Attached files

| file | filename |

|---|---|

| EX-21 - Blue Earth, Inc. | blue_ex21.htm |

| EX-4.1 - Blue Earth, Inc. | blue_ex4-1.htm |

| EX-31.1 - Blue Earth, Inc. | blue_ex31-1.htm |

| EX-32.1 - Blue Earth, Inc. | blue_ex32-1.htm |

| EX-10.9 - Blue Earth, Inc. | blue_ex10-9.htm |

| EX-10.33 - Blue Earth, Inc. | blue_ex10-33.htm |

| EX-10.28 - Blue Earth, Inc. | blue_ex10-28.htm |

| EX-10.39 - Blue Earth, Inc. | blue_ex10-39.htm |

| EX-10.34 - Blue Earth, Inc. | blue_ex10-34.htm |

| EX-10.31 - Blue Earth, Inc. | blue_ex10-31.htm |

| EX-10.35 - Blue Earth, Inc. | blue_ex10-35.htm |

| EX-10.30 - Blue Earth, Inc. | blue_ex10-30.htm |

| EX-10.32 - Blue Earth, Inc. | blue_ex10-32.htm |

| EX-10.29 - Blue Earth, Inc. | blue_ex10-29.htm |

| EX-10.19 - Blue Earth, Inc. | blue_ex10-19.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

(Mark One)

|

||

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended December 31, 2010

OR

|

[ ]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _______ to _______

Commission file number 333-148346

BLUE EARTH, INC.

(Exact Name of Registrant as specified in its charter)

|

Nevada

|

8700

|

98-0531496

|

||

|

(State or other jurisdiction

of incorporation or organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification No.)

|

2298 Horizon Ridge Parkway, Suite 205

Henderson, NV 89052

Telephone: 702-608-5476

Telecopier: 866-314-5824

(Address and telephone number of principal executive offices)

Dr. Johnny R. Thomas, CEO

Blue Earth, Inc.

2298 Horizon Ridge Parkway, Suite 205

Henderson, NV 89052

Telephone: 702-263-1808

Telecopier: 702-263-1824

(Name, address and telephone number of agent for service)

Copy to:

Elliot H. Lutzker, Esq.

Davidoff Malito & Hutcher LLP

605 Third Avenue

New York, New York 10158

Telephone: (212) 557-7200

Telecopier: (212) 286-1884

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes [X] No [ ]

1

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ ] No [X] *(1)

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ] *(2)

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer [ ]

|

Accelerated filer [ ]

|

Non-accelerated filer [ ]

(Do not check if a smaller reporting company)

|

Smaller reporting company [X]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates or an aggregate of approximately 11,321,580 shares computed by reference to the $2.50 per share price at which the common stock was last sold as of the last business day of the registrant’s second fiscal quarter was $28,303,950.

As of March 28, 2011, there were 13,446,532 shares of Common Stock, par value $0.001 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: NONE

________________

*(1) This issuer is not currently subject to the filing requirements of the Exchange Act, however, has filed all reports.

*(2) the issuer has not yet transitioned into the rule.

2

BLUE EARTH, INC. AND SUBISIDIARIES

Table of Contents

|

Page

|

|

3

PART I

Forward Looking Statements

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. These statements relate to future events or future predictions, including events or predictions relating to our future financial performance, and are generally identifiable by use of the words "may," "will," "should," "expect," "plan," "anticipate," "believe," "feel," "confident," "estimate," "intend," "predict," "forecast," "potential" or "continue" or the negative of such terms or other variations on these words or comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks described under "Risk Factors" that may cause the Company's or its industry's actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. In addition to the risks described in Risk Factors, important factors to consider and evaluate in such forward-looking statements include: (i) general economic conditions and changes in the external competitive market factors which might impact the Company's results of operations; (ii) unanticipated working capital or other cash requirements including those created by the failure of the Company to adequately anticipate the costs associated with acquisitions and other critical activities; (iii) changes in the Company's corporate strategy or an inability to execute its strategy due to unanticipated changes; (iv) the inability or failure of the Company's management to devote sufficient time and energy to the Company's business; (v) the failure of the Company to complete any or all of the transactions described herein on the terms currently contemplated; (vi) competitive factors in the industries in which we compete; (vii) changes in tax requirements (including tax rate changes, new tax laws and revised tax law interpretations); and (viii) other capital market conditions, including availability of funding sources. In light of these risks and uncertainties, many of which are described in greater detail elsewhere under Risk Factors, there can be no assurance that the forward-looking statements contained in this report will in fact transpire.

Although the Company believes that the expectations reflected in the forward-looking statements are reasonable, the Company cannot guarantee future results, levels of activity, performance or achievements. Moreover, neither the Company nor any other person assumes responsibility for the accuracy and completeness of such statements. We do not undertake any duty to update any of the forward-looking statements after the date of this prospectus to conform such statements to actual results or changes in our expectations.

Item 1. Business.

Overview

Blue Earth is engaged in a mergers and acquisition strategy to acquire, license, develop, market, install and monitor clean-tech related, innovative technologies and energy management systems. These technologies are designed to enable customers to reduce their energy consumption, lower their generating and maintenance costs and realize environmental benefits. The targeted technologies typically include various measures designed for a specific customer or facility in our target market of small commercial businesses and residences to improve the efficiency of building systems, such as heating, ventilation, air conditioning, lighting and refrigeration.

Effective January 1, 2011, the Company acquired Castrovilla, Inc. based in Mountain View California which manufactures, sells and installs commercial refrigeration and freezer gaskets and sells and installs motors and controls to approximately 5,400 small commercial businesses. See “Castrovilla Acquisition” below.

Management also intends to accelerate introduction of the acquired technology/products by offering and installing them through energy management service companies, which have an established base of customers at the local, state, regional and national levels. In order to accelerate product introduction, management expects to enter into varying types of agreements with these energy management service companies, including acquisition agreements and/or joint venture agreements, as may be appropriate, for each company and geographic territory.

Blue Earth, Inc. management has identified commercially viable, innovative energy efficient technologies that can be utilized by companies it hopes to acquire to provide their established customer base with cutting-edge products and services. We are continuing to identify innovative technologies and will continue to identify and negotiate the rights for other clean-tech technologies. Management has also identified several energy management and energy management service companies that have been successfully operating in the residential and small commercial business segment of the energy efficiency sector. We have initiated acquisition discussions with energy service companies that specialize in three categories that address small commercial businesses energy efficiency needs: refrigeration, lighting and HVAC. The targeted acquisition candidates currently provide energy efficiency retrofit services to the small commercial businesses space.

4

Management believes that these companies are ideal candidates from which to build a nationwide distribution, installation and service network though a combination of joint venture/associate relationships and/or acquisitions. We believe they will become important building blocks in our efforts to establish a presence in the multi-billion dollar energy efficiency/water and wastewater sectors of the clean technology industry.

