Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - Vaulted Gold Bullion Trust | ex32_1.htm |

| EX-31.1 - EXHIBIT 31.1 - Vaulted Gold Bullion Trust | ex31_1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended October 31, 2017 |

or

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from _________ to __________ |

Commission File Number:

001-___________

001-___________

VAULTED GOLD BULLION TRUST

(Exact name of registrant as specified in its charter)

____________________________________________________________________________________

|

Delaware

|

46-7176227

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

c/o Bank of Montreal

3 Times Square

New York, New York 10036

Attention: Legal Department

(Address of principal executive offices)

(212) 885-4000

(Registrant’s telephone number, including area code)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or, an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company”, in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

|

Accelerated filer ☐

|

|

Non-accelerated filer ☒

|

|

Smaller reporting company ☐

|

|

(Do not check if a smaller reporting company)

|

Emerging growth company ☒

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of October 31, 2017, there were 29,656 Gold Deposit Receipts outstanding.

VAULTED GOLD BULLION TRUST

FORM 10-K

FOR THE FISCAL YEAR ENDED OCTOBER 31, 2017

INDEX

FORM 10-K

FOR THE FISCAL YEAR ENDED OCTOBER 31, 2017

INDEX

|

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

|

1 | |

| PART I |

|

2 |

|

Item 1.

|

Business

|

2 |

|

Item 1A.

|

Risk Factors

|

5 |

|

Item 2.

|

Properties

|

12 |

|

Item 3.

|

Legal Proceedings

|

13 |

|

Item 4.

|

Mine Safety Disclosures

|

13 |

| PART II |

|

13 |

|

Item 5.

|

Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity

Securities

|

13 |

|

Item 6.

|

Selected Financial Data

|

13 |

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

13 |

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

16 |

|

Item 8.

|

Financial Statements and Supplementary Data

|

16 |

|

Item 9.

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure.

|

17 |

|

Item 9A.

|

Controls and Procedures

|

17 |

|

Item 9B.

|

Other Information

|

17 |

| PART III |

|

17 |

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

17 |

|

Item 11.

|

Executive Compensation

|

17 |

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

17 |

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

17 |

|

Item 14.

|

Principal Accounting Fees and Services

|

17 |

| PART IV |

|

18 |

|

Item 15.

|

Exhibits, Financial Statement Schedules

|

18 |

| SIGNATURES | 20 | |

i

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

The statements contained in this report that are not purely historical are forward-looking statements. The Vaulted Gold Bullion Trust’s (the “Trust”) forward-looking statements include, but are not limited to, statements regarding its expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predicts,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this report may include, for example, statements about:

| · |

The gold industry;

|

| · |

Sources of and demand for gold bullion; and

|

| · |

The performance of the gold market.

|

The forward-looking statements contained in this report are based on the Trust’s current expectations and beliefs concerning future developments and their potential effects on the Trust. There can be no assurance that future developments affecting the Trust will be those that it has anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Trust’s control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include those factors described under the heading “Risk Factors” in this Form 10-K. Should one or more of these risks or uncertainties materialize, or should any of the Trust’s assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. The Trust undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

1

PART I

| Item 1. |

Business

|

Introduction

The Trust issues Depositary Receipts (the “Gold Deposit Receipts”) representing an undivided beneficial ownership in a fixed quantity of unencumbered, allocated gold bullion (“Gold Bullion”). The Gold Bullion is held for the benefit of holders of Gold Deposit Receipts in an account operated by Bank of Montreal at the Royal Canadian Mint (the “Mint”). The Bank of New York Mellon serves as the trustee of the Trust. The Gold Deposit Receipts are separate from the Gold Bullion.

About the Trust

General. This discussion highlights information about the Trust.

The Vaulted Gold Bullion Trust. The Trust was initially formed on December 10, 2013. The Trust is governed by the Second Amended and Restated Depositary Trust Agreement, dated May 11, 2017 (the “Depositary Trust Agreement”), by and among The Bank of New York Mellon, as “Trustee,” BNY Trust of Delaware, as “Delaware Trustee,” Bank of Montreal, as “Initial Depositor,” and BMO Capital Markets Corp., as “Underwriter.” The Trust is not a registered investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Trust is not a commodity pool for purposes of the Commodity Exchange Act (the “CEA”), and the Initial Depositor is not subject to regulation by the Commodity Futures Trading Commission (the “CFTC”) as a commodity pool operator, or a commodity trading advisor.

The Trust issues Gold Deposit Receipts representing an undivided beneficial ownership in a fixed quantity of unencumbered, allocated Gold Bullion. The Gold Bullion is held for the benefit of holders of Gold Deposit Receipts in an account operated by Bank of Montreal at the Mint.

Initial Depositor. The initial depositor of the Trust is Bank of Montreal (“Bank of Montreal” or the “Bank”). The Bank commenced business in Montreal in 1817 and was incorporated in 1821 by an Act of Lower Canada as the first Canadian chartered bank. Since 1871, the Bank has been a chartered bank under the Bank Act, and is named in Schedule I of the Bank Act (Canada) (the “Bank Act”). The Bank Act is the charter of the Bank and governs its operations. The Bank is a registered holding company under the Bank Holding Company Act of 1956 and is certified as a financial holding company under the Gramm-Leach-Bliley Act. The Bank’s head office is located at 129 rue Saint Jacques, Montreal, Quebec, H2Y 1L6, and its executive offices are located at 100 King Street West, First Canadian Place, Toronto, Ontario, M5X 1A1. The Bank’s telephone number is (416) 867-6785.

Bank of Montreal offers a broad range of products and services directly and through Canadian and non-Canadian subsidiaries, offices, and branches. As of October 31, 2017, Bank of Montreal had more than 12 million customers and more than 45,000 full-time equivalent employees. The Bank has over 1,500 bank branches in Canada and the United States and operates internationally in major financial markets and trading areas through its offices in 27 other jurisdictions, including the United States. BMO Financial Corp. (“BFC”) is based in Chicago and wholly-owned by Bank of Montreal. BFC operates primarily through its subsidiary BMO Harris Bank N.A. (“BHB”), which provides banking, financing, investing, and cash management services in select markets in the U.S. Midwest. Bank of Montreal provides a full range of investment dealer services through entities, including BMO Nesbitt Burns Inc., a major fully integrated Canadian investment dealer, and BMO Capital Markets Corp., Bank of Montreal’s wholly-owned registered securities dealer in the United States.

Bank of Montreal conducts business through three operating groups: Personal and Commercial Banking (“P&C”), made up of Canadian P&C and U.S. P&C; Wealth Management; and BMO Capital Markets. Canadian P&C operates across Canada, offering a broad range of products and services, including banking, lending and treasury management. Operating predominately in the U.S. Midwest under the BMO Harris brand, U.S. P&C offers personal and commercial clients banking, lending, and treasury management products and services. Wealth Management serves a full range of client segments from mainstream to ultra-high net worth and institutional, with a broad offering of wealth management products and services including insurance. Wealth Management is a global business with an active presence in markets across Canada, the United States, Europe and Asia. BMO Capital Markets is a North American-based financial services provider offering a complete range of products and services to corporate, institutional and government clients. These include equity and debt underwriting, corporate lending and project financing, mergers and acquisitions advisory services, securitization, treasury management, risk management, debt and equity research, and institutional sales and trading. With approximately 2,400 professionals in 30 locations around the world, including 16 offices in North America, BMO Capital Markets works proactively with clients to provide innovative and integrated financial solutions. Corporate Services consists of Corporate Support Areas and Technology and Operations (“T&O”). Corporate Support Areas provide enterprise-wide expertise and governance support in a variety of areas, including strategic planning, risk management, finance, legal and regulatory compliance, marketing, communications and human resources. T&O manages, maintains and provides governance over information technology, operations services, real estate and sourcing for the Bank.

