Attached files

| file | filename |

|---|---|

| EX-31.2 - Andatee China Marine Fuel Services Corp | v175210_ex31-2.htm |

| EX-31.1 - Andatee China Marine Fuel Services Corp | v175210_ex31-1.htm |

| EX-32.1 - Andatee China Marine Fuel Services Corp | v175210_ex32-1.htm |

| EX-21.1 - Andatee China Marine Fuel Services Corp | v175210_ex21-1.htm |

| EX-32.2 - Andatee China Marine Fuel Services Corp | v175210_ex32-2.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

|

(Mark

One)

|

|

|

|

x

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d)

OF

THE SECURITIES EXCHANGE ACT OF

1934

|

For

the Fiscal Year Ended December 31, 2009

OR

|

¨

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d)

OF

THE SECURITIES EXCHANGE ACT OF

1934

|

For

the Transition Period from ___ to ____

Commission

File Number 001-34608

Andatee

China Marine Fuel Services Corporation

(Exact

Name of Registrant as Specified in Its Charter)

|

Delaware

|

80-0445030

|

|

|

(State

or Other Jurisdiction of

Incorporation

or Organization)

|

(IRS

Employer

Identification

No.)

|

(Address

of Principal Executive Offices) (Zip Code)

(Registrant’s

Telephone Number, Including Area Code)

Dalian

Ganjingzi District, Dalian Wan Lijiacun

Unit

C, No. 68 West Binhai Road, Xigang District Dalian

People’s

Republic of China

011

(86411) 8360 4683

Securities

registered under Section 12(b) of the Exchange Act:

Common

Stock, par value $0.001

Name of

each exchange on which registered:

The

Nasdaq Global Market LLC

Indicate by check mark if the

registrant is a well-known seasoned issuer, as defined in Rule 405 of the

Securities Act. Yes ¨ NO x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes ¨ NO

x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes x NO

¨

Indicate by check mark whether the

registrant has submitted electronically and posted on its corporate web site, if

any, every Interactive Data File required to be submitted and posted pursuant to

Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter

period that the registrant was required to submit and post such files). Yes

¨ NO ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not

be contained, to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a non-accelerated filer. See definition of “accelerated

filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check

one):

|

Large Accelerated Filer¨

|

Accelerated Filer ¨

|

Non-accelerated Filer ¨

|

Smaller Reporting Company x

|

Indicate by check mark whether the

registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ NO x

As of the

close of business on February 26, 2010, the aggregate market value of the voting

stock (common stock) held by non-affiliates of the registrant was approximately

$22.08 million based on the closing sale price of the Common stock on the Nasdaq

Global Market on that date. The registrant does not have any non-voting common

equity.

The

Company had 9,134,921 shares of common stock issued and outstanding as of

February 26, 2010.

Documents

Incorporated by Reference

None.

Table

of Contents

|

Page

|

||||

|

|

Part

I

|

1

|

||

|

Item

1.

|

Business

|

2

|

||

|

Item

1A.

|

Risk

Factors

|

12

|

||

|

Item

1B.

|

Unresolved

Staff Comments

|

25

|

||

|

Item

2

|

Properties

|

25

|

||

|

Item

3.

|

Legal

Proceedings

|

26

|

||

|

Item

4.

|

Submission

of Matters to a Vote of Security Holders

|

27

|

||

|

Part

II

|

28

|

|||

|

Item

5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

28

|

||

|

Item

6.

|

Selected

Financial Data

|

29

|

||

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

30

|

||

|

Item

7A.

|

Quantitative

and Qualitative Disclosures About Market Risk

|

50

|

||

|

Item

8.

|

Financial

Statements and Supplementary Data

|

50

|

||

|

Item

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

51

|

||

|

Item

9A.

|

Controls

and Procedures

|

51

|

||

|

Item

9B.

|

Other

Information

|

52

|

||

|

Part

III

|

53

|

|||

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance

|

53

|

||

|

Item

11.

|

Executive

Compensation

|

57

|

||

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

|

60

|

||

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

61

|

||

|

Item

14.

|

Principal

Accounting Fees and Services

|

62

|

||

|

Part

IV

|

63

|

|||

|

Item

15.

|

Exhibits

and Financial Statement Schedules

|

63

|

||

|

Signatures

|

64

|

|||

|

Exhibit

Index

|

|

|||

i

Part

I

Cautionary

Note Regarding Forward Looking Statements

This

Annual Report on Form 10-K (including the section regarding Management’s

Discussion and Analysis of Financial Condition and Results of Operations)

contains certain “forward-looking statements” within the meaning of Section 27A

of the Securities Act of 1933, as amended, and Section 21E of the Securities

Exchange Act of 1934, as amended, as well as information relating to Andatee

China Marine Fuel Services Corporation that is based on management’s exercise of

business judgment and assumptions made by and information currently available to

management. Although forward-looking statements in this Annual Report on Form

10-K reflect the good faith judgment of our management, such statements can only

be based on facts and factors currently known by us. Consequently,

forward-looking statements are inherently subject to risks and uncertainties and

actual results and outcomes may differ materially from the results and outcomes

discussed in or anticipated by the forward-looking statements. When used in this

document and other documents, releases and reports released by us, the words

“anticipate,” “believe,” “estimate,” “expect,” “intend,” “the facts suggest” and

words of similar import, are intended to identify any forward-looking

statements. You should not place undue reliance on these forward-looking

statements. These statements reflect our current view of future events and are

subject to certain risks and uncertainties as noted below. Should one or more of

these risks or uncertainties materialize, or should underlying assumptions prove

incorrect, our actual results could differ materially from those anticipated in

these forward-looking statements. Actual events, transactions and results may

materially differ from the anticipated events, transactions or results described

in such statements. Although we believe that our expectations are based on

reasonable assumptions, we can give no assurance that our expectations will

materialize. Many factors could cause actual results to differ materially from

our forward looking statements including those set forth in Item 1A of this

report. Other unknown, unidentified or unpredictable factors could materially

and adversely impact our future results. We undertake no obligation and do not

intend to update, revise or otherwise publicly release any revisions to our

forward-looking statements to reflect events or circumstances after the date

hereof or to reflect the occurrence of any unanticipated events.

We file

reports with the Securities and Exchange Commission (“SEC” or “Commission”). We

make available on our website (http://www.andatee.com) free of charge our public

reports filed pursuant to the Exchange Act and amendments to those reports as

soon as reasonably practicable after we electronically file such materials with

or furnish them to the SEC. Information appearing at our website is not a part

of this Annual Report on Form 10-K. You can also read and copy any materials we

file with the Commission at its Public Reference Room at 100 F Street, NE,

Washington, DC 20549. You can obtain additional information about the operation

of the Public Reference Room by calling the Commission at 1-800-SEC-0330. In

addition, the Commission maintains an Internet site (www.sec.gov) that contains

reports, proxy and information statements, and other information regarding

issuers that file electronically with the Commission, including our

reports.

Our

fiscal year begins on January 1, and ends on December 31, and any references

herein to “Fiscal 2009” mean the year ended December 31, 2009, and references to

other “Fiscal” years mean the year ending December 31, of the year

indicated.

We

obtained statistical data, market data and other industry data and forecasts

used in this Form 10-K from publicly available information. While we believe

that the statistical data, industry data, forecasts and market research are

reliable, we have not independently verified the data, and we do not make any

representation as to the accuracy of that information.

