Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - MAXIMUS, INC. | a2195568zex-32_1.htm |

| EX-32.2 - EXHIBIT 32.2 - MAXIMUS, INC. | a2195568zex-32_2.htm |

| EX-31.2 - EXHIBIT 31.2 - MAXIMUS, INC. | a2195568zex-31_2.htm |

| EX-23.1 - EXHIBIT 23.1 - MAXIMUS, INC. | a2195568zex-23_1.htm |

| EX-99.1 - EXHIBIT 99.1 - MAXIMUS, INC. | a2195568zex-99_1.htm |

| EX-21.1 - EXHIBIT 21.1 - MAXIMUS, INC. | a2195568zex-21_1.htm |

| EX-31.1 - EXHIBIT 31.1 - MAXIMUS, INC. | a2195568zex-31_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2009

Commission file number: 1-12997

MAXIMUS, INC.

(Exact name of registrant as specified in its charter)

| VIRGINIA (State or other jurisdiction of incorporation or organization) |

54-1000588 (I.R.S. Employer Identification No.) |

|

11419 Sunset Hills Road, Reston, Virginia (Address of principal executive offices) |

20190 (Zip Code) |

Registrant's telephone number, including area code: (703) 251-8500

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, no par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of outstanding voting stock held by non-affiliates of the registrant as of March 31, 2009 was $687,368,720 based on the last reported sale price of the registrant's Common Stock on The New York Stock Exchange as of the close of business on that day.

There were 17,653,436 shares of the registrant's Common Stock outstanding as of October 30, 2009.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive Proxy Statement for its 2010 Annual Meeting of Shareholders to be held on March 18, 2010, which definitive Proxy Statement will be filed with the Securities and Exchange Commission not later than 120 days after the end of the registrant's fiscal year, are incorporated by reference into Part III of this Form 10-K.

MAXIMUS, Inc.

Form 10-K

September 30, 2009

Table of Contents

2

General

We provide operations program management and consulting services focused in the areas of health and human services primarily for government-sponsored programs such as Medicaid and the Children's Health Insurance Program (CHIP). Founded in 1975, we are one of the largest pure-play health and human services provider to government in the United States and are at the forefront of innovation in meeting our mission of Helping Government Serve the People®. We use our expertise, experience, and advanced technological solutions to help government agencies run more efficient and cost-effective programs, while improving the quality of services provided to program beneficiaries. We operate in the United States, Australia, Canada, the United Kingdom, and Israel. We have held contracts with government agencies in all 50 states in the U.S.

Over the last five years, our core health and human services business has continued to expand. This growth was offset by isolated program challenges, which have since been largely resolved. Fiscal 2007 results were impacted by a $25.2 million loss on the Texas Integrated Eligibility project where MAXIMUS served as a subcontractor to Accenture to provide services to the Texas Health and Human Services Commissions (TX HHSC). In February 2007, we terminated our subcontract with Accenture. In March 2007, TX HHSC terminated its contract with Accenture and contracted directly with us to provide support services for its CHIP and Medicaid programs. We continue to provide services under these programs, but on a profitable basis. In 2008, TX HHSC, Accenture and MAXIMUS settled all claims relating to those programs. In connection with that settlement, MAXIMUS paid a total of $40.0 million and agreed to provide services, valued at an additional $10.0 million, to TX HHSC over the next five years.

Our core health and human services business has benefited from steady demand over the last five years. In fiscal 2008 and fiscal 2009, many states experienced budgetary challenges; however, we have not experienced any material change in demand. Legislation such as the Deficit Reduction Act of 2005, Medicare Improvements for Patients and Providers Act (MIPPA), the American Recovery and Reinvestment Act (ARRA), the Reauthorization of the Children's Health Insurance Program (CHIP) in 2009, The Flexible New Deal in the United Kingdom, and the recent expansion of the Australian Human Service program has kept demand levels high. We believe that demand for our services is reasonably insulated since we provide domestic state and federal clients with administrative services for critical programs including Medicaid, Medicare, and CHIP, and, abroad, we administer several international government-sponsored health and human services programs. We believe we remain well positioned to benefit from pending initiatives related to health care reform, as well as increasing demand from domestic and international government clients who are dealing with increasing caseloads in government-run health and human service programs. Nevertheless, protracted fiscal pressures could adversely impact our business.

In fiscal 2009, MAXIMUS committed to the divesture of the non-strategic ERP business unit. This is in addition to five business units divested in fiscal 2008. These divestitures are designed to enable the Company to better focus on our core health and human services business portfolio where we are the leading pure-play provider in the administration of government health and human services programs.

For the fiscal year ended September 30, 2009, we had revenue from continuing operations of $717.3 million and net income of $46.5 million.

Market Overview

Our primary customers are government agencies. In fiscal 2009, approximately 66% of our total revenue was derived from state government agencies whose programs received significant federal

3

funding, 17% from foreign government agencies, 9% from U.S.-based federal government agencies, and 8% from other sources (such as commercial customers).

We believe we are well positioned to benefit from demand for operations program management and consulting services in an environment where governments are required to maintain or improve services to an increasing number of constituents.

We believe governments will continue to review current program operations and seek improved operating capability and cost savings through the use of partnering and managed services. For example, many states are in the process of considering changes to how they administer government-sponsored programs and implementing legislative changes such as the reauthorization of CHIP. Additionally, states are seeking new ways to find cost savings by implementing new systems and business process reengineering. Much of our work in the United States is related to federally mandated and federally funded programs such as Medicaid, CHIP, and Temporary Assistance to Needy Families (TANF). International governments are also grappling with many of the same social issues related to the delivery of cost effective health and human services programs and, as a result, they are turning to managed services providers such as MAXIMUS to provide repeatable process and proven solutions. Overall, we expect the underlying demand for our existing programs to increase due to the fundamental need for governments worldwide to provide these services to program recipients.

We deliver valued-added services to government agencies by providing operations program management and consulting services that help governments operate more efficiently and effectively. Demand for our services is contingent upon factors that affect government spending and drive demand for our services, including:

- •

- The requirement of state governments that are running federally mandated and federally funded programs to efficiently and

cost-effectively meet minimum federal requirements to maintain federal funding levels.

- •

- The requirement of state governments to implement federal initiatives, such the reauthorization of the Children's Health

Insurance Program in 2009, which increases federal matching dollars to states with the goal to increase participants over the next five years from seven million to 11 million children.

- •

- The need for governments to operate more programs with the same level of resources. We believe that clients may seek

additional partnering or managed services options to manage increasing demand for government-funded programs and will seek providers that offer greater flexibility in balancing resources

(e.g. workforce) with demand.

- •

- The impact of continued budgetary pressures on governments and the need for most states to maintain balanced budgets.

These budgetary requirements increase the desire by governments to seek and maximize federal funding to which they are entitled.

- •

- The need to improve business processes and update technology as governments face the possibility of an increasing number of workers eligible for retirement. It is estimated that over the next five years, one-fifth of state and local government managers, and one-third of the federal government's full-time permanent workforce will be eligible for retirement.

As a result, governments utilize outside companies, such as MAXIMUS, that possess the knowledge and resources to efficiently operate federally funded programs and maintain minimum federal requirements to achieve maximum efficiency and ongoing federal funding.

4

Our Business Segments

During the last three fiscal years, our revenues by segment were as follows (in thousands):

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | |||||||

Operations |

$ | 507,486 | $ | 629,226 | $ | 659,204 | ||||

Consulting |

$ | 75,534 | $ | 64,437 | $ | 58,095 | ||||

Total |

$ | 583,020 | $ | 693,663 | $ | 717,299 | ||||

The following discussion describes our business segments and each of our operating divisions within the business segments as they existed on September 30, 2009. From time to time, we implement certain organizational or management changes that realign our internal infrastructure and enable us to manage our business better.

