Attached files

| file | filename |

|---|---|

| EX-99.2 - EXHIBIT 99.2 - INDEPENDENT BANK CORP /MI/ | ex99_2.htm |

| EX-99.1 - EXHIBIT 99.1 - INDEPENDENT BANK CORP /MI/ | ex99_1.htm |

| 8-K - 8-K - INDEPENDENT BANK CORP /MI/ | form8k.htm |

Exhibit 99.3

2 Cautionary Note Regarding Forward-Looking Statements This presentation may contain

“forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Any statements that are not historical facts, including statements about our expectations, beliefs, plans, strategies, predictions,

forecasts, objectives, or assumptions of future events or performance, may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipates,” “believes,” “expects,” “can,” “could,”

“may,” “predicts,” “potential,” “opportunity,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “seeks,” “intends” and similar words or phrases. Accordingly, these statements involve estimates, known and

unknown risks, assumptions, and uncertainties that could cause actual strategies, actions, or results to differ materially from those expressed in them, and are not guarantees of timing, future results, events, or performance. Because

forward-looking statements are necessarily only estimates of future strategies, actions, or results, based on management’s current expectations, assumptions, and estimates on the date hereof, there can be no assurance that actual strategies,

actions or results will not differ materially from expectations. Therefore, readers are cautioned not to place undue reliance on such statements. Factors that could cause or contribute to such differences are changes in general economic,

political or industry conditions; changes in monetary and fiscal policies, including the interest rate policies of the Federal Reserve Board; volatility and disruptions in capital and credit markets; the interdependence of financial service

companies; changes in regulation or oversight; unfavorable developments concerning credit quality; any future acquisitions or divestitures; the effects of more stringent capital or liquidity requirements; declines or other changes in the

businesses or industries of Independent Bank Corporation's customers; the implementation of Independent Bank Corporation's strategies and business models; Independent Bank Corporation's ability to utilize technology to efficiently and

effectively develop, market and deliver new products and services; operational difficulties, failure of technology infrastructure or information security incidents; changes in the financial markets, including fluctuations in interest rates

and their impact on deposit pricing; competitive product and pricing pressures among financial institutions within Independent Bank Corporation's markets; changes in customer behavior; management's ability to maintain and expand customer

relationships; management's ability to retain key officers and employees; the impact of legal and regulatory proceedings or determinations; the effectiveness of methods of reducing risk exposures; the effects of terrorist activities and other

hostilities; the effects of catastrophic events; changes in accounting standards and the critical nature of Independent Bank Corporation's accounting policies. In addition, factors that may cause actual results to differ from expectations

regarding the recent acquisition of TCSB Bancorp, Inc. include, but are not limited to, the reaction to the transaction of customers, employees and counterparties; customer disintermediation; inflation; expected synergies, cost savings and

other financial benefits of the transaction might not be realized within the expected timeframes or might be less than projected; credit and interest rate risks associated with the parties' respective businesses, customers, borrowings,

repayment, investment, and deposit practices; general economic conditions, either nationally or in the market areas in which the parties operate or anticipate doing business, are less favorable than expected; new regulatory or legal

requirements or obligations; and other risks. Certain risks and important factors that could affect Independent Bank Corporation's future results are identified in its Annual Report on Form 10-K for the year ended December 31, 2017 and other

reports filed with the SEC, including among other things under the heading “Risk Factors” in such Annual Report on Form 10-K. Any forward-looking statement speaks only as of the date on which it is made, and Independent Bank Corporation

undertakes no obligation to update any forward-looking statement, whether to reflect events or circumstances after the date on which the statement is made, to reflect new information or the occurrence of unanticipated events, or otherwise.

3 Agenda Formal Remarks.William B. (Brad) Kessel, President and Chief Executive OfficerRobert N.

Shuster, Executive Vice President and Chief Financial OfficerQuestion and Answer session.Closing Remarks.Note: This presentation is available at www.IndependentBank.com in the Investor Relations area under the “Presentations” tab.

