Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☒

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2019

OR

|

☐

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _____ to _____

Commission File Number: 001-38599

Aquestive Therapeutics, Inc.

(Exact Name of Registrant as Specified in its Charter)

|

Delaware

|

82-3827296

|

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer Identification Number)

|

|

30 Technology Drive, Warren, NJ

|

07059

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

(908) 941-1900

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Trading Symbol(s)

|

Name of each exchange on which registered

|

||

|

Common Stock, par value $0.001 per share

|

AQST

|

NASDAQ Global Market

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or

for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (section 232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the

definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act of 1934.

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

|

Non-accelerated filer ☒

|

Smaller reporting company ☒

|

|

Emerging growth company ☒

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

As of June 30, 2019, the last day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the common stock held by non-affiliates of the registrant was

approximately $101.0 million based on the closing price of the registrant’s common stock on such date.

The number of outstanding shares of the registrant’s par value $0.001 common stock as of the close of business on March 6, 2020 was 33,582,234.

The registrant intends to file a definitive proxy statement pursuant to Regulation 14A in connection with its 2020 Annual Meeting of Shareholders within 120 days of the end of its fiscal year ended

December 31, 2019. Portions of such definitive proxy statement are incorporated by reference into Part III of this Annual Report on Form 10-K.

|

Page No.

|

||

|

3

|

||

|

Item 1.

|

4

|

|

|

Item 1A.

|

28 | |

|

Item 1B.

|

70 | |

|

Item 2.

|

70 | |

|

Item 3.

|

70

|

|

|

Item 4.

|

72

|

|

| 72 | ||

|

Item 5.

|

72 | |

|

Item 6.

|

74

|

|

|

Item 7.

|

75

|

|

|

Item 7A.

|

94 | |

|

Item 8.

|

94

|

|

|

Item 9.

|

94

|

|

|

Item 9A.

|

94 | |

|

Item 9B.

|

94 | |

| PART III |

95 | |

|

Item 10.

|

95 | |

|

Item 11.

|

95 | |

|

Item 12.

|

95 | |

|

Item 13.

|

95 | |

|

Item 14.

|

95 | |

| 96 | ||

|

Item 15.

|

96 |

Forward-Looking Statements

This Annual Report on Form 10-K and certain other communications made by us include forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Words such

as “believe,” “anticipate,” “plan,” “expect,” “estimate”, “intend,” “may,” “will,” or the negative of those terms, and similar expressions, are intended to identify forward-looking statements. These forward-looking statements may include, but are

not limited to, statements regarding therapeutic benefits and plans and objectives for regulatory approvals of AQST-108, Libervant TM and our other product candidates; ability to obtain FDA approval and advance AQST-108, Libervant and

our other product candidates to the market; statements about our growth and future financial and operating results and financial position, regulatory approval and pathways, clinical trial timing and plans, our and our competitors’ orphan drug

approval and resulting drug exclusivity for our products or products our competitors; short-term and long-term liquidity and cash requirements, cash funding and cash burn, business strategies, market opportunities, and other statements that are

not historical facts.

These forward statements are based on our current expectations and beliefs and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those

described in the forward-looking statements. Such risks and uncertainties include, but are not limited to, risks associated with the Company’s development work, including any delays or changes to the timing, cost and success of our product

development activities and clinical trials and plans; risk of delays in FDA approval of Libervant and our other drug candidates or failure to receive approval; risk of our ability to demonstrate to the FDA “clinical superiority” within the

meaning of the FDA regulations of our drug candidate Libervant relative to FDA-approved diazepam rectal gel and nasal spray products including by establishing a major contribution to patient care within the meaning of FDA regulations relative to

the approved products and there can be no assurance that we will be successful; risk that a competitor obtains FDA orphan drug exclusivity for a product with the same active moiety as any of our other drug products for which we are seeking FDA

approval and that such earlier approved competitor orphan drug blocks such other product candidates in the U.S. for seven years for the same indication; risk-inherent in commercializing a new product (including technology risks, financial risks,

market risks and implementation risks and regulatory limitations); risk of development of our sales and marketing capabilities; risk of legal costs associated with and the outcome of our patent litigation challenging third party at risk generic

sale of our proprietary products; risk of sufficient capital and cash resources, including access to available debt and equity financing and revenues from operations, to satisfy all of our short-term and longer-term cash requirements and other

cash needs, at the time and in the amounts needed; risk of failure to satisfy all financial and other debt covenants and of any default; risk-related to government claims against Indivior for which we license, manufacture and sell Suboxone and

which accounts for the substantial part of our current operating revenues; risk associated with Indivior’s cessation of production of its authorized generic buprenorphine naloxone film product, including the impact from loss of orders for the

authorized generic product and risk of eroding market share for Suboxone® and risk of sunsetting product; risks related to coronavirus and potential impact on global businesses as well as on clinical trials, sourcing, regulatory

approval and commercialization of our products and product candidates; risks related to the outsourcing of certain sales, marketing and other operational and staff functions to third parties; risk of the rate and degree of market acceptance of

our product and product candidates; the success of any competing products, including generics; risk of the size and growth of our product markets; risks of compliance with all FDA and other governmental and customer requirements for our

manufacturing facilities; risks associated with intellectual property rights and infringement claims relating to the Company’s products; risk of unexpected patent developments; the impact existing and future legislation and regulatory provisions

on product exclusivity; legislation or regulatory actions affecting pharmaceutical product pricing, reimbursement or access; claims and risks that may arise regarding the safety or efficacy of the Company’s products and product candidates; risk

of loss of significant customers; risks related to legal proceedings, including patent infringement, investigative and antitrust litigation matters; changes in government laws and regulations; risk of product recalls and withdrawals;

uncertainties related to general economic, political, business, industry, regulatory and market conditions and other unusual items; and other risks and uncertainties affecting the Company including those described in the “Risk Factors” section

and in other sections included in this Annual Report on Form10-K, in our Quarterly Reports on Form 10-Q, and in our Current Reports on Form 8-K filed with the Securities and Exchange Commission (SEC). Given these uncertainties, you should not

place undue reliance on these forward-looking statements, which speak only as the date made. All subsequent forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by this

cautionary statement. The Company assumes no obligation to update forward-looking statements, or outlook or guidance after the date of this Annual Report whether as a result of new information, future events or otherwise, except as may be

required by applicable law. Readers should not rely on the forward-looking statements included in this Annual Report as representing our views as of any date after the date of the filing of this Annual Report on Form 10-K.

These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to differ materially

from those expressed or implied by these statements. These factors include the matters discussed and referenced in Part I-Item 1A. Risk Factors of this Form 10-K.

References

Aquestive Therapeutics, Inc., a Delaware corporation, was formed effective on January 1, 2018 via the conversion of MonoSol Rx, LLC, a Delaware limited liability company and predecessor or Aquestive

Therapeutics, Inc., into a C corporation and a simultaneous name change to Aquestive Therapeutics, Inc. (referred to in this Annual Report on Form 10-K as the “January 2018 Conversion”). Unless the context otherwise indicates, references to

“Aquestive”, “AQST”, “we”, the “Company”, “us” and “our” in this Annual Report on Form 10-K refers to Aquestive Therapeutics, Inc. Our principal executive offices are located in Warren, New Jersey.

