Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - MAXIMUS, INC. | a6715087ex99_1.htm |

| 8-K - MAXIMUS, INC. 8-K - MAXIMUS, INC. | a6715087.htm |

Exhibit 99.2

FINAL TRANSCRIPT

MMS - Q2 2011 Maximus Inc Earnings Conference Call

Event Date/Time: May. 05. 2011 / 1:00PM GMT

F I N A L T R A N S C R I P T

May. 05. 2011 / 1:00PM, MMS - Q2 2011 Maximus Inc Earnings Conference Call

C O R P O R A T E P A R T I C I P A N T S

Lisa Miles

Maximus Inc - VP of Investor Relations

David Walker

Maximus Inc - CFO

Rich Montoni

Maximus Inc - President, CEO

Bruce Caswell

Maximus Inc - President and General Manager, Health Services Segment

C O N F E R E N C E C A L L P A R T I C I P A N T S

Torin Eastburn

CJS Securities - Analyst

Brian Kinstlinger

Sidoti - Analyst

P R E S E N T A T I O N

Operator

Greetings and welcome to the Maximus fiscal 2011 second quarter conference call. (Operator Instructions)It is now my pleasure to introduce your host, Lisa Miles, Vice-President of Investor Relations for Maximus. Thank you, Miss Miles; you may begin.

Lisa Miles - Maximus Inc - VP of Investor Relations

Good morning. Thank you for joining us on today's conference call. I would like to point out that we have posted a presentation to our website under the Investor Relations page to assist you in following along with today's call. With me today is Rich Montoni, Chief Executive Officer and David Walker Chief Financial Officer. Following Rich's prepared comments we will open the call up for Q & A.

Before we begin I would like to remind everyone that a number of statements made today will be forward looking in nature. Please remember that such statements are only predictions and actual results or events may differ materially as a result of risks we face including those discussed in exhibit 99.1 out of our SEC filings. We encourage you to review the summary of these risks in our most recent 10-K filed with the SEC. The Company does not assume any obligation to revise or update these forward-looking statements to reflect subsequent events or circumstances. And with that, I'll turn the call over to Dave.

David Walker - Maximus Inc - CFO

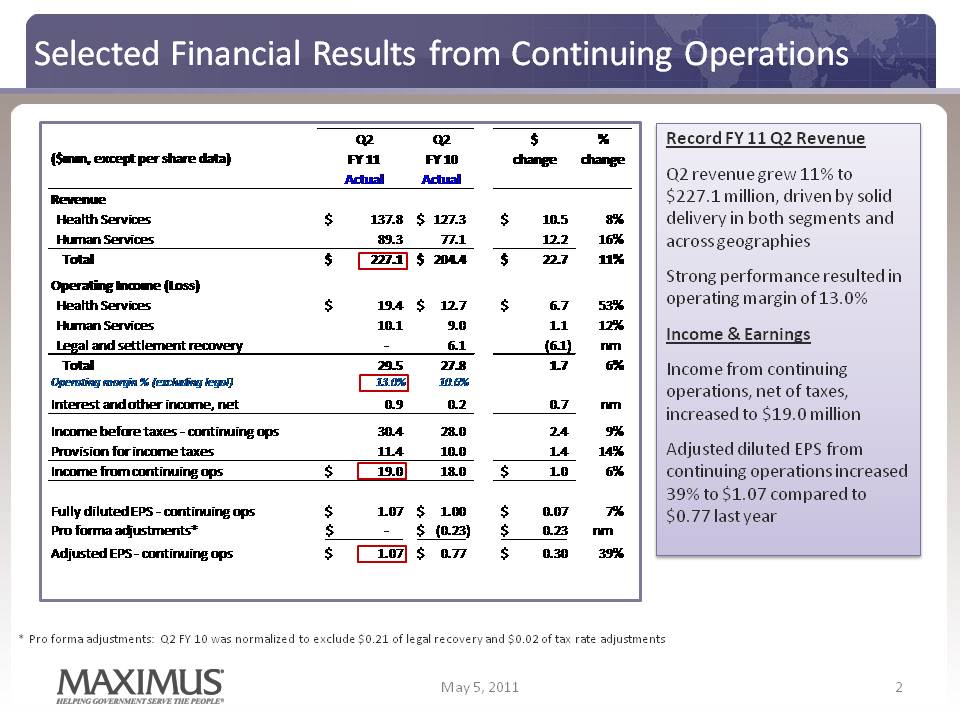

Thanks, Lisa. This morning Maximus reported record second quarter results from continuing operations,that exceeded both top line and bottom line expectations. Revenue from continuing operations increased 11% to $227.1 million, or 8% on a constant currency basis,compared to the same period last year. Revenue growth was driven by solid delivery in both segments and across all geographies. Strong operational performance in the second quarter resulted in an operating margin of 13%.

As we have discussed on prior calls investors should expect quarterly fluctuations in operating margin. We view this as normal course when you consider the portfolio of transaction-based BPO contracts that we manage, contract life cycles and the timing of expenses. For the second quarter of fiscal 2011, income from continuing operations, net of taxes, grew year-over-year to $19 million. Diluted earnings per share from continuing operations increased 39% to $1.07 for the second quarter compared to adjusted diluted earnings per share of $0.70 last year.

Last year's EPS was adjusted to exclude a pre-tax benefit of $6 million or $0.21 per diluted share related to a net legal recovery. We have included a normalization table on the last page of this morning's press release to provide investors with a consistent comparison to the prior year. We are pleased with the results in the quarter, which demonstrate our ongoing commitment to deliver profitable growth. We have worked hard over the last several years to create a healthy portfolio of projects and we remain dedicated to ensuring that new work meets our profit targets.