4 Quarterly Financial Summary 2Q’18 1Q’18 4Q’17 3Q’17 2Q’17 Diluted EPS (1) $ 0.36 $

0.42 $ 0.08 $ 0.32 $ 0.27 Income before taxes $ 10,884 $ 11,199 $ 11,231 $ 10,018 $ 8,594 Net income (1) $ 8,817 $ 9,161 $ 1,711 $ 6,859 $ 5,931 Return on average assets (1) 1.12% 1.34% 0.25% 1.01% 0.92% Return on

average equity (1) 10.57% 14.04% 2.51% 10.27% 9.15% Total assets $3,234,522 $2,793,119 $2,789,355 $2,753,446 $2,665,367 Total portfolio loans $2,467,317 $2,071,435 $2,018,817 $1,937,094 $1,811,677 Total

deposits $2,780,516 $2,430,401 $2,400,534 $2,343,761 $2,246,219 Loans to deposits ratio 88.74% 85.23% 84.10% 82.65% 80.65% Shareholders’ equity $ 337,083 $ 267,917 $ 264,933 $ 267,710 $ 262,453 Tangible BV per share $

12.47 $ 12.46 $ 12.34 $ 12.47 $ 12.22 TCE to tangible assets 9.41% 9.54% 9.45% 9.67% 9.79% Note: Dollars in thousands, except per share data. (1) Excluding the impact of the $5.96 million revaluation of net deferred tax assets in

4Q’17, diluted EPS is $0.35; net income is $7.676 million, ROA is 1.11%; and ROE is 11.28%.

5 2Q 2018 Financial Highlights Income StatementNet income of $8.8 million, or $0.36 per diluted

share. Return on average assets of 1.12% and return on average equity of 10.57%Net interest income of $29.0 million, up $7.5 million, or 34.8%, from the year ago quarter.Merger related expenses of $3.1 million reduced diluted EPS by $0.10,

after tax.An increase in the fair value of capitalized mortgage loan servicing rights (due to price) increased non-interest income by $0.5 million, or diluted EPS by $0.02, after tax.$0.7 million loan loss provision expense (compared to an

expense of $0.6 million in year ago quarter). Provision expense driven primarily by portfolio loan growth.Gains on mortgage loans of $3.3 million is essentially unchanged from the year ago quarter. Slightly higher mortgage loan sales volume

was offset by a lower margin.Balance Sheet/CapitalCompleted acquisition of TCSB Bancorp, Inc., the parent company of Traverse City State Bank, on April 1, 2018 (“TCSB Merger”). Data processing conversions completed in June 2018.Total

portfolio loans grew $101.4 million, or 19.6% annualized (excluding $294.5 million of portfolio loans acquired in the TCSB Merger). Deposits totaled $2.78 billion at 6/30/18 compared to $2.40 billion at 12/31/17. 2Q’18 growth of $62.4

million, or 10.3% annualized (excluding $287.7 million of deposits acquired in TCSB Merger). The 2Q’18 growth was primarily in brokered time deposits.No share repurchases during 2Q ‘18. New 2018 share repurchase plan authorized for up to 5%

of outstanding shares. TBV per share increased to $12.47 at 6/30/18 from $12.34 at 12/31/17.Paid a 15 cent per share cash dividend on common stock on 5/15/18.

6 YTD Financial Summary 6ME 6/30/18 6ME 6/30/17 6ME 6/30/16 6ME 6/30/15 Net interest

income $ 52,916 $ 42,958 $ 39,393 $ 36,792 Income before taxes $ 22,083 $ 17,189 $ 15,106 $ 13,804 Net income $ 17,978 $ 11,905 $ 10,538 $ 9,400 Diluted EPS $ 0.78 $ 0.55 $ 0.48 $ 0.40 Return on average assets,

annualized 1.22% 0.93% 0.87% 0.83% Return on average equity, annualized 12.09% 9.38% 8.67% 7.46% Note: Dollars in thousands, except per share data. 2018 YTD net interest income increased $10.0 million, or 23.2%.2018 YTD net income

increased $6.1 million, or 51.0%.2018 YTD diluted EPS increased $0.23, or 41.8%.2018 YTD ROA and ROE (annualized) both improved.

