Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FIRST MARBLEHEAD CORP | d244223d8k.htm |

ABS East

Presentation October 16 -

18, 2011

Exhibit 99.1 |

ABS East

Conference Investor Presentation - 2

Forward-Looking Statements

Statements in this presentation regarding First Marblehead’s strategy, future financial

and operational results, competitive position, future opportunities and

platform, and the future performance of loan portfolios that First Marblehead has previously

facilitated, including projected forbearance, prepayment, delinquency and default

rates, as well as any other statements that are not purely historical, constitute forward-looking statements for purposes of the safe

harbor provisions of The Private Securities Litigation Reform Act of 1995. These

forward-looking statements are based on our historical performance, the historical

performance of the securitization trusts that we have facilitated (the “Trusts”), and on our plans, estimates and expectations as of October 14, 2011.

The inclusion of this forward-looking information should not be regarded as a

representation by us or any other person that the future results, plans, projections,

estimates or expectations expressed or implied by us will actually be achieved. You are cautioned that matters subject to forward-looking

statements involve known and unknown risks and uncertainties, including economic, legislative,

regulatory, competitive and other factors, which may cause actual financial or

operational results, including the performance of the Trusts and facilitated loan volumes, or the timing of events, including loan defaults, to

be materially different than those expressed or implied by our forward-looking statements.

Important factors that could cause or contribute to such differences include: market

acceptance of and demand for our Monogram platform and fee-based service offerings; our success in designing, implementing and

commercializing private education loan programs through Union Federal Savings Bank, including

receipt of and compliance with regulatory approvals and conditions with respect to such

programs; the successful marketing and sales of our clients’ Monogram-based loan offerings; the volume, timing and

performance of facilitated loans; the size and structure of any credit enhancement provided by

us in connection with our Monogram platform; capital market receptivity to private

student loan asset-backed securities and our ability to structure securitizations or alternative financings; the size, structure and timing of

any such securitizations or alternative financings; our success in realizing the anticipated

benefits of our acquisition of Tuition Management Systems, LLC; economic, legislative,

regulatory, competitive and other factors affecting discount, default, recovery and prepayment rates on private student loan portfolios,

including general economic conditions, the consumer credit environment, interest rates and

unemployment rates; borrower defaults and the Trusts’ ability to recover principal

and interest from such borrowers, including the effectiveness of various risk mitigation strategies, such as alternative payment plans; any

investigation, audit, claim, regulatory action or suit relating to the transfer of the trust

certificate of NC Residuals Owner Trust or the asset services agreement between the

purchaser and us, including as a result of the audit being conducted by the Internal Revenue Service relating to tax refunds previously received;

resolution of pending litigation pertaining to our Massachusetts state income tax returns;

management’s determination of which qualitative and quantitative factors,

including macroeconomic indicators and historical experience, should be weighted in our projections, and the weight to be given to each such factor;

and the other factors set forth under the caption "risk factors" in our annual report

on Form 10-K filed with the Securities and Exchange Commission on September 8,

2011. We specifically disclaim any obligation to update any forward-looking statements as a result of developments occurring after October 14,

2011.

Disclaimer

The information in this presentation is intended to provide a broad overview of a portfolio of

private education loans previously facilitated by First Marblehead. Neither First

Marblehead nor any other party is offering any securities by making this presentation or soliciting any action based upon the information provided.

Nothing in this presentation should be relied upon as a representation by First Marblehead, or

any other person, as to the future performance of any securitization trust described in

this presentation or as to any securities that may be issued in the future. The information contained herein is intended to be

illustrative only, and historical collateral pools may not be representative of any future

collateral pool. growth

prospects,

liquidity,

the

demand

for

private

education

loans,

the

characteristics

and

performance

of

future

loan

pools

based

on

our

Monogram

® |

ABS East

Conference Investor Presentation - 3

Section I

FMD Corporate Update & Overview

Section II

Legacy Portfolio Experience

Section III

Data Driven Approach to Risk & Portfolio Management

Section IV

Monogram

®

Platform –

The Next Generation of Private Student Lending

TABLE OF CONTENTS |

ABS East

Conference Investor Presentation - 4

Section I

FMD Corporate Update & Overview |

ABS East

Conference Investor Presentation - 5

Corporate Update –

Recent Highlights

Entered peak student loan origination season for the first time since 2008 with

programs in place at three lenders

•

Since the launch of these programs, we have processed ~50,000 applications requesting

over

$525

million

in

funds,

and

approved

~$124

million

•

Credit characteristics of booked loan volume is strong:

88% cosigned

Weighted

average

FICO

score

is

757

60% of applicants have selected immediately cash flowing options

76% of applicants have selected repayment terms of 10 years or less

In the quarter ended 06/30/11, Tuition Management Systems, LLC (TMS) provided

$623,000 of positive cash flow, excluding capital expenditures

•

TMS is the largest volume tuition payment plan provider in the U.S.