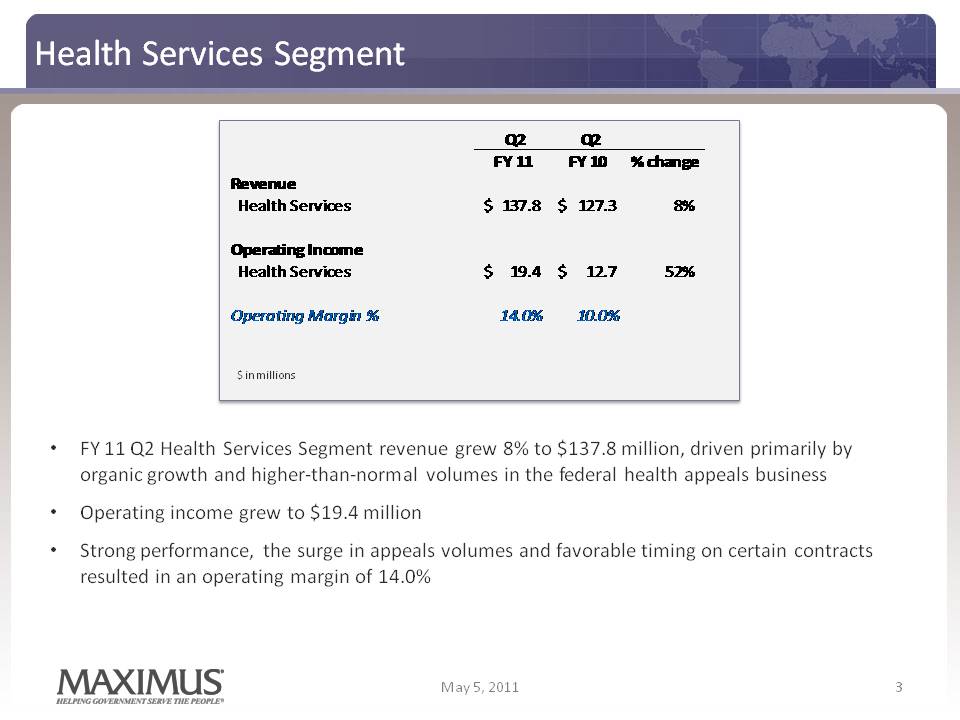

Now, let's look at the performance of our business by segment. Revenue in the health services segment grew 8% to $137.8 million in the second quarter, compared to the same period last year, driven primarily by organic growth and higher than normal volumes in our federal health appeals business. Second quarter operating income for the health services segment grew to $19.4 million compared to $12.7 million in the second quarter of fiscal 2010.

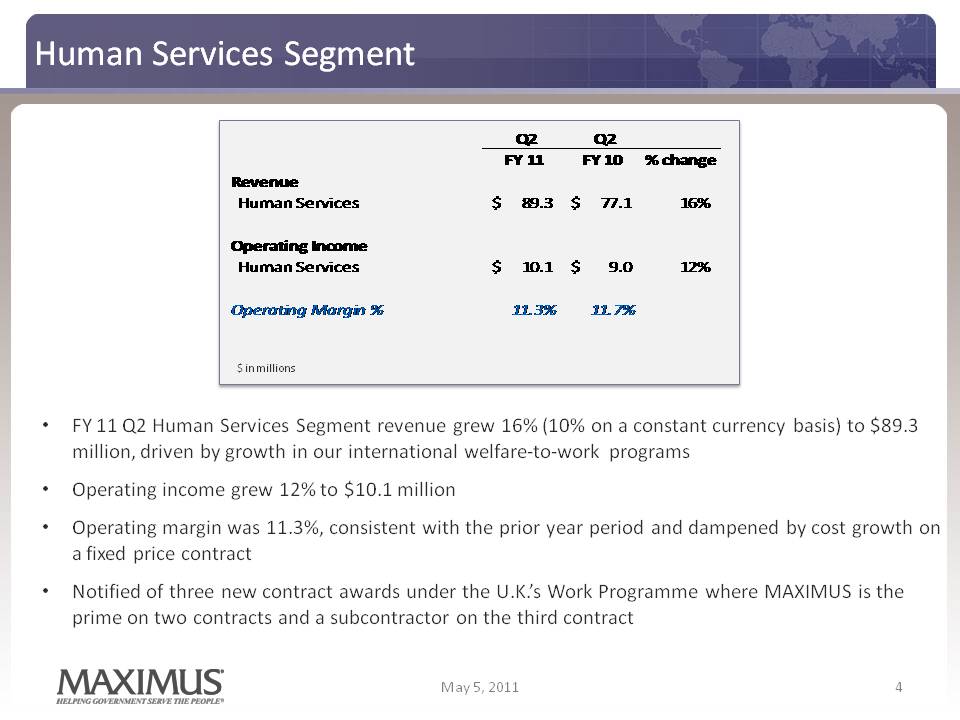

As previously discussed, quarterly margin fluctuations are to be expected. Operating margin of 14% compares favorably to the prior year, in part, because the prior year had fluctuated downward. The strong 14% margin in the second quarter is attributable to strong performance, a surge in appeal volumes and favorable timing on certain contracts. Turning to our human services segment, second quarter revenue for the segment grew 16%, or 10% on a constant currency basis. To $89.3 million compared to the same period last year.

As expected, growth was driven by our international welfare-to-work programs. Segment operating income grew 12%, to $10.1 million compared to the second quarter of last year. Second quarter operating margin was consistent with the prior year, at 11.3%, but was dampened by a cost growth on a fixed contract.

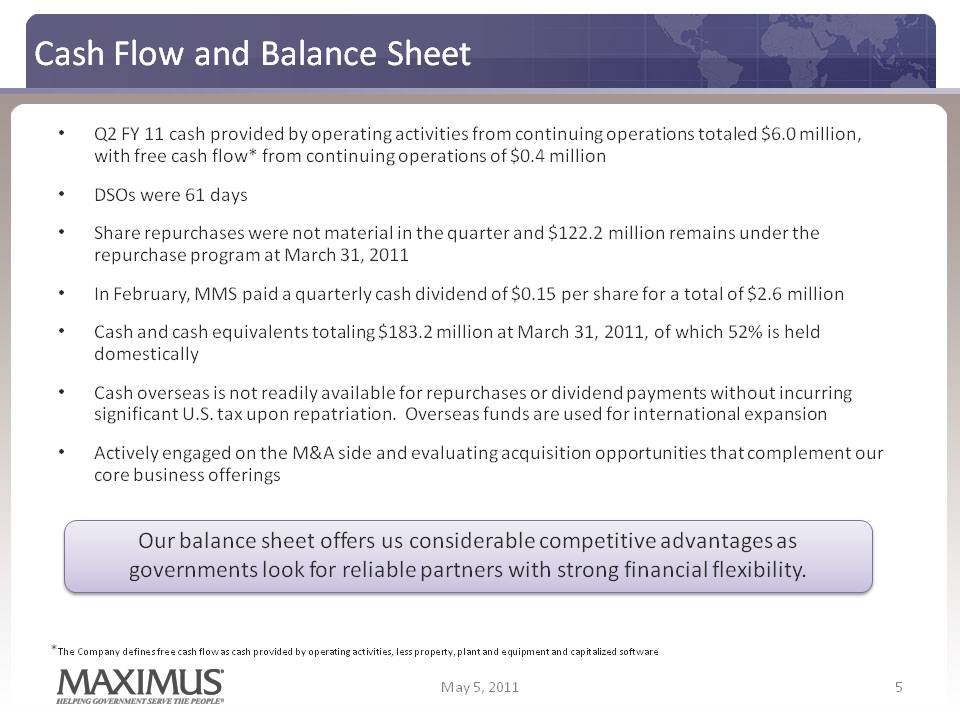

During the quarter we were notified of award on three new contracts under the United Kingdoms work program. Two as a prime and one as a sub-contractorI'll discuss the financial implications of these contracts in greater detail when I cover guidance. Moving on to cash flow and balance sheet items, cash provided by operating activities from continuing operations for the three months ended March 31st, was $6 million, with free cash flow from continuing operations of $374,000. As expected cash flows were lower compared to last quarter as receivables balances increased to a DSO level of 61 days.

