Attached files

| file | filename |

|---|---|

| EX-21.1 - PARETEUM Corp | v179446_ex21-1.htm |

| EX-23.1 - PARETEUM Corp | v179446_ex23-1.htm |

| EX-31.1 - PARETEUM Corp | v179446_ex31-1.htm |

| EX-32.2 - PARETEUM Corp | v179446_ex32-2.htm |

| EX-31.2 - PARETEUM Corp | v179446_ex31-2.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form

10-K

|

x

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

fiscal year ended December 31, 2009

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES

EXCHANGE ACT OF 1934

|

For the

transition period from ____________________ to ____________________

Commission

file number 000-30061

Elephant

Talk Communications, Inc.

(Exact

name of registrant as specified in its charter)

|

California

|

95-4557538

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

(I.R.S.

Employer

Identification

No.)

|

|

Schiphol

Boulevard 249

1118

BH Schiphol

The

Netherlands

|

N/A

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

Issuer’s

telephone number: 31

0 20 653 5916

Securities

registered pursuant to Section 12(b) of the Act: None

Securities

registered pursuant to Section 12(g) of the Act:

Common

Stock, no par value

(Title of

class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. o

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. o

Indicate by check mark whether the

registrant (1) has filed all reports required to be filed by Section 13 or 15(d)

of the Securities Exchange Act of 1934 during the preceding 12 months (or for

such shorter period that the registrant was required to file such reports), and

(2) has been subject to such filing requirements for the past 90

days. Yes o No x

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a non-accelerated filer or a smaller reporting

company. See definition of “large accelerated filer”, “accelerated

filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

|

Large

accelerated filer o

|

Accelerated

filer o

|

|

|

Non-accelerated

filer o

|

Smaller

reporting company x

|

|

|

(Do

not check if a smaller reporting company)

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act).Yes o No x

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates as of June 30, 2009 was approximately $12,786,514 based on

the closing sale price of the Company’s common stock on such date of U.S. $0.95

per share, as reported by the OTC BB.

State the

number of shares outstanding of each of the issuer’s classes of common equity,

as of the latest practicable date: As of March 30, 2010 there were 64,260,437

shares of common stock outstanding.

Form

10-K

For

the fiscal year ended December 31, 2009

TABLE

OF CONTENTS

|

Note

on Forward-Looking Statement

|

1

|

|

|

PART

I

|

||

|

Item

1.

|

Description

of Business.

|

2

|

|

Item

2.

|

Description

of Property.

|

26

|

|

Item

3.

|

Legal

Proceedings.

|

27

|

|

PART

II

|

||

|

Item

4.

|

Reserved

|

28

|

|

Item

5.

|

Market

for Common Equity and Related Stockholder Matters.

|

28

|

|

Item

6.

|

Selected

Financial Data.

|

31

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations.

|

32

|

|

Item

8.

|

Financial

Statements.

|

39

|

|

Item

9.

|

Changes

In and Disagreements with Accountants on Accounting and Financial

Disclosure.

|

67

|

|

Item

9A(T).

|

Controls

and Procedures.

|

67

|

|

PART

III

|

||

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance.

|

69

|

|

Item

11.

|

Executive

Compensation.

|

74

|

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Shareholder Matters.

|

74

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence.

|

76

|

|

Item

14.

|

Principal

Accountant Fees and Services.

|

78

|

|

|

||

|

PART

IV

|

||

|

|

||

|

Item

15.

|

Exhibits,

Financial Statement Schedules.

|

79

|

NOTE

ON FORWARD LOOKING STATEMENTS

This

Report, including the documents incorporated by reference in this Report,

includes forward-looking statements. We have based these

forward-looking statements on our current expectations and projections about

future events. Our actual results may differ materially from those

discussed herein, or implied by, these forward-looking

statements. Forward-looking statements are generally identified by

words such as “believe,” “expect,” “anticipate,” “intend,” “estimate,” “plan,”

“project” and other similar expressions. In addition, any statements that refer

to expectations or other characterizations of future events or circumstances are

forward-looking statements. Forward-looking statements included in this Report

or our other filings with the SEC include, but are not necessarily limited to,

those relating to:

|

|

·

|

risks

and uncertainties associated with the integration of the assets and

operations we have acquired and may acquire in the

future;

|

|

|

·

|

our

possible inability to raise or generate additional funds that will be

necessary to continue and expand our

operations;

|

|

|

·

|

our

potential lack of revenue growth;

|

|

|

·

|

our

potential inability to add new products and services that will be

necessary to generate increased

sales;

|

|

|

·

|

our

potential lack of cash flows;

|

|

|

·

|

our

potential loss of key personnel;

|

|

|

·

|

the

availability of qualified

personnel;

|

|

|

·

|

international,

national regional and local economic political

changes;

|

|

|

·

|

general

economic and market conditions;

|

|

|

·

|

increases

in operating expenses associated with the growth of our

operations;

|

|

|

·

|

the

possibility of telecommunications rate changes and technological

changes;

|

|

|

·

|

the

potential for increased competition;

and

|

|

|

·

|

other

unanticipated factors.

|

The

foregoing does not represent an exhaustive list of risks. Please see “Risk

Factors” for additional risks which could adversely impact our business and

financial performance. Moreover, new risks emerge from time to time and it is

not possible for our management to predict all risks, nor can we assess the

impact of all risks on our business or the extent to which any risk, or

combination of risks, may cause actual results to differ from those contained in

any forward-looking statements. All forward-looking statements included in this

Report are based on information available to us on the date of this Report.

Except to the extent required by applicable laws or rules, we undertake no

obligation to publicly update or revise any forward-looking statement, whether

as a result of new information, future events or otherwise. All subsequent

written and oral forward-looking statements attributable to us or persons acting

on our behalf are expressly qualified in their entirety by the cautionary

statements contained throughout this Report.

1

ITEM

1. DESCRIPTION OF BUSINESS

We

provide Internet, telephony, and data communications software services to both

mobile phone companies and businesses

Elephant

Talk Communications, Inc. also referred to as “we”, “us”, “Elephant Talk” and

“the Company” is an international provider of business software and services to

the telecommunications and financial services industry. Elephant Talk installs

its operating software at the network operating centers of mobile carrier and

receives a fee per month per cell phone subscriber on the network. Currently the

subscribers are wholesale customers of Vizzavi (a subsidiary of the Vodafone

group) in Spain and T-Mobile in the Netherlands. Elephant Talk

typically signs a five- year exclusive with one carrier per

country. Negotiations with mobile carriers are currently under way in

a number of other countries. We also operate landline telephony services in nine

European countries and Bahrain. Our network components, hardware, software

systems, telecom switches and interconnections with other telecom operators are

located in secured data-centers in eight countries.

