Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - City Office REIT, Inc. | d770111dex322.htm |

| EX-32.1 - EX-32.1 - City Office REIT, Inc. | d770111dex321.htm |

| EX-31.2 - EX-31.2 - City Office REIT, Inc. | d770111dex312.htm |

| EX-31.1 - EX-31.1 - City Office REIT, Inc. | d770111dex311.htm |

| EX-23.1 - EX-23.1 - City Office REIT, Inc. | d770111dex231.htm |

| EX-21.1 - EX-21.1 - City Office REIT, Inc. | d770111dex211.htm |

| EX-4.3 - EX-4.3 - City Office REIT, Inc. | d770111dex43.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file no: 001-36409

CITY OFFICE REIT, INC.

| Maryland | 98-1141883 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

666 Burrard Street

Suite 3210

Vancouver, BC

V6C 2X8

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (604) 806-3366

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Trading Symbol(s) |

Name of each Exchange on Which Registered | ||

| Common Stock, $0.01 par value 6.625% Series A Cumulative Redeemable Preferred Stock, $0.01 par value per share |

“CIO” “CIO.PrA” |

New York Stock Exchange New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filter | ☐ | Accelerated filter | ☒ | |||

| Non-accelerated filter | ☐ | Smaller reporting company | ☐ | |||

| Emerging Growth Company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of June 30, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $465.7 million, based on the closing sales price of $11.99 per share as reported on the New York Stock Exchange.

As of February 24, 2020, the registrant had 54,591,047 shares of common stock outstanding.

Documents incorporated by reference: Portions of the registrant’s Definitive Proxy Statement for the 2020 Annual Meeting of Shareholders (to be filed with the United States Securities and Exchange Commission no later than 120 days after the end of the registrant’s fiscal year end) are incorporated by reference in this Annual Report on Form 10-K in response to Part II, Item 5 and Part III, Items 10, 11, 12, 13 and 14.

CITY OFFICE REIT, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2019

Table of contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of the federal securities laws. These forward-looking statements are included throughout this Annual Report on Form 10-K, including in the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business” and “Certain Relationships and Related Person Transactions,” and relate to matters such as our industry, business strategy, goals and expectations concerning our market position, future operations, margins, profitability, capital expenditures, financial condition, liquidity, capital resources, cash flows, results of operations and other financial and operating information. We have used the words “approximately,” “anticipate,” “assume,” “believe,” “budget,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “future,” “intend,” “may,” “outlook,” “plan,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “will” and similar terms and phrases to identify forward-looking statements in this Annual Report on Form 10-K. All of our forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that we are expecting, including:

| • | adverse economic or real estate developments in the office sector or the markets in which we operate; |

| • | changes in local, regional, national and international economic conditions; |

| • | our inability to compete effectively; |

| • | our inability to collect rent from tenants or renew tenants’ leases on attractive terms if at all; |

| • | demand for and market acceptance of our properties for rental purposes; |

| • | defaults on or non-renewal of leases by tenants; |

| • | increased interest rates and any resulting increase in financing or operating costs; |

| • | decreased rental rates or increased vacancy rates; |

| • | our failure to obtain necessary financing or access the capital markets on favorable terms or at all; |

| • | changes in the availability of acquisition opportunities; |

| • | availability of qualified personnel; |

| • | our inability to successfully complete real estate acquisitions or dispositions on the terms and timing we expect, or at all; |

| • | our failure to successfully operate acquired properties and operations; |

| • | changes in our business, financing or investment strategy or the markets in which we operate; |

| • | our failure to generate sufficient cash flows to service our outstanding indebtedness; |

| • | environmental uncertainties and risks related to adverse weather conditions and natural disasters; |

| • | our failure to qualify and maintain our status as a real estate investment trust (“REIT”); |

| • | government approvals, actions and initiatives, including the need for compliance with environmental requirements; |

| • | outcome of claims and litigation involving or affecting us; |

| • | financial market fluctuations; |

| • | changes in real estate, taxation and zoning laws and other legislation and government activity and changes to real property tax rates and the taxation of REITs in general; and |

| • | additional factors discussed under the sections captioned “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” |

1

The forward-looking statements contained in this Annual Report on Form 10-K are based on historical performance and management’s current plans, estimates and expectations in light of information currently available to us and are subject to uncertainty and changes in circumstances. There can be no assurance that future developments affecting us will be those that we have anticipated. Actual results may differ materially from these expectations due to the factors, risks and uncertainties described above, changes in global, regional or local political, economic, business, competitive, market, regulatory and other factors described in “Risk Factors,” many of which are beyond our control. We believe that these factors include those described in “Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove to be incorrect, our actual results may vary in material respects from what we may have expressed or implied by these forward-looking statements. We caution that you should not place undue reliance on any of our forward-looking statements. Any forward-looking statement made by us in this Annual Report on Form 10-K speaks only as of the date of this Annual Report on Form 10-K. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by applicable securities laws.

2

| ITEM 1. | BUSINESS |

Overview

We are an internally-managed corporation organized in the state of Maryland on November 26, 2013 focused on acquiring, owning and operating high-quality office properties located in “18-hour cities” in the Southern and Western United States. Our target markets possess a number of attractive demographic and employment characteristics that we believe will lead to capital appreciation and growth in rental income at our properties. Our senior management team has extensive industry relationships and a proven track record in executing this strategy, which we believe provides a competitive advantage to our stockholders. We have elected, and intend to continue to qualify, to be taxed as a REIT for U.S. federal income tax purposes.

We believe that our target markets offer the opportunity for attractive risk-adjusted returns due to the following characteristics: favorable economic growth trends, growing populations with above average employment growth forecasts, a large number of government offices, large international, national and regional employers across diversified industries, low-cost centers for business operations, proximity to large universities and increasing office occupancy rates. Within our target markets, we focus primarily on Class A and B properties with a purchase price between $25 million and $100 million. We believe that we have a competitive advantage in acquiring these properties in our target markets because of our local relationships, prior transaction experience and reduced competition from large institutional investors in our typical transaction size.

Our senior management team has extensive experience in real estate markets and is made up of James Farrar, our Chief Executive Officer, Gregory Tylee, our President and Chief Operating Officer, and Anthony Maretic, our Chief Financial Officer, each with over 20 years of experience. We internally asset manage our properties but use local firms for property management and leasing in our markets to benefit from their local market knowledge, efficient operations and existing infrastructure.

