Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE - ESSENDANT INC | d246996dex991.htm |

| 8-K - FORM 8-K - ESSENDANT INC | d246996d8k.htm |

October 24, 2011

1

United Stationers Inc.

Earnings Presentation

Third Quarter 2011

TO BE FILED IN

CONJUNCTION WITH

PRESS RELEASE

Exhibit 99.2 |

October 24, 2011

2

Forward Looking Statements and

Non-GAAP Measures

This

presentation

contains

forward-looking

statements,

including

references

to

goals,

plans,

strategies,

objectives,

anticipated

future

performance,

results

or

events

and

other

statements

that

are

not

strictly

historical

in

nature.

These

statements

are

based

on

management’s

current

expectations,

forecasts

and

assumptions.

This

means

they

involve

a

number

of

risks

and

uncertainties

that

could

cause

actual

results

to

differ

materially

from

those

expressed

or

implied

here.

These

risks

and

uncertainties

include,

but

are

not

limited

to,

the

following:

Prevailing

economic

conditions

and

changes

affecting

the

business

products

industry

and

the

general

economy;

United’s

ability

to

effectively

manage

its

operations

and

to

implement

growth,

cost-reduction

and

margin-enhancement

initiatives;

United’s

reliance

on

key

customers,

and

the

business,

credit

and

other

risks

inherent

in

continuing

or

increased

customer

concentration;

United’s

reliance

on

key

suppliers

and

the

supplier

allowances

and

promotional

incentives

they

offer;

United’s

reliance

on

independent

resellers

for

a

significant

percentage

of

its

net

sales

and

therefore

the

importance

of

the

continued

independence,

viability

and

success

of

these

resellers;

continuing

or

increasing

competitive

activity

and

pricing

pressures

within

existing

or

expanded

product

categories,

including

competition

from

product

manufacturers

who

sell

directly

to

United’s

customers;

the

impact

of

variability

in

customer

and

end-user

demand

patterns

on

United’s

product

sales

mix

and,

in

turn,

on

profit

margins;

the

impact

of

a

loss

of,

or

substantial

decrease

in,

the

availability

of

products

or

service

from

key

suppliers

at

competitive

prices;

the

availability

of

financing

sources

to

meet

United’s

business

needs;

United’s

ability

to

manage

inventory

in

order

to

maximize

sales

and

supplier

allowances

while

minimizing

excess

and

obsolete

inventory;

United’s

ability

to

maintain

its

existing

information

technology

and

e-commerce

systems

and

to

successfully

procure

and

implement

new

systems

without

business

disruption

or

other

unanticipated

difficulties

or

costs;

United’s

ability

to

effectively

identify,

consummate

and

integrate

acquisitions;

United’s

reliance

on

key

management

personnel,

both

in

day-to-day

operations

and

in

execution

of

new

business

initiatives;

and

the

effects

of

hurricanes,

acts

of

terrorism

and

other

natural

or

man-made

disruptions.

Shareholders,

potential

investors

and

other

readers

are

urged

to

consider

these

risks

and

uncertainties

in

evaluating

forward-looking

statements

and

are

cautioned

not

to

place

undue

reliance

on

the

forward-looking

statements.

For

additional

information

about

risks

and

uncertainties

that

could

materially

affect

United’s

results,

please

see

the

company’s

Securities

and

Exchange

Commission

filings.

The

forward-looking

information

in

this

presentation

is

made

as

of

this

date

only,

and

the

Company

does

not

undertake

to

update

any

forward-

looking

statement.

Investors

are

advised

to

consult

any

further

disclosure

by

United

regarding

the

matters

discussed

in

this

release

in

its

filings

with

the

Securities

and

Exchange

Commission

and

in

other

written

statements

it

makes

from

time

to

time.

It

is

not

possible

to

anticipate

or

foresee

all

risks

and

uncertainties,

and

investors

should

not

consider

any

list

of

risks

and

uncertainties

to

be

exhaustive

or

complete.

*

This

is

non-GAAP

information.

A

reconciliation

of

these

items

to

the

most

comparable

GAAP

measures

is

presented

on

the

company’s

Website

(www.unitedstationers.com)

under

the

Investor

Information

section.