Overview

We are a pharmaceutical company focused on developing and commercializing differentiated products to address unmet medical needs. We have proprietary products focused on the treatment of diseases of the

Central Nervous System, or CNS, including one commercial-product, one commercial-stage product and a late-stage pipeline product candidate. We believe that the characteristics of these patient populations and shortcomings of available treatment

options create opportunities for the development and commercialization of meaningfully differentiated medicines. In December 2018, we commercially launched the first of our CNS products, Sympazan® (clobazam) Oral Film, for use as an

adjunctive therapy for seizures associated with Lennox-Gastaut Syndrome, or LGS, in patients two years and older. In November 2019, we received FDA approval of our product, Exservan®, which has been licensed for European marketing and for which we

are seeking a licensee in the U.S.

Our most advanced proprietary product is Libervant™ (diazepam) Buccal Film. Libervant is a buccally, or inside of the cheek, administered soluble film formulation of diazepam. Epilepsy patients have

been underserved for some time with little choice beyond device-based products such as rectally administered gels and a recently approved diazepam nasal spray. Aquestive is developing Libervant as an alternative to the current standard of care

rescue therapy for patients with refractory epilepsy, which is a rectal gel, that is invasive, inconvenient, and difficult to administer. As a result, a large portion of the patient population has not received adequate treatment or foregoes

treatment altogether. It is anticipated that Libervant, if approved by the U.S. Food and Drug Administration (FDA), will enable a larger share of these patients to receive more appropriate treatment by providing consistent therapeutic dosing in

a non-invasive and innovative treatment form for epileptic seizures. The Company filed an NDA for Libervant in November 2019. The filing was accepted by the FDA in February 2020 and we have received a PDUFA goal date of September 27, 2020. On

January 10, 2020, a competitor of Aquestive obtained FDA approval of its diazepam nasal spray drug candidate and was granted orphan-drug-exclusivity for this drug commencing as of January 10, 2020. A company that obtains FDA approval for a

designated orphan drug receives market exclusivity for that drug for the designated indication for a period of seven years from the grant date in the United States. This orphan drug exclusivity approval may prevent a subsequent product seeking

FDA approval from being marketed in the United States during the exclusivity period for the same active moiety for the same orphan drug indication except in the case where the drug candidate sponsor is able to demonstrate, and the FDA concludes,

that the later drug is “clinically superior” to the approved products, e.g., safer, more effective, or providing a major contribution to patient care within the meaning of FDA regulations and guidance. In assessing whether a drug candidate

sponsor has demonstrated that its drug candidate provides a “major contribution to patient care” over and above the currently approved drugs, which is evaluated by the FDA on a case by case basis, there is no one objective standard and the FDA

may, in appropriate circumstances, consider such factors as convenience of treatment location, duration of treatment, patient comfort, reduced treatment burden, advances in ease and comfort of drug administration, longer periods between doses,

and potential for self-administration. We believe that our product candidate Libervant is “clinically superior” to the two currently FDA-approved products with the same moiety and for the same indication as Libervant, as qualifying as “a major

contribution to patient care” within the meaning of the FDA regulation and guidance. However, such a demonstration to overcome such seven-year market exclusivity is difficult to establish with limited precedents and there can be no assurance

that we will be successful in these efforts. Any failure to obtain FDA approval of and to demonstrate clinical superiority for Libervant would have a material adverse effect on our business, financial condition and results of operations in 2021

and later. More details on this product approval are described in “Competition” section below in this Item 1. Business of this Form10-K.

We have developed a proprietary pipeline of complex molecule products addressing large market opportunities beyond CNS indications, including AQST-108, a sublingual film formulation

of epinephrine for the treatment of anaphylaxis. In February of 2020, we had a constructive face-to-face pre-Investigational New Drug (IND) application meeting with the FDA for this drug candidate. A pre-IND meeting provides an opportunity for an

open communication between a drug sponsor and the FDA to discuss the sponsor’s IND development plan and to obtain the agency’s guidance for clinical studies for the sponsor’s new drug candidate. The FDA has confirmed that the clinical development

for AQST-108 will be reviewed under the 505(b)(2) pathway as proposed by Aquestive and that no additional studies would be necessary prior to opening the proposed IND application. The FDA indicated that there appears to be an unmet medical need

among patients who resist the standard of care use of intramuscular injection in the treatment of anaphylaxis and that AQST-108 may potentially address some of those unmet needs. Aquestive expects to move forward with opening an IND and initiating

its pharmacokinetic (PK) clinical trials before the end of 2020.

In addition to these products and product candidates, we have a portfolio of commercialized and development-stage drug products that we license to other companies. These products include Suboxone®, a

sublingual film formulation of buprenorphine and naloxone, for the treatment of opioid dependence, and Exservan (riluzole), an oral film product for the treatment of amyotrophic lateral sclerosis (ALS).

We manufacture all of our licensed and proprietary products at our FDA and Drug Enforcement Agency, or DEA, inspected facilities and anticipate that our current manufacturing capacity is sufficient for

commercial quantities of our products and product candidates currently in development. We have produced over 2.2 billion doses of Suboxone since 2010. Our products are developed using our proprietary PharmFilm® technology and know-how. Our patent

portfolio currently comprises at least 200 issued patents worldwide, of which at least 40 are U.S. patents, and more than 90 pending patent applications worldwide.

Our Product Portfolio and Pipeline

The following table outlines our pipeline of products and product candidates

(a) Aquestive holds rights for worldwide commercialization

Sympazan®, Suboxone®, Zuplenz®, Exservan®, PharmFilm® and the Aquestive logo are registered trademarks of Aquestive Therapeutics, Inc. All other registered

trademarks referenced herein are the property of their respective owners.

We have initially focused our proprietary product pipeline on certain difficult to treat CNS diseases. Our PharmFilm® technology allows us to develop medicines that offer non-invasive delivery,

customized suitability for patients with dysphagia, or trouble swallowing, can be administered without water and ensures consistent therapeutic dosing. We believe that these characteristics will permit us to achieve the desired patient outcomes,

while potentially reducing the total cost of patient care.

Our two most advanced assets within our proprietary CNS portfolio, focused in epilepsy, are as follows:

|

•

|

Sympazan – an oral soluble film formulation of clobazam, a benzodiazepine used as an adjunctive therapy for seizures associated with LGS. We developed

Sympazan as an alternative to the Onfi® brand and clobazam generic, which were previously only available in either tablet form or liquid suspensions. LGS patients often have difficulty swallowing pills and large volume suspensions leading

to uncertain and inconsistent dosing. These challenges increase the burden of care, particularly for patients that have difficulty swallowing or who may be combative or resistant during treatment administration. We believe that Sympazan

addresses these treatment obstacles because it is mucoadhesive, dissolves rapidly and cannot be easily spit out. Following approval by the FDA, we launched Sympazan in December 2018.

|

|

•

|

Libervant – a buccally, or inside of the cheek, administered soluble film formulation of diazepam. Aquestive is developing Libervant as an alternative

to the current standard of care rescue therapy for patients with refractory epilepsy, which as a rectal gel, is invasive, inconvenient, and difficult to administer, as well as a recently approved nasal spray. Libervant was designated an

orphan drug by the FDA and has been granted a PDUFA goal date of September 27, 2020. More details on this product approval are described in the “Competition” section of this Item I. Business of this Form 10-K.

|

Proprietary Complex Molecule Portfolio

We are utilizing our technology and know-how to target acceptable market opportunities by developing orally administered complex molecule therapies as alternatives to invasively administered standard of

care injectable therapeutics. We currently have two active complex molecule programs in clinical development. The first is focused on the oral delivery of the hormone epinephrine. The second is focused on the delivery of a peptide known as

octreotide. If it achieves regulatory approval, which we cannot assure, octreotide would be the first peptide delivered orally using our technology and may create other opportunities for peptides and biologics.