As

of

6/30/11,

FMD

had

$267.4

million

in

cash,

cash

equivalents,

&

short-term

investments

1

1

1

Origination and credit data is as of October 10, 2011 and includes all FMD-facilitated

programs. Weighted average FICO score is based upon the cosigner’s FICO

score if the loan is cosigned, otherwise it is based upon the borrower’s FICO score. |

ABS East

Conference Investor Presentation - 6

Focus. Flexibility. Innovation.

Work with lender and school clients to create responsible, affordable choices for students and

their families as they prepare to meet the cost of higher education

Approach credit with data-driven quantitative analysis based on 20 years of industry

experience Operate a highly specialized business model deriving revenue from

fee-for-service operations, partnered lending platforms and capital markets

execution strategies What We Do

Industry

leading

financial

services

intermediary

specializing

in

the

design,

origination,

management

and financing of private student loan programs

Outsourced tuition planning, billing and payment technology services through our subsidiary

Tuition Management Systems, LLC

Our bank subsidiary, Union Federal, offers banking services and products including private

student loans

Over 6 million loan applications processed totaling over $16.5 billion volume; 38

asset-backed bond securitizations sponsored totaling over $16 billion in

issuance Who We Are |

ABS East

Conference Investor Presentation - 7

Focus. Flexibility. Innovation.

Families

struggling

more

than

ever

to

fill

the

“funding

gap”

created

by

ever-increasing

college

costs,

limits on federal student loans along with shrinking state and institutional aid

Legislative changes and the credit crisis have tempered lending activities

Number of competitors has diminished

Ensure

the

right

students

at

the

right

schools

receive

the

right

student

loans

Why We Do It

Leverage extensive private student loan experience applying sophisticated risk analysis

capabilities and high-touch portfolio management strategies designed to optimize

performance Utilize a seasoned national sales force and transparent loan application

process to deliver customized

loan

products

uniquely

designed

to

meet

borrowers’

needs

Coordinate with investment banks, rating agencies and investors to strategically deploy

capital to create viable and flexible disposition strategies for clients

How We Do It |

ABS East

Conference Investor Presentation - 8

Diversified Revenue Sources

Private Student Loan Origination

•

Union Federal offers traditional higher education and K-12 loan programs nationally;

earns net interest margin by holding loans to term

Partnered Lending

•

Provide customized loan programs to lender clients; earn up-front fees for loan

origination and marketing; can earn a share of ongoing borrower interest income in

exchange for providing credit enhancement and portfolio management

Capital Markets

•

Long-term financing solutions for FMD-facilitated loan programs; earn ongoing fees

for trust administration and portfolio management; earn net interest margin by

retaining residual interests

Fee-For-Service

•

Services provided in our Private Student Loan Origination, Partnered Lending, Trust

Administration and Capital Markets businesses available on an a la carte basis

Tuition Payment Plans

•

Offer schools a suite of outsourced billing, payment processing and education payment

counseling products and services from TMS |

ABS East

Conference Investor Presentation - 9

Building Blocks for Growth in Place

Industry Expertise

•

Historical focus on non-Federal student loan programs

•

Highly skilled and analytically focused Risk and Portfolio Management groups

•

Experienced Capital Markets team

•

Top flight National Sales team

•

Decisions driven by over 20 years of private student loan performance data

Strong Synergies with Subsidiaries and Strategic Partners

•

TMS tuition payment programs provide potential lead-generation for loan marketing

•

TMS deposit base provides scalability for Union Federal

•

Federally chartered thrift provides platform for national programs

•

Industry leading loan servicer and top-tier collections agencies used in portfolio

management

•

Highly reputable and stable regional banks for Partnered Lending

Monogram Platform –

The Next Generation of Private Student Lending

•

Flexible design aimed at producing medium and long-term, high quality assets

•

More granular assessment of risk

•

Exceptional transparency and increased disclosure throughout borrower application