Except

as

noted,

all

references

to

financial

results

within

this

presentation

are

presented

in

accordance

with

U.S.

Generally

Accepted

Accounting

Principles. |

October 24,

2011 3

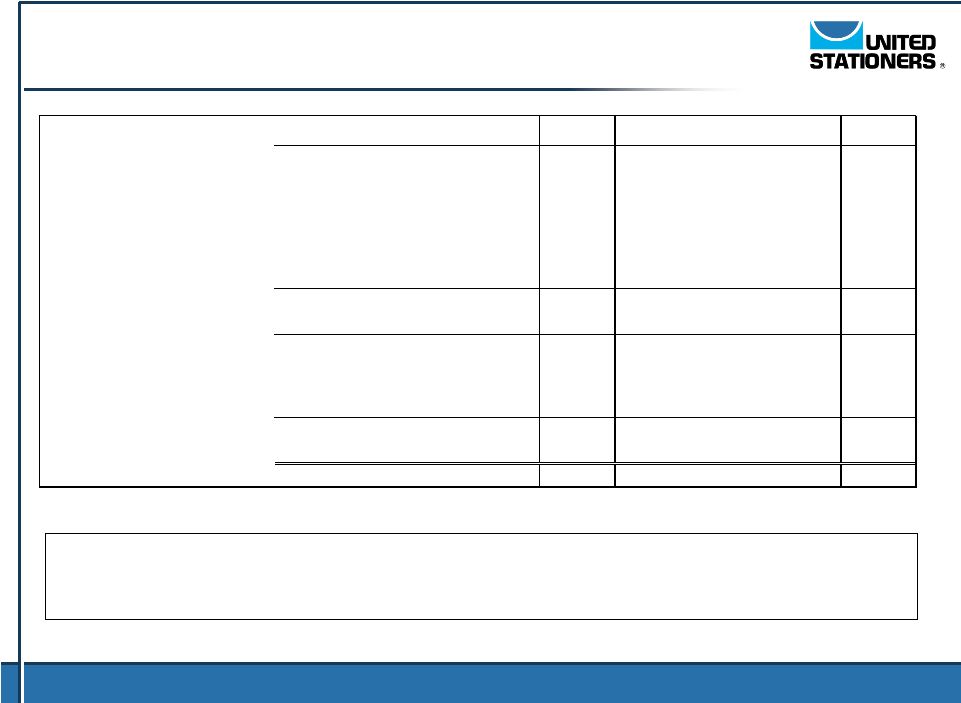

Q3 2011 Headlines

Sales increased 3.1% from Q3 2010 to $1.31 billion.

Earnings per diluted share were $0.81, up 13%* from an adjusted Q3 2010

EPS of $0.72*.

Gross margin rate of 15.3% was flat with last year.

Operating expenses in Q3 2011 were $135.1 million, compared to an

adjusted $132.6 million* in the prior-year quarter, and were 10.3% of sales,

down from 10.4%* of sales in the prior-year quarter.

Operating income as a percent of sales was 4.9%, flat with last year’s

adjusted 4.9%*.

Net

income

increased

4%*

to

$35.8

million

from

an

adjusted

$34.4

million*

in Q3 2010.

Net cash provided by operating activities was $26.2 million in Q3 2011.

Debt was up $47.9 million from the prior-year end and from the prior-year

quarter end.

