Attached files

| file | filename |

|---|---|

| EX-99.3 - EX-99.3 - CONTANGO OIL & GAS CO | d170200dex993.htm |

| EX-99.2 - EX-99.2 - CONTANGO OIL & GAS CO | d170200dex992.htm |

| EX-99.1 - EX-99.1 - CONTANGO OIL & GAS CO | d170200dex991.htm |

| EX-2.1 - EX-2.1 - CONTANGO OIL & GAS CO | d170200dex21.htm |

| 8-K - 8-K - CONTANGO OIL & GAS CO | d170200d8k.htm |

Exhibit 99.4 j*V © Independence + Energy Contango . IT, J « -A 1 i Transformative Merger with Independence June 2021 +Exhibit 99.4 j*V © Independence + Energy Contango . IT, J « -A 1 i Transformative Merger with Independence June 2021 +

Disclaimer This presentation relates to a proposed business combination transaction (the “Transaction”) between Independence Energy LLC (the “Company”) and Contango Oil & Gas (“Contango”), and contains “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical fact, included in this communication that address activities, events or developments that Contango or Independence expects, believes or anticipates will or may occur in the future are forward-looking statements. Words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “create,” “intend,” “could,” “may,” “foresee,” “plan,” “will,” “guidance,” “look,” “outlook,” “goal,” “future,” “assume,” “forecast,” “build,” “focus,” “work,” “continue” or the negative of such terms or other variations thereof and words and terms of similar substance used in connection with any discussion of future plans, actions, or events identify forward-looking statements. However, the absence of these words does not mean that the statements are not forward-looking. These forward-looking statements include, but are not limited to, statements regarding the Transaction, pro forma descriptions of the combined company and its operations, integration and transition plans, synergies, opportunities, anticipated future performance, future commodity prices, future production targets, future earnings, EBITDA, leverage targets, future capital spending plans, operational efficiencies, inventory life, hedging activities, business strategy, estimated reserves, cash flows and liquidity, financial strategy, budget, projections and future operating results. There are a number of risks and uncertainties that could cause actual results to differ materially from the forward-looking statements included in this communication. These include the expected timing and likelihood of completion of the Transaction, including the timing, receipt and terms and conditions of any required governmental and regulatory approvals of the Transaction that could reduce anticipated benefits or cause the parties to abandon the Transaction, the ability to successfully integrate the businesses, the occurrence of any event, change or other circumstances that could give rise to the termination of the transaction agreement, the possibility that stockholders of Contango may not approve the Transaction, the risk that the parties may not be able to satisfy the conditions to the Transaction in a timely manner or at all, risks related to disruption of management time from ongoing business operations due to the Transaction, the risk that any announcements relating to the Transaction could have adverse effects on the market price of Contango’s common stock, the risk that the Transaction and its announcement could have an adverse effect on the ability of Contango and Independence to retain customers and retain and hire key personnel and maintain relationships with their suppliers and customers and on their operating results and businesses generally, the risk the pending Transaction could distract management of both entities and they will incur substantial costs, the risk that problems may arise in successfully integrating the businesses of the companies, which may result in the combined company not operating as effectively and efficiently as expected, the risk that the combined company may be unable to achieve synergies or it may take longer than expected to achieve those synergies, the impact of reduced demand for Contango’s or the Company’s products and products made from them due to governmental and societal actions taken in response to the COVID-19 pandemic; the uncertainties, costs and risks involved in Contango’s and the Company’s operations, including as a result of employee misconduct; natural disasters, pandemics, epidemics (including COVID-19 and any escalation or worsening thereof) or other public health conditions and other important factors that could cause actual results to differ materially from those projected. All such factors are difficult to predict and are beyond Contango’s or the Company’s control, including those detailed in Contango’s annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K that are available on its website at http://www.contango.com and on the SEC’s website at http://www.sec.gov. All forward-looking statements are based on assumptions that Contango or the Company believe to be reasonable but that may not prove to be accurate. Any forward-looking statement speaks only as of the date on which such statement is made, and Contango and the Company undertake no obligation to correct or update any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by applicable law. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date hereof. Reserve engineering is a process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data and price and cost assumptions made by reservoir engineers. In addition, the results of drilling, testing and production activities may justify revisions of estimates that were made previously. If significant, such revisions would change the schedule of any further production and development drilling. Unless otherwise indicated, reserve estimates shown herein are based on third party reserve reports as of December 31, 2020, and were prepared using commodity prices based on Henry Hub and WTI futures prices, referred to herein as “strip” pricing, rather than SEC pricing guidelines. The Company believes that the use of strip pricing provides useful information about its reserves, as the forward prices are based on the market’s forward-looking expectations of oil and natural gas prices as of a certain date. Strip prices are not necessarily a projection of future oil and natural gas prices, and should be carefully considered in addition to, and not as a substitute for, SEC prices, when considering the Company’s oil, natural gas and NGL reserves. This presentation contains guidance regarding our estimated future production, capital expenditures, expenses and other matters and such guidance is based on an assumption that prevailing commodity prices over the relevant time periods will be consistent with NYMEX strip pricing as of June 4, 2021 and assumes a cumulative reinvestment rate of ~41% through 2021 and 2022. This guidance is also based on certain additional assumptions and analyses made by the Company and is affected by such factors as market demand for oil and natural gas, commodity price volatility and the Company’s actual drilling program, which will be directly affected by the availability of capital, drilling and production costs, developmental drilling tests and results, commodity prices, availability of drilling services and equipment, lease expirations, transportation constraints, regulatory approvals, field spacing rules and actual drilling results. This guidance is speculative by its nature and, accordingly, is subject to great risk of not being actually realized by the Company. This presentation includes certain financial measures that are not calculated in accordance with U.S. generally accepted accounting principles (“GAAP”). These measures include (i) EBITDA, (ii) Adj. EBITDA, (iii) Net debt, (iv) leverage, (v) PV-0, (vi) PV-10, (vii) Levered Free Cash Flow and (viii) Reinvestment Rate. The Company defines EBITDA as net income (loss) before interest expense, taxes, depreciation, depletion and amortization, and oil and gas exploration expenses. The Company defines Adjusted EBITDA as net income before interest expense, realized (gain) loss on interest expense derivatives, income tax expense, depreciation, depletion and amortization, exploration expense, non-cash gain (loss) on derivative contracts, impairment of oil and natural gas properties, equity-based compensation, other (income) expense, transaction expenses and other non-recurring expenses. The Company defined Net Debt as total debt less unrestricted cash & cash equivalents. The Company defined Leverage as Net Debt / Adjusted EBITDA. The Company defines PV-0 as the sum of estimated future cash inflows from proved natural gas and crude oil reserves, less future development and production costs using pricing assumptions in effect at the end of the period. The Company defines PV-10 as the present value, discounted at 10% per year, of estimated future cash inflows from proved natural gas and crude oil reserves, less future development and production costs using pricing assumptions in effect at the end of the period. The Company defines Levered Free Cash Flow as Adj. EBITDA less cash paid for interest, cash paid or refunded for income tax and capital expenditures associated with the development of oil and gas properties and purchases of other property and equipment. The Company defined Reinvestment Rate as capital expenditures as a percentage of Adj. EBITDA. The Company has not provided reconciliations for forward-looking non-GAAP measures because the Company cannot do so without unreasonable effort and any attempt to do so would be inherently imprecise. This presentation shall not constitute an offer to purchase or sell, or the solicitation of an offer to purchase or sell, any securities in any jurisdiction where such an offer or solicitation would be in violation of any local laws. Nothing contained herein constitutes tax, accounting, financial, investment, regulatory, legal or other advice, and all investors are advised to consult with their tax, accounting, financial, investment, regulatory or legal advisers regarding any potential investment. The information presented in these materials has been developed internally and/or obtained from sources believed to be reliable; however, the parties do not guarantee or give any warranty as to the accuracy, adequacy, timeliness or completeness of such information, and assumes no responsibility for independent verification of such information. The Company was formed in 2020 for purposes of completing a series of reorganization transactions. Historical financial and operating date of the Company has been presented on a recast basis to account for the reorganization of entities under common control. In addition, certain financial and operating data is presented on a “pro forma” basis. As used herein, the term “pro forma” or “PF” when used with respect to any financial and operating data refers to the historical data of the Company, as adjusted to give effect to (i) the redemption by certain of the Company’s consolidated subsidiaries of the noncontrolling equity interests held in such subsidiaries by certain third-party investors in exchange for membership interests in the Company in April 2021 (the “Exchange”); (ii) the redemption by certain of the Company’s consolidated subsidiaries of the noncontrolling equity interests held in such subsidiaries by a certain third-party investor in exchange for its proportionate share of the underlying oil and natural gas interests held directly or indirectly by such subsidiaries (the “Carve-Out”); (iii) the entry into the new RBL facility, the issuance of the new senior unsecured notes and the use of proceeds therefrom (the “Refinancing”); and (iv) the Transaction (as defined below and, together with the Exchange, the Carve-Out and the Refinancing, the “Transactions”). Unless otherwise indicated, pro forma financial and operating data used in this presentation gives effect to each of the Transactions as if they had been consummated on January 1, 2021, in the case of statement of operations data, or March 31, 2021, in the case of balance sheet data. In each case, the pro forma financial and operating data are presented for illustrative purposes only and should not be relied upon as an indication of the financial condition or the operating results that would have achieved if the Transactions had taken place on the specified dates. In addition, future results may vary significantly from the results reflected in such pro forma financial and operating data and should not be relied on as an indication of future results. The financial data included in this presentation was prepared by the Company’s management. The Company’s independent auditors have not expressed any opinion or any form of assurance on such information. In addition, the pro forma financial data presented herein is based on certain assumptions that may prove incorrect. Such financial data should not be viewed as a substitute for full financial statements prepared in accordance with GAAP and audited by the Company’s independent auditors, and it should not be viewed as indicative of the Company’s financial condition or results of operations for any future period. + 2Disclaimer This presentation relates to a proposed business combination transaction (the “Transaction”) between Independence Energy LLC (the “Company”) and Contango Oil & Gas (“Contango”), and contains “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical fact, included in this communication that address activities, events or developments that Contango or Independence expects, believes or anticipates will or may occur in the future are forward-looking statements. Words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “create,” “intend,” “could,” “may,” “foresee,” “plan,” “will,” “guidance,” “look,” “outlook,” “goal,” “future,” “assume,” “forecast,” “build,” “focus,” “work,” “continue” or the negative of such terms or other variations thereof and words and terms of similar substance used in connection with any discussion of future plans, actions, or events identify forward-looking statements. However, the absence of these words does not mean that the statements are not forward-looking. These forward-looking statements include, but are not limited to, statements regarding the Transaction, pro forma descriptions of the combined company and its operations, integration and transition plans, synergies, opportunities, anticipated future performance, future commodity prices, future production targets, future earnings, EBITDA, leverage targets, future capital spending plans, operational efficiencies, inventory life, hedging activities, business strategy, estimated reserves, cash flows and liquidity, financial strategy, budget, projections and future operating results. There are a number of risks and uncertainties that could cause actual results to differ materially from the forward-looking statements included in this communication. These include the expected timing and likelihood of completion of the Transaction, including the timing, receipt and terms and conditions of any required governmental and regulatory approvals of the Transaction that could reduce anticipated benefits or cause the parties to abandon the Transaction, the ability to successfully integrate the businesses, the occurrence of any event, change or other circumstances that could give rise to the termination of the transaction agreement, the possibility that stockholders of Contango may not approve the Transaction, the risk that the parties may not be able to satisfy the conditions to the Transaction in a timely manner or at all, risks related to disruption of management time from ongoing business operations due to the Transaction, the risk that any announcements relating to the Transaction could have adverse effects on the market price of Contango’s common stock, the risk that the Transaction and its announcement could have an adverse effect on the ability of Contango and Independence to retain customers and retain and hire key personnel and maintain relationships with their suppliers and customers and on their operating results and businesses generally, the risk the pending Transaction could distract management of both entities and they will incur substantial costs, the risk that problems may arise in successfully integrating the businesses of the companies, which may result in the combined company not operating as effectively and efficiently as expected, the risk that the combined company may be unable to achieve synergies or it may take longer than expected to achieve those synergies, the impact of reduced demand for Contango’s or the Company’s products and products made from them due to governmental and societal actions taken in response to the COVID-19 pandemic; the uncertainties, costs and risks involved in Contango’s and the Company’s operations, including as a result of employee misconduct; natural disasters, pandemics, epidemics (including COVID-19 and any escalation or worsening thereof) or other public health conditions and other important factors that could cause actual results to differ materially from those projected. All such factors are difficult to predict and are beyond Contango’s or the Company’s control, including those detailed in Contango’s annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K that are available on its website at http://www.contango.com and on the SEC’s website at http://www.sec.gov. All forward-looking statements are based on assumptions that Contango or the Company believe to be reasonable but that may not prove to be accurate. Any forward-looking statement speaks only as of the date on which such statement is made, and Contango and the Company undertake no obligation to correct or update any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by applicable law. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date hereof. Reserve engineering is a process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data and price and cost assumptions made by reservoir engineers. In addition, the results of drilling, testing and production activities may justify revisions of estimates that were made previously. If significant, such revisions would change the schedule of any further production and development drilling. Unless otherwise indicated, reserve estimates shown herein are based on third party reserve reports as of December 31, 2020, and were prepared using commodity prices based on Henry Hub and WTI futures prices, referred to herein as “strip” pricing, rather than SEC pricing guidelines. The Company believes that the use of strip pricing provides useful information about its reserves, as the forward prices are based on the market’s forward-looking expectations of oil and natural gas prices as of a certain date. Strip prices are not necessarily a projection of future oil and natural gas prices, and should be carefully considered in addition to, and not as a substitute for, SEC prices, when considering the Company’s oil, natural gas and NGL reserves. This presentation contains guidance regarding our estimated future production, capital expenditures, expenses and other matters and such guidance is based on an assumption that prevailing commodity prices over the relevant time periods will be consistent with NYMEX strip pricing as of June 4, 2021 and assumes a cumulative reinvestment rate of ~41% through 2021 and 2022. This guidance is also based on certain additional assumptions and analyses made by the Company and is affected by such factors as market demand for oil and natural gas, commodity price volatility and the Company’s actual drilling program, which will be directly affected by the availability of capital, drilling and production costs, developmental drilling tests and results, commodity prices, availability of drilling services and equipment, lease expirations, transportation constraints, regulatory approvals, field spacing rules and actual drilling results. This guidance is speculative by its nature and, accordingly, is subject to great risk of not being actually realized by the Company. This presentation includes certain financial measures that are not calculated in accordance with U.S. generally accepted accounting principles (“GAAP”). These measures include (i) EBITDA, (ii) Adj. EBITDA, (iii) Net debt, (iv) leverage, (v) PV-0, (vi) PV-10, (vii) Levered Free Cash Flow and (viii) Reinvestment Rate. The Company defines EBITDA as net income (loss) before interest expense, taxes, depreciation, depletion and amortization, and oil and gas exploration expenses. The Company defines Adjusted EBITDA as net income before interest expense, realized (gain) loss on interest expense derivatives, income tax expense, depreciation, depletion and amortization, exploration expense, non-cash gain (loss) on derivative contracts, impairment of oil and natural gas properties, equity-based compensation, other (income) expense, transaction expenses and other non-recurring expenses. The Company defined Net Debt as total debt less unrestricted cash & cash equivalents. The Company defined Leverage as Net Debt / Adjusted EBITDA. The Company defines PV-0 as the sum of estimated future cash inflows from proved natural gas and crude oil reserves, less future development and production costs using pricing assumptions in effect at the end of the period. The Company defines PV-10 as the present value, discounted at 10% per year, of estimated future cash inflows from proved natural gas and crude oil reserves, less future development and production costs using pricing assumptions in effect at the end of the period. The Company defines Levered Free Cash Flow as Adj. EBITDA less cash paid for interest, cash paid or refunded for income tax and capital expenditures associated with the development of oil and gas properties and purchases of other property and equipment. The Company defined Reinvestment Rate as capital expenditures as a percentage of Adj. EBITDA. The Company has not provided reconciliations for forward-looking non-GAAP measures because the Company cannot do so without unreasonable effort and any attempt to do so would be inherently imprecise. This presentation shall not constitute an offer to purchase or sell, or the solicitation of an offer to purchase or sell, any securities in any jurisdiction where such an offer or solicitation would be in violation of any local laws. Nothing contained herein constitutes tax, accounting, financial, investment, regulatory, legal or other advice, and all investors are advised to consult with their tax, accounting, financial, investment, regulatory or legal advisers regarding any potential investment. The information presented in these materials has been developed internally and/or obtained from sources believed to be reliable; however, the parties do not guarantee or give any warranty as to the accuracy, adequacy, timeliness or completeness of such information, and assumes no responsibility for independent verification of such information. The Company was formed in 2020 for purposes of completing a series of reorganization transactions. Historical financial and operating date of the Company has been presented on a recast basis to account for the reorganization of entities under common control. In addition, certain financial and operating data is presented on a “pro forma” basis. As used herein, the term “pro forma” or “PF” when used with respect to any financial and operating data refers to the historical data of the Company, as adjusted to give effect to (i) the redemption by certain of the Company’s consolidated subsidiaries of the noncontrolling equity interests held in such subsidiaries by certain third-party investors in exchange for membership interests in the Company in April 2021 (the “Exchange”); (ii) the redemption by certain of the Company’s consolidated subsidiaries of the noncontrolling equity interests held in such subsidiaries by a certain third-party investor in exchange for its proportionate share of the underlying oil and natural gas interests held directly or indirectly by such subsidiaries (the “Carve-Out”); (iii) the entry into the new RBL facility, the issuance of the new senior unsecured notes and the use of proceeds therefrom (the “Refinancing”); and (iv) the Transaction (as defined below and, together with the Exchange, the Carve-Out and the Refinancing, the “Transactions”). Unless otherwise indicated, pro forma financial and operating data used in this presentation gives effect to each of the Transactions as if they had been consummated on January 1, 2021, in the case of statement of operations data, or March 31, 2021, in the case of balance sheet data. In each case, the pro forma financial and operating data are presented for illustrative purposes only and should not be relied upon as an indication of the financial condition or the operating results that would have achieved if the Transactions had taken place on the specified dates. In addition, future results may vary significantly from the results reflected in such pro forma financial and operating data and should not be relied on as an indication of future results. The financial data included in this presentation was prepared by the Company’s management. The Company’s independent auditors have not expressed any opinion or any form of assurance on such information. In addition, the pro forma financial data presented herein is based on certain assumptions that may prove incorrect. Such financial data should not be viewed as a substitute for full financial statements prepared in accordance with GAAP and audited by the Company’s independent auditors, and it should not be viewed as indicative of the Company’s financial condition or results of operations for any future period. + 2

Disclaimer (Cont’d) Important Additional Information In connection with the proposed Transaction, IE PubCo Inc., a wholly owned subsidiary of the Company (“NewCo”), will file with the U.S. Securities and Exchange Commission (“SEC”) a registration statement on Form S-4, that will include a proxy statement of Contango and a prospectus of NewCo. The Transaction will be submitted to Contango’s stockholders for their consideration. NewCo and Contango may also file other documents with the SEC regarding the Transaction. The definitive proxy statement/prospectus will be sent to Contango’s stockholders. This document is not a substitute for the registration statement and proxy statement/prospectus that will be filed with the SEC or any other documents that Contango or NewCo may file with the SEC or send to stockholders of Contango in connection with the Transaction. INVESTORS AND SECURITY HOLDERS OF CONTANGO ARE URGED TO READ THE REGISTRATION STATEMENT AND THE PROXY STATEMENT/PROSPECTUS REGARDING THE TRANSACTION WHEN IT BECOMES AVAILABLE AND ALL OTHER RELEVANT DOCUMENTS THAT ARE FILED OR WILL BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE TRANSACTION AND RELATED MATTERS. Investors and security holders will be able to obtain free copies of the registration statement and the proxy statement/prospectus (when available) and all other documents filed or that will be filed with the SEC by Contango or NewCo through the website maintained by the SEC at http://www.sec.gov. Copies of documents filed with the SEC by NewCo will be made available free of charge on the Company’s website at www.independenceenergy.com, under the heading “SEC Filings,” or by directing a request to Investor Relations, Independence Energy LLC, Tel. No. +1 (713) 481-7782. Copies of documents filed with the SEC by Contango will be made available free of charge on Contango’s website at http://www.contango.com, or by directing a request to Investor Relations, Contango Oil & Gas Company, 717 Texas Avenue, Suite 2900, Tel. No. (713) 236-7400. Participants in the Solicitation Contango, the Company and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies in respect to the Transaction. Information regarding Contango’s executive officers and directors is contained in the proxy statement for Contango’s 2021 Annual Meeting of Stockholders filed with the SEC on April 30, 2021, and certain of its Current Reports on Form 8-K. Information regarding Independence’s directors and executive officers will be made available in the Proxy Statement/Prospectus that NewCo will file with the SEC. You can obtain free copies of these documents at the SEC’s website at www.sec.gov or by accessing Contango’s website at http://www.contango.com. Information about the Company’s executive officers will be contained in the proxy statement/prospectus that NewCo file with the SEC. When available, you can obtain free copies of these documents at the SEC’s website at www.sec.gov. Investors may obtain additional information regarding the interests of those persons and other persons who may be deemed participants in the Transaction by reading the proxy statement/prospectus regarding the Transaction when it becomes available. You may obtain free copies of this document as described above. + 3Disclaimer (Cont’d) Important Additional Information In connection with the proposed Transaction, IE PubCo Inc., a wholly owned subsidiary of the Company (“NewCo”), will file with the U.S. Securities and Exchange Commission (“SEC”) a registration statement on Form S-4, that will include a proxy statement of Contango and a prospectus of NewCo. The Transaction will be submitted to Contango’s stockholders for their consideration. NewCo and Contango may also file other documents with the SEC regarding the Transaction. The definitive proxy statement/prospectus will be sent to Contango’s stockholders. This document is not a substitute for the registration statement and proxy statement/prospectus that will be filed with the SEC or any other documents that Contango or NewCo may file with the SEC or send to stockholders of Contango in connection with the Transaction. INVESTORS AND SECURITY HOLDERS OF CONTANGO ARE URGED TO READ THE REGISTRATION STATEMENT AND THE PROXY STATEMENT/PROSPECTUS REGARDING THE TRANSACTION WHEN IT BECOMES AVAILABLE AND ALL OTHER RELEVANT DOCUMENTS THAT ARE FILED OR WILL BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE TRANSACTION AND RELATED MATTERS. Investors and security holders will be able to obtain free copies of the registration statement and the proxy statement/prospectus (when available) and all other documents filed or that will be filed with the SEC by Contango or NewCo through the website maintained by the SEC at http://www.sec.gov. Copies of documents filed with the SEC by NewCo will be made available free of charge on the Company’s website at www.independenceenergy.com, under the heading “SEC Filings,” or by directing a request to Investor Relations, Independence Energy LLC, Tel. No. +1 (713) 481-7782. Copies of documents filed with the SEC by Contango will be made available free of charge on Contango’s website at http://www.contango.com, or by directing a request to Investor Relations, Contango Oil & Gas Company, 717 Texas Avenue, Suite 2900, Tel. No. (713) 236-7400. Participants in the Solicitation Contango, the Company and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies in respect to the Transaction. Information regarding Contango’s executive officers and directors is contained in the proxy statement for Contango’s 2021 Annual Meeting of Stockholders filed with the SEC on April 30, 2021, and certain of its Current Reports on Form 8-K. Information regarding Independence’s directors and executive officers will be made available in the Proxy Statement/Prospectus that NewCo will file with the SEC. You can obtain free copies of these documents at the SEC’s website at www.sec.gov or by accessing Contango’s website at http://www.contango.com. Information about the Company’s executive officers will be contained in the proxy statement/prospectus that NewCo file with the SEC. When available, you can obtain free copies of these documents at the SEC’s website at www.sec.gov. Investors may obtain additional information regarding the interests of those persons and other persons who may be deemed participants in the Transaction by reading the proxy statement/prospectus regarding the Transaction when it becomes available. You may obtain free copies of this document as described above. + 3

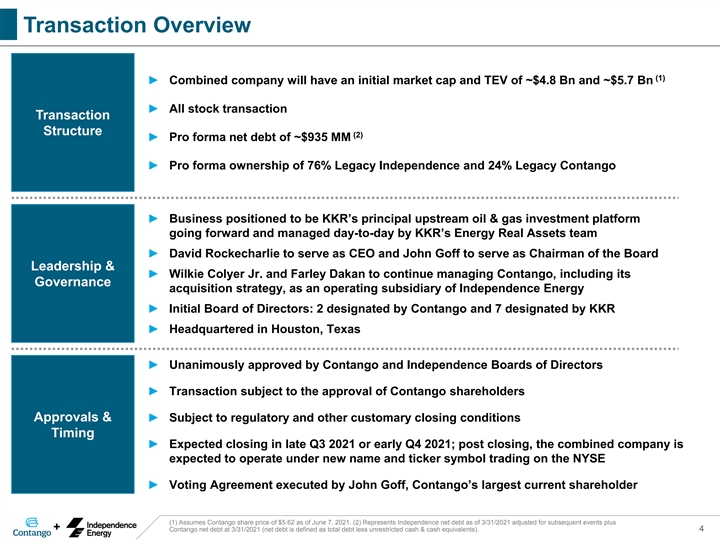

Transaction Overview (1) ► Combined company will have an initial market cap and TEV of ~$4.8 Bn and ~$5.7 Bn ► All stock transaction Transaction Structure (2) ► Pro forma net debt of ~$935 MM ► Pro forma ownership of 76% Legacy Independence and 24% Legacy Contango ► Business positioned to be KKR’s principal upstream oil & gas investment platform going forward and managed day-to-day by KKR’s Energy Real Assets team ► David Rockecharlie to serve as CEO and John Goff to serve as Chairman of the Board Leadership & ► Wilkie Colyer Jr. and Farley Dakan to continue managing Contango, including its Governance acquisition strategy, as an operating subsidiary of Independence Energy ► Initial Board of Directors: 2 designated by Contango and 7 designated by KKR ► Headquartered in Houston, Texas ► Unanimously approved by Contango and Independence Boards of Directors ► Transaction subject to the approval of Contango shareholders Approvals & ► Subject to regulatory and other customary closing conditions Timing ► Expected closing in late Q3 2021 or early Q4 2021; post closing, the combined company is expected to operate under new name and ticker symbol trading on the NYSE ► Voting Agreement executed by John Goff, Contango’s largest current shareholder (1) Assumes Contango share price of $5.62 as of June 7, 2021. (2) Represents Independence net debt as of 3/31/2021 adjusted for subsequent events plus + Contango net debt at 3/31/2021 (net debt is defined as total debt less unrestricted cash & cash equivalents). 4Transaction Overview (1) ► Combined company will have an initial market cap and TEV of ~$4.8 Bn and ~$5.7 Bn ► All stock transaction Transaction Structure (2) ► Pro forma net debt of ~$935 MM ► Pro forma ownership of 76% Legacy Independence and 24% Legacy Contango ► Business positioned to be KKR’s principal upstream oil & gas investment platform going forward and managed day-to-day by KKR’s Energy Real Assets team ► David Rockecharlie to serve as CEO and John Goff to serve as Chairman of the Board Leadership & ► Wilkie Colyer Jr. and Farley Dakan to continue managing Contango, including its Governance acquisition strategy, as an operating subsidiary of Independence Energy ► Initial Board of Directors: 2 designated by Contango and 7 designated by KKR ► Headquartered in Houston, Texas ► Unanimously approved by Contango and Independence Boards of Directors ► Transaction subject to the approval of Contango shareholders Approvals & ► Subject to regulatory and other customary closing conditions Timing ► Expected closing in late Q3 2021 or early Q4 2021; post closing, the combined company is expected to operate under new name and ticker symbol trading on the NYSE ► Voting Agreement executed by John Goff, Contango’s largest current shareholder (1) Assumes Contango share price of $5.62 as of June 7, 2021. (2) Represents Independence net debt as of 3/31/2021 adjusted for subsequent events plus + Contango net debt at 3/31/2021 (net debt is defined as total debt less unrestricted cash & cash equivalents). 4

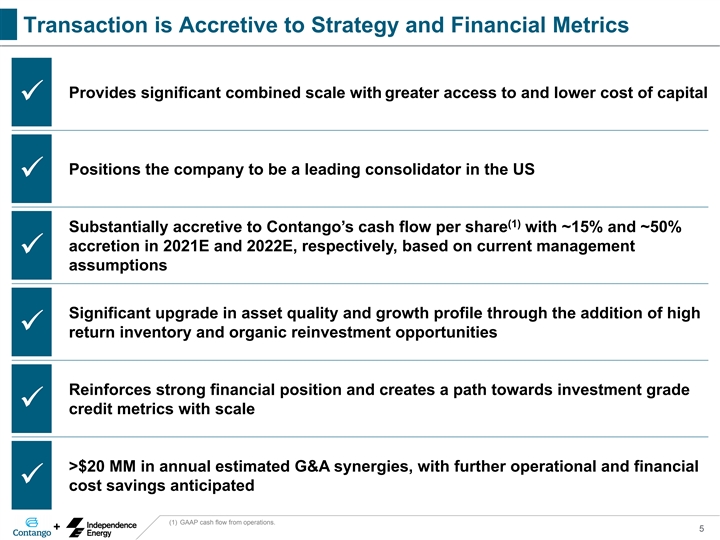

Transaction is Accretive to Strategy and Financial Metrics Provides significant combined scale with greater access to and lower cost of capital ✓ Positions the company to be a leading consolidator in the US ✓ (1) Substantially accretive to Contango’s cash flow per share with ~15% and ~50% accretion in 2021E and 2022E, respectively, based on current management ✓ assumptions Significant upgrade in asset quality and growth profile through the addition of high ✓ return inventory and organic reinvestment opportunities Reinforces strong financial position and creates a path towards investment grade ✓ credit metrics with scale >$20 MM in annual estimated G&A synergies, with further operational and financial ✓ cost savings anticipated (1) GAAP cash flow from operations. + 5Transaction is Accretive to Strategy and Financial Metrics Provides significant combined scale with greater access to and lower cost of capital ✓ Positions the company to be a leading consolidator in the US ✓ (1) Substantially accretive to Contango’s cash flow per share with ~15% and ~50% accretion in 2021E and 2022E, respectively, based on current management ✓ assumptions Significant upgrade in asset quality and growth profile through the addition of high ✓ return inventory and organic reinvestment opportunities Reinforces strong financial position and creates a path towards investment grade ✓ credit metrics with scale >$20 MM in annual estimated G&A synergies, with further operational and financial ✓ cost savings anticipated (1) GAAP cash flow from operations. + 5

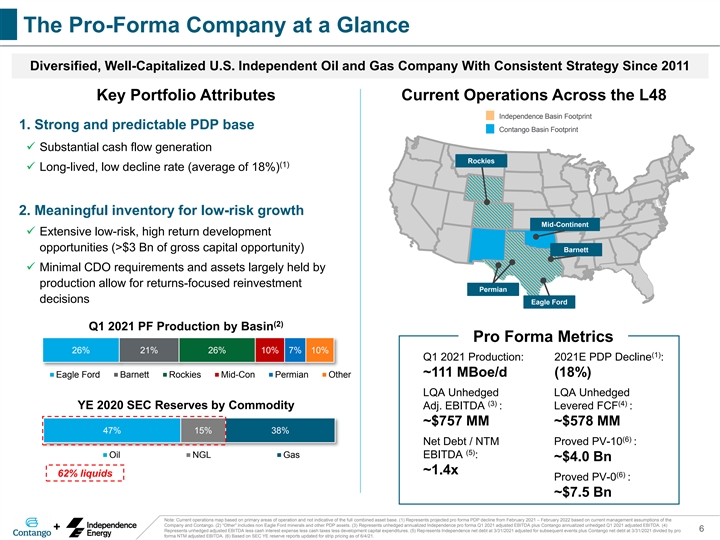

The Pro-Forma Company at a Glance Diversified, Well-Capitalized U.S. Independent Oil and Gas Company With Consistent Strategy Since 2011 Key Portfolio Attributes Current Operations Across the L48 Independence Basin Footprint 1. Strong and predictable PDP base Contango Basin Footprint ✓ Substantial cash flow generation Rockies (1) ✓ Long-lived, low decline rate (average of 18%) 2. Meaningful inventory for low-risk growth Mid-Continent ✓ Extensive low-risk, high return development opportunities (>$3 Bn of gross capital opportunity) Barnett ✓ Minimal CDO requirements and assets largely held by production allow for returns-focused reinvestment Permian decisions Eagle Ford (2) Q1 2021 PF Production by Basin Pro Forma Metrics 26% 21% 26% 10% 7% 10% (1) Q1 2021 Production: 2021E PDP Decline : ~111 MBoe/d (18%) Eagle Ford Barnett Rockies Mid-Con Permian Other LQA Unhedged LQA Unhedged (3) (4) YE 2020 SEC Reserves by Commodity Adj. EBITDA : Levered FCF : ~$757 MM ~$578 MM 47% 15% 38% (6) Net Debt / NTM Proved PV-10 : (5) Oil NGL Gas EBITDA : ~$4.0 Bn ~1.4x 62% liquids (6) Proved PV-0 : ~$7.5 Bn Note: Current operations map based on primary areas of operation and not indicative of the full combined asset base. (1) Represents projected pro forma PDP decline from February 2021 – February 2022 based on current management assumptions of the Company and Contango. (2) “Other” includes non Eagle Ford minerals and other PDP assets. (3) Represents unhedged annualized Independence pro forma Q1 2021 adjusted EBITDA plus Contango annualized unhedged Q1 2021 adjusted EBITDA. (4) + Represents unhedged adjusted EBITDA less cash interest expense less cash taxes less development capital expenditures. (5) Represents Independence net debt at 3/31/2021 adjusted for subsequent events plus Contango net debt at 3/31/2021 divided by pro 6 forma NTM adjusted EBITDA. (6) Based on SEC YE reserve reports updated for strip pricing as of 6/4/21.The Pro-Forma Company at a Glance Diversified, Well-Capitalized U.S. Independent Oil and Gas Company With Consistent Strategy Since 2011 Key Portfolio Attributes Current Operations Across the L48 Independence Basin Footprint 1. Strong and predictable PDP base Contango Basin Footprint ✓ Substantial cash flow generation Rockies (1) ✓ Long-lived, low decline rate (average of 18%) 2. Meaningful inventory for low-risk growth Mid-Continent ✓ Extensive low-risk, high return development opportunities (>$3 Bn of gross capital opportunity) Barnett ✓ Minimal CDO requirements and assets largely held by production allow for returns-focused reinvestment Permian decisions Eagle Ford (2) Q1 2021 PF Production by Basin Pro Forma Metrics 26% 21% 26% 10% 7% 10% (1) Q1 2021 Production: 2021E PDP Decline : ~111 MBoe/d (18%) Eagle Ford Barnett Rockies Mid-Con Permian Other LQA Unhedged LQA Unhedged (3) (4) YE 2020 SEC Reserves by Commodity Adj. EBITDA : Levered FCF : ~$757 MM ~$578 MM 47% 15% 38% (6) Net Debt / NTM Proved PV-10 : (5) Oil NGL Gas EBITDA : ~$4.0 Bn ~1.4x 62% liquids (6) Proved PV-0 : ~$7.5 Bn Note: Current operations map based on primary areas of operation and not indicative of the full combined asset base. (1) Represents projected pro forma PDP decline from February 2021 – February 2022 based on current management assumptions of the Company and Contango. (2) “Other” includes non Eagle Ford minerals and other PDP assets. (3) Represents unhedged annualized Independence pro forma Q1 2021 adjusted EBITDA plus Contango annualized unhedged Q1 2021 adjusted EBITDA. (4) + Represents unhedged adjusted EBITDA less cash interest expense less cash taxes less development capital expenditures. (5) Represents Independence net debt at 3/31/2021 adjusted for subsequent events plus Contango net debt at 3/31/2021 divided by pro 6 forma NTM adjusted EBITDA. (6) Based on SEC YE reserve reports updated for strip pricing as of 6/4/21.

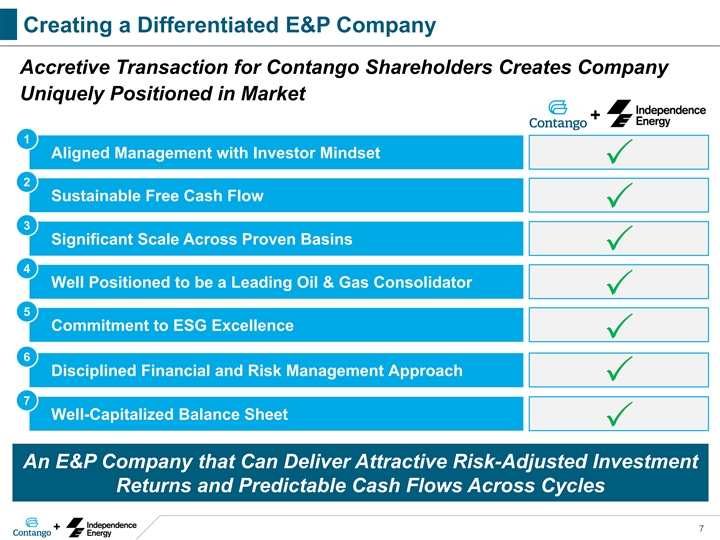

Creating a Differentiated E&P Company Accretive Transaction for Contango Shareholders Creates Company Uniquely Positioned in Market + 1 Aligned Management with Investor Mindset P 2 Sustainable Free Cash Flow P 3 Significant Scale Across Proven Basins P 4 Well Positioned to be a Leading Oil & Gas Consolidator P 5 Commitment to ESG Excellence P 6 Disciplined Financial and Risk Management Approach P 7 Well-Capitalized Balance Sheet P An E&P Company that Can Deliver Attractive Risk-Adjusted Investment Returns and Predictable Cash Flows Across Cycles + 7Creating a Differentiated E&P Company Accretive Transaction for Contango Shareholders Creates Company Uniquely Positioned in Market + 1 Aligned Management with Investor Mindset P 2 Sustainable Free Cash Flow P 3 Significant Scale Across Proven Basins P 4 Well Positioned to be a Leading Oil & Gas Consolidator P 5 Commitment to ESG Excellence P 6 Disciplined Financial and Risk Management Approach P 7 Well-Capitalized Balance Sheet P An E&P Company that Can Deliver Attractive Risk-Adjusted Investment Returns and Predictable Cash Flows Across Cycles + 7

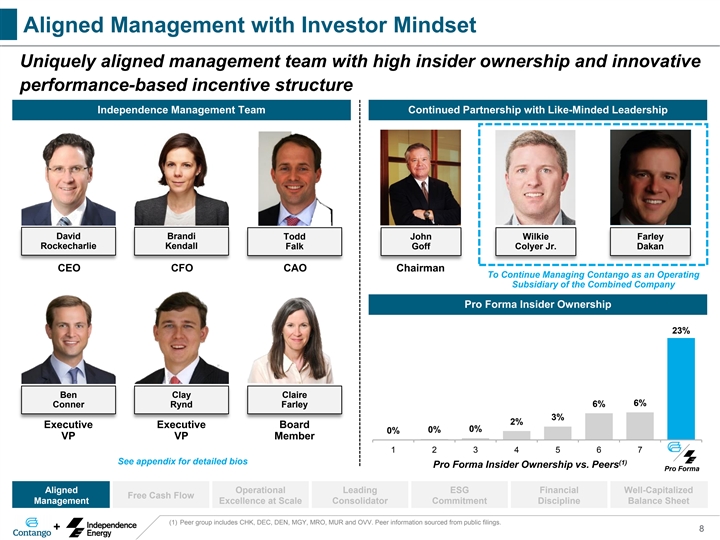

Aligned Management with Investor Mindset Uniquely aligned management team with high insider ownership and innovative performance-based incentive structure Independence Management Team Continued Partnership with Like-Minded Leadership David Brandi Todd John Wilkie Farley Rockecharlie Kendall Falk Goff Colyer Jr. Dakan CEO CFO CAO Chairman To Continue Managing Contango as an Operating Subsidiary of the Combined Company Pro Forma Insider Ownership 23% Ben Clay Claire 6% 6% Conner Rynd Farley 3% 2% Executive Executive Board 0% 0% 0% VP VP Member 1 2 3 4 5 6 7 PF See appendix for detailed bios (1) Pro Forma Insider Ownership vs. Peers Pro Forma Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Peer group includes CHK, DEC, DEN, MGY, MRO, MUR and OVV. Peer information sourced from public filings. + 8Aligned Management with Investor Mindset Uniquely aligned management team with high insider ownership and innovative performance-based incentive structure Independence Management Team Continued Partnership with Like-Minded Leadership David Brandi Todd John Wilkie Farley Rockecharlie Kendall Falk Goff Colyer Jr. Dakan CEO CFO CAO Chairman To Continue Managing Contango as an Operating Subsidiary of the Combined Company Pro Forma Insider Ownership 23% Ben Clay Claire 6% 6% Conner Rynd Farley 3% 2% Executive Executive Board 0% 0% 0% VP VP Member 1 2 3 4 5 6 7 PF See appendix for detailed bios (1) Pro Forma Insider Ownership vs. Peers Pro Forma Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Peer group includes CHK, DEC, DEN, MGY, MRO, MUR and OVV. Peer information sourced from public filings. + 8

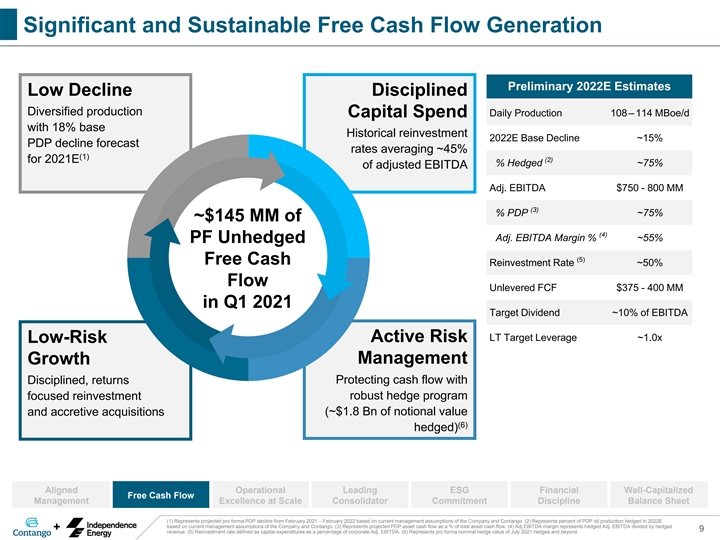

Significant and Sustainable Free Cash Flow Generation Preliminary 2022E Estimates Low Decline Disciplined Diversified production Daily Production 108– 114 MBoe/d Capital Spend with 18% base Historical reinvestment 2022E Base Decline ~15% PDP decline forecast rates averaging ~45% (1) (2) for 2021E % Hedged ~75% of adjusted EBITDA Adj. EBITDA $750 - 800 MM (3) % PDP ~75% ~$145 MM of ~$95MM of (4) Adj. EBITDA Margin % ~55% PF Unhedged Free Cash (5) Free Cash Reinvestment Rate ~50% 1 Flow Flow Unlevered FCF $375 - 400 MM in Q1 2021 in Q1 2021 Target Dividend ~10% of EBITDA LT Target Leverage ~1.0x Active Risk Low-Risk Management Growth Disciplined, returns Protecting cash flow with focused reinvestment robust hedge program (~$1.8 Bn of notional value and accretive acquisitions (6) hedged) Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Represents projected pro forma PDP decline from February 2021 – February 2022 based on current management assumptions of the Company and Contango. (2) Represents percent of PDP oil production hedged in 2022E based on current management assumptions of the Company and Contango. (3) Represents projected PDP asset cash flow as a % of total asset cash flow. (4) Adj EBITDA margin represents hedged Adj. EBITDA divided by hedged + 9 revenue. (5) Reinvestment rate defined as capital expenditures as a percentage of corporate Adj. EBITDA. (6) Represents pro forma nominal hedge value of July 2021 hedges and beyond.Significant and Sustainable Free Cash Flow Generation Preliminary 2022E Estimates Low Decline Disciplined Diversified production Daily Production 108– 114 MBoe/d Capital Spend with 18% base Historical reinvestment 2022E Base Decline ~15% PDP decline forecast rates averaging ~45% (1) (2) for 2021E % Hedged ~75% of adjusted EBITDA Adj. EBITDA $750 - 800 MM (3) % PDP ~75% ~$145 MM of ~$95MM of (4) Adj. EBITDA Margin % ~55% PF Unhedged Free Cash (5) Free Cash Reinvestment Rate ~50% 1 Flow Flow Unlevered FCF $375 - 400 MM in Q1 2021 in Q1 2021 Target Dividend ~10% of EBITDA LT Target Leverage ~1.0x Active Risk Low-Risk Management Growth Disciplined, returns Protecting cash flow with focused reinvestment robust hedge program (~$1.8 Bn of notional value and accretive acquisitions (6) hedged) Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Represents projected pro forma PDP decline from February 2021 – February 2022 based on current management assumptions of the Company and Contango. (2) Represents percent of PDP oil production hedged in 2022E based on current management assumptions of the Company and Contango. (3) Represents projected PDP asset cash flow as a % of total asset cash flow. (4) Adj EBITDA margin represents hedged Adj. EBITDA divided by hedged + 9 revenue. (5) Reinvestment rate defined as capital expenditures as a percentage of corporate Adj. EBITDA. (6) Represents pro forma nominal hedge value of July 2021 hedges and beyond.

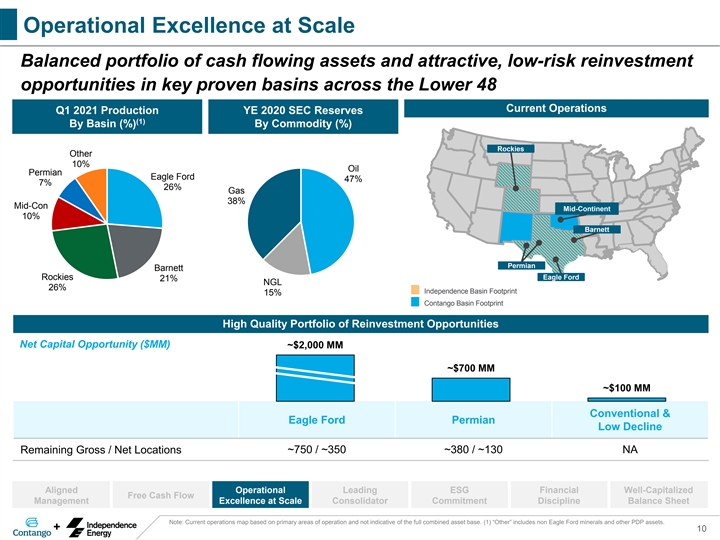

Operational Excellence at Scale Balanced portfolio of cash flowing assets and attractive, low-risk reinvestment opportunities in key proven basins across the Lower 48 Current Operations Q1 2021 Production YE 2020 SEC Reserves (1) By Basin (%) By Commodity (%) Rockies Other 10% Oil Permian Eagle Ford 47% 7% 26% Gas 38% Mid-Con Mid-Continent 10% Barnett Permian Barnett Rockies Eagle Ford 21% NGL 26% Independence Basin Footprint 15% Contango Basin Footprint High Quality Portfolio of Reinvestment Opportunities Net Capital Opportunity ($MM) ~$2,000 MM ~$700 MM ~$100 MM Conventional & Eagle Ford Permian Low Decline ~750 / ~350 ~380 / ~130 NA Remaining Gross / Net Locations Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet Note: Current operations map based on primary areas of operation and not indicative of the full combined asset base. (1) “Other” includes non Eagle Ford minerals and other PDP assets. + 10Operational Excellence at Scale Balanced portfolio of cash flowing assets and attractive, low-risk reinvestment opportunities in key proven basins across the Lower 48 Current Operations Q1 2021 Production YE 2020 SEC Reserves (1) By Basin (%) By Commodity (%) Rockies Other 10% Oil Permian Eagle Ford 47% 7% 26% Gas 38% Mid-Con Mid-Continent 10% Barnett Permian Barnett Rockies Eagle Ford 21% NGL 26% Independence Basin Footprint 15% Contango Basin Footprint High Quality Portfolio of Reinvestment Opportunities Net Capital Opportunity ($MM) ~$2,000 MM ~$700 MM ~$100 MM Conventional & Eagle Ford Permian Low Decline ~750 / ~350 ~380 / ~130 NA Remaining Gross / Net Locations Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet Note: Current operations map based on primary areas of operation and not indicative of the full combined asset base. (1) “Other” includes non Eagle Ford minerals and other PDP assets. + 10

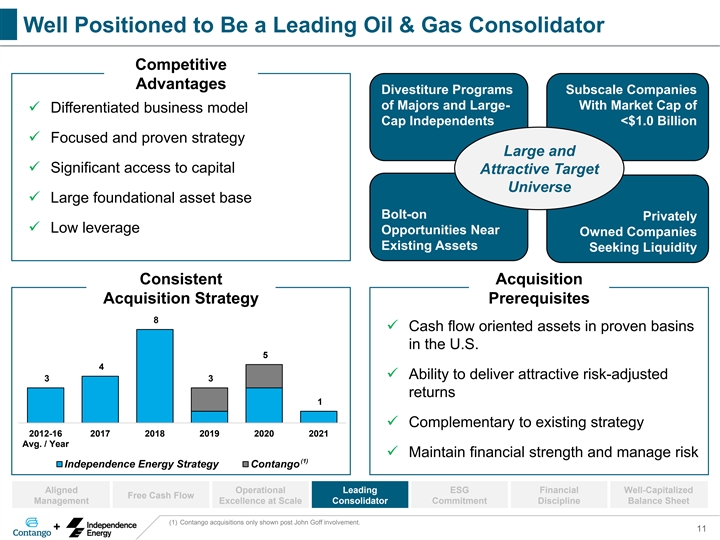

Well Positioned to Be a Leading Oil & Gas Consolidator Competitive Advantages Divestiture Programs Subscale Companies of Majors and Large- With Market Cap of ✓ Differentiated business model Cap Independents <$1.0 Billion ✓ Focused and proven strategy Large and ✓ Significant access to capital Attractive Target Universe ✓ Large foundational asset base Bolt-on Privately ✓ Low leverage Opportunities Near Owned Companies Existing Assets Seeking Liquidity Consistent Acquisition Acquisition Strategy Prerequisites 8 ✓ Cash flow oriented assets in proven basins in the U.S. 5 4 ✓ Ability to deliver attractive risk-adjusted 3 3 returns 1 ✓ Complementary to existing strategy 2012-16 2017 2018 2019 2020 2021 Avg. / Year ✓ Maintain financial strength and manage risk (1) Independence Energy Strategy Contango Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Contango acquisitions only shown post John Goff involvement. + 11Well Positioned to Be a Leading Oil & Gas Consolidator Competitive Advantages Divestiture Programs Subscale Companies of Majors and Large- With Market Cap of ✓ Differentiated business model Cap Independents <$1.0 Billion ✓ Focused and proven strategy Large and ✓ Significant access to capital Attractive Target Universe ✓ Large foundational asset base Bolt-on Privately ✓ Low leverage Opportunities Near Owned Companies Existing Assets Seeking Liquidity Consistent Acquisition Acquisition Strategy Prerequisites 8 ✓ Cash flow oriented assets in proven basins in the U.S. 5 4 ✓ Ability to deliver attractive risk-adjusted 3 3 returns 1 ✓ Complementary to existing strategy 2012-16 2017 2018 2019 2020 2021 Avg. / Year ✓ Maintain financial strength and manage risk (1) Independence Energy Strategy Contango Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Contango acquisitions only shown post John Goff involvement. + 11

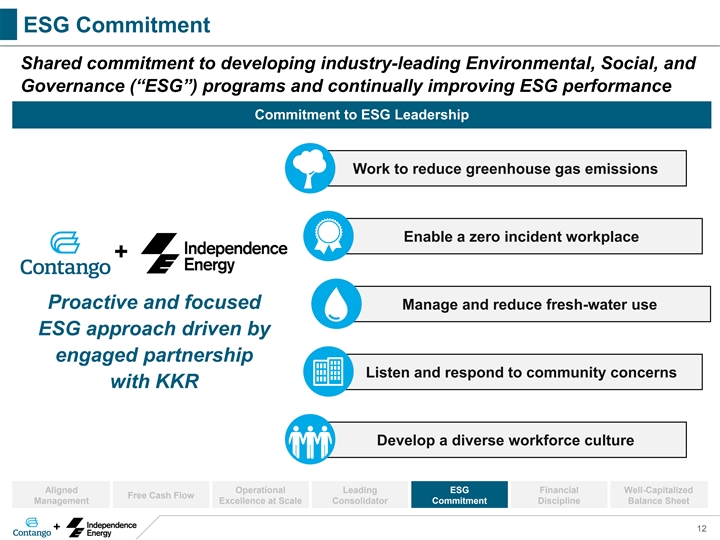

ESG Commitment Shared commitment to developing industry-leading Environmental, Social, and Governance (“ESG”) programs and continually improving ESG performance Commitment to ESG Leadership Work to reduce greenhouse gas emissions Enable a zero incident workplace + Proactive and focused Manage and reduce fresh-water use ESG approach driven by engaged partnership Listen and respond to community concerns with KKR Develop a diverse workforce culture Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet + 12ESG Commitment Shared commitment to developing industry-leading Environmental, Social, and Governance (“ESG”) programs and continually improving ESG performance Commitment to ESG Leadership Work to reduce greenhouse gas emissions Enable a zero incident workplace + Proactive and focused Manage and reduce fresh-water use ESG approach driven by engaged partnership Listen and respond to community concerns with KKR Develop a diverse workforce culture Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet + 12

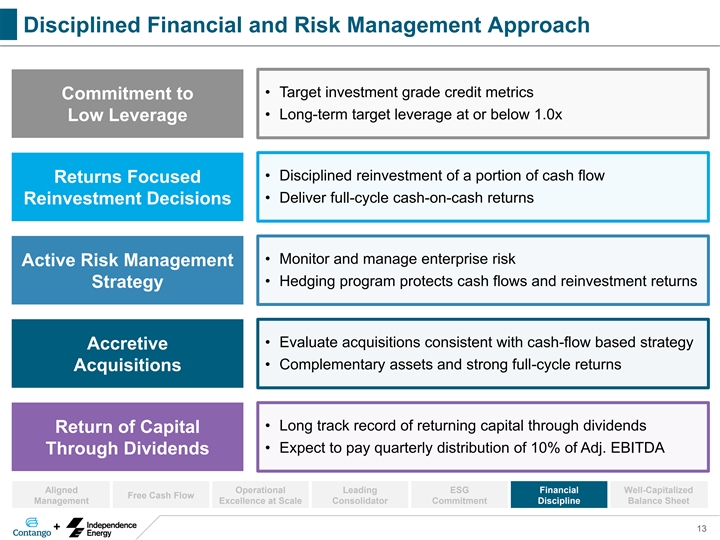

Disciplined Financial and Risk Management Approach • Target investment grade credit metrics Commitment to • Long-term target leverage at or below 1.0x Low Leverage • Disciplined reinvestment of a portion of cash flow Returns Focused • Deliver full-cycle cash-on-cash returns Reinvestment Decisions • Monitor and manage enterprise risk Active Risk Management • Hedging program protects cash flows and reinvestment returns Strategy • Evaluate acquisitions consistent with cash-flow based strategy Accretive • Complementary assets and strong full-cycle returns Acquisitions • Long track record of returning capital through dividends Return of Capital • Expect to pay quarterly distribution of 10% of Adj. EBITDA Through Dividends Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet + 13Disciplined Financial and Risk Management Approach • Target investment grade credit metrics Commitment to • Long-term target leverage at or below 1.0x Low Leverage • Disciplined reinvestment of a portion of cash flow Returns Focused • Deliver full-cycle cash-on-cash returns Reinvestment Decisions • Monitor and manage enterprise risk Active Risk Management • Hedging program protects cash flows and reinvestment returns Strategy • Evaluate acquisitions consistent with cash-flow based strategy Accretive • Complementary assets and strong full-cycle returns Acquisitions • Long track record of returning capital through dividends Return of Capital • Expect to pay quarterly distribution of 10% of Adj. EBITDA Through Dividends Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet + 13

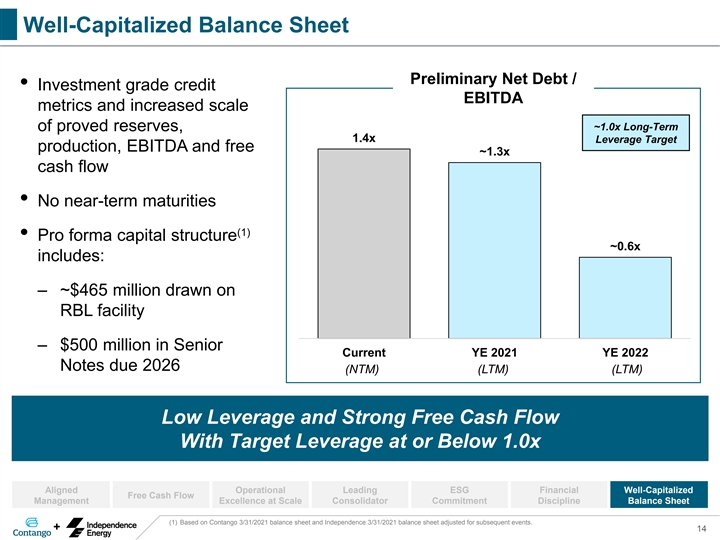

Well-Capitalized Balance Sheet Preliminary Net Debt / • Investment grade credit EBITDA metrics and increased scale ~1.0x Long-Term of proved reserves, 1.4x Leverage Target production, EBITDA and free ~1.3x cash flow • No near-term maturities (1) • Pro forma capital structure ~0.6x includes: – ~$465 million drawn on RBL facility – $500 million in Senior Current YE 2021 YE 2022 Notes due 2026 (NTM) (LTM) (LTM) Low Leverage and Strong Free Cash Flow With Target Leverage at or Below 1.0x Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Based on Contango 3/31/2021 balance sheet and Independence 3/31/2021 balance sheet adjusted for subsequent events. + 14Well-Capitalized Balance Sheet Preliminary Net Debt / • Investment grade credit EBITDA metrics and increased scale ~1.0x Long-Term of proved reserves, 1.4x Leverage Target production, EBITDA and free ~1.3x cash flow • No near-term maturities (1) • Pro forma capital structure ~0.6x includes: – ~$465 million drawn on RBL facility – $500 million in Senior Current YE 2021 YE 2022 Notes due 2026 (NTM) (LTM) (LTM) Low Leverage and Strong Free Cash Flow With Target Leverage at or Below 1.0x Aligned Operational Leading ESG Financial Well-Capitalized Free Cash Flow Management Excellence at Scale Consolidator Commitment Discipline Balance Sheet (1) Based on Contango 3/31/2021 balance sheet and Independence 3/31/2021 balance sheet adjusted for subsequent events. + 14

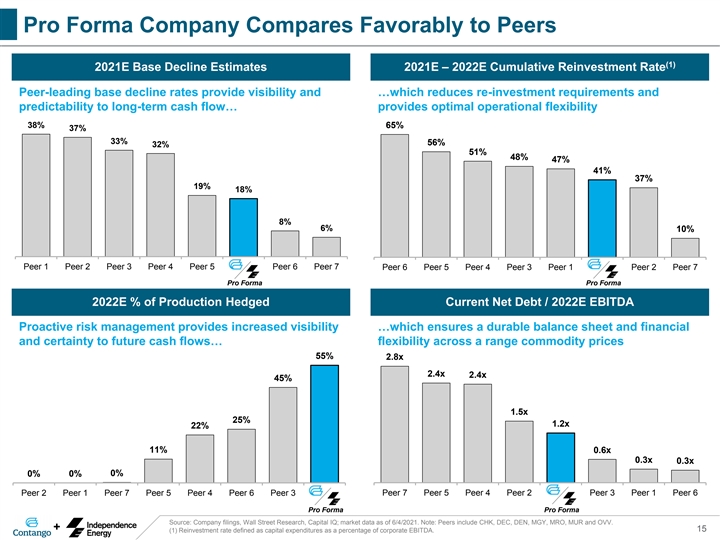

Pro Forma Company Compares Favorably to Peers (1) 2021E Base Decline Estimates 2021E – 2022E Cumulative Reinvestment Rate Peer-leading base decline rates provide visibility and …which reduces re-investment requirements and predictability to long-term cash flow… provides optimal operational flexibility 38% 65% 37% 33% 56% 32% 51% 48% 47% 41% 37% 19% 18% 8% 6% 10% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Pro Forma Peer 6 Peer 7 Peer 6 Peer 5 Peer 4 Peer 3 Peer 1 Pro Forma Peer 2 Peer 7 Pro Forma Pro Forma 2022E % of Production Hedged Current Net Debt / 2022E EBITDA Proactive risk management provides increased visibility …which ensures a durable balance sheet and financial and certainty to future cash flows… flexibility across a range commodity prices 55% 2.8x 2.4x 2.4x 45% 1.5x 25% 1.2x 22% 11% 0.6x 0.3x 0.3x 0% 0% 0% Peer 2 Peer 1 Peer 7 Peer 5 Peer 4 Peer 6 Peer 3 Pro Forma Peer 7 Peer 5 Peer 4 Peer 2 Pro Forma Peer 3 Peer 1 Peer 6 Pro Forma Pro Forma Source: Company filings, Wall Street Research, Capital IQ; market data as of 6/4/2021. Note: Peers include CHK, DEC, DEN, MGY, MRO, MUR and OVV. + 15 (1) Reinvestment rate defined as capital expenditures as a percentage of corporate EBITDA.Pro Forma Company Compares Favorably to Peers (1) 2021E Base Decline Estimates 2021E – 2022E Cumulative Reinvestment Rate Peer-leading base decline rates provide visibility and …which reduces re-investment requirements and predictability to long-term cash flow… provides optimal operational flexibility 38% 65% 37% 33% 56% 32% 51% 48% 47% 41% 37% 19% 18% 8% 6% 10% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Pro Forma Peer 6 Peer 7 Peer 6 Peer 5 Peer 4 Peer 3 Peer 1 Pro Forma Peer 2 Peer 7 Pro Forma Pro Forma 2022E % of Production Hedged Current Net Debt / 2022E EBITDA Proactive risk management provides increased visibility …which ensures a durable balance sheet and financial and certainty to future cash flows… flexibility across a range commodity prices 55% 2.8x 2.4x 2.4x 45% 1.5x 25% 1.2x 22% 11% 0.6x 0.3x 0.3x 0% 0% 0% Peer 2 Peer 1 Peer 7 Peer 5 Peer 4 Peer 6 Peer 3 Pro Forma Peer 7 Peer 5 Peer 4 Peer 2 Pro Forma Peer 3 Peer 1 Peer 6 Pro Forma Pro Forma Source: Company filings, Wall Street Research, Capital IQ; market data as of 6/4/2021. Note: Peers include CHK, DEC, DEN, MGY, MRO, MUR and OVV. + 15 (1) Reinvestment rate defined as capital expenditures as a percentage of corporate EBITDA.

Why Own the Combined Company? + Aligned Management with Investor Mindset Sustainable Free Cash Flow Significant Scale Across Proven Basins Well Positioned to be a Leading Oil & Gas Consolidator Commitment to ESG Excellence Disciplined Financial and Risk Management Approach Well-Capitalized Balance Sheet + 16Why Own the Combined Company? + Aligned Management with Investor Mindset Sustainable Free Cash Flow Significant Scale Across Proven Basins Well Positioned to be a Leading Oil & Gas Consolidator Commitment to ESG Excellence Disciplined Financial and Risk Management Approach Well-Capitalized Balance Sheet + 16

