Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Rangers Sub I, LLC | felcorlpexhibit32212312019.htm |

| EX-32.1 - EXHIBIT 32.1 - Rangers Sub I, LLC | rangersexhibit32112312019.htm |

| EX-31.4 - EXHIBIT 31.4 - Rangers Sub I, LLC | felcorlpexhibit31412312019.htm |

| EX-31.3 - EXHIBIT 31.3 - Rangers Sub I, LLC | felcorlpexhibit31312312019.htm |

| EX-31.2 - EXHIBIT 31.2 - Rangers Sub I, LLC | rangersexhibit31212312019.htm |

| EX-31.1 - EXHIBIT 31.1 - Rangers Sub I, LLC | rangersexhibit31112312019.htm |

| EX-21.1 - EXHIBIT 21.1 - Rangers Sub I, LLC | rangersfelcorlpexhibit2111.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2019 | ||

OR | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission File Number 333-220497 (Rangers Sub I, LLC)

Commission File Number 333-39595-01 (FelCor Lodging Limited Partnership)

RANGERS SUB I, LLC

FELCOR LODGING LIMITED PARTNERSHIP

(Exact Name of Registrant as Specified in Its Charter)

Maryland (Rangers Sub I, LLC) | 30-1001580 | |

Delaware (FelCor Lodging Limited Partnership) | 75-2544994 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

c/o RLJ Lodging Trust | ||

3 Bethesda Metro Center, Suite 1000 | ||

Bethesda, Maryland | 20814 | |

(Address of Principal Executive Offices) | (Zip Code) | |

(301) 280-7777

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

Title of Class | Trading Symbol | Name of Exchange on Which Registered | ||

Not applicable (1) | ||||

(1) Neither Rangers Sub I, LLC nor FelCor Lodging Limited Partnership has securities registered pursuant to Section 12(b) of the Act. | ||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Rangers Sub I, LLC (refer to the Note below) o Yes ý No

FelCor Lodging Limited Partnership (refer to the Note below) o Yes ý No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Rangers Sub I, LLC (refer to the Note below) ý Yes o No

FelCor Lodging Limited Partnership (refer to the Note below) ý Yes o No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Rangers Sub I, LLC (refer to the Note below) o Yes ý No

FelCor Lodging Limited Partnership (refer to the Note below) o Yes ý No

Note: As voluntary filers not subject to the filing requirements of the Securities Exchange Act of 1934, the registrants have filed all reports pursuant to Section 13 or 15(d) for the preceding 12 months as if they were subject to such filing requirements.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Rangers Sub I, LLC ý Yes o No

FelCor Lodging Limited Partnership ý Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Rangers Sub I, LLC:

Large accelerated filer | o | Accelerated filer | o | |||

Non-accelerated filer | ý | Smaller reporting company | o | |||

Emerging growth company | o | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o | ||||||

FelCor Lodging Limited Partnership:

Large accelerated filer | o | Accelerated filer | o | |||

Non-accelerated filer | ý | Smaller reporting company | o | |||

Emerging growth company | o | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Rangers Sub I, LLC o Yes ý No

FelCor Lodging Limited Partnership o Yes ý No

As of February 26, 2020, RLJ Lodging Trust, L.P. owns 100% of the percentage interests of Rangers Sub I, LLC. As of February 26, 2020, FelCor Holdings Trust, a wholly-owned subsidiary of RLJ Lodging Trust, L.P., owns 99% of the percentage interests of FelCor Lodging Limited Partnership, and Rangers General Partner, LLC, a wholly-owned subsidiary of RLJ Lodging Trust, L.P., owns 1% of the percentage interests of FelCor Lodging Limited Partnership.

EXPLANATORY NOTE

On August 31, 2017 (the "Acquisition Date"), RLJ Lodging Trust ("RLJ"), RLJ Lodging Trust, L.P. ("RLJ LP"), Rangers Sub I, LLC, a wholly-owned subsidiary of RLJ LP ("Rangers"), and Rangers Sub II, LP, a wholly-owned subsidiary of RLJ LP ("Partnership Merger Sub"), consummated the transactions contemplated by the Agreement and Plan of Merger (the "Merger Agreement") dated as of April 23, 2017 with FelCor Lodging Trust Incorporated ("FelCor") and FelCor Lodging Limited Partnership ("FelCor LP"), pursuant to which Partnership Merger Sub merged with and into FelCor LP, with FelCor LP surviving as a wholly-owned subsidiary of RLJ LP (the "Partnership Merger"), and, immediately thereafter, FelCor merged with and into Rangers, with Rangers surviving as a wholly owned subsidiary of RLJ LP (the "REIT Merger" and, together with the Partnership Merger, the "Mergers").

Where it is important to distinguish between the entities, we either refer specifically to Rangers, FelCor, as predecessor to Rangers, or FelCor LP. Otherwise, we use the terms "we" or "our" to refer to (i) Rangers and FelCor LP, collectively (including their consolidated subsidiaries) following the Mergers and (ii) FelCor and FelCor LP, collectively (including their consolidated subsidiaries) prior to consummation of the Mergers, unless the content indicates otherwise.

This annual report on Form 10-K for the fiscal year ended December 31, 2019 combines the filings for Rangers and FelCor LP. Rangers indirectly owns a 99% partnership interest in FelCor LP. Through FelCor LP, Rangers owns hotel properties and conducts other business.

We believe combining the periodic reports for Rangers and FelCor LP into a single combined report results in the following benefits:

• | presents the business as a whole (the same way management views and operates the business); |

• | eliminates duplicative disclosure and provides a more streamlined presentation (a substantial portion of our disclosure applies to both Rangers and FelCor LP); and |

• | saves time and cost by preparing combined reports instead of separate reports. |

Rangers consolidates FelCor LP for financial reporting purposes. Rangers has no assets other than its indirect investment in FelCor LP and no liabilities separate from FelCor LP. Therefore, the reported assets and liabilities for Rangers and FelCor LP are substantially identical.

RLJ LP owns 100% of Rangers. Rangers indirectly owns 99% of FelCor LP. A wholly-owned subsidiary of RLJ LP owns the remaining 1% of FelCor LP, which is a noncontrolling interest that is reflected within the equity section of the consolidated balance sheets and in the consolidated statements of equity. Apart from the different equity treatment, the consolidated financial statements for Rangers and FelCor LP are nearly identical, except that net income (loss) attributable to the 1% noncontrolling interest in FelCor LP is deducted from Rangers' net income (loss) in order to arrive at net income (loss) attributable to Rangers.

We present the sections in this report combined unless separate disclosure is required for clarity.

RLJ accounted for the Mergers noted above under the acquisition method of accounting in ASC 805, Business Combinations. In accordance with the guidance, RLJ elected to apply pushdown accounting to our consolidated financial statements in order to reflect the new basis of accounting established by RLJ for the individual assets acquired and the liabilities assumed in the Mergers. Accordingly, our consolidated financial statements for the periods before and after the Acquisition Date reflect different bases of accounting, and the financial positions and the results of operations for those periods are not comparable. As a result, the consolidated financial statements and the notes to those financial statements are separated into two distinct periods; the periods prior to the Acquisition Date are identified as "Predecessor," and the periods after the Acquisition Date are identified as "Successor." The new basis of accounting for the assets and liabilities that existed on the Acquisition Date will be used in the preparation of our future financial statements and footnotes.