Operations Segment:

Our Operations Segment generated 92% of our total revenue in fiscal 2009. Financial information with respect to this segment is provided in Notes 16 and 17 of our consolidated financial statements (See Item 8 below). The Operations Segment provides a variety of program management and operations support services for state, federal, national, and county funded public programs, and focuses on the delivery of administrative services for government health and human services programs, including: Medicare, Medicaid, CHIP, TANF and related workforce services programs, and child support enforcement programs. Our Operations Segment provides these services through the following support organizations:

Child Support. Child Support provides managed services, consulting, and system support services to state and local agencies. These services include full and specialized child support case management services, call center operations, and program and systems consulting services. Child Support engages with child support enforcement agencies to locate non-custodial parents, establish paternity and support orders, and enforce payments to families. This operation also provides Supplemental Security Income advocacy services for children in foster care, as well as Title IV-E, which sets forth standards for federal payments for foster care, TANF, and adoption assistance eligibility services. Child Support develops, implements, and operates full-service child care programs and associated systems.

Federal Operations. Federal Operations contracts with federal agencies to support health, human services, and justice programs. Our federal operations group provides independent appeals of health insurance denials for government health plan enrollees and providers for Medicare Parts A, B (South), C, and D, the U.S. Office of Personnel Management Federal Employees Health Benefits Plan, the Department of Defense TRICARE program, and over 30 state health insurance regulatory agencies. Federal Operations provides quality of care services including protected medical peer review, evaluation of medical malpractice claims, quality of care standards definition and screening, provider facility review, quality assurance plan review, and health data monitoring. They also provide financial investigations and compliance oversight for the U.S. Department of Justice, which includes monitoring of federally seized businesses to ensure compliance with court-ordered monitoring requirements for the U.S. Marshals Service and conducting a wide range of forensic and investigative services for the Drug Enforcement Agency. In addition, MAXIMUS Federal partners with the Social Security Administration to serve individuals with disabilities through the Ticket to Work and Self-Sufficiency Program.

Health Services. Health Services provides a range of administrative support for publicly funded health services and health insurance programs, with a particular emphasis on eligibility and enrollment for state programs such as Medicaid Managed Care and CHIP. Health Services also operates one of the largest health claims processing systems in Canada, administering British Columbia's medical and drug

5

insurance plans. Under these public health programs, the Division provides the following services: beneficiary outreach and education, application assistance, eligibility support services, enrollment counseling, program data collection and reporting, and premium collection and processing. The Division delivers these services through customized automated information systems; design and development of print and web-based program educational materials; and full-service multi-contact customer service centers that include on-site multilingual assistance. Through the MAXIMUS Center for Health Literacy (CHL), Health Services also develops easy-to-read print materials and easy-to-use websites, and provides adapted translations to help individuals with educational, cultural, or linguistic barriers understand and use important information related to government health programs.

Workforce Services. Workforce Services manages government workforce-centered service programs in the United States, Australia, the United Kingdom, and Israel. Workforce Services helps disadvantaged individuals transition from government assistance programs to employment and economic independence by providing comprehensive services, including eligibility determination, case management, job-readiness preparation and search, job development and employer outreach, job retention and career advancement, and selected educational and training services. We also provide advocacy service for youth and disabled persons in the United States and rehabilitation services in Australia. Additionally, Workforce Services provides employers with tax credit and electronic I-9 management services, which are fully compliant with U.S. Department of Homeland Security guidelines and integrated with the U.S. Citizenship and Immigration Services E-Verify program.

Consulting Segment:

Our Consulting Segment generated 8% of our total revenue in fiscal 2009. Financial information with respect to this segment is provided in Notes 16 and 17 of our consolidated financial statements (See Item 8 below). The Consulting Segment provides management and financial consulting services for state and local clients, focusing on services that both directly support health and welfare and improve program operations, performance, and integrity. The Segment serves to create business opportunities for our core Operations Segment by providing the government market with a consulting option for improving program operations, performance and integrity. The Consulting Segment provides services, which oftentimes complement our Operations Segment services, through the following practice areas:

Program Performance Services. Program Performance Services helps clients analyze and optimize their business operations. Our services and solutions focus on the health and human services marketplace, including optimizing the eligibility and enrollment process and call center design for government-run programs such as CHIP and designing and creating outreach and education materials, client advocacy programs, human capital management strategies, program analytics, quality assurance processes and practices, as well as client portals. This practice area provides cost allocation advisory services, user fee program design and implementation, activity-based cost accounting and related financial services.

Program and Systems Integrity Services. Program and Systems Integrity Services helps government organizations plan and monitor large-scale program and technology systems initiatives including planning, funding, procuring, and implementing information systems. Program and Systems Integrity Services also provides standards-based project management, quality assurance and independent verification and validation services for government programs such as Medicaid, child welfare, child support, unemployment compensation, eligibility/TANF and WIC/EBT.

Educational Services. Educational Services provides a unique set of innovative management tools and professional consulting services for all levels of the educational system. Education Services offers K-12 special education case management solutions including our TIENET® software application, which helps schools manage special education instruction, assessment and intervention. The application includes Individualized Educational Programs (IEPs) to ensure compliance with federal and state laws

6

including the No Child Left Behind Act of 2001 (NCLB). The Division also offers AutismPro®, a Web-based solution that helps schools drive positive outcomes for special education students, and provides higher education consulting services that help institutions plan, manage and secure federal funding and grants for research and other sponsored programs.

Competitive Advantages

We offer a private sector alternative for the administration and management of critical government-funded programs as well as offering consulting services. Our reputation and extensive experience over the last 30 years give us a competitive advantage as governments value the level of expertise and brand recognition that MAXIMUS brings to its customers. The following are the competitive advantages that allow us to capitalize on various market opportunities:

Single-market focus. We are one of the largest publicly traded companies whose primary focus is offering a portfolio of operations program management and consulting services specifically to government customers. This single-market concentration allows us to dedicate time and resources fully in providing quality, customized solutions to government customers. Our extensive experience and detailed understanding of the regulation and operation of government programs allow us to apply our methodologies, skills, and solutions to new projects in a cost-effective and timely fashion. We believe our government program expertise differentiates us from other firms and non-profit organizations with limited resources and skill sets, as well as from large consulting firms that serve multiple industries but lack the focus necessary to manage the complexities of pursuing opportunities and serving government agencies efficiently.

Financial strength. We maintain a strong balance sheet, generate consistent annual cash flow and do not have any long-term debt. Many government clients have become concerned with the financial wherewithal of their vendors. We possess sufficient cash on-hand to support client operations including ongoing technology investments and start up operations. Clients are more comfortable engaging with vendors who have financial flexibility to support their needs, especially those related to high-profile public health and human services programs.

Focused portfolio of services. Customers seek a continuum of service capabilities from component services to full-service solutions in their health and human services programs. Engagements often require creative or complex solutions and we are able to draw upon our health and human services subject matter experts within our organization. Our focused range of capabilities, as described in the "Our Business Segments" discussion above, enables us to better pursue new business opportunities and positions us as a single-source provider of health and human services program management and consulting services to government agencies.

Established international presence. International governments are seeking to expand government-sponsored health and human services programs as demand for social services continues to rise and governments seek to contain costs. We have an established presence in Australia, Canada, the United Kingdom, and Israel as one of the preeminent providers in certain core health and human services programs including workforce services and health insurance enrollment operations. Our established presence and proven solutions have contributed to our success in competing for new contracts internationally.

