Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - AMERICAN WOODMARK CORP | awcex21.htm |

| EX-31.2 - EXHIBIT 31.2 - AMERICAN WOODMARK CORP | awcex312.htm |

| EX-32.1 - EXHIBIT 32.1 - AMERICAN WOODMARK CORP | awcex321.htm |

| EX-23.1 - EXHIBIT 23.1 - AMERICAN WOODMARK CORP | awcex231.htm |

| EX-31.1 - EXHIBIT 31.1 - AMERICAN WOODMARK CORP | awcex311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended April 30, 2011

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Commission File Number 000-14798

AMERICAN WOODMARK CORPORATION

(Exact name of registrant as specified in its charter)

|

VIRGINIA

|

54-1138147

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

3102 Shawnee Drive, Winchester, Virginia 22601

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: (540) 665-9100

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Stock (no par value)

|

NASDAQ Global Select Market

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [X] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the registrant's Common Stock, no par value, held by non-affiliates of the registrant as of October 29, 2010, the last business day of the Company’s most recent second quarter was $189,305,748.

As of June 20, 2011, 14,296,740 shares of the Registrant's Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement for the Annual Meeting of Shareholders to be held on August 25, 2011 (“Proxy Statement”) are incorporated by reference into Part III of this Form 10-K.

PART I

|

Item 1.

|

BUSINESS

|

American Woodmark Corporation (“American Woodmark” or the “Company”) manufactures and distributes kitchen cabinets and vanities for the remodeling and new home construction markets. American Woodmark was incorporated in 1980 by the four principal managers of the Boise Cascade Cabinet Division through a leveraged buyout of that division. American Woodmark was operated privately until 1986 when it became a public company through a registered public offering of its common stock.

American Woodmark currently offers framed stock cabinets in approximately 500 different cabinet lines, ranging in price from relatively inexpensive to medium-priced styles. Styles vary by design and color from natural wood finishes to low-pressure laminate surfaces. The product offering of stock cabinets includes 83 door designs in 18 colors. Stock cabinets consist of a common box with standard interior components and a maple, oak, cherry, or hickory front frame, door and/or drawer front.

Products are primarily sold under the brand names of American Woodmark®, Timberlake®, Shenandoah Cabinetry®, Potomac®, and Waypoint Living Spaces ®.

American Woodmark’s products are sold on a national basis across the United States to the remodeling and new home construction markets. The Company services these markets through three primary channels: home centers, builders, and independent dealers and distributors. The Company provides complete turnkey installation services to its direct builder customers via its network of nine service centers that are strategically located throughout the United States. The Company distributes its products to each market channel directly from four assembly plants through a third party logistics network.

The primary raw materials used include hard maple, oak, cherry, soft maple, and hickory lumber and plywood. Additional raw materials include paint, particleboard, manufactured components, and hardware. The Company currently purchases paint from one supplier; however, other sources are available. Other raw materials are purchased from more than one source and are readily available.

American Woodmark operates in a highly fragmented industry that is composed of several thousand local, regional, and national manufacturers. The Company’s principal means for competition is its breadth and variety of product offering, expanded service capabilities, geographic reach and affordable quality. The Company believes it is one of the three largest manufacturers of kitchen cabinets in the United States.

The Company’s business has historically been subject to seasonal influences, with higher sales typically realized in the second and fourth fiscal quarters. General economic forces and changes in the Company’s customer mix have reduced seasonal fluctuations in revenue over the past few years. The Company does not consider its level of order backlog to be material.

In recognition of the cyclicality of the housing industry, the Company’s policy is to operate with a minimal amount of financial leverage. The Company regularly maintains a debt to capital ratio below 15%, and working capital exclusive of cash of less than 6% of net sales. At April 30, 2011, debt to capital was 13.8%, and working capital net of cash was 3.1% of net sales.

During the last fiscal year, American Woodmark had two primary customers, The Home Depot and Lowe’s Companies, Inc., which together accounted for approximately 73% of the Company’s sales in its fiscal year ended April 30, 2011 (fiscal 2011). The loss of either customer would have a material adverse effect on the Company.

As of May 31, 2011, the Company had 3,693 employees. Approximately 10% of the Company’s employees are represented by labor unions. The Company believes that its employee relations are good.

2

American Woodmark’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, and all amendments to those reports are available free of charge on the Company’s web site at www.americanwoodmark.com as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission. The contents of the Company’s web site are not, however, part of this report.

|

Item 1A.

|

RISK FACTORS

|

There are a number of business risks and uncertainties that may affect the Company’s business, results of operations and financial condition. These risks and uncertainties could cause future results to differ from past performance or expected results, including results described in statements elsewhere in this report that constitute "forward-looking statements" under the Private Securities Litigation Reform Act of 1995. Additional risks and uncertainties not presently known to the Company or it currently believes to be immaterial also may adversely impact the business. Should any risks or uncertainties develop into actual events, these developments could have material adverse effects on the Company’s business, financial condition, and results of operations. These risks and uncertainties, which the Company considers to be most relevant to specific business activities, include, but are not limited to, the following, as well as additional risk factors included in Item 7A, "Quantitative and Qualitative Disclosures about Market Risk." Additional risks and uncertainties that may affect the Company’s business, results of operations and financial condition are discussed in this report, including in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under the headings “Forward-Looking Statements,” “Market Risks,” and “Outlook for Fiscal 2012”.

Our business relies on remodeling activity and residential construction. The Company’s results of operations are affected by levels of home improvement and residential construction activity, including repair and remodeling and new construction. Job creation levels, interest rates, availability of credit, energy costs, consumer confidence, national and regional economic conditions, and weather conditions and natural disasters can significantly impact levels of home improvement and residential construction activity.

Our future financial performance depends in part on the success of our new product development and other growth strategies. The Company has increased its emphasis on new product development in recent years and continues to focus solely on organic growth. Consequently, the Company’s financial performance will, in part, reflect its success in implementing its growth strategies in its existing markets and in introducing new products.

The loss of, or a reduction in business from, either of our key customers would have a material adverse effect on our business. The size and importance to the Company of its two largest customers is significant. These customers could make significant changes in their volume of purchases and could otherwise significantly affect the terms and conditions on which the Company does business. Sales to The Home Depot and Lowe’s Companies, Inc. were approximately 73% of total company sales for fiscal 2011. Although builders, dealers, and other retailers represent other channels of distribution for the Company's products, an unplanned loss of a substantial portion of sales to The Home Depot or Lowe’s Companies, Inc. would have a material adverse impact on the Company.

Our operating results are affected by the cost and availability of raw materials. Because the Company is dependent on outside suppliers for raw material needs, it must obtain sufficient quantities of quality raw materials from its suppliers at acceptable prices and in a timely manner. The Company has no long-term supply contracts with its key suppliers. A substantial decrease in the availability of products from the Company’s suppliers, the loss of key supplier arrangements, or a substantial increase in the cost of its raw materials could adversely impact the Company’s results of operations.

We may not be able to maintain or raise the prices of our products in response to inflation and increasing costs. Short-term market and competitive pressures may prohibit the Company from raising prices to offset inflationary raw material and freight costs, which would adversely impact profit margins.

The economic recession is adversely impacting demand for the housing industry. Through fiscal year 2011, the Company’s sales levels have fallen by 46% from their peak levels in 2006. If market conditions continue to decline, the Company’s sales, earnings, and cash flow would continue to be adversely impacted.

3

|

Item 1B.

|

UNRESOLVED STAFF COMMENTS

|

None.

|

Item 2.

|

PROPERTIES

|

American Woodmark leases its Corporate Office located in Winchester, Virginia. In addition, the Company leases 1 manufacturing facility in Hardy County, West Virginia and owns 10 manufacturing facilities located primarily in the eastern United States. The Company also leases 9 primary service centers, 2 satellite service centers, and 3 additional office centers located throughout the United States that support the sale and distribution of products to each market channel. The Company considers its properties suitable for the business and adequate for its needs.