process •

Proactive, analytical approach to portfolio management drives performance

|

ABS East

Conference Investor Presentation - 10

Opportunity for Growth Exists

Consumers Demanding Private Student Loans

•

Enrollment continues to increase

•

Cost of education continues to rise

•

Federal aid targeting weaker credits

Capital Markets Demanding Better Credits

•

Investors seeking high credit quality loans

•

Better risk-based pricing

•

Traditional schools

Innovative Products Needed

•

Greater ability to control risk

•

Fully transparent application

•

Better analytics

•

Compliant with all regulatory requirements |

Section

II Legacy Portfolio Experience

ABS East Conference Investor Presentation - 11 |

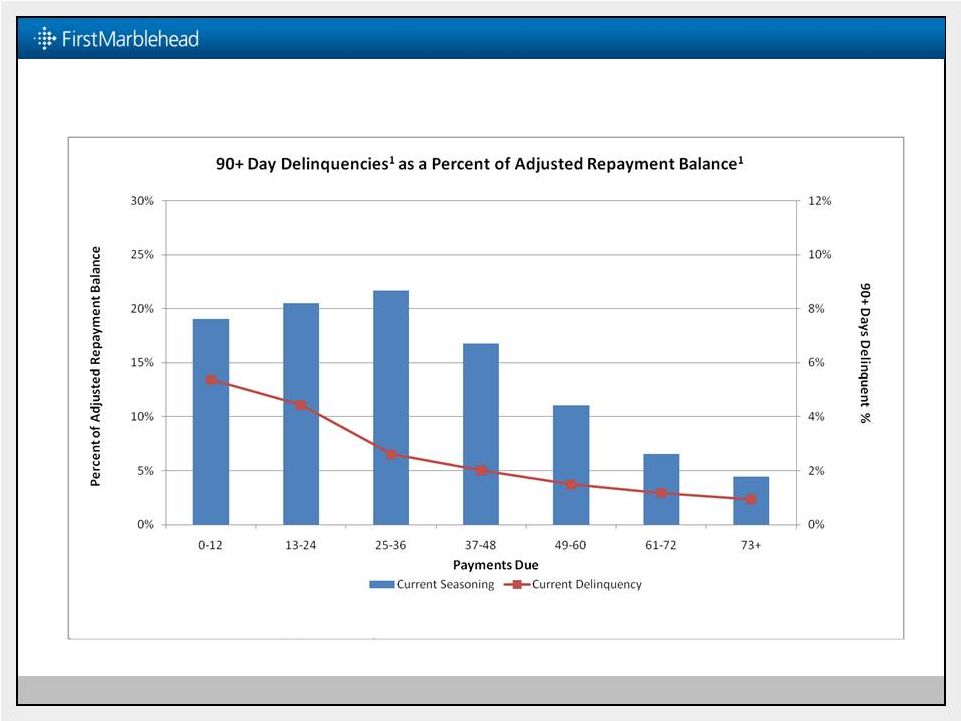

ABS East

Conference Investor Presentation - 12

Delinquency Rates

1

Improve as Loans Season

1

Based on NCSLT data on PHEAA serviced loans as of September 30, 2011. A borrower making

reduced payments for a limited period of time pursuant to an alternative payment plan

will be considered current if such reduced payments are timely made and delinquent if such reduced

payments are past due. Adjusted Repayment Balance includes all loans in repayment status on

