Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - TIDEWATER INC | d8k.htm |

| EX-99.2 - TRANSCRIPT OF THE PRESENTATION PRESENTED AT THE 2011 CS ENERGY SUMMIT CONFERENCE - TIDEWATER INC | dex992.htm |

CREDIT SUISSE

CREDIT SUISSE

2011 ENERGY SUMMIT

2011 ENERGY SUMMIT

February 8, 2011

February 8, 2011

Quinn P. Fanning

Quinn P. Fanning

Executive Vice President and

Executive Vice President and

Chief Financial Officer

Chief Financial Officer

Joseph M. Bennett

Joseph M. Bennett

Executive Vice President and

Executive Vice President and

Chief Investor Relations Officer

Chief Investor Relations Officer

Exhibit 99.1 |

FORWARD-LOOKING STATEMENTS

FORWARD-LOOKING STATEMENTS

2

Phone:

504.568.1010

Fax:

504.566.4580

Web:

www.tdw.com

Email:

connect@tdw.com

In accordance with the safe harbor provisions of the Private Securities Litigation Reform

Act

of

1995,

the

Company

notes

that

certain

statements

set

forth

in

this

presentation

provide other than historical information and are forward looking. The actual

achievement of any forecasted results, or the unfolding of future economic or business

developments in a way anticipated or projected by the Company, involve numerous risks

and uncertainties that may cause the Company’s actual performance to be materially

different from that stated or implied in the forward-looking statement. Among those risks

and uncertainties, many of which are beyond the control of the Company, include,

without limitation, fluctuations in worldwide energy demand and oil and gas prices;

fleet additions by competitors and industry overcapacity; changes in capital spending

by customers in the energy industry for offshore exploration, development and

production; changing customer demands for vessel specifications, which may make some of

our older vessels technologically obsolete for certain customer projects or in certain

markets; instability of global financial markets and difficulty accessing

credit or capital; acts of

terrorism and piracy; significant weather conditions; unsettled political conditions, war,

civil unrest and governmental actions, such as expropriation, especially in higher risk

countries of operations; foreign currency fluctuations; labor influences proposed by

international conventions; increased regulatory burdens and oversight following the

Deepwater Horizon incident; and enforcement of laws related to the environment, labor

and foreign corrupt practices. Participants should consider all of these risk factors

as well as other information contained in the Company’s form 10-K’s and

10-Q’s. |

KEY

TAKEAWAYS Culture of safety & operating excellence

History of earnings growth and solid returns

World’s largest and newest fleet provides

basis for continued earnings growth

Strong balance sheet allows us to act upon

available opportunities

3 |

SM

SAFETY –

SAFETY –

A TOP PRIORITY

A TOP PRIORITY

4 |

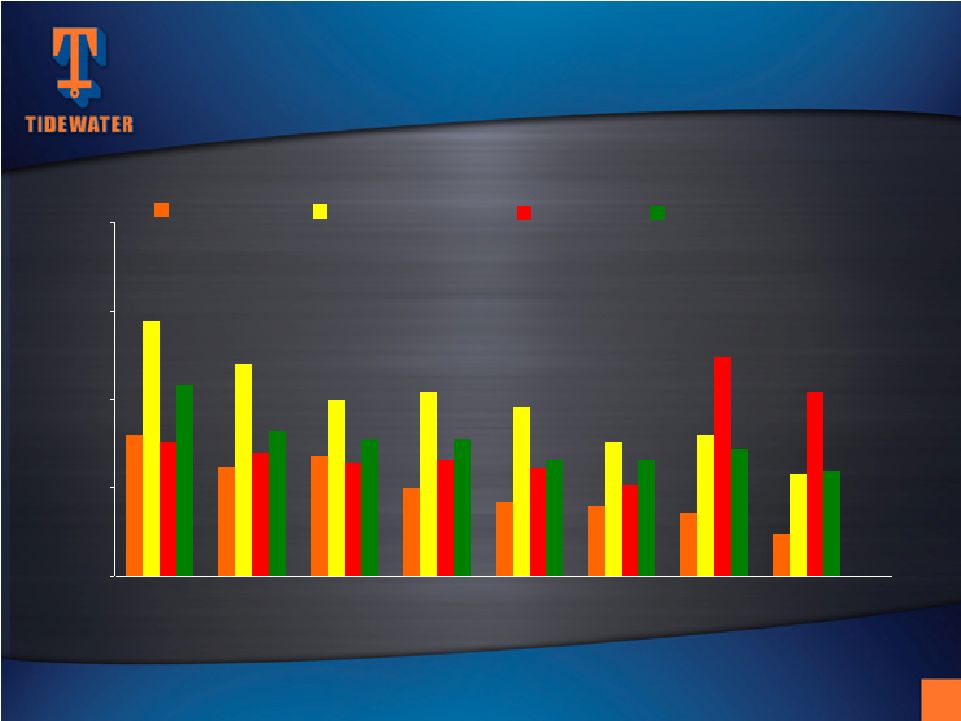

0.00

0.25

0.50

0.75

1.00

Total Recordable Incident Rates

Calendar Years

2002

2003

2004

2005

2006

2007

2008

2009

TIDEWATER

DUPONT

DOW CHEMICAL

EXXON MOBIL

SAFETY RECORD RIVALS

SAFETY RECORD RIVALS

LEADING COMPANIES

LEADING COMPANIES

5 |

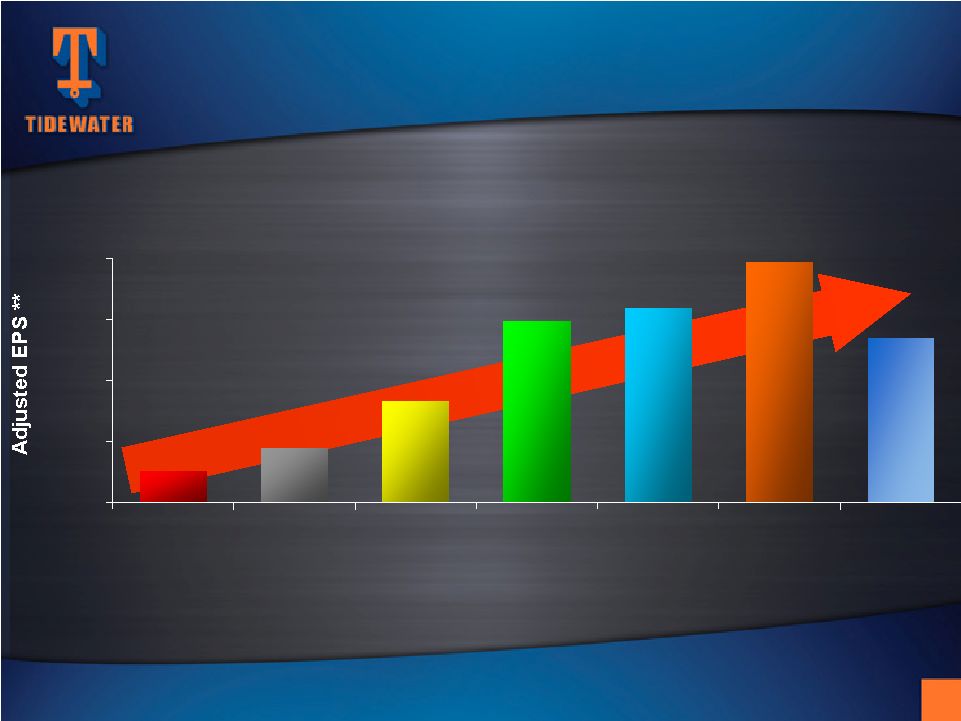

32%

Six-Year Compounded Annual Earnings Growth Rate

**

EPS

in

Fiscal

2004

is

exclusive

of

the

$.30

per

share

after

tax

impairment

charge.

