Attached files

| file | filename |

|---|---|

| EX-23.1 - STONERIDGE INC | v212433_ex23-1.htm |

| EX-32.1 - STONERIDGE INC | v212433_ex32-1.htm |

| EX-99.1 - STONERIDGE INC | v212433_ex99-1.htm |

| EX-23.2 - STONERIDGE INC | v212433_ex23-2.htm |

| EX-31.1 - STONERIDGE INC | v212433_ex31-1.htm |

| EX-32.2 - STONERIDGE INC | v212433_ex32-2.htm |

| EX-21.1 - STONERIDGE INC | v212433_ex21-1.htm |

| EX-31.2 - STONERIDGE INC | v212433_ex31-2.htm |

| EX-10.30 - STONERIDGE INC | v212433_ex10-30.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

OR

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ________to ________

Commission file number: 001-13337

STONERIDGE, INC.

(Exact name of registrant as specified in its charter)

|

Ohio

|

34-1598949

|

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

|

incorporation or organization)

|

|

Identification No.)

|

|

9400 East Market Street, Warren, Ohio

|

44484

|

|

|

(Address of principal executive offices)

|

|

(Zip Code)

|

(330) 856-2443

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Shares, without par value

|

|

New York Stock Exchange

|

Securities registered pursuant to section 12(g) of the Act:

None

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | o Yes | x No |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | o Yes | x No |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | x Yes | o No |

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | o Yes | o No |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ¨

|

Accelerated filer x

|

Non-accelerated filer ¨

|

Smaller reporting company ¨

|

|

(Do not check if a smaller reporting company)

|

|||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | o Yes | x No |

As of June 30, 2010, the aggregate market value of the registrant’s Common Shares, without par value, held by non-affiliates of the registrant was approximately $120.2 million. The closing price of the Common Shares on June 30, 2010 as reported on the New York Stock Exchange was $7.59 per share. As of June 30, 2010, the number of Common Shares outstanding was 25,440,338.

The number of Common Shares, without par value, outstanding as of February 8, 2011 was 25,994,265.

DOCUMENTS INCORPORATED BY REFERENCE

Definitive Proxy Statement for the Annual Meeting of Shareholders to be held on May 9, 2011, into Part III, Items 10, 11, 12, 13 and 14.

|

INDEX

|

||

|

Page

|

||

|

PART I

|

||

|

Item 1.

|

Business

|

1

|

|

Item 1A.

|

Risk Factors

|

6

|

|

Item 1B.

|

Unresolved Staff Comments

|

13

|

|

Item 2.

|

Properties

|

14

|

|

Item 3.

|

Legal Proceedings

|

15

|

|

Item 4.

|

(Removed and Reserved)

|

15

|

|

PART II

|

||

|

Item 5.

|

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

15

|

|

Item 6.

|

Selected Financial Data

|

17

|

|

Item 7.

|

Management's Discussion and Analysis of Financial Condition and Results of Operations

|

18

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

34

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

36

|

|

Item 9.

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure

|

69

|

|

Item 9A.

|

Controls and Procedures

|

69

|

|

Item 9B.

|

Other Information

|

71

|

|

PART III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

71

|

|

Item 11.

|

Executive Compensation

|

71

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

71

|

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

72

|

|

Item 14.

|

Principal Accounting Fees and Services

|

72

|

|

PART IV

|

||

|

Item 15.

|

Exhibits, Financial Statement Schedules

|

72

|

|

Signatures

|

73

|

|

i

PART I

Item 1. Business.

Overview

Founded in 1965, Stoneridge, Inc. (the “Company”) is a global designer and manufacturer of highly engineered electrical and electronic components, modules and systems for the commercial vehicle, automotive, agricultural and off-highway vehicle markets. Our products and systems are critical elements in the management of mechanical and electrical systems to improve overall vehicle performance, convenience and monitoring in areas such as emissions control, fuel efficiency, safety and security. Our extensive footprint, including our joint ventures, encompasses more than 25 locations in 14 countries and enables us to supply global and regional commercial vehicle, automotive, agricultural and

off-highway vehicle manufactures around the world. Our custom-engineered products and systems are used to activate equipment and accessories, monitor and display vehicle performance and control, and distribute electrical power and signals. Our product offerings consist of (i) vehicle instrumentation systems, (ii) vehicle management electronics, (iii) application-specific switches and actuators, (iv) sensors and (v) power and signal distribution systems. We supply our products, predominantly on a sole-source basis, to many of the world’s leading commercial vehicle and automotive original equipment manufacturers, (“OEMs”), and select non-vehicle OEMs, as well as certain commercial vehicle and automotive tier one suppliers. These OEMs are increasingly utilizing electronic technology to comply with more stringent regulations (particularly emissions and

safety) and to meet end-user demand for improved vehicle performance and greater convenience. As a result, per-vehicle electronic content has been increasing. Our technology and our partnership-oriented approach to product design and development enables us to develop next-generation products and to excel in the transition from mechanical-based components and systems to electrical and electronic components, modules and systems.

Products

We conduct our business in two reportable segments: Electronics and Control Devices. The Company’s operating segments are aggregated based on sharing similar economic characteristics. Other aggregation factors include the nature of the products offered and management and oversight responsibilities. The core products of the Electronics reportable segment include vehicle electrical power and distribution systems and electronic instrumentation and information display products. The core products of the Control Devices reportable segment include sensors, electronic and electrical switch products, valves and control actuation devices. We design and manufacture the following vehicle

products:

Electronics. Our Electronics segment designs and manufactures electronic instrument clusters, electronic control units, driver information systems and electrical distribution systems (primarily wiring harnesses and connectors for electrical power and signal distribution). These products collect, store and display vehicle information such as speed, pressure, maintenance data, trip information, operator performance, temperature, distance traveled and driver messages related to vehicle performance. In addition, power distribution systems regulate, coordinate and direct the operation of the electrical system within a vehicle. These products use state-of-the-art

hardware, software and multiplexing technology and are sold principally to the commercial vehicle, agricultural and off-highway vehicle markets. We also assemble entire instrument panels for the medium and heavy-duty truck markets that are configured specifically to the OEM customer’s specifications.

Control Devices. Our Control Devices segment designs and manufactures products that monitor, measure or activate specific functions within a vehicle. This segment includes product lines such as sensors, switches, valves, and actuators, as well as other electronic products. Sensor products are employed in major vehicle systems such as the emissions, safety, powertrain, braking, climate control, steering and suspension systems. Switches transmit signals that activate specific functions. Our switch technology is principally used in two capacities, user-activated and hidden. User-activated switches are used by a vehicle’s operator or passengers to manually

activate headlights, rear defrosters and other accessories. Hidden switches are not typically visible to vehicle operators or passengers and are engaged to activate or deactivate selected functions as part of normal vehicle operations, such as brake lights. In addition, our Control Devices segment designs and manufactures electromechanical actuator products that enable OEMs to deploy power functions in a vehicle and can be designed to integrate switching and control functions. We sell these products principally to the automotive market.