7 Our Michigan Markets Independent Bank branches – 68 (including 5 former TCSB branches) TCSB

branches acquired 4/1/2018. Since 2012, substantial changes have been implemented to streamline and optimize our branch delivery network.Significant market presence and opportunity to gain market share in attractive Michigan

markets.Acquisition of Traverse City State Bank adds five branches in attractive Northwestern Michigan.Forbes “Best in Banks and Credit Unions” Survey (published in June 2018) ranked Independent Bank second in the State of Michigan (and #1

for banks headquartered in Michigan) in customer satisfaction.Michigan’s unemployment rate was 4.5% in June 2018 (up 0.1% from one year ago and 0.5% above the June 2018 U.S. unemployment rate of 4.0%). Independent Bank loan production

offices (not pictured Fairlawn and Columbus, Ohio)

Our Markets – Regional Region Cities Branches 6/30/18Portfolio Loans(1) %

ofLoans(1) 6/30/18Deposits(3) % of Deposits(3) 6/30/17 Portfolio Loans(2) 6/30/17 Deposits(3) East / “Thumb” Bay City / Saginaw 23 $ 392 17% $ 772 32% $ 347 $ 742 West Grand Rapids /

Ionia 22 716 30% 699 29% 632 694 Central Lansing 11 211 9% 379 15% 210 336 Southeast Troy 7 591 25% 337 14% 458 344 Northwest Traverse

City 5 317 14% 249 10% n/a n/a Ohio Columbus -- 123 5% n/a n/a 33 n/a Total 68 $2,350 100% $2,436 100% $1,680 $2,116 Note: Dollars are in millions.Loans exclude those related to resort lending ($84 million) and

purchased mortgage loans ($33 million).Loans exclude those related to resort lending ($96 million) and purchased mortgage loans ($36 million). Deposits exclude reciprocal deposits, brokered deposits and certain other “non-market”

deposits. 8

9 Low Cost Deposit Franchise Focused on Core Deposit Growth Deposit Highlights$2.78 billion in total

deposits at 6/30/18.Substantially all core funding.$2.12 billion of transaction accounts (76.3% of total deposits).Total deposits increased $87.3 million, or 3.9%, since 6/30/17 (excluding brokered deposits and $287.7 million of deposits

acquired in TCSB Merger).Average deposits per branch of $37.6 million at 6/30/18 vs. $20.2 million at 12/31/11 (an increase of 86.1%).2018 focus:Commercial – small to middle market business and public funds.Treasury management services.Retail

– checking accounts and debit card services. Deposit Composition – 6/30/18 Cost of Deposits (%)/Total Deposits (billions)

Diversified Loan PortfolioFocused on High Quality Growth Lending Highlights17 consecutive quarters of

net loan growth.$2.531 billion in total loans at 6/30/18 (including $64.1 million of loans held for sale).2Q 2018 lending results include (growth rates below exclude $294.5 million of portfolio loans acquired in TCSB Merger):Commercial loans

net growth of $9.3 million, or 4.3% annualized.Consumer installment loans net growth of $42.4 million, or 52.3% annualized.Portfolio mortgage loans net growth of $49.8 million, or 22.4% annualized. 2Q’18 mortgage loan origination volume of

$226.3 million (down 3.8% from 2Q’17).2018 focus:Commercial – businesses with $1 million to $100 million in annual sales.Consumer – through branch network, internet and indirect channels.Residential mortgage – purchase money (both salable and

portfolio) and QRM and home equity lending opportunities. Loan Composition – 6/30/18 Yield on Loans (%)/Total Portfolio Loans (billions) 10