EPS

in

Fiscal

2006

is

exclusive

of

the

$.74

per

share

after

tax

gain

from

the

sale

of

six

KMAR

vessels.

EPS

in

Fiscal

2007

is

exclusive

of

$.37

per

share

of

after

tax

gains

from

the

sale

of

14

offshore

tugs.

EPS

in

Fiscal

2010

is

exclusive

of

$.87

per

share

Venezuelan

provision,

a

$.70

per

share

tax

benefit

related

to

favorable

resolution

of

tax

litigation

and

a

$0.22

per

share

charge

for

the

proposed

settlement

with

the

SEC

of

the

company’s

FCPA

matter.

Adjusted Return

On Avg. Equity

4.3% 7.2%

12.4%

18.5%

18.3%

19.5%

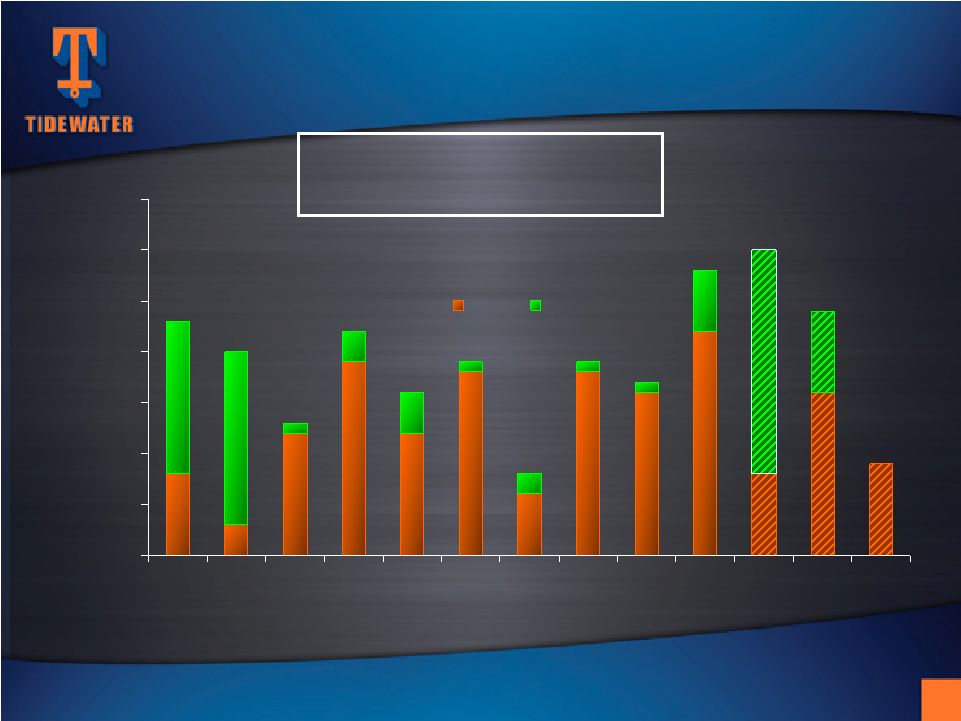

11.9% SIGNIFICANT EARNINGS GROWTH

SIGNIFICANT EARNINGS GROWTH

6

$5.41

$7.89

$1.03

$1.78

$3.33

$5.94

$6.39

$0.00

$2.00

$4.00

$6.00

$8.00

Fiscal 2004

Fiscal 2005

Fiscal 2006

Fiscal 2007

Fiscal 2008

Fiscal 2009

Fiscal 2010 |

Avg.

Dayrates $14,561*

$16,017

(+ 10%)

$17,619

(+ 10%)

85.8%*

85.0%

90.0%

~$4.20

EPS

~$6.00

EPS

~$9.50

EPS

273 vessels assumes (191 current new vessels + 37 under construction + ~ 20

additional new vessels per year for two and a quarter years).

WHERE COULD FISCAL 2014 FIND US?

WHERE COULD FISCAL 2014 FIND US?

Potential for Earnings Acceleration

Potential for Earnings Acceleration

* 12/31/10 nine month YTD actual stats

This info is not meant to be a

prediction of future earnings

performance, but simply an

indication of earning sensitivities

resulting from future fleet

additions and reductions and

varying operating assumptions.

7

~$400M+

EBITDA

~$525M+

EBITDA

~$750M+

EBITDA |

Unique global footprint; 50+ years of Int’l experience

Unmatched scale and scope of operations

International market opportunities

•

Growth

•

Longer contracts

•

Better utilization

•

Higher dayrates

Solid customer base of NOC’s and IOC’s

INTERNATIONAL STRENGTH

INTERNATIONAL STRENGTH

8 |

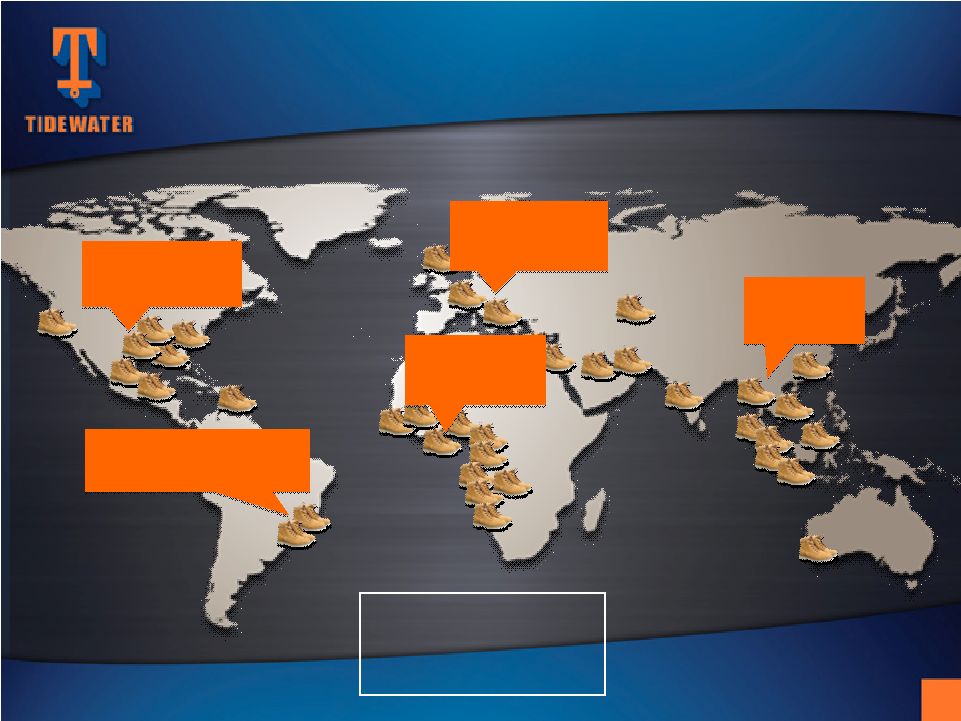

OUR

GLOBAL FOOTPRINT OUR GLOBAL FOOTPRINT

Vessel Distribution by Region

Vessel Distribution by Region

(excludes stacked vessels –

as of 12/31/10)

North America

17

(6%)

Central/South America

55

(20%)

West Africa

130

(47%)

Europe / M.E.