1

The following table sets forth for the periods indicated, the percentage of net sales attributable to our product categories and reportable segments for the years ended December 31:

|

Product Category

|

Segment

|

2010

|

2009

|

2008

|

||||||||||

|

Vehicle electrical power & distribution systems

|

Electronics

|

41 | % | 40 | % | 40 | % | |||||||

|

Electronic instrumentation & information display products

|

Electronics

|

22 | 23 | 29 | ||||||||||

|

Total Electronics

|

63 | % | 63 | % | 69 | % | ||||||||

|

Switch & position sensors

|

Control Devices

|

20 | % | 19 | % | 17 | % | |||||||

|

Actuator & temperature, pressure & speed sensors

|

Control Devices

|

17 | 18 | 14 | ||||||||||

|

Total Control Devices

|

37 | % | 37 | % | 31 | % | ||||||||

Our products and systems are sold to numerous OEM and tier one supplier customers, in addition to aftermarket suppliers, for use on many different vehicle platforms. We supply multiple different parts to many of our principal customers under requirements contracts for a particular model. These contracts range in duration from one year to the production life of the model, which commonly extends for three to seven years. Approximately 68%, 67% and 70% of our net sales in 2010, 2009 and 2008, respectively, were derived from the commercial, agricultural and off-highway vehicle markets. Approximately 32%, 33% and 30% of our net sales in 2010, 2009 and 2008, respectively, were made to the

automotive market.

For further information related to our reportable segments and financial information about geographic areas, see Note 12, “Segment Reporting,” to the consolidated financial statements included in this report.

Production Materials

The principal production materials used in the manufacturing process for both reportable segments include: copper wire, zinc, cable, resins, plastics, printed circuit boards, and certain electrical components such as microprocessors, memory devices, resistors, capacitors, fuses, relays and connectors. We purchase such materials pursuant to both annual contract and spot purchasing methods. Such materials are available from multiple sources, but we generally establish collaborative relationships with a qualified supplier for each of our key production materials in order to lower costs and enhance service and quality. As global demand for our production materials increases, we may have difficulties

obtaining adequate production materials from our suppliers to satisfy our customers. Any extended period of time for which we cannot obtain adequate production material or which we experience an increase in the price of production material could materially affect our results of operations and financial condition.

Patents and Intellectual Property

We maintain and have pending various U.S. and foreign patents and other rights to intellectual property relating to both reportable segments of our business, which we believe are appropriate to protect the Company's interests in existing products, new inventions, manufacturing processes and product developments. We do not believe any single patent is material to our business, nor would the expiration or invalidity of any patent have a material adverse effect on our business or ability to compete. We are not currently engaged in any material infringement litigation, nor are there any material infringement claims pending by or against the Company.

Industry Cyclicality and Seasonality

The markets for products in both of our reportable segments have been cyclical. Because these products are used principally in the production of vehicles for the commercial, automotive, agricultural and off-highway markets, sales, and therefore results of operations, are significantly dependent on the general state of the economy and other factors, like the impact of environmental regulations on our customers, which affect these markets. A decline in commercial, automotive, agricultural and off-highway vehicle production of our principal customers could adversely impact the Company. Seasonality within the markets that we serve also impacts our operations.

2

Customers

We are dependent on several customers for a significant percentage of our sales. The loss of any significant portion of our sales to these customers or the loss of a significant customer would have a material adverse impact on our financial condition and results of operations. We supply numerous different parts to each of our principal customers. Contracts with several of our customers provide for supplying their requirements for a particular model, rather than for manufacturing a specific quantity of products. Such contracts range from one year to the life of the model, which is generally three to seven years. These contracts are subject to renegotiation, which may affect product pricing and generally

may be terminated by our customers at any time. Therefore, the loss of a contract for a major model or a significant decrease in demand for certain key models or group of related models sold by any of our major customers could have a material adverse impact on the Company. We may also enter into contracts to supply parts, the introduction of which may then be delayed or cancelled. We also compete to supply products for successor models and are therefore subject to the risk that the customer will not select the Company to produce products on any such model, which could have a material adverse impact on our financial condition and results of operations. In addition, we sell products to other customers that are ultimately sold to our principal customers.

The following table presents our principal customers, as a percentage of net sales:

|

Years ended December 31

|

2010

|

2009

|

2008

|

|||||||||

|

Navistar International Corporation

|

24 | % | 27 | % | 26 | % | ||||||

|

Deere & Company

|

14 | 12 | 10 | |||||||||

|

Ford Motor Company

|

8 | 9 | 6 | |||||||||

|

General Motors Company

|

5 | 5 | 4 | |||||||||

|

Chrysler Group LLC

|

4 | 4 | 6 | |||||||||

|

Other

|

45 | 43 | 48 | |||||||||

|

Total

|

100 | % | 100 | % | 100 | % | ||||||

Backlog

Our products are produced from readily available materials and have a relatively short manufacturing cycle; therefore our products are not on backlog status. Each of our production facilities maintains its own inventories and production schedules. Production capacity is adequate to handle current requirements and can be expanded to handle increased growth if needed.

Competition

The markets for our products in both reportable segments are highly competitive. The principal methods of competition are technological innovation, price, quality, performance, service and delivery. We compete for new business both at the beginning of the development of new models and upon the redesign of existing models. New model development generally begins two to five years before the marketing of such models to the public. Once a supplier has been selected to provide parts for a new program, an OEM customer will usually continue to purchase those parts from the selected supplier for the life of the program, although not necessarily for any model redesigns.

Our diversity in products creates a wide range of competitors, which vary depending on both market and geographic location. We compete based on strong customer relations and a fast and flexible organization that develops technically effective solutions at or below target price. We compete against the following primary competitors:

Electronics. Our primary competitors include Actia Group S.A., AEES, Bosch, Continental AG, Delphi Automotive LLP, Nexans SA and Yazaki Corporation.

Control Devices. Our primary competitors include BEI Sensors, Bosch, Continental AG, Delphi Automotive LLP, Denso Corporation, Hella KGaA Hueck & Co., Methode Electronics, Inc. and TRW Automotive Holdings Corp.

3

Product Development

Our research and development efforts for both reportable segments are largely product design and development oriented and consists primarily of applying known technologies to customer requests. We work closely with our customers to creatively solve customer requests using innovative approaches. The majority of our development expenses are related to customer-sponsored programs where we are involved in designing custom-engineered solutions for specific applications or for next generation technology. To further our vehicle platform penetration, we have also developed collaborative relationships with the design and engineering departments of key customers. These collaborative efforts have

resulted in the development of new and complimentary products and the enhancement of existing products.

Our development work is largely performed on a decentralized basis. We have engineering and product development departments located at a majority of our manufacturing facilities. To ensure knowledge sharing among decentralized development efforts, we have instituted a number of mechanisms and practices whereby innovation and best practices are shared. The decentralized product development operations are complimented by larger technology groups in Canton, Massachusetts, Lexington, Ohio and Stockholm, Sweden. In addition, during 2010, we opened a product development center in Shanghai, China to focus on the developing Chinese market.

