Attached files

| file | filename |

|---|---|

| EX-3.5 - INTEGRATED FREIGHT Corp | ex35k093009.htm |

| EX-2.1 - INTEGRATED FREIGHT Corp | ex21k093009.htm |

| EX-31.2 - RULE 13A-14(A)/15D-14(A) CERTIFICATIONS - INTEGRATED FREIGHT Corp | ex312k093009.htm |

| EX-32.2 - SECTION 1350 CERTIFICATIONS - INTEGRATED FREIGHT Corp | ex322k093009.htm |

| EX-32.1 - SECTION 1350 CERTIFICATIONS - INTEGRATED FREIGHT Corp | ex321k093009.htm |

| EX-31.1 - RULE 13A-14(A)/15D-14(A) CERTIFICATIONS - INTEGRATED FREIGHT Corp | ex311k093009.htm |

| EX-2.1 - INTEGRATED FREIGHT Corp | ex21formk093009.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934: For the fiscal year ended September 30, 2009 |

|

[ ] |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000–14273

PLANGRAPHICS, INC.

(Exact name of registrant as specified in its charter)

|

Colorado |

84–0868815 |

|

State or other jurisdiction of incorporation or organization |

I.R.S. Employer Identification No. |

|

16827 Livingston Road, Lutz, Florida |

33559-7615 |

|

(Address of principal executive offices) |

(Zip code) |

Issuer’s telephone number: (888) 623-4378

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act:

|

Title of each class: |

Name of Exchange on which registered: |

|

Common Stock, no par value |

(None) |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. |

Yes o |

No x |

|||||

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. |

Yes o |

No x |

|||||

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. |

Yes x |

No o |

|||||

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). |

Yes x |

No o |

|||||

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. |

[ ] |

||||||

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. |

|||||||

|

Large accelerated filer |

[ ] |

|

Accelerated filer |

[ ] |

|

||

|

Non-accelerated filer |

[ ] |

|

Smaller reporting company |

[ X ] |

|||

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). |

Yes o |

No x |

|||||

|

The aggregate market value* of the voting and non-voting common equity held by non-affiliates: |

$235,001 |

||||||

|

* Computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. |

|||||||

|

The number of shares of our common stock outstanding at January 11, 2010 was: |

1,907,000,462 |

||||||

|

Table of Contents |

|

|

|

|

|

Page |

|

|

Part I |

|

|

Item 1. |

Business |

4 |

|

Item 1A. |

Risk Factors |

12 |

|

Item 1B. |

Unresolved Staff Comments |

19 |

|

Item 2. |

Properties |

19 |

|

Item 3. |

Legal Proceedings |

20 |

|

Item 4. |

Submission of Matters to a Vote of Security Holders |

20 |

|

|

Part II |

|

|

Item 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

21 |

|

Item 6. |

Selected Financial Data |

21 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

21 |

|

Item 7A. |

Quantitative and Qualitative Disclosures About Market Risk |

28 |

|

Item 8. |

Financial Statements and Supplementary Data |

28 |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

28 |

|

Item 9A. |

Controls and Procedures |

28 |

|

Item 9A(T). |

Evaluation of Disclosure Controls and Procedures |

29 |

|

Item 9B. |

Other Information |

30 |

|

|

Part III |

|

|

Item 10. |

Directors, Executive Officers and Corporate Governance |

30 |

|

Item 11. |

Executive Compensation |

33 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

35 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

35 |

|

Item 14. |

Principal Accounting Fees and Services |

36 |

|

|

Part IV |

|

|

Item 15. |

Exhibits, Financial Statement Schedules |

37 |

|

|

Signatures |

40 |

2

DOCUMENTS INCORPORATED BY REFERENCE

We have not incorporated any documents by reference.

SUMMARIES OF REFERENCED DOCUMENTS

This annual report on Form 10-K contains references to, summaries of and selected information from agreements and other documents. These agreements and documents are not incorporated by reference; but, they are filed as exhibits to this annual report or to other reports we have filed with the U.S. Securities and Exchange Commission. The summaries of and selected information from those agreements and other documents are qualified in their entirely by the full text of the agreements and documents, which you may obtain from the Public Reference Section of or online from the Commission. See “Where You Can Find Additional Information About Us And Exhibits” for instructions as to how to access and obtain this information. Whenever we make reference in this annual report to any of our agreements and other documents, the references are not necessarily complete and you should refer to the exhibits attached to the registration statement of which this annual report is a part for copies of the actual contract, agreement or other document.

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10–K and the information incorporated by reference may include “forward–looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities and Exchange Act of 1934, as amended. We intend the forward–looking statements to be covered by the safe harbor provisions for forward–looking statements in these sections.

This annual report contains forward-looking statements that involve risks and uncertainties. We use words such as “project,” “believe,” “anticipate,” “plan,” “expect,” “estimate,” “intend,” “should,” “would,” “could,” “will,” or “may,” or other such words, verbs in the future tense and words and phrases that convey similar meaning and uncertainty of future events or outcomes to identify these forward-looking statements. There are a number of important factors beyond our control that could cause actual results to differ materially from the results anticipated by these forward-looking statements. While we make these forward–looking statements based on various factors and derived using numerous assumptions, we have no assurance the factors and assumptions will prove to be materially accurate when the events they anticipate actually occur in the future.

These important factors include those that we discuss in this annual report under the caption “Risk Factors”, as well as elsewhere in this annual report. You should read these factors and the other cautionary statements made in this annual report as being applicable to all related forward-looking statements wherever they appear in this annual report. If one or more of these factors materialize, or if any underlying assumptions prove incorrect, our actual results, performance or achievements may vary materially from any future results, performance or achievements expressed or implied by these forward-looking statements. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise.

WHERE YOU CAN FIND AGREEMENTS AND OTHER DOCUMENTS REFERRED TO

IN THIS ANNUAL REPORT

We file reports with the U.S. Securities and Exchange Commission pursuant to Section 13 of the Securities Exchange Act of 1934. You may read and copy any reports and other materials we have filed with the Commission at the Commission’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the Commission at 1-800-SEC-0330. The Commission maintains an Internet site at which you may obtain all reports, proxy and information statements, and other information that we file with the Commission. The address of that web site is http://www.sec.gov.

3

PART I

Item 1. Business.

Our corporate and business history -

“We”, “our” and “us", as used in this annual report, refer to PlanGraphics, Inc., and includes the following wholly owned subsidiaries, during the applicable periods:

|

PlanGraphics, Inc., a Maryland corporation, (“PGI-MD”) our only subsidiary until December 27, 2009, when we sold it. |

|

Integrated Freight Corporation, a Florida corporation, between December 3 and 23, 2009, when we merged Integrated Freight into us. |

|

Morris Transportation, Inc., an Arkansas corporation, beginning December 23, 2009, when we acquired it by merger with Integrated Freight. |

|

Smith Systems Transportation, Inc., a Nebraska corporation, beginning December 23, 2009, when we acquired it by merger with Integrated Freight.

|

The address of our principal executive offices is 16827 Livingston Road, Lutz, Florida 33559-7615, and our telephone number at that address is 888-623-4378. The address of our web site is www.integrated-freight.com.

