Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - REX ENERGY CORP | d8k.htm |

Rex

Energy Rex Energy

Corporate Presentation

Corporate Presentation

Rex Energy Corporation | 476 Rolling Ridge Drive | State College, PA 16801

P: (814) 278-7267 | F: (814) 278-7286

E: InvestorRelations@RexEnergyCorp.com

www.rexenergy.com

Together We Can Make A Difference

May 2011

May 2011

Exhibit 99.1 |

Forward

Looking Statements Except for historical information, statements made in this

release, including those relating to significant potential, future earnings, cash flow, capital expenditures,

production growth and planned number of wells (as well as the timing of rig operations,

natural gas processing plant commissioning and operations, fracture stimulation

activities and the completion of wells and the expected dates that wells are producing hydrocarbons that are sold), are forward-looking statements

within

the

meaning

of

Section

27A

of

the

Securities

Act

of

1933,

as

amended,

and

Section

21E

of

the

Securities

Exchange

Act

of

1934,

as

amended.

These

forward-

looking

statements

are

indicated

by

words

such

as

“expected”,

“expects”,

“anticipates”

and

similar

words.

These

statements

are

based

on

assumptions

and

estimates that management believes are reasonable based on currently available

information; however, management's assumptions and the company's future

performance are subject to a wide range of business risks and uncertainties, and there is

no assurance that these goals and projections can or will be met. Any number of

factors could cause actual results to differ materially from those in the forward-looking statements, including (without limitation) the following:

•adverse economic conditions in the United States and globally;

•the difficult and adverse conditions in the domestic and global capital and credit

markets; •domestic and global demand for oil and natural gas;

•sustained

or

further

declines

in

the

prices

the

company

receives

for

oil

and

natural

gas;

•the

effects

of

government

regulation,

permitting

and

other

legal

requirements;

•the geologic quality of the company’s properties with regard to, among other things, the existence of hydrocarbons in economic

quantities; •uncertainties about the estimates of the company’s oil and natural gas reserves;

•the company’s ability to increase production and oil and natural gas income through exploration and

development; •the company’s ability to successfully apply horizontal drilling techniques and tertiary recovery

methods; •the number of well locations to be drilled, the cost to drill and the time frame within

which they will be drilled; •the effects of adverse weather on operations;

•drilling and operating risks;

•the ability of contractors to timely and adequately perform their drilling, construction,

well stimulation, completion and production services;

•the availability of equipment, such as drilling rigs and transportation pipelines;

•changes in the company’s drilling plans and related budgets;

•the adequacy of capital resources and liquidity including (without limitation) access to

additional borrowing capacity; and •uncertainties associated with our legal proceedings and the outcome.

The company undertakes no obligation to publicly update or revise any forward-looking

statements. Further information on the company’s risks and uncertainties is

available in the company's filings with the Securities and Exchange Commission.

The company's internal estimates of reserves may be subject to revision and may be

different from estimates by the company's external reservoir engineers at year

end. Although the company believes the expectations and forecasts reflected in these and other forward-looking statements are reasonable, it can give no

assurance they will prove to have been correct. They can be affected by inaccurate

assumptions or by known or unknown risks and uncertainties. 2

Forward Looking Statements

Forward Looking Statements |

Hydrocarbon Volume Estimates

Hydrocarbon Value Estimates

Hydrocarbon Value Estimates

3

This presentation includes management’s estimates of Marcellus Shale potential

recoverable resources, per well EUR (estimated ultimate recovery of resources)

and upside potential of recoverable resources. Except as noted, these have been estimated internally by the Company without review by

independent engineers and do not necessarily constitute reserves. These estimates

are included to demonstrate the potential for future drilling by the

Company. Actual recovery of these potential volumes is inherently more speculative

than recovery of estimated proved reserves. Estimates of potential

recoverable resources, per well EURs and upside potential for Company oil and gas shale

acreage are particularly speculative due to the limited experience in Marcellus

Shale horizontal development, with its limited production history. Ultimate recoveries will be dependent upon numerous factors including actual

encountered geological conditions, the impact of future oil and gas pricing and

exploration costs, and our future drilling decisions and budgets based upon our

future evaluation of risk, returns and the availability of capital and, in many areas, the outcome of negotiation of drilling arrangements with holders of

adjacent or fractional interest leases. In addition, potential recoverable

resources are based on undesignated future well locations under assumed acreage

spacing which may not have been specifically included in any definitive development plan

and ultimately may not be drilled. Accordingly, such estimates may differ

significantly from the hydrocarbon quantities that are ultimately recovered.

