Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the transition period from _______ to __________

Commission file number: 000-55205

Alpine 4 Technologies Ltd.

(Exact name of registrant as specified in its charter)

|

Delaware

|

46-5482689

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer Identification No.)

|

|

|

|

|

4742 N. 24th Street Suite 300

|

|

|

Phoenix, AZ

|

85016

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

Registrant's telephone number, including area code: 855-777-0077 ext 801

(Former name, former address and former fiscal year, if changed since last report)

Securities Registered pursuant to Section 12(b) of the Act: None

Securities Registered pursuant to Section 12(g) of the Act: Class A Common Stock, $0.0001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No⌧

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes No ⌧

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ⌧ No ◻

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ⌧ No ◻

Indicate by check mark if disclosure of delinquent filings pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

|

Large accelerated filer

|

◻

|

Accelerated filer

|

◻

|

|

Non-accelerated filer

|

◻

|

Smaller reporting company

|

⌧

|

|

Emerging Growth Company

|

⌧

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ◻ No ⌧

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter. As of June 30, 2017, the aggregate market value of the voting and non-voting common equity held by non-affiliates, computed based on the average bid and asked price of the Class A common stock, was $2,499,935.

State the number of shares outstanding of each of the issuer's classes of common equity, as of the latest practicable date: As of April 10, 2018, the issuer had 24,507,853 shares of its Class A common stock issued and outstanding and 1,600,000 shares of its Class B common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

1

ALPINE 4 TECHNOLOGIES LTD.

FISCAL YEAR ENDED DECEMBER 31, 2016

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

PART I

|

Page

|

|

|

|

|

|

|

ITEM 1.

|

BUSINESS

|

3

|

|

ITEM 1A.

|

RISK FACTORS

|

10

|

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

15

|

|

ITEM 2.

|

PROPERTIES

|

16

|

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

16

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

16

|

|

PART II

|

||

|

ITEM 5.

|

MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

21

|

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

21

|

|

ITEM 7.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

21

|

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

22

|

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

22

|

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURES

|

23

|

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

22

|

|

ITEM 9B.

|

OTHER INFORMATION22

|

|

|

PART III

|

||

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

23

|

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

23

|

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

23

|

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

23

|

|

ITEM 14.

|

PRINCIPAL ACCOUNTING FEES AND SERVICES

|

23

|

|

PART IV

|

||

|

ITEM 15.

|

EXHIBITS, FINANCIAL STATEMENT SCHEDULES

|

23

|

|

SIGNATURES

|

36 | |

2

PART I

Special Note Regarding Forward-Looking Statements

Information included or incorporated by reference in this Annual Report on Form 10-K contains forward-looking statements. All forward-looking statements are inherently uncertain as they are based on current expectations and assumptions concerning future events or future performance of the Company. Readers are cautioned not to place undue reliance on these forward-looking statements, which are only predictions and speak only as of the date hereof. Forward-looking statements may contain the words "believes," "project," "expects," "anticipates," "estimates," "forecasts," "intends," "strategy," "plan," "may," "will," "would," "will be," "will continue," "will likely result," and similar expressions, and are subject to numerous known and unknown risks and uncertainties. Additionally, statements relating to implementation of business strategy, future financial performance, acquisition strategies, capital raising transactions, performance of contractual obligations, and similar statements may contain forward-looking statements. In evaluating such statements, prospective investors and shareholders should carefully review various risks and uncertainties identified in this Report, including the matters set forth under the captions "Risk Factors" and in the Company's other SEC filings. These risks and uncertainties could cause the Company's actual results to differ materially from those indicated in the forward-looking statements. The Company disclaims any obligation to update or publicly announce revisions to any forward-looking statements to reflect future events or developments.

Although forward-looking statements in this Annual Report on Form 10-K reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties, and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those specifically addressed under the heading "Risk Factors Related to Our Business" below, as well as those discussed elsewhere in this Annual Report on Form 10-K. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report on Form 10-K. We file reports with the Securities and Exchange Commission ("SEC"). You can read and copy any materials we file with the SEC at the SEC's Public Reference Room, 100 F. Street, NE, Washington, D.C. 20549. You can obtain additional information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us.

We disclaim any obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this Annual Report on Form 10-K. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this Annual Report, which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

ITEM 1. BUSINESS.

