Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - Li3 Energy, Inc. | v244816_ex23-1.htm |

| EX-23.2 - EXHIBIT 23.2 - Li3 Energy, Inc. | v244816_ex23-2.htm |

As filed with the Securities and Exchange Commission on January 6, 2012

Registration No. 333-175329

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3 to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

LI3 ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

1479

|

20-3061907

|

||

|

(State or other jurisdiction of

|

(Primary Standard Industrial

|

(I.R.S. Employer

|

||

|

incorporation or organization)

|

Classification Code Number)

|

Identification No.)

|

Av. Pardo y Aliaga 699

Oficina 802

San Isidro, Lima, Peru

(51) 1-212-1880

(Address, including zip code, and telephone number, including area code,

of registrant’s principal executive offices)

|

Copy to:

|

||

|

Luis Saenz

|

||

|

Chief Executive Officer

|

Adam S. Gottbetter, Esq.

|

|

|

Li3 Energy, Inc.

|

Gottbetter & Partners, LLP

|

|

|

c/o Gottbetter & Partners, LLP

|

488 Madison Avenue, 12th Floor

|

|

|

488 Madison Avenue, 12th Floor

|

New York, NY 10022

|

|

|

New York, NY 10022

|

(212) 400-6900

|

|

|

(212) 400-6900

|

(Name, address, including zip code, and

telephone number, including area code, of agent for service)

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

Non-accelerated filer ¨

(Do not check if a smaller reporting company)

|

Smaller reporting company x

|

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered

|

Amount to be

Registered(1)

|

Proposed

Maximum

Offering

Price

Per Unit(2)

|

Proposed

Maximum

Aggregate

Offering Price

|

Amount of

Registration Fee(3)

|

||||||||||

|

Common stock, par value $0.001 per share

|

83,636,790 shares

|

$

|

0.07

|

$

|

5,854,575

|

$

|

679

|

|||||||

|

(1)

|

Consists of 42,797,958 issued and outstanding shares of our common stock plus 40,838,832 shares of our common stock issuable upon the exercise of outstanding warrants. This registration statement shall also cover any additional shares of our common stock that shall become issuable by reason of any stock dividend, stock split, recapitalization or other similar transaction effected without the receipt of consideration that results in an increase in the number of the outstanding shares of our common stock.

|

|

(2)

|

Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(c) under the Securities Act of 1933, as amended, based on the average of the high and low prices for the registrant’s common stock as reported by the OTC Bulletin Board on January 3, 2012. The shares offered hereunder may be sold by the selling stockholders from time to time in the open market, through privately negotiated transactions or a combination of these methods, at market prices prevailing at the time of sale or at negotiated prices.

|

|

(3)

|

Filing fee of $2,323 was previously paid.

|

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and the selling stockholders are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated January 6, 2012

LI3 ENERGY, INC.

Prospectus

83,636,790 Shares

Common Stock

This prospectus relates to the offer and sale of up to 42,797,958 issued and outstanding shares of our common stock, par value $0.001 per share, and 40,838,832 shares of our common stock issuable upon the exercise of outstanding warrants, by the selling stockholders of Li3 Energy, Inc., a Nevada corporation, named in this prospectus. The shares offered by this prospectus may be sold by the selling stockholders from time to time in the open market, through privately negotiated transactions or a combination of these methods, at market prices prevailing at the time of sale or at negotiated prices.

We are registering the offer and sale of the common stock to satisfy registration rights we have granted to the selling stockholders. The distribution of the shares by the selling stockholders is not subject to any underwriting agreement. We will not receive any proceeds from the sale of the shares by the selling stockholders. However, we may receive the proceeds from the exercise of the warrants held by the selling stockholders, to the extent the warrants are not exercised on a cashless basis. We will bear all expenses of registration incurred in connection with this offering, but all selling and other expenses incurred by the selling stockholders will be borne by them.

Our common stock is traded on the OTC Bulletin Board under the symbol “LIEG.OB”. On January 3, 2012, the last reported sale price for our common stock was $0.07 per share.

Investing in our common stock involves a high degree of risk. Before making any investment in our securities, you should read and carefully consider risks described in the “Risk Factors” section beginning on page 9 of this prospectus.

You should rely only on the information contained in this prospectus or any prospectus supplement or amendment thereto. We have not authorized anyone to provide you with different information. This prospectus may only be used where it is legal to sell these securities. The information in this prospectus is only accurate on the date of this prospectus, regardless of the time of any sale of securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus is dated ___________, 2012 .

TABLE OF CONTENTS

|

SUMMARY

|

2

|

|

|

THE OFFERING

|

7

|

|

|

NOTE REGARDING FORWARD-LOOKING STATEMENTS

|

8

|

|

|

RISK FACTORS

|

9

|

|

|

SELLING STOCKHOLDERS

|

18

|

|

|

USE OF PROCEEDS

|

33

|

|

|

DETERMINATION OF OFFERING PRICE

|

33

|

|

|

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

|

33

|

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

35

|

|

|

DESCRIPTION OF BUSINESS

|

47

|

|

|

DESCRIPTION OF PROPERTIES

|

71

|

|

|

LEGAL PROCEEDINGS

|

71

|

|

|

DIRECTORS, EXECUTIVE OFFICERS, PROMOTERS AND CONTROL PERSONS

|

71

|

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

|

75

|

|

|

EXECUTIVE COMPENSATION

|

78

|

|

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

|

82

|

|

|

PLAN OF DISTRIBUTION

|

83

|

|

|

DESCRIPTION OF SECURITIES

|

85

|

|

|

LEGAL MATTERS

|

90

|

|

|

EXPERTS

|

90

|

|

|

WHERE YOU CAN FIND MORE INFORMATION

|

90

|

|

|

DISCLOSURE OF COMMISSION POSITION ON INDEMNIFICATION FOR SECURITIES ACT LIABILITIES

|

91

|

|

|

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

|

F-1

|

SUMMARY

The following summary highlights information contained elsewhere in this prospectus. Potential investors should read the entire prospectus carefully, including the more detailed information regarding our business provided below in the “Description of Business” section, the risks of purchasing our common stock discussed under the “Risk Factors” section, and our consolidated financial statements and the accompanying notes to the consolidated financial statements.

Unless the context indicates otherwise, all references in this registration statement to “Li3 Energy,” “the Company,” “we,” “us” and “our” refer to Li3 Energy, Inc., and its subsidiaries.

