Attached files

| file | filename |

|---|---|

| EX-3.2 - EX-3.2 - WESTWATER RESOURCES, INC. | a09-35906_1ex3d2.htm |

| EX-32.1 - EX-32.1 - WESTWATER RESOURCES, INC. | a09-35906_1ex32d1.htm |

| EX-23.2 - EX-23.2 - WESTWATER RESOURCES, INC. | a09-35906_1ex23d2.htm |

| EX-23.1 - EX-23.1 - WESTWATER RESOURCES, INC. | a09-35906_1ex23d1.htm |

| EX-31.2 - EX-31.2 - WESTWATER RESOURCES, INC. | a09-35906_1ex31d2.htm |

| EX-32.2 - EX-32.2 - WESTWATER RESOURCES, INC. | a09-35906_1ex32d2.htm |

| EX-31.1 - EX-31.1 - WESTWATER RESOURCES, INC. | a09-35906_1ex31d1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-33404

URANIUM RESOURCES, INC.

(Exact name of Registrant as specified in its charter)

|

DELAWARE |

|

75-2212772 |

|

(State of Incorporation) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

405 State Highway Bypass 121, |

|

|

|

Building A, Suite 110 |

|

|

|

Lewisville, Texas |

|

75067 |

|

(Address of principal executive offices) |

|

(Zip code) |

(972) 219-3330

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value

per share

(Title of class)

Indicate by check mark if the Registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceeding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o |

Accelerated filer x |

|

|

|

|

Non-accelerated filer o |

Smaller reporting company o |

|

(Do not check if a smaller reporting company) |

|

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the Common Stock held by non-affiliates of the Registrant at June 30, 2009, was approximately $61,457,206. Number of shares of Common Stock, $0.001 par value, outstanding as of March 12, 2010: 56,847,612 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III of this Form 10-K report are incorporated by reference to the Registrant’s Definitive Proxy Statement for the Registrant’s 2009 Annual Meeting of Stockholders.

URANIUM RESOURCES, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2009

|

1 |

|

|

|

|

|

1 |

|

|

|

|

|

1 |

|

|

|

|

|

1 |

|

|

|

|

|

1 |

|

|

|

|

|

2 |

|

|

|

|

|

2 |

|

|

|

|

|

3 |

|

|

|

|

|

3 |

|

|

|

|

|

4 |

|

|

|

|

|

5 |

|

|

|

|

|

5 |

|

|

|

|

|

6 |

|

|

|

|

|

7 |

|

|

|

|

|

8 |

|

|

|

|

|

8 |

|

|

|

|

|

9 |

|

|

|

|

|

9 |

|

|

|

|

|

9 |

|

|

|

|

|

9 |

|

|

|

|

|

14 |

|

|

|

|

|

15 |

|

|

|

|

|

15 |

|

|

|

|

|

22 |

|

|

|

|

|

31 |

|

|

|

|

|

31 |

|

|

|

|

|

32 |

|

|

|

|

|

32 |

|

|

|

|

|

32 |

|

|

|

|

|

33 |

|

|

|

|

|

33 |

|

|

|

|

|

Kingsville Dome Production Disposal Well Permit Renewals and Area Authorization 3 |

33 |

|

|

|

|

34 |

|

|

|

|

|

34 |

|

|

|

|

|

34 |

|

|

|

|

|

35 |

|

|

|

|

|

35 |

|

|

|

|

|

36 |

|

|

|

|

|

36 |

|

|

|

|

|

37 |

|

|

|

|

|

Securities Authorized for Issuance Under Equity Compensation Plans |

37 |

|

|

|

|

38 |

|

|

|

|

|

38 |

The “Company” or “Registrant” or “URI” is used in this report to refer to Uranium Resources, Inc. and its consolidated subsidiaries. This 10-K contains “forward-looking statements.” These statements include, without limitation, statements relating to management’s expectations regarding the Company’s ability to remain solvent, capital requirements, mineralized materials, timing of receipt of mining permits, production capacity of mining operations planned for properties in South Texas and New Mexico and planned dates for commencement of production at such properties, business strategies and other plans and objectives of the Company’s management for future operations and activities and other such matters. The words “believes,” “plans,” “intends,” “strategy,” “projects,” “targets,” or “anticipates” and similar expressions identify forward-looking statements. The Company does not undertake to update, revise or correct any of the forward-looking information. Readers are cautioned that such forward-looking statements should be read in conjunction with the Company’s disclosures under the heading: “Risk Factors” beginning on page 9.

Certain terms used in this Form 10-K and other industry terms are defined in the “Glossary of Certain Terms” appearing at the end of Part I hereto.

Uranium Resources, Inc. (URI) is a uranium exploration, mine development and production company. We were organized in 1977 to acquire and develop uranium mines in South Texas using the in-situ recovery mining process (ISR). Since its founding, URI has produced over 8 million pounds U3O8 from five Texas projects, two of which have been fully restored and returned to the land owners. The Company currently has two fully licensed ISR processing facilities in Texas: Kingsville Dome and Rosita. Since 1986, the Company has built a significant asset base in New Mexico that includes 101.4 million pounds U3O8 of in-place mineralized uranium material on 183,000 acres of uranium mineral holdings. We have also been issued a Nuclear Regulatory Commission (NRC) license to build a 3 million pound U3O8 per year ISR processing facility at Crownpoint, New Mexico. As of March 12, 2010 we had 30 employees.

URI holds a NRC source materials license to build and operate an ISR uranium processing facility on company-owned property at Crownpoint, New Mexico. The license allows for ISR mining at the Churchrock and Crownpoint projects that together hold nearly 34 million pounds U3O8 of in-place mineralized uranium material. The license allows for the production of up to 1 million pounds per year from Churchrock until a successful commercial demonstration of restoration is made; after which the quantity of production can be increased and mining on other properties can begin. Total production under the license is limited to 3 million pounds U3O8 per year. This project is currently being delayed due to depressed uranium prices and by a lawsuit to determine whether the U.S. Environmental Protection Agency (“USEPA”) or the State of New Mexico has the jurisdiction to issue the Underground Injection Control (UIC) program permits. The Company believes production could begin within 18 - 24 months after obtaining this permit assuming the market for uranium improves.

Overall in New Mexico, the Company owns 183,000 acres of mineral holdings that contain approximately 101.4 million pounds U3O8 of in-place mineralized uranium material that has been verified by an independent engineering firm. A substantial amount of our total acreage remains unexplored or currently has insufficient data to estimate in-place mineralized materials. These properties were acquired during the 1980s and 1990s along with a vast database of exploration logs and drill results that were developed by Conoco, Homestake Mining, Mobil Oil, Kerr-McGee, Phillips Petroleum, United Nuclear and Westinghouse Electric Corporation. Three of our properties were in various stages of being developed as conventional underground mines in the early 1980s with a total designed capacity to produce approximately 4.5 million pounds U3O8 per year. We also possess a 16.5% royalty interest on a partial section of the Mount Taylor Mine owned by Rio Grande Resources, a division of General Atomics.

Since 2007, we have digitized approximately 18,800 drill logs in order to secure the data and allow for easier analysis of drill hole information. These logs total nearly 23 million feet of hole drilled in the 1970s and 1980s with an estimated drilling and logging replacement cost of $700 million.

The Company plans to develop its uranium assets in New Mexico using the most economic and efficient method for each project and will be subject to improvements in uranium prices. These mining methods may include the use of ISR, old stope leaching, and conventional mining techniques.

Texas Production History and Current Status

The Company developed and produced over 560,000 pounds U3O8 from the Longoria and Benavides projects in the early 1980s. These properties were fully restored between 1986 and 1991. From 1988 through 1999, we produced approximately 6.1 million pounds U3O8 from two South Texas projects: 3.5 million pounds from the Kingsville Dome project and 2.6 million pounds U3O8 from the Rosita project. In 1999, we shut-down production at both projects due to depressed uranium prices. We had no revenue from

uranium sales between 2000 and the fourth quarter of 2004, and therefore had to rely on equity infusions to fund operations and maintain our critical employees and assets.

After uranium prices rose significantly in 2004, we placed our South Texas Vasquez property into production during the fourth quarter of that year. In April 2006, Kingsville Dome returned to production followed by a startup of Rosita in June 2008. From 2004 to the end of 2009, these three projects produced a total of 1.4 million pounds of U3O8.

The Vasquez project was mined out in 2008 and is now being restored. Rosita production was shut-in in October 2008 due to depressed pricing and technical challenges in the first new wellfield that made mining uneconomical. The decline in uranium prices throughout 2008 also led to a decision in October 2008 to defer new wellfield development at Rosita and Kingsville Dome. Production continued in two existing wellfields at Kingsville Dome and was completed in July 2009. The Company has not had any operating mines in Texas since that time, and does not plan to return to production until uranium prices recover.

The Company believes it has sufficient in-place mineralized uranium material to produce a total of 300,000 to 500,000 pounds U3O8 over a one to two year period should realized uranium prices recover to a profitable level. Production could begin within 6 - 12 months after a decision to restart is made. Longer-term, additional production could come from new production area authorizations at Kingsville Dome, however, this may take a considerable period of time given local opposition and there can be no assurance that such production will be realized.

