Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 29, 2010

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 000-50845

MCCORMICK & SCHMICK’S SEAFOOD RESTAURANTS, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 20-1193199 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S Employer Identification No.) | |

| 1414 NW Northrup Street, Suite 700 Portland, Oregon | 97209 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (503) 226-3440

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001 per share

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates (based on the closing price on December 29, 2010 on The Nasdaq Stock Market Global Market) was $133,814,695. There were 14,835,332 shares of common stock outstanding as of March 1, 2011.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference information from the registrant’s Proxy Statement for the 2011 Annual Meeting of Stockholders.

Table of Contents

| PART I |

||||||||

| ITEM 1. | 1 | |||||||

| ITEM 1A. | 14 | |||||||

| ITEM 1B. | 20 | |||||||

| ITEM 2. | 20 | |||||||

| ITEM 3. | 20 | |||||||

| ITEM 4. | 20 | |||||||

| ITEM 4A. | 20 | |||||||

| PART II |

||||||||

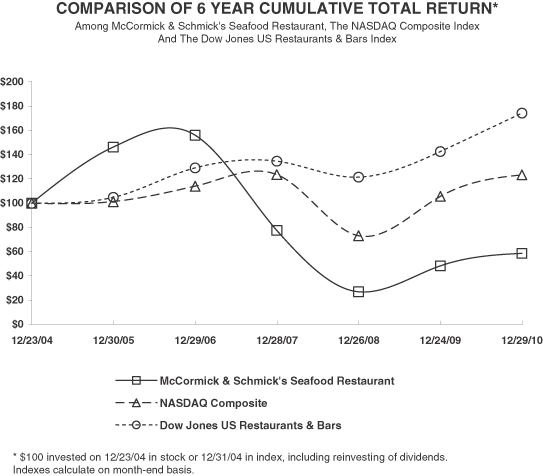

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS |

22 | ||||||

| ITEM 6. | 25 | |||||||

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

27 | ||||||

| ITEM 7A. | 43 | |||||||

| ITEM 8. | 45 | |||||||

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

67 | ||||||

| ITEM 9A. | 67 | |||||||

| ITEM 9B. | 67 | |||||||

| PART III |

||||||||

| ITEM 10. | 68 | |||||||

| ITEM 11. | 68 | |||||||

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

68 | ||||||

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

68 | ||||||

| ITEM 14. | 68 | |||||||

| PART IV |

||||||||

| ITEM 15. | 69 | |||||||

| 70 | ||||||||

| 71 | ||||||||

i

Table of Contents

Forward Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include all statements other than those that expressly state historical facts. Among others, this Annual Report includes forward-looking statements regarding our plans, expectations or beliefs concerning future events, including the following: any statements regarding future sales, costs and expenses and gross profit percentages; any statements regarding the continuation of historical trends; any statements regarding the expected number of future restaurant openings and expected capital expenditures; and any statements regarding the sufficiency of our cash balances and cash generated from operating and financing activities for future liquidity and capital resource needs. In addition, the words “believes,” “anticipates,” “plans,” “expects,” “should,” “estimates” and similar expressions are intended to identify forward-looking statements, but are not the exclusive means of identifying such statements.

Important factors that could cause actual results to differ materially from those stated or implied in the forward-looking statements include those listed in Item 1A, “Risk Factors.” These risks include, but are not limited to, our ability to maintain adequate working capital to fund our ongoing operations and necessary capital expenditures; worsening economic conditions, particularly conditions that disproportionately affect discretionary spending; failure of our growth strategy; and changes in food availability or costs. We do not undertake any duty to update forward-looking statements after the date they are made or to conform them to actual results or to changes in circumstances or expectations.

Unless the context otherwise indicates, all references in this Annual Report to the “Company,” “McCormick & Schmick’s,” “we,” “us,” or “our” or similar words are to McCormick & Schmick’s Seafood Restaurants, Inc., and its wholly-owned subsidiaries.

PART I

| ITEM 1. | BUSINESS |

Overview

McCormick & Schmick’s Seafood Restaurants, Inc. is a leading national seafood restaurant owner and operator in the affordable upscale dining segment. We have successfully grown our business during the past 39 years by focusing on serving a broad selection of fresh seafood. As of December 29, 2010, we had 96 restaurants, including 89 restaurants in the United States, of which one is operated pursuant to a management agreement, and seven restaurants in Canada under The Boathouse name.

Our menu is printed daily and includes an extensive selection of international, national, regional and local varieties of seafood. Our signature “Fresh List,” prominently displayed at the top of our daily-printed menus, features 20 to 30 varieties of fresh seafood, based on seasonality, product availability, price and guest preferences. We also offer several alternatives to seafood, including high quality beef, creative salads and fresh pasta dishes.

Our restaurants are designed to capture the distinctive characteristics of each local market, positioning us to compete successfully in a sector comprised primarily of locally owned and operated seafood restaurants. We seek to create an inviting atmosphere which enables us to attract a diverse guest base of men and women, primarily ages 30 to 60, typically college-educated and in the middle to upper-middle income brackets. We believe the combination of our restaurant atmosphere, our extensive menu offerings, superior service and broad range of price points appeals to a diverse guest base from casual diners, families and tourists to business travelers and special occasion diners.

1

Table of Contents

We believe we are the only high quality seafood restaurant that operates on a national scale, and we have successfully differentiated ourselves from our competitors by focusing on the following core strengths.

Fresh Seafood

Our primary business focus for more than 39 years has been to consistently offer a broad selection of fresh seafood, which commands strong loyalty from our guests. Our daily-printed menu typically includes an extensive selection of nationally available species such as Alaskan king crab, Atlantic lobster and Alaskan halibut, as well as regional and seasonal products such as wild king salmon, Louisiana redfish and Columbia River sturgeon to name a few. All of our restaurants also offer an extensive variety of cold water oysters. The executive chef at the majority of our restaurants tailors the menu, at least once daily, based on the availability and price of different varieties of fresh seafood, as well as local guest preferences.

Our menu’s signature “Fresh List”, featuring 20 to 30 fresh seafood varieties sourced each day, differentiates us from many of our competitors. Through our close and long-standing relationships with a broad network of reputable local and national seafood vendors, we are able to offer a wide variety of consistently fresh, high quality seafood from international, national, regional and local waters. We encourage our vendors to adopt preferred and sustainable fishing practices to guarantee the current and future quality and supply of our seafood. During our daily “fresh talk,” the executive chef at each of our restaurants educates our restaurant staff on the menu items of the day so we can effectively communicate the sourcing, freshness, quality and method of preparation of our products to our guests.

In 2010 we completed the roll-out of several enhancements to our menu offerings that include a diversified Small Plate section ranging in price from $5.95 to $9.95, a sushi selection, including five to seven traditional and unique offerings, and a Seafood Bar section that offers items such as shrimp, oysters and crab by the piece, so guests can build their own combinations.