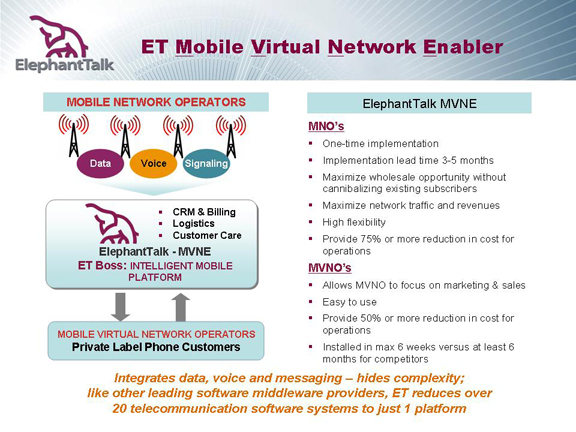

Our

ET Boss software enables mobile carriers to outsource their entire back office

to Elephant Talk. By outsourcing operations the mobile carriers can reduce the

number of vendor software, employees, and consultants. ET Boss

reduces the number of software modules / vendors form over twenty to

one. Additionally, ET Boss enables mobile virtual network operators

(MVNO’s) to control their pricing and product offerings with the touch of a

keypad from a windows interface. This compares with the current

situation often experienced by virtual operators whereby it can take up to six

month to effect a change in their product offerings.

Due to

the large capital outlays required for the construction of new towers, switches,

and infrastructure, mobile network operations such as Sprint (outsourced to

Ericson) have been outsourcing elements of their networks in an effort to reduce

costs. Our software platform offers operators the potential to

realize significant savings; we are currently providing these services to

Vodafone’s subsidiary in Spain and T-Mobile in the Netherlands. We simply take

three pipes from the mobile network operator (MNO) – voice, data, and signaling

(see above) – and plug them into our ET Boss platform (see below).

2

We are

developing and acquiring application software to enable our virtual clients to

offer various dynamic products that include remote health care monitoring on a

watch or pendant credit card fraud prevention, mobile internet ID security,

multi-country discounted phone services, loyalty management services, and a

whole range of other emerging customized mobile services. In line with our

strategy to develop and market customized mobile solutions, we acquired

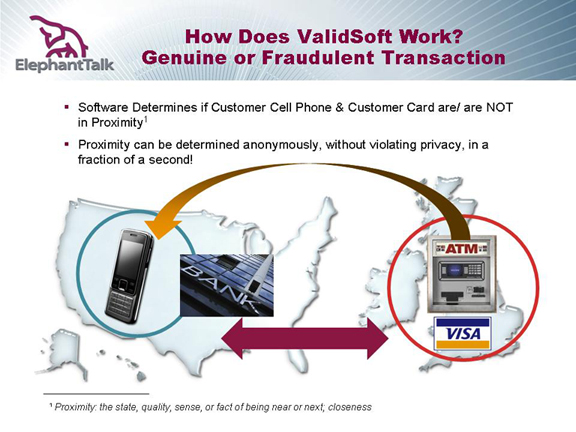

ValidSoft, Ltd. (“ValidSoft”) on March 17, 2010. ValidSoft provides strong

authentication and transaction verification capabilities that allow

organizations to quickly implement solutions that protect against certain of the

latest forms of credit and debit card fraud, and on-line transaction and

identity theft. By correlating the relative location of a person’s credit card

with the location of their mobile phone, this service can tell a bank in less

than half a second if the transaction is likely genuine or fraudulent (see

diagram below). We anticipate generating revenues on a per transaction

verification fee from banks. This acquisition combines ValidSoft’s

best in class proprietary software with our superior telecommunication platform

to create what we believe is the best electronic fraud prevention total solution

available.

We

currently generate in excess of $40 million in revenues in 2009, employ 89

employees and have retained 27 independent contractors on a long-term basis. Our

principal offices are located in The Netherlands, Spain and China. Mobile

services are currently provided in Spain and The Netherlands, whereas landline

telephony services are provided in nine European countries and Bahrain. Our

network components, hardware, software systems, telecom switches and

interconnections with other telecom operators are located in secured

data-centers in eight countries.

3

Background of Elephant Talk

Communications, Inc.

Elephant

Talk Communications Inc. was formed in 2001 as a result of a merger between

Staruni Corporation (USA, 1962) and Elephant Talk Limited (Hong Kong, 1994).

Staruni Corporation - named Altius Corporation, Inc., until 1997 - was a web

developer and Internet Service Provider since 1997 following its acquisition of

Starnet Universe Internet Inc. Elephant Talk Limited (Hong Kong)

began operating in 1994 as an international long distance services provider,

specializing in international call termination into China. In 2006 Elephant Talk

Communications, Inc., decided to abandon its strategy of focusing on

international calls into China.

In 2000

Staruni Corporation became a reporting company on the OTC Bulletin Board under

the symbol “SRUN”, replaced by “ETLK” following the merger with Elephant Talk

Limited (Hong Kong), and in turn changed to “ETAK” pursuant to a 2008

stock-split.

In

January 2007, through our acquisition of Benoit Telecom (Switzerland), we

established a foothold in the European Telecommunications Market, particularly

within the market for Service Numbers (Premium Rate Services and Toll Free

Services) and to a smaller extent Carrier (Pre) Select

Services. Furthermore, through the human capital, IT resources and

software acquired, we obtained the experience and expertise of individuals and

software deeply connected to telecom and multi-media systems, telecom

regulations and European markets.

In March

2010, we acquired ValidSoft. We believe this acquisition is in line

with our strategy to develop and market customized mobile

solutions. ValidSoft provides strong authentication and transaction

verification capabilities that allow organizations to quickly implement

solutions which protect against the latest forms of credit and debit card fraud,

on-line transaction and identity theft. This acquisition combines ValidSoft’s

best in class proprietary software with our superior telecommunication platform

to create the best electronic fraud prevention total solution available on the

market today.

Further

details on the above acquisitions, other (smaller) acquisitions and

incorporations can be found under “legal structure of the company”.

Product

– Service Strategy

Our

corporate strategy results in the following three main types of value

propositions offered to the market, each building upon our

converged network and access capabilities in combination with “ET Boss”, our

proprietary telecommunications Operating Support System (OSS) and Business

Support System (BSS):

|

|

·

|

Customized mobile

services, such as our ValidSoft credit card fraud

solution

|

|

|

·

|

Mobile Enabling Platform (ET

BOSS), including our MVNE/MVNO

services

|

|

|

·

|

Landline network outsourcing

services

|

Industry

Developments

A number

of relevant factors in the converging telecommunications industry, combined with

consumers and businesses increasing adoption of mobile and wireless based

applications, drive our investments and services, are as follow:

4

The

mobile phone will become the channel of choice for consumers

We

believe that the mobile phone will ultimately be the (handheld) device chosen by

consumers and businesses to best bring personalized, contextual and time-wise

relevant services such as:

|

|

·

|

mobile

banking

|

|

|

·

|

telemedicine

|

|

|

·

|

location

based services

|

|

|

·

|

use

of near field communications for cashless payments, couponing, cashless

tickets, vending machine payments, grocery store

payments

|

|

|

·

|

credit

card applications

|

|

|

·

|

communities;

social, entertainment and loyalty

|

|

|

·

|

customer

profiling and data mining to support one-on-one

marketing

|

|

|

·

|

security

and trust sensitive applications; the mobile phone as

authenticator.