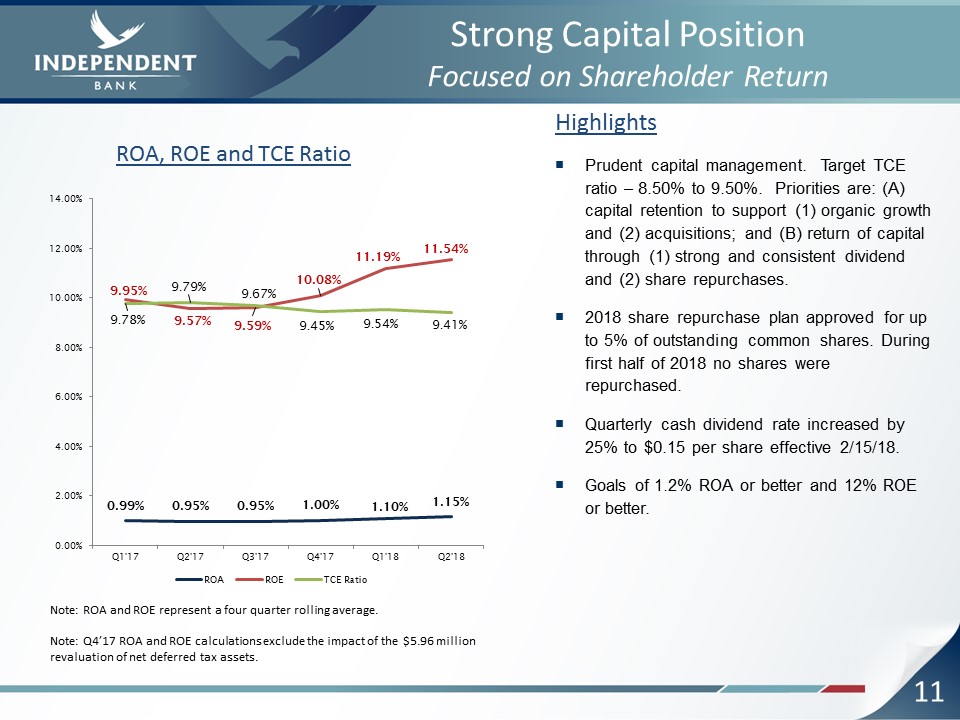

11 Strong Capital PositionFocused on Shareholder Return HighlightsPrudent capital management. Target

TCE ratio – 8.50% to 9.50%. Priorities are: (A) capital retention to support (1) organic growth and (2) acquisitions; and (B) return of capital through (1) strong and consistent dividend and (2) share repurchases.2018 share repurchase plan

approved for up to 5% of outstanding common shares. During first half of 2018 no shares were repurchased. Quarterly cash dividend rate increased by 25% to $0.15 per share effective 2/15/18.Goals of 1.2% ROA or better and 12% ROE or

better. Note: ROA and ROE represent a four quarter rolling average. ROA, ROE and TCE Ratio Note: Q4’17 ROA and ROE calculations exclude the impact of the $5.96 million revaluation of net deferred tax assets.

12 Net Interest Margin/Income HighlightsInterest rate sensitivity profile of the loan and securities

portfolios, in combination with a low cost core deposit base, positions us to slightly benefit from a rising interest rate environment.Net interest income increased 21.1% in 2Q’18 vs. 1Q’18 due primarily to a 22 basis point increase in the

net interest margin and a $352.1 million increase in average interest-earning assets.2018 goal (IBCP only) is to grow net interest income by approximately 10% to 11% over 2017 as average loans increase. Seeing pressure on deposit rates due to

the increases in the target federal funds rate/short-term interest rates. Net Interest Margin (TE)(%) Net Interest Income ($ in Millions)

13 Net Interest Income and Net Interest Margin Details Summary2Q’18 net interest income of $28.980

million, up $5.044 million from 1Q’18. The linked quarter increase was due to a $6.321 million increase in interest income and fees on loans that was partially offset by a $15K decrease in interest income on securities and investments and by

a $1.262 million increase in interest expense on deposits and borrowings. The increase in interest income and fees on loans was due to an increase in average balance and in the average yield. Interest recoveries (net) on previously

charged-off or non-accrual loans declined by $3K. One more day in the quarter increased net interest income by $162K net. The tax equivalent net interest margin (NIM) increased 22 bps (3.93% vs. 3.71%) due to a 34 bps increase in the yield on