Primary properties as of April 30, 2011 include:

|

LOCATION

|

DESCRIPTION

|

|

Allegany County, MD

|

Manufacturing Facility

|

|

Berryville, VA

|

Service Center*

|

|

Chavies, KY

|

Manufacturing Facility

|

|

Coppell, TX

|

Service Center*

|

|

Gas City, IN

|

Manufacturing Facility

|

|

Hardy County, WV

|

Manufacturing Facility*

|

|

Hardy County, WV

|

Manufacturing Facility

|

|

Houston, TX

|

Satellite Service Center*

|

|

Humboldt, TN

|

Manufacturing Facility

|

|

Huntersville, NC

|

Service Center*

|

|

Jackson, GA

|

Manufacturing Facility

|

|

Kingman, AZ

|

Manufacturing Facility

|

|

Kennesaw, GA

|

Service Center*

|

|

Montgomeryville, PA

|

Service Center*

|

|

Monticello, KY

|

Manufacturing Facility

|

|

Orange, VA

|

Manufacturing Facility

|

|

Orlando, FL

|

Service Center*

|

|

Raleigh, NC

|

Satellite Service Center*

|

|

Phoenix, AZ

|

Service Center*

|

|

Rancho Cordova, CA

|

Service Center*

|

|

Tampa, FL

|

Service Center*

|

|

Toccoa, GA

|

Manufacturing Facility

|

|

Winchester, VA

|

Corporate Office*

|

|

Winchester, VA

|

Office (Customer Service)*

|

|

Winchester, VA

|

Office (MIS)*

|

|

Winchester, VA

|

Office (Product Dev./Logistics)*

|

*Leased facility.

In addition, American Woodmark owns one manufacturing facility that is permanently closed and one facility with operations suspended.

4

|

Item 3.

|

LEGAL PROCEEDINGS

|

The Company is involved in suits and claims in the normal course of business, including without limitation product liability and general liability claims, and claims pending before the Equal Employment Opportunity Commission. On at least a quarterly basis, the Company consults with its legal counsel to ascertain the reasonable likelihood that such claims may result in a loss. As required by ASC Topic 450, “Contingencies” (ASC 450), the Company categorizes the various suits and claims into three categories according to their likelihood for resulting in potential loss: those that are probable, those that are reasonably possible and those that are deemed to be remote. The Company accounts for these loss contingencies in accordance with ASC 450. Where losses are deemed to be probable and estimable, accruals are made. Where losses are deemed to be reasonably possible or remote, a range of loss estimates is determined and considered for disclosure. Where no loss estimate range can be made, the Company and its counsel perform a worst-case estimate. In determining these loss range estimates, the Company considers known values of similar claims and consultation with independent counsel.

The Company believes that the aggregate range of estimated loss stemming from the various suits and asserted and unasserted claims which were deemed to be either probable or reasonably possible was not material as of April 30, 2011.

Also see the information under “Legal Matters” under “Note K – Commitments and Contingencies” to the Consolidated Financial Statements included in this report under Item 8, “Financial Statements and Supplementary Data”.

|

Item 4.

|

(REMOVED AND RESERVED)

|

EXECUTIVE OFFICERS OF THE REGISTRANT

Executive officers of the Company are elected by the Board of Directors and generally hold office until the next annual election of officers. There are no family relationships between any executive officer and any other officer or director of the Company or any arrangement or understanding between any executive officer and any other person pursuant to which such officer was elected. The executive officers of the Company as of April 30, 2011 are as follows:

|

Name

|

Age

|

Position(s) Held During

Past Five Years

|

|

Kent B. Guichard

|

55

|

Company Chairman, President and Chief Executive Officer from August 2009 to present; Company President and Chief Executive Officer from August 2007 to August 2009; Company President and Chief Operating Officer from August 2006 to August 2007; Company Executive Vice President and Chief Operating Officer from August 2005 to August 2006; Company Director from November 1997 to present.

|

|

Jonathan H. Wolk

|

49

|

Company Senior Vice President and Chief Financial Officer from September 2010 to present; Company Vice President and Chief Financial Officer from December 2004 to September 2010; Company Corporate Secretary from May 2005 to present.

|

|

S. Cary Dunston

|

46

|

Company Senior Vice President, Manufacturing and Logistics from October 2006 to present; Vice President, Global Operations of Diamond Innovations (a private supplier of industrial diamonds) from March 2005 to September 2006.

|

5

|

Bradley S. Boyer

|

53

|

Company Senior Vice President, Remodeling Sales and Marketing from September 2010 to present; Company Vice President, Remodeling Sales and Marketing from July 2008 to September 2010; Company Vice President, Home Center Sales and Marketing from January 2005 to July 2008.

|

PART II

|

Item 5.

|

MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

MARKET INFORMATION

American Woodmark Corporation common stock is quoted on The NASDAQ Global Select Market under the “AMWD” symbol. Common stock per share market prices and cash dividends declared during the last two fiscal years were as follows:

|

MARKET PRICE

|

DIVIDENDS

|

|||||||||||

|

(in dollars)

|

High

|

Low

|

DECLARED

|

|||||||||

|

FISCAL 2011

|

||||||||||||

|

First quarter

|

$ | 25.41 | $ | 15.51 | $ | 0.09 | ||||||

|

Second quarter

|

20.56 | 15.00 | 0.09 | |||||||||

|

Third quarter

|

25.16 | 17.09 | 0.09 | |||||||||

|

Fourth quarter

|

21.99 | 18.12 | 0.09 | |||||||||

|

FISCAL 2010

|

||||||||||||

|

First quarter

|

$ | 24.99 | $ | 17.35 | $ | 0.09 | ||||||

|

Second quarter

|

25.33 | 18.67 | 0.09 | |||||||||

|

Third quarter

|

21.12 | 18.21 | 0.09 | |||||||||

|

Fourth quarter

|

25.72 | 18.11 | 0.09 | |||||||||

As of May 24, 2011, there were approximately 5,200 shareholders of record of the Company's common stock. Included are approximately 75% of the Company's employees, who are shareholders through the American Woodmark Stock Ownership Plan. The Company has paid dividends on its common stock during each fiscal quarter presented above. The determination as to the payment and the amount of any future dividends will be made by the Board of Directors from time to time and will depend on the Company’s then-current financial condition, capital requirements, results of operations and any other factors then deemed relevant by the Board of Directors.

On August 24, 2007, the Company announced that the Company’s Board of Directors approved the repurchase of up to $100 million of the Company’s common stock. This authorization has no expiration date. In the fourth quarter of 2011, the Company did not repurchase any shares under this authorization. At April 30, 2011, $93.3 million remained authorized by the Company’s Board of Directors to repurchase shares of the Company’s common stock.

6

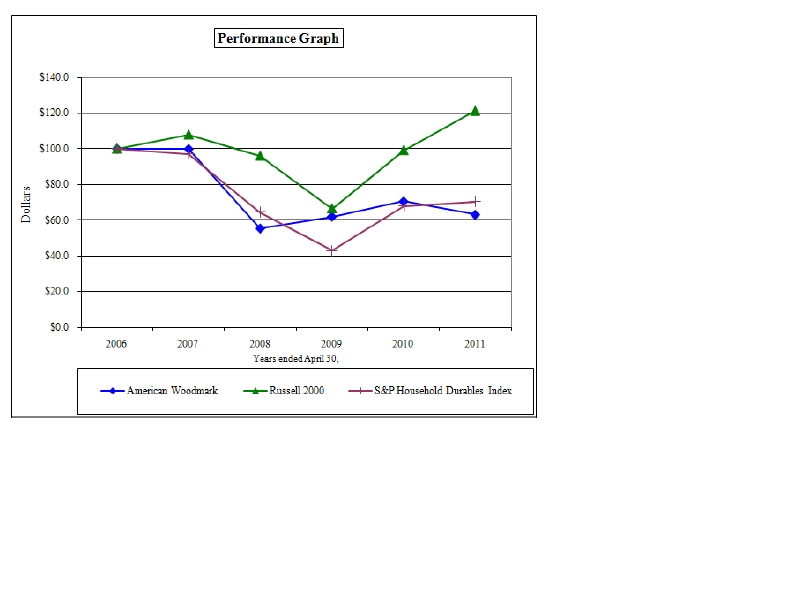

STOCK PERFORMANCE GRAPH

Set forth below is a graph comparing the five-year cumulative total shareholder return, including reinvestment of dividends, from investing $100 on May 1, 2006 through April 30, 2011 in American Woodmark Corporation common stock, the Russell 2000 Index and the S&P Household Durables Index:

7

|

Item 6.

|

SELECTED FINANCIAL DATA

|

|

FISCAL YEARS ENDED APRIL 30

|

||||||||||||||||||||

|

(in millions, except per share data)

|

2011 | 1 | 2010 | 1 | 2009 | 1 | 2008 | 2007 | ||||||||||||

|

FINANCIAL STATEMENT DATA

|

||||||||||||||||||||

|

Net sales

|

$ | 452.6 | $ | 406.5 | $ | 545.9 | $ | 602.4 | $ | 760.9 | ||||||||||

|

Income (loss) before income taxes

|

(30.0 | ) | (37.1 | ) | (6.2 | ) | 5.7 | 51.2 | ||||||||||||

|

Net income (loss)

|

(20.0 | ) | (22.3 | ) | (3.2 | ) | 4.3 | 32.6 | ||||||||||||

|

Earnings (loss) per share:

|

||||||||||||||||||||

|

Basic

|

(1.40 | ) | (1.58 | ) | (0.23 | ) | 0.30 | 2.08 | ||||||||||||

|

Diluted

|

(1.40 | ) | (1.58 | ) | (0.23 | ) | 0.29 | 2.04 | ||||||||||||

|

Depreciation and amortization expense

|

26.7 | 30.9 | 35.1 | 35.2 | 35.9 | |||||||||||||||

|

Total assets

|

268.4 | 282.4 | 303.7 | 314.8 | 348.7 | |||||||||||||||

|

Long-term debt, less current maturities

|

24.7 | 25.6 | 26.5 | 26.0 | 26.9 | |||||||||||||||

|

Total shareholders’ equity

|

154.0 | 175.3 | 203.7 | 214.6 | 226.1 | |||||||||||||||

|

Cash dividends declared per share

|

0.36 | 0.36 | 0.36 | 0.33 | 0.21 | |||||||||||||||

|

Average shares outstanding

|

||||||||||||||||||||

|

Basic

|

14.3 | 14.1 | 14.1 | 14.5 | 15.7 | |||||||||||||||

|

Diluted

|

14.3 | 14.1 | 14.1 | 14.5 | 16.0 | |||||||||||||||

|

PERCENT OF SALES

|

||||||||||||||||||||

|

Gross profit

|

11.7 | % | 12.0 | % | 16.4 | % | 17.1 | % | 20.5 | % | ||||||||||

|

Selling, general and administrative expenses

|

18.5 | 20.5 | 15.9 | 16.4 | 14.0 | |||||||||||||||

|

Income (loss) before income taxes

|

(6.6 | ) | (9.1 | ) | (1.1 | ) | 0.9 | 6.7 | ||||||||||||

|

Net income (loss)

|

(4.4 | ) | (5.5 | ) | (0.6 | ) | 0.7 | 4.3 | ||||||||||||

|

RATIO ANALYSIS

|

||||||||||||||||||||

|

Current ratio

|

2.4 | 2.5 | 2.6 | 2.6 | 2.4 | |||||||||||||||

|

Inventory turnover2

|

16.1 | 12.3 | 11.5 | 9.7 | 9.7 | |||||||||||||||

|

Collection period – days3

|

30.1 | 32.9 | 33.5 | 31.9 | 34.9 | |||||||||||||||

|

Percentage of capital (long-term debt plus equity):

|

||||||||||||||||||||

|

Long-term debt, less current maturities

|

13.8 | % | 12.7 | % | 11.5 | % | 10.8 | % | 10.6 | % | ||||||||||

|

Equity

|

86.2 | 87.3 | 88.5 | 89.2 | 89.4 | |||||||||||||||

|

Return on equity (average %)

|

(12.2 | ) | (11.8 | ) | (1.5 | ) | 1.9 | 13.9 | ||||||||||||

| 1 |

The Company performed a reduction-in-force of salaried personnel and announced plans to realign its manufacturing network during fiscal 2009. The impact of these initiatives in fiscal 2009 reduced operating income (loss), net income (loss) and earnings (loss) per share by $9,743,000, $6,050,000 and $0.43, respectively. During fiscal 2010, these same initiatives increased operating loss, net loss and loss per share by $2,808,000, $1,722,000 and $0.12, respectively. During fiscal 2011, these same initiatives increased operating loss, net loss and loss per share by $62,000, $39,000 and $0.00, respectively.

|

|

| 2 |

Based on the average of beginning and ending inventory.

|

|

| 3 |

Based on the ratio of average monthly customer receivables to average sales per day.

|

8

|

Item 7.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

Results of Operations

The following table sets forth certain income and expense items as a percentage of net sales:

|

PERCENTAGE OF NET SALES

|

||||||||||||

|

Years Ended April 30

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

Net sales

|

100.0 | % | 100.0 | % | 100.0 | % | ||||||

|

Cost of sales and distribution

|

88.3 | 88.0 | 83.6 | |||||||||

|

Gross profit

|

11.7 | 12.0 | 16.4 | |||||||||

|

Selling and marketing expenses

|

13.5 | 14.0 | 11.0 | |||||||||

|

General and administrative expenses

|

5.0 | 6.5 | 4.9 | |||||||||

|

Restructuring charges

|

0.0 | 0.7 | 1.8 | |||||||||

|

Operating loss

|

(6.8 | ) | (9.2 | ) | (1.3 | ) | ||||||

|

Interest expense/other (income) expense

|

(0.2 | ) | (0.1 | ) | (0.2 | ) | ||||||

|

Loss before income taxes

|

(6.6 | ) | (9.1 | ) | (1.1 | ) | ||||||

|

Income tax benefit

|

(2.2 | ) | (3.6 | ) | (0.5 | ) | ||||||

|

Net loss

|

(4.4 | ) | (5.5 | ) | (0.6 | ) | ||||||

The following discussion should be read in conjunction with the Selected Financial Data and the Consolidated Financial Statements and the related notes contained elsewhere in this report.

Forward-Looking Statements

This report contains statements concerning the Company’s expectations, plans, objectives, future financial performance and other statements that are not historical facts. These statements are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. In most cases, the reader can identify these forward-looking statements by words such as “anticipate,” “estimate,” “forecast,” “expect,” “believe,” “should,” “could,” “would,” “plan,” “may,” or other similar words. Forward-looking statements contained in this annual report, including in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, are based on current expectations and our actual results may differ materially from those projected in any forward-looking statements. In addition, the Company participates in an industry that is subject to rapidly changing conditions and there are numerous factors that could cause the Company to experience a decline in sales and/or earnings or deterioration in financial condition. These include: (1) overall industry demand at reduced levels, (2) economic weakness in a specific channel of distribution, (3) the loss of sales from specific customers due to their loss of market share, bankruptcy or switching to a competitor, (4) a sudden and significant rise in basic raw material costs, (5) a dramatic increase to the cost of diesel fuel and/or transportation related services, (6) the need to respond to price or product initiatives launched by a competitor, (7) the Company’s ability to successfully implement initiatives related to increasing market share, new products, maintaining and increasing its sales force and new product displays and (8) sales growth at a rate that outpaces the Company’s ability to install new capacity. Additional information concerning the factors that could cause actual results to differ materially from those in forward-looking statements is contained in this report, including elsewhere in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, Item 1A, “Risk Factors”, and Item 7A, “Quantitative and Qualitative Disclosures about Market Risk”. While the Company believes that these risks are manageable and will not adversely impact the long-term performance of the Company, these risks could, under certain circumstances, have a material adverse impact on its operating results and financial condition.

Any forward-looking statement that the Company makes, speaks only as of the date of this report. The Company undertakes no obligation to publicly update or revise any forward-looking statements or cautionary factors, as a result of new information, future events or otherwise, except as required by law.