Overview

We are an emerging exploration company (as defined below), focused on the discovery and development of lithium and potassium brine and nitrate and iodine deposits in Chile, Argentina and Peru.

|

|

·

|

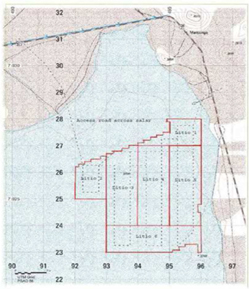

In May 2011, we acquired 60% ownership of six companies that collectively own the Maricunga project, which covers an area of approximately 3,553 acres (1,438 hectares), comprising six exploitation mining concessions in areas prospective for lithium (which is non-concessible) and potassium brines, and is located in the northeast section of the Salar de Maricunga in Region III of Atacama in northern Chile. We have conducted preliminary due diligence exploration work on this property involving digging and sampling of test pits and brine analysis, as described under “Description of Business—Our Projects—Chile—Maricunga” below.

|

|

|

·

|

In September, 2011, POSCO Canada Ltd., a wholly owned subsidiary of POSCO (“POSCAN”) (together, the “POSCO Agreements”) purchased 38,095,300 Units of our securities for approximately $8 million, with each “Unit” consisting of one share of our common stock and a three-year warrant to purchase one share of our common stock at an exercise price of $0.40. POSCAN will purchase an additional 47,619,000 Units at the same $0.21 price per Unit (for an aggregate additional purchase price of approximately $10 million) upon satisfaction of certain conditions. The agreement with POSCAN includes provisions for POSCAN to purchase brine from the Maricunga property and test it at POSCAN’s test facility in Korea. In addition, we and POSCAN will discuss and evaluate the development, financing and construction of a brine testing facility on the Maricunga property, and if such a facility is built, we would supply the test facility with brine and other materials and utilities and assist POSCAN in obtaining any rights, licenses and permits required to build and operate such facility. POSCO (with its subsidiaries) is a diversified company, with operations in energy, chemicals and materials and is one of the largest steel manufacturers in the world. For a more complete description of these agreements, see “Description of Business—Our Projects—Chile—Maricunga—POSCO” below.

|

|

|

·

|

In August 2010 we acquired 100% ownership of Alfredo Holdings, Ltd. (“Alfredo”), which, through its Chilean subsidiary, Pacific Road Mining Chile S.A. (“PRMC”), had an option to purchase mining concessions on approximately 6,670 acres (2,700 hectares) of mining tenements near Pozo Almonte, Chile (the “Alfredo Property”), prospective for saleable iodine and (aided by the potassium we expect to generate from our brine properties that are prospective for lithium) nitrate products. That option has terminated as a result of our not making the required option payments. As of the date of this Prospectus, we are not in discussions with the owners of Alfredo to reacquire the option to purchase the Alfredo Property, and there can be no assurance that a new option will be executed. We are also actively exploring opportunities to acquire other iodine/sodium nitrate prospects in addition to or in lieu of the Alfredo property; however, there can be no assurance that suitable prospects will be available on terms acceptable to us or that any such acquisition will be successfully completed. We have not undertaken any exploration and development activities on the Alfredo Property. See “Description of Business—Our Projects—Chile—Alfredo” below.

|

|

|

·

|

In July 2010 we acquired 100% ownership of Noto Energy S.A., an Argentinean corporation (“Noto”), which beneficially owns a 100% interest over 2,995 acres (1,212 hectares) situated on brine salars in Argentina, known as Cauchari. We are in the process of evaluating the Noto property, but we currently do not anticipate spending material amounts on exploration work with respect to this project over the next 12 months. See “Description of Business—Our Projects—Argentina—Puna Lithium Corporation, Lacus Minerals S.A and Noto Energy S.A Transactions” below.

|

|

|

·

|

In February 2010, we acquired 100% of the assets of the Loriscota, Suches and Vizcachas projects located respectively in the Regions of Puno, Tacna and Moquegua, Peru. The assets consist of nine undeveloped mineral claims prospective for lithium and potassium covering a total area of 19,500 acres (7,890 hectares). We continue to evaluate these properties to determine if they meet our criteria, but we currently do not anticipate spending material amounts on exploration work with respect to these projects over the next 12 months. See “Description of Business—Our Projects—Peru” below.

|

|

|

·

|

We have determined that other properties we had acquired in Nevada and Argentina do not meet our integration and deposit criteria, and the options for these properties have been terminated.

|

Each of these acquisitions is described in more detail below.

To date, we have never generated revenue from operations and currently do not expect to generate any such revenues in the near term.

The life cycle of a brine mining operation can be divided into six phases:

|

|

·

|

Mining activity begins with the “exploration phase,” in which one seeks to define the type, extent, location and value of deposits and to estimate the grade and size of the deposits;

|

|

|

·

|

The exploration phase is followed by the “pre-feasibility phase,” in which the economics and risks of the project are determined;

|

|

|

·

|

The “feasibility phase” then ensues to address the financial viability of the project (including any permitting requirements) and to determine whether or not to proceed to development – the end of the feasibility stage is marked by the conclusion of a feasibility study;

|

|

|

·

|

If the decision is made to move forward after the feasibility stage, then the “development phase” follows, in which the infrastructure needed to begin operations is constructed;

|

|

|

·

|

Upon completion of such infrastructure, a project enters the “production phase,” during which the applicable minerals are extracted, produced and sold;

|

|

|

·

|

Once all economically extractable minerals have been produced, a mine is closed and it enters the “reclamation phase,” in which the area is made suitable for future uses.

|

Li3 is currently in the exploration phase, seeking to define the type, extent, location and value of deposits.

Strategic Plan

Our strategic plan is to explore and develop our existing projects and to identify opportunities and generate new projects with near-term production potential, with the goal of becoming a company with valuable lithium and other industrial minerals properties. Our primary objective is to become a low cost lithium producer as well as a significant producer of potassium nitrate. The key to achieving this objective is to become an integrated chemical company through the strategic acquisition and development of lithium assets as well as other assets that have by-product synergies.

2

We have acquired a 60% interest in the Maricunga project, an advanced lithium and potassium chloride project in Chile. We continue to explore other lithium and industrial minerals prospects in the region, in order to achieve integration of operations to produce metallurgical grade lithium, commercial grade fertilizer and pharmaceutical grade iodine.

We recorded an impairment charge to Alfredo of $4,070,000 during the year ended June 30, 2011, as a result of our not making required option payments and the consequent termination of the option.