Attraction of Our Full-Service Bar

Our bar operations are an integral part of the McCormick & Schmick’s brand and central to our broad appeal. This philosophy dates back to our first restaurant, Jake’s Famous Crawfish, the success of which was largely driven by its bar operation, enhancing the dining room business by creating a social environment and building clientele. Our bar operation remains a cornerstone of our restaurant concept today, showcasing our commitment to traditionalism and quality. We attract patrons to our bar as a final destination where they can enjoy a broad selection of liquors, wines and beers in a traditional yet lively environment. Our cocktails are created using traditional methods and are hand-shaken, hand-poured and made with freshly squeezed juices, underlining our focus on product quality. We also offer value-priced food items in our bars during our happy hour, which tends to attract younger guests whom we aim to secure as regular restaurant guests.

As a result of our focus on our bar operations as an integral part of our business, our bars drive sales in our dining rooms. We run our bar operations as a profit center rather than a mere holding area for diners. In 2010, bar sales accounted for approximately 27.8% of our gross sales and contributed higher gross margins than food sales. The higher gross margins we generate from bar sales allows us the flexibility to offer lower prices on some of our bar food menu items, helping us maintain our broad guest appeal.

Broad Appeal of Our Concept

We appeal to a broad range of guests by providing an attractive price-value proposition, with prices that are generally more affordable than those of our upscale competitors. Additionally, we offer service that is superior to that of most other restaurants. The price of a typical meal, including beverages, ranges from $16 to $33 for lunch and $36 to $61 for dinner, with averages of approximately $23 and $50, respectively. Over the past few years, we

2

Table of Contents

have enhanced our menu to offer our guests more affordable dining options by including a selection of lower priced, yet still high-quality items on our menus for both lunch and dinner. Even the price sensitive diner values our superior service, and we have received recognition from our guests and industry awards for our service quality. The combination of our high quality seafood, pricing strategy and guest service enables us to attract a broad guest demographic. Most of our guests are 30 to 60 years old, primarily college-educated, in the middle to upper-middle income brackets. Our bar operations allow us to also capture the 25 to 35 year old professionals, positioning us to attract a younger clientele as dedicated restaurant guests.

In 2010, we continued to implement a number of new initiatives launched in mid-2009 to evolve our concept with the primary goals of increasing our connection to our current guests, broadening our guest base to include a younger audience, increasing our brand relevance, and improving our overall satisfaction ratings with our guests. This strategy involved rebranding our bar experience, expanding our culinary offerings, and synergizing our marketing efforts to include more digital and social marketing strategies to complement traditional marketing tactics.

More recently, we have announced a multi-faceted program aimed at building upon the successes of the past 39 years, strengthening our connectivity with our core guests while also increasing the visibility of our brand among a broader audience. This initiative is designed to bolster our existing restaurant management and staff, continue our cost-control programs, and improve our menu offerings in a way that increases guest satisfaction, improves traffic trends, and builds a better connection with a younger audience.

Entrepreneurial Culture with Corporate Control

A key component of our success for more than 39 years has been our commitment to promoting and sustaining an entrepreneurial culture throughout our restaurants, while maintaining strong corporate oversight and financial controls. Within this strong corporate infrastructure, each restaurant has profit and loss responsibility and a high degree of operating autonomy. The executive chef at each restaurant has the flexibility, within clearly defined corporate guidelines, to structure menus that cater to guest preferences in that restaurant’s market and respond to changes in product availability and market conditions. We offer quarterly and annual cash performance incentives to certain exempt employees at the restaurant level based on the restaurant’s revenues, costs and profitability, compliance with corporate administrative and payroll guidelines, and the success of other initiatives, such as local community involvement.

Our company’s strong culture helps us to attract and retain highly qualified and motivated individuals. Our average annual retention rate for our restaurant general managers and executive chefs is approximately 80%. Our decentralized, employee-oriented, entrepreneurial culture creates a sense of pride in our company and allows us to ensure quality service execution at the restaurant level. The stability of our management team and operating personnel, coupled with our disciplined but entrepreneurial culture, positions us for the continued success and growth of our concept.

As we seek to build upon our core strengths, we are implementing a variety of measures designed to improve our financial performance. These initiatives include a comprehensive service training and recertification program for all management and staff, committing additional financial resources to add depth to our management teams, and upgrading our “back-of-the-house” systems to provide additional support for day-to-day management. These investments do not stop at the individual restaurant levels: we also have added two new members to our Board of Directors with specific skills in human capital and branding strategy, and are actively searching to fill three key executive management positions to support our long-term strategic plan.

Portability of Our Brand

We have expanded the McCormick & Schmick’s Seafood Restaurant concept throughout the United States and have competed successfully with both national and regional restaurant chains and independent local

3

Table of Contents

operators, due in part to the flexibility of our real estate model and our nationwide infrastructure. As of December 29, 2010, we had 96 restaurants, including 89 restaurants in the United States, of which one is operated pursuant to a management agreement, and seven restaurants in Canada operating under The Boathouse name.

Our restaurants are designed to have broad consumer appeal. We customize our restaurant design and appearance to appeal to local consumer affinities and preferences, and have many restaurants located in buildings that have local significance, including some historic buildings. We have a proven track record of successfully opening restaurants in a variety of sizes, typically ranging from 6,000 to 14,000 square feet and in a number of real estate formats, including both freestanding and in-line locations. The typical size for our current restaurant prototype is approximately 8,000 square feet. The flexibility of our real estate model is a competitive advantage, allowing us to cost-effectively and opportunistically open restaurants in attractive markets without being constrained by a standard prototype or other limiting real estate factors.

We compete on a restaurant-by-restaurant basis with independent local restaurant operators while leveraging the operating strengths of our national infrastructure. The breadth and scale of our restaurant operations and our more than 39 years of experience in the business give us a competitive advantage in terms of the quality, sourcing and freshness of our menu offerings and flexibility of price points, making our model difficult to replicate. This competitive advantage contributes to our brand’s reputation for quality and service in the affordable upscale dining sector, which commands strong loyalty from our guests.

Our Growth Strategy

Our flexible business model, combined with our fresh menu offerings, professional customer service and inviting restaurant environment, provide us with significant opportunities to further grow our business. Key elements of our growth strategy include the following:

Market Expansion

We remain focused on the disciplined growth of our McCormick & Schmick’s brand in our existing markets. We have established the necessary market analysis and site selection procedures for identifying new restaurant opportunities in these markets. In particular, we will continue to evaluate opportunities in affluent suburban areas near existing restaurants in downtown areas to better diversify our presence in existing markets. This strategy enables us to achieve a higher degree of market penetration and brand awareness, resulting in increased repeat business from our broad and diverse customer base. Additionally, we intend to further leverage the economies of scale of our operations to enhance our competitive advantage against independent local competitors, principally in the areas of advertising, marketing, purchasing and distribution infrastructure.

In selecting new market opportunities, we continue to focus on downtown and affluent suburban areas that have large middle to upper-middle income populations, have high guest traffic from thriving businesses or retail markets, and that are convenient for and appealing to business and leisure travelers. We will continue to promote the McCormick & Schmick’s brand image and our broad appeal by opening new restaurants in prime real estate locations and by customizing each new restaurant to the local market. Based on our strategic plan we may or may not open additional restaurants in 2011, but we currently expect that most of our growth will result from reinvestment in the current portfolio.