9/30/2011 excluding loans in basic forbearance. |

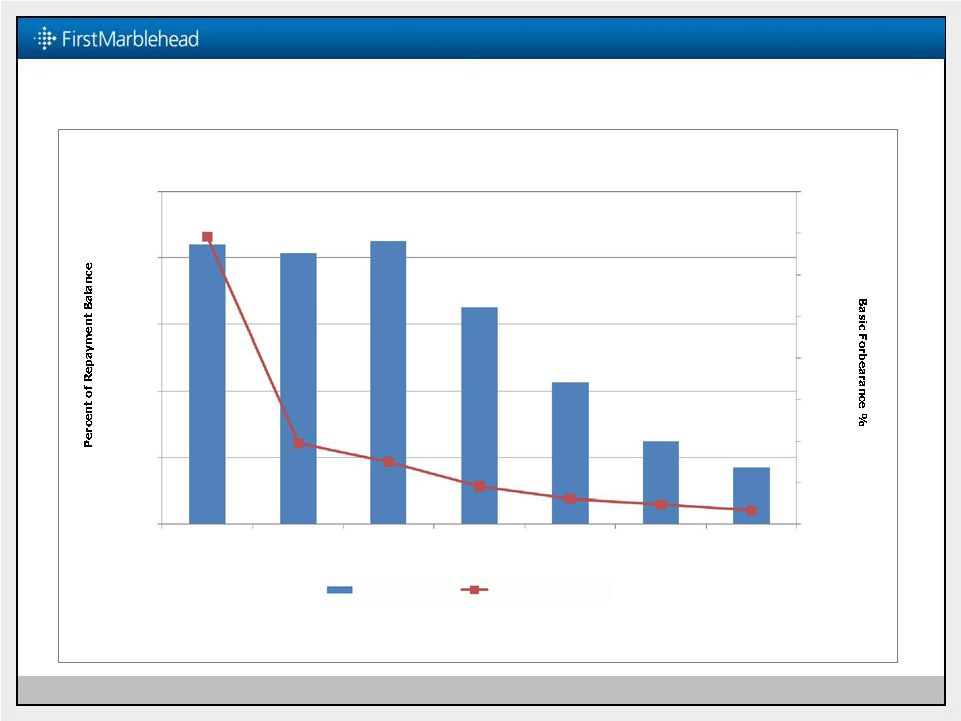

ABS East

Conference Investor Presentation - 13

Basic Forbearance

Most Prevalent in Year 1 of Repayment

Payments Due at Time of Entering Basic Forbearance

Current

Seasoning

Current

Forbearance

25%

20%

15%

10%

5%

0%

0-12

13-24

25-36

37-48

49-60

61-72

73+

0%

2%

4%

6%

8%

10%

12%

14%

16%

Basic

Forbearance

as

a

Percent

of

Repayment

Balance

¹

1

1

Based on NCSLT data on PHEAA serviced loans as of September 30, 2011. Basic Forbearance does

not include loans in alternative payment plans, and alternative payment plans may

reduce utilization of basic forbearance. Repayment Balance includes all loans in repayment status

as of 9/30/2011, including loans in basic forbearance, alternative payment plans, and loans

that have entered repayment status and subsequently deferred payment.

|

ABS East

Conference Investor Presentation - 14

Legacy Portfolio Risk Segmentation

1)

Outstanding

aggregate

principal

and

capitalized

interest

balance

as

of

June

30,

2011.

2)

Loans “not in repayment”

include loans in deferment or basic forbearance status as of June 30, 2011. We

classify loans subject to alternative payment plans, a form of forbearance, as “in

repayment.” 3)

Historical and projected defaults over the lives of the trusts as a percentage of original

outstanding aggregate principal.

4)

Historical and projected recoveries, net of historical and projected collection costs, as a

percentage of historical and projected cumulative gross defaults.

5)

Historical and projected defaults over the lives of the trusts less historical and projected

recoveries, net of collection costs, as a percentage of original outstanding aggregate

principal. 6)

Amount presented is the weighted average conditional prepayment rate (CPR) over the lives of

the trusts. The CPR is an estimate of the likelihood that a loan will be prepaid

during a period given that it has not previously defaulted or been repaid in

full. Source: FMD 10-K for the fiscal year ending June 30, 2011

June 30, 2011

NCSLT Portfolio

Segment 1

Segment 2

Segment 3

Distribution by original loan amount

25.5%

27.0%

47.5%

Distribution by total outstanding loan amount(1):

Not in repayment(2)

2.4

4.1

11.0

In repayment(2)

20.8

23.6

38.0

Gross default rate(3)

10.5

21.4

52.2

Recovery rate(4)

36.3

32.1

22.1

Net default rate(5)

6.7

14.5

40.7

Prepayment rate(6)

