Attached files

| file | filename |

|---|---|

| EX-31 - REX AMERICAN RESOURCES Corp | c61126_ex31.htm |

| EX-32 - REX AMERICAN RESOURCES Corp | c61126_ex32.htm |

| EX-4.(K) - REX AMERICAN RESOURCES Corp | c61126_ex4-k.htm |

| EX-4.(L) - REX AMERICAN RESOURCES Corp | c61126_ex4-l.htm |

| EX-4.(J) - REX AMERICAN RESOURCES Corp | c61126_ex4-j.htm |

| EX-99.(A) - REX AMERICAN RESOURCES Corp | c61126_ex99-a.htm |

| EX-99.(B) - REX AMERICAN RESOURCES Corp | c61126_ex99-b.htm |

| EX-23.(D) - REX AMERICAN RESOURCES Corp | c61126_ex23-d.htm |

| EX-21.(A) - REX AMERICAN RESOURCES Corp | c61126_ex21-a.htm |

| EX-23.(C) - REX AMERICAN RESOURCES Corp | c61126_ex23-c.htm |

| EX-23.(A) - REX AMERICAN RESOURCES Corp | c61126_ex23-a.htm |

| EX-23.(B) - REX AMERICAN RESOURCES Corp | c61126_ex23-b.htm |

|

|

|

|

UNITED STATES |

|

|

SECURITIES AND EXCHANGE COMMISSION |

|

|

WASHINGTON, D.C. 20549 |

|

|

FORM 10-K |

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF |

|

|

THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

FOR THE FISCAL YEAR ENDED JANUARY 31, 2010 |

COMMISSION FILE NO. 001-09097 |

|

|

|

|

|

|

|

REX STORES CORPORATION |

|

|

(Exact name of registrant as specified in its charter) |

|

|

|

|

|

Delaware |

31-1095548 |

|

(State or other jurisdiction of |

(I.R.S. Employer Identification No.) |

|

incorporation or organization) |

|

|

|

|

|

2875 Needmore Road, Dayton, Ohio |

45414 |

|

(Address of principal executive offices) |

(Zip Code) |

|

|

|

|

|

Registrant’s telephone number, including area code (937) 276-3931 |

|

|

|

|

|

Securities registered pursuant to Section 12(b) of the Act: |

|

|

|

|

Title of each class |

Name of each exchange |

|

|

|

|

Common Stock, $.01 par value |

New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one):

|

|

|

Large accelerated filer o Accelerated filer x Non-accelerated filer o Smaller reporting company o |

|

(Do not check if a smaller reporting company) |

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes o No x |

At the close of business on July 31, 2009 the aggregate market value of the registrant’s outstanding Common Stock held by non-affiliates of the registrant (for purposes of this calculation, 2,048,795 shares beneficially owned by directors and executive officers of the registrant were treated as being held by affiliates of the registrant), was $80,172,960.

There were 9,842,083 shares of the registrant’s Common Stock outstanding as of April 15, 2010.

|

|

|

Documents Incorporated by Reference |

|

Portions of REX Stores Corporation’s definitive Proxy Statement for its Annual Meeting of Shareholders on June 9, 2010 are incorporated by reference into Part III of this Form 10-K. |

AVAILABLE INFORMATION

REX makes available free of charge on its Internet website its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. REX’s Internet website address is www.rextv.com. The contents of the Company’s website are not a part of this report.

PART I

|

|

|

|

Item 1. |

Business |

Overview

REX was incorporated in Delaware in 1984 as a holding company to succeed to the entire ownership of three affiliated corporations, Rex Radio and Television, Inc., Stereo Town, Inc. and Kelly & Cohen Appliances, Inc., which were formed in 1980, 1981 and 1983, respectively. Our principal offices are located at 2875 Needmore Road, Dayton, Ohio 45414. Our telephone number is (937) 276-3931. Historically, we were a specialty retailer in the consumer electronics and appliance industry serving small to medium-sized towns and communities. In addition, we have been an investor in various alternative energy entities beginning with synthetic fuel partnerships in 1998 and later ethanol production facilities beginning in 2006.

In fiscal year 2007, we began to evaluate strategic alternatives for our retail segment with a focus on closing unprofitable or marginally profitable retail stores and monetizing our retail-related real estate assets. We did not believe that we were generating an adequate return from our retail business due to the competitive nature of the consumer electronics and appliance industry and the overall economic conditions in the United States. Reflecting this focus, we sold approximately 60% of our owned retail and vacant stores in fiscal year 2007 and leased back a portion of the stores which had been operating as electronics and appliance retail stores. In fiscal year 2008, we commenced an evaluation of a broad range of alternatives intended to derive value from the remaining retail operations and our remaining real estate portfolio. We engaged an investment banking firm to assist us in analyzing and ultimately marketing our retail operations. As part of those marketing efforts, late in fiscal year 2008, we initially leased 37 owned store locations to an unrelated third party. During fiscal year 2009, the lease agreements were terminated. We are marketing these vacant properties to lease or sell. Should our marketing efforts result in additional tenants to whom we lease property, we would expect to execute leases with terms of five to twenty years.

We completed our exit of the retail business as of July 31, 2009. Going forward, we expect that our only retail related activities will consist of the administration of extended service plans we previously sold and the payment of related claims. Net sales and expenses related to extended service plans are classified as discontinued operations.

We currently have approximately $111 million of equity and debt investments in four ethanol production entities, two of which we have a majority ownership interest in. We are considering making additional investments in the alternative energy segment during fiscal year 2010.

Our ethanol operations are highly dependent on commodity prices, especially prices for corn, sorghum, ethanol, distillers grains and natural gas. As a result of price volatility for these commodities, our operating results can fluctuate substantially. The price and availability of corn and sorghum are subject to significant fluctuations depending upon a number of factors that affect commodity prices in general,

2

including crop conditions, weather, federal policy and foreign trade. Because the market price of ethanol is not always directly related to corn and sorghum prices, at times ethanol prices may lag movements in corn prices and, in an environment of higher prices, reduce the overall margin structure at the plants. As a result, at times, we may operate our plants at negative or marginally positive operating margins.

We expect our ethanol plants to produce approximately 2.8 gallons of ethanol for each bushel of grain processed in the production cycle. We refer to the difference between the price per gallon of ethanol and the price per bushel of grain (divided by 2.8) as the “crush spread.” Should the crush spread decline, it is possible that our ethanol plants will generate operating results that do not provide adequate cash flows for sustained periods of time. In such cases, production at the ethanol plants may be reduced or stopped altogether in order to minimize variable costs at individual plants. We expect these decisions to be made on an individual plant basis, as there are different market conditions at each of our ethanol plants.

We attempt to manage the risk related to the volatility of grain and ethanol prices by utilizing forward grain purchase and forward ethanol and distillers grain sale contracts. We attempt to match quantities of ethanol and distillers grains sale contracts with an appropriate quantity of grain purchase contracts over a given period of time when we can obtain an adequate gross margin resulting from the crush spread inherent in the contracts we have executed. However, the market for future ethanol sales contracts is not a mature market. Consequently, we generally execute contracts for no more than three months into the future at any given time. As a result of the relatively short period of time our contracts cover, we generally cannot predict the future movements in the crush spread for more than three months; thus, we are unable to predict the likelihood or amounts of future income or loss from the operations of our ethanol facilities.