interest earning assets that was partially offset by a 12 bps increase in the cost of funds (interest expense as a percentage of average interest-earning assets). 2Q’18 discount accretion on the TCSB acquired loans of $0.628 million increased

the NIM by 8.5 basis points. Average yield on new/renewed commercial loans was 5.39% on fixed rate (52.5% of production) and 4.87% on variable rate (47.5% of production), 2Q’18 volume of $83.4 million with an estimated average duration of 2.7

years. Average yield on new retail loans (mortgage and consumer installment) was 4.49%, 2Q’18 volume of $169.6 million with an estimated average duration of 3.7 years.Loan Portfolio DetailsCommercial loans: Interest income increased $4.497

million due to a 50 bps increase in the average yield (5.38% vs. 4.88%), a $249.9 million increase in the average balance and one more day in the quarter ($162K impact). Interest recoveries (net) increased by $15K. This increased the average

yield by 1 bps. Mortgage loans (includes loans held for sale): Interest income increased $1.458 million due to a $197.7 million increase in the average balance and a 12 bps increase in the average yield (4.40% vs. 4.28%) . Interest recoveries

(net) decreased by $22K, this decreased the average yield by 1 bps.Consumer installment loans: Interest income increased $366K due to a $28.6 million increase in the average balance and one more day in the quarter ($42K impact) The average

yield was unchanged (at 4.54%). Interest recoveries (net) increased by 4K (negligible impact on average yield).Other FactorsSecurities and investments: Interest income decreased $15K due to a $34.117 million decrease in average balance that

was partially offset by a 14 bps increase in the average TE yield (2.75% vs. 2.61%) and one more day in the quarter ($3K impact).Deposits and borrowings: Interest expense increased $1.262 million due to a $222.1 million increase in the

average balance of interest-bearing liabilities, an 18 basis point increase in the average cost of interest-bearing liabilities (0.85% vs. 0.67%), and one more day in the quarter ($45K impact). Analysis of Linked Quarter Increase

14 Non-interest Income HighlightsDiverse sources of non-interest income which totaled $12.3 million

in 2Q’18.2Q’18 total non-interest income represents approximately 29.8% of total revenue (net interest income and non-interest income).Service charges on deposits declined by $0.2 million, or 3.0%, YTD 2018 vs. 2017.Interchange revenue

increased by $0.8 million, or 21.0%, YTD 2018 vs. 2017, due primarily to a reclassification under ASU 2014-09 (which also increased interchange expense by $0.7 million).2Q’18 gains on mortgage loans totaled $3.3 million, which was essentially

unchanged from 2Q’17, as higher loan sales volumes were offset by margin pressure.2Q’18 mortgage loan servicing includes a $0.518 million increase in fair value adjustment due to price. 2Q’17 included a $0.648 million decrease in fair value

adjustment due to price. YTD 2018 Non-interest Income Breakout Non-interest Income Trends ($ in Millions)