Corporate Strategy

Blue Earth, Inc. management will focus its mergers and acquisitions activities on opportunities with the following profile.

|

|

·

|

Innovative and commercially proven technologies, which increase energy efficiency/water and wastewater, for the small commercial business segment and residential segment.

|

|

|

·

|

Energy management and energy management service companies, which have an established customer base seeking growth capital to expand their capabilities, product offerings and substantially increase their revenues and operating profits.

|

Bundled Retrofits. An important element of the M&A strategy is to acquire energy management service companies with an established customer base in each of the afore-mentioned categories. The customer base of each potential acquisition will present an opportunity to cross-sell bundled retrofits to the other acquired companies customer base. For example, when we acquire a company that primarily specializes in refrigeration, we will be in position to contact its customer base and offer to provide energy management services for lighting and HVAC.

Another important criteria is an acquisition candidate’s existing relationship with utilities. We are actively seeking private companies that have successfully provided utility funded rebate programs as incentives to their customers to adopt energy efficiency measures that a particular utility based rebate program is offering.

We are targeting energy management companies that specialize in several aspects of utility run energy efficiency programs including: Program Development; Program Implementation; Program Management; Program Tracking; and Program Reporting as required by oversight agencies.

We intend to acquire innovative technologies and established, reputable energy management and energy management service companies, using restricted common stock; cash and/debt in combinations appropriate for each potential acquisition.

Continue to Maintain Entrepreneurial Approach. We will maintain an entrepreneurial approach toward our customers and remain flexible in designing projects tailored specifically to meet their needs.

Expand Scope of Product and Service Offerings. We plan to continue to expand our offerings by including new types of energy efficiency services, products and improvements to existing products based on technological advances in energy savings strategies, equipment and materials.

Meet Market Demand for Cost-Effective, Environmentally-Friendly Solutions . Through our energy efficiency measures and products, we enable customers to conserve energy and reduce emissions of carbon dioxide and other pollutants. We plan to continue to focus on providing sustainable energy solutions that will address the growing demand for products and services that create environmental benefits for customers.

5

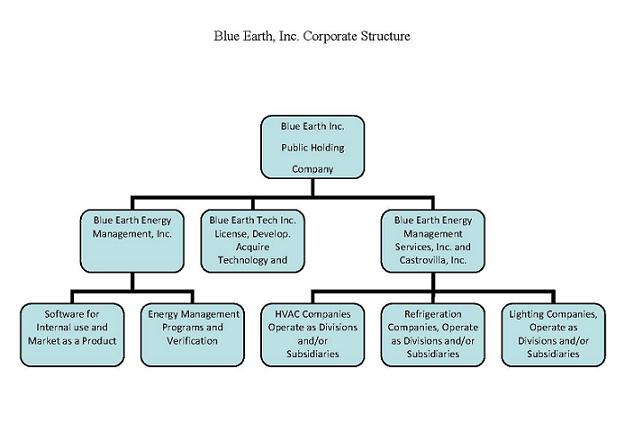

Corporate Structure

Our corporate structure for energy efficiency related acquisitions is designed to separate the acquired companies into three wholly-owned subsidiaries of the Company, which will be operated as separate business units.

Although the three subsidiaries will operate independently, they will work in concert to develop, manage, implement and monitor energy efficiency programs for the utilities and the small commercial businesses established customer base.

We believe that the implementation and execution of our corporate strategy will benefit our shareholders and attract investors who are looking at two bottom lines: financial profitability and social or environmental benefits produced by the Company and its products and services.

Castrovilla Acquisition

On January 19, 2011, Castrovilla Energy, Inc., a recently formed California subsidiary of the Company, acquired substantially all of the assets of Humitech of Northern California, LLC (“Humitech”), a California limited liability company and its related company, Castrovilla, Inc. (the “Castrovilla Acquisition”) with an Effective Date (as defined) of January 1, 2011. Founded in 2004, Castrovilla based in Mountain View, California, had approximately $3.5 million in unaudited revenues in 2010, which is more than twice its 2008 revenues. Castrovilla serves approximately 5,400 small commercial businesses in Northern California with its 24 employees. Castrovilla manufactures, sells and installs commercial refrigeration gaskets and strip curtains, which it sells and installs alongside many other energy efficiency products, such as EC motors, LED lights and a variety of control technologies. Castrovilla’s strategy is to sell lighting and HVAC bundled retrofits to its customer base.

Castrovilla participates in several ratepayer funded utility companies energy efficiency rebate programs, both through third-party programs and through its own small commercial business program, Keep Your Cool. The KeepYour Cool program was created in response to a Request For Proposals put out by a local municipal utility, Silicon Valley Power. Castrovilla’s proposal was accepted and the program funded several hundred thousand dollars. This eventually resulted in contracts with over a dozen municipal utilities throughout Northern California to provide turnkey program administration and implementation. In 2008, Castrovilla acquired the assets of Bay Area Refrigeration, a fully licensed commercial refrigeration contractor that has serviced the San Francisco Bay Area for nearly 30 years.

Castrovilla has created a business model for sustainably generating and delivering kW and kWh that benefits both the utility and the end user. Castrovilla provides energy efficiency services to small commercial businesses and delivers custom programs directly to utilities. The model is both expandable and scalable. Castrovilla is well positioned in terms of capabilities and relationships with utilities and the energy service companies (ESCO) running the third–party programs. Castrovilla intends to become a statewide and regional supplier of utility scale energy efficiency resources delivered by its customized, turnkey vertically integrated small commercial programs.

Since acquiring Bay Area Refrigeration and the C-38 refrigeration contractor’s license, Castrovilla is qualified to install Electronically Commutated (EC) motors, Evaporator Fan Controllers, Anti-Sweat Heater Controllers and LED Case Lighting and other technologies. This has made the Company’s retrofit projects far more comprehensive, which is a significant competitive advantage over companies that target only a single measure. In fact the largest rebate programs require comprehensive retrofits to qualify for rebates.

In addition to energy efficiency retrofits, Castrovilla also has on-going contracts to provide periodic maintenance to numerous restaurants and other refrigerated facilities throughout the San Francisco Bay Area. This includes 24 x 7 emergency refrigeration services.

6

In mid-2009 Castrovilla opened an online-store (www.bayarearefrigeration.com) to sell manufactured gaskets and strip curtains on both a wholesale and retail basis. The web site also allows us to distribute refrigeration hardware.

The purchase price for Humitech, under the Asset Purchase Agreement (“APA”) was $600,000. This consisted of the payment of $150,000 of affiliated debt and the issuance of 267,857 shares of restricted Common Stock of Blue Earth, Inc. with an agreed upon value of $450,000, or $1.68 per share, the average closing price of the Company’s Common Stock from September 1-23, 2010 when the terms of the transaction were agreed to. The Company also assumed trade debt of approximately $121,000. Humitech will remain an unaffiliated non-operating entity in order to pay its other liabilities with the proceeds of the shares received from the Company, as well as from an inter-company note in the amount of $356,707 from Castrovilla, Inc.