We were incorporated as DCX, Inc. in Colorado in 1981. In 1997, we acquired all of the outstanding shares of PGI–MD and, in 1998, changed our name to Integrated Spatial Information Solutions, Inc. from DCX, Inc. In 2002, we changed our name to PlanGraphics, Inc. from Integrated Spatial Information Solutions, Inc.

As of May 1, 2009, Integrated Freight acquired 401,599,467 shares, or 80.2 percent, of our issued and outstanding common stock, in redemption of 500 shares of our issued and outstanding preferred stock which we had sold for $500,000 to the Nutmeg/Fortuna Fund LLLP in 2006. Nutmeg/Fortuna Fund is a private investment company, which is now in receivership in Chicago, Illinois. Integrated Freight paid Nutmeg/Fortuna Fund 1,307,822 shares of its common stock and a one-year promissory note in the amount of $167,000 to purchase our preferred stock. At the date of this transaction, the preferred stock had a cash redemption value of $562,573.12, including accrued and unpaid dividends, which we were unable and had no reasonable expectation of being able to pay upon demand. The redemption request submitted by Nutmeg/Fortuna Fund included an offer for redemption of the preferred stock and accrued and unpaid dividends by the issuance of our common stock, the number of shares to be determined by dividing the redemption value by $0.0016, which represented the per share volume weighted average of the highest and lowest closing prices for our common stock published by OTC Bulletin Board for the period of February 15 to April 15, 2009.

Negotiations for the sale and purchase of our preferred stock and the related transactions were conducted over a period of several months. The negotiations involved Nutmeg/Fortuna Fund’s management company and the managements of Integrated Freight and us. Prior to the commencement of the negotiations, there was no then existing or former relationship between and among any of the parties to the negotiations or their respective controlling stockholders. At and prior to the commencement of negotiations, Integrated Freight had been exploring “reverse mergers” with reporting “shell companies”, as defined in the federal securities laws, trading on the OTC Bulletin Board, as a means of acquiring a public stockholder base and an existing public market. By itself, Integrated Freight has only seventeen stockholders, an insufficient number it believed to initiate a public market of its own by filing a Form 10 registration statement with the Commission. As a publicly traded company, its management believed it would be able to more easily obtain equity and debt funding than it could as a privately held company, and publicly traded stock would be more readily acceptable to stockholders of companies Integrated Freight would want to acquire at least partially for stock. Furthermore, the two acquisitions it had made included an obligation for Integrated Freight to become a publicly traded company. Integrated Freight had been offered control of “public shell companies” for prices in the range of $300,000. Integrated Freight decided to utilize us as its vehicle to achieve a public market, because we do not have the stigma of having been a “shell company”. Valuing its stock at $0.10 per share at that time, Integrated Freight concluded that the stock and note it was able to negotiate with Nutmeg/Fortuna Fund was within the price range it would have to pay for an alternative, reporting, OTC Bulletin Board shell company, with the added benefit of deferring the cash portion of the price with the one-year note.

4

Integrated Freight originally intended to merge us into itself, thus succeeding to our registration under the Securities Exchange Act of 1934 and our public market. In a related transaction, we were to sell PGI-MD to our then director and chief executive officer, John C. Antenucci. Integrated Freight was not interested in continuing the business of PGI-MD, which had been experiencing poor financial performance as a publicly traded company and was facing either bankruptcy or voluntary termination of its securities registration, or both. Mr. Antenucci believed that PGI-MD represented a viable business as a privately owned company, and as its founder, was interested in purchasing PGI-MD from us. See “Terms of our sale of PGI-MD”, below.

This merger and the related reverse stock split and sale of PGI-MD (as our only substantial asset, at that time) required stockholder approval under Colorado corporation law pursuant to an effective registration statement on Form S-4 under the Securities Act of 1933. This created uncertainty as to when an effective date for the registration statement and the stockholder vote would occur. As a consequence of this uncertainty, Integrated Freight found it could not obtain sufficient debt or equity funding it needed (a) to complete the audits and reviews of financial statements required to amend the pending registration statement on Form S-4 and (b) pursue and close additional acquisitions it was negotiating.

Our combination with Integrated Freight was restructured as a parent – subsidiary merger under Colorado and Florida law, thus eliminating the need for stockholder approval of the merger and the sale of PGI-MD (no longer a substantial asset, after the merger) and an effective registration statement on Form S-4. The new structure was approved by both Integrated Freight and us concurrently on November 10, 2009. At that date, the same five persons served on Integrated Freight’s board and on our board.

In furtherance of the restructured transaction, we acquired 93.797 percent of the issued and outstanding common stock of Integrated Freight, including all of the stock it was obligated to issue, in exchange for 1,406,284,229 shares of our authorized but unissued common stock. We acquired the Integrated Freight stock from The Integrated Freight Stock Exchange Trust, a Florida business trust (“Trust”) established to hold all of Integrated Freight’s common stock for purposes of the exchange and all of our stock which was owned by Integrated Freight. At the conclusion of this transaction, the Trust now owns 94.8 percent of our issued and outstanding common stock. On December 23, 2009, we merged Integrated Freight into us.

In order to achieve the additional outcomes that would have resulted from the original transaction structure, we have filed a preliminary Schedule 14C information statement with the Commission for a special stockholders meeting at which the following actions will be approved by the Trust:

• a reverse stock split in a ratio of one new share for each 244.8598 shares of our issued and

outstanding common stock;

|

|

• |

a change of our name to Integrated Freight Corporation; and |

|

|

• |

a change in our state of incorporation to Florida from Colorado. |

Following the approval of these actions by our stockholders, we will issue an additional number of our shares of common stock to:

• the Trust so that it can transfer to its beneficiaries one of our shares for each share of Integrated Freight deposited into the Trust and which would have been deposited into the Trust by persons to whom Integrated Freight was obligated to issue shares but had not yet delivered certificates;

• two other stockholders of Integrated Freight who did not deposit their certificates with the Trust, one of our shares for each share of Integrated Freight which they owned prior to the merger.

The reverse stock split ratio was based on two factors. First, the number of shares held by Integrated Freight’s stockholders after the merger would be equal to the number of shares they held on May 1, 2009. Second, the number of shares held by Integrated Freight’s stockholders after the merger would be equal to ninety percent of our issued and outstanding common stock. The balance of ten percent would be held by public stockholders, the Nutmeg/Fortuna Fund, PGI-MD, Mr. Antenucci and Frederick G. Beisser. See “Terms of our sale of PGI-MD”, below. The 90:10 ratio was in the range of stock ownership percentages that Integrated Freight had been offered in transactions with alternative, reporting, OTC Bulletin Board shell companies.

The restructured transaction and the additional actions to be taken subject to stockholder approval, as described above, will have the same outcome for stockholders and the constituent companies as the original structure of the transactions.

5

The principal business of PGI–MD beginning at inception to the present is life–cycle systems integration and implementation, providing a broad range of services in the design and implementation of information technology solutions within the public and commercial sectors. Our customers have primarily included federal, state and local governments, utility companies, and commercial enterprises in the United States and foreign markets. PGI-MD’s focus and specialty is on spatial information management technologies, including web–enabled GIS and applications. Spatial information management systems, which include GIS, provide a means for accessing, managing, integrating, analyzing and interpreting disparate data sets that require locational or “spatial” information by relating the geographic location of a feature or event to other descriptive information. GIS software allows data, in both graphic or map format and alphanumeric data to be combined, segregated, modeled, analyzed and displayed, thus becoming useful information for managers. This was also our only business until December 3, 2009, when we acquired the stock of Integrated Freight. We completed the sale of MDI-PG to Mr. Antenucci on December 27, 2009.