1

TABLE OF CONTENTS

Item No. | Form 10-K Report Page | |

PART I | ||

PART II | ||

PART III | ||

PART IV | ||

2

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

Certain statements in this Annual Report on Form 10-K, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives and expected operating results, and the assumptions upon which those statements are based, are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements generally are identified by the use of the words "believe," "project," "expect," "anticipate," "estimate," "plan," "may," "will," "will continue," "intend," "should," "may" or similar expressions. Although we believe that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, beliefs and expectations, such forward-looking statements are not predictions of future events or guarantees of future performance and our actual results could differ materially from those set forth in the forward-looking statements. Some factors that might cause such a difference include the following: the current global economic uncertainty, increased direct competition, changes in government regulations or accounting rules, changes in local, national and global real estate conditions, declines in the lodging industry, seasonality of the lodging industry, risks related to natural disasters, such as earthquakes and hurricanes, hostilities, including future terrorist attacks or fear of hostilities that affect travel, our ability to obtain lines of credit or permanent financing on satisfactory terms, changes in interest rates, and inaccuracies of our accounting estimates. A discussion of these and other risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included in "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" within this Annual Report on Form 10-K. Given these uncertainties, undue reliance should not be placed on such statements. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Except where the context suggests otherwise, we define certain terms in this Annual Report on Form 10-K as follows:

• | "our company," "we," "us" and "our" refer to Rangers and FelCor LP, collectively (including their consolidated subsidiaries) following the Mergers and to FelCor and FelCor LP, collectively (including their consolidated subsidiaries) prior to consummation of the Mergers, unless the content indicates otherwise; |

• | "our hotel properties" refers to the 28 hotels owned by us as of December 31, 2019; |

• | a "compact full-service hotel" typically refers to any hotel with (1) less than 300 guestrooms and less than 12,000 square feet of meeting space or (2) more than 300 guestrooms where, unlike traditional full-service hotels, the operations focus primarily on the rental of guestrooms such that a significant majority of its total revenue is generated from room rentals rather than other sources, such as food and beverage; |

• | "Average Daily Rate" ("ADR") represents the total hotel room revenues divided by the total number of rooms sold in a given period; |

• | "Occupancy" represents the total number of hotel rooms sold in a given period divided by the total number of rooms available; and |

• | "Revenue Per Available Room" ("RevPAR") is the product of ADR and Occupancy. |

For a more in depth discussion of ADR, Occupancy and RevPAR, please refer to the "Key Indicators of Operating Performance" section.

3

PART I

Item 1. Business

Our Company

Rangers is a Maryland limited liability company that, through FelCor LP, owns hotel properties and conducts other business. Substantially all of Rangers' assets and liabilities are held by, and all of its operations are conducted through, FelCor LP. 100% of the ownership interests of Rangers are held by RLJ LP, which is the operating partnership of RLJ, one of the largest U.S. publicly traded lodging real estate investment trusts ("REIT") in terms of both number of hotels and number of rooms. Rangers indirectly owns a 99% partnership interest in FelCor LP. Rangers General Partner, LLC ("Rangers GP"), a wholly-owned subsidiary of RLJ LP, owns the remaining 1% partnership interest and is the sole general partner of FelCor LP.

Our hotels are concentrated in markets that we believe exhibit multiple demand generators and attractive long-term growth prospects. We believe premium-branded, compact full-service hotels with these characteristics generate high levels of RevPAR, strong operating margins and attractive returns.

As of December 31, 2019, we owned 28 hotel properties with approximately 8,100 rooms, located in 13 states. We owned, through wholly-owned subsidiaries, a 100% interest in 25 of our hotel properties, a 95% controlling interest in The Knickerbocker, and 50% interests in entities owning two hotel properties. We consolidate our real estate interests in the 26 hotel properties in which we hold a controlling financial interest, and we record the real estate interests in the two hotel properties in which we hold an indirect 50% interest using the equity method of accounting. We lease 27 of the 28 hotel properties to subsidiaries of RLJ LP.

Merger with RLJ

On August 31, 2017, RLJ, RLJ LP, Rangers, Partnership Merger Sub, FelCor and FelCor LP consummated the transactions contemplated by the Merger Agreement, whereby Partnership Merger Sub merged with and into FelCor LP, with FelCor LP surviving as a wholly-owned subsidiary of RLJ LP, and immediately thereafter, FelCor merged with and into Rangers, with Rangers surviving as a wholly-owned subsidiary of RLJ LP.

Upon completion of the REIT Merger and under the terms of the Merger Agreement, each issued and outstanding share of FelCor common stock (other than shares held by any wholly-owned subsidiary of FelCor) was converted into the right to receive 0.362 (the “Common Exchange Ratio”) of RLJ's common shares, and each issued and outstanding share of FelCor $1.95 Series A cumulative convertible preferred stock was converted into the right to receive one of RLJ's $1.95 Series A cumulative convertible preferred shares.

Upon completion of the Partnership Merger and under the terms of the Merger Agreement, each limited partner of FelCor LP was entitled to elect to exchange its outstanding common limited partnership units in FelCor LP (the "FelCor LP Common Units") for a number of RLJ's newly issued common shares based on the Common Exchange Ratio. Upon completion of the Partnership Merger, each outstanding FelCor LP Common Unit of any holder who did not make the foregoing election was converted into the right to receive a number of units of limited partnership interest in RLJ LP ("OP units") based on the Common Exchange Ratio. No fractional shares or units of RLJ's common shares or RLJ LP's OP units were issued in the Mergers, and the value of any fractional interests was paid in cash.

At the closing of the Mergers, FelCor LP had controlling financial interests in various hotel property-owning subsidiaries (the "FelCor Lessors"), and FelCor TRS Holdings, LLC ("FelCor TRS") and its property-operating subsidiaries (the "FelCor Lessees"). The hotel properties were leased through intercompany lease agreements between the FelCor Lessors and the FelCor Lessees, resulting in the FelCor Lessees' payments being eliminated in consolidation. Immediately after the consummation of the Mergers and RLJ's push down of the allocation of the purchase price consideration, FelCor LP distributed the equity interests in FelCor TRS to RLJ LP. As a result of the distribution of the equity interests in FelCor TRS, the FelCor Lessees' payments pursuant to the leases are no longer eliminated in consolidation of our consolidated financial statements.

Additional information on the Mergers can be found in Note 2 to our accompanying consolidated financial statements.

The Lodging Industry

The lodging industry in the United States consists of public and private entities that operate in an extremely diversified market under a variety of brand names. The key participants in the lodging industry are as follows:

4

• | Owners — own the hotel property and typically enter into a management agreement with an independent third party to manage the hotel property. The hotel properties may be branded and operated under the manager’s brand or branded under a separate franchise agreement. |

• | Franchisors — own a brand or brands and provide the franchised hotels with brand recognition, marketing support and worldwide reservation systems. |

• | Managers — responsible for the day-to-day operation of the hotel property, including the employment of the hotel staff, the determination of room rates, the development of sales and marketing plans, the preparation of operating and capital expenditure budgets and the preparation of financial reports for the owner. |

Our Investment and Business Strategies

Both Rangers and FelCor LP are wholly-owned subsidiaries of RLJ LP, therefore, Rangers and FelCor LP carry out RLJ's investment and business strategies, which are noted below.