During the quarter, the Company repurchased 2.2 million shares for $67.8

million and paid a cash dividend of $6 million to common shareholders. |

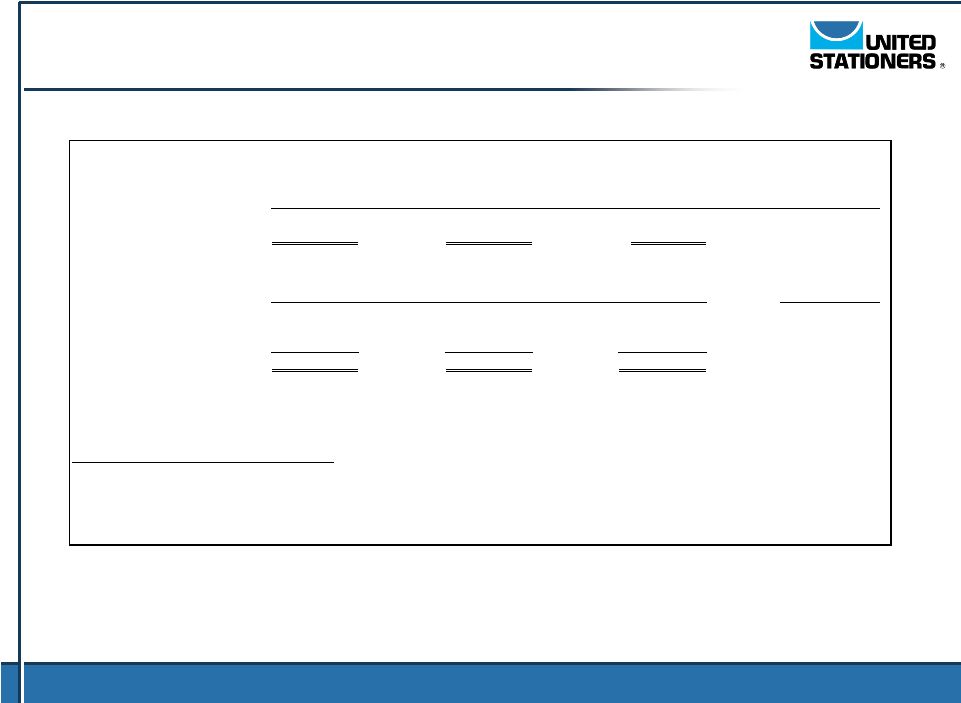

October 24, 2011

4

Third Quarter 2011 P&L

% to sales change

$

% to Sales

$

% to Sales

$ change

% change

Fav (Unfav)

$ Millions (except EPS)

QTD Q3 2011

QTD Q3 2011

QTD Q3 2010

QTD Q3 2010

Fav (Unfav)

Fav (Unfav)

basis points

Net Sales

1,310.0

$

1,270.7

$

39.3

$

3.1%

Workday Adjusted Sales Growth

3.1%

Gross Margin

199.7

15.25%

194.8

15.33%

4.9

2.5%

(8)

Operating Expense

135.1

10.32%

129.3

10.18%

(5.8)

(4.5%)

(14)

Operating Income

64.6

4.93%

65.5

5.15%

(0.9)

(1.4%)

(22)

Interest & Other

7.0

0.53%

6.6

0.52%

(0.4)

(6.1%)

(1)

Taxes

21.8

1.67%

22.4

1.77%

0.6

2.7%

10

Net Income

35.8

$

2.73%

36.5

$

2.87%

(0.7)

$

(1.9%)

(14)

Diluted Shares (000s)