The active programs in our complex molecule portfolio are:

• AQST-108 – a “first of its kind” oral sublingual film formulation delivering systemic epinephrine that is in development for the

treatment of anaphylaxis using Aquestive’s proprietary PharmFilm® technologies. Epinephrine is the standard of care in the treatment of anaphylaxis and is currently administered via subcutaneous or intramuscular injection. The current market

leader is EpiPen®, a single-dose, pre-filled automatic injection device. As a result of its administration via subcutaneous or intra-muscular injection, many patients and their caregivers are reluctant to use currently available products, resulting

in increased hospital visits and overall cost of care to treat anaphylactic events. The data from a completed Phase 1 dose escalation study demonstrated that AQST-108 achieved similar ranges of mean values of maximum concentration (Cmax) and time

to reach maximum concentration (Tmax) to that reported for injectables EpiPen® and Auvi-Q®, provided a greater total exposure (AUC0-t; area under the curve) than that reported for EpiPen and Auvi-Q, had less interpatient variability when compared

to degree of variation (CV%) data reported for EpiPen and Auvi-Q, and was well tolerated, with no study participants discontinuing participation due to an adverse event. We believe that, as a result of its sublingual administration, AQST-108 will

improve patient compliance and lower the total cost of care. After a constructive pre-IND meeting with the FDA in early February 2020, the Company is in the process of preparing the IND for AQST-108, which is expected to be submitted to the FDA in

the coming months. The Company expects to utilize the 505(b)(2) regulatory approval pathway for AQST-108 and expects to begin clinical trials later in 2020.

• AQST-305 – a sublingual film formulation of octreotide, a small peptide that has a similar pharmacological profile to natural

somatostatin, for the treatment of acromegaly, as well as severe diarrhea and flushing associated with carcinoid syndrome. Acromegaly is a hormone disorder that results from the overproduction of growth hormone in middle-aged adults. Octreotide

is the standard of care for the treatment of acromegaly. The current market leader, Sandostatin®, is administered via deep subcutaneous or intramuscular injections once a month. This monthly treatment regimen can result in loss of

efficacy toward the end of the monthly treatment cycle. We are developing AQST-305 as a non-invasive, pain-free alternative to Sandostatin to reduce treatment burden, healthcare costs and the potential loss of efficacy of the treatment cycle.

ASQST-305 has shown promising preclinical results. We completed a human proof of concept study in Canada. As a result of the early stage proof of concept work, further optimization of this formulation is currently underway.

Licensed Products

Our portfolio also includes products and product candidates that we have licensed, or will seek to license, for commercialization. In the years ended December 31, 2019 and 2018, our licensed product

portfolio generated over $1 billion in revenue for our licensees in each year, resulting in $49.7 million and $67.2 million in revenue to Aquestive, respectively. Our key licensed products and products that we intend to license include:

|

•

|

Suboxone – a sublingual film formulation of buprenorphine and naloxone that is marketed in the United States and internationally for the treatment of

opioid dependence. Suboxone Sublingual Film was launched by licensee, Indivior Inc., or Indivior, in 2010. Suboxone Sublingual Film is the most prescribed branded product in its category and is the first sublingual film product for the

treatment of opioid dependence. We are the sole and exclusive supplier and manufacturer of Suboxone Sublingual Film and Indivior’s authorized generic product of the drug.

|

On October 15, 2019, Indivior publicly announced that, in order to mitigate the impact from the recent passage of H.R. 438 – Continuing Appropriations Act, 2020, and Health Extenders Act of 2019, which came into effect

on October 1, 2019, and which includes changes to the methodology for calculating average manufacturers price for branded dosage, Indivior has discontinued offering its authorized generic sublingual film product. As of early March 2020, Suboxone

branded products retain approximately 43% of film market share. We do not expect any meaningful revenue in 2020 and in future years from sales of the authorized generic product of Suboxone, but we do expect the branded Suboxone products for U.S.

and rest of world to continue to provide meaningful revenue in the future.

Since the launch of this product in 2010, we have produced over 2.2 billion doses of Suboxone. On February 20, 2019, Dr. Reddy’s Labs and Alvogen, Inc. launched competing generic formulations of this product at

risk, and on February 22, 2019 Mylan Pharmaceuticals, Inc. announced it launch of a similar generic formulation. We filed and continue to pursue patent infringement lawsuits against these companies. More details regarding these lawsuits are

described in the “Legal Proceedings” section below in Item 3 of this Form 10-K.

|

•

|

Exservan (riluzole) Oral Film – utilizing Aquestive’s proprietary PharmFilm® technology, has been developed for the treatment of amyotrophic lateral

sclerosis (ALS). Exservan may potentially fulfill a critical need for ALS patients, given it can be administered safely and easily, twice daily, without water. We believe that Exservan, via our orally administered dosage form, can bring

meaningful assistance to patients who are diagnosed with ALS and face difficulties swallowing traditional forms of medication. Exservan was approved by the FDA in November 2019. During the 2019 fourth quarter, the Company granted a

license to Zambon S.p.A (“Zambon”) for the development and commercialization of Exservan in the European Union (EU) for the treatment of ALS. Zambon is a multinational pharmaceutical company with a focus on the central nervous system

(CNS) therapeutics area. Under the terms of the license agreement, an upfront payment was paid to Aquestive for the development and commercialization rights of Exservan in the EU, and Aquestive will be paid development and sales

milestone payments and low double-digit royalties on net sales of the product in the EU. Zambon will be responsible for the regulatory approval and marketing of Exservan in the countries where Zambon seeks to market the product, and

Aquestive will be responsible for the development and manufacture of the product. The Company seeks to license the commercialization rights for Exservan in the United States.

|

|

•

|

Zuplenz – an oral soluble film formulation of ondansetron, a 5-HT antagonist approved for the treatment of nausea and vomiting associated with

chemotherapy and post-operative recovery. Ondansetron is available as intravenous injections, intramuscular injections, orally dissolving tablets, oral solution tablets, and film. Generic and branded products are available, with the

branded product marketed as Zofran® by GlaxoSmithKline. We licensed commercial rights for Zuplenz to Fortovia Therapeutics (previously Midatech Pharma PLC) in the United States, Canada, and China. Fortovia launched Zuplenz in the United

States in 2015. We are the sole and exclusive manufacturer of Zuplenz for Fortovia.

|

|

•

|

APL-130277 – a sublingual film formulation of apomorphine, which is a dopamine agonist in development to treat episodic off-periods in Parkinson’s

disease. APL-130277 is being developed by a licensee as a sublingual alternative to an injectable form of apomorphine. We licensed intellectual property for APL-130277 to Cynapsus Therapeutics,

Inc., a company that was acquired by Sunovion Pharmaceuticals Inc., or Sunovion. Sunovion received a Complete Response Letter from the FDA on January 29, 2019 and announced that no additional clinical trials were necessary to submit a

revised NDA. Sunovion announced in November 2019 that the NDA was re-submitted, and its PDUFA goal date was May 21, 2020. Assuming FDA approval for this product candidate, which we cannot assure, we intend to explore royalty

monetization opportunities for the expected royalty and milestone revenue streams from this product which, if successful, could lead to additional non-dilutive capital for the Company.

|

PharmFilm® – Our Oral Film Technology

We are presently the worldwide leader in oral film drug delivery and manufacturing, having historically supplied the substantial majority of the world’s oral films for prescription pharmaceutical use,

and we have the capability to produce more than one billion commercial doses a year. We developed our PharmFilm® technology to provide meaningful clinical and therapeutic advantages over other existing dosage forms and, in turn, to improve the

lives of patients and caregivers. PharmFilm® is protected by our patent portfolio, which currently includes at least 200 issued patents worldwide, of which at least 40 are U.S. patents, and more than 90 pending patent applications worldwide.