2

Additional information about the Bank is available by accessing the Bank’s public filings with the SEC, file number 001-13354.

Relationship Between the Initial Depositor and the Trust. The Trust issues Gold Deposit Receipts and uses the proceeds of such issuances to purchase Gold Bullion from Bank of Montreal. The amount paid per ounce of Gold Bullion by the Trust is equal to the spot price at the time of sale to the investor for one troy ounce of Gold Bullion, determined by BMO Capital Markets Corp. using EBS, an offering of EBS BrokerTec (“EBS”), as the source for the spot price of gold, without adjustment or modification. Any deposit fees are remitted promptly to Bank of Montreal which pays all of the Trust’s expenses. The Gold Bullion purchased from Bank of Montreal is held in Bank of Montreal’s account at the Mint, on behalf of the Trust for the benefit of the holders of the Gold Deposit Receipts.

The Mint. The Mint is a Canadian Crown Corporation, incorporated in 1969 by the Royal Canadian Mint Act and is an agent corporation of Her Majesty in right of Canada. Bank of Montreal’s account at the Mint is governed by the gold storage agreement between the Mint and Bank of Montreal (the “Gold Storage Agreement”).

The Mint carries such insurance as it deems appropriate for its businesses and its position as custodian of the Trust’s Gold Bullion. Based on information provided by the Mint, we believe that the insurance carried by the Mint, together with its status as a Canadian Crown corporation with its obligations generally constituting unconditional obligations of the Government of Canada, provides the Trust with such protection in the event of loss or theft of the Trust’s Gold Bullion stored at the Mint that is consistent with the protection afforded under insurance carried by other custodians that store gold commercially. In addition, if the Mint were to become a private enterprise, Bank of Montreal on behalf of the Trust will make a determination whether the Mint should remain the custodian of the Trust’s Gold Bullion in light of applicable circumstances, such as the level of insurance carried by the Mint after such privatization, the availability of other custodians and the risk in moving the Trust’s Gold Bullion to another custodian.

Trust Objective

The objective of the Trust is to provide a secure and convenient way for investors to make an investment in unencumbered, allocated Gold Bullion on a spot basis. As a result, at any given time, the value of the Gold Deposit Receipts is intended to reflect the spot price of gold held by the Trust for the holders of Gold Deposit Receipts.

The Trust issues Gold Deposit Receipts upon the contribution by Bank of Montreal to the Trust of a fixed quantity of Gold Bullion purchased with the proceeds, less the deposit fee and any sales fee, from the sale of Gold Deposit Receipts. Bank of Montreal holds the Gold Bullion in an account that is operated by Bank of Montreal at the Mint in custody for the holders of Gold Deposit Receipts.

BMO Capital Markets Corp. acts as the Underwriter for the sale of Gold Deposit Receipts, pursuant to a distribution agreement among the Trust, Bank of Montreal and BMO Capital Markets Corp. (the “Distribution Agreement”). BMO Capital Markets Corp. has entered, and will continue to enter, into dealer agreements with certain third parties that are registered broker-dealers, or banks or trust companies regulated by the Office of the Comptroller of the Currency and/or one or more state banking regulators that are either direct or indirect DTC Participants. We refer to these third parties, as well as any other dealer that becomes a party to the distribution agreement, as “Authorized Participants.” Only Authorized Participants will be involved in the distribution of Gold Deposit Receipts. Holders of Gold Deposit Receipts may elect to redeem their Gold Deposit Receipts for Gold Bullion or exchange their Gold Deposit Receipts for cash either through an Authorized Participant or through an approved registered broker-dealer or similar entity that is not an Authorized Participant.

The Depositary Trust Agreement

General. The Depositary Trust Agreement provides that the Gold Deposit Receipts represent the owner’s undivided beneficial ownership interest in the Trust assets.

The Trustee. The Bank of New York Mellon serves as Trustee. The Bank of New York Mellon, which was founded in 1784, was New York’s first bank and is the oldest bank in the country still operating under its original name. The Bank of New York Mellon is organized under the law of the State of New York authorized to conduct a banking business and a member of the Federal Reserve System. The Bank of New York Mellon conducts a national and international wholesale banking business and a retail banking business in the New York City, New Jersey and Connecticut areas, and provides a comprehensive range of corporate and personal trust, securities processing and investment services.

3

Termination of the Trust. The Trust will terminate if: (i) the Trustee resigns and no successor trustee is appointed by Bank of Montreal, as Initial Depositor, within 60 days from the date the Trustee provides notice to Bank of Montreal, as Initial Depositor, and BMO Capital Markets Corp., as Underwriter, of its intent to resign; (ii) the owners of 75 percent of the outstanding Gold Deposit Receipts (other than those held by Bank of Montreal for its own account) acting through an Authorized Participant vote to dissolve and liquidate the Trust; (iii) an event of liquidation or dissolution occurs as to Bank of Montreal; (iv) Bank of Montreal ceases to store Gold Bullion at the Mint and does not make alternative arrangements that it deems appropriate; or (v) if the Trust fails to qualify for treatment, or ceases to be treated, for U.S. federal income tax purposes, as a grantor trust.

If a termination event occurs, the beneficial owners of Gold Deposit Receipts will surrender their Gold Deposit Receipts as provided in the Depositary Trust Agreement, including payment of any fees of the trustee or applicable taxes or governmental charges due. The Initial Depositor will sell the Gold Bullion and the Trustee will deliver to you the resulting proceeds as promptly as practicable after the termination event occurs.

Amendment of the Depositary Trust Agreement. The Trustee and Bank of Montreal, as Initial Depositor, may amend any provisions of the Depositary Trust Agreement without the consent of any of the owners of the Gold Deposit Receipts. Promptly after the execution of any amendment to the Depositary Trust Agreement, Bank of Montreal, as Initial Depositor, must furnish or cause to be furnished written notification of the substance of the amendment to each owner of Gold Deposit Receipts.

Any amendment that imposes or increases any fees or charges, subject to exceptions, or that otherwise prejudices any substantial existing right of the owners of Gold Deposit Receipts will not become effective until 30 days after notice of the amendment is given to the owners of Gold Deposit Receipts.

Listing. The Gold Deposit Receipts are not listed or traded on any securities exchange.

Trustee Fees. The fees of The Bank of New York Mellon are borne by Bank of Montreal.

Address of the Trustee. The Bank of New York Mellon, Corporate Trust Department, 101 Barclay Street, Floor 7 East, New York, New York 10286.

Gold Bullion

About the Gold Bullion. Subject to the terms of the Gold Storage Agreement, Bank of Montreal, in its sole and absolute discretion, will determine whether the Gold Bullion holdings in its account with the Mint are in coin, bar, wafer, or ingot form. For purposes of this annual report, “allocated” means that the Gold Bullion is segregated and identifiable from all other metal held at the Mint and segregated from Bank of Montreal’s assets. Title to the Gold Bullion is unencumbered and secure in Bank of Montreal’s custody account. The Gold Bullion will be purchased on a daily basis on behalf of holders, and will be allocated to the Trust and held in Bank of Montreal’s account at the Mint.