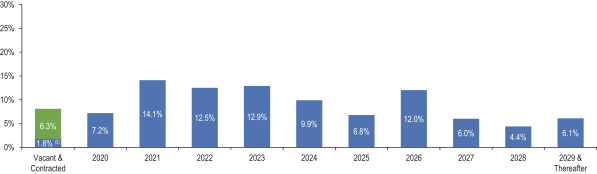

At December 31, 2019, we owned 65 office buildings with a total of approximately 5.8 million square feet of net rentable area (“NRA”) in the metropolitan areas of Dallas, Denver, Orlando, Phoenix, Portland, San Diego, Seattle and Tampa. We believe that our properties are high quality assets that provide excellent access to transportation options, are located near affluent neighborhoods, contain extensive amenities and are well-maintained. We also believe that our properties have a stable and diverse tenant base, including federal and state governmental agencies and national and regional businesses. As of December 31, 2019, our portfolio was approximately 91.9% occupied. Our properties also have a stable, long-term tenancy profile and our occupied leases have staggered expirations and a weighted average remaining lease term to maturity of 4.4 years at December 31, 2019. The majority of our leases are full service gross leases pursuant to which our tenants reimburse us for operating expenses, property taxes and insurance in excess of a base amount. This structure helps insulate us from increases in certain operating expenses and provides a more predictable cash flow. Our leases typically include rent escalation provisions designed to provide annual growth in our rental income.

For further information on our target markets and the composition of our tenant base, see “Item 2—Properties.”

As of December 31, 2019, we had 20 full-time employees. We believe that our relations with our employees are satisfactory.

Business Objectives and Growth Strategies

Our principal business objective is to provide attractive risk-adjusted returns to our investors over the long-term through a combination of dividends and capital appreciation. We believe the following strategies will help

3

us achieve our business objective and continue to distinguish us from other owners and operators of office properties in our markets:

Drive Cash Flow Increases through Rent Growth: Our leases typically provide for contractual increases in base rental rates. These rental escalations are expected to result in predictable increases in rental revenues for us over time. We will continue to seek to include contractual rent escalators in future leases to further facilitate predictable growth in rental income. In circumstances where in-place rental rates are below market rental rates, we will aim to capture increases in cash flow by increasing rents to market.

Leverage Strong Relationships of Our Management Team: Our senior management team has extensive relationships within our markets, including with real estate owners, developers, operators and brokers. We have strong relationships with our local third-party real estate operators, which typically manage or lease a large number of properties in the submarkets and markets where our properties are located, providing economies of scale and local market insight. In addition, our management team has strong lending relationships with various banks and insurance companies.

Acquire Properties in Our Target Markets: We seek to expand our portfolio through acquisitions of office properties primarily located in our target 18-hour cities. We believe that current economic conditions and relatively low levels of competition from institutional buyers in our typical transaction size have created attractive investment opportunities for the acquisition of office properties in our target markets. We also use our management team’s market-specific knowledge as well as the expertise of our local real estate operators and our investment partners to identify acquisitions that we believe offer cash flow stability and value enhancement.

Lease Currently Vacant Space: As of December 31, 2019, our portfolio was approximately 91.9% occupied, and we believe that there is potential to generate additional rental income by leasing space in these properties that is currently unoccupied. We have been successful in enhancing the appeal of vacant spaces by completing improvements to vacancies, creating or improving building amenities and renovating common areas.

Implement Improvements and Cost-Saving Initiatives: We actively pursue cost reduction initiatives, such as eliminating redundant or unnecessary expenses and engaging property tax appeal specialists to lower property tax costs, and make an ongoing effort to increase expense recoveries from tenants on new and renewed leases.

2019 Highlights

| • | Acquired $144 million of high-quality office properties, including expanding our geographic footprint into Seattle and deepening our presence in Portland and Denver; |

| • | Disposed of three assets for an aggregate sale price of $47 million, selectively enhancing our portfolio; |

| • | Completed 692,000 square feet of new and renewal leasing, increasing portfolio occupancy from 90.4% to 91.9%; |

| • | Issued an aggregate 14,900,000 shares of common stock pursuant to the Company’s at-the-market offering program and a follow-on public offering, generating aggregate gross proceeds of approximately $202.1 million; |

| • | Upsized our unsecured credit facility (the “Unsecured Credit Facility”) from $250 million to $300 million; |

| • | Modified loan agreements at four of our properties, generating significant interest savings; |

| • | Achieved inclusion to the MSCI US REIT Index (RMZ); and |

| • | Declared and paid an aggregate of $0.94 of dividends per share of common stock. |

4

Competition

We compete with other REITs (both public and private), public and private real estate companies, private real estate investors and lenders, both domestic and foreign, in acquiring properties. We also face competition in leasing or subleasing available properties to prospective tenants.

We believe that our management’s experience and relationships in, and local knowledge of, the markets in which we operate put us at a competitive advantage when seeking acquisitions. However, some of our competitors have greater resources than we do, or may have a more flexible capital structure when seeking to finance acquisitions. We also face competition in leasing or subleasing available properties to prospective tenants. Some real estate operators may be willing to enter into leases at lower contractual rental rates. However, we believe that our intensive management services are attractive to tenants and serve as a competitive advantage.

Segment and Geographic Financial Information

During 2019, we had one reportable segment, our office properties segment. For information about our office property revenues and long-lived assets and other financial information, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations.”

Environmental Matters

A wide variety of environmental and occupational health and safety laws and regulations affect our properties. These complex laws, and their enforcement, involve a myriad of regulations, many of which involve strict liability on the part of the potential offender. Some of these laws may directly impact us. Under various local environmental laws, ordinances and regulations, an owner of real property, such as us, may be liable for the costs of removal or remediation of hazardous or toxic substances at, under or disposed of in connection with such property, as well as other potential costs relating to hazardous or toxic substances (including government fines and damages for injuries to persons and adjacent property). The cost of any required remediation, removal, fines or personal or property damages and the owner’s liability therefore could exceed or impair the value of the property, and/or the assets of the owner. In addition, the presence of such substances, or the failure to properly dispose of or remediate such substances, may adversely affect the owner’s ability to sell or rent such property or to borrow using such property as collateral which, in turn, could reduce our revenues.

We believe that our properties are in compliance in all material respects with all federal, state and local environmental laws and regulations regarding hazardous or toxic substances and other environmental matters. We have not been notified by any governmental authority of any material non-compliance, liability or claim relating to hazardous or toxic substances or other environmental matter in connection with any of our properties.

Availability of Reports Filed with the Securities and Exchange Commission

A copy of this Annual Report on Form 10-K, as well as our quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to such reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are available, free of charge, on our Internet website (www.cityofficereit.com). All of these reports are made available on our website as soon as reasonably practicable after they are electronically filed with or furnished to the United States Securities and Exchange Commission (the “SEC”). Our Governance Guidelines and Code of Business Conduct and Ethics and the charters of the Audit, Compensation, Investment, and Nominating and Corporate Governance Committees of our Board of Directors are also available on our website at www.cityofficereit.com, and are available in print to any stockholder upon written request to City Office REIT, Inc., c/o Investor Relations, Suite 3210-666 Burrard Street, Vancouver, British Columbia, V6C 2X8. The Company may, from time to time, amend these charters and policies, and such amended charters and policies will be posted on the Company’s website. Our telephone number is +1 (604) 806-3366. The information on or accessible through our website is not, and shall not be deemed to be, a part of this report or incorporated into any other filing we make with the SEC.

