Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NuStar GP Holdings, LLC | d8k.htm |

Curt Anastasio, CEO and

President May 26, 2011

2011 Master Limited Partnership

Investor Conference

Exhibit 99.1 |

Statements contained in this presentation that state management’s

expectations or predictions of the future are forward-looking statements as

defined

by

federal

securities

law.

The

words

“believe,”

“expect,”

“should,”

“targeting,”

“estimates,”

and other similar expressions identify forward-

looking

statements.

It

is

important

to

note

that

actual

results

could

differ

materially from those projected in such forward-looking statements. We

undertake no duty to update any forward-looking statement to conform the

statement to actual results or changes in the company’s expectations.

For more information concerning factors that could cause actual results to

differ from those expressed or forecasted, see NuStar Energy L.P.’s and

NuStar GP Holdings, LLC’s respective annual reports on Form 10-K and

quarterly reports on Form 10-Q, filed with the Securities and Exchange

Commission and

available

on

NuStar’s

websites

at

www.nustarenergy.com

and

www.nustargpholdings.com.

Forward Looking Statements

2 |

NuStar Overview

3 |

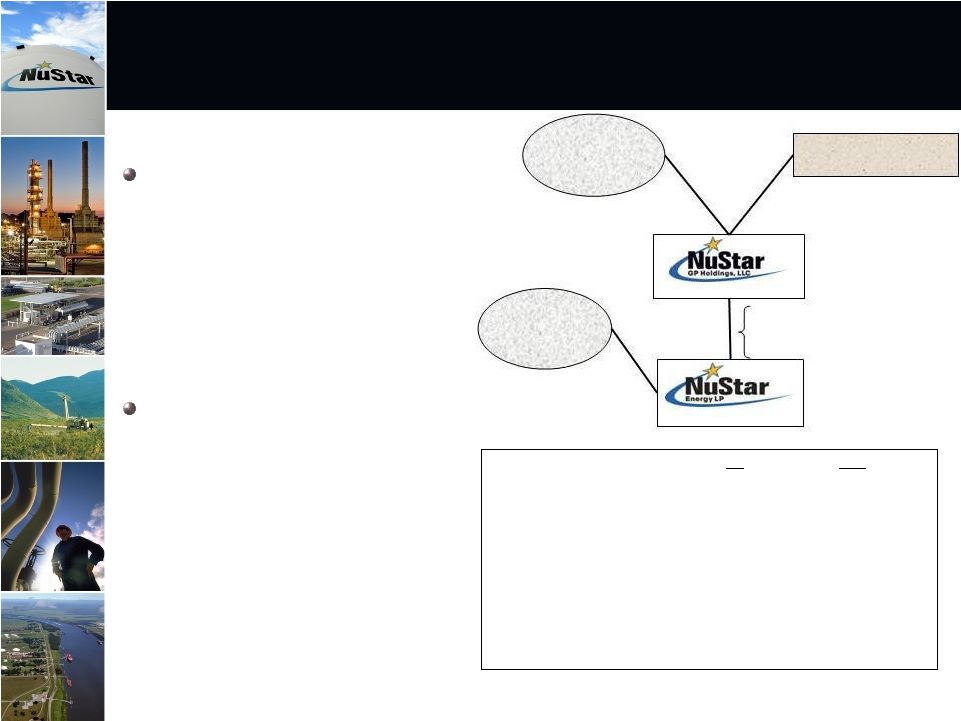

NuStar Energy L.P. (NYSE: NS) is

a leading publicly traded

partnership with a market

capitalization of around $4.0 billion

and an enterprise value of

approximately $6.3 billion

NuStar GP Holdings, LLC (NYSE:

NSH) holds the 2% general

partner interest, incentive

distribution rights and 15.6% of the

common units in NuStar Energy

L.P. with a market capitalization of

around $1.5 billion

Two Publicly Traded Companies

NS

NSH

IPO Date:

4/16/2001

7/19/2006

Unit Price (05/20/11):

$62.09

$36.22

Annual Distribution/Unit:

$4.30

$1.92

Yield (05/20/11):

6.93%

5.30%

Market Capitalization:

$4,012 million

$1,542 million

Enterprise Value

$6,304 million

$1,551 million

Credit Ratings –

Moody’s

Baa3/Stable

n/a

S&P and Fitch

BBB-/Stable

n/a

82.9%

Membership Interest

82.4%

L.P. Interest

Public Unitholders

35.3 Million NSH Units

Public Unitholders

54.4 Million NS Units

17.1%

Membership

Interest

2.0% G.P. Interest

15.6% L.P. Interest

Incentive Distribution Rights

William E. Greehey

7.3 Million NSH Units

NYSE: NSH

NYSE: NS

4 |

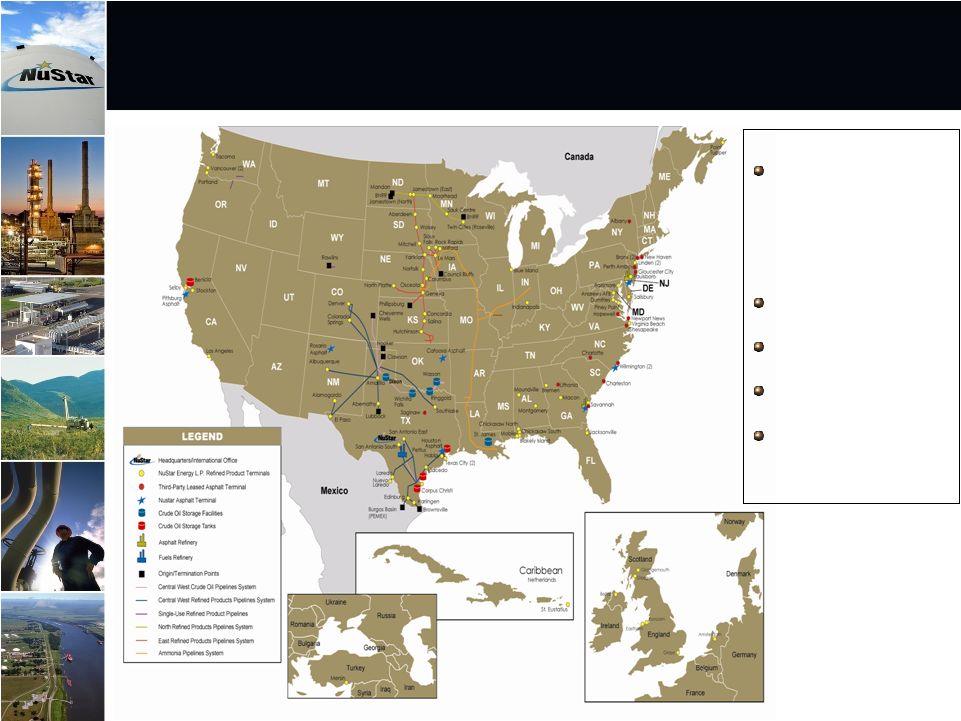

Large

and Diverse Geographic Footprint

with Assets in Key Locations

Asset Stats:

Operations in eight different

countries including the U.S.,

Mexico, the Netherlands,

including St. Eustatius in

the Caribbean, England,

Ireland, Scotland, Canada

and Turkey.