SEC rules prohibit a publicly-reporting oil and gas company from including oil and

gas resource estimates in their filings with the SEC, except proved, probable and

possible reserves that meet the SEC’s definitions of such terms. Illinois Basin estimates (including Lawrence Field) of oil in place and other

resource volumes, oil in place and other reserve volumes indicated herein are not based

on SEC definitions and guidelines. Unless otherwise indicated, estimates of

non-proved reserves and other hydrocarbons included herein may not meet specific definitions of reserves or resource categories within the

meaning of the SPE/SPEE/WPC Petroleum Resource Management System. |

Rex Energy

Overview Rex Energy Overview

Significant upside in two high growth shale plays and tertiary oil recovery

•

1.4

–

2.1

Tcfe

in

non-proven

Marcellus

Shale

resource

potential

•

9.4

–

22.7

Mmboe

in

non-proven

Niobrara

Shale

resource

potential

(1)

•

24.9

–

62.2

Mmbls

in

non-proven

Tertiary

Recovery

oil

resource

potential

(1)

Liquids Rich Production & Proven Reserves

•

Total

production

of

27.8

Mmcfe/d

(4,628

BOE/d)

(2)

o

49% oil and NGLs

•

201.7

Bcfe

(33.6

Mmbls)

proven

reserves

(3)

o

62% of proved developed is attributable oil and NGLs

o

85% liquids rich capture

•

PV-10

value

of

$269.4

million

(3)

Strong

Balance

Sheet

&

Liquidity

•

$10.2 million cash

•

$30.0 million in debt

•

Borrowing base increased to $160.0 million in March 2011

•

$130.0 million available on line of credit

•

$6.4 million in Marcellus drilling carries

1. Assumptions

based

on

full

development

program.

Actual

results

may

vary

significantly.

Not

proved.

See

“Hydrocarbon

Volume

Estimates”

on

page

3

and

page

11.

2. First quarter 2011 results

3. Based on year-end 2010 reserves

4. Unaudited financial results as of 3/31/2011

4

(1)

(4) |

Areas of

Operation Areas of Operation

Appalachian Region

•

~ 59,100 net acres in Marcellus Shale fairway

o

63% of acreage in liquids rich portion of the play

o

Total

non-proven

resource

potential

of

1.4

–

2.1

Tcfe

(1)

o

$6.4 million in drilling carries

(2)

Rockies Region

•

39,000 net acres in Niobrara Shale fairway

o

100% of acres in oil window of the

Niobrara in the DJ Basin

o

Total non-proven resource potential

of 9.4 –

22.7 MMBoe

(1)

Illinois Region

•

Tertiary recovery oil projects

o

Total

non-proven

resource

potential

of

24.9

–

62.2

MMBbls

from

ASP

flooding

in

the

Lawrence

Field

1. Assumptions

based

on

full

development

program.

Actual

results

may

vary

significantly.

Not

proved.

See

“Hydrocarbon

Volume

Estimates”

on

page

3

and

page

11.

2. Unaudited financial results as of 3/31/2011

3. Includes 8,300 net farm in acres

5

(3)

(1) |

Key

Investment Highlights for 2011 Key Investment Highlights for 2011

•

Rex Energy is poised for growth

o

Strong position in oil and liquids-rich areas

o

Company expects 2011 production growth of 71%-95% over 2010

•

Strong core position in the Appalachian Basin

o

Solid core position in Butler County with 385 potential drill sites

in the Marcellus Shale, with additional potential in the Utica and

Upper Devonian Shale

•

Strong track record of growth with a historical reserve

CAGR of 75% and low F&D cost

•

Rex Energy is equipped to thrive in a low gas price

environment

o

79% of the 2011 capital budget is dedicated to oil and

liquids rich project areas

o

73% of the Appalachian capital budget is allocated to

liquids rich Butler County

•

Secured key drilling, fracture stimulation, and tubular

services for the next two years

•

Opportunities for growth within tertiary recovery projects in

the Illinois Basin and preliminary results in the Niobrara

•

Investment in human capital

6 |

Positioned

For Growth Positioned For Growth

•

Poised to achieve 71% -

95% production growth in 2011

•

Expect to see 22% -

40% growth in oil and NGL production in 2011

•

A mid case December exit rate of 45.6 Mmcfe/day in 2011 represents an 83% increase

compared to the 2010 exit rate 7

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2008 Actual

2009 Actual

2010 Actual

2011 Low Case

2011 High Case

2011 Mid Case Dec

Exit Rate

0%

20%

40%

60%

80%

100%

120%

140%

Dry Gas

Wet Gas

NGL & Condensate

Oil

Annual Growth |

Reserve

Growth Reserve Growth

Proved Reserve & Compound Annual Growth Rate

Year-End 2010

(1)

