Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - Voyager Therapeutics, Inc. | vygr-20170930ex3217e18eb.htm |

| EX-31.2 - EX-31.2 - Voyager Therapeutics, Inc. | vygr-20170930ex31293915d.htm |

| EX-31.1 - EX-31.1 - Voyager Therapeutics, Inc. | vygr-20170930ex311002dfe.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the quarterly period ended September 30, 2017.

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the transition period from ______ to ______

Commission file number: 001-37625

Voyager Therapeutics, Inc.

(Exact name of Registrant as specified in its charter)

|

Delaware |

|

46-3003182 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

|

|

|

|

75 Sidney Street, |

|

02139 |

|

(Address of principal executive offices) |

|

(Zip Code) |

(857) 259-5340

(Registrant’s telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☒ |

|||||

|

Non-accelerated filer |

☐ |

(Do not check if a smaller reporting company) |

Smaller reporting company |

☐ |

|||||

|

|

|

|

Emerging growth company |

☒ |

|||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of outstanding shares of the registrant’s common stock, par value $0.001 per share, as of October 30, 2017 was 26,949,523.

Forward-Looking Statements

This Quarterly Report on Form 10-Q contains forward-looking statements that involve substantial risks and uncertainties. All statements other than statements of historical facts contained in this Quarterly Report on Form 10-Q, including statements regarding our strategy, future operations, future financial position, future revenue, projected costs, prospects, plans, objectives of management and expected market growth, are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

The words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “predict,” “project,” “target,” “potential,” “goals,” “will,” “would,” “could,” “should,” “continue,” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. These forward-looking statements include, among other things, statements about:

|

· |

our plans to develop and commercialize our product candidates based on adeno-associated virus, or AAV, gene therapy; |

|

· |

our ability to identify and optimize product candidates and novel AAV gene therapy capsids; |

|

· |

our ongoing and planned clinical trials, including our ability to continue to advance VY-AADC through the current Phase 1b clinical trial and into a planned Phase 2-3 clinical program as a treatment for advanced Parkinson’s disease, and our preclinical development efforts and studies; |

|

· |

the timing of and our ability to submit applications for, and obtain and maintain regulatory approvals for, our product candidates, including our ability to file Investigational New Drug applications, or INDs, for our lead candidate in our program for the treatment of a monogenic form of amyotrophic lateral sclerosis, VY-HTT01 for the treatment of Huntington’s disease, and VY-FXN01 for the treatment of Friederich’s ataxia; |

|

· |

our estimates regarding expenses, future revenues, capital requirements, and needs for additional financing; |

|

· |

our ability to continue to develop our product engine; |

|

· |

our ability to develop a manufacturing capability compliant with current good manufacturing practices for our product candidates; |

|

· |

our ability to access, develop, and obtain regulatory clearance for devices to deliver our AAV gene therapies to critical targets of neurological disease; |

|

· |

our intellectual property position and our ability to obtain and maintain intellectual property protection for our proprietary assets; |

|

· |

our estimates regarding the size of the potential markets for our product candidates and our ability to serve those markets; |

|

· |

the rate and degree of market acceptance of our product candidates for any indication once approved; |

|

· |

the possibility and timing of Sanofi Genzyme’s exercise of their options to the programs identified in our Collaboration Agreement; |

|

· |

our plans and ability to raise additional capital, including through equity offerings, debt financings, collaborations, strategic alliances, and licensing arrangements; |

|

· |

our competitive position and the success of competing products that are or become available for the indications that we are pursuing; |

|

· |

the impact of government laws and regulations including in the United States, the European Union, and other important geographies such as Japan; |

2

|

· |

our ability to sustain consistency with recently announced results from our ongoing Phase 1b clinical trial in future clinical trials; and |

|

· |

our ability to enter into future collaborations, strategic alliances, or licensing arrangements. |

These forward-looking statements are only predictions and we may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements. You should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our business, financial condition and operating results. We have included important factors in the cautionary statements included in this Quarterly Report on Form 10-Q, particularly in Part II, Item 1A. Risk Factors that could cause actual future results or events to differ materially from the forward-looking statements that we make. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make.