7.1

5.1

3.2 |

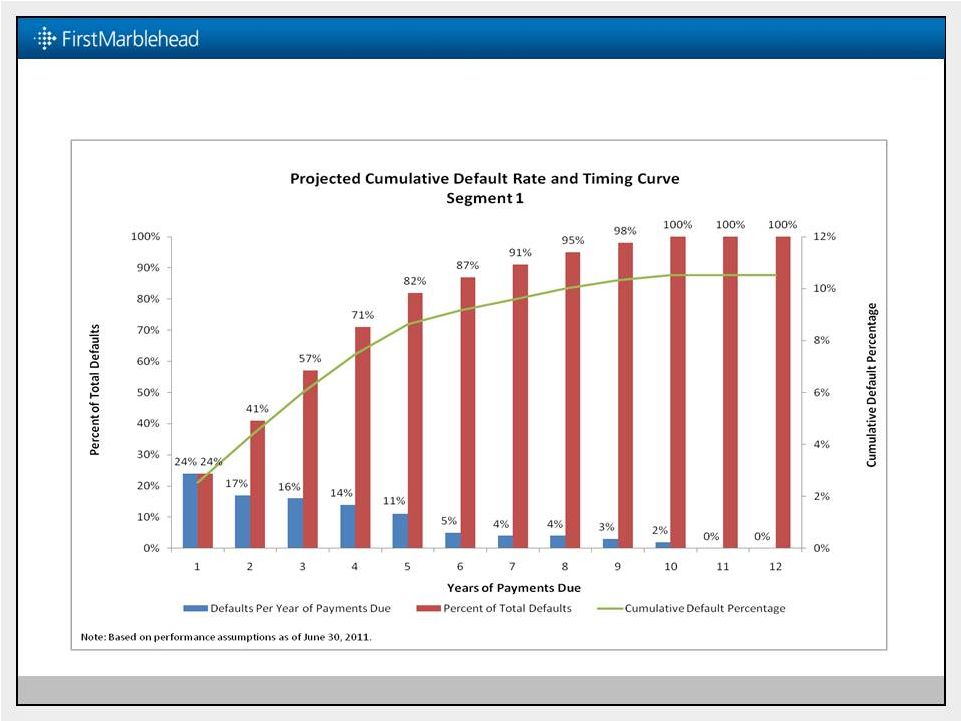

Better Credits

Tend to Follow the Economy ABS East Conference Investor Presentation - 15 |

Segment 2 Curve

More Frontloaded Than Segment 1 ABS East Conference Investor Presentation - 16 |

Lower Credits at

Higher Risk of First Payment Default ABS East Conference Investor Presentation -

17 |

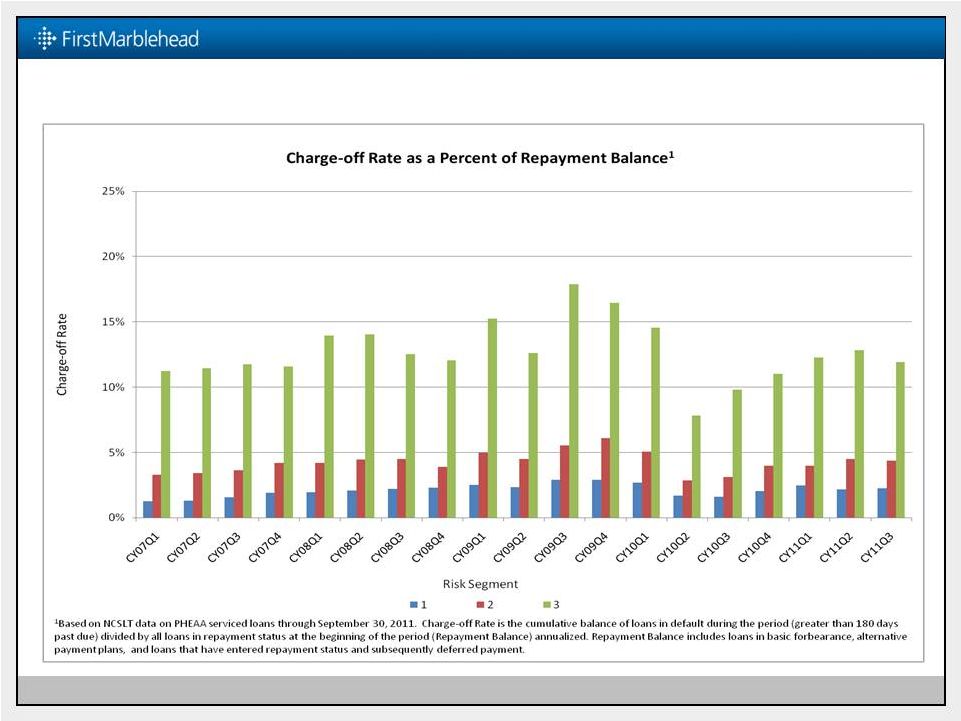

Charge-off

Rates Down From Peak in CY 2009 ABS East Conference Investor Presentation -

18 1

|

ABS East

Conference Investor Presentation - 19

Section III

Data Driven Approach to Risk & Portfolio Management |

Core Principles

of Credit Risk for Private Student Loans ABS East Conference Investor Presentation -

20 Data and Analytics

must be a Priority

Effective,

Quantitative

Underwriting

Market Responsibly

to Students

Dynamic Portfolio

Management

Ongoing Effort to

Determine LTV for

Student Loans

•

Complex asset class requires sophisticated analytical capabilities

•

Integration of multiple sources of historical data with prospective

modeling

•

Proprietary underwriting scorecard looks extensively at credit

profile of both student and cosigner

•

Approve schools based on risk parameters

•

Prevent over-borrowing

•

Seek to avoid adverse selection

•

Involve the cosigner early and often

•

•

Ideally, assign a value to the student’s education

•

Pursue through data gathering and analysis of borrower behavior

Apply adaptive strategies to fit borrowers’ changing credit profiles

|

ABS East

Conference Investor Presentation - 21

FMD Proprietary Scorecard: Summary

Scorecard Results

•

Target variable: probability of default within first 2 years of time in repayment (exposure

time)

•

Effectively ranks applications from high to low risk of default

•

Requires

fewer

declined

applications

in

order

to

reduce

defaults

than

using

traditional

credit

score or previous version of the score

•

Variables scrutinized by internal legal and compliance functions

Predictive Attributes

•

Product

attributes:

repayment

option,

loan

amount,

expected

time

in

deferment,

applicant

income and homeowner status, student’s grade level and undergraduate/graduate

status •

Cosigner presence and credit

•

Credit bureau data across multiple asset classes: FICO, charge-offs, inquiries,

indebtedness, performance on all assets

•

The score attributes can be grouped into the following:

–

Application information

–

Wealth of credit experience

–

Delinquencies and derogatory information

–

Level of recent credit activity

–

Utilization of credit and level of indebtedness

Result:

FMD

Scorecard

continues

to

outperform

other

generic

credit

scores

for

underwriting

private

student

loans |

ABS East

Conference Investor Presentation - 22

FMD Proprietary Scorecard: Version 2 Implemented in 2011

Updating a scorecard is standard procedure

•

We expect to deploy updates every 12-24 months

•

External validation of model part of update process

Updated Scorecard uses additional 18 months of performance data

•

Now includes 2008-2009 performance data

•

Doubled

the

number

of

loans

with

at

least

two

years

of

repayment

history

•

Now includes recession period data

Continued analysis leads to enhancements

•

Refinement of variables, such as:

–

Presence and type of mortgage handled differently and separately

–

Utilization of credit on other accounts looked at more granularly

–

‘Hunger for credit’

looks beyond just inquiries

–

Thick vs. thin files

•

New variables, such as:

–

Income

–

Year in school, including undergraduate vs. graduate student

–

Amount of deferment requested

Refined structure

•

Sub-scores for both student and cosigner

•

Traditional credit score not used in sub-scores; instead it is combined with the

sub-scores on segments of population

|

ABS East

Conference Investor Presentation - 23

* Analysis based on historical school-certified volume from institutions currently on

FMD School List FMD Proprietary Scorecard: Improved Default Capture Rate

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Percent of Applications

To Remove 75% of Defaults

•

Eliminate worst 55% using FICO

•

Eliminate worst 35% using FMD1

•

Eliminate worst 26% using FMD2

•

Worst 15% assigned by FMD Score Version 2

captures 58% of defaults

•

Worst 15% assigned by FMD Score Version 1 captures 50%

of defaults

•

Worst 15% assigned by FICO Score captures 35% of

defaults

Cosigner FICO

FMD Score Version 1

FMD Score Version 2

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% |

ABS East

Conference Investor Presentation - 24

Robust Analytics Throughout Life Cycle

Credit Scoring

Fraud Mitigation

Prepayment

Drop-Out Probability

Early Awareness

Collectability

Recoverability

Monthly Default Risk Score

Our suite of risk models are used throughout the life cycle of a

loan to optimize profitability and manage risk |

ABS East

Conference Investor Presentation - 25

Validation and Controls are Vital to Protecting Monogram Platform’s

Integrity

Internal Controls

Maintain a dedicated Enterprise Risk

Management staff

Internal controls are regularly audited by

KPMG and Corporate Audit staffs

External Validation

Third-party review and validation of

proprietary rank order model

Third-party review and validation of method

of performance data analysis

Regulatory Oversight

Subject to SEC and NYSE regulation and

oversight as a publicly traded company

Subject to FRB supervision and examination

as a savings and loan holding company

MONOGRAM

PLATFORM |

ABS East

Conference Investor Presentation - 26

Performance-Driven Portfolio Management Strategy

•

Account segmentation strategy driven by risk-based scoring model outcomes

•

Proactive borrower contact strategies to yield favorable repayment performance

•

Aggressive early delinquency coordination with servicer to decrease roll rates

•

Rigorous collection agency management to improve liquidation rates

•

Robust skip tracing techniques to increase success in locating borrowers

•

Efficient recovery process to result in greater and faster loss mitigation

•

Granular performance-based portfolio reporting to improve transparency

|

ABS East

Conference Investor Presentation - 27

Section IV

Monogram

®

Platform –

The Next Generation of Private Student Lending |

Monogram

Platform Incorporates FMD’s Core Competencies •School Focused

(GATE)

•Consumer

Focused (NCSLT)

•Credit Focused

(Monogram

Platform)

Customized

Program

Design

Dedicated

Sales

Support

Credit-driven

Loan

Origination

Process

Capital

Markets

Expertise

Active

Portfolio

Management

MONOGRAM

PLATFORM

1

Generation

Product

2

Generation

Product

3

Generation

Product

st

nd

rd

ABS East Conference Investor Presentation - 28 |

ABS East

Conference Investor Presentation - 29

Monogram Platform Designed to Source the Best Credits

Targeting and approving only higher credit quality applicants

•

Focuses

on

the

best

legacy

loans

–

Segment

1

•

Removes any non-school-certified historical products

•

Limits school list to traditional Title IV schools with lower FFELP cohort default