The acquisition of The Boathouse restaurants in 2007 marked our entry into the Canadian market through a well established brand known for its premier locations, broad appeal and operational excellence. We initially acquired five existing restaurants and one under construction, which we opened in October 2007, in the greater Vancouver, B.C. area. Our acquisition of The Boathouse restaurants was our first significant expansion through acquisition. In 2010, we opened our seventh The Boathouse restaurant in the greater Vancouver, B.C. area. We continue to evaluate acquisition opportunities in new markets and existing markets as they arise, paying particular attention to how restaurants or restaurant groups would fit with our existing restaurants, culture and business plan.

4

Table of Contents

Reinvestment in existing restaurants

Just as important as growth opportunities outside of our restaurant base is the opportunity to reinvest in our existing restaurants to expand the top line sales potential. Beginning in 2009 and throughout 2010, we implemented upgrades in several restaurant locations to patios and/or restaurant décor, as well as to audio-visual equipment. Early in 2011 we announced a significant portfolio upgrade, which we expect will span the next two to three years, with a goal of improving long-term top-line sales and restaurant-level margins, leveraging our current leases, and refining our key design principles. We are assessing individual restaurant locations across our portfolio, with a goal of enhancing our customers’ experience while tailoring our enhancements based on a variety of factors including age of the location, competitive market analysis and local guest preferences. Some of our locations will require only basic cosmetic refreshing, while others will undergo more significant remodeling. We expect that this program will result in restaurant designs which blend traditional elements that have been instrumental to our success over the past four decades, with more updated features that will better connect with current guest preferences in each market. We have budgeted up to $15 million for this program in 2011, a portion of which is intended to cover deferred capital maintenance.

Capture of Ancillary Business Opportunities

We will continue to pursue secondary opportunities that are complementary to our primary concept and further our growth objectives. We operate a collection of individually branded restaurants that include The Heathman Restaurant, McCormick & Kuleto’s Seafood Restaurant, William Douglas Steakhouse, Jake’s Famous Crawfish, Jake’s Grill and Spenger’s Fresh Fish Grotto. We also operate seven restaurants under the name M&S Grill and seven restaurants in Canada under the name The Boathouse Restaurants. Our uniquely branded concepts offer an alternative menu to that of our McCormick and Schmick’s branded seafood restaurants. We will also continue to consider catering opportunities and management agreements with hotels. As of December 29, 2010, we operated one restaurant under a management agreement.

Unit Level Economics

Our average cash investment per restaurant opened since 1997 has been approximately $2.9 million, including leasehold improvements, furniture, fixtures and equipment, net of landlord incentive allowances. We have reduced the size of our restaurant prototype to facilitate our entry into a greater variety of markets and provide us with increased flexibility with site selection. We anticipate that our average investment per restaurant will be between approximately $2.2 million and $3.2 million going forward.

The average annualized restaurant sales volume in 2010 for restaurants opened as of December 29, 2010 was approximately $3.7 million. Restaurants opened prior to 2003, were, on average, approximately 10,000 square feet each. Since 2002, we have added 61 company-owned restaurants (including the restaurants acquired in The Boathouse acquisition), which average approximately 8,000 square feet each.

Menu, Food Preparation, Quality Control and Purchasing

Most of our menu items are prepared from scratch daily at each restaurant and each order is assembled when the order is placed with the kitchen staff. Each restaurant has an executive chef responsible for overseeing kitchen operations, including planning the daily-printed menu and ordering necessary ingredients and supplies. At a typical McCormick and Schmick’s restaurant, the executive chef is assisted by one to three sous chefs, who help to manage food preparation and service timing.

We maintain strict quality standards at all of our restaurants. We require each of our employees to adhere to these standards, and it is the responsibility of the general manager and the executive chef at each restaurant to ensure these standards are upheld. We are committed to providing our guests with high quality, fresh products and superior service. We regularly hold regional management meetings designed to re-emphasize McCormick & Schmick’s philosophy, culture, standards of operation and culinary development.

5

Table of Contents

At the restaurant level, purchasing is primarily directed by the executive chef, who is trained in our purchasing practices and philosophy and is supervised by an experienced regional chef. This provides the freshest ingredients and products while improving operating efficiencies between purchase and use. Each executive chef determines the daily requirements for food ingredients, products and supplies. The executive chef orders accordingly from local suppliers and regional and national distributors selected by our Director of Purchasing. Fresh seafood is sourced through multiple vendors in varying geographic regions and delivered daily to each restaurant. Through use of our standard training materials and our commitment to the hiring, development and training of chefs, we are able to maintain high standards and guidelines for our regularly purchased seafood species.

The majority of our restaurants primarily purchase seafood from a network of preferred vendors we have identified as consistently supplying seafood that meets our high standards. The identification and selection of seafood suppliers is reviewed regularly based on product quality, sanitation, fishing practices, pricing and customer service. We prefer suppliers who use day-boats rather than those who are at sea for multiple days because their product is typically fresher. Our national and regional presence allows us to achieve better quality and pricing terms for key products, such as fresh fin fish and shellfish, than most of our competitors. In 2010, other food products, such as high quality beef and dry goods, were sourced primarily from SYSCO Corporation, a national food distributor, while liquor, beer and wine were, and will continue in 2011 to be purchased from local distributors. SYSCO accounted for approximately 21% of our food purchases in 2010. No other vendor accounted for more than 10% of our purchases in 2010.

We terminated our existing supply agreement with SYSCO Corporation as of January 31, 2011. We entered into a new Foodservice Distribution Agreement with Market Advantage, Inc., which became effective on January 31, 2011 and expires on January 31, 2014, and we believe that this shift will improve our cost structure while allowing us to maintain the quality our customers have come to expect.

Restaurant Design and Atmosphere

Our restaurant designs and decor are intended to capture distinctive attributes of each local market, varying from traditional New England-style fish houses to classic contemporary dinner houses with waterfront views. Some of our restaurants are located in historic buildings, reinforcing our commitment to local design elements and further promoting the appeal and ambience of our restaurants. Our flexible approach to restaurant design contributes to the uniqueness of each restaurant and allows us to successfully compete in a sector comprised primarily of independent, locally-owned and operated seafood restaurants.

Restaurant Locations, Lease Arrangements and Management Fee Arrangements

As of December 29, 2010 we operated 96 restaurants, including 89 restaurants in the United States, of which one is operated pursuant to a management agreement, and seven restaurants in Canada under The Boathouse name. We lease all but two of our restaurant sites, one we operate under a management agreement and one we own. Terms vary by restaurant, but we generally lease space for 10 to 20 years with one to three five-year renewal options.