Our strategy currently principally involves the exploration of the Maricunga property and the acquisition and exploration of the Alfredo property or another iodine/nitrate property. On the Maricunga project, we expect to spend approximately $18.2 million of exploration and development expenses in order to complete a feasibility study on Maricunga. (A “feasibility study” means a comprehensive study of a mineral deposit in which all geological, engineering, legal, operating, economic, social, environmental and other relevant factors are considered in sufficient detail that it could reasonably serve as the basis for a final decision whether to advance the development of the deposit for mineral production.) The Company is dividing this into two phases: (i) Spending $8 million to reach a Measured and Indicated 43-101compliant resource, which is expected in the first calendar quarter of 2012; and, if phase one is successful, (ii) spending $10 million to complete a feasibility study on Maricunga. If we are acquire the Alfredo Property, we would expect to spend approximately $6.3 million of acquisition costs (not including an additional up to $5.5 million payable to the Alfredo Sellers (as defined below) upon certain post-feasibility milestones), and we would expect to incur approximately $2.7 million of exploration expenses in order to bring the Alfredo Property to the feasibility stage. In the event we are unable to acquire the Alfredo Property, we will focus our efforts on the exploration of the Maricunga property, and we are actively exploring opportunities to acquire other iodine/sodium nitrate prospects in addition to or in lieu of the Alfredo property, although there can be no assurance that suitable prospects will be available on terms acceptable to us or that any such acquisition will be successfully completed.

In order to finance the up to approximately $15 million of expected acquisition and exploration costs outlined above over the next twelve months, as well as to fund the approximately $2.5 million of working capital we expect to require over the next twelve months, we will need to raise a substantial amount of funds through one or more offerings of our debt, equity or convertible securities, which may include the $10 million of equity financing conditionally committed by POSCAN. There can be no assurance that such financing will be available, or will be available on acceptable terms, for us to meet these requirements.

In order to acquire the Alfredo Property, we must successfully negotiate a new option or other acquisition agreement. There can be no assurance that we will be successful in obtaining a new option on, or otherwise acquiring, Alfredo or in financing the cost of acquiring the Alfredo Property or the costs of exploring and developing Maricunga and Alfredo.

We believe that successful execution of this first phase of our strategic acquisition program will establish Li3 Energy as a major holder of prime lithium, iodine and nitrate acreage among junior lithium explorers.

Lithium Exploitation Permitting Uncertainty

In Chile, where our Maricunga property is located, lithium is not exploitable via regular mining concessions. The Chilean Mining Code (“CMC”) establishes the reserve of lithium to the State of Chile and expressly provides that the exploration or exploitation of “non-concessible” substances (including lithium) can be performed only directly by the State of Chile, or its companies, or by means of administrative concessions or special operation contracts, fulfilling the requirements and conditions set forth by the President of the Republic of Chile for each case. Currently neither we nor our subsidiaries have sufficient authority (or permits) to explore and exploit lithium in Chile. However, the government of Chile has announced its intention to increase the exploitation of lithium in Chile, and it may seek to amend the law to allow exploitation by private enterprises. However, there can be no assurance that the government will be successful in these efforts (due to political and other considerations). Alternatively, the government may begin granting operating contracts to private companies such as Li3 Energy. The failure of the government to allow private exploitation of lithium within our development horizon for Maricunga would have a material adverse effect on our prospects.

Unlike exploitation permitting, exploration permitting is not mineral-specific in Chile. Therefore, our current exploratory activities, whether with respect to lithium or otherwise, are permitted. We believe we may be able to mitigate somewhat the risk of any inability to obtain permissions for lithium exploitation because (a) we expect to be able to exploit other minerals on our properties and (ii) we believe the current political environment in Chile favors the removal or reduction of legal impediments to lithium exploitation.

In Argentina, there has been a recent trend, at the National and Provincial levels, of seeking to limit and/or to restrict certain mining activities within the territory of certain Provinces. The Province of Jujuy, which is adjacent to the Province of Salta, where the Noto Properties are located, issued in March 2011 a Decree declaring lithium reserves as strategic natural resources for the Province, subjecting lithium exploration and exploitation projects to the evaluation of an Experts Committee, and the subsequent approval of different government bodies and the favorable recommendation of the Experts Committee. There can be no assurance that similar regulations won’t be issued in the Province of Salta.

In October 2010 the National Law No. 26,639, "Regime of Minimum Principles for the Preservation of Glaciers and Periglacial Environment" (the "Glaciers Law"), was promulgated. The Glaciers Law is aimed at the protection and preservation of glaciers and the periglacial environment. The Glaciers Law regulates, limits and in certain cases bans, certain activities developed on glacial and periglacial areas. Depending on how the Glaciers Law is interpreted – and, specifically, the definition of the term “periglacial” – this regulation could have a negative effect on the potential activities to be conducted on the Noto Properties.

We believe that we are in compliance with all material laws and regulations that currently apply to our activities but there can be no assurance that we can continue to remain in compliance. Current laws and regulations could be amended and we might not be able to comply with them, as amended. Further, there can be no assurance that we will be able to obtain or maintain all permits necessary for our future operations, or that we will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, we may be delayed or prohibited from proceeding with planned exploration or development of our mineral properties.

Until we complete our exploration activities and a feasibility study, we cannot be sure what minerals, if any, may be economically extracted from our properties. Accordingly, we cannot predict precisely what permits or other authorizations may be required to support our business plan. Furthermore, since we believe any Chilean permitting process with respect to lithium is likely to be done through an auction process, any cost estimate would be inherently speculative as well as harmful to our competitive position.

Capital Needs

As described above and as further discussed below under “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources, ” we expect to require an aggregate of approximately $17.5 million over the next twelve months to pay our acquisition, exploration and development costs associated with our projects as well as our currently anticipated general and administrative and other costs. Furthermore, if we succeed in acquiring any other projects, then we would expect to incur additional financial commitments with respect to such projects. As a result of the funds invested by investors in our April and May 2011 private placement and the funds invested by POSCAN on September 14, 2011, we estimate that we have sufficient funds to carry out our current strategic plan of exploration and development and meet our ongoing operational working capital needs through March 2012 (assuming we do not expend cash for other acquisitions). We plan to seek to raise additional capital through additional sales of our equity or debt securities. There can be no assurance, however, that such financing will be available to us or, if it is available, that it will be available on terms acceptable to us and that it will be sufficient to fund our expected needs. If we are unable to obtain sufficient financing, we may not be able to continue with our exploration and development plans, make additional acquisitions or meet our ongoing operational working capital needs.

Weaknesses in Internal Controls

Our management assessed the effectiveness of our internal control over financial reporting and disclosure controls and procedures as at June 30, 2011, and concluded that our internal control over financial reporting and disclosure controls and procedures were ineffective. Management concluded that the following were material weaknesses in our internal controls over financial reporting: (a) we did not maintain proper segregation of duties for the preparation of our financial statements, and (b) we have not established an Audit Committee of our Board independent of management. Although we intend to remediate such material weaknesses, we have not yet been able to address these material weaknesses and they may continue to remain unremedied for some time, which could adversely impact the accuracy and timeliness of future reports and filings we make to the SEC and compliance with any future listing standards and could have a material adverse effect on our business, results of operations, financial condition and liquidity.

