Attached files

| file | filename |

|---|---|

| 8-K - Delek US Holdings, Inc. | a8-kinvestormarketing11x11.htm |

Investor Presentation

November 2011

Safe Harbor ProvisionDelek US Holdings is traded on the New York Stock Exchange in the United States under the symbol “DK” and, as such, is governed by the rules and regulations of the United States Securities and Exchange Com mission. This presentation may contain forward-looking statements that are based upon current expectations and involve a number of risks and uncertainties. Statements concerning our current estimates, expectations and projections about our future results, performance, prospects and opportunities and other statements, concerns, or matters that are not historical facts are “forward-looking statements,” as that term is defined under United States securities laws.

Safe Harbor ProvisionDelek US Holdings is traded on the New York Stock Exchange in the United States under the symbol “DK” and, as such, is governed by the rules and regulations of the United States Securities and Exchange Com mission. This presentation may contain forward-looking statements that are based upon current expectations and involve a number of risks and uncertainties. Statements concerning our current estimates, expectations and projections about our future results, performance, prospects and opportunities and other statements, concerns, or matters that are not historical facts are “forward-looking statements,” as that term is defined under United States securities laws. Investors are cautioned that the following important factors, among others, may affect these forward-looking statements. These factors include but are not limited to: management’s ability to execute its strategy of growth through acquisitions and transactional risks in acquisitions; our competitive position and the effects of competition; the projected growth of the industry in which we operate; changes in the scope, costs, and/or timing of capital projects; losses from derivative instruments; general economic and business conditions, particularly levels of spending relating to travel and tourism or conditions affecting the southeastern United States; risks and uncertainties with the respect to the quantities and costs of crude oil, the costs to acquire feedstocks and the price of the refined petroleum products we ultimately sell; potential conflicts of interest between our majority stockholder and other stockholders; and other risks contained in our filings with the Securities and Exchange Commission.

Forward-looking statements should not be read as a guarantee of future performance or results and will not be accurate indications of the times at, or by which such performance or results will be achieved. Forward-looking information is based on information available at the time and/or management’s good faith belief with respect to future events, and is subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in the statements. Delek US undertakes no obligation to update or revise any such forward-looking statements.

Integrated Downstream Energy Company(1) Breadth of Exposure Across Refining, Wholesale Marketing and Retail Distribution Refining Segment Operates 140,000 BPD of refined production capacity in Texas and Arkansas Marketing Segment Owned product terminals and pipeline assets in Texas, Arkansas and Tennessee Retail Segment 384 convenience stores -- primarily in Tennessee, Alabama and Georgia Strategically Located Refineries Allow For Broad Wholesale and Retail Product Distribution Opportunities Own more than 600,000 barrels of crude storage (tank farm) capacity in Longview, Texas El Dorado Refinery 80,000 BPD 9.0 complexity Tyler Refinery 60,000 BPD 9.4 complexity (1) As of September 30, 2011

Integrated Downstream Energy Company(1) Breadth of Exposure Across Refining, Wholesale Marketing and Retail Distribution Refining Segment Operates 140,000 BPD of refined production capacity in Texas and Arkansas Marketing Segment Owned product terminals and pipeline assets in Texas, Arkansas and Tennessee Retail Segment 384 convenience stores -- primarily in Tennessee, Alabama and Georgia Strategically Located Refineries Allow For Broad Wholesale and Retail Product Distribution Opportunities Own more than 600,000 barrels of crude storage (tank farm) capacity in Longview, Texas El Dorado Refinery 80,000 BPD 9.0 complexity Tyler Refinery 60,000 BPD 9.4 complexity (1) As of September 30, 2011