44,202

47,548

Diluted EPS

0.81

$

0.77

$

0.04

$

5.2%

Effective Tax Rate

37.8%

38.1%

Adjusted to exclude non-operating items *

Adjusted Operating Income

64.6

$

4.93%

62.2

$

4.89%

2.4

$

3.9%

4

Adjusted Net Income

35.8

2.73%

34.4

2.71%

1.4

4.1%

2

Adjusted Diluted EPS

0.81

$

0.72

$

0.09

$

12.5% |

October 24,

2011 5

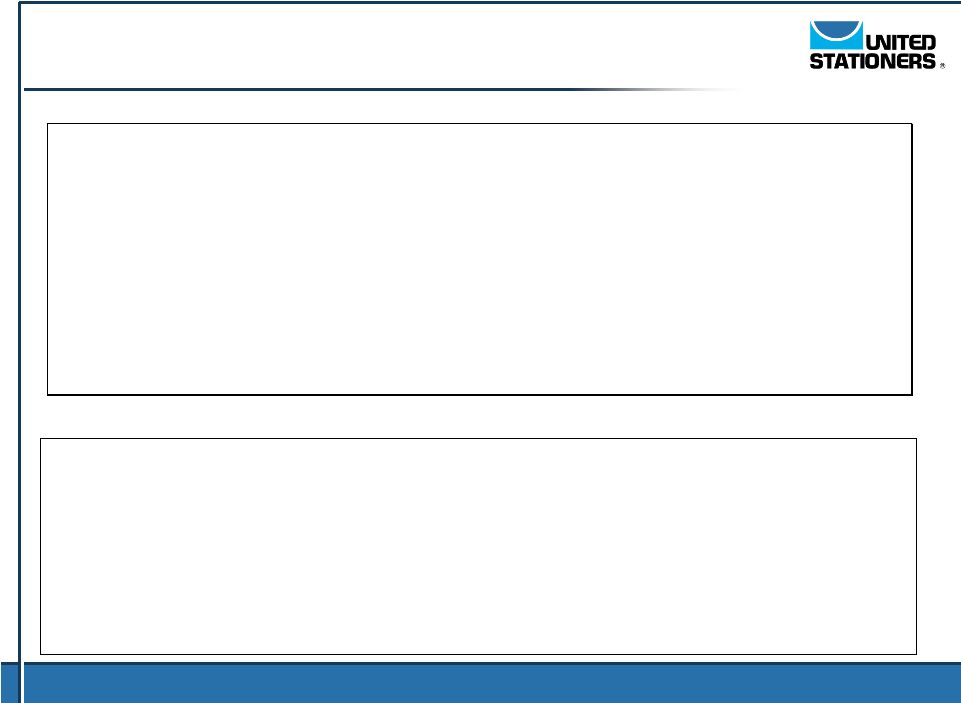

YTD September 2011 Headlines

Sales increased 3.8%, workday adjusted, from YTD September 2010 to

$3.80 billion.

Adjusted earnings per diluted share were $1.87*, up 17%* from YTD

September 2010 EPS of $1.60*.

Gross margin rate of 14.9% was up from 14.8% last year.

Adjusted operating expenses in YTD September 2011 were $407.9

million*, up from $395.4 million* in the prior-year period, and were 10.7%*

of sales versus 10.9%* in the prior-year period.

Adjusted operating income as a percent of sales was 4.2%*, up from 4.0%*

in YTD September 2010.

Adjusted net income increased 10%* to $85.4 million* from $77.9 million* in

YTD September 2010.

Net cash provided by operating activities was $99.5 million YTD September

2011 compared to $114.4 million YTD September 2010.

Through YTD September 30, 2011, the Company repurchased 4.3 million

shares

for

$137.7

million,

paid

cash

dividends

of

$12

million

to

common

shareholders, and declared another $0.13 per share dividend. |

October 24, 2011

6

Year-to-Date 2011 P&L

% to sales change

$ Millions (except EPS)

$

% to Sales

$

% to Sales

$ change

% change

Fav (Unfav)

YTD Q3 2011

YTD Q3 2011

YTD Q3 2010

YTD Q3 2010

Fav (Unfav)

Fav (Unfav)

basis points

Net Sales

3,804.1

$

3,645.8

$

158.3

$

4.3%

Workday Adjusted Sales Growth

3.8%

Gross Margin

566.3

14.89%

541.0

14.84%

25.3

4.7%

5

Operating Expense

413.9

10.88%

389.3

10.68%

(24.6)

(6.3%)

(20)

Operating Income

152.4

4.01%

151.7

4.16%

0.7

0.5%

(15)

Interest & Other

20.4

0.54%

19.3

0.53%

(1.1)

(5.7%)

(1)

Taxes

50.9

1.34%

50.7

1.40%

(0.2)

(0.4%)

6

Net Income

81.1

$

2.13%

81.7

$

2.24%

(0.6)

$

(0.7%)

(11)

Diluted Shares (000s)