On March 6, 2009, URI received notification from Itochu Corporation (“Itochu”) terminating URI’s joint venture with Itochu to develop our Churchrock property in New Mexico. The Joint Venture provided Itochu an opportunity to participate in New Mexico uranium production in exchange for renegotiating their sales contract with the Company. The contract had also included a provision that allowed the Company to receive up to an additional $2.10 per pound for certain South Texas uranium production sold to Itochu from 2006 through the termination of the Joint Venture on March 6, 2009.

As a result of the termination of the joint venture, URI now retains 100% ownership of the 18.6 million pounds of in place mineralized uranium material subject to applicable royalties based on sales at Churchrock. However we presently have no committed source of financing for development of this project.

On April 17, 2009, a three-judge panel of the United States Court of Appeals for the Tenth Circuit affirmed the USEPA decision and held that Section 8 of URI’s Churchrock property in New Mexico is Indian Country. One of the members of the panel dissented. The Company petitioned the Tenth Circuit for and was granted an en banc review of the panel’s decision. Oral arguments were presented to the Court on January 12, 2010 and we are waiting for the Court to render a decision.

In July, 2009, URI entered into a definitive agreement to purchase from NZ Uranium, LLC (NZU) 113,000 acres of mineral rights in the Crownpoint area of New Mexico, however in September, 2009, the agreement for the acquisition was terminated because of the existence of title issues that were not resolved.

On September 3, 2009, David N. Clark stepped down as the President and Chief Executive Officer and a Director of the Company. At that time, the Board appointed Donald C. Ewigleben as President, CEO and COO to succeed Mr. Clark and also named Mr. Ewigleben as a director to fill the vacancy on the Board created by Mr. Clark’s resignation.

In October 2009, the New Mexico Mining and Minerals Division approved the Company’s request for a renewal of the Minimal Impact Exploration Permit Application on its Section 13 in-situ (ISR) exploration project. Section 13 is in Ambrosia Lake (See New Mexico Properties-Potential ISR and OSL areas), the historic mining district near Grants, New Mexico. The permit allows URI to drill up to 10 holes for the purpose of extracting core samples to evaluate the suitability of the property for ISR mining and we intend to perform these drilling activities within the current permitting period. URI owns the Section 13 property in fee and the permit renewal is now valid until November 2010.

The Company produced 59,000 pounds U3O8 in 2009 primarily from our Kingsville Dome project. This production was sourced from the two remaining Kingsville Dome operating wellfields as we had shut in production at Rosita and produced out the Vasquez project at the end of 2008. The Company’s focus in 2009 was on restoration activities at Vasquez, Kingsville Dome and Rosita. Full scale restoration activities of the groundwater at the Vasquez project commenced in the 4th quarter of 2008 and substantial progress has been made towards completion of the groundwater restoration. At Kingsville Dome, the Company has been conducting full-scale

restoration in Production Areas (“PA”) #1 and #2 and began pre-restoration preparations on PA#3 in the 3rd quarter of 2009. Full-scale restoration in the fully depleted wellfields of PA#3 is expected to begin in the 1st quarter of 2010.

The Company in conjunction with the Kenedy Memorial Foundation (the “Foundation”), conducted testing on 165 water wells on a portion of the Kenedy Ranch, located in South Texas for the presence of radium and radon to determine if there is a potential for uranium mineralization. These tests were conducted in 2009, the results have been evaluated and the Company is in the process of presenting the findings to the Foundation.

The Company is also working with Texas A&M-Kingsville to evaluate the use of dissolved hydrogen to enhance bioremediation of mined zones at Kingsville Dome. A test was completed on a small portion of a previously mined wellfield at Kingsville Dome in 2009. The analysis of the test results is ongoing and is expected to be completed by the end of 2010. We are also working with other active ISR mining companies as well as several government labs and agencies including Sandia National Laboratory, Los Alamos National Laboratory and the United States Geological Service, on methods to improve the efficiency of groundwater restoration at ISR wellfields.

During 2009, our focus in New Mexico was on government and public relations activities needed to advance toward production at all of our projects, with our fully licensed Churchrock mine of the Crownpoint Project as a priority. The Company also undertook a study with the Navajo Nation EPA to perform a comprehensive environmental characterization of the Churchrock mine site at Section 17 and lands adjacent to the site area. This study was completed in September 2009 and concluded that any off-site mine-related impacts at Section 17 and adjacent lands are expected to be minor. We will continue to work with the Navajo Nation in this endeavor to achieve the remediation objectives.

The Company has adopted a new strategic plan which emphasizes cash preservation as its priority. The Company is committed to seeking sources of near to mid-term sources of capital to provide sufficient working capital for the Company to maintain its liquidity through at least 2011. The strategic plan also includes the development of options for unlocking potential value for shareholders by utilizing the Companys current assets and by evaluating possible regional and structural synergies. Key operational points of the strategic plan for our Texas properties include (1) positioning the Company to return to production in Texas should the price of uranium return to a level sufficient to generate positive cash flow; (2) complete an analysis of the exploration potential in South Texas and enhance the Company’s exploration capabilities; (3) continue to maintain our restoration activities in South Texas in accordance with the Company’s existing agreements and regulatory requirements and (4) analyze any synergistic opportunities and potential asset monetization prospects in Texas.

In New Mexico, our strategic plan calls for continuing to advance our discussions with others in the region that also hold uranium assets, as well as with entities that would benefit from the production of the uranium. In addition, we will continue our communication efforts with the local communities, State and local governments and the Navajo Nation to address legacy issues while continuing education efforts on the safety of today’s uranium mining practices with the objective of bridging the gap that currently exists between uranium mining entities and others with stakeholder interests in the State.

Uranium Reserves/Mineralized Material

In accordance with the SEC’s Guideline on Non-Reserve Mineralized Material, and as shown in the following table, we estimate 101.4 million pounds of in-place mineralized uranium material on our New Mexico properties as of December 31, 2009. This estimate reflects our ongoing reevaluation of our New Mexico properties, including our decision to consider development of certain properties by conventional mining and milling methods in addition to ISR methods. The estimate for each New Mexico property is based on studies and geologic reports prepared by prior owners, along with studies and reports prepared by geologists engaged by the Company. The estimates presented below were reviewed and affirmed by Behre Dolbear & Company (USA) an independent private engineering firm in their report dated February 26, 2008. Since the date of the report, the Company has maintained its ownership position on these properties, the properties have not been subject to any production activities and the estimates remain unchanged.

SUMMARY OF IN-PLACE NON-RESERVE MINERALIZED

MATERIAL IN NEW MEXICO

|

Property |

|

Tonnage |

|

Grade |

|

Non-Reserve |

|

|

Mancos |

|

5.2 |

|

0.11 |

% |

11.3 |

|

|

Churchrock |

|

7.8 |

|

0.12 |

% |

18.6 |

|

|

Nose Rock |

|

7.6 |

|

0.15 |

% |

21.9 |

|

|

West Largo |

|

2.8 |

|

0.30 |

% |

17.2 |

|

|

Roca Honda |

|

3.9 |

|

0.19 |

% |

14.7 |

|

|

Crownpoint |

|

4.8 |

|

0.16 |

% |

15.3 |

|

|

Ambrosia Lake |

|

0.71 |

|

0.17 |

% |

2.4 |

|

|

|

|

|

|

Total |

|

101.4 |

|

The following table summarizes our estimates of Proven Reserves for our Kingsville Dome and Rosita properties in South Texas. These estimates have been produced by the Company’s professional engineering and geologic staff.

SUMMARY OF IN-PLACE RESERVES IN SOUTH TEXAS

|

Property |

|

Tonnage |

|

Grade |

|

Proven Uranium Reserves |

|

|

Kingsville Dome |

|

0.033 |

|

0.075 |

% |

0.050 |

|

|

Rosita |

|

0.138 |

|

0.081 |

% |

0.224 |

|

|

|

|

|

|

Total |

|

0.274 |

|

Prior to March 2006 we had two contracts with Itochu Corporation and two with UG USA, Inc. Under those contracts we were obligated to deliver an aggregate of 600,000 pounds in each of the years 2005 through 2008, and the buyer had the right to increase or decrease those deliveries by 15%. The average price for such deliveries was $17.95 per pound in 2005 and was anticipated to have been $14.58 per pound in 2006. These contracts were entered into at a time when the spot price for uranium was less than $15 per pound, substantially below the $40 per pound in effect as of March 25, 2006. Two other contracts with these buyers called for aggregate deliveries of 645,000 pounds by December 31, 2007 priced at the spot price at the time of delivery less an average of $3.80 per pound.

In March 2006 we entered into new contracts with Itochu and UG that superseded the existing contracts. Each of the new contracts calls for delivery of one-half of our actual production from our Vasquez property and other properties in Texas currently owned or hereafter acquired by the Company (excluding certain large potential exploration plays). The terms of these new contracts are summarized below.