Recent Financial Performance Growth In Contribution Margin ($MM)(1,2,3) Refining Contribution Margin ($MM) Retail, Marketing & Other Contribution Margin ($MM) $124.4mm $138.5mm $103.3mm $400.4 mm NME 2008 NME 2009 NME 2010 NME 2011 Substantial Growth In Net Income ($MM)(2,3) “Golden Age” of Refining (2006-2007) $91.5 mm 2006 $95.5 mm 2007 Generated Record Net Income During the Nine Months Ended 2011 $16.9 mm 1Q11 $54.9 mm 2Q11 $92.5 mm 3Q11 $164.3 mm NME 2011 Segment contribution margin = net sales less cost of sales and operating expenses, excluding depreciation and amortization. Periods are for the nine months ended Sept. 30, 2011. Represents net income from continuing operations

Delek US assumed operational control of the El Dorado refinery and related assets through the acquisition of a majority equity interest in Lion Oil on April 29, 2011

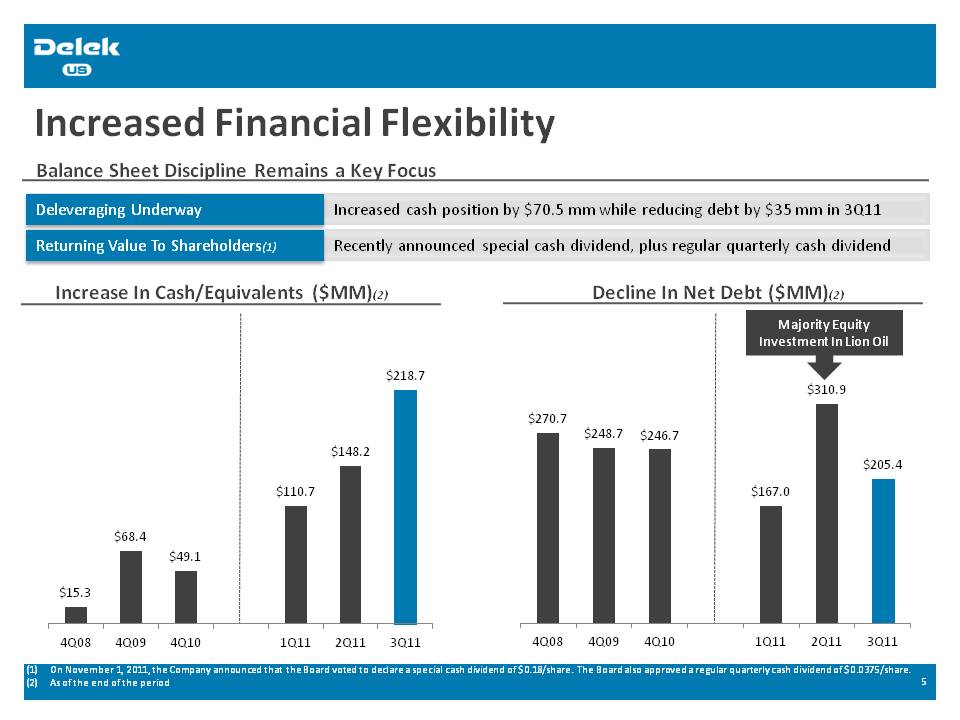

Increased Financial Flexibility Balance Sheet Discipline Remains a Key Focus Deleveraging Underway Increased cash position by $70.5 mm while reducing debt by $35 mm in 3Q11 Returning Value To Shareholders(1) Recently announced special cash dividend, plus regular quarterly cash dividend Increase In Cash/Equivalents ($MM)(2) $15.3 4Q08 $68.4 4Q09 $49.1 4Q10 $110.7 1Q11 $148.2 2Q11 $218.7 3Q11 Decline in Net Debt ($MM)(2) $270.7 4Q08 $248.7 4Q09 $246.7 4Q10 $167.0 1Q11 $310.9 2Q11 $205.4 3Q11 Major Equity Investment in Lion Oil On November 1, 2011, the Company announced that the Board voted to declare a special cash dividend of $0.18/share. The Board also approved a regular quarterly cash dividend of $0.0375/share. As of the end of the period