Proven track record and exceptional brand recognition. Since 1975, we have successfully and profitably assisted governments by offering efficient, cost-effective solutions. We have provided hundreds of large-scale program management operations for government agencies, many of which we continue to run today, serving millions of beneficiaries. The successful execution of these projects has improved the quality of services provided to program beneficiaries, which has enhanced our brand

7

recognition with government agencies. Our proven records of accomplishment and exceptional brand recognition have contributed significantly to our ability to compete successfully and win new contracts.

Expertise in competitive bidding. Government agencies typically award contracts to third-party providers through a comprehensive, complex and competitive bidding process. With over 30 years of experience responding to Requests for Proposals (RFPs) and executing oral presentations, we have the necessary experience to navigate these government procurement processes. The complex nature of competitive bidding creates significant barriers to entry for potential new competitors unfamiliar with the nature of government procurement. We possess the expertise and experience to assess and allocate the appropriate resources necessary for successful project completion in accordance with contractual terms. Our proposals demonstrate our ability to meet all customer requirements at a price that is both attractive to the customer and profitable to MAXIMUS. Given the reluctance of government agencies to award contracts to unproven companies, we believe that our expertise in the competitive bidding process has contributed significantly to our success.

Intellectual property that supports the administration of government programs. We have software products that enhance our operations program management offerings. Further, our ability to focus our subject matter experts to aid in the support and enhancement of our product offerings provides advantages over pure service providers who are dependent on third-party software.

MAXIMUS develops proprietary case management solutions to support our health and human services business lines. By leveraging a common framework, MAXIMUS can shorten our development lifecycle, and possibly eliminate it, to enable configuration for accelerated takeover of operations, providing clients with a significant amount of flexibility and support. By taking advantage of a large number of shared technical and business components, we can reduce development costs and deliver clients increased capabilities and efficiencies related to workflow, calendaring, and action plan management. We have deployed these proven product solutions across several health and human services projects for clients such as Pennsylvania, New York, and the United Kingdom.

Competition

The market for providing our services to government agencies is competitive and subject to rapid change. Our Consulting Segment typically competes against large global consulting firms, as well as smaller niche players. Our Operations Segment, which primarily serves health and human services departments and agencies, competes for program management contracts with the government services divisions of large organizations, such as Affiliated Computer Services, Inc., EDS, an HP Company, and International Business Machines Corporation, as well as more specialized private service providers, and local non-profit organizations, such as the United Way of America, Goodwill Industries, and Catholic Charities USA.

Business Growth Strategy

Our goal is to enable future growth by remaining a leading provider of operations program management and consulting services to government agencies. The key components of our business growth strategy include the following:

- •

- Pursue new domestic and international business opportunities and expand customer

base. With over 30 years of business expertise in the government market, we continue to be a leader in developing innovative solutions to meet the evolving needs of

government agencies. We will continue to seek to grow our domestic and international base business by leveraging our existing core capabilities and pursuing opportunities with new and current clients.

- •

- Grow long-term, recurring revenue streams. We seek to enter into long-term relationships with clients to meet their ongoing and long-term business objectives. As a result, long-term contracts

8

- •

- Pursue strategic acquisitions. We will selectively

identify and pursue strategic acquisition opportunities. Acquisitions can provide us with a rapid, cost-effective method to enhance our services, obtain additional skill sets, expand our

customer base, cross-sell additional services, enhance our technical capabilities, and establish or expand our geographic presence.

- •

- Continue to optimize our current operations. MAXIMUS

continues to seek efficiencies and optimize operations. Over the last several years, we have moved away from a volume-driven sales approach towards a tighter focus on risk management and project

execution, resulting in improved profitability from continuing operations. We enhanced our contracts and compliance team and initiated organization-wide training requirements to facilitate

project improvements and efficiencies. We continue to evaluate new business as well as the current portfolio of projects in a manner that is more aligned with increasing our overall profitability and

not driven by volume sales.

- •

- Recruit and retain highly skilled professionals. We

continually strive to recruit motivated individuals including top managers from larger organizations, former government officials, and consultants experienced in our service areas. We believe we can

continue to attract and retain experienced personnel by capitalizing on our single-market focus and our reputation as a premier government services provider.

- •

- Focus on core offerings and selectively divest non-strategic business lines. Our fundamental strategy is to be the leading provider of health and human services offerings principally to government clients. During 2008 and 2009, management has divested or committed to divest a total of six non-strategic business units. We believe this tighter focus better positions us to benefit from increasing demand for the administration of government health and human services programs as a result of emerging legislative initiatives both domestically and abroad as well as the overall economic environment. We believe this will drive scalable, long-term future growth.

(three to five years with additional option years) are often the preferred method of delivery for customers and are also beneficial to the Company.

See Exhibit 99.1 of this Annual Report on Form 10-K under the caption "Special Considerations and Risk Factors" for information on risks and uncertainties that could affect our business growth strategy.

Marketing and Sales

We generate new business opportunities by establishing and maintaining relationships with key government officials, policy makers and decision makers to understand the evolving needs of government agencies as they seek to optimize their programs. We have a team of business development professionals who ensure that we understand the needs, requirements, legislative initiatives, and priorities of our current and prospective customers. In conjunction with our subject matter experts and marketing consultants, our business development professionals create and identify new business opportunities and ensure that we proactively introduce our solutions and services early in the procurement cycle. We also subscribe to government procurement databases that track government bid activity and make every effort to ensure that we are on bidders' lists as well as approved vendor lists for government procurement offices. We participate in professional associations of government administrators and industry seminars featuring presentations by our executives and employees. Senior executives also develop leads through on-site presentations to decision-makers.

For the year ended September 30, 2009, we derived approximately 11% and 18% of our consolidated revenue from contracts with the States of California and Texas, respectively, principally within our Operations Segment.

9

Legislative Initiatives

During the last several years, federal and state legislative initiatives created new growth opportunities and potential markets for MAXIMUS. Legislation passed in Congress has large public policy implications for state and local government and presents viable business opportunities, notably in the health and human services arena. MAXIMUS is well positioned to meet the operations program management and consulting needs resulting from legislative actions and subsequent regulatory efforts. MAXIMUS is actively monitoring these initiatives to respond to opportunities that develop.

Some recent federal legislative initiatives that have created new growth opportunities for us in the government market include the following:

Medicare Improvements for Patients and Providers Act (MIPPA). Enacted in July 15, 2008, MIPPA made several changes to the Medicare program, including improvements to the low-income assistance provisions of the Part D prescription drug program. We analyzed the bill and provisions for any impact on MAXIMUS business and potential opportunities arising from the bill. In particular, new funding is provided in Section 119 for an information clearing house and technical assistance and training to improve services to low-income Medicare beneficiaries.

Children's Health Insurance Program Reauthorization Act (CHIPRA). CHIPRA was signed into law on February 2, 2009, extending the previous SCHIP program. This bill extended federal support for CHIP through 2013, while adding an additional $44 billion between 2009 and 2013 to the baseline funding of $5 billion a year. By expanding state options to find and enroll students through "express lane eligibility" and "auto-enrollment," CHIPRA has presented MAXIMUS with an opportunity to expand our partnerships with states administering CHIP programs.

