurred by certain foreign subsidiaries.

Net income for 2011 was 3.0% of revenue or $0.71 per diluted share, compared with net income of 2.5% of revenue or $0.52 per diluted share in 2010. Diluted earnings per share were calculated using 16.7 million weighted-average equivalent shares outstanding in 2011 and 16.1 million 2010. The increase in shares year-over-year is due to the dilutive effect of incremental shares outstanding under the Company’s equity-based compensation plans. This increase was partially offset by purchases of approximately 0.3 million shares for treasury by the Company during 2011.

2010 as compared with 2009

In 2010, the Company recorded revenue of $331.4 million, an increase of 20.3% as compared with revenue of $275.6 million recorded in 2009. Revenue from the Company’s North American operations totaled $270.7 million in 2010, an increase of 27.2% when compared with revenue of $212.8 million in 2009. Revenue from the Company’s European operations totaled $60.7 million in 2010, a decrease of 3.2% when compared with 2009 revenue of $62.8 million. The European revenue represented 18.3% and 22.8% of 2010 and 2009 consolidated revenue, respectively. The Company’s revenue includes reimbursable expenses billed to customers. These expenses totaled $9.1 million and $6.1 million in 2010 and 2009, respectively.

In North America, the significant revenue increase in 2010 as compared with 2009 was due to strengthening demand for both the Company’s IT solutions and IT staffing services. IT solutions revenue increased 21.5% and IT staffing revenue increased 19.6% in 2010 as compared with 2009. The IT solutions revenue increase totaled $19.7 million and was driven by an increase in the Company’s EMR work, but was partially offset by a reduction in demand from a large client in the Company’s energy vertical market. The IT staffing revenue increase totaled $36.1 million as the Company’s customers filled staffing requirements that had remained open from 2008 and 2009 due to the economic recession in the United States.