Except

where the context otherwise requires and for purposes of this Annual

Report:

|

|

·

|

the

terms “we,” “us,” “our company,” “our” refer to Andatee China Marine Fuel

Services Corporation, a Delaware corporation, its subsidiaries Goodwill

Rich International Limited and Dalian Fusheng Consulting Co. Ltd., its

variable interest entity (VIE), Dalian Xingyuan Marine Bunker Co. Ltd.,

through which entity we conduct all of our business operations, and the

subsidiaries of our VIE entity, which are Donggang Xingyuan Marine Bunker

Company Ltd., Xiangshan Yongshinanlian Petrol Company Ltd., and Rongcheng

Xinfa Petrol Company Ltd.;

|

|

|

·

|

the

term “Andatee” refers to Andatee China Marine Fuel Services Corporation,

the parent company;

|

|

|

·

|

the

term Goodwill’’ refers to Goodwill Rich International Limited, a

subsidiary of Andatee, which for financial reporting purposes is the

predecessor to Andatee; and

|

|

|

·

|

“China”

and “PRC” refer to the People’s Republic of China, and for the purpose of

this Annual Report only, excluding Taiwan, Hong Kong and

Macau.

|

1

The

standard barrel of 42 US gallons is used in the United States as a measure of

crude oil, and the producers of other petroleum products as reported on the US

commodities or stock exchanges tend to convert their production volumes into

barrels for global reporting purposes. Elsewhere in the world, oil is commonly

measured in liters or cubic meters (1,000 liters equals one cubic meter, and 159

liters equals one US 42 gallon barrel) or in tons (the latter customarily used

by European oil companies). The fuel oils produced by the company, however, are

qualitatively different products from crude oil. In its essence, they are types

of heavy oil, with densities ranging from 0.82 to 0.95, thus, making it

impracticable to use US barrels for measuring and reporting purposes. In

addition, all of the company supply, vendor and client contracts are executed in

tons, not in barrels.

The

conversion chart below illustrates the conversions between barrels or liters and

tons, as applied to our product line:

|

Product#

|

Temperature

|

Density

|

Liters/Ton

|

Barrels/Ton

|

||||

|

2#

|

20°C

|

0.850

|

1,176

|

7.40

|

||||

|

3#

|

20°C

|

0.895

|

1,117

|

7.03

|

||||

|

4#

|

20°C

|

0.947

|

1,056

|

6.64

|

||||

|

120CST

|

20°C

|

0.988

|

1,012

|

6.36

|

||||

|

180CST

|

20°C

|

0.988

|

1,012

|

6.36

|

This

Annual Report contains translations of certain Renminbi, or RMB, the legal

currency of China, amounts into U.S. dollars at the rate of RMB6.8225 to $1.00,

the noon buying rate in effect on December 31, 2009, in New York City for cable

transfers of Renminbi as certified for customs purposes by the Federal Reserve

Bank of New York. We make no representation that the Renminbi or U.S. dollar

amounts referred to in this report could have been or can be converted into

U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.

On February 22, 2010, the noon buying rate was approximately RMB6.83 to

$1.00.

Unless

the context indicates otherwise, all share and per share data in

this report give effect to a 1-for-1.333334 reverse share split that became

effective on October 19, 2009.

|

Item

1.

|

Business

|

Overview

of our Company

We carry

out all of our business through our Hong Kong subsidiary, Goodwill, its

wholly-owned Chinese subsidiary, Fusheng, and Fusheng’s variable interest entity

(VIE), Dalian Xingyuan, and Dalian Xingyuan’s subsidiaries (Dalian Xingyuan and

its subsidiaries being collectively referred to as the VIE

entities). Through these VIE entities, we are engaged in the

production, storage, distribution and wholesale purchases and sales of blended

marine fuel oil for cargo and fishing vessels with operations mainly in

Liaoning, Shandong and Zhejiang Provinces in People’s Republic of China (PRC).

We compete by providing our customers value added benefits, including

single-supplier convenience, competitive pricing, logistical support and fuel

quality control. Our sales of marine oil for fishing boats represented

approximately 79% of our total revenue for the period 2006 − 2009 as compared

with the sale of marine oil for cargo vessels which represented the remaining

21% of our total revenue for the same periods. Currently, we sell approximately

57% of our products through distributors and approximately 43% to retail

customers. Our products are substitutes for diesel used throughout east China

fishing industry by small to medium sized cargo vessels. Our core facilities

include as storage tanks, berths (the space allotted to a vessel at the wharf),

marine fuel pumps, blending facilities and tankers. Our sales network covers

major depots along the towns of Dandong, Shidao and Shipu along the east coast

of China.

Our

operations in China are conducted through our VIE, Dalian Xingyuan Marine Bunker

Company, Ltd and its three subsidiaries: Donggang Xingyuan Marine Bunker

Company, Ltd. (located in Dandong City, Liaoning Province, and established in

April 2008 under the laws of the PRC), Xiangshan Yongshi Nanlian Petrol Company,

Ltd. (located in Xiangshan City, Zhejiang Province, and established in May 1997

under the laws of the PRC) and Rongcheng Xinfa Petrol Company, Ltd. (located in

Rongcheng City, Shandong Province, and established in September 2007 under the

laws of the PRC).

Our

marine fuel for cargo vessels is classified as CST180 and CST120; our marine

fuel for fishing boats/vessels, - #2 fuel (for engines with 1,800 rpm capacity),

#3

fuel (for engines with 1,600 rpm capacity) and #4 fuel (for engines with 1,400

rpm capacity). We also produce blended marine fuel according to customer

specifications using our proprietary blending technology. Our own blend of

Marine Diesel Oil, #3 fuel and #4 fuel are substitutes for the traditional

diesel oil, commonly known as #0 diesel oil, used by most small to medium

vessels. We generate virtually all of our revenues from our own brands of

blended oil products.

2

Andatee

China Marine Fuel Services Corporation is a Delaware corporation. Our

executive offices are located in the City of Dalian, a key international

shipping hub and international logistics center in North China. Our main offices

are located in the city of Dalian, Dalian Ganjingzi District, Dalian Wan

Lijiacun, at Unit C, No. 68 West Binhai Road, Xigang District Dalian, China. Our

telephone and fax numbers are (86411) 8360 4683 and (86411) 8360 4683,

respectively. Our website address is http://www.andatee.com. The information on

our website is not part of this Annual Report.

The

following map shows locations of our VIE’s in various parts across the coast of

east China:

Organizational

Structure and Corporate History

Our VIE

operating entity, Dalian Xingyuan, has three subsidiaries: Donggang Xingyuan

Marine Bunker Company Ltd. (located in Dandong City, Liaoning Province, and

established in April 2008 under the laws of the PRC), Xiangshan Yongshinanlian

Petrol Company Ltd. (located in Xiangshan City, Zhejiang Province, and

established in May 1997 under the laws of the PRC) and Rongcheng Xinfa Petrol

Company Ltd. (located in Rongcheng City, Shandong Province, and established in

September 2007 under the laws of the PRC). Dalian Xingyuan and its three

subsidiaries are collectively referred to as the ‘‘VIE’’. Dalian Xingyuan was

established in September 2001 with a registered capital of RMB7 million and

began providing refueling services to the marine vessels in Dalian Port in

Dalian City. The Board of Directors of Dalian Xingyuan consists of 3 members,

including An Fengbin, Wang Yu and Liu Shaoyuan. Mr. An is Chairman of the Board

and General Manager of Dalian Xingyuan. Upon the October 28, 2008 incorporation

of Goodwill, Goodwill and the shareholders of Dalian Xingyuan had entered into a

series of separate agreements under which Goodwill and Dalian Xingyuan were

deemed, until March 2009, to be under the common control of the shareholders of

Dalian Xingyuan.