Share repurchases were not material in the quarter and at March 31st, we had $122.2 million available for repurchases under our board authorized program. Also in the quarter, we paid add quarterly cash dividend of $0.15 per share for a total of $2.6 million. This reflects the 25% increase to the dividend that we announced in January. We exited the second quarter with $183.2 million in cash, and cash equivalents of which 52% has held domestically.

It is important to recognize that our international subsidiaries typically generate solid cash flows and that cash is held overseas. These overseas cash balances are not readily available for repurchases or dividend payments without incurring significant U.S. tax upon repatriationThese overseas funds are used for our international expansion. While we remain committed to returning excess capital to shareholders, we are actively engaged on the M&A side, and are evaluating acquisition opportunitiesthat will further compliment our footprint or enhance our core offerings.

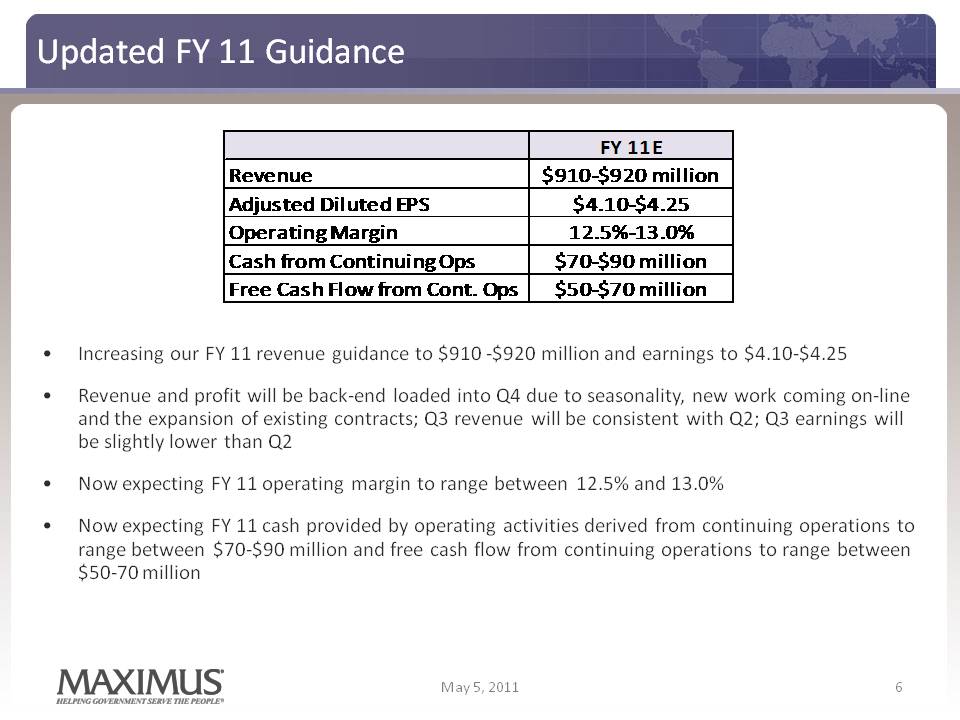

Moving on to guidance. As noted in this morning's press release, we are increasing our fiscal 2011 revenue and earnings guidance. To recap, we now expect revenue in the range of $910 million to $920 million and adjusted diluted EPS from continuing operations to range between $4.10 and $4.25 for fiscal 2011. Both revenue and profit will be back end loaded in the fourth quarter due to seasonality, new work coming on line, and the expansion of existing contracts. So for the third quarter we expect that revenue will be consistent with the second quarter, and earnings will be slightly below our second quarter results. For the full fiscal year, we now expect operating margin to range between 12.5% and 13%.

We are also making a slight adjustment to our fiscal 2011 cash flow guidance, and now expect cash provided by operating activities derived from continuing operations to be in the range of $70 million to $90 million for fiscal 2011. We expect pre-cash flow from continuing operation in the range of $50 million to $70 million. Our revised fiscal 2011 guidance includes the impact from the new UK contracts in this fiscal year. Our UK revenue estimates for fiscal 2011 remain unchanged, and we still expect revenue from the programs in the range of $35 million to $40 million in fiscal 2011. This assumes certain revenue and profit benefits that we expect to realize in the fourth quarter as the current FND program winds down. These benefits will help offset start up costs as the new work program begins in the fourth quarter.

Let's turn our attention to the expected impacts of the UK program on fiscal 2012 and beyond. As a reminder, the three new contracts do not include work in our current encumbered region, as a result we are winding down an accretive, fully ramped revenue stream. At the same time, we will be launching the three new contracts from the ground up. So this means that our revenue run rate for the UK is expected to be approximately 40% lower in fiscal 2012. As a result, we now expect fiscal 2012 revenue from the UK contracts to range between $20 million and $25 million.

As noted in our press release on April 1st, vendor compensation is tied to longer term outcomes and we expect that revenue will ramp over a two year period. This will result in start up, pretax losses, of approximately $9 million to $11 million in fiscal 2012, with the majority of the loss in the first half of the year, and then nearing break even in the fourth quarter of fiscal 2012. The Company routinely expects contract life cycles to impact earnings. Despite the relative size of the UK contract when we blend in the rest of our business portfolio, we still believe that fiscal 2012 is shaping up to be a solid year for Maximus with lots of opportunities within our core markets.

As Rich will talk about in greater detail, the longer term economics of the UK program are compelling. Since our public announcement we have also refined our model for the work program contracts. And we are increasing our financial expectations. We now estimate that the contracts will contribute in excess of $90 million in annual revenue when fully ramped with operating margins north of 15%. The programs are expected to hit their full run rate in the fourth quarter of fiscal 2013. Now, I'll turn the call over to Rich to provide additional details on fiscal 2012, the UK programs, and how the overall business is tracking.