Specifications of the Gold Bullion. All Gold Bullion will be unencumbered, allocated, and physical with a minimum fineness of 995 parts per 1000.

If the Gold Bullion is in coin form, each coin will also: (i) have been produced by the Mint and be legal tender in Canada for its denomination; and (ii) have a fair market value not exceeding 110 percent of the fair market value of the coin’s gold content.

If the Gold Bullion is in bar, wafer, or ingot form, the Gold Bullion will also (i) have been fabricated by a metal refiner included in the London Bullion Market Association’s (the “LBMA”) good delivery list of acceptable refiners for gold; and (ii) bear basic identification markings that are recognized and accepted for trading in Canadian financial markets, including the hallmark of the metal refiner that produced it and a stamp indicating its fineness and weight, and no other markings.

4

In its account at the Mint, Bank of Montreal will not use or hold unallocated gold, gold certificates, exchange-traded products, derivatives, financial instruments, or any product that represents encumbered gold. Bank of Montreal and its affiliates will not lend, pledge, hypothecate or otherwise encumber any of the Gold Bullion.

Ownership of Gold Bullion. The Gold Bullion purchased on behalf of holders is held at the Mint in Bank of Montreal’s account for the benefit of the holders. Consequently under Canadian federal law, the Gold Bullion held by the Trust would not be available to meet the claims of creditors of Bank of Montreal in the event of any bankruptcy, insolvency or similar event involving Bank of Montreal.

Emerging Growth Company Status

The Trust is an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). For as long as the Trust is an “emerging growth company,” the Trust may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in the Trust’s periodic reports, and exemptions from the requirements of holding advisory “say-on-pay” votes on executive compensation and shareholder advisory votes on golden parachute compensation.

Under the JOBS Act, the Trust will remain an “emerging growth company” until the earliest of:

| · |

the last day of the fiscal year during which the Trust has total annual gross revenues of $1.07 billion or more;

|

| · |

October 31, 2021, which is the last day of the Trust’s fiscal year following the fifth anniversary after the Trust’s initial public offering of Gold Deposit Receipts;

|

| · |

the date on which the Trust has, during the previous three-year period, issued more than $1 billion in non-convertible debt; and

|

| · |

the date on which the Trust is deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) (the Trust will qualify as a large accelerated filer as of the first day of the first fiscal year after the Trust has (i) more than $700 million in outstanding equity held by non-affiliates and (ii) been public for at least 12 months; the value of its outstanding equity will be measured each year on the last day of its second fiscal quarter).

|

The JOBS Act also provides that an “emerging growth company” can utilize the extended transition period provided in Section 7(a) (2)(B) of the Securities Act of 1933, as amended for complying with new or revised accounting standards.

However, the Trust has chosen to “opt out” of such extended transition period, and, as a result, the Trust will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for companies that are not “emerging growth companies.” Section 107 of the JOBS Act provides that the Trust’s decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

| Item 1A. |

Risk Factors

|

Bank of Montreal has a limited history of operating investment vehicles similar to the Trust. Its experience may be inadequate or unsuitable to manage the Trust.

Bank of Montreal has a limited history of operating investment vehicles like the Trust. Bank of Montreal’s performance in connection with sponsoring or managing other investment vehicles is not indicative of its ability to sponsor the Trust.

The value of the Gold Deposit Receipts relates directly to the value of the Gold Bullion held by the Trust and fluctuations in the price of gold could materially adversely affect an investment in the Gold Deposit Receipts.

The Gold Deposit Receipts are designed to mirror as closely as possible the performance of the price of gold, and the value of the Gold Deposit Receipts relates directly to the value of the Gold Bullion held by the Trust. The price of gold has fluctuated widely over the past several years.

5

Several factors may affect the price of gold, including:

| · |

Global gold supply and demand, which is influenced by such factors as forward selling by gold producers, purchases made by gold producers to unwind gold hedge positions, central bank purchases and sales, and production and cost levels in major gold-producing countries such as South Africa, the United States and Australia;

|

| · |

Global or regional political, economic or financial events and situations;

|

| · |

Investors’ expectations with respect to the rate of inflation;

|

| · |

Currency exchange rates;

|

| · |

Interest rates; and

|

| · |

Investment and trading activities of hedge funds and commodity funds.

|

Throughout 2015, market participants reported a significant decrease in global demand for gold. In 2016, gold prices experienced notable volatility. If gold markets continue to be subject to sharp fluctuations, the price of the Gold Deposit Receipts may experience significant price fluctuation and this may result in losses if you need to sell your Gold Deposit Receipts at a time when the price of gold is lower than it was when you made your investment. Even if you are able to hold Gold Deposit Receipts for the long term, you may never experience a profit, since gold markets have historically experienced extended periods of flat or declining prices, in addition to sharp fluctuations.

In addition, investors should be aware that there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. In the event that the price of gold declines, the Initial Depositor expects the value of an investment in the Gold Deposit Receipts to decline proportionately.

The value of Gold Bullion is not guaranteed, which may cause your investment in the Gold Deposit Receipts to be volatile.

An investment in Gold Bullion is speculative and may be subject to greater price volatility than other investments. Appreciation in the market price of gold is the sole manner in which you can realize gains. Past performance of the price of gold is not indicative of future performance. Bank of Montreal does not provide any guarantee as to the value of Gold Bullion, which may be affected by many international, economic, monetary and political factors, many of which are unpredictable.

Future governmental decisions may have significant impact on the price of Gold Bullion, which will impact the price of the Gold Deposit Receipts.

Generally, gold prices reflect the supply and demand of available Gold Bullion. Governmental decisions, such as the executive order issued by the President of the United States in 1933 requiring all persons in the United States to deliver Gold Bullion to the Federal Reserve or the abandonment of the gold standard by the United States in 1971, have been viewed as having a significant impact on the supply and demand of Gold Bullion and the price of Gold Bullion. Other more recent governmental actions have indirectly impacted the price of Gold Bullion, such as the United Kingdom’s referendum held on June 23, 2016 to leave the European Union (i.e., Brexit). Future governmental decisions, whether in the United States, Canada or other relevant jurisdictions, may, either directly or indirectly, have an impact on the price of Gold Bullion, and may result in a significant decrease or increase in the value of the Gold Bullion and the Gold Deposit Receipts.

Disruptions in trading may materially adversely affect the Gold Deposit Receipts.

Occasional disruptions in trading, including temporary distortions or other disruptions due to various factors, such as the lack of liquidity in markets, the participation of speculators and governmental regulation and intervention may result in a significant decrease or increase in the value of Gold Bullion, which will affect the Gold Deposit Receipts.

6

The Trust is a passive investment vehicle. This means that the value of the Gold Deposit Receipts may be adversely affected by Trust losses that, if the Trust had been actively managed, it might have been possible to avoid.

The Trustee does not actively manage the gold held by the Trust. This means that the Trustee does not sell gold at times when its price is high, or acquire gold at low prices in the expectation of future price increases. It also means that the Trustee does not make use of any of the hedging techniques available to professional gold investors to attempt to reduce the risks of losses resulting from price decreases. Any losses sustained by the Trust will adversely affect the value of the Gold Deposit Receipts.