On December 30, 2010, Castrovilla Energy, Inc. (“CEI”), a wholly-owned subsidiary of the Company’s subsidiary, Blue Earth Energy Management Services, Inc. (“BEEMS”) entered into an Agreement and Plan of Merger (the “Plan”) with Castrovilla, Inc. and the Stockholders of Castrovilla, Inc. with an Effective Date of January 1, 2011, subject to final Board approval which was obtained on January 18, 2011. CEI merged with and into Castrovilla, Inc. on January 21, 2011, which will continue its existence as a wholly-owned California subsidiary of BEEMS.

Under the Plan, the Company issued an aggregate of 1,011,905 shares of its Common Stock valued at $1.68 per share or $1,700,000 to the stockholders of Castrovilla, Inc. in exchange for all of the outstanding capital stock of Castrovilla, Inc. All of the 1,279,762 shares issued in the Castrovilla Acquisition (collectively, the “Company Shares”) are subject to Lock-up/Leak-out and Guaranty Agreements. The two Castrovilla, Inc. stockholders, John Pink, who continued as President of Castrovilla, Inc. and Adam Sweeney, together with Humitech (the “Stockholders”) cannot sell any of the Company Shares for a six-month period beginning on January 1, 2011 and thereafter the three stockholders may sell up to 2,461 Company Shares per trading day in the aggregate until all Company Shares are sold (the “Lock-up Period”) ending 2½ years from January 1, 2011. The Company guaranteed to the Stockholders the net sales price of $1.68 per share, provided the Stockholders are in compliance with the terms and conditions of the Lock-up Agreement.

The Stockholders and the Company will share equally the profits, if any, from the sale of shares and/or profits from sales above $3.36 per share during the Lock-up Period. Any deficit from sales below $1.68 per share and/or profits from sales above $3.36 per share shall be paid (i) 50% in cash, and (ii) the remaining 50% in either cash or shares of Common Stock of the Company (at their then current fair market value, or any combination thereof, at the sole discretion of the party making the payment).

In the event that Castrovilla Inc.'s EBITDA during the Lock-up Period is below agreed to budgeted amounts of $722,000 of EBITDA per year for each of the fiscal years ending December 31, 2011, 2012 and 2013, the $1.68 per share guaranteed price shall be decreased by the same percentage decrease that EBITDA is below the projected $722,000 of EBITDA.

In addition, under the Plan, the Company paid $50,000 to an unaffiliated third party for an existing obligation of Castrovilla, Inc.

There was no relationship between the Company or its affiliates and any of the other parties, prior to this transaction and with respect to the APA and the Plan.

Castrovilla Products and Services

In 2009 and 2010, Castrovilla’s revenues were generated primarily from sales of parts and equipment for refrigeration and LED Case Lighting, refrigeration service, preventative maintenance, consulting, and on-line sales. Currently, the only materials that are purchased in large quantities are its gasket materials. All other inventory including EC motors, Anti-Sweat heaters (ASH) controllers, LED Case Lights and other hardware are kept in low quantities or purchased on an as needed basis.

Castrovilla accesses a variety of rebate programs, always choosing the best one for a given project. The funds that pay for the rebate programs utilized by Castrovilla are the result of California Public Utilities Commission (CPUC) requirements that all utilities in the State of California collect a “Public Benefits” charge as a percentage of the total bill. These funds are required to be invested in energy savings programs. This pool of money measures in the billions of dollars and pays for many programs. Several of these programs are provided through third-party programs, which are usually administered by ESCO and consulting companies and implemented by Refrigeration, Lighting, HVAC and Solar companies. Each program has different eligibility requirements and/or is available in different areas. Participating in the programs in its market area allows Castrovila to provide the broadest coverage to its customers.

7

Castrovilla management believes that the key to sustaining and expanding its program is to take part in or take advantage of a constant stream of technological innovation. By identifying, evaluating and verifying the best new measures Castrovilla is able to serve its 5,400 small commercial customers and bring in new ones. In some cases Castrovilla is introduced to new measures through its work for other companies, which it can assimilate into Keep Your Cool.

Rapid Dewatering System (RDS)

On August 31, 2010, pursuant to a Stock Purchase Agreement, the Company sold to various shareholders including its former Chairman and interim CEO, all of the issued and outstanding common stock of Genesis Fluid Solutions, Ltd. (“GFS”) then a wholly-owned subsidiary. As described under Item 13. “Certain Relationships and Related Transactions – Discontinued Operations”, in addition to 6,331,050 shares of Common Stock of the Company and approximately 3,011,000 options and warrants returned to the Company by the purchasers of GFS, we received a 6% royalty on all gross revenues derived from dewatering operations and the sale, lease or licensing arrangements of the Rapid Dewatering System (“RDS”) and/or any of the dewatering boxes of its affiliates until the Company receives $4 million and a royalty of 3% of gross revenues thereafter not to exceed a cumulative royalty of $15 million.

The GFS patented RDS removes different types of debris, sediments, and contaminates from waterways and industrial sites, which assists in the recovery of lakes, canals, reservoirs and harbors. The RDS system separates water from the solid materials that are dredged, a process that is known as dewatering. GFS believes its technologies have a variety of benefits for both industry and the environment, however GFS has had very limited revenues to date.

Water Recovery Industry

Many waterways worldwide suffer from eutrophication or deterioration, leading to the formation of wetlands. This typically results from agricultural run-off and other man-made causes. Some waterways are so polluted and stagnant that their animal and plant life die off and, in the case of rivers and streams, the current ceases to flow. Having continued access to healthy, clean lakes, rivers, marinas, shipping ports and other waterways is vital to maintaining affordable water supplies, vibrant economies and entire ecosystems. Additionally, mining operations and paper mills can greatly limit their water usage by recycling their carriage water in their industrial circuit, instead of discharging it into natural waterways or disposal sites.

Cleaning a waterway often requires dredging. Dredging empties the water body of large quantities of built-up debris along the bottom, ranging from coarse material, such as shells, organic vegetation and garbage, to sand and fine grained sediment, such as clays, silts and organics.

The methodologies currently employed in the industry to dewater dredged sediment from waterways primarily fall into three categories: (1) upland disposal sites, (2) belt presses and thickeners, and (3) geo-synthetic tubes.

Market Size

According to a 2009 McKinsey & Company report there are a total of $130 billion worth of energy saving opportunities annually in the U.S. economy that go unrealized. The central conclusion of the report states that energy efficiency offers a vast, low-cost energy resource for the U.S. economy. Significant and persistent barriers will need to be addressed at multiple levels to stimulate demand for energy efficiency and manage its delivery across more than 100 million buildings and literally billions of electronic devices. If executed at scale, a holistic approach would yield gross energy savings of more than $1.2 trillion, well above the $520 billion needed through 2020 for upfront investment in efficiency measures (not including program costs). Such a program is estimated to reduce energy consumption in 2010 by 9.1 quadrillion BTU’s, roughly 23% of projected demand, potentially abating up to 1.1 gigatons of greenhouse gases annually.