36

(13%)

Far East

39

(14%)

International / U.S.

2010: 94% / 6%

2000: 62% / 38%

9 |

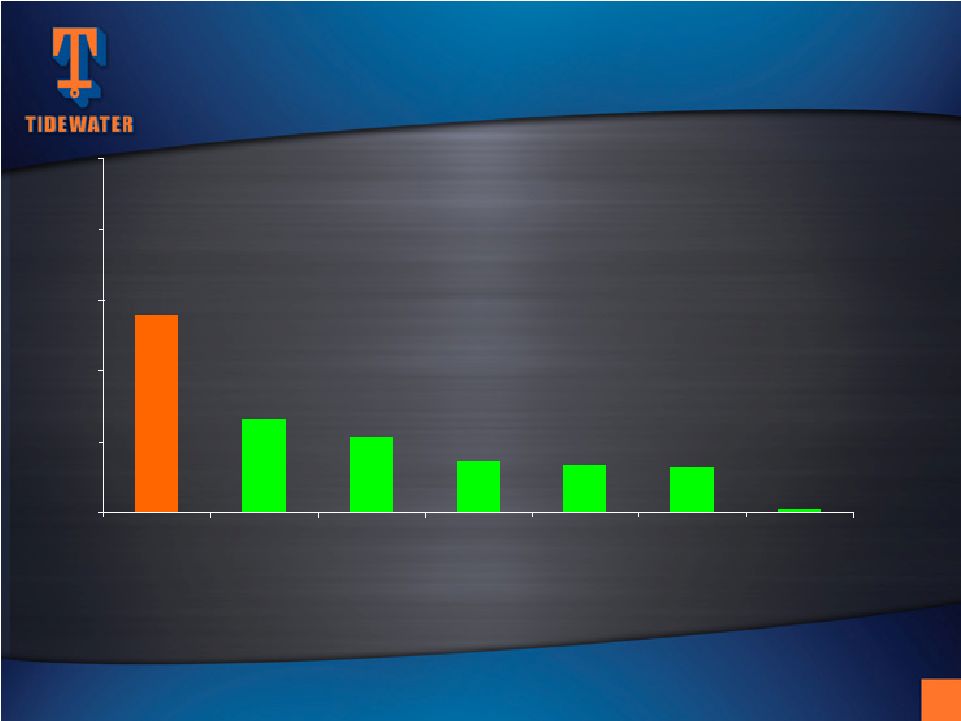

VESSEL POPULATION BY OWNER

VESSEL POPULATION BY OWNER

(Includes AHTS and PSV’s

only) Estimated as of Mid-January 2011

Source:

ODS-Petrodata

and

Tidewater

Tidewater

Competitor #2

Competitor #3

Competitor #4

Competitor # 5

Competitor #1

Avg.

All Others (1,867

total

vessels for

350+ owners)

5

64

67

72

106

132

280

0

100

200

300

400

500

Tidewater fleet includes 138 vessel additions since 2000

10 |

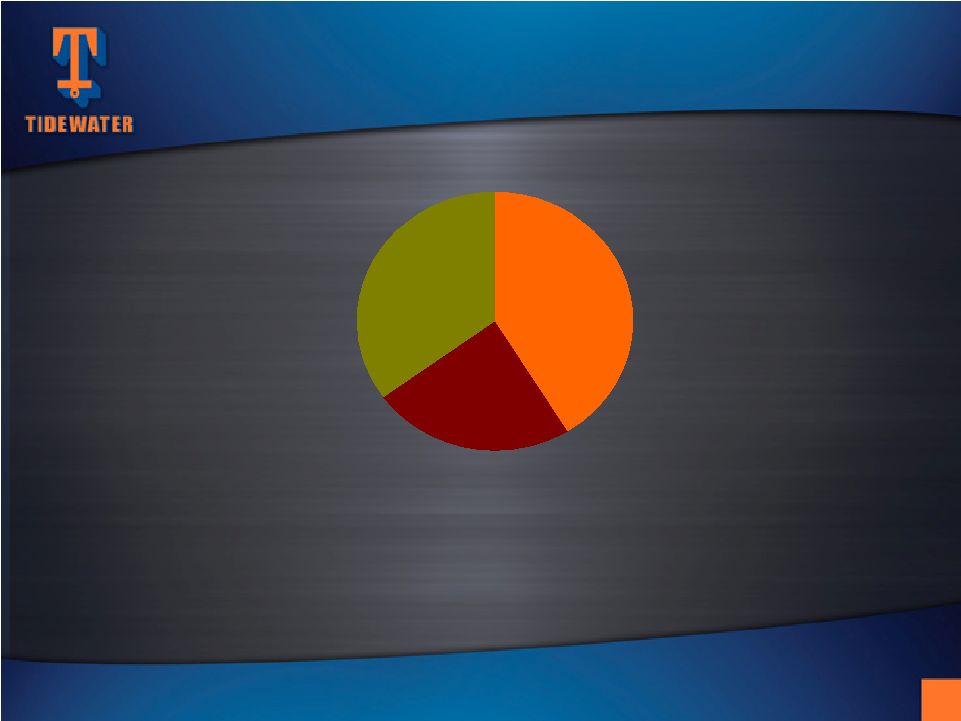

NOC's

24%

Others

35%

Super Majors

41%

Our top 10 customers in Fiscal 2010 (6 Super Majors,

3 NOC’s and one large independent) accounted for 63% of our revenue

CURRENT REVENUE MIX

CURRENT REVENUE MIX

Quality of Customer Base

Quality of Customer Base

11 |

0

50

100

150

200

250

300

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

THE WORLDWIDE FLEET -

THE WORLDWIDE FLEET -

RETIREMENTS

RETIREMENTS

EXPECTED TO EXCEED NEW DELIVERIES

EXPECTED TO EXCEED NEW DELIVERIES

(Includes AHTS and PSV’s

only) Estimated as of Mid-January2011

Source:

ODS-Petrodata

and

Tidewater

As of mid-January 2011, there are approximately 387 additional AHTS

and PSV’s

(~15% of the global fleet) under construction.

Global fleet estimated at 2,588 vessels, including 331 vessels

that are 30+ yrs old (13%),

and another 454 vessels that are

25-29 yrs old (18%)