Several of the patents in this intellectual property portfolio are utilized in each of our proprietary pipeline products. We are continuing to develop additional intellectual property and know-how related to the applications and engineering of

PharmFilm® alone or in combination with other technologies to create product capabilities that have compelling value propositions.

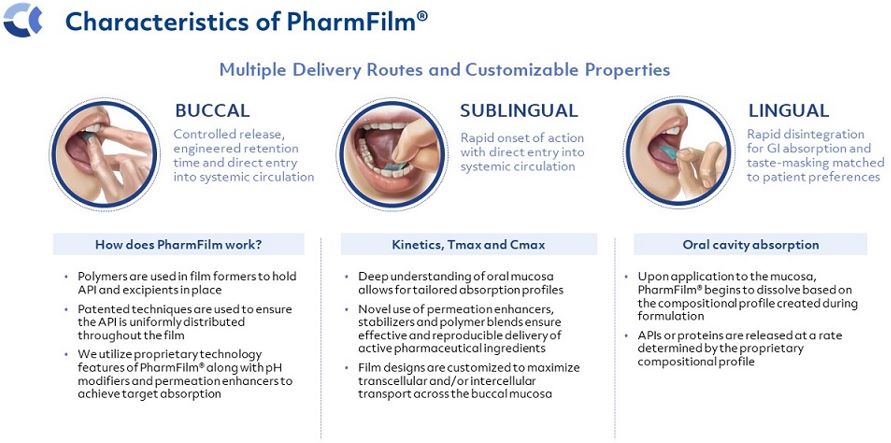

PharmFilm® is comprised of proprietary polymer compositions that serve as film formers to hold active pharmaceutical ingredients, or APIs, and excipients in place. Proprietary and patent-protected

compositions, formulations and manufacturing techniques and technology are employed to ensure that the API is distributed uniformly throughout the film and that target absorption levels are achieved. Our proprietary technology and manufacturing

processes enable PharmFilm® to be engineered to fit a variety of target product profiles in order to best address unmet patient needs present within specific disease states. PharmFilm®, which is similar in thickness and size to a postage stamp, can

be administered via buccal, sublingual or lingual oral delivery.

We believe the innovative nature of our drug delivery platform has the potential to offer a number of meaningful advantages to patients, caregivers and physicians compared to current standard of care

therapies, including:

|

•

|

preferred alternative to more invasive drug administration methods such as injection, rectal or nasal applications;

|

|

•

|

faster, or at least equivalent, onset of action;

|

|

•

|

ease of administration and availability (no device required, no gel to transport);

|

|

•

|

direct absorption into the bloodstream reducing or avoiding “first pass” effects in the liver;

|

|

•

|

reduced gastrointestinal, or GI, side effects;

|

|

•

|

positive dosing outcomes, especially for patients with physical (e.g., dysphagia) or psychological barriers to other methods of drug administration;

|

|

•

|

stable, durable, portable and quick dissolving (with or without water);

|

|

•

|

customizable delivery routes for tailored pharmacokinetic, or PK, profiles (buccal, sublingual or lingual); and

|

|

•

|

customizable taste profiles.

|

We chose to initially focus our development efforts on the CNS market because we believe the application of PharmFilm® is particularly valuable and relevant to patients suffering from certain CNS

disorders where there are unmet patient needs or shortcomings in current standards of care. We believe there remains significant opportunity to develop additional products in the CNS market. Additionally, our know-how and proprietary position have

broad application beyond CNS, and we plan to explore the applications of PharmFilm® in other disease areas.

Our Management Team

Our management team is a critical component to the development of our business model and the execution of our strategy. We are led by executives with an average of over 18 years of relevant senior

leadership experience, including developing and commercializing branded and generic pharmaceuticals at large multinational pharmaceutical companies such as Johnson & Johnson, GlaxoSmithKline PLC, Novartis AG and AstraZeneca. Additionally, our

team has significant experience in the commercialization of pharmaceutical products, translational science, drug evaluation, clinical development, significant FDA experience, regulatory affairs and business development. During 2019 we hired our

Chief Medical Officer. Our management team is supervised and supported by a board of directors with expertise in finance, strategy, medicine and drug development.

Our Strategy

We are a patient-centric pharmaceutical company developing and commercializing products that address unmet needs and improve the lives of patients and their caregivers. We focus on developing medicines

for patient populations suffering from the shortcomings of available treatment options, which can create an opportunity for differentiated medicines. Our pipeline is initially focused on developing treatments for CNS diseases, as well as orally

administered complex molecules that we believe can be alternatives to invasively administered standard of care therapies. Our strategy leverages our global intellectual property portfolio, know-how, demonstrated research and development

capabilities and proprietary manufacturing platform.

To achieve these goals, our strategy includes the following key elements:

|

•

|

Advance our late stage proprietary portfolio of CNS product candidates to solve critical healthcare problems and make a meaningful improvement in the lives

of patients and caregivers. We have focused development efforts on three proprietary CNS products, two of which have been approved and one product candidate in development. These products and product candidates address

treatment challenges associated with epilepsy and ALS. We have received FDA approval and subsequently began, in December 2018, distribution and sales of Sympazan. We received FDA approval of Exservan in November 2019. We completed the

rolling submission for our NDA filing with the FDA for our drug candidate Libervant, with a PDUFA goal date of September 27, 2020. A competitor was approved for a diazepam nasal product in January 2020 and was granted orphan

exclusivity. As described in more detail above under “Our Product Portfolio and Pipeline” and below under “Competition”, we believe and intend to seek to demonstrate to the FDA that our product candidate Libervant is clinically superior

to the two existing approved products utilizing the same active moiety in that it represents a major contribution to patient care when compared to device driven rectal and nasal applications, although there can be no assurances that we

will be successful. See additional information concerning the Libervant FDA approval process in the “Competition” section of Item 1. Business of this Form-10K.

|

|

•

|

Scale our commercial platform to maximize the value of our proprietary product candidates. In order to maximize the value of our

proprietary product candidates, we are continuing our plan to self-commercialize our proprietary product candidates. We will continue to right size our capabilities in marketing, sales, payor and market access management and medical

affairs in order to appropriately support the products we commercialize and the revenue opportunity they represent.

|

|

•

|

Exploit our technology and know-how to develop oral versions of more complex injectable drugs and other drug delivery administrations to

address unmet patient needs. Based on promising preclinical and early clinical results, we intend to continue to develop oral transmucosal versions of epinephrine, a product that is currently available in injectable form. We

believe the success of these efforts may lead to additional opportunities in developing oral transmucosal versions of some proteins, peptides and other complex molecule drugs, which have historically been administered by means other than

oral intake, such as injection or infusion or nasal spray.

|

|

•

|

Continue to identify product opportunities within CNS and other markets to expand our proprietary product pipeline. We intend to

identify additional product candidates that provide clinical differentiation and solve unmet needs. In the CNS space, we will leverage our relationships with key stakeholders including patients, caregivers, key opinion leaders and patient

advocacy groups to identify new product opportunities. Additionally, we will continue to evaluate other therapeutic areas, indications and products where we believe that our expertise and know-how can create differentiation and value.

|

|

•

|

Acquire and market products, or establish licensing relationships to develop and manufacture products, utilizing new chemical entities.