We

conduct all of our business operations through Dalian Xingyuan, our operating

entity, wihch was established in September 2001 with a registered capital of

RMB7 million and began providing refueling services to the marine vessels in

Dalian Port in Dalian City. We do not own any equity interests in Dalian

Xingyuan. Our relationships with Dalian Xingyuan and its shareholders are

governed by a series of contractual arrangements Dalian Xingyuan has with our

wholly-owned onshore subsidiary, Dalian Fusheng Consulting Co., Ltd.

(“Fusheng”). Under Chinese laws, each of Fusheng and Dalian Xingyuan is an

independent legal entity and neither of them is exposed to liabilities incurred

by the other party. Other than pursuant to the contractual arrangements between

Fusheng and Dalian Xingyuan, Dalian Xingyuan does not transfer any other funds

generated from its operations to Fusheng. Fusheng entered into these contractual

arrangements with Dalian Xingyuan in March 2009, as discussed in detail below.

Subsequently, Fusheng assigned its rights under these contractual arrangements

to us. Thus, we control and receive the economic benefits of their

business operations through contractual arrangements. Dalian Xingyuan holds the

licenses and approvals necessary to operate its business in China. We have

contractual arrangements with Dalian Xingyuan and its shareholders pursuant to

which we provide technology consulting and other general business operation

services to Dalian Xingyuan. Through these contractual arrangements, we also

have the ability to substantially influence Dalian Xingyuan’s daily operations

and financial affairs, since we are able to appoint its senior executives and

approve all matters requiring shareholder approval. As a result of these

contractual arrangements which enable us to control Dalian Xingyuan and to

receive, through our offshore subsidiary and VIE’s, all of Dalian Xingyuan’s

profits, we are considered the primary beneficiary of Dalian Xingyuan.

Accordingly, we consolidate Dalian Xingyuan’s results, assets and liabilities in

our financial statements, which is a typical arrangement for companies that are

traded and registered in the United States that maintain operations in the

PRC.

In 2003,

Xingyuan became the sole supplier of fuel oil to China Shipping Group Co.,

Ltd.’s vessels in Dalian. In 2005, through our partnership with the Dalian

University of Technology, Xingyuan successfully developed its own blend of

marine fuel as an alternative fuel substitute which, while reducing cost by

approximately 20%, maintains the same energy efficiency as major marine fuel

brands. Following the success of our fuel substitutes, we established

distribution centers in Shandong Shidao, Liaoning Donggang and Zhejiang Nanlian.

Before October 2007, we were a joint venture company through a subsidiary of

China Petroleum in Northern China, which is the largest petroleum company in the

PRC. We purchased 100% of the joint venture and commenced our operations as a

private company. Xingyuan also developed the blending ability for CST120 and

CST180 brands of its fuel which are used for cargo vessels.

3

In

December 2008, Xingyuan entered into an agreement with the shareholder of

Xiangshan Nanlian, which is located in the town of Shipu, Xiangshan county,

Zhejiang Province. We purchased a 63% ownership stake in Xiangshan Nanlian for a

purchase price of approximately $2.2 million (RMB15.12 million). Also in late

December 2008, we entered into an agreement with shareholders of Rongcheng Xinfa

to acquire its 90% ownership stake in the entity for a purchase price of

approximately US$1.45 million (RMB9.9 million). The purpose of these agreements

was to establish and extend our distribution network in an orderly and sustained

way. Subsequently, on March 26, 2009, Fusheng, Xingyuan and the shareholders of

Xingyuan entered into a series of agreements, including the Consulting Services

Agreement, the Operating Agreement, the Equity Pledge Agreement, the Option

Agreement and the Proxy and Voting Agreement. Xingyuan entered into these

agreements with Fusheng because of the PRC laws and regulations restricting the

ability of offshore entities to acquire or dispose of ownership of domestic

companies. These agreements ensure that the original minority shareholders of

Xingyuan will regain their respective pro rata ownership upon triggering of the

conditions set forth in the agreements. Under these agreements, the Company

obtained the ability to direct the operations of Xingyuan and its subsidiaries

and to obtain the economic benefit of their operations. Therefore, management

determined that Xingyuan became a variable interest entity and the Company was

determined to be the primary beneficiary of Xingyuan and its subsidiaries.

Accordingly, beginning March 26, 2009, the Company has consolidated the assets,

liabilities, results of operations and cash flows of Xingyuan and its

subsidiaries its financial statements.

In August

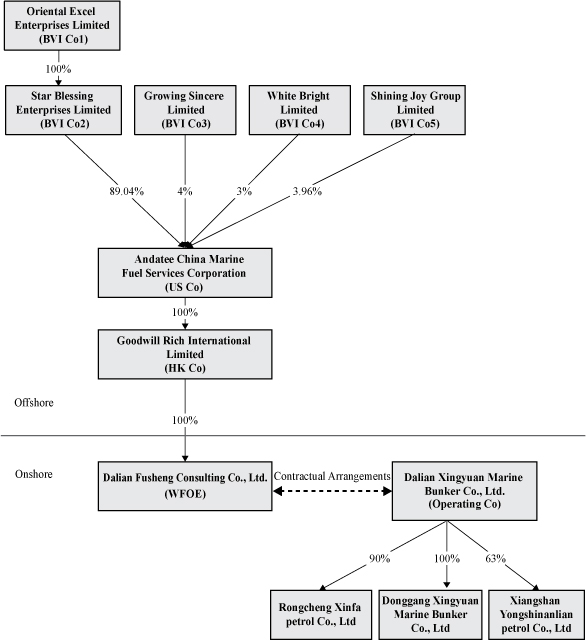

2009, Andatee entered into a share exchange agreement (the “Exchange Agreement”)

with all of the shareholders of Goodwill Rich International Limited, a Hong Kong

company (“Goodwill”). Pursuant to the Exchange Agreement, Andatee agreed to

issue 6,000,000 shares of its common stock in exchange for all of the issued and

outstanding securities of Goodwill (”Share Exchange”). The Goodwill shareholders

included Star Blessing Enterprise Limited (“SBE”), a company organized under the

laws of the British Virgin Islands, (i) Growing Sincere Limited (“GSL”) a

company organized under the laws of the British Virgin Islands, (ii) White

Bright Limited (“WBL”), a company organized under the laws of the British Virgin

Islands, and (iii) Shining Joy Group Limited (“SJG”) a company organized under

the laws of the British Virgin Islands. Prior to the Share Exchange, SBE, GSL,

WBL and SJG beneficially owned 89.04%, 4%, 3% and 3.96% of equity securities in

Goodwill, respectively. The Share Exchange closed on October 16, 2009. Andatee

did not issue any fractional shares in connection with the Share Exchange. Upon

the closing of the Share Exchange, Andatee (i) became the 100% parent of

Goodwill, and its wholly-owned subsidiary, Dalian Fusheng Consulting Co., Ltd.,

and (ii) assumed the operations of Goodwill and its subsidiaries. The

transactions contemplated by the Exchange Agreement, as amended, were intended

to be a ‘‘tax-free’’ incorporation pursuant to the provisions of Section 351 of

the Internal Revenue Code of 1986, as amended. The organization of Andatee and

its acquisition of Goodwill Rich did nothing more than to change the name of

Goodwill Rich to Andatee, change its place of incorporation/organization, and

change its capital structure from 10,000 shares outstanding to 8,000,000 shares

outstanding (prior to the October 2009 reverse stock split). For financial

reporting purposes, the Share Exchange will be accounted for as a

recapitalization of Goodwill affected through a combination of companies

(Andatee and Goodwill) under common control, which will be recorded at

historical cost. As a result, Goodwill is deemed to be the predecessor of

Andatee for financial reporting purposes, and the historical financial

statements of Goodwill presented in this report will become the historical

financial statements of Andatee (after being adjusted to retroactively reflect

the effects of the recapitalization to 6,000,000 issued and outstanding common

shares) at such time as Andatee issues financial statements for the period that

includes October 16, 2009.

