Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - GRAHAM ALTERNATIVE INVESTMENT FUND I LLC | brhc10022160_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - GRAHAM ALTERNATIVE INVESTMENT FUND I LLC | brhc10022160_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - GRAHAM ALTERNATIVE INVESTMENT FUND I LLC | brhc10022160_ex31-1.htm |

| EX-4.1 - EXHIBIT 4.1 - GRAHAM ALTERNATIVE INVESTMENT FUND I LLC | brhc10022160_ex4-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 0-53965

GRAHAM ALTERNATIVE INVESTMENT FUND I LLC

BLENDED STRATEGIES PORTFOLIO

(Exact name of registrant as specified in its charter)

|

DELAWARE

|

20-4897069

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

c/o GRAHAM CAPITAL MANAGEMENT, L.P.

40 Highland Avenue

Rowayton, CT 06853

(Address of principal executive offices) (zip code)

Brian Douglas

Graham Capital Management, L.P.

40 Highland Avenue

Rowayton, CT 06853

(203) 899-3400

(Name, address, including zip code, and telephone number, including area code,

of agent for service)

Copies to:

Christopher Wells

Proskauer Rose LLP

11 Times Square

New York, NY 10036

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Trading Symbol(s)

|

Name of each exchange on which registered

|

|||

|

None

|

N/A

|

None

|

|

Securities registered pursuant to Section 12(g) of the Act:

|

Blended Strategies Portfolio: Units of Interests

|

|

|

(Title of Class)

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to section 13 or section 15(d) of the Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated file, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated

filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated

filer

☐

|

Accelerated

filer

☐

|

Non-accelerated filer ☐

|

Smaller reporting company

☑

|

Emerging Growth Company

☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange

Act. ☐

Indicate by check mark whether the registrant has filed a report on attestation to its management’s assessment of the effectiveness of internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by

the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

Yes ☐ No ☑

Units of the Blended Strategies Portfolio with an aggregate value of $27,475,546 were outstanding and held by non-affiliates as of June 30, 2020.

As of March 1, 2021, 192,441.009 Units of the Blended Strategies Portfolio were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

2

|

Item 1:

|

BUSINESS

|

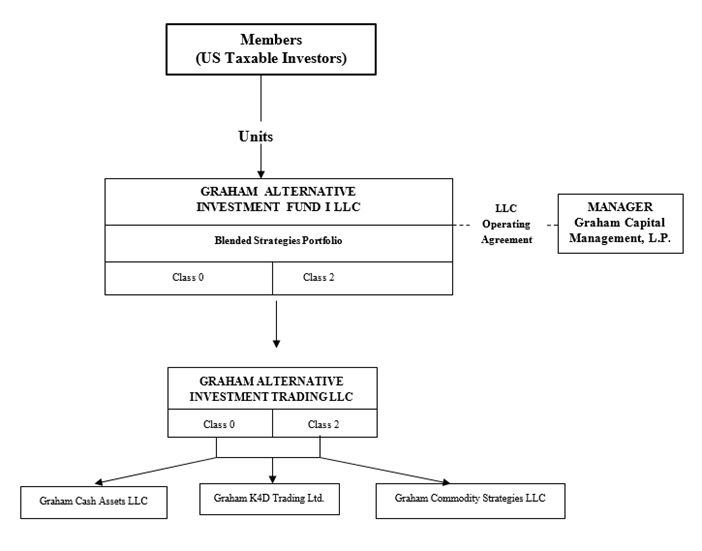

GRAHAM ALTERNATIVE INVESTMENT FUND I LLC

General Development of Business

Graham Alternative Investment Fund I LLC (“GAIF I”) is a Delaware Series Limited Liability Company established through an amendment to the certificate of

formation, effective March 28, 2013. Prior to March 28, 2013, GAIF I was organized as a Delaware Limited Liability Company which was formed on May 16, 2006. GAIF I was

formed to enable U.S. taxable investors to achieve long-term capital appreciation through professionally managed trading in both U.S. and foreign markets, primarily in futures contracts, forward currency and metals contracts, spot currency

contracts and associated derivative instruments such as options and swaps. GAIF I commenced operations on August 1, 2006.

The Blended Strategies Portfolio uses a systematic trading program and a discretionary trading program. The Blended Strategies Portfolio units of interest (the “Units”) of GAIF I are registered under

the Securities Exchange Act of 1934, as amended, (the “Exchange Act”) and the financial information and statements contained herein are solely with respect to that Portfolio.

GAIF I invests in Graham Alternative Investment Trading LLC, a Delaware limited liability company (the “Feeder Fund”). Specifically, the assets of GAIF I

subscribed for investment in the Blended Strategies Portfolio will be invested in Graham Alternative Investment Trading LLC. Trading on behalf of the Fund will be conducted in separate master funds (in a “master-feeder” fund structure) managed by

the Manager (as defined below). For the purposes of this report, the term “Fund” shall include GAIF I, the Feeder Fund and the master funds in which they invest, unless the context implies otherwise. Graham

Capital Management, L.P. (the “Manager”) is the Fund’s manager and the investment advisor to the Fund. The Manager’s website is www.grahamcapital.com.

The investment objective of the portfolio of the Fund is to achieve long-term capital appreciation through professionally managed trading in both U.S. and foreign markets,

primarily in futures contracts, forwards contracts, spot currency contracts and associated derivative instruments such as options and swaps. The Fund seeks profit opportunities in the global financial markets, including interest rates, foreign

exchange, global stock indices and energy, metals and agricultural futures, as a professionally managed multi-strategy investment vehicle.

The portfolio of the Fund consists of multiple trading strategies of the Manager, which the Manager has combined in an effort to diversify the investment exposure

of the portfolio and to make the performance returns of the portfolio less volatile and more consistently profitable. The Manager seeks to combine in the portfolio investment strategies that trade in different markets and display relatively low

correlation to each other. Through such composition, the Manager aims to provide the portfolio with the potential to make profits and have strong risk-adjusted returns in both rising and falling markets and during both expanding and recessionary

economic cycles. In discretionary programs, a trader determines trades subjectively based on his personal assessment of trading data and trading experience, while in systematic programs, trades are based almost entirely on computerized

mathematical models. The Fund, at all times, will look primarily to commodity interests as its principal intended source of gains and anticipates that at all times commodity interests will present the Fund’s primary risk of loss, and the

Fund will not acquire any financial instrument or enter into any financial transaction if to do so would cause the Fund to look to securities as its principal intended source of gains or anticipate that securities will present the Fund’s primary risk

of loss. Examples of the types of instruments that the Fund may trade by market include, but are not limited to:

Global fixed income: U.S. Treasury futures, Eurodollar futures and Japanese government bond futures

Global stock indices: futures contracts on the Russell 2000, S&P 500 and TOPIX

Foreign exchange: forward contracts on the British pound, euro, Japanese yen and Swiss franc

Energy: futures contracts on heating oil, natural gas and crude oil

Agriculture and Softs: futures contracts on cotton, feeder cattle, lean hogs and soybeans

Metals: futures or forward contracts on aluminum, copper and gold

3

The Manager believes strongly in the importance of its ongoing research activities, particularly in the development of new trading programs, and expects to develop additional

trading systems for the Fund and to modify the systems currently in use for the Fund over time. The Manager also seeks to add new trading strategies to its discretionary programs and to modify such strategies over time. There is no maximum number of

trading programs that the Manager may see fit to include in the Blended Strategies Portfolio, and the Manager may increase or decrease the number of programs included in the portfolio over time. The Manager continually updates and modifies its

trading programs and may make such additions or deletions of trading programs to the Blended Strategies Portfolio at any time– such as changes in the leverage of, or in the asset allocations to, any of the Fund’s trading programs – in its sole

discretion. The Fund is not required to provide prior, or any, notice of any such changes to investors.