45,718

48,624

Diluted EPS

1.77

$

1.68

$

0.09

$

5.4%

Effective Tax Rate

38.6%

38.3%

Adjusted to exclude non-operating items*

Adjusted Operating Income

158.5

$

4.17%

145.6

$

3.99%

12.9

$

8.9%

18

Adjusted Net Income

85.4

2.24%

77.9

2.14%

7.5

9.6%

10

Adjusted Diluted EPS

1.87

$

1.60

$

0.27

$

16.9% |

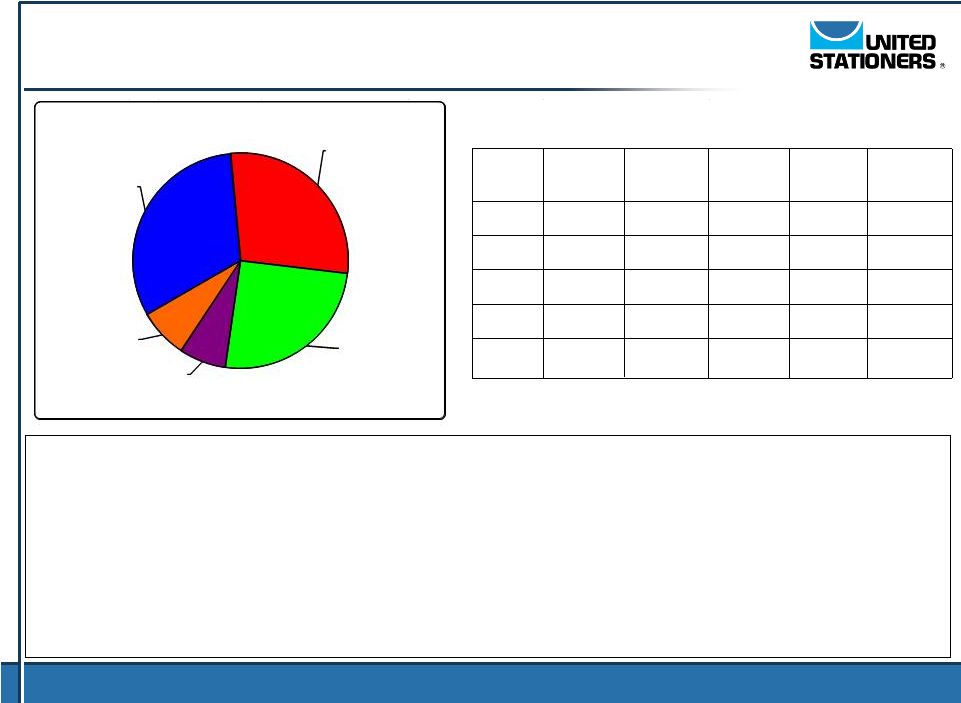

October 24, 2011

7

Sales

by Product Category –

Q3 2011

•

Technology sales were relatively flat with lower purchases from National Accounts

being offset by significant growth in New Channels and from other targeted

initiatives. •

Office Products sales remained even with last year with decreases in National

Accounts offset by growth from New Channels.

•

Janitorial/Breakroom growth reflects increases across all channels and is a result

of continued strategic initiatives to build share.

•

Industrial sales growth was due to continued strong demand and strategic

initiatives. •

Furniture sales were negatively impacted by a challenging transactional market and

a sourcing shift in some national account business.

Sales

Sales

Sales

Sales

Sales

growth (decline)

growth (decline)

growth (decline)

growth (decline)

growth (decline)

Q3 2011

Q2 2011

Q1 2011

Q4 2010

Q3 2010

Category

vs Q3 2010

vs Q2 2010

vs Q1 2010

vs Q4 2009

vs Q3 2009

Technology

(0.6%)

(5.8%)

3.6%

(2.8%)

(1.4%)

Office Products

(0.6%)

4.4%

3.4%

0.4%

6.7%

Janitorial/

Breakroom

10.6%

11.5%

7.5%

(1.7%)

(4.4%)

Industrial

23.7%

20.5%

26.1%

25.2%

29.6%

Furniture

(9.8%)

(3.9%)

(0.9%)

0.9%

(0.1%)

Technology

32%

Office Products

28%

Janitorial/

Breakroom

25%

Furniture

7%

Industrial

8%

Q3 2011 |

October 24, 2011

8

Sales by Channel –

Q3 2011

Sales growth

Sales growth

Sales growth

Sales growth

Sales growth

(decline)

(decline)

(decline)

(decline)

(decline)

Q3 2011

Q2 2011

Q1 2011

Q4 2010

Q3 2010

Channel

vs Q3 2010

vs Q2 2010

vs Q1 2010

vs Q4 2009

vs Q3 2009

Independent

& Other

5.7%

4.4%

6.2%

1.2%

3.7%

Nationals

(12.1%)

(5.6%)

1.8%

(4.3%)

(7.6%)

Independent

& Other

87%

Nationals

13%

Q3 2011

•

Independent/Other channel sales growth was attributable to 24% growth in

Industrial, continued success with growth initiatives and strong

double-digit growth with New Channel customers, including e-tail.