5

| ITEM 1A. | RISK FACTORS |

Risks Relating to Our Business and Our Properties

There are inherent risks associated with real estate investments and with the real estate industry, each of which could have an adverse impact on our financial performance and the value of our properties.

Real estate investments are subject to various risks and fluctuations and cycles in value and demand, many of which are beyond our control. Our financial performance and the value of our properties can be affected by many of these factors, including the following:

| • | adverse changes in financial conditions of buyers, sellers and tenants of our properties, including bankruptcies, financial difficulties or lease defaults by our tenants; |

| • | the national, regional and local economy, which may be negatively impacted by concerns about inflation, government deficits or government budgets, unemployment rates, decreased consumer confidence, industry slowdowns, reduced corporate profits, liquidity concerns in our markets and other adverse business concerns; |

| • | local real estate conditions, such as an oversupply of, or a reduction in, demand for office space and the availability and creditworthiness of current and prospective tenants; |

| • | vacancies or ability to rent space on favorable terms, including possible market pressures to offer tenants rent abatements, tenant improvements, early termination rights or below-market renewal options; |

| • | changes in operating costs and expenses, including, without limitation, increasing labor and material costs, insurance costs, energy prices, environmental restrictions, real estate taxes and costs of compliance with laws, regulations and government policies, which we may be restricted from passing on to our tenants; |

| • | fluctuations in interest rates, which could adversely affect our ability, or the ability of buyers and tenants of our properties, to obtain financing on favorable terms or at all, or impact the market price of our properties we own or target for investment; |

| • | competition from other real estate investors with significant capital, including other real estate operating companies, other publicly traded REITs and institutional investment funds; |

| • | inability to refinance our indebtedness, which could result in a default on our obligation and trigger cross default provisions that could result in a default on other indebtedness; |

| • | the convenience and quality of competing office properties; |

| • | inability to collect rent from tenants; |

| • | our ability to secure adequate insurance; |

| • | our ability to secure adequate management services and to maintain our properties; |

| • | changes in, and changes in enforcement of, laws, regulations and governmental policies, including, without limitation, health, safety, environmental, zoning, immigration and tax laws, government fiscal, monetary and trade policies and the Americans with Disabilities Act of 1990 (the “ADA”); and |

| • | civil unrest, acts of war, cyber attacks, terrorist attacks and natural disasters, including earthquakes, wind damage and floods, which may result in uninsured and underinsured losses. |

In addition, because the yields available from equity investments in real estate depend in large part on the amount of rental income earned, as well as property operating expenses and other costs incurred, a period of economic slowdown or recession, or declining demand for real estate, or the public perception that any of these

6

events may occur, could result in a general decline in rents or an increased incidence of defaults among our existing leases, and, consequently, our properties, including any held by joint ventures, may fail to generate revenues sufficient to meet operating, debt service and other expenses. As a result, we may have to borrow amounts to cover fixed costs, and our financial condition, results of operations, cash flow, per share market price of our common stock and ability to satisfy our principal and interest obligations and to make distributions to our stockholders may be adversely affected.

Significant competition may decrease or prevent increases in our properties’ occupancy and rental rates and may reduce our investment opportunities.

We compete with numerous owners, operators and developers of office properties, many of which own properties similar to ours in the same submarkets in which our properties are located. Furthermore, undeveloped land in many of the markets in which we operate is generally more readily available and less expensive than in gateway markets, which are commonly defined as New York, Los Angeles, Washington, D.C., Boston, Chicago and San Francisco. If our competitors offer space from existing or new buildings at rental rates below current market rates, or below the rental rates that we currently charge our tenants, we may lose existing or potential tenants and we may be pressured to reduce our rental rates below those that we currently charge or to offer more substantial rent abatements, tenant improvements, early termination rights or below-market renewal options in order to retain or attract tenants when our tenants’ leases expire. Our competitors may have substantially greater financial resources than we do and may be able to accept more risk than we can prudently manage. In the future, competition from these entities may reduce the number of suitable investment opportunities offered to us or increase the bargaining power of property owners seeking to sell. As a result, our financial condition, results of operations, cash flows and market price of our common stock could be adversely affected.

We are dependent on our key personnel and the loss of such key personnel could materially adversely affect our business, financial condition and results of operations and our ability to pay distributions to our stockholders.

We are dependent on the efforts of our key officers and employees, including James Farrar, our Chief Executive Officer, Gregory Tylee, our President and Chief Operating Officer, and Anthony Maretic, our Chief Financial Officer, Secretary and Treasurer. The loss of Mr. Farrar’s, Mr. Tylee’s and/or Mr. Maretic’s services could have a material adverse effect on our business, financial condition and results of operations and our ability to pay distributions to our stockholders. Although we have employment agreements with them, we cannot assure you they will remain employed with us.

A decrease in demand for office space may have a material adverse effect on our financial condition and results of operations.

Our portfolio of properties consists entirely of office properties and because we seek to acquire similar properties, a decrease in the demand for office space may have a greater adverse effect on our business and financial condition than if we owned a more diversified real estate portfolio. If parts of our properties are leased within a particular sector, a significant downturn in that sector in which the tenants’ businesses operate would adversely affect our results of operations. In addition, where a government agency is a tenant, which is the case for a number of our properties, austerity measures, the inability of the federal, state or local government to approve a budget, and governmental deficit reduction programs may lead government agencies to stop paying rent, consolidate and reduce their office space, terminate their lease or decrease their workforce, which may reduce demand for office space in the government sector.

Failure by any major tenant to make rental payments to us, because of a deterioration of its financial condition, a termination of its lease, a non-renewal of its lease or otherwise, could seriously harm our results of operations.

As of December 31, 2019, approximately 27.8% of the base rental revenue of our properties was derived from our ten largest tenants. At any time, our tenants may experience a downturn in their businesses that may

7

significantly weaken their financial condition, whether as a result of general economic conditions or otherwise. As a result, our tenants may fail to make rental payments when due, delay lease commencements, decline to extend or renew leases upon expiration or declare bankruptcy. Any of these actions could result in the termination of the tenants’ leases or the failure to renew a lease and the loss of rental income attributable to the terminated leases. The occurrence of any of the situations described above could seriously harm our results of operations.

We may be unable to secure funds for future tenant or other capital improvements or payment of leasing commissions, which could limit our ability to attract or replace tenants and adversely impact our ability to make cash distributions to our stockholders.