rates Granular risk segmentation allows for better risk-based pricing

•

Credit quality of borrower and cosigner evaluated in decision process

•

FICO only part of the story

•

Repay type and term are controlled

School involved in the process

•

Student enrollment and loan amount certified by school

•

Funds disbursed directly to school

Monitor results

•

Daily review of actual portfolio distribution

•

Proactive portfolio management

•

Agility to evolve program as necessary in a timely manner |

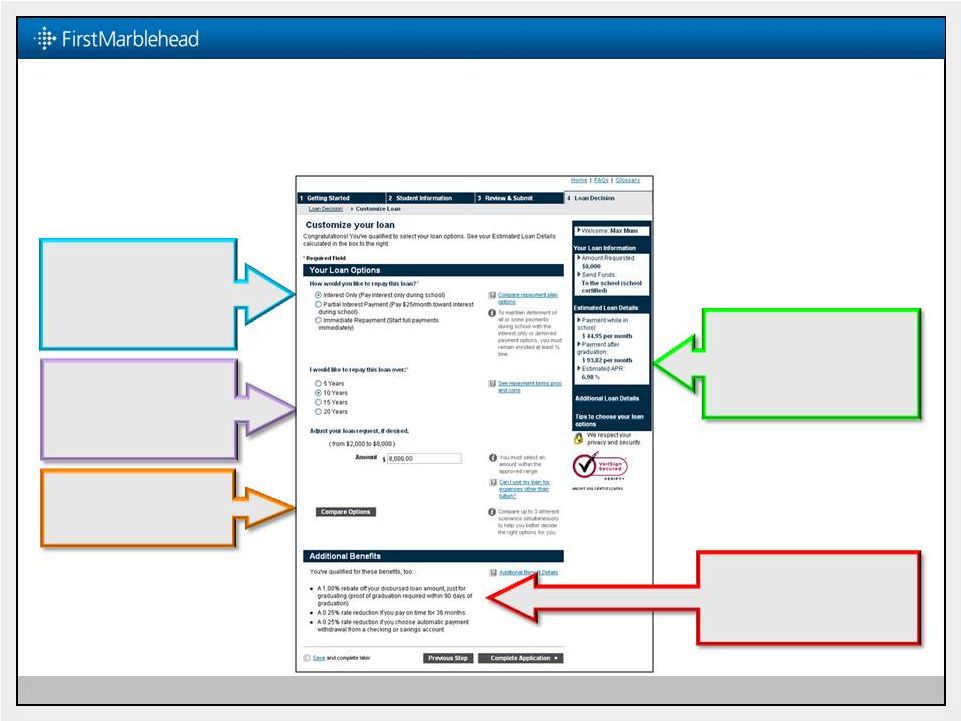

ABS East

Conference Investor Presentation - 30

Innovative Application Process Keeps Borrower Informed at All Times

•

Real-time product

comparison and

analysis is available

•

Choice of repayment

option and repayment

term will impact

borrower’s loan

interest rate

•

Borrower can adjust

the approved loan

amount to meet

optimal needs

•

Borrower sees, in real-

time, how changing the

combination of these

attributes affect interest

rate and monthly payment

•

Borrower benefits can be

tied to any of the product

attributes to influence

portfolio composition |

ABS East

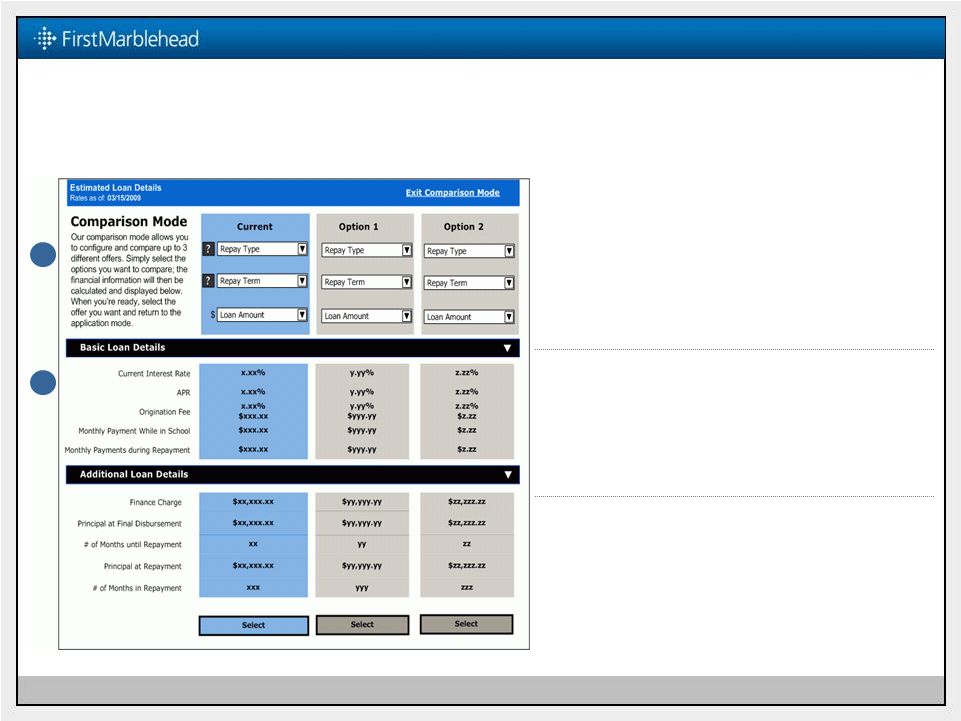

Conference Investor Presentation - 31

1

2

Product Comparison Page Encourages Smart Borrowing

1

Product

Comparison

Feature

Borrowers can compare up to 3

product options by selecting

Repayment Type and Repayment

Term. Loan amount will be pre-

populated

2

Loan Details

Borrowers can expand the additional

pricing details to view and compare

the impact of their choices side-by-

side to drive smarter decisions |

ABS East

Conference Investor Presentation - 32

Monogram Platform Yielding High Quality Portfolios

Union Federal Booked Volume Characteristics through October 10, 2011

Weighted Average Interest Rate

One Month LIBOR + 6.1%

Booked Volume

$18.6 million

Application Request Volume

$310.4 million

Weighted Average FICO Score

753

Immediate Repay/Interest Only/Reduced