Going Concern

We currently have no sources of recurring revenue, had working capital of $20,926 at March 31, 2011, and have generated net losses of $37,386,124 and negative cash flows from operations of $4,809,444 during the period from June 24, 2005 (inception) through March 31, 2011.

3

In the course of our exploration and development activities, we have sustained and continue to sustain losses. We do not anticipate positive cash flow from operations before 2013 and cannot predict if and when we may generate profits. In the event that we identify commercial reserves of minerals, we will require substantial additional capital to develop those reserves. We expect to finance our operations primarily through future issuances of securities. However, there exists substantial doubt about our ability to continue as a going concern because there is no assurance that we will be able to obtain such capital, through equity or debt financing, or any combination thereof, on satisfactory terms or at all. Additionally, no assurance can be given that any such financing, if obtained, will be adequate to meet our ultimate capital needs and to support our growth. If adequate capital cannot be obtained on a timely basis and on satisfactory terms, then our operations would be materially negatively impacted.

Our ability to complete additional equity or debt offerings is dependent on the state of the debt and/or equity markets at the time of any proposed offering, and such market’s reception of us and the offering terms. In addition, our ability to complete an offering may be dependent on the status of our exploration activities, which cannot be predicted. There is no assurance that capital in any form would be available to us, and if available, on terms and conditions that are acceptable.

These conditions raise substantial doubt about our ability to continue as a going concern. Our continuation as a going concern is dependent on our ability to meet our obligations and to obtain additional financing as may be required until such time as we can generate sources of recurring revenues and to ultimately attain profitability. Our consolidated financial statements included in this prospectus have been prepared in accordance with generally accepted accounting principles applicable to a going concern, which implies we will continue to meet our obligations and continue our operations for the next twelve months. Realization values may be substantially different from carrying values as shown, and our consolidated financial statements do not include any adjustments relating to the recoverability or classification of recorded asset amounts or the amount and classification of liabilities that might be necessary in the event we are unable to continue as a going concern. Additionally, our independent registered public accounting firm included an explanatory paragraph in their report on our consolidated financial statements for the year ended June 30, 2010, included in this prospectus, that raises substantial doubt about our ability to continue as a going concern.

About This Offering

This prospectus relates to the public offering, which is not being underwritten, of up to 42,797,958 outstanding shares of our common stock plus 40,838,832 shares of our common stock issuable upon the exercise of our outstanding warrants (described under Selling Stockholders below) by the selling stockholders listed in this prospectus. This prospectus shall also cover any additional shares of our common stock that shall become issuable by reason of any stock dividend, stock split, recapitalization or other similar transaction effected without the receipt of consideration that results in an increase in the number of the outstanding shares of our common stock.

The shares offered by this prospectus may be sold by the selling stockholders from time to time in the open market, through negotiated transactions or otherwise at market prices prevailing at the time of sale or at negotiated prices. We will receive none of the proceeds from the sale of the shares by the selling stockholders. However, we may receive the proceeds from the exercise of the warrants held by the selling stockholders, to the extent the warrants are not exercised on a cashless basis. We will bear all expenses of registration incurred in connection with this offering, but all selling and other expenses incurred by the selling stockholders will be borne by them.

The number of shares being offered by this prospectus (including the shares issuable upon exercise of our outstanding warrants) represents approximately 26.0% of our outstanding shares of common stock as of January 5, 2012.

Corporate Information and History

We were incorporated on June 24, 2005, in Nevada as Mystica Candle Corp. We were originally in the business of manufacturing, marketing and distributing soy-blend scented candles and oils, but we could not continue with those business operations because of a lack of financial results and resources. We have redirected our focus, therefore, towards identifying and pursuing options regarding the development of a new business plan and direction.

4

In 2008 we engaged in discussions with NanoDynamics, Inc., a Delaware corporation (“NanoDynamics”), regarding a possible business combination with NanoDynamics, and with the permission of NanoDynamics, we changed our name to NanoDynamics Holdings, Inc. to facilitate these discussions. We determined not to proceed with that business combination, however.

On October 19, 2009, we changed our name to Li3 Energy, Inc., to reflect our plans to focus our business strategy on the energy sector and related lithium mining opportunities in North and South America.

On February 23, 2010, we acquired 100% of the assets of the Loriscota, Suches and Vizcachas Projects located respectively in the Regions of Puno, Tacna and Moquegua, Peru. These projects consist solely of mineral claims and have, and have had, no operations or revenues.

Prior to this acquisition, we were a “shell company” (as such term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”)). As a result of the acquisition, we ceased to be a shell company. Since exiting “shell company” status, we have acquired certain additional assets and entered into certain agreements, as described in this prospectus.

Our principal executive offices are located at Av. Pardo y Aliaga 699, Oficina 802, San Isidro, Lima, Peru, and our telephone number at our principal executive offices is (51) 1-212-1880. Our website address is www.li3energy.com; however, the material included in our website does not constitute a part of this prospectus and should not be relied on by prospective purchasers in the offering. Our fiscal year end is June 30.

All common stock share and per share numbers herein give retroactive effect to our 3.031578-for-1 forward stock split in the form of a dividend which was effected on July 29, 2008, and our 15.625-for-1 forward stock split in the form of a dividend which was effected on November 16, 2009, unless otherwise stated.

5

Summary Financial Information

The following tables summarize historical financial data regarding our business and should be read together with the information in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included in this prospectus.

|

Fiscal Year Ended

June 30,

|

Three Months Ended

September 30,

|

June 24,

2005

(inception)

Through

September 30,

2011

|

||||||||||||||||||

|

2011

|

2010

|

2011

|

2010

|

(unaudited)

|

||||||||||||||||

|

(unaudited)

|

(unaudited)

|

|||||||||||||||||||

|

Statement of Operations Data

|

||||||||||||||||||||

|

Revenues

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

2,278

|

||||||||||

|

Gross profit

|

-

|

-

|

-

|

-

|

1,096

|

|||||||||||||||

|

Total operating expenses

|

11,626,242

|

9,816,666

|

1,718,438

|

1,103,869

|

23,351,326

|

|||||||||||||||

|

Change in fair value of derivative liability – warrant instruments

|

6,116,147

|

6,223,547

|

(6,948,644

|

)

|

(2,772,726

|

)

|

5,391,050

|

|||||||||||||

|

Net income (loss)

|

(19,219,382

|

)

|

(16,048,682)

|

3,839,980

|

1,663,543

|

(31,621,794

|

)

|

|||||||||||||

|

Statement of Cash Flows Data

|

||||||||||||||||||||

|

Cash used in operating activities

|

$

|

(3,594,823

|

)