•

National accounts sales decline was mainly due to a shift to more direct purchases

from manufacturers, primarily in furniture and certain technology

products. |

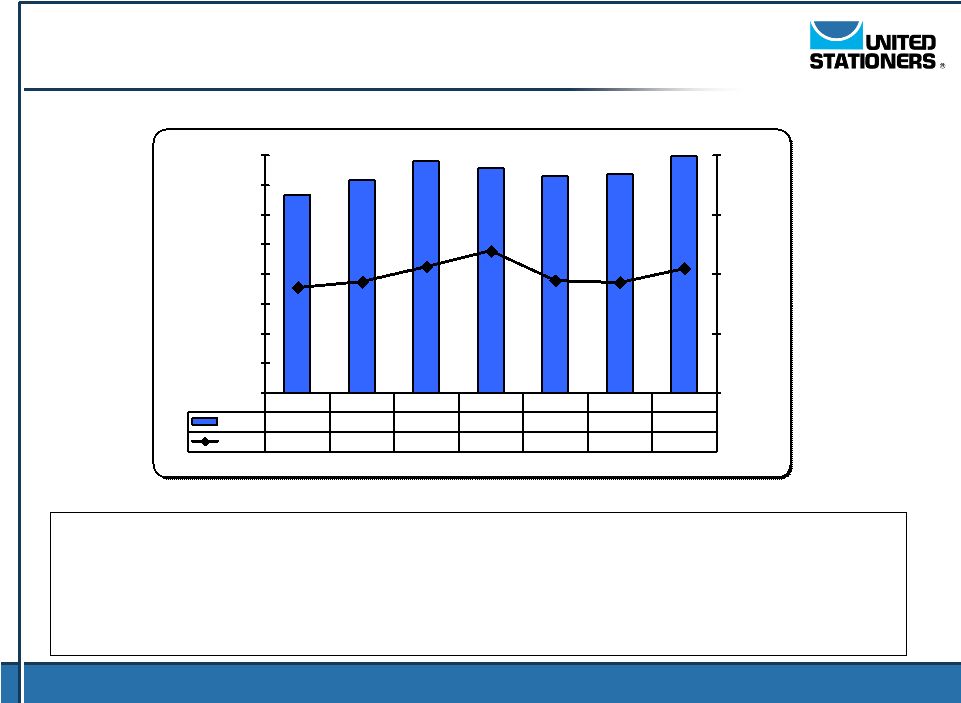

October 24, 2011

9

Gross Margin

dollars in millions

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Dollars

$166.9

$179.2

$194.8

$189.5

$182.4

$184.2

$199.7

Rate

14.5%

14.7%

15.3%

16.0%

14.7%

14.7%

15.3%

10.0%

12.5%

15.0%

17.5%

20.0%

$-

$25.0

$50.0

$75.0

$100.0

$125.0

$150.0

$175.0

$200.0

•

Margins were flat in Q3 2011 versus Q3 2010 due to lower margin-mix, continued

competitive pricing

pressures,

and

higher

diesel

fuel

costs

offset

by

higher

product

cost

inflation,

higher

inventory purchase-related supplier allowances, other inventory-related

items and “War on Waste”

(WOW) savings. |

October 24, 2011

10

Adjusted Operating Expense*

dollars in millions

Q1 10

Q2 10 *

Q3 10 *

Q4 10 *

Q1 11 *

Q2 11 *

Q3 11

Dollars

$131.1

$131.7

$132.6

$136.9

$140.8

$132.0

$135.1

Rate

11.4%

10.8%

10.4%

11.5%

11.4%

10.5%

10.3%

7.5%

10.0%

12.5%

15.0%

$-

$25.0

$50.0

$75.0

$100.0

$125.0

$150.0

•

Adjusted

operating

expense

dollars

increased

slightly

in

Q3

2011

versus

the

prior-year

quarter

mainly

due

to

sales

growth,

investment

in

strategic

growth

initiatives,

and

higher

bad

debt

costs.

These

increases

were

partially

offset

by

lower

depreciation,

favorable

resolution

of

non-income

based

tax

liabilities, and savings from WOW initiatives.