•

33.6 Mmboe

(201.7Bcfe)

•

Drill Bit F&D cost of $0.68/ Mcfe

•

$269.4 million PV-10

o

42% proved developed

o

37% oil & NGLs

o

85% liquids rich capture

Year-End 2009

(2)

•

20.9 Mmboe

(125.2 Bcfe)

•

$190.5 million PV-10

o

54% proved developed

o

55% oil & NGLs

Year-End 2008

(3)

•

10.9 Mmboe

(65.4 Bcfe)

•

$84.0 million PV-10

o

62% proved developed

o

52% oil

1. Year-end 2010 reserves calculated using $75.96 per Bbl and $4.38 per Mcf.

2. Year-end 2009 reserves calculated using $57.65 per Bbl and $3.87 per Mcf.

3. Year-end 2008 reserves calculated using $41.00 per Bbl and $5.71 per Mcf.

8

0

50

100

150

200

250

300

Year-End

2008

Year-End

2009

Year-End

2010

Natural Gas

NGLs

Oil

CAGR |

2011

Capital Budget 2011 Capital Budget

•79%

of

the

total

budget

is

allocated

to

oil

and

liquids

rich

gas

operations.

•73% of the Appalachian

budget is dedicated to liquids rich Butler County operations.

9 |

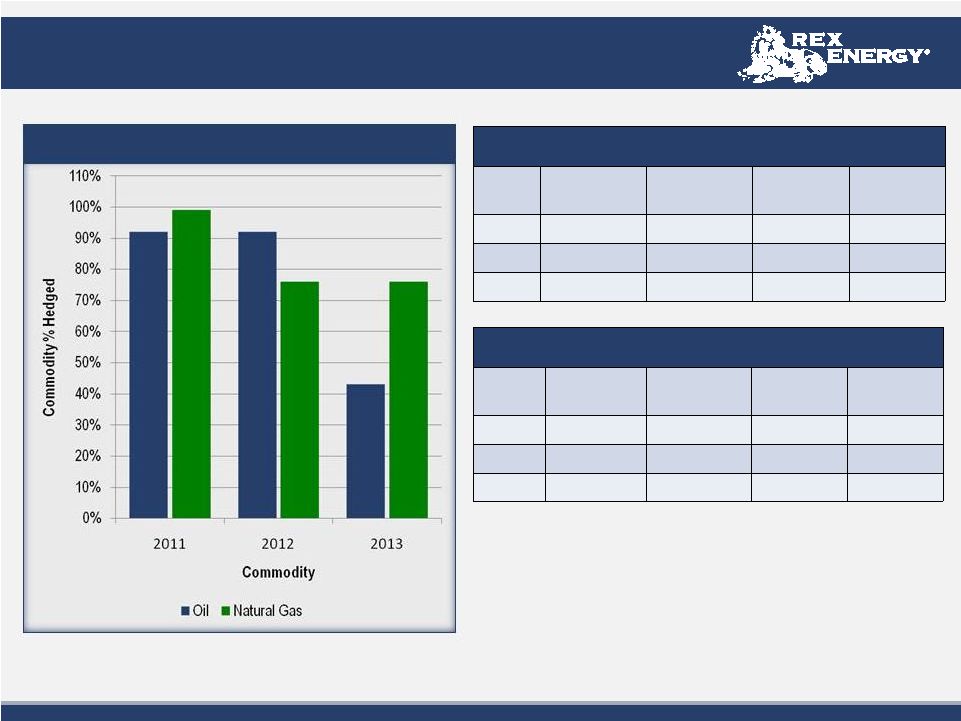

Current

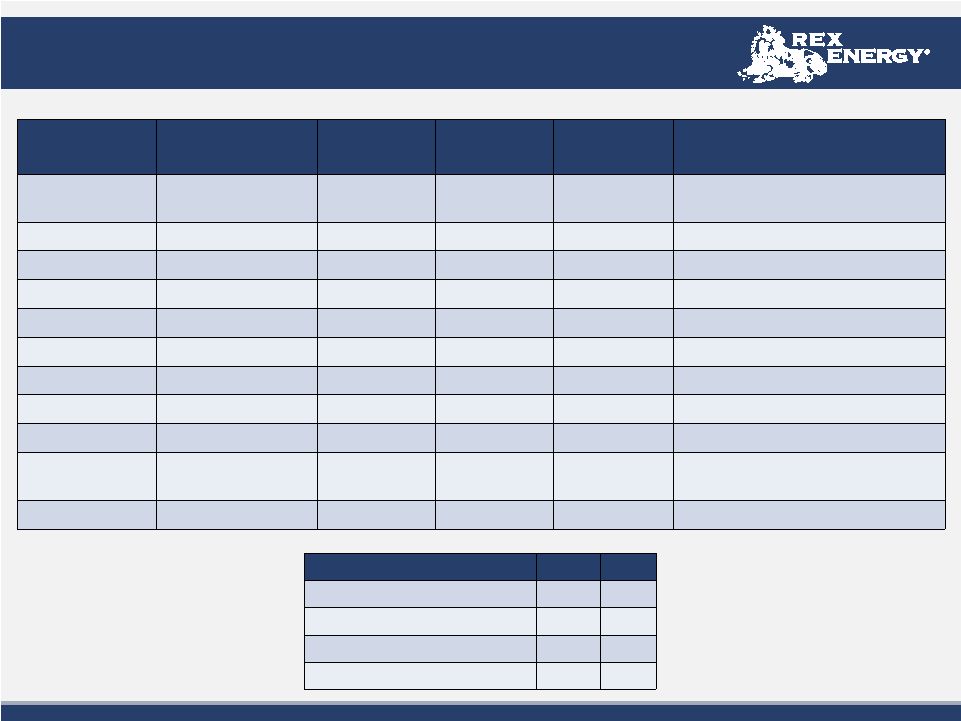

Hedging Summary Current Hedging Summary

Current Production Hedged

Natural Gas

% of Current

with Floor

% of Current

with Ceiling

Avg. Floor

Price

Avg. Ceiling

Price

2011

(1)(2)

99%

87%

$ 5.26

$ 5.67

2012

(2)

76%

76%

$ 4.94

$ 5.89

2013

76%

76%

$ 5.00

$6.25

Crude Oil

% of Current

with Floor

% of Current

with Ceiling

Avg. Floor

Price

Avg. Ceiling

Price