Integrated Freight was incorporated in Florida on May 13, 2008 by Paul A. Henley, its founder, under the name of “Integrated Freight System, Inc.” We changed our name to Integrated Freight Corporation on July 27, 2009. Mr. Henley is currently one of our directors and our chief executive officer. Mr. Henley founded Integrated Freight for the purpose of acquiring and consolidating operating motor freight companies. Integrated Freight acquired our two existing business units, which are:

|

Company Name |

Year Established |

Acquisition Date |

|

Morris Transportation, Inc. |

1998 |

As of September 1, 2008 |

|

Smith Systems Transportation, Inc. |

1992 |

As of September 1, 2008 |

We are operating these subsidiaries as independent companies under the management of their founders and stockholders from whom we purchased them. We expect this management arrangement to continue until we have paid the cash and note component of the acquisition consideration, after which we intend to gradually combine and consolidate the elements of their operations that are duplicative.

Overview of Our Truck Transportation Business

We are, beginning December 27, 2009, exclusively a motor freight carrier providing truck load service primarily in two markets in the mid-West United States. We do not specialize in any specific types of freight or commodities. We carry dry freight, refrigerated freight and hazmat and hazwaste (hazardous materials and waste). We provide long-haul, regional and local service to our customers.

Our Strategy

Truck transportation in general has suffered during the current economic recession. Over 3,000 trucking companies are believed to have ceased operations in 2008. We believe the trucking companies that have survived in the current economic recession, whether presently profitable or marginally unprofitable, represent good future value at the prices for which we believe many of them can be acquired. Many of them will not survive longer without debt and equity funding and cost reductions which they are unlikely to obtain individually. When our economy recovers, we believe that the demand for truck transportation services will return to pre recession levels, with an initially inadequate supply of trucks to meet demand. When the economic recovery occurs, which we cannot predict, we believe we will be well positioned to fill part of the demand for over-the-road freight services.

We intend to continue acquiring well established trucking companies when we can do so at prices which we deem to be advantageous. In the alternative, we may acquire assets. We also plan to expand beyond our truckload service through acquisitions into logistics, brokering, less than a load (LTL) and expedite/just-in-time services, as opportunities are presented to us.

We believe that we can achieve savings in operating costs by centralizing certain common functions of our subsidiaries, such as fuel and tire purchasing, billing and collections, dispatching, maintenance scheduling and other functions. We believe that with a larger service territory and customer base than any one subsidiary would have working alone, we will be able to achieve greater efficiencies in route and equipment utilization.

6

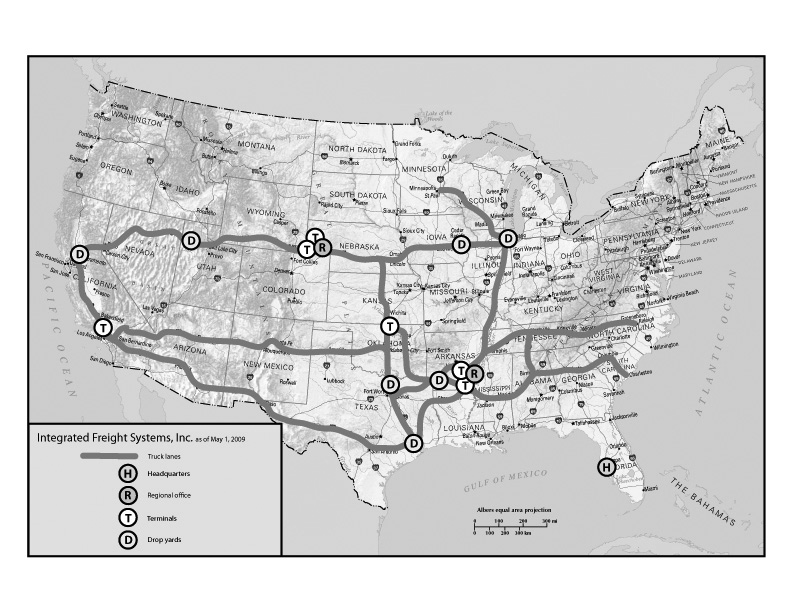

Our Markets

Historically our subsidiary companies have operated in well-established geographic traffic lanes or routes. These lanes are defined by our customers’ distribution patterns. Because there is some overlap within the most heavily traveled lanes, especially between points in the upper Midwest and Texas, management believes that it will continue to realize increased cost and productivity improvements.

The following map displays information about the lanes our trucks most routinely or most frequently travel.

*A drop yard is a temporary or semi permanent location we rent where we store trailers when not in use between pick-ups and deliveries. Typically, we rent drop yards in terminal facilities of other motor freight carriers, which provide security.

Our Customers and Marketing

We serve approximately 175 customers on a regular basis. The following table presents information regarding our relationship with our customers derived from analysis of our operating data. Although we do not have contracts with any of these customers, we have long-standing relationships with most of them.

The following table presents information regarding the percentage-of-revenue concentration of the business with our customers.

|

Four customers |

Up to 35% |

|

All other customers |

65% or more |

The following table presents information regarding the average length of our trips.

|

Longest haul (overnight) |

1,950 miles |

|

Shortest haul |

175 miles |

|

Average haul |

850 miles |

Ninety-eight percent of the freight we haul is dry van freight. The following table presents information regarding the approximate percentage makeup of the freight we haul.

|

Forest and paper products |

38% |

|

Hazmat and hazwaste |

39% |

|

All other freight (freight of all kinds – FAK) |

23% |

Marketing

Mr. Morris, Mr. Smith and one sales person specializing in hazmat and hazwaste constitute our sales and marketing force. We have no formal marketing plan at the present time. We attend relevant trade shows and trade association meetings, and seek to maintain good relations with our existing customers. As we grow our carrier base, of which there is no assurance, we plan to establish a central marketing group that will support the sales and customer service efforts of each subsidiary.

7

Our People

We believe our employees are our most important asset. The following table presents information about our employees.

|

Drivers - company |

75 |

|

Drivers – independent contract* |

48 |

|

Platform and warehouse |

2 |

|

Fleet technicians |

6 |

|

Dispatch |

6 |

|

Sales |

1 |

|

Office |

3 |

|

Administrative and Executive |

5 |

*This is an average number. The number of our contract drivers, who typically own or lease from third parties the tractors they drive, varies depending on our needs. The average number of contract drivers we employed during calendar 2009 was forty-six.

None of our employees are represented by a collective bargaining unit. We consider relations with our employees to be good. We offer basic health insurance coverage to all employees.

Our Drivers

We believe that maintaining a safe and productive professional driver group is essential to providing excellent customer service and achieving profitability. All of our drivers must have three years of verifiable driving experience, a hazmat endorsement (if hauling hazmat), no major violation in the previous thirty-six months and comply with all requirements of employment by federal Department of Transportation and applicable state laws.