Rich Montoni - Maximus Inc - President, CEO

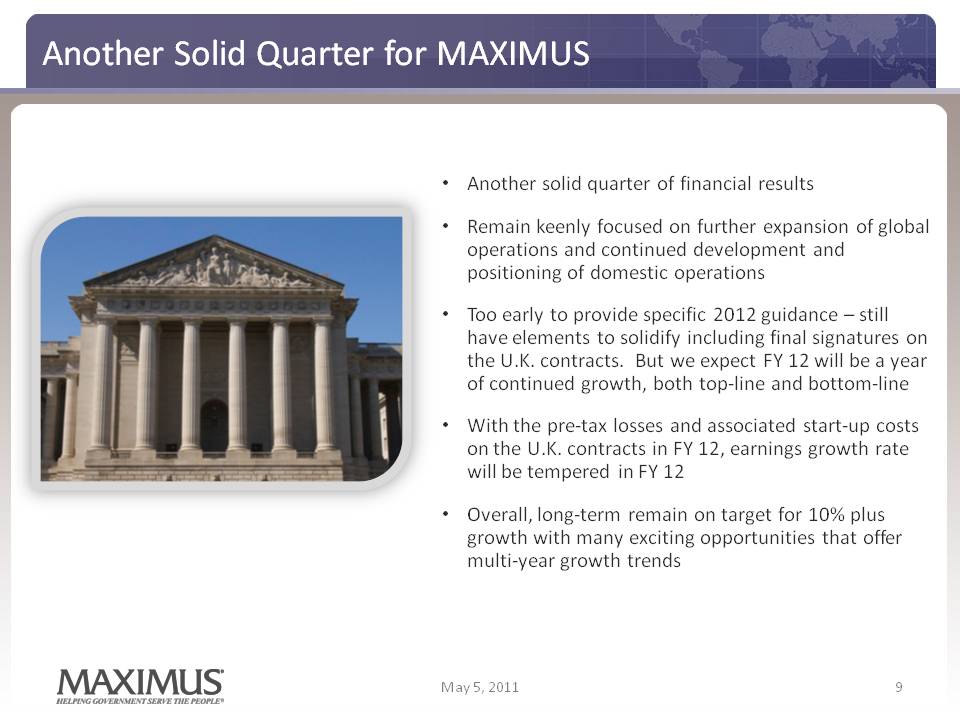

Thanks, David, and good morning everyone. Today Maximus reported another quarter of solid financial results. I am pleased with the progress we've made in the second quarter both operationally and financially. We remain keenly focused on our two primary growth opportunities, further expansion of our global operations and continued development and positioning of our domestic operations as governments seek ways to improve the efficiencies of their health and human services programs.

Let me start where David left off. It is too early to provide specific fiscal 2012 guidance as there are many elements to solidify including final negotiations on the UK contracts. Yet, we believe fiscal 2012 will be a year of continued growth both top line and bottom line. As you know, our long term growth targets are 10% plus both revenue and earnings. This takes into account that some years we will have accelerated growth, like we experienced in fiscal 2010 along with a solid opportunity to deliver in fiscal 2011. While in other years the pace of growth may be slower, mostly driven by procurement cycles.

With a ramp-up of the UK program in fiscal 2012, in the associated start up losses, we believe our earnings growth in fiscal 2012 that that rate will be tempered. But most importantly, overall, our long term 10% plus growth outlook remains on target, and we have a lot of exciting opportunities that will offer multi-year trends for growth. Starting with our international operations. We were recently notified of an award for three welfare-to-work contract in the United Kingdom under the work program. We are very pleased to receive the right balance of awarded territories in pricing terms, which represent an increased presence and a doubling of our current annual run rate in the UK.

I want to address the number of awards we received in related terms. It is important to acknowledge that heavy price discounting played a factor in the selection process. And while some vendors heavily discounted their prices, Maximus offered a price structure that we believe reflects our commitment to prudent, balanced, profitable growth. Most importantly, this sets the table for us to make the necessary investments to deliver the outcomes that will drive the UK government's success of the program. Our model is to deliver the outcomes that matter for a fair return, not the lowest price.

All three contracts were awarded to Maximus and its alliance partner Careers Development Group. Maximus will serve as prime on two of the contracts and CDG will prime the third. Maximus and CDG work collaboratively under the prior FND program, and delivered some of the finest results in the country. This alliance combines the very best expertise in both the private and non-profit sectors. Maximus brings robust international experience in some of the most innovative welfare-to-work programs including those in Australia. At the same time, CDG offers expertise in engaging hard to reach job seekers and brings established relationships with community-based organizations throughout the United Kingdom. Both Maximus and CDG possess enviable track records of moving high volumes of job seekers into long term sustainable employment.

As David noted, the overall economics of these contracts are very favorable to those vendors who can perform over the long haul. Margins for the overall life of the program are expected to be north of 15%, with the possibility to drive additional upside, contingent upon performance and outcome achievement. As we have mentioned in the past, the UK's redesign welfare-to-work model ties provider compensation to job-seeker sustained employment. This model is directly aligned with our core competency of hitting performance requirements on outcomes-based programs.

As the highest rated provider in the United Kingdom, under FND, and a top rated provider in Australia, we are well positioned to help job seekers achieve meaningful employment and economic independence. The additional UK work is only part of our larger land and expand strategy that provides us with a more meaningful platform from which to grow our operations. Our emphasis will remain on balanced profitable growth, where each new opportunity will be subject to the same rigorous criteria for pricing and program scope that we have applied to all our markets. We view every new win as a building block to our strategy. Our experience in Australia is a good example of how we successfully executed the strategy. Our strong track record of delivery there has allowed us to grow revenue 800% since we acquired that business in 2002. Just recently, Maximus gained five new location sites through Australia's performance-based star rating system. The star rating system was established as a means to assess and compare provider outcomes. This flexible model allows the government to shift under-performing welfare-to-work site locations to higher rated vendors. The model incentivises vendors to focus on transitioning people from welfare to sustainable employment. We expect the United Kingdom will implement a similar rating system for vendor performance under the work program. The five new locations represent a couple of million dollars of new annual revenue, a small addition to our Australian book of business, but one that represents our disciplined land and expand approach to growth.

Turning now to our domestic operations, we are very pleased with the recent news from GartnerGartner awarded Maximus the 2011 Business Process Management Program of the year. We also received top honors for delivering innovative BPM solutions, beating out world class industry giants and business process experts. The Gardner award speaks volumes to our efforts to drive innovation, quality, and efficiencies in the government programs by optimizing people, process, and technology. These awards recognize the business process re-engineering disciplines we have implemented in our Texas health operations.

We use data driven analytics to improve overall operations and service delivery, while at the same time offering enhanced data reporting to the client. Our innovation in Texas has a direct impact in winning new work in Colorado and offers us advantages with new opportunities going forward. Our business process management disciplines and best practices can be replicated across other programs to help government clients improve efficiencies and reduce costs. And as you know, states remain constrained by fiscal and budgetary pressures while at the same time, they are facing an increasing demand for services. Many states are employing a variety of levers to reduce cost and manage budgets.

As we have talked about on the last call, many states are actively shifting Medicaid populations from fee-for-service to managed care to help rein in cost. In California, we are enrolling new populations such as seniors and persons with disabilities, commonly referred to as SPD populations, into managed care. And in Texas, we where Medicaid managed care is already mandatory in major metropolitan areas like Dallas, Houston, Austin, and San Antonio, the state is now expanded managed care into the rest of the state including rural Texas. As the existing Medicaid administrative enrollment broker for the state, Maximus will help approximately 980,000 individuals select and enroll into managed care plans. Also, Texas is introducing the Texas dental program, a new managed care program for all clients under age 21. Maximus will assist clients in their selection of dental plans as well.