|

$

|

(2,377,417)

|

$

|

(1,052,692

|

)

|

$

|

(606,968

|

)

|

$

|

(7,198,229

|

)

|

||||||

|

Cash used in investing activities

|

(6,550,000

|

)

|

(1,418,785)

|

(56,845

|

)

|

(180,000

|

)

|

(8,045,130

|

)

|

|||||||||||

|

Cash provided by financing activities

|

10,794,403

|

4,089,320

|

7,484,069

|

487,998

|

22,475,292

|

|||||||||||||||

|

At June 30,

|

At September 30,

|

|||||||||||

|

2011

|

2010

|

2011

|

||||||||||

|

(unaudited)

|

||||||||||||

|

Balance Sheet Data

|

||||||||||||

|

Total current assets

|

$

|

1,097,460

|

$

|

359,297

|

$

|

7,458,126

|

||||||

|

Total assets

|

65,138,460

|

703,243

|

71,554,684

|

|||||||||

|

Total current liabilities

|

1,271,770

|

1,745,321

|

2,747,825

|

|||||||||

|

Total liabilities

|

16,516,524

|

9,775,049

|

14,261,948

|

|||||||||

|

Total shareholders’ equity (deficit)

|

48,621,936

|

(9,071,806

|

)

|

57,292,736

|

||||||||

6

THE OFFERING

|

Common stock currently outstanding

|

322,209,220 shares (1)

|

|

|

Common stock offered by the Company

|

None

|

|

|

Common stock offered by the selling stockholders

|

83,636,790 shares (2)

|

|

|

Use of proceeds

|

We will not receive any of the proceeds from the sales of our common stock by the selling stockholders. However, we may receive the proceeds from the exercise of the warrants held by the selling stockholders, to the extent the warrants are not exercised on a cashless basis.

|

|

|

OTCBB symbol

|

LIEG

|

|

|

Risk Factors

|

You should carefully consider the information set forth in this prospectus and, in particular, the specific factors set forth in the “Risk Factors” section beginning on page 9 of this prospectus before deciding whether or not to invest in shares of our common stock.

|

|

(1)

|

As of January 5, 2012. Does not include 2,000,000 shares of restricted stock which remain subject to certain vesting milestones.

|

|

(2)

|

Consists of 42,797,958 issued and outstanding shares of common stock and 40,838,832 shares of common stock issuable upon the exercise of outstanding warrants (described under Selling Stockholders below).

|

7

NOTE REGARDING FORWARD-LOOKING STATEMENTS

Various statements in this prospectus, including those that express a belief, expectation or intention, as well as those that are not statements of historical fact, are forward-looking statements. The forward-looking statements may include projections and estimates concerning the timing and success of specific projects, revenues, income and capital spending. We generally identify forward-looking statements with the words “believe,” “intend,” “expect,” “seek,” “may,” “should,” “anticipate,” “could,” “estimate,” “plan,” “predict,” “project” or their negatives, and other similar expressions. All statements we make relating to our estimated and projected earnings, margins, costs, expenditures, cash flows, growth rates, financial results and project developments and acquisitions or to our expectations regarding future industry or economic trends are forward-looking statements.

These forward-looking statements are subject to risks and uncertainties that may change at any time, and, therefore, our actual results may differ materially from those that we expect. The forward-looking statements contained in this prospectus are largely based on our expectations, which reflect many estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe such estimates and assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors and it is impossible for us to anticipate all factors that could affect our actual results. In addition, management’s assumptions about future events may prove to be inaccurate. Management cautions all readers that the forward-looking statements contained in this prospectus are not guarantees of future performance, and we cannot assure any reader that such statements will be realized or the forward looking events and circumstances will occur. Actual results may differ materially from those anticipated or implied in the forward-looking statements due to the factors listed in the “Risk Factors” section and elsewhere in this prospectus. All forward-looking statements are based upon information available to us on the date of this prospectus. We undertake no obligation to update or revise any forward-looking statements as a result of new information, future events or otherwise, except as otherwise required by law. These cautionary statements qualify all forward-looking statements attributable to us, or persons acting on our behalf.

8

RISK FACTORS

An investment in shares of our common stock is highly speculative and involves a high degree of risk. We face a variety of risks that may affect our operations or financial results and many of those risks are driven by factors that we cannot control or predict. Before investing in our common stock you should carefully consider the following risks, together with the financial and other information contained in this prospectus. If any of the following risks actually occurs, our business, prospects, financial condition and results of operations could be materially adversely affected. In that case, the trading price of our common stock would likely decline and you may lose all or a part of your investment. Only those investors who can bear the risk of loss of their entire investment should participate in this offering.

RISKS RELATED TO OUR BUSINESS AND FINANCIAL CONDITION

We are an exploration stage company and have no revenues. Our business plan depends on our ability to explore for and develop mineral reserves and place any such reserves into extraction. Because we have a limited operating history, it is difficult to predict our future performance.

Although we were formed in June 2005, we have been and continue to be an exploration stage company. Therefore, we have limited operating and financial history available to help potential investors evaluate our past performance and the risks of investing in us. Moreover, our limited historical financial results may not accurately predict our future performance. Companies in their initial stages of development present substantial business and financial risks and may suffer significant losses. As a result of the risks specific to our new business and those associated with new companies in general, it is possible that we may not be successful in implementing our business strategy.

We have generated no revenues to date and do not anticipate generating any revenues in the near term. Our activities to date have been limited to capital formation, organization, acquisition of interests in mining properties and limited exploration on our projects, including digging and sampling of test pits and brine analysis on our Maricunga property. We have yet to generate positive earnings and there can be no assurance that we will ever operate profitably. Our success is significantly dependent on a successful exploration, mining and production program. Our operations will be subject to all the risks inherent in the establishment of a developing enterprise and the uncertainties arising from the absence of a significant operating history. We may be unable to locate exploitable quantities of mineral resources or operate on a profitable basis. We are in the exploration stage and potential investors should be aware of the difficulties normally encountered by enterprises in the exploration stage. If our business plan is not successful, and we are not able to operate profitably, investors may lose some or all of their investment in our Company.

Our past losses raise doubt about our ability to continue as a going concern.

The Consolidated Financial Statements contained herein have been prepared assuming we will continue as a going concern. We currently have no sources of recurring revenue, and have generated net losses of $31,621,794 and negative cash flows from operations of $7,198,229 during the period from June 24, 2005 (inception) through September 30, 2011. We cannot predict if and when we may generate profits. As a result of the funds invested by investors in our April and May 2011 private placement and the funds invested by POSCAN on September 14, 2011, we estimate that we have sufficient funds to carry out our current strategic plan of exploration and development and meet our ongoing operational working capital needs through March 2012 (assuming we do not expend cash for other acquisitions). After that, we expect to finance our operations primarily through future sales of our equity or debt securities. However, as discussed in the notes to our Consolidated Financial Statements included in this prospectus, there exists substantial doubt about our ability to continue as a going concern because there is no assurance that we will be able to obtain such capital, through equity or debt financing, or any combination thereof, on satisfactory terms or at all. The Consolidated Financial Statements do not include any adjustments that might result from the outcome of this uncertainty.