We select drivers, including independent contractors, using our specific guidelines for safety records, driving experience, and personal evaluations. We maintain stringent screening, training, and testing procedures for our drivers to reduce the potential for accidents and the corresponding costs of insurance and claims. We train new drivers in all phases of our policies and operations, as well as in safety techniques and fuel-efficient operation of the equipment. All new drivers also must pass DOT required tests prior to assignment to a vehicle.

We primarily pay company-employed drivers a fixed rate per mile. The rate increases based on length of service. Drivers also are eligible for bonuses based upon safe, efficient driving. We pay independent contractors on a fixed rate per mile. Independent contractors pay for their own fuel, insurance, maintenance, and repairs.

Competition in the trucking industry for qualified drivers is normally intense. Our operations have been impacted, and from time-to-time we have experienced under-utilization and increased expense, as a result of a shortage of qualified drivers. We place a high priority on the recruitment and retention of an adequate supply of qualified drivers. Our average annual turn-over rate is less than twenty percent, compared to an industry average of forty-three percent as published in Transport Topics, January 4, 2010.

Our Operations

We currently conduct all of our freight transportation operations, including dispatch and accounting functions, from the headquarters facilities of our operating subsidiaries, using different information management systems and personnel that were employed when acquired our operating subsidiaries. These arrangements produce many overlaps and duplications in facilities, office systems and personnel. We believe that these operating arrangements provide less than optimal results. We intend to centralize many of these functions, as noted above. Centralization is subject to obtaining adequate internal or external financing, of which there is no assurance.

8

Our Revenue Equipment

The following table presents information regarding our revenue producing equipment.

|

Power units (tractors) – sleeper |

86 |

|

|

Power units (tractors) – day cab |

2 |

|

|

Trailers |

|

|

|

|

Flatbed |

6 |

|

|

Dry van |

329 |

|

|

Refrigerated |

30 |

|

|

Other specialized |

9 |

|

|

Tanker |

9 |

The average age of our power units is approximately 3.8 years. All of our power units are GPS equipped. The majority of our power units are Freightliner vehicles. This uniformity allows for reduced inventory of parts required by our maintenance departments. In addition, the training required for our technicians is greater focused on a primary product line. We replace our power units at approximately four years of age. The average age of our trailers is approximately 3.3 years for general freight and twelve years (as needed) for hazmat and hazwaste which may sit idle for extended periods of time. We maintain all of our revenue producing equipment in good order and repair.

We believe we have an optimal tractor to trailer ratio based upon our current and anticipate customer activity.

Our planned acquisition of assets in the bankruptcy of Gulf Coast Transport and affiliated companies of Sunnyvale, Texas

We have submitted an Asset Purchase Agreement to the Bankruptcy Court for the Northern District of Texas which, if approved by the creditors of Gulf Coast Transport, will enable us to purchase for $250,000 the intangible assets of the bankruptcy debtors, including customer information. In a related transaction, subject to approval of the asset purchase agreement, we intend to renegotiate the financing of approximately 140 tractors and 350 trailers which have been operated by Gulf Coast Transport, and to acquire, subject to renegotiation of the mortgage, approximately thirteen acres of property in Sunnyvale, Texas which Gulf Coast Transport has used as its headquarters office, terminal and yard. There is no assurance we will obtain creditor approval of the asset purchase agreement and related transactions.

Diesel Fuel Availability and Cost

Our operations are heavily dependent upon the use of diesel fuel. The price and availability of diesel fuel can vary and are subject to political, economic, and market factors that are beyond our control. Fuel prices have fluctuated dramatically and quickly at various times during the last three years. They remain high based on historical standards and can be expected to increase with increased demand for truck transportation in a recovering economy. We actively manage our fuel costs with volume purchasing arrangements with national fuel centers that allow our drivers to purchase fuel at a discount while in transit. During 2008, over eighty-five percent of our fuel purchases were made at contracted locations.

To help further reduce fuel consumption, we began installing auxiliary power units in our tractors during 2007. These units reduce fuel consumption by providing quiet climate control and electrical power for our drivers without idling the tractor engine. We anticipate having these units installed in approximately ninety-six percent of our company-owned fleet by December 31, 2010.

Our cost-cutting measures include utilizing technology such as Peoplenet and carrierweb to monitor travel speed/idling/rpms/high overspeed operations. In addition, governing the top speed of our power units helps reduce our fuel costs. We are installing the newly designed roll resistant, and thus more fuel efficient, tires as replacements are needed.

We further manage our exposure to changes in fuel prices through fuel surcharge programs with our customers and other measures that we have implemented. We have historically been able to pass through most long-term increases in fuel prices and related taxes to customers in the form of fuel surcharges. These fuel

9

surcharges, which adjust with the cost of fuel, enable us to recover a substantial portion of the higher cost of fuel as prices increase, except for non-revenue miles, out-of-route miles or fuel used while the tractor is idling. As of December 31, 2009 (our most recently completed fiscal year), we had no derivative financial instruments to reduce our exposure to fuel price fluctuations.

Our Competition and Industry

Trucks provide transportation services to virtually every industry operating in the United States and generally offer higher levels of reliability and faster transit times than other surface transportation options. The estimated total revenues from this industry sector are $255.5 billion annually. The transportation industry is highly competitive on the basis of both price and service. The trucking industry is comprised principally of two types of motor carriers: truckload and less than a load, generally identified as LTL. Truckload carriers generally provide an entire trailer to one customer from origin to destination. LTL carriers pick up multiple shipments from multiple customers on a single truck and then route those shipments through service centers, where freight may be transferred to other trucks with similar destinations for delivery. All of our service is truckload service.

The surface freight transportation market in which we operate is frequently referred to as highly fragmented and competitive. There are an estimated 360,000 motor freight companies in the United States, with ninety-six percent operating twenty-eight or fewer trucks. Even the largest motor freight companies haul a small percentage of the total freight. The following table presents information regarding the estimated percentage of freight hauled by the largest trucking companies compared to all other trucking companies.

|

Ten largest trucking companies |

16.4% |

|

All other trucking companies |

83.6% |

[Industry information obtained from the Bureau of Transportation Statistics, www.bts.gov, of the U.S. Department of Transportation.]

Competition in the motor freight industry is based primarily on service (including on-time pickup and delivery), price, equipment availability and business relationships. We believe that we are able to compete effectively in our markets by providing high-quality and timely service at competitive prices. We believe our relationships with our customers are good. We compete with smaller and several larger transportation service providers. Our larger competitors may have more equipment, a broader coverage network and a wider range of services than we have. They may also have greater financial resources and, in general, the ability to reduce prices to gain business, especially during times of reduced growth rates in the economy. This could potentially limit our ability to maintain or increase prices, and could also limit our growth in shipments and tonnage.

We believe that we do not compete with transportation by train, barge or ship, which we believe are not options for our existing customers.

Regulation

Our operations as a for-hire motor freight carrier are subject to regulation by the U.S. Department of Transportation (DOT) and the Federal Motor Carrier Safety Administration (FMCSA), and certain business is also subject to state rules and regulations. These agencies exercise broad powers over our business, generally governing such activities as authorization to engage in motor carrier operations, safety and insurance requirements. The DOT periodically conducts reviews and audits to ensure our compliance with all federal safety requirements, and we report certain accident and other information to the DOT.