Our Business

Company Background and History

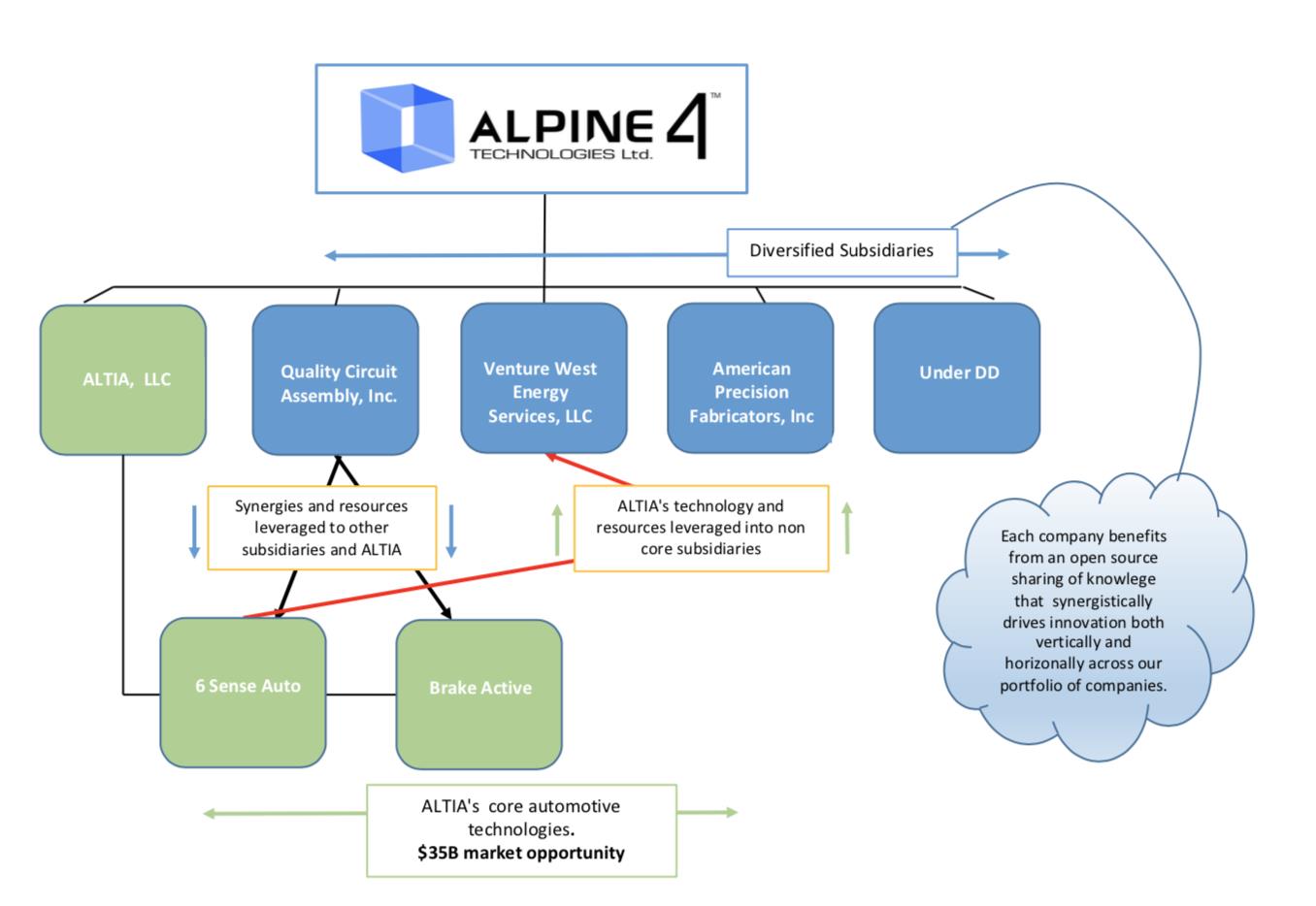

Alpine 4 Technologies Ltd. (the "Company") was incorporated under the laws of the State of Delaware on April 22, 2014. The Company was formed to serve as a vehicle to effect an asset acquisition, merger, exchange of capital stock, or other business combination with a domestic or foreign business. As of the date of this Report, the Company is a technology holding company owning three companies (ALTIA, LLC, Quality Circuit Assembly, Inc., and Venture West Energy Services (formerly Horizon Well Testing, LLC).

3

Who We Are

Alpine 4 is a publicly held enterprise with four principles at the core of its business: Synergy, Innovation, Drive, and Excellence (S.I.D.E.). At Alpine 4, we believe synergistic innovation drives excellence. By anchoring these words to our combined experience and capabilities, we are able to aggressively pursue opportunities within and across vertical markets. We deliver solutions that not only drive industry standards, but also increase value for our shareholders.

At Alpine 4, we understand the nature of how technology and innovation can accentuate a business. We strive to develop strategic synergies between our holdings to create value and operational excellence within a unique long-term perspective.

Our Strategy

Alpine 4's strategy is to provide Fortune 500-level execution strategies in its subsidiary companies and market segments to businesses and companies that have the most to benefit from this access.

Alpine 4 feels this opportunity exists in smaller middle market operating companies with revenues between $5 to $150 million. In this target rich environment, businesses generally sell at more reasonable multiples, presenting greater opportunities for operational and strategic improvements and have greater potential for growth. Implementation of our strategy within our holdings is accomplished by the offering of strategic and tactical MBA-level training and development, delivered via the following modules:

|

-

|

Alpine 4 Mini MBA program; and

|

|

-

|

An Alpine 4 developed ERP (Enterprise Resource Planning system) and collaboration system called SPECTRUMebos. SPECTRUMebos is what we are defining as an Enterprise Business Operating System (ebos). This system will combine the key technology software components of Accounting and Financial Reporting, an Enterprise Resource Planning System (ERP), a Document Management System (DMS), a Business Intelligence (BI) platform and a Customer Resource Management (CRM) hub which will be tethered to management reporting and collaboration toolsets. Management believes that these tools will help drive real-time information in two directions: first, to the front lines by empowering customer-facing stakeholders; and second, back to management for planning, problem solving, and integration. Management believes that SPECTRUMebos will be the technology "secret sauce" in managing our portfolio of companies and, in time, may be offered to external customers.

|

4

All great strategies must have trades offs. Therefore, Alpine 4 avoids companies that have unionized employees, businesses that have more than $150 million in revenue and companies that reside in highly regulated business industries.

Diversification

It is our goal to help drive Alpine 4 into a leading multi-faceted holding company with diverse products and services that not only benefit from one another as whole but also have the benefit of independence. This type of corporate structure is about having our subsidiaries prosper through strong onsite leadership, while working synergistically with other Alpine 4 holdings. Alpine 4 has been set up with a holding company model, with Presidents who will run each business, and Managers with specific industry related experience who, along with Kent Wilson, the CEO of Alpine 4, will help guide our portfolio of companies as needed. Alpine 4 will work with our Presidents and Managers to ensure that our motto of S.I.D.E (Synergistic, Innovation, Drives, Excellence) is utilized. Further, we plan to work with our subsidiaries and capital partners to provide the proper capital allocation and, to work to make sure each business is executing at high levels.

In 2016, we saw the beginning of our plan for diversification take hold with the acquisition of Quality Circuit Assembly, Inc. ("QCA") when Alpine 4 acquired 100% of QCA's stock effective April 1, 2016. Additional information relating to our acquisition of QCA can be found in our Current Report on Form 8-K, filed with the SEC on March 15, 2016.

In October of 2016, Alpine 4 formed a new Limited Liability Company called ALTIA (Automotive Logic & Technology In Action) to create an independent subsidiary for Alpine 4's 6th Sense Auto product and its BrakeActive product.

Effective, January 1, 2017, Alpine 4 acquired 100% of Venture West Energy Services ("VWES") (formerly Horizon Well Testing, LLC). . Additional information about the acquisition of VWES can be found below under "Recent Developments" and in our Current Reports on Form 8-K filed with the SEC on December 8, 2016, and January 13, 2017.

As of the date of this Annual Report, our subsidiaries and product groups consisted of the following:

At the core of our business strategy is our focus on scalable corporate platform solutions. We have built a strong portfolio of manufacturing, software, and energy driven businesses with a focus on long-term value creation.

Subsidiaries & Product Groups

|

-

|

ALTIA, LLC is an automotive technology company with several core product offerings.

|

|

|

|

– | 6th Sense Auto is a connected car technology that provides a distinctive and powerful advantage to management, sales, finance and service departments at automotive dealerships in order to increase productivity, profitability and customer retention. 6thSenseAuto uses disruptive technology to improve inventory management, reduce costs, increase sales, and enhance service. |

|

|

– | BrakeActive™ is a safety device that improves a vehicle's third brake light's ability to greatly reduce or prevent a rear end collision by as much as 40%. According to the Nation Highway Safety Administration (2010), most rear end collisions can be reduced by 90% if trailing vehicles had one additional second to react. The Company's new programmable technology and device aims to do just that. |

|

-

|

QCA - Since 1988, Quality Circuit Assembly ("QCA") has been providing electronic contract manufacturing solutions delivered to its customers via strategic business partnerships. Our abilities encompass a wide variety of skills, beginning with prototype development and culminating in the ongoing manufacturing of a complete product or assembly. Turnkey solutions are tailored around each customer's specific requirements. Conveniently located in San Jose, California with close proximity to San Jose airport and all major carriers, QCA's primary aim is to provide contract-manufacturing solutions to market leading companies within the industrial, scientific, instrumentation, military, medical and green industries.

|

|

|

-

|

Venture West Energy Services (formerly Horizon Well Testing) - Based in Oklahoma City, OK. Verizon West Energy Services ("VWES") is focused on supporting the oil and gas industry in Texas, Oklahoma, and Arkansas. Our knowledgeable team provides complete flow back, water transfer, and roustabout services to several of the largest oil producers in the United States. VWES utilizes a high-quality fleet of manifolds, sand separators and testing units as well as a highly experienced workforce to provide customers with timely and accurate measurements.

|

|

|

-

|

American Precision Fabricators – Based in Fort Smith, Arkansas is a sheet metal fabricator that provides American made fabricated metal parts, assemblies and sub - assemblies to Original Equipment Manufacturers ("OEM"). The Company supplies several industries with fabricated parts that it creates in-house. It offers several production capabilities with its state-of-the-art machinery.

|

|

5

Recent Developments

Termination of Letter of Intent with Lattice Incorporated

On February 28 2018, the Company terminated its previously announced letter of intent to acquire all of the outstanding securities of Lattice Incorporated ("Lattice"), together with letters of intent with certain of Lattice's creditors to convert their debt in Lattice into equity. After conducting due diligence, the Company determined to not proceed with the acquisition.