Our option on the Alfredo Property has expired, and we are not currently negotiating to acquire a new option.

Under the option for the Alfredo Property, our subsidiary PRMC was required to make periodic payments aggregating $360,000 between June 30, 2010 and December 30, 2010. We paid $80,000 in August 2010 and were required to make payments of $100,000 by October 30, 2010, and $180,000 by December 30, 2010, in order to maintain our option rights. Then, in order to exercise the option and purchase the Alfredo Property, we would have been required to pay the option exercise price of $4,860,000 by March 30, 2011. We did not make the $100,000 payment on October 30, 2010, the $180,000 payment on December 30, 2010 or the option exercise price payment of $4,860,000 on March 30, 2011. Under the terms of the option agreement, the option terminated as a result of our not making the required option payments within the specified default and cure periods, and we therefore recorded impairment expense for the Alfredo property of $4,070,000 during the year ended June 30, 2011. Although we have had some discussions with the owners of the Alfredo Property to reacquire the option to purchase the Alfredo Property on modified terms, as of the date of this prospectus we are not actively negotiating a new option, and there can be no assurance that any new option will be executed. We are actively exploring opportunities to acquire other iodine/sodium nitrate prospects in addition to or in lieu of the Alfredo property; however, there can be no assurance that suitable prospects will be available on terms acceptable to us or that any such acquisition will be successfully completed.

9

We have not made certain scheduled payments under agreements with respect to certain properties we were considering acquiring. If we are deemed to be liable for such payments (and/or damages arising out of their non-payment), then our business, financial condition and prospects could be materially adversely affected.

Pursuant to our Option Agreements with GeoXplor Corp. on the Nevada Claims, we were required to make periodic and milestone payments and also to maintain the relevant mineral claims in good standing for certain time periods. We failed to make a periodic payment of $100,000 due on June 30, 2010. During the year ended June 30, 2011, we became obligated to pay approximately $57,000 of claim maintenance fees on the Nevada Claims and approximately $32,600 of Nevada state taxes, which we have not paid.

If and to the extent we are found liable for, or deliver value in settlement of, any claims that may arise from the foregoing, and/or our expenses related to those matters become significant, then our business, financial condition and prospects could be materially adversely affected and the value of our stockholders' interests in us could be impaired.

All of our properties are in the exploration stage. Investment in exploration projects increases the risks inherent in our mining activities. There is no assurance that we can establish the existence of any mineral resource on any of our properties in commercially exploitable quantities, and our mining operations may not be successful.

We have not established that any of our mineral properties contains any meaningful levels of mineral reserves. There can be no assurance that future exploration and mining activities will be successful.

A mineral reserve is defined by the SEC in its Industry Guide 7 (which can be viewed at http://www.sec.gov/divisions/corpfin/forms/industry.htm#secguide7 ) as that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. There can be no assurance that we will ever establish any mineral reserves.

Even if we do eventually discover a meaningful mineral reserve on one or more of our properties, there can be no assurance that we will be able to develop our properties into producing mines and extract those resources. Both mineral exploration and development involve a high degree of risk and few properties which are explored are ultimately developed into producing mines. Furthermore, we cannot be sure that an overall exploration success rate or extraction operations within a particular area will ever come to fruition and, in any event, production rates inevitably decline over time. The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the resource to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral resource unprofitable.

We have limited financial resources and may not be able to fund our anticipated exploration activities. If we are unable to fund our exploration activities, our potential profitability will be adversely affected.

Our anticipated exploration activities will require financial resources substantially in excess of our current working capital. If we are not able to finance our exploration activities, then we will be unable to identify commercially exploitable resources even if present on our properties. If we fail to adequately support our exploration activities, it could have a material adverse effect on our results of operations and the market price of our shares. There can be no assurance that capital will be available to us when needed, on favorable terms or at all.

10

Mineral operations are subject to applicable law and government regulation. Even if we discover a mineral resource in a commercially exploitable quantity, these laws and regulations could restrict or prohibit the exploitation of that mineral resource.

Both mineral exploration and extraction require permits from various foreign, federal, state, provincial and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. There can be no assurance that we will be able to obtain or maintain any of the permits required for the continued exploration of our mineral properties or for the construction and operation of a mine on our properties at economically viable costs.

In Chile, lithium is not exploitable via regular mining concessions. The Chilean Mining Code (“CMC”) establishes the reserve of lithium to the State of Chile and expressly provides that the exploration or exploitation of “non-concessible” substances (including lithium) can be performed only directly by the State of Chile, or its companies, or by means of administrative concessions or special operation contracts, fulfilling the requirements and conditions set forth by the President of the Republic of Chile for each case. Currently neither the Company nor its subsidiaries have sufficient authority (or permits) to explore and exploit lithium in Chile. However, the government of Chile has announced its intention to increase the exploitation of lithium in Chile, and it may seek to amend the law to allow exploitation by private enterprises. However, the approval of a two-thirds majority of the Chilean Congress will be required to amend the existing law, and there can be no assurance that the government will be successful in these efforts (due to political and other considerations). Alternatively, the government may begin granting operating contracts to private companies such as Li3 Energy. The failure of the government to allow private exploitation of lithium within our development horizon for Maricunga would have a material adverse effect on our prospects. Unlike exploitation permitting, exploration permitting is not mineral specific in Chile. Accordingly, there can be no assurance that we will be able to obtain the permits necessary to exploit any minerals that our exploration activities discover.

There has been a recent trend in Argentina, at the National and Provincial levels, of seeking to limit and/or to restrict certain mining activities within the territory of certain Provinces.

The Province of Jujuy, which is adjacent to the Province of Salta, where the Noto Properties are located, issued in March 2011 a Decree declaring lithium reserves as strategic natural resources for the Province, subjecting lithium exploration and exploitation projects to the evaluation of an Experts Committee, and the subsequent approval of different government bodies and the favorable recommendation of the Experts Committee. There can be no assurance that similar regulations won’t be issued in the Province of Salta.