Because the Trust holds solely Gold Bullion, an investment in the Trust may be more volatile than an investment in a more broadly diversified portfolio.

The Trust holds solely Gold Bullion for the benefit of the holders of the Gold Deposit Receipts. As a result, the Trust’s holdings are not diversified. Accordingly, the asset value of the Trust may be more volatile than another investment vehicle with a broadly diversified portfolio and may fluctuate substantially over time.

Crises may motivate large-scale sales of gold which could decrease the price of gold and adversely affect an investment in the Gold Deposit Receipts.

The possibility of large-scale distressed sales of gold in times of crisis may have a short-term negative impact on the price of gold and adversely affect an investment in the Gold Deposit Receipts. For example, the 1998 Asian financial crisis resulted in significant sales of gold by individuals, which depressed the price of gold. Crises in the future may impair gold’s price performance which would, in turn, adversely affect an investment in the Gold Deposit Receipts.

Purchasing activity in the gold market associated with the delivery of Gold Bullion to the Trust in exchange for Gold Deposit Receipts may cause a temporary increase in the price of gold. This increase may adversely affect an investment in the Gold Deposit Receipts.

Purchasing activity associated with acquiring the Gold Bullion that is transferred into the Trust in connection with the issuance of additional Gold Deposit Receipts may temporarily increase the market price of gold, which will result in higher prices for the Gold Deposit Receipts. Temporary increases in the market price of gold may also occur as a result of the purchasing activity of other market participants. Other market participants may attempt to benefit from an increase in the market price of gold that may result from increased purchasing activity of gold connected with the issuance of Gold Deposit Receipts. Consequently, the market price of gold may decline immediately after Gold Deposit Receipts are purchased. If the price of gold declines, the trading price of the Gold Deposit Receipts will also decline.

Holders of Gold Deposit Receipts do not have the protections associated with ownership of interests in an investment company registered under the 1940 Act or the protections afforded by the CEA.

The Trust is not registered as an investment company under the 1940 Act and is not required to register under such act. Consequently, holders of Gold Deposit Receipts do not have the regulatory protections provided to investors in investment companies. The Trust will not hold or trade commodity interests regulated by the CEA, as administered by the CFTC. Furthermore, the Trust is not a commodity pool for purposes of the CEA, and none of the Initial Depositor, the Trustee or the Authorized Participants is subject to regulation by the CFTC in any capacity, including as a commodity pool operator or a commodity trading advisor in connection with the Gold Deposit Receipts. Consequently, holders of Gold Deposit Receipts do not have the regulatory protections provided to investors in CEA-regulated instruments or commodity pools.

The Trust may be required to terminate and liquidate at a time that is disadvantageous to holders.

If the Trust is required to terminate and liquidate, such termination and liquidation could occur at a time which is disadvantageous to holders, such as when gold prices are lower than the gold prices at the time when holders purchased their Gold Deposit Receipts. In such a case, when the Trust’s Gold Bullion is sold as part of the Trust’s liquidation, the resulting proceeds distributed to holders will be less than if gold prices were higher at the time of sale.

7

The price of gold may be affected by the sale of gold by exchange-traded funds or other exchange-traded vehicles tracking gold markets.

To the extent existing exchange-traded funds, or ETFs, or other exchange-traded vehicles tracking gold markets represent a significant proportion of demand for Gold Bullion, large redemptions of the securities of these ETFs or other exchange-traded vehicles could negatively affect Gold Bullion prices and the price of the Gold Deposit Receipts.

An investment in the Gold Deposit Receipts may be adversely affected by competition from other methods of investing in gold.

The Trust competes with other financial vehicles, including traditional debt and equity securities issued by gold industry participants and direct investments in gold. Market and financial conditions, and other conditions beyond Bank of Montreal’s control, may make it more attractive to invest in other financial vehicles or to invest in gold directly, which could limit the market for the Gold Deposit Receipts and reduce the liquidity of the Gold Deposit Receipts.

The Trust may postpone, suspend or reject redemption requests in certain circumstances, which may limit the ability of a holder of Gold Deposit Receipts to obtain liquidity.

If notified by Bank of Montreal or BMO Capital Markets Corp. of any postponement, suspension or rejection of settlement, the trustee shall suspend the redemption right or postpone the settlement date for any redemption to have physical gold delivery for you. Any such postponement, suspension or rejection may affect a holder’s ability to obtain liquidity. Under the Depositary Trust Agreement, the Initial Depositor, the Trustee and the Underwriter have no liability for any loss or damage that may result from any such suspension or postponement. Physical delivery may be suspended generally, or refused with respect to particular requested deliveries only in the case of a force majeure event or market disruption event where the Initial Depositor is prevented for reasons outside of its control from delivering the Gold Bullion, and such suspension or refusal shall only last so long as the Initial Depositor continues to be so prevented from delivering the Gold Bullion.

Redemptions or repurchases of Gold Deposit Receipts by the Initial Depositor for Cash Delivery may be suspended at any time as a result of suspensions in the purchase of Gold Bullion by Bank of Montreal.

As a holder of Gold Deposit Receipts, you will only have the option to elect that Bank of Montreal repurchase the withdrawn Gold Bullion represented by your Gold Deposit Receipts for cash if Bank of Montreal is then effecting such purchases, but Bank of Montreal is under no obligation to do so. Accordingly, you should only purchase the Gold Deposit Receipts if you are prepared to maintain an ownership interest in the Gold Deposit Receipts for an indefinite period. Bank of Montreal does not have any obligation to the Trust or to any holder of Gold Deposit Receipts to repurchase Gold Bullion at any time.

In the event that a holder redeems Gold Deposit Receipts for cash or physical gold, an Authorized Participant or other approved broker-dealer that processes that transaction may charge additional fees.

Holders who redeem their Gold Deposit Receipts for cash or physical gold using the services of an Authorized Participant or other approved broker-dealer (for example, the holder’s broker) may be charged additional fees or commissions by that Authorized Participant or other approved broker-dealer. No additional fees (other than any applicable withdrawal and delivery fee in connection with the delivery of physical gold) will be charged by Bank of Montreal, the Trust or BMO Capital Markets Corp.

Physical delivery of Gold Bullion is not available in every state, and the states approved for delivery may change at any time.

Gold Bullion will be delivered only to addresses within the United States that are within a state specifically approved by the Underwriter for delivery. The Initial Depositor will maintain a list of states approved for delivery and provide the same to the Authorized Participants from time to time. The Initial Depositor has no obligation to deliver Gold Bullion to a state that is not approved for delivery, and there is no guarantee that delivery will remain available in any particular state. If an investor changes its address to a state that is not approved for delivery, delivery will no longer be available to that investor.

8

A request for sale or redemption is irrevocable.

In order to sell or redeem Gold Deposit Receipts for cash or physical gold, a holder must provide a notice to the Trust through an Authorized Participant or other approved broker-dealer. Except when sales or redemptions have been suspended, once a notice has been received, it can no longer be revoked by the holder under any circumstances, though it may be rejected by the Trust if it does not comply with the requirements for such notice.

The fees charged to holders for redemption of their Gold Deposit Receipts may change.