Financial Snapshot | Third Quarter 2011Executive Summary Reported Record Quarterly Profit Generated a record $92.5 million in net income Strong Benefit From Refining Segment Refining segment generated approximately 90% of total contribution margin Optimized Production, Product Sales Both Tyler and El Dorado operated near nameplate capacity Strong Gulf Coast Refining Economics Gulf Coast 532 crack spread was above $30/bbl, vs. $7.45/bbl in prior year period Benefit From Improved Refining Margins, Addition of El Dorado Sales Volumes(1) Tyler Sales Volumes El Dorado Sales Volumes Gulf Coast 5-3-2 Crack Spread/bbl Total Sales Volumes (BPD) 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 46,500 bpd 3Q10 54,405 bpd 4Q10 58,261 bpd 1Q11 127,962 bpd 2Q11 142,237 bpd 3Q11 $0.00 $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 Crack Spread Per Barrel (1) Crack spread calculation based on data supplied by Platts

Identified “Quick-Hit” Capital Projects

Low-Cost, High-Return Capital Projects at Tyler and El Dorado(1) LSR/Sat Gas Project (LSR) Scope: Improves liquid recovery of Butane & Propane at El Dorado Anticipated Cost: $16 million Anticipated Return: $20 million contribution margin annually Anticipated Completion: Third Quarter 2012 Vacuum Tower Bottoms Project (VTB)(2) Scope: Convert El Dorado asphalt to light product via Coker at Tyler Anticipated Cost: $5 million Anticipated Return: $10 million contribution margin annually Anticipated Completion: Third Quarter 2012 Quick-Hit Return Analysis(1) LSR/SatGas VTB Cost = $21 mm VTB = $5 mm LSR/Sat Gas = $16 mm Project Payback In Under One Year Return = $30 mm/yr VTB = $10 mm/yr LSR/Sat Gas = $20 mm/yr Anticipated Cost Anticipated Return Delek US anticipated that, based on market prices as of November 2011, these projects may generate up to $30 million in incremental annual contribution margin

Ensure Operational Reliability Focus on safe, compliant and cost-effective operations

Optimize production of higher-value refined products Increase Crude Slate Flexibility Run LP to maximize margin capture Crude procurement synergies between Tyler and El Dorado Access Cost-Advantaged Feedstocks(1) In early 2013, anticipate the ability to receive additional supply of WTI-linked barrels for delivery to Tyler & El Dorado refineries Complete Value-Enhancing Capital Projects(1) Refining: “Quick-Hit” capital projects Retail: New store construction, store reimaging program Expand Product Distribution Opportunities(1) Identify new distribution opportunities through mid-stream assets Supply up to 10,000 BPD from El Dorado to MAPCO within 5 years Maintain Balance Sheet Discipline Maintain adequate cash balance, reduce remaining debt Return value to shareholders Objective: To drive superior returns for our shareholders by increasing the scale and functional integration of our downstream asset base (1) As indicated on the Company’s third quarter earnings call dated November 3, 2011

Lion Oil Transaction Executive Summary

Acquired Remaining Minority Interest In Lion Oil Lion Is Now Wholly Owned By Delek US DK Owns 100% Equity Interest In Lion Acquired remaining 11.7% minority equity interest on October 11, 2011 Acquired at a Cost Below Book Value Acquired from a consortium of private investors for ~$13 million in cash Elimination of Non-Controlling Interest Delek US realizes full impact of Lion beginning in the fourth quarter 2011(1) Inception of Lion Oil 1922 Ergon and other investors assume ownership 1985 DK acquires 28.4% interest July 2007 DK acquires 6.2% interest Sept. 2007 DK acquires 53.7% interest Apr 2011 DK Assumes 100% Equity Ownership Oct. 2011 (1) Delek US’ third quarter 2011 results included a reduction to net income of $4.0 million, or $0.07 per diluted share, related to earnings attributable to the non-controlling interest in Lion Oil.

