Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Korth Direct Mortgage Inc. | ex32_2.htm |

| EX-32.1 - EXHIBIT 32.1 - Korth Direct Mortgage Inc. | ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - Korth Direct Mortgage Inc. | ex31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - Korth Direct Mortgage Inc. | ex31_1.htm |

| EX-23.1 - EXHIBIT 23.1 - Korth Direct Mortgage Inc. | ex23_1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020.

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission File Number: 000-1695962

| KORTH DIRECT MORTGAGE INC. |

| (Exact name of registrant as specified in its charter) |

| Florida | 27-0644172 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

135 San Lorenzo Avenue, Suite 600, Coral Gables, FL 33146 |

| (Address of principal executive offices) |

|

|

| (305) 668-8485 |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o |

| Non-accelerated filer | o | Smaller Reporting company | þ |

| Emerging growth company | þ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.o

| 1 |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ¨ No þ

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ¨ No þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

There is no market for the common equity of Korth Direct Mortgage Inc. As of December 31, 2020, there were 5,000,000 common shares of KDM outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

No documents are incorporated in this Form 10-K by reference.

| 2 |

KORTH DIRECT MORTGAGE, Inc.

| 3 |

FORWARD-LOOKING STATEMENTS

Some of the information contained in this Report constitutes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements may include current expectations of future events based on certain assumptions and statements that do not directly relate to any historical or current fact. When used in this Annual Report, in future filings by the Company with the Securities and Exchange Commission, in the Company’s press releases or other public or shareholder communications, on the Company’s website, or in oral statements made with the approval of an authorized executive officer, the words or phrases “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimate,” “project,” “plans,” “believes,” or similar expressions are intended to identify forward-looking statements. The Company’s forward-looking statements are based on management’s current expectation and assumption regarding the Company’s business and performance, the economy, and other future conditions and forecasts of future events, circumstances and results. As with any projection statement or forecast, forward-looking statements are inherently susceptible to uncertainty and changes in circumstances. The Company’s actual results may vary materially from those expressed or implied in its forward-looking statements. Important factors that could cause the Company’s actual results to differ materially from those in its forward-looking statements include, among other things, our inability to predict the extent to which the COVID-19 pandemic and related impacts may adversely impact our business operations, financial performance, results of operations, financial position, and the achievement of our strategic objectives; the status of borrowers; the ability of borrowers to repay CM Loans, as defined below; the plans of borrowers; expected rates of return and interest rates; mortgage default rates; property values; the commercial real estate market; the attractiveness of our CM Loans and Notes; our financial performance; the availability of a secondary market for our Notes; our ability to retain and hire competent employees and appropriately staff our operation; government regulation; regional and national economic conditions, substantial changes in levels of market interest rates; and competitive and regulatory factors.

The Company does not undertake and specifically disclaims any obligation to update any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements.

PART I

Throughout this Report we use the terms “KDM,” “we,” “Company,” and “us” to refer to Korth Direct Mortgage Inc.

Our principal executive offices are located at 135 San Lorenzo Avenue Suite 600, Coral Gables, Florida 33146, and our telephone number is (305) 668-8485. Our website address is korthdirect.com.

Korth Direct Mortgage Inc., began its formal operations in October of 2016 when we engaged our Chief Lending Officer. KDM is a licensed Mortgage Lender Servicer with the State of Florida. Our NMLS License Number is 1579547. KDM converted from a Florida limited liability company to a Florida corporation effective June 6, 2019. On July 31, 2020 KDM’s ownership was reorganized, and its former sole shareholder, J. W. Korth & Company Limited Partnership (“J. W. Korth”), a FINRA and SEC registered broker-dealer founded in 1982, is now a wholly owned subsidiary of the Company.

Overview

KDM originates and funds CM Loans, as herein defined, to borrowers The CM Loans are held by KDM as lender. KDM also services its CM Loans, though it may use a sub-servicer for some loans. KDM funds its CM Loans directly in the capital markets through issuance of Mortgage Secured Notes (“MSNs” or “Notes”). The MSNs are special obligations of KDM, payable to the extent that the underlying mortgage is paid by the borrower. MSNs are secured by KDM’s interest in the underlying Corresponding Mortgage Loan (“CM Loan”). CM Loans are secured obligations of the borrowers, which are generally a single-purpose entity formed or existing that owns the underlying property that is financed.

Our loan origination team is comprised of employees and a network of brokers that have joined the KDM Broker Network to submit loans to us via our website and email. We have created software that integrates with our customer relationship management (“CRM”) software to optimize our digital marketing campaigns and streamline our origination program. We also engage in traditional email, internet, trade show, and telephone marketing as well as leveraging our broker network to source new deals.

We have positioned ourselves in the lending market as a source for commercial real estate loans of higher quality borrowers, and borrowers that may not qualify or may not want to go through the process for bank loans, but whose loans have strong property and mortgage-related metrics. We fill the gap between traditional lenders and hard money lenders, which we call Middle-Money.. Property metrics depend on the type of CM Loan being offered and are described below.

| 4 |

KDM is currently focused on the market for loans secured by mortgages on commercial-tenanted properties, including multi-family housing, offices, industrial, and warehouses, but may fund other types of commercial real estate.

KDM funds its loans by securitizing them in the capital markets as MSNs. J. W. Korth & Company acts as underwriter of the Notes and distributes them to institutional investors. The cash from the closing of each MSN issuances is used to complete the funding of the CM Loan or CM Loans underlying each MSN.

The KDM Process

When KDM identifies a property proposed for financing, it is screened by KDM’s origination underwriting team. If the proposed financing passes underwriting, KDM creates a summary sheet and an estimated KDM Rating which it sends to the underwriter to gauge an indication of interest. When the underwriter believes it has sufficient interest to move forward, it will notify KDM and KDM will complete the loan underwriting and prepare the loan for closing and funding. The underwriter or initial purchaser will execute orders and funds will transfer on the settlement date to one of KDM’s segregated accounts. KDM will then fund the CM Loan and issue the MSNs.

KDM receives monthly interest and principal payments from CM Loan borrowers. KDM collects its service fee from the interest portion of the payment and then disburses the remaining interest and principal via wire transfer to DTC for credit to investors’ accounts at their respective DTC member or those brokerage firms corresponding with DTC members.

We make CM Loans to borrowers throughout the United States. As of the date of this Report, we were not dependent on any single party for a material amount of our revenue.

Borrowers who use us must identify their intended use of CM Loan proceeds in their initial CM Loan request. We do not verify or monitor a borrower’s actual use of funds following the funding of a CM Loan unless otherwise specified in the offering memorandum for the MSN.

The KDM Ratings System

In order to assist us with pricing and underwriting CM Loans, KDM has created an internal CM Loan ratings system.

The scoring matrix consists of seven factors, each weighted according to its relative importance in how we view the loans we choose to make. The seven factors are: loan to value, debt service coverage ratio, property type, property/improvement age, property demand/metropolitan statistical area, building condition, and sponsor experience.

We grade each CM Loan on these factors when it is presented to us, which results in a numerical figure that we then translate to a traditional AAA-BBB scale with + and – gradation. We publish our KDM Rating along with each note term sheet and offering memorandum and update it annually in our annual reviews in the quarterly or annual report that corresponds with the anniversary of the CM Loan issuance.

The KDM Loan Committee meets annually to review the KDM Ratings System. We review the performance, the factors, and how well those factors are weighted. The KDM Loan Rating Committee met on February 9, 2021 to review the KDM Rating Methodology. The methodology considers seven key criteria and is then subject to adjustment on a deal-by-deal basis. The seven criteria are: LTV, DSCR, Property Type, Property Age, MSA Population Growth, Building Condition and Sponsor Experience. After our discussions, we decided to a) double the importance of LTV, b) add more property types. c) replace Property Age with Lease Quality, d) replace MSA Population Growth with Location (Primary, Secondary, Tertiary) and e) slightly adjusted Sponsor Experience points.

KDM UNDERWRITING PROCESS

Step One: Identify Loan Parameters

Through market research, KDM identifies CM Loan parameters and related investor parameters that it expects will be of value to both borrowers and investors. It then uses its network of mortgage brokers, real estate agents, and lending platforms to identify properties that potentially meet these parameters. The parameters identified will include the loan type, expected interest rate, maturity, pre-payment terms, loan-to-value, minimum debt service coverage ratio, and basic loan structure.

Step Two: Identify and Screen Property

The KDM origination team works to bring in leads on new properties on which KDM can potentially lend. The team has a network of mortgage brokers, real estate agents, lending platforms, as well as lead generation databases that it uses on a daily basis to identify potential loans. Once the team finds a potential property it creates a deal scorecard that identifies critical preliminary underwriting information, including potential loan value-to-cost ratio, debt service coverage of the proposed loan, real estate comparison prices, last appraised value, and estimated current value, along with information about the property and location, including city, neighborhood, number of units, rent roll, vacancy rate, and use of proceeds.

| 5 |

Step Three: Create a Summary Sheet

KDM creates a deal summary sheet for our underwriter or initial purchaser, J. W. Korth & Company (the “Underwriter”), to use to gauge interest from selling group members. The Underwriter uses its network of selling group members to assess whether there is adequate investor appetite for the terms of a proposed note, which will be issued pursuant to an offering memorandum. The notes to be offered and sold pursuant to an offering memorandum are referred to herein as the “MSN” or the “Note(s).” If there appears to be sufficient interest, then the Underwriter will communicate that to KDM.

Step Four: Complete Underwriting and Due Diligence

Once KDM believes that the CM loan can be funded by the proceeds of a note, it executes a commitment letter with a borrower (subject to funding). When the borrower executes the commitment letter, it pays KDM a processing fee, and KDM then orders an appraisal and a subsequent appraisal review. Simultaneously, we complete the underwriting and due diligence on the property and create the offering summary and offering memorandum for the MSN.

Step Five: Underwriter and Sales Process

The Underwriter takes “when, as and if issued” orders for a series of our Notes. Once the MSN offering is fully subscribed, the Underwriter distributes the final offering memorandum and confirms final orders with other dealers and clients. The Underwriter then execute orders according to a mutually agreed upon trade date with KDM.

Step Six: Funding the Note, Closing the CM Loan

KDM will schedule closing for the CM Loan on or before the trade date of the Notes. The CM Loan is closed awaiting final funding. Documents and title are reviewed by both KDM and its attorneys. Upon approval of closing documents, and within one business day of the settlement date, funds, net of selling concession, are wired by the Underwriter to KDM’s segregated account for loan funding. KDM wires funds for the CM Loan closing as soon as practicable after receipt.

Once funds are collected, the CM Loan is closed and documents are filed in the proper jurisdiction showing KDM as mortgagee. Concurrently, KDM creates and executes a physical note for issuance to Cede & Company, or its nominee, and delivery to Depository Trust Company (“DTC”), or its agent. DTC credits each participating dealer with the appropriate face amount of the Note for further credit to each of its participating client accounts. Also, as soon as possible, but in no case more than five business days, documents will be filed with the Trustee.

How KDM operates if KDM Acquires Existing CM Loans and Issues Corresponding Notes

When KDM acquires an existing CM Loan or group of loans and issues corresponding Notes, the Notes sale and CM Loan closing process is the same as for loans that we originate, except that KDM will purchase the CM Loan from a third party. Information about the borrower of an existing loan may be more limited and appraisals may be less current than for a loan originated by KDM. In such instances, an estimate of value from a local expert may be required to supplement an existing appraisal. A history of CM Loan payments will be included in the offering memorandum for the notes to be issued to purchase an existing CM Loan.

CM Loans may also be acquired by purchasing a participation in CM Loans from another lending institution. In these cases, the pricing of the participation and the net mark-up or down of the CM Loan in the form of the corresponding Note will be fully described to investors as well as a detailed description of the financial institution selling the participation interest(s).

How KDM Prices CM Loans and Corresponding Notes

Note maturities and yields to investors must be competitive with other options they have for secured investments. Notes are not guaranteed by any federal agency, so they must be competitively priced when compared with other types of lower-risk debt, such as lower investment grade corporate bonds or other mortgage loans. Borrowers may have other options for acquiring new mortgage funding. KDM must be competitive with these options in order to acquire new CM Loans. The dynamic between these two marketplaces is a principal factor in the determination of the terms of KDM Notes.

| 6 |

How our Servicing Fee Applies

KDM services the underlying CM Loans and manages the distribution and payment of interest and principal on the corresponding Notes. For these services it charges an annual servicing fee (“Servicing Fee”) targeted at 1.00%. The Servicing Fee could be lower or higher for a given CM Loan based on that CM Loan and the corresponding Note’s terms, as disclosed in the offering material for each Note. The Servicing Fee accrues to KDM and is paid by the borrower from the borrower’s CM Loan interest payments. The Servicing Fee is the difference between the rate paid by the borrower and the rate paid to investors on the MSN. However, the Servicing Fee may sometimes be shared with other parties, and not accrue directly to KDM. The Servicing Fee is applied to every interest payment received on the underlying CM Loan. Therefore, if we receive 7.00% interest annually from the underlying CM Loan and the Servicing Fee is 1%, the Note payments will be 6.00% annually, barring any other expenses. For 2020, the average Servicing Fee collected was 1.01%,

CM Loan Servicing

KDM is responsible for servicing all the loans it makes to mortgage borrowers and collecting payments from those borrowers and delivering payments to investors on its Notes. KDM also manages the tax and insurance escrow accounts of the borrowers and their annual tax and insurance payments. KDM has staff with extensive back office and accounting experience and uses loan servicing software to assist with the accounting and operations of the servicing process. Currently, KDM services 100% of its loans itself; we may engage a third-party servicer in the future.

KDM makes advances of funds from time-to-time as it believes necessary. KDM may advance payments to Noteholders if it believes a borrower will return to current status promptly. KDM also may advance payments to local tax authorities and insurance carriers as it believes necessary.

KDM has custodial responsibility for the CM Loans and pursuant to the Trust Indenture for the Notes. There are no limitations in KDM’s liability as servicer of its loans.

KDM retains a Servicing Fee for each CM Loan. See “How our Servicing Fee Applies,” above. Currently there are no specific arrangements for a back-up servicer. If KDM chooses a back-up servicer for any CM Loan or series of Notes, it will be identified in the offering documents for the Notes.

CM Loan payments are deposited or transmitted via ACH to the KDM In Trust For 2 Segregated Account. This segregated account collects payments from all CM Loans, and is segregated from the KDM operating funds. This account is managed as an omnibus account and funds received are disbursed for their respective payment on the Notes to DTC for credit to each participating broker dealer’s account. Broker-dealer participants then make further credit to customer accounts of Noteholders. We also debit this account for our Servicing Fee as described above.

CM Loans may also have retention of an impound or escrow amount for taxes and insurance and a replacement reserve for roof repairs, tenant improvements, leasing commissions, debt service, or other items necessary to the proper functioning of the property. Such escrowed funds are currently in the KDM In Trust For 1 Segregated account.

In the event it becomes necessary to expend funds for the collection or protection of a CM Loan, or for the preservation or protection of a CM Loan property, including the institution of foreclosure proceedings, such expenses will initially be covered by KDM and recouped at disposition of the property. Ultimately, all costs and expenses will be funded (or reimbursed to us) from the proceeds of any foreclosure or settlement, including reimbursement to us of any expenses we have disbursed toward collection of a CM Loan. These expenses may reduce interest or principal payments on a Note. See “Risk Factors.”

On our website www.korthdirect.com, we disclose borrowers’ payment performance on our CM Loans at least annually. We have made arrangements for collection procedures in the event of borrower default. When a CM Loan is past due and payment has not been received, we contact the borrower to request payment. After a 10-day grace period, we may, in our discretion, assess a late payment fee. This fee may be charged only once per late payment. Amounts equal to any late payment fees we receive are paid to holders of the Notes if and only if a payment on the Notes is also late. We may waive a late payment fee when a borrower promises to return a delinquent CM Loan to current status and fulfills that promise. Each time a payment request is denied due to insufficient funds in the borrower’s account or for any other reason, we may assess an unsuccessful payment fee to the borrower in an amount of $35.00 per unsuccessful payment, or such lesser amount as may be provided by applicable law. We retain 100% of this unsuccessful payment fee to cover our costs incurred due to the denial of the payment.

| 7 |

If the CM Loan becomes 31 days overdue (see “Certain Definitions,” below), we will identify the CM Loan as “Late (31-120),” and we may refer the CM Loan to a real estate attorney for foreclosure proceedings. However, we may pursue other remedies to bring the loan back to performance before foreclosure. In these cases, the interest rate on the CM Loan is increased to the highest legal rate in the state in which the property is located. The costs from a foreclosure and resale of a defaulted CM Loan and mortgaged property are applied against the proceeds payable to Noteholders. If funds remain after a property is resold and all expenses are paid, they would be distributed to Noteholders on a pro-rata basis.

Certain Definitions

We define delinquent accounts as accounts that are more than 31 days overdue with no immediate plan to repair the delinquency. Charge offs are defined as the unpaid principal balance of a specific CM Loan minus the expected recovery based on current market conditions for the foreclosed property. Uncollectable accounts are defined as those CM Loans where no recovery is expected to be made. These definitions are regardless of any grace period, re-aging, restructure, or partial payments received. A CM Loan that is categorized as a delinquent account could be re-categorized as current if the borrower brought all payments up to date. Charge-offs would be adjusted for properties in foreclosure based on an annual review of the current market conditions for the geography of the property. Uncollectible accounts will be reviewed quarterly and could be reclassified as collectible if market conditions change for the property subject to the mortgage and foreclosure. As of the date of this Report on Form 10-K, we have no delinquent CM Loans.

Summary of How KDM Fees Affect Return Sales, Marketing and Customer Service

Our marketing efforts are designed to attract borrowers to contact us and to enroll them as clients, and to close transactions with them. Our origination team primarily does this through the substantial network of commercial mortgage brokers we have assembled. We employ primarily email correspondence to mortgage brokers, banks, real estate agents, and commercial property owners to encourage them to present CM Loans to us for possible funding through the issuance of corresponding Notes. We attend trade shows, subscribe to lead generation databases, and loan and property platforms to find loans. We contact other financial institutions, directly and through brokers, that may own commercial mortgages, and may attempt to purchase mortgages for KDM.

Fraud detection

We consider fraud detection to be of utmost importance to the successful operation of our business. We employ a combination of proprietary technologies and commercially available licensed technologies and solutions to prevent and detect fraud. We use services from third-party vendors for user identification and OFAC compliance.

Notwithstanding KDM’s due diligence examination of the information provided to KDM by a borrower, there can be no assurance that the information provided to us, and on which we rely, is true and accurate.

Competition

The market for mortgage lending is competitive and rapidly evolving. We believe the following are the principal competitive factors in the lending market:

| · | pricing and fees; |

| · | experience, including borrower full funding rates and investor returns; |

| · | branding; and |

| · | ease of use. |

We face competition from major banking institutions, credit unions, and other consumer finance companies as well as smaller private lenders.

We may also face future competition from new companies entering our market. These companies may have significantly greater financial, technical, marketing and other resources than we do and may be able to devote greater resources to the development, promotion, sale and support of their consumer lending programs. These potential competitors may be in a stronger position to respond quickly to new technologies and may be able to undertake more extensive marketing campaigns. These potential competitors may have more extensive potential borrower bases than we do. In addition, these potential competitors may have longer operating histories and greater name recognition than we do. Moreover, if one or more of our competitors were to merge or partner with another of our competitors or a new market entrant, the change in competitive landscape could adversely affect our ability to compete effectively.

Our success depends on further developing our network of transaction referral sources and working with an underwriter to build a ready market for our Notes to finance our lending. We believe both the mortgage broker network and the distribution network for Notes is accessible through email and direct contacts and advertising in key spots. We have ascertained that there is a large niche for the types of Notes that KDM is issuing.

| 8 |

It is highly likely that another brokerage firm or mortgage company may use our program as a model and attempt to execute it in a similar fashion. The market for commercial loans like our CM Loans is more than $5 trillion and the market for retail securities is estimated by us to be about three times that. This makes room for competitors. We, as a first mover, can be expected to benefit as others enter the marketplace and market saturation can be expected to be several years in the future.

Intellectual Property

We have intellectual property that is our brand, our process, our ratings system, our KDM Broker Network, and our internal applications and systems. We have applied for a trade mark for the term “Middle-Money.”

Employees

As of the date of this Report, we employ twenty two full-time people and one part-time person. Five J. W. Korth & Company employees devote partial time to KDM.

Facilities

We maintain offices at 135 San Lorenzo Avenue, Suite 600, Coral Gables, Florida 33146.

Subsidiaries

As of the date of this report, KDM has one subsidiary, J. W. Korth, a FINRA and SEC registered broker-dealer founded in 1982 by James W. Korth, our CEO. J. W. Korth was previously the parent company of KDM. The companies were reorganized as of July 31, 2020, when KDM acquired a majority of the equity of J. W. Korth.

The following discussion of risk factors contains “forward-looking statements,” as discussed in the forward-looking statements Section of this Form 10-K Report. These risk factors may be important to understanding any statement in this Annual Report on Form 10-K or elsewhere. The following information should be read in conjunction with the Management’s Discussion and Analysis of Financial Condition and Results of Operations section and the Financial Statements and related notes of this Report on Form 10-K. Any of these factors, or others, many of which are beyond the Company’s control, could negatively affect the Company’s revenues, profitability or cash flows in the future. These factors include:

Certain Risks Related to COVID-19 Pandemic.

The spread of COVID-19 has had a material adverse impact on the United States economy. We cannot now anticipate whether, or to what extent, the pandemic may affect our business. Risks of the pandemic include those associated with economic conditions, increased volatility in financial markets, and the possibility of prolonged adverse economic conditions. These risks also include decreases in market value of loans and securities, borrower defaults resulting from tenants’ failures to pay rent, interruption of our growth and other strategic plans, and financial and other risks of government programs addressing the impacts of COVID-19 proving to be ineffective. Governmental regulators have required lenders to suspend foreclosures on certain mortgage loans.

In addition to the actions described above, there is risk that COVID-19 will continue to significantly affect the U.S. commercial real estate markets, resulting in reduced U.S. mortgage rates, decreased property values (which, among other effects, may both increase the risk of defaults and reduce the value of real estate collateral, thereby diminishing recovery in the event of default), and reduce demand for commercial and multifamily real estate and increase vacancies if businesses fail or close locations. We note that although the COVID-19 pandemic appears to have an end on the horizon, it is unknown whether further variants could cause additional outbreaks or lockdowns and that there is a potential for additional waves of COVID-19 or new strains of coronavirus even after COVID-19 appears contained in an area.

As a result of the COVID-19 outbreak in the United States, financial and operational challenges have arisen in many industries. The Company has been able to enact procedures to abate the financial and operational effects of the outbreak without a reduction in its workforce. Although the Company has been able to adapt sufficiently so far, there is no certainty that this will remain the case going forward.

| 9 |

Investors in our Notes may lose some or all of their investment in the Notes.

The regular payment of the Notes depends entirely on payments to KDM of a borrower’s CM Loan. The Notes are special, limited obligations of KDM payable only from KDM’s receipts of CM Loan proceeds, net of KDM’s servicing Fee and cost of collection. If the borrower defaults on the CM Loan, Noteholders will be dependent on proceeds from the Assignment of Rents held by KDM and on the proceeds if any, from foreclosure of the CM Loan mortgage for payments on the Notes. The failure of the borrower to repay the CM Loan is not an event of default by KDM. Notes are suitable purchases only for investors of adequate financial means who, in the event of a default on the underlying CM Loan, may have to wait for a foreclosure to recover some or all of the principal invested in their Note.

We rely on third-party appraisals to value the property securing the CM Loan, and information from the borrower on cash flow and profitability of the income property.

While we make every effort to engage responsible licensed third-party appraisers, we cannot be certain that the information and presentations they make are reliable. Appraisals are subject to mistakes that could affect the value of a property. Further, appraisers may make judgments of value based on cash flow presented by borrowers. If a borrower were to falsify its cash flow, it could affect the value shown in the appraisal. To verify cash flows, we receive bank statements from borrowers. KDM is not responsible for mistakes or fraudulent activities of borrowers or appraisers.

We rely on industry default and recovery rates for underwriting our CM Loans. Our default rates are untested against industry rates and may be higher.

Due to our limited operational and origination history, we do not have significant historical performance data regarding borrower performance and we do not yet know what our long-term CM Loan loss experience may be. It is possible that our default rates may be higher than the industry averages and our recovery rates may be lower than the industry averages.

If we believe it is in the best interest of the Noteholders, we have the right to adjust the terms of a CM Loan.

It is possible that due to natural disasters, local disruption of services, political unrest, changes in local laws, market competition or disruptions and other unforeseen events that affect the property pledged under a CM Loan or affect the borrower’s ability to make its CM Loan payments, it might be in the best interest of the Noteholders to provide a borrower with an accommodation regarding loan terms rather than be forced to foreclose on a loan. If we adjust a CM Loan, it may reduce interest payments, suspend interest payments, lengthen the time when principal may be received or change other terms of the CM Loan which could reduce the expected benefits of the CM Loan to the Noteholders.

There may be a default on a CM Loan.

CM Loan default rates may be significantly affected by general economic conditions beyond our control and beyond the control of the individual borrower. Default on a CM Loan is subject to many factors, such as prevailing interest rates, the rate of unemployment, the level of consumer confidence, residential or commercial real estate values, the value of the U.S. dollar, energy prices, changes in consumer spending, the number of personal bankruptcies, disruptions in the credit markets, and other factors, none of which can be predicted with certainty.

Information supplied by the borrower could be inaccurate or intentionally false.

While we perform due diligence on each borrower, including verifying property ownership, rent collections, property values, coverage ratios and other appropriate due diligence materials, a borrower could present us with false information which we may not discover during our due diligence process.

We do not monitor our borrowers’ use of funds.

It is possible the borrower may not use the funds for the purposes it has asserted, for example, to improve the property. Additionally, the borrower could potentially misuse the proceeds it receives from the loan in a way that negatively impacts their ability to make timely payments on the CM Loan, their credit, or the value of the underlying property.

CM Loan Guarantees May Not Be Collectable

Some CM Loans may have a personal guarantee. We may ask for guarantees from the owners, or the owners of the owner, if the owner is not an individual. Because we primarily focus our underwriting on the value of the mortgaged property, the loan to value ratio, and the debt service coverage ratio, we generally do not investigate the net worth of the borrowers, and therefore, the ultimate value of the guarantee on a CM Loan, if any. In the event a CM Loan goes into foreclosure and the money realized in the foreclosure does not pay off the entire principal owed on the CM Loan, investors should not count on the guarantee being collectible. Should such a situation arise, investors may not see repayment of the entire principal amount of their Notes.

If payments on a CM are not paid when due, Noteholders may not receive the full principal and interest payments that they expect to receive on Notes.

Payment to holders of Notes is completely dependent on payments received from corresponding CM Loans. If the borrower fails to make a required payment on a CM Loan within 30 days of a due date, we will pursue collection. Referral of a delinquent CM Loan to an attorney on the 31st day of its delinquency will be considered reasonable collection efforts. If we refer a CM Loan to an attorney, we will monitor that CM Loan until either the CM Loan is paid or the property is foreclosed and resold and investors are paid. We may also pursue collection of a delinquent CM Loan directly. In the case of collection efforts, the cost of attorney’s fees will be charged against the CM Loan and will reduce the net payments on a Note.

| 10 |

The CM Loans underlying the Notes are typically payable on an interest-only basis until maturity, at which time the entire principal balance is due. Therefore, borrowers may have to refinance to pay off a balloon payment on the CM Loan.

If a borrower must refinance to pay off a CM Loan, such refinancing could be impossible due to market conditions or other factors. In such a case, the CM Loan would default. Such a default could reduce or eliminate principal payment of the Notes.

A CM Loan may be prepaid at any time. Borrower CM Loan prepayments will reduce payments of interest on the Notes.

The borrower may prepay some or all of the principal amount of a CM Loan. A borrower may decide to prepay all, or a portion of, the remaining principal at any time. Notwithstanding the prepayment of all or a portion of the CM Loan, the borrower must pay all of the interest that would be due on the principal amount of the CM Loan until the expiration of borrower’s interest guarantee, typically a guarantee of from two to three years interest. Noteholders will receive such prepayment, net of our servicing fee. Interest will not accrue after the date on which the CM Loan is paid in full. If the borrower prepays a portion of the remaining unpaid principal balance on the CM Loan, we will reduce the outstanding principal amount and interest will cease to accrue on the prepaid portion. On an amortizing loan, we will require the borrower to pay the same amount on the CM Loan as the borrower paid prior to any partial repayment of principal. As a result of the combination of the reduced principal amount and the unchanged monthly payment, the effective term of the CM Loan will decrease. On an interest only CM Loan, the monthly payment Noteholders receive will be reduced proportionally by the amount of principal repaid. If the borrower prepays the CM Loan in full or in part, Noteholders will in all probability not receive all the interest payments that they expected to receive on their Notes.

Prevailing interest rates may change during the term of the CM Loan on which a Note is dependent.

If a CM Loan is prepaid, Noteholders may be unable to invest prepaid Note proceeds at a rate comparable to the interest payable on the Notes. Further, if interest rates rise, there is a market for the Notes, and a Noteholder decides to sell a Note prior to maturity, the Noteholder may receive a discounted return on the Note.

Investor funds in a KDM segregated account do not earn interest.

Proceeds of the sale of the Notes are held in a non-interest bearing segregated account pending completion of the Note Offering pursuant to an effective registration statement and investment in the Notes. Further, we place borrower loan payments in a segregated account under our control and pay all loan payments collected from the prior payment date at least four business days prior to the payment date on the twenty-fifth day of each month, with an extension to the next business day if required. Funds held in segregated accounts do not earn interest. These segregated accounts are held at Bank United and are managed by KDM. There is no escrow agreement with the bank.

The Notes will not be listed on any securities exchange, and it is unlikely that a trading market for the Notes will develop. An underwriter of the Notes may make a market in the Notes, but is not obligated to do so.

There can be no assurance that a market for Notes will develop or that there will be a buyer for any particular Notes offered for resale. Therefore, investors must be prepared to hold their Notes to maturity.

We may have to limit our business to avoid being deemed an investment company under the Investment Company Act.

In general, a company that is or holds itself out as being engaged primarily in the business of investing, reinvesting or trading in securities may be deemed to be an investment company under the Investment Company Act of 1940, as amended (Investment Company Act). The Investment Company Act contains substantive legal requirements that regulate the manner in which “investment companies” are permitted to conduct their business activities. We believe we are excluded from registration by Section 3(c)(5)(c) of the Investment Company Act and have conducted, and we intend to continue to conduct, our business in a manner that does not result in our company being characterized as an investment company. This section of the Investment Company Act contains an exemption for companies that make mortgages and do not issue redeemable shares. To avoid being deemed an investment company, we may not be able to broaden our offerings, which could require us to forego attractive opportunities. If we are ever deemed to be an investment company under the Investment Company Act, we may be required to institute burdensome compliance requirements and our activities may be restricted, which could materially adversely affect our business, financial condition, and results of operations.

Funds Received for all CM Loans are commingled in a Segregated Account.

We hold all funds received from CM Loans in a segregated account title In-Trust For 2 at Bank United bank. We then use our internal accounting system to determine which funds are applied to which Note investors. While our internal accounting system is backed up into separate record keeping systems managed by service providers, should our systems fail and the back-up systems fail for any reason we may have difficulty determining which payments are to be applied to which Noteholder and your payments could be delayed until such a determination is made. We also could make an accounting error that would send too much money to one Noteholder and leave other Noteholders short of funds until we could recover the erroneous payments through the payment systems we utilize to distribute funds to investors. In such a case, recovery of over payments may not be achieved and it would leave the account permanently short for investors who did not receive the over payments.

| 11 |

KDM deposits all interest and principal payments which it receives on CM Loans in a single segregated bank account, and payments on real tax and insurance escrows in another segregated account, which accounts and the funds deposited in them may be subject to claims of general creditors of KDM in the event of a KDM bankruptcy.

In the event of a KDM bankruptcy, general creditors of KDM may assert a claim that funds on deposit in the segregated account maintained by KDM for the benefit of Noteholders, and the separate segregated account maintained by KDM for real estate tax and insurance payments, are subject to the claims of general creditors. Principal and interest payments on CM Loans are deposited in a segregated bank account, and payments of real estate taxes and insurance on mortgaged properties are deposited in another segregated account, when and as received by KDM. Receipts deposited in those accounts are disbursed to Noteholders monthly and annually to property insurers and taxing authorities. KDM performs all accounting for these accounts, including sub-accounts for each Noteholder and property, and maintains all accounting records at its principal office. Under the Trust Indenture, the Trustee will have a first lien on the principal and interest account for the benefit of Noteholders. If the bankruptcy court were to determine that the funds in the account were subject to claims of creditors other than Noteholders or the Trustee acting on their behalf, the amount that Noteholders would receive from the account could be adversely affected. Further, amounts on deposit to pay real estate taxes and insurance could be reduced or entirely eliminated if paid to general creditors of KDM in the bankruptcy proceeding. The bankruptcy court could temporarily stay disbursements to Noteholders, taxing authorities and insurers even if the court were ultimately to determine that the funds in the account should be distributed to the Noteholders, the Trustee acting on their behalf, and, also, as appropriate, to taxing authorities and property insurers, resulting in delays to Noteholders in the receipt of payments on their Notes and penalties imposed by insurers and taxing authorities.

The market in which we participate is competitive and, if we do not compete effectively, our operating results could be harmed.

The commercial mortgage market is competitive and rapidly changing. We expect competition to persist and intensify in the future, which could harm our ability to increase volume.

Our principal competitors include major banking institutions, credit unions, credit card issuers and other consumer finance companies. It is possible that one or more of these companies decide to compete directly with us. The results of such competition could harm our operating results and, in that event, our ability to continue to service the CM Loan and Notes could be adversely affected.

We rely on third-party banks to disburse CM Loan proceeds and process CM Loan payments, and we rely on third-party computer hardware and software. If we are unable to continue utilizing these services, our business and ability to service the CM Loans on which the Notes are dependent may be adversely affected.

We rely on a third-party bank to disburse CM Loan amounts. Additionally, because we are not a bank, we cannot belong to and directly access the ACH payment network, and we must rely on an FDIC-insured depository institution to process our transactions, including CM Loan payments and remittances to holders of the Notes. We currently use Bank United for these purposes. We also rely on computer hardware purchased and software licensed from third parties. This purchased or licensed hardware and software may not continue to be available on commercially reasonable terms, or at all. If we cannot continue to obtain such services from this institution or elsewhere, or if we cannot transition to another processor quickly, our ability to process payments will suffer and your ability to receive principal and interest payments on the Notes will be delayed or impaired.

Competition for our employees is intense, and we may not be able to attract and retain the highly skilled employees who we need to support our business.

Competition for highly skilled technical and financial personnel is extremely intense. We may not be able to hire and retain these personnel at compensation levels consistent with our existing compensation and salary structure. Many of the companies with which we compete for experienced employees have greater resources than we have and may be able to offer more attractive terms of employment.

In addition, we invest significant time and expense in training our employees, which increases their value to competitors that may seek to recruit them. If we fail to retain our employees, we could incur significant expenses in hiring and training their replacements and the quality of our services and our ability to service the CM Loans could diminish, resulting in a material adverse effect on our business and our ability to service the Notes.

If we fail to retain our key personnel, we may not be able to achieve our anticipated level of growth and our business could suffer.

Our future depends, in part, on our ability to attract and retain key personnel. Our future also depends on the continued contributions of our executive officers and other key technical personnel, each of whom would be difficult to replace. The loss of the services of any of the executive officers or key personnel, and the process to replace any of our key personnel would involve significant time and expense and may significantly delay or prevent the achievement of our business objectives.

| 12 |

Purchasers of Notes will have no control over KDM and will not be able to influence KDM corporate matters.

Our Notes grant no equity interest in KDM to the purchaser nor grant the purchaser the ability to vote on or influence our management decisions, including forbearance or foreclosure. As a result, our parent company, J.W. Korth & Company, exercises voting control over all our company operations, including the election of managers and officers and the approval of significant transactions, such as a merger or other sale of our Company or its assets. Any such actions which we take may adversely affect our business and our ability to service the CM Loan and Notes.

Unforeseeable Adverse Events.

Events beyond our control may damage our ability to maintain adequate records, or perform our servicing obligations. If such events result in a system failure, Noteholders’ ability to receive principal and interest payments on Notes could be substantially harmed.

If a catastrophic event resulted in an outage and physical data loss, our ability to perform our servicing obligations would be materially and adversely affected. Such events include, but are not limited to, fires, earthquakes, hurricanes, terrorist attacks, natural disasters, computer viruses and telecommunications failures. We store back-up records via cloud storage services via several different companies. If our electronic data storage and backup storage system are affected by such events, we cannot guarantee that Noteholders would be able to recoup their investment in the Notes.

Federal and State regulatory bodies may create new rules and regulations that could adversely affect our business.

In the wake of the last financial crisis, banking and finance regulation continues to evolve, and increasing regulation by federal and state governments may become more likely. Our business could be negatively affected by the application of existing laws and regulations or the enactment of new laws applicable to lending, mortgages, mortgage servicing, or securities distribution. The cost to comply with such laws or regulations could be significant and would increase our operating expenses, and we may be unable to pass along those costs to our investors in the form of increased fees.

If we discover a material weakness in our internal control over financial reporting which we are unable to remedy, or otherwise fail to maintain effective internal control over financial reporting, our ability to report our financial results on a timely and accurate basis may be adversely affected.

Should our auditors discover a material weakness in our internal controls, our ability to report our financial results on a timely and accurate basis may be adversely affected.

New Government Regulation may limit our ability to make CM Loans

We do not believe that we are subject to Risk Retention under RR (17 CFR 246), as our entity type is not within scope of the rule according to 12 CFR 244.1(c). However, if we become subject to risk retention rules, we could be required to raise significant capital in order to continue doing business.

Our Proprietary Ratings System is untested and based on broad assumptions for which we have no statistical basis

We created the KDM Ratings System internally, and based it on very broad assumptions and experience of staff members. Our staff members have no experience in creating a ratings system. We are not affiliated with nor do we have experience in creating ratings of debt or mortgage securities. The Rating System has no track record and has not been tested against any known data set. The Rating System is still evolving, and we add items as we add property types. It should not be relied upon as a predictable measure of performance of the underlying CM Loan at this time. We also have conflicts of interest with respect to our Ratings System. See “Conflicts of Interest Regarding Our Proprietary Ratings System.”

Item 1B. Unresolved Staff Comments

Not applicable.

We do not own any real property for use in our operations or otherwise. We lease office space in Coral Gables, Florida and through our subsidiary, J. W. Korth, in Lansing, Michigan.

The Company is not subject to any material legal proceedings.

| 13 |

The Company’s broker-dealer subsidiary is subject to an investigation of technical aspects of its financial advisory activities by the SEC regarding the reporting and treatment of certain trades and the disclosures made in the subsidiary’s financial advisory brochure. The inquiry involves rule interpretations by the subsidiary of the technical aspects of recording and reporting for purchases and sales of bonds and the relevance of certain disclosures in the brochure. The transactions in question do not involve KDM issued securities. The firm is fully cooperating with the SEC and believes at this time the outcome of the investigation is not expected to have a material effect on KDM or its subsidiary.

Item 4. Mine Safety Disclosures

Not applicable.

| 14 |

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

There is no market for the Company’s common equity.

Holders

As of December 31, 2020, the Company had issued and outstanding (i) 5,000,000 shares of its common stock, all which were issued to J.W. Korth & Company Limited Partnership, and (ii) 200,000 shares of its Series A 6% Cumulative Perpetual Convertible Preferred Stock (the “Series A Preferred”), all of which were issued to Cede & Company. The number of holders was determined from the records of our transfer agent and does not include beneficial owners of common or preferred stock whose shares are held in the names of Cede & Company, broker-dealers, or registered clearing agencies. The transfer agent of our common stock and preferred stock is Continental Transfer and Trust Company, One State Street, New York, New York 10004.

Dividends

The Company has not paid, and has no plans to pay, dividends on its common stock. Holders of the Series A Preferred are entitled to receive, when, as, and if declared by the Board of Directors, cash dividends at a rate of 6% per annum based of the Series A Preferred liquidation preference of $25.00 per share. Holders of the Company’s 200,000 issued shares of Series A Preferred were paid a dividend totaling $1.50 per share over the four quarterly payments for the year ended December 31, 2020.

Securities Authorized for Issuance Under Equity Compensation Plans.

For information regarding securities authorized for issuance under our 2019 Stock Plan, please refer to the disclosure included below under the caption “Item 11. Executive Compensation—Equity Compensation Plan Information.”

Sales of Unregistered Securities

There were no sales of unregistered equity securities of the Company during the year ended December 31, 2020.

Purchases of Equity Securities.

The Company did not purchase any of its equity securities during the year ended December 31, 2020.

Item 6. Selected Financial Data

Not applicable.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion in conjunction with our audited historical financial statements, which are included elsewhere in this Form 10-K. Management’s Discussion and Analysis of Financial Condition and Results of Operations contains statements that are forward-looking. These statements are based on current expectations and assumptions, which are subject to risk, uncertainties and other factors, including, but not limited to, those described in the subsection titled “Risk Factors,” located in Part I, Item 1A, of this Form 10-K. We urge you to review our discussion of Risk Factors relating to our business, including, without limitation, risks related to the impact on our company of the COVID-19 pandemic, which factors individually or as a group could materially affect the discussion which follows.

Overview

Korth Direct Mortgage, LLC, was organized in Florida on July 24, 2009, under the name HCMK Consulting, LLC. We changed our name to J. W. Korth & Company, LLC, in November 2010, and then to Korth Direct Mortgage, LLC, on August 24, 2016. KDM converted into a Florida corporation, Korth Direct Mortgage Inc., on June 6, 2019. Our principal executive offices are located at 135 San Lorenzo Avenue Suite 600, Coral Gables, Florida 33146, and our telephone number is (305) 668-8485. Our website address is www.korthdirect.com. We also operate under the trade name KDM Financial, and our subsidiary is J W Korth & Company, L.P.

| 15 |

Korth Direct Mortgage began its formal operations in October of 2016 when we engaged our Chief Lending Officer. KDM is a licensed Mortgage Lender Servicer with the State of Florida. Our NMLS License Number is 1579547.

Reorganization

Prior to July 31, 2020, we were wholly owned by J. W. Korth & Company, L.P., a FINRA and SEC registered broker-dealer founded in 1982. On July 31, 2020, we acquired substantially all of the equity of J.W. Korth.

We originate, fund and service loans which are made to commercial borrowers. The loans are held by KDM as the lender. We fund our loans directly in the capital markets through issuance of Mortgage Secured Notes (“MSNs” or “Notes”), which are sold through J.W. Korth as underwriter through exemptions from registration available under Rule 144A, Regulation D, and other exemptions from registration. The Company and J.W. Korth determined that the we could operate more efficiently if J.W. Korth became a wholly-owned subsidiary of the Company. J.W. Korth submitted its then-proposed sale to FINRA, as required by FINRA rules, and FINRA advised J.W. Korth that it could proceed with the closing.

Pursuant to the Purchase Agreement, as a condition of closing J.W. Korth agreed to distribute all of its 5,000,000 shares of common stock in the Company to its partners ratably in accordance with their partnership interests in J.W. Korth pursuant to exemptions from registration available under Section 4(a)(2) of the Securities Act of 1933, as amended, and Rule 506 promulgated under the Securities Act.

As post-closing commitments the Company agreed to (i) retain Mr. Korth as the managing partner of J.W. Korth, Ms. MacDonald-Korth as J.W. Korth’s chief financial officer, and all other employees of J.W. Korth who were employed at closing of the Transactions; (ii) operate J.W. Korth as an SEC registered broker-dealer and investment advisor; (iii) pay the J.W. Korth Preferred Capital Interest Partners quarterly dividends concurrently with its payment of the Company’s Series A Preferred Stock dividends at least annually; (iv) in such years as it pays Series A Preferred dividends, redeem 25% annually of the JW Korth Preferred Capital Interest partners through a capital contribution to J.W. Korth; and (v) make a discretionary redemption of all accounts of the limited partners of J.W. Korth under the J.W. Korth partnership agreement. Upon redemption of the limited partners’ accounts and the payment of the other consideration to described above to the JW Korth partners, KDM will own 100% of the voting interests in J.W. Korth.

The following table summarizes the consideration paid, or to be paid, for the Acquisitions:

| Consideration | ||||

| Accrued & unpaid dividends to the Preferred Capital Interest partners | $ | 213,443 | ||

| JW Korth LLC’s Common Capital Interest account | 150,000 | |||

| Contingent liability to redeem J.W. Korth Preferred Capital Interest Partners | 696,253 | |||

| Disposition of outstanding loan due from J.W. Korth Executive Officer | 69,780 | |||

| Total Consideration Paid | $ | 1,129,476 | ||

The following table summarizes the net book value of assets and liabilities acquired as of the closing date, July 31, 2020:

| Net Book Value | ||||

| J.W. Korth Net Book Value | $ | 889,131 | ||

| Less: Preferred Interest in J.W. Korth by Company prior to acquisition | (250,000 | ) | ||

| Adjusted Net Book Value acquired | $ | 639,131 | ||

Since the acquisition was between related parties, the transaction was recorded at net book value as of the closing date. The difference of $490,345 between the consideration paid and the net book value of the assets and liabilities acquired was recorded as an offset to equity, specifically to Additional Paid-in Capital. Disclosure of supplemental pro forma information for revenue and earnings related to the acquisition, assuming the acquisition was made at the beginning of the earliest period presented, has not been disclosed since the effects of the acquisition would not have been material to the results of operation for the periods presented.

| 16 |

Results of Operations for Year Ended December 31, 2020

The Company generated revenues of $2,772,776 for the year ended December 31, 2020, an increase of $2,182,653 compared with revenues of $590,123 for the year ended December 31, 2019. The increase in revenues generated from origination fees, servicing revenue, and interest income was due to an increase of $89.7 million in mortgages owned and serviced from December 31, 2019, to December 31, 2020. As of December 31, 2020, the Company owned mortgages of $175,370,850 compared with mortgages of $85,692,812 as of December 31, 2019, an increase of 105%.

Total Revenue increased by 370% year over year, from $590,123 in 2019 to $2,772,776 for the year ended December 31, 2020. This growth was due to a 300% increase in servicing revenue, to $1,186,743, as well as $922,527 attributable to the acquisition of J.W. Korth. Of this revenue, $309,210 is for Underwriting Income, which, due to the reorganization, allows KDM to re-capture the underwriting fees it pays for distribution of its MSNs. KDM also earned $176,345 in interest income from its balance sheet lending.

Gross profits increased by $1,667,384 (561%) to $1,964,355 during the year ended December 31, 2020, compared with gross profits of $296,971 during the year ended December 31, 2019. The increase in gross profits was attributed to the increase in the amount of mortgages serviced during the year ended December 31, 2020, with lower levels of mortgage related costs as a percentage of revenues, which generated higher gross margins. In addition, gross profits increased by $840,348 during the year ended December 31, 2020, as a result of the acquisition of J.W. Korth, primarily generated from trading profits and broker underwriting income.

In spite of positive year over year revenues, KDM growth slowed significantly during the second and third quarters of 2020 due to the global pandemic and the pull-back in credit markets. Our sector of the market began to recover in Q3 of 2020 and we were able to complete nearly $62.8M of lending from August through December 2020.

Operating expenses were $2,240,436 during the year ended December 31, 2020, which was an increase of $1,330,841 compared with operating expenses of $909,595 during the year ended December 31, 2019. The increase in operating expenses was the result of increases of $1,136,892 in payroll related costs, $118,452 in accounting, professional and legal fees, $66,430 in rent expense, and $70,220 in other operating expenses to support the growth of the overall business. These increases were partially offset by a decrease of $64,544 in non-cash stock compensation expense related to options issued to employees and directors in 2019. Of the $1,330,841 increase in operating expenses, $792,793 (60%) of the increase in operating expenses, primarily payroll related costs, for the year ended December 31, 2020, were generated by J.W. Korth, which was acquired on July 31, 2020.

Other income decreased by $1,665,834 to $1,263,455 during the year ended December 31, 2020, compared with other income of $2,929,289 during the year ended December 31, 2019. The decrease in other income was due to the forgiveness of $548,802 of debt due to J. W. Korth, our parent company at the time, during the year ended December 31, 2019. In addition, unrealized gain on mortgages decreased by $1,112,017 during the year ended December 31, 2020, due to lower net margins on new loans generated during the year ended December 31, 2020, compared with the prior year.

In June 2019, the Company transitioned from a limited liability company to a C-corporation. Beginning in June 2019, the Company began recording a provision for income taxes. During the year ended December 31, 2020, the Company recorded $260,875 in deferred income tax expense compared with $380,236 of deferred income tax expense from June 2019 through December 31, 2019.

Net income decreased $1,209,930 to $726,499 for the year ended December 31, 2020, compared with net income of $1,936,429 during the year ended December 31, 2019. The decrease in 2020 was primarily attributed to the decrease in Other Income of $1,665,834. The Other Income category is dominated by the Unrealized Gain on Mortgages, which is the net present value of the future income expected from each loan. In 2020, we closed several loans with shorter guaranteed prepayment periods, as well as one large loan with slim net margin to the Company, which resulted in a lower total Unrealized Gain than might be expected from the loan volume. This decrease was partially offset by a decrease in net loss from operations of $336,543 (a 55% improvement) and a decrease of $119,361 in deferred income taxes generated during the year ended December 31, 2020, compared with the year ended December 31, 2019.

We are pleased with our growth given the difficult year we just completed due to the global pandemic. We have a large and ever-growing pipeline of new loans and actively pursuing additional capital sources to help speed our time to close as well as our net margin at securitization.

| 17 |

Financial Condition for the year ended December 31, 2020

As of December 31, 2020, we had $2,037,177 in cash and loans on forty-three properties across twenty-two securitizations on our balance sheet for a total of $175,370,850 at fair value. The original loan amounts totaled $176,456,054; however, three loans are amortizing and are carried at their remaining principal balances, and one loan was partially redeemed. We have recognized an unrealized gain of $1,268,470, which is the net present value of the future servicing income we receive from the loans made to date. This value is highly subjective and includes such variables as constant prepayment rate (CPR), discount rate, and market pricing data. This value is calculated quarterly. The current value was provided by a third-party consulting firm and uses 15.0% for the discount rate and includes an14.95% CPR, along with other assumptions customary to the industry.

Capital and Liquidity Needs

The Company completed the sales of $5,000,000 (less issue costs of $250,000) in Series A 6% Cumulative Perpetual Convertible Preferred Stock in September 2019. We did not need to access additional capital in 2020. We expect to raise additional capital in 2021and as necessary in succeeding years.

The Company is also looking to secure lines of credit and lender financing in forms that will comply with covenants of our trust indentures, but allow us the flexibility to continue to grow the business.

Status of our CM Loans

All of our CM Loans are currently performing. We report annually in our quarterly or annual reports on the anniversary of the CM Loan, its updated status. Although no late payments have been made to Noteholders, KDM elected to put KDM2019-N001 in lockbox on January 31, 2020. This loan continues to perform with the additional support of the lockbox. The lockbox was put in place after a single payment became over 30 days late.

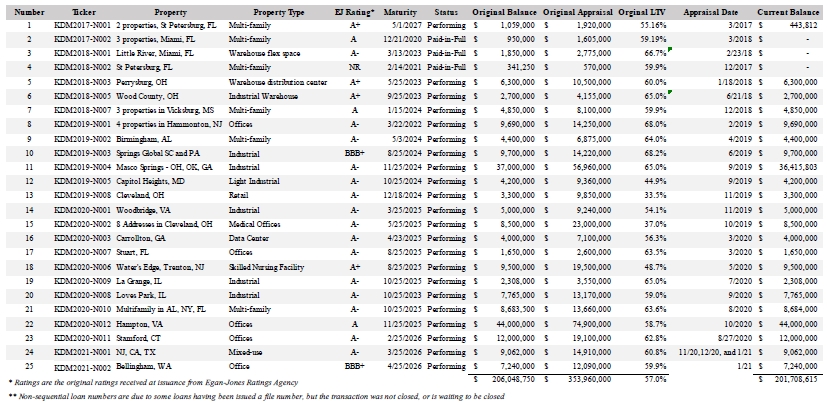

Loan Information as of March 31, 2021

| 18 |

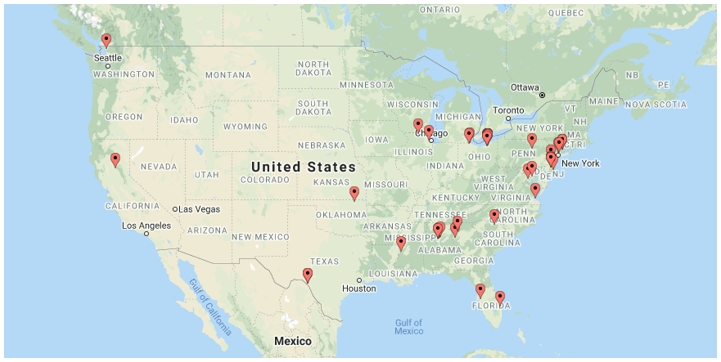

Map of Current Loans

| 19 |

Sales, Marketing and Customer Service

Our marketing efforts are designed to attract borrowers and mortgage brokers to our platform and to close transactions with them. We employ primarily digital marketing and email correspondence to mortgage brokers, banks, real estate agents, and commercial property owners to encourage them to present loan packages to us for possible financing. We subscribe to lead generation databases and loan and property platforms to find loans. We also contact other financial institutions directly and through brokers who may own commercial mortgages, and will attempt to purchase mortgages for KDM.

Fraud Detection

We consider fraud detection to be of utmost importance to the successful operation of our business. We employ a combination of proprietary technologies and commercially available licensed technologies and solutions to prevent and detect fraud. We use services from third-party vendors for user identification and OFAC compliance.

Competition

The market for mortgage lending is competitive and rapidly evolving. We believe the following are the principal competitive factors in the lending market:

| · | pricing and fees; |

| · | experience, including borrower full funding rates and investor returns; |

| · | branding; and |

| · | ease of use. |

We face competition from major banking institutions, credit unions, credit card issuers and other consumer finance companies as well as smaller private lenders.

We may also face future competition from new companies entering our market. These companies may have significantly greater financial, technical, marketing and other resources than we do and may be able to devote greater resources to the development, promotion, sale and support of their consumer lending programs. These potential competitors may be in a stronger position to respond quickly to new technologies and may be able to undertake more extensive marketing campaigns. These potential competitors may have more extensive potential borrower bases than we do. In addition, these potential competitors may have longer operating histories and greater name recognition than we do. Moreover, if one or more of our competitors were to merge or partner with another of our competitors or a new market entrant, the change in competitive landscape could adversely affect our ability to compete effectively. Another brokerage firm or mortgage company may use our program as a model and attempt to execute it in a similar fashion.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

Not required.

Item 8. Consolidated Financial Statements

The following is an index to the Consolidated Financial Statements of the Company being filed here-with commencing at page F-1 below:

| Report of Independent Registered Public Accounting Firm | F-2 | |

Consolidated Statements of Financial Condition as of December 31, 2020 and 2019 |

F-5 | |

Consolidated Statements of Operations for the fiscal years ended December 31, 2020 and 2019 |

F-6 | |

Consolidated Statements of Changes in Members’ Equity (Deficit)

for the fiscal years ended |

F-7 | |

Consolidated Statements of Cash Flows for the fiscal years ended December 31, 2020 and 2019 |

F-8 | |

Notes to the Consolidated Financial Statements |

F-9 |

| 20 |

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

We have had no changes in nor disagreements with our independent accountants on accounting and financial disclosure during the fiscal years ended December 2020 and 2019, nor in any subsequent interim period.

Item 9A. Controls and Procedures

Evaluation of Disclosure Controls and Procedures

Disclosure controls and procedures are controls and other procedures that are designed to ensure that information required to be disclosed in our reports filed or submitted under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the Securities and Exchange Commission’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed in our reports filed under the Exchange Act is accumulated and communicated to management, including our Chief Executive Officer and Chief Financial Officer, to allow timely decisions regarding required disclosure.

We carried out an evaluation of the effectiveness of the design and operation of our disclosure controls and procedures (as defined in Securities Exchange Act Rules 13a-15(e) and 15d-15(e)) as of December 31, 2019. Based upon that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were effective as of December 31, 2020.

Management’s Report on Internal Control Over Financial Reporting

We are responsible for establishing and maintaining adequate internal control over financial reporting as such term is defined by Securities Exchange Act Rule 13a-15(f). Our internal controls are designed to provide reasonable assurance as to the reliability of our financial statements for external purposes in accordance with accounting principles generally accepted in the United States.

Internal control over financial reporting has inherent limitations and may not prevent or detect misstatements. Therefore, even those systems determined to be effective can provide only reasonable, not absolute, assurance with respect to financial statement preparation and presentation. Further, because of changes in conditions, the effectiveness of internal control over financial reporting may vary over time.

A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of the Company’s annual or interim financial statements will not be prevented or detected on a timely basis.

Under the supervision and with the participation of our President and Chief Financial Officer, we have evaluated the effectiveness of our internal control over financial reporting as of December 31, 2020, as required by Securities Exchange Act Rule 13a-15(c). In making our assessment, we have utilized the criteria set forth by the 2013 Internal Control Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. We concluded that based on our evaluation, our internal control over financial reporting was effective as of December 31, 2020.

Changes in internal control over financial reporting

There have been no changes in our internal control over financial reporting that occurred during the fourth quarter ended December 31, 2020, or subsequent to the date the Company completed its evaluation, that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

None

| 21 |

PART III

Item 10. Directors, Executive Officers and Corporate Governance

As of the date of this Report, the Executive Officers and Directors of the Company were:

| Name | Age | Office |

| James W. Korth | 70 | Chairman of the Board, Chief Executive Officer, and Director |

| Holly C. MacDonald-Korth | 45 | President, Chief Financial Officer and Director |

| Pamela J. Hipp | 52 | Director of Securities Marketing and Director |

| Daniel Llorente | 41 | Chief Lending Officer and Director |

| Jonathan L. Shepard | 77 | Secretary and Director |