We use efficient and quality oriented work processes to address our customers’ high standards. Our product development technical resources include a full complement of computer-aided design and engineering (“CAD/CAE”) software systems, including (i) virtual three-dimensional modeling, (ii) functional simulation and analysis capabilities and (iii) data links for rapid prototyping. These CAD/CAE systems enable us to expedite product design and the manufacturing process to shorten the development time and ultimately time to market.

We have further strengthened our electrical engineering competencies through investment in equipment such as (i) automotive electro-magnetic compliance test chambers, (ii) programmable automotive and commercial vehicle transient generators, (iii) circuit simulators and (iv) other environmental test equipment. Additional investment in product machining equipment has allowed us to fabricate new product samples in a fraction of the time required historically. Our product development and validation efforts are supported by full service, on-site test labs at most manufacturing facilities, thus enabling cross-functional engineering teams to optimize the product, process and system performance before tooling

initiation.

We have invested, and will continue to invest in technology to develop new products for our customers. Product development costs incurred in connection with the development of new products and manufacturing methods, to the extent not recoverable from the customer, are charged to selling, general and administrative expenses, as incurred. Such costs amounted to approximately $37.6 million, $33.0 million and $45.5 million for 2010, 2009 and 2008, respectively, or 5.9%, 6.9% and 6.0% of net sales for these periods.

We will continue shifting our investment spending toward the design and development of new products rather than focusing on sustaining existing product programs for specific customers, which allows us to sell our products to multiple customers. The typical product development process takes three to five years to show tangible results. As part of our effort to shift our investment spending, we reviewed our current product portfolio and adjusted our spending to either accelerate or eliminate our investment in these products, based on our position in the market and the potential of the market and product.

Environmental and Other Regulations

Our operations are subject to various federal, state, local and foreign laws and regulations governing, among other things, emissions to air, discharge to water and the generation, handling, storage, transportation, treatment and disposal of waste and other materials. We believe that our business, operations and facilities have been and are being operated in compliance, in all material respects, with applicable environmental and health and safety laws and regulations, many of which provide for substantial fines and criminal sanctions for violations.

4

Employees

As of December 31, 2010, we had approximately 6,800 employees, approximately 1,600 of whom were salaried and the balance of whom were paid on an hourly basis. Although we have no collective bargaining agreements covering U.S. employees, certain employees located in Estonia, France, Mexico, Spain, Sweden and the United Kingdom either (i) are represented by a union and are covered by a collective bargaining agreement or (ii) are covered by works council or other employment arrangements required by law. We believe that relations with our employees are good.

Joint Ventures

We form joint ventures in order to achieve several strategic objectives including (i) diversifying our business by expanding in high-growth regions, (ii) employing complementary design processes, growth technologies and intellectual capital and (iii) realizing cost savings from combined sourcing. We have joint ventures in Brazil, PST Eletrônica S.A. (“PST”) and India, Minda Stoneridge Instruments Ltd. (“Minda”) and continue to explore similar business opportunities in other global markets. We have a 50% interest in PST and a 49% interest in Minda. We entered into our PST joint venture in October 1997 and our Minda joint venture in August 2004. Each of these

investments is accounted for using the equity method of accounting.

PST specializes in the design, manufacture and sale of electronic vehicle security, vehicle tracking and infotainment devices. PST sells its products through the aftermarket distribution channel, to factory authorized dealer installers, also referred to as original equipment services and to OEMs. PST has experienced rapid growth driven by strong demand for vehicle security products in South America. PST generated net sales of $182.9 million, $140.7 million and $174.3 million in 2010, 2009 and 2008, respectively. We received dividend payments of $5.5 million, $7.3 million and $4.2 million from PST in 2010, 2009 and 2008,

respectively.

Minda manufactures electromechanical/electronic instrumentation equipment primarily for the automotive, motorcycle and commercial vehicle markets. We leverage our investment in Minda by sharing our knowledge and expertise in electrical components and systems and expanding Minda’s product offering through the joint development of our products designed for the market in India.

Our joint ventures have contributed positively to our financial results in 2010, 2009 and 2008. Equity earnings by joint venture are summarized in the following table (in thousands):

|

Years ended December 31

|

2010

|

2009

|

2008

|

|||||||||

|

PST

|

$ | 9,490 | $ | 7,385 | $ | 12,788 | ||||||

|

Minda

|

856 | 390 | 702 | |||||||||

|

Total equity earnings of investees

|

$ | 10,346 | $ | 7,775 | $ | 13,490 | ||||||

Executive Officers of the Company

Each executive officer of the Company is appointed by the Board of Directors, serves at its pleasure and holds office until a successor is appointed, or until the earlier of death, resignation or removal. The Board of Directors generally appoints executive officers annually. The executive officers of the Company are as follows:

|

Name

|

Age

|

Position

|

||

|

John C. Corey

|

63

|

President, Chief Executive Officer and Director

|

||

|

George E. Strickler

|

63

|

Executive Vice President, Chief Financial Officer and Treasurer

|

||

|

Thomas A. Beaver

|

57

|

Vice President of the Company and Vice President of Global Sales and Systems Engineering

|

||

|

Michael D. Sloan

|

54

|

Vice President of the Company and President of the Control Devices Division

|

||

|

Mark J. Tervalon

|

44

|

Vice President of the Company and President of the Electronics Division

|

5

John C. Corey, President, Chief Executive Officer and Director. Mr. Corey has served as President and Chief Executive Officer since being appointed by the Board of Directors in January 2006. Mr. Corey has served as a Director on the Board of Directors since January 2004. Prior to his employment with the Company, Mr. Corey served from October 2000, as President and Chief Executive Officer and Director of Safety Components International, a supplier of airbags and components, with worldwide operations. Mr. Corey has served as a Director and Chairman of the

Board of Haynes International, Inc., a producer of metal alloys since 2004.

George E. Strickler, Executive Vice President, Chief Financial Officer and Treasurer. Mr. Strickler has served as Executive Vice President and Chief Financial Officer since joining the Company in January of 2006. Mr. Strickler was appointed Treasurer of the Company in February 2007. Prior to his employment with the Company, Mr. Strickler served as Executive Vice President and Chief Financial Officer for Republic Engineered Products, Inc. (“Republic”), from February 2004 to January of 2006. Before joining Republic, Mr. Strickler was BorgWarner

Inc.’s Executive Vice President and Chief Financial Officer from February 2001 to November 2003.

Thomas A. Beaver, Vice President of the Company and Vice President of Global Sales and Systems Engineering. Mr. Beaver has served as Vice President of the Company and Vice President of Global Sales and Systems Engineering since January of 2005. Prior to that, Mr. Beaver served as Vice President of Stoneridge Sales and Marketing from January 2000 to January 2005.

Michael D. Sloan, Vice President of the Company and President of the Control Devices Division. Mr. Sloan has served as President of the Control Devices Division since July of 2009 and Vice President of the Company since December of 2009. Prior to that, Mr. Sloan served as Vice President and General Manager of Stoneridge Hi-Stat from February 2004 to July 2009.