The crush spread realized in 2009 was subject to significant volatility. For example, for calendar year 2009, the average Chicago Board of Trade (“CBOT”) near-month corn price was approximately $3.74 per bushel, with highs reaching nearly $4.20 per bushel and retreating to approximately $3.20 per bushel in the fall. Ethanol prices were generally in a range of approximately $1.50 to $1.70 per gallon for most of the year. Ethanol prices increased during the last three months of 2009 reaching as high as $2.00 per gallon. We believe this market volatility with respect to the crush spread was attributable to a number of factors, including but not limited to export demand, speculation, currency valuation, global economic conditions, ethanol demand and current production concerns. In 2009, the CBOT crush spread ranged from approximately $0.19 to $0.63 per gallon of ethanol.

We reported segment profit (before income taxes and noncontrolling interests) from our alternative energy segment of approximately $17.8 million in fiscal year 2009 compared to a loss of approximately $9.0 million in fiscal year 2008. The swing to profitability resulted from favorable crush spreads, particularly in the later parts of fiscal year 2009, and One Earth commencing production operations in the second quarter of fiscal year 2009. We expect that future operating results will be based upon annual production of between 130 and 140 million gallons, which assumes that Levelland Hockley and One Earth will operate at or near nameplate capacity. However, due to the inherent volatility of the crush spread, we cannot predict the likelihood of future operating results being similar to the 2009 results.

We plan to seek and evaluate various investment opportunities including energy related, agricultural or other ventures we believe fit our investment criteria. We can make no assurances that we will be successful in our efforts to find such opportunities.

Additional information regarding our business segments is presented below and in Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) in this Form 10-K. See Note 20 of the Notes to the Consolidated Financial Statements for information regarding the net sales

3

and revenues and operating results for each of our business segments for the fiscal years ended January 31, 2010, 2009 and 2008.

Fiscal Year

All references in this report to a particular fiscal year are to REX’s fiscal year ended January 31. For example, “fiscal year 2009” means the period February 1, 2009 to January 31, 2010. We refer to our fiscal year by reference to the year immediately preceding the January 31 fiscal year end date.

Alternative Energy Overview

As part of our ongoing efforts to diversify and increase our earnings, we began investing in the ethanol industry during fiscal year 2006. Our business strategy focuses on partnering with farmer groups, local groups, or farmer-controlled cooperatives to develop and operate ethanol production plants. We seek to identify quality ethanol plant opportunities characterized by strong plant construction partners and plant management, located near adequate feedstock supply with good transportation capabilities or other economically beneficial attributes, and that utilize leading ethanol production technology. Our partnership model generally enables farmer groups to retain local management of the project, including control of their crops as a supplier to the project, while we provide capital and additional business administration experience.

We follow a flexible model for our investments in ethanol plants, taking both minority and majority ownership positions. The form and structure of our investments is tailored to the specific needs and goals of each project and the local farmer group or investor with whom we are partnering. We actively participate in the management of our projects through our membership on the board of managers of the limited liability companies that own the plants.

Alternative Energy Strategy

The key elements of our alternative energy business strategy include:

Investing in Plants that Meet our Investment Criteria. We have stringent and structured criteria to evaluate our plant investments. We focus on identifying projects with efficient cost structure, superior infrastructure and logistics and quality partners. We evaluate the projects using the following criteria:

Partners. We judge our partners on the strength of their connection with the local community, ability to support the plant through construction and when in operation, as well as their willingness and desire for an outside partner.

Plant Location. We generally look for locations in areas that are near large quantities of feedstock or feedlots which we believe will be important to procure commodities cost effectively as demand for key feedstock commodities increases. We also look for accessibility to rail, highways or waterways for ease of transportation of ethanol and distillers grains and feedstock. Access to feedlots and utilities such as water and natural gas are also important considerations for our plant locations.

Technology and Construction. We look for plants that are built or will be built using the latest but proven production technology in order to facilitate cost efficient conversion of raw material into ethanol. Our plants were designed and built by leading plant builder and design firms, such as Fagen, Inc. or ICM, Inc.

Marketing Alliance. Each project independently chooses its own marketing alliance. We prefer marketing partners that have strong positions in the industry based on their experience and national reach,

4

which we believe will become increasingly important as ethanol becomes a more available alternative to petroleum based fuels. We also sell our ethanol and related products in the local markets when it is advantageous to do so.

Adding Value to Our Partnerships. We look for ways to add to the operational characteristics of our projects by being a source of development support and information on practices in the ethanol industry. We believe the diversification of our investments in terms of geography, ownership, management, plant size and financial and operational agreements allow us to provide our partners with value added information with respect to risk management, feedstock procurement, plant management and ethanol and co-products marketing.

Ethanol Investments

We have invested in four entities as of January 31, 2010, utilizing both equity and debt investments. As of January 31, 2010, all of the entities we are invested in are operating. The following table is a summary of our ethanol investments at January 31, 2010 (amounts in thousands, except operating capacity and ownership percentages):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Entity |

|

Initial |

|

Operating |

|

Effective |

|

Debt |

|

Contingent |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Levelland Hockley County Ethanol, LLC |

|

$ |

16,500 |

|

|

40 |

|

|

56 |

% |

$ |

6,255 |

|

$ |

1,532 |

|

|

Big River Resources, LLC-W Burlington |

|

|

|

|

|

92 |

|

|

10 |

% |

|

— |

|

|

— |

|

|

Big River Resources, LLC-Galva |

|

|

20,025 |

|

|

100 |

|

|

10 |

% |

|

— |

|

|

— |

|

|

Big River United Energy, LLC |

|

|

|

|

|

100 |

|

|

5 |

% |

|

— |

|

|

— |

|

|

Patriot Renewable Fuels, LLC |

|

|

16,000 |

|

|

100 |

|

|

23 |

% |

|

1,014 |

|

|

— |

|

|

One Earth Energy, LLC |

|

|

50,765 |

|

|

100 |

|

|

74 |

% |

|

— |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

$ |

103,290 |

|

|

|

|

|

|

|

$ |

7,269 |

|

$ |

1,532 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Levelland Hockley County Ethanol, LLC

On September 30, 2006, we acquired 47% of the outstanding membership units of Levelland Hockley County Ethanol, LLC, or Levelland Hockley, for $11.5 million. On December 29, 2006, we purchased a $5.0 million convertible secured promissory note from Levelland Hockley. On July 1, 2007, we converted the note into equity and increased our ownership percentage to approximately 56%. On February 20, 2008, we purchased an additional $5.0 million convertible secured promissory note from Levelland Hockley. The balance of this note at January 31, 2010 was $4.8 million, including accrued interest. The conversion of the note into equity would increase our ownership percentage to approximately 62%. On January 29, 2009, we agreed to fund up to $2.0 million in the form of a subordinated revolving line of credit with Levelland Hockley and to issue a $1.0 million letter of credit for the benefit of Levelland Hockley. In connection with the subordinated revolving line of credit and the letter of credit, we were granted warrants to purchase membership units of Levelland Hockley for $3.08 per unit. Our ownership percentage would increase to approximately 62% if we exercise only our rights under the warrants but do not convert the promissory note. At January 31, 2010, there was $1.5 million outstanding under the subordinated revolving line of credit. We consolidate Levelland Hockley with our financial results and include them in our alternative energy segment.