The Itochu Contract. Under the Itochu contract all production from the Vasquez property will be sold at a price equal to the average spot price for the eight weeks prior to the date of delivery less $6.50 per pound, with a floor for the spot price of $37.00 per pound and a ceiling of $46.50 per pound. Other Texas production will be sold at a price equal to the average spot price for the eight weeks prior to the date of delivery less $7.50 per pound, with a floor for the spot price of $37.00 per pound and a ceiling of $43.00 per pound. On non-Vasquez production the price paid will be increased by 30% of the difference between the actual spot price and the $43.00 ceiling up to and including $50.00 per pound. If the spot price is over $50.00 per pound, the price on all Texas production will be increased by 50% of such excess. The floor and ceiling and sharing arrangement over the ceiling applies to 3.65 million pounds of deliveries, after which there is no floor or ceiling. Itochu has the right to cancel any deliveries on six-month’s notice. Since the inception of the new contract through December 31, 2009 we have delivered approximately 510,000 pounds to Itochu.

On December 5, 2006, HRI-Churchrock, Inc., a wholly-owned subsidiary of the Company, entered into an agreement with a wholly-owned subsidiary of Itochu to develop jointly our Churchrock property in New Mexico (the “Joint Venture”). This agreement was terminated on March 6, 2009. (See “Business—Joint Venture for Churchrock Property”, below).

The UG Contract. Under the UG contract all production from the Vasquez property and other Texas production will be sold at a price equal to the month-end long-term contract price for the second month prior to the month of delivery less $6 per pound until (i) 600,000 pounds have been sold in a particular delivery year and (ii) an aggregate of 3 million pounds of uranium has been sold. After the 600,000 pounds in any year and 3 million pounds total have been sold, UG will have a right of first refusal to purchase other Texas production at a price equal to the average spot price for a period prior to the date of delivery less 4%. In consideration of UG’s agreement to restructure its previously existing contract, we paid UG $12 million in cash with funds raised in our equity offering

completed in April 2006. Since the inception of the new contract through December 31, 2009 we have delivered approximately 482,000 pounds to UG.

Joint Venture for Churchrock Property

On December 5, 2006, HRI-Churchrock, Inc., a wholly-owned subsidiary of the Company, entered into a Joint Venture with a wholly-owned subsidiary of Itochu to develop jointly our Churchrock property in New Mexico. The Joint Venture provided Itochu an opportunity to participate in New Mexico uranium production in exchange for renegotiating their sales contract with the Company. The new contract included a provision to allow the Company to receive up to an additional $2.10 per pound for certain South Texas uranium production sold to Itochu.

A feasibility study was completed and delivered at the end of 2006 at a cost of $675,000 that was funded by Itochu. Under the terms of the Joint Venture, both parties had until April 2, 2007 to make a decision regarding whether to move forward with the Joint Venture. That date was ultimately extended until March 2, 2009.

On March 6, 2009 we received notification that Itochu had decided to terminate the Joint Venture. This eliminated the potential for reinstatement of the original delivery contracts with Itochu for South Texas production. However, depending on spot market prices, our sales price may be reduced by up to $2.10 per pound on some of our South Texas production for future deliveries under the Itochu contract. As a result of the termination of the joint venture, the Company now retains 100% ownership of the 18.6 millions pounds of in place mineralized uranium material subject to applicable royalties based on sales at Churchrock. However, we presently have no committed source of financing for development of this project.

Overview of the Uranium Industry

The only significant commercial use for uranium is as a fuel for nuclear power plants for the generation of electricity. According to the World Nuclear Association (“WNA”), as of February 2010 there were 436 nuclear power plants operating in the world with an annual consumption of about 162 million pounds of uranium. In addition, the WNA lists 53 reactors under construction, 142 being planned, and 327 being proposed.

Based on reports by Ux Consulting Company, LLC, or Ux, the preliminary estimate for worldwide production of uranium in 2009 is 120 million pounds. Ux reported that the gap between production and demand was filled by secondary supplies, such as inventories held by governments, utilities and others in the fuel cycle, including the highly enriched uranium, or HEU, inventories which are a result of the agreement between the US and Russia to blend down nuclear warheads. These secondary supplies are currently meeting nearly a third of worldwide demand, but are depleting.

Spot market prices rose from $21.00 per pound in January 2005 to a high of $136.00 per pound in June 2007 in anticipation of sharply higher projected demand as a result of a resurgence in nuclear power, and by the fact that secondary supplies are either becoming depleted or will not be available. The sharp price increase was driven in part by high levels of utility buying, which resulted in most utilities covering their requirements through 2009. A decrease in near-term utility demand coupled with rising levels of supplies from producers and traders led to downward pressure being placed on uranium prices since the third quarter of 2007. The spot market price for uranium began in January 2009 at $53.00 per pound and ranged between a low of $40.00 per pound in April to a high of $54.00 per pound in June. The spot price closed 2009 at $44.50 per pound As of March 8, 2010, the spot price was $40.75 per pound and the long-term contract price was $60.00 per pound. We believe the higher long-term price reflects the continued strong future fundamentals for the uranium market.

The following graph shows annual average spot prices per pound from 1982 to 2009 and the average price for the period January 1, 2010 to March 8, 2010, as reported by Trade Tech and Ux.

Ux Average Annual U3O8 Spot Price

The ISR mining process is a form of solution mining. It differs dramatically from conventional mining techniques. The ISR technique avoids the movement and milling of significant quantities of rock and ore as well as mill tailing waste associated with more traditional mining methods. It is generally more cost-effective and environmentally benign than conventional mining. Historically, the majority of United States uranium production resulted from either open pit surface mines or underground shaft operations.

The ISR process was first tested for the production of uranium in the mid-1960s and was first applied to a commercial-scale project in 1975 in South Texas. It was well established in South Texas by the late 1970’s, where it was employed in about twenty commercial projects, including two operated by us.

In the ISR process, groundwater fortified with oxygen and other solubilizing agents is pumped into a permeable ore body causing the uranium contained in the ore to dissolve. The resulting solution is pumped to the surface. The fluid-bearing uranium is then circulated to an ion exchange column on the surface where uranium is extracted from the fluid onto resin beads. The fluid is then reinjected into the ore body. When the ion exchange column’s resin beads are loaded with uranium, they are removed and flushed with a salt-water solution, which strips the uranium from the beads. This leaves the uranium in slurry, which is then dried and packaged for shipment as uranium concentrates.

For greater operating efficiency and lower capital expenditures, when developing new wellfields we use a wellfield-specific remote ion exchange methodology as opposed to a central plant as we had done historically. Instead of piping the solutions over large distances through large diameter pipelines and mixing the waters of several wellfields together, each wellfield is being mined using a dedicated satellite ion exchange facility. This allows ion exchange to take place at the wellfield instead of at the central plant. A wellfield consists of a series of injection wells, production (extraction) wells and monitoring wells drilled in specified patterns. Wellfield pattern is crucial to minimizing costs and maximizing efficiencies of production. The satellite facilities allow mining of each wellfield using its own native groundwater.

Environmental Considerations and Permitting

Uranium mining is regulated by the federal government, states and, where conducted in Indian Country, by Indian tribes. Compliance with such regulation has a material effect on the economics of our operations and the timing of project development. Our primary regulatory costs have been related to obtaining licenses and permits from federal and state agencies before the commencement of mining activities.

U.S. regulations pertaining to climate change continue to evolve in both the U.S. and internationally. We do not anticipate any adverse impact from these regulations that would be unique to our operations.

Radioactive Material License. Before commencing operations in both Texas and New Mexico, we must obtain a radioactive material license. Under the federal Atomic Energy Act, the United States Nuclear Regulatory Commission has primary jurisdiction over the issuance of a radioactive material license. However, the Atomic Energy Act also allows for states with regulatory programs deemed satisfactory by the Commission to take primary responsibility for issuing the radioactive material license. The Commission has ceded jurisdiction for such licenses to Texas, but not to New Mexico. Such ceding of jurisdiction by the Commission is hereinafter referred to as the “granting of primacy.”

The Texas Commission of Environmental Quality (TCEQ) is the administrative agency with jurisdiction over the radioactive material license. For operations in New Mexico, radioactive material licensing is handled directly by the United States Nuclear Regulatory Commission.

See “Properties” and “Legal Proceedings” for the status of our radioactive material license for New Mexico and our Texas properties.

Underground Injection Control Permits (“UIC”). The federal Safe Drinking Water Act creates a nationwide regulatory program protecting groundwater. This law is administered by the United States Environmental Protection Agency (the “USEPA”). However, to avoid the burden of dual federal and state (or Indian tribal) regulation, the Safe Drinking Water Act allows for the UIC permits issued by states (and Indian tribes determined eligible for treatment as states) to satisfy the UIC permit required under the Safe Drinking Water Act under two conditions. First, the state’s program must have been granted primacy. Second, the USEPA must have granted, upon request by the state, an aquifer exemption. The USEPA may delay or decline to process the state’s application if the USEPA questions the state’s jurisdiction over the mine site.

Texas has been granted primacy for its UIC programs, and the Texas Commission on Environmental Quality administers UIC permits. In addition to the radioactive materials license described above, the TCEQ also regulates air quality and surface deposition or discharge of treated wastewater associated with the ISR mining process.