6

Table of Contents

The following is a schedule of restaurants we operated as of December 29, 2010:

| Restaurant Name |

City | Year Added | ||||||

| Alabama |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Birmingham | 2004 | ||||||

| Arizona |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Phoenix | 1999 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Scottsdale | 2008 | ||||||

| California |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Irvine | 1989 | ||||||

| McCormick & Kuleto’s Seafood Restaurant |

San Francisco | 1991 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Los Angeles | 1992 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Pasadena | 1993 | ||||||

| McCormick & Schmick’s a Pacific Seafood Grill |

Beverly Hills | 1994 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

El Segundo | 1998 | ||||||

| Spenger’s Fresh Fish Grotto |

Berkeley | 1999 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

San Jose | 2004 | ||||||

| McCormick & Schmick’s Seafood Restaurant* |

San Diego | 2004 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Burbank | 2006 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Sacramento | 2007 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Santa Ana | 2007 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Anaheim | 2008 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Roseville | 2009 | ||||||

| Colorado |

||||||||

| McCormick’s Fish House & Bar |

Denver | 1987 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Denver | 2004 | ||||||

| District of Columbia |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Washington | 1996 | ||||||

| M&S Grill |

Washington | 1998 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Washington | 2004 | ||||||

| Florida |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Orlando | 2002 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Boca Raton | 2006 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Naples | 2008 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

West Palm Beach | 2010 | ||||||

| Georgia |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Atlanta | 2000 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Atlanta | 2002 | ||||||

| Illinois |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Chicago | 1998 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Chicago | 2006 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Schaumburg | 2007 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Oak Brook | 2007 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Skokie | 2007 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Rosemont | 2008 | ||||||

| Indiana |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Indianapolis | 2005 | ||||||

| Maryland |

||||||||

| McCormick & Schmick’s Seafood Restaurant |

Baltimore | 1998 | ||||||

| McCormick & Schmick’s Seafood Restaurant |

Bethesda | 1999 | ||||||

7

Table of Contents

| Restaurant Name |

City | Year Added | ||

| M&S Grill |

Baltimore | 2003 | ||

| McCormick & Schmick’s Seafood Restaurant |

Annapolis | 2007 | ||

| McCormick & Schmick’s Seafood Restaurant |

National Harbor | 2008 | ||

| Massachusetts |

||||

| McCormick & Schmick’s Seafood Restaurant |

Boston | 2000 | ||

| McCormick & Schmick’s Seafood Restaurant |

Boston | 2001 | ||

| Michigan |

||||

| McCormick & Schmick’s Seafood Restaurant |

Troy | 2001 | ||

| Minnesota |

||||

| McCormick & Schmick’s Seafood Restaurant |

Minneapolis | 2000 | ||

| M&S Grill |

Minneapolis | 2006 | ||

| McCormick & Schmick’s Seafood Restaurant |

Edina | 2008 | ||

| Missouri |

||||

| McCormick & Schmick’s Seafood Restaurant |

Kansas City | 2000 | ||

| M&S Grill |

Kansas City | 2005 | ||

| McCormick & Schmick’s Seafood Restaurant |

St. Louis | 2009 | ||

| Nevada |

||||

| McCormick & Schmick’s Seafood Restaurant |

Las Vegas | 1998 | ||

| New Jersey |

||||

| McCormick & Schmick’s Seafood Restaurant |

Hackensack | 2002 | ||

| McCormick & Schmick’s Seafood Restaurant |

Bridgewater | 2003 | ||

| McCormick & Schmick’s Seafood Restaurant |

Atlantic City | 2008 | ||

| McCormick & Schmick’s Seafood Restaurant/William Douglas Steakhouse |

Cherry Hill | 2008 | ||

| New York |

||||

| McCormick & Schmick’s Seafood Restaurant |

New York | 2004 | ||

| North Carolina |

||||

| McCormick & Schmick’s Seafood Restaurant |

Charlotte | 2005 | ||

| McCormick & Schmick’s Seafood Restaurant |

Charlotte | 2005 | ||

| McCormick & Schmick’s Seafood Restaurant |

Raleigh | 2008 | ||

| Ohio |

||||

| McCormick & Schmick’s Seafood Restaurant |

Columbus | 2006 | ||

| McCormick & Schmick’s Seafood Restaurant |

Cincinnati | 2006 | ||

| McCormick & Schmick’s Seafood Restaurant |

Cleveland | 2007 | ||

| McCormick & Schmick’s Seafood Restaurant |

Dayton | 2007 | ||

| Oregon |

||||

| Jake’s Famous Crawfish |

Portland | 1972 | ||

| McCormick’s Fish House & Bar |

Beaverton | 1981 | ||

| McCormick & Schmick’s Harborside at the Marina |

Portland | 1985 | ||

| Jake’s Grill / Jake’s Catering |

Portland | 1994 | ||

| The Heathman Restaurant |

Portland | 2000 | ||

| McCormick & Schmick’s Seafood Grill |

Tigard | 2005 | ||

| Pennsylvania |

||||

| McCormick & Schmick’s Seafood Restaurant |

Philadelphia | 2001 | ||

| McCormick & Schmick’s Seafood Restaurant |

Pittsburgh | 2005 | ||

| McCormick & Schmick’s Seafood Restaurant |

Pittsburgh | 2007 | ||

| Rhode Island |

||||

| McCormick & Schmick’s Seafood Restaurant |

Providence | 2004 | ||

8

Table of Contents

| Restaurant Name |

City | Year Added | ||

| Texas |

||||

| McCormick & Schmick’s Seafood Restaurant |

Houston | 1999 | ||

| McCormick & Schmick’s Seafood Restaurant |

Dallas | 2003 | ||

| McCormick & Schmick’s Seafood Restaurant |

Austin | 2004 | ||

| McCormick & Schmick’s Seafood Restaurant |

Austin | 2007 | ||

| McCormick & Schmick’s Seafood Restaurant |

Houston | 2008 | ||

| McCormick & Schmick’s Seafood Restaurant |

Houston | 2010 | ||

| Virginia |

||||

| McCormick & Schmick’s Seafood Restaurant |

Reston | 1997 | ||

| McCormick & Schmick’s Seafood Restaurant |

McLean | 2000 | ||

| M&S Grill |

Reston | 2004 | ||

| McCormick & Schmick’s Seafood Restaurant |

Arlington | 2004 | ||

| McCormick & Schmick’s Seafood Restaurant |

Virginia Beach | 2007 | ||

| Washington |

||||

| McCormick’s Fish House & Bar |

Seattle | 1977 | ||

| McCormick & Schmick’s Seafood Restaurant |

Seattle | 1984 | ||

| McCormick & Schmick’s Catering at the Museum of Flight in Seattle |

Seattle | 1994 | ||

| McCormick & Schmick’s Harborside on Lake Union |

Seattle | 1996 | ||

| McCormick & Schmick’s Seafood Restaurant |

Bellevue | 2005 | ||

| Wisconsin |

||||

| McCormick & Schmick’s Seafood Restaurant |

Milwaukee | 2008 | ||

| Canada |

||||

| The Boathouse Restaurant |

Vancouver, B.C. | 2007 | ||

| The Boathouse Restaurant |

New Westminster, B.C. | 2007 | ||

| The Boathouse Restaurant |

White Rock, B.C. | 2007 | ||

| The Boathouse Restaurant |

Richmond, B.C. | 2007 | ||

| The Boathouse Restaurant |

Horseshoe Bay, B.C. | 2007 | ||

| The Boathouse Restaurant |

Port Moody, B.C. | 2007 | ||

| The Boathouse Restaurant |

Vancouver, B.C. | 2010 | ||

| * | Operated under a management agreement. |

Site Selection

We believe our site selection is critical to our growth strategy and financial results. We carefully consider potential markets and devote a substantial amount of time and effort to evaluate each potential restaurant site. We identify new restaurant opportunities through an established real estate broker network and developer relationships. Our site specifications are flexible. We believe this allows us to consider a broader range of possible locations than most of our regional and national competitors. The criteria we consider in developing our expansion plans and in selecting new restaurants include:

| • | Population density, and income and education level of the population; |

| • | Competitive conditions, presence of other retail or traffic generators and menu prices; |

| • | Estimated return on investment; |

| • | Available square footage and lease economics; |

| • | The proximity of hotels and office space and the density of pedestrian and vehicle traffic; |

| • | The suitability of the site for an affordable, upscale restaurant with a traditional ambience; |

| • | Capacity expansion possibilities; and |

| • | Management’s experience in the market and the proximity of any of our existing restaurants. |

9

Table of Contents

A majority of our restaurants are located in high-traffic, metropolitan areas and several are located in historic buildings. We believe there are many additional markets both in the United States and internationally that meet our demographic and geographic profiles.