Our company drivers and independent contract drivers also must comply with the safety and fitness regulations promulgated by the DOT, including those relating to drug and alcohol testing and hours-of-service. In November 2008, the FMCSA adopted final provisions of the Agency’s December 17, 2007, interim final rule concerning hours of service for commercial vehicle drivers. This final rule allows drivers to continue to drive up to eleven hours within a fourteen-hour non-extendable window from the start of the workday, following at least ten consecutive hours off duty. The rule also allows motor freight carriers and drivers to continue to restart calculations of weekly on-duty limits after the driver has at least thirty-four consecutive hours off duty. The rule was effective January 19, 2009. We believe these regulations will not have a significant negative impact on our operations or financial results in fiscal year 2010.

10

We are also subject to various environmental laws and regulations dealing with the handling of hazardous materials, air emissions from our vehicles and facilities, engine idling, and discharge and retention of storm water. These regulations have not had a significant impact on our operations or financial results and we do not expect a negative impact in the future.

Terms of Our Acquisitions

We acquired Morris Transportation and Smith Systems Transportation in the merger with Integrated Freight. The following table describes the material terms of these acquisitions, as amended and in effect at the date of this annual report.

|

|

Morris Transportation |

Smith Systems Transportation |

|

Shares of our stock |

3,000,000 shares |

825,000 shares |

|

Note amounts and due dates |

$600,000 due October 31, 2009 (1)(2) |

none |

|

Cash payment - basic |

$150,000 due October 31, 2009 |

none |

|

Cash payment - additional |

$250,000 due October 31, 2009 |

none |

|

Refinancing of equipment |

Required by March 31, 2010 (4) |

Required by March 31, 2010 (5) |

|

Working capital infusion |

$100,000 |

none |

(1) The interest rate on the note is eight percent per annum.

(2) Secured by a pledge of Morris Transportation stock. The note is convertible at the election of the holder into our common stock at $1 per share.

(3) The principal amount of the cash payment will reduced dollar for dollar (i) for any decline in net profits in the twelve months ended August 31, 2009 compared to the same period in 2008 and (ii) for any capital infusion required to sustain the company’s operations.

(4) For the purpose of eliminating personal guaranties. In the alternative, we may make an additional capital infusion of $100,000 to Morris Transportation and pay Mr. Morris $50,000.

(5) For the purpose of eliminating personal guaranties.

We have been unable to pay the principal and interest when due on the $600,000 note held by Mr. Morris. Mr. Morris may exercise his security interest in the stock of Morris Transportation; however, he has agreed to forbear in exercising his security interest until he believes we have exhausted our ability to obtain financing with which to pay the $600,000 note. He has agreed in writing to release his security interest and restructure other terms of the acquisition for a principal payment of $250,000. In the event Mr. Morris exercises his security interest, we would receive a return of our common stock and repayment of amounts that we have paid to him, but not capital infusions we have made to Morris Transportation. Mr. Morris has advance approximately $150,000 in working capital to Morris Transportation since the date of our acquisition, which we have agreed to repay in 150,000 shares of our common stock on a post reverse stock split basis.

Terms of our sale of PGI-MD

The agreement to sell PGI-MD to Mr. Antenucci was made in connection with Integrated Freight’s purchase of our preferred stock from Nutmeg/Fortuna Fund described above. The agreement included the following provisions, as modified due to delays in completing the merger with Integrated Freight, which were satisfied in the completion of the sale on December 27, 2009:

|

|

• |

We transferred all of our assets to PGI-MD with a depreciated book value of nil, excluding the stock PlanGraphics owned in PGI and the assets we acquired by merger with Integrated Freight. |

|

|

• |

PGI-MD assumed all of our operating debts and obligations as of May 1, 2009, totaling $88,340, excluding $28,000 in accrued auditing fees and our operating costs incurred subsequent to May 1, 2009. |

|

|

• |

We issued a promissory note to PGI-MD for $22,345 of our operating costs incurred subsequent to May 1, 2009 which PGI-MD had paid. |

|

|

• |

We are subject, as a result of the merger, to Integrated Freight’s obligation to issue 177,170 shares of common stock and 177,170 common stock purchase warrants good for two years at a price of $0.50 per share in consideration for PGI-MD’s release of us from our obligation to repay inter-company loans totaling $684,311. |

11

We accepted Mr. Antenucci’s termination of his employment agreement as our chief executive officer, which included an obligation for us to pay him approximately $335,000 in severance, as full payment for his purchase of PGI-MD.

As a result of the merger, we are subject to Integrated Freight’s obligation to issue to Mr. Antenucci 59,327 shares of common stock and 59,327 common stock purchase warrants good for two years at a price of $0.50 per share in consideration for Mr. Antenucci’s release from payment of his deferred compensation and expensation and expense reimbursement in the amount of $88,954.

As a result of the merger, we are subject also to Integrated Freight’s obligation to issue to Frederick G. Beisser, our former senior vice president - finance, 75,525 shares of common stock and 75,525 common stock purchase warrants good for two years at a price of $0.50 per share in consideration for Mr. Beisser’s release from payment of his deferred compensation in the amount of $112,830. (but not including unpaid wages, automobile allowance and reimbursable expenses totaling $24,126 owed to him at November 9, 2009).

We are also required to maintain directors and officers tail coverage for three years for the benefit of Messrs. Antenucci and Beisser.

Integrated Freight had no interest in maintaining, managing and funding the business of PGI-MD as a subsidiary company. The transactions outlined above resulted in relief from liabilities in an aggregate amount of $1,309,435, in consideration for common stock which Integrated Freight valued at the time at $0.10 per share (the price at which it was selling its common stock at that time in private placements), for an aggregate value of $31,175, before valuing the warrants. Furthermore, the sale of PGI-MD will remove approximately $3,281,679 in liabilities from our consolidated balance sheet that were liabilities of PGI-MD and relieved us of all the operational and business difficulties centered in PGI-MD. We did not obtain an independent appraisal of PGI-MD. Nor, did we seek other buyers for PGI-MD or its business and technologies. We believe that our management composed of Mr. Antenucci during our negotiations with Integrated Freight would have been less interested or uninterested in entering into the transactions with Integrated Freight, as compared to declaring bankruptcy or terminating our reporting status under the Securities Exchange Act if the transactions had not involved our sale of PGI-MD to Mr. Antenucci. Notwithstanding the foregoing, at May 1, 2009, our management, the management of Integrated Freight and Mr. Antenucci believed that these related transactions were fair and acceptable to all parties. We believe the negotiations for our sale of PGI-MD were conducted at arms’ length, because fundamentally Mr. Antenucci was not negotiating against us, when he was our sole director and chief executive officer, but was negotiating against Integrated Freight.

Item 1A. Risk Factors.

In addition to the forward-looking statements outlined previously in this annual report and other comments regarding risks and uncertainties included in the description of our business, the following risk factors should be carefully considered when evaluating our business. Our business, financial condition or financial results could be materially and adversely affected by any of these risks.

The terms of our amended secured acquisition note enable the Mr. Morris to recover ownership of Morris Transportation, which would represent a significant loss of business.