Convertible Notes

On October 4, 2017, the Company entered into a convertible note with an unrelated lender for $60,000 with net proceeds of $55,000. The note is due July 4, 2018 and bears interest at 12% per annum. After 180 days, the note is convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from October 5, 2017. The prepayment penalty is equal to 20% to 25% of the outstanding note amount depending on when prepaid.

On October 11, 2017, the Company entered into a convertible note with an unrelated lender for $58,500 with net proceeds of $55,500. The note is due July 20, 2018 and bears interest at 12% per annum. After 180 days, the note is convertible to the Company's Class A common stock at a discount of 38% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from October 11, 2017. The prepayment penalty is equal to 10% to 27% of the outstanding note amount depending on when prepaid.

On November 2, 2017, the Company entered into a variable convertible note with unrelated 3rd party for $115,000 with net proceeds of $107,000. The note is due May 2, 2018 and bears interest at 10% per annum. The note is immediately convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from November 2, 2017 with a $750 prepayment penalty.

On November 1, 2017, in contemplation of entering into the November 2, 2017 note, the Company released 150,000 shares of the 500,000 returnable shares (see Note 8 – Other items Related to Equity). The shares were consideration for the second note dated November 2, 2017, and as such will be accounted for as a discount associated with that note.

On November 28, 2017, the Company entered into a variable convertible note with unrelated 3rd party for $105,000. The note is due June 15, 2018 and bears interest at 10% per annum. The note is immediately convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from November 28, 2018 with a $750 prepayment penalty.

On December 6, 2017, the Company entered into a variable convertible note with unrelated 3rd party for $86,000 with net proceeds of $79,000. The note is due June 6, 2018 and bears interest at 10% per annum. After 180 days, the note is convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion.

6

Other Equity transaction

On November 1, 2017, the Company entered into an agreement with the investor relations firm RedChip Companies Inc. ("RedChip"). The agreement is for six months with a review after 90 days. The Company will pay RedChip $2,500 per month for months 1-3 and $5,000 per month for months 4-6. For the first 90 days of service the Company issued 275,000 shares of the Company's Class A common shares which are restricted pursuant to the provisions of Rule 144. For the second 90 days of service the Company will issue 125,000 shares for the Company's Class A common shares which are restricted pursuant to the provisions of Rule 144.

Completion of Earnhardt Auto Center Pilot Program

On July 12, 2017, the Company announced that its subsidiary ALTIA had successfully concluded its 90 day pilot with Phoenix, AZ-based Earnhardt Auto Centers of its innovative 6th Sense Auto product platform. The pilot program was installed at the Earnhardt Chevrolet dealership in Chandler, AZ, and performed well above expectations and will continue on in the store for the foreseeable future. ALTIA is also in negotiations with several other large automotive groups regarding its 6th Sense Auto and BrakeActive aftermarket products and anticipates larger orders in 2018.

6th Sense Auto is designed for the modern "connected car" and dedicated to helping large dealerships like Earnhardt improve their inventory management, engine diagnostics, service maintenance and personalized customer support through wireless, cloud-based software.

With approximately 40 million new and used cars sold in the United States annually, management believes that ALTIA's market opportunity is very large, and believes that the Company's 6th Sense Auto product is positioned to be a dominant player in this industry.

Amendment of Amended and Restated Certificate of Incorporation; Change in Capitalization

At the annual shareholders meeting, held on November 18, 2017, the Company's shareholders approved an amendment (the "Amendment") to the Company's Amended and Restated Certificate of Incorporation (the "Certificate of Incorporation"), to reduce the number of shares of the Company's Class A Common Stock authorized from 500,000,000 shares to 100,000,000 shares; to reduce the number of shares of the Company's Class B Common Stock authorized from 100,000,000 shares to 5,000,000 shares; and to increase the number of shares of Preferred Stock from 5,000,000 to 10,000,000 shares. The Company filed the Amendment on December 15, 2017.

Resignation of Chief Financial Officer

On December 31, 2017, the Company's Board of Directors accepted the resignation of David Schmitt as the Company's Chief Financial Officer. Mr. Schmitt decided to leave the Company for personal reasons and to spend more time with family. There were no disputes or disagreements with the Company.

Following Mr. Schmidt's resignation, the Company's Board of Directors began a search for a new Chief Financial Officer.

Issuance of Options

On July 31, 2017, the Company issued options to purchase 488,500 shares of the Company's Class A common stock to employees and consultants of the Company. The options were issued pursuant to the Company's 2016 Stock Option and Stock Award Plan (the "Plan"). The options granted vest over four years, and the exercise price of the options granted is $0.13, which was the last closing bid price of the Company's common stock as traded on the OTCQB Market.

7

The options were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

Acquisition of Horizon Well Testing / Venture West Energy Services, LLC

On November 30, 2016, the Company entered into a Stock Purchase Agreement (the "HWT SPA") with Horizon Well Testing, L.L.C., an Oklahoma limited liability company ("HWT") and its sole shareholder Adam Martin (the "HWT Seller"). Effective as of January 1, 2017, Alpine 4 acquired and took full control of HWT.

Since 2010, VWES has been providing services to the oil and gas industry. This acquisition is another step in Alpine 4's strategy of diversification through acquisitions.

Pursuant to the HWT SPA, Alpine 4, HWT and the HWT Seller agreed on the terms pursuant to which Alpine 4 would purchase from HWT Seller all of the outstanding membership interests of HWT (the "HWT Interests"). The purchase price paid by Alpine 4 for the HWT Interests consisted of cash, a note, a convertible note, and securities consideration. The "Cash Consideration" paid was $2,200,000. The "Note" consisted of a secured note in the amount of $300,000, secured by a subordinated security interest in the assets of HWT. The Note bears interest at 1% and will be payable in full by July 31, 2017. The "Convertible Note" consisted of a secured convertible note in the amount of $1,500,000, secured by a subordinated security interest in the assets of HWT. The HWT Seller has the opportunity to convert the Convertible Note into shares of Alpine 4's Class A common stock at a conversion price of $8.50 after a restricted period according to securities laws. The Convertible Note bears interest at 5% and is payable in full with a balloon payment on the 18-month anniversary of the closing date of the transaction with no monthly payments. The "Securities" consisted of two components, an aggregate of 379,403 shares of Alpine 4's Class A common stock issued to the Seller, and a warrant to purchase an additional 75,000 shares of Class A common stock.