RLJ's objective is to generate strong returns for its shareholders by acquiring and owning primarily premium-branded, focused-service and compact full-service hotels at prices where it believes it can generate attractive returns on investment and long-term value appreciation through proactive asset management. RLJ also intends to selectively dispose of hotel properties when it believes the returns have been maximized or the hotel properties no longer meet its strategy in order to have investment capacity for other opportunities, which may include acquisitions. RLJ intends to pursue this objective through the following investment and business strategies:

Investment Strategies

• | Targeted ownership of premium-branded, focused-service and compact full-service hotels. RLJ believes that premium-branded, focused-service and compact full-service hotels have the potential to generate attractive returns relative to other types of hotels due to their ability to achieve RevPAR levels at or close to those generated by traditional full-service hotels, while achieving higher profit margins due to their more efficient operating model and less volatile cash flows. |

• | Use of premium hotel brands. RLJ believes in affiliating its hotels with premium brands owned by leading international franchisors such as Hilton, Wyndham and Marriott. RLJ believes that utilizing premium brands provides significant advantages because of their guest loyalty programs, worldwide reservation systems, effective product segmentation, global distribution and strong customer awareness. |

• | Focus on high-growth markets. RLJ focuses on owning and acquiring hotel properties in markets that it believes exhibit multiple demand generators and attractive long-term growth prospects. As a result, RLJ believes that these hotel properties generate higher returns on investment. |

Business Strategies

• | Maximize returns from our hotel properties. RLJ believes that its hotel properties have the potential to generate improvements in RevPAR and earnings before interest, taxes, depreciation and amortization ("EBITDA") as a result of its proactive asset management and the anticipated long-term growth in the United States economy. RLJ actively monitors and advises its third-party management companies on most aspects of its hotels' operations, including property positioning, physical design, capital planning and investment, guest experience and overall strategic direction. RLJ regularly reviews opportunities to further invest in its hotel properties in an effort to enhance quality and attractiveness, increase long-term value and generate attractive returns on investment. |

• | Pursue a disciplined hotel acquisition strategy. RLJ seeks to acquire additional hotel properties at prices below replacement cost where it believes it can generate attractive returns on investment. RLJ intends to target acquisition opportunities where it can enhance value by pursuing proactive investment strategies such as renovation, repositioning or rebranding. |

• | Pursue a disciplined capital recycling program. RLJ intends to continue to pursue a disciplined capital allocation strategy designed to maximize the return on its investments by selectively selling hotel properties that are no longer consistent with its investment strategy or whose returns appear to have been maximized. To the extent that RLJ sells its hotel properties, RLJ intends to redeploy the capital into other investment opportunities, including without limitation, acquisitions, brand conversions, green initiatives and space configuration opportunities. |

5

• | Continue to improve its balance sheet. RLJ intends to continue to maintain a flexible capital structure that allows it to execute its strategy. RLJ believes that a strong balance sheet is a key competitive advantage that affords it a lower cost of capital and positions it for growth. RLJ structures its debt profile to maintain financial flexibility and a balanced maturity schedule with access to different forms of financing. |

• | Execute its share repurchase program. RLJ intends to create value over the long-term for its shareholders by deploying investment capacity into share repurchases during periods of share price dislocation. |

Our Hotels

Our hotel properties operate under strong, premium brands, with approximately 93% of our hotel properties operating under existing relationships with Hilton, Wyndham or Marriott. The following table sets forth the brand affiliations of our hotel properties as of December 31, 2019:

Brand Affiliations | Number of hotels | Percentage of total hotels | Number of rooms | Percentage of total rooms | ||||||||

Hilton | ||||||||||||

Embassy Suites | 15 | 53.6 | % | 4,293 | 52.7 | % | ||||||

DoubleTree | 2 | 7.1 | % | 417 | 5.1 | % | ||||||

Subtotal | 17 | 60.7 | % | 4,710 | 57.8 | % | ||||||

Marriott | ||||||||||||

Marriott | 1 | 3.6 | % | 401 | 4.9 | % | ||||||

Subtotal | 1 | 3.6 | % | 401 | 4.9 | % | ||||||

Wyndham | ||||||||||||

Wyndham | 8 | 28.6 | % | 2,528 | 31.1 | % | ||||||

Subtotal | 8 | 28.6 | % | 2,528 | 31.1 | % | ||||||

Other Brand Affiliation | 2 | 7.1 | % | 501 | 6.2 | % | ||||||

Total | 28 | 100.0 | % | 8,140 | 100.0 | % | ||||||

Asset Management

RLJ has a dedicated team of asset management professionals that proactively work with the third-party management companies to maximize profitability at each of our hotels. The asset management team monitors the performance of our hotels on a daily basis and holds frequent ownership meetings with corporate operations executives and key personnel at the hotels. The asset management team works closely with the third-party management companies on key aspects of each hotel's operation, including, among others, revenue management, market positioning, cost structure, capital and operational budgeting, as well as the identification and evaluation of return on investment initiatives and overall business strategy. In addition, RLJ retains approval rights on key staffing positions at many of our hotels, such as the hotel's general manager and director of sales. We believe that the strong asset management process helps to ensure that each hotel is being operated to our and the franchisors' standards, that our hotel properties are being adequately maintained in order to preserve the value of the asset and to ensure the safety of our customers, and that the management companies are maximizing revenues, profits and operating margins.

Competition

The U.S. lodging industry is highly competitive. Our hotel properties compete with other participants in the lodging industry for guests in each of their markets on the basis of several factors, including, among others, location, quality of accommodations, convenience, brand affiliation, room rates, service levels, amenities and the availability of lodging and event space. Competition is often specific to the individual markets in which our hotel properties are located and includes competition from existing and new hotels in the compact full-service hotel segment and non-traditional accommodations for travelers, such as online room sharing services. We believe that hotels, such as our hotels, that are affiliated with leading national brands, such as the Hilton, Wyndham and Marriott brands, will enjoy competitive advantages associated with operating under such brands.

Seasonality

6

The lodging industry is seasonal in nature, which can cause quarterly fluctuations in our revenues. For example, our hotels in Pennsylvania experience lower revenues and profits during the winter months of December through March, while our hotels in Florida generally have higher revenues in the months of January through April. This seasonality can be expected to cause periodic fluctuations in a hotel's room revenues, occupancy levels, room rates, operating expenses and cash flows.

Our Financing Strategy

We carry out RLJ's financing strategy, which is to continue to maintain a prudent capital structure by limiting its net debt-to-EBITDA ratio to 4.0x or below. RLJ defines net debt as total indebtedness minus cash and cash equivalents. Over time, RLJ intends to finance its long-term growth with equity issuances and debt financing with staggered maturities. RLJ's strategy with respect to its debt profile is to primarily have unsecured debt and a greater percentage of fixed rate and hedged floating rate debt as compared to unhedged floating rate debt. Our debt is currently comprised of unsecured senior notes and mortgage loans secured by our hotel properties. We have a mix of fixed and floating rate debt; however, the majority of our debt bears interest at fixed rates.

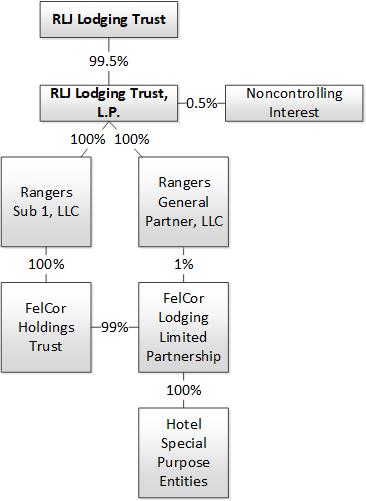

Organizational Structure

RLJ is a Maryland real estate investment trust that conducts its business through a traditional umbrella partnership real estate investment trust ("UPREIT") in which its hotel properties are indirectly owned by RLJ LP, through limited partnerships, limited liability companies or other subsidiaries. RLJ is the sole general partner of RLJ LP and, as of December 31, 2019, RLJ owned 99.5% of the OP units in RLJ LP.