5

Levelland Hockley, which is located in Levelland, Texas, commenced production operations in the first quarter of fiscal year 2008. The plant has a nameplate capacity of 40 million gallons of ethanol and 135,000 tons of dried distillers grains (“DDG”) per year.

Big River Resources, LLC

We have invested $20 million in Big River Resources, LLC, or Big River, for a 10% ownership interest. Big River is a holding company for several entities including Big River Resources West Burlington, LLC which operates a 92 million gallon dry-mill ethanol manufacturing facility in West Burlington, Iowa. The facility has been in operation since 2004.

Big River completed construction in the second quarter of fiscal year 2009 of its second plant which has a nameplate capacity of 100 million gallons of ethanol and 320,000 tons of DDG per year. This plant is located in Galva, Illinois.

In August 2009, Big River acquired a 50.5% interest in an ethanol production facility which has a nameplate capacity of 100 million gallons of ethanol and 320,000 tons of DDG per year. The plant is located in Dyersville, Iowa. Reflecting REX’s 10% ownership interest in Big River, REX has an effective 5% ownership interest in this entity.

Patriot Renewable Fuels, LLC

On December 4, 2006, we acquired a 23% ownership interest in Patriot Renewable Fuels, LLC, or Patriot, for $16 million. Patriot commenced production operations in the second quarter of fiscal year 2008. The plant is located in Annawan, Illinois and has a nameplate capacity of 100 million gallons of ethanol and 320,000 tons of DDG per year.

One Earth Energy, LLC

On October 30, 2007, we acquired 74% of the outstanding membership units of One Earth Energy, LLC, or One Earth, for $50.8 million. We consolidate One Earth with our financial results and include them in our alternative energy segment. One Earth completed construction in the second quarter of fiscal year 2009 of its ethanol production facility in Gibson City, Illinois. The plant has a nameplate capacity of 100 million gallons of ethanol and 320,000 tons of DDG per year.

One Earth commenced production operations late in the second quarter of fiscal year 2009 and began generating revenue in the third quarter of fiscal year 2009.

Ethanol Industry

Ethanol is a renewable fuel source produced by processing corn and other biomass through a fermentation process that creates combustible alcohol that can be used as an additive or replacement to fossil fuel based gasoline. The majority of ethanol produced in the United States is made from corn because of its wide availability and ease of convertibility from large amounts of carbohydrates into glucose, the key ingredient in producing alcohol that is used in the fermentation process. Ethanol production can also use feedstocks such as grain sorghum, switchgrass, wheat, barley, potatoes and sugarcane as carbohydrate sources. Most ethanol plants have been located near large corn production areas, such as Illinois, Indiana, Iowa, Minnesota, Nebraska, Ohio and South Dakota. Railway access and interstate access are vital for ethanol facilities due to the large amount of demand in the east- and west-coast markets, primarily as a result of the stricter air quality requirements in large parts of those markets, and the limited ethanol production facilities.

6

According to the Renewable Fuels Association, or RFA, the United States fuel ethanol industry experienced record production of 10.6 billion gallons in 2009. As of January 2010, the number of operating ethanol plants increased to 189, up from 54 in 2000 and are located in 25 states with a total capacity of 11.9 billion gallons annually.

On December 19, 2007, the Energy Independence and Security Act of 2007 (the “Energy Act of 2007”) was enacted. The Energy Act of 2007 established new levels of renewable fuel mandates, including two different categories of renewable fuels: conventional biofuels and advanced biofuels. Corn-based ethanol is considered conventional biofuels which was subject to a renewable fuel standard (“RFS”) of at least 12.0 billion gallons per year in 2010, with an expected increase to at least 15.0 billion gallons per year by 2015. Advanced biofuels includes ethanol derived from cellulose, hemicellulose or other non-corn starch sources; biodiesel; and other fuels derived from non-corn starch sources. Advanced biofuels RFS levels are set to reach at least 21.0 billion gallons per year, resulting in a total RFS from conventional and advanced biofuels of at least 36.0 billion gallons per year by 2022.

Ethanol Production

The plants we have invested in are designed to use the dry milling method of producing ethanol. In the dry milling process, the entire corn kernel is first ground into flour, which is referred to as “meal,” and processed without separating out the various component parts of the grain. The meal is processed with enzymes, ammonia and water, and then placed in a high-temperature cooker. It is then transferred to fermenters where yeast is added and the conversion of sugar to ethanol begins. After fermentation, the resulting liquid is transferred to distillation columns where the ethanol is separated from the remaining “stillage” for fuel uses. The anhydrous ethanol is then blended with denaturant, such as natural gasoline, to render it undrinkable and thus not subject to beverage alcohol tax. With the starch elements of the corn consumed in the above described process, the principal co-product produced by the dry milling process is dry distillers grains with solubles, or DDGS. DDGS is sold as a protein used in animal feed and recovers a significant portion of the total corn cost.

The Primary Uses of Ethanol

Blend component. Today, much of the ethanol blending in the U.S. is done for the purpose of extending the volume of fuel sold at the gas pump. Blending ethanol allows refiners to produce more fuel from a given barrel of oil. Currently, ethanol is blended into nearly 80% of the gasoline sold in the United States, the majority as E10 (a blend of 10% ethanol and 90% gasoline), according to the RFA. Going forward, the industry is attempting to expand the E-85 market, as well as to raise the federal cap on ethanol blend above the current 10% for most vehicles in use. The U.S. Environmental Protection Agency is expected to reach a decision on allowing ethanol blends of up to 15% for most vehicles by mid to late 2010.

Clean air additive. Ethanol is employed by the refining industry as a fuel oxygenate, which when blended with gasoline, allows engines to combust fuel more completely and reduce emissions from motor vehicles. Ethanol contains 35% oxygen, approximately twice that of Methyl Tertiary Butyl Ether, or MTBE, an alternative oxygenate to ethanol, the use of which is being phased out because of environmental and health concerns. The additional oxygen in ethanol results in more complete combustion of the fuel in the engine cylinder. Ethanol is non-toxic, water soluble and quickly biodegradable.

7

Octane enhancer. Ethanol increases the octane rating of gasoline with which it is blended. As such, ethanol is used by gasoline suppliers as an octane enhancer both for producing regular grade gasoline from lower octane blending stocks and for upgrading regular gasoline to premium grades.

Legislation

The United States ethanol industry is highly dependent upon federal and state legislation. See Item 1A. Risk Factors for a discussion of legislation affecting the U.S. ethanol industry.

Synthetic Fuel Partnerships

We had invested in three limited partnerships which owned facilities producing synthetic fuel. The partnerships earned federal income tax credits under Section 29/45K of the Internal Revenue Code based upon the tonnage and content of solid synthetic fuel produced and sold to unrelated parties. The Section 29/45K tax credit program expired on December 31, 2007. As such, we do not expect to receive additional income from these investments except for the possibility of an additional payment on a facility formerly located in Gillette, Wyoming. Based upon the modified terms of a sales agreement we are currently not able to predict the likelihood and timing of payments for production from September 30, 2006 to December 31, 2007 for this facility. We expect the payments, if any, to be made within the next two years. We have not recognized this income and will recognize income, if any, upon receipt of payment or upon our ability to reasonably assure ourselves of the timing and collectability of payment.

See Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations and Notes 5 and 19 of the Notes to the Consolidated Financial Statements for further discussions.