Own 90 terminal and

storage facilities

Over 94 million barrels of

storage capacity

8,417 miles of crude oil and

refined product pipelines

2 asphalt refineries and a

fuels refinery capable of

processing 118,500 bpd of

crude oil

5 |

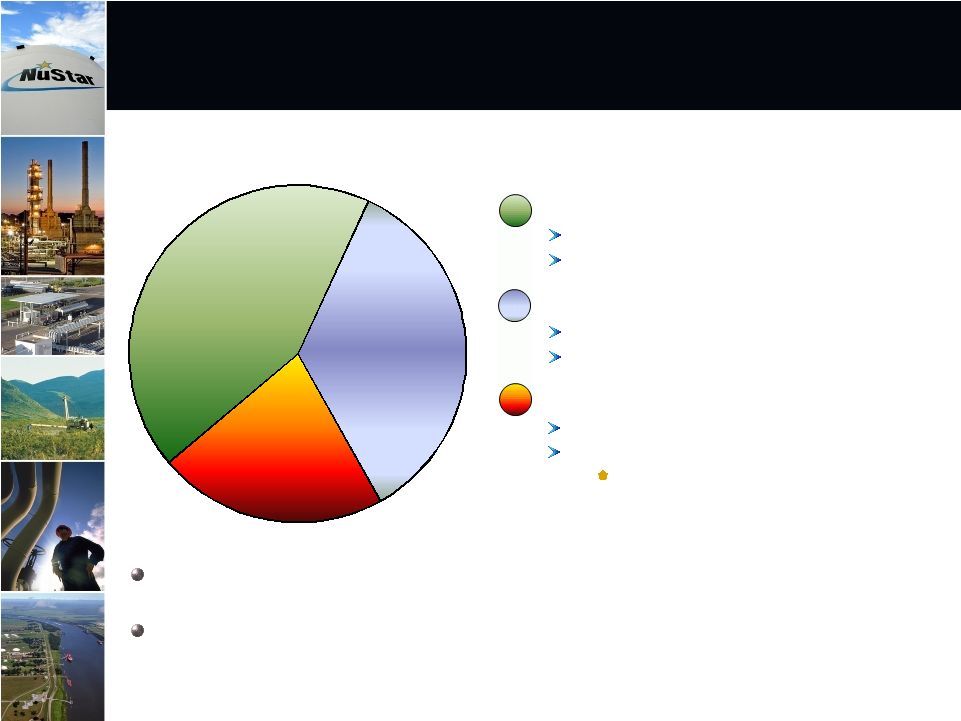

43%

35%

22%

Percentage of 2010

Segment Operating Income

Approximately 78% of NuStar Energy’s 2010 segment operating income came

from fee-based transportation and storage segments

Approximately 75% of 2011 segment operating income should come from fee-

based transportation and storage segments

Storage: 43%

Transportation: 35%

Refined Product Terminals

Crude Oil Storage

Refined Product Pipelines*

Crude Oil Pipelines

Asphalt & Fuels Marketing: 22%

Asphalt

Fuels Marketing

Product Supply, Bunkering and Fuel Oil

Marketing

Diversified Operations from Three

Business Segments

* Includes primarily distillates, gasoline, propane, jet fuel, ammonia and

other light products. Does not include natural gas. 6

|

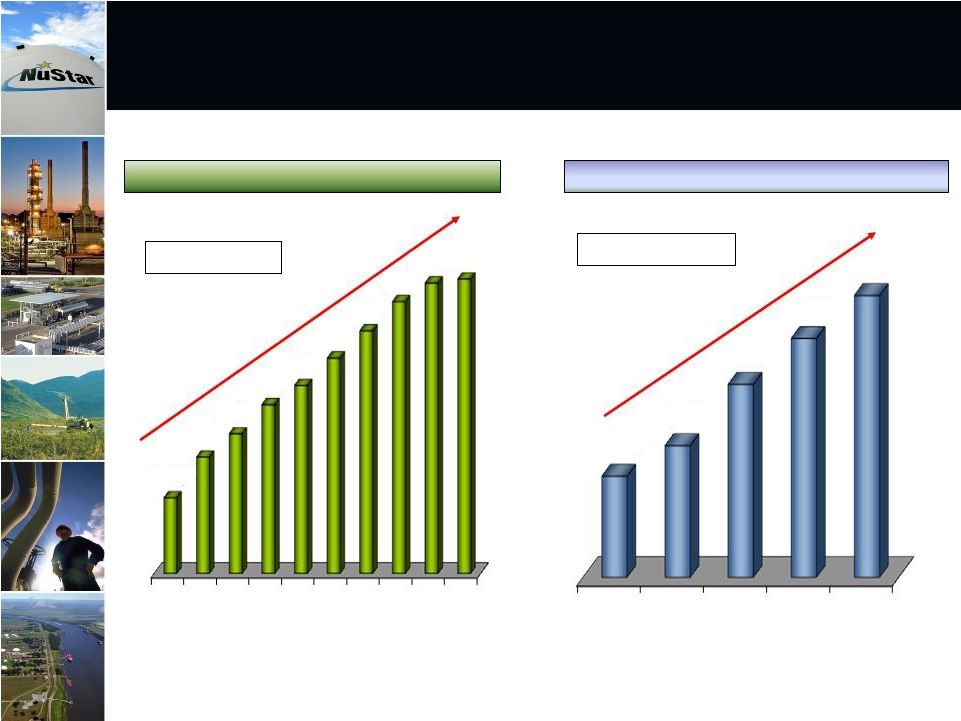

Distributions for both NS and NSH have grown every year since IPO’s…

Expect 2011 distribution growth rate to be higher than 2010

7

NS Distribution ($ per Unit)

NSH Distribution ($ per Unit)

~6.6% CAGR

~9.9% CAGR

* Annualized Distribution

*

*

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

$2.75

$2.95

$3.20

$3.37

$3.60

$3.84

$4.09

$4.245

$4.28

2006

2007

2008

2009

2010

$1.38

$1.58

$1.73

$1.87

$2.40

$1.28 |

Storage Segment Overview

8 |

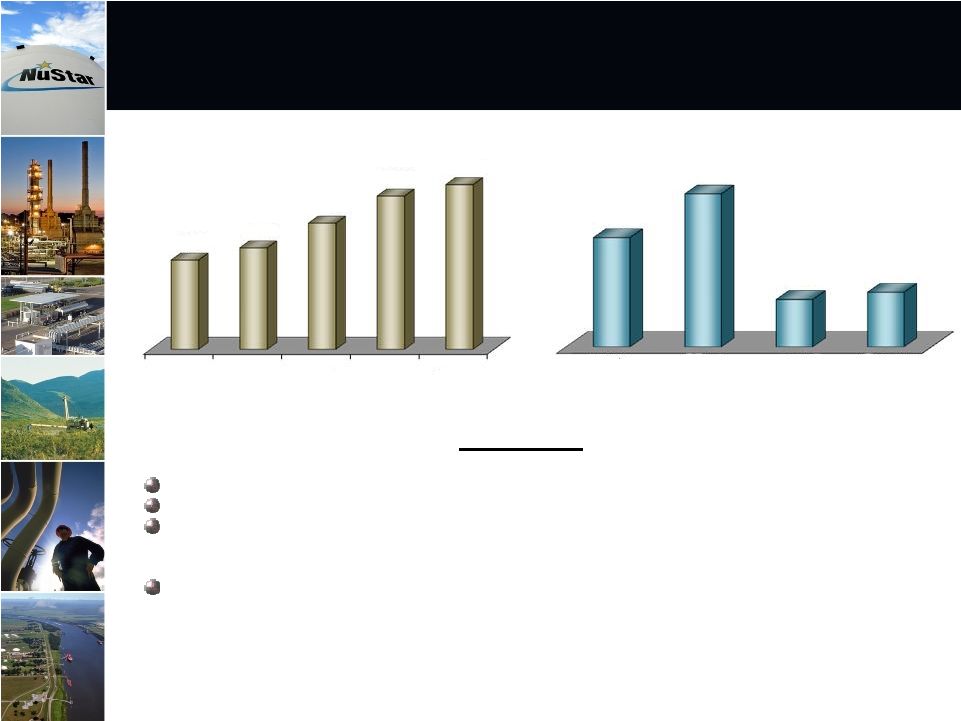

9

Storage Segment EBITDA ($ in Millions)

Storage Contract Renewals (% of Revenues)

1 Year

or Less

1 to 3

Years

3 to 5

Years

Greater

Than 5

Years

2011 Storage Segment

EBITDA Expected to be Higher than 2010

2006

2007

2008

2009

2010

$162

$177

$208

$242

$256

30%

42%

13%

15%

2011 Outlook

Full year 2011 segment EBITDA expected to be $25 to $35 million higher than 2010 2

Full year of EBITDA from May 2010 Mobile, AL terminal acquisition and St. Eustatius

terminal

acquisition that closed in February 2011 quarter

2011

segment

EBITDA

should

be

slightly

higher

than

2

nd

quarter

2010

project

completed

in

4

th

quarter

2010;

partial

year

of

EBITDA

from

Turkey

terminal

Benefits

from

St.