On

October 16, 2009, our Board approved a reverse split in the 1-for-1.333334

ratio. Following shareholder approval of the split, we effected the split on

October 19, 2009. Immediately following the reverse stock split, all outstanding

shares of our common stock was exchanged for the newly issued shares of common

stock on the basis of the reverse split ratio. The par value of common stock was

not affected by the split. As a result of the split, the number of shares

available for future issuances has increased and the number of currently

outstanding shares of our common stock decreased. The purpose of the split was

to recapitalize all of our outstanding shares of capital stock into shares of

the same class of common stock to be sold in the January 2010 initial public

offering.

The

following diagram illustrates our corporate structure following the consummation

of the Exchange Agreement:

Industry

Overview

According

to Oil & Gas Journal (OGJ), China had 18.3 billion barrels of proven oil

reserves as of January 2006, flat from the previous year. EIA estimates that

China will produce 3.8 million barrels per day (Mmbbl/d) of oil in 2006,

slightly higher than the previous year. Of this, 96% is expected to be crude

oil. EIA estimates that China will consume 7.4 Mmbbl/d of oil in 2006,

representing nearly a half million barrels per day increase from 2005. For 2006,

EIA data forecasts that China’s increase in oil demand will represent 38% of the

world total increase in demand. China’s petroleum industry has undergone major

changes over the last decade. In 1998, the Chinese government reorganized most

state owned oil and gas assets into two vertically integrated firms: the China

National Petroleum Corporation (CNPC) and the China Petroleum and Chemical

Corporation (Sinopec). Each of these companies operates a range of local

subsidiaries. The other major state sector firm is the China National Offshore

Oil Corporation (CNOOC), which handles offshore exploration and production and

accounts for roughly 15% of China’s domestic crude oil

production.

4

According

to OGJ, China had 6.2 Mmbbl/d of crude oil refining capacity as of January 2006.

Sinopec and CNPC are the two dominant players in China’s oil refining sector.

The expansive sector is undergoing modernization and consolidation, with dozens

of small refineries shut down in recent years and larger refineries expanding

and upgrading their existing facilities. In July 2006, PetroChina completed the

expansion of its Dalian refining center, raising the plant’s capacity from

210,000 bbl/d to 410,000 bbl/d, making it the largest refinery in China. China

has been ranked the highest in the world for the volume of the cargo and

container output for the last 5 consecutive years. According to the National

Development and Reform Commission and the National Bureau of Statistics of

China, in 2007, total logistics industry output increased to RMB 75,228.3

billion, or by 26.2%. The same report estimated that by 2010, the total industry

output will reach RMB 1.2 trillion, with 20% growth annually. By the end of

2007, China had 14 harbors with 100 million ton capacity, up from 12 in 2006. In

total, there are over 1,400 harbors in China with more than 35,000 dock berth

with cargo capacity of 3.4 billion tons and 61.5 million shipping containers.

Also, in 2007, China sea infrastructure and logistics industries added RMB 341.4

billion in value, an increase of more than 21%. In 2007, the total fuel

consumption in the PRC exceeded 40.7 billion tons; for the same period, the

total consumption by region, including Liaoning, Shandong and Zhejiang

Provinces, where we primarily operate, was in excess of 818 million

tons.

The

market for oil for small and medium size vessels, i.e. less than 3,000 tons, is

very fragmented with no discernible market leader. It is characterized by

intense price competition, uneven product and service quality and is dominated

by many small fuel trading companies. Most of these trading companies do not

have stable supply sources or a strong working capital to withstand market risk.

Unstable supplies often lead to chronic shortages of oil in the market resulting

in black market operations and counterfeit products. Boats and vessels operators

when docking at berths for refueling are often at the mercy of oil merchants

selling them assortments of fuel oil from various suppliers in the market. Boat

and vessel operators are at high risk when oil merchants market them poor

quality oil or counterfeit products that have insufficient energy efficiency or

cause damages to engines. Therefore, our experience has consistently shown that

vessel operators are willing to pay a premium for consistent quality products

and services.

Our

Products and Services

We blend

and supply marine fuel as an alternative fuel for Chinese cargo and fishing

vessels. Our sales of fuel for fishing boats represented approximately 79% of

our total revenue for the period 2006 − 2009 as compared with the sale of fuel

for cargo vessels which represented the remaining 21% of our total revenue for

the same periods. Our cargo vessel fuel is designated as CST180 and CST120;

fishing boat/vessel fuel - #2 fuel (for engines with 1,800 rpm capacity), #3

fuel (for engines with 1600 rpm capacity) and #4 fuel (for engines with 1400 rpm

capacity). We also blend fuel to specific customer specifications using our

proprietary blending technology. Our own blend of Marine Diesel Oil, #3 fuel oil

and #4 fuel oil are able to replace the traditional diesel oil, commonly known

as #0 diesel oil, used by most small to medium vessels and boats. Currently, we

sell approximately 57% of our products through distributors and approximately

43% of our products to retail customers. Fuel is classified into 6 classes,

numbered 1 through 6, each according to its boiling point, composition and

purpose. The boiling point, in the range of 175 − 600°C, and carbon chain

length, in the range of 20 − 70 atoms, of the fuel increases with fuel number,

i.e. the higher the class number, the higher the boiling point and the carbon

chain length as well as oil’s viscosity. Price of oil, on the other hand,

usually decreases as the fuel number increases since higher number fuel must be

heated to overcome its viscosity.