In October 2010 the National Law No. 26,639, "Regime of Minimum Principles for the Preservation of Glaciers and Periglacial Environment" (the "Glaciers Law"), was promulgated. The Glaciers Law is aimed at the protection and preservation of glaciers and the periglacial environment. The Glaciers Law regulates, limits and in certain cases bans, certain activities developed on glacial and periglacial areas. Depending on how the Glaciers Law is interpreted – and, specifically, the definition of the term “periglacial” – this regulation could have a negative effect on the potential activities to be conducted on the Noto Properties.

We believe that we are in compliance with all material laws and regulations that currently apply to our activities but there can be no assurance that we can continue to remain in compliance. Current laws and regulations could be amended and we might not be able to comply with them, as amended. Further, there can be no assurance that we will be able to obtain or maintain all permits necessary for our future operations, or that we will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, we may be delayed or prohibited from proceeding with planned exploration or development of our mineral properties.

Argentinean foreign exchange regulations may make it difficult to transfer funds in and out of Argentina, which could adversely affect our liquidity and operations.

Argentinean foreign exchange regulations impose numerous restrictions to the transfer of funds in and out of the territory of Argentina. Additional restrictions on the ability to access the Argentinean foreign exchange market and transfer foreign currency in and out of Argentina could adversely affect our liquidity and operations in Argentina and, to the extent we generate funds from activities in Argentina, our ability to access such funds.

If we establish the existence of a mineral resource on any of our properties in a commercially exploitable quantity, we will require additional capital in order to develop the property into a producing mine. If we are unable to obtain additional funding, our business operations will be harmed and if we do obtain additional financing, existing shareholders may suffer substantial dilution.

If we do discover mineral resources in commercially exploitable quantities on any of our properties, we will be required to expend substantial sums of money to establish the extent of the resource, develop processes to extract it and develop extraction and processing facilities and infrastructure. Although we may derive substantial benefits from the discovery of a major deposit, there can be no assurance that such a resource will be large enough to justify commercial operations, nor can there be any assurance that we will be able to raise the funds required for development on a timely basis.

We have raised some capital to date, including through the sale of equity securities and convertible notes, but we currently do not have any contracts or firm commitments for additional financing. There can be no assurance that additional financing will be available in amounts or on terms acceptable to us, if at all. An inability to obtain additional capital would restrict our ability to grow and could diminish our ability to continue to conduct our business operations. If we are unable to obtain additional financing, we will likely be required to curtail exploration and development plans and possibly cease operations. Any additional equity financing may involve substantial dilution to then existing shareholders.

Newer battery and/or fuel cell technologies could decrease demand for lithium over time.

Many materials and technologies are being researched and developed with the goal of making batteries lighter, more efficient, faster charging and less expensive. Some of these technologies could be successful and could impact demand for lithium batteries in personal electronics, electric and hybrid vehicles and other applications. Advances in nanotechnology, in particular, offer the prospect of significantly better batteries in the future. For example, researchers at Stanford University have recently demonstrated ultra-lightweight, bendable batteries and supercapacitors made from paper coated with ink made of carbon nanotubes and silver nanowires; the material charges and discharges very quickly, making it potentially useful in hybrid and electric vehicles, which need rapid power for acceleration and would benefit from quicker charging than is available with current technologies. We cannot predict which new technologies may ultimately prove to be commercializable and on what time horizon. While lithium battery technology is currently among the best available for electronics, vehicles and other applications, commercialized battery technologies that offer superior weight, capacity, charging time and/or cost could significantly adversely affect the demand for lithium in the future and thus could significantly adversely impact our prospects and future revenues.

11

Mineral exploration and development is subject to extraordinary operating risks. We do not currently insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which could have an adverse impact on us.

Mineral exploration, development and production involve many risks which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Our operations will be subject to all the hazards and risks inherent in the exploration for mineral resources and, if we discover a mineral resource in commercially exploitable quantity, our operations could be subject to all of the hazards and risks inherent in the development and production of resources, including liability for pollution, cave-ins or similar hazards against which we cannot insure or against which we may elect not to insure. Any such event could result in work stoppages and damage to property, including damage to the environment. We do not currently maintain any insurance coverage against these operating hazards. The payment of any liabilities that arise from any such occurrence would have a material adverse impact on us.

Lithium, iodine and nitrates prices are subject to unpredictable fluctuations.

We may derive revenues, if any, either from the extraction and sale of lithium, iodine and potassium nitrate, as well as other potentially economic salts produced from the lithium salar brines, or from the sale of our mineral resource properties. The price of these commodities may fluctuate widely, and is affected by numerous factors beyond our control, including international, economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumptive patterns, speculative activities, increased production due to new extraction developments and improved extraction and production methods and technological changes in the markets for the end products. The effect of these factors on the price of these minerals, and therefore the economic viability of any of our exploration properties and projects, cannot accurately be predicted.

The mining industry is highly competitive, and we face competition from many established domestic and foreign companies. We may not be able to compete effectively with these companies.

The markets in which we operate are highly competitive. The mineral exploration, development, and production industry is largely un-integrated. We compete against numerous well-established national and foreign companies in every aspect of the mineral mining industry. Some of our competitors have longer operating histories and greater technical facilities, and significantly greater recognition in the market and financial and other resources, than we. We may not compete effectively with other exploration companies in locating and acquiring mineral resource properties, and customers may not buy any or all of the mineral products that we expect to produce.

Because we are small and do not have much capital, we may have to limit our exploration and developmental mining activity which may result in a loss of your investment.

Because we are a small exploration stage company and do not have much capital, we must limit our exploration and production activity. As such, we may not be able to complete an exploration program that is as thorough as we would like. In that event, existing reserves may go undiscovered. Without finding reserves, we cannot generate revenues and you may lose any investment you make in our shares.

Compliance with environmental and other government regulations could be costly and could negatively impact production.

Our operations are subject to numerous federal, state and local laws and regulations governing the operation and maintenance of our facilities and the discharge of materials into the environment or otherwise relating to environmental protection. These laws and regulations may:

|

|

•

|

require that we acquire permits before commencing extraction operations;

|

|

|

•

|

restrict the substances that can be released into the environment in connection with mining and extraction activities;

|

|

|

•

|

limit or prohibit mining activities on protected areas such as wetland or wilderness areas; and

|

|

|

•

|

require remedial measures to mitigate pollution from former operations, such as dismantling abandoned production facilities.

|

12

Under these laws and regulations, we could be liable for personal injury and clean-up costs and other environmental and property damages, as well as administrative, civil and criminal penalties. We do not believe that insurance coverage for environmental damages that occur over time is available at a reasonable cost, and we do not maintain any such insurance. Also, we do not believe that insurance coverage for the full potential liability that could be caused by sudden and accidental environmental damages is available at a reasonable cost. Accordingly, we may be subject to liability or we may be required to cease production (subsequent to any commencement) from properties in the event of environmental damages.