8

We intend to focus our efforts in the multi-billion dollar energy efficiency segment of the clean-tech industry. Energy efficiency companies, sometimes referred to as energy services companies, generally develop, install and arrange financing for projects designed to improve the energy efficiency of buildings and other facilities. Typical products and services offered by energy efficiency companies include boiler and chiller replacement, HVAC upgrades, lighting retrofits, equipment installations, on-site cogeneration, renewable energy plants, load management, energy procurement, rate analysis, risk management and billing administration. Energy efficiency companies often offer their products and services through ESPCs. Under these contracts, energy efficiency companies assume certain responsibilities for the performance of the installed measures, under assumed conditions, for a portion of the project’s economic lifetime. According to a 2010 Lawrence Berkeley National Laboratory study, which analyzes the current size of the energy services sector, sector growth projections to 2011 and market trends for energy efficiency related services, the sector in aggregate will have annual revenues exceeding $7 billion in 2011. This represents an average annual growth rate of 26% per year between 2009 and 2011. Key drivers for energy services growth include the large infusion of funding from the American Recovery and Reinvestment Act (“ARRA”) to support state and local government energy efficiency programs, increased spending in ratepayer-funded energy efficiency programs, and increased customer interest in strategies that mitigate higher utility bills and/or address environmental emissions.

The $7 billion in estimated annual revenues by energy service companies does not include the cost of installing bundled retrofits by refrigeration, lighting and HVAC sub contractors.

Investment levels in energy efficiency in buildings in the private and public sectors and industrial manufacturing facilities have remained strong despite the global recession according to the Energy Efficiency Indicator (EEI) recently released by Johnson Controls, Inc. The EEI tracks energy management priorities, practices and investment plans among decision makers responsible for managing commercial buildings and their energy use.

Across all regions surveyed, energy management is considered an important priority among commercial decision-makers. While motivations differ from region to region, cost savings is consistently the most important factor driving investments. The current economic environment has led many organizations to search for opportunities to reduce their operating costs. There has been a growing awareness that reduced energy consumption presents an opportunity for significant long-term savings in operating costs and that the installation of energy efficiency measures can be a cost-effective way to achieve such reductions. After cost savings, lowering greenhouse gas emissions is the second most important motivator for energy efficiency in all regions except North America, where boosting public image and taking advantage of government/utility incentives rank higher in importance.

According to the American Council for an Energy-Efficient Economy (“ACEEE”) there is approximately 67 billion square feet of commercial floor space in the U.S. Commercial buildings account for 17% of total energy consumed in the U.S. at an average cost of $1.21 per square foot of commercial floor space. ACEEE points to energy efficiency in buildings as the cleanest, lowest-cost, most sensible way of promoting economic prosperity, energy security and environmental protection.

The ACEEE 2010 State Energy Efficiency Scorecard reports that states are demonstrating their growing interest in energy efficiency as a means to bolster their economies. Governors, state legislators, officials and citizens, increasingly recognize energy efficiency – the kilowatt hours and gallons of gasoline saved that we don’t use thanks to improved technologies and practices – as the cheapest, cleanest and quickest energy resource to deploy. Other key findings include:

|

|

·

|

California has retained its #1 ranking for the fourth year in a row, outpacing all other states in the level of investment in energy efficiency across all sectors of the economy.

|

|

|

·

|

State budgets for energy efficiency in 2009 are almost double the level spending in 2007, increasing from $2.5 billion to $4.3 billion. Reported electricity savings from energy efficiency programs across all states increased 8% between 2007 and 2008.

|

|

|

·

|

Twenty-seven states have adopted or have pending Energy Efficiency Resource Standards (EERS) that establish long-term, fixed efficiency savings targets, double the number of states in 2006. These states account for two-thirds of electricity sales in the U.S.

|

9

|

|

·

|

Twenty states have either adopted or have made significant progress toward the adoption of the latest energy saving building codes for homes and commercial properties, double the number of states in their 2009 Scorecard.

|

|

|

·

|

The injection of more than $11 billion of ARRA funds directly to state energy efficiency has helped stimulate significant funding and creating new energy-saving programs that are saving consumers’ money and putting people to work.

|

Additional Market Drivers

Castrovilla’s key markets in 2009 and 2010 were third-party utility rebate programs, Keep Your Cool rebate program, restaurant and convenience store maintenance and service, consulting and wholesale and Internet sales. Castrovilla primarily services the San Francisco Bay Area, as well as California’s Central Valley region.

Utility Rebate Programs. In a number of markets throughout the U.S., local electrical utilities and related organizations are offering rebates for the purchase and installation of energy efficient products and systems. Ratepayer funded programs are offered by utilities to encourage load reductions by its customers. These incentives may be structured as one-time up-front rebates on energy efficient equipment or may consist of payments per measured kWh saved over a course of several years. Small commercial businesses can leverage the cost of retrofits with incentives received through ratepayer-funded energy efficiency programs.

Rebate incentives are typically used to buy down utility retrofit project costs for energy efficiency programs. The customer can receive the rebate directly from the utility, or the energy service company may assist in identifying programs that the small commercial business may qualify for and may collect the rebate on the customer’s behalf.

Many utility companies employ demand side management (DSM) programs to help reduce energy consumption. These regulated programs benefits the customer by subsidizing the first cost of capital improvements that provide long – term energy and operational cost savings. Currently, energy efficiency rebates are only offered by specific electrical utilities and the respective rebate programs and requirements change frequently.

Rising and Volatile Energy Prices. Over the past decade, energy-linked commodity prices, including oil, gas, coal and electricity, have all increased and exhibited significant volatility. From 1999 to 2009, average U.S. retail electricity prices have increased by more than 50%.

Aging and Inefficient Facility Infrastructure. Many organizations continue to operate with an energy infrastructure that is significantly less efficient and cost-effective than what is now available through more advanced technologies applied to lighting, heating, cooling and other building systems. As these organizations explore alternatives for renewing their aging facilities, they often identify multiple areas within their facilities that could benefit from the implementation of energy efficiency measures, including the possible use of renewable sources of energy.

Movement Toward Industry Consolidation. As energy efficiency solutions continue to increase in technological complexity and customers look for service providers that can offer broad geographic and product coverage, we believe smaller niche energy efficiency companies will continue to look for opportunities to combine with larger companies such as the Company that can better serve their customers’ needs. Increased market presence and size of energy efficiency companies should, in turn, create greater customer awareness of the benefits of energy efficiency measures.

Increased Use of Third-Party Financing. Many organizations desire to use their existing sources of capital for core investments or do not have the internal capacity to finance improvements to their energy infrastructure. These organizations often require innovative structures to facilitate the financing of energy efficiency and renewable energy projects.

10

Castrovilla Sales and Marketing

Castrovilla utilizes direct marketing through four (4) outside sales representatives, who are compensated with a base salary and commission, and relationships with utility representatives, program representatives and trade organizations to generate new projects. Castrovilla also maintains the following web sites: www.BARefrigeration.com (on-line commerce capabilities); www.Bay Area Refrigeration.com (redirects to www.BARefrigeration.com); and www.KeepYourCool.org.