9

Overview

American Woodmark Corporation manufactures and distributes kitchen cabinets and vanities for the remodeling and new home construction markets. Its products are sold on a national basis directly to home centers, major builders and home manufacturers and through a network of independent dealers and distributors. At April 30, 2011, the Company operated 11 manufacturing facilities and 9 service centers across the country.

During the Company’s fiscal year that ended on April 30, 2011 (fiscal 2011), the Company experienced a continuation of difficult housing market conditions that have prevailed since the housing market peaked five years ago. Several emerging positive factors were overshadowed by negatives. Positive factors included private sector job creation of approximately 1.3 million during the Company’s fiscal 2011 and mortgage delinquencies, as reported by the Mortgage Banking Association, reaching their lowest levels in two years. Negative factors included Gross Private Residential Fixed Investment, as reported by the U.S. Department of Commerce, declining during the third and fourth calendar quarters of 2010 and first calendar quarter of 2011 and housing starts declining by 17% and 5% during the three- and twelve-month periods ended April 30, 2011, respectively.

In new home construction, housing starts reached a 50-year low of only 554,000 during fiscal 2011, a decline of 74% compared with 2.1 million housing starts in fiscal 2006. In the remodeling market, sales of existing homes during fiscal 2011 were 4.9 million homes, a 10% reduction from the prior year’s Federal housing stimulus-aided levels and the median home price of houses sold declined by 2%. Although existing home sales levels have stabilized, the combination of declining home prices and elevated unemployment levels have led to relatively weak consumer confidence, causing the Company’s overall market to decline by approximately 5% during fiscal 2011, based upon sales reported by the Kitchen Cabinet Manufacturers Association.

Faced with these challenging market conditions, the Company’s largest remodeling customers chose to utilize aggressive sales promotions during the fall 2010 and spring 2011 selling seasons to boost sales. These promotions consisted of free products and cash discounts to consumers based upon the amount and/or type of cabinets they purchased. The Company’s competitors participated vigorously in these promotional activities and the Company chose to meet these competitive offerings. Price-conscious consumers responded favorably to these promotional offerings and the Company and its large remodeling customers realized increased sales order volumes. The Company’s remodeling sales rose more than 20% in the second half of fiscal 2011 and rose in the low teens for the entire fiscal year.

The Company also realized a mid single digit increase in its new construction sales during fiscal 2011, despite the 5% decline in housing starts. Management believes this result, combined with the Company’s increase in remodeling sales, indicates that the Company realized market share gains in both of its sales channels during fiscal 2011.

In the face of these difficult market conditions, the Company’s net sales, gross profit, net loss and free cash flow all improved during fiscal 2011. Net sales grew by 11%, gross margin grew by 8%, net loss was reduced by 10% and free cash flow (defined as cash from operating activities less cash used for investing activities) improved by nearly $18 million.

Despite the present housing market downturn, the Company believes that the long-term fundamentals for the American housing industry continue to remain positive, based upon favorable population growth, favorable demographics, job creation and low long-term interest rates. Based upon this belief, the Company has continued to invest in improving its operations and its capabilities to service its customers. The Company remains focused on growing its market share and has continued to invest in developing and launching new products and expanding its marketing reach to new customers.

During fiscal 2009, the Company announced cost reduction initiatives, including a salaried reduction-in-force, closure of two of its oldest manufacturing plants and suspension of operations in a third plant. These initiatives were completed during the first quarter of fiscal 2010. The majority

10

of the restructuring charges related to these actions were reflected in the Company’s results for fiscal 2009 and fiscal 2010.

Gross margin for fiscal 2011 was 11.7%, down from 12.0% in fiscal 2010. The slight reduction in the Company’s gross margin rate was driven by increased sales promotion costs. These promotions consisted of free products and cash payments to the Company’s large remodeling customers based upon the amount and/or type of cabinets purchased. The Company’s competitors participated vigorously in these promotional activities and the Company chose to maintain competitive parity by participating as well.

The Company regularly assesses its long-lived assets to determine if any impairment has occurred and regularly evaluates its deferred tax assets to determine whether a valuation allowance is necessary. Although the Company is presently operating at a loss in what appears to be the bottom of the housing market, the Company expects that improvements in market demand and continued market share gains will enable it to return to profitability well before the expiration of the useful lives of its long-lived assets and any applicable tax carryforward periods. Accordingly, the Company has concluded that neither its long-lived assets pertaining to its 11 manufacturing plants nor any of its other long-lived assets were impaired and that no valuation allowance on its deferred tax assets was necessary as of April 30, 2011.

Restructuring charges recorded in connection with the Company’s cost reduction initiatives aggregated $(0.0) million net of tax in fiscal 2011, $(1.7) million net of tax in fiscal 2010 and $(6.0) million net of tax in fiscal 2009. Exclusive of these charges, the Company generated a net loss of $(20.0) million in fiscal 2011, $(20.6) million in fiscal 2010 and net income of $2.8 million in fiscal 2009.

Results of Operations

|

FISCAL YEARS ENDED APRIL 30

|

||||||||||||||||||||

|

(in thousands)

|

2011

|

2010

|

2009

|

2011 vs. 2010 PERCENTCHANGE

|

2010 vs. 2009 PERCENTCHANGE

|

|||||||||||||||

|

Net sales

|

$ | 452,589 | $ | 406,540 | $ | 545,934 | 11 | % | (26 | )% | ||||||||||

|

Gross profit

|

52,751 | 48,921 | 89,490 | 8 | (45 | ) | ||||||||||||||

|

Selling and marketing expenses

|

61,034 | 56,935 | 60,033 | 7 | (5 | ) | ||||||||||||||

|

General and administrative expenses

|

22,709 | 26,434 | 26,875 | (14 | ) | (2 | ) | |||||||||||||

|

Interest expense

|

572 | 637 | 716 | (10 | ) | (11 | ) | |||||||||||||

Net Sales

Net sales were $452.6 million in fiscal 2011, an increase of $46.0 million, or 11%, compared with fiscal 2010. Overall unit volume for fiscal 2011 was 8% higher than in fiscal 2010, driven primarily by the Company’s increased market share. Average revenue per unit increased 3% in fiscal 2011, driven primarily by shifts in product mix.

Net sales for fiscal 2010 decreased 26% to $406.5 million from $545.9 million in fiscal 2009. Overall unit volume for fiscal 2010 was 23% lower than in fiscal 2009, driven primarily by weaker remodeling sales volume. Average revenue per unit decreased 3% during fiscal 2010, driven primarily by an increased proportion of new construction sales within the Company’s sales mix.

Gross Profit

Gross profit as a percentage of sales decreased to 11.7% in fiscal 2011 as compared with 12.0% in fiscal 2010. The impact of increased sales volume in fiscal 2011 created improved labor efficiencies and more favorable absorption of manufacturing overhead costs, which were more than offset by

11

increased sales promotion costs, diesel fuel and material costs. Specific changes and additional information included:

|

·

|

Sales promotion costs increased in order to meet competitors’ promotional offerings to drive sales growth in a challenging market. Most of the sales promotions involved the use of free products or cash reimbursements back to the Company’s large retail customers and were deducted from gross margin as opposed to being classified as operating expenses. Sales promotion costs offset against gross margin increased by 2.2% of net sales during fiscal 2011;

|

|

·

|

Materials and freight costs increased as a percentage of net sales by 1.1% during fiscal 2011 as compared with fiscal 2010, driven primarily by increases in paint, cartons, particleboard and imported components, as well as diesel fuel; and

|

|

·

|

Labor and overhead costs decreased by 3.0% as a percentage of net sales compared with the prior fiscal year, as increased sales volume caused increased productivity of direct labor and absorption of fixed overhead costs.

|

During fiscal 2010, the Company’s gross profit declined as a percentage of net sales from 16.4% to 12.0%. The impact of reduced sales volume in fiscal 2010 created inefficiencies from unabsorbed manufacturing overhead and in labor productivity, which more than offset the beneficial impact of reduced overhead costs related to plant closures, reduction in diesel fuel and material costs and the impact of a $1.3 million insurance recovery. Specific changes and additional information included:

|

·

|

Materials and freight costs decreased as a percentage of net sales by 0.8% during fiscal 2010 as compared with fiscal 2009, driven primarily by declines in diesel fuel and lumber prices; and

|

|

·

|

Labor and overhead costs increased by 5.2% as a percentage of net sales compared with the prior fiscal year, as the 23% decline in sales volume caused reduced productivity of direct labor and under-absorption of fixed overhead costs that more than offset the $17.9 million reduction in overhead driven by the Company’s restructuring initiatives.

|

Selling and Marketing Expenses

Selling and marketing expenses in fiscal 2011 were 13.5% of net sales, compared with 14.0% of net sales in fiscal 2010. The decreased cost as a percent of sales in fiscal 2011 resulted from increased sales levels, which resulted in favorable leverage.