|

Mobile

operators need to reduce total cost of ownership (TCO) and increase utilization

of their assets

Mobile

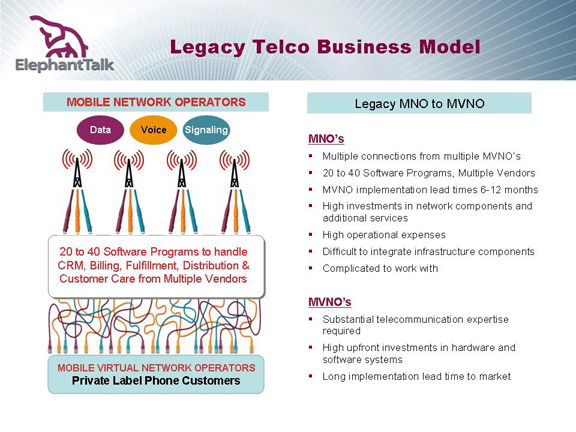

Network Operators typically have twenty or more vendors for their software to

handle Network Management, Customer Relationship Management (CRM), billing,

fulfillment, distribution and customer care. This has resulted in legacy systems

that are expensive to maintain and difficult to adapt to changing market

conditions. In addition, MNO’s are looking for new ways to attract traffic over

their networks, since the traditional mass marketing of voice and messaging

focused on end-users (“retail”) shows little or no growth. MNO’s are required to

shift their organization from a mass marketing oriented retail focus to a

wholesale focus; thereby allowing other organizations such as MVNO’s to serve

smaller and specifically targeted end-user groups with specialized and converged

solutions in order to increase traffic (e.g. voice, text, data or media) over

the operators networks.

Trust

and security aspects are increasingly important in a networked and digitalized

environment

The open

nature of the Internet as well as exponential digitalization and globalization

of society has resulted in increased (international) fraud, attention for

privacy intrusions and national security concerns.

Summary

Services and Solutions

ValidSoft

Ltd: customized mobile solution for credit card fraud prevention

In line

with our strategy to develop and market customized mobile solutions, we recently

acquired ValidSoft Ltd. Validsoft provides strong authentication and

transaction verification capabilities, which allow organizations to quickly

implement solutions that protect against the latest forms of credit and debit

card fraud, on-line transaction and identity theft. This acquisition

combines Validsoft’s advanced proprietary software with what we believe is a

superior telecommunication platform to create a leading electronic fraud

prevention total solution.

We

believe the ValidSoft solution can save US banks significant time,

energy and “zero-liability” funds in connection with credit and debit card

fraud. ValidSoft has successfully completed trials with two major banks and is

in advanced discussions with leading global payment processors, international

banks and credit card providers. Validsoft was recently awarded the European

Privacy Seal from EuroPrise, underscoring the prudent set-up of its systems as

to privacy matters. Revenues generated from the ValidSoft business are expected

to become our highest margin contributor.

MVNE/MVNO

Since

2006, significant investments have been made in mobile enabling services and

platforms. We invest and operate as a full Mobile Virtual Network Enabler

(MVNE), offering MNO’s various parts of the back office network including core

network, messaging platforms, data platforms and billing

solutions. As a result, we are positioning ourselves as the MVNE

partner of choice for the larger, global MNO’s, and a one-stop convergent

solutions provider for specialized MVNO customers.

5

The first

revenues from these mobile services began during the fourth quarter of 2008 with

T-Mobile in the Netherlands and with Vizzavi (a subsidiary of Vodafone group) in

Spain during 2009. Currently we have 6 MVNO’s running on our platforms in The

Netherlands and Spain, and are rapidly expanding our geographic service

areas.

Currently

we are negotiating agreements with various MNO’s and MVNO’s in numerous

countries in order to realize our strong growth objectives, both in revenues and

margin improvement.

Landline

Outsourced solutions

At the

base of our advanced mobile services, and currently still the largest revenue

contributor, is our landline services, which we offer in nine European countries

and Bahrain. These services are provided by operating a switch-based telecom

network with national licenses and direct land line interconnects with the

Incumbents/National Telecom Operators. Together with our centrally operated and

managed IN-CRM platform, we offer geographical, premium rate, toll free,

personal, nomadic and Voice over Internet Protocol (“VoIP”) services to our

primarily business customers. We position our customers as if they

are a fully networked telecommunications company themselves by providing them

with the tools and resources necessary to manage their businesses, particularly

the telecommunications segment, as an integrated component of their overall

offering.

Network

Landline

and Mobile Network

Our

network is based on landline and MVNO telecommunications licenses, mobile access

agreements and network interconnections. Our geographical cross-border

footprint, established through existing relationships with national telecom

incumbents, is well positioned for international traffic because we have

established our own facilities-based infrastructure on two continents.

Currently, as a fully licensed carrier, we are interconnected with incumbents in

the Netherlands (KPN), Spain (Telefonica), Austria (Telekom Austria), Belgium

(Belgacom), Switzerland (Swisscom), Italy (Telecom Italia), the United Kingdom

(BT) and Bahrain (Batelco). Through partners, we have access to interconnections

in France, Germany, Poland, Finland, Sweden, Norway and Ireland. For

our premium rate services we added to our national interconnect with KPN a

direct connection in the Netherlands with the mobile operators Vodafone and

T-Mobile.

For our

mobile services we need, in addition to the landline interconnections and switch

facilities, mobile access coverage. In 2008 we entered into our first MVNE

agreement with T-Mobile/Orange in the Netherlands where in 2010 we were

servicing six of our own MVNO’s. In 2009 we were awarded an MVNE agreement with

Vizzavi (a subsidiary of the Vodafone group) of Spain, and provide managed

services for their MVNO portfolio, to be followed by the hosting of our own

MVNO’s.

In order to reduce the investments

required for our MVNO’s, as well as increase our flexibility and depth of mobile

service offerings to MVNO’s and MNO’s, we

operate as a full MVNE; meaning that we procure, integrate and operate the

relevant mobile components, including core network, application platform,

subscriber management and MVNO billing and CRM.

Network

Operations Center (NOC)

Our

global 24/7 Network Operations Center is located in Guangzhou, China and

monitors all landline, data and mobile traffic throughout our global clear

bandwidth and IP network.

Proprietary

Software Technology

ET’s

Business Operating Support System (“ET BOSS”)

|

|

§

|

To

maintain flexibility and allow for growth, we have chosen to develop our

own proprietary software and systems including: 1) a fully integrated

rating, mediation, and provisioning CRM and billing system for

multi-country and multimedia use, and applications, and 2) an advanced

Infitel IN platform.

|

6

|

|

§

|

Our

internally developed customer provisioning, rating and billing system,

also known as “ET BOSS”, ensures proper support for all of our

services. Further, the reliable data provided by the ET BOSS

system is the basis for customer satisfaction(?). We believe our network

and system platforms are able to handle the high demands of national

incumbents and other telecom operators on our globally interconnected

network. The key component of our business strategy is the fully automated

capturing and recording of any event on our global network through a

standard Call Data Record, or CDR. CDR’s are globally

recognized and accepted by all of our suppliers and customers because of

their high quality, reliability and consistency. As a result, on a real

time/on-line basis, we believe our billing engine provides reliable

inter-company payment overviews, and will continue to do so as we develop

and implement our global network.

|

|

|

§

|

The

core

modules have been designed to address all of our major business

processes, and those of our partners in such a manner that the

state of the art flexibility, level of integration and dynamic feature set

ensures rapid and low-cost deployments. The core modules and their

sub-modules include amongst others:

|

|

|

§

|

Billing;

(dynamic) rating management, bill mediation, invoicing and automatic

payment script generation

|

|

|

§

|

Payment;

credit card, direct debit, Paypal etc. enabled

functionalities

|

|

|

§

|

Provisioning;

switches, HLR, porting

|

|

|

§

|

Self

Care; mobile, carrier(pre)select, premium rate & toll free

services

|

|

|

§

|

CRM

; trouble ticketing, customer management, provisioning

|

|

|

§

|

Sales

& Marketing; prospect management, sales management, analysis

tools

|

|

|

§

|

Revenue

Collection Assurance; end-user credit management, credit control, fraud

management, routing analysis

|

|

|

§

|

Control;

dashboard overview, reporting, quality analysis, quality

control

|

The

sub-modules are unique and tailored to local situations.