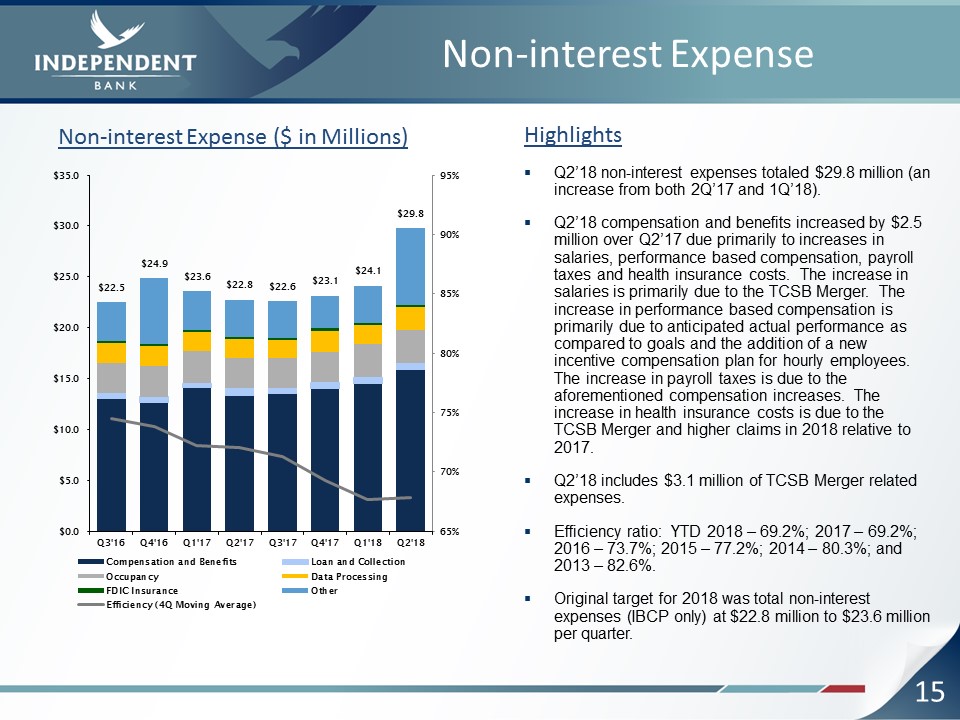

15 Non-interest Expense HighlightsQ2’18 non-interest expenses totaled $29.8 million (an increase from

both 2Q’17 and 1Q’18).Q2’18 compensation and benefits increased by $2.5 million over Q2’17 due primarily to increases in salaries, performance based compensation, payroll taxes and health insurance costs. The increase in salaries is primarily

due to the TCSB Merger. The increase in performance based compensation is primarily due to anticipated actual performance as compared to goals and the addition of a new incentive compensation plan for hourly employees. The increase in payroll

taxes is due to the aforementioned compensation increases. The increase in health insurance costs is due to the TCSB Merger and higher claims in 2018 relative to 2017.Q2’18 includes $3.1 million of TCSB Merger related expenses. Efficiency

ratio: YTD 2018 – 69.2%; 2017 – 69.2%; 2016 – 73.7%; 2015 – 77.2%; 2014 – 80.3%; and 2013 – 82.6%.Original target for 2018 was total non-interest expenses (IBCP only) at $22.8 million to $23.6 million per quarter. Non-interest Expense ($ in

Millions)

16 Investment Securities Portfolio HighlightsHigh quality, liquid, diverse portfolio with relatively

short duration.Fair value of $453.1 million(1) at 6/30/18.Net unrealized loss of $5.6 million at 6/30/18.65% of the portfolio is AAA rated (or backed by the U.S. Government).3.09 year estimated average duration with a weighted average yield

of 2.91% (with TE gross up).Approximately 29% of the portfolio is variable rate. (1) Includes investments in bank CD’s of $2.5 million but excludes equity securities of $0.3 million. Investment Portfolio by Type (6/30/18) Investment

Portfolio by Rating (6/30/18)

17 Credit Quality Summary Note 1: Non-performing loans and non-performing assets exclude troubled

debt restructurings that are performing.Note 2: 12/31/16 30 to 89 days delinquent data excludes $1.63 million of payment plan receivables that were held for sale. Non-performing Assets ($ in Millions) ORE/ORA ($ in Millions) Non-performing

Loans ($ in Millions) 30 to 89 Days Delinquent ($ in Millions)

18 Credit Cost Summary Note: Dollars all in millions. Provision for Loan Losses Loan Net

Charge-Offs/Recoveries Allowance for Loan Losses

19 Classified Assets and New Default Trends Note: Dollars all in millions. Total Classified

Assets Commercial Loan New Defaults Total Loan New Defaults Retail Loan New Defaults

20 Troubled Debt Restructurings (TDRs) TDR HighlightsWorking with client base to maximize sustainable

performance.The specific reserves allocated to TDRs totaled $6.3 million at 6/30/18.A majority of our TDRs are performing under their modified terms but remain in TDR status for the life of the loan.93.1% of TDRs are current as of