Real Estate Operations

At January 31, 2010, we had lease or sub-lease agreements, as landlord, for all or parts of ten former retail stores (108,000 square feet leased and 35,000 square feet vacant). We own nine of these properties and are the tenant/sub landlord for one of the properties. We have 31 owned former retail stores (385,000 square feet), and one former distribution center (180,000 square feet), that are vacant at January 31, 2010. We are marketing these vacant properties to lease or sell. In addition, one former distribution center is partially leased (156,000 square feet), partially occupied by our corporate office personnel (10,000 square feet) and partially vacant (300,000 square feet).

A typical lease agreement has an initial term of five to twenty years with renewal options. Most of our lessees are responsible for a portion of maintenance, taxes and other executory costs. We require our lessees to maintain adequate levels of insurance. We recognized lease revenue of approximately $1,089,000 and $415,000 during fiscal years 2009 and 2008, respectively.

Retail

We began fiscal year 2009 with 90 retail stores in operation, all of which were closed in the first half of the year as planned.

When we operated retail stores, we offered extended service contracts to our customers which typically provided, inclusive of manufacturers’ warranties, one to five years of warranty coverage. We plan to manage and administer these contracts and to recognize the associated income and expenses, including the cost to repair or replace covered products, over the remaining life of the contracts. We have classified

8

as discontinued operations all retail related activities, including those activities associated with extended service plans, in the Consolidated Statements of Operations for all periods presented.

Facilities

At January 31, 2010, we owned nine former retail store properties that were leased to outside, unrelated parties. Of the nine leased properties, three of the properties are only partially leased. There were also 31 vacant properties that we were attempting to either lease or sell. In addition, we have one former distribution center partially leased and partially vacant and another former distribution center that is vacant.

Employees

At January 31, 2010, we had 11 hourly and salaried employees supporting our corporate functions. None of our employees are represented by a labor union. We expect this employment to remain relatively stable at its current level as we have completed our exit from the retail business.

At January 31, 2010, Levelland Hockley had 54 employees and One Earth had 49 employees.

We consider our relationship with our employees to be good.

Service Marks

We have registered our service mark “REX”, and we own an application to register the mark “Farmers Energy”, with the United States Patent and Trademark Office. We are not aware of any adverse claims concerning our service marks.

|

|

|

|

Item 1A. |

Risk Factors |

We encourage you to carefully consider the risks described below and other information contained in this report when considering an investment decision in REX common stock. Any of the events discussed in the risk factors below may occur. If one or more of these events do occur, our results of operations, financial condition or cash flows could be materially adversely affected. In this instance, the trading price of REX stock could decline, and investors might lose all or part of their investment.

We have concentrations of cash deposits at financial institutions that exceed federal insurance limits.

We generally have cash deposits that exceed federal insurance limits. Should the financial institutions we deposit our cash at experience insolvency or other financial difficulty, our access to cash deposits could be limited. In extreme cases, we could lose our cash deposits entirely. This would negatively impact our liquidity and results of operations.

The current interest rate environment has resulted in lower yields on our excess cash.

We have experienced lower yields on our excess cash compared to historical yields. Should the present economic conditions result in a sustained period of historically low interest rates, our interest income would be negatively impacted.

Risks Related to our Synthetic Fuel Investments

We face synthetic fuel risks as future IRS audits may result in the disallowance of previously recognized tax credits.

9

We have recognized investment income of approximately $59.3 million from the sales of our partnership interests from years that the partnerships have not been audited by the Internal Revenue Service (IRS). Should the tax credits be denied on any future audit and we fail to prevail through the IRS or the legal process, there could be significant refunds of previously recognized income with a significant adverse impact on earnings and cash flows.

The production and sale of synthetic fuel qualified for Section 29/45K tax credits if certain requirements were satisfied, including a requirement that the synthetic fuel differs significantly in chemical composition from the coal used to produce the synthetic fuel and that the fuel was produced from a facility placed in service before July 1, 1998.

We may not be able to generate sufficient taxable income to realize our deferred tax assets.

We have approximately $14.8 million of deferred tax assets recorded on our consolidated financial statements. Should future results of operations or other factors cause us to determine that it is unlikely that we will generate sufficient taxable income to fully utilize our deferred tax assets; we would then be required to establish a valuation allowance against such deferred tax assets. We would increase our income tax expense by the amount of the tax benefit we do not expect to realize. This would reduce our net income and could have a material adverse effect on our results of operations and our financial position.

Risks Related to our Alternative Energy Business

Certain of our ethanol investments are subject to the risks of a development stage business which could adversely affect returns on our ethanol investment and our results of operations.

We do not have long term experience investing in the ethanol industry. We entered into our first agreement to invest in an ethanol plant in November 2005. At January 31, 2010, we remain invested in four entities that own and operate six ethanol production facilities. One facility has been in production since 2004, two facilities have been in production since 2008, two facilities became operational and one facility was acquired (by an equity method investee) in fiscal year 2009. Our ethanol investments have been managed by our Chief Executive Officer, our Vice President and our Chief Financial Officer. We do not otherwise have a dedicated ethanol development or management staff. As a consequence, our ethanol investments are subject to many of the risks associated with a development stage company, including an unproven business model, a lack of operating history and an undeveloped operating structure. These development stage risks could result in our making investments in ethanol plants that perform substantially below our expectations, which would adversely affect our results of operations and financial condition.

One Earth and Big River recently completed construction of new ethanol plants.

As these new plants recently became operational, they face uncertainties of whether they will perform to specifications and whether they will achieve anticipated operating results.

If cash flow from operations of our ethanol plants is not sufficient to service debt, the plants could fail and we could lose our entire investment.

Our ethanol plants financed approximately 60% of plant construction cost with debt. The debt typically has a balloon payment due after five years. The ability of each company owning the plant to repay borrowings incurred will depend upon the plant’s financial and operating performance. The cash flows and capital resources of an ethanol plant may be insufficient to repay its debt obligations. If a plant cannot service its debt, it may be forced to reduce or delay capital expenditures, sell assets, restructure its

10

indebtedness or seek additional capital. If unable to do so, the value of our investment could decline significantly.

The institutional senior lenders to the companies which own and operate our ethanol plants hold liens on the plant’s assets. If a company fails to make its debt service payments, the senior lender will have the right to repossess the plant’s assets in addition to other remedies, which are superior to our rights as an equity investor or subordinated lender. Such action could have a materially adverse impact on our investment in the ethanol plant.

The financial returns on our ethanol investments are highly dependent on commodity prices, which are subject to significant volatility and uncertainty, and the availability of supplies, so our results could fluctuate substantially.

The financial returns on our ethanol investments are substantially dependent on commodity prices, especially prices for corn or other feedstock, natural gas, ethanol and unleaded gasoline. As a result of the volatility of the prices for these items, the returns may fluctuate substantially and our investments could experience periods of declining prices for their products and increasing costs for their raw materials, which could result in operating losses at our ethanol plants.

Our returns on ethanol investments are highly sensitive to grain prices. Corn or sorghum are the principal raw materials our ethanol plants use to produce ethanol and co-products. As a result, changes in the price of corn or sorghum can significantly affect their businesses. Rising corn or sorghum prices result in higher costs of ethanol and co-products. Because ethanol competes with non-corn-based fuels, our ethanol plants generally will be unable to pass along increased grain costs to their customers. At certain levels, grain prices may make ethanol uneconomical to produce.