In the HWT SPA, the HWT Seller acknowledged and agreed that his entry into consulting agreements with Alpine 4 was an integral part of the transaction contemplated by the HWT SPA. As such, the HWT Seller agreed to enter into consulting agreements with Alpine 4 and HWT, and continue to work with HWT for a period of time agreed upon by Alpine 4 and the HWT Seller.

HWT subsequently changed its name to Venture West Energy Services ("VWES").

Employees

As of the date of this Report, we had 132 full-time and 5 part-time employees. We believe that our relationship with our employees is good. Other than as disclosed in this Report or previously filed with the SEC, we have no employment agreements with our employees.

ITEM 1A. RISK FACTORS

Because of the following factors, as well as other factors affecting the Company's financial condition and operating results, past financial performance should not be considered to be a reliable indicator of future performance, and investors should not use historical trends to anticipate results or trends in future periods.

8

Risks Associated With Our Business and Operations

Alpine 4 is an "emerging growth company," and the reduced disclosure requirements applicable to "emerging growth companies" could make our common stock less attractive to investors.

Alpine 4 is an "emerging growth company," as defined in the JOBS Act. For as long as we are an emerging growth company, we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding advisory "say-on-pay" votes on executive compensation and shareholder advisory votes on golden parachute compensation. We will remain an "emerging growth company" until the earliest of (i) the last day of the fiscal year during which we have total annual gross revenues of $1 billion or more; (ii) the last date of the fiscal year following the fifth anniversary of the date of the first sale of common stock under the Company's first filed registration statement; (iii) the date on which we have, during the previous three-year period, issued more than $1 billion in non-convertible debt; and (iv) the date on which we are deemed to be a "large accelerated filer" under the Exchange Act. We will be deemed a large accelerated filer on the first day of the fiscal year after the market value of our common equity held by non-affiliates exceeds $700 million, measured on October 31.

We cannot predict if investors will find our common stock less attractive to the extent we rely on the exemptions available to emerging growth companies. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. An emerging growth company can therefore delay the adoption of certain accounting standards until those standards would otherwise apply to private companies.

A Company that elects to be treated as an emerging growth company shall continue to be deemed an emerging growth company until the earliest of (i) the last day of the fiscal year during which it had total annual gross revenues of $1,000,000,000 (as indexed for inflation), (ii) the last day of the fiscal year following the fifth anniversary of the date of the first sale of common stock under the Company's first filed registration statement; (iii) the date on which it has, during the previous 3-year period, issued more than $1,000,000,000 in non-convertible debt; or (iv) the date on which is deemed to be a 'large accelerated filer' as defined by the SEC, which would generally occur upon it attaining a public float of at least $700 million.

However, we are choosing to "opt out" of such extended transition period, and as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Our independent auditors have expressed substantial doubt about our ability to continue as a going concern.

Alpine 4 has incurred net losses of $20,433,875 since inception through December 31, 2017. This net loss was primarily driven in 2015 by stock issuance to employees. Because we have yet to attain profitable operations, in their report on our financial statements for the period ended December 31, 2017, our independent auditors included an explanatory paragraph regarding their substantial doubt about our ability to continue as a going concern. While management believes Alpine 4 will have net operating gains beginning in the second quarter of 2018, there can be no guarantee that we will be able to achieve these net operating gains. Our ability to continue as a going concern is subject to our ability to generate a profit and/or obtain necessary funding from outside sources, including obtaining additional funding from the sale of our securities, increasing sales or obtaining loan from various financial institutions where possible. Our net operating losses increase the difficulty in meeting such goals and there can be no assurances that such methods will prove successful. Our financial statements contain additional note disclosures describing the management's assessment of our ability to continue as a going concern.

9

Management of Alpine 4 cannot guarantee that Alpine 4 will continue to generate revenues which could result in a total loss of the value of your investment if it is unsuccessful in its business plans.

While Alpine 4 and its subsidiaries have long term Purchase Order arrangements with its large Contract Manufacturing customers and Master Service Agreements with its Oil Field Services customers that can provide a level of dependable revenue, there can be no assurance that Alpine 4 will be able to continue to generate revenues or that revenues will be sufficient to maintain its business. As a result, investors or shareholders could lose all of their investment if Alpine 4 is not successful in its proposed business plans.

Alpine 4's needs could exceed the amount of time or level of experience its officers and directors may have. Alpine 4 will be dependent on key executives, and the loss of the services of the current officers and directors could severely impact Alpine 4's business operations.

Alpine 4's business plan does not provide for the hiring of any additional employees other than outlined in its plan of operations until sales will support the expense. Until that time, the responsibility of developing Alpine 4's business and fulfilling the reporting requirements of a public company will fall upon the officers and the directors. In the event they are unable to fulfill any aspect of their duties to Alpine 4, it may experience a shortfall or complete lack of sales resulting in little or no profits and eventual closure of our business.

Additionally, the management of future growth will require, among other things, continued development of Alpine 4's financial and management controls and management information systems, stringent control of costs, increased marketing activities, and the ability to attract and retain qualified management, research, and marketing personnel. The loss of key executives or the failure to hire qualified replacement personnel would compromise Alpine 4's ability to generate revenues or otherwise have a material adverse effect on Alpine 4. There can be no assurance that Alpine 4 will be able to successfully attract and retain skilled and experienced personnel.

Significant time and management resources are required to ensure compliance with public company reporting and other obligations. Taking steps to comply with these requirements will increase our costs and require additional management resources, and does not ensure that we will be able to satisfy them.

We are a publicly reporting company. As a public company, we are required to comply with applicable provisions of the Sarbanes-Oxley Act of 2002, as well as other federal securities laws, and rules and regulations promulgated by the SEC and the various exchanges and trading facilities where our common stock may trade, which result in significant legal, accounting, administrative and other costs and expenses. These rules and requirements impose certain corporate governance requirements relating to director independence, distributing annual and interim reports, stockholder meetings, approvals and voting, soliciting proxies, conflicts of interest, and codes of conduct, depending on where our shares trade. Our management and other personnel will need to devote a substantial amount of time to ensure that we comply with all applicable requirements.

As we review our internal controls and procedures, we may determine that they are ineffective or have material weaknesses, which could impact the market's acceptance of our filings and financial statements.

In connection with the preparation of this Annual Report, we conducted a review of our internal control over financial reporting for the purpose of providing the management report required by these rules. During the course of our review and testing, we have identified deficiencies and have been unable to remediate them before we were required to provide the required reports. Furthermore, because we have material weaknesses in our internal control over financial reporting, we may not detect errors on a timely basis and our financial statements may be materially misstated. Even if we are able to remediate the material weaknesses, we may not be able to conclude on an ongoing basis that we have effective internal controls over financial reporting, which could harm our operating results, cause investors to lose confidence in our reported financial information and cause the trading price of our stock to fall. In addition, as a public company we are required to file in a timely manner accurate quarterly and annual reports with the SEC under the Securities Exchange Act of 1934 (the "Exchange Act"), as amended. Any failure to report our financial results on an accurate and timely basis could result in sanctions, lawsuits, delisting of our shares from the market or trading facility where our shares may trade, or other adverse consequences that would materially harm our business.