Rangers was formed as a Maryland corporation in April 2017 and FelCor LP was formed as a Delaware limited partnership in May 1994. RLJ LP owns 100% of Rangers. Rangers indirectly owns a 99% partnership interest in FelCor LP. A wholly-owned subsidiary of RLJ LP owns the remaining 1% of FelCor LP. Through FelCor LP, Rangers owns hotel properties and conducts other business.

7

The following chart generally depicts our corporate structure as of December 31, 2019:

Regulation

General

Our hotel properties are subject to various U.S. federal, state and local laws, ordinances and regulations, including regulations relating to common areas and fire and life safety requirements. We believe that each of our hotel properties has the necessary permits and approvals to operate its business.

Americans with Disabilities Act

Our hotel properties must comply with the applicable provisions of the Americans with Disabilities Act of 1990 and the Accessibility Guidelines promulgated thereunder (the "ADA"), to the extent that such hotels are "public accommodations" as defined by the ADA. The ADA may require the removal of structural barriers to access by persons with disabilities in certain public areas of our hotels where such removal is readily achievable. We believe that our hotel properties are in substantial compliance with the ADA and that we will not be required to make substantial capital expenditures to address the requirements of the ADA. However, non-compliance with the ADA could result in imposition of fines or an award of damages to private litigants. The obligation to make readily achievable accommodations is an ongoing one, and we will continue to assess our hotels and to make alterations as appropriate in this respect.

8

Environmental Matters

Under various federal, state and local laws, ordinances and regulations relating to the protection of the environment, a current or previous owner or operator (including tenants) of real estate may be subject to liability related to contamination resulting from the presence or discharge of hazardous or toxic substances at that property and may be required to investigate and clean up such contamination at that property or emanating from that property. These costs could be substantial and liability under these laws may attach without regard to whether the owner or operator knew of, or was responsible for, the presence of the contaminants, and the liability may be joint and several. The presence of contamination or the failure to remediate contamination at our hotels may expose us to third-party liability for cleanup costs, property damage or bodily injury, natural resource damages and costs or expenses related to liens or property use restrictions and materially and adversely affect our ability to sell, lease or develop the real estate or to incur debt using the real estate as collateral.

Our hotel properties are subject to various federal, state, and local environmental, health and safety laws and regulations. Our hotel properties incur costs to comply with these laws and regulations and could be subject to fines and penalties for non-compliance. The costs of complying with environmental, health and safety laws could increase as new laws are enacted and existing laws are modified.

Some of our hotel properties contain asbestos-containing building materials. We believe that the asbestos is appropriately contained in accordance with current environmental regulations and that we have no need for any immediate remediation or current plans to remove the asbestos.

We believe that our hotel properties are in compliance, in all material respects, with all federal, state and local environmental ordinances and regulations regarding hazardous or toxic substances and other environmental matters, the violation of which could have a material adverse effect on us. Although we have not received written notice from any governmental authority of any material noncompliance, liability or claim relating to hazardous or toxic substances or other environmental matters in connection with any of our present properties, we can offer no assurance that a material environmental claim will not be asserted against us in the future.

Insurance

RLJ carries comprehensive general liability, fire, extended coverage, business interruption, rental loss coverage and umbrella liability coverage on all of our hotels, and earthquake, wind, flood and hurricane coverage on hotels in areas where RLJ believes such coverage is warranted, in each case with limits of liability that RLJ deems adequate. Similarly, RLJ is insured against the risk of direct physical damage in amounts it believes to be adequate to reimburse itself, on a replacement cost basis, for the costs incurred to repair or rebuild each hotel, including loss of income during the reconstruction period. RLJ has selected policy specifications and insured limits which it believes to be appropriate given the relative risk of loss, the cost of the coverage and industry practice. RLJ does not carry insurance for generally uninsurable risks, including, but not limited to losses caused by riots, war or acts of God. In the opinion of RLJ's management, our hotels are adequately insured.

Employees

As of December 31, 2019, RLJ LP had 87 employees. Rangers and FelCor LP do not have any employees.

Corporate Information

Our principal executive offices are located at 3 Bethesda Metro Center, Suite 1000, Bethesda, Maryland 20814, which is RLJ's corporate headquarters. Our telephone number is (301) 280-7777. We do not have our own website, but RLJ's website is located at www.rljlodgingtrust.com. The information that is found on or accessible through RLJ's website is not incorporated into, and does not form a part of, this Annual Report on Form 10-K or any other report or document that we file with or furnish to the Securities and Exchange Commission (the "SEC"). We have included RLJ's website address in this Annual Report on Form 10-K as an inactive textual reference and do not intend it to be an active link to RLJ's website.

RLJ does not make available on its website our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. However, upon filing those reports with, or furnishing them to, the SEC, those reports can be viewed on the SEC's website. On RLJ's website, specifically the Corporate Governance page under the Investor Relations section, there are various documents related to RLJ's corporate governance including its: Board Committee Charters; Corporate Governance Guidelines; Code of Business Conduct and Ethics; Complaint Procedures for Financial and Auditing Matters; Declaration of Trust; and Bylaws.

9

This Annual Report on Form 10-K and other reports filed with the SEC are available on the SEC's website, which contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The SEC's website address is www.sec.gov.

Item 1A. Risk Factors

Set forth below are the risks that we believe are material to our stakeholders. You should carefully consider the following risks in evaluating our Company and our business. The occurrence of any of the following risks could materially and adversely impact our financial condition, results of operations, cash flows, and our ability to, among other things, satisfy our debt service obligations. Some statements in this report including statements in the following risk factors constitute forward-looking statements. Please refer to the section entitled "Special Note About Forward-Looking Statements" at the beginning of our Annual Report on Form 10-K.

Risks Related to Our Business and Hotel Properties

We will continue to be significantly influenced by the economies and other conditions in the specific markets in which we operate, particularly in the metropolitan areas where we have high concentrations of hotels.

Our hotels are located in metropolitan and resort areas which may be susceptible to adverse market conditions, including industry downturns, relocation of businesses, any oversupply of hotel rooms, political unrest or a reduction in lodging demand. Adverse economic developments in the markets in which we have a concentration of hotels, or in any of the other markets in which we operate, or any increase in hotel supply or decrease in lodging demand resulting from the local, regional or national business or political climate, could materially and adversely affect us.

We are dependent on the performance of the third-party management companies that manage the operations of each of our hotels and we could be materially and adversely affected if such third-party hotel managers do not manage our hotels in our best interests.

Our hotel properties are operated by third-party hotel managers pursuant to management agreements. There are individual management agreements for all of our hotel properties.

Under the terms of the management agreements, the hotel managers are responsible for all aspects of the operations of our hotels, including ensuring those operations are conducted in accordance with applicable laws and regulations and in our best interests, and our ability to participate in operating decisions regarding our hotels is limited to certain matters, including approval of the annual operating budget. While we closely monitor the performance and operations of the third-party hotel managers, we cannot assure you that the hotel managers will manage our hotels in a manner that is consistent with their respective obligations under the applicable management agreement or the obligations under the franchise agreements our hotel properties are subject to.