Castrovilla Customers

Castrovilla’s key customers in 2009 were the Keep Your Cool utility rebate program, Ecology Action - Right Lights utility program, KEMA and San Francisco Energy Watch and third-party utility rebate programs. In 2010, the key customers were KEMA, Keep Your Cool, and Ecology Action-Right Lights utility program

Competition

Energy Efficiency

The clean-tech industry is highly competitive. The energy efficiency segment for small commercial businesses is also highly competitive. Castrovilla competes with various types and sizes of companies ranging from local and national service providers, local refrigeration contractors, such as Egain and Energywise and rebate program administrators. Castrovilla differentiates itself as the only fully-licensed, comprehensive contractor in Northern California which sells and installs energy efficiency projects through utility rebate programs, and which contracts directly with utilities, allowing it to perform retrofit services and secure rebates for its small and large customers who operate locations served by multiple utilities.

Few contractors in Castrovilla’s market area actually participate in the third-party program process. The reluctance is attributable to the considerable amount of paperwork required for each project. Having completed thousands of applications, Castrovilla is accustomed to preparing the appropriate documents. Because of the new comprehensiveness requirement for refrigeration projects, several of the previously participating companies are no longer qualified. Finally, both the utilities and the third-party administrators have become stricter about contractor participation requirements, which is actively removing unqualified and unscrupulous vendors. As a contractor who is regularly contacted by the utilities and the third-party program administrators to repair issues left behind by others, Castrovilla’s reputation is among the best.

We intend to compete based on the following:

Comprehensive Service Provider. We intend to offer our customers expertise in addressing almost all aspects of energy efficiency. Our staff from acquired companies is expected to provide the capability and flexibility to determine what energy efficiency measures are best suited to achieve the customer’s energy efficiency and environmental goals.

Independence. We are an independent company with no affiliation to any equipment manufacturer, utility or fuel company. Unlike affiliated service companies, we have the freedom and flexibility to be objective in selecting particular products and technologies available from different acquisition candidates and suppliers in order to optimize our solutions for customers’ particular needs.

Experienced Management. Our executive officers each has over 25 years of experience in founding, acquiring and operating publicly held companies in diverse business sectors.

Federal and State Qualifications. The federal governmental program under which federal agencies and departments can enter into ESPCs requires that energy service providers have a track record in the industry and meet other specified qualifications. Over 20 states require similar qualifications. We intend to acquire companies which meet these qualifications. This will provide us with the opportunity to continue to grow our business with federal, state and other governmental customers and differentiates us from energy efficiency companies that have not been similarly qualified.

|

|

§

|

Federal. In 2007, the United States enacted the Energy Independence and Security Act which mandates that federal buildings reduce energy consumption by 30% by 2015 compared to their 2003 baseline and contains multiple provisions promoting long-term ESPCs. The U.S. Department of Energy also has a number of research, development, grant and financing programs – most notably the DOE Loan Guarantee Program — to encourage energy efficiency and renewable energy. Additionally, the United States has adopted federal incentives for renewable energy, including the production tax credit, investment tax credit and accelerated depreciation.

|

11

|

|

§

|

States. At the U.S. state level, significant measures to support energy efficiency and renewable energy have been implemented, including as of December 31, 2009, the following:

|

|

|

·

|

20 states have adopted energy efficiency resource standards, or EERS, and long-term energy savings targets for utilities.

|

|

|

·

|

29 U.S. states and the District of Columbia have renewable portfolio standards, or RPS, in place, and six states have renewable portfolio goals.

|

|

|

·

|

14 states have passed legislation enabling a new financing mechanism known as Property Assessed Clean Energy (PACE) Bonds. The bonds provide funds that can be used by commercial and residential property owners to finance efficiency measures and small-scale renewable energy systems.

|

|

|

§

|

Economic Stimuli. Governments worldwide have allocated significant portions of economic stimuli to clean energy. The American Recovery and Reinvestment Act of 2009 allocated $67 billion to promote clean energy, energy efficiency and advanced vehicles. Additionally, the Emergency Economic Stabilization Act instituted a grant program that provides cash in lieu of the investment tax credit for eligible renewable energy generation sources which commence construction in 2010.

|

Key factors in the award of contracts include system and service performance, quality, price, design, reputation, technology, application engineering capability and energy management services. Competitors for contracts in the small commercial businesses marketplace include many local, regional, national and international companies with greater resources than we have.

The domestic energy services market for small commercial businesses is highly fragmented, which we believe, provides a viable point-of-entry for acquiring established, reputable, profitable energy services companies who are seeking access to growth capital and innovative, commercially proven, cost-effective energy efficient technologies.

There are three principal types of energy efficiency companies:

|

|

·

|

Independent Energy Services Companies — Energy efficiency companies such as the Company, which are not associated with an equipment manufacturer, utility or fuel company. Most of these companies are small and focus either on a specific geography or specific customer base.

|

|

|

·

|

Utility-Affiliated Energy Services Companies – Companies owned by regulated North American utilities, many of which were traditionally focused on the service territories of their affiliated utilities, but have since expanded their geographical markets. Examples include Constellation Energy Projects and Services and ConEdison Solutions.

|

|

|

·

|

Equipment Manufacturers — Companies owned by building equipment or controls manufacturers. Many of these companies have a national presence through an extensive network of branch offices. Examples include Honeywell, Johnson Controls and Siemens.

|

Water Recovery

The dewatering business is highly competitive. GFS expects to depend on government contracts for a significant portion of its business. Competition for government contracts depends upon its ability to satisfy bidding requirements, as well as subcontracting requirements in the event that GFS is a subcontractor to a prime contractor. Many larger more well capitalized companies may be able to satisfy the financial, size, equipment, employment, bonding, certification, track record, and other government regulatory requirements more readily than GFS is able to. Typical competitors are represented by the following companies:

GFS will directly market services to government and other users, and licensing its technology to others. GFS intends to initially focus our efforts on the United States, Europe and the Pacific Rim.

GFS may provide the equipment and training necessary to launch projects while retaining ownership of equipment and intellectual property. By seeking to cultivate strategic relationships with large, established companies in various regions of the world, GFS believes it can grow more quickly than establishing offices throughout the world.

12

Government and Environmental Regulation

Energy Efficiency

Various regulations will affect the conduct of our business. Federal and state legislation and regulations enable us to enter into ESPCs with government agencies in the United States. The applicable regulatory requirements for ESPCs differ in each state and between agencies of the federal government.

Our projects must conform to all applicable electric reliability, building and safety, and environmental regulations and codes, which vary from place to place and time to time. Various federal, state, provincial and local permits are required to construct an energy efficiency project or renewable energy plant.

Water Recovery

GFS’ operations are subject to various environmental laws and regulations related to, among other things: dredging operations; the disposal of dredged material; protection of wetlands; storm water and waste water discharges; and, transportation and disposal of hazardous substances and materials. GFS is also subject to laws designed to protect certain marine species and habitats. Compliance with these statutes and regulations can delay appropriation and/or performance of particular projects and increase related expenses. GFS projects may involve transportation and disposal of hazardous waste and other hazardous substances and materials. Various laws strictly regulate the removal, treatment and transportation of hazardous substances and materials and impose liability for human health effects and environmental contamination caused by these materials. We cannot predict what environmental legislation or regulations will be enacted in the future, how existing or future laws or regulations will be enforced, administered or interpreted, or the amount of future expenditures that may be required to comply with these environmental or health and safety laws or regulations, or to respond to future cleanup matters or other environmental claims.