Over the short term, we expect this volume expansion and additional scope to increase the value of our Medicaid contract in fiscal 2012. And we continue to see healthy pipeline of opportunities as states contemplate new models for helping Medicaid beneficiaries. In addition to managed care expansion, we continue to see forward movement on health care reform. Six states have enacted insurance exchange laws and several other states appear to be making progress on similar legislation. And while the political cross currents remain headline news, we are seeing an increase in activity from the recipients of the early innovator grants. Additionally, as budgets remain under close scrutiny, governments continue to face increased emphasis on accountability, deficit reduction, and expense management. Ultimately, the fundamental need to reduce healthcare costs through broad-based reform, still remains a top priority for everyone on both sides of the aisle.

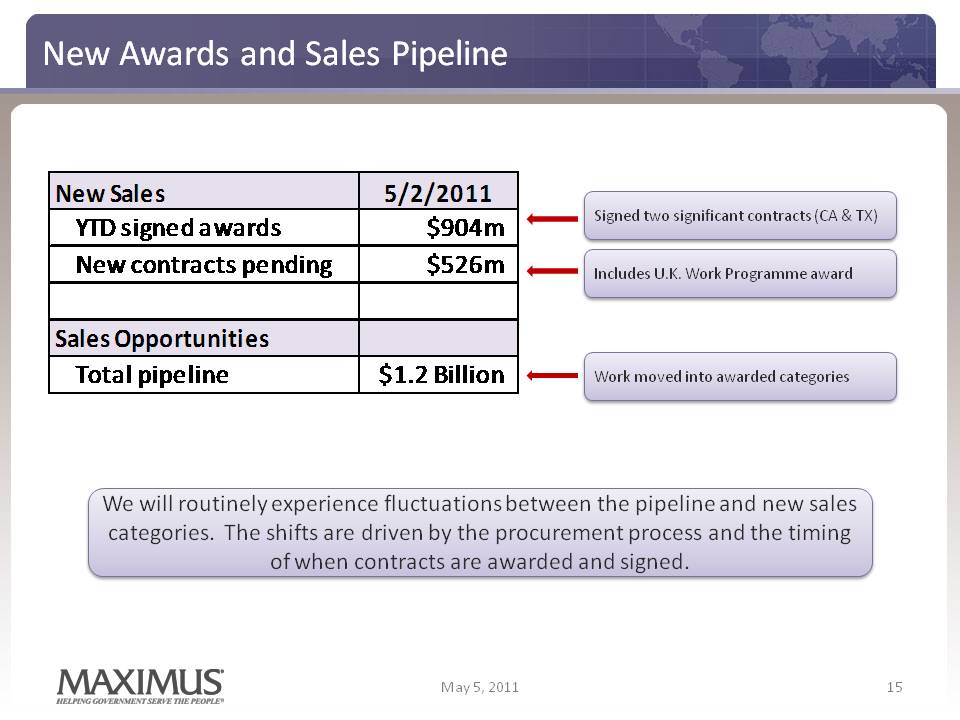

Moving on to new awards and sales pipeline. On May 2nd, our fiscal year to date signed contract wins total $904 million. Compared to $304 million reported last year. The increase in new signed awards includes over $500 million for previously announced rebid awards in California, and Texas. These two contracts alone represent an annualized contract value of approximately $160 million.

New contracts pending or those contracts that are awarded but unsigned, were exceptionally strong in the quarter driven by the award of the United Kingdom contracts. New contracts pending totaled $526 million compared to $470 million last year. Our pipeline of sales opportunities on May 2nd totalled $1.2 billionand this reflects the movement of work into awarded categories. As a reminder, we will routinely experience fluctuations between the sales pipeline and new sales awards driven by the procurement process and the timing of when contracts are awarded and signed.

Looking beyond fiscal 2011, our portfolio of longer-term contracts provides us with a more predictable stream of recurring revenue. Since we have several multi-year programs underway at various stages of maturity and profitability we are able to absorb the diluted impacts of the first year of the UK program and still achieve growth. So even when you consider the ramp-up effects of the new work in the UK, the overall dynamics in our portfolio today set the stage for continued top and bottom line growth in fiscal 2012 and beyond. With consistent solid performance over the last couple of years Maximus stands well positioned to capitalize on the many opportunities in front of us. We have a healthy balance sheet and will continue to return excess cash to our shareholders through our ongoing dividend and repurchase programs.

It's important that we strike a balance for cash deployment as we look forward to our longer term strategic initiatives which may include complimentary acquisitions to expand our offerings or geographic reach. In closing, we generated continued gains in our performance in the second quarter with an increased outlook for fiscal 2011, in anticipated growth into 2012. Our recent UK wins re-enforce our commitment to profitable and long term growth. We are also benefiting from important awards in the domestic healthcare arena that highlight our eligibility in enrollment capabilities, which will be a critical component of any health care reform effort.

Before we turn the call back to the operator, I would like to highlight our upcoming Investor Day on June 29th. This event will feature business and market trends as well as panel discussions with former governors, and health care and welfare reform policy experts. For those who will not be able to join us in New York City on the 29th of June, we will provide a webcast of the day's events on our website. Invitations will be forthcoming.

And with that, let's open it up for questions,

Q U E S T I O N S A N D A N S W E R S

Operator

Thank you. (Operator Instructions). Our first question comes from Torin Eastburn with CJS Securities. Please state your question.

Torin Eastburn - CJS Securities - Analyst

Good morning.

Rich Montoni - Maximus Inc - President, CEO

Good morning, Torin. How are you?

Torin Eastburn - CJS Securities - Analyst

I'm good. My first question is putting aside new business for a second, what are the volume trends like in the existing business that you have now?

Rich Montoni - Maximus Inc - President, CEO

Well, I think from a volume trend perspective I think it is fair to say that we are experiencing increasing volumes. Most notably in our health business, and I think the driver behind that as we talked about on the prepared remarks, Torin. Really is the shift from fee-for-service to managed care. So I think as a general rule we are increasing volumes.

Torin Eastburn - CJS Securities - Analyst

Okay. And my second question you have had three great years of new contract wins and my brain's tendency to (inaudible) revert wondering if that is sustainable. On the other hand, obviously you have got a big tail wind from health care reform. You have done a great job expanding internationally. How do you view the new contract environment for the next three years as opposed to, say, the last three years?

Rich Montoni - Maximus Inc - President, CEO

Next three years versus the last three years, we actually think -- I have to break it up a little bit in terms of different camps. One would be the domestic camp, and the health side in particular. I think it's from a general perspective, Torin, I think it is fair to say that in the last couple of years we have seen a lot of activity really at the planning level around health care reform, a bit of pause around health care reform as the legislation was being contemplated and formed and enacted. We continue to see a fair amount of states in the planning stage. I think we are seeing more traction with states emerging from the thought stage into the planning stage. I have Bruce Caswell here who runs our health business, Bruce, any comments in that regard?