James

Phase

1

storage

project

should

begin

in

3

rd

quarter

2011

nd |

Plan

to expand our St. James, Louisiana terminal in two phases

Phase 1 –

Third-Party Crude Oil Storage

Construct 3.2 million barrels of crude oil storage

Projected CAPEX of $125 to $145 million, with projected average annual

EBITDA of $15 to $25 million

Expected in-service 3

rd

quarter 2011

Phase 2 –

Third-Party Crude Oil Storage

Project in early planning stages

Should be similar in size to Phase 1 project

Could grow in size based on customer demand

Expected in-service last half of 2012

10 |

Plan

to construct new tanks for distillate service at our St. Eustatius

terminal Construct one million barrels of new storage for distillate

service Interested customers include several large oil companies

Projected CAPEX of $45 to $55 million, with projected average

annual EBITDA of $5 to $10 million

Expected in-service 3 quarter 2012

11

rd |

Transportation Segment

Overview

12 |

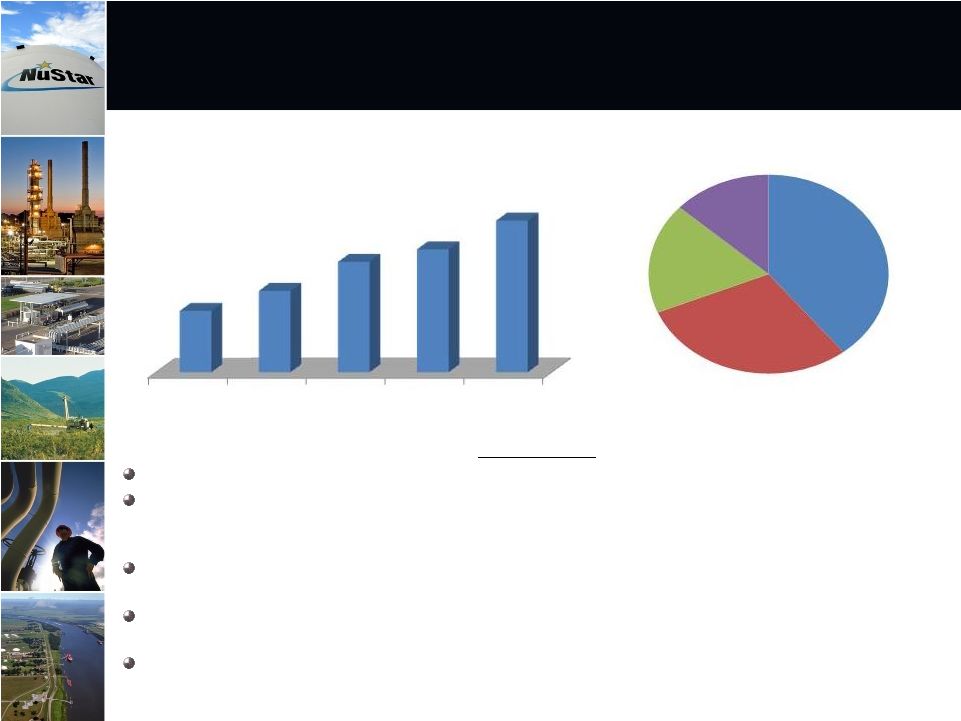

13

Transportation Segment EBITDA ($ in Millions)