New Mexico has also been granted primacy for its program. The Navajo Nation has been determined eligible for treatment as a state, but it has not requested the grant of primacy from the USEPA for uranium related UIC activity. Until the Navajo Nation has been granted primacy, ISR uranium mining activities within Navajo Nation jurisdiction will require a UIC permit from the USEPA. Despite some procedural differences, the substantive requirements of the Texas, New Mexico and USEPA underground injection control programs are very similar.

Properties located in Indian Country remain subject to the jurisdiction of the USEPA. Some of our properties are located in areas that are in Indian Country or in areas that are in dispute.

See “Properties” and “Legal Proceedings” for a description of the status of our UIC permits in Texas and New Mexico.

Other. In addition to radioactive material licenses and underground injection control permits, we are also required to obtain from governmental authorities a number of other permits or exemptions, such as for wastewater discharge, for land application of treated wastewater, and for air emissions.

In order for a licensee to receive final release from further radioactive material license obligations after all of its mining and post-mining clean up have been completed in Texas, approval must be issued by the TCEQ along with concurrence from the United States Nuclear Regulatory Commission and in New Mexico by the United States Nuclear Regulatory Commission.

In addition to the costs and responsibilities associated with obtaining and maintaining permits and the regulation of production activities, we are subject to environmental laws and regulations applicable to the ownership and operation of real property in general, including, but not limited to, the potential responsibility for the activities of prior owners and operators.

The current environmental regulatory program for the ISR industry is well established. Many ISR mines have gone full cycle without any significant environmental impact. However, the public anti-nuclear lobby can make environmental permitting difficult and timing unpredictable.

Reclamation and Restoration Costs and Bonding Requirements

At the conclusion of mining, a mine site is decommissioned and decontaminated, and each wellfield is restored and reclaimed. Restoration involves returning the aquifer to its pre-mining use and removing evidence of surface disturbance. Restoration can be accomplished by flushing the ore zone with native ground water and/or using reverse osmosis to remove ions, minerals and salts to provide clean water for reinjection to flush the ore zone. Decommissioning and decontamination entails dismantling and removing the structures, equipment and materials used at the site during the mining and restoration activities.

The Company is required by the State of Texas regulatory agencies to obtain financial surety relating to certain of its future restoration and reclamation obligations. The Company has a combination of bank Letters of Credit (the “L/C’s) and performance bonds issued for the benefit of the Company to satisfy such regulatory requirements. The L/C’s were issued by Bank of America and the performance bonds have been issued by United States Fidelity and Guaranty Company (“USF&G”). The L/C’s relate primarily to our operations at our Kingsville Dome and Vasquez projects and amounted to $5,761,000 and $5,629,000, at December 31, 2009 and 2008, respectively. The L/C’s are collateralized in their entirety by certificates of deposit.

The performance bonds were $2,835,000 on December 31, 2009 and 2008, and related primarily to our operations at Kingsville Dome and Rosita. USF&G has required that the Company deposit funds collateralizing a portion of the bonds, and we have deposited approximately $386,000 and $385,000 at December 31, 2009 and 2008, respectively, as cash collateral for such bonds. We are obligated by agreement with the bonding company to increase the cash collateral to an amount equal to 50% of the amount of the bonds, plus an additional $0.50 for each pound of uranium produced until the account accumulates an additional $1.0 million.

We estimate that our actual reclamation liabilities for prior operations at Kingsville Dome, Vasquez and Rosita at December 31, 2009, are about $8.4 million of which the net present value of $5.5 million is recorded as a liability on our balance sheet as of December 31, 2009. Under an agreement reached on March 1, 2004 with the Texas regulatory agencies and our bonding company, we agreed to fund ongoing groundwater restoration at the Kingsville Dome and Rosita mine sites at specified treatment rates, utilizing a portion of our cash flow from sales of uranium from the Vasquez site as a substitute for additional bonding. This agreement expired on August 31, 2007. As a result, the Company is now required to post adequate financial surety, and as of December 31, 2009 has posted letters of credit in the amount of $5.8 million, which are cash collateralized in full.

These financial surety obligations are reviewed and revised periodically by the Texas regulators.

In New Mexico, surety bonding will be required before commencement of mining and will be subject to annual review and revision by the United States Nuclear Regulatory Commission and the State of New Mexico or the USEPA.

Water is essential to the ISR process. It is readily available in South Texas. In Texas, water is subject to capture, and we do not have to acquire water rights through a state administrative process. In New Mexico, water rights are administered through the New Mexico State Engineer and can be subject to Indian tribal jurisdictional claims. New water rights or changes in purpose or place of use or points of diversion of existing water rights, such as those in the San Juan and Gallup Basins where our properties are located, must be obtained by permit from the State Engineer. Applications may be approved subject to conditions that govern exercise of the water rights.

Jurisdiction over water rights becomes an issue in New Mexico when an Indian nation, such as the Navajo Nation, objects to the State Engineer’s authority and claims tribal jurisdiction over Indian Country. This issue may result in litigation between the Indian nation and the state, which may delay action on water right applications, and can require applications to the appropriate Indian nation and continuing jurisdiction by the Indian nation over use of the water. The foregoing issues arise in connection with certain of our New Mexico properties.

In New Mexico, we hold approved water rights to provide sufficient water to conduct mining at the Churchrock project and Section 24 for the Crownpoint project for the projected life of these mines. We also hold two unprotested senior water rights applications that, when approved, would provide sufficient water for future extensions of the Crownpoint project.

A primary area of competition is in the identification and acquisition of properties with high prospects of potential producible reserves that are suitable for our size operation. We believe that we compete with multiple junior exploration companies for both properties as well as skilled personnel.

The Company competes for markets for our uranium primarily based on price. We market uranium to utilities and commodity brokers and are in direct competition with supplies available from various sources worldwide. We believe we compete with approximately multiple operating companies in the mining and sale of uranium.

Our Internet website address is www.uraniumresources.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports of Form 8-K, and amendments to those reports filed or furnished pursuant to section 13(a) of 15(d) of the Exchange Act, are available free of charge through our website under the tab “Investor Relations” as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission. We also make available on our website copies of materials regarding our corporate governance policies and practices, including our Code of Ethics, Nominating Committee Charter, Audit Committee Charter and Compensation Committee Charter. You may also obtain a printed copy of the foregoing materials by sending written request to: Uranium Resources, Inc., 405 State Highway 121 Bypass, Building A, Suite 110, Lewisville, Texas 75067, Attention: Information Request or by calling 972.219.3330.

The factors identified below are important factors (but not necessarily all of the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement made by, or on behalf of, the Company. Where any such forward-looking statement includes a statement of the assumptions or bases underlying such forward-looking statement, we caution that, while we believe such assumptions or bases to be reasonable and make them in good faith, assumed facts or bases almost always vary from actual results, and the differences between assumed facts or bases and actual results can be material, depending upon the circumstances. Where, in any forward-looking statement, the Company, or its management, expresses an expectation or belief as to the future results, such expectation or belief is expressed in good faith and believed to have a reasonable basis, but there can be no assurance that the statement of expectation or belief will result, or be achieved or accomplished. Taking into account the foregoing, the following are identified as important risk factors that could cause actual results to differ materially from those expressed in any forward-looking statement made by, or on behalf of, the Company.

General Risks and Uncertainties

We are not producing uranium at this time, nor do we expect to begin production in the near future unless uranium prices recover to a profitable level. As a result, we currently have no sources of operating cash. If we cannot monetize certain existing Company assets, partner with another Company that has cash resources, find other means of generating revenue other than uranium production and/or have the ability to access additional sources of private or public capital we may not be able to remain in business.

We will not commence production at our existing properties until uranium prices recover to a profitable level. Until uranium prices recover we will have no way to generate cash inflows unless we monetize certain Company assets or find other means to generate cash. In addition, our Vasquez project has been depleted of its economically recoverable reserves and our Rosita and Kingsville Dome projects have limited identified economically recoverable reserves. Our future uranium production, cash flow and income are dependent upon our ability to bring on new, as yet unidentified wellfields and to acquire and develop additional reserves. We can provide no assurance that our properties will be placed into production or that we will be able to continue to find, develop, acquire and finance additional reserves.

We are presently out of compliance with the continuing listing requirements of the NASDAQ Global Market, the exchange on which our common stock is traded. If our stock is delisted from NASDAQ, a reliable trading market for our securities could cease to exist, the market price of our common stock could be negatively impacted and we could face difficulty raising additional capital.

On January 10, 2010, the NASDAQ Stock Market, the exchange on which our common stock is traded, notified us that the bid price for our common stock closed below the minimum $1.00 per share for a period of 30 consecutive business days, which means that we fail to meet the requirements for continued listing set forth in Marketplace Rule 5550(a)(1). If we cannot regain compliance with the minimum bid requirements before July 7, 2010, NASDAQ may take steps to delist our common stock from the NASDAQ.

Delisting would have an adverse effect on the liquidity of our common stock and, as a result, the market price for our common stock might decline. Delisting could also make it more difficult for us to raise additional capital.