If you choose to redeem your Gold Deposit Receipts for physical gold, you will be responsible for payment of certain fees and expenses. The fees and expenses may be increased or decreased by Bank of Montreal in its sole and absolute discretion.

Holders do not have the rights enjoyed by investors in certain other vehicles.

As interests in the Gold Bullion held by the Trust, the Gold Deposit Receipts have none of the statutory rights normally associated with the ownership of shares of a corporation (including, for example, the right to bring “derivative” actions). In addition, the Gold Deposit Receipts have limited voting and distribution rights (for example, holders do not have the right to elect directors and will not receive dividends).

Each of the parties to the offering of Gold Deposit Receipts maintains several roles, which may present certain conflicts of interest.

Bank of Montreal is the Initial Depositor of the Trust and holds Gold Bullion that it will transfer to the Trust from time to time in connection with the sale by the Trust of the Gold Deposit Receipts. The price at which Gold Deposit Receipts will be sold to the public will equal the price at which Gold Bullion is transferred to the Trust by Bank of Montreal. Transactions in the Gold Deposit Receipts will be executed promptly by BMO Capital Markets Corp. and Bank of Montreal. Bank of Montreal may earn revenues (or suffer losses) from the sale of Gold Bullion to the Trust. As discussed above, under “Purchasing activity in the gold market associated with the delivery of Gold Bullion to the Trust in exchange for Gold Deposit Receipts may cause a temporary increase in the price of gold. This increase may adversely affect an investment in the Gold Deposit Receipts,” activity in the gold market may affect the price of Gold Deposit Receipts. In addition to acting as the Initial Depositor, Bank of Montreal also will redeem the Gold Deposit Receipts for Gold Bullion and purchase the Gold Deposit Receipts for cash. Furthermore, BMO Capital Markets Corp. functions as the Underwriter of the continuous offerings of Gold Deposit Receipts and as the calculation agent responsible for calculating the spot price of gold, using the spot price of gold reflected on EBS as the source for the spot price of gold, without adjustment or modification. Each party will play various roles, which may give rise to certain conflicts of interest of which you should be aware.

Substantial sales of gold by the official sector could adversely affect an investment in the Gold Deposit Receipts.

The official sector consists of central banks, other governmental agencies and multi-lateral institutions that buy, sell and hold gold as part of their reserve assets. The official sector holds a significant amount of gold, most of which is static, meaning that it is held in vaults and is not bought, sold, leased or swapped or otherwise mobilized in the open market. A number of central banks have sold portions of their gold over the past ten years, with the result that the official sector, taken as a whole, has been a net supplier to the open market. Since 1999, most sales have been made in a coordinated manner under the terms of the Central Bank Gold Agreement under which 15 of the world’s major central banks agree to limit the level of their gold sales and lending to the market. In the event that future economic, political or social conditions or pressures require members of the official sector to liquidate their gold assets all at once or in an uncoordinated manner, the demand for gold might not be sufficient to accommodate the sudden increase in the supply of gold to the market. Consequently, the price of gold could decline significantly, which would adversely affect an investment in the Gold Deposit Receipts.

The Trust does not insure its assets and there may not be adequate sources of recovery if its Gold Bullion is lost, damaged, stolen or destroyed.

The Trust does not insure its assets, including the Gold Bullion stored at the Mint. Consequently, if there is a loss of assets of the Trust through theft, destruction, fraud or otherwise, the Trust and holders will need to rely on insurance carried by applicable third parties, if any, or on such third party’s ability to satisfy any claims against it. The amount of insurance available or the financial resources of a responsible third party may not be sufficient to satisfy the Trust’s claim against such party. Also, holders of Gold Deposit Receipts are unlikely to have any right to assert a claim directly against such third party; such claims may only be asserted by the Trustee on behalf of the Trust. In addition, if a loss is covered by insurance carried by a third party, the Trust, which is not a beneficiary on such insurance, may have to rely on the efforts of the third party to recover its loss. This may delay or hinder the Trust’s ability to recover its loss in a timely manner or otherwise.

9

A loss with respect to the Trust’s Gold Bullion that is not covered by insurance and for which compensatory damages cannot be recovered would have a negative impact on the Gold Deposit Receipts and would adversely affect an investment in the Gold Deposit Receipts. In addition, any event of loss may adversely affect the operations of the Trust and, consequently, an investment in the Gold Deposit Receipts.

A redeeming holder of the Gold Deposit Receipt that suffers loss of, or damage to, its Gold Bullion during delivery will not be able to claim damages from the Service Carrier, Bank of Montreal, the Trust or the storage provider.

If a holder exercises its option to redeem Gold Deposit Receipts for Gold Bullion, the holder’s Gold Bullion will be transported by a third-party service carrier (“Service Carrier”). Because ownership of Gold Bullion will transfer to such holder at the time Bank of Montreal surrenders the Gold Bullion to the Service Carrier, the redeeming holder will bear the risk of loss from the moment the Service Carrier takes possession of the Gold Bullion on behalf of such holder. Under the terms of the Gold Carrier Agreement, in the event of any loss or damage in connection with the delivery of the Gold Bullion, such holder will not be able to claim damages from the Service Carrier, nor will such holder be able to claim damages from Bank of Montreal, the Trust or the Mint.

Bank of Montreal, the Mint and service providers engaged by the Trust may not carry adequate insurance to cover claims against them by the Trust.

Holders cannot be assured that Bank of Montreal, the Mint or service providers engaged by the Trust will maintain insurance with respect to the Trust’s assets or the services that such parties provide to the Trust and, if they maintain insurance, that such insurance is sufficient to satisfy any losses incurred by them in respect of their relationship with the Trust. The Mint, to the extent it incurs any liability, will be liable only to Bank of Montreal directly in the event of loss, damage or destruction of the Trust’s Gold Bullion. In addition, none of the Trust’s service providers are required to include the Trust as a named beneficiary of any such insurance policies that are purchased. Accordingly, the Trust will have to rely on the efforts of the service provider to recover from their insurer compensation for any losses incurred by the Trust in connection with such arrangements.

If there is a loss, damage or destruction of the Trust’s Gold Bullion in the custody of the Mint and Bank of Montreal does not give timely notice, all claims against the Mint will be deemed waived.

In the event of loss, damage or destruction of the Trust’s Gold Bullion in the Mint’s custody, care and control, Bank of Montreal must give written notice to the Mint within five Mint business days (a Mint business day means any day other than a Saturday, Sunday or a holiday observed by the Mint) after the discovery by Bank of Montreal of any such loss, damage or destruction, but in any event no more than 30 days after the delivery by the Mint to Bank of Montreal of an inventory statement in which the discrepancy first appears. If such notice is not given in a timely manner, all claims against the Mint will be deemed to have been waived. In addition, no action, suit or other proceeding to recover any loss or shortage can be brought against the Mint unless timely notice of such loss or shortage has been given and such action, suit or proceeding will have commenced within 12 months from the time a claim is made. The loss of the right to make a claim or of the ability to bring an action, suit or other proceeding against the Mint may mean that any such loss will be non-recoverable, which will have an adverse effect on the value of the net assets of the Trust.

The Trustee and Trust shall have no responsibility or liability for actions taken by the Initial Depositor or the Mint.

Pursuant to the terms of the Depositary Trust Agreement, neither the Trustee nor the Trust can be held responsible, or liable, for any misconduct, bad faith or negligence of the Initial Depositor or the Mint.