Bruce Caswell - Maximus Inc - President and General Manager, Health Services Segment

I think that's exactly right, Rich. In fact, we see it kind of a gap developing between those states that are pressing on the accelerator pedal and moving ahead, whether it's through using the planning funds that they were granted, or the establishment, the early innovator grants that have been granted, and those states that for various reasons are holding back. As a consequence, I think it places an emphasis on working with those early innovator states, those pace car states and ensuring that a solution is available to those that are going to need a plan B down the road.

Rich Montoni - Maximus Inc - President, CEO

So when you add all of that up, we had been in a position, if we had this conversation a year ago, we are expecting a fairly significant pause on our domestic health business, awaiting the real rollout of health care reform. If anything, that seems to be moving forward a little bit sooner than we had expected. I think we are getting some traction with those states that feel compelled to be ready for the roll out on January 1st, 2013. But in addition, a bit of a pleasant surprise has been the significance of the trend from managed -- from fee-for-service to managed care, and that's actually driving increased revenues today and most notably expecting a fairly significant increase in 2012 because of that.

Torin Eastburn - CJS Securities - Analyst

Thank you.

Rich Montoni - Maximus Inc - President, CEO

Okay.

Operator

Our next question comes from Bryan Kinstlinger from Sidoti. Please state your question.

Brian Kinstlinger - Sidoti - Analyst

Right, thanks. Hi guys.

Rich Montoni - Maximus Inc - President, CEO

Hi, Brian

Brian Kinstlinger - Sidoti - Analyst

The first question I wanted to ask about was a follow-up on the -- on some of the points you made on the fee-for-service to managed care. You had mentioned that the health appeals, I think in your prepared remarks, were the primary dive for the growth, so my guess is managed care was helping modestly so far. So I guess my real question is when do you expect that transition and the enrollments to really start to have more meaningful of an impact on your numbers?

Rich Montoni - Maximus Inc - President, CEO

Well, first in the form of confirmation, you are correct. And we specifically noted the higher volumes in our federal health appeals business was a key factor in this quarter. I do think generally at this point in time we are getting some modest lift, but we expect increasing lift from this trend fee-for-service to managed care. Bruce Caswell, you can as to this as well. You're the one who handles this book of business day in and day out.

Bruce Caswell - Maximus Inc - President and General Manager, Health Services Segment

Rich, I think you are absolutely right. We are starting to see now as state legislatures have approved these expansions and as we see as kind of negating factors, first the legislature approval, and then the MCO procurement process, and then the actual implementation kicks in. We're starting to see that traction as we turn the corner. I would say Q4 this year, but really mostly in fiscal 2012 that impact will be most felt in the states that we serve.

Brian Kinstlinger - Sidoti - Analyst

Great. And then I'm not sure -- I was in and out, but the eligibility services systems you are putting in, where are we are RFPs from states? I know where we were with California, New York, last quarter you talked about a lot of opportunities. Can you touch on where the RFP states are? Do you have bids in already? Thanks.

Bruce Caswell - Maximus Inc - President and General Manager, Health Services Segment

First I would just -- this is Bruce Caswell. I would say I'd make a distinction between eligibility systems vs.. eligibility support services which is BPO business that we're in.

Brian Kinstlinger - Sidoti - Analyst

Right.

Bruce Caswell - Maximus Inc - President and General Manager, Health Services Segment

We don't actually implement eligibility systems as turnkey systems in the marketplace as you might find other vendors doing. That said, states continue to show great interest in reforming the administrative processes by which they support these populations and we have continued to do presentations and respond to RFIs and we anticipate some RFPs as well forth coming in the market. So it is definitely a vibrant marketplace, particularly given the budgetary challenges that Medicaid officials are facing.

Brian Kinstlinger - Sidoti - Analyst

Great. Can you just talk about the, maybe I missed this too, the tick up in SG&A on the health services side? It seemed abnormally large, just quarter-over-quarter. Is there anything particular there?

Rich Montoni - Maximus Inc - President, CEO

We going to ask Dave Walker to address that, Brian.

David Walker - Maximus Inc - CFO

That's just normal timing and we always tell people to look at the operating income. Our operational people move up to the G&A when they are working a lot of proposals, there's no rhyme or reason on the timing of proposals and that's all it is.

Brian Kinstlinger - Sidoti - Analyst

Okay. And the contract execution last quarter you talked about a troubled contract David, or Rich, sorry, maybe talk about how that's played out this quarter and is that something behind us?

Rich Montoni - Maximus Inc - President, CEO

YesDuring the quarter we saw a cost growth of about $4.2 million that we recorded. We anticipate no future losses on this contract, and on balance we think our risk management program, although we're not risk free, is really working and has allowed us to lever consistent operating income margins.

Brian Kinstlinger - Sidoti - Analyst

So there was still a modest loss on that income this quarter? You said that is going to end? Is that what you're saying?

Rich Montoni - Maximus Inc - President, CEO

We recorded $4.2 million in the quarter.

Brian Kinstlinger - Sidoti - Analyst

$4.2 million, okay.

Rich Montoni - Maximus Inc - President, CEO

And we do not anticipate future losses going forward.

Brian Kinstlinger - Sidoti - Analyst

Okay. The -- I'm curious on your original FND contract, how you expect the delayed revenue from the job placements to play out? Is that identified yet?

Rich Montoni - Maximus Inc - President, CEO

Bryan, it is identified. It's a complicated situation to begin with. But as we transfer off the existing FND contracts and ramp up the new work program contracts obviously the hand offs and the wind downs are very very important. So it is a subject of discussion between the government and all the providers. So the way this is being constructed to work, l'll give you a little bit of a walk through so you can understand the different moving pieces here.

First off, on the new work, we are going to pick up we are going to pick up about 20 sites. We expect we will launch those sites on June 15th. We will be taking referrals at that point in time, and we'll be keying those up for actually face-to-face client engagement towards the end of June. And as you know that's a five year contract, but the outcomes fall -- the tail end will run for a couple of years after the five years. And we're in the process -- our team is in the process of finalizing those locations. Looking for the right sites and negotiating leases etc.

So we are in full-fledged design, ramp up mode as it relates to the new contract, on the prior contract, we are closing down 12 sites. We will keep five to service clients. That contract formally ends on June 30th, but we will continue to service accounts through those five locations in our central operation through December, possibly February, and so there will be a tail during which we expect to receive the outcomes that would have occurred in the normal course, even post June 30th.

Brian Kinstlinger - Sidoti - Analyst

So that will help partially offset the losses in early fiscal 2012 it sounds like? Not by a huge amount but a little bit?