10

Because Alpine 4 has shown a net loss since inception, ownership of Alpine 4 shares is highly risky and could result in a complete loss of the value of your investment if Alpine 4 is unsuccessful in its business plans.

Based upon current plans, Alpine 4 expects to stop incurring operating losses in future periods as its subsidiaries move from their Optimization Phase to its Asset Producing Phase. However new additional subsidiaries may incur significant expenses associated with the growth of those businesses. Further, there is no guarantee that it will be successful in realizing future revenues or in achieving or sustaining positive cash flow at any time in the future. Any such failure could result in the possible closure of its business or force Alpine 4 to seek additional capital through loans or additional sales of its equity securities to continue business operations, which would dilute the value of any shares you receive in connection with the Share Exchange.

Growth and development of operations will depend on the growth in the Alpine 4 acquisition model and from organic growth from its subsidiaries businesses. If Alpine 4 cannot find desirable acquisition candidates it may not be able to generate growth with future revenues.

Alpine 4 expects to acquire two additional companies in 2018 resulting in projected annualized revenue of $41 million by the end of Q4 2018. There is no guarantee that it will be successful in realizing future revenue growth from its acquisition model. As such it is highly dependent on suitable candidates to acquire which the supply of those candidates cannot be guaranteed and is driven from the market for M&A.

Alpine 4 has limited management resources, and will be dependent on key executives. The loss of the services of the current officers and directors could severely impact Alpine 4's business operations and future development, which could result in a loss of revenues and adversely impact the ability to ever sell any Exchange Shares received through participation in the Share Exchange.

Alpine 4 is relying on a small number of key individuals to implement its business and operations and, in particular, the professional expertise and services of Kent B. Wilson, our President, Chief Executive Officer, and Secretary, and Charles Winters, our Chairman of the Board of Directors. Mr. Wilson intends to serve full time in his capacities with Alpine 4 to work to develop and grow the Company. Nevertheless, Alpine 4 may not have sufficient managerial resources to successfully manage the increased business activity envisioned by its business strategy. In addition, Alpine 4's future success depends in large part on the continued service of Mr. Wilson. If he chooses not to serve as an officer or if he is unable to perform his duties, this could have an adverse effect on Company business operations, financial condition and operating results if we are unable to replace Mr. Wilson or Mr. Winters with other individuals qualified to develop and market our business. The loss of their services could result in a loss of revenues, which could result in a reduction of the value of any ownership of Alpine 4.

Competition that Alpine 4 faces is varied and strong.

Alpine 4's subsidiaries' products and industries as a whole are subject to competition. There is no guarantee that we can sustain our market position or expand our business.

We compete with a number of entities in providing products to our customers. Such competitor entities include a variety of large nationwide corporations, including but not limited to public entities and companies that have established loyal customer bases over several decades.

Many of our current and potential competitors are well established and have significantly greater financial and operational resources, and name recognition than we have. As a result, these competitors may have greater credibility with both existing and potential customers. They also may be able to offer more competitive products and services and more aggressively promote and sell their products. Our competitors may also be able to support more aggressive pricing than we will be able to, which could adversely affect sales, cause us to decrease our prices to remain competitive, or otherwise reduce the overall gross profit earned on our products.

Our success in business and operations will depend on general economic conditions.

The success of Alpine 4 and its subsidiaries depends, to a large extent, on certain economic factors that are beyond its control. Factors such as general economic conditions, levels of unemployment, interest rates, tax rates at all levels of government, competition and other factors beyond Alpine 4's control may have an adverse effect on the ability of our subsidiaries to sell its products, to operate, and to collect sums due and owing to them.

11

Alpine 4 may not be able to successfully implement its business strategy, which could adversely affect its business, financial condition, results of operations and cash flows. If Alpine 4 cannot successfully implement its business strategy, it could result in the loss of the value of your investment.

Successful implementation of our business strategy depends on our being able to acquire additional businesses and grow our existing subsidiaries, as well as on factors specific to the industries in which our subsidiaries operate, and the state of the financial industry and numerous other factors that may be beyond our control. Adverse changes in the following factors could undermine our business strategy and have a material adverse effect on our business, our financial condition, and results of operations and cash flow:

|

o

|

The competitive environment in the industries in which our subsidiaries operate that may force us to reduce prices below the optimal pricing level or increase promotional spending;

|

|

o

|

Our ability to anticipate changes in consumer preferences and to meet customers' needs for our products in a timely cost effective manner; and

|

|

o

|

Our ability to establish, maintain and eventually grow market share in these competitive environments.

|

Our revenue growth rate depends primarily on our ability to satisfy relevant channels and end-customer demands, identify suppliers of our necessary ingredients and to coordinate those suppliers, all subject to many unpredictable factors.

We may not be able to identify and maintain the necessary relationships with suppliers of product and services as planned. Delays or failures in deliveries could materially and adversely affect our growth strategy and expected results. As we supply more customers, our rate of expansion relative to the size of such customer base will decline. In addition, one of our biggest challenges is securing an adequate supply of suitable product. Competition for product is intense, and commodities costs subject to price volatility.

Our ability to execute our business plan also depends on other factors, including:

|

o

|

ability to keep satisfied vendor relationships

|

|

o

|

hiring and training qualified personnel in local markets;

|

|

o

|

managing marketing and development costs at affordable levels;

|

|

o

|

cost and availability of labor;

|

|

o

|

the availability of, and our ability to obtain, adequate supplies of ingredients that meet our quality standards; and

|

|

o

|

securing required governmental approvals in a timely manner when necessary.

|

Risks Related to Our Common Stock

Alpine 4 stockholders, and others who choose to purchase shares of Alpine 4 common stock if and when offered, may have difficulty in reselling their shares due to the limited public market or state Blue Sky laws.

Our common stock is currently quoted on the OTC market. Current Alpine 4 stockholders and persons who desire to purchase them in any trading market should be aware that there might be additional significant state law restrictions upon the ability of investors to resell our shares. Accordingly, investors should consider any secondary market for our securities to be a limited one.

12

Sales of our common stock under Rule 144 could reduce the price of our stock.

Under Rule 144 affiliates of Alpine 4 may not sell more than one percent of the total issued and outstanding shares in any 90-day period and must resell the shares in an unsolicited brokerage transaction at the market price. If substantial amounts of our common stock become available for resale under Rule 144 once a market has developed for our common stock, the then-prevailing market prices for our common stock may be reduced.

We may, in the future, issue additional securities, which would reduce our stockholders' percent of ownership and may dilute our share value.

Our Certificate of Incorporation, as amended to date, authorizes us to issue 100,000,000 shares of Class A common stock, and 5,000,000 shares of Class B common stock. As of the date of this Annual Report, we had 24,507,853 shares of Class A common stock outstanding, and 1,600,000 shares of Class B common stock outstanding. Accordingly, we may issue up to an additional 75,492,147 shares of Class A common stock, and an additional 3,400,000 shares of Class B common stock. The future issuance of additional shares of Class A common stock may result in additional dilution in the percentage of our Class A common stock held by our then existing stockholders. We may value any Class A common stock issued in the future on an arbitrary basis including for services or acquisitions or other corporate actions that may have the effect of diluting the value of the shares held by our stockholders, and might have an adverse effect on any trading market for our Class A common stock. Additionally, our board of directors may designate the rights terms and preferences of one or more series of preferred stock at its discretion including conversion and voting preferences without prior notice to our stockholders. Any of these events could have a dilutive effect on the ownership of our shareholders, and the value of shares owned.