The price of corn and sorghum is influenced by weather conditions and other factors affecting crop yields, transportation costs, farmer planting decisions, exports, the value of the U.S. dollar and general economic, market and regulatory factors. These factors include government policies and subsidies with respect to agriculture and international trade, and global and local demand and supply. The significance and relative effect of these factors on the price of corn and sorghum is difficult to predict. Any event that tends to negatively affect the supply of corn or sorghum, such as adverse weather or crop disease, could increase corn and sorghum prices and potentially harm the business of our ethanol plants. Increasing domestic ethanol capacity could boost the demand for corn and sorghum and result in increased corn or sorghum prices. Our ethanol plants may also have difficulty, from time to time, in physically sourcing corn or sorghum on economical terms due to supply shortages. Such a shortage could require our ethanol plants to suspend operations which would have a material adverse effect on the financial returns on our ethanol investments.

The spread between ethanol and corn and sorghum prices can vary significantly. The gross margin at our ethanol plants depends principally on the spread between ethanol and corn or sorghum prices. Fluctuations in the spread are likely to continue to occur. A sustained narrow spread or any further reduction in the spread between ethanol and corn prices, whether as a result of sustained high or increased corn prices or sustained low or decreased ethanol prices, would adversely affect the results of operations at our ethanol plants.

The market for natural gas is subject to market conditions that create uncertainty in the price and availability of the natural gas that our ethanol plants use in their manufacturing process. Our ethanol plants rely upon third parties for their supply of natural gas, which is consumed as fuel in the manufacture of ethanol. The prices for and availability of natural gas are subject to volatile market conditions. These

11

market conditions often are affected by factors beyond the ethanol plants’ control, such as weather conditions, overall economic conditions and foreign and domestic governmental regulation and relations. Significant disruptions in the supply of natural gas could impair the ethanol plants’ ability to economically manufacture ethanol for their customers. Furthermore, increases in natural gas prices or changes in our natural gas costs relative to natural gas costs paid by competitors may adversely affect results of operations and financial position at our ethanol plants.

Fluctuations in the selling price and production costs of gasoline may reduce profit margins at our ethanol plants. Ethanol is marketed as a fuel additive to reduce vehicle emissions from gasoline, as an octane enhancer to improve the octane rating of gasoline with which it is blended and, to a lesser extent, as a gasoline substitute. As a result, ethanol prices are influenced by the supply and demand for gasoline and our ethanol plants’ results of operations and financial position may be materially adversely affected if gasoline demand or price decreases.

New plants under construction or decreases in demand for ethanol may result in excess production capacity in the ethanol industry, which may cause the price of ethanol and/or distillers grains to decrease.

According to the Renewable Fuels Association, or RFA, domestic ethanol production nameplate capacity has increased to approximately 13.0 billion gallons per year at January 2010. The RFA estimates that, as of January 2010, approximately 1.4 billion gallons per year of additional production capacity is under construction. Excess capacity in the ethanol industry would have an adverse effect on the results of our ethanol investments. In a manufacturing industry with excess capacity, producers have an incentive to manufacture additional products for so long as the price exceeds the marginal cost of production (i.e., the cost of producing only the next unit, without regard for interest, overhead or fixed costs). This incentive could result in the reduction of the market price of ethanol to a level that is inadequate to generate sufficient cash flow to cover costs.

Excess capacity may also result from decreases in the demand for ethanol, which could result from a number of factors, including, but not limited to, regulatory developments and reduced U.S. gasoline consumption. Reduced gasoline consumption could occur as a result of increased prices for gasoline or crude oil, which could cause businesses and consumers to reduce driving or acquire vehicles with more favorable gasoline mileage or acquire hybrid vehicles.

In addition, because ethanol production produces distillers grains as a co-product, increased ethanol production will also lead to increased supplies of distillers grains. An increase in the supply of distillers grains, without corresponding increases in demand, could lead to lower prices or an inability to sell our ethanol plants’ distillers grains production. A decline in the price of distillers grains or the distillers grains market generally could have a material adverse effect on the results of our ethanol investments.

We depend on our partners to operate our ethanol investments.

Our investments currently represent both majority and minority equity positions, and day-to-day operating control of each plant generally remains with the local farmers’ cooperative or investor group that has promoted the plant. We may not have the ability to directly modify the operations of the plants in response to changes in the business environment or in response to any deficiencies in local operations of the plants. In addition, local plant operators, who also represent the primary suppliers of corn and other crops to the plants, may have interests, such as the price and sourcing of corn and other crops, that may differ from our interest, which is based solely on the operating profit of the plant. The limitations on our ability to control day-to-day plant operations could adversely affect plant results of operations.

12

We may not successfully acquire or develop additional ethanol investments.

The growth of our ethanol business depends on our ability to identify and develop new ethanol investments. Our ethanol development strategy depends on referrals, and introductions, to new investment opportunities from industry participants, such as ethanol plant builders, financial institutions, marketing agents and others. We must continue to maintain favorable relationships with these industry participants, and a material disruption in these sources of referrals would adversely affect our ability to expand our ethanol investments.

Any expansion strategy will depend on prevailing market conditions for the price of ethanol and the costs of corn and natural gas and the expectations of future market conditions. The significant expansion of ethanol production capacity in the United States could impede any expansion strategy. There is increasing competition for suitable sites for ethanol plants. Even if suitable sites or opportunities are identified, we may not be able to secure the services and products from contractors, engineering firms, construction firms and equipment suppliers necessary to build or expand ethanol plants on a timely basis or on acceptable economic terms. Construction costs associated with expansion may increase to levels that would make a new plant too expensive to complete or unprofitable to operate. Additional financing may also be necessary to implement any expansion strategy, which may not be accessible or available on acceptable terms.

Our ethanol plants may be adversely affected by technological advances and efforts to anticipate and employ such technological advances may prove unsuccessful.

The development and implementation of new technologies may result in a significant reduction in the costs of ethanol production. For instance, any technological advances in the efficiency or cost to produce ethanol from inexpensive, cellulosic sources such as wheat, oat or barley straw could have an adverse effect on our ethanol plants, because those facilities are designed to produce ethanol from corn, which is, by comparison, a raw material with other high value uses. We cannot predict when new technologies may become available, the rate of acceptance of new technologies by competitors or the costs associated with new technologies. In addition, advances in the development of alternatives to ethanol could significantly reduce demand for or eliminate the need for ethanol.

Any advances in technology which require significant unanticipated capital expenditures to remain competitive or which reduce demand or prices for ethanol would have a material adverse effect on the results of our ethanol investments.

In addition, alternative fuels, additives and oxygenates are continually under development. Alternative fuel additives that can replace ethanol may be developed, which may decrease the demand for ethanol. It is also possible that technological advances in engine and exhaust system design and performance could reduce the use of oxygenates, which would lower the demand for ethanol, and the results of our ethanol investments may be materially adversely affected.

The U.S. ethanol industry is highly dependent upon a myriad of federal and state legislation and regulation and any changes in legislation or regulation could materially and adversely affect our results of operations and financial position.