Mark J. Tervalon, Vice President of the Company and President of the Stoneridge Electronics Division. Mr. Tervalon has served as President of the Stoneridge Electronics Division and Vice President of the Company since August of 2006. Prior to that, Mr. Tervalon served as Vice President and General Manager of the Electronic Products Division from May 2002 to December 2003 when he became Vice President and General Manager of the Stoneridge Electronics Group until August 2006.

Available Information

We make available, free of charge through our website (www.stoneridge.com), our Annual Report on Form 10-K (“Annual Report”), Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, all amendments to those reports, and other filings with the U.S. Securities and Exchange Commission (“SEC”), as soon as reasonably practicable after they are filed with the SEC. Our Corporate Governance Guidelines, Code of Business Conduct and Ethics, Code of Ethics for Senior Financial Officers, Whistleblower Policy and Procedures and the charters of the Board’s Audit, Compensation and Nominating and Corporate Governance Committees are posted on our website as well. Copies of these documents

will be available to any shareholder upon request. Requests should be directed in writing to Investor Relations at 9400 East Market Street, Warren, Ohio 44484.

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F. Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including the Company.

Item 1A. Risk Factors.

Set forth below are some of the principal risks and uncertainties that could cause our actual business results to differ materially from any forward-looking statements contained in this Annual Report. In addition, future results could be materially affected by general industry and market conditions, changes in laws or accounting rules, general U.S. and non-U.S. economic and political conditions, including a global economic slow-down, fluctuation of interest rates or currency exchange rates, terrorism, political unrest or international conflicts, political instability or major health concerns, natural disasters, commodity prices or other disruptions of expected economic and business conditions. These risk factors

should be considered in addition to our cautionary comments concerning forward-looking statements in this Annual Report, including statements related to markets for our products and trends in our business that involve a number of risks and uncertainties. Our separate section, "Forward-Looking Statements," should be considered in addition to the following statements.

6

Our business is cyclical and seasonal in nature and downturns in the commercial, automotive, agricultural and off-highway vehicle markets could reduce the sales and profitability of our business.

The demand for our products is largely dependent on the domestic and foreign production of commercial, automotive, agricultural and off-highway vehicles. The markets for our products have been cyclical, because new vehicle demand is dependent on, among other things, consumer spending and is tied closely to the overall strength of the economy. Because our products are used principally in the production of vehicles for the commercial, automotive, agricultural and off-highway vehicle markets, our net sales, and therefore our results of operations, are significantly dependent on the general state of the economy and other factors which affect these markets. A decline in commercial, automotive, agricultural and off-highway

vehicle production could adversely impact our results of operations and financial condition. In 2010, approximately 68% of our net sales were derived from commercial, agricultural and off-highway vehicle markets and approximately 32% were derived from the automotive market. Seasonality experienced by our served markets also impacts our operations.

We may not realize sales represented by awarded business.

We base our growth projections, in part, on commitments made by our customers. These commitments generally renew annually during a program life cycle. Failure of actual production orders from our customers to approximate these commitments could have a material adverse effect our business, financial condition or results of operations.

The prices that we can charge some of our customers are predetermined and we bear the risk of costs in excess of our estimates, in addition to the risk of adverse effects resulting from general customer demands for cost reductions and quality improvements.

Our supply agreements with some of our customers require us to provide our products at predetermined prices. In some cases, these prices decline over the course of the contract and may require us to meet certain productivity and cost reduction targets. In addition, our customers may require us to share productivity savings in excess of our cost reduction targets. The costs that we incur in fulfilling these contracts may vary substantially from our initial estimates. Unanticipated cost increases or the inability to meet certain cost reduction targets may occur as a result of several factors, including increases in the costs of labor, components or materials. In some cases, we are permitted to pass on to our customers

the cost increases associated with specific materials. Cost overruns that we cannot pass on to our customers could adversely affect our business, financial condition or results of operations.

OEM customers have exerted considerable pressure on component suppliers to reduce costs, improve quality and provide additional design and engineering capabilities and continue to demand and receive price reductions and measurable increases in quality through their use of competitive selection processes, rating programs, and various other arrangements. We may be unable to generate sufficient production cost savings in the future to offset required price reductions. Additionally, OEMs have generally required component suppliers to provide more design engineering input at earlier stages of the product development process, the costs of which have, in some cases, been absorbed by the suppliers. Future price reductions,

increased quality standards and additional engineering capabilities required by OEMs may reduce our profitability and have a material adverse effect on our business, financial condition or results of operations.

Our business is very competitive and increased competition could reduce our sales.

The markets for our products are highly competitive. We compete based on quality, service, price, performance, timely delivery and technological innovation. Many of our competitors are more diversified and have greater financial and other resources than we do. In addition, with respect to certain of our products, some of our competitors are divisions of our OEM customers. We cannot assure you that our business will not be adversely affected by competition or that we will be able to maintain our profitability if the competitive environment changes.

We are dependent on the availability and price of raw materials and other supplies.

We require substantial amounts of raw materials and other supplies and substantially all such materials we require are purchased from outside sources. The availability and prices of raw materials and other supplies may be subject to curtailment or change due to, among other things, new laws or regulations, suppliers’ allocations to other purchasers and interruptions in production by suppliers, changes in exchange rates and worldwide price levels. As demand for raw materials and other supplies increases as a result of a recovering economy, we may have difficulties obtaining adequate raw materials and other supplies from our suppliers to satisfy our customers. At times, we have experienced difficulty

obtaining adequate supplies of semiconductors and memory chips for our Electronics segment and nylon and resins for our Control Devices segment. If we cannot obtain adequate raw materials and other supplies or if we experience an increase in the price of raw materials and other supplies, our business, financial condition or results of operations could be materially adversely affected.

7

We use a variety of commodities, including copper, zinc, resins and certain other commodities. Increasing commodity costs could have an impact on our results. We have sought to alleviate the impact of increasing costs by including a material pass-through provision in our customer contracts whenever possible and at times by selectively hedging a portion of our copper exposure. The inability to pass-through increasing commodity costs may have a material adverse effect on our business, financial condition or results of operations.

The loss or insolvency of any of our major customers would adversely affect our future results.

We are dependent on several principal customers for a significant percentage of our net sales. In 2010, our top three customers were Navistar International Corporation, Deere & Company and Ford Motor Company, which comprised 24%, 14% and 8% of our net sales, respectively. In 2010, our top ten customers accounted for 70% of our net sales. The loss of any significant portion of our sales to these customers or any other customers would have a material adverse impact on our results of operations and financial condition. The contracts we have entered into with many of our customers provide for supplying the customers’ requirements for a particular model, rather than for manufacturing a specific quantity of

products. Such contracts range from one year to the life of the model, which is generally three to seven years. These contracts are subject to renegotiation, which may affect product pricing and generally may be terminated by our customers at any time. Therefore, the loss of a contract for a major model or a significant decrease in demand for certain key models or any group of related models sold by any of our major customers could have a material adverse impact on our results of operations and financial condition by reducing cash flows and our ability to spread costs over a larger revenue base. We also compete to supply products for successor models and are subject to the risk that the customer will not select us to produce products on any such model, which could have a material adverse impact on our business, financial condition or results of operations. In addition, we have

significant receivable balances related to these customers and other major customers that would be at risk in the event of their bankruptcy.