The

following table represents the description of our sales organized by product and

geographical markets for the periods 2006 − 2009:

|

Year

ended December 31

|

||||||||||||||||||||||||

|

2009

|

2008

|

2007

|

||||||||||||||||||||||

|

Tons

|

%

|

Tons

|

%

|

Tons

|

%

|

|||||||||||||||||||

|

(in thousands)

|

(in thousands)

|

(in thousands)

|

||||||||||||||||||||||

|

Products

|

||||||||||||||||||||||||

|

2#

|

17.18 | 7.14 | % | - | 0 | % | - | 0 | % | |||||||||||||||

|

3#

|

22.81 | 9.48 | % | 18.58 | 14.58 | % | 7.13 | 3 | % | |||||||||||||||

|

4#

|

151.93 | 63.17 | % | 90.49 | 71 | % | 169.08 | 72 | % | |||||||||||||||

|

180CST

|

31.47 | 13.08 | % | 15.99 | 12.58 | % | 49.14 | 20.9 | % | |||||||||||||||

|

120CST

|

17.12 | 7.12 | % | 2.37 | 1.86 | % | 9.38 | 4.1 | % | |||||||||||||||

|

Areas

|

||||||||||||||||||||||||

|

Dalian

|

91.03 | 37.85 | % | 40.89 | 32.09 | % | 84.95 | 36.2 | % | |||||||||||||||

|

Shandong

|

109.48 | 45.52 | % | 79.08 | 62.06 | % | 149.79 | 63.8 | % | |||||||||||||||

|

Donggang

|

20.16 | 8.38 | % | 7.45 | 5.85 | % | - | 0 | % | |||||||||||||||

|

Zhejiang

|

19.85 | 8.25 | % | - | 0 | % | - | 0 | % | |||||||||||||||

5

Our

Competitive Strengths

Our

business objective is to become the premium ‘‘one-stop’’ marine service provider

for cargo, fishing and other vessels in China through our integrated

distribution networks. We believe that our business model offers competitive

advantages over our current market competition through:

|

|

·

|

Product Superiority and Price

Competitiveness - our blended marine fuel is price competitive as

compared with various brands of diesel oil available in the local PRC

market. In fact, based on quarterly 2009 price data, our blended fuel

(#4), while maintaining the same fuel efficiency, is, on average, US$144

per ton cheaper than the leading diesel fuel

brand.

|

|

|

·

|

Brand Recognition - our

consistent, what we believe to be superior product quality over the years

has resulted in our dominance in the fishing boat and vessel market in the

provinces where we maintain our operations. Through our VIE entities, we

are the largest privately owned company engaged in marine fuel industry in

northern China. We intend to take advantage of our brand to increase our

customer base and to leverage our brand and build an integrated

distribution system for our range of related oil products and services. We

believe our strong branding has allowed us to develop a broad base of

end-user customers, expand our sales channels and facilitate more rapid

acceptance of our new products.

|

|

|

·

|

Reliability of Our Supplies of

Raw Materials - We have stable and reliable raw material suppliers

for our production. Our relationships with upstream suppliers enables us

to be a low cost producer. We have a long-standing relationship with China

Petroleum (particularly, Dalian, Panjin and Liaoyang Branched) which,

combined, provided over 60% of all raw materials we require per year, in

2008 − 2009 with other suppliers, including Beijing XSSB, Fushun XC,

Qingdao Anbang, providing the remaining of our need for raw materials. We

will continue to explore new suppliers to reduce supply risk as

needed.

|

|

|

·

|

Extensive Sales and

Distribution Network - Our distribution consists of approximately

25 distributors throughout China in three provinces, we believe our

distribution network is one of the largest among marine fuel suppliers in

China. We are acquiring and building new facilities, which consist of

blending plants, storage tanks, and fueling ports, close to some of our

end customers or to a particular market in order to improve our product

distribution capacity. We focus on timely delivery and good customer

service. In addition our storage facilities are located close to our

customers, enabling us to sell directly to them resulting in lower

logistics costs. It also allows us to provide better after sales service

and to maintain a close relationship with our key distributors through

regular meetings, discussions and customer visits. Among our distributors,

in 2008, Zhonghai Dalian and Shidao Hekou represent 16% and 13% of our

sales, respectively.

|

|

|

·

|

Innovation and R&D

capabilities - We strive to identify market trends and developments

in the marine fuel industry and use our blending technology to produce

quality oils to satisfy the market demand. Since 2003, we have developed

more than 5 new products as a result of our research and development

capabilities. We operate several dedicated research and development

facilities with 3 professionals and collaborate with universities and

institutes, including Dalian University of Technology. We believe our

investment in research and development has enabled us to continuously

expand our product offerings and proactively anticipate market changes in

our industry.

|

|

|

·

|

Stringent Quality

Control - We have stringent quality control systems at all stages

of the blending process. Our periodic quality tests of our blended

products are conducted by the team of trained scientific personnel which

represent the area’s leading technical institutes and universities. We

test the consistency and quality of our blended products and adjust the

various components on an ‘‘as needed’’ basis. In addition, the quality of

our testing process is periodically and independently verified by the

governmental agencies in charge of overseeing quality and safety standards

of the oil products supplied in the

marketplace.

|

|

|

·

|

Strong Management Team

- We have key management staff that has extensive experience and technical

skills in oil processing, refining and blending

technology.

|

Our

Strategies

Our

strategy is to capitalize on our competitive strengths to expand our current

market penetration. We plan to grow our business by pursuing the following

strategies:

6

|

|

·

|

Expand our Product

Offerings - We are focused on becoming a ‘‘one-stop’’ product

supplier for our end-user customers. We plan to continue expanding our

product offerings to increase the customization of marine fuels and

address the key elements of our end-user customers’ needs for lower

prices, easier access to fuel and a wide variety of complementary

services. We believe offering these integrated systems will promote higher

end-user customer satisfaction, higher margins, the establishment of

long-term service contracts to maintain the systems and increased barriers

to entry for potential competitors.

|

|

|

·

|

Focus on Advanced

Technologies - We are currently utilizing our research and

development capabilities to develop new blending processes and

applications. We believe there will be a growing demand for products

possessing such features as governments, businesses and consumers become

increasingly focused on sustainable economic growth and environmental

issues. We follow advanced project selection procedures prior to the

development of new products, including the use of detailed market and

technological analyses. All new products are subject to rigorous testing

at our facilities prior to production and sample products are often

delivered to end-user customers for their trial use. We begin

manufacturing new products only after the sample product from a trial

production passes internal inspection and achieves customer satisfaction.

This integrated approach allows us to identify potential difficulties in

commercializing our product and make adjustments as necessary to develop

cost-efficient manufacturing processes prior to mass production. We

recognize the importance of customer satisfaction for our newly-developed

products and continue to seek feedback from our end-user customers even

after the formal launch of a

product.

|

|

|

·

|

Pursue Selective Strategic

Acquisitions - While we have experienced substantial organic

growth, we plan to pursue a disciplined and targeted acquisition strategy

to accelerate our growth. Our strategy will focus on obtaining

complementary product offerings and locations, product line extensions,

research and development capabilities and access to new markets and

customers. We seek vertical growth through the acquisition of retail

facilities which increase revenue line by having these newly acquired

facilities to purchase more goods from parent and enjoying the profit

margin on wholesale and retail distribution. Our acquisitions have

historically enabled us to increase our product and service offerings and

expand into other geographies. We may continue to acquire companies that

provide us with storage capacities, customer and distribution network

access. We expect that our acquisition targets will have the same core

expertise as we do, maintain suitable storage facilities/berth locations,

an established customer base to market our existing line of products and

services. We anticipate that this strategy will enhance our time to market

and our customer base, and will reduce local market entry risk. We intend

to target profitable companies with annual revenues of at least US$6

million. Our proposed strategy is to acquire an entity at a discount to

public company trading multiples at a purchase price consisting of cash

and common stock at closing, contingent earn-out cash payments payable

upon the attainment of post-closing performance

milestones.

|

|

|

·

|

Increase Our Market Share in

China - We plan to continue to expand our market share of the

industry in China. To do so, we are developing additional advanced

products across our comprehensive product lines, which will further create

cross-selling opportunities and production and marketing synergies. We

also intend to increase our marketing activities and are actively seeking

to increase the number of distributors carrying our products, specifically

new distributors that will provide us with greater access to a wider range

of end-user customers.

|

|

|

·

|

Expand Our Blending Capacity

and Increase In-house Production - We currently plan to build new

manufacturing and blending facilities and production lines to produce new

brands of marine fuel products. We also plan to improve and upgrade our

existing manufacturing facilities and production lines to enhance our

quality control and to meet increasing demand for our current products.