Of our 96 restaurants, including one we operate under a management agreement, 16, or 17%, were opened or acquired within the last three years and 39, or 41%, were opened or acquired within the last five years. In the past few years, economic conditions have caused us to slow our development. We opened two restaurants in 2009 and three restaurants in 2010. Based on capital availability and economic conditions, we may or may not open additional restaurants in 2011, but we currently expect that most of our growth will take the form of reinvestment in our current portfolio. The typical lead-time from the selection of a new construction location to the opening of a restaurant is approximately 12 to 15 months. In certain circumstances involving conversions of existing restaurants this time period could be shorter. We evaluate acquisition opportunities as they arise, paying particular attention to how restaurants or restaurant groups would fit with our existing restaurants and our business plan.

In addition to our ongoing portfolio management process, we announced early in 2011 that we would undertake a significant capital improvement program in which we evaluate each of our properties on a site- and market-specific basis, taking into account such factors as age of the location, comprehensive market analysis, customer profile, lease terms and options, and location characteristics. Expected enhancements may range from basic cosmetic refreshing to more extensive remodeling which will, in some cases, require temporary closure of a location. We have budgeted up to $15 million for locations that will undergo this process during 2011.

Marketing and Advertising

The goals of our marketing and advertising efforts are to:

| • | Increase comparable restaurant sales by attracting new guests; |

| • | Increase the frequency of visits by our current guests; |

| • | Support new restaurant openings to achieve sales and profit goals; and |

| • | Communicate and promote the uniqueness, appeal, quality and consistency of our brand. |

In 2010, our marketing and advertising expenditures were approximately 1% of revenues.

Local Marketing

Our approach to local marketing is as unique as each of our restaurants. From the time we start construction on a new location to decades after we have opened a restaurant, we strive to build a connection to the guests and the community around our restaurants. For each location, our marketing and local and regional management teams work together to build a variety of customized local marketing initiatives to support the growth of that location.

For new restaurants, we work with a public relations firm to establish our restaurant with the local media, to publicize our restaurant opening and to generate awareness of our brand. We host social events to generate publicity and build relationships with community and thought leaders before the official opening of a restaurant. We work to build partnerships that add to the experience we are able to offer our guest. We also promote the new location through targeted print, broadcast and digital media.

For each of our locations, we advertise with local daily and weekly publications, key monthly magazines and local business journals in urban markets. We also promote our destination locations in travel and tourism publications. We periodically offer promotional certificates and work to build relationships with organizations in the travel and convention industries, such as hotels, travel agents, convention centers and local retailers, to further enhance our brand, and to target specific guest groups. We actively work to build and promote local initiatives to our frequent and preferred guests using our e-marketing platform.

10

Table of Contents

We encourage all of our restaurants sponsor community events and support charitable and non-profit organizations through both monetary and in-kind donations. We believe that, in addition to benefiting our local communities, these activities generate positive media attention and publicity for our brand and enhance our local public image.

National Advertising and Public Relations

For many years, the mainstay of our national advertising program has been daily print advertising through USA Today and travel periodicals such as WHERE magazine. In the last two years, we have worked to expand our guest base and our reach through a more integrated strategy to market our brand. This includes an aggressive approach to leveraging digital media channels. Our digital approach includes online advertising, social media outreach through Facebook, Twitter and Foursquare, and third-party online outlets such as Yelp! and Google.

Additionally, we work with a national public relations firm to deliver our restaurants’ core messages to a broad variety of print, broadcast and online media outlets and to create publicity programs that reinforce our brand image on a national scale. Our fully integrated public relations effort is instrumental in delivering a wide range of messages from brand differentiation, to seasonal promotions and culinary initiatives.

We also utilize our e-marketing platform for communications on a national scale to both our preferred guests and e-club members with a monthly newsletter called Fresh Talk and through periodic seasonal and promotional emails. Through all our communications, national or local, we seek to differentiate our brand by highlighting our commitment to premium seafood, aged steaks and fine wines.

Operations

Restaurant Management

Our U.S. restaurant operations are managed by regional managers who are led by a vice president who oversees our restaurant operations and a vice president who oversees our culinary program. Each of our vice presidents reports to our executive vice president of operations.

Our typical restaurant management team consists of a general manager and an executive chef, one to three assistant managers, one to three sous chefs and, in some cases, a meeting planner/banquet coordinator. The remaining restaurant-level employees are hourly personnel varying in number based on restaurant size. Our typical restaurant employs 50 to 80 full-time and part-time employees. The general manager is responsible for all management functions, including purchasing (other than for food), hiring and terminations and oversight of restaurant-level bookkeeping and cash controls. The executive chef is responsible for managing all kitchen functions, including training, menu design and food purchasing, quality and presentation.

We emphasize frequent interaction between our vice presidents, regional managers and restaurant level management. As a result, neither vice presidents nor regional managers operate out of our corporate office and are routinely accessible to restaurant staff.

All management levels in operations, from vice presidents to assistant managers, participate in incentive bonus programs. These incentive programs are designed to establish specific goals and objectives and to ensure accountability and reward performance.

Restaurant Operations

Our restaurants are generally open 365 days each year, serve lunch and dinner and are generally open from 11:00 a.m. to 11:00 p.m. Sunday through Thursday and 11:00 a.m. to 1:00 a.m. Friday and Saturday. In 2010, dinner comprised approximately 77% of revenues, while lunch comprised approximately 23% of revenues. To accommodate guests who have limited time available during lunch, we offer a 45-minute lunch guarantee.

11

Table of Contents

Additionally, we offer catering and banquet services both in our restaurants and at other locations as guests’ request. Our presence in and near hotels enables us to expand the reach of our banquet offerings.

Employees

As of December 29, 2010 we employed 6,582 persons, of whom 672 were salaried and 5,910 were hourly personnel. None of our employees are represented by unions and, in general, we consider our relationship with our employees to be excellent. Our employees are summarized by major functional area in the table below.

| Functional Area |

Number of Employees |

|||

| VPs/regional managers/regional chefs |

18 | |||

| General managers |

93 | |||

| Assistant managers |

240 | |||

| Executive chefs |

93 | |||

| Sous chefs |

153 | |||

| Non-salaried restaurant staff |

5,872 | |||

| Corporate salaried |

75 | |||

| Corporate non-salaried |

38 | |||

| Total |

6,582 | |||

Management Information Systems

All of our information processing is managed from our headquarters in Portland, Oregon. Point-of-sale terminals at each restaurant allow us to generate the daily reports needed to manage our restaurants and our business. These reports include, among other things, daily and weekly revenues, guest counts, meal period sales breakouts and food and liquor consumption. The data from the point-of-sale system is electronically transferred each night to a third party intranet provider, with the data then accessible by us through the Internet. Financial operating results are reviewed at the corporate office and studied by restaurant level and regional management. Variances from expectations are analyzed and addressed at frequent financial meetings.