Raising additional capital or purchasing businesses through the issuance of common stock will cause dilution to our existing stockholders.

We may seek additional capital through a combination of private and public equity offerings, debt financings, collaborations, and strategic and licensing arrangements, as well as issuing stock to make additional business or asset acquisitions. To the extent that we raise additional capital through the sale of common stock or securities convertible or exchangeable into common stock or through the issuance of equity for purchases of businesses or assets, your ownership interest in Alpine 4 will be diluted.

Raising additional capital may restrict our operations or require us to relinquish rights.

We may seek additional capital through a combination of private and public equity offerings, debt financings, collaborations, and strategic and licensing arrangements. To the extent that we raise additional capital through the sale of common stock or securities convertible or exchangeable into common stock, the terms of any such securities may include liquidation or other preferences that materially adversely affect your rights as a stockholder. Debt financing, if available, would increase our fixed payment obligations and may involve agreements that include covenants limiting or restricting our ability to take specific actions, such as incurring additional debt, making capital expenditures or declaring dividends. If we raise additional funds through collaboration, strategic partnerships and licensing arrangements with third parties, we may have to relinquish valuable rights to our intellectual property, future revenue streams or grant licenses on terms that are not favorable to us.

Market volatility may affect our stock price and the value of your shares.

The market price for our common stock is likely to be volatile, in part because the volume of trades of our common stock. In addition, the market price of our common stock may fluctuate significantly in response to a number of factors, most of which we cannot control, including, among others:

13

|

●

|

announcements of new products, brands, commercial relationships, acquisitions or other events by us or our competitors;

|

|

●

|

regulatory or legal developments in the United States and other countries;

|

|

●

|

fluctuations in stock market prices and trading volumes of similar companies;

|

|

●

|

general market conditions and overall fluctuations in U.S. equity markets;

|

|

●

|

variations in our quarterly operating results;

|

|

●

|

changes in our financial guidance or securities analysts' estimates of our financial performance;

|

|

●

|

changes in accounting principles;

|

|

●

|

our ability to raise additional capital and the terms on which we can raise it;

|

|

●

|

sales of large blocks of our common stock, including sales by our executive officers, directors and significant stockholders;

|

|

●

|

additions or departures of key personnel;

|

|

●

|

discussion of us or our stock price by the press and by online investor communities; and

|

|

●

|

other risks and uncertainties described in these risk factors.

|

If securities or industry analysts do not publish or cease publishing research or reports or publish misleading, inaccurate or unfavorable research about us, our business or our market, our stock price and trading volume could decline.

The trading market for our common stock will be influenced by the research and reports that securities or industry analysts may publish about us, our business, our market or our competitors. We currently have limited coverage and may never obtain increased research coverage by securities and industry analysts. If no or few securities or industry analysts cover our company, the trading price and volume of our stock would likely be negatively impacted. If we obtain securities or industry analyst coverage and if one or more of the analysts who covers us downgrades our stock or publishes inaccurate or unfavorable research about our business, or provides more favorable relative recommendations about our competitors, our stock price would likely decline. If one or more of these analysts ceases coverage of us or fails to publish reports on us regularly, demand for our stock could decrease, which could cause our stock price or trading volume to decline.

Future sales of our common stock may cause our stock price to decline.

Sales of a substantial number of shares of our common stock in the public market or the perception that these sales might occur could significantly reduce the market price of our common stock and impair our ability to raise adequate capital through the sale of additional equity securities.

Our compliance with the Sarbanes-Oxley Act and SEC rules concerning internal controls may be time consuming, difficult and costly.

Alpine 4's executive officers do not have experience being officers of a public company. It may be time consuming, difficult and costly for us to develop and implement the internal controls and reporting procedures required by Sarbanes-Oxley. We may need to hire additional financial reporting, internal controls and other finance staff in order to develop and implement appropriate internal controls and reporting procedures. If we are unable to comply with Sarbanes-Oxley's internal controls requirements, we may not be able to obtain the independent accountant certifications that Sarbanes-Oxley Act requires publicly-traded companies to obtain.

Alpine 4 may issue Preferred Stock with voting and conversion rights that could adversely affect the voting power of the holders of Common Stock.

Alpine 4's Board of Directors may issue Preferred Stock with voting and conversion rights that could adversely affect the voting power of the holders of Common Stock. Any such provision may be deemed to have a potential anti-takeover effect, and the issuance of Preferred Stock in accordance with such provision may delay or prevent a change of control of Alpine 4. The Board of Directors also may declare a dividend on any outstanding shares of Preferred Stock. All outstanding shares of Preferred Stock are fully paid and non-assessable.

14

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not applicable to Smaller Reporting Companies.

ITEM 2. PROPERTIES.

Alpine 4 Technologies, Ltd maintains our corporate office in rented offices at 4742 N. 24th Street, Suite 300, Phoenix, AZ 85016. The monthly rent obligation is approximately $3,600 per month.

Quality Circuit Assembly, Inc. rents a location at 1709 Junction Court #380 San Jose, CA 95112. The monthly rent obligation is approximately $27,500 per month.

Venture West Energy Services, LLC rent a property 6504 SW 29th, Bldg B Oklahoma City, OK 73179. The monthly rent obligation is approximately $4,500 per month.

American Precision Fabricators, rents a property 4401 Savannah St. Fort Smith, AR 72903 for $15,833 per month.

ITEM 3. LEGAL PROCEEDINGS.

Kevin Cannon et al. v. Alpine 4 Technologies Ltd., Jeff Hail, et al, Arizona Superior Court, Maricopa County, Cas No. CV2017-055699. On October 4, 2017, Kevin Cannon and Michelle Hanby, individually and on behalf of It's a Date LLC and Brake Plus NWA, Inc., filed a lawsuit in the Arizona Superior Court, Maricopa County, against the Company and several other defendants, including Jeff Hail, the Company's Sr. Vice President. The claim against the Company alleges tortious interference of contract by the Company. The Company brought a motion to dismiss the Complaint for failure to state a claim on which relief could be granted. The Court permitted the plaintiffs to amend their complaint, which they did. The Company has filed another motion dismiss the Complaint for failure to state a claim on which relief could be granted. As of the date of this Report, the second motion to dismiss had not been ruled on by the Court. The Company disputes the claim against it and intends to defend vigorously against the lawsuit.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

MARKET PRICES AND DIVIDEND DATA

Stock Prices

As of the date of this Report, our Class A common stock is listed on the OTCQB Market under the symbol ALPP. Alpine 4 plans to work with a market maker and other professionals to drive trading volume and interest in the stock.

The following table shows the range of high and low sales price information for our Class A common stock as quoted on the OTC Markets for the calendar years 2016 and 2017 and for the first quarter of 2018. Our Class A common stock was accepted for trading beginning on December 19, 2016. The quotations below reflect inter-dealer prices, without retail mark-up, mark-down or commissions and may not represent actual transactions.