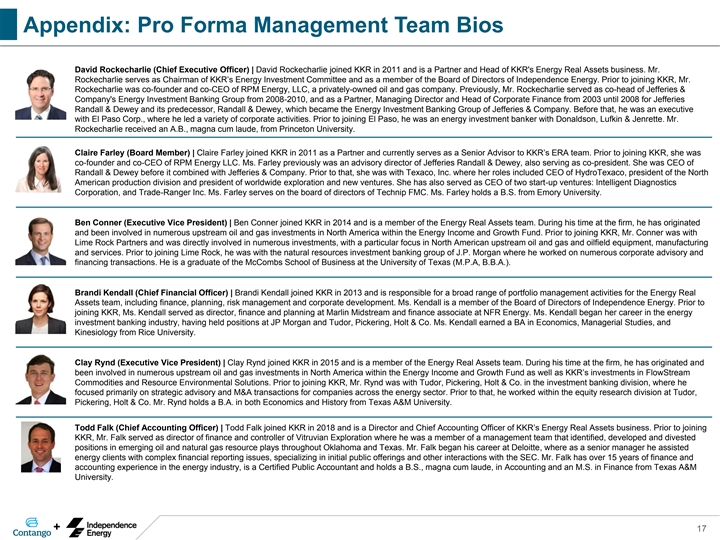

Appendix: Pro Forma Management Team Bios David Rockecharlie (Chief Executive Officer) | David Rockecharlie joined KKR in 2011 and is a Partner and Head of KKR's Energy Real Assets business. Mr. Rockecharlie serves as Chairman of KKR’s Energy Investment Committee and as a member of the Board of Directors of Independence Energy. Prior to joining KKR, Mr. Rockecharlie was co-founder and co-CEO of RPM Energy, LLC, a privately-owned oil and gas company. Previously, Mr. Rockecharlie served as co-head of Jefferies & Company's Energy Investment Banking Group from 2008-2010, and as a Partner, Managing Director and Head of Corporate Finance from 2003 until 2008 for Jefferies Randall & Dewey and its predecessor, Randall & Dewey, which became the Energy Investment Banking Group of Jefferies & Company. Before that, he was an executive with El Paso Corp., where he led a variety of corporate activities. Prior to joining El Paso, he was an energy investment banker with Donaldson, Lufkin & Jenrette. Mr. Rockecharlie received an A.B., magna cum laude, from Princeton University. Claire Farley (Board Member) | Claire Farley joined KKR in 2011 as a Partner and currently serves as a Senior Advisor to KKR’s ERA team. Prior to joining KKR, she was co-founder and co-CEO of RPM Energy LLC. Ms. Farley previously was an advisory director of Jefferies Randall & Dewey, also serving as co-president. She was CEO of Randall & Dewey before it combined with Jefferies & Company. Prior to that, she was with Texaco, Inc. where her roles included CEO of HydroTexaco, president of the North American production division and president of worldwide exploration and new ventures. She has also served as CEO of two start-up ventures: Intelligent Diagnostics Corporation, and Trade-Ranger Inc. Ms. Farley serves on the board of directors of Technip FMC. Ms. Farley holds a B.S. from Emory University. Ben Conner (Executive Vice President) | Ben Conner joined KKR in 2014 and is a member of the Energy Real Assets team. During his time at the firm, he has originated and been involved in numerous upstream oil and gas investments in North America within the Energy Income and Growth Fund. Prior to joining KKR, Mr. Conner was with Lime Rock Partners and was directly involved in numerous investments, with a particular focus in North American upstream oil and gas and oilfield equipment, manufacturing and services. Prior to joining Lime Rock, he was with the natural resources investment banking group of J.P. Morgan where he worked on numerous corporate advisory and financing transactions. He is a graduate of the McCombs School of Business at the University of Texas (M.P.A, B.B.A.). Brandi Kendall (Chief Financial Officer) | Brandi Kendall joined KKR in 2013 and is responsible for a broad range of portfolio management activities for the Energy Real Assets team, including finance, planning, risk management and corporate development. Ms. Kendall is a member of the Board of Directors of Independence Energy. Prior to joining KKR, Ms. Kendall served as director, finance and planning at Marlin Midstream and finance associate at NFR Energy. Ms. Kendall began her career in the energy investment banking industry, having held positions at JP Morgan and Tudor, Pickering, Holt & Co. Ms. Kendall earned a BA in Economics, Managerial Studies, and Kinesiology from Rice University. Clay Rynd (Executive Vice President) | Clay Rynd joined KKR in 2015 and is a member of the Energy Real Assets team. During his time at the firm, he has originated and been involved in numerous upstream oil and gas investments in North America within the Energy Income and Growth Fund as well as KKR’s investments in FlowStream Commodities and Resource Environmental Solutions. Prior to joining KKR, Mr. Rynd was with Tudor, Pickering, Holt & Co. in the investment banking division, where he focused primarily on strategic advisory and M&A transactions for companies across the energy sector. Prior to that, he worked within the equity research division at Tudor, Pickering, Holt & Co. Mr. Rynd holds a B.A. in both Economics and History from Texas A&M University. Todd Falk (Chief Accounting Officer) | Todd Falk joined KKR in 2018 and is a Director and Chief Accounting Officer of KKR’s Energy Real Assets business. Prior to joining KKR, Mr. Falk served as director of finance and controller of Vitruvian Exploration where he was a member of a management team that identified, developed and divested positions in emerging oil and natural gas resource plays throughout Oklahoma and Texas. Mr. Falk began his career at Deloitte, where as a senior manager he assisted energy clients with complex financial reporting issues, specializing in initial public offerings and other interactions with the SEC. Mr. Falk has over 15 years of finance and accounting experience in the energy industry, is a Certified Public Accountant and holds a B.S., magna cum laude, in Accounting and an M.S. in Finance from Texas A&M University. + 17Appendix: Pro Forma Management Team Bios David Rockecharlie (Chief Executive Officer) | David Rockecharlie joined KKR in 2011 and is a Partner and Head of KKR's Energy Real Assets business. Mr. Rockecharlie serves as Chairman of KKR’s Energy Investment Committee and as a member of the Board of Directors of Independence Energy. Prior to joining KKR, Mr. Rockecharlie was co-founder and co-CEO of RPM Energy, LLC, a privately-owned oil and gas company. Previously, Mr. Rockecharlie served as co-head of Jefferies & Company's Energy Investment Banking Group from 2008-2010, and as a Partner, Managing Director and Head of Corporate Finance from 2003 until 2008 for Jefferies Randall & Dewey and its predecessor, Randall & Dewey, which became the Energy Investment Banking Group of Jefferies & Company. Before that, he was an executive with El Paso Corp., where he led a variety of corporate activities. Prior to joining El Paso, he was an energy investment banker with Donaldson, Lufkin & Jenrette. Mr. Rockecharlie received an A.B., magna cum laude, from Princeton University. Claire Farley (Board Member) | Claire Farley joined KKR in 2011 as a Partner and currently serves as a Senior Advisor to KKR’s ERA team. Prior to joining KKR, she was co-founder and co-CEO of RPM Energy LLC. Ms. Farley previously was an advisory director of Jefferies Randall & Dewey, also serving as co-president. She was CEO of Randall & Dewey before it combined with Jefferies & Company. Prior to that, she was with Texaco, Inc. where her roles included CEO of HydroTexaco, president of the North American production division and president of worldwide exploration and new ventures. She has also served as CEO of two start-up ventures: Intelligent Diagnostics Corporation, and Trade-Ranger Inc. Ms. Farley serves on the board of directors of Technip FMC. Ms. Farley holds a B.S. from Emory University. Ben Conner (Executive Vice President) | Ben Conner joined KKR in 2014 and is a member of the Energy Real Assets team. During his time at the firm, he has originated and been involved in numerous upstream oil and gas investments in North America within the Energy Income and Growth Fund. Prior to joining KKR, Mr. Conner was with Lime Rock Partners and was directly involved in numerous investments, with a particular focus in North American upstream oil and gas and oilfield equipment, manufacturing and services. Prior to joining Lime Rock, he was with the natural resources investment banking group of J.P. Morgan where he worked on numerous corporate advisory and financing transactions. He is a graduate of the McCombs School of Business at the University of Texas (M.P.A, B.B.A.). Brandi Kendall (Chief Financial Officer) | Brandi Kendall joined KKR in 2013 and is responsible for a broad range of portfolio management activities for the Energy Real Assets team, including finance, planning, risk management and corporate development. Ms. Kendall is a member of the Board of Directors of Independence Energy. Prior to joining KKR, Ms. Kendall served as director, finance and planning at Marlin Midstream and finance associate at NFR Energy. Ms. Kendall began her career in the energy investment banking industry, having held positions at JP Morgan and Tudor, Pickering, Holt & Co. Ms. Kendall earned a BA in Economics, Managerial Studies, and Kinesiology from Rice University. Clay Rynd (Executive Vice President) | Clay Rynd joined KKR in 2015 and is a member of the Energy Real Assets team. During his time at the firm, he has originated and been involved in numerous upstream oil and gas investments in North America within the Energy Income and Growth Fund as well as KKR’s investments in FlowStream Commodities and Resource Environmental Solutions. Prior to joining KKR, Mr. Rynd was with Tudor, Pickering, Holt & Co. in the investment banking division, where he focused primarily on strategic advisory and M&A transactions for companies across the energy sector. Prior to that, he worked within the equity research division at Tudor, Pickering, Holt & Co. Mr. Rynd holds a B.A. in both Economics and History from Texas A&M University. Todd Falk (Chief Accounting Officer) | Todd Falk joined KKR in 2018 and is a Director and Chief Accounting Officer of KKR’s Energy Real Assets business. Prior to joining KKR, Mr. Falk served as director of finance and controller of Vitruvian Exploration where he was a member of a management team that identified, developed and divested positions in emerging oil and natural gas resource plays throughout Oklahoma and Texas. Mr. Falk began his career at Deloitte, where as a senior manager he assisted energy clients with complex financial reporting issues, specializing in initial public offerings and other interactions with the SEC. Mr. Falk has over 15 years of finance and accounting experience in the energy industry, is a Certified Public Accountant and holds a B.S., magna cum laude, in Accounting and an M.S. in Finance from Texas A&M University. + 17