Intellectual Property

GFS has invested significantly in the development of proprietary technology and also to establish and maintain an extensive knowledge of the leading technologies, and incorporate these technologies into the RDS and the services that GFS offers and provides to its customers. GFS holds a patent, which expires in 2021, that covers the European Union, China, South Africa, Eurasia and New Zealand; a patent pending in the United States, which is expected in the next 12 months; and, a number of other patent applications. GFS believes that it holds adequate rights to all intellectual property used in its business and that it does not infringe upon any intellectual property rights held by other parties.

Employees

As of March 21, 2011, Blue Earth, Inc. had three employees, consisting of its two executive officers and a corporate administrator. Castrovilla, Inc. had 24 full time, non-union, employees, including its President, John Pink and no part-time employees. Castrovilla employees include 9 key management, 8 technicians who perform product installation and field service, 4 engaged in sales and marketing and 3 in shop/gasket manufacturing. The Company expects to continue to use subcontractors and independent consultants until such time as further acquisitions are made.

13

Item 1A. Risk Factors.

Investing in our common stock involves a high degree of risk. Prospective investors should carefully consider the risks described below, together with all of the other information included or referred to in this prospectus, before purchasing shares of our common stock. There are numerous and varied risks that may prevent us from achieving our goals. If any of these risks actually occurs, our business, financial condition or results of operations may be materially adversely affected. In such case, the trading price of our common stock could decline and investors in our common stock could lose all or part of their investment.

Risks Relating to Our Business

Since we have limited operating history, it is difficult for potential investors to evaluate our business.

In August 2010 we spun-off GFS, our wholly-owned operating subsidiary, retaining only a royalty interest. We completed our initial acquisition as of January 1, 2011. Therefore, our limited operating history makes it difficult for potential investors to evaluate our business or prospective operations and your purchase of our securities. Prior to our acquisition of Castrovilla, we generated only limited revenues. As an early stage company, we are subject to all the risks inherent in the initial organization, financing, expenditures, complications and delays inherent in a new business. Accordingly, our business and success faces risks from uncertainties faced by developing companies in a competitive environment. There can be no assurance that our efforts will be successful or that we will ultimately be able to attain profitability.

Single source of revenue.

At this point in time, the Company has a single source of revenue from Castrovilla as it has not received any royalty income to date and had an operating loss for 2010. In addition, we are subject to many business risks, including, but not limited to, unforeseen capital requirements, failure of market acceptance, failure to acquire an operating businesses, and competitive disadvantages against larger and more established companies. In addition, there can be no assurance that the Company will ever be able to generate sufficient revenues to become profitable.

We are dependent upon key personnel whose loss may adversely impact our business.

We rely heavily on the expertise, experience and continued services of Dr. Johnny Thomas, our Chief Executive Officer and John Francis, our Vice President-Corporate Development and Investor Relations. Both officers are employed under employment contracts at will, and the loss of either of their services and the inability to replace them and/or attract or retain other key individuals, could materially adversely affect us. If either Dr. Thomas or Mr. Francis were to leave, we could face substantial difficulty in hiring a qualified successor and could experience a loss in productivity while any successor obtains the necessary training and experience. We do not have key man life insurance policies on our management.

We face risks associated with our international business.

We may establish and expand over time, through acquisitions, international commercial or licensing operations and activities in various countries. These international business operations will be subject to a variety of risks associated with conducting business internationally. We do not know the impact that these regulatory, geopolitical and other factors may have on our international business in the future, including the following:

|

•

|

changes in or interpretations of foreign regulations that may adversely affect our ability to perform services or repatriate profits to the United States;

|

|

|

•

|

the imposition of tariffs;

|

|

|

•

|

economic or political instability in foreign countries;

|

|

|

•

|

imposition of limitations on or increase of withholding and other taxes on remittances and other payments by foreign subsidiaries or joint ventures or customers;

|

|

|

•

|

conducting business in places where business practices and customs are unfamiliar and unknown;

|

14

|

•

|

the imposition of restrictive trade policies;

|

|

|

•

|

the existence of inconsistent laws or regulations;

|

|

|

•

|

the imposition or increase of investment requirements and other restrictions or requirements by foreign governments;

|

|

|

•

|

uncertainties relating to foreign laws and legal proceedings;

|

|

|

•

|

fluctuations in foreign currency and exchange rates; and

|

|

|

•

|

compliance with a variety of U.S. laws, including the Foreign Corrupt Practices Act.

|

We may need additional financing to execute our business plan and fund operations, which additional financing may not be available on reasonable terms or at all.

As of December 31, 2010 we had $3,900,096 cash on hand. In view of our acquisition strategy we may not be able to execute our current business plan and fund business operations long enough to achieve profitability. Our ultimate success may depend upon our ability to raise additional capital. There can be no assurance that additional funds will be available when needed from any source or, if available, will be available on terms that are acceptable to us. We may be required to pursue sources of additional capital through various means, including joint venture projects and debt or equity financing. Future financing through equity investments is likely to be dilutive to existing stockholders. Also, the terms of securities we may issue in future capital transactions may be more favorable to new investors than our current investors. Newly issued securities may include preferences, superior voting rights, the issuance of warrants or other derivative securities, and the issuance of incentive awards under employee equity incentive plans, which may have additional dilutive effects. Further, we may incur substantial costs in pursuing future capital and/or financing, including investment banking fees, legal fees, accounting fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our financial condition and results of operations. Our ability to obtain needed financing may be impaired by factors, including the condition of the economy and capital markets, both generally and specifically in our industry, and the fact that we are not profitable, which could impact the availability or cost of future financing. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs, even to the extent that we reduce our operations accordingly, we may be required to cease operations.

Compliance with environmental laws could adversely affect our operating results.

Costs of compliance with federal, state, local and other foreign existing and future environmental regulations could adversely affect our cash flow and profitability. We will be required to comply with numerous environmental laws and regulations and to obtain numerous governmental permits in connection with energy efficiency products, and we may incur significant additional costs to comply with these requirements. If we fail to comply with these requirements, we could be subject to civil or criminal liability, damages and fines. Existing environmental regulations could be revised or reinterpreted and new laws and regulations could be adopted or become applicable to us or our customers, and future changes in environmental laws and regulations could occur. These factors may impose additional expense on our operations.

In addition, private lawsuits or enforcement actions by federal, state, and/or foreign regulatory agencies may materially increase our costs. Certain environmental laws make us potentially liable on a joint and several basis for the remediation of contamination at or emanating from properties or facilities which we may acquire that arranged for the disposal of hazardous substances. Although we will seek to obtain indemnities against liabilities relating to historical contamination at the facilities we own or operate, we cannot provide any assurance that we will not incur liability relating to the remediation of contamination, including contamination we did not cause.

We may not be able to obtain or maintain, from time to time, all required environmental regulatory approvals. A delay in obtaining any required environmental regulatory approvals or failure to obtain and comply with them could adversely affect our business and operating results.