The elimination or significant reduction of the blender’s credit could have a material adverse effect on the results of our ethanol investments. The cost of production of ethanol is made significantly more competitive with regular gasoline by federal tax incentives. The American Jobs Creation Act of 2004 created the Volumetric Ethanol Tax Credit, referred to as the “blender’s credit.” This credit currently

13

allows gasoline distributors who blend ethanol with gasoline to receive a federal excise tax credit of $0.45 per gallon of pure ethanol, or $0.045 per gallon if blended with 10% ethanol (E10), and $0.3825 per gallon if blended with 85% ethanol (E85). The $0.45 per gallon incentive for ethanol is scheduled to expire on December 31, 2010. The blender’s credit could be eliminated or reduced at any time through an act of Congress and may not be renewed in 2010 or may be renewed on different terms. In addition, the blender’s credit, as well as other federal and state programs benefiting ethanol (such as tariffs), generally are subject to U.S. government obligations under international trade agreements, including those under the World Trade Organization Agreement on Subsidies and Countervailing Measures, and might be the subject of challenges thereunder, in whole or in part.

Ethanol can be imported into the U.S. duty-free from some countries, which may undermine the ethanol industry in the U.S. Imported ethanol is generally subject to a $0.54 per gallon tariff that was designed to offset the $0.45 per gallon ethanol incentive that is available under the federal excise tax incentive program for refineries that blend ethanol in their fuel. A special exemption from the tariff, known as the Caribbean Basin Initiative, exists for ethanol imported from 24 countries in Central America and the Caribbean Islands, which is limited to a total of 7% of U.S. production per year. Imports from the exempted countries may increase as a result of new plants under development. Since production costs for ethanol in these countries are estimated to be significantly less than what they are in the U.S., the duty-free import of ethanol through the countries exempted from the tariff may negatively affect the demand for domestic ethanol and the price at which our ethanol plants sell ethanol. Any changes in the tariff or exemption from the tariff could have a material adverse effect on the results of our ethanol investments. In addition, the North America Free Trade Agreement, or NAFTA allows Canada and Mexico to export ethanol to the United States duty-free.

The effect of the renewable fuel standard (“RFS”) program in the Energy Independence and Security Act of 2007 (the “2007 Act”) is uncertain. The mandated minimum level of use of renewable fuels in the RFS under the 2007 Act will increase from 9 billion gallons per year in 2008 to 36 billion gallons per year in 2022. The RFS mandate level for conventional biofuels, which includes corn-based ethanol, for 2010 is 12 billion gallons. This requirement progressively increases to 15 billion gallons by 2015 and remains at that level through 2022. The 2007 Act also requires the increased use of “advanced” biofuels, which are alternative biofuels produced without using corn starch such as cellulosic ethanol and biomass-based diesel, with 21 billion gallons of the mandated 36 billion gallons of renewable fuel required to come from advanced biofuels by 2022. Required RFS volumes for both general and advanced renewable fuels in years to follow 2022 will be determined by a governmental administrator, in coordination with the U.S. Department of Energy and U.S. Department of Agriculture. Increased competition from other types of biofuels could have a material adverse effect on the results of our ethanol investments.

The RFS program and the 2007 Act also include provisions allowing “credits” to be granted to fuel producers who blend in their fuel more than the required percentage of renewable fuels in a given year. These credits may be used in subsequent years to satisfy RFS production percentage and volume standards and may be traded to other parties. The accumulation of excess credits could further reduce the impact of the RFS mandate schedule and result in a lower ethanol price or could result in greater fluctuations in demand for ethanol from year to year, both of which could have a material adverse effect on the results of our ethanol investments.

Waivers of the RFS minimum levels of renewable fuels included in gasoline could have a material adverse effect on the results of our ethanol investments. Under the RFS as passed as part of the Energy Policy Act of 2005, the U.S. Environmental Protection Agency, in consultation with the Secretary of Agriculture and the Secretary of Energy, may waive the renewable fuels mandate with respect to one or more states if the Administrator of the U.S. Environmental Protection Agency, or EPA, determines upon

14

the petition of one or more states that implementing the requirements would severely harm the economy or the environment of a state, a region or the U.S., or that there is inadequate supply to meet the requirement. In addition, the 2007 Act allows any other person subject to the requirements of the RFS or the EPA Administrator to file a petition for such a waiver. Any waiver of the RFS with respect to one or more states could adversely offset demand for ethanol and could have a material adverse effect on the results of our ethanol investments.

Changes in corporate average fuel economy standards could adversely impact ethanol prices. Flexible fuel vehicles receive preferential treatment in meeting federally mandated corporate average fuel economy (“CAFE”) standards for automobiles manufactured by car makers. High blend ethanol fuels such as E85 result in lower fuel efficiencies. Absent the CAFE preferences, car makers would not likely build flexible-fuel vehicles. Any change in CAFE preferences could reduce the growth of E85 markets and result in lower ethanol prices.

Various studies have criticized the efficiency of ethanol, in general, and corn-based ethanol in particular, which could lead to the reduction or repeal of incentives and tariffs that promote the use and domestic production of ethanol or otherwise negatively impact public perception and acceptance of ethanol as an alternative fuel.

Although many trade groups, academics and governmental agencies have supported ethanol as a fuel additive that promotes a cleaner environment, others have criticized ethanol production as consuming considerably more energy and emitting more greenhouse gases than other biofuels and as potentially depleting water resources. Other studies have suggested that corn-based ethanol is less efficient than ethanol produced from switchgrass or wheat grain and that it negatively impacts consumers by causing prices for dairy, meat and other foodstuffs from livestock that consume corn to increase. If these views gain acceptance, support for existing measures promoting use and domestic production of corn-based ethanol could decline, leading to reduction or repeal of these measures. These views could also negatively impact public perception of the ethanol industry and acceptance of ethanol as an alternative fuel.

Federal support of cellulosic ethanol may result in reduced incentives to corn-derived ethanol producers.

The American Recovery and Reinvestment Act of 2009 and the Energy Independence and Security Act of 2007 provide funding opportunities in support of cellulosic ethanol obtained from biomass sources such as switchgrass and poplar trees. The amended RFS mandates an increasing level of production of non-corn derived biofuels. These federal policies may suggest a long-term political preference for cellulosic processes using alternative feedstocks such as switchgrass, silage or wood chips. Cellulosic ethanol has a smaller carbon footprint and is unlikely to divert foodstuff from the market. Several cellulosic ethanol plants are under development and there is a risk that cellulosic ethanol could displace corn ethanol. Our plants are designed as single-feedstock facilities, located in corn production areas with limited alternative feedstock nearby, and would require significant additional investment to convert to the production of cellulosic ethanol. The adoption of cellulosic ethanol as the preferred form of ethanol could have a significant adverse effect on our ethanol business.

Our ethanol business is affected by environmental and other regulations which could impede or prohibit our ability to successfully operate our plants.

Our ethanol production facilities are subject to extensive air, water and other environmental regulations. We have had to obtain numerous permits to construct and operate our plants. Regulatory agencies could

15

impose conditions or other restrictions in the permits that are detrimental or which increase our costs. More stringent federal or state environmental regulations could be adopted, which could significantly increase our operating costs or require us to expend considerable resources.