Under the Limited Liability Company Agreement of GAIF I (the “Company Agreement”), the Manager has complete and exclusive responsibility for management and administration of the

affairs of GAIF I. The Manager is currently registered as a commodity pool operator (“CPO”) and commodity trading advisor (“CTA”) with the Commodity Futures Trading Commission (“CFTC”), as an investment adviser with the Securities and Exchange

Commission (“SEC”) and is a member of the National Futures Association (“NFA”). GAIF I is not required to be, and is not, registered under the Investment Company Act of 1940, as amended. Investors purchasing units of interests (the “Units”) in GAIF I

have no rights to participate in the management of the Fund. Units are sold through dealers that are not affiliated with the Fund or the Manager.

Pursuant to the Company Agreement, GAIF I’s term will end upon the first to occur of the following:

| • |

December 31, 2050;

|

| • |

the withdrawal (voluntary or involuntary), bankruptcy or an assignment for the benefit of creditors or dissolution of the Manager; or

|

| • |

any date prior to December 31, 2050 on which the Manager elects to dissolve GAIF I.

|

GAIF I’s business constitutes only one segment for financial reporting purposes (i.e., a speculative commodity pool). GAIF I does not engage in sales of goods or services.

As of February 29, 2020, the aggregate Net Asset Value (as defined below under “Allocation of Profit and Loss”) of the Units in GAIF I was $25,612,671. GAIF I operates on a

calendar fiscal year.

Narrative Description of Business

| (i) |

General

|

GAIF I offers two classes (each a “Class”) of Units, being Class 0 Units and Class 2 Units of the Blended Strategies Portfolio. As further described below under “Fees,” Class 0

and Class 2 Units of the portfolio differ only as to their applicable fees. Subscriptions for Units of any Class may be accepted by GAIF I as of the first business day of each month upon written notice of at least three business days prior to the

last business day of the preceding month, and on such other notice and dates as the Manager may permit in its sole and absolute discretion.

Units of each Class are offered at their Net Asset Value per Unit as of the end of each month. The minimum initial investment for Class 0 Units is $10,000 (this Class is

primarily for “wrap fee programs”) and the minimum additional investment is $5,000. Wrap fee programs bundle the various services provided to a client by a broker or financial advisor in a single fee arrangement rather than charging the client fees

for specific transactions. The minimum initial investment for Class 2 Units is $10,000 and the minimum additional investment is $5,000. GAIF I will be continuously offered and has no limit on the maximum aggregate amount of subscriptions that may

be contributed to it.

4

Capital contributions by a single subscriber for any Class of Units, upon acceptance of the subscriber as a member, represent a single interest in GAIF I for that subscriber’s

respective Class of Units. A Unit of each Class reflects a member’s interest in GAIF I’s member’s capital with respect to the Class of Units owned by the member. Although separate Classes of Units in a portfolio are offered, all capital contributions

to a particular portfolio are pooled by GAIF I and invested in GAIT. Units may be purchased only by investors who qualify as accredited investors under Regulation D of the Securities Act of 1933 (“Securities Act”). The principal differences among the

separate Classes of Units within the same portfolio are their fees. Holders of Units, regardless of which Class of a portfolio they hold, participate pro rata in the profits and losses of that portfolio in proportion to the Net Asset Value of the

Class and have identical rights, as members, under the Company Agreement.

5

|

ii)

|

The Manager

|

The Manager was organized in May 1994 as a Delaware limited partnership. The general partner of the Manager is KGT, Inc., a Delaware corporation of which Kenneth G.

Tropin is the sole director and sole shareholder. KGT, Inc. became a listed Principal of the Manager effective July 27, 1994. The Manager has been registered as a CPO and CTA under the Commodity Exchange Act (“CEA”) and has been a member of the

NFA since July 27, 1994 and has been registered as an investment adviser with the Securities and Exchange Commission since March 20, 2012. As of March 1, 2021, the Manager has approximately 172 personnel and manages assets of over $16.4 billion.

The Manager’s principal office is located at 40 Highland Avenue, Rowayton, Connecticut 06853 and its telephone number is (203) 899-3400. The Manager’s advisory services may in part be performed out of its branch office in West Palm Beach,

Florida and the office of the Manager’s London affiliate, Graham Capital LLP.

|

(iii)

|

The Trading Program

|

The Manager’s Investment Committee, which is comprised of Kenneth G. Tropin, Pablo Calderini, Robert E. Murray, Brian Douglas, Barry S. Fox, James A. Medeiros, William Pertusi,

Christopher McCann, Timothy Sperry, Isaac Finkle, Ed Tricker, Kelly Tropin, and George Schrade makes decisions with respect to the selection of strategies traded on behalf of the Fund.

Biographical information regarding the members of the Investment Committee as of December 31, 2020 is set forth below.

Kenneth G. Tropin, 67, is the Chairman and the founder of the Manager. In May 1994, he founded the Manager and

became an Associated Person and Principal effective July 27, 1994. Mr. Tropin developed the firm's original trading programs and is responsible for the overall management of the organization, including the

investment of its proprietary trading capital.

Pablo Calderini, 56, is the President and Chief Investment Officer of the Manager and, among other things, is responsible for the

management and oversight of the discretionary and systematic trading businesses at the Manager. He joined the Manager in August 2010 and became an Associated Person and Principal of the Manager effective August 13, 2010. Mr. Calderini received a B.A.

in Economics from Universidad Nacional de Rosario in 1987 and a Masters in Economics from Universidad del Cema in 1988, each in Argentina.

Robert E. Murray, 60, is the Vice Chairman of the Manager and serves as a member of the Manager’s executive leadership team responsible

for the management of the firm and oversees important business and strategic initiatives of the Manager. He joined the Manager in June 2003 and became an Associated Person and Principal of the Manager effective June 27, 2003. Mr. Murray received

a Bachelor’s Degree in Business with a Finance concentration from Geneseo State University in 1983.

James A. Medeiros, 47, is Chief Executive Officer of the Manager responsible for the management and oversight of the firm's investor

relations, risk management and technology infrastructure and development efforts at the Manager. He joined the Manager in July 2009 and became an Associated Person of the Manager effective July 21, 2009 and a Principal on February 7, 2013. Mr.

Medeiros received a Bachelor of Science from the Edmund A. Walsh School of Foreign Service at Georgetown University in 1996 and received an M.B.A. from the Wharton School at the University of Pennsylvania in 2003.

Brian Douglas, 47, C.P.A., is the Chief Operating Officer of the Manager and oversees the operation of the trading services, legal, compliance, facilities and administration departments of the Manager. He became an Associated Person of the Manager effective February 1, 2013 and a Principal on

April 1, 2013. In July 2004, he joined the Manager as Manager of Financial Reporting and became Chief Financial Officer in April 2013 and Chief Operating Officer in March 2019. Mr. Douglas received a B.A. in accounting from Western Connecticut State

University in May 1996.

George Schrade, 46, C.P.A., is the Chief Financial Officer of the Manager and is responsible for the finance

department of the Manager. He joined the Manager in June 2007 and became an Associated Person of the Manager effective December 21, 2016 and a Principal on February 28, 2019. Mr. Schrade received a B.S in Accounting from Quinnipiac University in May

1996.

Isaac Finkle, 68, is Chief Legal Officer of the Manager. He joined the Manager in May 2003 and

became an Associated Person of the Manager effective April 16, 2004 and a Principal on June 5, 2007. Mr. Finkle received a J.D. from New York University School of Law in 1985, a Ph.D. from the University of Pennsylvania in 1998 specializing in

sociological theory, and a B.A. with honors in philosophy from Haverford College in 1973.

6

Barry S. Fox, 57, is Managing Director of Quantitative Operations and Execution of the Manager. He became an Associated Person of the Manager effective November 10, 2000 and a Principal on November 15, 2007. Mr. Fox joined the Manager in

August 2000. Mr. Fox received a B.S. in Business Administration from State University of New York at Buffalo in 1986.

William Pertusi, 60, is the Co-Chief Risk Officer of the Manager, responsible for identifying, monitoring and acting upon financial risks relative to financial returns in the Manager’s diverse trading strategies. He became an

Associated Person of the Manager effective July 24, 2006 and a Principal on November 28, 2006. Mr. Pertusi received a B.S. in Electrical Engineering from Lehigh University in 1983, an M.B.A. from Harvard in 1987, and an M.S. in Mathematics from

Fairfield University in 2006.

Christopher McCann, 50, is the Chief Risk Officer of the Manager, responsible for identifying, monitoring and

acting upon financial risks relative to financial returns in Manager's diverse trading strategies. He became an Associated Person of the Manager effective May 29, 2009 and a Principal effective June 24, 2019. He was previously registered as a

Principal of the Manager effective September 12, 2012 through February 22, 2016. Mr. McCann received an M.B.A. in Finance from New York University Stern School of Business in May 1998, a M.S. in Industrial Engineering from Rutgers University in

May 1995, and a B.S. in Chemical Engineering from Washington University in May 1992.

Tim Sperry, 53, is Executive Director and Chief Compliance Officer of the Manager. He joined the Manager in June 2004. He became an Associated Person of the

Manager effective October 9, 2012 and a Principal on October 10, 2012. As Chief Compliance Officer, he oversees compliance and regulatory matters related to the firm’s business. Mr. Sperry received a J.D. from New England School of Law in May 1998

and a B.A. in Political Science in 1989 from Boston University.

Edward Tricker, 37, is Chief Investment Officer of Quantitative Strategies of the Manager and is responsible for the

management and oversight of the firm's Quantitative Strategies team, including quantitative operations and execution, research, alpha technology, and data science. He became an Associated Person of the Manager effective February 4, 2013 and a

Principal on April 30, 2014. Mr. Tricker received a Ph.D. in Statistics from Imperial College of Science and Technology in London in October 2009 and a B.S. in Mathematics and Statistics from the University of Oxford in June 2005.

Kelly Tropin, 30, is Chief Economist and Senior Managing Director of the Manager and is responsible for leading the firm’s economic research efforts in

addition to playing a key role in the management of the firm’s discretionary trading team. She became an Associated Person and Principal of the Manager effective September 6, 2018. Ms. Tropin received a Bachelor of Arts in Government from Dartmouth

College in June 2013.

Jennifer Ancker Whelen, 47, is Chief Client Officer, Co-Head of Institutional Relations, and Managing Director of GCM. She became an Associated Person of GCM

effective June 6, 2007 and a Principal January 15, 2021. Mrs. Ancker Whelen is responsible for the development of strategic relationships with GCM’s global client base, including consultants and institutional investors. Prior to joining GCM in April

2007, Mrs. Ancker Whelen was Principal and Director of Marketing & Investor Relations at Stadia Capital, LLC, a long/short equity hedge fund. Mrs. Ancker Whelen graduated cum laude from Colby College in 1995 with a B.A. in Economics and a minor

in Sociology.

On February 6, 2020, William Pertusi, Co-Chief Risk Officer, resigned from the Manager in connection with his retirement. Upon Mr. Pertusi’s resignation, Christopher McCann

assumed the position of sole Chief Risk Officer of the Manager. On March 2, 2020, Isaac Finkle, Chief Legal Officer, resigned from the Manager in connection with his retirement. Upon Mr. Finkle’s resignation, Jason Slutsky assumed the position of

Chief Legal Officer of the Manager. On February 12, 2021, Robert Murray, Vice Chairman, resigned from the Manager in connection with his retirement. Jennifer Ancker Whelen became a member of the Investment Committee effective February 2021.

The discretionary traders for any discretionary investment strategy selected to trade on behalf of the Fund make the trading decisions for that discretionary

strategy. The Manager has developed sophisticated proprietary software to study optimal portfolio weighting strategies and the effect of specific markets on the performance, risk, correlation and volatility characteristics of each of its trading

strategies. As a result, the weighting or leverage that a trading strategy uses in each market may change to address changes in market conditions. With such software, the Manager devotes considerable attention to risk management at the portfolio

level in an effort to ensure balance between markets and that the overall leverage used by the portfolio is consistent with the Manager’s overall views on risk. The Manager’s objective in forming the investment program of the portfolio is to

provide the portfolio with significant potential for capital appreciation in both rising and falling markets and during expanding or recessionary economic cycles. Currently, 50% of the assets of the Blended Strategies Portfolio are

allocated to trading the Manager’s Discretionary Trading Program and 50% of the assets are allocated to trading to the Manager’s K4D-15V Program, but the Manager may alter these allocations at any time within its sole discretion.

7

The Fund will trade actively in both U.S. and foreign markets, primarily on major futures exchanges as well as the inter-bank cash currency and swaps markets. The Fund also

engages in exchange for physical (EFP) transactions, which involve a privately negotiated and simultaneous exchange of a futures position for a corresponding position in the underlying physical commodity, and the Fund may use other derivatives in

addition to swaps. The Manager may also trade other financial instruments as it endeavors to achieve superior results for investors and enhanced portfolio diversification. The Manager reserves the right in extraordinary market conditions to reduce

leverage and portfolio risk if it feels in its sole discretion that it is in the potential best interest of the Fund. While such actions are anticipated to occur very infrequently, no assurance can be given that the Manager’s actions will enhance

performance or that any efforts by the Manager to achieve portfolio diversification will be successful.

The Manager expects to add additional trading strategies and programs to the portfolio and to modify the strategies currently in use for the portfolio over time

and may in the future offer other portfolios. There is no maximum number of strategies and programs that the Manager may see fit to include in the Fund or the portfolio, and the Manager may increase or decrease the

number of strategies and programs included in the Fund or the portfolio over time or increase the number of markets or contracts that are traded on behalf of the Fund or the portfolio. The Manager may make such additions or deletions of trading

programs to the Fund or the portfolio at any time and may make such additions, deletions or any other changes, such as changes in the leverage of, or in the asset allocations to, any of the Fund’s trading strategies and programs, in its sole

discretion and without prior notice to members.

The Manager conducts risk analysis and employs risk management controls at various levels of the Fund, including portfolio risk, strategy risk, market risk and execution risk.

The objectives of its risk management approach are to measure a Portfolio’s quantitative and qualitative exposures to the risks identified; formulate appropriate policies and procedures in an effort prudently to manage overall risk; monitor

compliance with the Manager’s risk policies and procedures; and report identified and measured risks to the Manager’s Risk Committee.

In constructing a Portfolio, the Manager employs various risk management protocols. Using a proprietary asset allocation model, the Manager’s Investment Committee determines the

appropriate strategies for a Portfolio and the weighting of each in the Portfolio. At the individual strategy level, the Manager works closely with each discretionary trader to design an appropriate investment profile, including return objective and

volatility level, for each individual trading strategy. Through continuous monitoring and an active dialogue with every discretionary trader, the Manager seeks to identify and minimize any deviations from the investment profile. In addition, the

Manager has implemented a uniform set of risk guidelines for all discretionary traders designed to reduce a strategy’s downside risk. The Manager has developed a trade execution and reporting infrastructure designed to minimize the risk of errors.

For example, where appropriate, trades are manually checked for accuracy by the Manager’s middle office staff and are subject to additional cross checking using computerized means. Each discretionary trader’s positions must adhere to established risk

management guidelines and position limits, which are regularly monitored by the Manager’s risk management team.

Effective testing, reporting and review are critical elements of the Manager’s risk management process. Daily stress testing is performed to evaluate a strategy’s risk exposure.

Daily reporting of Value-at-Risk (VaR), plus intraday reporting of net gains or losses for each strategy enables the risk management team and the Investment Committee to observe the strategy’s adherence to its investment profile as well as market

exposure. VaR is a probabilistic measure of the amount of loss, often referred to as the threshold, that a portfolio of investments will experience over a specified time period. Finally, each strategy is formally reviewed by the Investment Committee

on a monthly basis.

To manage risk the Manager limits the size and structure of positions taken on behalf of the Fund so that they comply with various risk parameters, both those defined by the

Manager and those defined by each of the individual discretionary traders for the Fund’s underlying trading strategies.

8

The Manager subjects the trading of all its discretionary traders to a risk monitoring regime that includes a set of defined drawdown limits and a series of risk measurements.

Drawdown limits are used as a risk management tool to enforce risk reduction on a discretionary strategy if the discretionary trader is experiencing losses and has not yet reduced overall risk levels. The Manager generally defines a drawdown as

losses experienced over a specified period of time, expressed as a percentage of net assets at the beginning of the period. The Manager imposes daily, monthly, and overall drawdown limits for all discretionary traders. There is a daily move that

requires a prompt report to the risk manager, a monthly peak to trough drawdown that likely leads to risk reduction, and a total peak to trough drawdown that likely leads to risk reduction. There is also a drawdown limit where the Manager’s

Investment Committee would meet to consider closing a given program. Further, the Manager conducts a daily risk process measuring VaR and reviewing stress tests for the portfolio. The Manager evaluates the validity of VaR as a risk management tool by

comparing the number of instances that profit and loss exceeded expected parameters over various time frames. For example, the Manager utilizes a one day 97.5% VaR, which means that in respect of the Portfolio that it is analyzing it expects the

Portfolio to experience a loss in excess of VaR on approximately 1 out of every 40 days. In addition, the Manager runs an extensive series of stress tests, including historical scenarios as well as specific foreign exchange, equity and interest rate

shocks.

In addition to the risk monitoring procedures employed by the Manager, each discretionary trader trading on behalf of a discretionary program for the Fund has established his own

proprietary risk measures and parameters. These generally include measures of first order sensitivities (i.e., the sensitivity of the Portfolio to a change in a parameter of the underlying instruments) to the most relevant risk factors for a given

book (for example dollar value of a basis point in the case of interest rate products), measurement of stress loss in extreme market events, or the use of explicit stop loss points. When individual limits on any of these are breached, the

discretionary trader likely will reduce risk even if within the Manager’s guidelines.

The Fund currently employs a master-feeder structure for its individual trading programs such that the portfolio’s trading program may, but will not necessarily in

all cases, be conducted through one or more master funds. Each of the master funds is managed by one or more employees of the Manager. The master funds were organized by the Manager in order to facilitate the management of various funds

and accounts managed by the Manager using in whole or in part the same trading program. The Fund, alternatively, may trade its individual trading programs through one or more managed accounts in the Fund’s name.

Discretionary Trading Program

The Manager has been trading discretionary programs since February 1998. Discretionary programs, unlike systematic programs which are based almost entirely on computerized

mathematical models, determine trades subjectively on the basis of a trader’s personal assessment of trading data and trading experience. Although the Manager has had over a decade of experience trading various discretionary programs, Discretionary

Trading Program (“DTP”) itself commenced trading as of August 2008. DTP seeks to invest in various global macro markets that are highly liquid. DTP consists of several of the Manager’s leading discretionary strategies traded by employees of the

Manager that focus on the global fixed income, stock index, currency, energy, commodity and metals markets, but over time it may participate in any other liquid market that is available as the Manager deems appropriate.

The Manager’s discretionary programs have generally displayed a significant degree of non-correlation with traditional and other alternative investments, including with the

Manager’s own quantitative investment programs. In its composition of DTP, the Manager will seek an investment portfolio that continues to offer such non-correlation and that provides diversification to other investments. DTP may take both long and

short positions and thus may generate successful performance results in both rising and declining markets. The holding periods of its positions may range, depending on the individual trading strategies, from just a few hours to months, such that DTP

may potentially profit in markets that exhibit either short-term moves or long-term trends. As with its systematic investment programs, the Manager may add or delete trading strategies or trading markets in DTP or alter their individual weightings or

leverage as it deems appropriate, and no notice will be given to investors of such allocation changes; in addition, discretionary strategies that have previously traded on behalf of the Fund may be included in DTP. The Manager may make such

allocation changes based on a proprietary allocation model, its assessment of market conditions or the availability of additional discretionary trading strategies, in its discretion.

The descriptions contained herein of DTP should not be understood as in any way limiting its investment activities. In addition, the Fund may engage in investment strategies and

programs not described herein that the Manager considers appropriate.

9

Systematic Trading Program

The Manager’s systematic investment programs employ various quantitatively based systems that are designed to participate selectively in potential profit

opportunities that can occur in a diverse number of U.S. and international markets. Such systems generally are based on computerized mathematical models and can rely both on technical (i.e., historic price and volume data) and fundamental (i.e.,

general economic, interest rate and industrial production data) information as the basis for their trading decisions. The systems establish positions in markets where the price action of a particular market signals the computerized systems used by

the Manager that a potential move in prices is occurring. The systems are designed to analyze mathematically the recent trading characteristics of each market and to statistically compare such characteristics to the historical trading patterns of

the particular market. The systems also employ proprietary risk management and trade filter strategies that seek to benefit from price moves while reducing risk

and volatility exposure.

Each systematic investment program of the Manager incorporates trading strategies developed by the Manager’s research department. While the Manager’s systematic investment

programs have employed long-term systematic strategies from their inception, the programs may also include trend systems with varying time horizons.

The Manager believes strongly in the importance of research and development of new trading strategies and expects to develop additional trading systems and strategies and to modify the systems

currently in use in its systematic programs over time in its ongoing efforts to keep pace with changing market conditions. The decision to add or subtract systems or strategies from any investment program or to change the leverage of, or the asset

allocations to, any of the trading strategies of such investment program shall be at the Manager’s sole discretion. The Manager anticipates that the constellation of trading strategies comprising the K4D-15V program will continue to grow and evolve

over time. There is no maximum number of strategies that the Manager may include in the K4D-15V investment program.

In connection with its programs’ systematic trading, the Manager may employ discretion in determining the leverage and timing of trades for new accounts and the market weighting

and participation. In unusual or emergency market conditions, the Manager may also utilize discretion in establishing positions or liquidating positions or otherwise reducing portfolio risk where the Manager believes, in its sole discretion, that it

is in the potential best interest of the Fund to do so. While such actions are anticipated to occur very infrequently, no assurance can be given that the Manager’s discretionary actions in these programs will enhance performance.

The K4D-15V Program features the first system that the Manager developed, which began trading client accounts in 1995. It utilizes multiple computerized trading models and

offers broad diversification in both financial and non-financial markets, trading in approximately 80-90 global markets. The K4D-15V Program’s legacy trend system is primarily long-term in nature, but the program also includes short-term and

intermediate trend-following as well carry, fundamental macro, momentum, value/reversion and other diversifying strategies, and is intended to generate significant returns over time with an acceptable degree of risk and volatility. The computer

models on a daily basis analyze the recent price action, the relative strength and the risk characteristics of each market and compare statistically the quantitative results of this data to years of historical data on each market.

The investment objectives and methods summarized above represent the Manager’s current intentions. Depending on conditions in the financial and securities markets and the

economy in general, the Manager may pursue other objectives, employ other investment techniques or purchase any type of financial instrument that it considers appropriate and in the best interests of the Fund, whether or not described in this

section.

| (iv) |

Use of Proceeds

|

Northern Trust International Banking Corporation serves as the Fund’s banker for purposes of receiving subscription funds, disbursing redemption payments and processing cash

transactions not directly related to the Fund’s portfolio.

Bank of America, N.A. serves as the Fund’s banker for transactions on behalf of the portfolio. A significant portion of the Fund’s assets may be held by Bank of America, N.A. in

addition to the futures clearing brokers utilized on behalf of the Fund as well as OTC counterparties. The Fund may also hold excess funds not required for trading in bank accounts at Bank of America, N.A. or elsewhere. The Manager, in its

discretion, may change the brokerage and custodial arrangements described herein without notice to investors.

10

GAIF I currently has no direct arrangement with any futures commission broker; rather each master fund that trades on behalf of the Fund may have its separate clearing

arrangements with a futures broker. At present, Credit Suisse Securities (USA) LLC, BofA Securities Inc., and Barclays Capital Inc. are the primary futures clearing brokers for the master funds, but neither the Fund nor the master funds are required

or under any contractual obligation to continue to employ them as futures clearing brokers (together with additional or replacement clearing brokers the Manager may select from time to time without notice to investors, the “Futures Brokers”). The

Manager is authorized to determine the Futures Brokers (or the counterparty, if concerning a foreign currency or swap transaction) to be used for the portfolio transactions for the Fund. The Manager is not affiliated with any futures commission

merchant or broker-dealer.

Each Futures Broker will obtain, safe-keep and maintain custody of all of the Fund’s fully paid assets held by it in a customer account identified on the books of the Futures

Broker as belonging to the Fund and segregated from the broker’s own proprietary positions. All of the Fund’s assets, funds, securities and other property held by each Futures Broker are held as security or collateral for the Fund’s obligations to

the broker. The margin levels required to initiate or maintain open positions are established from time to time by each Futures Broker and applicable regulatory authorities. Each Futures Broker may close out positions, purchase securities, or cancel

orders for the Fund’s account at any time it deems necessary for its protection, generally without the consent of or notice to the Fund.

Agreements with Futures Brokers in general provide that the broker will not be liable in connection with the execution, clearing, handling, purchasing, or selling of commodities,

or other property, or other action, except for negligence or misconduct on the broker’s part. Such agreements also may provide that the Futures Broker will be indemnified and held harmless by the Fund from and against any loss, claim, or expense

(including attorney’s fees) incurred by the broker in connection with it acting or declining to act for the Fund, and that the Fund will fully reimburse the broker for any legal or other expenses (including the cost of any investigation and

preparation) which the broker may incur in connection with any claim, action, proceeding, or investigation arising out of or in connection with the agreement or the transactions contemplated thereunder.

In addition to trading in the Interbank market for foreign exchange, the Fund currently trades on all the major U.S. futures exchanges and may also trade on, but is not limited

to, the following foreign exchanges:

ASX Trade24

Bolsa de Mercadorias and Futuros

Borsa Italiana (IDEM)

Eurex Exchange

EURONEXT/London International Financial Futures and Options Exchange

EURONEXT/Paris MONEP

European Options Exchange

Hong Kong Exchanges and Clearing Ltd.

ICE Futures Canada

Intercontinental Exchange

Korea Futures Exchange

London Metal Exchange Ltd.

Montreal Exchange

OMX Nordic Exchange Stockholm

Osaka Securities Exchange

Singapore Exchange Ltd.

South African Exchange

Stockholm Stock Exchange

Tokyo Commodity Exchange

Tokyo Financial Exchange

Tokyo Stock Exchange

Turkish Derivatives Exchange

In connection with such trading on foreign exchanges, the Fund’s assets may be deposited by the futures brokers with foreign brokers or banks. Although these foreign brokers or

banks are subject to local regulation in their jurisdiction, the protections afforded by foreign regulatory bodies and rules may differ significantly from those afforded by United States regulators and rules.

11

The Fund earns interest on cash not required to be posted as margin for its trading. Cash not required by the Fund’s investment programs for trading is currently invested by the

Manager in a separate cash management master fund, Graham Cash Assets LLC (“Cash Assets”), managed by the Manager. The Fund pays the Manager no additional fees for managing the Fund’s assets invested in Cash Assets. It is currently anticipated that

on average between 70% and 90% of the assets of the portfolio will be invested in Cash Assets. Various investment funds managed by the Manager and other entities affiliated with the Manager may invest in Cash Assets and each such entity bears its

proportional share of the operating expenses of Cash Assets. Cash Assets may pay some third-party fees to unaffiliated custodians or managers in connection with the management of its portfolio, which fees will effectively be borne pro rata by all

investment vehicles that invest in Cash Assets. Cash Assets may deposit a portion of its assets in an interest bearing bank account with Bank of America N.A. or other banks or in brokerage accounts, or it may purchase securities which are direct

obligations of or obligations guaranteed as to principal or interest by the United States (e.g. U. S. Treasury Bills or Bonds), or other securities issued or guaranteed by corporations in which the United States has a direct or indirect interest

(e.g., U.S. government agency securities) which have been designated pursuant to section 3(a)(12) of the Securities Exchange Act of 1934 as exempted securities.

In addition to exchange-traded futures contracts and swaps, the Fund trades spot and forward contracts on foreign currencies and, to a lesser degree, OTC swap and derivatives

contracts, currently the only non-CFTC regulated instruments the Fund anticipates trading. The Manager estimates that 20-60% of the Fund’s trades for the portfolio may be in forward contracts and 5-15% in swap contracts, but depending on market

conditions, the percentage of the portfolio’s trades constituted by forward or swap contracts may fall substantially outside that range. Bank of America, N.A. and Barclays currently serve as the Fund’s primary counterparties for foreign currency

forward transactions. All of the Fund’s assets, funds, securities, and other property held by Bank of America, N.A. or Barclays as a Fund counterparty, and any other bank or broker-dealer acting as a foreign currency forward counterparty or OTC swap

counterparty of the Fund are held as security or collateral for the Fund’s obligations to such entity. As the forward and OTC swap markets currently are unregulated, the Fund bears additional risks (e.g., the credit risk of trading with

counterparties) not present in exchange-traded futures and swaps trading. Under the Dodd–Frank Wall Street Reform and Consumer Protection Act, the CFTC, sometimes together with the SEC, has enacted regulations to govern these contracts and requires

many of them to be cleared through an exchange or clearinghouse.

The Manager determines, in its sole and absolute discretion, the amount of distributions, if any, to be made by the Fund. It is expected that dividends ordinarily will not be

paid and that all portfolio earnings will be retained for reinvestment (subject to the redemption privilege).

Fees

| (i) |

Advisory Fee

|

Pursuant to the Company Agreement, each Class of the Blended Strategies Portfolio of the Fund paid the Manager an advisory fee (the “Advisory Fee”) at an aggregate

annual rate equal to 1.50% of the Net Asset Value of such Class. For purposes of calculating the Advisory Fee, the Net Asset Value of each Class equals the total fair market value of the assets of the Fund attributable to that Class less the

liabilities of the Fund attributable to that Class. Profits and losses are allocated among the Classes in proportion to their respective Net Asset Values (before accrual of the Sponsor Fee and the Incentive Allocation set forth below). The

Advisory Fee is payable monthly in arrears calculated as of the last business day of each month (before giving effect to any redemptions as of the last business day of the month and subscriptions as of the beginning of the next business day, and

before deduction or accrual of fees payable to the Manager and the Incentive Allocation). A portion of the Advisory Fee may be paid to third parties as compensation for offering or selling activities in connection with the Fund. If the Company Agreement is terminated as of a date other than the last business day of a month, the Advisory Fee will be prorated through the termination date.

|

(ii)

|

Sponsor Fee

|

Each Class 0 and Class 2 of the Fund pays the Manager a sponsor fee (the “Sponsor Fee”) at an annual rate of the Members’ Capital specified in the table below. The Sponsor Fee, in each case payable

monthly in arrears, determined in the same manner as the Advisory Fee.

|

Class 0

|

Class 2

|

|

0.50%

|

1.25%

|

12

A significant portion of the Sponsor Fees is paid to third parties as compensation for offering or selling activities in connection with the Fund. The Manager may pay initial service fees as well as

on-going service fees to its selling agents. When an initial service fee is paid, the on-going service fee to a selling agent will generally commence the 13th month with respect to which the Fund investor of such selling agent has been

invested in the Fund. The service fees paid by the Manager to selling agents range up to 2% of net assets with respect to Class 2 investors.

| (iii) |

Incentive Allocation

|

Each Class of the Blended Strategies Portfolio bears a quarterly Incentive Allocation, payable to the Manager as of the end of each calendar quarter, equal to 20% of the net

profits of the Class for the quarter, subject to a “loss carryforward” provision. The loss carryforward provision generally provides that the Manager will not receive an Incentive Allocation in respect of the Class for a calendar quarter to the

extent that the Class experiences net loss since the last calendar quarter for which an Incentive Allocation was earned and such loss has not been recouped through subsequent net profits. The Incentive Allocation is calculated and paid as follows:

At the end of each calendar quarter, the Incentive Allocation is deducted from the Net Asset Value of each Class and credited to the Capital Account of the Manager in the Feeder Funds, in an amount equal to 20% of New High Net Trading Profits (as

defined below) with respect to each class of the Blended Strategies Portfolio for such period. “New High Net Trading Profits” for any Class for any quarter shall mean the Net Capital Appreciation (which includes unrealized gains and losses and

interest income and expense, less all accrued debts, liabilities and obligations of the Class (but before any accrual for the Incentive Allocation) for such period) for the quarter minus the Carryforward Loss (as defined below), if any, as of the

beginning of the quarter, for such Class. The “Carryforward Loss” shall be increased as of the end of each calendar quarter by the amount of any Net Capital Depreciation with respect to such Class during the quarter then ended and shall be decreased

(but not below zero) as of the end of each calendar quarter by the amount of any Net Capital Appreciation with respect to such Class during the quarter then ended. In addition, the Carryforward Loss for a Class for any calendar quarter shall be

proportionately reduced effective as of the date of redemption of any Units of such Class by multiplying (i) the Carryforward Loss for such Class immediately prior to such redemption by (ii) the ratio that the amount of assets redeemed from such

Class bears to the Net Assets of such Class immediately prior to such redemption. The Carryforward Loss of a Class must be recouped before any subsequent Incentive Allocation can be made to the Manager. The Incentive Allocation is also accrued and

allocable on the date of redemption with respect to any Units that are redeemed on any date not the end of a calendar quarter, as if the date of redemption were the end of a calendar quarter and the Incentive Allocation shall only be deducted with

respect to such redeemed Units.

A portion of any of the above fees (including the Incentive Allocation) may be paid by the Manager to third parties as compensation for offering or selling activities in

connection with the Fund.

Expenses

Each Class of the Fund is responsible for its proportionate share of the Fund’s operating, administrative, trading and other direct expenses of the relevant

Portfolio, including all trading commissions (including exchange and clearing and regulatory fees relating to its trades), legal expenses, internal and external accounting,

audit and tax preparation expenses, fees and expenses of an Administrator, costs of preparing any required regulatory filings, and printing and mailing costs, together with a proportionate share of the costs incurred in connection with the

organization of the Fund (including government incorporation charges and professional fees and expenses in connection with the preparation of the Fund’s offering documents and the preparation of the basic corporate and contract documents of the

Fund) and the Fund’s continuing offering of Units. The Fund’s operating, administrative and trading expenses are estimated, based on recent experience, to amount to approximately 1.00% of net assets annually for the Blended Strategies

Portfolio. These expenses will be calculated and payable monthly in arrears in the same manner as the Advisory Fee.

The Manager provides and pays for its own professional and administrative staff, office space, business equipment and facilities and other general overhead expenses incidental to

its advisory services.

Taxes, interest and other expenses related to borrowing, extraordinary expenses of the Fund, such as litigation expenses, or any other fees or expenses not described above in the

section “Fees,” will also be separately borne by the Fund. All fees and expenses of the Fund (including the Incentive Allocation) will be assessed at the Feeder Fund level.

13

Each investor should understand that the costs of the Fund’s operating, administrative and operational expenses may vary, and that these costs (including the costs described above) are no longer

capped and may be higher than the above estimated amounts. The Fund makes no representation that in the future these expenses may not increase and may not exceed these estimates.

Allocation of Profit and Loss

A separate Capital Account is maintained for each member with respect to each Class of Units held by such member. The initial balance of each Capital Account of each member will

equal the net initial contribution to the Fund by such member with respect to the Class to which such Capital Account relates. Each Capital Account of each member is increased by any additional capital contributions by such member with respect to the

Class to which such Capital Account relates and decreased by any redemptions of Units of such Class by such member. Net realized and unrealized appreciation or depreciation in the value of assets of the portfolio of the Fund, including investment

income and expenses, is allocated at the end of each fiscal period among the Capital Accounts of the members in proportion to the relative values of such Capital Accounts as of the commencement of such fiscal period (in the case of any month end that

is not also the end of a calendar year, before any accrual for the Incentive Allocation).

On the last day of each fiscal period, an allocation is made of the net profit or net loss attributable to the investments of the portfolio for such fiscal period. The net profit

or net loss for a fiscal period is allocated among all the Classes of the portfolio pro rata in the proportion that the Net Asset Value of each Class as of the date of the commencement of such fiscal period bears to the Net Asset Value of the

portfolio as of such date.

The Net Asset Value of each Class means the total value of the Fund’s assets, at fair value, attributable to that Class less the liabilities of the Fund attributable to that

Class. The Net Asset Value per Unit of any Class is determined as of the close of business on the last business day of the month (a “Valuation Day”) by dividing the Net Asset Value of that Class by the number of outstanding Units of that Class. Such

deductions will include an accrual for the Incentive Allocation and the fees to be paid to the Manager.

The net profit or net loss of each Class for a fiscal period in turn is allocated among all holders of Units of that Class pro rata in the proportion that the Net Asset Value of

each member’s holding of Units of that Class as of the date of the commencement of such fiscal period (after adjustment for any contributions to the capital of the Fund which are effective on such date) bears to the aggregate Net Asset Value of that

Class as of such date.

The Manager is responsible for determining the value of the Fund’s assets. The Fund has appointed SEI Global Services Inc. as the Fund’s independent administrator

(“Administrator”), and in connection with that role SEI is responsible, subject to the ultimate supervision of the Manager, for calculating the Net Asset Value of the Fund and the Net Asset Value per Unit of each Class of Units. In determining the

Net Asset Value of the Fund and the Net Asset Value per Unit of each Class of Units, the Administrator will follow the valuation policies and procedures adopted by the Fund as set out below. If the Manager is involved in the pricing of any of the

Fund’s portfolio assets, the Administrator may accept, use and rely on such prices in determining the Net Asset Value of the Fund and shall not be liable to the Fund, any investor in the Fund, the Manager or any other person in so doing.

For all purposes, including subscriptions, redemptions and the calculation of the fees paid to the Manager, the Manager shall determine the fair market value of any investment

made by the Fund. In general, investments will be valued as follows:

| a. |

The value of unrealized appreciation or depreciation on open futures contracts shall be recorded as the difference between the contract price on the trade date and the closing price reported as of the Valuation

Day on the primary exchange on which such contracts are traded.

|

| b. |

The value of any option listed or traded on any recognized foreign or U.S. exchange shall be the settlement price published by the principal exchange on which it is traded on the relevant Valuation Day. If the

recognized foreign or U.S. exchange does not publish a settlement price, the value of any option shall be the last reported sale price on the relevant Valuation Day on the principal exchange on which such option is traded. If no such sale of

such option was reported on that date, the market value shall be the average of the last reported bid and asked price. The market value of any over-the-counter option for which representative broker’s quotations are available shall be

determined in like manner by reference to the last reported sale price, or, if none is available, to the average of the last reported bid and asked quotation. Premiums for the sale of such options written by the Fund shall be included in the

assets of the portfolio, and the market value of such options shall be included as a liability.

|

14

| c. |

The value of any U.S. government security shall be the cost of such security plus accrued interest, discount and amortization of premium.

|

The fair value of any assets not referred to in clauses (a) through (c) above (or the valuation of any assets referred to therein in the event that the Manager shall determine

that there is no active market or that another method of valuation is advisable in the circumstances) shall be determined by or pursuant to the direction of the Manager. Prospective investors should be aware that situations involving uncertainties as

to the valuation of portfolio positions could have an adverse effect on Net Asset Value if management’s judgments regarding appropriate valuations should prove incorrect. Absent bad faith or manifest error, the Fund’s Net Asset Value determinations

are conclusive and binding on all investors. Net Asset Values are expressed in U.S. dollars, and any items denominated in other currencies are translated at prevailing exchange rates as determined by the Administrator in consultation with the

Manager.

The Manager may, in its sole and absolute discretion, permit any other method of valuation to be used if it considers that such method of valuation better reflects fair value and

is in accordance with good accounting practice.

Reporting

The Fund is required to furnish audited annual reports to its members containing financial statements examined by the Fund’s independent registered public accounting firm. The

Fund is also required to provide members with monthly performance updates and monthly unaudited financial statements.

Regulation

The Manager has been registered as a CPO and CTA under the CEA, and as an investment adviser with the Securities and Exchange Commission and has been a member of the NFA since

July 27, 1994. GAIF I is regulated as a commodity pool by the CFTC and NFA.

The CFTC may suspend a CPO’s or CTA’s registration if it finds that its trading practices tend to disrupt orderly market conditions or in certain other situations. In the event

that the registration of the Manager was terminated or suspended, the Manager would be unable to continue to manage the business of the Fund. Should the Manager’s registration be suspended, termination of GAIF I might result. In addition to such

registration requirements, the CFTC and certain commodity exchanges have established limits on the maximum net long or net short positions that any person may hold or control in particular commodities. Most exchanges also limit the changes in

futures contract prices that may occur during a single trading day.

All persons who provide services directly to the Fund (as opposed to those persons who provide services through a third-party service provider) are employed by the Manager. The

Fund has no employees of its own.

15

|

Item 1A:

|

RISK FACTORS

|

All investments risk the loss of capital. No guarantee or representation is made that either portfolio of the Fund will achieve its investment objective. An

investment in the Fund is speculative and involves certain considerations and risk factors that prospective investors should consider before subscribing. The practices of leverage and derivatives trading and other investment techniques, which the

Fund expects to employ, can, in certain circumstances, result in significant losses. Under certain circumstances, an investment in the Fund involves the risk of a substantial loss of such investment. Investors should be able to bear the loss of their

entire investment in the Fund, and their investment in the Fund should not be their sole significant investment.

Past performance is not necessarily indicative of future results.

Class 0 of the Fund has been operating since August 1, 2006, and Class 2 since November 1, 2007 with respect to its original portfolio, now the Blended Strategies Portfolio.

Moreover, DTP became a part of the Blended Strategies Portfolio as of August 2008. There can be no assurance that any portfolio of the Fund will achieve its investment objective.

Futures and Options Trading Is Speculative and Volatile. Futures and options prices are highly volatile. Such volatility

may lead to substantial risks and returns, generally much larger than in the case of equity or fixed-income investments. Price movements for futures are influenced by, among other things: changing supply and demand relationships; weather;

agricultural, trade, fiscal, monetary, and exchange control programs and policies of governments; macro political and economic events and policies; changes in national and international interest rates and rates of inflation; currency devaluations and

revaluations; and emotions of other market participants. None of these factors can be controlled by the Fund and no assurance can be given that the Manager’s advice will result in profitable trades for a participating customer or that a customer will

not incur substantial losses. The Fund may purchase and write options. The purchaser of an option is subject to the risk of losing the entire purchase price of the option, while the writer of an option is subject to an unlimited risk of loss, namely

the risk of loss resulting from the difference between the premium received for the option and the price of the futures contract or other asset underlying the option which the writer must purchase or deliver upon exercise of the option. Thus, an

investment in the Fund is suitable only for those investors with speculative capital who understand the risks of futures and options markets.

To the extent the Fund invests in a commodity futures contract or long option that is physically settled, unless an offsetting trade is made, the Fund would be required to take

physical delivery of the commodity underlying the future or option. To the extent the Fund fails to enter into such offsetting trade prior to the expiration of the contract, the Fund may suffer a loss since neither the Fund nor the Manager expects it

has the operational capacity to accept physical delivery of commodities.

The Fund’s Trading Is Highly Leveraged, Which May Result in Substantial Losses for the Fund. The Fund trades futures and options on a leveraged basis due to the low margin deposits

normally required for trading. As a result, a relatively small price movement in a contract may result in immediate and substantial gains or losses for the Fund. For example, $3,000 in margin may be required to hold a U.S. Treasury futures contract

with a face value of $100,000. If the value of the contract were to decline by 3%, the entire margin deposit would be lost.

Market Illiquidity May Cause Less Favorable Trade Prices. Futures trading at times may be illiquid. Most United States

commodity exchanges limit price fluctuations in certain commodity interest prices during a single day by means of “daily price fluctuation limits” or “daily limits.” The daily limit, which is set by most exchanges for all but a portion of the

expiration month, imposes a floor and a ceiling on the prices at which a trade may be executed, as measured from the last trading day’s close. While these limits were put in place to lessen margin exposure, they may have certain negative consequences

for the Fund’s trading. For example, once the price of a particular contract has increased or decreased by an amount equal to the daily limit, thereby producing a “limit-up” or “limit-down” market, positions in the contract can neither be taken nor

liquidated unless traders are willing to effect trades at or within the limit. Contract prices in various commodities have occasionally moved the daily limit for several consecutive days with little or no trading. Similar occurrences could prevent

the Fund from promptly liquidating unfavorable positions, subjecting the Fund to substantial losses. Market intervention may also create liquidity issues. For instance, countries may impose limits on the ability to engage in short sales on

instruments traded on exchanges that are subject to their regulation. During the current COVID-19 outbreak, various EU countries have enacted such bans, impacting shares of companies traded on their exchanges as well as on derivatives related to

those companies and indices of which such companies are constituents.