Selling and marketing expenses were 14.0% of net sales in fiscal 2010 compared with 11.0% in fiscal 2009. The higher cost as a percent of sales in fiscal 2010 was driven by a 26% reduction in net sales that exceeded the reduction in spending as volume-based reductions in compensation costs were offset in part by increased promotional costs and increased business development activities compared with the prior year.

General & Administrative Expenses

General and administrative expenses for fiscal 2011 declined by $3.7 million, or 14%, compared with fiscal 2010 and represented 5.0% of net sales, compared with 6.5% of net sales for fiscal 2010. The majority of the decline was related to a reduction in the Company’s pay-for-performance variable compensation and reduced bad debt and related costs pertaining to insolvent customers. As of April 30, 2011, the Company had receivables from customers with a higher perceived level of risk aggregating less than $0.1 million.

General and administrative expenses in fiscal 2010 declined by $0.4 million, or 2%, compared with fiscal 2009 and represented 6.5% of net sales, as compared with 4.9% of net sales for fiscal 2009. Declines associated with the Company’s pay-for-performance variable compensation program and reduced bad debt expense were partially offset by the absence of a prior fiscal year gain of $0.6 million on the termination of a retiree health care plan. As of April 30, 2010, the Company had receivables from customers with a higher perceived level of risk aggregating $0.1 million.

12

Effective Income Tax Rates

The Company generated a pre-tax loss of $30.0 million during fiscal 2011. Based upon statutory tax rates in effect and the impact of permanent tax differences for meals and entertainment, a tax basis adjustment and other permanent differences, the Company’s effective tax rate was 33.2%.

The Company’s effective tax rate for fiscal 2010 was 39.7%, reflecting the impact of statutory tax rates in effect during the years to which the pre-tax loss was carried back, combined with permanent tax differences for general business credits and the domestic production deduction.

Outlook for Fiscal 2012

The Company follows several indices, including but not limited to housing starts, existing home sales, mortgage interest rates, new jobs growth, GDP growth and consumer confidence that it believes are near-term leading indicators of overall demand for kitchen and bath cabinetry. The Company believes that while these indicators collectively suggest the long-term economic outlook for housing is positive, the near-term outlook remains subdued.

The Company expects that the economic recovery will continue at roughly its current pace and that new job creation will average approximately 200,000 per month during its fiscal 2012. This in turn should translate into a gradual improvement in consumer confidence and enable the remodeling market to be roughly neutral to slightly positive compared with prior year levels, as the benefits from increased employment continue to be hampered by uncertain home prices and credit availability.

The Company believes momentum from improving employment will result in improvement in new household formation from its recent low levels. This in turn should help improve housing starts by approximately 10%, to a range of 600,000 to 625,000 during fiscal 2012.

The Company expects that it will maintain the market share gains it has made, enabling it to generate sales growth of approximately 5% to 8%.

The Company plans to increase its capital expenditures from $8.5 million in fiscal 2011 to approximately $15 million in fiscal 2012, driven by increasing the number of sales display units deployed with customers and deploying machinery and equipment to enable production volume to increase.

The Company expects that its operating cash flow may decline, driven by a decline in the amount of expected income tax refunds and increased working capital requirements as the Company’s sales grow.

The Company also expects it will experience inflationary pressures in lumber, plywood and various other materials that could negatively impact profitability during fiscal 2012.

Additional risks and uncertainties that could affect the Company’s results of operations and financial condition are discussed elsewhere in this report, including under “Forward-Looking Statements” and elsewhere in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, under Item 1A, “Risk Factors” and Item 7A, “Quantitative and Qualitative Disclosures about Market Risk”.

Liquidity and Capital Resources

The Company’s cash, cash equivalents and restricted cash totaled $69.8 million at April 30, 2011, which represented an increase of $2.2 million from April 30, 2010. Total debt was $25.6 million at April 30, 2011, $0.9 million lower than in the prior fiscal year and long-term debt, excluding current maturities, to capital was 13.8% at April 30, 2011, up from 12.7% at April 30, 2010.

The Company maintains a $35 million secured revolving credit facility with Wells Fargo Bank, N. A. (Wells Fargo). Pursuant to the terms of the Wells Fargo credit facility, at April 30, 2011, $14.4 million of the Company’s cash served as security for borrowings under this facility and was classified as restricted cash.

13

OPERATING ACTIVITIES

The Company’s main source of liquidity is its cash and cash equivalents on hand and cash generated from its operating activities. Primarily because of its non-cash operating expenses that are included in net income, the Company’s cash provided by operating activities has historically been considerably higher than the Company’s net income. During the three-year period ended April 30, 2011, the Company generated a total of $61.3 million in cash from operating activities, as compared with a cumulative net loss during this period of $45.6 million. Of the $105.5 million difference between these two amounts, $105.9 million related to non-cash depreciation and amortization and stock-based compensation expense.

Cash provided by operating activities in fiscal 2011 was $13.2 million, compared with $1.3 million in fiscal 2010. The $11.9 million increase in cash provided by operating activities was primarily attributable to the $2.3 million decrease in net loss, proceeds of $8.8 million collected from income tax refunds and the absence of payments made in relation to the Company’s cost reduction initiatives in the prior year of approximately $9 million. Partially offsetting these improvements were declines in the amount of non-cash depreciation, amortization and stock-based compensation expense of $4.6 million and an increase in the Company’s net working capital investment in inventory and customer receivable levels of $9.8 million.

Cash provided by operating activities in fiscal 2010 was $1.3 million, compared with $46.8 million in fiscal 2009. The significant reduction in cash provided by operating activities was primarily attributable to the $19.1 million increase in net loss, payments of previously accrued restructuring charges and severance costs of approximately $9 million, the building of an income tax benefit, of which nearly $9 million was collected during fiscal 2011 and declines in the amount of non-cash depreciation, amortization and stock-based compensation expense of $4.7 million. The Company’s net working capital contribution from changes in inventory and customer receivables was $4.6 million less favorable in fiscal 2010, offset by the Company’s utilization of pension credits that avoided the requirement to fund pension plan contributions of $5.0 million.

INVESTING ACTIVITIES

The Company’s investing activities consist of capital expenditures and investments in promotional displays. Net cash used by investing activities in fiscal 2011 was $5.5 million, compared with $11.5 million in fiscal 2010 and $13.8 million in fiscal 2009. Investments in property, plant and equipment for fiscal 2011 were $5.0 million, compared with $2.9 million in fiscal 2010 and $4.8 million in fiscal 2009. Investments in promotional displays were $3.5 million in fiscal 2011, compared with $8.7 million in fiscal 2010 and $9.0 million in fiscal 2009.

During fiscal 2011, the Company increased its investments in capital expenditures by $2.1 million and reduced its investment in promotional displays by $5.2 million. The Company also received proceeds of $2.9 million during fiscal 2011 from the sale of two previously closed manufacturing plants. Capital expenditures rose in fiscal 2011 as the Company began to deploy machinery and equipment to facilitate increased production levels, while reductions in customers’ new store growth and store re-merchandising activities caused the Company to reduce its investment in promotional displays.

FINANCING ACTIVITIES

The Company’s financing activities typically consist of returning a portion of its free cash flow (defined as cash provided by operating activities less cash used for investing activities) to its shareholders, repaying debt and satisfying its other credit obligations, net of any proceeds received from the exercise of stock options.