15

We will need to increase the size of our organization, and we may experience difficulties in managing growth.

We are a small company with three full-time employees and independent management, as of the date of this report. In addition to prospective employees hired from companies which we may acquire, we will need to expand our employee infrastructure for managerial, operational, financial and other resources. Future growth will impose significant added responsibilities on members of management, including the need to identify, recruit, maintain and integrate additional employees. Our future financial performance and our ability to commercialize our product candidates and to compete effectively will depend, in part, on our ability to manage any future growth effectively.

In order to manage our future growth, we will need to continue to improve our management, operational and financial controls and our reporting systems and procedures. All of these measures will require significant expenditures and will demand the attention of management. If we do not continue to enhance our management personnel and our operational and financial systems and controls in response to growth in our business, we could experience operating inefficiencies that could impair our competitive position and could increase our costs more than we had planned. If we are unable to manage growth effectively, our business, financial condition and operating results could be adversely affected.

Our corporate strategy will not be successful if demand for energy efficiency and renewable energy solutions does not develop.

We believe, and our corporate strategy assumes, that the market for energy efficiency and renewable energy solutions will continue to grow, that we will increase our penetration of this market and that our revenue from selling into this market will continue to increase with future acquisitions. If our expectations as to the size of this market and our ability to sell our products and services in this market are not correct, our corporate strategy will be unsuccessful and our business will be harmed.

Certain projects we may undertake for our customers may require significant capital, which our customers or we may finance through third parties, and such financing may not be available to our customers or to us on favorable terms, if at all.

Certain energy efficiency projects are typically financed by third parties. The significant disruptions in the credit and capital markets in the last several years have made it more difficult for customers to obtain financing on acceptable terms or, in some cases, at all. Any inability by us or our customers to raise the funds necessary to finance our projects, or any inability by us to obtain a revolving credit facility, could materially harm our business, financial condition and operating results.

Our business may be affected by seasonal trends and construction cycles, and these trends and cycles could have an adverse effect on our operating results.

We expect that our business will be subject to seasonal fluctuations and construction cycles, particularly in climates that experience colder weather during the winter months, such as the northern United States and Canada, or at educational institutions, where large projects are typically carried out during summer months when their facilities are unoccupied. In addition, government customers, many of which have fiscal years that do not coincide with ours, typically follow annual procurement cycles and appropriate funds on a fiscal-year basis even though contract performance may take more than one year. Further, government contracting cycles can be affected by the timing of, and delays in, the legislative process related to government programs and incentives that help drive demand for energy efficiency and renewable energy projects. As a result, our revenue and operating income in the third quarter is expected to be typically higher, and our revenue and operating income in the first quarter is expected to be typically lower, than in other quarters of the year. As a result of such fluctuations, we may occasionally experience declines in revenue or earnings as compared to the immediately preceding quarter, and comparisons of our operating results on a period-to-period basis may not be meaningful.

Our business depends in part on federal, state and local government support for energy efficiency and renewable energy, and a decline in such support could harm our business.

We depend, in part, on government legislation and policies that support energy efficiency and renewable energy projects and that enhance the economic feasibility of our energy efficiency services and small-scale renewable energy projects. The U.S. government and several states support potential customers’ investments in energy efficiency and renewable energy through legislation and regulations that authorize and regulate the manner in which certain governmental entities do business with companies like us, encourage or subsidize governmental procurement of our services, provide regulatory, tax and other incentives to others to procure our services and provide us with tax and other incentives that reduce our costs or increase our revenue.

16

For example, U.S. legislation in 1992 authorized federal agencies to enter into energy savings performance contracts (“ESPCs”), such as those which we may enter into with customers at a later date. In 2007, three years after the expiration of the original legislation, new ESPC legislation was enacted without an expiration provision, and in the same year, the President of the United States issued an executive order requiring federal agencies to set goals to reduce energy use and increase renewable energy sources and use. In addition, the American Recovery and Reinvestment Act of 2009 (“ARRA”) allocated $67 billion to promote clean energy, energy efficiency and advanced vehicles. Additionally, the Emergency Economic Stabilization Act of 2008 instituted the 1603 cash grant program, which may provide cash in lieu of an investment tax credit for eligible renewable energy generation sources for which construction commences prior to the end of 2010 where the project is placed in service by various dates set out in the act. The Internal Revenue Code (the “Code”), currently provides production tax credits for the generation of electricity from wind projects and from LFG-fueled power projects, and an investment tax credit or grant in lieu of such tax credits for investments in LFG, wind, biomass and solar power generation projects. Various state and local governments have also implemented similar programs and incentives, including legislation authorizing the procurement of ESPCs.

Prospective customers frequently depend on these programs to help justify the costs associated with, and to finance, energy efficiency and renewable energy projects. If any of these incentives are adversely amended, eliminated or not extended beyond their current expiration dates, or if funding for these incentives is reduced, it could adversely affect our ability to obtain project commitments from new customers. A delay or failure by government agencies to administer, or make procurements under, these programs in a timely and efficient manner could have a material adverse effect on our potential customers’ willingness to enter into project commitments with us.

Changes to tax, energy and environmental laws could reduce our prospective customers’ incentives and mandates to purchase certain kinds of services that we may supply, and could thereby adversely affect our business, financial condition and operating results.

A significant decline in the fiscal health of federal, state, provincial and local governments could reduce demand for our energy efficiency and renewable energy projects.

A significant decline in the fiscal health of federal, state or local governmental entities may make it difficult for them to enter into contracts for our services or to obtain financing necessary to fund such contracts.

Failure of third parties to manufacture quality products or provide reliable services in a timely manner could cause delays in the delivery of our services and completion of our projects, which could damage our reputation, have a negative impact on our relationships with our customers and adversely affect our growth.

Our success depends on our ability to provide services and products in a timely manner, which, in part, depends on the ability of third parties to provide us with timely and reliable services and products, such as boilers, chillers, cogeneration systems, PV panels, lighting and other complex components. In providing our services we intend to rely on products that meet our design specifications and components manufactured and supplied by third parties, as well as on services performed by subcontractors.

Warranties provided by third-party suppliers and subcontractors typically limit any direct harm we might experience as a result of our relying on their products and services. However, there can be no assurance that a supplier or subcontractor will be willing or able to fulfill its contractual obligations and make necessary repairs or replace equipment. In addition, these warranties generally expire within one to five years or may be of limited scope or provide limited remedies. If we are unable to avail ourselves of warranty protection, we may incur liability to our customers or additional costs related to the affected products and components, including replacement and installation costs, which could have a material adverse effect on our business, financial condition and operating results.

Moreover, any delays, malfunctions, inefficiencies or interruptions in these products or services — even if covered by warranties — could adversely affect the quality and performance of our solutions. This could cause us to experience difficulty retaining current customers and attracting new customers, and could harm our brand, reputation and growth. In addition, any significant interruption or delay by our suppliers in the manufacture or delivery of products or services on which we depend could require us to expend considerable time, effort and expense to establish alternate sources for such products and services.