12

Vessels > 25 years old today |

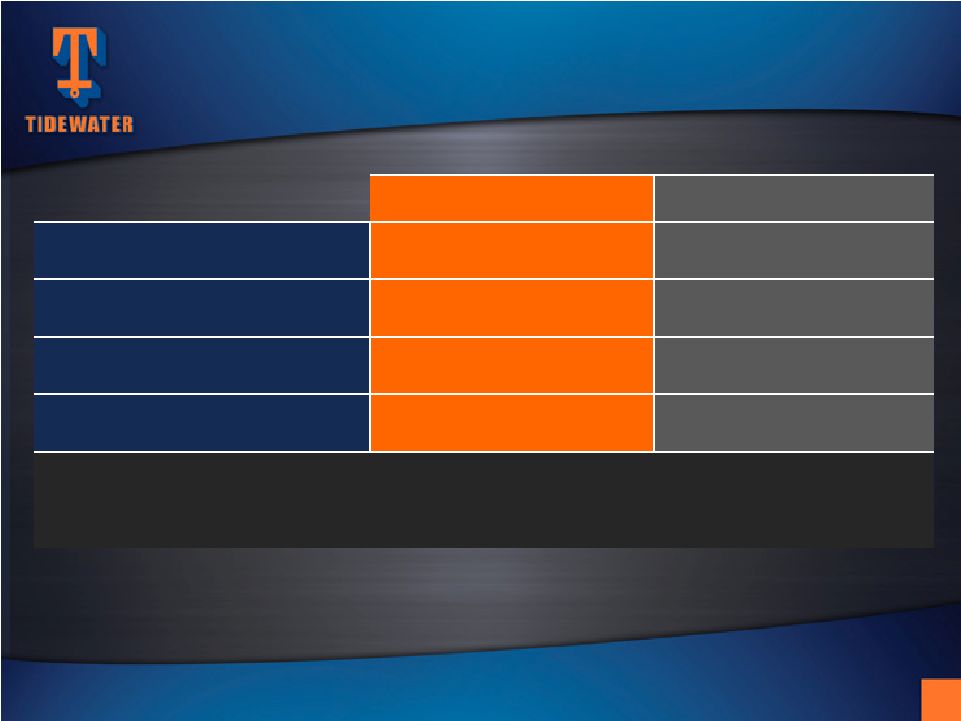

Vessel Count

Estimated Cost

AHTS

99

$1,735m

PSV’s

82

$1,651m

Crewboats & Tugs

67

$290m

TOTALS:

248

$3,676m

(1)

(1) $3,190m (87%) funded through 12/31/10

.

THE LARGEST MODERN FLEET

THE LARGEST MODERN FLEET

IN THE INDUSTRY…

IN THE INDUSTRY…

At 12/31/10, 191 new vessels in fleet with ~4.5 year average age

Vessel Commitments

Jan. ’00 –

December ‘10

13 |

0

5

10

15

20

25

30

35

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Built

Acquired

VESSEL DELIVERIES

VESSEL DELIVERIES

14

Fiscal Year

Fiscal years 2011-2013 include actual deliveries through 12/31/10 and

estimated deliveries of vessels committed to build or acquire as

of 12/31/10

At 12/31/10, total 248 vessels with

a capital cost of $3.68 billion |

Count

AHTS

18

PSV

18

Crew and Tug

1

Total

37

Vessels Under Construction*

As of December 31, 2010

…

…

AND OUR LEAD IS GROWING

AND OUR LEAD IS GROWING

* Includes eleven new vessels committed to purchase as of 12/31/10

Estimated delivery schedule –

4 in remainder of FY ‘11,

24 in FY ‘12 and 9 thereafter

CAPX of $130m in remainder of FY ‘11,

$303m in FY ‘12 and $53m in FY ‘13

15 |

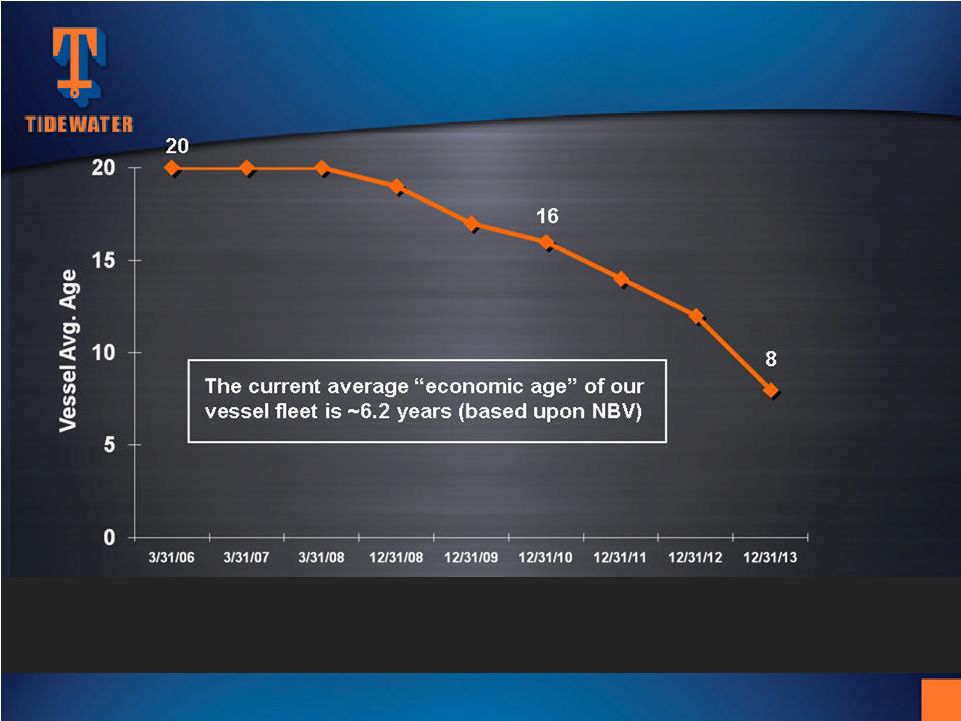

SIGNIFICANT AVERAGE AGE IMPROVEMENT

SIGNIFICANT AVERAGE AGE IMPROVEMENT

Assumptions: 1) Average 45 vessel disposals per year in future (averaged 47 per

year last three years). 2) Includes 37 vessels under construction (including

eleven purchase commitments) in year delivered plus additional

newbuilds/acquisitions from approximately $500 million per year of future

commitments (average additional 20 vessels

per year). Tidewater is not committed to spending $500 million annually, but this

level is used as an assumption in estimating average fleet age in the

future. 16 |

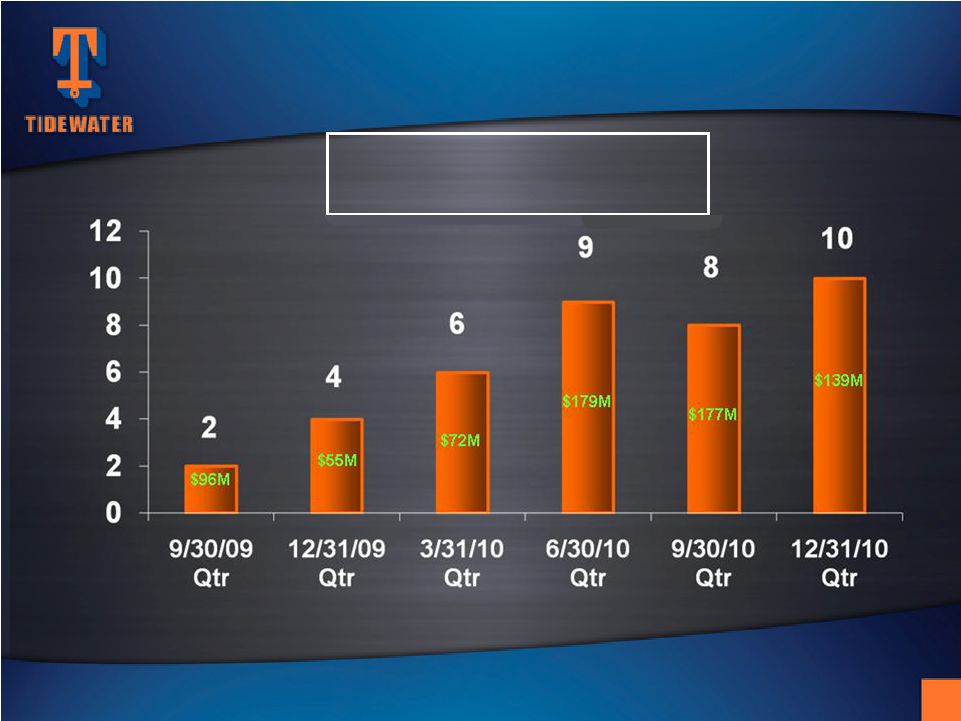

RECENT VESSEL COMMITMENTS

RECENT VESSEL COMMITMENTS

17

Amounts depict vessel count and total cost in quarter commitment

was made to acquire (not when delivery or payments were made)