The Trust is exposed to various operational risks.

The Trust is exposed to various operational risks, including information technology failures, human error and failures to comply with procedures intended to mitigate such risks.

10

Under Canadian law, the Trust may have limited recourse against the Mint.

The Mint is a Canadian Crown corporation. A Canadian Crown corporation may be sued for breach of contract or for wrongdoing in tort where it has acted on its own behalf or on behalf of the Crown. However, a Canadian Crown corporation may be entitled to immunity if it acts as agent of the Crown rather than in its own right and on its own behalf. The Mint has entered into the Gold Storage Agreement between Bank of Montreal and the Mint relating to the custody of the Gold Bullion in Bank of Montreal’s account for the Trust. The Mint has entered into this agreement on its own behalf and not on behalf of the Crown; nevertheless, a court may determine that, when acting as custodian of the Trust’s Gold Bullion, the Mint acted as agent of the Crown and, accordingly, that the Mint may be entitled to immunity of the Crown.

Consequently, the Trust or a holder of Gold Deposit Receipts may not be able to recover for any losses incurred as a result of the Mint’s acting as custodian of the Gold Bullion.

The Mint may become a private enterprise, in which case its obligations will not constitute the unconditional obligations of the Government of Canada.

In the past, there has been speculation regarding whether the Government of Canada might privatize the Mint. The Mint will not remain a Canadian Crown corporation if the Government of Canada privatizes the Mint. If the Mint were to become a private entity, its obligations would no longer generally constitute unconditional obligations of the Government of Canada and, although it would continue to be responsible for and bear the risk of loss of, and damage to, the Trust’s Gold Bullion that is in its custody, there would be no assurance that the Mint would have the resources to satisfy claims of the Trust against the Mint based on a loss of, or damage to, the Trust’s Gold Bullion in the custody of the Mint.

An investment in Gold Bullion may not be appropriate for all investors.

You should decide to buy the Gold Deposit Receipts, which constitute an investment in Gold Bullion, only after carefully considering with your investment or financial advisor whether Gold Bullion is a suitable investment in light of the information contained in this annual report having regard to your financial or investment objectives and expectations.

Changes in laws or regulations may affect the Gold Deposit Receipts and the Gold Bullion.

The promulgation of new laws or regulations or by the reinterpretation of existing laws or regulations (including, without limitation, those relating to taxes and duties on commodities or commodity components) by one or more governments, governmental agencies or instrumentalities, courts, or other official bodies may result in a significant decrease or increase in the value of the Gold Deposit Receipts and the Gold Bullion. The United States or foreign governments may pass laws or regulations limiting metal investments for strategic or other policy reasons.

Potential risks could arise with respect to the Trust and the holders of Gold Deposit Receipts from an insolvency event relating to Bank of Montreal.

The Gold Deposit Receipts represent interests in Gold Bullion held by the Trust. The Gold Bullion is held by the Trust on behalf of purchasers and held at an account of Bank of Montreal with the Mint. The Gold Bullion is not, and will not, be owned by Bank of Montreal. Consequently, under Canadian federal law, the Gold Bullion would not be available to meet the claims of creditors of Bank of Montreal in the event of any bankruptcy, insolvency or similar event involving Bank of Montreal. However, any such event could lead to delays in restoring the ability of holders of Gold Deposit Receipts to transact in such Gold Bullion, depending upon the outcome of any relevant bankruptcy or related proceedings.

Transactions through an Authorized Participant or other approved broker-dealer are subject to risks related to that Authorized Participant or broker-dealer.

All transactions in the Gold Deposit Receipts will take place through an Authorized Participant or other approved broker-dealer, and you assume the risks of the Authorized Participant’s or broker-dealer’s failure to fulfill its obligations to you.

11

The Gold Deposit Receipts are not subject to deposit insurance.

The Gold Deposit Receipts are not securities of The Bank of New York Mellon, BNY Mellon Trust of Delaware, Bank of Montreal or any other bank, and do not constitute deposits that are insured under the U.S. Federal Deposit Insurance Act, the Canada Deposit Insurance Corporation Act or any other deposit insurance regime.

There is no assurance that your investment in the Gold Deposit Receipts will be subject to protection by the Securities Investor Protection Corporation.

In the case of the failure of a brokerage firm that is a member of the Securities Investor Protection Corporation (the “SIPC”), the SIPC would protect customers against the loss of cash and securities. The SIPC does not protect commodity or related futures contracts or investment contracts. The Gold Deposit Receipts are not commodity futures or investment contracts. In the opinion of Morrison & Foerster LLP, the Gold Deposit Receipts should be viewed as securities for which SIPC protection should be available. However, given that the Gold Deposit Receipts are novel instruments, there can be no assurance that the SIPC or a court having jurisdiction on this matter would concur with this legal conclusion.

The Trust is an “emerging growth company” and it cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make the Gold Deposit Receipts less attractive to investors.

The Trust is an “emerging growth company” as defined in the JOBS Act. For as long as the Trust continues to be an emerging growth company it may choose to take advantage of certain exemptions from various reporting requirements applicable to other public companies but not to emerging public companies, which include, among other things:

| · |

exemption from the auditor attestation requirements under Section 404 of the Sarbanes-Oxley Act;

|

| · |

reduced disclosure obligations regarding executive compensation in the Trust’s periodic reports;

|

| · |

exemption from the requirements of holding non-binding stockholder votes on executive compensation arrangements; and

|

| · |

exemption from any rules requiring mandatory audit firm rotation and auditor discussion and analysis and, unless the SEC otherwise determines, any future audit rules that may be adopted by the Public Company Accounting Oversight Board.

|

The Trust could be an emerging growth company until October 31, 2021, the last day of the Trust’s fiscal year following the fifth anniversary after its initial public offering, or until the earliest of: (i) the last day of the fiscal year in which it has annual gross revenue of $1.07 billion or more; (ii) the date on which it has, during the previous three year period, issued more than $1 billion in non-convertible debt; or (iii) the date on which it is deemed to be a large accelerated filer under the federal securities laws.

The Trust will qualify as a large accelerated filer as of the first day of the first fiscal year after it has (i) more than $700 million in outstanding equity held by non-affiliates and (ii) been public for at least 12 months. The value of the Trust’s outstanding equity will be measured each year on the last day of its second fiscal quarter.

Under the JOBS Act, emerging growth companies are also permitted to elect to delay adoption of new or revised accounting standards until companies that are not subject to periodic reporting obligations are required to comply, if such accounting standards apply to non-reporting companies. The Trust has made an irrevocable decision to opt out of this extended transition period for complying with new or revised accounting standards.

The Trust cannot predict if investors will find an investment in the Trust less attractive if it relies on these exemptions.

| Item 2. |

Properties

|

The property of the Trust consists of the Gold Bullion and all monies or other property, if any, received by the Trustee.

12

| Item 3. |

Legal Proceedings

|

None.

| Item 4. |

Mine Safety Disclosures

|

Not applicable.

PART II

| Item 5. |

Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

|

None.

| Item 6. |

Selected Financial Data

|

Not applicable.