6/30/18.Commercial TDR Statistics:45 loans with $8.0 million book balance.97.0% performing.WAR of 5.60% (accruing loans).Well seasoned portfolio; over 92% of accruing loans are not only performing but have been for over a year since

modification.Retail TDR Statistics:604 loans with $53.4 million book balance.94.0% performing.WAR of 5.44% (accruing loans).Well seasoned portfolio; over 98% of accruing loans are not only performing but have been for over a year since

modification. TDRs ($ in Millions) 93% of TDRs are Current

21 Acquisition of TCSB Bancorp, Inc.Status Update Category Comments Loans TCSB total loans on

April 1, 2018 were $301.8 million (including $1.3 million of loans held for sale). Non PCI (purchase credit impaired) portfolio loans totaled $297.0 million with an estimated fair value of $291.3 million (a discount of $5.74 million, or

1.9%). PCI portfolio loans totaled $3.6 million with an estimated fair value of $2.9 million (a discount of $0.74 million, or 20.3%). The total discount was $6.48 million or 2.2% of the total TCSB portfolio loans. This discount will be

accreted into interest income based on the estimated lives of the related loans. In 2Q’18 approximately $0.6 million of this discount was accreted into interest income. Future expected discount accretion is approximately: $0.6 million is

3Q’18; $0.5 million in 4Q’18; $1.8 million in 2019 and $1.1 million in 2020. Deposits TCSB total deposits were $288.1 million on April 1, 2018. A discount of $0.4 million was recorded on time deposits and brokered time deposits. This

discount will be accreted into interest expense over the life of the related deposits. In addition, a core deposit intangible of $5.8 million was recorded. This core deposit intangible will be amortized into non-interest expense on an

accelerated basis over ten years ($0.208 million per quarter in 2018; $0.186 million per quarter in 2019; and $0.169 million per quarter in 2020). Borrowings and subordinated debentures TCSB total borrowings and subordinated debentures

were $14.5 million and $5.2 million, respectively. A discount of $0.15 million and $1.39 million was recorded on these borrowings and subordinated debentures, respectively. These discounts will be accreted into interest expense over the

remaining life of the related borrowings or subordinated debentures. Goodwill Based on the preliminary valuations, IBCP acquired $342.8 million of total assets and assumed $307.3 million of total liabilities, resulting in net assets

acquired of $35.5 million in the TCSB Merger. Given the total purchase price of $64.5 million for TCSB, the resulting goodwill in the TCSB merger is $29.0 million. Integration and conversion Integration efforts proceeded as planned. The

core data processing conversion occurred on June 16 and 17, 2018 and the mortgage loan servicing conversion occurred on June 30, and July 1, 2018). IBCP expects to meet its previously announced 31% reduction (or approximately $0.9 million per

quarter) in TCSB non-interest expenses beginning in 3Q’18. Merger related expenses TCSB Merger related expenses totaled $3.1 million and $3.3 million for the second quarter and first six months of 2018, respectively. Only a minor amount

(less than $0.1 million) of TCSB Merger related expenses are expected in 3Q’18. These expenses include investment banking fees (for IBCP), certain accounting and legal costs, various contract termination fees, data processing conversion

costs, payments made on officer change-in-control contracts, and employee severance costs.

22 YTD 2018 Actual Performance vs. Original Outlook Category Outlook Lending Continued growthIBCP

only goal of 15 to 18% overall loan growth in 2018, primarily supported by increases in commercial loans, mortgage loans and consumer loans. Expect much of this growth to occur in the last three quarters of 2018. This growth forecast also

assumes a stable Michigan economy. 2Q’18 update: Annualized quarterly loan growth of 19.6% (excluding $294.5 million of acquired TCSB portfolio loans). The second quarter is generally stronger due to seasonal factors. Expect full year 2018

actual loan growth to be generally consistent with original outlook. First half 2018 actual loan growth of 15.4% (annualized) is consistent with outlook. Net Interest Income Growth driven primarily by higher portfolio loan balances, expect

total deposits (IBCP only, excluding brokered) to be relatively flat in 2018 IBCP only goal of approximately 10% to 11% increase in net interest income (NII) over 2017. Expect the net interest margin to be relatively stable. Forecast assumes