Rich Montoni - Maximus Inc - President, CEO

Actually, the way it plays out I think it is a bigger factor in the fourth quarter ended September 30th, 2011. And that obviously is factored into our guidance, the revised guidance we shared with you today.

Brian Kinstlinger - Sidoti - Analyst

Got it. And then I do want to touch before I go on Australia. And how it relates to the UK. It's great to hear you have added five new sites. How often are they going to re-evaluate now with this system, is there a big re-evaluation coming? I thought it was every year.

And then when we look at the UK, it seems you're sharing market share from Australia, without naming any particular names are you stealing share or any of the vendors losing share, the three major ones on the UK program that won so much work? Are they the ones that are losing share, if so maybe why?

Rich Montoni - Maximus Inc - President, CEO

I think that the Australian program which we admire, we think it's just a world class program and is really a great program, I think they do a great job to balance what they pay in the outcomes that are important to the government to the people. And it is a model that very much focuses on rebalancing the work, and reallocating the work from those vendors whose are not delivering the outcomes and assigning it to those that are delivering the outcomes. So the whole model itself is based upon a shifting in market share.

I don't think it's so regimented that this occurs -- this rebalancing occurs religiously every month or three months or year, it's the government's discretion, but over the past year, I think that the -- years, they have routinely reallocated work, and that's the real reason that Maximus has grown its Australian business to the size that it is today. So -- and I do think it's been to the demise of those vendors who take a different approach, including some of those that were awarded a fair amount of work in the United Kingdom, so it really sets up a test of the models. We are comfortable with our model, we are comfortable that our value add is that we seek to deliver the out comes that matter to the government, and our primary goal is not to be the lowest cost provider, rather the best outcomes provider.

Brian Kinstlinger - Sidoti - Analyst

One last question, sorry. On the dividend side, was the piece where you mentioned where your cash is sitting, a message that you don't plan to increase your dividend given where the cash sits? I guess I'm just wondering given your strong cash flow, more than adequate to obviously pay much higher dividends. So I guess I'm curious, is that the message you're sending?

Rich Montoni - Maximus Inc - President, CEO

No, not at all. That's not the message. We thought it would be helpful data for our shareholders and interested parties to understand a little bit more about our cash and the cash situation. But it is not intended to be a message that we do not intend to consider increasing in our dividend.

Brian Kinstlinger - Sidoti - Analyst

Great, thanks so much.

Rich Montoni - Maximus Inc - President, CEO

You bet. Thank you.

Operator

Thank you. Just a reminder if you would like to ask a question at this time, please press star one on your telephone keypad. We will pause for a couple moments and poll for questions. Thank you. Ladies and gentlemen, there are no questions at this time. This concludes today's conference. All parties may now disconnect. Have a great day, thank you.

D I S C L A I M E R

Thomson Reuters reserves the right to make changes to documents, content, or other information on this web site without obligation to notify any person of such changes. In the conference calls upon which Event Transcripts are based, companies may make projections or other forward-looking statements regarding a variety of items. Such forward-looking statements are based upon current expectations and involve risks and uncertainties. Actual results may differ materially from those stated in any forward-looking statement based on a number of important factors and risks, which are more specifically identified in the companies' most recent SEC filings. Although the companies may indicate and believe that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate or incorrect and, therefore, there can be no assurance that the results contemplated in the forward-looking statements will be realized.

THE INFORMATION CONTAINED IN EVENT TRANSCRIPTS IS A TEXTUAL REPRESENTATION OF THE APPLICABLE COMPANY'S CONFERENCE CALL AND WHILE EFFORTS ARE MADE TO PROVIDE AN ACCURATE TRANSCRIPTION, THERE MAY BE MATERIAL ERRORS, OMISSIONS, OR INACCURACIES IN THE REPORTING OF THE SUBSTANCE OF THE CONFERENCE CALLS. IN NO WAY DOES THOMSON REUTERS OR THE APPLICABLE COMPANY ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED ON THIS WEB SITE OR IN ANY EVENT TRANSCRIPT. USERS ARE ADVISED TO REVIEW THE APPLICABLE COMPANY'S CONFERENCE CALL ITSELF AND THE APPLICABLE COMPANY'S SEC FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISIONS.

©2011, Thomson Reuters. All Rights Reserved. 3981363-2011-05-06T07:

David N. Walker Chief Financial Officer and Treasurer Second Quarter – Fiscal Year 2011May 5, 2011 A number of statements being made today will be forward-looking in nature. Such statements are only predictions and actual events or results may differ materially as a result of risks we face, including those discussed in our SEC filings. We encourage you to review the summary of these risks in Exhibit 99.1 to our most recent Form 10-K filed with the SEC. The Company does not assume any obligation to revise or update these forward-looking statements to reflect subsequent events or circumstances.

Selected Financial Results from Continuing Operations Record FY 11 Q2 RevenueQ2 revenue grew 11% to $227.1 million, driven by solid delivery in both segments and across geographiesStrong performance resulted in operating margin of 13.0%Income & EarningsIncome from continuing operations, net of taxes, increased to $19.0 millionAdjusted diluted EPS from continuing operations increased 39% to $1.07 compared to $0.77 last yearOther Placeholder: May 5, 2011 * Pro forma adjustments: Q2 FY 10 was normalized to exclude $0.21 of legal recovery and $0.02 of tax rate adjustments

Health Services Segment FY 11 Q2 Health Services Segment revenue grew 8% to $137.8 million, driven primarily by organic growth and higher-than-normal volumes in the federal health appeals businessOperating income grew to $19.4 millionStrong performance, the surge in appeals volumes and favorable timing on certain contracts resulted in an operating margin of 14.0% May 5, 2011 (Gp:) $ in millions

Human Services Segment FY 11 Q2 Human Services Segment revenue grew 16% (10% on a constant currency basis) to $89.3 million, driven by growth in our international welfare-to-work programsOperating income grew 12% to $10.1 million Operating margin was 11.3%, consistent with the prior year period and dampened by cost growth on a fixed price contract Notified of three new contract awards under the U.K.’s Work Programme where MAXIMUS is the prime on two contracts and a subcontractor on the third contractOther May 5, 2011 (Gp:) $ in millions

Cash Flow and Balance Sheet Q2 FY 11 cash provided by operating activities from continuing operations totaled $6.0 million, with free cash flow* from continuing operations of $0.4 millionDSOs were 61 daysShare repurchases were not material in the quarter and $122.2 million remains under the repurchase program at March 31, 2011In February, MMS paid a quarterly cash dividend of $0.15 per share for a total of $2.6 million Cash and cash equivalents totaling $183.2 million at March 31, 2011, of which 52% is held domesticallyCash overseas is not readily available for repurchases or dividend payments without incurring significant U.S. tax upon repatriation. Overseas funds are used for international expansion Actively engaged on the M&A side and evaluating acquisition opportunities that complement our core business offerings *The Company defines free cash flow as cash provided by operating activities, less property, plant and equipment and capitalized software Our balance sheet offers us considerable competitive advantages as governments look for reliable partners with strong financial flexibility. May 5, 2011