Infitel

Suite - IN Platform

In order

to achieve real time session control, rating and charging, telecom value added

applications as well as improved enrichment of data generated in and passing

through our networks, we have acquired the carrier grade next generation IN

(Intelligent Network) platform “Infitel”, including the source code and

trademark. We own and develop this platform, thereby ensuring the flexibility

and integration we strive for in and between all our software and network

components.

Inficore is the core of the IN

platform, defines the framework, administrative modules and SLP (Service Logic

Processor) that runs the scripts (call flows) created with

Infiscript.

Infiscript is the SCE (Service

Creation Environment) this is a graphical suite with which the call flows and

business logic can be developed and compiled to be distributed to running

Inficore environments.

Infitel Suite comprises the

applications and call-flows that are running on top of Inficore and that have

been created with Infiscript, customized SIBs (C++ core code) and stored

procedures.

The

Infitel Suite comprises amongst others

the following value added services:

|

|

§

|

Intelligent

Call Routing, Service Numbers

|

7

|

|

§

|

Universal

Prepaid (Residential, Phoneshop, Reseller)

|

|

|

§

|

Flexible

Number Portability

|

|

|

§

|

EasyVote

(Televoting)

|

|

|

§

|

VPN/CUG

|

|

|

§

|

Advanced

Call Completion

|

|

|

§

|

NJoy-Dial

|

|

|

§

|

Personal

Call Manager

|

|

|

§

|

Advanced

Business Communication

|

|

|

§

|

Zonal

Call Manager

|

ValidSoft -

Fraud Prevention and Security Software Solutions

In 2009,

we began investing and developing the integration of our systems into

those of (at that time still) joint venture partner ValidSoft, in order to be

able to offer a full fledged security solution over mobile networks. These

investments in development were part of our overall strategy to becoming a

leading player in the area of “Customized Mobile Solutions”.

ValidSoft,

as a software engineering company, has made significant investments in

intellectual property in processes and software pertaining to Intelligent

Identity & Transaction Verification, and is considered to have developed

thought leadership in countering electronic fraud. The essence of the ValidSoft

product suite is in providing Card-(not) Present fraud prevention, on-line

Banking fraud prevention, Strong Mutual Authentication (multi-channel),

Transaction Verification (Out of Band – OOB), Identity Verification and

Non-Repudiation.

The main

components of the VALid® product suite are:

§ VALid-IVR is the Real-Time

Interactive Voice Response (IVR) Internet, Phone Banking and Call Center mutual

authentication and transaction verification solution providing a holistic

multi-channel approach to fraud prevention. VALid-IVR provides outbound and

inbound telephony all with configurable Transaction Verification. VALid-IVR

integrates with Text-To-Speech (TTS), Speech Recognition and Voice Biometrics

functionality, providing a seamless and intuitive customer experience while

delivering the most secure and functionally rich authentication capability

available.

§ VALid-SMS is the

Store-and-Forward based protocol that provides Standard, Premium and Flash based

messages, all with configurable Transaction Verification. Though SMS does not

provide the multi-channel capability and real-time conversational functionality

of voice services, it is a simple delivery mechanism for alerts, OTP’s (One Time

Passcodes) and lower priority messages, and provides a migration path strategy

for organizations wishing to extend their existing SMS based solutions.

§ VALid-SVP stands for Speaker

Verification Platform and is the biometric voice verification capability of the

VALid® platform. The VALid-SVP solution is based on a completely modular,

plug-in based architecture that allows organizations to integrate their existing

or preferred biometric engines into the VALid® framework. VALid-SVP supports

text-dependent, text-independent and conversational voice verification models,

all deliverable over multiple electronic channels. ValidSoft’s own biometric

voice verification engine is based on Alize, a state-of-the-art speaker

verification platform developed in the European Union.

§ VALid-TDS is the Transaction

Data Signing capability of VALid®, crucial in the provision of Non-Repudiation

for Internet based financial transactions. VALid-TDS cryptographically ties the

One Time Passcode (OTP) to the underlying transaction, as distinct to a randomly

generated OTP. This enables the underlying transaction detail to be determined

through the code, critical in proving or disproving transaction

repudiation. VALid-TDS also interoperates with external tamper

evident stores, storing the encrypted transaction data, authentication details

and real-time call recording for further use in Non-Repudiation.

8

§ VALid-POS® is the Card-Present

fraud prevention solution from ValidSoft. VALid-POS® targets one of the fastest

growing fraud threats; card skimming. VALid-POS® combines the functionality of

VALid’s real-time Out-of-Band transaction verification capability with proximity

based mathematical models that assists banks in determining whether the genuine

customer is conducting the card-based transaction. Where in doubt, VALid® can

contact the customer and resolve the potential threat in real-time, providing

massive advantages to bank and their customers alike.

§ VALid-ARM stands for Advanced

Risk Management and provides organizations with a suite of tools to enhance

their fraud prevention capability and increase the effectiveness of their risk

management function. Included within VALid-ARM is the Risk Adjusted Rules Engine

(RARE), real-time alerting, Panic-PIN, advanced voice analysis techniques such

as voice pattern analysis and VALid’s proximity correlation tool

VALid-POS.

§ VALid-TTS - The pluggable

Text-to-Speech option that can run in parallel with a WAV based voice service or

replace it completely. VALid-TTS enables organizations to apply Transaction

Integrity Verification (TIV) to totally dynamic data such as individual or

company names and address information. A classic example of a manual

transaction that could be enabled for the web is an Address Change, where

VALid-TTS would be used to perform the TIV function on the actual address

detail.

§ VALid-VPN - The Virtual

Private Network client that allows users to gain secure remote access to an

organization’s protected network. Remote network access is becoming a greater

issue for many organizations through the growth of home working, remote workers,

extended enterprise and disaster recovery and business disruption planning.

VALid-VPN supports most of the major remote access solution providers, including

Citrix, Juniper, Checkpoint and Cisco. The VALid-VPN solution has

been designing as a generic solution enabling simple, low-cost integration into

additional remote access technologies and providers, should this be

necessary.

§ VALid-ISA - VALid’s ISA

integration provides secure access to applications accessed through ISA, e.g.

Microsoft OWA. Currently many companies disallow remote access to ISA hosted

applications (e.g. OWA) due to security concerns. VALid-ISA solves this problem

and, through its zero client-footprint model, enables instant wide scale

distribution. VALid-ISA also enables one secure point of access to

any number of web based application sitting behind ISA.

§ VALid-FOB (Disconnected Model)

– The mobile phone or PDA based VALid® client option for customers who may not

have regular access to a telecommunications signal, either mobile or landline,

but who do have access to the Internet. VALid-FOB is a J2ME (Java) based

application that can be downloaded to the mobile phone or PDA and be used to

provide Authentication, Mutual Authentication and Transaction Data Signing

functions in contingency situations.