We may be unable to amend the mining claims that we are seeking to acquire to cover the primary minerals that we plan to develop.

Our business plan includes acquisition, exploration and development of lithium brine properties. However, we may pursue this goal by acquiring salt-mining claims and/or options or other interests in salt-mining claims or other types of claims, which we intend to seek to have amended to cover lithium extraction. There can be no assurance that we will be successful in amending any such claims timely, economically or at all. See Risk Factors – “Mineral operations are subject to applicable law and government regulation. . .,” above.

We may have difficulty managing growth in our business.

Because of the relatively small size of our business, growth in accordance with our long-term business plans, if achieved, will place a significant strain on our financial, technical, operational and management resources. As we increase our activities and the number of projects we are evaluating or in which we participate, there will be additional demands on our financial, technical, operational and management resources. The failure to continue to upgrade our technical, administrative, operating and financial control systems or the occurrence of unexpected expansion difficulties, including the recruitment and retention of required personnel could have a material adverse effect on our business, financial condition and results of operations and our ability to timely execute our business plan.

If we are unable to keep our key management personnel, then we are likely to face significant delays at a critical time in our corporate development and our business is likely to be damaged.

Our success depends upon the skills, experience and efforts of our management and other key personnel, including our Chief Executive Officer. As a relatively new company, much of our corporate, scientific and technical knowledge is concentrated in the hands of a few individuals. We do not have employment agreements with any of our employees other than our Chief Executive Officer and our Chief Operating Officer. We do not maintain key-man life insurance on any of our management or other key personnel. The loss of the services of one or more of our present management or other key personnel could significantly delay our exploration and development activities as there could be a learning curve of several months or more for any replacement personnel. Furthermore, competition for the type of highly skilled individuals we require is intense and we may not be able to attract and retain new employees of the caliber needed to achieve our objectives. Failure to replace key personnel could have a material adverse effect on our business, financial condition and operations.

Our Interim Chief Financial Officer has other substantial business activities that limit the amount of time that he can devote to managing our business.

Our Interim Chief Financial Officer, Eric E. Marin, currently serves as the Interim Chief Financial Officer of another publicly traded company, and has other business interests. Accordingly, Mr. Marin is only able to devote a portion of his time to our activities. This may make it more difficult for our management to respond quickly and completely to challenges and opportunities that we may encounter, may limit our ability to timely consummate strategic transactions and may have an adverse effect on our results of operations.

13

Difficult conditions in the global capital markets may significantly affect our ability to raise additional capital to continue operations.

The ongoing worldwide financial and credit upheaval may continue indefinitely. Because of reduced market liquidity, we may not be able to raise additional capital when we need it. Because the future of our business will depend on our ability to explore and develop the mineral resources on our existing properties and to complete the acquisition of one or more additional mineral resource properties for which, most likely, we will need additional capital, we may not be able to complete such development and acquisition projects or develop or acquire revenue producing assets. As a result, we may not be able to generate income and, to conserve capital, we may be forced to curtail our current business activities or cease operations entirely.

Being a public company has increased our expenses and administrative workload.

As a public company, we must comply with various laws and regulations, including the Sarbanes-Oxley Act of 2002 and related rules of the SEC. Complying with these laws and regulations requires the time and attention of our board of directors and management, and increases our expenses. Among other things, we must:

|

|

•

|

maintain and evaluate a system of internal control over financial reporting in compliance with the requirements of Section 404 of the Sarbanes-Oxley Act and the related rules and regulations of the SEC and the Public Company Accounting Oversight Board;

|

|

|

•

|

maintain policies relating to disclosure controls and procedures;

|

|

|

•

|

prepare and distribute periodic reports in compliance with our obligations under federal securities laws;

|

|

|

•

|

institute a more comprehensive compliance function, including with respect to corporate governance; and

|

|

|

•

|

involve to a greater degree our outside legal counsel and accountants in the above activities.

|

In addition, being a public company has made it more expensive for us to obtain director and officer liability insurance. In the future, we may be required to accept reduced coverage or incur substantially higher costs to obtain this coverage. These factors could also make it more difficult for us to attract and retain qualified executives and members of our board of directors, particularly directors willing to serve on an audit committee which we expect to establish.

RISKS RELATED TO OUR COMMON STOCK

There is not now, and there may not ever be, an active market for our common stock.

There currently is a limited public market for our common stock. Further, although our common stock is currently quoted on the OTC Bulletin Board (the “OTCBB”), trading of our common stock may be extremely sporadic. For example, several days may pass before any shares may be traded. As a result, an investor may find it difficult to dispose of, or to obtain accurate quotations of the price of, our common stock. Accordingly, investors must assume they may have to bear the economic risk of an investment in our common stock for an indefinite period of time. There can be no assurance that a more active market for our common stock will develop, or if one should develop, there is no assurance that it will be sustained. This severely limits the liquidity of our common stock, and would likely have a material adverse effect on the market price of our common stock and on our ability to raise additional capital.

We cannot assure you that our common stock will become liquid or that it will be listed on a securities exchange.

Until our common stock is listed on a national securities exchange such as the New York Stock Exchange or the Nasdaq National Market, we expect our common stock to remain eligible for quotation on the OTCBB, or on another over-the-counter quotation system. In those venues, however, an investor may find it difficult to obtain accurate quotations as to the market value of our common stock. In addition, if we fail to meet the criteria set forth in SEC regulations, various requirements would be imposed by law on broker-dealers who sell our securities to persons other than established customers and accredited investors. Consequently, such regulations may deter broker-dealers from recommending or selling our common stock, which may further affect the liquidity of our common stock. This would also make it more difficult for us to raise capital.

14

Our common stock is subject to the “penny stock” rules of the SEC and FINRA’s sales practice requirements, and the trading market in our common stock is limited, which makes transactions in our common stock cumbersome and may reduce the value of an investment in the stock.

The SEC has adopted Rule 15g-9 which establishes the definition of a “penny stock,” for the purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require:

|

|

•

|

that a broker or dealer approve a person’s account for transactions in penny stocks; and

|

|

|

•

|

the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased.

|

In order to approve a person’s account for transactions in penny stocks, the broker or dealer must:

|

|

•

|

obtain financial information and investment experience objectives of the person; and

|

|

|

•

|

make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks.

|

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the SEC relating to the penny stock market, which, in highlight form sets forth:

|

|

•

|

the basis on which the broker or dealer made the suitability determination; and

|

|

|

•

|

that the broker or dealer received a signed, written agreement from the investor prior to the transaction.

|

Generally, brokers may be less willing to execute transactions in securities subject to the “penny stock” rules. This may make it more difficult for investors to dispose of common stock and cause a decline in the market value of stock.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.