2010 Pipeline Receipts by Commodity

Lower throughputs should cause

Transportation Segment EBITDA to be down in 2011

Gasoline

29%

Other*

13%

*Other includes ammonia, jet fuel, propane, naphtha

and light end refined products

Crude Oil

40%

Distillate

18%

2011 Outlook

Full year 2011 segment EBITDA expected to be $10 to $20 million lower than

2010 $1-$5 million of additional EBITDA from internal growth

projects. Eagle Ford shale crude project with Koch Pipeline Company

should increase throughputs 30,000 BPD and should be completed in

mid-2011. Throughputs projected to be down ~8%. Heavy customer

refinery turnaround schedule and changing market conditions could negatively

impact throughputs Tariff increase of 6.9%, effective July 1, 2011, includes a

2.65% FERC approved index adjustment factor that will be applicable on an

annual basis through June 30, 2016 2

quarter

2011

segment

EBITDA

should

be

$5

to

$10

million

lower

than

2

quarter

2010

nd

nd

2006

2007

2008

2009

2010

$170

$176

$186

$190

$199 |

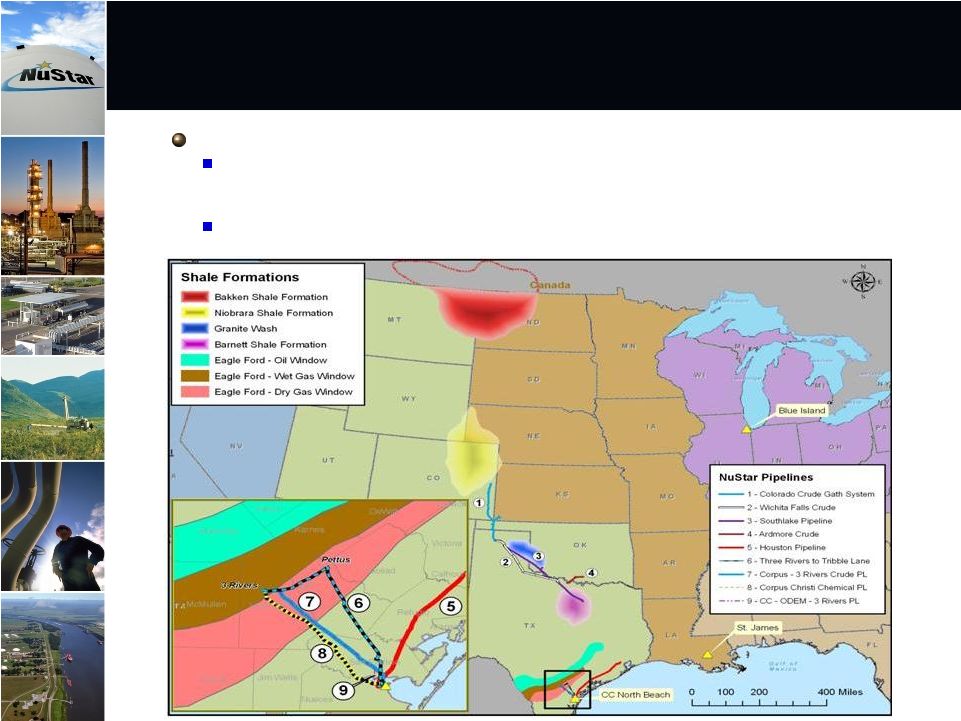

Transportation Segment Assets in close

proximity to key Shale Formations

Shale Development Strategy should increase

Transportation Segment Throughputs

Shale Development Strategy

There are key shale developments located in NuStar’s Mid-Continent and Gulf

Coast regions, including the Eagle Ford, Bakken, Granite Wash, Barnett, and

Niobrara

Our

strategy is to optimize and grow the existing asset base, and maximize the

value of the assets located in or near shale developments

14 |

15

Two Eagle Ford Shale Projects have been

announced to date….expect to announce

additional projects in the near future

Previously discussed Pipeline Connection & Capacity Lease Agreement

with Koch Pipeline

In April 2011, announced the signing of a LOI with TexStar Midstream

Services to develop a new pipeline system

TexStar plans to construct a 65-mile, 12-inch pipeline to transport crude

and condensate from Frio County, TX to Three Rivers, TX

Pipeline

should

be

interconnected

with

a

new

storage

facility

to

be

constructed at Three Rivers, TX by NuStar

Plan to connect storage facility to NuStar’s existing 16-inch pipeline that

can transport 200,000 BPD to NuStar’s Corpus Christi North Beach

storage terminal

Expected in-service date of system 2Q 2012

Currently in discussions with several parties regarding the potential of

converting some of our underutilized assets into Eagle Ford, Granite Wash

and Barnett shale service |

Asphalt & Fuels Marketing

Segment Overview

16 |

Earnings from recent refinery acquisition as well as

improved earnings in Asphalt and Fuels Marketing

operations should lead to improved segment results

Asphalt & Fuels Marketing

U.S. East Coast Product Margin ($ per barrel)

17

2009

Actual

2008

Actual

2000-2007

Average

2011 Outlook

April

2011

San

Antonio

refinery

acquisition

already

contributing

to

2011

earnings

Comparable to slightly lower asphalt demand more than offset by tight supply

Full year benefit from new U.S. heavy fuels and bunker fuels markets entered in

2010 2

nd

quarter

2011

segment

EBITDA

should

be

$40

to

$45

million

higher

than

2

nd

quarter

2010

Full year 2011 segment EBITDA expected to be $45 to $55 million higher than

2010 EBITDA (MM$)

2010

Actual

2006

2007

2008

2009

2010

$80

$111

$127

$27

$22

$37

$10

$37

$90

$70

$74

Asphalt

Fuels Marketing

$3.78

$8.75

$6.37

$7.73 |

18

San Antonio Refinery acquisition immediately

accretive to Distributable Cash Flow

Approximately 70% of current refinery production of 12,000 BPD is

hedged over the next three to four years

Expect refinery to generate $30 to $40 million of EBITDA and $20

to $30

million

of

distributable

cash

flow

per

year

over

the

life

of

the

hedges

$18 to $22 million of EBITDA and $12 to $16 million of

distributable cash flow projected for 2011

14,500 BPD refinery acquired for $41

million

Processes crude and condensate from

Eagle Ford shale formation

Produces and sells jet fuel, ULSD,

naphtha, reformate and LPG’s |

Financial Overview

19 |

20

3/31/11 Revolver Availability

NuStar Revolver Availability close to $300 million….

Credit Metrics improving as earnings increase

Total Bank Credit

$1,222

Less:

Borrowings

(421)

Letters of Credit

Go Zone Financing

(294)

Other

(5)

Revolver Availability

$502

Standard

&

Poor’s:

BBB

-

(Stable

Outlook)

Moody’s: Baa3 (Stable Outlook)

Fitch: BBB-

(Stable Outlook)

Debt/EBITDA (3/31/11): 4.4x

Debt/Capitalization (3/31/11): 47%

Credit Ratings/Metrics

(Dollars in Millions)