1 MPSV

1 PSV

4 AHTS

6 AHTS

6 AHTS

3 PSV’s

39 vessels over six quarters with

total capital cost of $718 million

4 PSV’s

4 AHTS

1 PSV

9 AHTS |

Senior Unsecured Notes

$425 million

Average Life to Maturity

~ 9 years

Weighted Average Coupon

4.25%

Closing Dates

$310 million 10/15/10

$115 million 12/30/10

NEW PRIVATE PLACEMENT FINANCING

NEW PRIVATE PLACEMENT FINANCING

18 |

Term Loan*

$125 million

Revolving Line of Credit

$450 million

Term

Five years

Interest Rate

Prime plus 0.5 to 1.25%, or

Eurodollar plus 1.5 to 2.25%

NEW CREDIT FACILITIES

NEW CREDIT FACILITIES

19

*

Term loan allows for multiple draws for up to 180 days from 1/27/11.

|

A

STRONG BALANCE SHEET A STRONG BALANCE SHEET

AND READY LIQUIDITY

AND READY LIQUIDITY

20

December 31, 2010 info:

Cash & Cash Equivalents

$308 million

Total Debt

$700 million

Shareholders Equity

$2,506 million

Net Debt / Net Capitalization

14%

Total Debt / Capitalization

22%

Pro forma liquidity as of 12/31/10 of ~ $885 million,

including $575 million available under credit facilities

|

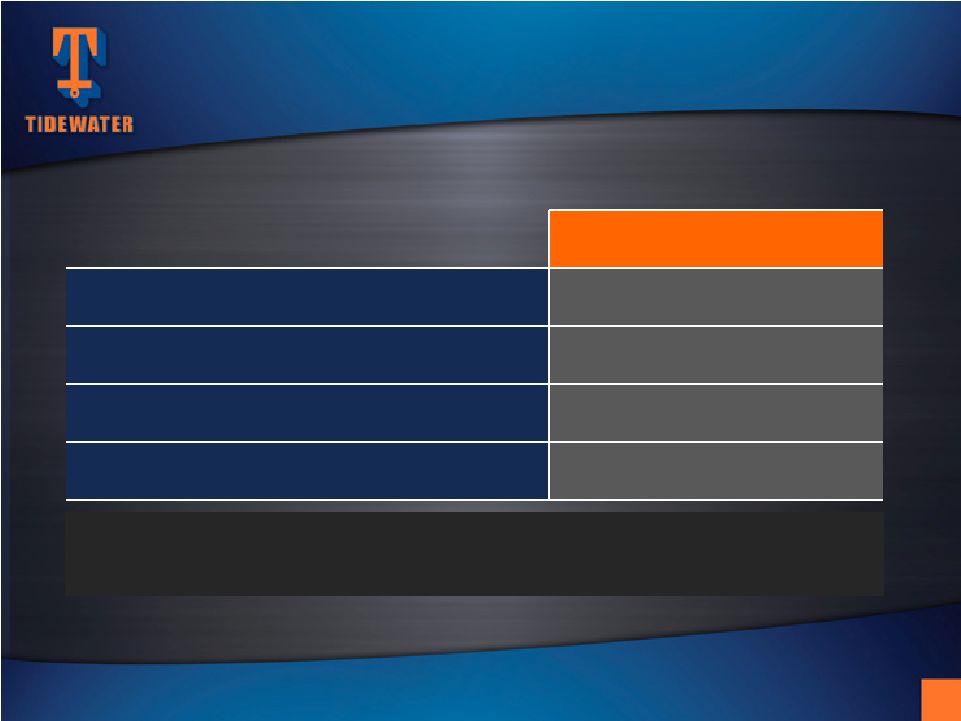

Nine Months Ended

12/31/10

12/31/09

Revenues

$801

$909

Adjusted Net Earnings*

$102

$216

Adjusted EPS*

$1.99

$4.21

Net Cash from Operations

$218

$299

Capital Expenditures

$509

$304

* Adjusted Net Earnings and Adjusted EPS for the nine months ended 12/31/10 exclude

an after-tax $4.35 million, or $0.09 per share, charge related to

settlement with DOJ for FCPA matters, and an after-tax $3.9 million, or $0.08 per

share, charge related to participation in a multi-company U.K.-based

pension plan. Adjusted net earnings and EPS for the nine months ended

12/31/09 exclude $48.1 million, or $0.94 per share, related to provision for Venezuelan operations and

$34.3 million, or $0.66 per share, tax benefit related to favorable resolution of

tax litigation.. SELECTED FINANCIAL

HIGHLIGHTS SELECTED FINANCIAL HIGHLIGHTS

$ in Millions,

Except Per Share Data

21 |

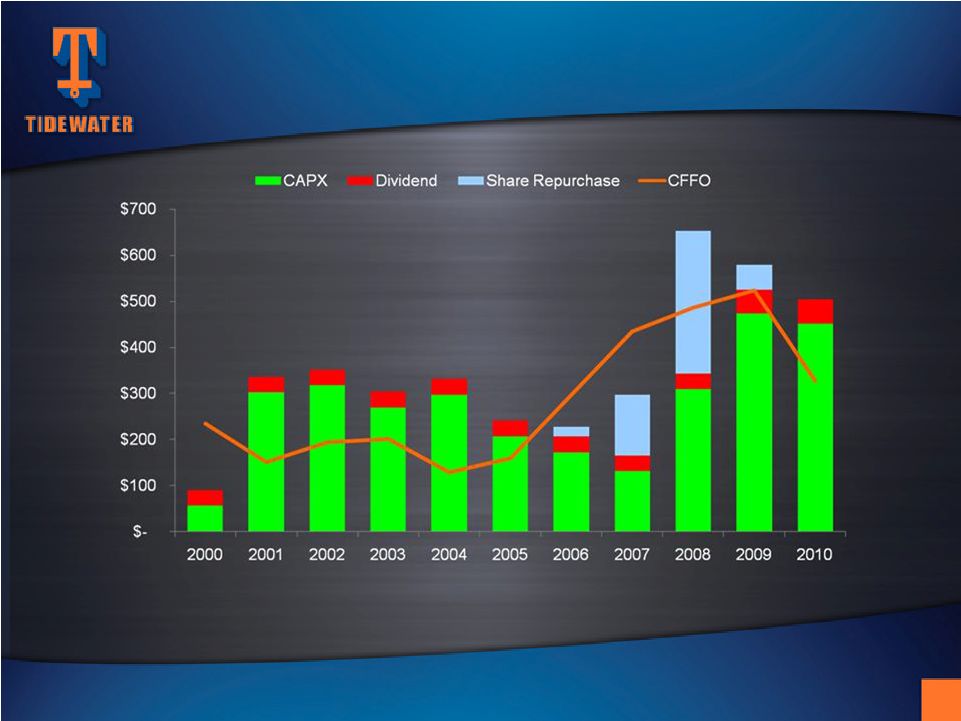

Over

an 11-year period, Tidewater invested $3.2 billion in CAPX ($2.8 billion in the “new”