Our ethanol plants emit various airborne pollutants as by-products of the ethanol production process, including carbon dioxide. In 2007, the U.S. Supreme Court classified carbon dioxide as an air pollutant under the Clean Air Act in a case seeking to require the EPA to regulate carbon dioxide in vehicle emissions. In February 2010, the EPA released its final regulations on the Renewable Fuel Standard program (RFS2). We believe our plants are grandfathered at their current operating capacity, but plant expansion will need to meet a 20% threshold reduction in greenhouse gas (GHG) emissions from a 2005 baseline measurement to produce ethanol eligible for the RFS2 mandate. Additionally, legislation is pending in Congress on a comprehensive carbon dioxide regulatory scheme, such as a carbon tax or cap-and-trade system. To expand our plant capacity, we may be required to obtain additional permits, install advanced technology such as corn oil extraction, or reduce drying of certain amounts of distillers grains.

The California Air Resources Board has adopted a Low Carbon Fuel Standard requiring a 10% reduction in GHG emissions from transportation fuels by 2020. An Indirect Land Use Charge is included in this lifecycle GHG emission calculation. While this standard is being challenged by lawsuits, implementation of such a standard could have an adverse impact on our market for corn-based ethanol if determined that in California corn-based ethanol fails to achieve lifecycle GHG emission reductions.

We face significant competition in the ethanol industry.

We face significant competition for new ethanol investment opportunities. There are varied enterprises seeking to participate in the ethanol industry. Some enterprises provide financial and management support similar to our business model. Other enterprises seek to acquire or develop plants which they will directly own and operate. Many of our competitors are larger and have greater financial resources and name recognition than we do. We must compete for investment opportunities based on our strategy of supporting and enhancing local development of ethanol plant opportunities. We may not be successful in competing for investment opportunities based on our strategy.

The ethanol industry is primarily comprised of smaller entities that engage exclusively in ethanol production and large integrated grain companies that produce ethanol along with their base grain business. Recently, several large oil companies have entered the ethanol production market. If these companies increase their ethanol plant ownership or other oil companies seek to engage in direct ethanol production, there would be less of a need to purchase ethanol from independent producers like our ethanol plants.

There is a consolidation trend in the ethanol industry, partly a result of companies recently seeking protection under the United States Bankruptcy Code. As a result, firms are growing in size and scope. Larger firms offer efficiencies and economies of scale, resulting in lower costs of production. In addition, plants currently being sold as part of a bankruptcy proceeding may have significantly lower costs than our ethanol plants. Absent significant growth and diversification, our ethanol plants may not be able to operate profitably in a more competitive environment. No assurance can be given that our ethanol plants will be able to compete successfully or that competition from larger companies with greater financial resources will not have a materially adverse affect on the results of our ethanol investments.

16

There is a risk of foreign competition in the ethanol industry.

Ethanol produced or processed in several countries in Central America and the Caribbean region is eligible for tariff reduction or elimination under the Caribbean Basin Initiative. Brazil, currently the world’s second largest ethanol producer, makes ethanol primarily from sugarcane which historically has been less expensive to produce than producing ethanol from corn. Other foreign producers may be able to produce ethanol at lower input costs, including feedstock, facilities and personnel, than our plants. Ethanol imported from Brazil or other foreign countries, even with the import tariff, or from a Caribbean Basin source may be a less expensive alternative to domestically produced ethanol.

Our plants depend on an uninterrupted supply of energy and water to operate. Unforeseen plant shutdowns could harm our business.

Our plants require a significant and uninterrupted supply of natural gas, electricity and water to operate. We generally rely on third parties to provide these resources. If there is an interruption in the supply of energy or water for any reason, such as supply, delivery or mechanical problems and we are unable to secure an adequate alternative supply to sustain plant operations, we may be required to stop production. A production halt for an extended period of time could result in material losses.

Potential business disruption from factors outside our control, including natural disasters, severe weather conditions, accidents, strikes, unexpected equipment failures and unforeseen plant shutdowns, could adversely affect our cash flow and operating results.

The debt agreements for the ethanol plants contain restrictive financial and performance covenants.

Ethanol facility debt covenants contain several financial and performance restrictions. A breach of any of these covenants could result in a default under the applicable agreement. If a default were to occur, we would likely seek a waiver of that default, attempt to reset the covenant, or refinance the instrument and accompanying obligations. If we were unable to obtain this relief, the default could result in the acceleration of the total due related to that debt obligation. If a default were to occur, we may not be able to pay our debts or borrow sufficient funds to refinance them. In addition, certain lease agreements could also be in default if a default of the debt agreement occurs. Any of these events, if they occur, could materially adversely affect our results of operations, financial condition, and cash flows.

Changes in interest rates could have a material adverse effect on the results of our ethanol investments.

Levelland Hockley, One Earth and Patriot all have interest rate swaps at January 31, 2010 that, in essence, fix the interest rate on a portion of their variable rate debt. During fiscal year 2009, we recognized losses on these swaps of approximately $2.5 million. Further reductions in interest rates could increase the liability position of the interest rate swaps, requiring us to record additional expense which could be material. The liability for these interest rate swaps could also result in a default of the term loan agreements’ restrictive financial covenants.

In addition, increases in interest rates could have a negative impact on results of operations as all of the debt our ethanol plants have is variable rate debt. Furthermore, the interest rate swaps do not fix the interest rate on the entire portion of the related debt. Levelland Hockley’s interest rate swap expires in April 2010.

17

Risks Related to the wind down and exit of our retail business and our real estate segment.

Our future costs associated with administering extended product service contracts may result in higher than expected costs.

We will continue to administer extended product service contracts that have contractual maturities over the next four years. To the extent we do not have products or an adequate repair service network to satisfy warranty claims, we may incur material costs as we would be required to refund cash to customers for warranted products.

We have a significant amount of vacant warehouse and retail space after the completion of the wind down of our retail business.

At January 31, 2010, we own two distribution facilities and 34 former retail store properties comprising approximately 911,000 square feet that are completely or partially vacant. We are currently marketing these facilities for lease or sale. We may not be able to successfully lease or sell these properties which could result in lost opportunities for revenue or future impairment charges related to the carrying value of the associated assets. We would also have costs related to the vacant properties such as property taxes and utilities that we would have to bear without any revenue from such properties.

|

|

|

|

Item 1B. |

Unresolved Staff Comments |

None.

|

|

|

|

Item 2. |

Properties |

The information required by this Item 2 is set forth in Item 1 of this report under “Retail Overview,” “Real Estate Operations” and “Facilities” and is incorporated herein by reference.

|

|

|

|

Item 3. |

Legal Proceedings |

We are involved in various other legal proceedings incidental to the conduct of our business. We believe that these other proceedings will not have a material adverse effect on our financial condition or results of operations.

Executive Officers of the Company

Set forth below is certain information about each of our executive officers.

|

|

|

|

|

|

|

Name |

|

Age |

|

Position |

|

|

|

|

|

|

|

|

|

|

|

|

|

Stuart Rose |

|

55 |

|

Chairman of the Board and Chief Executive Officer* |

|

Douglas Bruggeman |

|

49 |

|

Vice President-Finance, Chief Financial Officer and Treasurer |

|

Edward Kress |

|

60 |

|

Secretary* |

|

Zafar Rizvi |

|

60 |

|

Vice President, and President of Farmers Energy Incorporated |

*Also serves as a director.

Stuart Rose has been our Chairman of the Board and Chief Executive Officer since our incorporation in 1984 as a holding company to succeed to the ownership of Rex Radio and Television, Inc., Kelly &

18

Cohen Appliances, Inc. and Stereo Town, Inc. Prior to 1984, Mr. Rose was Chairman of the Board and Chief Executive Officer of Rex Radio and Television, Inc., which he founded in 1980 to acquire the stock of a corporation which operated four retail stores.