2011

92%

92%

$68.54

$104.69

2012

92%

92%

$67.10

$112.03

2013

43%

43%

$70.50

$120.00

•

Percentage hedged based on low case of second quarter

guidance with decline built in

10

1. ~12%

of

current

natural

gas

production

covered

in

2011

by

put

spread

with

a

$3.68

short

put

price

for

a

$1.04

put

spread

2.

~13%

of

current

natural

gas

production

covered

in

2011

and

2012

by

put

spread

with

a

$4.00

short

put

price

for

a

$1.75

put

spread |

Marcellus

Overview Marcellus Overview

Butler County (Operated)

•

~54,000 gross (37,000 net) acres

•

Joint Venture with Sumitomo in Butler County

o

70% Rex / 30% Sumitomo

•

Butler Midstream Joint Venture

o

60% Stonehenge / 28% Rex / 12% Sumitomo

o

Operation of 40 Mmcf/d cryogenic plant

o

Pipeline infrastructure

Westmoreland, Centre, and Clearfield Counties

(Non Operated)

•

~47,000 gross (19,000 net) acres

•

Joint Venture among Williams, Rex, and Sumitomo

o

50% Williams / 40% Rex / 10% Sumitomo

o

JV includes interest in gathering and transportation

o

$6.4 million in Sumitomo drilling carries remaining

Other Operated Marcellus Acreage

•

~17,700 gross (3,100 net) acres in areas of Clearfield, Centre, Somerset and Fayette

counties 1. Assumptions

based

on

full

development

program.

Individual

well

results

may

vary

significantly.

Not

proved.

See

“Hydrocarbon

Volume

Estimates”

on

page

3.