The amended $600,000 promissory note we have given to the purchase Morris Transportation is secured by a pledge of the stock in the acquired companies. We are presently in default under that note. We will require additional equity or debt funding, of which there is no assurance, in order to satisfy our financial obligations under the acquisition note. Mr. Morris has verbally agreed to forbear in exercising his security interest until he believes we will not be able to obtain financing to pay the note. In the event he does exercise his security interest, which he could do at any time, he would recover his ownership of Morris Transportation. In that event we would lose one of our operating subsidiaries resulting in either a material reduction in our business. Events of default include:

12

We may experience difficulty in combining and consolidating the management and operations of our acquired companies which could have a material adverse impact on our operations and financial performance.

We have purchased our operating subsidiaries and expect any additional subsidiaries we purchase to be made from the founders and management of the acquired companies, all of whom have been responsible for their own businesses and methods of operations as independent business owners. While these individuals will continue to be responsible to a degree for the continuing operations of our operating subsidiaries, we intend to centralize and standardize many areas of operations. Notwithstanding that many of these individuals from whom we have and plan to acquire our operating subsidiaries will serve on our board of directors, we may be unable to develop a cohesive corporate culture in which these individuals will be willing to forego their former independence. Our inability to successfully combine and consolidate the policies, procedures and operations of our subsidiaries can be expected to have a material adverse effect on our business and prospects, financial and otherwise.

Our information management systems are diverse, may prove inadequate and may be difficult to integrate or replace.

We depend upon our information management systems for many aspects of our business. Each company we acquire will have its own information management system with which its employees are acquainted. None of these systems may be adequate to our consolidated operations and may not be compatible with a centralized information management system. We expect to require additional software to initially integrate existing systems or to ultimately replace these diverse systems. Switching to new information management systems is often difficult, resulting in disruption, delays and lost productivity, which could impact our dispatching, collections and other operations. Our business will be materially and adversely affected if our information management systems are disrupted or if we are unable to improve, upgrade, integrate, expand or replace our systems as we continue to execute our growth strategy.

Our management information systems are subject to certain risks that we cannot control.

Our management information systems, including dispatching and accounting systems, are dependent upon third-party software, global communications providers, telephone systems and other aspects of technology and Internet infrastructure that are susceptible to failure. Our management information systems is susceptible to outages, computer viruses, break-ins and similar disruptions that may inhibit our ability to provide services to our customers and the ability of our customers to access our systems. This may result in the loss of customers or a reduction in demand for our services.

If we are unable to successfully execute our growth strategy, our business and future results of operations may suffer.

Our growth strategy includes the acquisition of additional motor freight companies to increase revenues, to selectively expand our geographic footprint and to broaden the scope of our service offerings. If we are unable to acquire additional motor freight companies at prices that meet our financial model, our growth will be limited to expanding sales and reducing expenses in our existing subsidiaries. In connection with our growth strategy, we may purchase additional equipment, expand and upgrade service centers, hire additional personnel and increase our sales and marketing efforts.

Our growth strategy exposes us to a number of risks, including the following:

|

|

• |

|

geographic expansion and acquisitions require start-up costs that could expose us to temporary losses; |

|

|

• |

|

growth and geographic expansion is dependent on the availability of real estate. Shortages of suitable real estate may limit our geographic expansion and might cause congestion in our service center network, which could result in increased operating expenses; |

|

|

• |

|

growth may strain our management, capital resources, information systems and customer service; |

|

|

• |

|

hiring new employees may increase training costs and may result in temporary inefficiencies until those employees become proficient in their jobs; |

|

|

• |

|

expanding our service offerings may require us to enter into new markets and encounter new competitive challenges; and |

13

|

|

• |

|

growth through acquisition could require us to temporarily match existing freight rates of the acquiree’s markets, which may be lower than the rates that we would typically charge for our services.

|

We have no assurance we will overcome the risks associated with our growth. If we fail to overcome those risks, we may not realize additional revenue or profits from our efforts, we may incur additional expenses and therefore our financial position and results of operations could be materially and adversely affected.

We are significantly dependent on the continued services of Paul A. Henley to realize our growth strategy.

We are dependent upon the vision and efforts of Mr. Henley, our founder and principal stockholder, for the realization of our growth strategy. In the event Mr. Henley’s services were to be unavailable to us, our continued activity to expand our business operations through acquisition could be substantially impaired or be abandoned.

Our management owns more than a majority of our outstanding common stock and outside stockholders will be unable to influence management decisions or elect their nominees to our board of directors, if they should so desire.

Our management will control 55.523 percent of our common stock after the reverse stock split and the issue of the additional shares required by our plan of merge with Integrated Freight. All corporate actions involving amendment of our articles of incorporation (such as name change and increase in authorized shares), election of directors and other extraordinary actions and transactions such as certain mergers, consolidations and recapitalizations and sales of all or substantially all of our assets, require the approval of only a majority of the issued and outstanding shares of our common stock. Accordingly, our management will be able to approve any such actions and transactions and elect all directors even if all of the outside stockholders oppose such transactions, or in the case of directors, nominate other persons for election. Our minority stockholders will be unable to effect changes in our management or in our business.

We have significant ongoing cash requirements and expect to incur additional cash requirements that could limit our growth and adversely affect our profitability if we are unable to obtain sufficient financing.

Our business is capital intensive, involving the frequent purchase of new power units and trailers. In 2008, 2009 and to date in fiscal year 2010, we made capital expenditures for new equipment of approximately $50,000 in each year. We anticipate that we may spenc as much as $250,000 in new equipment in fiscal year 2011. In addition, we have issued promissory notes to cover part of the costs of our acquisitions and expect to continue issuing promissory notes for part of the cost of acquisitions. We expect to pay for projected capital expenditures with cash flows from operations and borrowings under credit facilities, which at the date of this annual report are $is estimated at $250,000. Due to the existing uncertainty in the capital and credit markets, capital and loans may not be available on terms acceptable to us. If we are unable in the future to generate sufficient cash flow from operations or borrow the necessary capital to fund our operations and acquisitions, we will be forced to operate our equipment for longer periods of time and to limit our growth, which could have a material adverse effect on our operating results. In addition, our business has significant operating cash requirements. If our cash requirements are high or our cash flow from operations is low during particular periods, we may need to seek additional financing, which may be costly or difficult to obtain. If any of the financial institutions that have extended credit commitments to us are or continue to be adversely affected by current economic conditions and disruption to the capital and credit markets, they may become unable to fund borrowings under their credit commitments or otherwise fulfill their obligations to us, which could have a material and adverse impact on our financial condition and our ability to borrow additional funds, if needed, for working capital, capital expenditures, acquisitions and other corporate purposes.

Recent instability of the credit markets and the resulting effects on the economy could have a material adverse effect on our operating results.

Recently, there has been widespread concern over the instability of the credit markets and the current credit market effects on the economy. If the economy and credit markets continue to weaken, our business, financial results, and results of operations could be materially and adversely affected, especially if consumer confidence declines and domestic spending decreases. Although we think it is unlikely given our current cash position, we may need to incur indebtedness, which may include drawing on our Credit Facility, or issue debt securities in the future to fund working capital requirements, make investments, or for general corporate purposes. Additionally, the stresses in the credit market have caused uncertainty in the equity markets, which may result in volatility of the market price for our securities.

14

We derive twenty-five percent of our revenue from four customers, the loss of one or more of which could have a material adverse effect on our business.