American Recovery and Reinvestment Act of 2009 (ARRA). ARRA provides states with a 6.2% increase in the Federal Medical Assistance Percentage (FMAP) for fiscal years 2009 through 2011, with states with the highest unemployment rates receiving a higher percentage increase. The passage of this bill has both preserved and expanded Medicaid potential business for MAXIMUS. ARRA also created a new Temporary Assistance for Needy Families (TANF) Emergency Fund of $5 billion available to states, territories, and tribes for federal fiscal years 2009 and 2010 that experience a rise in TANF caseloads.

Health Reform Legislation. Health reform legislation is pending and has a variety of provisions that have the potential to increase MAXIMUS business. The four areas that present business opportunities are: eligibility determination for subsidies, enrollment brokers for plans in the exchange, increased appeals work, and, as Medicaid will likely expand, the bill may provide the opportunity for MAXIMUS to increase its Medicaid work.

President's Emergency Plan for AIDS Relief (PEPFAR). PEPFAR authorizes $48 billion to combat Global HIV/AIDS, tuberculosis and malaria. This legislation responds to the President's call to expand the U.S. Government's commitment to this successful program for five additional years, from 2009 through 2013. We continue to monitor the PEPFAR program and Congressional appropriations and pursue business opportunities for MAXIMUS in assisting governments in strengthening their health systems and developing their capacity to address the HIV/AIDS epidemic.

The Flexible New Deal (FND) The FND is a government-sponsored program designed to provide skills, support, and employment assistance to job seekers in the United Kingdom. In October of 2009, the FND replaced the New Deal employment programs in England, Scotland, and Wales under phase one of the program. Under the FND, unemployed program participants receive 12 months of allowance and job search assistance and, after the initial 12 month period, are passed on to private and non-profit contractors with payment based on the number of participants receiving job placement.

10

Deficit Reduction Act of 2005 (DRA). Enacted in the spring of 2006, the DRA reauthorized the TANF program of 1996 and provides states with additional flexibility to make reforms to their Medicaid Programs. This legislation touches upon a number of key health and human service issues important to the MAXIMUS base business. In reauthorizing TANF, the DRA requires states to engage more TANF cases in productive activities leading to self-sufficiency. The law recalibrates a caseload reduction credit, increases childcare funding, retains maintenance of level of effort and promotes healthy marriage and responsible fatherhood initiatives. States are also required to establish and maintain work participation and verification procedures with new penalties of one to five percent for failure to comply. The DRA allows states to change their Medicaid benefit packages to mirror certain commercial insurance packages (termed alternative or benchmark packages) and allows states to vary the premiums and cost sharing they charge and gives them the option to require payment of alternative premiums as a condition of eligibility. These provisions, and many others in the DRA, are central to the MAXIMUS health and human service experience base in our Operations and Consulting segments. The new requirements of the TANF program will create certain new challenges for states and localities, which in turn provide opportunities for companies like MAXIMUS. Additionally, the flexibility and encouragement offered in the DRA to innovate state Medicaid programs should be a catalyst for new operations and consulting opportunities.

Backlog

Backlog represents an estimate of the remaining future revenue from existing signed contracts and revenue from contracts that have been awarded, but not yet signed. Our backlog estimate includes revenue expected under the current terms of executed contracts and revenue from contracts in which the scope and duration of the services required are not definite but estimable (such as performance-based contracts), but does not assume any contract renewals.

Changes in backlog result from additions to future revenue from the execution of new contracts or extension or renewal of existing contracts, reductions from fulfilling contracts, reductions from the early termination of contracts and adjustments to estimates of previously-included contracts. Our contracts typically contain provisions permitting government customers to terminate the contract on short notice, with or without cause. We believe that period-to-period backlog comparisons are difficult and do not necessarily accurately reflect future revenue we may receive. The actual timing of revenue receipts, if any, on projects included in backlog could change for any of the aforementioned reasons. The dollar amount by segment of our backlog as of September 30, 2008 and 2009, were as follows:

| |

As of September 30, |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

2008 | 2009 | ||||||

| |

(In millions) |

|||||||

Operations |

$ | 1,162 | $ | 1,702 | ||||

Consulting |

138 | 98 | ||||||

Total |

$ | 1,300 | $ | 1,800 | ||||

Of the $1.8 billion balance outstanding at September 30, 2009, the Company anticipate recognizing approximately 41% of this total during fiscal 2010. Management also estimates that approximately 93% of forecasted fiscal 2010 revenue is in the form of backlog and option periods. Option periods are not included in the backlog calculation.

Seasonal Nature of Business

We may experience seasonality in our Operations Segment in our fourth fiscal quarter as a result of tax credit work. In addition, the summer and winter holiday vacations can impact the financial

11

results for all of our segments. Specifically, reductions in working days due to holidays and vacations may impact our sales and accounts receivable, primarily in our first fiscal quarter.

Employees

As of September 30, 2009, we had 6,594 employees, consisting of 6,204 employees in the Operations Segment, 201 employees in the Consulting Segment and 189 corporate administrative employees. Our success depends in large part on attracting, retaining, and motivating talented, innovative, and experienced professionals at all levels.

As of September 30, 2009, 389 of our employees in Canada were covered under three different collective bargaining agreements, each of which has different components and requirements. There are 219 employees covered by the MAXIMUS BC Health Benefits Operations, Inc. collective bargaining agreement with the British Columbia Government and Services Employees' Union ("BCGEU"). Within Themis Program Management and Consulting Limited, we have two agreements. Under the first agreement, 159 employees are covered by a collective bargaining agreement with the BCGEU and, under the second agreement, 11 employees are covered by a collective bargaining agreement with the Professional Employees Association ("PEA"). These collective bargaining agreements expire on March 31, 2010.

As of September 30, 2009, 746 of our employees in Australia were covered under a Collective Agreement, which is similar in form to a collective bargaining agreement. The Collective Agreement is renewed annually.

None of our other employees are covered under any such agreement. We consider our relations with our employees to be good.

Foreign Operations

We currently operate predominantly in the United States. Our revenues derived from operations in foreign countries for fiscal years 2007, 2008 and 2009 were $88.0 million, $121.2 million and $119.1 million, respectively. We had $43.0 million and $57.2 million of long-lived assets located in foreign countries at September 30, 2008 and 2009, respectively.

Website Access to U.S. Securities and Exchange Commission Reports

Our Internet address is http://www.maximus.com and includes access to our corporate governance materials and our code of business conduct and ethics. Through our website, we make available, free of charge, access to all reports filed with the U.S. Securities and Exchange Commission (SEC) including our Annual Reports on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K, Section 16 filings by our officers and directors, as well as amendments to these reports, as filed with or furnished to the SEC pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, after we electronically file such material with, or furnish it to, the SEC. Copies of any materials we file with, or furnish to, the SEC can also be obtained free of charge through the SEC's website at http://www.sec.gov or at the SEC's Public Reference Room at 100 F St., N.E., Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

Our operations are subject to many risks that could adversely affect our future financial condition and performance and, therefore, the market value of our securities. See Exhibit 99.1 of this Annual Report on Form 10-K under the caption "Special Considerations and Risk Factors" for information on

12

risks and uncertainties that could affect our future financial condition and performance. The information in Exhibit 99.1 is incorporated by reference into this Item 1A.

We own a 60,000 square foot office building in Reston, Virginia. We also lease offices for management and administrative functions in connection with the performance of our services. At September 30, 2009, we leased 79 offices in the United States totaling approximately 1,158,000 square feet. In four countries outside the United States, we leased 103 offices containing approximately 368,000 square feet. The lease terms vary from month-to-month to six-year leases and are generally at market rates.

We believe that our properties are maintained in good operating condition and are suitable and adequate for our purposes.