Transaction Summary Asset Overview 80,000 BPD refinery in El Dorado, Arkansas

80-mile Magnolia-El Dorado crude oil system (Shreveport, LA to Magnolia terminal)

28-mile El Dorado crude oil system (Magnolia terminal to El Dorado refinery)

Crude oil gathering system with more than 600 miles of operable pipelines

3 light product distribution terminals (Memphis and Nashville, TN; El Dorado, AR)

Owned asphalt distribution terminal in El Dorado, Arkansas Purchase Summary Transaction completed on April 29, 2011

Delek US acquired Ergon’s 53.7% equity interest in Lion Oil for a combination of cash, stock and the payment and replacement of all debt owed by Lion to Ergon as follows:

$45 million in restricted Delek US Common Stock(1)

$50 million cash payment to Ergon

$50 million term note executed by Lion Oil payable to Ergon; secured by Delek US

Lion Oil divested certain non-refining assets to Ergon

Delek US has assisted Lion Oil in obtaining third-party financing of working capital Determined by the average closing price of Delek US’ common stock as reported on the NYSE for the ten consecutive trading days immediately preceding the closing date on April 29, 2011. In total, 3,292,844 shares of common stock issued to Ergon in conjunction with the purchase agreement.

Light Product Marketing Throughout the Mid-Continent Access To The Enterprise Products Pipeline(1) Expands marketing opportunity into the Mid-Continent Tyler and El Dorado Expected To Ship Product North Supply markets that support better margins Integration Opportunity El Dorado expected to supply MAPCO store locations in Tennessee and Arkansas Expand Retail Store Presence In Adjacent Markets Opportunity to build/acquire new store locations in markets adjacent to El Dorado (i.e. Little Rock, Arkansas) (1) Formerly the TEPPCO pipeline system