For the year ended March 31, 2009, our top four customers, based on revenue, accounted for approximately twenty-five percent of our revenue. A reduction in or termination of our services by one or more of our major customers could have a material adverse effect on our business and operating results. A default in payments of invoices by one or more of these customers could have a material adverse effect on our financial condition. See “Our Business – Our customers and marketing”.

We operate in a highly competitive and fragmented industry, and our business will suffer if we are unable to adequately address potential downward pricing pressures and other factors that may adversely affect our operations and profitability.

We compete with many other truckload carriers that provide dry-van and temperature-sensitive service of varying sizes and, to a lesser extent, with less-than-truckload carriers, railroads and other transportation companies, many of which have more equipment, a wider range of services and greater capital resources than we do or have other competitive advantages. In particular, several of the largest truckload carriers that offer primarily dry-van service also offer temperature-sensitive service, and these carriers could attempt to increase their business in the temperature-sensitive market. Numerous other competitive factors could impair our ability to maintain our revenues and achieve profitability. These factors include, but are not limited to, the following:

|

|

• |

|

we compete with many other transportation service providers of varying sizes, some of which may have more equipment, a broader coverage network, a wider range of services, greater capital resources or have other competitive advantages; |

|

|

• |

|

some of our competitors periodically reduce their prices to gain business, especially during times of reduced growth rates in the economy, which may limit our ability to maintain or increase prices or maintain revenue growth; |

|

|

• |

|

many customers reduce the number of carriers they use by selecting “core carriers,” as approved transportation service providers, and in some instances we may not be selected; |

|

|

• |

|

many customers periodically accept bids from multiple carriers for their shipping needs, and this process may depress prices or result in the loss of some business to competitors; |

|

|

• |

|

the trend towards consolidation in the ground transportation industry may create other large carriers with greater financial resources and other competitive advantages relating to their size; |

|

|

• |

|

advances in technology require increased investments to remain competitive, and our customers may not be willing to accept higher prices to cover the cost of these investments; and |

|

|

• |

|

competition from non-asset-based logistics and freight brokerage companies may adversely affect our customer relationships and pricing policies. |

If our employees were to unionize, our operating costs would increase and our ability to compete would be impaired.

None of our employees are currently represented under a collective bargaining agreement. From time to time there may be efforts to organize our employees. There is no assurance that our employees will not unionize in the future, particularly if legislation is passed that facilitates unionization such as the Employee Free Choice Act (“EFCA”). The unionization of our employees could have a material adverse effect on our business, financial condition and results of operations because:

|

|

• |

|

some shippers have indicated that they intend to limit their use of unionized trucking companies because of the threat of strikes and other work stoppages; |

|

|

• |

|

restrictive work rules could hamper our efforts to improve and sustain operating efficiency; |

|

|

• |

|

restrictive work rules could impair our service reputation and limit our ability to provide next-day services; |

15

|

|

• |

|

a strike or work stoppage would negatively impact our profitability and could damage customer and employee relationships; and |

|

|

• |

|

an election and bargaining process could divert management’s time and attention from our overall objectives and impose significant expenses. |

Insurance and claims expenses could significantly reduce our profitability.

We are exposed to claims related to cargo loss and damage, property damage, personal injury, workers’ compensation, long-term disability and group health. We have insurance coverage with third-party insurance carriers, but retain or self-insure a portion of the risk associated with these claims. If the number or severity of claims increases, or we are required to accrue or pay additional amounts because the claims prove to be more severe than our original assessment, our operating results would be adversely affected. Insurance companies may require us to obtain letters of credit to collateralize our self-insured retention. If these requirements increase, our borrowing capacity could be adversely affected. Our future insurance and claims expense might exceed historical levels, which could reduce our earnings. We expect our growth strategy to require a periodic reassessment or our insurance strategy, including self-insurance of a greater portion of our claims exposure resulting from workers’ compensation, auto liability, general liability, cargo and property damage claims, as well as employees’ health insurance under pending federal legislation, which we are unable to predict. We may also become responsible for our legal expenses relating to such claims. With growth, we will be required to periodically evaluate and adjust our claims reserves to reflect our experience. However, ultimate results may differ from our estimates, which could result in losses over our reserved amounts. We maintain insurance above the amounts for which we self-insure with licensed insurance carriers. Although we believe the aggregate insurance limits should be sufficient to cover reasonably expected claims, it is possible that one or more claims could exceed our aggregate coverage limits. Insurance carriers have raised premiums for many businesses, including trucking companies. As a result, our insurance and claims expense could increase, or we could raise our self-insured retention when our policies are renewed. If these expenses increase, or if we experience a claim in excess of our coverage limits, or we experience a claim for which coverage is not provided, results of our operations and financial condition could be materially and adversely affected.

Our customers and suppliers’ business may be impacted by the current downturn in the worldwide economy and disruption of financial markets.

Our business is dependent on a number of general economic and business factors that may have a materially adverse effect on our results of operations, many of which are beyond our control. These factors include excess capacity in the trucking industry, strikes or other work stoppages, and significant increases or fluctuations in interest rates, fuel taxes, and license and registration fees. We are affected by recessionary economic cycles and downturns in customers’ business cycles, particularly in market segments and industries where we have a significant concentration of customers. Economic conditions may adversely affect our customers and their ability to pay for our services. Current economic conditions have adversely affected and may continue to adversely affect our customers’ business levels, the amount of transportation services they need and their ability to pay for our services. Customers encountering adverse economic conditions may be unable to obtain additional financing, or financing under acceptable terms, because of the disruptions to the capital and credit markets. These customers represent a greater potential for bad debt losses, which may require us to increase our reserve for bad debt. Economic conditions resulting in bankruptcies of one or more of our large customers could have a significant impact on our financial position, results of operations or liquidity in a particular year or quarter. Our supplier’s business levels have also been and may continue to be adversely affected by current economic conditions or financial constraints, which could lead to disruptions in the supply and availability of equipment, parts and services critical to our operations. A significant interruption in our normal supply chain could disrupt our operations, increase our costs and negatively impact our ability to serve our customers.

We may be adversely impacted by fluctuations in the price and availability of diesel fuel.

We require large amounts of diesel fuel to operate our tractors and to power the temperature-control units on our trailers. Fuel is one of our largest operating expenses. Fuel prices tend to fluctuate, and prices and availability of all petroleum products are subject to political, economic and market factors that are beyond our control. We do not hedge against the risk of diesel fuel price increases. We depend primarily on fuel surcharges, auxiliary power units for our tractors, volume purchasing arrangements with truck stop chains and bulk purchases of fuel at our terminals to control and recover our fuel expenses. We have no assurance that we will be able to collect fuel surcharges or enter into volume purchase agreements in the future. An increase in diesel

16

fuel prices or diesel fuel taxes, or any change in federal or state regulations that results in such an increase, could have a material adverse effect on our operating results, unless the increase is offset by increases in freight rates or fuel surcharges charged to our customers. Historically, we have been able to offset significant increases in diesel fuel prices through fuel surcharges to our customers, and we were able to minimize the negative impact on our profitability in 2008 that resulted from the rapid and significant increase to the cost of diesel fuel. Depending on the base rate and fuel surcharge levels agreed upon by individual shippers, a rapid and significant decline in the cost of diesel fuel could also have a material adverse effect on our operating results. We continuously monitor the components of our pricing, including base freight rates and fuel surcharges, and address individual account profitability issues with our customers when necessary. While we have historically been able to adjust our pricing to offset changes to the cost of diesel fuel, through changes to base rates and/or fuel surcharges, we cannot be certain that we will be able to do so in the future. The absence of meaningful fuel price protection through these measures, fluctuations in fuel prices, or a shortage of diesel fuel, could materially and adversely affect our results of operations.