fleet),

and paid out $923 million through dividends and share repurchases. Over the

same period, CFFO and proceeds from dispositions were $3.1 billion and $640

million, respectively PRIMARY USES OF CASH

PRIMARY USES OF CASH

22 |

Maintain

Financial Strength

EVA-Based Investments

On Through-cycle Basis

Deliver Results

FINANCIAL STRATEGY FOCUSED ON

FINANCIAL STRATEGY FOCUSED ON

CREATING LONG-TERM SHAREHOLDER VALUE

CREATING LONG-TERM SHAREHOLDER VALUE

23 |

CREDIT SUISSE

CREDIT SUISSE

2011 ENERGY SUMMIT

2011 ENERGY SUMMIT

February 8, 2011

February 8, 2011

Quinn P. Fanning

Quinn P. Fanning

Executive Vice President and

Executive Vice President and

Chief Financial Officer

Chief Financial Officer

Joseph M. Bennett

Joseph M. Bennett

Executive Vice President and

Executive Vice President and

Chief Investor Relations Officer

Chief Investor Relations Officer |

Appendix

Appendix

25 |

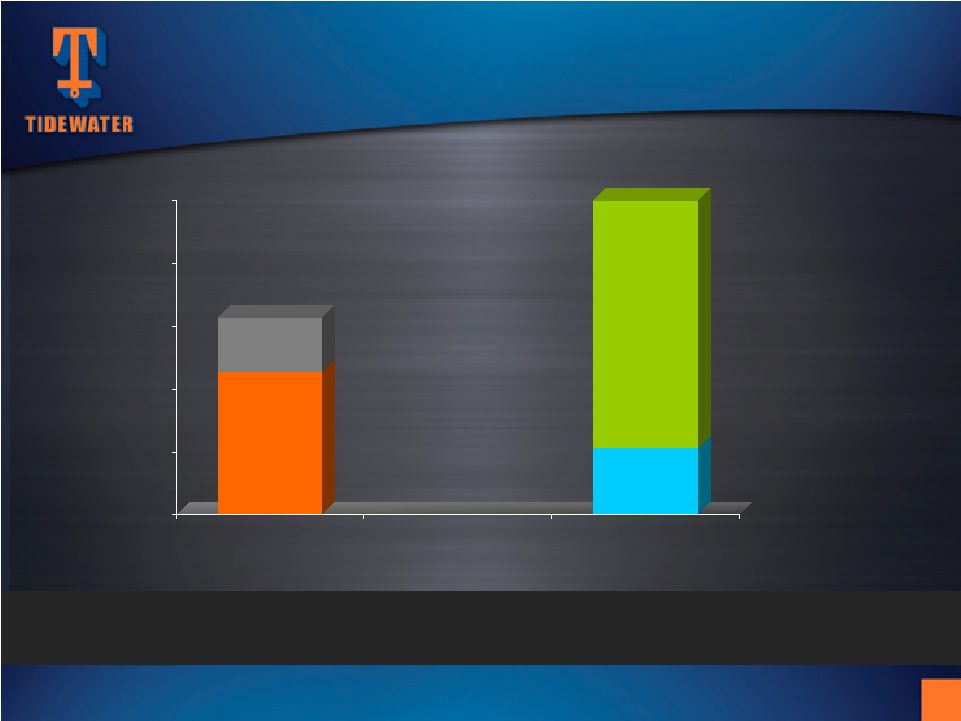

RECENT ACCOMPLISHMENTS

RECENT ACCOMPLISHMENTS

First full fiscal year without a lost time accident (FY 2010)

Respectable earnings & returns in a trough (tough) market

Selected acquisitions of choice assets

Disciplined disposal of traditional equipment

Delivery of 45 new vessels over last two full fiscal years

Balance sheet still solid

Strategy working –

Poised to seize opportunities

26 |

0

100

200

300

400

500

Active Fleet

Dispositions

CONTINUALLY ACQUIRING NEW AND

CONTINUALLY ACQUIRING NEW AND

DISPOSING OF MATURE VESSELS

DISPOSING OF MATURE VESSELS

(As of 12/31/10)

(As of 12/31/10)

314

(B)

539

(C)

228 New Vessels (A)

434 Sold

105 Scrapped

(A)

Net

new

vessels

added

to

the

fleet

since

January

2000,

including

37

vessels

under

construction

at

12/31/10.

This

new

vessel total excludes 20 new vessels that were acquired, then disposed (mostly to a

TDW joint venture.) (B) Total fleet count excludes 92 stacked vessels as of

12/31/10. (C) 539 vessel dispositions generated $682 million of proceeds and

$284 million of gains over the last 11 years. 27

|

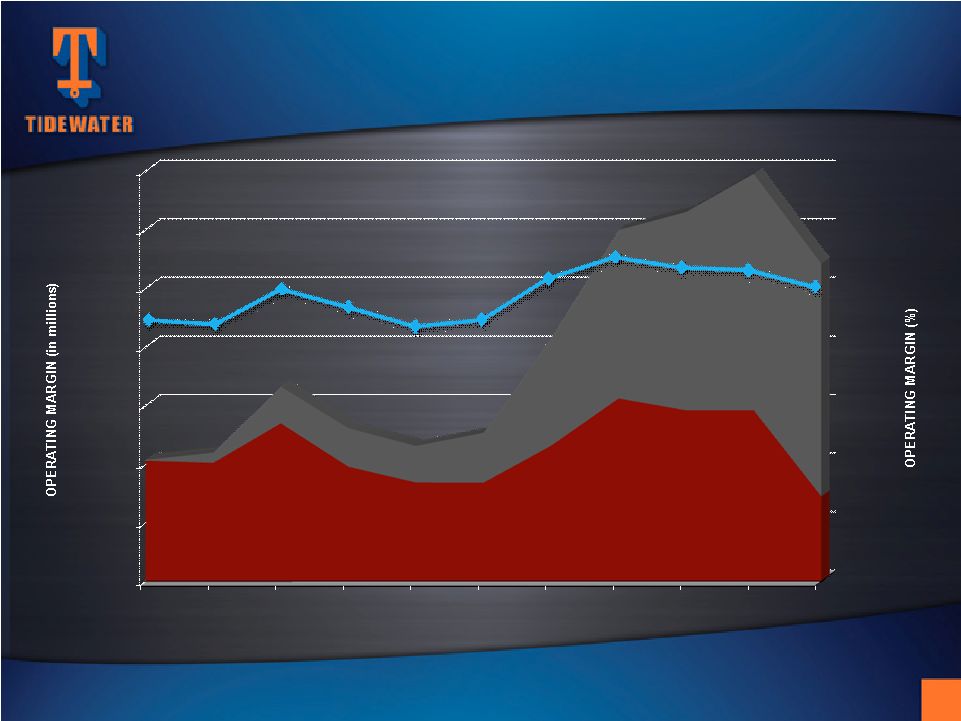

FLEET CASH OPERATING MARGINS

FLEET CASH OPERATING MARGINS

Note:

Cash

operating

margins

are

defined

as

vessel

revenue

less

vessel

operating

expenses

$0

$100

$200

$300

$400

$500

$600

$700

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Fiscal Years

50%

40%

30%

20%

10%

60%

Total Fleet

Operating Margin %

New Vessels

Traditional Vessels

38.6%

37.6%

46.5%

41.9%

36.9%

38.7%

49.1%

54.6%

51.9%

51.3%

46.8%

28 |

50%

60%

70%

80%

90%

12/07

6/08

12/08

6/09

12/09

6/10

12/10

Utilization

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

Dayrate

* Dayrate and utilization information is for all classes of vessels operating

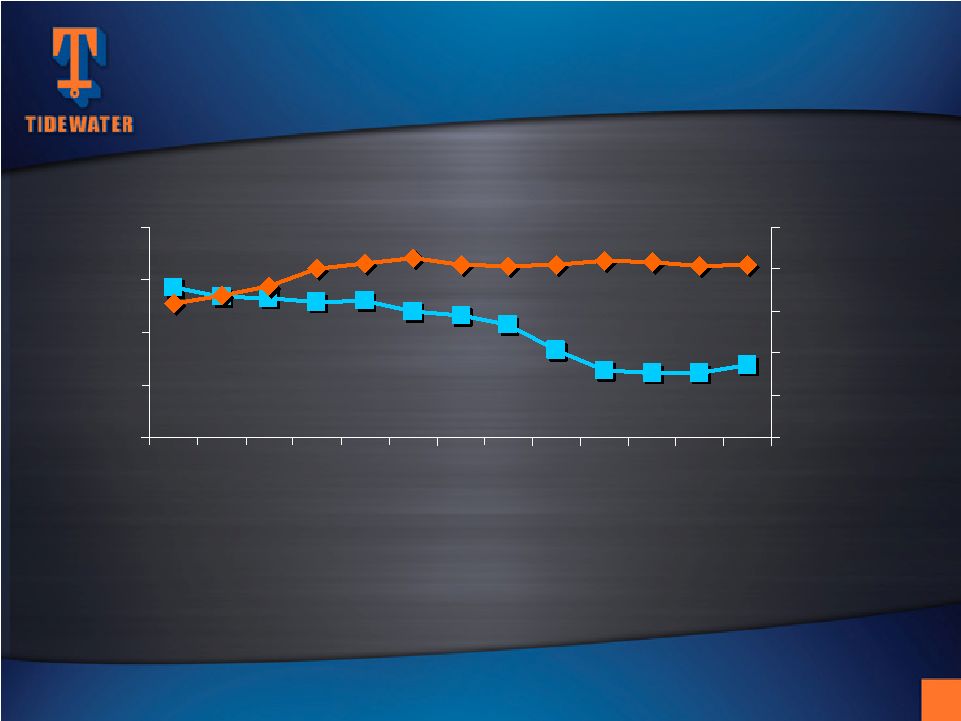

international INTERNATIONAL VESSELS

INTERNATIONAL VESSELS

Dayrates and Utilization

Dayrates and Utilization

$100 change in dayrate = ~$8.1M in annual revenue

1% change in utilization = ~$15.5M in annual revenue

29 |

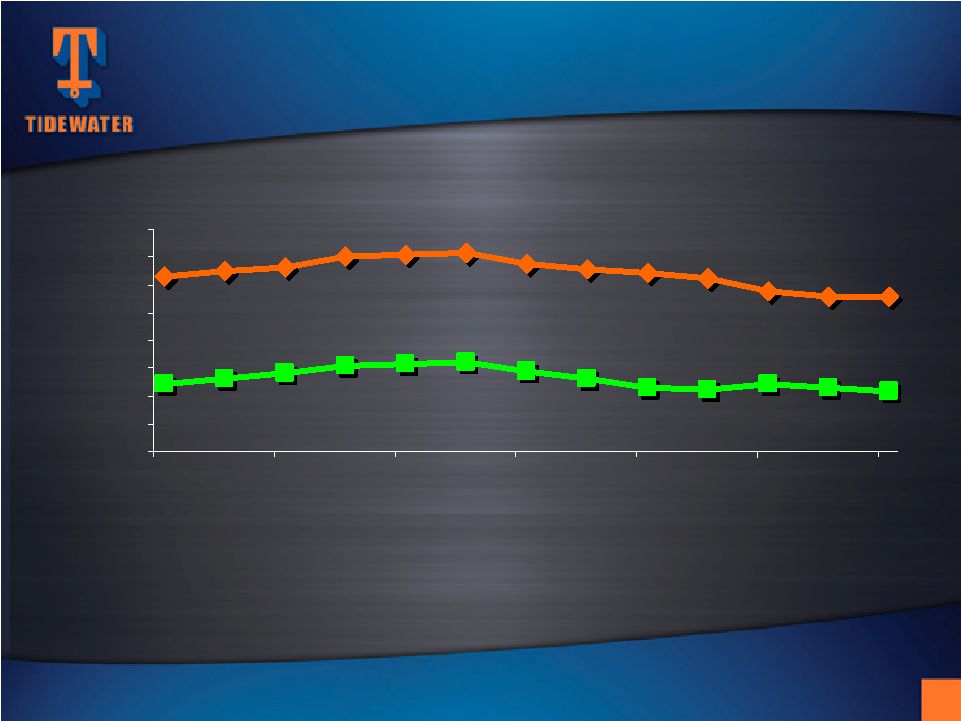

INTERNATIONAL VESSEL DAYRATES

INTERNATIONAL VESSEL DAYRATES

* Dayrate and utilization information is for all classes of vessels operating

international $3,000

$5,000

$7,000

$9,000

$11,000

$13,000

$15,000

$17,000

$19,000

12/07

06/08

12/08

06/09

12/09

06/10

12/10

Traditional Vessels

New Vessels

30 |

30%

40%

50%

60%

70%

80%

90%

12/07

6/08

12/08

6/09

12/09

6/10

12/10

Utilization

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

Dayrate

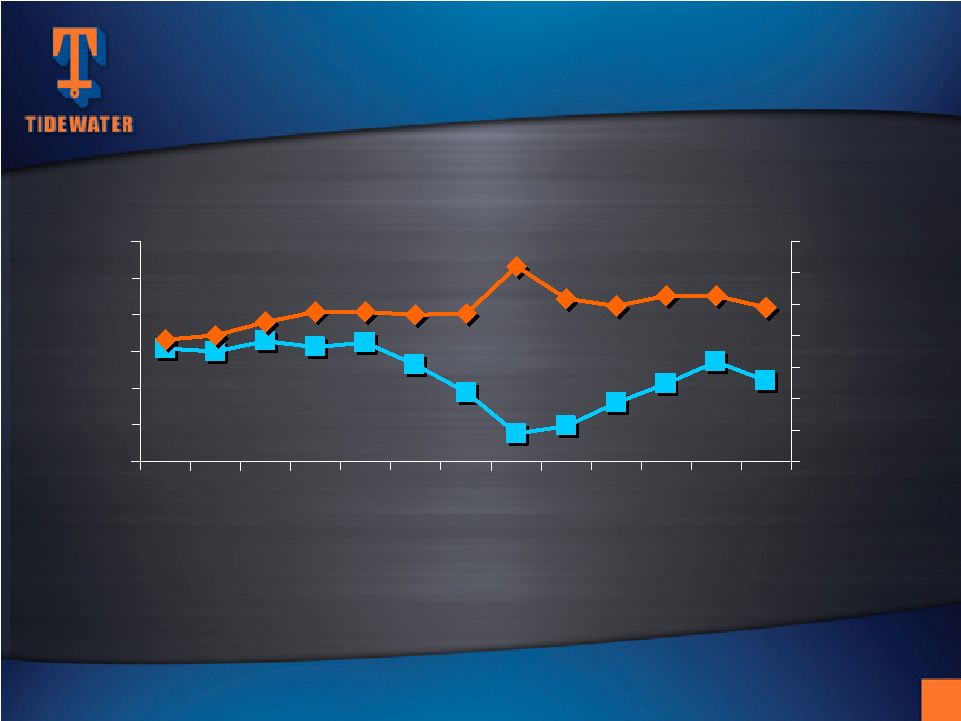

DOMESTIC VESSELS

DOMESTIC VESSELS

Dayrates and Utilization

Dayrates and Utilization

* Dayrate and utilization information is for all classes of vessels operating in the