Updated FY 11 Guidance February 2010 Increasing our FY 11 revenue guidance to $910 -$920 million and earnings to $4.10-$4.25Revenue and profit will be back-end loaded into Q4 due to seasonality, new work coming on-line and the expansion of existing contracts; Q3 revenue will be consistent with Q2; Q3 earnings will be slightly lower than Q2Now expecting FY 11 operating margin to range between 12.5% and 13.0%Now expecting FY 11 cash provided by operating activities derived from continuing operations to range between $70-$90 million and free cash flow from continuing operations to range between $50-70 million May 5, 2011

May 5, 2011 Financial Impacts from the new U.K. Contracts Revised fiscal 2011 total Company guidance includes contributions from new U.K. contracts; U.K. revenue estimates for FY 11 remain unchanged at $35-40 millionRevenue and profit benefits from the wind down of FND will offset start-up costs for the Work Programme in Q4 of 2011Fiscal 2012 and long-term implications of U.K. contracts: Three new contracts do not include incumbent region so we are winding down an accretive fully-ramped revenue stream and starting up three new contractsRevenue from U.K. contracts in FY 12 will be approximately 40% lower than in F Y11 Expect revenue of from U.K. contracts to range between $20-25 million in FY 12Vendor compensation tied to longer-term outcomes and expect revenue to ramp over a two-year period, resulting in start-up losses in FY 12 of approximately $9 million to $11 million, pre-tax, with the majority of the loss in the first half of FY 12 and the contracts nearing breakeven by Q4 FY 12Longer-term economics are compelling and we are increasing our long-term financial expectations for the U.K. contracts. Once fully ramped, expect that they will contribute in excess of $90 million in annual revenue with operating margins north of 15%; programs will hit full run rate in Q4 of FY 13 When we blend the U.K. contracts with the rest of our business portfolio, FY 12 is shaping up to be a solid year for MAXIMUS.

Richard A. Montoni President and Chief Executive Officer Second Quarter – Fiscal Year 2011May 5, 2011

Another solid quarter of financial resultsRemain keenly focused on further expansion of global operations and continued development and positioning of domestic operationsToo early to provide specific 2012 guidance – still have elements to solidify including final signatures on the U.K. contracts. But we expect FY 12 will be a year of continued growth, both top-line and bottom-lineWith the pre-tax losses and associated start-up costs on the U.K. contracts in FY 12, earnings growth rate will be tempered in FY 12Overall, long-term remain on target for 10% plus growth with many exciting opportunities that offer multi-year growth trends May 5, 2011 Another Solid Quarter for MAXIMUS

United Kingdom’s Work Programme Update Awarded three contracts under the U.K.’s Work ProgrammeWhile many vendors heavily discounted prices, MAXIMUS offered a price structure that reflects commitment to prudent, balanced, profitable growth; the awards are the right balance of awarded territories and pricing termsMAXIMUS will serve as prime contractor on two contracts and Careers Development Group (CDG) will prime the thirdMAXIMUS-CDG alliance combines the best of private and non-profit sectors; CDG offers expertise in engaging hard-to-reach jobseekers and relationships with local community-based organizationsOverall economics of the contracts are favorable to vendors who perform over the long-haul; program model aligned with our core competency of hitting outcome-based performance requirements Both MAXIMUS and CDG possess enviable track records of moving high volumes of jobseekers into long-term, sustainable employment. May 5, 2011

U.K. work part of larger “land and expand” strategy that provides more meaningful platform for balanced, profitable growthExperience in Australia demonstrates our successfully execution of this strategy; since the acquisition in 2002, revenue has grown 800%Recently gained five location sites as a result of Star Rating system where the Australian government shifts under-performing welfare-to-work sites to higher-rated vendorsExpect the U.K. will implement a similar rating system to incentivize vendors to focus on transitioning people from welfare to sustainable employment May 5, 2011 A Proven “Land and Expand” Model

Gartner Names MAXIMUS BPM Program of the Year Gartner awarded MAXIMUS the 2011 Business Process Management Program of the Year and top honors for Delivering Innovative BPM SolutionsDriving innovation, quality and efficiencies into government programs by optimizing people, process and technologyThe award recognizes the business process reengineering disciplines, including data-driven analytics and reporting to improve overall operations and service delivery, we implemented in our Texas Health operationsThese disciplines and best practices helped us win new work in Colorado and can be replicated across other programs to help states improve efficiencies and reduce costs May 5, 2011

States Shift to Medicaid Managed Care Many states actively shifting Medicaid populations from fee-for-service to managed care as a way to rein in costsIn California, we are enrolling seniors and persons with disabilities (SPD populations) into Medicaid managed care plansIn Texas, mandatory Medicaid managed care is moving beyond major cities and into rural regions where MMS will help 980,000 individuals select and enroll into plansTexas also introducing a new managed care dental program for all Medicaid clients under 21In the short-term, the additional volume and scope from these two initiatives will increase the value of our TX Medicaid contract in FY 12 May 5, 2011

May 5, 2011 Health Care Reform Update We continue to see forward movement on health care reformSix states have enacted health insurance exchange laws and several states appear to be making progress on similar legislationIncrease in activity from the recipients of the “Early Innovator” grantsPolitical cross-currents continue to make headline news, but budgets remain under close scrutiny and governments face emphasis on accountability, deficient reduction and expense managementReducing health care costs through broad-based reform still remains a top priority for both parties

New Awards and Sales Pipeline May 5, 2011 (Gp:) Signed two significant contracts (CA & TX) We will routinely experience fluctuations between the pipeline and new sales categories. The shifts are driven by the procurement process and the timing of when contracts are awarded and signed. (Gp:) Work moved into awarded categories (Gp:) Includes U.K. Work Programme award

Conclusion Portfolio of longer-term contracts provides a more predictable stream of recurring revenueWith several multi-year programs at different stages of maturity and profitability, we can absorb the dilutive impacts of the first year of the new U.K. program and still growThe overall dynamics in our portfolio today set the stage for continued top- and bottom-line growth in FY 12 and beyondWe maintain a healthy balance sheet and continue to return excess cash to shareholders and look forward to longer-term strategic initiatives, which may include acquisitionsWe generated continued gains in our financial and operational performance, both domestically and internationally, with an increased outlook for FY 11 and anticipated growth in FY 12Recent wins reinforce our commitment to profitable growth With consistent, solid performance over the last couple of years, MAXIMUS stands well-positioned to capitalize on the many opportunities in front of us. May 5, 2011 MAXIMUS Investor Day June 29th in New York City; Invitations forthcoming