5.0x Revolver Debt/EBITDA covenant limits true Revolver availability to

~$300 million at 3/31/11 |

21

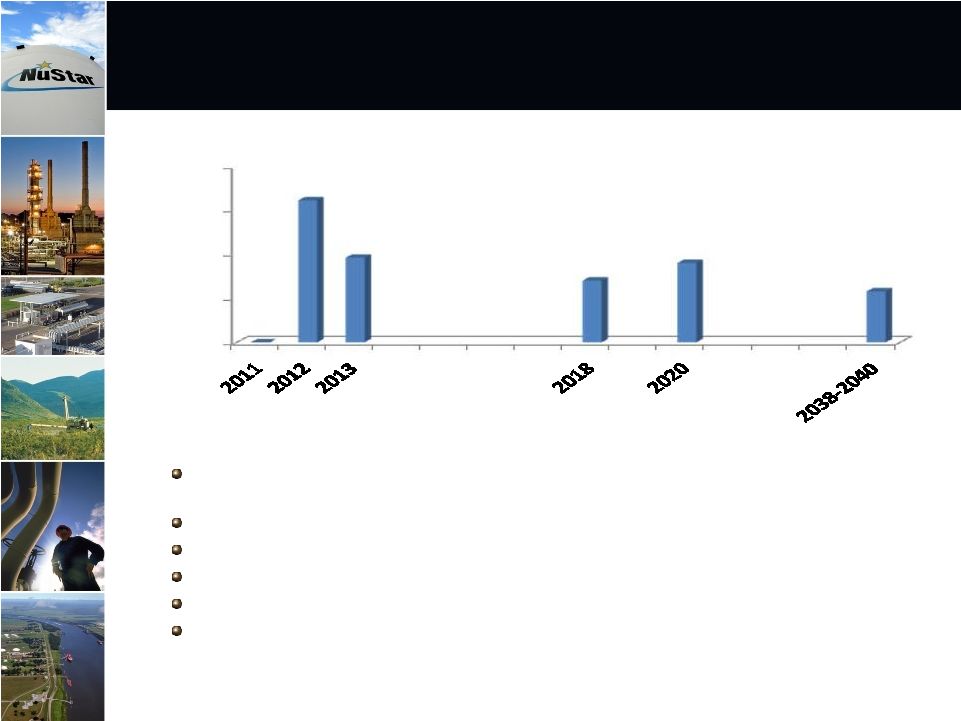

No Significant Debt Maturities Until 2012

No significant debt maturities until 2012 at which time the revolver and some

senior notes become due

New Credit Revolver terms & pricing seem to be improving as economy

improves Current plan is to hold off closing on a new Revolver until

2012 $290

million

worth

of

GO

Zone

financing

matures

in

2038

–

2040

Debt

structure

approximately

40%

fixed

rate

–

60%

variable

rate

Entered into $200 million Equity Distribution Agreement on May 23, 2011

Debt Maturities as of March 31, 2011

(Millions $)

0

250

500

750

1000

1

806

480

350

450

290 |

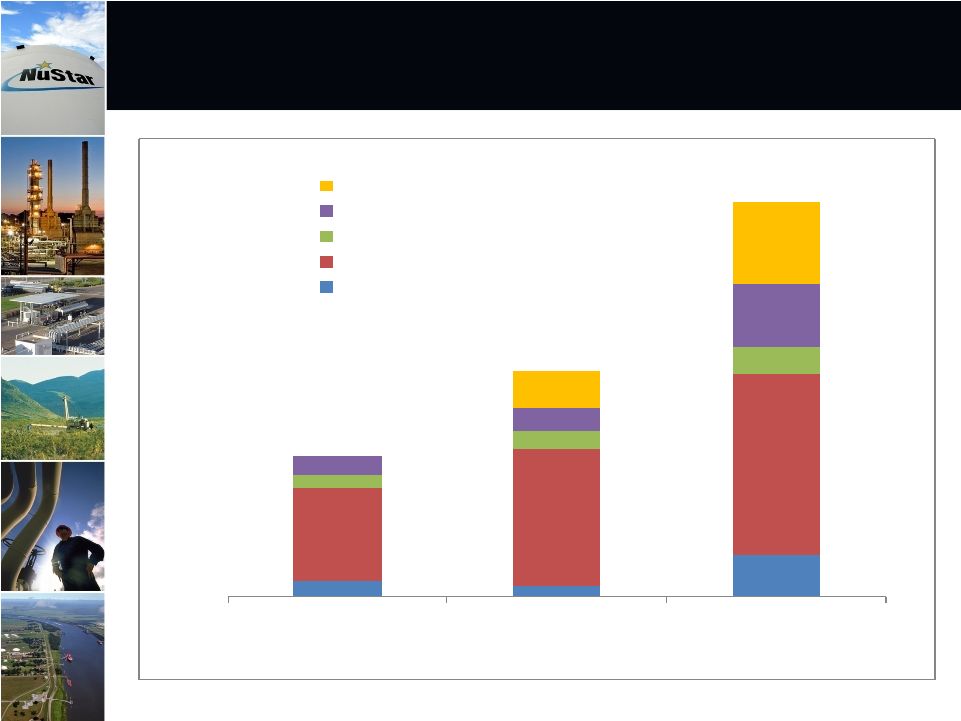

$20

$13

$49

$107

$159

$210

$14

$20

$31

$23

$27

$73

$43

$94

2009 Actual

2010 Actual

2011 Forecast

Acquisitions

Corporate

Asphalt & Fuels Marketing

Storage

Transportation

2011 Total Spending on Internal Growth Projects &

Acquisitions currently projected to be around

$450 million

22

(

Dollars in Millions)

$164

$262

$457 |

High quality, large and diverse asset footprint supporting energy infrastructure

both in the U.S. and internationally

Contracted fee-based storage and transportation assets provide stable cash

flows, delivering 78% of 2010 operating income

Fourth largest independent liquids terminal operator in the world

Diverse and high quality customer base composed of large integrated oil companies,

national oil companies and refiners

Strong balance sheet, credit metrics and commitment to maintain investment grade

credit ratings

Lower cost of capital than majority of peers

Experienced and proven management team with substantial equity ownership and

industry experience

Recognized nationally for safety and environmental record as well as one of the

best places to work

Why Invest in NuStar?