With the increased manufacturing capacity, we also expect to bring

additional production steps in-house and increase the in-house

manufacturing of certain core components to further improve our cost

structure, the protection of our intellectual property, the quality and

performance of our products and our operational

efficiencies.

|

Sales

& Marketing

Our main

customers are located in Liaoning, Shandong and Zhejiang Provinces. Currently,

we have eight full-time sales and marketing personnel responsible for promoting

our products and services to our customers and distributors. We maintain close

relationships with our key customers through regular meetings and discussions to

keep them updated on the variety of products and services we offer. In addition,

we maintain strong relationships in our local communities and government for

favorable business expansion in each individual geographical area. Our sales and

marketing approach varies depending on the peculiarities of a particular market.

In Shandong Province, for instance, our focus has been on partnering with

certain owners of the local oil storage tanks and reservoirs whose facilities

are generally underutilized, which allows us certain additional storage

capacity, up to an additional 8,000 tons a month in that Province. In Zhoushan

City, Zhejiang province, on the other hand, we sell raw materials to our

customers who then blend such raw materials into final products and sell them in

the market.

7

Supply

of Raw Materials

Although

we intend to diversify our raw material supplies by engaging international

sources, presently, we purchase all of our raw materials only from Chinese

suppliers. Our operating company, Xingyuan, maintains a contractual relationship

with Panjin Liaohe Oil Field Dali Group Petrochemical Co., Ltd. (“Panjin”) for

purchases of wax fuel oil, which we commenced in October 2005, which provides

over 20% of all raw materials as we need every year. These contracts are renewed

on a monthly basis whereby the quantities of oil purchased vary from period to

period at then prevailing market prices. We purchase our heavy oil from

PetroChina Company Limited, the largest oil and gas producer and distributor in

China, from its Huhehaote refinery, in the amount of approximately 1,000 tons

per month at prevailing market prices. Xingyuan also purchases, at market

prices, rubber filling oil and extract oil from PetroChina Dalian Petrochemical

Company in amounts of 3,000 − 5,000 and 3,000 tons per month, respectively,

which provides over 30% of all raw materials as we need every year. These

contracts are also renewed on a monthly basis whereby the quantities of oil

purchased vary from period to period at then prevailing market prices.

Similarly, Xingyuan maintains a contractual relationship with Qingdao Anbang

Refining and Chemical Co., Ltd. (“Qingdao”) for our needs of catalytic diesel

oil. These contracts are also renewed on a rolling monthly basis whereby the

quantities of oil purchased vary from period to period at then prevailing market

prices. We commenced our relationship with Qingdao in February 2007. The use of

domestic, local suppliers in close proximity to our facilities enables us to

closely monitor the quality of the raw supplies obtained from such suppliers,

provide technical training relating to our raw material requirements and suggest

technical improvements. We obtain raw materials and components from suppliers

through non-exclusive purchase orders and supply contracts. The purchase order

or contract specifies the price for the raw material. Although we allow for

adjustments in the price for certain raw materials under extraordinary

circumstances, the prices for our materials are generally fixed for the

effective term of the purchase agreement. Our contracts with our suppliers are

generally renewable on an annual basis, but the price is not fixed and remains

flexible and reflective of the prevailing market conditions. We typically

negotiate with our suppliers to renew supply contracts at the beginning of each

year, taking into account the quality and consistency of the materials and

services provided. We maintain multiple supply sources for each of our key raw

materials so as to minimize any potential disruption of our operations and

maintain sourcing stability.

In 2007,

2008 and 2009, purchases from PetroChina Dalian Petrochemical Company (as

described above), our largest supplier, accounted for 39.9%, 46.3% and 33.4%,

respectively, of our total purchases of raw materials. For the same periods, our

ten largest suppliers combined accounted for 78%, 86% and 92%, respectively, of

our total purchases of raw materials. The raw materials required for our

products are low value crude oil refinement byproducts which conventionally are

disposed of by the major oil producing and refining companies. We negotiate

prices for our raw material supplies on a monthly basis to accommodate for our

short-term production requirements.

We

maintain a procurement team that has established relationships with various raw

material suppliers to ensure constant and reliable supply. In addition, we have

successfully employed and continue to employ a number of methods to hedge

against the risks of fluctuations in the raw material prices. Namely,

we:

|

|

·

|

Shorten

our production cycle from 30 to 14 days to reduce the price

risk;

|

|

|

·

|

Review

raw material price agreements on a weekly

basis;

|

|

|

·

|

Reduce

purchase amounts, or buy on an ‘‘as needed’’

basis;

|

|

|

·

|

Place

our blending facilities in close proximity to our customers to reduce

delivery time;

|

|

|

·

|

Increase

the proportion of direct sales to end users by building more

infrastructure to reduce reliance on

distributors;

|

|

|

·

|

Leverage

our brand, i.e. seek customers who are willing to pay quality and brand

premium.

|

Quality

Control

We have

implemented a rigid quality control system and devote significant attention to

quality control procedures at every stage of our process. We monitor our

manufacturing process closely and conduct performance and reliability testing to

ensure our products meet our end-user customer expectations. Our quality control

group as of December 31, 2009 included 7 employees that implement various

management systems to improve product quality programs. We inspect our raw

materials to ensure compliance with quality standards. We also evaluate the

quality and delivery performance of each supplier periodically and adjust

quantity allocations accordingly. We also monitor in-process and outgoing stages

of our processes.

8

Seasonality

The

Chinese government prohibits fishing boats and vessels from fishing from June

15th to September 15th of each year, the breeding season for many varieties of

fish, in order to protect marine resources and prevent overfishing. As a result,

the demand for our blended fuel drops by approximately 15% during this period.

In addition, we are also subject to the reduced commercial activity during the

Chinese New Year, the most important of the traditional Chinese holidays. During

this time, both cargo and fishing traffic decrease and we expect the demand for

our products to decrease accordingly.

Research

& Development

As of

December 31, 2009, we had 7 members in our research and development group. Our

research and development activities are based in our research and development

center located in the City of Dalian, where we maintain 3 laboratories,

including one at the Dalian University of Technology. Each of our laboratories

is staffed with several support personnel and is headed by an experienced member

of the faculty with whom we enter into contractual arrangements to provide

research and development services to the Company. We own all rights, title and

interest in any proprietary information resulting from the research work at our

R & D facilities. In addition to improving our existing product offerings,

our research and development efforts focus on the development of new products,

as well as the development of new production methodologies to improve our

manufacturing processes.

Competition

The

market for oil for small and medium size vessels, i.e. less than 3,000 tons, is

very fragmented with no discernible market leader. We estimate the total value

of this market to be approximately US$1.6 billion as of December 31, 2009. It is

characterized by intense price competition, uneven product and service quality

and is dominated by many small fuel trading companies. Most of these trading

companies do not have stable supply sources or a strong working capital to

withstand market risk, which may lead to chronic shortages of oil in the market.

Boat and vessel operators are at high risk when oil merchants market them poor

quality oil or counterfeit products that have insufficient energy efficiency or

cause damage to engines. Therefore, our experience and market research have

consistently shown that boat and vessel operators are willing to pay a premium

for consistent quality products and services. High barriers of entry for new

entrants into this industry include heavy regulatory hurdles, scarcity of

suitable operation and storage sites, capital intensity and skilled management.