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

Overview

The Trust holds Gold Bullion for the benefit of owners of Gold Deposit Receipts. One receipt represents the undivided beneficial ownership of one troy ounce of Gold Bullion. The Trustee performs only administrative and ministerial acts. The property of the Trust consists of the Gold Bullion and all monies or other property, if any, received by the Trustee. The Initial Depositor sells Gold Bullion to the Trust and arranges custodial services through its gold storage account. The Trust commenced operations during the period covered by this annual report, and as of October 31, 2017, there were 29,656 Gold Deposit Receipts outstanding.

The Trust is not managed like a corporation or an active investment vehicle. It does not have any officers, directors, or employees and is administered by the Trustee pursuant to the Depositary Trust Agreement. The expenses of the Trust are borne by the Initial Depositor.

The fiscal year end for the Trust is October 31.

Gold Industry

The participants in the gold industry may be classified in the following sectors: (1) mining and producer; (2) banking; (3) official; (4) investment; and (5) manufacturing. The following is a brief description of each of the sectors.

Mining and Producer Sector. This group includes mining companies that specialize in gold and silver production; mining companies that produce gold as a byproduct of other production (such as a copper or silver producer); scrap merchants; and recyclers.

Banking Sector. Bullion banks provide a variety of services to the gold industry and its participants, thereby facilitating interactions between other parties. Services provided by the bullion banking community include traditional banking products as well as mine financing, physical gold purchases and sales, hedging and risk management, inventory management for industrial users and consumers, and gold deposit and loan instruments.

The Official Sector. The official sector encompasses the activities of the various central banking operations of gold-holding countries. In September 1999, a group of 15 central banks acting to clarify their intentions with respect to their gold holdings signed the Central Bank Gold Agreement commonly called the “Washington Agreement on Gold.” The signatories included the European Central Bank (the “ECB”) and the central banks of Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden, Switzerland, and England. The original agreement limited incremental sales by the 15 signatories to 400 tonnes per annum over the ensuing five-year period. The original Washington Agreement on Gold expired in September 2004, and was renewed by almost all of the original signatories for a second five-year period (England did not renew in 2004). The second Washington Accord Agreement expired in September 2009 and was renewed again by all signatories of the second agreement for a third agreement to last another five-year period. In addition, the central banks of Cyprus, Greece, Malta, Slovakia and Slovenia signed in 2009. The annum limit on gold sales under the third agreement was 400 tonnes, with total sales not to exceed 2,000 tonnes in the five-year period. In May 2014, before the third agreement was set to expire in September 2014, a fourth agreement was reached between the ECB and the central banks of Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia, Spain, Sweden and Switzerland, which will expire after a five-year period. The signatories have agreed to, among other things, continue to coordinate their gold transactions to avoid disturbances to the gold market and have acknowledged that they each do not have plans to sell significant amounts of gold.

13

The Investment Sector. This sector includes the investment and trading activities of both professional and private investors and speculators. These participants range from large hedge and mutual funds to day-traders on futures exchanges and retail-level coin collectors.

The Manufacturing Sector. The fabrication and manufacturing sector represents all the commercial and industrial users of gold for whom gold is a daily part of their business. The jewelry industry is a large user of gold. Other industrial users of gold include the electronics and dental industries.

World Gold Supply and Demand (2007-2017)

The following table sets forth a summary of the world gold supply and demand from 2007-2017:

|

WORLD GOLD SUPPLY AND DEMAND†

(tonnes)

|

2007

|

2008

|

2009

|

2010

|

2011

|

2012

|

2013

|

2014

|

2015

|

2016

|

2017

(Q3) * |

|

Supply

|

|||||||||||

|

Mine Production

|

2,538

|

2,467

|

2,651

|

2,775

|

2,868

|

2,883

|

3,077

|

3,172

|

3,209

|

3,222

|

841

|

|

Scrap

|

1,029

|

1,388

|

1,765

|

1,743

|

1,704

|

1,700

|

1,303

|

1,158

|

1,172

|

1,268

|

308

|

|

Net Hedging Supply

|

-432

|

-357

|

-234

|

-106

|

18

|

-40

|

-39

|

108

|

21

|

21

|

8

|

|

Total Supply

|

3,134

|

3,497

|

4,182

|

4,411

|

4,590

|

4,544

|

4,341

|

4,438

|

4,401

|

4,511

|

1,157

|

|

Demand

|

|||||||||||

|

Jewelry

|

2,474

|

2,355

|

1,866

|

2,083

|

2,091

|

2,061

|

2,610

|

2,469

|

2,395

|

1,891

|

527

|

|

Industrial Fabrication

|

492

|

479

|

426

|

480

|

471

|

429

|

421

|

403

|

365

|

354

|

92

|

|

…of which Electronics

|

345

|

334

|

295

|

346

|

343

|

307

|

300

|

290

|

258

|

254

|

66

|

|

…of which Dental & Medical

|

58

|

56

|

53

|

48

|

43

|

39

|

36

|

34

|

32

|

30

|

8

|

|

…of which Other Industrial

|

89

|

89

|

79

|

86

|

85

|

83

|

85

|

79

|

76

|

70

|

18

|

|

Net Official Sector

|

-484

|

-235

|

-34

|

77

|

457

|

544

|

409

|

466

|

436

|

257

|

71

|

|

Retail Investment

|

448

|

937

|

866

|

1,263

|

1,616

|

1,407

|

1,873

|

1,163

|

1,162

|

1,057

|

210

|

|

…of which Bars

|

238

|

667

|

562

|

946

|

1,247

|

1,056

|

1,444

|

886

|

876

|

787

|

157

|

|

…of which Coins

|

211

|

270

|

304

|

317

|

369

|

351

|

429

|

278

|

286

|

271

|

54

|

|

Physical Demand

|

2,930

|

3,536

|

3,125

|

3,903

|

4,635

|

4,441

|

5,314

|

4,501

|

4,357

|

3,559

|

900

|

|

Physical Surplus/Deficit

|

204

|

-38

|

1,057

|

508

|

-45

|

102

|

-973

|

-62

|

44

|

952

|

257

|

|

ETF Inventory Build

|

253

|

321

|

623

|

382

|

185

|

279

|

-880

|

-155

|

-125

|

524

|

30

|

|

Exchange Inventory Build

|

-10

|

34

|

39

|

54

|

-6

|

-10

|

-98

|

1

|

-48

|

86

|

-4

|

|

Net Balance

|

-39

|

-394

|

394

|

73

|

-224

|

-167

|

5

|

92

|

217

|

342

|

230

|

|

Gold Price (London PM, US$/oz)

|

695.39

|

871.96

|

972.35

|

1,224.52

|

1,571.69

|

1,668.98

|

1,411.23

|

1,266.40

|

1,160.06

|

1,250.80

|

1,277.90

|

| Note: |

Totals may not add due to independent rounding. Net producer hedging is the change in the physical market impact of mining companies’ gold loans, forwards and options positions. Implied net investment is the residual from combining all other Thomson Reuters GFMS data on the gold supply/demand as shown in the Summary Table. As such, it captures the net physical impact of all transactions not covered by the other supply/demand variables.

|

| (1) |

“Tonne” refers to one metric ton. This is equal to 1,000 kilograms or 32,150.7465 troy ounces.

|

† Source: Gold Survey 2017, Thomson Reuters GFMS

* Source: Gold Survey 2017: Q3 Update & Outlook, Thomson Reuters GFMS

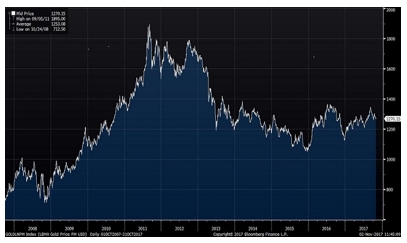

Historic Movements in the Price of Gold

As movements in the price of gold are expected to directly affect the price of the Gold Deposit Receipts, investors should understand what the recent movements in the price of gold have been. Investors, however, should also be aware that past movements in the gold price are not indicators of future movements.