The Company generated free cash flow of $7.7 million in fiscal 2011, which represented an increase of $17.9 million compared with fiscal 2010. The Company used $5.5 million for financing activities,

14

considerably less than the $19.4 million used for financing activities in fiscal 2010. The primary financing activity use of cash in fiscal 2011 was $5.1 million to pay dividends to the Company’s common stockholders.

The Company generated negative free cash flow of $10.2 million in fiscal 2010 and used $19.4 million for financing activities, including $14.4 million to serve as security in the form of restricted cash for the Company’s credit facility with Wells Fargo and $5.1 million to pay dividends.

The Company generated $33.0 million of free cash flow in fiscal 2009 and chose to build its cash balance by $25.9 million to create additional financial flexibility, using $7.2 million for financing activities, including $5.1 million to pay dividends and $2.5 million to repurchase stock.

Under a stock repurchase authorization approved by its Board of Directors in 2007, the Company is authorized to repurchase its common stock from time to time, when management believes the Company’s liquidity and expected cash flows are ample and the market price for its common stock presents an attractive return on investment for its shareholders. At April 30, 2011, approximately $93.3 million remained authorized by the Company’s Board of Directors to repurchase shares of the Company’s common stock. The Company has purchased a total of 4.3 million shares of its common stock, for $126.7 million, since 2001. The Company made no stock repurchases in fiscal 2010 or 2011.

The Company can borrow up to $35 million under the Wells Fargo credit facility; however, the Company’s aggregate debt with Wells Fargo cannot exceed the collateral value of the Company’s cash and specified investments held in accounts pledged to Wells Fargo. At April 30, 2011, $10 million of loans and $3.7 million of letters of credit were outstanding under the Wells Fargo facility and $14.4 million of the Company’s cash was held as security. Under the terms of the Wells Fargo credit facility, the Company must maintain at the end of each fiscal quarter a ratio of total liabilities to tangible net worth not greater than 0.9 to 1.0 and must comply with other customary affirmative and negative covenants. The Company’s ratio of total liabilities to tangible net worth at April 30, 2011 was 0.7 to 1.0. The credit facility does not limit the Company’s ability to use unrestricted cash to pay dividends or repurchase its common stock as long as the Company maintains the required ratio of total liabilities to tangible net worth. As of April 30, 2011, the Company was in compliance with all covenants specified in the credit facility.

Cash flow from operations combined with accumulated cash and cash equivalents on hand are expected to be more than sufficient to support forecasted working capital requirements, service existing debt obligations and fund capital expenditures for fiscal 2012.

The timing of the Company’s contractual obligations as of April 30, 2011 is summarized in the table below:

|

FISCAL YEARS ENDED APRIL 30

|

||||||||||||||||||||

|

(in thousands)

|

Total Amounts

|

2012

|

2013 – 2014 | 2015 – 2016 |

2017 and Thereafter

|

|||||||||||||||

|

Revolving credit facility

|

$ | 10,000 | $ | -- | $ | 10,000 | $ | -- | $ | -- | ||||||||||

|

Economic development loans

|

3,524 | -- | -- | -- | 3,524 | |||||||||||||||

|

Term loans

|

4,359 | 416 | 761 | 763 | 2,419 | |||||||||||||||

|

Capital lease obligations

|

7,700 | 512 | 1,057 | 1,099 | 5,032 | |||||||||||||||

|

Interest on long-term debt1

|

2,494 | 500 | 731 | 556 | 707 | |||||||||||||||

|

Operating lease obligations

|

15,772 | 3,707 | 5,909 | 5,079 | 1,077 | |||||||||||||||

|

Pension contributions2

|

35,936 | 2,871 | 18,565 | 14,500 | -- | |||||||||||||||

|

Total

|

$ | 79,785 | $ | 8,006 | $ | 37,023 | $ | 21,997 | $ | 12,759 | ||||||||||

| 1 |

Interest commitments under interest bearing debt consist of interest under the Company’s primary loan agreement, term loans and capitalized lease agreements. Amounts outstanding under the Company’s revolving credit facility, $10 million at April 30, 2011, bears a variable interest rate determined by the London Interbank Offered Rate (LIBOR) plus 1.25%. Interest under the Company’s term loans and capitalized lease agreements is fixed at rates between 2% and 6%. Interest commitments under interest bearing debt for the Company’s revolving credit facility are at LIBOR plus the spread as of April 30, 2011, throughout the remaining term of the facility.

|

15

| 2 |

The estimated cost of the Company’s two defined benefit pension plans is determined annually based upon the discount rate and other assumptions at fiscal year end. Future pension funding contributions beyond 2016 have not been determined at this time.

|

Off-Balance Sheet Arrangements

As of April 30, 2011 and 2010, the Company had no off-balance sheet arrangements.

Critical Accounting Policies

Management has chosen accounting policies that are necessary to give reasonable assurance that the Company’s operational results and financial position are accurately and fairly reported. The significant accounting policies of the Company are disclosed in Note A to the Consolidated Financial Statements. The following discussion addresses the accounting policies that management believes have the greatest potential impact on the presentation of the financial condition and operating results of the Company for the periods being reported and that require the most judgment.

Management regularly reviews these critical accounting policies and estimates with the Audit Committee of the Board of Directors.

Long-lived Asset Impairment. The Company reviews its long-lived assets for impairment whenever events or changes in circumstances indicate that the related carrying amounts may not be recoverable. For purposes of assessing if impairment exists, assets are grouped at the lowest level for which there are identifiable cash flows that are largely independent of the cash flows of other groups of assets. To determine whether an impairment has occurred, the Company compares estimates of the future undiscounted net cash flows of groups of assets to their carrying values. The Company has not recognized impairments of long-lived assets in the last three years.

Revenue Recognition. The Company utilizes signed sales agreements that provide for transfer of title to the customer upon delivery. The Company must estimate the amount of sales that have been transferred to third-party carriers but not delivered to customers. The estimate is calculated using a lag factor determined by analyzing the actual difference between shipment date and delivery date of orders over the past 12 months. Revenue is only recognized on those shipments which the Company believes have been delivered to the customer.

The Company recognizes revenue based on the invoice price less allowances for sales returns, cash discounts and other deductions as required under U.S. generally accepted accounting principles. Collection is reasonably assured as determined through an analysis of accounts receivable data, including historical product returns and the evaluation of each customer’s ability to pay. Allowances for sales returns are based on the historical relationship between shipments and returns. The Company believes that its historical experience is an accurate reflection of future returns.

Self Insurance. The Company is self-insured for certain costs related to employee medical coverage and workers’ compensation liability. The Company maintains stop-loss coverage with third-party insurers to limit total exposure. The Company establishes a liability at the balance sheet date based on estimates for a variety of factors that influence the Company’s ultimate cost. In the event that actual experience is substantially different from the estimates, the financial results for the period could be adversely affected. The Company believes that the methodologies used to estimate all factors related to employee medical coverage and workers’ compensation are an accurate reflection of the liability as of the date of the balance sheet.

Pensions. The Company has two non-contributory defined benefit pension plans covering substantially all of the Company’s employees.

16

The estimated cost, benefits and pension obligation of these plans are determined using various assumptions. The most significant assumptions are the long-term expected rate of return on plan assets, the discount rate used to determine the present value of the pension obligations and the future rate of compensation level increases. In fiscal 2011, the Company determined the discount rate by referencing the Hewitt Above Median Yield Curve. Previously, the Company referred to the AON Yield Curve in establishing the discount rate. The Company believes that using a yield curve approach more accurately reflects changes in the present value of liabilities over time since each cash flow is discounted at the rate at which it could effectively be settled. The long-term expected rate of return on plan assets reflects the current mix of the plan assets invested in equities and bonds. The future rate of compensation levels reflects expected compensation trends.