When tenants do not renew their leases or otherwise vacate their space, it is common that, in order to attract replacement tenants, we will be required to expend funds for tenant improvements, payment of leasing commissions and other concessions related to the vacated space. Such tenant improvements may require us to incur substantial capital expenditures. We may not be able to fund capital expenditures solely from cash provided from our operating activities because we must distribute at least 90% of our REIT taxable income, determined without regard to the deduction for dividends paid and excluding net capital gains, each year to qualify as a REIT. As a result, our ability to fund tenant and other capital improvements or payment of leasing commissions through retained earnings may be limited. If we have insufficient capital reserves, we will have to obtain financing from other sources. We may also have future financing needs for other capital improvements to refurbish or renovate our properties. If we are unable to secure financing on terms that we believe are acceptable or at all, we may be unable to make tenant and other capital improvements or payment of leasing commissions or we may be required to defer such improvements. If this happens, it may cause one or more of our properties to suffer from a greater risk of obsolescence or a decline in value, as a result of fewer potential tenants being attracted to the property or existing tenants not renewing their leases. If we do not have access to sufficient funding in the future, we may not be able to make necessary capital improvements to our properties, pay leasing commissions or other expenses or pay distributions to our stockholders.

We may be required to make rent or other concessions and significant capital expenditures to improve our properties in order to retain and attract tenants, which could adversely affect our financial condition, results of operations and cash flow.

In order to retain existing tenants and attract new clients, we may be required to offer more substantial rent abatements, tenant improvements and early termination rights or accommodate requests for renovations, build-to-suit remodeling and other improvements or provide additional services to our tenants. As a result, we may have to make significant capital or other expenditures in order to retain tenants whose leases expire and to attract new tenants in sufficient numbers, which could adversely affect our results of operations and cash flow. Additionally, if we need to raise capital to make such expenditures and are unable to do so, or such capital is otherwise unavailable, we may be unable to make the required expenditures. This could result in non-renewals by tenants upon expiration of their leases, which could adversely affect our financial condition, results of operations and cash flow.

We depend on external sources of capital that are outside of our control, which may affect our ability to seize strategic opportunities, satisfy our debt obligations and make distributions to our stockholders.

In order to maintain our qualification as a REIT, we are generally required under the U.S. Internal Revenue Code of 1986, as amended (the “Code”) to annually distribute at least 90% of our REIT taxable income, determined without regard to the deduction for dividends paid and excluding any net capital gain. In addition, as a REIT, we will be subject to income tax at regular corporate rates to the extent that we distribute less than 100% of our REIT taxable income, including any net capital gains. Because of these distribution requirements, we may not be able to fund future capital needs (including redevelopment, acquisition, expansion and renovation activities, payments of principal and interest on and the refinancing of our existing debt, tenant improvements

8

and leasing costs), from operating cash flow. Consequently, we may rely on third-party sources to fund our capital needs. We may not be able to obtain the necessary financing on favorable terms, in the time period that we desire or at all. Any additional debt we incur will increase our leverage, expose us to the risk of default and may impose operating restrictions on us, and any additional equity we raise could be dilutive to existing stockholders. Our access to third-party sources of capital depends, in part, on:

| • | general market conditions; |

| • | the market’s view of the quality of our assets; |

| • | the market’s perception of our growth potential; |

| • | our current debt levels; |

| • | our current and expected future earnings; |

| • | our cash flow and cash distributions; and |

| • | the market price of securities we may issue from time to time. |

If we cannot obtain capital from third-party sources, we may not be able to acquire or develop properties when strategic opportunities exist, satisfy our principal and interest obligations or make the cash distributions to our stockholders necessary to maintain our qualification as a REIT.

Covenants in the Credit Agreement governing our Unsecured Credit Facility may cause us to fail to qualify as a REIT.

In order to maintain our qualification as a REIT, we are generally required under the Code to distribute annually at least 90% of our net taxable income, determined without regard to the deduction for dividends paid and excluding any net capital gain. In addition, we will be subject to income tax at regular corporate rates to the extent that we distribute less than 100% of our net taxable income, including any net capital gains. Under the credit agreement governing our Unsecured Credit Facility (the “Credit Agreement”), we are subject to various financial covenants that may inhibit our ability to make distributions to our stockholders. If we are unable to make distributions to our stockholders, we will not be able to make sufficient distributions to maintain our REIT status.

We have a substantial amount of indebtedness outstanding which may affect our ability to pay distributions, may expose us to interest rate fluctuation risk and may expose us to the risk of default under our debt obligations.

Our total consolidated principal indebtedness, as of December 31, 2019, was approximately $612.3 million. We do not anticipate that our internally generated cash flows will be adequate to repay our existing indebtedness upon maturity, and, therefore, we expect to repay our indebtedness through refinancings and future offerings of equity and debt securities, either of which we may be unable to secure on favorable terms or at all. Our substantial outstanding indebtedness, and the limitations imposed on us by our debt agreements, could have other significant adverse consequences, including the following:

| • | our cash flow may be insufficient to meet our required principal and interest payments; |

| • | we may be unable to borrow additional funds as needed or on favorable terms, which could, among other things, adversely affect our ability to capitalize upon emerging acquisition opportunities or meet operational needs; |

| • | we may be unable to refinance our indebtedness at maturity or the refinancing terms may be less favorable than the terms of our original indebtedness; |

| • | we may be forced to dispose of one or more of our properties, possibly on disadvantageous terms; |

9

| • | we may be forced to enter into financing arrangements with particularly burdensome collateral requirements or restrictive covenants; |

| • | we may violate restrictive covenants in our loan documents, which would entitle the lenders to accelerate our debt obligations or require us to retain cash for reserves; |

| • | we may be unable to hedge floating rate debt, counterparties may fail to honor their obligations under our hedge agreements and these agreements may not effectively hedge interest rate fluctuation risk; |

| • | we may default on our obligations and the lenders or mortgagees may foreclose on our properties that secure their loans; |

| • | our default under any of our indebtedness with cross default provisions could result in a default on other indebtedness; and |

| • | cross default provisions on properties with minority parties could trigger indemnity obligations. |

If any one of these events were to occur, our financial condition, results of operations, cash flows, market price of our common stock and preferred stock and ability to satisfy our debt service obligations and to pay distributions to you could be adversely affected. In addition, any foreclosure on our properties could create taxable income without accompanying cash proceeds, which could adversely affect our ability to meet the distribution requirements necessary to maintain our qualification as a REIT.

We could become highly leveraged in the future because our organizational documents contain no limitations on the amount of debt that we may incur.

As of December 31, 2019, our principal indebtedness represented approximately 49.8% of our total assets. However, our organizational documents contain no limitations on the amount of indebtedness that we or City Office REIT Operating Partnership, L.P. (our “Operating Partnership”) may incur. We could alter the balance between our total outstanding indebtedness and the value of our properties at any time. If we become more highly leveraged, the resulting increase in outstanding debt could adversely affect our ability to make debt service payments, to pay our anticipated distributions and to make the distributions required to maintain our qualification as a REIT. The occurrence of any of the foregoing risks could adversely affect our business, financial condition and results of operations, our ability to make distributions to our stockholders and the trading price of our securities.