14

The following chart provides historical background on the price of gold. The chart illustrates movements in the price of gold in U.S. dollars per ounce over the period from October 2007 to October 2017, and is based on the LBMA (PM) Gold Price, an offering of ICE Benchmark Administration.

Source: Bloomberg (accessed Oct. 2017)

After a rapid rise starting in the second half of 2005 through mid-2006, there was a period of short decline and volatility in the price of gold lasting through the end of that year. In May 2006, the peak was $725 per ounce. Until about August of 2007, prices were below that high, but since have moved up strongly, reaching a new high of $1,011.25 on March 17, 2008, and ending at $869.75 per ounce on December 30, 2008. Gold prices were quite volatile between the March 2008 high and the end of December 2008 with run-ups and falls of over $150 in each direction. The significant price movements reflect the battles between inflationary and deflationary pressures, U.S. Dollar strengthening against many major currencies and global economic uncertainty going into 2009.

The price of gold continued its upward trend in 2009. After rallying to $1,212.50 per ounce in early December 2009, it fell back down to $1,087.50 per ounce to close the year following the collapse of Lehman Brothers. This still resulted in a gain of over 25 percent for 2009. Upward price movement for gold price continued in 2010, reaching a new pre-inflation adjusted record high of $1,421.00 per ounce on November 9, 2010 and closing at $1,405.50 per ounce on December 30, 2010. In August 2011, the price of gold experienced a notable increase partially due to the first U.S. downgrade by Standard & Poor’s, reaching a high of $1895.00 per ounce on September 5, 2011. By December 29, 2011, the price of gold had fallen to $1,531.00 per ounce. The annual average price of gold in 2012 was 6.2 percent higher than 2011, reaching a high of $1,791.75 on October 4, 2012. In particular, uncertainty over U.S. monetary policy became an increasingly significant driver of market appetite towards the end of 2012, and on December 28, 2012, the price of gold had fallen slightly to $1,657.50 per ounce.

In 2013, the twelve-year bull run of gold ended. 2013 opened near the annual high, and the price declined approximately 29 percent over the year to $1,204.50 per ounce on December 30, 2013. For 2013, the price of gold was impacted, in part, by improving sentiment towards the U.S. economy, which contributed to a strengthening of the U.S. dollar and equities, luring investors away from gold in the process. During 2014, the underlying driver behind investor sentiment of gold was global monetary policy. On one end, the improving economic conditions in the United States (along with the announcement of the Federal Reserve Board’s tapering measures at the end of 2013) diminished demand for gold for U.S. investors, while loosening of monetary policy in other advanced and emerging markets enhanced demand for gold globally, causing gold prices to fluctuate between a low of $1,132.00 and a high of $1,392.00 per ounce. Gold prices deteriorated throughout 2015, in part as a result of the Federal Reserve Board’s announcement that it would raise interest rates as well as a significant rally of the U.S. dollar index, falling to $1,060.00 per ounce on December 30, 2015. However, the price of gold rebounded during the first half of 2016. In July 2016, gold prices experienced a rapid increase following the United Kingdom’s referendum held on June 23, 2016 to leave the European Union (i.e., “Brexit”), reaching a 28-month high of $1,366.25 per ounce on July 6, 2016. The initial market volatility and negative sentiment in connection with Brexit has somewhat subsided and gold prices have receded from the high prices displayed during July 2016, leveling off at prices similarly exhibited during the beginning of 2016.

As of January 25, 2018, the price of gold was $1,354.95 per ounce.

15

Liquidity and Capital Resources

The Trust is not aware of any trends, demands, commitments, events or uncertainties that are reasonably likely to result in material changes to its liquidity needs. In exchange for the Initial Depositor’s fee, the Initial Depositor has agreed to assume the expenses incurred by the Trust.

Off-Balance Sheet Arrangements

The Trust has no off-balance sheet arrangements.

Critical Accounting Policies

The Trust prepares its financial statements in accordance with accounting principles generally accepted in the United States of America.

The Trust has adopted the provisions of Topic 946, Investment Companies, and follows specialized accounting. As a result of the adoption of this provision, the Trust records its investment in gold at fair value and expects that there will be fluctuations in the value of investments based on changes in the price of gold.

| Item 7A. |

Quantitative and Qualitative Disclosures About Market Risk

|

The Trust does not engage in transactions in foreign currencies which could expose the Trust or holders of Gold Deposit Receipts to any foreign currency related market risk. The Trust does not invest in any derivative financial instruments or long-term debt instruments.

| Item 8. |

Financial Statements and Supplementary Data

|

Index to Financial Statements

|

Report of Independent Registered Public Accounting Firm

|

F-1

|

|

Statements of Assets and Liabilities

|

F-2

|

|

Schedules of Investments

|

F-3

|

|

Statements of Operations

|

F-4

|

|

Statements of Changes in Net Assets

|

F-5

|

|

Notes to the Financial Statements

|

F-6

|

16

Report of Independent Registered Public Accounting Firm

To Bank of Montreal, Bank of New York Mellon and Receipt Holders of the

Vaulted Gold Bullion Trust:

Vaulted Gold Bullion Trust:

We have audited the accompanying statements of assets and liabilities of the Vaulted Gold Bullion Trust (the “Trust”), including the schedules of investments as of October 31, 2017 and 2016, the related statements of operations and changes in net assets for the year ended October 31, 2017 and the period from August 5, 2016 (commencement of operations) through October 31, 2016. These financial statements are the responsibility of the Trust’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statements presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Trust as of October 31, 2017 and 2016, and the results of its operations and changes in its net assets for the year ended October 31, 2017 and the period from August 5, 2016 through October 31, 2016, in conformity with U.S. generally accepted accounting principles.

/s/ KPMG LLP

New York, New York

January 26, 2018

January 26, 2018

F-1

VAULTED GOLD BULLION TRUST

Financial Statements

Statements of Assets and Liabilities

|

(Amounts in US$, except for Receipt data)

|

As of October

31, 2017 |

As of October

31, 2016 |

||||||

|

ASSETS

|

||||||||

|

Investment in gold (Cost: $36,067,530 and $48,347,

respectively) (see Notes 2.2, 2.5) |

$

|

37,667,568

|

$

|

48,336

|

||||

|

Total assets

|

37,667,568

|

48,336

|

||||||

|

Paid In Capital

|

$

|

36,067,530

|

$

|

27,995

|

||||

|

Receipts Issuable

|

-

|

20,352

|

||||||

|

Unrealized gain (loss) on investment in gold

|

1,600,038

|

(11

|

)

|

|||||

|

NET ASSETS

|

37,667,568

|

48,336

|

||||||

|

Receipts issued, issuable and outstanding

|

29,656

|

38

|

||||||

|

Net Asset Value per Receipt

|

$

|

1,270.15

|

$

|

1,272.00

|

||||