We intend to continue to seek and to evaluate strategically expanding our product portfolio by considering the development of products that would incorporate new chemical entities to treat disorders with high unmet need.

|

|

•

|

Continue to expand and solidify our intellectual property portfolio for our products, product candidates and manufacturing processes.

We believe that our global intellectual property portfolio is a significant source of competitive advantage. We have built a two-tier patent estate consisting of composition-of-matter and method of manufacture patents and patent

applications. We intend to seek to expand our intellectual property estate, where appropriate, as we advance our PharmFilm® and other technologies and as we develop new and existing product candidates.

|

Market Overview

CNS Market

CNS diseases affect the brain or spinal cord and cause neurological and psychiatric disorders. Driven by an increase in mental health awareness and an aging population, the global market for

therapeutics indicated for CNS disorders was estimated by EvaluatePharma to be $82 billion in 2018, with anticipated growth to $115 billion by 2024.

Epilepsy

Epilepsy is a chronic CNS disorder characterized by recurrent seizure activity. There are 3.4 million people in the United States suffering from epilepsy. According to IQVIA data, antiepileptic

medications generated billions of dollars of sales in the United States in 2019. The direct (medical) and indirect (lost wages and productivity) annual costs associated with epileptic patients in the United States are significant.

Epilepsy treatment regimens typically consist of chronic and acute management therapies. Chronic medicines are used on a daily basis to suppress seizure activity. Approximately 1.2 million of those 3.4

million people suffering from epilepsy will continue to suffer with breakthrough seizures and may require an acute (rescue) management strategy. Patients are routinely prescribed antiepileptic drugs, or AEDs, as “maintenance” therapy to control

chronic seizure activity. Most AEDs specifically target neuronal excitation or neuronal inhibitory pathways. There are currently more than 20 AEDs approved for use in the United States, and therapeutic choice depends on the epileptic syndrome being

considered. Patients are routinely prescribed benzodiazepines as “rescue” therapy for the management of acute seizure emergencies.

Rescue therapies are administered as needed in the event of an acute seizure to rapidly terminate seizure activity. One of the most effective benzodiazepines currently available for the treatment of

acute seizures is diazepam. Diazepam is currently marketed as a product administered rectally, and a recently approved nasal spray product which is not yet available commercially. Historically, the rectal gel has been the only rescue medication

available on the market. Although the rectal gel has been the preferred drug prescribed by physicians, its rectal administration presents a particular challenge for patients. As a result, only approximately 100,000 patients out of 1.2 million

potential patients who could benefit from this treatment currently use this therapy. The remaining sufferers either pursue less effective treatments or forego treatment altogether. We have been developing Libervant to reduce the burden associated

with this rescue therapy. See “Our Product Portfolio and Pipeline” above and “Competition” below in this Item 1. Business of this Form 10-K for additional information concerning the Libervant FDA approval process and market access issues.

There are multiple epileptic syndromes including LGS, which is a rare, intractable form of epilepsy and affects approximately 48,000 patients in the United States. Patients with LGS are often drug

resistant, predisposing them to recurrent seizures, and are typically prescribed a combination of antiepileptic medications, which often includes clobazam. Clobazam (branded name Onfi) is available in both a tablet and suspension formulation.

Generic versions of the clobazam tablet and suspension formulation are available to patients as well. Clobazam generated combined sales revenue of $336 million with more than 603,000 prescriptions filled in 2019. Sympazan was developed to reduce

the burden associated with drug administration and cost.

Amyotrophic Lateral Sclerosis

ALS is a progressive neurodegenerative disease affecting nerve cells responsible for controlling voluntary muscle movement. Patients suffering from ALS have progressive degeneration of motor neurons,

which ultimately leads to death, primarily due to respiratory failure. Diagnosis of ALS typically occurs between the ages of 40 and 60, with more than 15,000 patients living with ALS in the U.S.

There are currently no treatments available that reverse the damage caused by ALS. However, there are two treatment molecules that have been shown to slow disease progression, riluzole, marketed as

Rilutek or Tiglutik, and edaravone marketed as Radicava.

In addition to therapeutics aimed at slowing disease progression, patients are often prescribed multiple medications and receive additional therapies, including breathing care, physical therapy,

occupational therapy, speech therapy, nutritional support, and psychological and social support, to ease the burden of the disease.

As a result of the degenerative muscle function associated with ALS, patients eventually lose the ability to swallow. Because riluzole may slow disease progression and delay the need for a tracheotomy,

dysphagia represents a barrier to treatment for many of these patients. We developed Exservan to allow patients to remain on riluzole therapy for more extended periods of time, delaying the need for procedures like tracheotomies, prolonging the

quality of life for those patients and lowering the overall cost of treatment. Exservan is approved for marketing in the U.S., and the Company is seeking a marketing licensee for this product in the U.S. Exservan has been licensed to Zambon for

marketing in the EU.

Other Therapeutic Areas

In addition to products to treat CNS conditions, we are developing a number of product candidates in other therapeutic areas, such as anaphylaxis and acromegaly to address those unmet needs.

Anaphylaxis

Anaphylaxis is a systemic allergic reaction caused by a wide range of allergen exposure, estimated to affect one in 50 people in the United States. Anaphylaxis typically occurs quickly once allergen

exposure has occurred and, if untreated, can lead to death via airway restriction.

Treatment of anaphylaxis typically consists of an intramuscular injection of epinephrine administered at the earliest opportunity, followed by additional intramuscular or intravenous injections as

needed. While generic versions of epinephrine are currently available, they are provided as a vial of medication administered via syringes, as well as several auto-injector products. A branded form of epinephrine known as the EpiPen, which utilizes

a proprietary auto-injector device administered through a deep intramuscular injection, dominates the market. In addition, in the past, manufacturing issues that resulted in injector malfunctions had led to patient concern regarding the reliability

of auto-injectors. EpiPen, which is marketed by Mylan Pharmaceuticals, Inc., represents over 70% of the current branded market on a prescription volume basis. Proper dosing and the ability to effectively administer epinephrine in a timely,

reliable manner is critical for patients experiencing anaphylaxis as well as other acute allergic reactions. However, we believe that the inability to administer complex molecules via oral administration has limited the development of treatments

that have the potential to provide significant patient benefit. We designed AQST-108, a “first of its kind” oral sublingual film formulation delivering systemic epinephrine that is in development for the treatment of anaphylaxis using Aquestive’s

proprietary PharmFilm® technologies, to offer a more convenient and cost-effective oral form of epinephrine as an alternative to the current standard of care. We expect to open an IND with the U.S. FDA in mid-2020 to continue to pursue the

development and approval of this product under the 505(b)(2) regulatory approval pathway.

Acromegaly

Acromegaly is a hormone disorder that results from the overproduction of growth hormone in middle-aged adults. The condition is typically caused by a benign tumor present in the pituitary gland that

excretes excessive amounts of growth hormone and leads to exaggerated bone growth over time. Due to the gradual progression of the disorder, patients are often not diagnosed for years. The prevalence of acromegaly is estimated to be 77cases per

million people, indicating approximately 25,000 diagnosed patients within the United States.

Depending on the placement and size of the tumor, patients may be eligible for endoscopic trans nasal transsphenoidal surgery, a procedure in which pituitary tumors are removed through the nose and

sphenoid sinus. However, surgeons may be unable to completely remove the tumor, leading to persistently elevated growth hormone levels post-surgery. The standard of care for post-surgery patients includes the use of somatostatin analogues to lower

production or block the action of growth hormones. The somatostatin analogues currently available, octreotide and lanreotide, are administered by deep subcutaneous or intramuscular injections once a month, or subcutaneous injections three times

daily.