The Company is involved in various legal proceedings, including contract and employment claims, in the ordinary course of its business. The matters reported on below involve significant pending or potential claims against us.

(a) In December 2008, MAXIMUS, Accenture LLP and the Texas Health and Human Services Commission ("HHSC") entered into an agreement settling all claims among the parties arising from a prime contract between Accenture and HHSC for integrated eligibility services and a subcontract between MAXIMUS and Accenture in support of the prime contract. In connection with that settlement, MAXIMUS paid a total of $40.0 million and agreed to provide services to HHSC valued at an additional $10.0 million. The Company's primary insurance carrier paid $12.5 million of the amount due from MAXIMUS. In May 2009, the Company recovered an additional $6.3 million from one of its excess insurance carriers. The Company continues to pursue additional insurance recoveries from its other excess insurance carriers; however, such recoveries are not assured.

(b) In November 2007, MAXIMUS was sued by the State of Connecticut in the Superior Court in the Judicial District of Hartford. MAXIMUS had entered into a contract in 2003 with the Connecticut Department of Information Technology to update the State's criminal justice information system. The State claims that MAXIMUS breached its contract and also alleges negligence and breach of the implied warranty of fitness for a particular purpose. MAXIMUS has sued its primary subcontractor on the effort (ATS Corporation) which abandoned the project before completing its obligations. Although the State did not specify damages in its complaint, it demanded payment of alleged damages of approximately $6.2 million in a letter sent to the Company in September 2007. The Company denies that it breached its contract with the State. The Company cannot predict the outcome of the legal proceedings or any settlement negotiations or the impact they may have on the Company's operating results or financial condition.

(c) In March 2009, a state Medicaid agency asserted a claim against MAXIMUS in the amount of $2.3 million in connection with a contract MAXIMUS had through February 1, 2009 to provide Medicaid administrative claiming services to school districts in the state. MAXIMUS entered into separate agreements with the school districts under which MAXIMUS helped the districts prepare and submit claims to the state Medicaid agency which, in turn, submitted claims for reimbursement to the Federal government. No legal action has been initiated. The state has asserted that its agreement with MAXIMUS requires the Company to reimburse the state for the amounts owed to the Federal government. However, the Company's agreements with the school districts require them to reimburse MAXIMUS for such payments and therefore MAXIMUS believes the school districts are responsible for any amounts disallowed by the state Medicaid agency or the Federal government. Accordingly, the Company believes its exposure in this matter is limited to its fees associated with this work and that the

13

school districts will be responsible for the remainder. During the second quarter of fiscal 2009,MAXIMUS recorded a $0.7 million reduction of revenue reflecting the fees it earned under the contract in the accompanying condensed consolidated statements of operations. No additional charges have been recorded since then. MAXIMUS has exited the Federal healthcare claiming business and no longer provides the services at issue in this matter.

(d) In July 2009 the District of Columbia ("District") initiated a civil action against MAXIMUS in the Superior Court of the District of Columbia, Civil Division. The District alleged violations of the District's False Claims Act ("Act"), fraud and unjust enrichment arising from the Company's preparation and submission of federal Medicaid reimbursement claims on behalf of the District. The District was seeking treble its actual damages plus a penalty of $10,000 per claim as provided under the Act. MAXIMUS previously settled a Federal investigation and related whistleblower lawsuit concerning these same activities in 2007. In connection with that settlement, MAXIMUS entered into a two-year Deferred Prosecution Agreement ("DPA"), a five-year Corporate Integrity Agreement ("CIA") and paid a settlement of $30.5 million. The DPA has since expired by its terms and the CIA has been suspended in light of the Company's exit from the Federal health care claiming business. The District was, in fact, a named party in the prior whistleblower lawsuit that was dismissed with prejudice, and MAXIMUS believes that the District's claims are barred. In October 2009, the District voluntarily dismissed the lawsuit without prejudice.

14

ITEM 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock trades on the New York Stock Exchange under the symbol "MMS." The following table sets forth, for the fiscal periods indicated, the range of high and low sales prices for our common stock and the cash dividends per share declared on the common stock.

| |

Price Range | |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | Dividends | ||||||||

Year Ended September 30, 2008: |

|||||||||||

First Quarter |

$ | 48.33 | $ | 37.05 | $ | 0.10 | |||||

Second Quarter |

38.91 | 33.76 | 0.10 | ||||||||

Third Quarter |

39.09 | 34.49 | 0.10 | ||||||||

Fourth Quarter |

38.59 | 32.82 | 0.10 | ||||||||

Year Ended September 30, 2009: |

|||||||||||

First Quarter |

$ | 37.02 | $ | 25.94 | $ | 0.10 | |||||

Second Quarter |

40.93 | 32.78 | 0.12 | ||||||||

Third Quarter |

43.61 | 37.27 | 0.12 | ||||||||

Fourth Quarter |

48.49 | 39.10 | 0.12 | ||||||||

As of October 30, 2009, there were 76 holders of record of our outstanding common stock. The number of holders of record is not representative of the number of beneficial owners due to the fact that many shares are held by depositories, brokers, or nominees. We estimate there are approximately 9,984 beneficial owners of our common stock.

We declared quarterly cash dividends on our common stock at the rate of $0.10 per share beginning with the quarter ended March 31, 2005, increasing the rate to $0.12 per share beginning with the period ended March 31, 2009. We expect to continue our policy of paying regular cash dividends, although there is no assurance as to future dividends. Future cash dividends, if any, will be paid at the discretion of our Board of Directors and will depend, among other things, upon our future operations and earnings, capital requirements and surplus, general financial condition, contractual restrictions and such other factors as our Board of Directors may deem relevant.

15

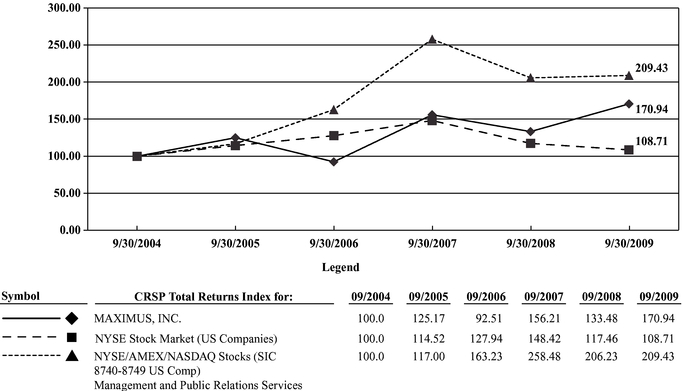

The following graph compares the cumulative total shareholder return on our common stock for the five-year period from September 30, 2004 to September 30, 2009, with the cumulative total return for the NYSE Stock Market (U.S. Companies) Index and the NYSE/AMEX/NASDAQ Stocks (SIC 8740-8749 U.S. Companies) Management and Public Relations Services Index. This graph assumes the investment of $100 on September 30, 2004 in our common stock, the NYSE Stock Market (U.S. Companies) Index and the NYSE/AMEX/NASDAQ Stocks (SIC 8740-8749 U.S. Companies) Management and Public Relations Services Index and assumes dividends are reinvested.

Comparison of Five—Year Cumulative Total Returns

Performance Graph for

MAXIMUS, INC.

Notes:

- A.

- The

lines represent index levels derived from compounded daily returns that include all dividends.

- B.

- The

indexes are reweighted daily, using the market capitalization on the previous trading day.

- C.

- If

the monthly interval, based on the fiscal year-end, is not a trading day, the preceding trading day is used.

- D.