Lenders may require us to enter into restrictive covenants relating to our operations, which could limit our ability to make distributions to our stockholders.

In providing financing to us, a lender may impose restrictions on us that would affect our ability to incur additional debt, make certain investments, reduce liquidity below certain levels, make distributions to our stockholders and otherwise affect our distribution and operating policies. In general, we expect that our loan agreements will restrict our ability to encumber or otherwise transfer our interest in the respective property without the prior consent of the lender. Such loan documents may contain other negative covenants that may limit our ability to discontinue insurance coverage or impose other limitations. Any such restriction or limitation may limit our ability to make distributions to you. Further, such restrictions could make it difficult for us to satisfy the requirements necessary to maintain our qualification as a REIT.

We may engage in hedging transactions, which can limit our gains and increase exposure to losses.

Subject to maintaining our qualification as a REIT, we may enter into hedging transactions to protect us from the effects of interest rate fluctuations on floating rate debt. Our hedging transactions may include entering into interest rate swap agreements or interest rate cap or floor agreements, or other interest rate exchange contracts. Hedging activities may not have the desired beneficial impact on our results of operations or financial

10

condition. No hedging activity can completely insulate us from the risks associated with changes in interest rates. Moreover, interest rate hedging could fail to protect us or adversely affect us because, among other things:

| • | available interest rate hedging may not correspond directly with the interest rate risk for which we seek protection; |

| • | the duration of the hedge may not match the duration of the related liability; |

| • | the party owing money in the hedging transaction may default on its obligation to pay; |

| • | the credit quality of the party owing money on the hedge may be downgraded to such an extent that it impairs our ability to sell or assign our side of the hedging transaction; and |

| • | the value of derivatives used for hedging may be adjusted from time to time in accordance with accounting rules to reflect changes in fair value, such as downward adjustments, or “mark-to-market losses,” which would reduce our stockholders’ equity. |

Hedging involves risk and typically involves costs, including transaction costs, that may reduce our overall returns on our investments. These costs increase as the period covered by the hedging increases and during periods of rising and volatile interest rates. These costs will also limit the amount of cash available for distribution to stockholders. We generally intend to hedge as much of the interest rate risk as we determine is in our best interests given the cost of such hedging transactions. The REIT tax rules may limit our ability to enter into hedging transactions by requiring us to limit our income from non-qualifying hedges. If we are unable to hedge effectively because of the REIT tax rules, we will face greater interest rate exposure than may be commercially prudent.

In September 2019, in connection with the increase in authorized borrowings under our Unsecured Credit Facility from $250.0 million to $300.0 million, we entered into the five-year interest rate swap for a notional amount of $50.0 million (the “Interest Rate Swap”). Pursuant to the Interest Rate Swap, the Company will pay a fixed rate of approximately 1.27% of the notional amount annually, payable monthly, and receive floating rate 30-day LIBOR payments.

The Interest Rate Swap has been designated and qualifies as a cash flow hedge and has been recognized on the consolidated balance sheets at fair value. Gains and losses resulting from changes in the fair value of derivatives that are designated and qualify as cash flow hedges are reported as a component of other comprehensive income (loss) and reclassified into earnings in the periods during which the hedged forecasted transaction affects earnings.

As of December 31, 2019, the Interest Rate Swap was reported as an asset at its fair value of approximately $0.7 million, which is included in other assets on the Company’s consolidated balance sheet. For the year ended December 31, 2019 the amount of realized gains reclassified to interest expense due to payments received by the swap counterparty was $0.1 million. Accordingly, the fair value of the Interest Rate Swap has been classified as a Level 2 fair value measurement. See Note 7 to our consolidated financial statements in this report.

Changes in the method pursuant to which reference rates are determined and phasing out of LIBOR after 2021 may affect our financial results.

The chief executive of the United Kingdom Financial Conduct Authority (“FCA”), which regulates LIBOR, has announced that the FCA intends to stop compelling banks to submit rates for the calculation of LIBOR after 2021. It is not possible to predict the effect of these changes, other reforms or the establishment of alternative reference rates in the United Kingdom or elsewhere. Furthermore, in the United States, efforts to identify a set of alternative U.S. dollar reference interest rates include proposals by the Alternative Reference Rates Committee of the Federal Reserve Board and the Federal Reserve Bank of New York. The U.S. Federal Reserve, in conjunction with the Alternative Reference Rates Committee, a steering committee comprised of large U.S. financial

11

institutions, is considering replacing U.S. dollar LIBOR with the Secured Overnight Financing Rate (“SOFR”), a new index calculated by short-term repurchase agreements, backed by Treasury securities. The Federal Reserve Bank of New York began publishing SOFR rates in April 2018. The market transition away from LIBOR and towards SOFR is expected to be gradual and complicated. There are significant differences between LIBOR and SOFR, such as LIBOR being an unsecured lending rate and SOFR a secured lending rate, and SOFR is an overnight rate and LIBOR reflects term rates at different maturities. Although there have been some issuances utilizing SOFR, it is unknown whether this alternative reference rate will attain market acceptance as a replacement for LIBOR. These and other differences create the potential for basis risk between the two rates. The impact of any basis risk between LIBOR and SOFR may negatively affect our operating results. In addition, there is currently no definitive information regarding the future utilization of LIBOR or of any particular replacement rate. Any of these alternative methods may result in interest rates that are higher than if LIBOR were available in its current form, which could have a material adverse effect on results. As such, the potential effect on us cannot yet be determined.

Any changes announced by the FCA, including the FCA Announcement, other regulators or any other successor governance or oversight body, or future changes adopted by such body, in the method pursuant to which the reference rates are determined may result in a sudden or prolonged increase or decrease in the reported reference rates. If that were to occur, the level of interest payments we incur may change. In addition, although certain of our LIBOR based obligations provide for alternative methods of calculating the interest rate payable on certain of our obligations if LIBOR is not reported, which include requesting certain rates from major reference banks in London or New York, or alternatively using LIBOR for the immediately preceding interest period or using the initial interest rate, as applicable, uncertainty as to the extent and manner of future changes may result in interest rates and/or payments that are higher than, lower than or that do not otherwise correlate over time with the interest rates and/or payments that would have been made on our obligations if LIBOR rate was available in its current form.

Economic conditions may adversely affect the real estate market and our income.

Uncertainty over whether the U.S. economy will be adversely affected by inflation or stagflation, volatile energy costs, geopolitical issues, the possibility of any pandemic, the availability and cost of credit, future policy and fiscal decisions of the federal government, the mortgage market in the United States and the late-cycle real estate market may contribute to increased market volatility or threaten business and consumer confidence. This uncertain operating environment could adversely affect our ability to generate revenues, thereby reducing our operating income and earnings.