The market leading product for acromegaly is octreotide, which is marketed as Sandostatin LAR by Novartis, and is administered monthly via depot injections.

Ease of administration has been identified as an unmet patient need within this market, with at least one other company pursing an oral formulation of octreotide. Our PharmFilm® formulation has the

potential to reduce treatment burden and healthcare costs for patients and improve clinical differentiation.

Proprietary CNS Product Candidate

Libervant™ (diazepam)Buccal Film

Libervant™ is a buccally, or inside of the check, administered soluble film formulation of diazepam. Epilepsy patients have been underserved for some time with little choice beyond device-based

products such as rectally administered gels and a recently approved diazepam nasal spray. As an early administered buccal film product that quickly dissolves when applied to the buccal mucosa, Libervant has a rapid onset of action and provides a

consistent therapeutic dosing. See “Our Product Portfolio and Pipeline” above and “Competition” below.

We are developing Libervant, which has been designated an orphan drug and received a PDUFA goal date of September 27, 2020, as an alternative to currently approved diazepam products in the form of a

rectal gel and a recently approved nasal spray, the latter of which received orphan drug market exclusivity for this drug. It is anticipated that Libervant, if approved by the FDA, will enable a portion of the patient population who do not

receive adequate treatment or forego treatment altogether to receive an alternative treatment by providing consistent therapeutic dosing in a non-invasive and innovative treatment form for epileptic seizures. As a first oral product available

utilizing this active moiety for this indication, we believe, and we intend to seek to demonstrate to the FDA that, Libervant is clinically superior in that it represents a major contribution to patient care for this group of patients within the

meaning of the FDA regulations and guidance. The FDA has recently indicated that, when evaluating clinical superiority for drugs demonstrating a “major contribution to patient care,” it may consider, where appropriate, such factors as

convenience of treatment location, duration of drug administration, longer periods between doses, and potential for self-administration. On January 10, 2020, a competitor of Aquestive obtained FDA approval of its diazepam nasal spray drug

candidate and was granted orphan-drug-exclusivity for this drug commencing as of January 10, 2020. A company that obtains FDA approval for a designated orphan drug receives orphan market exclusivity for that drug for the designated indication

for a period of seven years from the grant date in the United States. This orphan drug exclusivity approval may prevent a subsequent product seeking FDA approval from being marketed in the United States during the exclusivity period for the same

active moiety for the same orphan drug indication except in the case where the drug candidate sponsor is able to demonstrate, and the FDA concludes, that the later drug is “clinically superior” to the approved products, e.g., safer, more

effective, or providing a major contribution to patient care within the meaning of FDA regulations and guidance. In assessing whether a drug candidate sponsor has demonstrated that its drug candidate provides a “major contribution to patient

care” over and above the currently approved drugs, which is evaluated by the FDA on a case by case basis, there is no one objective standard and the FDA may, in appropriate circumstances, consider such factors as convenience of treatment

location, duration of treatment, patient comfort, reduced treatment burden, advances in ease and comfort of drug administration, longer periods between doses, and potential for self-administration. We believe that our product candidate Libervant

is “clinically superior” to the two currently FDA-approved products with the same moiety and for the same indication as Libervant, as qualifying as “a major contribution to patient care” within the meaning of the FDA regulation and guidance.

However, such a demonstration to overcome such seven-year market exclusivity is difficult to establish with limited precedents and there can be no assurance that we will be successful in these efforts. Any failure to obtain FDA approval of and

to demonstrate clinical superiority for Libervant would have a material adverse effect on our business, financial condition and results of operations in 2021 and later.

Proprietary Complex Molecule Candidates

AQST-108 (Epinephrine)

AQST-108 is a sublingual film formulation of epinephrine that we are developing for the treatment of anaphylaxis, a severe and potentially life-threatening allergic reaction.

Anaphylaxis is a severe systemic allergic reaction that can be triggered by certain foods, insect stings, certain medications and latex, among other allergens. Signs and

symptoms of anaphylaxis typically occur within seconds or minutes of exposure and may include low blood pressure, skin rash or itching, constriction of the airway and difficulty breathing and nausea and vomiting. If not treated immediately,

anaphylaxis can lead to death due to airway restriction or cardiac arrest. Anaphylaxis is a potentially life-threatening systemic allergic reaction, with an estimated incidence of 50 to 112 episodes per 100,000 people per year. The frequency of

hospital admissions for anaphylaxis has increased 500-700% in the last 10-15 years. The most common causes of reactions that can include anaphylaxis are medications, foods (such as peanuts), and venom from insect stings. Epinephrine injection is

the current standard of treatment intended to reverse the potentially severe manifestation of anaphylaxis, which may include red rash, throat swelling, respiratory problems, gastrointestinal distress and loss of consciousness. Epinephrine, a

non-selective adrenergic agonist, is administered via intramuscular injection. Because anaphylaxis can progress quickly, the ability to administer a reliable and accurate dose of epinephrine as quickly as possible following a reaction is critical

for patient recovery and survival. Epinephrine is typically administered in a single-dose, pre-filled automatic injection device, or an auto-injector. People with known allergies and who are at risk for anaphylaxis are advised to carry an

auto-injector with them at all times and self-administer at the first signs of an anaphylactic reaction. The EpiPen® and similar products can be inconvenient to transport and many patients and caregivers dislike injections as a delivery method.

Additionally, injector malfunction issues and user administration errors may prevent successful and timely dosing which can result in danger to patients.

We are developing AQST-108, a “first of its kind” oral sublingual film formulation delivering systemic epinephrine that is in development for the treatment of anaphylaxis using Aquestive’s proprietary

PharmFilm® technologies, as an alternative to the currently marketed intramuscular injections. We believe there is a market opportunity for a non-injectable, easier to administer product with a fast onset of action. A product with this profile

would enable patients to conveniently and rapidly self-administer a reliable and accurate dose of epinephrine during an anaphylactic reaction, which we believe would result in greater patient compliance. Subject to our achieving regulatory approval

of this product candidate, which we cannot assure, we believe AQST-108 has the potential to reduce the treatment burden currently associated with intramuscular injections and may lower costs to the healthcare system associated with anaphylaxis,

such as hospitalizations, due to inaccurate or untimely dosing.

We have conducted proof-of-concept studies to demonstrate our ability to deliver epinephrine via a non-invasive sublingual film. The data from our completed Phase 1 dose escalation study demonstrated

that AQST-108 achieved similar ranges of mean values of maximum concentration (Cmax) and time to reach maximum concentration (Tmax) to that reported for injectables EpiPen and Auvi-Q®, provided a greater total exposure (AUC0-t; area under the

curve) than that reported for EpiPen and Auvi-Q, had less interpatient variability when compared to degree of variation (CV%) data reported for EpiPen and Auvi-Q, and was well tolerated, with no study participants discontinuing participation due to

an adverse event. We believe that this proof of concept study in humans demonstrates our ability to deliver epinephrine via the oral cavity.