- The index level for all series was set to $100.0 on 09/30/2004.

Prepared by Zacks Investment Research, Inc. Copyright 1960-2009 CRSP Center for Research in Security Prices, Graduate School of Business, University of Chicago. Used with permission. All rights reserved.

16

ITEM 6. Selected Financial Data.

We have derived the selected consolidated financial data presented below, as adjusted for discontinued operations, from our consolidated financial statements and the related notes. The revenue and operating results related to the acquisition of companies using the purchase accounting method are included from the respective acquisition dates. The selected financial data should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" included as Item 7 of this Annual Report on Form 10-K and with the Consolidated Financial Statements and related Notes included as Item 8 of this Annual Report on Form 10-K. The historical results set forth in this Item 6 are not necessarily indicative of the results of operations to be expected in the future.

| |

Year Ended September 30, | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2005 | 2006(1) | 2007 | 2008(2) | 2009 | ||||||||||||

| |

(In thousands, except per share data) |

||||||||||||||||

Statement of Operations Data: |

|||||||||||||||||

Revenue |

$ | 491,295 | $ | 557,974 | $ | 583,020 | $ | 693,663 | $ | 717,299 | |||||||

Legal and settlement expense (recovery), net(3) |

7,000 | 9,394 | 44,438 | 38,358 | (4,271 | ) | |||||||||||

Write-off of deferred contract costs(4) |

— | 17,109 | — | — | — | ||||||||||||

Gain on sale of building(5) |

— | — | — | 3,938 | — | ||||||||||||

Operating income (loss) from continuing operations |

31,199 | (13,590 | ) | (7,048 | ) | 46,616 | 89,815 | ||||||||||

Income (loss) from continuing operations |

20,898 | (4,052 | ) | (10,893 | ) | 29,818 | 54,583 | ||||||||||

Income (loss) from discontinued operations |

15,171 | 6,512 | 2,638 | (23,141 | ) | (8,043 | ) | ||||||||||

Net income (loss) |

36,069 | 2,460 | (8,255 | ) | 6,677 | 46,540 | |||||||||||

Basic Earnings (loss) per share: |

|||||||||||||||||

Income (loss) from continuing operations |

$ | 0.98 | $ | (0.19 | ) | $ | (0.50 | ) | $ | 1.56 | $ | 3.11 | |||||

Income (loss) from discontinued operations |

$ | 0.71 | $ | 0.30 | $ | 0.12 | $ | (1.21 | ) | $ | (0.46 | ) | |||||

Basic earnings (loss) per share |

$ | 1.69 | $ | 0.11 | $ | (0.38 | ) | $ | 0.35 | $ | 2.65 | ||||||

Diluted Earnings (loss) per share: |

|||||||||||||||||

Income (loss) from continuing operations |

$ | 0.97 | $ | (0.19 | ) | $ | (0.50 | ) | $ | 1.54 | $ | 3.05 | |||||

Income (loss) from discontinued operations |

$ | 0.70 | $ | 0.30 | $ | 0.12 | $ | (1.19 | ) | $ | (0.45 | ) | |||||

Diluted earnings (loss) per share |

$ | 1.67 | $ | 0.11 | $ | (0.38 | ) | $ | 0.35 | $ | 2.60 | ||||||

Weighted average shares outstanding: |

|||||||||||||||||

Basic |

21,331 | 21,465 | 21,870 | 19,060 | 17,570 | ||||||||||||

Diluted |

21,653 | 21,465 | 21,870 | 19,305 | 17,886 | ||||||||||||

Cash dividends per share of common stock |

$ | 0.30 | $ | 0.40 | $ | 0.40 | $ | 0.40 | $ | 0.46 | |||||||

17

| |

At September 30, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2005 | 2006 | 2007 | 2008 | 2009 | |||||||||||

| |

(In thousands) |

|||||||||||||||

Balance Sheet Data: |

||||||||||||||||

Cash, cash equivalents, and marketable securities |

$ | 178,363 | $ | 156,860 | $ | 196,682 | $ | 119,605 | $ | 87,815 | ||||||

Working capital |

246,595 | 254,811 | 267,145 | 149,966 | 164,646 | |||||||||||

Total assets |

534,562 | 558,501 | 564,464 | 454,954 | 433,234 | |||||||||||

Total capital lease obligations, less current portion |

3,606 | 2,044 | 417 | — | — | |||||||||||

Total shareholders' equity |

405,954 | 404,899 | 409,400 | 275,706 | 297,128 | |||||||||||

- (1)

- During

fiscal year 2005, the Company valued stock option grants using the intrinsic value at date of grant. For fiscal years 2006 and following, stock

option grants were valued based upon the fair value using a Black-Scholes model. At October 1, 2005, options which had previously been granted but had not vested were revalued based upon their

grant date fair value and the fair value related to the remaining vesting period was expensed over the remaining vesting period of the options. The results for 2005 and prior periods were not restated

to reflect this change in accounting policy.

- (2)

- Since

October 1, 2007, the Company has accounted for uncertain tax positions by recognizing the financial statement effects of a tax position only

when, based upon the technical merits, it is "more-likely-than-not" that the position will be sustained upon examination. See "Note 12. Income Taxes" to our

consolidated financial statements.

- (3)

- Legal

and settlement expense (recovery), net consists of costs, net of reimbursed insurance claims, related to significant legal settlements and

non-routine legal matters, including future probable legal costs estimated to be incurred in connection with those matters. Legal expenses incurred in the ordinary course of business are

included in selling, general and administrative expense. See "Note 20. Legal and Settlement Expense (Recovery), Net" to our consolidated financial statements for additional information.

- (4)

- During

the quarter ended June 30, 2006, we determined that the estimated undiscounted cash flows associated with the Texas Integrated Eligibility

project over its remaining term were insufficient to recover the project's deferred contract costs. As a result, we recognized a non-cash impairment charge of $17.1 million to write

off the full unamortized balance of the project's deferred contract costs. The write-off is included in the results of the Operations Segment. Additional information regarding the Texas

Integrated Eligibility project is disclosed in "Note 19. Texas Integrated Eligibility Project" to our consolidated financial statements.

- (5)

- During the quarter ended June 30, 2008, the Company sold a 21,000 square foot administrative building in McLean, Virginia and recognized a pre-tax gain on the sale of $3.9 million. This gain has been classified as a gain on sale of building in the consolidated statement of operations. See "Note 22. Sale of Building" to our consolidated financial statements for additional information.

18

ITEM 7. Management's Discussion and Analysis of Financial Condition and Results of Operation.

The following discussion and analysis of financial condition and results of operations is provided to enhance the understanding of, and should be read in conjunction with, our Consolidated Financial Statements and the related Notes.

Forward-Looking Statements

Included in this Annual Report on Form 10-K are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on current expectations, estimates, forecasts and projections about our company, the industry in which we operate and other matters, as well as management's beliefs and assumptions and other statements that are not historical facts. Words such as "anticipate," "believe," "could," "expect," "estimate," "intend," "may," "opportunity," "plan," "potential," "project," "should," and "will" and similar expressions are intended to identify forward-looking statements and convey uncertainty of future events or outcomes. These statements are not guarantees and involve risks, uncertainties and assumptions that are difficult to predict. Actual outcomes and results may differ materially from such forward-looking statements due to a number of factors, including without limitation, the factors set forth in Exhibit 99.1 of this Annual Report on Form 10-K under the caption "Special Considerations and Risk Factors." As a result of these and other factors, our past financial performance should not be relied on as an indication of future performance. Additionally, we caution investors not to place undue reliance on any forward-looking statements as these statements speak only as of the date when made. We undertake no obligation to publicly update or revise any forward-looking statements, whether resulting from new information, future events or otherwise.