Refining Segment Operational Update

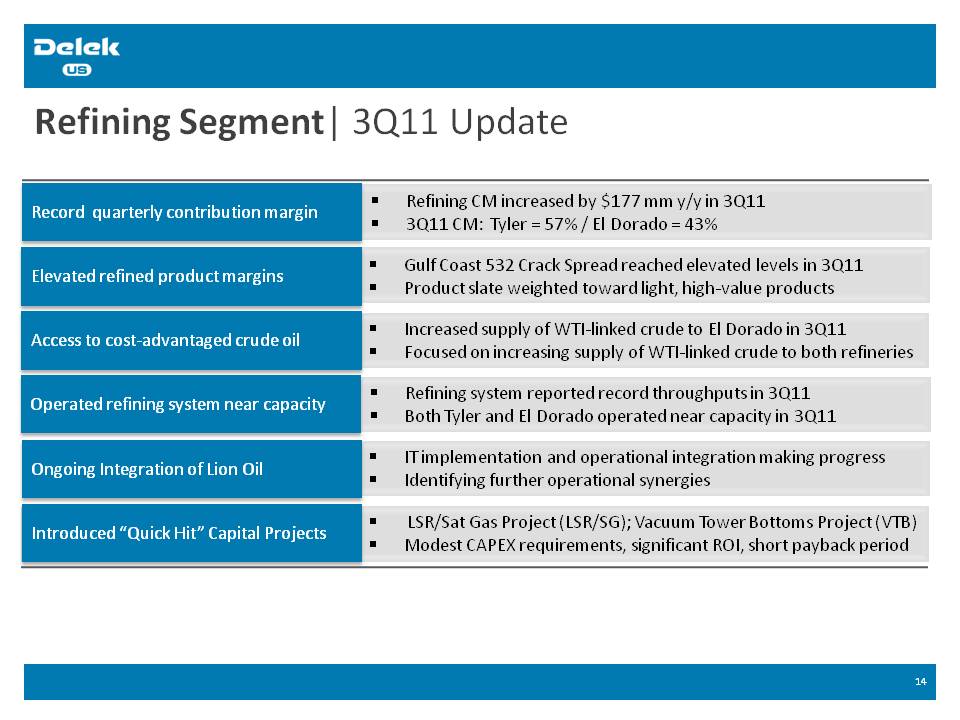

Refining Segment| 3Q11 Update Record quarterly contribution margin Refining CM increased by $177 mm y/y in 3Q11 3Q11 CM: Tyler = 57% / El Dorado = 43% Elevated refined product margins Gulf Coast 532 Crack Spread reached elevated levels in 3Q11 Product slate weighted toward light, high-value products Access to cost-advantaged crude oil Increased supply of WTI-linked crude to El Dorado in 3Q11 Focused on increasing supply of WTI-linked crude to both refineries Operated refining system near capacity Refining system reported record throughputs in 3Q11 Both Tyler and El Dorado operated near capacity in 3Q11 Ongoing Integration of Lion Oil IT implementation and operational integration making progress Identifying further operational synergies Introduced “Quick Hit” Capital Projects LSR/Sat Gas Project (LSR/SG); Vacuum Tower Bottoms Project (VTB) Modest CAPEX requirements, significant ROI, short payback period

Optimized Production Capabilities The Addition of El Dorado has Contributed To Record System-Wide Throughputs Tyler Throughputs (BPD) El Dorado Throughputs (BPD) 58,128 bpd FY06 56,163 bpd FY07 56,922 FY08 53,802 bpd FY09 54,286 bpd FY10 58,461 bpd 1Q11 127,784 bpd 2Q11 145,878 bpd 3Q11 El Dorado Diversified Our System-Wide Production Slate To Include Asphalt Gasoline/Distillate as % of Total Production Asphalt as a % of Total Production Other Industrial Products as % of Total Production Sold Primarily Light-Product Prior to Lion Oil Acquisition 80% Light Product 20% Industrial Product 120.0% 100.0% 80.0% 60.0% 40.0% 20.0% 0.0% 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11

Tyler, Texas Refinery Update Overview Niche, Inland Refiner In PADD III 60,000 barrels per day located in East Texas High Conversion, Moderate Complexity 9.4 complexity; equipped with a delayed coking unit Processes Mostly Light Sweet Crudes Primarily local domestic crudes such as WTI and East Texas Crude Production Sold Into Local Niche Market Generally produces more than 90% light products; sold at rack in Tyler market Tyler Refining Margin vs. Utilization(1,2) Tyler Contribution Margin ($MM) Tyler Refining Margin ($bbl) Tyler Utilization $30.00 $20.00 $10.00 $0.00 3Q10 4Q10 1Q11 2Q11 3Q11 100% 90% 80% 70% 60% Tyler Contribution Margin ($MM) $73.6 2008 $91.0 2009 $51.8 2010 $237.1 NME 2011 Tyler refining margin per barrel excludes intercompany marketing fees

Utilization calculation defined as total crude throughputs divided by 60,000 bpd nameplate capacity of the Tyler refinery

\El Dorado, Arkansas Refinery Update Overview Inland refinery in PADD III 80,000 BPD, 9.0 complexity refinery located in Southern Arkansas Process Local, Offshore, Foreign Crudes Crude slate transitioning from Brent-based to WTI-based crudes Produce Mainly Light Products Historically, ~80% of production is gasoline and distillate Mid-Continent Distribution Strategy Serves Arkansas, Tennessee and North into the Ohio River Valley region El Dorado Refining Margin vs. Utilization(1,2,3) El Dorado Refining Margin ($bbl) El Dorado Utilization $20.00 $15.00 $10.00 $5.00 $0.00 2Q11 3Q11 110% 100% 90% 80% 70% 60% Lion Oil Contribution Margin ($MM)(2,3) $27.5 2Q11 $76.2 3Q11 Utilization calculation defined as total crude throughputs divided by 80,000 bpd nameplate capacity of the El Dorado refinery Second quarter 2011 data is from the 63 days between April 29 and June 30, 2011. A temporary disruption in the El Dorado refinery’s crude supply caused the El Dorado refinery to operate at reduced rates between May 8 and June 15, 2011.