Products

and Markets

Full

MVNE

We are

positioning ourselves as a complete MVNE with our own integrated platforms,

switches and network capabilities for back-office and customer interaction

solutions. The back-office services range from provisioning and administration

to Operation Service Support (“OSS”) and Business Service Support (“BSS”)

running on our global IN/CRM/Billing platform “ET BOSS”. Our “ET BOSS” platform

is designed to provide an all-in-one solution for both the traditional MNO’s:

(i) the operators of vast Antenna Networks and (ii) managers of wireless

spectrum granted through licenses by national governments, as well as for

MVNO’s. MVNO’s are generally fast-moving sales and marketing

companies reselling refocused, re-priced, re-bundled and repackaged mobile

telecom services. We partner with MNO’s to bypass their legacy systems to

profitably accommodate these wholesale MVNO customers with service levels and

applications that satisfy the instant service flexibility, and pricing

capability that MVNO’s require to specifically address their niche

markets. At the same time, we can offer additional market share to

MNO’s by marketing and contracting our own range of MVNO’s that look for the

very specific capabilities that our mobile service delivery platforms may offer.

Bundled together with attractively priced wholesale airtime packages provided by

our MNO partners, our MVNO’s are positioned to run their operations effortlessly

without the technical and financial burden associated with the development,

maintenance and ownership of their own mobile network, while at the same time

focusing on sales, marketing and distribution and the application of all

elements required to be successful in these rapidly evolving consumer

markets.

9

These

in-depth MVNE (Mobile Virtual Network Enabler) platform services are now fully

operational in The Netherlands as of the end of the third quarter of 2008 and

operational in Spain since June 2009.

For

companies that aspire to enter the mobile telephone market, the MVNO business

model is attractive because it eliminates the expenses associated with

establishing and managing a mobile network of their own. The initial

capital expenditures required to enter the field are very low, as are the

corresponding operational costs. Traditionally MNO and MVNO propositions

required substantial capital and operational expenditures and attention to

multiple technical components. Our business model offers a solution for MVNO’s,

which allows them to concentrate on sales and marketing, and which allows MNO’s

to cater to often smaller, niche market MVNO’s without the cumbersome burden of

their legacy systems and other resources, which are not designed to efficiently

service such wholesale customers.

In

addition to more traditional voice and SMS services, we are focusing our MVNE

platform on wireless data services, content, applications and E-commerce. The

traditional voice services of MVNO’s are likely to be marginalized over time and

will follow a similar price erosion pattern as landline telecom services.

Therefore, it is unlikely MVNO’s will be able to effectively compete over time

without value-added services. Moreover, the emerging market of 3G/3.5/4G mobile

services, including WIFI, WIMAX and LTE, create great opportunities to attract

new subscribers with new and improved business models. Mobile devices

are an effective medium to communicate commercial messages to subscribers,

especially if supported by proper customer profiling tools in combination with

our IN/CRM/Billing platform “ET BOSS”. Mobile messages can be personalized per

subscriber becoming contextually relevant, and thereby migrate from being

perceived as intruding advertising to meaningful information, segmented within

the client base or just to be used as a mass communication means. A mobile

device is one of the most personal communication tools to connect with and

stimulate customers, thus an MVNO channel might offer excellent opportunities to

a variety of companies with a non-telecommunication core business, such as fast

moving consumer goods companies looking to expand and broaden their markets,

while at the same time creating focused marketing communication channels with

their existing customer bases, providing these contextual services that, we

believe, will be perceived as adding value to communications. We are well

positioned to provide such market entrants with a one stop, full service and

instantly available platform to effectively cater to these markets, and thereby

support any application that might help our customers to quickly offer a truly

differentiating service into the marketplace. We believe that many new business

models, especially within Security, Logistics, Heath Care and Banking, will

become viable through a networked environment, thereby helping such businesses

to enter such models without having to go through yearlong learning cycles to

understand, master and manage all the relevant technologies. We are positioning

ourselves as the enabling partner for all these new entrants, whereby we will

cover all these elements on their behalf, coach and guide them and deliver all

the tools these future business partners may require to drive these new business

models successfully.

Through

an integrated platform built around our network we offer our customers a turnkey

solution for both pre-paid and post-paid mobile services, as well as more

traditional landline telecommunication services like toll free, shared cost and

premium rate services, supported by content & payment provisioning

systems.

Our

global network enables our customers to distribute all their information in a

fully managed environment that we believe is more secure than the Internet.

Together with a fully integrated back office system, we are opening up these

networked platforms to our B2B customers, providing them with an efficient and

effective tool designed to substantially improve their productivity.

Additionally, through a customer friendly, web-based interface, our customers

may run these networked delivery platforms as if they were their own. This

feature will allow our B2B customers to see mobile, landline, Internet, WiFi,

WiMax and local, regional or multi-country, as just one integrated network, with

all of the advantages of one single network interface, centralized customer

recognition and financial controls.

With the

support of our back office system combined with our integrated “ET BOSS” system,

we believe our B2B customers have all the necessary tools to create their own

virtual telecom business environment; thereby enabling our customers to

recognize and serve their own clients, employees, partners or affiliates through

any device, at any place and at any time. Our vision is that access to our

global network will revolve around our central data and information base, which

will allow our customers to provide their clients with worldwide access

authorization to our services through a familiar interface and/or workplace,

preferred format and language.

10

As a

consequence of the above, we are positioning ourselves as the preferred telecom

outsourcing partner to all of our B2B customers. These long term business

partners include a wide variety of marketing organizations and content providers

who fundamentally require telecommunications services to drive their own revenue

and growth, and as a necessary element of their overall product, market and

distribution offering. We empower our partners as if they are a fully networked

telecommunications company themselves, by providing them with all the tools and

resources necessary to manage their businesses, particularly the

telecommunications segment, as an integrated component of their overall

offering. Additionally, and for many reasons both strategic and financial in

nature, we see an increasing interest by other telecom companies to partner with

us to easily expand their geographical footprint or services offered, without

first having to commit to substantial telecom and IT related capital and

operational expenditures.

Customized

Mobile Solutions – ValidSoft Fraud prevention and security

solutions

The

essence of the ValidSoft product suite is in providing:

■ Card-Present fraud prevention and

resolution – Card Skimming is one of the fastest growing fraud threats.

In the UK, this type of fraud in 2007 accounted for over half a billion pounds,

and in the US, a leading research company is predicting that the cost of plastic

card fraud will rise from 25 basis points to over 150 basis points over the next

12 to 18 months. VALid-POS combines the functionality of VALid’s real-time

Out-of-Band transaction verification capability with proximity based

mathematical models that assists Issuing Banks in determining whether the

genuine customer is conducting the card-based transaction. Where in

doubt, VALid® can contact the customer and resolve the potential threat in

real-time.

§ Card-not-Present fraud prevention and

resolution – Card-not-Present fraud, i.e. fraud associated with online

retailing, is a significant problem worldwide. The vast majority of this type of

fraud involves the use of card details that have been fraudulently obtained

through methods such as skimming, data hacking or through unsolicited emails or

telephone calls. The card details are then used to make fraudulent

card-not-present transactions, most commonly via the Internet. As the number of

Internet retailers has grown, fraudsters have increasingly targeted the online

shopping environment. The global cost of this type of fraud is estimated at over

$5 billion globally. VALid-POS combines the functionality of VALid’s real-time

Out-of-Band transaction verification capability with proximity based

mathematical models that assists retail providers in determining whether the

genuine customer is conducting the online transaction. Where in doubt, VALid®

can contact the customer and resolve the potential threat in

real-time.