Our ability to function as an operating mining company will be dependent on our ability to mine our properties at a profit sufficient to finance further mining activities and for the acquisition and development of additional properties. The volatility of uranium prices makes long-range planning uncertain and raising capital difficult.

In addition to ceasing all production, we have deferred all activities for delineation and development of new wellfields at our South Texas projects. This decision limits our ability to be immediately ready to begin production should uranium prices improve suddenly. Our ability to operate on a positive cash flow basis will be dependent on mining sufficient quantities of uranium at a profit sufficient to finance our operations and for the acquisition and development of additional mining properties. Any profit will necessarily be dependent upon, and affected by, the long and short term market prices of uranium, which are subject to significant fluctuation. Uranium prices have been and will continue to be affected by numerous factors beyond our control. These factors include the demand for nuclear power, political and economic conditions in uranium producing and consuming countries, uranium supply from secondary sources and uranium production levels and costs of production. A significant, sustained drop in uranium prices may make it impossible to operate our business at a level that will permit us to cover our fixed costs or to remain in operation.

We face risks related to exploration and development, if warranted, on our properties.

Our level of profitability, if any, in future years will depend to a great degree on uranium prices and whether any of our exploration stage properties can be brought into production. The exploration for and development of uranium deposits involves significant risks. It is impossible to ensure that the current and future exploration programs and/or feasibility studies on our existing properties will establish reserves. Whether a uranium ore body will be commercially viable depends on a number of factors, including, but not limited to: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; uranium prices, which cannot be predicted and which have been highly volatile in the past; mining, processing and transportation costs; perceived levels of political risk and the willingness of lenders and investors to provide project financing; labor costs and possible labor strikes; and governmental regulations, including, without limitation, regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting materials, foreign exchange, environmental protection, employment, worker safety, transportation, and reclamation and closure obligations. Most exploration projects do not result in the discovery of commercially mineable deposits of uranium and there can be no assurance that any of our exploration stage properties will be commercially mineable or can be brought into production.

The only market for uranium is nuclear power plants world-wide, and there are a limited number of customers.

We are dependent on a limited number of electric utilities that buy uranium for nuclear power plants. Because of the limited market for uranium, a reduction in purchases of newly produced uranium by electric utilities for any reason (such as plant closings) would adversely affect the viability of our business.

The price of alternative energy sources affects the demand for and price of uranium.

The attractiveness of uranium as an alternative fuel to generate electricity may to some degree be dependent on the relative prices of oil, gas, coal and hydro-electricity and the possibility of developing other low cost sources for energy. If the price of alternative energy sources decrease or new low-cost alternative energy sources are developed, the demand for uranium could decrease, which may result in the decrease in the price of uranium.

Public acceptance of nuclear energy is uncertain.

Maintaining the demand for uranium at current levels and future growth in demand will depend upon acceptance of nuclear technology as a means of generating electricity. Lack of public acceptance of nuclear technology would adversely affect the demand for nuclear power and potentially increase the regulation of the nuclear power industry.

The Navajo Nation ban on uranium mining in Indian Country encompasses approximately 84% of our in-place mineralized uranium material on our properties in New Mexico and will adversely affect our ability to mine unless the ban is overturned.

In April 2005, the Navajo Nation Council passed the Diné Natural Resources Protection Act of 2005 prohibiting uranium mining and processing on any sites within Indian Country as defined under 18 U.S.C. § 1151. We believe that the ban is beyond the jurisdiction of the Navajo Nation. However, the ban may prevent us from developing and operating our properties located in Indian Country until the jurisdictional issue is resolved.

In February 2007, the United States Environmental Protection Agency, or USEPA, determined that Section 8 of our Churchrock property was Indian Country and that the USEPA and not the state of New Mexico has the authority to issue the Underground Injection Control, or UIC, permits for Section 8 that are a precondition to mining. We appealed that decision to the United States Court of Appeals for the Tenth Circuit, which ruled 2 to 1 that Section 8 of the Churchrock property is Indian Country. The Company was granted an en banc review of the Tenth Circuit’s decision and oral arguments were presented to the Court on January 12, 2010. We are waiting for the Court to render a decision. The expansive definition of Indian Country adopted by the USEPA may encompass properties owned by non-Indians within Navajo chapters in New Mexico. If that expansive definition prevails, as much as 84% of our in-place mineralized uranium materials in New Mexico could be deemed to be in Indian Country, which could subject these properties to the Navajo Nation ban on uranium mining. Our inability to mine our New Mexico properties could have a material adverse impact on our results of operations.

We may not be able to mine a substantial portion of our uranium in New Mexico until a mill is built in New Mexico.

A substantial portion of our uranium in New Mexico lends itself most readily to conventional mining methods and may not be able to be mined unless a mill is built in New Mexico. We have no immediate plans to build, nor are we aware of any third party’s plan to build, a mill in New Mexico and there can be no guaranty that a mill will be built. In the event that a mill is not built a substantial portion of our uranium may not be able to be mined. Our inability to mine all or a portion of our uranium in New Mexico would have a material adverse effect on future operations.

Itochu elected to terminate our Joint Venture with them for the development of the Churchrock Property and we do not have a committed source of financing for the development of our Churchrock Property.

On December 5, 2006, HRI-Churchrock, Inc., a wholly owned subsidiary of the Company, entered into a joint venture with a wholly owned subsidiary of Itochu Corporation to develop jointly our Churchrock property in New Mexico. Under the terms of the joint venture, both parties had until April 2, 2007 to make a preliminary investment decision whether to move forward with the joint venture. The parties agreed to extend that date to March 2, 2009. On March 6, 2009, we received notification that Itochu had elected to terminate the Joint Venture. As a result, we no longer have a committed source of financing for the development of our Churchrock property. There can be no assurance that we will be able to obtain financing for this project. Our inability to develop the Churchrock property would have a material adverse effect on our future operations.

Our operations are subject to environmental risks.

We are required to comply with environmental protection laws and regulations and permitting requirements, and we anticipate that we will be required to continue to do so in the future. We have expended significant resources, both financial and managerial, to comply with environmental protection laws, regulations and permitting requirements and we anticipate that we will be required to continue to do so in the future. The material laws and regulations within the U.S. that the Company must comply with include the Atomic Energy Act, Uranium Mill Tailings Radiation Control Act of 1978, or UMTRCA, Clean Air Act, Clean Water Act, Safe Drinking Water Act, Federal Land Policy Management Act, National Park System Mining Regulations Act, and the State Mined Land Reclamation Acts or State Department of Environmental Quality regulations, as applicable.

We are required to comply with the Atomic Energy Act, as amended by UMTRCA, by applying for and maintaining an operating license from the NRC and the state of Texas. Uranium operations must conform to the terms of such licenses, which include provisions for protection of human health and the environment from endangerment due to radioactive materials. The licenses encompass protective measures consistent with the Clean Air Act and the Clean Water Act. We intend to utilize specific employees and consultants in order to comply with and maintain our compliance with the above laws and regulations. Mining operations may be subject to other laws administered by the federal Environmental Protection Agency and other agencies.

The uranium industry is subject not only to the worker health and safety and environmental risks associated with all mining businesses, but also to additional risks uniquely associated with uranium mining and milling. The possibility of more stringent regulations exists in the areas of worker health and safety, storage of hazardous materials, standards for heavy equipment used in mining or milling, the disposition of wastes, the decommissioning and reclamation of exploration, mining and in-situ sites, climate change and other environmental matters, each of which could have a material adverse effect on the cost or the viability of a particular project.

We cannot predict what environmental legislation, regulation or policy will be enacted or adopted in the future or how future laws and regulations will be administered or interpreted. The recent trend in environmental legislation and regulation, generally, is toward stricter standards, and this trend is likely to continue in the future. This recent trend includes, without limitation, laws and regulations relating to air and water quality, mine reclamation, waste handling and disposal, the protection of certain species and the

preservation of certain lands. These regulations may require the acquisition of permits or other authorizations for certain activities. These laws and regulations may also limit or prohibit activities on certain lands. Compliance with more stringent laws and regulations, as well as potentially more vigorous enforcement policies or stricter interpretation of existing laws, may necessitate significant capital outlays, may materially affect our results of operations and business, or may cause material changes or delays in our intended activities.

Our operations may require additional analysis in the future including environmental, cultural and social impact and other related studies. Certain activities require the submission and approval of environmental impact assessments. Environmental assessments of proposed projects carry a heightened degree of responsibility for companies and directors, officers, and employees. We cannot provide assurance that we will be able to obtain or maintain all necessary permits that may be required to continue our operation or our exploration of our properties or, if feasible, to commence development, construction or operation of mining facilities at such properties on terms which enable operations to be conducted at economically justifiable costs. If we are unable to obtain or maintain permits or water rights for development of our properties or otherwise fail to manage adequately future environmental issues, our operations could be materially and adversely affected.

Because mineral exploration and development activities are inherently risky, we may be exposed to environmental liabilities and other dangers. If we are unable to maintain adequate insurance, or liabilities exceed the limits of our insurance policies, we may be unable to continue operations.