2. Includes

approximately

129

Bcfe

of

Marcellus

Shale

proved

reserves

as

of

December

31,

2010

11 |

Marcellus

Operated Overview Marcellus Operated Overview

Butler County, PA

•

2011 Operational Assumptions

o

Drilling the full year with one rig, and two additional rigs

beginning in mid April

o

Plan to drill 34 gross (22 net) wells

o

Fracture and complete at least 24 gross (15 net) wells

o

Construction of the second cryogenic plant (Bluestone),

proposed commissioning in first quarter 2012

o

Primary leasing strategy will fill in future drilling units, and

other contiguous acreage blocks within the core operational

area

•

2011 Operational Update

o

Drilled 10 gross (6 net) wells

o

Fractured and completed 6 gross (4 net) wells

o

Placed in service 10 gross (7 net) wells

o

5 day average rate on four of the five Drushel

wells at 3.7

Mmcfe/day

Average lateral length of 3,200 feet

Fifth well not yet fractured

o

Bluestone cryogenic plant capacity permit request increased

from 40.0 Mmcf/d

to 50.0 Mmcf/d

o

Third cryogenic plant permit filed

Marcellus Operated Area in PA

12

Columbia

Dominion

Natural Fuel

REX Leasehold |

•

Core acreage position of 36,000 gross (22,00 net) acres

o

Allows for minimal rig movement

o

Decreases in drilling time

o

Maximizes unitized acreage

•

Close access to infrastructure and pipelines

•

Terrain composition very accessible

•

Low risk geological area

•

Additional production possibilities in the Utica and

Upper Devonian Shale

•

Maintaining a two rig drilling program allows for

minimal lease expirations

Why Rex Values its Presence in Butler County

Why Rex Values its Presence in Butler County

Prospective Butler Units

13

•

Approximately 385 drilling locations

•

Favorable commodity price differentials |

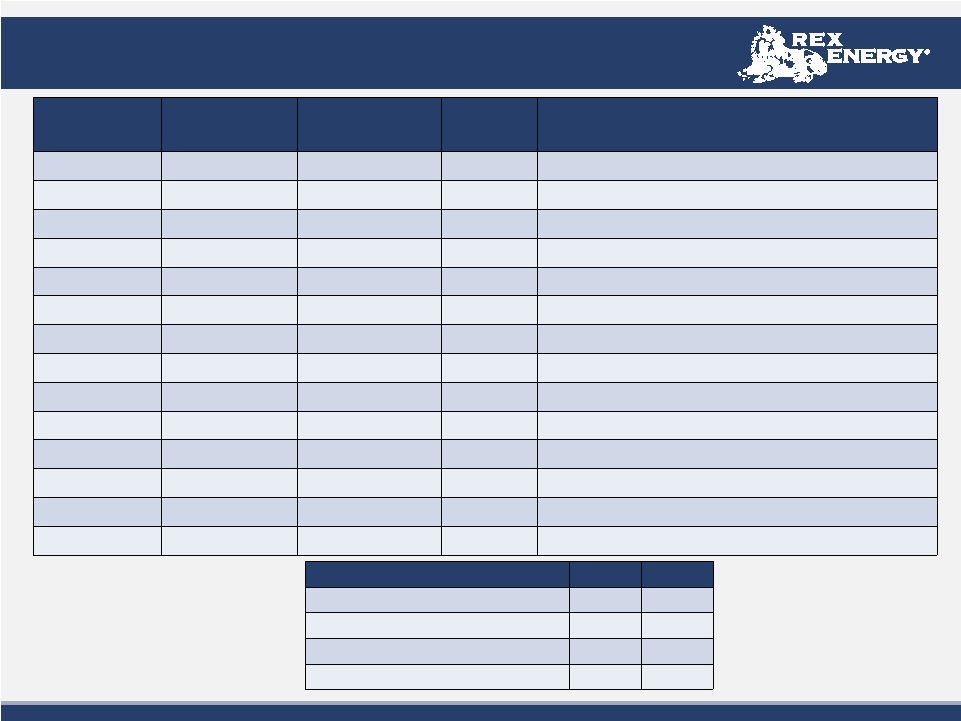

Butler

Operated Drilling & Completion Schedule Butler Operated Drilling &

Completion Schedule Rig

Pad

Pad

Gross Well

Gross Well

Count

Count

Net Well

Net Well

Count

Count

Status

Status

UDI 54

Drushel

(1)

5.0

3.5

4 of 5 wells frac’d with 5 day average rates of 3.7 Mmcfepd

UDI 54

Talarico

3.0

2.1

All wells drilled; frac initiated on 5/1

UDI 54

Grosick

(2)

7.0

3.0

Drilling

5

of

7

wells

UDI 54

Carson

3.0

2.1

Pad construction complete

UDI 54

Bricker

4.0

2.8

Permitting

Total UDI 54

22.0

13.5

UDI 52

McElhinney

2.0

1.4

Both wells drilled: Frac scheduled in June

UDI 52

Behm

3.0

2.1

Second of three wells drilling

UDI 52

Grahm

3.0

2.1

Pad construction complete

UDI 52

Meyer

2.0

1.4

Pad construction phase

Total UDI 52

10.0

7.0

Bronco 10

Gilliland

(3)

6.0

4.2

1

well drilling

Bronco 10

Cheeseman

(4)