In February of 2020, we had a constructive face-to-face pre-Investigational New Drug (IND) application meeting with the FDA. A pre-IND meeting provides an opportunity for an open

communication between a drug sponsor and the FDA to discuss the sponsor’s IND development plan and to obtain the agency’s guidance for clinical studies for the sponsor’s new drug candidate. The FDA has confirmed that the clinical development for

AQST-108 will be reviewed under the 505(b)(2) regulatory approval pathway, as proposed by Aquestive, and that no additional studies would be necessary prior to opening the proposed IND application. The FDA indicated that there appears to be an

unmet medical need among patients who resist the standard of care use of intramuscular injection in the treatment of anaphylaxis and that AQST-108 may potentially address some of those unmet needs. Aquestive expects to move forward with opening an

IND and initiating its pharmacokinetic (PK) clinical trials before the end of 2020.

AQST-305 (Octreotide)

AQST-305 is a sublingual film formulation of octreotide, an 8 amino acid peptide that has a similar pharmacological profile to natural somatostatin, for the treatment of acromegaly. We completed human

proof of concept studies in Canada in 2019 and, based on the results of these studies, we are completing additional reengineering of the formulation.

Acromegaly is a hormone disorder that results from the overproduction of growth hormone in middle-aged adults. The condition is typically caused by a benign tumor present in the pituitary gland that

excretes excessive amounts of growth hormone and leads to exaggerated bone growth over time.

First-line treatment of acromegaly usually involves surgery to remove the tumor. Some patients are not eligible for surgery depending on the placement and size of the tumor and, in some cases, surgery

does not completely remove the tumor, leading to persistently elevated growth hormone levels. The standard of care for post-surgery patients includes the chronic use of somatostatin analogues to lower production or block the action of growth

hormones. The somatostatin analogues currently on the market, octreotide and lanreotide, are administered by deep subcutaneous or intramuscular injections once a month, which are invasive and painful and can represent a treatment burden for

patients. Such treatment burdens associated with the somatostatin analogues currently on the market include injection site reactions, sub-optimal symptom control and adverse emotional impact. We believe there is a market opportunity for a

non-injectable, easier to administer product that delivers a reliable and consistent dose of octreotide.

We have designed AQST-305 for twice daily administration, which we believe will reduce the burden of monthly depot intramuscular injections and address the potential loss of efficacy over the treatment

life cycle with currently marketed products. AQST-305 can be administered by the patient, rather than having to receive monthly injections in a physician’s office. Additionally, because AQST-305 is administered twice-daily, we believe patients

would receive a consistent dose of octreotide and will not need to be concerned with the potential loss of efficacy that may otherwise result when receiving only a monthly dosage administered via injection. Subject to our achieving FDA approval of

this product candidate, which we cannot assure, we believe AQST-305 will reduce the burden for patients who are looking for a non-invasive, pain-free, easier to administer product.

Licensed Products and Product Candidates

Suboxone (Buprenorphine and Naloxone)

Suboxone is a sublingual film formulation of buprenorphine and naloxone. Buprenorphine and naloxone are respectively an opioid agonist and antagonist that, when combined, are effective for treating

opioid addiction. Suboxone reduces the potential for abuse and improves safety, clinical differentiation, dissolution, taste and texture for patients suffering from opioid addiction. According to the American Society of Addiction Medicine, drug

overdose is the leading cause of accidental death in the United States, with opioid addiction driving this epidemic. Opioid dependence is estimated to affect several million people in the United States. Patients overcoming opioid addiction can

experience painful withdrawal symptoms, which can be mitigated with the use of opioid antagonists.

Suboxone Sublingual Film was launched in partnership with Indivior in 2010 to treat opioid dependence pursuant to a commercialization agreement. We have granted Indivior an exclusive worldwide license

to this product. Since the launch of the product in 2010, over 2.2 billion doses have been delivered to patients. We are the sole and exclusive manufacturer of Suboxone Sublingual Film worldwide for Indivior. See “Material Agreements – Commercial

Exploitation Agreement with Indivior” section in this Form 10-K. On February 20, 2019, Dr. Reddy’s Labs and Alvogen, Inc. launched competing generic formulations of this product and, on February 22, 2109, Mylan Pharmaceuticals, Inc. announced its

launch of a similar generic formulation. In early 2019 Indivior, through Sandoz Inc., began to market and sell an authorized generic sublingual film product for Suboxone. On October 15, 2019, Indivior publicly announced the discontinuance of

production of the authorized generic sublingual film product in order to mitigate the impact from the recent passage of H.R. 438 – Continuing Appropriations Act, 2020, and Health Extender Act of 2019, which came into effect on October 1, 2019 and

which includes changes to the methodology for calculating average manufacture price branded drugs. In addition, although Indivior, through the branded Suboxone, has continued to retain significant market share, we have continued to anticipate the

erosion of this sunsetting product over time.

Zuplenz (Ondansetron)

Zuplenz is an oral soluble film formulation of ondansetron, a 5-HT3 antagonist approved for the treatment of nausea and vomiting associated with chemotherapy and post-operative recovery.

Ondansetron is available as intravenous injections, intramuscular injections, orally dissolving tablets, oral solution, tablets, and film. Generic and branded products are available, with the branded product marketed as Zofran by GlaxoSmithKline.

We licensed commercial rights for Zuplenz to Fortovia (formerly Midatech Pharma PLC) in the United States, Canada, and China. Fortovia launched Zuplenz in the United States in 2015. We are the sole and exclusive manufacturer of Zuplenz for

Fortovia.

APL-130277 (Apomorphine)

APL-130277 is a sublingual film using apomorphine, a dopamine agonist indicated as an intermittent therapy to overcome episodic off periods in Parkinson’s disease. Parkinson’s disease affects

approximately 650,000 people in the United States aged greater than 45 years old. APL-130277 is designed to address an unmet need in patients who suffer from dysphagia and/or patients who have discontinued or avoided use of the existing injectable

product due to site irritation. We licensed intellectual property rights for PharmFilm® technology associated with APL-130277 to Cynapsus Therapeutics, Inc., which was acquired by Sunovion Pharmaceuticals, Inc. (Sunovion). Subject to receiving FDA

approval, which we cannot assure, we will earn royalties and other milestone payments contingent upon worldwide sales of APL-130277. See “Material Agreements – License Agreement with Sunovion Pharmaceuticals, Inc.” in this Form 10-K. In January

2019, we learned that Sunovion received a Complete Response Letter (a CRL) from the FDA in response to its submission of an NDA for APL-130277. In a subsequent press release, Sunovion advised that additional information and analyses were required,

but that no new clinical studies were required. In the 2019 fourth quarter, Sunovion announced that the FDA had given a PDUFA goal date of May 21, 2020 after a resubmission of the NDA for this product. Assuming FDA approval for this product

candidate, we intend to explore royalty monetization opportunities for the expected royalty and milestone revenue streams from this product which, if successful, could lead to additional non-dilutive capital for the Company.

Manufacturing and Product Supply

We operate two redundant manufacturing and primary packaging facilities located in Portage, Indiana, where we currently manufacture proprietary CNS products, as well as our licensed products, Suboxone

and Zuplenz, on an exclusive basis. These facilities are expected to have a combined capacity to accommodate the production of our proprietary and licensed products, as well as our pipeline product candidates, without any current need for

additional infrastructure. We will continue to consider our anticipated facilities and infrastructure needs as our product development grows. We have produced over 1.1 billion doses in the last four years. As a company, our research and

development laboratories are registered with the DEA for Schedule II-V drugs.