In addition, local real estate conditions such as an oversupply of properties or a reduction in demand for properties, competition from other similar properties, our ability to provide or arrange for adequate maintenance, insurance and management and advisory services, increased operating costs (including real estate taxes), the attractiveness, location of the property, changes in market rental rates and region-specific legislation or political initiatives may adversely affect a property’s income and value. A rise in energy costs could result in higher operating costs, which may affect our results of operations. In addition, local conditions in the markets in which we own or intend to own properties may significantly affect occupancy or rental rates at such properties. Events that could prevent us from raising or maintaining rents or cause us to reduce rents include layoffs, plant closings, relocations of significant local employers and other events reducing local employment rates, an oversupply of—or a lack of demand for—office space, a decline in household formation, the inability or unwillingness of tenants to pay rent increases, and geopolitical developments having a disproportionate effect on the markets in which we operate.

12

Our joint venture investments could be adversely affected by the capital markets, our lack of sole decision-making authority, our reliance on joint venture partners’ financial condition and any disputes that may arise between us and our joint venture partners.

We have in the past co-invested, and may in the future co-invest, with third parties through partnerships, joint ventures or other structures, acquiring non-controlling interests in, or sharing responsibility for managing the affairs of, a property, partnership, co-tenancy or other entity. Investments in joint ventures may, under certain circumstances, involve risks not present when a third party is not involved, including potential deadlocks in making major decisions, restrictions on our ability to exit the joint venture, reliance on our joint venture partners and the possibility that joint venture partners might become bankrupt or fail to fund their share of required capital contributions, thus exposing us to liabilities in excess of our share of the investment or take action that could jeopardize our REIT status. The funding of our capital contributions may be dependent on proceeds from asset sales, credit facility advances and/or sales of equity securities. Joint venture partners may have business interests or goals that are inconsistent with our business interests or goals and may be in a position to take actions contrary to our policies or objectives. We may in specific circumstances be liable for the actions of our joint venture partners. In addition, any disputes that may arise between us and joint venture partners may result in litigation or arbitration that would increase our expenses.

We may incur significant costs complying with various federal, state and local laws, regulations and covenants that are applicable to our properties, which could have an adverse impact on our financial condition, results of operations, cash flows and market price of our common stock.

The properties in our portfolio are subject to various covenants and federal, state and local laws and regulatory requirements, including permitting and licensing requirements. Local regulations, including municipal or local ordinances, zoning restrictions and restrictive covenants imposed by community developers may restrict our use of our properties and may require us to obtain approval or waivers from local officials or restrict our use of our properties and may require us to obtain approval from local officials of community standards organizations at any time with respect to our properties, including prior to acquiring a property or when undertaking renovations of any of our existing properties. Among other things, these restrictions may relate to fire and safety, seismic or hazardous material abatement requirements. There can be no assurance that existing or future laws and regulatory policies, including federal laws or executive actions affecting the markets in which we operate, will not adversely affect us or the timing or cost of any future acquisitions or renovations, or that additional regulations will not be adopted that could increase such delays or result in additional costs. Our growth strategy may be affected by our ability to obtain permits, licenses and zoning relief. Our failure to obtain such permits, licenses and zoning relief or to comply with applicable laws could have an adverse effect on our financial condition, results of operations, cash flow and per share market price of our common stock or preferred stock.

We could incur significant costs related to government regulation and private litigation over environmental matters involving the presence, discharge or threat of discharge of hazardous or toxic substances, which could adversely affect our operations, the value of our properties and our ability to make distributions to our stockholders.

Our properties may be subject to environmental liabilities. Under various federal, state and local laws, a current or previous owner, operator or tenant of real estate can face liability for environmental contamination created by the presence, discharge or threat of discharge of hazardous or toxic substances. Liabilities can include the cost to investigate, clean up and monitor the actual or threatened contamination and damages caused by the contamination or threatened contamination.

The liability under such laws may be strict, joint and several, meaning that we may be liable regardless of whether we knew of, or were responsible for, the presence of the contaminants, and the government entity or private party may seek recovery of the entire amount from us even if there are other responsible parties.

13

Liabilities associated with environmental conditions may be significant and can sometimes exceed the value of the affected property. The presence of hazardous substances on a property may adversely affect our ability to sell or rent that property or to borrow using that property as collateral.

Environmental laws also:

| • | may require the removal or upgrade of underground storage tanks; |

| • | regulate the discharge of storm water, wastewater and other pollutants; |

| • | regulate air pollutant emissions; |

| • | regulate hazardous materials’ generation, management and disposal; and |

| • | regulate workplace health and safety. |

Existing conditions at some of our properties may expose us to liability related to environmental matters.

Independent environmental consultants have conducted Phase I or similar environmental site assessments on all of our properties. Site assessments are intended to discover and evaluate information regarding the environmental condition of the surveyed property and surrounding properties. These assessments do not generally include subsurface investigations or mold or asbestos surveys. None of the recent site assessments revealed any past or present environmental liability that we believe would have a material adverse effect on our business, financial condition, cash flows or results of operations. However, the assessments may have failed to reveal all environmental conditions, liabilities or compliance concerns. Material environmental conditions, liabilities or compliance concerns may have arisen after the review was completed or may arise in the future; and future laws, ordinances or regulations may impose material additional environmental liability.

Costs of future environmental compliance could negatively affect our ability to make distributions to our stockholders, and remedial measures required to address such conditions could have a material adverse effect on our business, financial condition, cash flows or results of operations.

Our properties may contain asbestos or develop harmful mold, which could lead to liability for adverse health effects and costs of remediating the problem, which could adversely affect the value of the affected property and our ability to make distributions to our stockholders.

We are required by federal regulations with respect to our properties to identify and warn, via signs and labels, of potential hazards posed by workplace exposure to installed asbestos-containing materials (“ACMs”) and potential ACMs. We may be subject to an increased risk of personal injury lawsuits by workers and others exposed to ACMs and potential ACMs at our properties as a result of these regulations. The regulations may affect the value of any of our properties containing ACMs and potential ACMs. Federal, state and local laws and regulations also govern the removal, encapsulation, disturbance, handling and disposal of ACMs and potential ACMs when such materials are in poor condition or in the event of construction, remodeling, renovation or demolition of a property.

When excessive moisture accumulates in buildings or on building materials, mold growth may occur, particularly if the moisture problem remains undiscovered or is not addressed over a period of time. Some molds may produce airborne toxins or irritants. Concern about indoor exposure to mold has been increasing because exposure to mold may cause a variety of adverse health effects and symptoms, including allergic or other reactions.

The presence of ACMs or significant mold at any of our properties could require us to undertake a costly remediation program to contain or remove the ACMs or mold from the affected property. In addition, the presence of ACMs or significant mold could expose us to claims of liability to our tenants, their or our employees, and others if property damage or health concerns arise.

14

Potential losses, including from adverse weather conditions, natural disasters and title claims, may not be covered by insurance.