1.0

0.7

Pad complete; conductor being set

Total Bronco 10

7.0

4.9

14

1. Four of the five Drushel wells were drilled in 2010

2. Rex has a 43.1% WI after Gastar and Sumitomo

3. Includes one Burkett test well

4. Utica test well

Gross

Net

YTD Wells Placed in Service

10.0

7.0

YTD Wells Awaiting Completion

11.0

4.4

YTD Wells Drilled

10.0

5.9

Wells Currently Drilling

3.0

1.7

th

st |

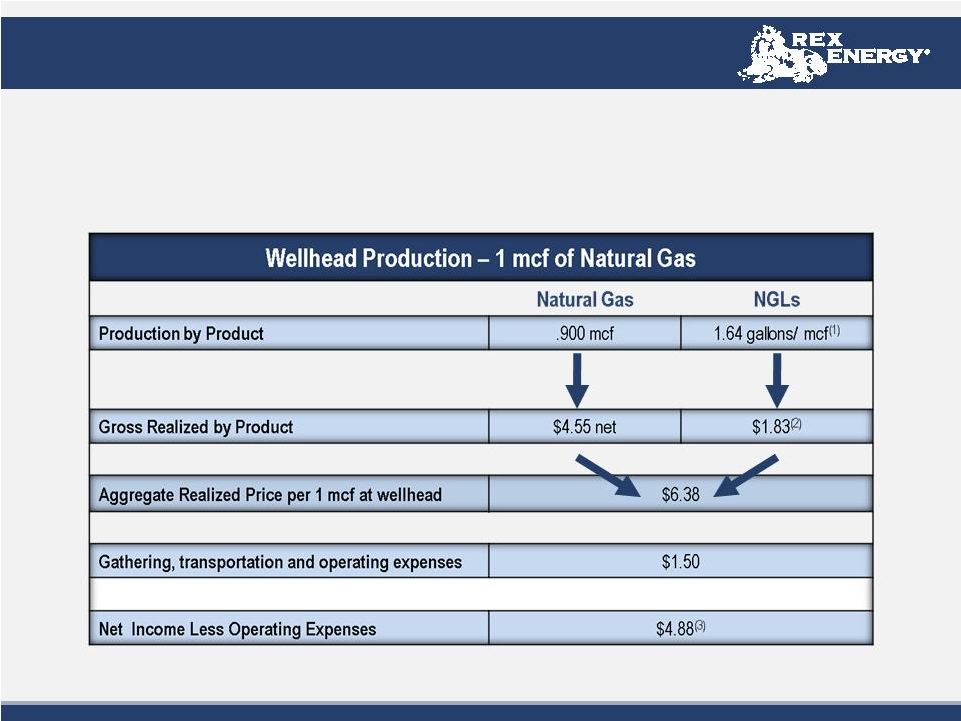

Wet Gas

Economic Yields Wet Gas Economic Yields

$5.00 NYMEX equates to $6.38 per mcf

price

•

$5.00 NYMEX Henry Hub

o

$0.05 added to NYMEX Henry Hub for premium

•

$90.00 NYMEX WTI

1.

.85 gallon/ mcf

is excluded since it is used as fuel for compressors at the cryogenic

plant 2.

Price assumption of 52% of $90.00 NYMEX WTI

3.

Does not include Rex’s 28% interest in cash flow from the cryogenic plant

partnership 15 |

Marcellus

Non-Operated Overview Marcellus Non-Operated Overview

16

1. Includes non operated acreage only |

County

Rig

Pad

Pad

Gross Well

Gross Well

Count

Count

Net Well

Net Well

Count

Count

Status

Status

Westmoreland

H&P 287

Uschak

#2

(1)

5.0

2.0

Two placed in service

Remaining three awaiting on completion

Westmoreland

H&P 287

Androstic

3.0

1.2

Drilled, awaiting completion

Westmoreland

H&P 287

National Metals

2.0

0.8

Drilled, awaiting completion

Westmoreland

H&P 287

Frye

2.0

0.8

Drilling the first well

Westmoreland

H&P 287

McBroom

3.0

1.2

Awaiting drilling rig

Total H&P 287

15.0

6.0

Westmoreland

Patterson 480

Uschak #1

4.0

1.6

Drilled, awaiting completion

Westmoreland

Patterson 480

Marco

3.0

1.2

Rig drilling second of three wells

Total Patterson 480

7.0

2.8

Clearfield

Patterson 332

Resource

Recovery #1

4.0

1.6

Rig Drilling first of four wells

Total Patterson 332

4.0

1.6

Westmoreland & Clearfield Non Operated

Westmoreland & Clearfield Non Operated

Drilling & Completion Schedule

Drilling & Completion Schedule

17

Gross

Net

YTD Wells Placed in Service

3.0

1.2

Wells Awaiting Completion

13.0

5.2

YTD Wells drilled

10.0

4.0

Wells Currently Drilling

3.0

1.2

1. Four of the five Uschak wells were drilled in 2010 |

Conceptual Marcellus Economics

Conceptual Marcellus Economics

Butler County (Wet Gas) Assumptions

(1)