You should read this Quarterly Report on Form 10-Q and the documents that we have filed as exhibits to the Quarterly Report on Form 10-Q with the understanding that our actual future results may be materially different from what we expect. We do not assume any obligation to update any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

3

FORM 10-Q

TABLE OF CONTENTS

4

Voyager Therapeutics, Inc.

Condensed Consolidated Balance Sheets

(amounts in thousands, except share and per share data)

(unaudited)

|

|

|

September 30, |

|

December 31, |

|

||

|

|

|

2017 |

|

2016 |

|

||

|

Assets |

|

|

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

48,201 |

|

$ |

36,641 |

|

|

Marketable securities, current |

|

|

77,386 |

|

|

137,777 |

|

|

Prepaid expenses and other current assets |

|

|

2,604 |

|

|

4,368 |

|

|

Total current assets |

|

|

128,191 |

|

|

178,786 |

|

|

Property and equipment, net |

|

|

10,558 |

|

|

7,893 |

|

|

Deposits and other non-current assets |

|

|

1,206 |

|

|

1,527 |

|

|

Marketable securities, non-current |

|

|

960 |

|

|

1,360 |

|

|

Total assets |

|

$ |

140,915 |

|

$ |

189,566 |

|

|

Liabilities and stockholders’ equity |

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

Accounts payable |

|

$ |

911 |

|

$ |

550 |

|

|

Accrued expenses |

|

|

10,493 |

|

|

6,488 |

|

|

Deferred revenue, current portion |

|

|

9,537 |

|

|

6,764 |

|

|

Total current liabilities |

|

|

20,941 |

|

|

13,802 |

|

|

Deferred rent |

|

|

5,385 |

|

|

4,999 |

|

|

Deferred revenue, net of current portion |

|

|

28,368 |

|

|

34,818 |

|

|

Other non-current liabilities |

|

|

1,015 |

|

|

25 |

|

|

Total liabilities |

|

|

55,709 |

|

|

53,644 |

|

|

Commitments and contingencies (see note 6) |

|

|

|

|

|

|

|

|

Stockholders’ equity: |

|

|

|

|

|

|

|

|

Preferred stock $0.001 par value: 5,000,000 shares authorized at September 30, 2017 and December 31, 2016; no shares issued and outstanding at September 30, 2017 and December 31, 2016 |

|

|

— |

|

|

— |

|

|

Common stock, $0.001 par value: 120,000,000 shares authorized at September 30, 2017 and December 31, 2016; 26,250,327 and 25,597,912 shares issued and outstanding at September 30, 2017 and December 31, 2016, respectively |

|

|

26 |

|

|

26 |

|

|

Additional paid-in capital |

|

|

234,519 |

|

|

225,963 |

|

|

Accumulated other comprehensive loss |

|

|

(455) |

|

|

(52) |

|

|

Accumulated deficit |

|

|

(148,884) |

|

|

(90,015) |

|

|

Total stockholders’ equity |

|

|

85,206 |

|

|

135,922 |

|

|

Total liabilities and stockholders’ equity |

|

$ |

140,915 |

|

$ |

189,566 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

5

Voyager Therapeutics, Inc.

Condensed Consolidated Statements of Operations and Comprehensive Loss

(amounts in thousands, except share and per share data)

(unaudited)

|

|

|

Three Months Ended |

|

Nine Months Ended |

|

||||||||

|

|

|

September 30, |

|

September 30, |

|

||||||||

|

|

|

2017 |

|

2016 |

|

2017 |

|

2016 |

|

||||

|

Collaboration revenue |

|

$ |

1,148 |

|

$ |

3,308 |

|

$ |

3,790 |

|

$ |

11,858 |

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Research and development |

|

|

19,561 |

|

|

10,309 |

|

|

48,933 |

|

|

29,526 |

|

|

General and administrative |

|

|

4,942 |

|

|

3,370 |

|

|

14,372 |

|

|

9,789 |

|

|

Total operating expenses |

|

|

24,503 |

|

|

13,679 |

|

|

63,305 |

|

|

39,315 |

|

|

Operating loss |

|

|

(23,355) |

|

|

(10,371) |

|

|

(59,515) |

|

|

(27,457) |

|

|

Other income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest income, net |