23 |

|

25

Appendix |

Reconciliation of Non-GAAP Financial

Information: Transportation Segment

26

(Unaudited, Dollars in Thousands)

The following is a reconciliation of operating income to EBITDA for the

Transportation Segment: 2006

2007

2008

2009

2010

Operating income

122,714

$

126,508

$

135,086

$

139,869

$

148,571

$

Plus depreciation and amortization expense

47,145

49,946

50,749

50,528

50,617

EBITDA

169,859

$

176,454

$

185,835

$

190,397

$

199,188

$

Projected incremental operating income range

$ 1,000 -

4,000

Plus projected incremental depreciation and

amortization expense range

0 -

1,000

Projected incremental EBITDA range

$ 1,000 -

5,000

The following is a reconciliation of projected decrease in operating income to

projected decrease in EBITDA: Projected decrease in operating income

($ 5,000 -

10,500)

($ 10,000 -

20,500)

Plus projected incremental depreciation and

amortization expense range

0 -

500

0 -

500

Projected decrease in EBITDA range

($ 5,000 -

10,000)

($ 10,000 -

20,000)

Three Months

Ended

June 30, 2011

Year Ended

December 31,

2011

Year Ended December 31,

NuStar

Energy

L.P.

utilizes

two

financial

measures,

EBITDA

and

distributable

cash

flow,

which

are

not

defined

in

United

States

generally

accepted

accounting

principles

(GAAP).

Management

uses

these

financial

measures

because

they

are

widely

accepted

financial

indicators

used

by

investors

to

compare

partnership

performance.

In

addition,

management

believes

that

these

measures

provide

investors

an

enhanced

perspective

of

the

operating

performance

of

the

partnership's

assets

and

the

cash

that

the

business

is

generating.

EBITDA

in

the

following

reconciliations

relate

to

our

reportable

segments

or

a

portion

of

a

reportable

segment.

We

do

not

allocate

general

and

administrative

expenses

to

our

reportable

segments

because

those

expenses

relate

primarily

to

the

overall

management

at

the

entity

level.

Therefore,

EBITDA

reflected

in

the

following

reconciliations

excludes

any

allocation

of

general

and

administrative

expenses

consistent

with

our

policy

for

determining

segmental

operating

income,

the

most

directly

comparable

GAAP

measure.

EBITDA

should

not

be

considered

in

isolation

or

as

a

substitute

for

a

measure

of

performance

prepared

in

accordance

with

GAAP.

Neither

EBITDA

nor

distributable

cash

flow

are

intended

to

represent

cash

flows

for

the

period,

nor

are

they

presented

as

an

alternative

to

net

income.

They

should

not be considered in isolation or as a substitute for a measure of performance

prepared in accordance with GAAP. Year Ended

December 31,

2011

The following is a reconciliation of projected incremental operating income to

projected incremental EBITDA related to our internal growth program: |

Reconciliation of Non-GAAP Financial

Information: Storage Segment

27

(Unaudited, Dollars in Thousands)

The following is a reconciliation of operating income to EBITDA for the Storage Segment:

2006

2007

2008

2009

2010

Operating income

108,486

$

114,635

$

141,079

$

171,245

$

178,947

$

Plus depreciation and amortization expense

53,121

62,317

66,706

70,888

77,071

EBITDA

161,607

$

176,952

$

207,785

$

242,133

$

256,018

$

Projected incremental operating income range

$ 16,500 - 25,500

Plus projected incremental depreciation and

amortization expense range

8,500 - 9,500

Projected incremental EBITDA range

$ 25,000 - 35,000

St. James, LA

Terminal

Expansion

Phase 1

St. Eustatius

Distillate

Project

Projected annual operating income range

$ 11,000 - 20,000

$ 4,000 - 8,000

Plus projected annual depreciation and

amortization expense range

4,000 - 5,000

1,000 - 2,000

Projected annual EBITDA range

$ 15,000 - 25,000

$ 5,000 - 10,000

The

following

is

a

reconciliation

of

projected

annual

operating

income

to

projected

annual

EBITDA

for

certain

projects

in

our

storage

segment

related

to

our internal growth program:

The following is a reconciliation of projected incremental operating income to projected incremental

EBITDA: Year Ended December 31,

Year Ended

December 31, 2011

NuStar

Energy

L.P.

utilizes

two

financial

measures,

EBITDA

and

distributable

cash

flow,

which

are

not

defined

in

United

States

generally

accepted

accounting

principles

(GAAP).

Management

uses

these

financial

measures

because

they

are

widely

accepted

financial

indicators

used

by

investors

to

compare

partnership

performance.

In

addition,

management

believes

that

these

measures

provide

investors

an

enhanced

perspective

of

the

operating

performance

of

the

partnership's

assets

and

the

cash

that

the

business

is

generating.

EBITDA

in

the

following

reconciliations

relate

to

our

reportable

segments

or

a

portion

of

a

reportable

segment.

We

do

not

allocate

general

and

administrative

expenses

to

our

reportable

segments

because

those

expenses

relate

primarily

to

the

overall

management

at

the

entity

level.

Therefore,

EBITDA

reflected

in

the

following

reconciliations

excludes

any

allocation

of

general

and

administrative

expenses

consistent

with

our

policy

for

determining

segmental

operating

income,

the

most

directly

comparable

GAAP

measure.

EBITDA

should

not

be

considered

in

isolation

or

as

a

substitute

for

a

measure

of

performance

prepared

in

accordance

with

GAAP.

Neither

EBITDA

nor

distributable

cash

flow

are

intended

to

represent

cash

flows

for

the

period,

nor

are

they

presented

as

an

alternative

to

net

income.