Consolidation among vehicle parts customers and suppliers could make it more difficult for us to compete successfully.

The vehicle part supply industry has undergone a significant consolidation as OEM customers have sought to lower costs, improve quality and increasingly purchase complete systems and modules rather than separate components. As a result of the cost focus of these major customers, we have been, and expect to continue to be, required to reduce prices. Because of these competitive pressures, we cannot assure you that we will be able to increase or maintain gross margins on product sales to our customers. The trend toward consolidation among vehicle parts suppliers is resulting in fewer, larger suppliers who benefit from purchasing and distribution economies of scale. If we cannot achieve cost savings and operational

improvements sufficient to allow us to compete successfully in the future with these larger, consolidated companies, our business, financial condition or results of operations could be adversely affected.

The emergence of significant competitors from bankruptcy may adversely affect us.

Certain of our significant competitors have recently emerged from bankruptcy protection. The bankruptcy protection afforded to these competitors has allowed them to eliminate or substantially reduce contractual obligations, including significant amounts of debt, and avoid liabilities. The elimination or reduction of these obligations has made these competitors stronger financially, which could have an adverse effect on our competitive position and results of operations. The emergence of other significant competitors from bankruptcy protection could have further adverse effects on our competitive position and our business, financial condition or results of operations.

Our physical properties and information systems are subject to damage as a result of disasters, outages or similar events.

Our offices and facilities, including those used for design and development, material procurement, manufacturing, logistics and sales are located throughout the world and are subject to possible destruction, temporary stoppage or disruption as a result of any number of unexpected events. If any of these facilities or offices was to experience a significant loss as a result of any of the above events, it could disrupt our operations, delay production, shipments and revenue, and result in large costs to repair or replace these facilities or offices.

8

In addition, network and information system shutdowns caused by unforeseen events such as power outages, disasters, hardware or software defects, computer viruses and computer security violations pose increasing risks. Such an event could also result in the disruption of our operations, delay production, shipments and revenue, and result in large expenditures necessary to repair or replace such network and information systems.

We must implement and sustain a competitive technological advantage in producing our products to compete effectively.

Our products are subject to changing technology, which could place us at a competitive disadvantage relative to alternative products introduced by competitors. Our success will depend on our ability to continue to meet customers’ changing specifications with respect to quality, service, price, timely delivery and technological innovation by implementing and sustaining competitive technological advances. Our business may, therefore, require significant ongoing and recurring additional capital expenditures and investment in product development and manufacturing and management information systems. We cannot assure you that we will be able to achieve the technological advances or introduce new products that may be

necessary to remain competitive. Our inability to continuously improve existing products, to develop new products and to achieve technological advances could have a material adverse effect on our business, financial condition or results of operations.

We may experience increased costs and other disruptions to our business associated with labor unions.

As of December 31, 2010, we had approximately 6,800 employees, approximately 1,600 of whom were salaried and the balance of whom were paid on an hourly basis. Although we have no collective bargaining agreements covering U.S. employees, certain employees located in Estonia, France, Mexico, Spain, Sweden and the United Kingdom either (i) are represented by a union and are covered by a collective bargaining agreement or (ii) are covered by works council or other employment arrangements required by law. We cannot assure you that other of our employees will not be represented by a labor organization in the future or that any of our facilities will not experience a work stoppage or other labor disruption. Any work

stoppage or other labor disruption involving our employees, employees of our customers (many of which customers have employees who are represented by unions), or employees of our suppliers could have a material adverse effect on our business, financial condition or results of operations by disrupting our ability to manufacture our products or reducing the demand for our products.

Compliance with environmental and other governmental regulations could be costly and require us to make significant expenditures.

Our operations are subject to various federal, state, local and foreign laws and regulations governing, among other things:

|

|

•

|

the discharge of pollutants into the air and water;

|

|

|

•

|

the generation, handling, storage, transportation, treatment, and disposal of waste and other materials;

|

|

|

•

|

the cleanup of contaminated properties; and

|

|

|

•

|

the health and safety of our employees.

|

Our business, operations and facilities are subject to environmental and health and safety laws and regulations, many of which provide for substantial fines for violations. The operation of our manufacturing facilities entails risks and we cannot assure you that we will not incur material costs or liabilities in connection with these operations. In addition, potentially significant expenditures could be required in order to comply with evolving environmental, health and safety laws, regulations or requirements that may be adopted or imposed in the future. Changes in environmental, health and safety laws, regulations and requirements or other governmental regulations could increase our cost of doing business or

adversely affect the demand for our products.

We also may be required to investigate or clean up contamination resulting from past or current uses of our properties. At our Sarasota, Florida facility, for example, groundwater and soil contamination caused by operations before we acquired the facility will require future investigation and cleanup. This matter may have a material adverse impact on our business, financial condition or results of operations. Although no other environmental matters have been identified, other matters involving environmental contamination may also have a material adverse impact on our business, financial condition or results of operations.

9

We may incur material product liability costs.

We may be subject to product liability claims in the event that the failure of any of our products results in personal injury or death and we cannot assure you that we will not experience material product liability losses in the future. We maintain insurance against such product liability claims, but we cannot assure you that such coverage will be adequate for liabilities ultimately incurred or that it will continue to be available on terms acceptable to us. In addition, if any of our products prove to be defective, we may be required to participate in government-imposed or customer OEM-instituted recalls involving such products. A successful claim brought against us that exceeds available insurance coverage or a

requirement to participate in any product recall could have a material adverse effect on our business, financial condition or results of operations.

Increased or unexpected product warranty claims could adversely affect us.

We provide our customers a warranty covering workmanship, and in some cases materials, on products we manufacture. Our warranty generally provides that products will be free from defects and adhere to customer specifications. If a product fails to comply with the warranty, we may be obligated or compelled, at our expense, to correct any defect by repairing or replacing the defective product. We maintain warranty reserves in an amount based historical trends of units sold and payment amounts combined with our current understanding of the status of existing claims. To estimate the warranty reserves, we must forecast the resolution of existing claims, as well as expected future claims on products previously sold. The

amounts estimated to be due and payable could differ materially from what we may ultimately be required to pay. An increase in the rate of warranty claims or the occurrence of unexpected warranty claims could have a material adverse effect on our customer relations and our financial condition or results of operations.

Disruptions in the financial markets are adversely impacting the availability and cost of credit which could negatively affect our business.

The credit facility has a maximum borrowing level of $100.0 million and is scheduled to expire on November 1, 2012. The available borrowing capacity on this credit facility is based on eligible current assets, as defined. As of December 31, 2010, we had borrowing capacity of $61.3 million, based on eligible current assets. We will need to refinance the credit facility prior to its expiration. Disruptions in the financial markets, including the bankruptcy, insolvency or restructuring of certain financial institutions, and the general lack of liquidity may adversely impact the availability and cost of credit. We may be required to refinance the credit facility at terms and rates that are less

favorable than our current terms and rates, which could adversely affect our business, financial condition or results of operations.