§ Online Banking fraud

prevention – Online banking fraud is a significant threat to the take-up

of online banking worldwide. Fears concerning the safety of this type of banking

transactions prevent banks from realizing the massive cost savings provided by

self-service online banking. Globally less than 50% of internet users bank

online and security fears remain the primary inhibitor of

take-up. VALid’s real-time Out-of-Band strong mutual authentication

and real-time transaction verification enables the bank to apply a real-time

dynamic rules engine to identify anomalies and to contact the customer and

verify the transaction in real-time.

§ Strong Mutual Authentication

(multi-channel) – the need for the customer to know that the bank is

genuine is just as important as the need for the bank to know that it is

transacting with the genuine customer - this is essential in terms of fostering

consumer confidence, the lack of which is the single most significant deterrent

in terms of the adoption of online commerce. This is termed “Mutual

Authentication” and VALid® has one of the most intuitive and strongest forms of

Mutual Authentication available;

■ Transaction Verification (Out-of-Band

– OOB) – even if both parties to a transaction are genuine there is no

guarantee that the transaction will not be corrupted. A “Man-in-the-Middle” or

“Man-in-the-Browser” attack will succeed no matter how strong the authentication

process. Therefore banks need Transaction Verification. Most banks monitor

transactions to identify anomalies. When an exception is detected, banks for the

most part rely on a manual process of contacting the customer by phone to verify

the legitimacy of the transaction – this is expensive and also prone to security

risk itself as the customer is forced to reveal security credentials to unknown

third parties. VALid® addresses this issue since it has the ability to verify

the integrity of transactions in real-time and in a totally automated manner

over a separate telecommunications channel. Real-time OOB Transaction

Verification is regarded by Gartner as the only effective way to protect the

integrity of a transaction carried out on the Internet.

§ Identity Verification – In

mass market and extranet situations, service providers are struggling to find a

solution that does not require the distribution of hardware devices yet provides

strong authentication and transaction verification in a cost effective and

convenient manner. It is likely that going forward service providers will be

expected to comply with increasing regulation in this area. ValidSoft, through

its telephony based architecture enables service providers to implement the

strongest form of mutual authentication and transaction verification available.

Designed specifically for mass markets and extranet situations, VALid® combines

ease-of-use, cost effectiveness and strong security, from challenge response up

to and including conversational voice biometrics, to ensure that service

providers can verify to non-repudiation level if required, the verification of

identity of both internal employees, external contractors and customers who may

have access to sensitive material and also conduct transactions

electronically.

11

■ Non-Repudiation – PKI (Digital

Certificates), long regarded as a form of Non-Repudiation is now vulnerable to

Man-in-the-Browser attacks. This means that PKI can no longer guarantee the

integrity of transactions and therefore can be challenged in a Court of Law

where PKI is presented as a case for Non-Repudiation. VALid® has been designed

to address the issue of Non-Repudiation through its multi-layered approach,

which includes elements such as: Transaction Verification; Transaction Data

Signing (cryptographically linking a One Time Passcode to the underlying

transaction); Voice Biometrics (or OOB challenge/response); Customer

Authorization (Voice Recording) and Geometric Transaction Analysis, to achieve

the highest level of non-repudiation capability, presented to the customer in an

intuitive and easy-to-use manner.

■ Business Enabling – financial

institutions cannot leverage the full power and cost effectiveness of the

Internet as a Business Enabling/Self-Service medium because of security

concerns. Certain transactions requiring branch or telephone banking, or the

completion of paper-based forms with signatures (e.g. Address change), are

considered too high risk for Internet deployment, and as a consequence these

transactions continue to be processed manually resulting in high cost,

inefficiencies, poor quality data and customer inconvenience. VALid®, through

the combination of OOB Strong Mutual Authentication and Transaction

Verification, provides the capability to securely automate today’s manual

processes resulting in: dramatic cost savings; customer empowerment; increasing

the consistency, accuracy, timeliness and security of transactions; and creating

competitive advantage through market differentiation.

Landline

network outsourcing services

Even

though the majority of our investments in the past years have been in (mobile)

software development, mobile related acquisitions and implementing

MNO’s and MVNO’s, our largest revenue stream is currently still generated by our

traditional telecom services like Carrier Select and Carrier Pre-Select

Services, and Toll Free and Premium Rate Services. These services formed the

basis and gave us decade-long experience as an outsourcing partner in the field

of telecommunications services managed by our propriety Intelligent

Network/Customer Provisioning Management/Billing platform. This platform has

always been designed to put our customers, who purposely chose to outsource

their telecommunication requirements to a specialized company like us, in

control: our customers can work with our technology and our delivery platforms

as if these are their own. We empower and likewise facilitate our

customers to harness, to manage and to fully apply the power of some

of the most powerful mobile/landline delivery systems in the world through a

web-based self care user friendly interface, without the need to initiate,

install, fund, operate and support those global systems on a 24/7

basis.

Business

and Growth Strategy for 2010 and Beyond

Elephant

Talk is actively seeking additional MNO partners that understand the symbioses

between a mobile network operator and an applications-focused enabler that

brings the right services in the right format through a secure delivery platform

within reach of all business customers that may require such services as part of

their overall market and product strategy. We believe that over the next couple

of years MNO’s will proactively seek partners like our company, as it will be

the preferred way to successfully expand from retail focused markets to

wholesale markets, thereby more effectively using the capacity of their core

antenna networks and spectrum capabilities.

Especially

in markets where direct retail customer penetration reaches 80% plus levels,

MVNO’s can enhance bring market penetration and network usage levels. However,

only if these MVNO’s are capable of bringing significantly differentiated

service bundles into the market place - reflecting the specific requirements of

individualized communities - will they be less vulnerable to what has been

undermining the MNO’s basic business models: churn. Most important to an

operator’s success is to understand that a uniquely serviced community far

outweighs the pricing alone of any basic underlying service.

12

The

growing importance of converging services is an area where we see excellent

possibilities to combine our decade long in-depth experience in landline

services with our sophisticated mobile delivery platform. This will support both

our MNO as well as our MVNO customers to bring newly bundled services into the

marketplace through a single device that is capable of using landline, IP,

mobile, and wireless connectivity for any voice, data and multi-media

application. All this will be provisioned and managed through one single

customer account and one integrated bill that is supported by any relevant

payment mechanism.

We

see opportunities in customized mobile service, combining the individual profile

of a mobile customer and his or her exact location, with the “always-on” secured

connectivity of a mobile network, supported by our powerful mobile delivery

platforms. We believe these elements will create completely new business models

for MNOs and MVNOs alike, bringing personalized, contextual and time-wise

relevant services to billions of customers worldwide. One can easily think of

new applications in the areas of security, protection and logistics of people,

goods and services, remotely monitoring and escalating medical care,

individualized and contextual marketing communications for broad ranges of goods

and services, and supporting secure financial transactions.

Most

of these new business models, driven by customized mobile services, will be

created and operated by independent third party application providers that may

be directly or indirectly connected to mobile service delivery platforms like

our MVNE platform. In areas we see attractive opportunities to create, operate

and market such services ourselves, we may actively invest in such developments

or may acquire other companies that already have developed such applications. A

good example of such a service is the fraud prevention application that

ValidSoft offers, the company recently acquired by us.