•

As

a

percent

to

sales,

adjusted

operating

expenses

were

12

basis

points

favorable

versus

the

prior

year. |

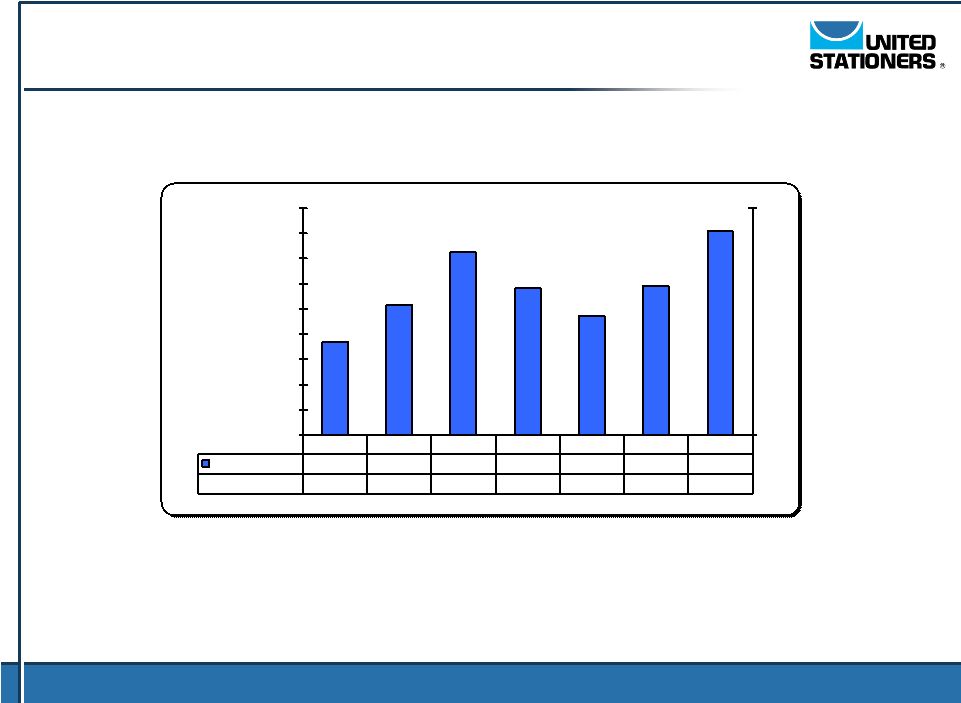

October 24, 2011

11

Adjusted Operating Income*

dollars in millions

Q1 10

Q2 10 *

Q3 10 *

Q4 10 *

Q1 11*

Q2 11*

Q3 11

Dollars

$35.8

$47.6

$62.2

$52.6

$41.6

$52.2

$64.6

Rate

3.1%

3.9%

4.9%

4.4%

3.4%

4.2%

4.9%

2.0%

3.0%

4.0%

5.0%

6.0%

$-

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0 |

October 24, 2011

12

Adjusted Earnings per Share*

shares in millions

Q1 10

Q2 10 *

Q3 10 *

Q4 10 *

Q1 11*

Q2 11*

Q3 11

EPS

$0.37

$0.51

$0.72

$0.58

$0.47

$0.59

$0.81

Diluted Shares

49.640

49.272

47.548

47.456

46.656

46.340

44.202

0.000

1.000

$-

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90 |

October 24, 2011

13

Working Capital Summary

$ Millions

3/31/2010

6/30/2010

9/30/2010

12/31/2010

3/31/2011

6/30/2011

9/30/2011

Accounts Receivable

606.2

$

642.6

$

655.1

$

628.1

$

648.1

$

669.5

$

699.2

$

Inventories (LIFO)

610.1

639.2

617.4

684.1

636.2

632.1

615.5

Accounts Payable

433.8

443.9

424.9

421.6

422.4

443.5

410.8

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Net Trade A/R DSO

43

42

41

41

42

41

42

Inventory Turns

6.6

6.7

6.8

6.1

6.4

6.8

7.1

A/P as % Inventory (LIFO)

71%

69%

69%

62%

66%

70%

67%

A/P as % Inventory (FIFO)

63%

61%

61%

55%

58%

61%

58%

•

Receivables

were

up

7%

versus

the

Q3

2010

and

up

11%

compared

to

Q4

2010.