•

3.0 MMcfe/d IP Rate

•

4.4 Bcfe gross EUR

•

$4.7 million drilling and completion costs

•

15% royalties

•

Gas Price Basis Adjustment: $0.26/Mcf

•

NGL

&

condensate

volumes:

1.64

gallons

per

Mcf

(~39

Bbls

per MMcf)

•

NGL price assumptions: $0.94/gal (~52% of NYMEX oil price)

•

Gathering transportation & operating expenses: $1.50/Mcf

Westmoreland & Central PA (Dry Gas)

Assumptions

(1)

•

3.5 MMcf/d IP Rate

•

3.0 Bcf gross EUR

•

$4.7 million drilling and completion costs

•

15% royalties

•

Gas price basis adjustment: ($.09)/Mcf

•

Gathering transportation & operating expenses: $0.67/Mcf

Type Curves

Before Tax IRR

1.

Based on the 2010 reserve report & current NGL Pricing in Butler

18 |

Marcellus

Well Cost Comparison Marcellus Well Cost Comparison

Reserve Well Economics

•Average Well Cost of $4.7

million •Average

Drilling and Completion cost -

$1.9 million

•Average Frac Cost -

$2.2 million

•Average Equipment cost

- $0.6

million 1. Results from the 2010 Drilling Program

19 |

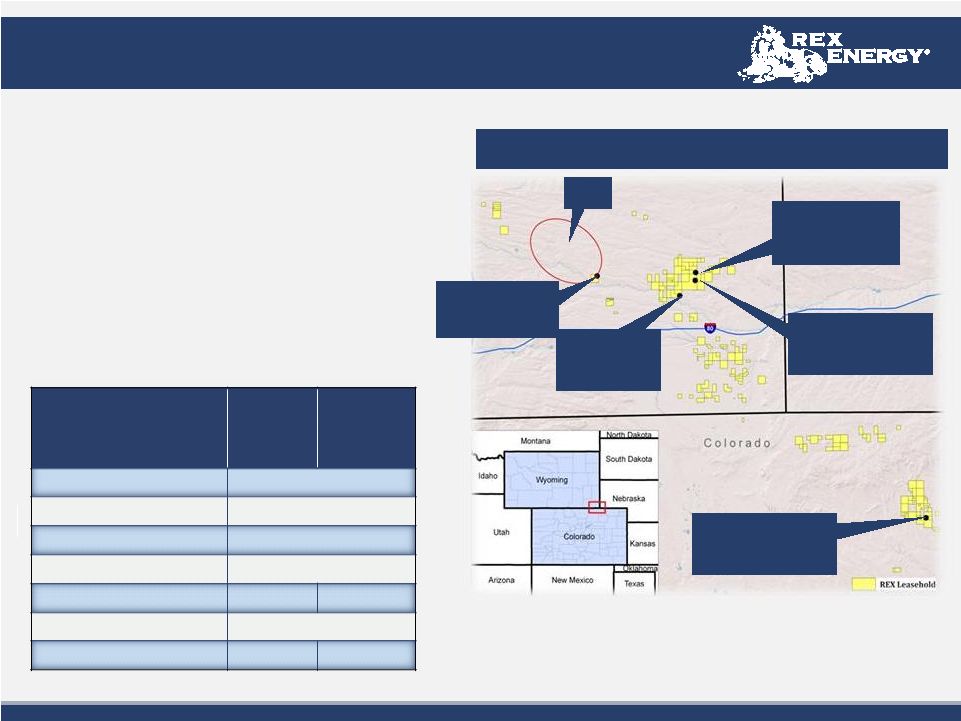

Niobrara

Overview Niobrara Overview

~56,000 gross (39,000 net) acres

•

3 horizontal wells drilled (infill and Matrix Porosity

results)

DJ Basin Niobrara Summary

•

Thick

“Source

Rock”

–

300+

ft.

•

High total organic content (TOC’s) of 2-10%

•

Strong matrix contribution from high porosity chalks

•

Production likely influenced by faults and fractures

•

Mature over large aerial extent

•

Expected

well

costs

of

$3.5

-

$4.2

MM

DJ Basin

Rex Energy

Silo State 41-22H

IP: 67 BOE/d

Rex Energy

BJB #1H

Appears Non-

Commercial

Rex Energy

Herrington Farms 1H

IP: 202 BOE/d

20

Silo

Field

Rex Energy

Shapley 14-45H

Drilling

Rex Energy

Steege 11-31H

Currently Drilling

Resource Potential

Low Case

“Matrix”

Porosity

High

Case

“Dual Matrix

Porosity”

Net Acres

~39k

Assumed % Drilled

75%

Well Spacing

320 acres

Net

Potential Wells

91

EUR (MBO)

(1)

125

300

Royalties

17%

Upside

Potential (MMBO)