two 0.25% increases in the federal funds rate (one in March 2018 and one in September 2018) and long-term rates up slightly over year end 2017 levels. 2Q’18 update: Net interest income increased $7.5 million, or 34.8%, over 2Q’17. Net

interest margin increased to 3.93% (from 3.60% in 2Q’17). Actual performance significantly better than original outlook. Provision for Loan Losses Steady asset quality metricsVery difficult area to forecast. Future provision levels will be

particularly sensitive to loan net charge-offs, watch credit levels, loan default volumes, and TDR portfolio performance as well as loan growth. The allowance as a percentage of total loans was at 1.12% at 12/31/17. Do not expect credit

provision in 2018 due to portfolio loan growth and a decline in recoveries of previously charged-off loans. Quarterly provision (expense) for loan losses averaging approximately $1.25 million (IBCP only) would not be unreasonable. 2Q’18

update: Actual provision for loan losses of $0.7 million. NPAs up $2.5 million from 3/31/18 but remain at low level. Loan net charge-offs of $0.2 million in 2Q’18. Actual performance better than original outlook. Non-interest Income IBCP

only - forecasted quarterly range of $9.8 million to $10.9 million with total for year comparable to 2017 (excluding securities net gains or losses)Expect mortgage-banking revenues and mortgage lending volumes in 2018 to be comparable to

2017. Expect service charges on deposits and interchange income in 2018 to be generally comparable to 2017. 2Q’18 update: Actual total non-interest income of $12.3 million. If adjust actual for $0.5 million fair value increase due to price in

capitalized mortgage loan servicing rights, adjusted total of $11.8 million, which is above the projected range due primarily to TCSB Merger. Expect 3Q’18 and 4Q’18 non interest income in range of $11.5 million to $11.7 million (inclusive of

TCSB). Non-interest Expenses IBCP only - forecasted quarterly range of $22.8 to $23.6 million with total for the year up slightly (under 1%) vs. 2017No significant changes in any particular line item expected in 2018 vs. 2017 2Q’18 update:

Actual total non-interest expenses of $29.8 million. This total included $3.2 million of Merger related expenses and $0.8 million of additional performance based compensation that was not included in the original forecast. Expect 3Q’18 and

4Q’18 total non-interest expenses in the range of $25.2 million to $25.8 million with variability within the range due primarily to performance based compensation. This range reflects cost saves of approximately $0.9 million per quarter from

TSCB integration that are in place beginning in 3Q’18. Income Taxes Approximately 19% to 20% effective tax rate in 2018. This assumes a 21% statutory federal corporate income tax rate during 2018. 2Q’18 update: Actual income tax expense of

$2.07 million, which is an effective tax rate of 19.0%.

23 Strategic Initiatives Balance SheetGenerate quality loan growth with continued focus on

commercial and consumer installment lending as well as salable and portfolio mortgage loans.Remain slightly asset sensitive and positioned to benefit from higher interest rates (short duration investment portfolio, large variable rate loan

portfolio and strong core deposit base with a significant amount of small to medium balance transaction accounts). Income StatementGenerate increased net interest income through change in earning asset mix (increased loans to deposits ratio

and reduced level of investment securities).Increase non-interest income with focus on transaction related revenue (treasury management and debit card) and mortgage banking revenue.Continued selective reductions in certain non-interest

expenses (credit related costs, branch optimization, process re-engineering and outsourcing). However, now expect growth in compensation and employee benefits expense and in occupancy expense due to expanded mortgage-banking

operations.Improved efficiency ratio: Mid 60% range near-term and low 60% range longer-term. Achieve improvements primarily through revenue growth.Enterprise Risk ManagementWell managed approach to lending with sound underwriting.Meet

increased compliance and regulatory requirements.Focus on data security and loss prevention.TCSB Bancorp, Inc.Successful integration of Traverse City State Bank (customers and associates).

24 Q&A and Closing Remarks Question and Answer SessionClosing RemarksThank you for attending

!NASDAQ: IBCP