The following is a summary of the potential impact of a hypothetical 1% change in actuarial assumptions for the discount rate, rate of compensation, expected return on plan assets and consumer price index:

|

(in millions)

|

IMPACT OF 1% INCREASE

|

IMPACT OF 1% DECREASE

|

||||||

|

(decrease) increase

|

||||||||

|

Effect on annual pension expense

|

$ | (3.4 | ) | $ | 2.9 | |||

|

Effect on projected pension benefit obligation

|

$ | (17.8 | ) | $ | 22.8 | |||

Pension expense for fiscal 2011 and the assumptions used in that calculation are presented in Note H of the Consolidated Financial Statements. At April 30, 2011, the discount rate was 5.66% compared to 5.91% at April 30, 2010. The expected return on plan assets is 8.0%, which is consistent with fiscal 2010. The assumed rate of increase in compensation levels is 4.0% for the fiscal year ended April 30, 2011, unchanged from the prior fiscal year.

The performance of the Company’s pension plans is largely dependent on the assumptions used to measure the obligations of the plans and to estimate future performance of the plans’ invested assets. Over the past two measurement periods, the most material deviations between results based on assumptions and the actual plan performance have been as a result of the changes to the discount rate used to measure the plans’ benefit obligations and the actual return on plan assets. Under accounting guidelines, the discount rate is to be set to market at each annual measurement date. From the fiscal 2009 to fiscal 2010 measurement dates, the discount rate decreased from 7.16% to 5.91%, which was the primary driver in an actuarial loss of $21.3 million. From the fiscal 2010 to fiscal 2011 measurement dates, the discount rate decreased from 5.91% to 5.66%, which was the primary driver in the actuarial loss of $4.5 million.

The Company strives to balance expected long-term returns and short-term volatility of pension plan assets. Favorable and unfavorable differences between the assumed and actual returns on plan assets are generally amortized over a period no longer than the average future working lifetime of the plans’ active participants. The actual rates of return on plan assets realized, net of investment manager fees were 11.9%, 21.5% and (16.8)% for fiscal years 2011, 2010 and 2009, respectively.

The fair value of plan assets at April 30, 2011 was $83.3 million compared to $78.4 million at April 30, 2010. The Company’s projected benefit obligation exceeded plan assets by $36.7 million in fiscal 2011 and $29.1 million in fiscal 2010. The Company’s $7.7 million increase in its net under-funded position during fiscal 2011 was driven by the Company’s $4.5 million actuarial losses due to the decrease in the discount rate used and a $4.7 million loss due to additional benefits accruing, offset in part by a higher actual return on plan assets than expected. The Company expects its pension expense to increase from $6.9 million in fiscal 2011 to $7.4 million in fiscal 2012, due primarily to a further decrease in the discount rate offset by a higher return on plan assets than expected. The Company expects to contribute $2.9 million to its pension plans in fiscal 2012, which represents both required and discretionary funding. Under the requirements of the Pension Protection Act of 2006, the Company was not required to make mandatory contributions to its pension plans in either fiscal 2011 or in fiscal 2010.

17

Promotional Displays. The Company invests in promotional displays in retail stores to demonstrate product features, product specifications, quality specifications and serve as a training tool for designers. The investment is carried at cost less applicable amortization. Amortization is provided by the straight-line method on an individual display basis over the estimated period of economic benefit, approximately 30 to 36 months. The Company believes that the estimated period of economic benefit provides an accurate reflection of the value of displays as of the date of the balance sheet based on historical experience.

Product Warranty. The Company estimates outstanding warranty costs based on the historical relationship between warranty claims and revenues. The warranty accrual is reviewed monthly to verify that it properly reflects the Company’s remaining obligation based on anticipated expenditures over the balance of the obligation period. Adjustments are made when actual warranty claim experience differs from estimates. Warranty claims are generally made within three months of the original shipment date.

Stock-Based Compensation Expense. The calculation of stock-based compensation expense involves estimates that require management’s judgment. These estimates include the fair value of each stock option and restricted stock unit award granted. Stock option awards are estimated on the date of grant using a Black-Scholes option pricing model. There are two significant inputs into the Black-Scholes option pricing model: expected volatility and expected term. The Company estimates expected volatility based on the historical volatility of the Company’s stock over a term equal to the expected term of the option granted. The expected term of stock option awards granted is derived from historical exercise experience under the Company’s stock option plans and represents the period of time that stock option awards granted are expected to be outstanding.

For performance-based restricted stock units, the Company estimates the number of shares that will be granted upon satisfaction of the performance conditions, based upon actual and expected future operating results. The assumptions used in calculating the fair value of stock-based payment awards represent management’s best estimates, but these estimates involve inherent uncertainties and the application of significant management judgment. As a result, if factors change or the Company uses different assumptions, stock-based compensation expense could be materially different in the future. In addition, the Company is required to estimate the expected forfeiture rate and only recognize expense for those shares expected to vest. If the Company’s actual forfeiture rate is materially different from its estimate, the stock-based compensation expense could be significantly different from what the Company has recorded in the current period. See Note G to the Consolidated Financial Statements for further discussion on stock-based compensation.

Valuation of Deferred Tax Assets. The Company considers the need for a valuation allowance against its deferred tax assets. The Company performed an analysis at April 30, 2011 and 2010 and determined in each case that a valuation allowance was not required. The Company considered all available evidence, both positive and negative, in determining the need for a valuation allowance. Based upon this analysis, including a consideration of recent losses, management determined that it is more likely than not that the Company’s deferred tax assets will be realized through expected future income and the reversal of taxable temporary differences. The Company will continue to update this analysis on a periodic basis and changes in expectations about future income or the timing of the reversal of taxable temporary differences could cause the Company to record a valuation allowance in a future period.

Recent Accounting Pronouncements

In January 2010, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2010-06, “Fair Value Measurements and Disclosures (Topic 820): Improving Disclosures about Fair Value Measurements”. ASU 2010-06 amends Subtopic 820-10 to clarify existing disclosures, require new disclosures and includes conforming amendments to guidance on employers’ disclosures about postretirement benefit plans. ASU 2010-06 was adopted by the Company on May 1, 2010. The adoption of the new guidance did not have a material impact on the Company’s financial statements.

18

Dividends Declared

On May 25, 2011, the Board of Directors approved a $.09 per share cash dividend on its common stock. The cash dividend was paid on June 27, 2011, to shareholders of record on June 13, 2011.

|

Item 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

The costs of the Company’s products are subject to inflationary pressures and commodity price fluctuations. The Company has generally been able, over time, to recover the effects of inflation and commodity price fluctuations through sales price increases.

On April 30, 2011, the Company had no material exposure to changes in interest rates for its debt agreements.

The Company does not currently use commodity or interest rate derivatives or similar financial instruments to manage its commodity price or interest rate risks.

19

|

Item 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

CONSOLIDATED BALANCE SHEETS

|

APRIL 30

|

||||||||

|

(in thousands, except share and per share data)

|

2011

|

2010

|

||||||

|

ASSETS

|

||||||||

|

Current Assets

|

||||||||

|

Cash and cash equivalents

|

$ | 55,420 | $ | 53,233 | ||||

|

Customer receivables, net

|

31,067 | 27,524 | ||||||

|

Inventories

|

24,471 | 25,239 | ||||||

|

Income taxes receivable and other

|

3,799 | 10,693 | ||||||

|

Deferred income taxes

|

5,659 | 6,355 | ||||||

|

Total Current Assets

|

120,416 | 123,044 | ||||||

|

Property, plant and equipment, net

|

100,628 | 114,107 | ||||||

|

Restricted cash

|

14,419 | 14,419 | ||||||

|

Promotional displays, net

|

7,330 | 11,738 | ||||||

|

Deferred income taxes

|

21,178 | 13,440 | ||||||

|

Other assets

|

4,399 | 5,685 | ||||||

|

TOTAL ASSETS

|

$ | 268,370 | $ | 282,433 | ||||

|

LIABILITIES AND SHAREHOLDERS’ EQUITY

|

||||||||

|

Current Liabilities

|

||||||||

|

Accounts payable

|

$ | 18,569 | $ | 14,035 | ||||

|

Current maturities of long-term debt

|

928 | 893 | ||||||

|

Accrued compensation and related expenses

|

15,607 | 20,409 | ||||||

|

Accrued marketing expenses

|

7,408 | 4,903 | ||||||

|

Other accrued expenses

|

8,332 | 9,339 | ||||||

|

Total Current Liabilities

|

50,844 | 49,579 | ||||||

|

Long-term debt, less current maturities

|

24,655 | 25,582 | ||||||

|

Defined benefit pension liabilities

|

36,726 | 29,065 | ||||||

|

Other long-term liabilities

|

2,180 | 2,889 | ||||||

|

Shareholders’ Equity

|

||||||||

|

Preferred stock, $1.00 par value; 2,000,000 shares authorized, none issued

|

---- | ---- | ||||||

|

Common stock, no par value; 40,000,000 shares authorized; issued and outstanding shares: at April 30, 2011: 14,295,540

at April 30, 2010: 14,205,462

|

92,408 | 88,153 | ||||||

|

Retained earnings

|

83,495 | 108,643 | ||||||

|

Accumulated other comprehensive loss -

|

||||||||

|

Defined benefit pension plans

|

(21,938 | ) | (21,478 | ) | ||||

|

Total Shareholders’ Equity

|

153,965 | 175,318 | ||||||

|

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY

|

$ | 268,370 | $ | 282,433 | ||||

|

See notes to consolidated financial statements.