17

We may need to assume responsibility under customer contracts for factors outside our control, including the risk that fuel prices will increase.

We do not expect to take responsibility under our proposed contracts for a wide variety of factors outside our control. However, we may sometimes need to assume some level of risk and responsibility for certain factors — sometimes only to the extent that variations exceed specified thresholds particularly with contracts for renewable energy projects. Although we intend to structure our contracts so that our obligation to supply a customer with electricity, for example, does not exceed the quantity produced by the production facility, in some circumstances we may commit to supply a customer with specified minimum quantities based on our projections of the facility’s production capacity. In such circumstances, if we are unable to meet such commitments, we may be required to incur additional costs or face penalties. Despite measures to mitigate risks under these and other contracts, such steps may not be sufficient to avoid the need to incur increased costs to satisfy our commitments, and such costs could be material. Increased costs that we are unable to pass through to our customers could have a material adverse effect on our operating results.

Our business will depend on experienced and skilled personnel, and if we are unable to attract and integrate skilled personnel, it will be more difficult for us to manage our business and complete projects.

The success of our business will depend on the skill of our personnel. Accordingly, it is critical that we maintain, and continue to build, a highly experienced management team and specialized workforce, including engineers, project and construction management, and business development and sales professionals. In addition, our construction projects require a significant amount of trade labor resources, and other skilled workers, as well as certain specialty subcontractor skills.

Competition for personnel, particularly those with expertise in the energy services and renewable energy industries, is high, and identifying candidates with the appropriate qualifications can be costly and difficult. We may not be able to hire the necessary personnel to implement our business strategy given our anticipated hiring needs, or we may need to provide higher compensation or more training to our personnel than we currently anticipate.

In the event we are unable to attract, hire and retain the requisite personnel and subcontractors, we may experience delays in completing projects in accordance with project schedules and budgets, which may have an adverse effect on our financial results, harm our reputation and cause us to curtail our pursuit of new projects. Further, any increase in demand for personnel and specialty subcontractors may result in higher costs, causing us to exceed the budget on a project, which in turn may have an adverse effect on our business, financial condition and operating results and harm our relationships with our customers.

We operate in a highly competitive industry, and our current or future competitors may be able to compete more effectively than we do, which could have a material adverse effect on our business, revenue, growth rates and market share.

Our industry is highly competitive, with many companies of varying size and business models, many of which have their own proprietary technologies, competing for the same business as we do. Our competitors have longer operating histories and greater resources than us, and could focus their substantial financial resources to develop a competing business model, develop products or services that are more attractive to potential customers than what we offer or convince our potential customers that they should require financing arrangements that would be impractical for smaller companies to offer. Our competitors may also offer energy solutions at prices below cost, devote significant sales forces to competing with us or attempt to recruit our key personnel by increasing compensation, any of which could improve their competitive positions. Any of these competitive factors could make it more difficult for us to attract and retain customers, cause us to lower our prices in order to compete, and reduce our market share and revenue, any of which could have a material adverse effect on our financial condition and operating results. We can provide no assurance that we will continue to effectively compete against our current competitors or additional companies that may enter our markets.

In addition, we may also face competition based on technological developments that reduce demand for electricity, increase power supplies through existing infrastructure or that otherwise compete with our products and services. We also encounter competition in the form of potential customers electing to develop solutions or perform services internally rather than engaging an outside provider such as us.

18

We may be unable to complete or operate our projects on a profitable basis or as we have committed to our customers.

Development, installation and construction of energy efficiency and renewable energy projects, and operation of renewable energy projects, entails many risks, including:

|

•

|

failure to receive critical components and equipment that meet our design specifications and can be delivered on schedule;

|

|

|

•

|

failure to obtain all necessary rights to land access and use;

|

|

|

•

|

failure to receive quality and timely performance of third-party services;

|

|

|

•

|

increases in the cost of labor, equipment and commodities needed to construct or operate projects;

|

|

|

•

|

permitting and other regulatory issues, license revocation and changes in legal requirements;

|

|

|

•

|

shortages of equipment or skilled labor;

|

|

|

•

|

unforeseen engineering problems;

|

|

|

•

|

failure of a customer to accept or pay for renewable energy that we supply;

|

|

|

•

|

weather interferences, catastrophic events including fires, explosions, earthquakes, droughts and acts of terrorism; and accidents involving personal injury or the loss of life;

|

|

|

•

|

labor disputes and work stoppages;

|

|

|

•

|

mishandling of hazardous substances and waste; and

|

|

|

•

|

other events outside of our control.

|

Any of these factors could give rise to construction delays and construction and other costs in excess of our expectations. This could prevent us from completing construction of projects, cause defaults under financing agreements or under contracts that require completion of project construction by a certain time, cause projects to be unprofitable for us, or otherwise impair our business, financial condition and operating results.

Provisions in government contracts may harm our business, financial condition and operating results.

In the event that we are able to secure contracts with the federal government and its agencies, and with state and local governments, these contracts customarily contain provisions that give the government substantial rights and remedies, many of which are not typically found in commercial contracts, including provisions that allow the government to:

|

•

|

terminate existing contracts, in whole or in part, for any reason or no reason;

|

|

|

•

|

reduce or modify contracts or subcontracts;

|

|

|

•

|

decline to award future contracts if actual or apparent organizational conflicts of interest are discovered, or to impose organizational conflict mitigation measures as a condition of eligibility for an award;

|

|

|

•

|

suspend or debar the contractor from doing business with the government or a specific government agency; and

|

|

|

•

|

pursue criminal or civil remedies under the False Claims Act, False Statements Act and similar remedy provisions unique to government contracting.

|

19

Generally, government contracts contain provisions permitting unilateral termination or modification, in whole or in part, at the government’s convenience. Under general principles of government contracting law, if the government terminates a contract for convenience, the terminated company may recover only its incurred or committed costs, settlement expenses and profit on work completed prior to the termination. If the government terminates a contract for default, the defaulting company is entitled to recover costs incurred and associated profits on accepted items only and may be liable for excess costs incurred by the government in procuring undelivered items from another source. The termination payment is designed to compensate us for the cost of construction plus financing costs and profit on the work completed.

In ESPCs for governmental entities, the methodologies for computing energy savings may be less favorable than for non-governmental customers and may be modified during the contract period. In the event we enter into ESPCs, we may be liable for price reductions if the projected savings cannot be substantiated.

In addition to the right of the federal government to terminate its contracts with us, federal government contracts are conditioned upon the continuing approval by Congress of the necessary spending to honor such contracts. Congress often appropriates funds for a program on a September 30 fiscal-year basis even though contract performance may take more than one year. Consequently, at the beginning of many major governmental programs, contracts often may not be fully funded, and additional monies are then committed to the contract only if, as and when appropriations are made by Congress for future fiscal years. If one or more of our government contracts were terminated or reduced, or if appropriations for the funding of one or more of our contracts is delayed or terminated, our business, financial condition and operating results could be adversely affected.

Government contracts normally contain additional terms and conditions that may increase our costs of doing business, reduce our profits and expose us to liability for failure to comply with these terms and conditions. These include, for example:

|

•

|