Growth

in Partnerships

As

a result of the convergence of information technology and telecommunications

solutions, our involvement with various partners has increased. On

the supply side, we work with dozens of other carriers and content providers to

either originate or terminate our traffic around the globe. On the customer

side, resellers have evolved from indirect channels to true partners bringing

specialized market knowledge, customer focus and a geographical reach to its

activities.

As

a key element of our low-cost and fast deployment strategy, we make use of

partners in all layers of our distribution platform. Our partners typically come

from the following disciplines:

Landline

Network Interconnect Partners

As

a fully licensed telecommunications carrier, we are entitled to be

interconnected with a variety of incumbent operators and cable companies as well

as more recently established telecom providers in over a dozen countries that

provide both network origination and termination, mostly at regulated

costs.

Mobile

Network Partners

As

a provider of full Mobile Virtual Network Enabling platforms, we partner with

Mobile Network Operators to strongly support them in better addressing the

specific needs of Mobile Virtual Network Operators, the sales, marketing and

distribution organizations that (re)package, (re)bundle and (re)position mobile

telecommunications as part of their overall service offering. Likewise, we help

our partner MNOs to improve the usage of their networks by also directly

contracting additional MVNOs for which we attractively bundle our systems

capabilities with the partner MNO’s airtime.

Content

& Customized Mobile Services Partners

These

partners can have a dual purpose whereby they are both a supplier as well as a

marketing client. Essentially Content and Customized Mobile Services Partners

provide a broad array of content and services available for distribution through

our mobile and landline networks which are then promoted and sold by a variety

of our marketing partners. However, at the same time we may also

generate revenue from such Content and Customized Mobile Services Partners by

providing them with all of the tools required to exploit and promote their

content and services through our delivery platforms.

13

Roaming

& LCR Wholesale Origination/Termination Partners

Our

network is connected to over a dozen wholesale partners that work together on a

commercial basis to provide each other with “Least Cost Routing” and roaming

capabilities to globally originate and terminate landline and mobile calls at

the best possible cost/quality levels.

Management

and Personnel

During

2009 we further strengthened our organization in order to prepare ourselves for

our current operational and revenue growth strategy, especially in the area of

mobile services, by strongly increasing the number of engineers and software

developers to expand our VoIP, Intelligent Network Platform, and Billing-CRM

capabilities. In addition some increases were made in the support and project

management departments.

In

addition to our corporate management staff, as of December 31, 2009, we employed

85 employees. We have retained, on a long term basis, the services of 27

independent contractors. We consider relations with our employees and

contractors to be good. Each of our current employees and contractors has

entered into confidentiality and non-competition agreements with

us.

At

the same time management is attempting to improve the internal structure of the

organization in order to realize a fully integrated organization. This will have

to be achieved not only on a corporate level but also in the financial,

technical and operational departments of the Company in order to implement new

services, connectivity in new countries, and additional capacity.

Competition

We

experience fierce competition in each of the market segments in which we

operate.

Traditional

Telecom Services

In all

segments where we offer traditional telecom services like carrier (pre)

select/dial around/2-stage dialing services, premium rate and toll free

services, we encounter heavy competition. Our stiffest competition comes from

each of the incumbent telecom operators such as BT, France Telecom, KPN,

Telefonica, Telecom Italia and Telekom Austria. The strongest price competition

usually comes from smaller, locally established and/or regional players,

although newer Pan-European carriers like Colt Telecom position themselves as

aggressively priced competition.

Mobile

Services

We

face competition from other MVNE’s, as well as from the traditional

MNO’s.

An

average MNO may have a few dozen technology suppliers; each may deliver a part

of the overall network, switching, control and administrative systems comprising

a mobile carrier’s infrastructure to service millions of retail customers.

Likewise, many companies are aiming to become a vendor/partner of a MNO in order

to assist the MNO to better service their wholesale business towards MVNO’s.

Some companies try to achieve this by selling various core components as a more

traditional vendor: stand alone switching systems, billing systems, CRM systems,

Intelligent Network systems, etc. Examples of our competition in this market are

companies like Highdeal, Comverse, Geneva, Amdocs and Artilium. In such cases

the MNO often contracts with a system integrator like Cap Gemini or Atos Origin

to help them to integrate all these components into effectively working systems.

Recently, more and more of these system integrators not only position themselves

anymore as onetime integrators, but they are also looking to assume the role as

an on-going service providers, keeping (part of) the system up and running on

behalf of the MNO; examples are Cap Gemini, Atos Origin, EDS, Accenture, and

IBM. Likewise, various vendors themselves assumed such roles of managing and

operating the systems they supplied. As such, we also face competition from

traditional telecom infrastructure companies like Nokia-Siemens, Ericsson and

Alcatel.

As a

consequence of these purchasing and outsourcing policies, many MNO’s have over

the years assembled large teams, sometimes as large as a dozen or more

vendors/integrators/service providers, whereby each of them delivers a crucial

part of the overall required capabilities. Not only have such larger teams,

usually involving hundreds of full time consultants, been requiring very intense

vendor management attention from the MNO to coordinate them, the result was

often a very complex operational structure and work environment for both the MNO

as well as the MVNO to work with. Instead of bringing superior, flexible

services at affordable cost levels that were supposed to better position the MNO

to easily go after MVNO business, the MNO is often struck with a whole range of

hard to manage, inflexible and expensive (and sometimes even incompatible)

platforms, that actually undermine the capability of the MNO to successfully and

profitably compete for MVNO business. Existing MVNO’s threaten to migrate to

another network provider, while new prospect are lost to other MNO’s that do

provide more flexible and affordable service.

14

Being

positioned for many years as an outsourcing partner for other businesses that

require telecoms as a part of their overall service offering, we believe we can

assist MNO’s to simplify and streamline these outsourced system requirements.

One of the key elements in our offering in landline telecommunications has

always been that all network, switching, control and administrative elements

would function within one system, and that our B2B customer would be able to

self-manage such system through an easy to use web based interface. In designing

its MVNE platform, our company has kept the same philosophy in place. As a

result, a MNO would only require one managed service provider to fully offer any

possible service requirement any type of MVNO may have. We therefore believe

that we not only eliminate an intense and costly vendor management role, but at

the same time offer flexible, superior service levels at a much lower

operational cost.

Other

companies that have positioned themselves as a MVNE platform provider, aiming to

assume the same role of a one stop solution provider to MNO’s, and as such are

direct competitors of us, include Aspider, primarily active in the Netherlands,

Vistream/Materna, primarily active in Germany, Effortel, primarily active in

Belgium and Italy, Transatel, primarily active in France, Telcordia,

primarily active in North America, Virtel, primarily active in Australia and the

combination Artilium/Atos Origin, active throughout Europe. However, none of

them cover the same depth and width of platform capabilities as Elephant Talk

provides. On top of that, on the supplier/vendor side we believe we compete

favorably with all the earlier mentioned telecom system vendors and integrators.

Even though we believe our company has a very good offering at a competitive

pricing level, many of our competitors may develop a comparable, fully

integrated MVNE platform in the near future. As many of these competitors are

much larger companies than ours, with much higher profiles, it may very well be

that these competitors will successfully sell their higher priced, less capable

solutions than comparable Elephant Talk systems.