|

||||||||

20

CONSOLIDATED STATEMENTS OF OPERATIONS

|

YEARS ENDED APRIL 30

|

||||||||||||

|

(in thousands, except per share data)

|

2011

|

2010

|

2009

|

|||||||||

|

Net sales

|

$ | 452,589 | $ | 406,540 | $ | 545,934 | ||||||

|

Cost of sales and distribution

|

399,838 | 357,619 | 456,444 | |||||||||

|

Gross Profit

|

52,751 | 48,921 | 89,490 | |||||||||

|

Selling and marketing expenses

|

61,034 | 56,935 | 60,033 | |||||||||

|

General and administrative expenses

|

22,709 | 26,434 | 26,875 | |||||||||

|

Restructuring charges

|

62 | 2,808 | 9,743 | |||||||||

|

Operating Loss

|

(31,054 | ) | (37,256 | ) | (7,161 | ) | ||||||

|

Interest expense

|

572 | 637 | 716 | |||||||||

|

Other income

|

(1,666 | ) | (838 | ) | (1,726 | ) | ||||||

|

Loss Before Income Taxes

|

(29,960 | ) | (37,055 | ) | (6,151 | ) | ||||||

|

Income tax benefit

|

(9,942 | ) | (14,714 | ) | (2,917 | ) | ||||||

|

Net Loss

|

$ | (20,018 | ) | $ | (22,341 | ) | $ | (3,234 | ) | |||

|

SHARE INFORMATION

|

||||||||||||

|

Net loss per share

|

||||||||||||

|

Basic

|

$ | (1.40 | ) | $ | (1.58 | ) | $ | (0.23 | ) | |||

|

Diluted

|

(1.40 | ) | (1.58 | ) | (0.23 | ) | ||||||

|

Cash dividends per share

|

0.36 | 0.36 | 0.36 | |||||||||

|

See notes to consolidated financial statements.

|

||||||||||||

21

CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY AND COMPREHENSIVE LOSS

|

ACCUMULATED

|

||||||||||||||||||||

|

(in thousands, except share data)

|

OTHER

|

TOTAL

|

||||||||||||||||||

|

COMMON STOCK

|

RETAINED

|

COMPREHENSIVE

|

SHAREHOLDERS'

|

|||||||||||||||||

|

SHARES

|

AMOUNT

|

EARNINGS

|

LOSS

|

EQUITY

|

||||||||||||||||

|

Balance, May 1, 2008

|

14,150,290 | $ | 76,409 | $ | 146,288 | $ | (8,063 | ) | $ | 214,634 | ||||||||||

|

Comprehensive Loss:

|

||||||||||||||||||||

|

Net loss

|

(3,234 | ) | (3,234 | ) | ||||||||||||||||

|

Other comprehensive loss, net of tax:

|

||||||||||||||||||||

|

Change in pension and postretirement benefits

|

(6,622 | ) | (6,622 | ) | ||||||||||||||||

|

Total Comprehensive Loss

|

(9,856 | ) | ||||||||||||||||||

|

Stock-based compensation

|

4,877 | 4,877 | ||||||||||||||||||

|

Cash dividends

|

(5,060 | ) | (5,060 | ) | ||||||||||||||||

|

Exercise of stock-based compensation awards

|

8,400 | 152 | 152 | |||||||||||||||||

|

Stock repurchases

|

(140,214 | ) | (549 | ) | (1,908 | ) | (2,457 | ) | ||||||||||||

|

Employee benefit plan contributions

|

75,973 | 1,404 | (12 | ) | 1,392 | |||||||||||||||

|

Balance, April 30, 2009

|

14,094,449 | $ | 82,293 | $ | 136,074 | $ | (14,685 | ) | $ | 203,682 | ||||||||||

|

Comprehensive Loss:

|

||||||||||||||||||||

|

Net loss

|

(22,341 | ) | (22,341 | ) | ||||||||||||||||

|

Other comprehensive loss, net of tax:

|

||||||||||||||||||||

|

Change in pension benefits

|

(6,793 | ) | (6,793 | ) | ||||||||||||||||

|

Total Comprehensive Loss

|

(29,134 | ) | ||||||||||||||||||

|

Stock-based compensation

|

4,392 | 4,392 | ||||||||||||||||||

|

Adjustments to excess tax benefit

from stock-based compensation

|

(439 | ) | (439 | ) | ||||||||||||||||

|

Cash dividends

|

(5,090 | ) | (5,090 | ) | ||||||||||||||||

|

Exercise of stock-based compensation awards

|

54,070 | 719 | 719 | |||||||||||||||||

|

Employee benefit plan contributions

|

56,943 | 1,188 | 1,188 | |||||||||||||||||

|

Balance, April 30, 2010

|

14,205,462 | $ | 88,153 | $ | 108,643 | $ | (21,478 | ) | $ | 175,318 | ||||||||||

|

Comprehensive Loss:

|

||||||||||||||||||||

|

Net loss

|

(20,018 | ) | (20,018 | ) | ||||||||||||||||

|

Other comprehensive loss, net of tax:

|

||||||||||||||||||||

|

Change in pension benefits

|

(460 | ) | (460 | ) | ||||||||||||||||

|

Total Comprehensive Loss

|

(20,478 | ) | ||||||||||||||||||

|

Stock-based compensation

|

3,995 | 3,995 | ||||||||||||||||||

|

Adjustments to excess tax benefit

from stock-based compensation

|

(1,347 | ) | (1,347 | ) | ||||||||||||||||

|

Cash dividends

|

(5,130 | ) | (5,130 | ) | ||||||||||||||||

|

Exercise of stock-based compensation awards

|

27,401 | 394 | 394 | |||||||||||||||||

|

Employee benefit plan contributions

|

62,677 | 1,213 | 1,213 | |||||||||||||||||

|

Balance, April 30, 2011

|

14,295,540 | $ | 92,408 | $ | 83,495 | $ | (21,938 | ) | $ | 153,965 | ||||||||||

|

See notes to consolidated financial statements.

|

||||||||||||||||||||

22

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

YEARS ENDED APRIL 30

|

||||||||||||

|

(in thousands)

|

2011

|

2010

|

2009

|

|||||||||

|

OPERATING ACTIVITIES

|

||||||||||||

|

Net loss

|

$ | (20,018 | ) | $ | (22,341 | ) | $ | (3,234 | ) | |||

|

Adjustments to reconcile net loss to net cash provided by operating activities:

|

||||||||||||

|

Depreciation and amortization

|

26,703 | 30,876 | 35,100 | |||||||||

|

Net loss on disposal of property, plant and equipment

|

209 | 209 | 271 | |||||||||

|

Gain on sale of assets held for sale

|

(982 | ) | ---- | ---- | ||||||||

|

Stock-based compensation expense

|

3,995 | 4,392 | 4,877 | |||||||||

|

Deferred income taxes

|

(8,185 | ) | (5,800 | ) | (5,715 | ) | ||||||

|