Certain of our properties are located in states where natural disasters such as tornadoes, hurricanes and earthquakes are more common than in other states. Given recent extreme weather events across parts of the United States, including devastating hurricanes in Florida and wildfires in California, it is also possible that our other properties could incur significant damage due to other natural disasters. While we carry insurance to cover a substantial portion of the cost of such events, such as droughts or flooding, our insurance includes deductible amounts and certain items may not be covered by insurance. Future natural disasters may significantly affect our operations and properties and, more specifically, may cause us to experience reduced rental revenue (including from increased vacancy), incur clean-up costs or otherwise incur costs in connection with such events. Any of these events may have a material adverse effect on our business, cash flows, financial condition, results of operations and ability to make distributions to our stockholders.

Furthermore, we do not carry insurance for certain losses, including, but not limited to, losses caused by certain environmental conditions, such as mold or asbestos, riots, civil unrest or war. In addition, our title insurance policies may not insure for the current aggregate market value of our portfolio, and we do not intend to increase our title insurance coverage as the market value of our portfolio increases. As a result, we may not have sufficient coverage against all losses that we may experience, including from adverse title claims.

If we experience a loss that is uninsured or exceeds policy limits, we could incur significant costs and lose the capital invested in the damaged properties as well as the anticipated future cash flows from those properties. In addition, if the damaged properties are subject to recourse indebtedness, we would continue to be liable for the indebtedness, even if these properties were irreparably damaged.

Moreover, we carry several different lines of insurance, placed with several large insurance carriers. If any one of these large insurance carriers were to become insolvent, we would be forced to replace the existing insurance coverage with another suitable carrier and any outstanding claims would be at risk for collection. In such an event, we cannot be certain that we would be able to replace the coverage at similar or otherwise favorable terms. Replacing insurance coverage at unfavorable rates and the potential of uncollectible claims due to carrier insolvency could adversely affect our results of operations and cash flows.

Climate change may adversely affect our business.

To the extent that climate change does occur, we may experience extreme weather and changes in precipitation and temperature, all of which may result in physical damage or a decrease in demand for our properties located in the areas affected by these conditions. Should the impact of climate change be material in nature or occur for lengthy periods of time, our financial condition or results of operations would be adversely affected. In addition, changes in federal and state legislation and regulation on climate change could result in increased capital expenditures to improve the energy efficiency of our existing properties in order to comply with such regulations.

We may be limited in our ability to diversify our investments making us more vulnerable economically than if our investments were diversified.

Our ability to diversify our portfolio may be limited both as to the number of investments owned and the geographic regions in which our investments are located. While we seek to diversify our portfolio by geographic location, we focus on our specified target markets that we believe offer the opportunity for attractive returns and, accordingly, our actual investments may result in concentrations in a limited number of geographic regions. As a result, there is an increased likelihood that the performance of any single property, or the economic performance of a particular region in which our properties are located, could materially affect our operating results.

15

We may acquire properties with lock-out provisions, or agree to such provisions in connection with obtaining financing, which may prohibit us from selling or refinancing a property during the lock-out period.

We may acquire properties in exchange for common units and agree to restrictions on sales or refinancing, called “lock-out” provisions, which are intended to preserve favorable tax treatment for the owners of such properties who sell them to us. In addition, we may agree to lock-out provisions in connection with obtaining financing for the acquisition of properties. Lock-out provisions could materially restrict us from selling, otherwise disposing of or refinancing properties. These restrictions could affect our ability to turn our investments into cash and thus affect cash available for distributions to our stockholders. Lock-out provisions could impair our ability to take actions during the lock-out period that would otherwise be in the best interests of our stockholders and, therefore, could adversely impact the market value of our common stock. In particular, lock-out provisions could preclude us from participating in major transactions that could result in a disposition of our assets or a change in control even though that disposition or change in control might be in the best interests of our stockholders.

Illiquidity of real estate investments could significantly impede our ability to respond to adverse changes in the performance of our properties and harm our financial condition.

The real estate investments made, and to be made, by us are relatively difficult to sell quickly. As a result, our ability to promptly sell one or more properties in our portfolio in response to changing economic, financial and investment conditions is limited. Return of capital and realization of gains, if any, from an investment generally will occur upon disposition or refinancing of the underlying property. We may be unable to realize our investment objectives by sale, other disposition or refinancing at attractive prices within any given period of time or may otherwise be unable to complete any exit strategy. In particular, our ability to dispose of one or more properties is subject to weakness in or even the lack of an established market for a property, changes in the financial condition or prospects of prospective purchasers, changes in national or international economic conditions and changes in laws, regulations or fiscal policies of jurisdictions in which the property is located.

In addition, the Code imposes restrictions on a REIT’s ability to dispose of properties that are not applicable to other types of real estate companies. In particular, the tax laws applicable to REITs effectively require that we hold our properties for investment, rather than primarily for sale in the ordinary course of business, which may cause us to forego or defer sales of properties that otherwise would be in our best interest. Therefore, we may not be able to adjust our portfolio in response to economic or other conditions promptly or on favorable terms, which may adversely affect our financial condition, results of operations, cash flow and per share market price of our common stock or preferred stock.

If we sell properties by providing financing to purchasers, we will bear the risk of default by the purchaser.

If we decide to sell any of our properties, we intend to use commercially reasonable efforts to sell them for cash. However, in some instances we may sell our properties by providing financing to purchasers. If we provide financing to purchasers, we will bear the risk of default by the purchasers which would reduce the value of our assets, impair our ability to make distributions to our stockholders and reduce the price of our common stock.

We may be unable to collect balances due on our leases from any tenants in bankruptcy, which could adversely affect our cash flow and the amount of cash available for distribution to our stockholders.

The bankruptcy or insolvency of one or more of our tenants may adversely affect the income produced by our properties. We cannot assure you that any tenant that files for bankruptcy protection will continue to pay us rent. If a tenant files for bankruptcy, any or all of the tenant’s or a guarantor of a tenant’s lease obligations could be subject to a bankruptcy proceeding pursuant to Chapter 11 or Chapter 7 of the U.S. Bankruptcy Code. Such a

16

bankruptcy filing would impose an automatic stay barring all efforts by us to collect pre-bankruptcy rents from these entities or their properties, unless we receive an order from the bankruptcy court lifting the automatic stay to permit us to pursue collections. A tenant or lease guarantor bankruptcy could delay our efforts to collect past due balances under the relevant leases and could ultimately preclude collection of these sums. If a lease is rejected by a tenant in bankruptcy, we would only have a general unsecured claim for damages. This claim could be paid only in the event funds were available and then only in the same percentage as that realized on other unsecured claims. Our claim would be capped at the rent reserved under the lease, without acceleration, for the greater of one year or 15% of the remaining term of the lease, but not greater than three years, plus rent already due but unpaid. Therefore, if a lease is rejected, it is possible that we would not receive payment from the tenant or that we would receive substantially less than the full value of any unsecured claims we hold, which would result in a reduction in our rental income, cash flow and the amount of cash available for distribution to our stockholders.