Although

we believe we will continue to create excellent opportunities for MNOs to

increase the addressable market they can service profitably, many MNOs may still

prefer to compete directly with us, not only for the business of larger MVNOs,

but also in servicing the many smaller MVNOs. This situation may become more

likely if new technologies make it easier for the MNOs to service both larger

and smaller non-retail customers directly on a lower cost basis. Also, other

MVNEs may create strong competition, especially if such new MVNEs will be

created by competing MNOs as a consequence of our success in profitably

cooperating with other MNOs that already have a successful MVNE relationship

with us.

Fraud

Prediction & Prevention Services

Our

current (ValidSoft) Fraud Prediction & Prevention Services face competition

from Authentify, Strikeforce, Finsphere, Tricipher for Out-of-Band (OBB), RSA,

VASCO and others for Tokens, and Verisign and others for Digital

Certificates.

ValidSoft’s products combined with the

Elephant Talk’s advanced telecommunications platform we believe combine the

complementary strengths which results in a state of the art and currently one of

a kind total solution in payment card (debit and credit) fraud

prevention.

More in

particular for the ValidSoft part, VALid® combines strong authentication and

transaction verification to counter not only the more traditional attacks, but

also the latest in session hijacking (Man-in-the-Middle, Man-in-the-Browser)

through its Transaction Integrity Verification (TIV) model. Alternative two

factor authentication solutions such as hardware tokens are vulnerable to these

types of threats. These vulnerabilities exist due to a number of issues and

weaknesses. VALid® provides flexibility in allowing banks to

authenticate at both the session and transaction level, with the device,

protocol and even authentication behavior completely configurable. Use of the

customers’ existing telephony devices, ensures complete interoperability between

multiple banks, while providing the necessary branding through the use of the

individual bank’s voice scripts. As VALid® supports remote access in a number of

ways it operates in exactly the same manner for internal enterprise access.

Managing conventional Two Factor authentication systems that use physical tokens

carry significant overheads, such as the end user token distribution process

(including retrieval and replacement), synchronization issues and time

sequencing problems. Managing these tokens is also cumbersome as in some cases a

master token must be used before an administrator can de-activate a token.

VALid® does not have these issues and provides banks with the added benefit of a

significant lower Total Cost of Ownership whilst dramatically improving security

levels. A user can be added to the system using an intuitive web based system

resulting in near real time for activation or deactivation.

15

Legal

structure of the company

The

following chart illustrates our company’s corporate structure as of December 31,

2009.

In 2007,

our company grew as a result of the acquisition, effective January 1, 2007, of

Elephant Talk Communication Holding AG (formerly known as “Benoit Telecom

Holding AG”) by Elephant Talk Europe Holding B.V.(the “Benoit Acquisition”).

Please see “Benoit Acquisition” below, for an overview of this transaction. In

addition to the Benoit Acquisition, on June 1, 2007, we acquired a French

entity: 3U Telecom SrL, from 3U Telecom AG, a German company. The name of this

entity was subsequently changed to Elephant Talk Communications France S.A.S.

(“ET France”). As a result of the preceding acquisitions, our corporate

structure and breadth of operations significantly expanded.

In

addition to the aforementioned acquisitions, we incorporated three new companies

in 2007. On May 24, 2007 we established Elephant Talk Global Holding B.V (“ET

Global”), a 100% Dutch subsidiary of ETCI. We created ET Global to act as the

holding company for several of our worldwide subsidiaries. On October 21, 2007

we incorporated Elephant Talk Business Services W.L.L. (“ET Business Services”),

a Bahrain based company, to act as an intra-group service provider outside

Europe (Elephant Talk Communication Carrier Services GmbH performs this activity

within Europe). On December 27, 2007 we formed Elephant Talk Communications

Luxembourg S.A. (“ET Luxembourg”) to initially focus on providing payment

collection services for other group companies. On March 20, 2008 Elephant Talk

Caribbean BV was incorporated in the Netherlands as a 100% subsidiary of

Elephant Talk Global Holding B.V. The purpose of this subsidiary is to act as

the joint venture partner of United Telecommunication Services N.V. in the

entity ET-UTS NV. ET-UTS NV was incorporated in Curacao, the Netherland

Antilles, on April 9, 2008 as a 51% subsidiary of Elephant Talk Caribbean B.V.

with the remaining 49% owned by our joint venture partner United

Telecommunication Services N.V. The total issued capital amounts to one hundred

thousand dollars ($100,000.00). The purpose of ET-UTS NV is to design, install,

maintain and exploit WIFI and WIMAX networks in the Caribbean area and

Surinam.

16

On August

14, 2008 we changed the name of Cardnet Clearing Services BV, a wholly-owned

affiliate of Elephant Talk Europe Holding BV, to Elephant Talk Mobile Services

BV. This company’s primary objective is to act as our vehicle to contract Mobile

Virtual Network Operators in the Netherlands. On August 20, 2008 Elephant Talk

Europe Holding BV signed an agreement for the acquisition of 100% of Moba

Consulting Services BV. The effective date of the transaction was

September 1, 2008 at an acquisition price of €1.00 plus 50,000 of our stock

options. We acquired Moba Consulting Services BV to obtain expertise and

manpower for certain aspects of the implementation of the Mobile Virtual Network

Operators on our platform.

Benoit

Acquisition

On

January 17, 2005, we entered into a Memorandum of Understanding with Beltrust

AG, a corporation organized and existing under the laws of Switzerland

(“Beltrust”), to acquire all of the issued and outstanding shares of Benoit

Telecom Holding AG, a corporation organized and existing under the laws of

Switzerland (“Benoit Telecom”). Benoit Telecom is a European-based telecom

company. On November 17, 2006, we executed an Agreement of Purchase and Sale

(the “Beltrust Agreement”), with Beltrust and Elephant Talk Europe Holding B.V.

(“ET Europe”), a corporation organized and existing under the laws of The

Netherlands, and our wholly owned subsidiary, providing for the purchase and

sale of all of the issued and outstanding shares of Benoit Telecom by ET Europe.

Pursuant to the Beltrust Agreement, ET Europe agreed to purchase from Beltrust

all of the 100,000 issued and outstanding shares of Benoit Telecom, in exchange

for a) cash payment of $6,643,080 and b) 40,000,000 shares of our common

stock.

ITEM

1A. RISK FACTORS

Risks

Related to Our Company

Our

substantial and continuing losses, coupled with significant ongoing operating

expenses, raise doubt about our ability to continue as a going

concern.

We have

incurred net losses of $17,299,884 and $16,015,359 for the years ended December

31, 2009 and 2008, respectively. As of December 31, 2009, we had an accumulated

deficit of $62,335,076 which has resulted in our need to raise capital via a

private placement offering in 2009 and subsequent bridge loans in 2010. In 2009,

through this offering $12.3 million gross was raised, with $6.08 million from

related parties.

Such

losses will continue during 2010 due to ongoing operating expenses in new Mobile

services and a lack of revenues sufficient to offset operating expenses plus the

need to fund the future development to satisfy our potential customers’ needs.

We have raised and continue to raise capital to fund ongoing operations by

private sales of our securities, some of which sales have been highly dilutive

and involve considerable expense, and will continue to do so provided market

conditions allow us.

In our

present circumstances there is substantial doubt about our ability to continue

as a going concern absent significant sales of our products and