We are subject to various regulatory requirements, such as the regulations of the FDA, the DEA, and other foreign health authorities such as the Australian Government Department of Health’s Therapeutics

Goods Administration, or TGA. We are required to register our facilities and adhere to current Good Manufacturing Practices (cGMP) standards. These standards require manufacturers to follow elaborate design, testing, control, documentation and

other quality assurance procedures throughout the entire manufacturing process. Our facilities have undergone inspections by the FDA, DEA, TGA, and several quality assurance inspections by pharmaceutical companies for cGMP compliance. In each case,

the facilities have passed inspection and are subject to periodic re-inspection. Failure to comply with these and other statutory and regulatory requirements subjects a manufacturer to possible legal or regulatory action, including warning letters,

the seizure or recall of products, injunctions, consent decrees placing significant restrictions on or suspending manufacturing operations and civil and criminal penalties. Adverse experiences with the product or product complaints must be reported

and could result in the imposition of market restrictions through labeling changes or in product removal. Product approvals may be withdrawn if compliance with regulatory requirements is not maintained or if problems concerning safety or efficacy

of the product occur following approval.

We purchase our raw materials, including active pharmaceutical ingredients, from qualified, approved vendors both domestically and internationally. While we typically source raw materials from the

lowest cost provider whenever possible, we continue to pursue a multi-supplier strategy for all of our critical raw materials, where available or appropriate. Our product packaging foil is supplied by a single manufacturer. Such manufacturer

utilizes multiple manufacturing facilities for production of our packaging foil. We may enter into more formal supply agreements in the future as production volumes increase and are more predictive.

Subject to the supervision of our internal clinical development staff, we use third-party contract research organizations, or CROs, to administer and conduct many aspects of our planned clinical trials

including monitoring and managing data, and we will rely upon such CROs, as well as medical institutions, clinical investigators and consultants, to conduct our trials in accordance with our clinical protocols. We intend for such CROs to play a

significant role in the subsequent collection and analysis of data from such trials. Additionally, we intend to continue to outsource secondary packaging and third-party logistics for our proprietary products.

Competition

We compete with pharmaceutical and biotechnology companies that develop and commercialize therapeutics for the treatment of a broad range of disease areas and indications. Additionally, we compete with

companies that utilize advanced drug administration platforms, such as oral, injectable, intranasal, transdermal patch and pulmonary delivery, to create improved therapeutics over current standards of care. This industry is highly competitive and

new products and technologies evolve and come to market at a rapid pace. The companies operating in this market include multinational organizations, established biotechnology companies, single product pharmaceutical and biotechnology companies,

specialty pharmaceutical companies, and generic drug companies. Many of the larger, established organizations currently have commercialization capabilities in-house, and may have partnership or license agreements in place with smaller companies for

commercialization rights. These companies may develop new drugs to treat the indications that we target or seek to have existing drugs approved for the treatment of the indications that we target.

We will compete with commercialized products in all markets for which we have approval and are seeking approval.

The biotechnology and pharmaceutical industries are characterized by rapid evolution and advancements of technologies, intense competition and strong defense of intellectual property. Any products and

product candidates that we successfully develop and commercialize will compete with existing therapies and new therapies that may become available in the future. Key product features that would affect our ability to effectively compete with other

therapeutics include the efficacy, safety and convenience of our products and the ease of use and effectiveness of any companion diagnostics. The level of generic competition and the availability of reimbursement from government and other

third-party payors will also significantly affect the pricing and competitiveness of our products.

On January 10, 2020, a competitor of Aquestive obtained FDA approval of its diazepam nasal spray drug candidate and was granted orphan-drug-exclusivity for this drug commencing as of January 10,

2020. A company that obtains FDA approval for a designated orphan drug receives orphan market exclusivity for that drug for the designated indication for a period of seven years from the grant date in the United States. This orphan drug

exclusivity approval prevents a subsequent product seeking FDA approval from being marketed in the United States during the exclusivity period for the same active moiety for the same orphan drug indication except in the case where the drug

candidate sponsor is able to demonstrate, and the FDA concludes, that the later drug is “clinically superior” to the approved products, e.g., safer, more effective, or providing a major contribution to patient care within the meaning of FDA

regulations and guidance. In assessing whether a drug candidate sponsor has demonstrated that its drug candidate provides a “major contribution to patient care” over and above the currently approved drugs, which is evaluated by the FDA on a case

by case basis, there is no one objective standard and the FDA may, in appropriate circumstances, consider such factors as convenience of treatment location, duration of treatment, patient comfort, reduced treatment burden, advances in ease and

comfort of drug administration, longer periods between doses, and potential for self-administration. We believe, and intend to seek to demonstrate to the FDA, that our product candidate Libervant is “clinically superior” to the two currently

FDA-approved products with the same moiety and for the same indication as Libervant, as qualifying as “a major contribution to patient care” within the meaning of the FDA regulation and guidance. However, such a demonstration to overcome such

seven-year market exclusivity is difficult to establish with limited precedents and there can be no assurance that we will be successful in these efforts. Any failure to obtain FDA approval of and to demonstrate clinical superiority for

Libervant would have a material adverse effect on our business, financial condition and results of operations in 2021 and later.

Material Agreements

Commercial Exploitation Agreement with Indivior

In August 2008, we entered into a Commercial Exploitation Agreement with Reckitt Benckiser Pharmaceuticals, Inc., or the Indivior License Agreement. Indivior, Inc. is the successor in interest to

Reckitt Benckiser Pharmaceuticals, Inc. Pursuant to the Indivior License Agreement, we have agreed to manufacture and supply Indivior’s requirements of Suboxone for both United States and international markets on an exclusive basis.

Under the terms of the Indivior License Agreement, we are required to manufacture Suboxone in accordance with cGMP standards and according to the specifications and processes set forth in the related

quality agreements with Indivior. Additionally, we are required to obtain API for the manufacture of Suboxone directly from Indivior. The Indivior License Agreement specifies a minimum annual threshold quantity of Suboxone that we are obligated to

fill and requires Indivior to provide us with a forecast of its requirements at various specified times throughout the year.

The Indivior License Agreement provides for payment by Indivior of a purchase price per unit that is subject to adjustment based on our ability to satisfy minimum product thresholds. Additionally, in

the event Indivior purchases certain large quantities of Suboxone during a specified period, Indivior will be entitled to scaled rebates on its purchases.

In addition to the purchase price for the Suboxone supplied, under the Indivior License Agreement, we are to be paid low single digit percentage royalty payments tied to net sales value, subject to

annual maximum amounts and limited to the life of related United States or international patents. Indivior exercised its right to buy out its future royalty obligations based on sales in the United States in 2012. Indivior remains obligated to pay

royalties for all sales outside the United States.

The Indivior License Agreement contains customary contractual termination provisions in the event of bankruptcy or corporate dissolution, the intellectual property surrounding Suboxone is found to be

invalid, or either party commits a material breach of the Indivior License Agreement. Additionally, Indivior may terminate the Indivior License Agreement if the FDA or other applicable regulatory authority declares our manufacturing site to no

longer be suitable for the manufacture of Suboxone or Suboxone is no longer suitable to be manufactured due to health or safety reasons. The initial term of the Indivior License Agreement was seven years from the commencement date. Thereafter, the

Indivior License Agreement has automatically renewed for successive one-year periods. One-year renewals are expected to continue in the absence of Indivior’s written notice of its intent not to renew at least one year prior to the expiration of any

prior renewal term.

Supplemental Agreement with Indivior

On September 24, 2017, we entered into an agreement with Indivior, or the Indivior Supplemental Agreement. Pursuant to the Indivior Supplemental Agreement, we conveyed to Indivior all of our existing

and future rights in the settlement of various ongoing patent enforcement legal actions and disputes related to the Suboxone product. We also conveyed to Indivior the right to sublicense manufacturing and marketing capabilities to enable an