Business Overview

We provide operations program management and consulting services focused in the areas of health and human services primarily for government-sponsored programs such as Medicaid and the Children's Health Insurance Program (CHIP). Founded in 1975, we are the largest pure-play health and human services provider to government in the United States and are at the forefront of innovation in meeting our mission of Helping Government Serve the People®. We use our expertise, experience and advanced technological solutions to help government agencies run more efficient and cost-effective programs, while improving the quality of services provided to program beneficiaries. We operate in the United States, Australia, Canada, the United Kingdom, and Israel. We have held contracts with government agencies in all 50 states in the U.S.

For the fiscal year ended September 30, 2009, we had revenue of $717.3 million and net income of $46.5 million.

We report each of our two lines of business (i.e., Operations and Consulting) as separate external reporting segments. See Note 17 to our consolidated financial statements for our unaudited quarterly segment income statement data.

19

Results of Operations

Consolidated

The following table sets forth, for the fiscal year ends indicated, selected statements of operations data:

| |

Year ended September 30, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | ||||||||

| |

(dollars in thousands, except per share data) |

||||||||||

Revenue |

$ | 583,020 | $ | 693,663 | $ | 717,299 | |||||

Gross profit |

$ | 134,869 | $ | 189,022 | $ | 192,267 | |||||

Selling, general and administrative expense |

$ | 97,930 | $ | 107,986 | $ | 106,723 | |||||

Selling, general and administrative expense as a percentage of revenue |

16.8 | % | 15.6 | % | 14.9 | % | |||||

Legal and settlement expense (recovery), net |

$ | 44,438 | $ | 38,358 | $ | (4,271 | ) | ||||

Gain on sale of building |

$ | — | $ | 3,938 | $ | — | |||||

Gain on sale of business |

451 | — | — | ||||||||

Operating income (loss) from continuing operations |

$ | (7,048 | ) | $ | 46,616 | $ | 89,815 | ||||

Operating margin (loss) from continuing operations percentage |

(1.2 | )% | 6.7 | % | 12.5 | % | |||||

Income (loss) from discontinued operations, net of income taxes |

$ | 2,638 | $ | (23,141 | ) | $ | (8,043 | ) | |||

Net income (loss) |

$ | (8,255 | ) | $ | 6,677 | $ | 46,540 | ||||

Basic Earnings (loss) per share: |

|||||||||||

Income (loss) from continuing operations |

$ | (0.50 | ) | $ | 1.56 | $ | 3.11 | ||||

Income (loss) from discontinued operations |

$ | 0.12 | $ | (1.21 | ) | $ | (0.46 | ) | |||

Basic earnings (loss) per share |

$ | (0.38 | ) | $ | 0.35 | $ | 2.65 | ||||

Diluted Earnings (loss) per share: |

|||||||||||

Income (loss) from continuing operations |

$ | (0.50 | ) | $ | 1.54 | $ | 3.05 | ||||

Income (loss) from discontinued operations |

$ | 0.12 | $ | (1.19 | ) | $ | (0.45 | ) | |||

Diluted earnings (loss) per share |

$ | (0.38 | ) | $ | 0.35 | $ | 2.60 | ||||

We discuss constant currency revenue information to provide a framework for assessing how our business performed excluding the effect of foreign currency fluctuations. To provide this information, revenue from foreign operations is converted to United States dollars using the average exchange rates from 2008. All our foreign operations are in the Operations Segment.

Revenue increased 3.4%, and increased 6.5% on a constant currency basis, in fiscal 2009 compared with fiscal 2008. The adverse impact of a strong United States Dollar on foreign sourced revenue offset strong revenue growth in our domestic health services division, federal operations and international workforce operations, as well as a full year of operations from the UK subsidiary acquired in fiscal 2008.

Revenue increased 19.0% in fiscal 2008 compared to fiscal 2007. The increase in revenue is attributable to organic growth driven by new work in the Operations Segment and the transformation of the Texas contract to a direct service agreement.

Operating income from continuing operations increased 93% in fiscal 2009, compared to fiscal 2008, from $46.6 million to $89.8 million. The increase of $43.2 is primarily attributable to a $4.3 million legal and settlement recovery in 2009 compared with a charge of $38.4 million in 2008. See the discussion of Legal and Settlement expense below for a breakdown of this balance. In addition, Consulting Segment operating income improved $3.6 million in fiscal 2009 compared to fiscal 2008. Fiscal 2008 benefited from a non-recurring $3.9 million gain on the sale of a property in McLean, Virginia.

Operating income from continuing operations in fiscal 2008 was $46.6 million, compared to an operating loss of $7.0 million in fiscal 2007. The increase in operating income from continuing

20

operations of $53.7 million is primarily attributable to (1) $50.0 million of improved performance in the Operations Segment as a result of the Texas project where we entered into a direct contract agreement with the Texas Health and Human Services Commission, (2) a $6.1 million decrease in legal and settlement expense, (3) a $3.9 million gain on sale of building, offset by (4) a $4.5 million decrease in operating income in the Consulting Segment. Fiscal 2007 also included a $4.2 million loss on the completed Ontario Child Support systems implementation project.

Selling, general and administrative expense (SG&A) consists of costs related to general management, marketing and administration. These costs include salaries, benefits, bid and proposal efforts, travel, recruiting, continuing education, employee training, non-chargeable labor costs, facilities costs, printing, reproduction, communications, equipment depreciation, intangible amortization, legal expenses incurred in the ordinary course of business, and non-cash equity based compensation. SG&A as a percentage of revenue for fiscal years 2007, 2008 and 2009 was 16.8%, 15.6%, and 14.9%, respectively.

Also included in SG&A were $3.8 million, $9.5 million and $7.3 million of non-cash, equity-based compensation related to stock options and RSUs for fiscal years 2007, 2008 and 2009. During the first quarter of fiscal 2008, the Company identified an error in prior periods in recorded stock-based compensation expense related to stock options and RSUs. The error was due, in part, to how the software used by the Company applied estimated forfeiture rates to fully vested stock options and RSUs. The impact was to underestimate stock compensation expense by $1.1 million in each of fiscal 2006 and 2007. The Company corrected this error by recording additional stock compensation expense of $2.2 million in the first quarter of fiscal 2008.

Legal and settlement expense (recovery), net for fiscal years 2007, 2008 and 2009 was $44.4 million, $38.4 million, and ($4.3 million), respectively. Legal and settlement expense consists of costs, net of reimbursed insurance claims, related to significant legal settlements and non-routine legal matters, including future probable legal costs estimated to be incurred in connection with those matters. Legal expenses incurred in the ordinary course of business are included in selling, general and administrative expense. The following table sets forth the matters that represent legal and settlement expense (recovery), net (dollars in thousands):

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | |||||||

Accenture Arbitration, Related Settlement and Insurance Recoveries, Net |

$ | 10,000 | $ | 38,377 | $ | (6,300 | ) | |||

District of Columbia Contract Investigation and Related Settlement |

31,980 | (19 | ) | — | ||||||

Computer Equipment Leases Settlement |

(150 | ) | — | — | ||||||

Ontario Child Support Project Settlement |

2,608 | — | — | |||||||

Other |

— | — | 2,029 | |||||||

Total |

$ | 44,438 | $ | 38,358 | $ | (4,271 | ) | |||

Legal and settlement expense (recovery) net for fiscal 2009 includes a $6.3 million recovery from one of the Company's excess insurance carriers for the Accenture arbitration matter. The Company continues to pursue additional insurance recoveries from its other excess insurance carriers; however, such recoveries are not assured.