Most of the operational, business and other activities in the storage, refining

and producing industries are heavily regulated and require layers of

governmental consents and approvals. In addition, storage hubs must be located

on sufficiently large sites in strategic locations with close proximity to

industrial ports and harbors with deep water access. Most of the infrastructure

requires significant upfront capital expenditures. Thus, we believe all of the

foregoing fortify our competitive positions in the industry.

Our

industry is characterized by the major national oil companies controlling the

upstream refineries and supplying the end products to the downstream. In

particular for marine fuel oil, China Marine Bunker (China Petrol) Co., Ltd. is

a major participant in the market. In the downstream, there are many traders

selling marine fuel oil in all the provinces feeding from the 1st tier

manufacturers. There are only a limited number of credible manufacturers that

have blending capability of and direct access to raw materials from national

refineries. Our competitors are numerous, ranging from large multinational

corporations, which have significantly greater capital resources, to relatively

small and specialized firms. In addition to competing with fuel resellers, we

also compete with the major oil producers that market fuel directly to the large

shipping companies. Such major oil producers do not include the PRC oil

companies since under the PRC laws, petroleum producers are precluded from

blending oil and oil products. Our business could be adversely affected because

of increased competition from the larger oil companies who may choose to

directly market to shipping companies, or to provide less advantageous price and

credit terms to us than our fuel reseller competitors.

We

believe we have no significant competition in the fuel market for small and

medium vessels. Potential competitors could include major domestic oil producing

and refining companies, including as Sinopec, China Petrol and CNOOC, none of

which are currently active in this marketplace or legally permitted to blend

oil. However, we believe it is unlikely they would enter into this segment of

the market in the near future since the entry opportunities diminish as we

develop our integrated distribution system through acquiring resources and sites

and strengthening our market position, thus creating high barriers to entry,

including regulatory and compliance hurdles capital and storage scarcity,

shortage of skilled management.

9

Insurance

The

insurance industry in China is still at an early state of its development.

Insurance companies in China offer limited business insurance products or offer

them at a high price. Business interruption or similar types of insurance are

not customary in China. We currently maintain insurance coverage with Tianan

Insurance Company Limited of China, which, as of December 31, 2009, was

approximately RMB8,630,000 (US$1,260,000) on our property and facilities and

approximately RMB3,600,000 (US$9,300,000) on our inventory. We do not carry any

third party liability insurance to cover claims in respect of personal injury,

property or environmental damage arising from accidents on our property or

relating to our operations other than on our transportation vehicles. We have

not had a third party liability claim filed against us during the last five

years.

Business,

Ownership, Environmental and Other Regulations

Petroleum

and Refining Industry Regulations

Although

the Chinese government is liberalizing its control over the petroleum and

petrochemical industries, significant government regulations remain. Central

government agencies and their local or provincial level counterparts do not own

or directly control our production facilities. However, they exercise

significant control over the petrochemical industry in areas such as production

quotas, quality standards, allocation of raw materials and finished products,

allocation of foreign exchange and Renminbi loans for capital construction

projects. Since 2003, at the national level, our operations are subject to the

supervision and industrial oversight, to various extent, by the State Assets

Regulatory and Management Commission, by the Ministry of Commerce and the

National Development and Reform Committee. At the local level, we are subject to

the supervision and oversight by the provincial branches of these national

agencies as well as local governments and agencies.

Foreign

Exchange and Dividend Distribution Regulations

The

principal regulations governing foreign currency exchange in China are the

Foreign Exchange Control Regulations (1996), as amended. Under these

regulations, the Renminbi is convertible for current account items, including

the distribution of dividends, interest payments, trade and service-related

foreign exchange transactions. Conversion of the Renminbi for capital account

items, such as direct investment, loans, repatriation of investment and

investment in securities outside China, however, is still subject to the

approval of the SAFE or its competent local branch. The dividends paid by a

subsidiary to its shareholder are deemed income of the shareholder and are

taxable in China. Pursuant to the Administration Rules of the Settlement, Sale

and Payment of Foreign Exchange (1996), foreign-invested enterprises in China

may purchase or remit foreign exchange, subject to a cap approved by the SAFE,

for settlement of current account transactions without the approval of the

SAFE.

The

principal regulations governing distribution of dividends of foreign holding

companies include the Foreign Investment Enterprise Law (1986), as amended, and

the Administrative Rules under the Foreign Investment Enterprise Law (2001).

Under these regulations, foreign-invested enterprises in China may pay dividends

only out of their accumulated profits, if any, determined in accordance with

Chinese accounting standards and regulations. In addition, foreign-invested

enterprises in China are required to allocate at least 10% of their respective

accumulated profits each year, if any, to fund certain reserve funds unless

these reserves have reached 50% of the registered capital of the enterprises.

These reserves are not distributable as cash dividends. Our Chinese VIE’s and

one PRC subsidiary, Fusheng, which are all foreign-invested enterprises, are

restricted from distributing any dividends to us until they have met these

requirements set out in the regulations.

According

to the new EIT law and the implementation rules on the new EIT law, if a foreign

legal person is not deemed to be a resident enterprise for Chinese tax purposes,

dividends generated after January 1, 2008 and paid to this foreign legal person

from business operations in China will be subject to a 10% withholding tax,

unless such foreign legal person’s jurisdiction of incorporation has a tax

treaty with the PRC that provides for a different withholding arrangement. Under

the new EIT law and its implementation rules, if an enterprise incorporated

outside China has its ‘‘de facto management organization’’ located within China,

such enterprise would be classified as a resident enterprise and thus would be

subject to an enterprise income tax rate of 25% on all of its income on a

worldwide basis, with the possible exclusion of dividends received directly from

another Chinese tax resident.

10

On

December 25, 2006, the People’s Bank of China, or PBOC, issued the

Administration Measures on Individual Foreign Exchange Control, and the

corresponding Implementation Rules were issued by SAFE on January 5, 2007. Both

of these regulations became effective on February 1, 2007. According to these

regulations, all foreign exchange matters relating to employee stock holding

plans, share option plans or similar plans in which PRC citizens’ participation

require approval from the SAFE or its authorized branch. On March 28, 2007, SAFE

promulgated the Application

Procedure of Foreign Exchange Administration for Domestic Individuals

Participating in Employee Stock Option Holding Plan or Stock Option Plan of

Overseas Listed Company, or the Stock Option Rule. The purpose of the

Stock Option Rule is to regulate foreign exchange administration of Chinese

citizens who participate in employee stock holding plans and share option plans

of offshore listed companies. According to the Stock Option Rule, if a Chinese

citizen participates in any employee stock holding plans or share option plans

of an offshore listed company, a Chinese domestic agent or the Chinese

subsidiary of the offshore listed company is required to file, on behalf of the

individual, an application with the SAFE to obtain approval for an annual

allowance with respect to the purchase of foreign exchange in connection with

stock holding or share option exercises. This restriction exists because a

Chinese citizen may not directly use offshore funds to purchase stock or

exercise share options. Concurrent with the filing of the required application

with the SAFE, the Chinese domestic agent or the Chinese subsidiary must obtain

approval from the SAFE to open a special foreign exchange account at a Chinese

domestic bank to hold the funds required in connection with the stock purchase

or option exercise, any returned principal profits upon sales of stock, any

dividends issued on the stock and any other income or expenditures approved by

the SAFE. The Chinese domestic agent or the Chinese subsidiary also is required

to obtain approval from the SAFE to open an offshore special foreign exchange

account at an offshore trust bank to hold offshore funds used in connection with

any employee stock holding plans. All proceeds obtained by a Chinese citizen

from dividends acquired from the offshore listed company through employee stock

holding plans or share option plans, or sales of the offshore listed company’s

stock acquired through other methods, must be remitted back to China after

relevant offshore expenses are deducted. The foreign exchange proceeds from

these sales can be converted into Renminbi or transferred to the individuals’

foreign exchange savings account after the proceeds have been remitted back to

the special foreign exchange account opened at a Chinese bank. If share options

are exercised in a cashless exercise, the Chinese individuals exercising them

are required to remit the proceeds to the special foreign exchange account.