Our debt obligations could limit our flexibility in managing our business and expose us to risks.

We are highly leveraged. As of December 31, 2010, the face amount of our senior secured notes was $175.0 million. In addition, we are permitted under the credit facility and the indenture governing the senior secured notes to incur additional debt, subject to specified limitations. Our high degree of leverage and the terms of our indebtedness may have important consequences including the following:

|

|

•

|

we may have difficulty satisfying our obligations with respect to our indebtedness, and if we fail to comply with these requirements, an event of default could result;

|

|

|

•

|

we may be required to dedicate a substantial portion of our cash flow from operations to required payments on indebtedness, thereby reducing the availability of cash flow for working capital, capital expenditures and other general corporate activities;

|

|

|

•

|

covenants relating to our debt may limit our ability to obtain additional financing for working capital, capital expenditures and other general corporate activities;

|

|

|

•

|

covenants relating to our debt may limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

|

|

|

•

|

we may be more vulnerable than our competitors to the impact of economic downturns and adverse developments in our business; and

|

|

|

•

|

we may be placed at a competitive disadvantage against any less leveraged competitors.

|

These and other consequences of our substantial leverage and the terms of our indebtedness could have a material adverse effect on our business, financial condition or results of operations.

10

Covenants in our credit facility and our indenture governing the senior secured notes may limit our ability to pursue our business strategies.

Our credit facility and the indenture governing our senior secured notes limit our ability to, among other things:

|

|

•

|

incur additional debt and guarantees;

|

|

|

•

|

pay dividends and repurchase our stock;

|

|

|

•

|

make other restricted payments, including investments;

|

|

|

•

|

create liens;

|

|

|

•

|

sell or otherwise dispose of assets, including capital stock of subsidiaries;

|

|

|

•

|

enter into agreements that restrict dividends from subsidiaries;

|

|

|

•

|

enter into transactions with our affiliates;

|

|

|

•

|

consolidate, merge or sell or otherwise dispose of all or substantially all of our assets; and

|

|

|

•

|

substantially change the nature of our business.

|

The agreement governing our credit facility also requires us to maintain a ratio of (1) consolidated EBITDA, as defined in the credit facility, less specified items to (2) consolidated fixed charges, as defined in the credit facility, of at least 1.10 to 1.00 whenever undrawn availability under the credit facility is less than $20 million. Our ability to comply with this fixed charge coverage ratio requirement, as well as the restrictive covenants under the terms of our indebtedness, may be affected by events beyond our control.

The restrictions contained in our indenture governing the senior secured notes and the agreement governing the credit facility could:

|

|

•

|

limit our ability to plan for or react to market conditions or meet capital needs or otherwise restrict our activities or business plans; and

|

|

|

•

|

adversely affect our ability to finance our operations, strategic acquisitions, investments or alliances or other capital needs or to engage in other business activities that would be in our interest.

|

A breach of any of the restrictive covenants under our indebtedness or our inability to comply with the fixed charge coverage ratio requirement in the credit facility could result in a default under the agreement governing the credit facility and the indenture governing the senior secured notes. If a default occurs, holders of the senior secured notes could declare all principal and interest to be due and payable, the lenders under the credit facility could elect to declare all outstanding borrowings, together with accrued interest and other fees, to be immediately due and payable and terminate any commitments they have to provide further borrowings, and holders of the senior secured notes and the credit facility

lenders could pursue foreclosure and other remedies against us and our assets.

We may not be able to generate sufficient cash flows to meet our debt service obligations.

Our ability to make scheduled payments on, or to refinance, our obligations with respect to our indebtedness will depend on our financial and operating performance, which in turn will be affected by general economic conditions and by financial, competitive, regulatory and other factors beyond our control. We cannot assure you that our business will generate sufficient cash flow from operations or that future sources of capital will be available to us in an amount sufficient to enable us to service our indebtedness or to fund our other liquidity needs. If we are unable to generate sufficient cash flow to satisfy our debt obligations, we may have to undertake alternative financing plans, such as refinancing or

restructuring our debt, selling assets, reducing or delaying capital investments or seeking to raise additional capital. We cannot assure you that any refinancing would be possible, that any assets could be sold or, if sold, of the timing of the sales and the amount of proceeds that may be realized from those sales, or that additional financing could be obtained on acceptable terms, if at all. The credit facility and the indenture governing the senior secured notes restrict our ability to dispose of assets and use the proceeds from the disposition. Our inability to generate sufficient cash flows to satisfy our debt obligations, or to refinance our indebtedness on commercially reasonable terms, would materially and adversely affect our business, financial condition and results of operations.

11

If we cannot make scheduled payments on our debt, we will be in default and, as a result, holders of the senior secured notes could declare all outstanding principal and interest to be due and payable, the lenders under the credit facility could terminate their commitments to lend us money, holders of the senior secured notes and the lenders under the credit facility could foreclose on or exercise other remedies against the assets securing the senior secured notes and borrowings under the credit facility and we could be forced into bankruptcy, liquidation or other insolvency proceedings, which, in each case, could result in your losing your investment in the Common Shares.

We are subject to risks related to our international operations.

Approximately 19.2% of our net sales in 2010 were derived from sales outside of North America. Non-current assets outside of North America accounted for approximately 8.7% of our non-current assets as of December 31, 2010. International sales and operations are subject to significant risks, including, among others:

|

|

•

|

political and economic instability;

|

|

|

•

|

restrictive trade policies;

|

|

|

•

|

economic conditions in local markets;

|

|

|

•

|

currency exchange controls;

|

|

|

•

|

labor unrest;

|

|

|

•

|

difficulty in obtaining distribution support and potentially adverse tax consequences; and

|

|

|

•

|

the imposition of product tariffs and the burden of complying with a wide variety of international and U.S. export laws.

|

Additionally, to the extent any portion of our net sales and expenses are denominated in currencies other than the U.S. dollar, changes in exchange rates could have a material adverse effect on our results of operations or financial condition.

We face risks arising from our equity investments in companies that we do not control.

Our consolidated results of operations include significant equity earnings from unconsolidated subsidiaries. For the year ended December 31, 2010, we recognized $10.3 million of equity earnings and received $5.5 million in cash dividends from our unconsolidated joint ventures, PST and Minda. Our ability to direct the operations of these entities is limited because we do not own a majority interest in either of them and we are bound by the terms of agreements with our joint venture partners. The performance of these joint ventures could also be adversely affected by disagreements between us and our joint venture partners, and sales of our equity interests in these entities are subject to rights of first refusal and

other contractual limitations.

Our annual effective tax rate could be volatile and materially change as a result of changes in the mix of earnings and other factors.

Our overall effective tax rate is equal to our total tax expense as a percentage of our total earnings before tax. However, tax expense and benefits are not recognized on a global basis, but rather on a jurisdictional or legal entity basis. Losses in certain jurisdictions may not provide a current financial statement tax benefit. As a result, changes in the mix of earnings between jurisdictions, among other factors, could have a significant impact on our overall effective tax rate.