Our operations are subject to various environmental laws and regulations, the violation of which could result in substantial fines or penalties.

We are subject to various federal, state and local environmental laws and regulations dealing with the handling and transportation of hazardous materials ("hazmat") and waste ("hazwaste") (which is a material portion of our existing business). We operate in industrial areas, where truck terminals and other industrial activities are located, and where groundwater or other forms of environmental contamination have occurred. Our operations involve the risks of fuel spillage or seepage, environmental damage and hazardous waste disposal, among others. If a spill or other accident involving fuel, oil or hazardous substances occurs, or if we are found to be in violation of applicable laws or regulations, it could have a material adverse effect on our business and operating results. One of our subsidiaries specializes in transport of hazardous materials and waste. If we should fail to comply with applicable environmental laws and regulations, we could be subject to substantial fines or penalties, to civil and criminal liability and to loss of our licenses to transport the hazardous materials and waste. Under certain environmental laws, we could also be held responsible for any costs relating to contamination at our past facilities and at third-party waste disposal sites. Any of these consequences from violation of such laws and regulations could be expected to have a material adverse effect on our business and prospects, financial and otherwise.

Increased prices, reduced productivity, and restricted availability of new revenue equipment could cause our financial condition, results of operations and cash flows to suffer.

Prices for new tractors have increased over the past few years, primarily as a result of higher commodity prices, better pricing power among equipment manufacturers, and government regulations applicable to newly manufactured tractors and diesel engines. We expect to continue to pay increased prices for revenue equipment and incur additional expenses and related financing costs for the foreseeable future. Our business could be harmed if we are unable to continue to obtain an adequate supply of new tractors and trailers or if we have to pay increased prices for new revenue equipment. The EPA adopted revised emissions control regulations, which require progressive reductions in exhaust emissions from diesel engines through 2010, for engines manufactured in October 2002, and thereafter. Some manufacturers have significantly increased new equipment prices, in part to meet new engine design requirements imposed by the EPA, increasing the cost of our new tractors. The revised regulations decrease the amount of emissions that can be released by tractor engines and affect tractors produced after the effective date of the regulations. Compliance with these regulations has, lowered fuel mileage and increased our operating expenses and maintenance costs. These adverse effects combined with the uncertainty as to the reliability of the vehicles equipped with the newly designed diesel engines and the residual values that will be realized from the disposition of older vehicles are expected increase our costs or otherwise adversely affect our business or operations. There is no assurance that continued increases in pricing or costs will not have an adverse effect on our business and operations.

Seasonality and the impact of weather can adversely affect our profitability.

Our tractor productivity generally decreases during the winter season because inclement weather impedes operations and some shippers reduce their shipments. At the same time, operating expenses generally increase, with harsh weather creating higher accident frequency, increased claims and more equipment repairs. We can also suffer short-term impacts from weather-related events such as hurricanes, blizzards, ice-storms, and floods that could harm our results or make our results more volatile.

17

Increases in driver compensation or difficulty in attracting drivers could affect our profitability and ability to grow.

We periodically experience difficulties in attracting and retaining qualified drivers, including independent contract drivers. With increased competition for drivers, we could experience greater difficulty in attracting sufficient numbers of qualified drivers. In addition, due in part to current economic conditions, including the cost of fuel and insurance, the available pool of independent contractor drivers is smaller than it has been historically. Accordingly, we may and periodically do face difficulty in attracting and retaining drivers for all of our current tractors and for those we may add. We may face difficulty in increasing the number of our independent contractor drivers. In addition, our industry suffers from high turnover rates of drivers. Our turnover rate requires us to recruit a substantial number of drivers. Moreover, our turnover rate could increase. If we are unable to continue to attract drivers and contract with independent contractors, we could be required to continue adjusting our driver compensation package beyond the norm or let equipment sit idle. An increase in our expenses or in the number of power units without drivers could materially and adversely affect our growth and profitability. Our operations may be affected in other ways by a shortage of qualified drivers in the future, such as temporary under-utilize our fleet and difficulty in meeting shipper demands. When we encounter difficulty in attracting or retaining qualified drivers, our ability to service our customers and increase our revenue could be adversely affected. A shortage of qualified drivers in the future could cause us to temporarily under-utilize our fleet, face difficulty in meeting shipper demands and increase our compensation levels for drivers.

We operate in a highly regulated industry and increased costs of compliance with, or liability for violation of, existing or future regulations could have a materially adverse effect on our business.

The DOT and various state and local agencies exercise broad powers over our business, generally governing such activities as authorization to engage in motor carrier operations, safety and insurance requirements. Our company drivers and independent contractors also must comply with the safety and fitness regulations promulgated by the DOT, including those relating to drug and alcohol testing and hours-of-service. We also may become subject to new or more restrictive regulations relating to fuel emissions, drivers’ hours-of-service, ergonomics, or other matters affecting safety or operating methods. Other agencies, such as the EPA and the Department of Homeland Security, or DHS, also regulate our equipment, operations, and drivers. Future laws and regulations may be more stringent and require changes in our operating practices, influence the demand for transportation services, or require us to incur significant additional costs. Higher costs incurred by us or by our suppliers who pass the costs onto us through higher prices could adversely affect our results of operations.

In the aftermath of the September 11, 2001 terrorist attacks, federal, state, and municipal authorities have implemented and continue to implement various security measures, including checkpoints and travel restrictions on large trucks. As a result, it is possible we may fail to meet the needs of our customers or may incur increased expenses to do so. These security measures could negatively impact our operating results.

Some states and municipalities have begun to restrict the locations and amount of time where diesel-powered tractors, such as ours, may idle, in order to reduce exhaust emissions. The State of California has recently enacted legislation which requires tractors weighing more than 10,000 pounds to use alternative sources, such as auxiliary power units, when powering their cabs at idle for more than five minutes. The State of California has also enacted legislation requiring compliance with exhaust emissions standards for refrigeration units on trailers. Compliance is being phased in by the state, beginning with 2001 and earlier models. Given our investment in auxiliary power units for our tractors and the average age of our trailer fleet, we do not expect these regulations will have a significant impact on our operations or financial results.

From time to time, various federal, state, or local taxes are increased, including taxes on fuels. We cannot predict whether, or in what form, any such increase applicable to us will be enacted, but such an increase could aversely affect our profitability.

Higher interest rates on borrowed funds would adversely impact our results of operations.

We rely on borrowings to finance our revenue equipment and receivables. We are subject to interest rate risk to the extent our borrowings. Even though we attempt to manage our interest rate risk by managing the amount of debt we carry, our debt levels are not entirely within our control in the short term. An increase in the rates of interest we incur on borrowings and financing we cannot decrease in the short term without adversely impacting our level of service to our customers and expansion of our business will adversely affect our results of operations.

18

Our financial results may be adversely impacted by potential future changes in accounting practices.