•

Net trade A/R DSO increased slightly compared to Q3 2010 as the economic

environment remains challenging for certain customers.

•

Inventories

were

down

0.3%

versus

Q3

2010

and

down

10%

versus

Q4

2010

as

the

Company

continues to manage working capital efficiently while maintaining high service

levels. •

Turnover

remained

strong

at

7.1

turns

vs.

6.8

turns

at

this

time

last

year.

•

Payables leverage ratios were down slightly from Q3 2010 but up from Q4 2010 and in

line with typical levels. |

October 24, 2011

14

Cash Flows

QTD

QTD

QTD

QTD

2010

QTD

QTD

QTD

2011

$ Millions

Q1 10

Q2 10

Q3 10

Q4 10

Total Year

Q1 11

Q2 11

Q3 11

YTD

Net Income

18.2

$

27.0

$

36.5

$

31.1

$

112.8

$

20.4

$

24.9

$

35.8

$

81.1

$

Depreciation & Amortization

9.4

9.4

9.4

9.4

37.6

9.0

8.9

8.7

26.6

Share-based compensation

3.3

3.5

3.7

3.6

14.1

3.7

6.7

2.7

13.1

Writedown on impaired assets

-

-

-

-

-

1.6

-

-

1.6

Change in Accounts Receivable

35.9

(36.7)

(12.3)

27.0

13.9

(19.8)

(21.3)

(30.6)

(71.7)

Change in Inventory

(18.1)

(29.4)

21.9

(66.5)

(92.1)

48.2

4.3

15.2

67.7

Change in Accounts Payable

42.5

9.9

(18.9)

(3.3)

30.2

1.0

21.0

(33.1)

(11.1)

Change in Other Working Capital

(4.1)

1.0

12.8

(6.6)

3.1

(18.7)

(3.3)

21.7

(0.3)

Change in Working Capital

56.2

(55.2)

3.5

(49.4)

(44.9)

10.7

0.7

(26.8)

(15.4)

Other

(4.2)

(12.9)

6.6

5.7

(4.8)

(4.4)

(8.9)

5.8

(7.5)

Adjusted cash provided by (used in)

operating activities

82.9

(28.2)

59.7

0.4

114.8

41.0

32.3

26.2

99.5

Capital Expenditures

(5.7)

(5.0)

(7.3)

(9.3)

(27.3)

(9.8)

(6.4)

(4.6)

(20.8)

Proceeds from disposition of fixed assets

-

-

0.1

-

0.1

-

0.0

0.1

0.1

Net cash used for capital expenditures *

(5.7)

(5.0)

(7.2)

(9.3)

(27.2)

(9.8)

(6.4)

(4.5)

(20.7)

Free Cash Flow *

77.2

$

(33.2)

$

52.5

$

(8.9)

$

87.6

$

31.2

$

25.9

$

21.7

$

78.8

$

•

Cash flow was positively affected by a significant reduction in inventory, offset

by higher accounts receivable and lower accounts payable.

|

October 24, 2011

15

Debt and Capitalization

$ Millions

3/31/2010

6/30/2010

9/30/2010

12/31/2010

3/31/2011

6/30/2011

9/30/2011

Debt

441.8

$

453.4

$

441.8

$

441.8

$

441.8

$

441.8

$

489.7

$

Equity

730.5

710.6

733.1

759.6

769.7

752.7

721.2

Total capitalization

1,172.3

$

1,164.0

$

1,174.9

$

1,201.4

$

1,211.5

$

1,194.5

$

1,210.9

$

Debt-to-total capitalization

37.7%

39.0%

37.6%

36.8%

36.5%

37.0%

40.4%

•

Operating cash flow generated continues to be used for investments in growth

initiatives, share repurchases, and quarterly dividends.

•

Total debt was up $47.9 million from Q3 2010 and Q4 2010. In September the Company

completed a five-year $700 million Revolving Credit Facility. This

facility replaces the Company’s $425 million revolver and $200 million

term loan. The Revolving Credit Facility will be used for strategic growth

initiatives, working capital needs and other general corporate purposes.

•

Share

repurchases

totaled

4.3

million

shares,

or

$137.7

million,

in

the

year

through

September

2011. |