If we fail to protect our intellectual property rights or maintain our rights to use licensed intellectual property or are found liable for infringing the rights of others, our business could be adversely affected.

Our intellectual property, including our patents, trademarks, copyrights, trade secrets and license agreements, are important in the operation of our businesses, and we rely on the patent, trademark, copyright and trade secret laws of the United States and other countries, as well as nondisclosure agreements, to protect our intellectual property rights. We may not, however, be able to prevent third parties from infringing, misappropriating or otherwise violating our intellectual property, breaching any nondisclosure agreements with us, or independently developing technology that is similar or superior to ours and not covered by our intellectual property. Any of the foregoing could reduce any competitive advantage we

have developed, cause us to lose sales or otherwise harm our business. We cannot assure you that any intellectual property will provide us with any competitive advantage or will not be challenged, rejected, cancelled, invalidated or declared unenforceable. In the case of pending patent applications, we may not be successful in securing issued patents, or securing patents that provide us with a competitive advantage for our businesses. In addition, our competitors may design products around our patents that avoid infringement and violation of our intellectual property rights.

12

We cannot be certain that we have rights to use all intellectual property used in the conduct of our businesses or that we have complied with the terms of agreements by which we acquire such rights, which could expose us to infringement, misappropriation or other claims alleging violations of third party intellectual property rights. Third parties have asserted and may assert or prosecute infringement claims against us in connection with the services and products that we offer, and we may or may not be able to successfully defend these claims. Litigation, either to enforce our intellectual property rights or to defend against claims regarding intellectual property rights of others, could result in substantial costs

and in a diversion of our resources. Any such claims and resulting litigation could require us to enter into licensing agreements (if available on acceptable terms or at all), pay damages and cease making or selling certain products and could result in a loss of our intellectual property protection. Moreover, we may need to redesign some of our products to avoid future infringement liability. We also may be required to indemnify customers or other third parties at significant expense in connection with such claims and actions. Any of the foregoing could have a material adverse effect on our business, financial condition or results of operations.

Our inability to recover from natural or man-made disasters or similar events could adversely affect our business.

Our business and financial results may be affected by certain events that we cannot anticipate or that are beyond our control, such as natural or man-made disasters, national emergencies, significant labor strikes, work stoppages, political unrest, war or terrorist activities that could curtail production at our facilities and cause delayed deliveries and canceled orders. In addition, we purchase components, raw materials, information technology and other services from numerous suppliers, and, even if our facilities are not directly affected by such events, we could be affected by interruptions at such suppliers. Such suppliers may not be able to quickly recover from such events and may be subject to additional risks

such as financial problems that limit their ability to conduct their operations. We cannot assure you that we will have insurance to adequately compensate us for any of these events.

We may not be able to successfully integrate acquisitions into our business or may otherwise be unable to benefit from pursuing acquisitions.

Failure to successfully identify, complete and/or integrate acquisitions could have a material adverse effect on us. A portion of our growth in sales and earnings has been generated from acquisitions and subsequent improvements in the performance of the businesses acquired. We expect to continue a strategy of selectively identifying and acquiring businesses with complementary products. We cannot assure you that any business acquired by us will be successfully integrated with our operations or prove to be profitable. We could incur substantial indebtedness in connection with our acquisition strategy, which could significantly increase our interest expense. Covenant restrictions relating to such indebtedness could

restrict our ability to pay dividends, fund capital expenditures and consummate additional acquisitions. We anticipate that acquisitions could occur in geographic markets, including foreign markets, in which we do not currently operate. As a result, the process of integrating acquired operations into our existing operations may result in unforeseen operating difficulties and may require significant financial resources that would otherwise be available for the ongoing development or expansion of existing operations. Any failure to successfully integrate such acquisitions could have a material adverse impact on our business, financial condition or results of operations.

Item 1B. Unresolved Staff Comments.

None.

13

Item 2. Properties.

The Company and its joint ventures currently own or lease 18 manufacturing facilities that are in use, which together contain approximately 1.6 million square feet of manufacturing space. Of these manufacturing facilities, 11 are used by our Electronics reportable segment, four are used by our Control Devices reportable segment and three are owned by our joint venture companies. The following table provides information regarding our facilities:

|

Owned/

|

Square

|

|||||||

|

Location

|

Leased

|

Use

|

Footage

|

|||||

|

Electronics

|

||||||||

|

Juarez, Mexico

|

Owned

|

Manufacturing/Division Office

|

183,854 | |||||

|

Portland, Indiana

|

Owned

|

Manufacturing

|

182,000 | |||||

|

Chihuahua, Mexico

|

Owned

|

Manufacturing

|

135,569 | |||||

|

Monclova, Mexico

|

Leased

|

Manufacturing

|

114,140 | |||||

|

Tallinn, Estonia

|

Leased

|

Manufacturing

|

85,911 | |||||

|

Walled Lake, Michigan

|

Leased

|

Manufacturing/Division Office

|

78,225 | |||||

|

Orebro, Sweden

|

Leased

|

Manufacturing

|

77,472 | |||||

|

Mitcheldean, England

|

Leased

|

Manufacturing (Vacant)

|

74,790 | |||||

|

Chihuahua, Mexico

|

Leased

|

Manufacturing

|

61,619 | |||||

|

El Paso, Texas

|

Leased

|

Warehouse

|

50,000 | |||||

|

Chihuahua, Mexico

|

Leased

|

Manufacturing

|

49,805 | |||||

|

Stockholm, Sweden

|

Leased

|

Engineering Office/Division Office

|

37,714 | |||||

|

Dundee, Scotland

|

Leased

|

Manufacturing/Sales Office/Engineering Office

|

32,753 | |||||

|

Portland, Indiana

|

Leased

|

Warehouse

|

25,000 | |||||

|

Warren, Ohio

|

Leased

|

Engineering Office/Division Office

|

24,570 | |||||

|

Chihuahua, Mexico

|

Leased

|

Engineering Office/Manufacturing

|

10,000 | |||||

|

Bayonne, France

|

Leased

|

Sales Office/Warehouse

|

9,655 | |||||

|

Stockholm, Sweden

|

Owned

|

Sales Office/Warehouse

|

2,013 | |||||

|

Madrid, Spain

|

Leased

|

Sales Office/Warehouse

|

1,560 | |||||

|

Rome, Italy

|

Leased

|

Sales Office

|

1,216 | |||||

|

Control Devices

|

||||||||

|

Lexington, Ohio

|

Owned

|

Manufacturing/Division Office

|

219,612 | |||||

|

Canton, Massachusetts

|

Owned

|

Manufacturing

|

132,560 | |||||

|

Sarasota, Florida

|

Owned

|

Manufacturing (Vacant)

|

115,000 | |||||

|

Suzhou, China

|

Leased

|

Manufacturing/Warehouse/Division Office

|

25,737 | |||||

|

Lexington, Ohio

|

Leased

|

Warehouse

|

15,000 | |||||

|

Lexington, Ohio

|

Leased

|

Warehouse

|

7,788 | |||||

|

Sarasota, Florida

|

Owned

|

Warehouse (Vacant)