The business of mineral exploration and extraction involves a high degree of risk. Few properties that are explored are ultimately developed into production. Unusual or unexpected formations, formation pressures, fires, power outages, labor disruptions, flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor are other risks involved in extraction operations and the conduct of exploration programs. Previous mining operations may have caused environmental damage at certain of our properties. It may be difficult or impossible to assess the extent to which such damage was caused by us or by the activities of previous operators, in which case, any indemnities and exemptions from liability may be ineffective. If any of our properties are found to have commercial quantities of uranium, we would be subject to additional risks respecting any development and production activities.

Although we carry liability insurance with respect to our mineral exploration operations, we may become subject to liability for damage to life and property, environmental damage, cave-ins or hazards against which we cannot insure or against which we may elect not to insure because of cost or other business reasons. In addition, the insurance industry is undergoing change and premiums are being increased. If we are unable to procure adequate insurance because of cost, unavailability or otherwise, we might be forced to cease operations.

Our inability to obtain financial surety would threaten our ability to continue in business.

Future bonding requirements to comply with federal and state environmental and remediation requirements and to secure necessary licenses and approvals will increase significantly when future development and production occurs at our sites in Texas and New Mexico. The amount of the bonding for each producing property is subject to annual review and revision by regulators. We expect that the issuer of the bonds will require us to provide cash collateral equal to the face amount of the bond to secure the obligation. In the event we are not able to raise, secure or generate sufficient funds necessary to satisfy these bonding requirements, we will be unable to develop our sites and bring them into production, which inability will have a material adverse impact on our business and may negatively affect our ability to continue to operate.

Competition from better-capitalized companies affects prices and our ability to acquire properties and personnel.

There is global competition for uranium properties, capital, customers and the employment and retention of qualified personnel. In the production and marketing of uranium, there are a number of producing entities, some of which are government controlled and all of which are significantly larger and better capitalized than we are. Many of these organizations also have substantially greater financial, technical, manufacturing and distribution resources than we have.

Our uranium production also competes with uranium recovered from the de-enrichment of highly enriched uranium obtained from the dismantlement of United States and Russian nuclear weapons and imports to the United States of uranium from the former Soviet Union and from the sale of uranium inventory held by the United States Department of Energy. In addition, there are numerous entities in the market that compete with us for properties and are attempting to become licensed to operate ISR facilities. If we are unable to successfully compete for properties, capital, customers or employees or alternative uranium sources, it could have a materially adverse effect on our results of operations.

Because we have limited capital, inherent mining risks pose a significant threat to us compared with our larger competitors.

Because we have limited capital, we are unable to withstand significant losses that can result from inherent risks associated with mining, including environmental hazards, industrial accidents, flooding, interruptions due to weather conditions and other acts of nature which larger competitors could withstand. Such risks could result in damage to or destruction of our infrastructure and production facilities, as well as to adjacent properties, personal injury, environmental damage and processing and production delays, causing monetary losses and possible legal liability.

We may need to obtain additional financing in order to implement our business plan, and the inability to obtain it could cause our business plan to fail.

As of December 31, 2009, we had approximately $6.1 million in cash. We may require additional financing in order to complete our plan of operations. We may not be able to obtain all of the financing we require. Our ability to obtain additional financing is subject to a number of factors, including the market price of uranium, market conditions, investor acceptance of our business plan, and investor sentiment. These factors may make the timing, amount, terms and conditions of additional financing unattractive or unavailable to us. In recognition of current economic conditions and the planned shut-down of production, we have significantly reduced our spending, delayed or cancelled planned activities and substantially changed our current corporate structure. However, these actions may not be sufficient to offset the detrimental effects of the weak economy and cessation of production, which could result in material adverse effects on our business, revenues, operating results, and prospects.

Our business could be harmed if we lose the services of our key personnel.

Our business and mineral exploration programs depend upon our ability to employ the services of geologists, engineers and other experts. In operating our business and in order to continue our programs, we compete for the services of professionals with other mineral exploration companies and businesses. In addition, several entities have expressed an interest in hiring certain of our employees. Our ability to maintain and expand our business and continue our exploration programs may be impaired if we are unable to continue to employ or engage those parties currently providing services and expertise to us or identify and engage other qualified personnel to do so in their place. To retain key employees, we may face increased compensation costs, including potential new stock incentive grants and there can be no assurance that the incentive measures we implement will be successful in helping us retain our key personnel.

Approximately 21.2% of our Common Stock is controlled by one record owner and management.

Approximately 13.1% of our common stock is controlled by one significant stockholder. In addition, our directors and officers are the beneficial owners of approximately 8.1% of our common stock. This includes, with respect to both groups, shares that may be purchased upon the exercise of outstanding options. Such ownership by the Company’s principal shareholders, executive officers and directors may have the effect of delaying, deferring, preventing or facilitating a sale of the Company or a business combination with a third party.

The availability for sale of a large amount of shares may depress the market price of our Common Stock.

As of December 31, 2009, 56,781,792 shares of our Common Stock were currently outstanding, all of which are registered or otherwise transferable. The availability for sale of a large amount of shares or conversion of the Company’s outstanding warrants by any one or several shareholders may depress the market price of our Common Stock and impair our ability to raise additional capital through the public sale of our Common Stock. We have no arrangement with any of the holders of the foregoing shares to address the possible effect on the price of our Common Stock of the sale by them of their shares.

Terms of subsequent financings may adversely impact our stockholders.

In order to finance our working capital needs, we may have to raise funds through the issuance of equity or debt securities in the future. We currently have no authorized preferred stock. Depending on the type and the terms of any financing we pursue, stockholder’s rights and the value of their investment in our Common Stock could be reduced. For example, if we have to issue secured debt securities, the holders of the debt would have a claim to our assets that would be prior to the rights of stockholders until the debt is paid. Interest on these debt securities would increase costs and negatively impact operating results. If the issuance of new securities results in diminished rights to holders of our common stock, the market price of our common stock could be negatively impacted.

Shareholders could be diluted if we were to use Common Stock to raise capital.

As previously noted, we may need to seek additional capital in the future to satisfy our working capital requirements. This financing could involve one or more types of securities including common stock, convertible debt, preferred stock or warrants to acquire common or preferred stock. These securities could be issued at or below the then prevailing market price for our common stock. Any issuance of additional shares of our common stock could be dilutive to existing stockholders and could adversely affect the market price of our common stock.

Item 1B. Unresolved Staff Comments.

None.

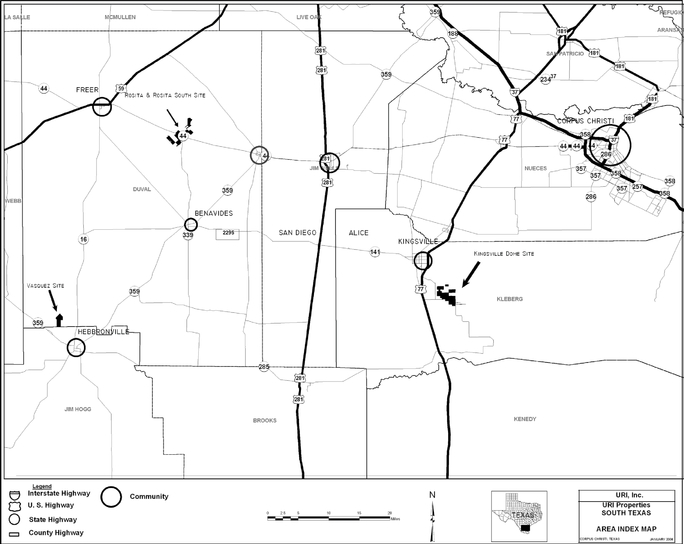

We currently control 3 major properties in the state of Texas. The Kingsville Dome, Rosita and Vasquez properties are shown in Figure No. 2.1 and are described below.

Figure No 2.1. Texas Properties Location Map

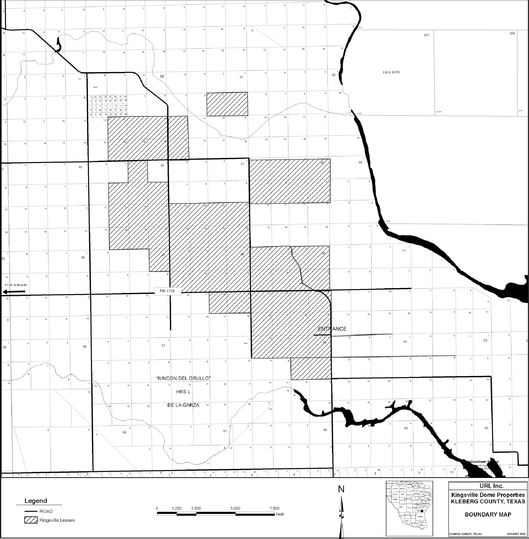

Kingsville Dome (Figure 2.2)

The Property. The Kingsville Dome property consists of mineral leases from private landowners on about 2,424 gross and 2,227 net acres located in central Kleberg County, Texas. The leases provide for royalties based upon a percentage of uranium sales of 6.25%. The leases have expiration dates ranging from 2000 to 2007, however we hold most of these leases by production; and with a few minor exceptions, all the leases contain clauses that permit us to extend the leases not held by production by payment of a per acre royalty ranging from $10 to $30. We have paid such royalties on all material acreage. Mineralization is found in the Goliad formation at depths of 600 to 750 feet.