15

Calendar Year

|

2018

|

2017

|

2016

|

||||||||||||||||||||||

| High | Low | High | Low | High | Low | |||||||||||||||||||

|

First quarter

|

$

|

0.34

|

$

|

0.123

|

$

|

14.00

|

$

|

2.40

|

|

|

|

|

||||||||||||

|

Second quarter

|

|

|

$

|

2.54

|

$

|

0.12

|

|

|

|

|

||||||||||||||

|

Third quarter

|

|

|

$

|

0.25

|

$

|

0.09

|

|

|

|

|

||||||||||||||

|

Fourth quarter

|

|

|

$

|

0.46

|

$

|

0.098

|

$

|

10.00

|

$

|

5.00

|

||||||||||||||

The high and low sales prices for our Class A common stock on April 9, 2018, were $0.125 and $0.122, respectively.

PLEASE NOTE: Trading in the Company's Class A common stock is limited, and as such, relatively small sales may have a disproportionately large impact on the trading price. The prices shown in the table above reflect the price fluctuations resulting from relatively low volume of trades.

Shareholders

As of April 9, 2018, Alpine 4 had 402 shareholders of record. This number does not include an indeterminate number of stockholders whose shares are held by brokers in street name. The holders of our common stock are entitled to one vote for each share held of record on all matters submitted to a vote of stockholders. Holders of our common stock have no preemptive rights and no right to convert their common stock into any other securities. There are no redemption or sinking fund provisions applicable to our common stock.

Dividends

Alpine 4 has not declared any cash dividends on its common stock since inception and does not anticipate paying such dividends in the foreseeable future. Any decisions as to future payments of dividends will depend on Alpine 4's earnings and financial position and such other facts, as the Board of Directors deems relevant.

Director Independence

Alpine 4 is not required by any outside organization (such as a stock exchange or trading facility) to have independent directors.

Securities Authorized for Issuance under Equity Compensation Plans

Adoption of 2016 Stock Option and Stock Award Plan

On November 10, 2016, the Company's Board of Directors adopted the Company's 2016 Stock Option and Stock Award Plan (the "Plan"). Pursuant to the Plan, the Company may issue stock options, including incentive stock options and non-qualifying stock options, and stock grants to employees and consultants of the Company, as set forth in the Plan, a copy of which was filed as an exhibit to the Company's Quarterly Report on Form 10-Q for the period ended September 30, 2016.

The Company has reserved 2,000,000 shares of the Company's Class A common stock for issuance under the Plan.

Equity Compensation Plan Information

|

Plan category

|

Number of securities to be issued upon exercise of outstanding options, warrants and rights

|

Weighted-average exercise price of outstanding options, warrants and rights

|

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a))

|

|||||||||

|

|

(a)

|

(b)

|

(c)

|

|||||||||

|

Equity compensation plans approved by security holders

|

782,250

|

$

|

0.42

|

1,217,750

|

||||||||

|

Equity compensation plans not approved by security holders

|

||||||||||||

|

Total

|

782,250

|

$

|

0.42

|

1,217,750

|

||||||||

16

Recent Sales of Unregistered Securities

Issuances in 2018

Issuance of Convertible Notes

Subsequent to the year ended December 31, 2017, the Company issued a series of short-term notes payable for aggregate proceeds of $260,000. The notes bear interest at 15% per annum.

On January 23, 2018, the Company entered into a fixed price convertible note for $150,000. The note is due October 8, 2018 and bears interest at 12% per annum. After 180 days, the note is convertible into shares of the Company's Class A common stock at a fixed rate of $0.16 per share.

On January 5, 2018, the Company entered into a variable convertible note for $64,000. The note is due July 5, 2018 and bears interest at 10% per annum. The note is immediately convertible into the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for the ten days prior to conversion.

On April 3, 2018, the Company entered into a variable convertible note with an unrelated lender for $85,000. The note is due January 2, 2019 and bears interest at 10% per annum. The note is immediately convertible into shares of the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion.

On April 5, 2018, the Company entered into a variable convertible note with an unrelated lender for $128,000. The note is due December 18, 2018 and bears interest at 12% per annum. After 180 days, the note is convertible into shares of the Company's Class A common stock at a discount of 40% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion.

On April 9, 2018, the Company entered into a variable convertible note for $124,199. The note is due January 9, 2019 and bears interest at 12% per annum. After 180 days, the note is convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for the ten days prior to conversion.

On April 9, 2018, the Company entered into a variable convertible note for $37,800. The note is due January 9, 2019 and bears interest at 12% per annum. After 180 days, the note is convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for the ten days prior to conversion.

The convertible notes issued between January and April 2018 were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

Issuances in 2017

During the quarter ended September 30, 2017, the Company issued 106,000 shares of its restricted Class A common stock in connection with services, 177,342 shares for note conversions and 500,000 shares which are fully returnable upon the payment of a convertible note. Of the 500,000 shares 150,000 have been released for return in exchange for another note with no issuance of shares on the second note.

17

The shares of Class A common stock were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

During the quarter ended June 30, 2017, the Company issued 154,000 shares of its restricted Class A common stock in connection with services.

The shares of Class A common stock were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

On July 31, 2017, the Company issued options to purchase 488,500 shares of the Company's Class A common stock to employees and consultants of the Company. The options were issued pursuant to the Company's 2016 Stock Option and Stock Award Plan (the "Plan"). The options granted vest over four years, and the exercise price of the options granted is $0.13, which was the last closing bid price of the Company's common stock as traded on the OTCQB Market.

The options were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

During the quarter ended March 31, 2017, the Company sold an aggregate of 2,001 shares of its restricted Class A common stock in private offerings. The Company raised an aggregate of approximately $15,000. The Company issued 36,964 shares of its restricted Class A common stock in connection with the conversion of convertible notes payable. Additionally, the Company issued 379,403 shares of its Class A common stock for the acquisition of HWT.

The shares of common stock were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

Convertible Notes

On October 4, 2017, the Company entered into a convertible note with an unrelated lender for $60,000 with net proceeds of $55,000. The note is due July 4, 2018 and bears interest at 12% per annum. After 180 days, the note is convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from October 5, 2017. The prepayment penalty is equal to 20% to 25% of the outstanding note amount depending on when prepaid.

On October 11, 2017, the Company entered into a convertible note with an unrelated lender for $58,500 with net proceeds of $55,500. The note is due July 20, 2018 and bears interest at 12% per annum. After 180 days, the note is convertible to the Company's Class A common stock at a discount of 38% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from October 11, 2017. The prepayment penalty is equal to 10% to 27% of the outstanding note amount depending on when prepaid.

On November 2, 2017, the Company entered into a variable convertible note with unrelated 3rd party for $115,000 with net proceeds of $107,000. The note is due May 2, 2018 and bears interest at 10% per annum. The note is immediately convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from November 2, 2017 with a $750 prepayment penalty.