The success of our hotel properties depends largely on RLJ's ability to establish and maintain good relationships with the hotel managers. From time to time, disputes may arise between RLJ and the third-party managers regarding their performance or compliance with the terms of the management agreements, which in turn could adversely affect our results of operations. If RLJ is unable to reach satisfactory results through discussions and negotiations, it may choose to terminate the management agreement, litigate the dispute or submit the matter to third-party dispute resolution, the outcome of which may be unfavorable to us.

In the event that any of the management agreements our hotel properties are subject to are terminated, we can provide no assurances that a replacement manager can be found or that the franchisors will consent to a replacement manager in a timely manner, or at all, or that any replacement manager will be successful in operating our hotels.

We are subject to the risks associated with the employment of hotel personnel, particularly with hotels that employ unionized labor.

10

The third-party management companies that manage our hotel properties are responsible for hiring and maintaining the labor force at each of our hotels. Although we do not directly employ or manage the employees at our hotels, we still are subject to many of the costs and risks generally associated with the hotel labor force, particularly those hotels with unionized labor. From time to time, the hotel operations may be disrupted as a result of strikes, lockouts, public demonstrations or other negative actions and publicity. The resolution of labor disputes or re-negotiated labor contracts could lead to higher labor costs, either by increases in wages or benefits or by changes in work rules that raise hotel operating costs. We do not have the ability to affect the outcome of these negotiations.

Restrictive covenants in certain of the management and franchise agreements our hotel properties are subject to contain provisions limiting or restricting the sale or financing of our hotels, which could have a material and adverse effect on us.

The management and franchise agreements typically contain restrictive covenants that limit or restrict our ability to sell or refinance a hotel without the consent of the management company or franchisor. Many of the franchise agreements our hotel properties are subject to provide the franchisor with a right of first offer in the event of certain sales or transfers of a hotel and provide that the franchisor has the right to approve any change in the management company engaged to manage the hotel. Generally, we may not agree to sell, lease or otherwise transfer particular hotels unless the transferee is not a competitor of the management company or franchisor and the transferee assumes the related management and franchise agreements. If the management company or franchisor does not consent to the sale or financing of our hotels, we may be prohibited from taking actions that would otherwise be in our best interests.

Substantially all of our hotel properties operate under either Hilton, Wyndham or Marriott brands; therefore, we are subject to the risks associated with concentrating our portfolio in just three brand families.

26 of the 28 hotel properties that we owned as of December 31, 2019 utilize brands owned by Hilton, Wyndham or Marriott. As a result, our success is dependent in part on the continued success of Hilton, Wyndham or Marriott and their respective brands. We believe that building brand value is critical to increasing demand and building customer loyalty. Consequently, if market recognition or the positive perception of Hilton and/or Wyndham and/or Marriott is reduced or compromised, the goodwill associated with the Hilton-, Wyndham- or Marriott-branded hotels in our portfolio may be adversely affected. Furthermore, if our relationship with Hilton, Wyndham or Marriott were to deteriorate or terminate as a result of disputes regarding the management of our hotels or for other reasons, Hilton and/or Wyndham and/or Marriott could, under certain circumstances, terminate the current franchise licenses that our hotel properties are subject to or decline to provide franchise licenses for our hotel properties in the future. If any of the foregoing were to occur, it could have a material adverse effect on us.

Any difficulties in obtaining the capital necessary to make required periodic capital expenditures and to renovate our hotel properties could materially and adversely affect our financial condition and results of operations.

Our hotel properties have an ongoing need for renovations and other capital improvements, including the replacement of furniture, fixtures and equipment ("FF&E"). Our lenders will also likely require that we set aside annual amounts for capital improvements to our hotel properties. The costs of these capital improvements could materially and adversely affect us. If we are unable to obtain the capital necessary to make the required periodic capital expenditures and to renovate our hotel properties on favorable terms, or at all, our financial condition, liquidity and results of operations could be materially and adversely affected.

Adverse global market and economic conditions and dislocations in the markets could materially and adversely affect the value of our hotel properties and our business, financial condition and results of operations.

We can provide no assurance that adverse changes in the global or domestic economy will not have an adverse effect on

the hotel revenue or earnings at our hotel properties. A reduction in our revenue or earnings as a result of an adverse change in

the economy may reduce our working capital and revenue, impact our long-term business strategy and impact the value of our

assets. In addition, we may incur impairment charges in the future, which charges will affect negatively our results of

operations. We can provide no assurance that an impairment loss recognized will not be material to our results of operations.

Competition from other lodging industry participants in the markets in which we operate could adversely affect occupancy levels and/or ADRs, which could have a material and adverse effect on us.

11

We face significant competition from owners and operators of other hotels and other lodging industry participants. In addition, we face competition from non-traditional accommodations for travelers, such as online room sharing services. We compete based on a number of factors, including location, quality of accommodations, convenience, brand affiliation, room rates, service levels, amenities, customer service, and the availability of lodging and event space. Our competitors may have an operating model that enables them to offer accommodations at lower rates than we can, which could result in our competitors increasing their occupancy at our expense and adversely affecting our ADRs. Given the importance of occupancy and ADR at compact full-service hotels, this competition could adversely affect our ability to attract prospective guests, which could materially and adversely affect our business, financial condition and results of operations.

At December 31, 2019, we had approximately $798.7 million of debt outstanding, which could materially and adversely affect our operating performance and put us at a competitive disadvantage.

Required repayments of debt and related interest may materially and adversely affect our operating performance. At December 31, 2019, we had approximately $798.7 million of outstanding debt, of which approximately $181.0 million bears interest at variable rates. Increases in interest rates on our existing or future variable rate debt would increase our interest expense, which could adversely affect our cash flows.

Because we anticipate that our operating cash will be adequate to repay only a portion of our debt at maturity, we expect that we will be required to repay debt through debt refinancings and/or offerings of our securities. The amount of our outstanding debt may adversely affect our ability to refinance our debt.

If we are unable to refinance our debt on acceptable terms, or at all, we may be forced to dispose of one or more of our hotels on disadvantageous terms, which may result in losses to us. In addition, if the prevailing interest rates or other factors at the time of refinancing result in higher interest rates upon refinancing, our interest expense would increase, which would adversely affect our future operating results and liquidity.

Our outstanding debt, and any additional debt borrowed in the future, may subject us to many risks, including the risk that:

• | our cash flows from operations may be insufficient to make required payments of principal and interest; |

• | we may be at a competitive disadvantage compared to our competitors that have less debt; |

• | we may be vulnerable to economic volatility, particularly if growth were to slow or stall and reduce our flexibility to respond to difficult market, industry, or economic conditions; |

• | the terms of any refinancing may not be in the same amount or on terms as favorable as the terms of the debt being refinanced; and |

• | the use of leverage could adversely affect our ability to borrow more money for operations and capital improvements. |

Disruptions in the financial markets could adversely affect our ability to obtain sufficient third-party financing for our capital needs on favorable terms, or at all, which could materially and adversely affect us.