Industry and Competition

Industry

We operate in a highly competitive industry that is affected by changes in consumer eating habits and dietary preferences, population trends and traffic patterns, and local and national economic conditions. Key competitive factors in the industry include the taste, quality and price of the food products offered, quality and speed of guest service, brand name identification, attractiveness of facilities, restaurant location, and overall dining experience. We believe we compete favorably with respect to each of these factors and successfully have navigated, and continue to navigate, the following obstacles often faced by seafood restaurants:

| • | Developing and maintaining consistent, reliable sources of high quality, fresh seafood; |

| • | Difficulty in hedging against increases in seafood costs; |

| • | Complications in preparing and handling seafood; and |

| • | Regional variations in consumer tastes for seafood products vary. |

Although we believe we compete favorably with respect to each of these factors, there are a substantial number of restaurant operations that compete directly and indirectly with us, many of which have significantly greater financial resources, higher revenue and greater economies of scale. (See “Risk Factors”).

12

Table of Contents

Competition

While we compete with a range of restaurant operators for consumers’ dining preferences and with both restaurants and retailers for site locations and personnel requirements, we feel we are uniquely positioned between the premium casual restaurants and fine dining establishments, as such, we consider our principal competitors to include the following:

| • | Independent, local seafood restaurants; |

| • | Regional seafood restaurant concepts; |

| • | National upscale casual restaurants; and |

| • | Upscale “steak and chop” restaurants. |

Seasonality

Our business is subject to seasonal fluctuations. Historically, sales in most of our restaurants have been higher during the second and fourth quarter of each year due, in part, to increased restaurant sales during holiday seasons.

Government Regulation

Our restaurants are subject to various federal, state and local government regulations, including those relating to employees, the preparation and sale of food and the sale of alcoholic beverages. These regulations affect our restaurant operations and our ability to open new restaurants.

Each of our restaurants must obtain licenses from regulatory authorities to sell liquor, beer and wine, and each restaurant must obtain a food service license from local health authorities. Each liquor license must be renewed annually and may be revoked at any time for cause, including violation by us or our employees of any laws and regulations relating to the minimum drinking age, advertising, wholesale purchasing and inventory control. In certain jurisdictions where we operate the number of alcoholic beverage licenses available is limited and licenses are traded at market prices.

We are subject to “dram shop” statutes in some states. These statutes generally allow a person injured by an intoxicated person to recover damages from an establishment that wrongfully served alcoholic beverages to the intoxicated person.

Various federal and state labor laws govern our relationship with our employees and affect operating costs. These laws include minimum wage requirements, overtime pay, unemployment tax rates, workers’ compensation rates, and citizenship requirements. Additional government-imposed increases in minimum wages, overtime pay, paid leaves of absence and mandated health benefits, increased tax reporting and tax payment requirements for employees who receive gratuities, or a reduction in the number of states that allow tips to be credited toward minimum wage requirements would increase our labor costs and could harm our operating results and financial condition.

Federal legislation, and state and local legislation in some areas where we operate restaurants has been adopted that will require us to provide nutritional information to our customers. Similar legislation has been proposed in other areas where we operate. Laws in several states and local jurisdictions require specific classes of restaurants to publish nutritional information on menus or to make that information available to customers. The federal Patient Protection and Affordable Care Act, signed into law March 23, 2010, will require restaurants with 20 or more locations operating under the same trade name to publish calorie counts and other information on menus and menu boards, and to make detailed nutritional information about standard menu items available to customers upon request. Compliance with the new law will not be required until after the Food and Drug Administration (FDA) issues regulations. The FDA is required to publish proposed regulations by March 23, 2011.

13

Table of Contents

Available Information

We make available free of charge on or through our website at www.mccormickandschmicks.com our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we file these materials with the Securities and Exchange Commission. These materials are also available on the Security and Exchange Commission’s website at www.sec.gov. The information on our website is not part of this Annual Report and is not otherwise to be considered filed with or furnished to the Securities and Exchange Commission.

| ITEM 1A. | RISK FACTORS |

Financial Risk Factors

Our operating results may fluctuate significantly. The failure of our existing or new restaurants to achieve expected results could have a negative impact on our revenues and financial results, including potential impairment of long-lived assets. Our results could fall below the expectations of securities analysts and investors due to seasonality and other factors, resulting in a decline in our stock price.

The results achieved by our restaurants may not be indicative of longer term performance or the potential market acceptance of restaurants in other locations. New restaurants we open may not have operating results similar to those of previously opened restaurants. The failure of restaurants to perform as predicted could result in an impairment charge, which could negatively impact our results of operations. Our operating results may fluctuate significantly because of several factors, including:

| • | Our ability to achieve and manage our planned expansion; |

| • | Our ability to achieve market acceptance, particularly in new markets; |

| • | Our ability to raise capital, or the availability of expansion capital generally; |

| • | Changes in the availability and costs of food; |

| • | The loss of key management personnel; |

| • | The concentration of our restaurants in specific geographic areas; |

| • | Our ability to protect our name and logo and other proprietary information; |

| • | Changes in consumer preferences or discretionary spending; |

| • | Fluctuations in the number of visitors or business travelers to our restaurants; |

| • | Health concerns about seafood or other foods; |

| • | Our ability to attract, motivate and retain qualified employees; |

| • | Increases in labor costs; |

| • | The impact of federal, state or local government regulations relating to our employees or the sale or preparation of food and the sale of alcoholic beverages; |

| • | The impact of litigation; |

| • | The effect of competition in the restaurant industry; |

| • | The effect of widespread adverse weather conditions; |

| • | Economic trends generally; |

| • | The ability of real estate developers, landlords and co-tenants, to meet commitments to fill space in developments where our restaurants are to be located, which would decrease guest traffic to our restaurants; and |

| • | Reduced corporate expenditures on meetings and/or conventions may impact our private dining business. |

14

Table of Contents

Our business also is subject to seasonal fluctuations. Historically, sales in most of our restaurants have been higher during the second and fourth quarter of each year. As a result, our quarterly and annual operating results and restaurant sales may fluctuate significantly as a result of seasonality and the factors discussed above. Accordingly, results for any one fiscal quarter are not necessarily indicative of results to be expected for any other quarter or for any year and comparable restaurant sales for any particular future period may decrease. Our operating results may be different than the expectations of securities analysts and investors. In that event, the price of our common stock may fluctuate.

Failure to establish, maintain and apply adequate internal control over our financial reporting could affect our reported results of operations.