Gulf Coast Refining Margin Benchmark Building a Refining Benchmark “Theoretical” Benchmark For Tyler HSD 532 Gulf Coast Crack Spread (+) Contango or (-) Backwardation High-Sulfur Diesel 5-3-2 Gulf Coast Crack Spread, Including Contango/Backwardation HSD 5-3-2 Gulf Coast Crack Spread Per Barrel 5-3-2 GCCS (+/-) Contango/Backwardation* $35.00 $30.00 $25.00 $20.00 $15.00 $10.00 $5.00 $0.00 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 Oct-11 Nov-11*WTI Backwardation/Contango data is supplied by Argus Media; all other data used to calculate the crack spread provided by Platts

WTI Priced At A Discount To Competing Crudes Refining System Benefits From Discounted WTI-Linked Crudes Crude differentials remain wide vs. historical levels Current cost to purchase WTI is significantly below competing crudes Wider differentials benefit refiners processing WTI Cheaper crude lowers the cost of production, benefiting refining margin WTI Is More Than $18/bbl Cheaper Than LLS Year-To-Date 2011(1) $20.00 $15.00 $10.00 $5.00 $0.00 ($5.00) ($10.00) 2008 2009 2010 YTD 2011 Source: Bloomberg; YTD 2011 is thru November 11, 2011

Forward Curve Indicates Wide WTI/Brent Differential Futures Markets Expect the WTI-Brent Differential To Remain Wide Over a Multi-Year Period(1) Forward Curve Indicates an Average WTI-Brent Differential of $7/bbl Thru 2014 $12.00 $10.00 $8.00 $6.00 $4.00 $2.00 $0.00 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Source: Bloomberg (as of November 16, 2011)