In recent years, the U.S. financial markets experienced significant price volatility, dislocations and liquidity disruptions, which caused stock market prices to fluctuate substantially and the spreads on prospective debt financings to widen considerably. Renewed volatility and uncertainty in the financial markets may negatively impact our ability to access additional financing for our capital needs, including growth, acquisition activities and other business initiatives, on favorable terms or at all, which may negatively affect our business. Additionally, due to this potential uncertainty, in the future we may be unable to refinance or extend our debt, or the terms of any refinancing may not be as favorable as the terms of our existing debt. If we are not successful in refinancing our debt when it becomes due, we may be forced to dispose of hotels on disadvantageous terms, which may adversely affect our ability to service other debt and to meet our other liquidity and business obligations. A prolonged downturn in the financial markets may cause us to seek alternative capital sources of potentially less attractive financing and may require us to further adjust our business plan accordingly. These events also may make it more difficult or costly for us to raise capital through the issuance of new equity or the incurrence of additional secured or unsecured debt, which could materially and adversely affect us.

Replacement of the LIBOR benchmark interest rate could materially and adversely affect our business, financial condition, results of operations and cash flows.

12

In 2017, the United Kingdom’s Financial Conduct Authority (“FCA”), which regulates the London Interbank Offered Rate (“LIBOR”), announced that the FCA intends to stop persuading or compelling banks to submit the rates required to calculate LIBOR after 2021. This announcement indicates that the continuation of LIBOR on the current basis cannot and will not be guaranteed after 2021. Consequently, at this time, it is not possible to predict whether and to what extent banks will continue to provide submissions for the calculation of LIBOR. Similarly, it is not possible to predict whether LIBOR will continue to be viewed as an acceptable market benchmark or what rate or rates may become acceptable alternatives to LIBOR. The transition from LIBOR could create considerable costs and additional risk, which could materially and adversely impact our financial condition or results of operations.

Our existing indebtedness contains covenants and our failure to comply with all covenants in our debt agreements could materially and adversely affect us.

Our existing indebtedness contains customary and financial covenants that may limit our ability to enter into future indebtedness. Our failure to comply with covenants in our existing or future indebtedness, as well as our inability to make required principal and interest payments, could cause a default under the applicable debt agreement, which could result in the acceleration of the debt and require us to repay such debt with capital obtained from other sources, which may not be available to us or may be available only on unattractive terms. Furthermore, if we default on secured debt, lenders can take possession of the hotel(s) securing such debt. In addition, debt agreements may contain specific cross-default provisions with respect to specified other indebtedness, giving the lenders the right to declare a default on its debt and to enforce remedies, including accelerating the maturity of such debt upon the occurrence of a default under such other indebtedness. If we default on our debt agreements, we could be materially and adversely affected.

Joint venture investments that we make could be adversely affected by our lack of sole decision-making authority, our reliance on joint venture partners' financial condition and liquidity and disputes between us and our joint venture partners.

We own certain hotel properties and other real estate investments through joint ventures. In the future, we may enter into additional joint ventures to acquire, develop, improve or partially dispose of hotel properties, thereby reducing the amount of capital required by us to make investments and diversifying our capital sources for growth. Such joint venture investments involve risks not otherwise present in a wholly-owned hotel property or a redevelopment project, including the following:

• | we may not have exclusive control over the development, financing, leasing, management and other aspects of the hotel property or the joint venture, which may prevent us from taking actions that are in our best interest but opposed by our partners; |

• | joint venture agreements often restrict the transfer of a partner's interest or may otherwise restrict our ability to sell the interest when we desire, or on advantageous terms; |

• | joint venture agreements may contain buy-sell provisions pursuant to which one partner may initiate procedures requiring the other partner to choose between buying the other partner's interest or selling its interest to that partner; |

• | a partner may, at any time, have economic or business interests or goals that are, or that may become, inconsistent with our business interests or goals; |

• | a partner may fail to fund its share of required capital contributions or may become bankrupt, which would mean that we and any other remaining partners generally would remain liable for the joint venture's liabilities; or |

• | we may, in certain circumstances, be liable for the actions of a partner, and the activities of a partner could adversely affect RLJ's ability to qualify as a REIT, even though we do not control the joint venture. |

Any of the above might subject a hotel property to liabilities in excess of those contemplated and adversely affect the value of our current and future joint venture investments.

13

Risks Related to the Lodging Industry

The seasonality of the lodging industry could have a material and adverse effect on us.

The lodging industry is seasonal in nature, which causes quarterly fluctuations in our revenues. Our quarterly earnings may be adversely affected by factors outside our control, including weather conditions and poor economic factors in certain markets in which we operate. The seasonality causes periodic fluctuations in room revenues, occupancy levels, room rates and operating expenses in particular hotels. We can provide no assurances that our cash flows will be sufficient to offset any shortfalls that occur as a result of these fluctuations. Consequently, volatility in our financial performance resulting from the seasonality of the lodging industry could have a material and adverse effect on us.

The cyclical nature of the lodging industry may cause fluctuations in our operating performance, which could have a material and adverse effect on us.

The lodging industry historically has been highly cyclical in nature. Fluctuations in lodging demand and, therefore, operating performance, are caused largely by general economic and local market conditions, which subsequently affect levels of business and leisure travel. In addition to general economic conditions, new hotel room supply is an important factor that can affect the lodging industry's performance, and overbuilding has the potential to further exacerbate the negative impact of an economic recession. Room rates and occupancy, and thus RevPAR, tend to increase when demand growth exceeds supply growth. We can provide no assurances regarding whether, or the extent to which, lodging demand will rebound or whether any such rebound will be sustained. An adverse change in lodging fundamentals could result in returns that are substantially below our expectations or result in losses, which could have a material and adverse effect on us.

Our ownership of hotel properties with ground leases exposes us to the risks that we may be forced to sell such hotel properties for a lower price, we may have difficulties financing such hotel properties, we may be unable to renew a ground lease or we may lose such hotel properties upon breach of a ground lease.

As of December 31, 2019, six of our consolidated hotel properties and two of our unconsolidated hotel properties were on land subject to ground leases. Accordingly, we only own a long-term leasehold or similar interest in those eight hotel properties. Two of the ground leases expire in 2028 and 2029. Our ground lease agreements require the consent of the lessor or sub-lessor prior to transferring our interest in the ground lease. These provisions may impact our ability to sell our hotel properties which, in turn, could adversely impact the price realized from any such sale. In addition, at any given time, investors may be disinterested in buying hotel properties subject to a ground lease and may pay a lower price for such hotel properties than for a comparable hotel property with a fee simple interest or they may not purchase such hotel properties at any price. Secured lenders may be unwilling to lend, or otherwise charge higher interest rates, for loans secured by a leasehold mortgage as compared to loans secured by a fee simple mortgage. If we are found to be in breach of a ground lease, we could lose the right to use the hotel property. In addition, unless we can purchase a fee simple interest in the underlying land and improvements or extend the terms of these leases before their expiration, as to which no assurance can be given, we will lose our right to own these hotel properties and our interest in the improvements upon expiration of the leases. If we were to lose the right to use a hotel property due to a breach or non-renewal of the ground lease, we would be unable to derive income from such hotel property and we would be required to purchase an interest in another hotel property in an attempt to replace that income, which could materially and adversely affect us.

Technology is used in our operations, and any material failure, inadequacy, interruption or security failure of that technology could harm the business.

We, and the hotel managers and franchisors, rely on information technology networks and systems to process, transmit and store electronic information, and to manage or support a variety of business processes, including financial transactions and records, personal identifiable information, reservations, billing and operating data. These information technology networks and systems can be vulnerable to threats such as system, network or internet failures; computer hacking or business disruption; cyber-terrorism; viruses, worms or other malicious software programs; and employee error, negligence or fraud. Although we believe we and the hotel managers and franchisors have taken commercially reasonable steps to protect the security of our systems, there can be no assurance that such security measures will prevent failures, inadequacies or interruptions in system services, or that system security will not be breached.