Douglas Bruggeman has been our Vice President–Finance and Treasurer since 1989 and was elected Chief Financial Officer in 2003. From 1987 to 1989, Mr. Bruggeman was our Manager of Corporate Accounting. Mr. Bruggeman was employed with the accounting firm of Ernst & Young prior to joining us in 1986.

Edward Kress has been our Secretary since 1984 and a director since 1985. Mr. Kress has been a partner of the law firm of Dinsmore & Shohl LLP (formerly Chernesky, Heyman & Kress P.L.L.), our legal counsel, since 1988. Mr. Kress has practiced law in Dayton, Ohio since 1974.

Zafar Rizvi has been our Vice President, and President of Farmers Energy Incorporated, our alternative energy investment subsidiary, since 2006. From 1991 to 2006, Mr. Rizvi was our Vice President – Loss Prevention. From 1986 to 1991, Mr. Rizvi was employed in the video retailing industry in a variety of management positions.

|

|

|

|

Item 4. |

Removed and Reserved |

PART II

|

|

|

|

Item 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

SHAREHOLDER INFORMATION

Common Share Information and Quarterly Share Prices

Our common stock is traded on the New York Stock Exchange under the symbol RSC.

|

|

|

|

|

|

|

|

|

|

|

Fiscal Quarter ended |

|

|

High |

|

Low |

|

||

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

April 30, 2008 |

|

$ |

21.15 |

|

$ |

15.84 |

|

|

|

July 31, 2008 |

|

|

16.98 |

|

|

10.78 |

|

|

|

October 31, 2008 |

|

|

13.46 |

|

|

6.50 |

|

|

|

January 31, 2009 |

|

|

10.48 |

|

|

5.76 |

|

|

|

|

|

|

|

|

|

|

|

|

|

April 30, 2009 |

|

$ |

13.50 |

|

$ |

5.52 |

|

|

|

July 31, 2009 |

|

|

12.99 |

|

|

9.36 |

|

|

|

October 31, 2009 |

|

|

13.02 |

|

|

9.75 |

|

|

|

January 31, 2010 |

|

|

15.41 |

|

|

11.89 |

|

|

As of April 15, 2010, there were 132 holders of record of our common stock, including shares held in nominee or street name by brokers.

Dividend Policy

19

We did not pay dividends in the current or prior years. We currently have no restrictions on the payment of dividends. Our consolidated ethanol subsidiaries have certain restrictions on their ability to pay us dividends.

Issuer Purchases of Equity Securities

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Period |

|

|

Total Number |

|

Average Price |

|

Total Number of |

|

Maximum Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

November 1-30, 2009 |

|

6,700 |

|

$ |

12.22 |

|

6,700 |

|

38,101 |

|

|

|

December 1-31, 2009 |

|

— |

|

$ |

— |

|

— |

|

538,101 |

|

|

|

January 1-31, 2010 |

|

715,357 |

|

$ |

14.07 |

|

55,400 |

|

482,701 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

722,057 |

|

$ |

14.06 |

|

62,100 |

|

482,701 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) |

A total of 659,957 shares of common stock were purchased by us other than through a publicly announced plan or program. These shares were acquired on January 8, 2010 in payment of the exercise price of stock options exercised by Stuart A. Rose, our Chairman and Chief Executive Office pursuant to the Company’s Stock-for-Stock and Cashless Option Exercise Rules and Procedures, adopted on June 4, 2001. The purchase price was $14.00 per share. |

|

|

|

|

|

|

(2) |

On December 1, 2009, our Board of Directors increased our share repurchase authorization by an additional 500,000 shares. At January 31, 2010, a total of 482,701 shares remained available to purchase under this authorization. |

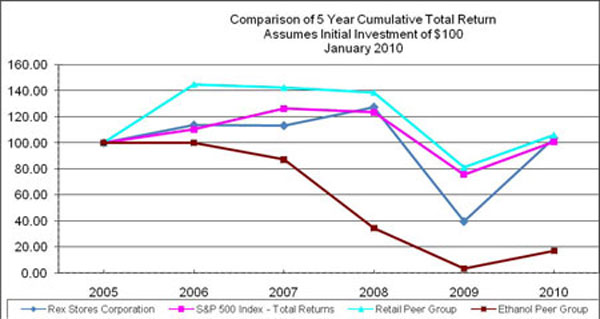

Performance Graph

The following graph compares the yearly percentage change in the cumulative total shareholder return on our Common Stock against the cumulative total return of the S&P 500 Stock Index and two peer groups comprised of selected publicly traded consumer electronics retailers and ethanol producers (*) for the period commencing January 31, 2005 and ended January 31, 2010. The graph assumes an investment of $100 in our Common Stock and each index on January 31, 2005 and reinvestment of all dividends.

20

* The retail peer group is comprised of Best Buy Co., Inc. and Conn’s, Inc. This is the last year we will show a retail peer group as we ceased our retail operations during fiscal year 2009.

* The ethanol peer group (and the month the companies went public) is comprised of Pacific Ethanol, Inc. (March 2005), BioFuel Energy Corp. (June 2007) and Green Plains Renewable Energy, Inc. (March 2006). In prior years, the ethanol peer group included Aventine Renewable Energy Holdings, Inc. which filed for Chapter 11 reorganization in February 2009 and has been removed from the ethanol peer group. We added Green Plains Renewable Energy, Inc. this year. Returns for the ethanol peer group are included upon a full year’s return being available as of January 31.

|

|

|

|

Item 6. |

Selected Financial Data |

The following statements of operations and balance sheet data have been derived from our consolidated financial statements and should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and the Consolidated Financial Statements and related Notes. Prior period amounts applicable to the statement of operations have been adjusted to recognize the reclassification of the results of our former retail segment and certain real estate assets to discontinued operations as a result of our exit of the retail business and real estate sales. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for a discussion of income from synthetic fuel, ethanol investments, derivative financial instruments, gain on sale of real estate and long-term debt. These items have fluctuated significantly in recent years and may affect comparability of years.

21

Five Year Financial Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(In Thousands,

Except Per |

|

Years Ended January 31, |

|

|||||||||||||

|

|

|

|

||||||||||||||

|

|

2010 |

|

2009 |

|

2008 |

|

2007 |

|

2006 |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales and revenue (a) |

|

$ |

170,264 |

|

$ |

68,638 |

|

$ |

382 |

|

$ |

316 |

|

$ |

233 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income (loss) from continuing operations attributable to REX common shareholders (a) (b) |

|

$ |

5,158 |

|

$ |

(2,919 |

) |

$ |

19,588 |

|

$ |

6,587 |

|

$ |

22,315 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) attributable to REX common shareholders (b) |

|

$ |

8,652 |

|

$ |

(3,297 |

) |

$ |

33,867 |

|

$ |

11,351 |

|

$ |

28,269 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic income per (loss) share from continuing operations attributable to REX common shareholders (a) |

|

$ |

0.55 |

|

$ |

(0.29 |

) |

$ |

1.88 |

|

$ |

0.64 |

|

$ |

2.09 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diluted income (loss) per share from continuing operations attributable to REX common shareholders (a) |

|

$ |

0.54 |

|

$ |

(0.29 |

) |

$ |

1.67 |

|

$ |

0.57 |

|

$ |

1.83 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|