We may face additional risks and costs associated with owning properties occupied by government tenants, which could negatively impact our cash flows and results of operations.

As of December 31, 2019, we owned seven properties in which some or all of the tenants are federal government agencies. We may continue to pursue the acquisition of office properties in which substantial space is leased to governmental agencies. As such, lease agreements with these federal government agencies contain certain provisions required by federal law, which require, among other things, that the contractor (which is the lessor or the owner of the property), agree to comply with certain rules and regulations, including, but not limited to, rules and regulations related to anti-kickback procedures, examination of records, audits and records, equal opportunity provisions, prohibition against segregated facilities, certain executive orders, subcontractor cost or pricing data, certain provisions intending to assist small businesses and contractual rights of termination by the tenants. We may be subject to requirements of the Employment Standards Administration’s Office of Federal Contract Compliance Programs and requirements to prepare affirmative action plans pursuant to the applicable executive order may be determined to be applicable to us.

In addition, some of our leases with government tenants may be subject to statutory or contractual rights of termination by the tenants, which will allow them to vacate the leased premises before the stated terms of the leases expire with little or no liability. For fiscal policy reasons, security concerns or other reasons, some or all of our government tenants may decide to vacate our properties. If a significant number of such vacancies occur, our rental income may materially decline, our cash flow and results of operations could be adversely affected and our ability to pay regular distributions to you may be jeopardized.

Our government tenants are also subject to discretionary funding from the federal government. Federal government programs are subject to annual congressional budget authorization and appropriation processes. For many programs, Congress appropriates funds on a fiscal year basis even though the program performance period may extend over several years. Laws and plans adopted by the federal government relating to, along with pressures on and uncertainty surrounding the federal budget, potential changes in priorities and spending levels, sequestration, the appropriations process, use of continuing resolutions (with restrictions, e.g., on new starts) and the permissible federal debt limit, could adversely affect the funding for our government tenants. The budget environment and uncertainty surrounding the appropriations processes remain significant long-term risks as budget cuts could adversely affect the viability of our government tenants.

Some of the leases at our properties contain “early termination” provisions which, if triggered, may allow tenants to terminate their leases without further payment to us, which could adversely affect our financial condition and results of operations and the value of the applicable property.

Certain tenants have a right to terminate their leases upon payment of a penalty, but others are not required to pay any penalty associated with an early termination. Most of our tenants that are federal or state governmental agencies, which account for approximately 12.0% of the base rental revenue from our properties as

17

of December 31, 2019, may, under certain circumstances, vacate the leased premises before the stated terms of the leases expire with little or no liability to us. There can be no assurance that tenants will continue their activities and continue occupancy of the premises. Any cessation of occupancy by tenants may have an adverse effect on our operations.

The federal government’s “green lease” policies may adversely affect us.

In recent years, the federal government has instituted “green lease” policies which allow a government tenant to require leadership in energy and environmental design for commercial interiors, or LEED®-CI, certification in selecting new premises or renewing leases at existing premises. In addition, the Energy Independence and Security Act of 2007 allows the General Services Administration to prefer buildings for lease that have received an “Energy Star” label. Obtaining such certifications and labels may be costly and time consuming, but our failure to do so may result in our competitive disadvantage in acquiring new or retaining existing government tenants.

We may be unable to complete acquisitions and, even if acquisitions are completed, we may fail to successfully operate acquired properties.

Our business plan includes, among other things, growth through identifying suitable acquisition opportunities, consummating acquisitions and leasing such properties. We will evaluate the market of available properties and may acquire properties when we believe strategic opportunities exist. Our ability to acquire properties on favorable terms and successfully develop or operate them is subject to, among others, the following risks:

| • | we may be unable to acquire a desired property because of competition from other real estate investors with substantial capital, including from other REITs and institutional investment funds; |

| • | even if we are able to acquire a desired property, competition from other potential acquirers may significantly increase the purchase price; |

| • | even if we enter into agreements for the acquisition of properties, these agreements are subject to customary conditions to closing, including completion of due diligence investigations to our satisfaction; |

| • | we may incur significant costs in connection with evaluation and negotiation of potential acquisitions, including acquisitions that we are subsequently unable to complete; |

| • | we may acquire properties that are not initially accretive to our results upon acquisition, and we may not successfully lease those properties to meet our expectations; |

| • | we may be unable to finance the acquisition on favorable terms in the time period we desire, or at all; |

| • | even if we are able to finance the acquisition, our cash flows may be insufficient to meet our required principal and interest payments; |

| • | we may spend more than budgeted to make necessary improvements or renovations to acquired properties; |

| • | we may be unable to quickly and efficiently integrate new acquisitions, particularly the acquisition of portfolios of properties, into our existing operations; |

| • | market conditions may result in higher than expected vacancy rates and lower than expected rental rates; and |

| • | we may acquire properties subject to liabilities and without any recourse, or with only limited recourse, with respect to unknown liabilities for clean-up of undisclosed environmental contamination, claims by tenants or other persons dealing with former owners of the properties and claims for indemnification by general partners, directors, officers and others indemnified by the former owners of the properties. |

18

Acquired properties may be located in new markets where we may face risks associated with investing in an unfamiliar market.

We may acquire properties in markets that are new to us. When we acquire properties located in new markets, we may face risks associated with a lack of market knowledge or understanding of the local economy, forging new business relationships in the area and unfamiliarity with local government and permitting procedures. We work to mitigate such risks through extensive diligence and research and associations with experienced service providers. However, there can be no guarantee that all such risks will be eliminated.

Adverse market and economic conditions could cause us to recognize impairment charges or otherwise impact our performance.

We intend to review the carrying value of our properties when circumstances, such as adverse market conditions, indicate a potential impairment may exist. We intend to base our review on an estimate of the future cash flows (excluding interest charges) expected to result from the property’s use and eventual disposition on an undiscounted basis. We intend to consider factors such as future operating income, trends and prospects, as well as the effects of leasing demand, competition and other factors. If our evaluation indicates that we may be unable to recover the carrying value of a real estate investment, an impairment loss will be recorded to the extent that the carrying value exceeds the estimated fair value of the property.

Impairment losses would have a direct impact on our operating results because recording an impairment loss results in an immediate negative adjustment to our operating results. The evaluation of anticipated cash flows is highly subjective and is based in part on assumptions regarding future occupancy, rental rates and capital requirements that could differ materially from actual results in future periods. If the real estate market deteriorates, we may reevaluate the assumptions used in our impairment analysis. Impairment charges could materially adversely affect our financial condition, results of operations, cash flows and ability to pay distributions on, and the per share market price of, our common stock or preferred stock.

Litigation may result in unfavorable outcomes.