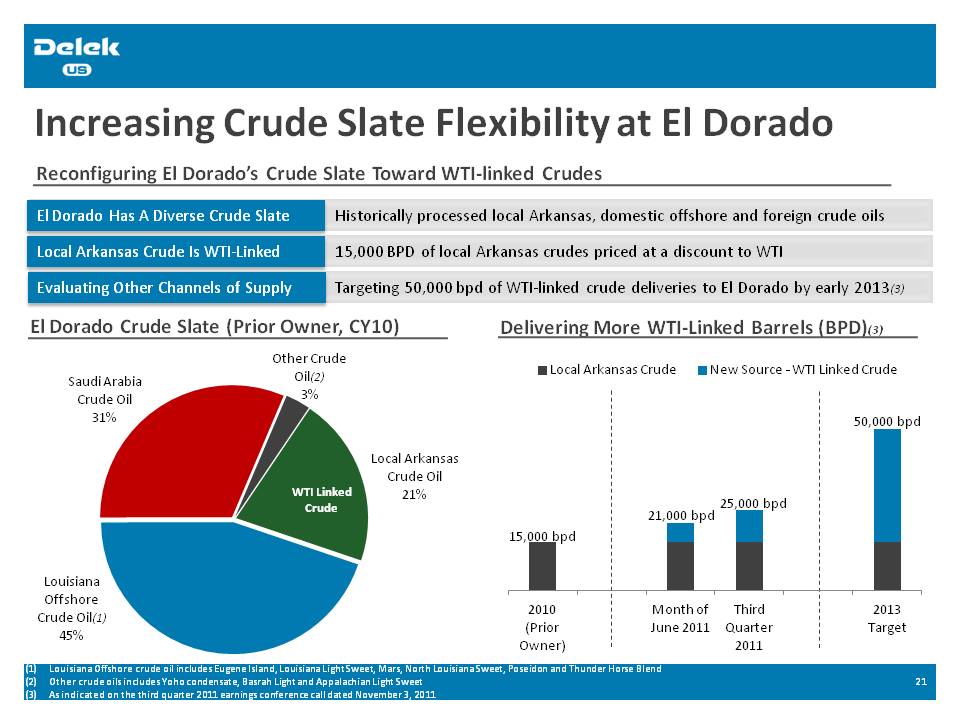

Increasing Crude Slate Flexibility at El Dorado Reconfiguring El Dorado’s Crude Slate Toward WTI-linked Crudes El Dorado Has A Diverse Crude Slate Historically processed local Arkansas, domestic offshore and foreign crude oils Local Arkansas Crude Is WTI-Linked 15,000 BPD of local Arkansas crudes priced at a discount to WTI Evaluating Other Channels of Supply Targeting 50,000 bpd of WTI-linked crude deliveries to El Dorado by early 2013(3) El Dorado Crude Slate (Prior Owner, CY10) Other Crude Oil(2) 3% Local Arkansas Crude Oil 21% WTI Linked Crude Saudi Arabia Crude Oil 31% Louisiana Offshore Crude Oil(1) 45% Delivering More WTI-Linked Barrels (BPD)(3) 15,000 bpd 2010 (Prior Owner) 21,000 bpd Month of June 2011 25,000 bpd Third Quarter 2011 50,000 2013 Target Louisiana Offshore crude oil includes Eugene Island, Louisiana Light Sweet, Mars, North Louisiana Sweet, Poseidon and Thunder Horse Blend

Other crude oils includes Yoho condensate, Basrah Light and Appalachian Light Sweet As indicated on the third quarter 2011 earnings conference call dated November 3, 2011

Retail Segment Operational Update

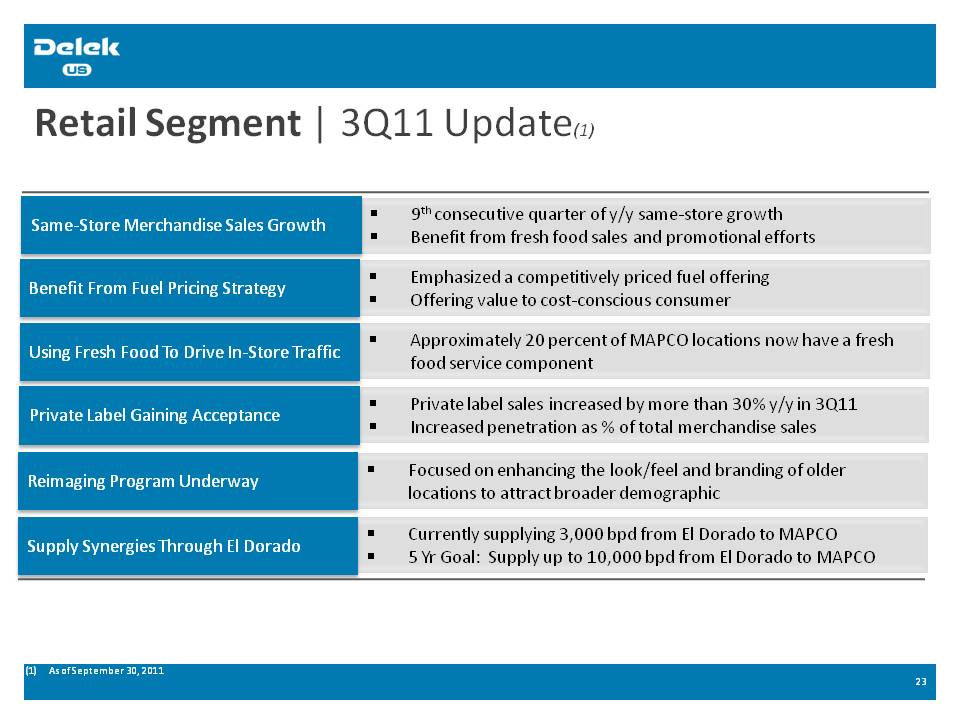

Retail Segment | 3Q11 Update(1) Same-Store Merchandise Sales Growth9th consecutive quarter of y/y same-store growth Benefit from fresh food sales and promotional efforts Benefit From Fuel Pricing Strategy Emphasized a competitively priced fuel offering Offering value to cost-conscious consumer Using Fresh Food To Drive In-Store Traffic Approximately 20 percent of MAPCO locations now have a fresh food service component Private Label Gaining Acceptance Private label sales increased by more than 30% y/y in 3Q11 Increased penetration as % of total merchandise sales Reimaging Program Underway Focused on enhancing the look/feel and branding of older locations to attract broader demographic Supply Synergies Through El Dorado Currently supplying 3,000 bpd from El Dorado to MAPCO 5 Yr Goal: Supply up to 10,000 bpd from El Dorado to MAPCO As of September 30, 2011