In addition to the information technology networks and systems of the hotel managers that are used to operate our hotel properties, RLJ has its own corporate information technology networks and systems that are used to access, store, transmit, and manage or support a variety of business processes. There can be no assurance that the security measures we have taken to protect the contents of these information technology networks and systems will succeed. Any failure to maintain proper

14

function, security and availability of information technology networks and systems could interrupt our operations, our financial reporting and compliance, damage our reputation, and subject us to liability claims or regulatory penalties, which could have a material and adverse effect on our business, financial condition and results of operations.

Future terrorist attacks or changes in terror alert levels could materially and adversely affect us.

Historically, terrorist attacks and subsequent terrorist alerts have adversely affected the U.S. travel and hospitality industries, often disproportionately to the effect on the overall economy. The extent of the impact that actual or threatened terrorist attacks in the U.S. or elsewhere could have on domestic and international travel and our business in particular cannot be determined, but any such attacks or the threat of such attacks could have a material and adverse effect on travel and hotel demand and our ability to insure our hotel properties, which could materially and adversely affect us.

The outbreak of influenza or other widespread contagious diseases could reduce travel and adversely affect hotel demand, which would have a material and adverse effect on us.

A widespread outbreak of an infectious or contagious disease in the U.S. could reduce travel and hotel demand within the lodging industry. If demand at our hotel properties decreases significantly or for a prolonged period of time as a result of an outbreak of an infectious or contagious disease, our revenue would be adversely affected, which could have a material and adverse effect on us.

We face possible risks associated with natural disasters, weather events, and the physical effects of climate change.

We are subject to the risks associated with natural disasters, weather events, and the physical effects of climate change, which can include more frequent or severe storms, droughts, hurricanes and flooding, any of which could have a material adverse effect on our properties, operations and business. Over time, our hotel properties located in coastal markets and other

areas that may be impacted by climate change, are expected to experience increases in storm intensity and rising sea-levels

causing damage to our hotel properties. As a result, we could become subject to significant losses and/or repair costs that may or may not be fully covered by insurance. Other markets may experience prolonged variations in temperature or precipitation that may limit access to the water needed to operate our hotel properties or significantly increase energy costs, which may subject those properties to additional regulatory burdens, such as limitations on water usage or stricter energy efficiency standards. Weather events and climate change may also affect our business by increasing the cost of (or making unavailable) property insurance on terms we find acceptable in areas most vulnerable to such events, increasing operating costs at our hotel properties, such as the cost of water or energy, and requiring us to expend funds as we seek to repair and protect our hotel properties against such risks. There can be no assurance that natural disasters, weather events, and climate change will not have a material adverse effect on our hotel properties, operations or business.

If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results.

To monitor the accuracy and reliability of our financial reporting, we have established an internal audit function that oversees our internal controls. In addition, we have developed policies and procedures with respect to company-wide business processes and cycles in order to implement an effective system of internal control over financial reporting. We have established controls and procedures designed to ensure that hotel revenues and expenses are properly recorded at our hotels. While we have undertaken substantial work to comply with Section 404 of the Sarbanes-Oxley Act of 2002, we cannot be certain that we will be successful in maintaining effective internal control over financial reporting and we may determine in the future that our existing internal controls need improvement. If we fail to maintain an effective system of internal control, we could be materially harmed or we could fail to meet our reporting obligations. In addition, the existence of a material weakness or significant deficiency in our internal controls could result in errors to our financial statements that could require a restatement, cause us to fail to meet our reporting obligations, result in increased costs to remediate any deficiencies, attract regulatory scrutiny or lawsuits and cause investors to lose confidence in our reported financial information.

Risks Related to the Real Estate Industry

The illiquid nature of real estate investments could significantly impede our ability to respond to changing economic, financial, and investment conditions or changes in the operating performance of our hotel properties, which could materially and adversely affect our cash flows and results of operations.

Real estate investments, including the compact full-service hotels in our portfolio, are relatively illiquid. As a result, we may not be able to sell a hotel or hotels quickly or on favorable terms in response to the changing economic, financial and

15

investment conditions or changes in the hotel's operating performance when it otherwise may be prudent to do so. We cannot predict whether we will be able to sell any hotel property we desire to sell for the price or on the terms set by us or whether any price or other terms offered by a prospective purchaser would be acceptable to us. We may be required to expend funds to correct defects or to make improvements before a hotel can be sold, and we cannot provide any assurances that we will have the funds available to correct such defects or to make such improvements. Our inability to dispose of assets at opportune times or on favorable terms could materially and adversely affect our cash flows and results of operations.

Uninsured and underinsured losses at our hotel properties could materially and adversely affect us.

We maintain comprehensive property insurance on all of our hotel properties and we intend to maintain comprehensive property insurance on any hotels that we acquire in the future, including fire, terrorism, and extended coverage. Our

comprehensive property insurance program has a $250,000 deductible per claim. In addition to the comprehensive property insurance, we maintain general liability insurance at all of our hotel properties. Our general liability insurance program has no deductible. Certain types of catastrophic losses, such as windstorms, earthquakes, floods, and losses from foreign and domestic terrorist activities may not be insurable or may not be economically insurable. Even when insurable, these policies may have high deductibles and/or high premiums. Our coastal hotel properties each have a deductible of 5% of total insured value for a named storm. Our lenders may require such insurance and our failure to obtain such insurance could constitute a default under the loan agreements, which could have a material and adverse effect on us.

In the event of a substantial loss, our insurance coverage may not be sufficient to cover the full current market value or replacement cost of our lost investment, which could have a material and adverse effect on us. Should an uninsured loss or a loss in excess of insured limits occur, or should we be unsuccessful in obtaining coverage from an insurance carrier, we could lose all or a portion of the capital we have invested in a hotel property, as well as the anticipated future revenue from the hotel property. In that event, we might nevertheless remain obligated for any mortgage debt or other financial obligations related to the hotel property.

Compliance or failure to comply with the ADA and other safety regulations and requirements could result in substantial costs.

Under the ADA, all public accommodations must meet various federal requirements related to access and use by disabled persons. Compliance with the ADA's requirements could require removal of access barriers, and non-compliance could result in the U.S. government imposing fines or private damage awards. If we are required to make substantial modifications to the hotel properties that we own or the hotel properties that we acquire, whether to comply with the ADA or other changes in governmental rules and regulations, we could be materially and adversely affected.

Our hotel properties are also subject to various federal, state and local regulatory requirements, such as state and local fire and life safety requirements. If we fail to comply with these requirements, we could incur fines or private damage awards. If we incur substantial costs to comply with the ADA or other safety regulations and requirements, our financial condition, results of operations, cash flows and our ability to satisfy our debt obligations could be materially and adversely affected.

We could incur significant costs related to government regulation and litigation with respect to environmental matters, which could have a material and adverse effect on us.

Our hotel properties are subject to various U.S. federal, state and local environmental, health and safety laws and regulations, certain of which impose liability for contamination. Under these laws, governmental entities have the authority to require us, as the current owner of a hotel property, to perform or pay for the clean-up of contamination (including hazardous substances, asbestos and asbestos-containing materials ("ACM"), waste or petroleum products) at, on, under or emanating from the hotel and to pay for natural resource damages arising from such contamination. Because these laws also impose liability on persons who owned or operated a property at the time it became contaminated, it is possible we could incur cleanup costs or other environmental liabilities even after we sell or no longer operate the hotel properties.