They

should

not

be

considered

in

isolation

or

as

a

substitute for a measure of performance prepared in accordance with GAAP.

|

Reconciliation of Non-GAAP Financial Information:

Asphalt and Fuels Marketing Segment

28

(Unaudited, Dollars in Thousands)

Asphalt

Operations

Fuels Marketing

Operations

Asphalt and

Fuels Marketing

Segment

Operating income

53,977

$

36,884

$

90,861

$

Plus depreciation and amortization expense

20,164

93

20,257

EBITDA

74,141

$

36,977

$

111,118

$

Asphalt

Operations

Fuels Marketing

Operations

Asphalt and

Fuels Marketing

Segment

Operating income

50,710

$

9,919

$

60,629

$

Plus depreciation and amortization expense

19,463

-

19,463

EBITDA

70,173

$

9,919

$

80,092

$

Year Ended

December 31, 2007

Year Ended

December 31, 2006

Asphalt

Operations

Fuels Marketing

Operations

Asphalt and

Fuels Marketing

Segment

Asphalt and Fuels

Marketing

Segment

Asphalt and Fuels

Marketing

Segment

Operating income

76,267

$

36,239

$

112,506

$

21,111

$

26,815

$

Plus depreciation and amortization expense

14,182

552

14,734

423

-

EBITDA

90,449

$

36,791

$

127,240

$

21,534

$

26,815

$

NuStar

Energy

L.P.

utilizes

two

financial

measures,

EBITDA

and

distributable

cash

flow,

which

are

not

defined

in

United

States

generally

accepted

accounting

principles

(GAAP).

Management

uses

these

financial

measures

because

they

are

widely

accepted

financial

indicators

used

by

investors

to

compare

partnership

performance.

In

addition,

management

believes

that

these

measures

provide

investors

an

enhanced

perspective

of

the

operating

performance

of

the

partnership's

assets

and

the

cash

that

the

business

is

generating.

EBITDA

in

the

following

reconciliations

relate

to

our

reportable

segments

or

a

portion

of

a

reportable

segment.

We

do

not

allocate

general

and

administrative

expenses

to

our

reportable

segments

because

those

expenses

relate

primarily

to

the

overall

management

at

the

entity

level.

Therefore,

EBITDA

reflected

in

the

following

reconciliations

excludes

any

allocation

of

general

and

administrative

expenses

consistent

with

our

policy

for

determining

segmental

operating

income,

the

most

directly

comparable

GAAP

measure.

EBITDA

should

not

be

considered

in

isolation

or

as

a

substitute

for

a

measure

of

performance

prepared

in

accordance

with

GAAP.

Neither

EBITDA

nor

distributable

cash

flow

are

intended

to

represent

cash

flows

for

the

period,

nor

are

they

presented

as

an

alternative

to

net

income.

They

should

not

be

considered

in

isolation

or

as

a

substitute

for

a

measure

of

performance

prepared

in

accordance

with GAAP.

The following tables reconcile operating income to EBITDA for asphalt operations and fuels marketing

operations in our asphalt and fuels marketing segment: Year Ended December 31, 2010

Year Ended December 31, 2009

Year Ended December 31, 2008 |

Reconciliation of Non-GAAP Financial Information:

Asphalt and Fuels Marketing Segment (continued)

29

(Unaudited, Dollars in Thousands)

The following is a reconciliation of projected incremental operating income to

projected incremental EBITDA: Projected incremental operating income

range $ 39,500 -

44,000

$ 43,000 -

52,000

Plus projected incremental depreciation and

amortization expense range

500 -

1,000

2,000 -

3,000

Projected incremental EBITDA range

$ 40,000 -

45,000

$ 45,000 -

55,000

Annually Over

Life of Hedges

Year Ended

December 31, 2011

Projected incremental operating income range

$ 26,000 -

34,000

$ 17,000 -

20,000

Plus projected incremental depreciation

and amortization expense range

4,000 -

6,000

1,000 -

2,000

Projected incremental EBITDA range

$ 30,000 -

40,000

$ 18,000 -

22,000

Less projected allocations for distributable

cash flow purposes

(10,000)

(6,000)

Projected incremental distributable cash

flow range

$ 20,000 -

30,000

$ 12,000 -

16,000

The

following

is

a

reconciliation

of

projected

incremental

operating

income

to

projected

incremental

EBITDA

to

projected

distributable

cash

flow

for

the

San

Antonio Refinery acquisition:

Three Months

Ended

June 30, 2011

Year Ended

December 31, 2011

NuStar

Energy

L.P.

utilizes

two

financial

measures,

EBITDA

and

distributable

cash

flow,

which

are

not

defined

in

United

States

generally

accepted

accounting

principles

(GAAP).

Management

uses

these

financial

measures

because

they

are

widely

accepted

financial

indicators

used

by

investors

to

compare

partnership

performance.

In

addition,

management

believes

that

these

measures

provide

investors

an

enhanced

perspective

of

the

operating

performance

of

the

partnership's

assets

and

the

cash

that

the

business

is

generating.

EBITDA

in

the

following

reconciliations

relate

to

our

reportable

segments

or

a

portion

of

a

reportable

segment.

We

do

not

allocate

general

and

administrative

expenses

to

our

reportable

segments

because

those

expenses

relate

primarily

to

the

overall

management

at

the

entity

level.

Therefore,

EBITDA

reflected

in

the

following

reconciliations

excludes

any

allocation

of

general

and

administrative

expenses

consistent

with

our

policy

for

determining

segmental

operating

income,

the

most

directly

comparable

GAAP

measure.

EBITDA

should

not

be

considered

in

isolation

or

as

a

substitute

for

a

measure

of

performance

prepared

in

accordance

with

GAAP.

Neither

EBITDA

nor

distributable

cash

flow

are

intended

to

represent

cash

flows

for

the

period,

nor

are

they

presented

as

an

alternative

to

net

income. They should not be considered in isolation or as a substitute for a

measure of performance prepared in accordance with GAAP. |