Growth In Same-Store Sales Key Factors That Drive Same-Store Sales Same-Store Merchandise Sales Relevant Factors: Location, size, appeal, offering, affordability, people Same-Store Gallons Sold Relevant Factors: Commodity prices, weather, employment, supply disruptions Same-Store Merchandise Sales 1.8% 5.0% 1.2% 4.6% 6.3% 4.4% 4.0% 0.6% 2.4% 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 Same-Store Fuel Gallons Sold 1.0% 4.2% -0.3% 3.4% 5.2% -0.8% -2.3% -1.3% 3.2% 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11

Private Label Initiative Making Progress Creating A New Unique Shopping Experience Quality, Affordable Replacement Option Higher margin, lower-cost option for consumers Countermeasure To Channel Blur Private label is an effective way of offering value to time-starved consumers Private Label vs. Branded Products(1) Private Label as % of Merchandise Sales(2) Gross Margin (%) 80% 70% 60% 50% 40% 30% 20% 10% 0% Single Serve Water Energy Drinks Iced Tea Juice Drinks Sport Drinks Potato Chips Private Label as % of Merchandise Sales(2) 3.3% 4.3% 10.0% 3Q10 3Q11 Long-Term Target Margin does not include rebates and other promotional subsidies from vendors Same-store sales of private label products as a percentage of total same-store merchandise sales; excludes lottery and services

Store Reimaging & New Construction Initiatives Reimaging and Construction Update Multi-Year Store Enhancement Initiative Approximately 43% of store base was reimaged / newly constructed as of 9/30/11 Multi-Year New Store Construction Plan ) Long-term target of at least 10-20 new large-format builds per annum Accelerating Store Reimaging Plan Reimaging at least 25 sites in 2011 Expanding Market Footprint Create a retail presence in markets capable of being supplied by El Dorado More Than 40% of Store Base Has Been Reimaged or Newly Constructed(1) Total Number of Stores (End of Period) Reimages/Prototypes as a % of Total Store Base Total Number of Stores (End of Period) 2006 2007 2008 2009 2010 9/30/11 50% 40% 30% 20% 10% 0% Total Remodeled Stores as % of Total Number of Stores (1) As of September 30, 2011

Marketing Segment Operational Update

Marketing Segment | 3Q11 Update Wholesale Marketing In West Texas Product Marketing Terminals Owned (San Angelo, Abilene, Tyler); Third-Party (Aledo, Odessa, Big Springs, Frost) Supply Synergies With Tyler Owned and leased pipelines transport crude to Tyler refinery Consistent Contribution Margin Positive contribution margin every quarter since 2006 Minimal CAPEX requirements ) Annual CAPEX less than $1 million per year 2006-2010 Total Sales Volumes (Barrels Per Day) 14,114 3Q10 14,352 4Q10 14,535 1Q11 15,946 2Q11 16,139 3Q11 $16.6 NME 2009 $18.2 NME 2010 $20.2 NME 2011(1) Periods are for the nine months ended September 30, 2011

Appendix Additional Data

Historical and Projected Capital Spending(1) Refining Retail, Marketing, Other Total $42.3 $14.5 $56.8 2010 (A) $40.9 $38.7 $79.6 2011 (E) $77.0 $33.0 $110.0 2012 (E) Capital spending estimates as provided in the Company’s latest form 10-Q filed with the Securities and Exchange n the Company’s third quarter earnings conference call held on November 3, 2011.

DK LISTED NYSE