On November 1, 2017, in contemplation of entering into the November 2, 2017 note, the Company released 150,000 shares of the 500,000 returnable shares (see Note 8 – Other items Related to Equity). The shares were consideration for the second note dated November 2, 2017, and as such will be accounted for as a discount associated with that note.

On November 28, 2017, the Company entered into a variable convertible note with unrelated third party for $105,000. The note is due June 15, 2018 and bears interest at 10% per annum. The note is immediately convertible to the Company's Class A common stock at a discount of 35% to the average of the three lowest trading closing prices of the stock for ten days prior to conversion. The Company can prepay the convertible note up to 180 days from November 28, 2018 with a $750 prepayment penalty.

The convertible notes issued between October and December 2017 were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

18

Other Equity transaction

On November 1, 2017, the Company entered into an agreement with the investor relations firm RedChip Companies Inc. ("RedChip"). The agreement is for six months with a review after 90 days. The Company will pay RedChip $2,500 per month for months 1-3 and $5,000 per month for months 4-6. For the first 90 days of service the Company issued 275,000 shares of the Company's Class A common shares which are restricted pursuant to the provisions of Rule 144. For the second 90 days of service the Company will issue 125,000 shares for the Company's Class A common shares which are restricted pursuant to the provisions of Rule 144.

The shares of common stock were issued and will be without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

Issuances in 2016

Subsequent to March 31, 2016, the Company issued an additional 1,550,000 shares of its Class A common stock. All of the 1,550,000 shares were issued in connection with employee and consultant compensation arrangements.

During the quarter ended June 30, 2016, the Company sold an aggregate of 670 shares of its restricted Class A common stock in private offerings. The Company raised an aggregate of approximately $6,000. The Company issued 58,520 shares of its restricted class A common stock in connection with the conversion of convertible notes payable. Additionally, the Company issued 161,548 (130,000 to employees) shares of its Class A common stock for services.

The shares of Class A common stock were issued without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder.

Issuance of Equity Securities in Venture West/Horizon Transaction

In connection with the acquisition of Venture West Energy Services ("VWES") (formerly Horizon Well Testing, L.L.C.), described in more detail above under "Recent Developments," Alpine 4 purchased all of the outstanding stock of VWES (the "VWES Stock") from Alan Martin (the "Seller"). The purchase price paid by Alpine 4 for the VWES Stock consisted of cash, a note, a convertible note, and securities consideration. The "Cash Consideration" paid was $2,200,000. The "Note" consisted of a secured note in the amount of $300,000, secured by a subordinated security interest in the assets of VWES . The Note bears interest at 1% and will be payable in full by April 30, 2017. The "Convertible Note" consisted of a secured convertible note in the amount of $1,500,000, secured by a subordinated security interest in the assets of VWES . The VWES Seller has the opportunity to convert the Convertible Note into shares of Alpine 4's Class A common stock at a conversion price of $8.50 after a restricted period according to securities laws. The Convertible Note bears interest at 5% and is payable in full with a balloon payment on the 18-month anniversary of the closing date of the transaction with no monthly payments. The "Securities" consisted of two components, an aggregate of 379,403 shares of Alpine 4's Class A common stock issued to the Seller, and a warrant to purchase an additional 75,000 shares of Class A common stock.

The Note, the Convertible Note, and the Securities was issued to the Seller pursuant to a share exchange agreement with the Seller, in which the Seller made certain representations and warranties, including that he was an accredited investor, that he was acquiring the securities for his own account and not for the account of another, that he was acquiring the securities for investment purposes and not with a view to distribute the securities acquired, and that he had sufficient knowledge and experience in financial and business matters to evaluate the merits and risks of an investment in the Company. As such, the securities were issued to the Seller without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and the rules and regulations promulgated thereunder. The VWES transaction did not involve a public offering.

19

Stock Options to Employees

On April 7, 2017, the Company issued 741,500 options to purchase shares of the Company's Class A common stock to 34 employees and consultants of the Company. The options were issued pursuant to the Company's 2016 Stock Option and Stock Award Plan (the "Plan"). The options granted vest and the exercise price of the options granted was $0.90, which was the last closing bid price of the Company's common stock as traded on the OTC QB Market..

The Company provided to each of the recipients of the Options copies of the Company's public filings including the financial information and other disclosures about the Company. The options were issued to the recipients without registration under the 1933 Act in reliance on Section 4(a)(2) of the 1933 Act and rules and regulations promulgated thereunder. The issuance of the options did not involve a public offering of the Company's securities.

Purchases of Equity Securities by the Company and Affiliated Purchasers

During the fourth quarter of 2017, there were no purchases of the Company's equity securities by the Company or affiliated purchasers

ITEM 6. SELECTED FINANCIAL DATA.

Not required for Smaller Reporting Companies.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

There are statements in this Report that are not historical facts. These "forward-looking statements" can be identified by use of terminology such as "believe," "hope," "may," "anticipate," "should," "intend," "plan," "will," "expect," "estimate," "project," "positioned," "strategy" and similar expressions. You should be aware that these forward-looking statements are subject to risks and uncertainties that are beyond our control. For a discussion of these risks, you should read this entire Report carefully, especially the risks discussed under "Risk Factors." Although management believes that the assumptions underlying the forward looking statements included in this Report are reasonable, they do not guarantee our future performance, and actual results could differ from those contemplated by these forward looking statements. The assumptions used for purposes of the forward-looking statements specified in the following information represent estimates of future events and are subject to uncertainty as to possible changes in economic, legislative, industry, and other circumstances. As a result, the identification and interpretation of data and other information and their use in developing and selecting assumptions from and among reasonable alternatives require the exercise of judgment. To the extent that the assumed events do not occur, the outcome may vary substantially from anticipated or projected results, and, accordingly, no opinion is expressed on the achievability of those forward-looking statements. In the light of these risks and uncertainties, there can be no assurance that the results and events contemplated by the forward-looking statements contained in this Report will in fact transpire. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of their dates. We expressly disclaim any obligation to update or revise any forward-looking statements.

Overview and Highlights

Company Background

Alpine 4 Technologies Ltd. (the "Company") was incorporated under the laws of the State of Delaware on April 22, 2014. The Company was formed to serve as a vehicle to affect an asset acquisition, merger, exchange of capital stock, or other business combination with a domestic or foreign business. The Company is a technology holding company owning three companies as of December 31, 2017 (ALTIA, LLC; Quality Circuit Assembly, Inc. ("QCA"); and Venture West Energy Services ("VWES") (formerly Horizon Well Testing, LLC). For 2016, QCA made up most of the revenue for the consolidated financial statements. VWES was not acquired until January 1, 2017, so it is not combined in our 2016 financial statements.

20

Business Strategy

Alpine 4's strategy is to provide Fortune 500-level execution strategies in its subsidiary companies and market segments to businesses and companies that have the most to benefit from this access.

Alpine 4 feels this opportunity exists in smaller middle market operating companies with revenues between $5 to $150 million. In this target rich environment, businesses generally sell at more reasonable multiples, presenting greater opportunities for operational and strategic improvements and have greater potential for growth. Implementation of our strategy within our holdings is accomplished by the offering of strategic and tactical MBA-level training and development, delivered via the following modules:

|

-

|

Alpine 4 Mini MBA program; and

|

|

-

|