Certain of our hotel properties contain ACM. Federal, state and local environmental, health and safety laws require that ACM be properly managed and maintained. Such laws regarding ACM may impose fines and penalties on building owners, employers and operators for failure to comply with these requirements. In addition, third parties may seek recovery from owners or operators for personal injury associated with exposure to asbestos-containing building materials.

The liabilities and the costs associated with environmental contamination at our hotel properties, defending against the claims related to alleged or actual environmental issues, or complying with environmental, health and safety laws could be

16

material and could materially and adversely affect us. The discovery of material environmental liabilities at our hotel properties could subject us to unanticipated costs, which could significantly reduce or eliminate our profitability.

We may from time to time be subject to litigation that could expose us to uncertain or uninsured costs.

As owners of hotel properties, we may from time to time face potential claims, litigation and threatened litigation from guests, visitors to our hotel properties, contractors, sub-contractors and others. These claims and proceedings are inherently uncertain and their costs and outcomes cannot be predicted with certainty. Some of these claims may result in defense costs, settlements, fines or judgments against us, and some of which are not, or cannot be, covered by insurance. Payment of any such costs, settlements, fines or judgments that are not insured could have a material and adverse impact on our financial position and results of operations. In addition, certain litigation or the resolution of certain litigation may affect the availability or cost of some of our insurance coverage, which could materially and adversely impact our results of operations and cash flows, expose us to increased risks that would be uninsured, and/or adversely impact our ability to attract officers and trustees.

Increases in real estate taxes on our hotel properties could materially and adversely affect us.

We are subject to a variety of state and local taxes, including real estate taxes. Real estate taxes on our hotel properties may increase as tax rates change and as the properties are assessed or reassessed by taxing authorities. As a result of the Mergers, some of our hotel properties located in jurisdictions that may provide for property tax reappraisal upon a change of ownership may face such a reassessment. Additionally, all our hotel properties located in California may be reassessed as a result of changes in California laws that contain certain limitations on annual increases of assessed real estate values. We would expect to appeal any such assessments or reassessments, but we may not be successful in our efforts. If real estate or other taxes increase, our result of operations would be materially and adversely affected.

Risks Related to Taxes and the Mergers

We would incur adverse tax consequences if FelCor failed to qualify as a REIT for U.S. federal income tax purposes prior to the Mergers.

In connection with the closing of the Mergers, FelCor received an opinion of counsel to the effect that it qualified as a REIT for U.S. federal income tax purposes under the Code through the time of the Mergers. FelCor, however, did not request a ruling from the Internal Revenue Service that it qualified as a REIT. If, notwithstanding this opinion, FelCor’s REIT status prior to the Mergers were successfully challenged, we would face serious tax consequences that would substantially reduce our core funds from operations and cash available for distribution because:

• | FelCor would be subject to U.S. federal, state and local income tax on its net income at regular corporate rates for the years that it did not qualify as a REIT (and, for such years, would not be allowed a deduction for dividends paid to shareholders in computing its taxable income) and we would succeed to the liability for such taxes; and |

• | The deemed sale of assets by FelCor in the REIT Merger would be subject to U.S. federal, state and local income tax at regular corporate rates (and FelCor would not be allowed a deduction for dividends paid for the deemed liquidating distribution paid to its shareholders) and we would succeed to the liability for such taxes. |

Item 1B. Unresolved Staff Comments

None.

17

Item 2. Properties

Our Hotel Properties

The following table provides a comprehensive list of our hotel properties as of December 31, 2019:

State | Hotel Property Name | Rooms | State | Hotel Property Name | Rooms | |

Alabama | Massachusetts | |||||

Embassy Suites Birmingham | 242 | Wyndham Boston Beacon Hill | 304 | |||

Arizona | Minnesota | |||||

Embassy Suites Phoenix - Biltmore | 232 | Embassy Suites Minneapolis - Airport | 310 | |||

California | New Jersey | |||||

Embassy Suites Los Angeles - International Airport South | 349 | Embassy Suites Secaucus - Meadowlands (2) | 261 | |||

Embassy Suites Mandalay Beach - Hotel & Resort | 250 | New York | ||||

Embassy Suites Milpitas Silicon Valley | 266 | The Knickerbocker New York (3) | 330 | |||

Embassy Suites San Francisco Airport - South San Francisco | 312 | Pennsylvania | ||||

Embassy Suites San Francisco Airport - Waterfront | 340 | Wyndham Philadelphia Historic District | 364 | |||

San Francisco Marriott Union Square | 401 | Wyndham Pittsburgh University Center | 251 | |||

Wyndham San Diego Bayside | 600 | South Carolina | ||||

Wyndham Santa Monica At The Pier | 132 | The Mills House Wyndham Grand Hotel | 216 | |||

Florida | Texas | |||||

DoubleTree Suites by Hilton Orlando - Lake Buena Vista | 229 | DoubleTree Suites by Hilton Austin | 188 | |||

Embassy Suites Deerfield Beach - Resort & Spa | 244 | Embassy Suites Dallas - Love Field | 248 | |||

Embassy Suites Fort Lauderdale 17th Street | 361 | Wyndham Houston - Medical Center Hotel & Suites | 287 | |||

Embassy Suites Miami - International Airport | 318 | |||||

Embassy Suites Orlando - International Drive South/Convention Center | 244 | |||||

Georgia | ||||||

Embassy Suites Atlanta - Buckhead | 316 | |||||

Louisiana | ||||||

Chateau LeMoyne - French Quarter, New Orleans (1) | 171 | |||||

Wyndham New Orleans - French Quarter | 374 | |||||

(1) | We own an indirect 50% ownership interest in this hotel property and we account for the ownership interest using the equity method of accounting. |

(2) | We own an indirect 50% ownership interest in the real estate at this hotel property, and we record the real estate interest using the equity method of accounting. |

(3) | We own a 95% controlling ownership interest in this hotel property. |

Management Agreements

In order for our parent, RLJ, to qualify as a REIT, it cannot directly or indirectly operate any of its hotel properties. Our hotel property-owning subsidiaries (the “Lessors”) lease our hotel properties to lessees owned by TRS subsidiaries of RLJ LP (the “Lessees”), which in turn engage hotel property management companies to manage our hotel properties. As discussed in Note 2 to our accompanying consolidated financial statements, we distributed our equity interests in FelCor TRS to RLJ LP immediately after consummation of the Mergers. As a result of the distribution of our equity interests in FelCor TRS, our consolidated financial statements do not include the financial information related to the Lessees' management agreements. Although the financial information related to the Lessees' management agreements is not included in our consolidated financial statements, the management agreements noted below are still in place at our hotel properties and we are dependent on the performance of the management companies to manage the operations of each of our hotel properties.

18

As of December 31, 2019, our 28 hotel properties were managed by six different management companies as follows:

Management Company | Number of Hotel Properties | |

Aimbridge Hospitality | 1 | |

Hilton Management and affiliates | 16 | |

Highgate Hotels | 1 | |

InterContinental Hotels Group | 1 | |

Marriott International, Inc. | 1 | |

Wyndham | 8 | |

28 | ||

All but three of our hotel properties receive the benefits of a franchise agreement pursuant to management agreements with Hilton, Wyndham, Marriott and InterContinental Hotels Group ("IHG").

The management agreements have initial terms that range from five to 20 years, and some provide for one or two automatic extension periods ranging from one to ten years. Each management company receives a base management fee between 2.0% and 3.0% of hotel revenues.