We are subject to the ongoing internal control provisions of Section 404 of the Sarbanes-Oxley Act of 2002. These provisions provide for the identification of material weaknesses in internal control over financial reporting, which is a process to provide reasonable assurance regarding the reliability of financial reporting for external purposes in accordance with accounting principles generally accepted in the United States. If we experience a material weakness in internal controls, there can be no assurance that we will be able to remediate that material weakness in a timely manner or maintain all of the controls necessary to remain in compliance which may impact our ability to detect and prevent fraud. Any failure to maintain an effective system of internal controls over financial reporting could limit the ability to report our financial results accurately and timely which could affect our reported results of operations.

The terms of our revolving credit facility impose financial restrictions that may be affected as we respond to changing business and economic conditions.

On November 17, 2010, the existing revolving credit facility was amended. In conjunction with the amendment, the availably under the facility was reduced from $90.0 million to $40.0 million, with an additional $20.0 million available at our request if specified conditions are met. We and our subsidiaries have agreed to a negative pledge on assets, with certain customary exceptions, and the credit facility places certain restrictions on our activities, including financial covenants and restrictions on certain payments to related parties and on capital expenditures. Our ability to comply with these provisions may be affected by events outside of our control. A breach of any of these provisions or our inability to comply with required financial ratios could result in a default under the credit facility. If that were to occur, the lenders have the right to declare all borrowings to be immediately due and payable.

Macro Economic Risk Factors

The global economic crisis adversely impacted our business and financial results during recent years. Challenging economic factors such as a decline in business travelers, changes in consumer preferences spending, labor shortages or increases in labor costs and increases in food costs could adversely affect our business.

The restaurant industry is being adversely affected by economic factors, including changes in national, regional, and local economic conditions, employment levels and consumer spending patterns. The increased concerns about the economy and financial markets have reduced consumer confidence and decreased restaurant traffic, particularly at upscale restaurants, which is harmful to our business and results of operations.

We depend on both local residents and business travelers to frequent our locations. If the number of visitors who frequent our locations declines due to economic or other conditions, changes in consumer preferences, changes in discretionary consumer spending or for other reasons, our revenues could decline significantly and our results of operations could be adversely affected.

The restaurant industry is characterized by the introduction of new concepts and is subject to rapidly changing consumer preferences, tastes and purchasing habits. Our continued success depends in part upon the popularity of seafood and the style of dining we offer. Shifts in consumer preferences away from this cuisine or dining style could materially and adversely affect our operating results.

15

Table of Contents

Our success depends in part upon our ability to attract, motivate and retain a sufficient number of qualified employees, including regional operational managers and regional chefs, restaurant general managers and executive chefs, necessary to continue our operations and keep pace with our growth. If we are unable to recruit and retain sufficient qualified individuals, our business and our growth could be adversely affected. Additionally, competition for qualified employees could require us to pay higher wages, which could result in higher labor costs. If our labor costs increase, our results of operations will be negatively affected.

Our profitability depends significantly on our ability to anticipate and react to changes in food costs. We rely on local, regional and national suppliers to provide our seafood, produce, beef and other ingredients. Increases in distribution costs or sale prices or failure to perform by these suppliers could cause our food costs to increase. We could also experience significant short-term disruptions in our supply if a significant supplier failed to meet its obligations.

Adverse weather conditions could unfavorably affect our restaurant sales.

Many of our restaurants are located in regions that may be susceptible to severe weather conditions. Adverse weather conditions can impact guest traffic at our restaurants, cause the temporary underutilization of outdoor patio seating, and cause temporary closures, sometimes for prolonged periods.

Many of our restaurants are concentrated in local or regional areas and, as a result, we are sensitive to economic and other trends and developments in these areas.

As of December 29, 2010, we operated five restaurants in the Seattle, Washington area, six in the Portland, Oregon area, 14 in California, and seven in the greater Vancouver, British Columbia area; our East Coast restaurants are concentrated in and around Washington, D.C. and Baltimore. As a result, adverse economic conditions, weather and labor markets in any of these areas could have a material adverse effect on our overall results of operations. In addition, given our geographic concentrations, negative publicity or events outside of our control regarding any of our restaurants in these areas could have a material adverse effect on our business and operations.

Growth Risk Factors

We may not be able to successfully integrate into our business the operations of restaurants that we acquire, which may adversely affect our business, financial condition and results of operations.

We may seek to selectively acquire existing restaurants and integrate them into our business operations. Achieving the expected benefits of any restaurants that we acquire will depend in large part on our ability to successfully integrate the operations of the acquired restaurants and personnel in a timely and efficient manner. The risks involved in such restaurant acquisitions and integration include:

| • | Challenges and costs associated with the acquisition and integration of restaurant operations located in markets where we have limited or no experience; |

| • | Possible disruption to our business as a result of the diversion of management’s attention from its normal operational responsibilities and duties; and |

| • | Consolidation of the corporate, information technology, accounting and administrative infrastructure and resources of the acquired restaurants into our business. |

We may be unable to successfully integrate the operations, or realize the anticipated benefits, of any restaurants that we acquire. If we cannot overcome the challenges and risks that we face in integrating the operations of newly acquired restaurants, our business, financial condition and results of operations could be adversely affected.

16

Table of Contents

Our failure to drive sufficient profitable sales growth through brand relevance, operating excellence, opening new restaurants, successfully refining existing restaurants and developing or acquiring new restaurants could adversely affect our results of operations.

As part of our business strategy, we intend to drive profitable sales growth by increasing same-restaurant sales at existing restaurants, continuing to expand our current portfolio of restaurant brands, and developing or acquiring additional brands that can be expanded profitably. This strategy involves numerous risks, and we may not be able to achieve our growth objectives. We may not be able to maintain brand relevance and restaurant operating excellence at existing brands to achieve sustainable same-restaurant sales growth and warrant new unit growth. In addition, we may not be able to open all of our planned new restaurants, and the new restaurants that we open may not be profitable or as profitable as our existing restaurants. New restaurants typically experience an adjustment period before sales levels and operating margins normalize, and even sales at successful newly-opened restaurants generally do not make a significant contribution to profitability in their initial months of operation. The opening of new restaurants can also have an adverse effect on sales levels at existing restaurants. Furthermore, we may not be able to develop or acquire additional brands that are as profitable as our existing restaurants.

Our business may suffer if we do not successfully, timely and economically implement our reinvestment initiatives.

In early 2011 we announced a significant initiative to align our facilities, our product offerings and our management expertise more closely with our goal of creating an exceptional upscale casual dining experience. This program includes a number of components focusing on more extensive training for our restaurant management and staff employees, targeted marketing designed to broaden our connection with younger customers and enhance our brand recognition across a broader range of diners, and significant reinvestment in our facilities. If we fail to implement this program effectively, we may be unable to strengthen our customer base (which would represent a failure to reap the intended results of our investments) or we may alienate a significant portion of our existing customer base (which would harm our revenues).

Moreover, we have budgeted significant capital expenditures toward enhancing our restaurant portfolio, including up to $15 million in 2011. A significant majority of those investments are targeting upgrades to individual properties based upon a variety of factors, with a goal of enhancing the dining experience, growing our customer base and traffic counts, and improving per-site revenues. Some of these projects will require the temporary closure of individual restaurants, which will eliminate revenues for the affected sites for a period of time. If one or more site closures are longer than expected, our revenues for such sites are likely to fall short of our expectations for those sites. In addition, the cost of these capital upgrade projects may exceed our expectations due to the age of our facilities and the need to comply with changes in building codes since our facilities were first built. Any of these potential outcomes, alone or in combination, may materially and adversely affect our financial condition, results of operations or cash flows.