Interest/Full Defer

15%/23%/19%/42%

5 Year/10 Year/15 Year

27%/40%/33%

% School-Certified/Disbursed to School

100%

% Undergraduate/Graduate Degree-granting

Programs

100%

% Cosigned

87%

Projected Weighted Average Life

5.7 yrs

Projected Cumulative Gross Default Rate

6.4%

Approval Rate

16% |

ABS East

Conference Investor Presentation - 33

Borrower Choices Reflect Smart Borrowing

Union Federal Booked Volume through October 10, 2011

88% Cosigned

67% of loans are 5-

or 10-year terms

58% are immediately cash flowing upon disbursement

Tier

Payment Option:

Term:

1

2

3

4

5

6

7

8

9

10

SubTotal:

Immediate

Repay

IM

5

0.3%

0.9%

1.2%

1.1%

1.2%

0.8%

0.5%

0.4%

0.2%

0.3%

6.8%

IM

10

0.2%

0.4%

1.0%

1.1%

1.0%

0.5%

0.5%

0.3%

0.2%

0.0%

5.2%

IM

15

0.2%

0.2%

0.2%

0.8%

0.4%

0.2%

0.5%

0.2%

0.1%

0.0%

2.8%

Interest

Only

IO

5

0.2%

0.8%

1.3%

1.7%

1.8%

1.2%

0.5%

0.5%

0.3%

0.3%

8.6%

IO

10

0.6%

0.8%

2.1%

1.9%

2.1%

1.5%

1.3%

0.5%

0.1%

0.3%

11.0%

IO

15

0.1%

0.1%

1.0%

0.5%

0.7%

1.1%

0.1%

0.2%

0.0%

0.0%

3.9%

Partial

Interest

PI

5

0.0%

0.3%

1.0%

0.5%

0.4%

0.4%

0.3%

0.2%

0.1%

0.0%

3.2%

PI

10

0.1%

0.3%

0.8%

1.5%

2.0%

1.5%

1.3%

0.8%

0.2%

0.6%

9.0%

PI

15

0.0%

0.4%

0.6%

0.8%

2.0%

1.7%

0.7%

0.3%

0.3%

0.5%

7.2%

Full

Deferment

DF

5

0.5%

0.9%

1.1%

1.1%

1.6%

1.2%

0.9%

0.4%

0.4%

0.5%

8.6%

DF

10

0.2%

1.3%

2.1%

2.0%

4.0%

2.3%

1.7%

0.8%

0.3%

0.6%

15.1%

DF

15

0.1%

0.9%

3.9%

2.6%

2.7%

2.1%

3.6%

1.0%

1.2%

0.5%

18.6%

SubTotal:

2.4%

7.2%

16.3%

15.4%

19.8%

14.4%

11.9%

5.7%

3.4%

3.5%

Wtd Avg. FICO Score:

789

777

770

768

755

743

736

720

721

722

753

% Homeownership

96.1%

93.0%

92.3%

86.7%

79.3%

74.5%

72.0%

70.7%

50.9%

64.4%

80.4%

Avg. age of oldest trade line (yrs)

23.6

22.0

23.0

21.3

20.1

19.2

17.2

16.7

16.6

16.0

20.0 |

ABS East

Conference Investor Presentation - 34

Capital Markets Contacts |