9.4

22.7

1. Assumptions based on full development program. Individual well results may vary

significantly. Not proved. See “Hydrocarbon Volume Estimates” on page 3. |

Conceptual Niobrara Economics

Conceptual Niobrara Economics

Niobrara Horizontal Well Assumptions

•

300 Bbls/d

IP

•

Gas sales start 18 months after oil sales

•

$4.2 million drilling and completion costs

•

18% royalties

•

Oil price basis adjustment: -$9.00/Bbls

•

Gathering transportation & operating expenses:

$13.05/Bbls

•

Severance & ad valorem taxes: 13%

21

Before Tax IRR

Silo Field Type Curve |

Lawrence

Field ASP Overview Lawrence Field ASP Overview

~ASP Project Summary

•

ASP stands for Alkali-Surfactant-Polymer flood

•

Alkali-Surfactant mix reduces interfacial tension allowing remaining oil to flow

easier through the formation •

Polymer

improves

sweep

efficiency

by

forcing

fluid

into

parts

of

the

field

not

effectively

swept

by

the

waterflood

•

Based on NSAI geological analysis and high grading of the acreage, 27 separate ASP units

have been designed to date. •

Laboratory

analysis

on

the

effect

of

ASP

flooding

of

cores

from

the

field

recovered

23%

of

OOIP

(16%

PV

(1)

Recovery)

•

Single

well

pilot

test

of

ASP

flooding

in

the

field

recovered

27%

of

OOIP

(20%

PV

(1)

Recovery)

Illinois Basin

~13,100 gross (13,000 net) acres in Lawrence Field

•

1 billion barrels of original-oil-in-place (OOIP)

•

Field has produced 400 MMBbls since 1906

•

Waterflooded in the 1950’s

•

Two successful surfactant-polymer flood pilots completed by Marathon

with 15-20% of OOIP recovered

•

Field currently produces ~1,600 gross (1,250 net) barrels per day under

waterflood

1.

Pore

volume

recovery

assumptions

based

on

full

development

program.

Individual

ASP

unit

results

may

vary

significantly.

Not

proved.

See

“Hydrocarbon

Volume

Estimates”

on

page

3.

Middaugh Unit, ASP

Project

22

REX Acreage |

ASP

Conceptual Economics ASP Conceptual Economics

•

Capital for the ASP plant has already been spent

•

90% of future capital will be chemical costs

•

North & Central areas of the field have been analyzed to date (~75% of the

field) o

Identified

18

target

continuous

sand

bodies

and

broke

these

down

into

27

separate

flood

units

(15

Bridgeport/

12 Cypress)

o

Base

case

probable

reserves

in

identified

floodable

sands:

39.4

MMBbls

(1)

in

the

Northern

&

Central

areas

of

the field at a 13% PV Recovery

Typical ASP Flood IRR vs Oil Price at Various PV Recoveries

1. Estimated

by

Netherland,

Sewell

&

Associates,

Inc.

Does

not

represent

proved

reserves.

See

“Hydrocarbon

Volume

Estimates”

on

page

3.

23

Total ASP Potential Reserves at Various PV Recoveries |

Project

Update •

Preliminary oil response seen:

o

Production increased from

16-62 gross BOPD

o

Oil cuts increased from

1.0% to 5.0% in total unit

o

Individual well oil cuts

increased from 1.5% to 15%

in first responding producer

o

Three additional producers

in early stages of response

o

Continue to monitor response

of pilot to determine future

ASP recovery models

•

Initiate expansion into 58 acre

Perkins-Smith area for $3MM in 2011:

o

ASP Plant complete:

no additional capx required

o

Drill 9 replacement wells

o

Complete flow line tie-ins

o

Initiate brine injection in 3Q

o

Initiate ASP injection in late 4Q

Lawrence

Lawrence

Field

Field

ASP

ASP

Update

Update

(1)

(1)

Perkins-Smith Project Area

58 Acres

Griggs Project Area

72 Acres

Middagh Pilot

15 Acres

24

1. Update as of May 3, 2011 |

•

Operationally

o

Estimated

annual

production

growth

of

71%

-

95%

in

2011

o

79% of 2011 capital budget allocated to oil and liquids rich operating areas

o

Strong growth with a historical reserve CAGR of 75%

o

Preliminary Niobrara results

o

Additional potential in the Utica and Upper Devonian shale

o

4 full time rig program in 2011

o

Large inventory of drilling locations

•

Financially

o

Conservative balance sheet

o

Total line of credit availability of $130 million

o

Diversified portfolio with both oil and gas

o

Strong hedging position

Why Invest in Rex Energy?

Why Invest in Rex Energy?

25 |