|

7,500 | |||||

|

Shanghai, China

|

Leased

|

Engineering Office/Sales Office

|

6,345 | |||||

|

Lexington, Ohio

|

Leased

|

Manufacturing

|

2,700 | |||||

|

Corporate

|

||||||||

|

Novi, Michigan

|

Leased

|

Sales Office/Engineering Office

|

9,400 | |||||

|

Warren, Ohio

|

Owned

|

Headquarters

|

7,500 | |||||

|

Stuttgart, Germany

|

Leased

|

Sales Office/Engineering Office

|

1,000 | |||||

|

Seoul, South Korea

|

Leased

|

Sales Office

|

330 | |||||

|

Joint Ventures

|

||||||||

|

Manaus, Brazil

|

Owned

|

Manufacturing

|

102,247 | |||||

|

Pune, India

|

Owned

|

Manufacturing/Engineering Office/Sales Office

|

80,000 | |||||

|

São Paulo, Brazil

|

Owned

|

Manufacturing/Engineering Office/Sales Office

|

45,467 | |||||

|

Buenos Aires, Argentina

|

Leased

|

Sales Office

|

3,551 | |||||

14

Item 3. Legal Proceedings.

We are involved in certain legal actions and claims arising in the ordinary course of business. However, we do not believe that any of the litigation in which we are currently engaged, either individually or in the aggregate, will have a material adverse effect on our business, consolidated financial position or results of operations. We are subject to the risk of exposure to product liability claims in the event that the failure of any of our products causes personal injury or death to users of our products and there can be no assurance that we will not experience any material product liability losses in the future. We maintain insurance against such product liability claims. In addition, if

any of our products prove to be defective, we may be required to participate in a government-imposed or customer OEM-instituted recall involving such products.

Item 4. (Removed and Reserved)

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our shares are listed on the New York Stock Exchange (“NYSE”) under the symbol “SRI.” As of February 8, 2011, we had 25,994,265 Common Shares without par value, issued and outstanding, which were owned by approximately 300 registered holders, including Common Shares held in the names of brokers and banks (so-called “street name” holdings) who are record holders with approximately 2,400 beneficial owners.

The Company has not historically paid or declared dividends, which are restricted under both the senior secured notes and the asset-based credit facility, on our Common Shares. We may only pay cash dividends in the future if immediately prior to and immediately after the payment is made, no event of default shall have occurred and outstanding indebtedness under our asset-based credit facility is not greater than or equal to $20.0 million before and after the payment of the dividend. We currently intend to retain earnings for acquisitions, working capital, capital expenditures, general corporate purposes and reduction in outstanding indebtedness. Accordingly, we do not expect to pay cash dividends in

the foreseeable future.

High and low sales prices for our Common Shares for each quarter ended during 2010 and 2009 are as follows:

|

Quarter Ended

|

High

|

Low

|

|||||||

|

2010

|

March 31

|

$ | 10.23 | $ | 6.00 | ||||

|

June 30

|

$ | 12.30 | $ | 7.57 | |||||

|

September 30

|

$ | 11.53 | $ | 7.02 | |||||

|

December 31

|

$ | 17.19 | $ | 10.02 | |||||

|

2009

|

March 31

|

$ | 4.80 | $ | 1.41 | ||||

|

June 30

|

$ | 4.89 | $ | 1.97 | |||||

|

September 30

|

$ | 7.20 | $ | 3.70 | |||||

|

December 31

|

$ | 9.60 | $ | 6.14 | |||||

The Company did not repurchase any Common Shares in 2010 or 2009.

15

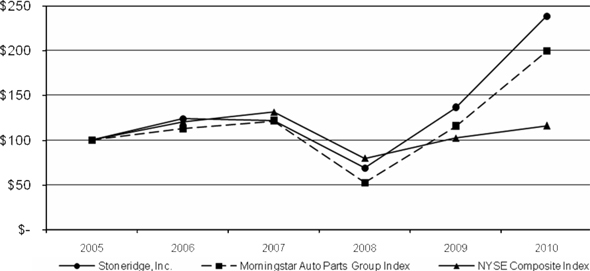

Set forth below is a line graph comparing the cumulative total return of a hypothetical investment in our Common Shares with the cumulative total return of hypothetical investments in the Morningstar Auto Parts Industry Group Index and the NYSE Composite Index based on the respective market price of each investment as of December 31, 2005, 2006, 2007, 2008, 2009 and 2010 assuming in each case an initial investment of $100 on December 31, 2005, and reinvestment of dividends.

|

2005

|

2006

|

2007

|

2008

|

2009

|

2010

|

|||||||||||||||||||

|

Stoneridge, Inc.

|

$ | 100 | $ | 124 | $ | 121 | $ | 69 | $ | 136 | $ | 239 | ||||||||||||

|

Morningstar Auto Parts Group Index (A)

|

$ | 100 | $ | 113 | $ | 121 | $ | 52 | $ | 115 | $ | 200 | ||||||||||||

|

NYSE Composite Index

|

$ | 100 | $ | 120 | $ | 131 | $ | 80 | $ | 102 | $ | 116 | ||||||||||||

|

(A)

|

The Morningstar Auto Parts Group Index was formerly known as the Hemscott Group – Industry Group 333 Index.

|

For information on “Related Stockholder Matters” required by Item 201(d) of Regulation S-K, refer to Item 12 of this report.

16

Item 6. Selected Financial Data.

The following table sets forth selected historical financial data and should be read in conjunction with the consolidated financial statements and notes related thereto and other financial information included elsewhere herein. The selected historical data was derived from our consolidated financial statements.

|

Years ended December 31 (in thousands, except per share data)

|

2010

|

2009

|

2008

|

2007

|

2006

|

|||||||||||||||

|

Statement of Operations Data:

|

||||||||||||||||||||

|

Net sales:

|

||||||||||||||||||||

|

Electronics

|

$ | 414,337 | $ | 311,268 | $ | 533,328 | $ | 458,672 | $ | 456,932 | ||||||||||

|

Control Devices

|

240,894 | 176,815 | 236,038 | 289,979 | 271,943 | |||||||||||||||

|

Eliminations

|

(20,005 | ) | (12,931 | ) | (16,668 | ) | (21,531 | ) | (20,176 | ) | ||||||||||

|

Total net sales

|

$ | 635,226 | $ | 475,152 | $ | 752,698 | $ | 727,120 | $ | 708,699 | ||||||||||

|

Gross profit

|

$ | 144,835 | $ | 87,985 | $ | 166,287 | $ | 167,723 | $ | 158,906 | ||||||||||

|

Operating income (loss) (A)

|

$ | 22,803 | $ | (18,243 | ) | $ | (43,271 | ) | $ | 34,799 | $ | 35,063 | ||||||||

|

Equity in earnings of investees

|

$ | 10,346 | $ | 7,775 | $ | 13,490 | $ | 10,893 | $ | 7,125 | ||||||||||

|

Income (loss) before income taxes (A), (B)

|

||||||||||||||||||||

|