Production History. Initial production commenced in May 1988. From then until July 1999, we produced a total of 3.5 million pounds. Production was stopped in July 1999, because of depressed uranium prices. We resumed production at Kingsville Dome in April 2006 and produced 94,100 pounds of uranium in 2006; 338,100 pounds in 2007, 254,000 pounds in 2008 and 56,000 pounds in 2009. We made approximately $8.0 million in capital expenditures in 2007, $3.6 million in 2008 and $159,000 in 2009.

Permitting Status. A radioactive material license and underground injection control permit have been issued. As new areas are proposed for production, additional authorizations under the area permit are required. Approval of our Production Area Authorization (“PA”) #3 was re-authorized in May 2006. In April 2006 we re-started production in PA #2 followed by production in PA #3 in February 2008. Production from PA#3 wellfields continued until July 2009. See “Legal Proceedings.”

Restoration and Reclamation. During 2009, we conducted restoration activities as required by the permits and licenses on this project spending approximately $963,000 on restoration activities. In 2008 and 2007, we spent approximately $349,000 and $595,000, respectively. Since we began our groundwater activities in 1998, we have processed and cleaned approximately 2.0 billion gallons of groundwater at the Kingsville Dome project.

Figure No. 2.2. Kingsville Dome Property

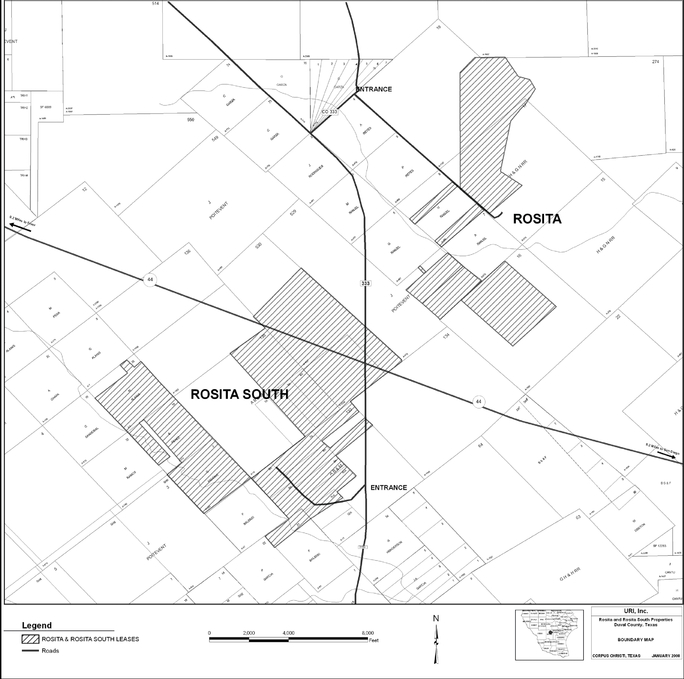

Rosita (Figure 2.3)

The Property: The Rosita property consists of mineral leases from private landowners on about 3,377 gross and net acres and the Rosita South property consists of mineral leases from private land owners on about 2,130 gross acres and 1,984 net acres located in north-central Duval County, Texas. The leases provide for sliding scale royalties based on a percentage of uranium sales. Royalty percentages on average increase from 6.25% up to 18.25% when uranium prices reach $80.00 per pound. The leases have expiration dates ranging from 2012 to 2015. We are holding these leases by payment of rental fees ranging from $10 to $30 per acre. Mineralization is found in the Goliad Formation at depths of 125 to 350 feet.

Production History: Initial production commenced in 1990. From then until July 1999, URI produced a total of 2.64 million pounds. Production was stopped in July of 1990 because of depressed uranium prices. Production from a new wellfield at Rosita wellfield was begun in June 2008. However, technical difficulties that raised the cost of production coupled with a sharp drop in uranium prices led to the decision to shut-in this wellfield after 10,200 pounds were produced.

Our capital expenditures were approximately $40,000, $4.5 million and $5.0 million in 2009, 2008 and 2007, respectively primarily for plant refurbishment and wellfield development.

Restoration and Reclamation. We are conducting restoration and reclamation activities at this project and are currently in stabilization in our first two PA’s. During 2009, our primary groundwater activity consisted of collecting groundwater samples throughout the year for stability testing. We spent approximately $247,000, $465,000 and $820,000 on restoration activities in 2009, 2008 and 2007, respectively. Since we began our groundwater activities in 2000, we have processed and cleaned approximately 1.3 billion gallons of groundwater at the Rosita project.

Permitting Status: A radioactive material license and an underground injection control permit have been issued for the Rosita property. The underground injection control permit is being amended to include the Rosita South property. Production could resume in areas already included in existing Production Area Authorizations. As new areas are proposed for production, additional authorizations under the permit will be required.

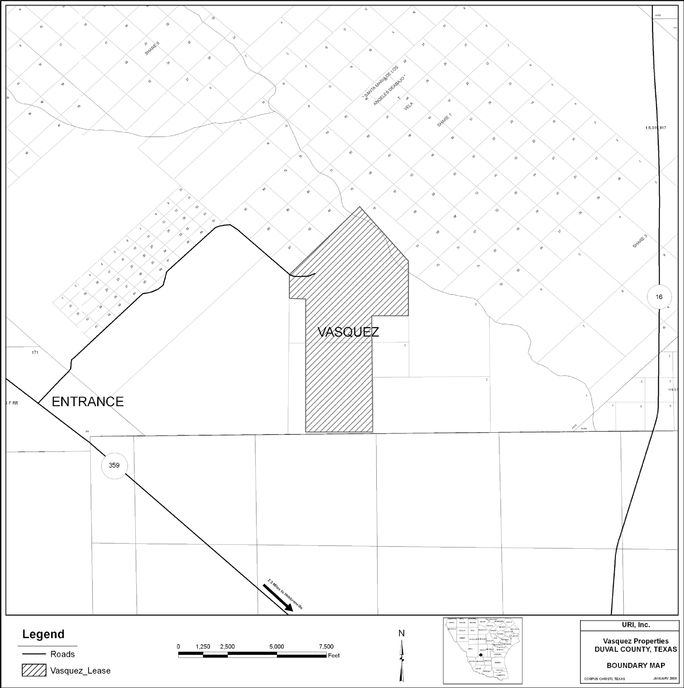

Vasquez (Figure 2.4)

The Property. We have a mineral lease on 872 gross and net acres located in southwestern Duval County, in South Texas. The primary term expired in February 2008; however, we held the lease by production and are currently in restoration. The lease provides for royalties based upon 6.25% of uranium sales below $25.00 per pound and royalty rate increases on a sliding scale up to 10.25% for uranium sales occurring at or above $40.00 per pound. Mineralization is found in the Oakville formation at depths of 200 to 250 feet.

Production History. We commenced production from this property in October 2004. Our capital expenditures in 2009 were approximately $194,000. We had approximately $355,000 in capital expenditures at Vasquez and produced 36,600 pounds of uranium in 2008. We had approximately $1.3 million in capital expenditures at Vasquez and produced 78,600 pounds of uranium in 2007.

Restoration and Reclamation. We are conducting ongoing restoration and reclamation activities at this project and have spent $591,000, $224,000 and $33,000 in 2009, 2008 and 2007, respectively for such activities. Since the commencement of groundwater restoration activities at the end of 2007, we have treated approximately 161 million gallons of groundwater.

Permitting Status. All of the required permits for this property have been received.

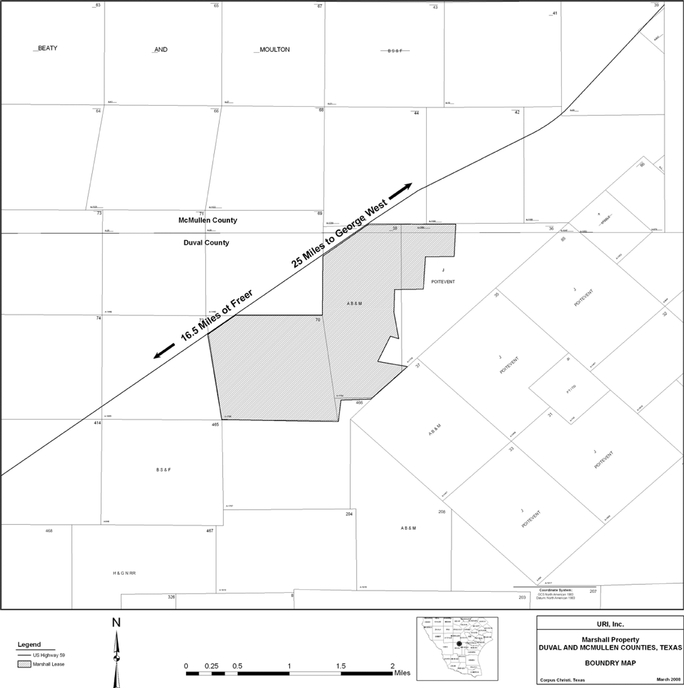

Marshall Exploration Property (figure 2.6).