Although the Stock Option Rule has been promulgated recently and many issues

require further interpretation, we and our Chinese employees who have been or

will be granted share options or shares will be subject to the Stock Option

Rule, as an offshore listed company.

Employee

Stock Option Regulations

Under

SAFE Notice No. 106, employee stock holding plans of offshore special purpose

companies must be filed with the SAFE, and employee share option plans of

offshore special purpose companies must be filed with the SAFE while applying

for the registration for the establishment of the offshore special purpose

company. After the employees exercise their options, they must apply for the

amendment to the registration for the offshore special purpose company with the

SAFE. If we or our Chinese employees fail to comply with the Stock Option Rule,

we and/or our Chinese employees may face sanctions imposed by foreign exchange

authority or any other Chinese government authorities.

On August

8, 2006, six Chinese regulatory agencies, including the Ministry of Commerce,

the State Assets Supervision and Administration Commission, the State

Administration for Taxation, the State Administration for Industry and Commerce,

the CSRC and the SAFE, jointly issued the Regulations on Mergers and

Acquisitions of Domestic Enterprises by Foreign Investors, or the New M&A

Rule, which became effective on September 8, 2006. Under the New M&A Rule,

equity or assets merger and acquisition of Chinese enterprises by foreign

investors will be subject to the approval from the Ministry of Commerce or its

competent local branches. This regulation also includes provisions that purport

to require special purpose companies formed for purposes of offshore listing of

equity interests in Chinese companies to obtain the approval of the CSRC prior

to the listing and trading of their securities on any offshore stock exchange.

As defined in the New M&A Rule, a special purpose vehicle is an offshore

company that is directly or indirectly established or controlled by Chinese

entities or individuals for the purposes of an overseas listing.

The CSRC

approval procedures require the filing of a number of documents with the CSRC

and it would take several months to complete the approval process. The

application of the New M&A Rule with respect to offshore listings of special

purpose companies remains unclear with no consensus currently existing among

leading Chinese law firms regarding the scope of the applicability of the CSRC

approval requirement. A loan made by foreign investors as shareholders in a

foreign-invested enterprise is considered to be foreign debt in China and

subject to several Chinese laws and regulations, including the Foreign Exchange

Control Regulations of 1997, the Interim Measures on Foreign Debts of 2003, or

the Interim Measures, the Statistical Monitoring of Foreign Debts Tentative

Provisions of 1987 and its Implementing Rules of 1998, the Administration

of the Settlement, Sale and Payment of Foreign Exchange Provisions of 1996, and

the Notice of the SAFE in Respect of Perfection of Issues Relating Foreign

Debts, dated October 21, 2005. Under these regulations, a shareholder loan in

the form of foreign debt made to a Chinese entity does not require the prior

approval of the SAFE. However, such foreign debt must be registered with and

recorded by the SAFE or its local branch in accordance with relevant Chinese

laws and regulations. Our Chinese VIE’s and our PRC subsidiary can legally

borrow foreign exchange loans up to their borrowing limits, which is defined as

the difference between the amount of their respective ‘‘total investment’’ and

‘‘registered capital’’ as approved by the Ministry of Commerce, or its local

counterparts. Interest payments, if any, on the loans are subject to 10%

withholding tax unless any such foreign shareholders’ jurisdiction of

incorporation has a tax treaty with China that provides for a different

withholding agreement. Pursuant to Article 18 of the Interim Measures, if the

amount of foreign exchange debt of our Chinese VIE’s and our PRC subsidiary

exceed their respective borrowing limits, we are required to apply to the

relevant Chinese authorities to increase the total investment amount and

registered capital to allow the excess foreign exchange debt to be registered

with the SAFE.

11

Environmental

Regulations

China’s

rapid economic growth over the last two decades has also brought with it several

energy related environmental problems. Environmental pollution from fossil fuel

combustion is damaging human health, air and water quality, agriculture, and

ultimately the economy. Many of China’s cities are among the most polluted in

the world. China is the world’s second-largest source of carbon dioxide

emissions behind the United States. EIA forecasts predict that China will

experience the largest growth in carbon dioxide emissions between now and the

year 2030. The Chinese government has taken several steps to improve

environmental conditions in the country. Chief among these is the new Law on

Renewable Energy, which took effect on January 1, 2006. The new law seeks to

promote cleaner energy technologies, with a stated goal of increasing the use of

renewable energy to 10% of the country’s electricity consumption by 2010 (up

from roughly 3% in 2003).

We are

subject to national and local environmental protection regulations, which

currently impose a graduated schedule of fees for the discharge of waste

substances, require the payment of fines for pollution and provide for the

forced closure of any facility that fails to comply with orders requiring it to

cease or cure certain environmentally damaging practices. We have established

environmental protection systems which consist of pollution control facilities

to treat certain of our waste materials and to safeguard against accidents. We

believe our environmental protection facilities and systems are adequate for the

existing national and local environmental protection regulations.

Employees

As of

December 31, 2009, we had 131 employees, 24 of which are engaged in management,

administration and related areas, and the remaining 107 - in operations at

various local sites throughout the east of China. None of our employees are

represented by a labor union or collective bargaining agreements. We consider

our employee relations to be good.

Intellectual

Property

We rely

on trademark and copyright laws, trade secret protection, non-competition and

confidentiality and/or licensing agreements with our executive officers,

clients, contractors, research and development personnel and others to protect

our intellectual property rights. We do not possess any licenses to use

third-party intellectual property rights nor do we license to third-parties any

intellectual property rights we own. The protection afforded by our intellectual

property may be inadequate. It may be possible for third parties to obtain and

use, without our consent, intellectual property that we own or are licensed to

use. Unauthorized use of our intellectual property by third parties, and the

expenses incurred in protecting our intellectual property rights, may adversely

affect our business. We may also be subject to litigation involving claims of

violation of intellectual property rights of third parties.

|

Item

1a.

|

Risk

Factors

|

The

Company faces many risks. The risks described below may not be the only risks

the Company faces. Additional risks not yet known or currently believed to be

immaterial may also impair the Company’s business. If any of the events or

circumstances described in the following risks actually occurs, the Company’s

business, financial condition or results of operations could suffer, and the

trading price of its common stock could decline. You should consider the

following risks, together with all of the other information in this Annual

Report on Form 10-K, before making an investment decision with respect to the

Company’s securities.

Risks

Relating to Our Operations

Our

limited operating history makes evaluation of our business

difficult

We have a

limited operating history and have encountered and expect to continue to

encounter many of the difficulties and uncertainties often faced by early stage

companies. Our limited operating history makes it difficult to evaluate our

future prospects, including our ability to develop a wide customer and