Operational Risk Factors

We rely on information technology in our operations, and any material failure, inadequacy or interruption could harm our ability to effectively operate our business.

We rely on information systems across our operations, including for management of our supply chain, point-of-sale processing system in our restaurants, and various other processes and transactions. Our ability to effectively manage our business and coordinate the production, distribution and sale of our products depends on the reliability and capacity of these systems. The failure of these systems to operate effectively, problems with transitioning to upgraded or replacement systems, or a breach in security of these systems could cause delays in customer service and reduce efficiency in our operations, and significant capital investments could be required to remediate the problem.

17

Table of Contents

A failure to develop and recruit effective leaders or the loss of key personnel could harm our ability to effectively operate our business.

Our future growth depends substantially on the contributions and abilities of key executives and other employees. Our future growth also depends substantially on our ability to recruit and retain high-quality employees to work in and manage our restaurants. We must continue to recruit, retain and motivate management and other employees in order to maintain our current business and support our projected growth. A failure to maintain leadership excellence and build adequate bench strength, a loss of key employees or a significant shortage of high-quality restaurant employees could jeopardize our ability to meet our growth targets.

We occupy most of our restaurants under long-term non-cancelable leases which may limit our flexibility as economic conditions change.

Most of our restaurants are located in leased premises with long-term non-cancelable leases. If we close restaurants, we may be obligated to continue making rental payments or make a lump-sum payment to exit the lease, which could have a material adverse effect on our business and results of operations. Alternatively, at the end of the lease term and any renewal period for a restaurant, we may be unable to renew the lease without substantial additional cost, if at all. If we are unable to renew our restaurant leases, we would have to close or relocate a restaurant, which could subject us to construction and other costs and risks, and could have a material adverse effect on our business and results of operations.

Legal, Regulatory and Health Risk Factors

Restaurant companies have been the target of class-actions and other lawsuits alleging, among other things, violation of federal and state law. Litigation could have a material adverse effect on our business.

We are subject to a variety of claims arising in the ordinary course of our business brought by or on behalf of our guests or employees, including personal injury claims, contract claims, and employment-related claims. In recent years, a number of restaurant companies have been subject to lawsuits, including class-action lawsuits, alleging violations of federal and state law regarding workplace, employment and similar matters. A number of these lawsuits have resulted in the payment of substantial damages by the defendants. Similar lawsuits have been instituted against us from time to time. In 2007, we incurred a $2.2 million charge for a class action legal settlement relating to an employment claim. Regardless of whether any claims against us are valid or whether we are ultimately determined to be liable, claims may be expensive to defend and may divert time and money away from our operations and hurt our performance. A judgment significantly in excess of our insurance coverage for any claims could materially adversely affect our financial condition or results of operations, and adverse publicity resulting from these allegations may materially adversely affect our business. We may incur substantial damages and expenses resulting from lawsuits, which could have a material adverse effect on our business.

Our insurance policies may not provide adequate levels of coverage against all claims.

We believe we maintain insurance coverage that is customary for businesses of our size and type. However, there are types of losses we may incur that cannot be insured against or that we believe are not commercially reasonable to insure. These losses, if they occur, could have a material and adverse effect on our business and results of operations. Our primary insurer in 2004 has informed us it believes we have exhausted our insurance coverage with respect to employment claims arising in our 2004 coverage year and that several claims arising in 2005 through 2008 coverage years are related to the 2004 coverage year. We disagree with this interpretation of our coverage, but we have taken this interpretation into account in connection with the charge we have taken related to our settlement of class action claims in California. See Item 3, “Legal Proceedings.” We may not succeed in our contest of our insurer’s conclusion. If we are unsuccessful, and if it is determined that other existing employment claims arose in 2004 and are therefore not covered, our resolution of those claims would be more expensive.

18

Table of Contents

Health concerns relating to the consumption of seafood or other foods could affect consumer preferences and could negatively impact our results of operations.

We may lose customers based on health concerns about the consumption of seafood or negative publicity concerning food quality, illness and injury generally, such as negative publicity concerning the accumulation of mercury or other carcinogens in seafood, e-coli, “mad cow” or “foot-and-mouth” disease, publication of government or industry findings about food products served by us, regulatory required disclosure of calorie or nutritional information or other health concerns or operating issues stemming from one of our restaurants. In addition, our operational controls and training may not be fully effective in preventing all food-borne illnesses. Some food-borne illness incidents could be caused by food suppliers and transporters and would be outside of our control. Any negative publicity, health concerns or specific outbreaks of food-borne illnesses attributed to one or more of our restaurants, or the perception of an outbreak, could result in a decrease in guest traffic to our restaurants and could have a material adverse effect on our business.

We may incur costs or liabilities and lose revenue, and our growth strategy may be adversely impacted, as a result of government regulation.

Our restaurants are subject to various federal, state and local government regulations, including those relating to employees, the preparation and sale of food and the sale of alcoholic beverages. These regulations affect our restaurant operations and our ability to open new restaurants.

Each of our restaurants must obtain licenses from regulatory authorities to sell liquor, beer and wine, and each restaurant must obtain a food service license from local health authorities. Each liquor license must be renewed annually and may be revoked at any time for cause, including violation by us or our employees of any laws and regulations relating to the minimum drinking age, advertising, wholesale purchasing and inventory control. In certain jurisdictions where we operate the number of alcoholic beverage licenses available is limited and licenses are traded at market prices.

The failure to maintain our food and liquor licenses and other required licenses, permits and approvals could adversely affect our operating results. Difficulties or failure in obtaining the required licenses and approvals could delay or result in our decision to cancel the opening of new restaurants.

We are subject to “dram shop” statutes in some states. These statutes generally allow a person injured by an intoxicated person to recover damages from an establishment that wrongfully served alcoholic beverages to the intoxicated person. A judgment substantially in excess of our insurance coverage could harm our operating results and financial condition.

Various federal and state labor laws govern our relationship with our employees and affect operating costs. These laws include minimum wage requirements, overtime pay, unemployment tax rates, workers’ compensation rates, and citizenship requirements. Additional government-imposed increases in minimum wages, overtime pay, paid leaves of absence and mandated health benefits, increased tax reporting and tax payment requirements for employees who receive gratuities, or a reduction in the number of states that allow tips to be credited toward minimum wage requirements would increase our labor costs and could harm our operating results and financial condition. We may be unable to increase our prices in order to pass these increased labor costs on to our guests, in which case our margins would be negatively affected. Because our labor costs are, as a percentage of revenues, higher than other industries, we may be significantly harmed by labor cost increases.

The Federal Americans with Disabilities Act prohibits discrimination on the basis of disability in public accommodations and employment. Although our restaurants are designed to be accessible to the disabled, we could be required to make modifications to our restaurants to provide service to, or make reasonable accommodations for, disabled persons.

19

Table of Contents

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |