Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - Acutus Medical, Inc. | afib-ex322_7.htm |

| EX-32.1 - EX-32.1 - Acutus Medical, Inc. | afib-ex321_6.htm |

| EX-31.2 - EX-31.2 - Acutus Medical, Inc. | afib-ex312_8.htm |

| EX-31.1 - EX-31.1 - Acutus Medical, Inc. | afib-ex311_9.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark one)

|

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2020

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-39430

ACUTUS MEDICAL, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

45-1306615 |

|

(State or other jurisdiction of |

(I.R.S. Employer |

|

|

|

|

2210 Faraday Ave., Suite 100, Carlsbad, CA |

92008 |

|

(Address of principal executive offices) |

(zip code) |

(Registrant’s telephone number, including area code) (442) 232-6080

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Trading Symbol |

|

Name of each exchange on which registered |

|

Common Stock, par value $0.001 per share |

|

AFIB |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically, if any, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). YES ☒ NO ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☐ |

Accelerated filer |

|

☐ |

|

|

|

|

|

|

|

|

Non-accelerated filer |

|

☒ |

Smaller reporting company |

|

☒ |

|

|

|

|

|

|

|

|

Emerging growth company |

|

☒ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

|

Class of Common Stock |

|

Outstanding Shares as of November 9, 2020 |

|

Common Stock, $0.001 par value |

|

27,846,083 |

ACUTUS MEDICAL, INC. AND SUBSIDIARIES

Form 10-Q

For the Quarter Ended September 30, 2020

Table of Contents

|

|

|

|

|

|

|

Page |

|

PART I. FINANCIAL INFORMATION |

|

|

|

|

|

|

|

Item 1. |

1 |

|

|

|

|

|

|

|

Condensed Consolidated Balance Sheets as of September 30, 2020 (unaudited) and December 31, 2019 |

1 |

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

Notes to Condensed Consolidated Financial Statements (unaudited) |

6 |

|

|

|

|

|

Item 2. |

Management’s Discussion and Analysis of the Results of Operations |

31 |

|

|

|

|

|

Item 3. |

47 |

|

|

|

|

|

|

Item 4. |

47 |

|

|

|

|

|

|

|

||

|

|

|

|

|

Item 1. |

48 |

|

|

|

|

|

|

Item 1A. |

48 |

|

|

|

|

|

|

Item 2. |

48 |

|

|

|

|

|

|

Item 6. |

49 |

|

|

|

|

|

|

50 |

||

Acutus Medical, Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

(in thousands, except share and per share amounts)

|

|

|

September 30, 2020 |

|

|

December 31, 2019 |

|

||

|

|

|

(unaudited) |

|

|

|

|

|

|

|

ASSETS: |

|

|

|

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

58,302 |

|

|

$ |

9,452 |

|

|

Marketable securities, short-term |

|

|

99,742 |

|

|

|

62,351 |

|

|

Restricted cash |

|

|

150 |

|

|

|

150 |

|

|

Accounts receivable |

|

|

1,893 |

|

|

|

263 |

|

|

Inventory |

|

|

10,932 |

|

|

|

8,424 |

|

|

Prepaid expenses and other current assets |

|

|

4,635 |

|

|

|

1,816 |

|

|

Total current assets |

|

|

175,654 |

|

|

|

82,456 |

|

|

|

|

|

|

|

|

|

|

|

|

Marketable securities, long-term |

|

|

8,789 |

|

|

|

— |

|

|

Property and equipment, net |

|

|

9,940 |

|

|

|

4,427 |

|

|

Right-of-use asset, net |

|

|

1,838 |

|

|

|

2,341 |

|

|

Intangible assets, net |

|

|

3,780 |

|

|

|

4,110 |

|

|

Goodwill |

|

|

12,026 |

|

|

|

12,026 |

|

|

Other assets |

|

|

482 |

|

|

|

95 |

|

|

Total assets |

|

$ |

212,509 |

|

|

$ |

105,455 |

|

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES, CONVERTIBLE PREFERRED STOCK AND STOCKHOLDERS' EQUITY (DEFICIT) |

|

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

|

Accounts payable |

|

$ |

4,723 |

|

|

$ |

3,882 |

|

|

Accrued liabilities |

|

|

6,500 |

|

|

|

10,076 |

|

|

Contingent consideration, short-term |

|

|

4,000 |

|

|

|

8,200 |

|

|

Operating lease liabilities, short-term |

|

|

907 |

|

|

|

833 |

|

|

Common and preferred stock warrant liability |

|

|

— |

|

|

|

8,919 |

|

|

Total current liabilities |

|

|

16,130 |

|

|

|

31,910 |

|

|

|

|

|

|

|

|

|

|

|

|

Operating lease liabilities, long-term |

|

|

1,365 |

|

|

|

2,054 |

|

|

Long-term debt |

|

|

38,762 |

|

|

|

38,244 |

|

|

Contingent consideration, long-term |

|

|

3,600 |

|

|

|

5,700 |

|

|

Other long-term liabilities |

|

|

8 |

|

|

|

— |

|

|

Total liabilities |

|

|

59,865 |

|

|

|

77,908 |

|

|

|

|

|

|

|

|

|

|

|

|

Commitments and contingencies (Note 12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Convertible preferred stock |

|

|

|

|

|

|

|

|

|

Series A convertible preferred stock, $0.001 par value; no shares authorized, issued and outstanding as of September 30, 2020; 3,848,696 shares authorized and 391,210 shares issued and outstanding as of December 31, 2019; liquidation preference of $3,245 as of December 31, 2019 |

|

|

— |

|

|

|

3,059 |

|

|

Series B convertible preferred stock, $0.001 par value; no shares authorized, issued and outstanding as of September 30, 2020; 30,032,100 shares authorized and 3,088,444 shares issued and outstanding as of December 31, 2019; liquidation preference of $41,294 as of December 31, 2019 |

|

|

— |

|

|

|

40,685 |

|

|

Series C convertible preferred stock, $0.001 par value; no shares authorized, issued and outstanding as of September 30, 2020; 48,184,000 shares authorized and 4,499,921 shares issued and outstanding as of December 31, 2019; liquidation preference of $75,000 as of December 31, 2019 |

|

|

— |

|

|

|

74,575 |

|

|

Series D convertible preferred stock, $0.001 par value; no shares authorized, issued and outstanding as of September 30, 2020; 90,000,000 shares authorized and 8,200,297 issued and outstanding as of December 31, 2019; liquidation preference of $136,675 as of December 31, 2019 |

|

|

— |

|

|

|

135,039 |

|

|

|

|

|

|

|

|

|

|

|

|

Stockholders' equity (deficit) |

|

|

|

|

|

|

|

|

|

Preferred stock, $0.001 par value; 5,000,000 shares authorized as of September 30, 2020 and no shares authorized as of December 31, 2019; no shares issued and outstanding as of each of September 30, 2020 and December 31, 2019, respectively |

|

|

— |

|

|

|

— |

|

|

Common stock, $0.001 par value; 260,000,000 shares authorized as of each of September 30, 2020 and December 31, 2019; 27,826,408 and 695,902 shares issued and outstanding as of September 30, 2020 and December 31, 2019, respectively |

|

|

28 |

|

|

|

1 |

|

|

Additional paid-in capital |

|

|

484,162 |

|

|

|

33,252 |

|

|

Accumulated deficit |

|

|

(331,613 |

) |

|

|

(259,034 |

) |

|

Accumulated other comprehensive income (loss) |

|

|

67 |

|

|

|

(30 |

) |

|

Total stockholders' equity (deficit) |

|

|

152,644 |

|

|

|

(225,811 |

) |

|

Total liabilities, convertible preferred stock and stockholders' equity (deficit) |

|

$ |

212,509 |

|

|

$ |

105,455 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

1

Acutus Medical, Inc. and Subsidiaries

Condensed Consolidated Statements of Operations and Comprehensive Loss

(in thousands, except share and per share amounts)

(Unaudited)

|

|

|

Three Months Ended September 30, |

|

|

Nine Months Ended September 30, |

|

||||||||||

|

|

|

2020 |

|

|

2019 |

|

|

2020 |

|

|

2019 |

|

||||

|

Revenue |

|

$ |

3,173 |

|

|

$ |

646 |

|

|

$ |

5,890 |

|

|

$ |

2,167 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Costs and operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cost of products sold |

|

|

5,141 |

|

|

|

2,267 |

|

|

|

10,998 |

|

|

|

6,878 |

|

|

Research and development |

|

|

8,343 |

|

|

|

5,865 |

|

|

|

24,492 |

|

|

|

15,489 |

|

|

Research and development - license acquired |

|

|

— |

|

|

|

15,000 |

|

|

|

— |

|

|

|

15,000 |

|

|

Selling, general and administrative |

|

|

15,833 |

|

|

|

7,978 |

|

|

|

35,193 |

|

|

|

18,998 |

|

|

Change in fair value of contingent consideration |

|

|

118 |

|

|

|

700 |

|

|

|

(1,466 |

) |

|

|

700 |

|

|

Total costs and operating expenses |

|

|

29,435 |

|

|

|

31,810 |

|

|

|

69,217 |

|

|

|

57,065 |

|

|

Loss from operations |

|

|

(26,262 |

) |

|

|

(31,164 |

) |

|

|

(63,327 |

) |

|

|

(54,898 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other income (expense): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change in fair value of warrant liability and embedded derivative |

|

|

(3,683 |

) |

|

|

(3 |

) |

|

|

(5,555 |

) |

|

|

(608 |

) |

|

Loss on debt extinguishment |

|

|

— |

|

|

|

(49 |

) |

|

|

— |

|

|

|

(1,447 |

) |

|

Interest income |

|

|

23 |

|

|

|

525 |

|

|

|

393 |

|

|

|

733 |

|

|

Interest expense |

|

|

(1,366 |

) |

|

|

(1,394 |

) |

|

|

(4,090 |

) |

|

|

(20,905 |

) |

|

Total other expense, net |

|

|

(5,026 |

) |

|

|

(921 |

) |

|

|

(9,252 |

) |

|

|

(22,227 |

) |

|

Net loss |

|

$ |

(31,288 |

) |

|

$ |

(32,085 |

) |

|

$ |

(72,579 |

) |

|

$ |

(77,125 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other comprehensive income (loss) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unrealized (loss) gain on marketable securities |

|

|

(9 |

) |

|

|

40 |

|

|

|

(50 |

) |

|

|

47 |

|

|

Foreign currency translation adjustment |

|

|

78 |

|

|

|

(45 |

) |

|

|

147 |

|

|

|

(57 |

) |

|

Comprehensive loss |

|

$ |

(31,219 |

) |

|

$ |

(32,090 |

) |

|

$ |

(72,482 |

) |

|

$ |

(77,135 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss per common share, basic and diluted |

|

$ |

(1.95 |

) |

|

$ |

(47.21 |

) |

|

$ |

(12.36 |

) |

|

$ |

(115.66 |

) |

|

Weighted average shares outstanding, basic and diluted |

|

|

16,080,467 |

|

|

|

679,591 |

|

|

|

5,870,861 |

|

|

|

666,823 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

2

Acutus Medical, Inc. and Subsidiaries

Condensed Consolidated Statements of Convertible Preferred Stock and Stockholders’ Equity (Deficit)

(in thousands, except share amounts)

(Unaudited)

For the Three Months Ended September 30, 2020

|

|

|

Series A |

|

|

Series B |

|

|

Series C |

|

|

Series D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accumulated |

|

|

Total |

|

||||||||||||||||||||||

|

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

|

Common Stock |

|

|

Additional Paid-in |

|

|

Accumulated |

|

|

Other Comprehensive |

|

|

Equity Stockholders' |

|

|||||||||||||||||||||||||||||

|

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Deficit |

|

|

Income (Loss) |

|

|

(Deficit) |

|

||||||||||||||

|

Balance as of June 30, 2020 (unaudited) |

|

|

391,210 |

|

|

$ |

3,059 |

|

|

|

3,088,444 |

|

|

$ |

40,685 |

|

|

|

4,499,921 |

|

|

$ |

74,575 |

|

|

|

8,593,360 |

|

|

$ |

142,236 |

|

|

|

|

775,403 |

|

|

$ |

1 |

|

|

$ |

36,355 |

|

|

$ |

(300,325 |

) |

|

$ |

(2 |

) |

|

$ |

(263,971 |

) |

|

Unrealized loss on marketable securities |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(9 |

) |

|

|

(9 |

) |

|

Foreign currency translation adjustment |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

78 |

|

|

|

78 |

|

|

Conversion of convertible preferred stock into common stock upon IPO |

|

|

(391,210 |

) |

|

|

(3,059 |

) |

|

|

(3,088,444 |

) |

|

|

(40,685 |

) |

|

|

(4,499,921 |

) |

|

|

(74,575 |

) |

|

|

(8,593,360 |

) |

|

|

(142,236 |

) |

|

|

|

16,572,935 |

|

|

|

17 |

|

|

|

260,538 |

|

|

|

— |

|

|

|

— |

|

|

|

260,555 |

|

|

Issuance of common stock for cash, net of issuance costs of $16,361 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

10,147,058 |

|

|

|

10 |

|

|

|

166,276 |

|

|

|

— |

|

|

|

— |

|

|

|

166,286 |

|

|

Reclassification of warrant liability to stockholders' equity |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

14,474 |

|

|

|

— |

|

|

|

— |

|

|

|

14,474 |

|

|

Stock option exercises |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

27,661 |

|

|

|

— |

|

|

|

145 |

|

|

|

— |

|

|

|

— |

|

|

|

145 |

|

|

Stock-based compensation |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

303,351 |

|

|

|

— |

|

|

|

6,374 |

|

|

|

— |

|

|

|

— |

|

|

|

6,374 |

|

|

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(31,288 |

) |

|

|

— |

|

|

|

(31,288 |

) |

|

Balance as of September 30, 2020 (unaudited) |

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

— |

|

|

|

|

27,826,408 |

|

|

$ |

28 |

|

|

$ |

484,162 |

|

|

$ |

(331,613 |

) |

|

$ |

67 |

|

|

$ |

152,644 |

|

For the Three Months Ended September 30, 2019

|

|

|

Series A |

|

|

Series B |

|

|

Series C |

|

|

Series D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|||||||||||||||||||||

|

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

|

Common Stock |

|

|

Additional Paid-in |

|

|

Accumulated |

|

|

Other Comprehensive |

|

|

Total Stockholders' |

|

|||||||||||||||||||||||||||||

|

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Deficit |

|

|

Income (Loss) |

|

|

Deficit |

|

||||||||||||||

|

Balance as of June 30, 2019 (unaudited) |

|

|

391,210 |

|

|

$ |

3,059 |

|

|

|

3,088,444 |

|

|

$ |

40,685 |

|

|

|

4,499,921 |

|

|

$ |

74,575 |

|

|

|

6,418,437 |

|

|

$ |

106,702 |

|

|

|

|

671,960 |

|

|

$ |

1 |

|

|

$ |

31,569 |

|

|

$ |

(207,035 |

) |

|

$ |

15 |

|

|

$ |

(175,450 |

) |

|

Unrealized gain on marketable securities |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

40 |

|

|

|

40 |

|

|

Foreign currency translation adjustment |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(45 |

) |

|

|

(45 |

) |

|

Issuance of Series D convertible preferred stock for cash, net of issuance costs of $1,358 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

1,781,860 |

|

|

|

28,341 |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Stock-based compensation |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

4,612 |

|

|

|

— |

|

|

|

812 |

|

|

|

— |

|

|

|

— |

|

|

|

812 |

|

|

Stock option exercises |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

7,452 |

|

|

|

— |

|

|

|

19 |

|

|

|

— |

|

|

|

— |

|

|

|

19 |

|

|

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(32,085 |

) |

|

|

— |

|

|

|

(32,085 |

) |

|

Balance as of September 30, 2019 (unaudited) |

|

|

391,210 |

|

|

$ |

3,059 |

|

|

|

3,088,444 |

|

|

$ |

40,685 |

|

|

|

4,499,921 |

|

|

$ |

74,575 |

|

|

|

8,200,297 |

|

|

$ |

135,043 |

|

|

|

|

684,024 |

|

|

$ |

1 |

|

|

$ |

32,400 |

|

|

$ |

(239,120 |

) |

|

$ |

10 |

|

|

$ |

(206,709 |

) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

3

Acutus Medical, Inc. and Subsidiaries

Condensed Consolidated Statements of Convertible Preferred Stock and Stockholders’ Equity (Deficit)

(in thousands, except share amounts)

(Unaudited)

For the Nine Months Ended September 30, 2020

|

|

|

Series A |

|

|

Series B |

|

|

Series C |

|

|

Series D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional |

|

|

Total |

|

||||||||||||||||||||||

|

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

|

Common Stock |

|

|

Additional Paid-in |

|

|

Accumulated |

|

|

Other Comprehensive |

|

|

Stockholders' Equity |

|

|||||||||||||||||||||||||||||

|

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Deficit |

|

|

Income (Loss) |

|

|

(Deficit) |

|

||||||||||||||

|

Balance as of December 31, 2019 |

|

|

391,210 |

|

|

$ |

3,059 |

|

|

|

3,088,444 |

|

|

$ |

40,685 |

|

|

|

4,499,921 |

|

|

$ |

74,575 |

|

|

|

8,200,297 |

|

|

$ |

135,039 |

|

|

|

|

695,902 |

|

|

$ |

1 |

|

|

$ |

33,252 |

|

|

$ |

(259,034 |

) |

|

$ |

(30 |

) |

|

$ |

(225,811 |

) |

|

Unrealized loss on marketable securities |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(50 |

) |

|

|

(50 |

) |

|

Foreign currency translation adjustment |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

147 |

|

|

|

147 |

|

|

Issuance of Series D convertible preferred stock for the Biotronik Asset Purchase |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

273,070 |

|

|

|

5,000 |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Issuance of Series D convertible preferred stock for the contingent consideration related to the Rhythm Xience Acquisition |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

119,993 |

|

|

|

2,197 |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Conversion of convertible preferred stock into common stock upon IPO |

|

|

(391,210 |

) |

|

|

(3,059 |

) |

|

|

(3,088,444 |

) |

|

|

(40,685 |

) |

|

|

(4,499,921 |

) |

|

|

(74,575 |

) |

|

|

(8,593,360 |

) |

|

|

(142,236 |

) |

|

|

|

16,572,935 |

|

|

|

17 |

|

|

|

260,538 |

|

|

|

— |

|

|

|

— |

|

|

|

260,555 |

|

|

Issuance of common stock for cash, net of issuance costs of $16,361 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

10,147,058 |

|

|

|

10 |

|

|

|

166,276 |

|

|

|

— |

|

|

|

— |

|

|

|

166,286 |

|

|

Reclassification of warrant liability to stockholders' equity |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

14,474 |

|

|

|

— |

|

|

|

— |

|

|

|

14,474 |

|

|

Stock option exercises |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

92,223 |

|

|

|

— |

|

|

|

350 |

|

|

|

— |

|

|

|

— |

|

|

|

350 |

|

|

Stock-based compensation |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

318,290 |

|

|

|

— |

|

|

|

9,272 |

|

|

|

— |

|

|

|

— |

|

|

|

9,272 |

|

|

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(72,579 |

) |

|

|

— |

|

|

|

(72,579 |

) |

|

Balance as of September 30, 2020 (unaudited) |

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

— |

|

|

|

— |

|

|

$ |

— |

|

|

|

|

27,826,408 |

|

|

$ |

28 |

|

|

$ |

484,162 |

|

|

$ |

(331,613 |

) |

|

$ |

67 |

|

|

$ |

152,644 |

|

For the Nine Months Ended September 30, 2019

|

|

|

Series A |

|

|

Series B |

|

|

Series C |

|

|

Series D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|||||||||||||||||||||

|

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

Convertible Preferred Stock |

|

|

|

Common Stock |

|

|

Additional Paid-in |

|

|

Accumulated |

|

|

Other Comprehensive |

|

|

Total Stockholders' |

|

|||||||||||||||||||||||||||||

|

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

Amount |

|

|

|

Shares |

|

|

Amount |

|

|

Capital |

|

|

Deficit |

|

|

Income (Loss) |

|

|

Deficit |

|

||||||||||||||

|

Balance as of December 31, 2018 |

|

|

388,558 |

|

|

$ |

3,059 |

|

|

|

3,088,444 |

|

|

$ |

40,685 |

|

|

|

4,499,921 |

|

|

$ |

74,575 |

|

|

|

— |

|

|

$ |

— |

|

|

|

|

656,654 |

|

|

$ |

1 |

|

|

$ |

30,150 |

|

|

$ |

(161,995 |

) |

|

$ |

20 |

|

|

$ |

(131,824 |

) |

|

Unrealized gain on marketable securities |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

47 |

|

|

|

47 |

|

|

Foreign currency translation adjustment |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(57 |

) |

|

|

(57 |

) |

|

Issuance of Series A preferred stock for cashless warrant exercise |

|

|

2,652 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Issuance of Series D convertible preferred stock for cash, net of issuance costs of $1,632 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

4,091,819 |

|

|

|

66,567 |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Issuance of Series D convertible preferred stock for 2018 Convertible Notes and 2019 Convertible Notes |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

4,108,478 |

|

|

|

68,476 |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Stock-based compensation |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

11,449 |

|

|

|

— |

|

|

|

2,174 |

|

|

|

— |

|

|

|

— |

|

|

|

2,174 |

|

|

Stock option exercises |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

15,921 |

|

|

|

— |

|

|

|

76 |

|

|

|

— |

|

|

|

— |

|

|

|

76 |

|

|

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(77,125 |

) |

|

|

— |

|

|

|

(77,125 |

) |

|

Balance as of September 30, 2019 (unaudited) |

|

|

391,210 |

|

|

$ |

3,059 |

|

|

|

3,088,444 |

|

|

$ |

40,685 |

|

|

|

4,499,921 |

|

|

$ |

74,575 |

|

|

|

8,200,297 |

|

|

$ |

135,043 |

|

|

|

|

684,024 |

|

|

$ |

1 |

|

|

$ |

32,400 |

|

|

$ |

(239,120 |

) |

|

$ |

10 |

|

|

$ |

(206,709 |

) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

Acutus Medical, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(in thousands)

(Unaudited)

|

|

|

Nine Months Ended September 30, |

|

|||||

|

|

|

2020 |

|

|

2019 |

|

||

|

Cash flows from operating activities |

|

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(72,579 |

) |

|

$ |

(77,125 |

) |

|

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

|

|

|

Depreciation expense |

|

|

1,754 |

|

|

|

1,676 |

|

|

Amortization of intangible assets |

|

|

330 |

|

|

|

125 |

|

|

Stock-based compensation expense |

|

|

9,272 |

|

|

|

2,174 |

|

|

Amortization of premiums/(accretion of discounts) on marketable securities, net |

|

|

113 |

|

|

|

(100 |

) |

|

Amortization of debt issuance costs |

|

|

518 |

|

|

|

17,438 |

|

|

Amortization of right-of-use assets |

|

|

507 |

|

|

|

470 |

|

|

Research and development - license acquired |

|

|

— |

|

|

|

15,000 |

|

|

Gain on disposal of property and equipment |

|

|

— |

|

|

|

(1 |

) |

|

Loss on debt extinguishment |

|

|

— |

|

|

|

1,447 |

|

|

Change in fair value of warrant liability and embedded derivative |

|

|

5,555 |

|

|

|

608 |

|

|

Change in fair value of contingent consideration |

|

|

(1,466 |

) |

|

|

700 |

|

|

Changes in operating assets and liabilities, net of effect from business combination: |

|

|

|

|

|

|

|

|

|

Accounts receivable |

|

|

(1,630 |

) |

|

|

(697 |

) |

|

Inventory |

|

|

(1,865 |

) |

|

|

(3,829 |

) |

|

Prepaid expenses and other current assets |

|

|

(2,729 |

) |

|

|

(306 |

) |

|

Other assets |

|

|

(387 |

) |

|

|

(8 |

) |

|

Accounts payable |

|

|

753 |

|

|

|

2,873 |

|

|

Accrued liabilities |

|

|

1,423 |

|

|

|

9,268 |

|

|

Operating lease liabilities |

|

|

(615 |

) |

|

|

(536 |

) |

|

Other long-term liabilities |

|

|

8 |

|

|

|

— |

|

|

Net cash used in operating activities |

|

|

(61,038 |

) |

|

|

(30,823 |

) |

|

|

|

|

|

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

|

|

|

|

|

Purchases of available-for-sale marketable securities |

|

|

(108,528 |

) |

|

|

(68,735 |

) |

|

Sales of available-for-sale marketable securities |

|

|

17,095 |

|

|

|

— |

|

|

Maturities of available-for-sale marketable securities |

|

|

45,000 |

|

|

|

11,550 |

|

|

Purchases of property and equipment |

|

|

(7,822 |

) |

|

|

(683 |

) |

|

Purchase of research and development license |

|

|

— |

|

|

|

(10,000 |

) |

|

Cash paid, net of cash acquired for the Rhythm Xience Acquisition |

|

|

— |

|

|

|

(3,000 |

) |

|

Net cash used in investing activities |

|

|

(54,255 |

) |

|

|

(70,868 |

) |

|

|

|

|

|

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

Proceeds from issuance of debt and warrants |

|

|

— |

|

|

|

77,000 |

|

|

Repayment of debt |

|

|

— |

|

|

|

(15,000 |

) |

|

Payment of issuance and extinguishment costs related to debt |

|

|

— |

|

|

|

(2,332 |

) |

|

Payment of contingent consideration |

|

|

(2,636 |

) |

|

|

— |

|

|

Proceeds from issuance of convertible preferred stock, net of issuance costs |

|

|

— |

|

|

|

66,567 |

|

|

Proceeds from issuance of common stock upon IPO, net of issuance costs |

|

|

166,286 |

|

|

|

— |

|

|

Proceeds from stock options exercises |

|

|

350 |

|

|

|

76 |

|

|

Net cash provided by financing activities |

|

|

164,000 |

|

|

|

126,311 |

|

|

|

|

|

|

|

|

|

|

|

|

Effect of exchange rate changes on cash, cash equivalents and restricted cash |

|

|

143 |

|

|

|

(50 |

) |

|

|

|

|

|

|

|

|

|

|

|

Net change in cash, cash equivalents and restricted cash |

|

|

48,850 |

|

|

|

24,570 |

|

|

Cash, cash equivalents and restricted cash, at the beginning of the period |

|

|

9,602 |

|

|

|

9,775 |

|

|

Cash, cash equivalents and restricted cash, at the end of the period |

|

$ |

58,452 |

|

|

$ |

34,345 |

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

|

|

|

Cash paid for income taxes |

|

$ |

— |

|

|

$ |

— |

|

|

Cash paid for interest |

|

$ |

3,526 |

|

|

$ |

4,647 |

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental disclosure of noncash investing and financing activities: |

|

|

|

|

|

|

|

|

|

Issuance of Series D convertible preferred stock for 2018 Convertible Notes and 2019 Convertible Notes |

|

$ |

— |

|

|

$ |

68,476 |

|

|

Issuance of Series D convertible preferred stock for Biotronik asset purchase |

|

$ |

5,000 |

|

|

$ |

— |

|

|

Issuance of Series D convertible preferred stock for Rhythm Xience Acquisition |

|

$ |

2,197 |

|

|

$ |

— |

|

|

Change in unrealized (gain) loss on marketable securities |

|

$ |

50 |

|

|

$ |

(47 |

) |

|

Warrants issued in conjunction with OrbiMed debt |

|

$ |

— |

|

|

$ |

872 |

|

|

Right-of-use assets exchanged for operating lease liabilities |

|

$ |

— |

|

|

$ |

2,978 |

|

|

Accrued purchase of research and development-license |

|

$ |

— |

|

|

$ |

5,000 |

|

|

Unpaid purchases of property and equipment |

|

$ |

88 |

|

|

$ |

35 |

|

|

Conversion of convertible preferred stock into common stock upon IPO |

|

$ |

260,555 |

|

|

$ |

— |

|

|

Reclassification of warrant liability to stockholders' equity |

|

$ |

14,474 |

|

|

$ |

— |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

5

Acutus Medical, Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 1—Organization and Description of Business

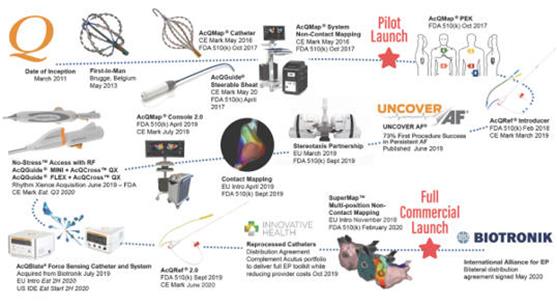

Acutus Medical, Inc. (the “Company”) is an arrhythmia management company focused on improving the way cardiac arrhythmias are diagnosed and treated. The Company designs, manufactures and markets a range of tools for catheter-based ablation procedures to treat various arrhythmias. The Company’s product portfolio includes novel access sheaths, transseptal crossing tools, diagnostic and mapping catheters, ablation catheters, mapping and imaging consoles and accessories, as well as supporting algorithms and software programs. The Company was incorporated in the state of Delaware on March 25, 2011, and is located in Carlsbad, California.

Reverse Stock Split

The Company’s board of directors approved a reverse split of shares of the Company’s common stock and convertible preferred stock on a 9.724-for-one basis (the “Reverse Stock Split”), which was effected on July 28, 2020. The par value and the number of authorized shares of the convertible preferred stock and common stock were not adjusted in connection with the Reverse Stock Split. All references to common stock, convertible preferred stock, warrants to purchase common stock, warrants to purchase convertible preferred stock, options to purchase common stock, restricted stock units, restricted stock awards, share data, per share data and related information contained in the condensed consolidated financial statements have been retrospectively adjusted to reflect the effect of the Reverse Stock Split for all periods presented. No fractional shares of the Company’s common stock were issued in connection with the Reverse Stock Split. Any fractional share resulting from the Reverse Stock Split was rounded down to the nearest whole share, and any stockholder entitled to a fractional share as a result of the Reverse Stock Split received a cash payment in lieu of receiving fractional shares.

Initial Public Offering

On August 10, 2020, the Company issued 10,147,058 shares of common stock in an initial public offering (“IPO”), which included 1,323,529 shares of common stock issued upon the underwriters’ exercise in full of an option to purchase, at the public offering price less underwriting discounts and commissions, up to an additional 1,323,529 shares. The price to the public for each share was $18.00. The Company received proceeds of $166.3 million from its IPO, net of underwriting discounts and commissions and other offering expenses.

On August 10, 2020, in connection with the closing of the IPO, 391,210 shares of Series A, 3,088,444 shares of Series B, 4,499,921 shares of Series C and 8,593,360 shares of Series D convertible preferred stock, respectively, automatically converted into an equal number of shares of common stock and the warrants to purchase 446,990 shares of Series D convertible preferred stock were automatically converted to an equal number of warrants to purchase common stock at an exercise price of $16.67 per share.

As a result of the IPO, the underwriters’ exercise of their option, and the conversions of the Series A, B, C and D convertible preferred stock, the Company’s total number of outstanding shares increased by 26,719,993 immediately following the closing of the IPO.

Going Concern, Liquidity and Capital Resources

The Company has limited revenue, has incurred operating losses since inception and expects to continue to incur significant operating losses for at least the next several years and may never become profitable. As of September 30, 2020 and December 31, 2019, the Company had an accumulated deficit of $331.6 million and $259.0 million, respectively, and working capital of $159.5 million and $50.5 million, respectively. The Company has historically funded its operations primarily through the sale of debt and equity securities, as well as other indebtedness. With the closing of the Company’s IPO, the Company’s current cash, cash equivalents and marketable securities are sufficient to fund operations for at least the next 12 months. However, the Company may need to raise additional funds through one or more of the following: issuance of additional debt, equity or both. Until such time, if ever, the Company can generate revenue sufficient to achieve profitability, the Company expects to finance its operations through equity or debt financings, which may not be available to the Company on the timing needed or on terms that the Company deems to be favorable. To the extent that the Company raises additional capital through the sale of equity or convertible debt securities, the ownership interest of its stockholders will be diluted, and the terms of these securities may include liquidation or other preferences that adversely affect the rights of common stockholders. Debt financing and preferred equity financing, if available, may involve agreements that include covenants limiting or restricting the Company’s ability to take specific actions, such as incurring additional

6

Acutus Medical, Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

debt, making acquisitions or capital expenditures or declaring dividends. If the Company is unable to maintain sufficient financial resources, its business, financial condition and results of operations will be materially and adversely affected. The Company may be required to delay, limit, reduce or terminate its product discovery and development activities or future commercialization efforts. There can be no assurance that the Company will be able to obtain the needed financing on acceptable terms or at all.

Beginning in early March 2020, the COVID-19 pandemic and the measures imposed to contain this pandemic disrupted the Company’s business. The effects of the pandemic began to decrease in late April 2020 as electrophysiology labs began reopening and procedure volumes began increasing as compared to COVID-19 related low points in March 2020. The Company could experience similar, or even more sustained, access restrictions or decreases in procedural activities as hospitals continue to deal with the COVID-19 pandemic. If cases of COVID-19 increase and hospitals again prioritize those patients, additional restrictions may be implemented which would adversely impact our business and financial results.

Note 2—Summary of Significant Accounting Policies

Basis of Presentation

The condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“U.S. GAAP”) for interim financial information and the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and notes required by U.S. GAAP for complete financial statements. In the opinion of management, the condensed consolidated financial statements reflect all adjustments, which include only normal recurring adjustments necessary for the fair statement of the balances and results for the periods presented. Certain information and note disclosures normally included in the Company’s annual financial statements prepared in accordance with U.S. GAAP have been condensed or omitted. These condensed consolidated financial statement results are not necessarily indicative of results to be expected for the full fiscal year or any future period.

Principles of Consolidation

The condensed consolidated financial statements include the accounts of Acutus Medical, Inc. and its wholly-owned subsidiary Acutus Medical NV (“Acutus NV”), which was incorporated under the laws of Belgium in August 2013. All intercompany balances and transactions have been eliminated in consolidation.

Use of Estimates and Assumptions

The preparation of the condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, expenses and disclosures of contingent assets and liabilities. The most significant estimates and assumptions in the Company’s condensed consolidated financial statements include, but are not limited to, revenue recognition, useful lives of intangible assets, assessment of impairment of goodwill, provisions for income taxes, measurement of operating lease liabilities, and the fair value of common stock, stock options, warrants, intangible assets, contingent consideration and goodwill. These estimates and assumptions are based on current facts, historical experience and various other factors believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the recording of expenses that are not readily apparent from other sources. Actual results could differ from those estimates.

Segments

Operating segments are identified as components of an enterprise about which separate discrete financial information is available for evaluation by the chief operating decision maker in making decisions regarding resource allocation and assessing performance. The Company views its operations and manages its business in one operating segment.

7

Acutus Medical, Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Cash and Cash Equivalents and Restricted Cash

The Company considers all highly liquid investments with maturities of three months or less when purchased to be cash equivalents. All of the Company’s cash equivalents have liquid markets and high credit ratings. The Company maintains its cash in bank deposits and other accounts, the balances of which, at times and as of September 30, 2020 and December 31, 2019, exceeded federally insured limits.

Restricted cash serves as collateral for the Company’s corporate credit card program. The following table reconciles cash, cash equivalents and restricted cash in the condensed consolidated balance sheets to the totals shown on the condensed consolidated statements of cash flows (in thousands):

|

|

|

September 30, |

|

|

December 31, |

|

||

|

|

|

2020 |

|

|

2019 |

|

||

|

|

|

(unaudited) |

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

58,302 |

|

|

$ |

9,452 |

|

|

Restricted cash |

|

|

150 |

|

|

|

150 |

|

|

Total cash, cash equivalents and restricted cash |

|

$ |

58,452 |

|

|

$ |

9,602 |

|

Marketable Securities

The Company considers its debt securities to be available-for-sale securities. Available-for-sale securities are classified as cash equivalents or short-term or long-term marketable securities based on the maturity date at time of purchase and their availability to meet current operating requirements. Marketable securities that mature in three months or less from the date of purchase are classified as cash equivalents. Marketable securities, excluding cash equivalents, that mature in one year or less are classified as short-term available-for-sale securities and are reported as a component of current assets.

Securities that are classified as available-for-sale are measured at fair value with temporary unrealized gains and losses reported in other comprehensive loss, and as a component of stockholders’ equity (deficit) until their disposition or maturity. See “Fair Value Measurements” below. The Company reviews all available-for-sale securities at each period end to determine if they remain available-for-sale based on the Company’s current intent and ability to sell the security if it is required to do so. Realized gains and losses from the sale of marketable securities, if any, are calculated using the specific-identification method.

Marketable securities are subject to a periodic impairment review. The Company may recognize an impairment charge when a decline in the fair value of investments below the cost basis is determined to be other-than-temporary. In determining whether a decline in market value is other-than-temporary, various factors are considered, including the cause, duration of time and severity of the impairment, any adverse changes in the investees’ financial condition and the Company’s intent and ability to hold the security for a period of time sufficient to allow for an anticipated recovery in market value. Declines in value judged to be other-than-temporary are included in the Company’s condensed consolidated statements of operations and comprehensive loss. The Company did not record any other-than-temporary impairments related to marketable securities in the Company’s condensed consolidated statements of operations and comprehensive loss for the nine-month periods ended September 30, 2020 and 2019.

Concentrations of Credit Risk and Off-Balance Sheet Risk

Financial instruments that potentially subject the Company to credit risk consist principally of cash, cash equivalents, restricted cash, accounts receivable and marketable securities. Cash and restricted cash are maintained in accounts with financial institutions, which, at times may exceed the Federal depository insurance coverage of $0.25 million. The Company has not experienced losses on these accounts and management believes, based upon the quality of the financial institutions, that the credit risk with regard to these deposits is not significant. The Company’s marketable securities portfolio consists primarily of investments in money market funds, commercial paper and short-term high credit quality corporate debt securities.

8

Acutus Medical, Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Revenue from Contracts with Customers

The Company accounts for revenue earned from contracts with customers under Accounting Standards Codification (“ASC”) 606, Revenue from Contracts with Customers (“ASC 606”). The core principle of the revenue standard is that a company should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. The following five steps are applied to achieve that core principle:

|

|

• |

Step 1: Identify the contract with the customer. |

|

|

• |

Step 2: Identify the performance obligations in the contract. |

|

|

• |

Step 3: Determine the transaction price. |

|

|

• |

Step 4: Allocate the transaction price to the performance obligations in the contract. |

|

|

• |

Step 5: Recognize revenue when, or as, the company satisfies a performance obligation. |

The Company usually places its medical diagnostic equipment, AcQMap System, at customer sites under loan agreements and generates revenue from disposable products used with the AcQMap System. Disposable products include AcQMap Catheters and AcQGuide Steerable Sheaths. The Company provides the disposable products in exchange for consideration, which occurs when a customer submits a purchase order and the Company provides disposables at the agreed upon prices in the invoice. Generally, customers purchase disposable products using separate purchase orders after the equipment has been provided to the customer for free with no binding agreement or requirement to purchase any disposable products. The Company also sells the AcQMap System to customers along with software updates on a when-and-if-available basis and equipment service. The Company has elected the practical expedient and accounting policy election to account for the shipping and handling as activities to fulfill the promise to transfer the disposable products and not as a separate performance obligation.

During the three months ended September 30, 2020, the Company entered into deferred equipment agreements that are generally structured such that the Company agrees to provide an AcQMap System at no up-front charge, with title of the device transferring to the customer at the end of the contract term, in exchange for the customer’s commitment to purchase disposables at a specified price over the term of the agreement, which generally ranges from two to four years. The Company determined that the deferred equipment agreements include embedded sales-type leases. The Company allocates contract consideration under deferred equipment agreements containing fixed annual disposable purchase commitments to the underlying lease and non-lease components at contract inception. The Company expenses the cost of the device at the inception of the agreement and records a financial lease asset equal to the gross consideration allocated to the lease. The lease asset will be reduced by payments for minimum disposable purchases that are allocated to the lease.

The following table sets forth the Company’s revenue for disposables and systems/service for the three and nine months ended September 30, 2020 and 2019 (in thousands):

|

|

|

Three Months Ended September 30, |

|

|

Nine Months Ended September 30, |

|

||||||||||

|

|

|

2020 |

|

|

2019 |

|

|

2020 |

|

|

2019 |

|

||||

|

|

|

(unaudited) |

|

|

(unaudited) |

|

||||||||||

|

Disposables |

|

$ |

2,179 |

|

|

$ |

643 |

|

|

$ |

4,358 |

|

|

$ |

2,155 |

|

|

Systems |

|

|

965 |

|

|

|

— |

|

|

|

1,485 |

|

|

|

— |

|

|

Service/Other |

|

|

29 |

|

|

|

3 |

|

|

|

47 |

|

|

|

12 |

|

|

Total |

|

$ |

3,173 |

|

|

$ |

646 |

|

|

$ |

5,890 |

|

|

$ |

2,167 |

|

The Company’s contracts only include fixed consideration. There are no discounts, rebates, returns or other forms of variable consideration. Customers are generally required to pay within 30 to 60 days.