U.S. 31 |

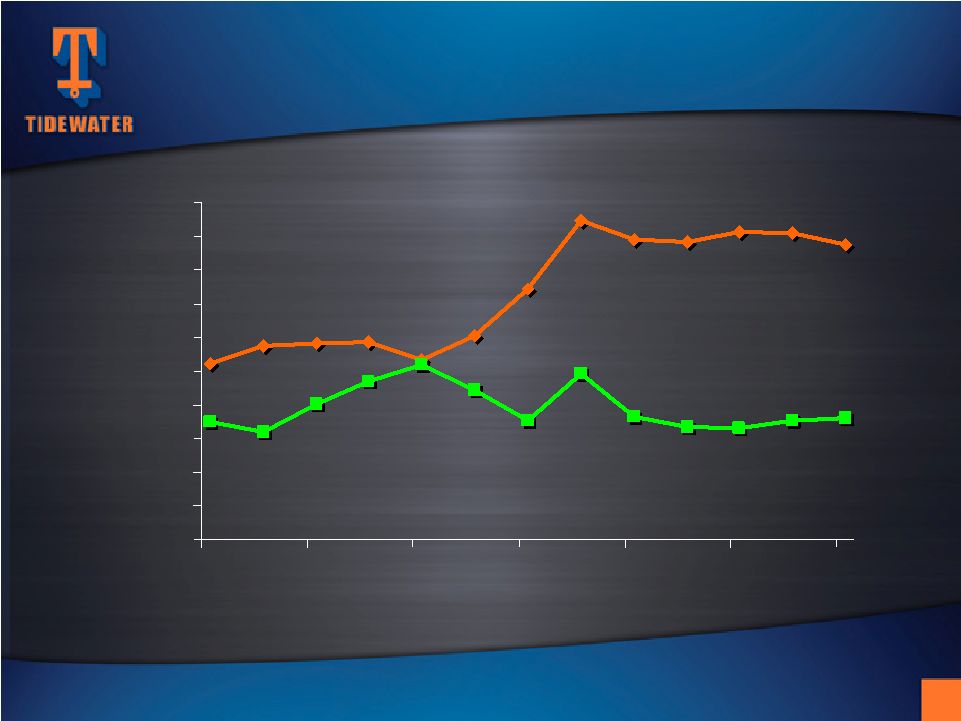

DOMESTIC VESSEL DAYRATES

DOMESTIC VESSEL DAYRATES

* Dayrate and utilization information is for all classes of vessels operating in the

U.S. $3,000

$5,000

$7,000

$9,000

$11,000

$13,000

$15,000

$17,000

$19,000

$21,000

$23,000

12/07

06/08

12/08

06/09

12/09

06/10

12/10

Traditional Vessels

New Vessels

32 |

Source:

ODS-Petrodata

and

Tidewater

WORKING RIG COUNTS

WORKING RIG COUNTS

“Peak to Present”

“Peak to Present”

GOM

accounts

for

32

of

the

74

working

jackup

count

variance

from

June

2008

(Peak)

to

January

2011

(post-Horizon)

GOM

Semi

&

Drillship

count

drops

by

21

units

(from

31

to

10)

between

April

2010

and

January

2011;

offset

by

an

increase

of

6

units

in

the

rest

of

world

Jackups

Semis

Drillships

Total

June 2008

(Peak)

379

145

30

554

Late-April 2010

(pre-Horizon)

323

150

46

519

Mid-Jan. 2011

(post-Horizon)

305

143

38

486

33 |

Other Operators

Top 10 Customers

Tidewater’s top 10 customers contract nearly 22% of the working

worldwide jackup

fleet and ~49% of the working worldwide floater fleet

Jackups

(305 Working Rigs)

Floater Rigs

(181 Working Rigs)

66

239

89

RIGS CONTRACTED BY OUR

RIGS CONTRACTED BY OUR

TOP

10 CUSTOMERS

10 CUSTOMERS

(Estimated as of Mid-January 2011)

34

Source:

ODS-Petrodata

and

Tidewater

Other Operators

Top 10 customers

92 |

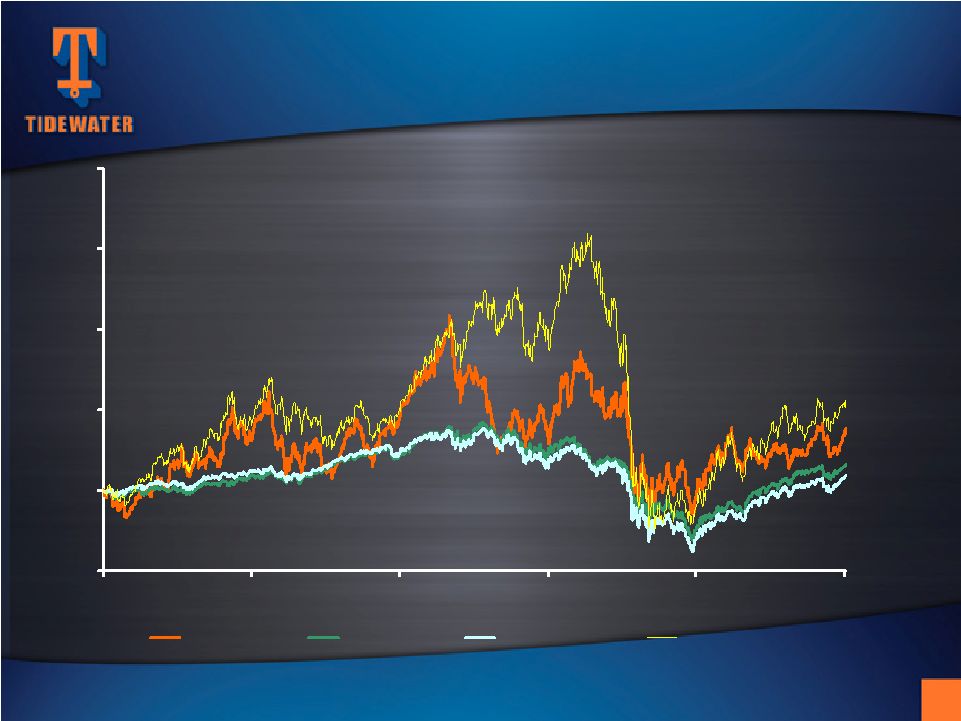

-50%

0%

50%

100%

150%

200%

Mar-05

Mar-06

Mar-07

Mar-08

Mar-09

Mar-10

TDW

DJIA

S&P500

OSX

OSX 52%

S&P 500 9%

DJIA 16%

TDW 36%

RETURNS vs the MARKET

RETURNS vs the MARKET

FIVE YEAR STOCKHOLDER RETURN

FIVE YEAR STOCKHOLDER RETURN

35 |