16

In Times of Market Stress, the Fund May Not Be Able to Diversify Its Portfolio and Risk Management Systems May Not be Effective.

Where the markets are subject to exceptional stress, trading strategies and programs may become less diversified and more highly correlated as the stress may cause diverse and otherwise unrelated markets all to act in a similar manner. Efforts by the

Manager to diversify the Fund’s trading strategies and investment exposure may not succeed in protecting the Fund from significant losses in the event of severe market disruptions. Furthermore, certain risk measures used by the Advisor as part of its

risk management systems and procedures, including VaR, are dependent on inputs derived from historical scenarios and data. Such inputs based on historical scenarios and data may not be reliable during periods of unusual or distressed market

conditions where the market ceases to function in a typical manner. As a result, the Advisor’s risk management systems and procedures may not operate as anticipated or be effective to prevent losses, in unusual or distressed market conditions. A

significant risk of any risk management system using stop loss limits is “gap risk,” which is the risk that liquidity suddenly becomes unavailable and/or markets simply move too quickly through the desired stop level, resulting in greater than

expected losses. The inability of a Portfolio or other investors to sell certain types of investments could also lead to a potential inability of the Portfolio and other investors to meet margin calls or fund withdrawals, the impact of which can be

further aggravated as dealers and counterparties reduce available credit lines and investors withdraw additional capital. The COVID-19 outbreak has placed tremendous stress on global markets, leading to a breakdown in typical asset class

correlations, decreasing liquidity in the cash markets, and increasing volatility across all markets. The impact of the outbreak has been broad-based, resulting in losses across all asset classes, thereby minimizing the potential benefits that

typically result from having a diversified portfolio.

The Fund Is Subject to Speculative Position Limits, Which May Limit the Fund’s Ability to Generate Profits or Result in Losses.

The CFTC and various exchanges impose speculative position limits on the number of futures positions a person or group may hold or control in particular futures. Most physical delivery and many financial futures and option contracts are subject to

speculative position limits. The CFTC has established position limits with respect to contracts for corn, oats, wheat, soybeans, soybean oil, soybean meal, and cotton. In other markets, the relevant exchanges are required to determine whether and to

what extent limits should apply. For purposes of complying with speculative position limits, the Fund’s outright futures positions will be required to be aggregated with any futures positions owned or controlled by the Manager or any principal of the

Manager. Similar types of limits apply to trading on EU commodity exchanges as a result of EU regulations that came into effect in 2018, albeit in a manner somewhat different to the manner in which limits apply on US commodity exchanges. As a result,

the Fund may be unable to take positions in particular futures or may be forced to liquidate positions in particular futures, which could limit the ability of the Fund to earn profits or cause it to experience losses.

Trading on Non-U.S. Exchanges Presents Greater Risks to the Fund than Trading on U.S. Exchanges. Unlike trading on U.S. commodity exchanges, trading on non-U.S. commodity exchanges is not regulated by the CFTC and may be subject to greater risks than trading on U.S. exchanges. For example, some non-U.S. exchanges are

“principals’ markets” in which no common clearing facility exists, and a trader may look only to the broker for performance of the contract. In addition, unless the Fund hedges against fluctuations in the exchange rate between the U.S. dollar (in

which Units are denominated) and other currencies in which trading is done on non-U.S. exchanges, any profits that the Fund might realize in trading could be reduced or eliminated by adverse changes in the exchange rate, or the Fund could incur

losses as a result of those changes. Additional costs could also be incurred in connection with international investment activities. Foreign brokerage commissions generally are higher than in the United States. Expenses also may be incurred

on currency exchanges when the Fund changes investments from one currency to another. Increased custodian costs as well as administrative difficulties (such as the applicability of foreign laws to foreign custodians in various circumstances,

including bankruptcy, ability to recover lost assets, expropriation, nationalization and record access) may be associated with the maintenance of assets in foreign jurisdictions.

The Unregulated Nature of the Over-The-Counter Markets Creates Counterparty Risks that Do Not Exist in Futures Trading on

Exchanges. Forward markets, including foreign currency markets, offer less protection against defaults in trading than is available when trading occurs on an exchange. Forward contracts are not guaranteed by an exchange or clearing house,

and, therefore, a non-settlement or default on the contract would deprive the Fund of unrealized profits or force the Fund to cover its commitment to purchase and resale, if any, at the current market price.

Additional risks of the forward markets include: (i) the forward markets are generally not regulated by any U.S. or foreign governmental authorities; (ii) there are generally no

limitations on daily price moves in forward transactions; (iii) speculative position limits are not applicable to forward transactions although the counterparties with which the Fund may deal may limit the size or duration of positions available as a

consequence of credit considerations; (iv) participants in the forward markets are not required to make continuous markets in forward contracts; and (v) the forward markets are “principals’ markets” in which performance with respect to a forward

contract is the responsibility only of the counterparty with which the trader has entered into a contract (or its guarantor, if any), and not of any exchange or clearing house. As a result, the Fund will be subject to the risk of inability or refusal

to perform with respect to such contracts on the part of the counterparties with which the Fund trades.

17

The Fund Has Credit Risk with respect to its Futures Brokers. The CEA requires a U.S. broker to segregate all funds

received from such broker’s customers in respect of regulated futures transactions from such broker’s proprietary funds. If the broker were not to do so to the full extent required by law, the assets of the Fund might not be fully protected in the

event of the bankruptcy of the broker. In the event of the broker’s bankruptcy, the Fund would be limited to recovering only a pro rata share of all available funds segregated on behalf of the broker’s combined customer accounts, even though certain

property specifically traceable to the Fund (for example, U.S. Treasury bills deposited by the Fund) was held by the broker. In addition, in the event of bankruptcy or insolvency of an exchange or an affiliated clearing house, the Fund might

experience a loss of funds deposited through its broker as margin with an exchange or affiliated clearing house, the loss of unrealized profits on its open positions, and the loss of funds owed to it as realized profits on closed positions. If the

Fund retains brokers that are not subject to U.S. regulation, its funds deposited with those brokers might not be segregated.

The Unregulated Nature of the Swaps and Derivatives Markets Creates Counterparty Risks that Do Not Exist in Futures Trading on

Exchanges. The Fund may enter into swap contracts and related derivatives agreements with various counterparties. Certain swaps and other forms of derivatives instruments currently are not guaranteed by an exchange or its clearing house or

regulated by any U.S. or foreign governmental authorities. Consequently, there are no requirements with respect to record keeping, financial responsibility or segregation of customer funds and positions. The default of a party with which the Fund has

entered into an OTC swap or other derivative may result in the loss of unrealized profits and force the Fund to cover its resale commitments, if any, at the then current market price. It may not be possible to dispose of or close out an OTC swap or

other derivative position without the consent of the counterparty, and the Fund may not be able to enter into an offsetting contract in order to be able to cover its risk.

The Fund Has Credit and Market Risks With Respect to Its Cash Management. The Fund currently invests all assets not

required for trading in Cash Assets, which in turn presently holds deposits in bank accounts or invests broadly in U.S. government or agency securities. With respect to its cash deposited in bank accounts, although the bank accounts themselves may be

insured by the United States Federal Deposit Insurance Corporation, the balances in such accounts will be largely uninsured, as the maximum amount of insurance available to such accounts will not be material relative to the balances that are expected