Provisions for income taxes in fiscal 2008 and 2009 were 39.2% and 39.3% of income from continuing operations for fiscal 2008 and 2009, respectively. Provision for income taxes for fiscal 2007 was $9.6 million which included:

- •

- a $9.3 million tax benefit related to legal and settlement expenses of $44.4 million (portions of the settlement expense related to the District of Columbia matter are not tax deductible),

21

- •

- a $0.7 million valuation allowance on certain deferred tax assets related to a foreign subsidiary's net operating

losses, and

- •

- a $18.8 million tax provision at 42.0% on income from continuing operations of $43.2 million (loss from continuing operations of $1.2 million offset by legal and settlement expenses of $44.4 million).

Operations Segment

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | |||||||

| |

(dollars in thousands) |

|||||||||

Revenue |

$ | 507,486 | $ | 629,226 | $ | 659,204 | ||||

Gross profit |

102,886 | 163,308 | 169,749 | |||||||

Operating income (loss) |

33,890 | 83,869 | 83,805 | |||||||

Operating margin (loss) percentage |

6.7 | % | 13.3 | % | 12.7 | % | ||||

The Operations Segment includes health services, workforce services, child support, and federal managed services and operations work.

Revenue increased 4.8% in fiscal 2009 compared to fiscal 2008. Revenue in fiscal 2008 included $6.9 million of non-recurring revenue related to hardware and software for a large health project. Normalized for non-recurring revenues and currency fluctuations, revenue increased 9.4% in fiscal 2009 compared to fiscal 2008. This increase was driven by growth in health services, federal operations and international workforce services operations. Operating income in fiscal 2009 was consistent with that in fiscal 2008. Although the Company recorded significant growth in federal and domestic health operations, this growth was offset by the effect of currency fluctuations as well as the start of a new contract which was successfully rebid in 2008. The reduced operating profit margin in 2009 also reflects required upfront investments and lagging revenue recognition related to operating costs for new work in Australia and Shelby County, Tennessee.

Revenue increased 24.0% in fiscal 2008 compared to fiscal 2007. The increase in revenue was primarily driven by new and expanding domestic and international work in our human and health services operations and the transformation of the Texas contract to a direct service agreement. Operating income in fiscal 2008 was $83.9 million, compared to $33.9 million in fiscal 2007. The increase in operating income of $50.0 million was driven by improvements related to the optimization of the business portfolio; new awards; and the resolution of certain legacy contracts, including the transformation of the Texas contract to a direct service agreement.

Consulting Segment

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | |||||||

| |

(dollars in thousands) |

|||||||||

Revenue |

$ | 75,534 | $ | 64,437 | $ | 58,095 | ||||

Gross profit |

31,983 | 25,714 | 22,518 | |||||||

Operating income (loss) |

3,586 | (909 | ) | 2,652 | ||||||

Operating margin percentage |

4.7 | % | (1.4 | )% | 4.6 | % | ||||

The Consulting Segment includes program performance services, program and systems integrity services, and educational services.

Revenues declined from $75.5 million in 2007 to $64.4 million in 2008 and $58.1 million in 2009. Year-over-year revenue declines are principally related to the Company's wind down of its federal healthcare claiming business, which the Company formally exited in fiscal 2009, as well as a general decline in consulting demand. Revenues for 2008 were also adversely affected by a charge of $2.7 million relating to a legacy federal claiming contract and revenues for 2009 benefited from $4.8 million related to hardware sales on a large Educational services project during the year.

22

Operating income was $3.6 million in 2007, a loss of $0.9 million in 2008, and income of $2.7 million in 2009. The overall decline in income relates to the Company's wind down of its federal healthcare claiming work, with 2008 being adversely affected by a charge of $2.7 million relating to a federal healthcare claiming contract.

Interest and Other Income, Net

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | |||||||

| |

(dollars in thousands) |

|||||||||

Interest and other income, net |

$ | 5,804 | $ | 2,423 | $ | 145 | ||||

Percentage of revenue |

0.9 | % | 0.3 | % | 0.0 | % | ||||

The decrease in interest and other income between 2007 and 2009 is primarily attributable to market rates and the use of $150 million of cash and marketable securities as part of the Accelerated Share Repurchase, completed in the first quarter of fiscal 2008, and a further $44.1 million used in additional share repurchases between the fourth quarter of fiscal 2008 and the second quarter of fiscal 2009.

Discontinued Operations

Enterprise Resource Planning (ERP)

In September 2009, the Company committed to a sale of its ERP business. We are actively pursuing a buyer and expect to complete this sale by the end of the 2010 fiscal year. The Company has recorded a loss of $1.3 million during 2009 relating to the long-term fixed assets and goodwill relating to this business.

In fiscal 2008, this division also recorded a loss of $7.6 million relating to goodwill. In fiscal 2009, the division recorded a charge of $14.3 million attributable to a fixed-price ERP contract. These charges are included in losses from discontinued operations.

Security Solutions

On April 30, 2008, the Company sold its Security Solutions division for cash proceeds of $4.6 million, net of transaction costs of $0.4 million, and recognized a pre-tax gain on the sale of $2.9 million.

Unison MAXIMUS, Inc.

On May 2, 2008, the Company sold its Unison MAXIMUS, Inc. subsidiary for proceeds of $6.5 million. The sale transaction is structured as a sale of stock to the current management team of the subsidiary. The sale price of $6.5 million consists of $0.1 million in cash and $6.4 million in the form of a promissory note secured by (1) a security interest in all of the assets of the former subsidiary; (2) a pledge of shares by the buyer; and (3) a personal guaranty by members of the current management team who are shareholders of the buyer. The Company has deferred recognition of a pre-tax gain on the sale of $3.9 million, and interest income on the promissory note, until realization is more fully assured. The deferred gain and deferred interest of $4.6 million is reflected as a deduction from the note receivable on the consolidated balance sheet as of September 30, 2009.

Justice Solutions, Education Systems and Asset Solutions

On September 30, 2008, the Company sold its Justice Solutions, Education Systems, and Asset Solutions divisions, which were previously reported as part of its Systems Segment. At that time, the Company recognized a pre-tax loss of $12.2 million, subject to adjustment for purchase price adjustments and estimated transaction costs. During fiscal 2009, the Company reached a final settlement with the purchaser, resulting in a pre-tax gain of $0.7 million.

23

The following table summarizes the operating results of the discontinued operations included in the Consolidated Statements of Operations (in thousands):

| |

Year Ended September 30, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2007 | 2008 | 2009 | ||||||||

Revenue |

$ | 155,626 | $ | 137,002 | $ | 32,202 | |||||

Income (loss) from operations before income taxes |

$ | 4,362 | $ | (28,920 | ) | $ | (10,704 | ) | |||

Provision (benefit) for income taxes |

1,724 | (11,414 | ) | (4,228 | ) | ||||||

Income (loss) from discontinued operations |

$ | 2,638 | $ | (17,506 | ) | $ | (6,476 | ) | |||

Loss on disposal before income taxes |

$ | — | $ | (9,314 | ) | $ | (686 | ) | |||

Provision (benefit) for income taxes |

— | (3,679 | ) | 881 | |||||||

Loss on disposal |

$ | — | $ | (5,635 | ) | $ | (1,567 | ) | |||

Income (loss) from discontinued operations |

$ | 2,638 | $ | (23,141 | ) | $ | (8,043 | ) | |||

Quarterly Results