The Marshall Property is a Goliad and Oakville prospect consisting of 1953 gross and net acres. It is located in Duval and McMullen counties, Texas. During 2008 we drilled 280 exploration holes and discovered significant mineralization. Further evaluation will need to be conducted to determine if this property can be mined using ISR methods.

Figure No. 2.6. Marshall Exploration Property

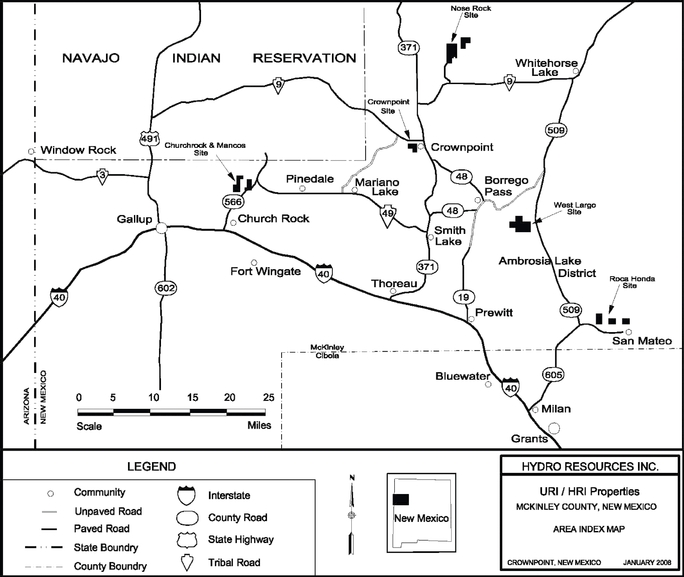

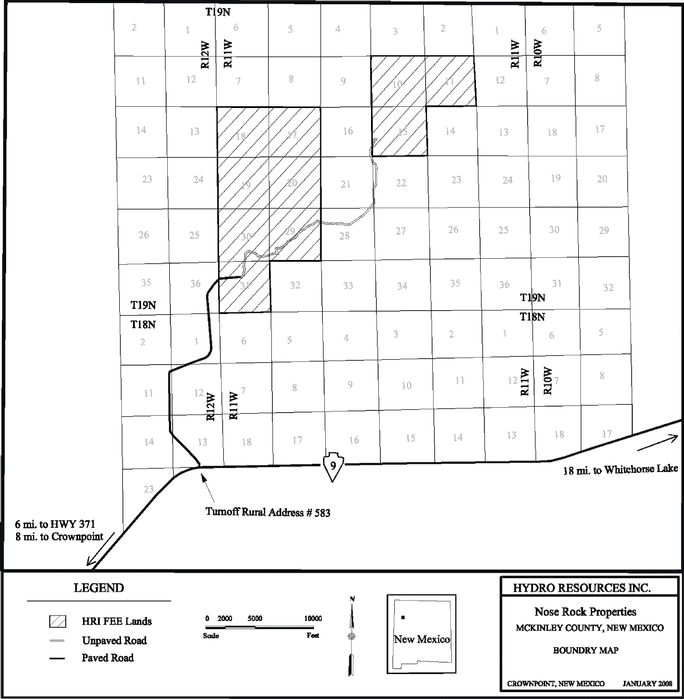

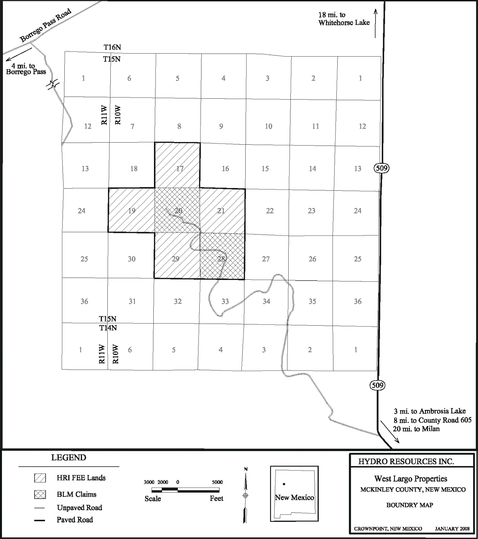

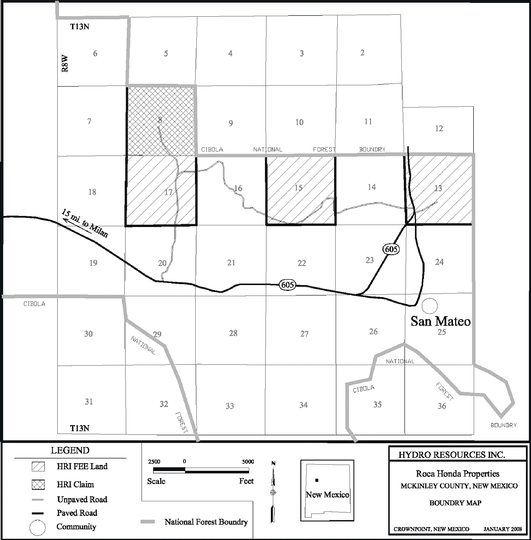

General. We have various interests in properties located in New Mexico (Figure 2.7). We have fee lands, patented and unpatented mining claims, mineral leases and some surface leases. We have spent $13.1 million to date on permitting for New Mexico. Additional expenditures will be required and could be material. We are unable to estimate the amount. We expect that these costs will be incurred over multiple years. See “Legal Proceedings” for a discussion of the current status of our license for New Mexico

Figure No. 2.7. Location of New Mexico Properties

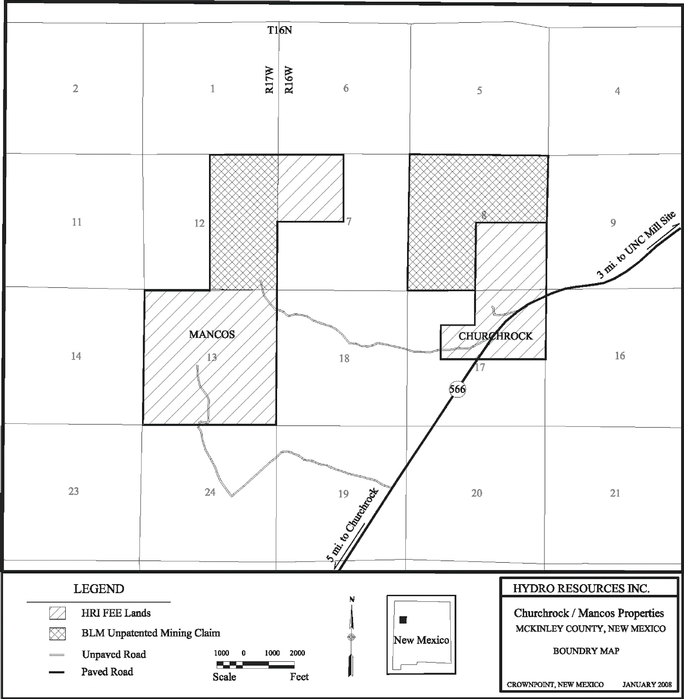

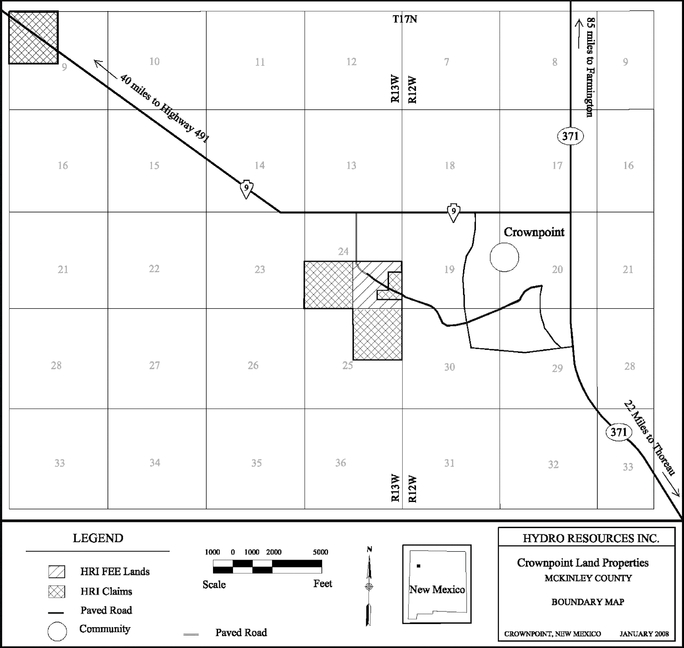

The Property. The Churchrock project encompasses about 2,200 gross and net acres. The properties are located in McKinley County, New Mexico and consist of three parcels, known as Section 8, Section 17 and Mancos. None of these parcels lies within the area generally recognized as constituting the Navajo Reservation. However, Section 8 has been designated by the USEPA as Indian Country. See, “Item 3. Legal Proceedings.” Access to the Churchrock property is via State Highway 566 and access to Mancos is via 4-wheel drive ranch roads west of State Highway 566.

Churchrock/Mancos (Figure 2.8)