|

|

291 |

|

|

1,171 |

|

|

799 |

|

|

2,069 |

|

|

Other expense, net |

|

|

(282) |

|

|

(99) |

|

|

(184) |

|

|

(435) |

|

|

Total other income |

|

|

9 |

|

|

1,072 |

|

|

615 |

|

|

1,634 |

|

|

Loss before income taxes |

|

|

(23,346) |

|

|

(9,299) |

|

|

(58,900) |

|

|

(25,823) |

|

|

Income tax benefit |

|

|

— |

|

|

303 |

|

|

31 |

|

|

303 |

|

|

Net loss |

|

$ |

(23,346) |

|

$ |

(8,996) |

|

$ |

(58,869) |

|

$ |

(25,520) |

|

|

Other comprehensive (loss) income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unrealized (loss) gain on available-for-sale-securities, net of income tax (benefit) provision of ($53) for the three months ended September 30, 2017, and $570 for the three and nine months ended September 30, 2016 |

|

|

(485) |

|

|

570 |

|

|

(403) |

|

|

881 |

|

|

Total other comprehensive (loss) income |

|

|

(485) |

|

|

570 |

|

|

(403) |

|

|

881 |

|

|

Comprehensive loss |

|

$ |

(23,831) |

|

$ |

(8,426) |

|

$ |

(59,272) |

|

$ |

(24,639) |

|

|

Net loss per share, basic and diluted |

|

$ |

(0.89) |

|

$ |

(0.35) |

|

$ |

(2.27) |

|

$ |

(1.01) |

|

|

Weighted-average common shares outstanding, basic and diluted |

|

|

26,164,527 |

|

|

25,374,381 |

|

|

25,968,849 |

|

|

25,227,058 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

6

Voyager Therapeutics, Inc.

Condensed Consolidated Statements of Cash Flows

(amounts in thousands)

(unaudited)

|

|

|

Nine Months Ended |

|

||||

|

|

|

September 30, |

|

||||

|

|

|

2017 |

|

2016 |

|

||

|

Cash flow from operating activities |

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(58,869) |

|

$ |

(25,520) |

|

|

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

|

|

Stock-based compensation expense |

|

|

6,945 |

|

|

4,528 |

|

|

Depreciation |

|

|

1,159 |

|

|

448 |

|

|

Amortization of premiums and discounts on marketable securities |

|

|

197 |

|

|

571 |

|

|

In-kind research and development expenses |

|

|

113 |

|

|

989 |

|

|

Other non-cash items |

|

|

139 |

|

|

(409) |

|

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

Prepaid expenses and other current assets |

|

|

1,764 |

|

|

(311) |

|

|

Other non-current assets |

|

|

— |

|

|

57 |

|

|

Deferred revenue |

|

|

(3,790) |

|

|

(12,219) |

|

|

Accounts payable |

|

|

361 |

|

|

175 |

|

|

Accrued expenses |

|

|

3,950 |

|

|

2,301 |

|

|

Other non-current liabilities |

|

|

1,000 |

|

|

— |

|

|

Lease incentive benefit |

|

|

515 |

|

|

— |

|

|

Net cash used in operating activities |

|

|

(46,516) |

|

|

(29,390) |

|

|

Cash flow from investing activities |

|

|

|

|

|

|

|

|

Purchases of property and equipment |

|

|

(3,824) |

|

|

(1,160) |

|

|

Change in restricted cash |

|

|

— |

|

|

(471) |

|

|

Purchases of marketable securities and warrants |

|

|

(49,856) |

|

|

(66,627) |

|

|

Proceeds from maturities of marketable securities |

|

|

110,100 |

|

|

129,700 |

|

|

Net cash provided by investing activities |

|

|

56,420 |

|

|

61,442 |

|

|

Cash flow from financing activities |

|

|

|

|

|

|

|

|

Proceeds from the exercise of stock options |

|

|

1,656 |

|

|

146 |

|

|

Net cash provided by financing activities |

|

|

1,656 |

|

|

146 |

|

|

Net increase in cash and cash equivalents |

|

|

11,560 |

|

|

32,198 |

|

|

Cash and cash equivalents, beginning of period |

|

|

36,641 |

|

|

31,309 |

|

|

Cash and cash equivalents, end of period |

|

$ |

48,201 |

|

$ |

63,507 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

7

VOYAGER THERAPEUTICS, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. Nature of business

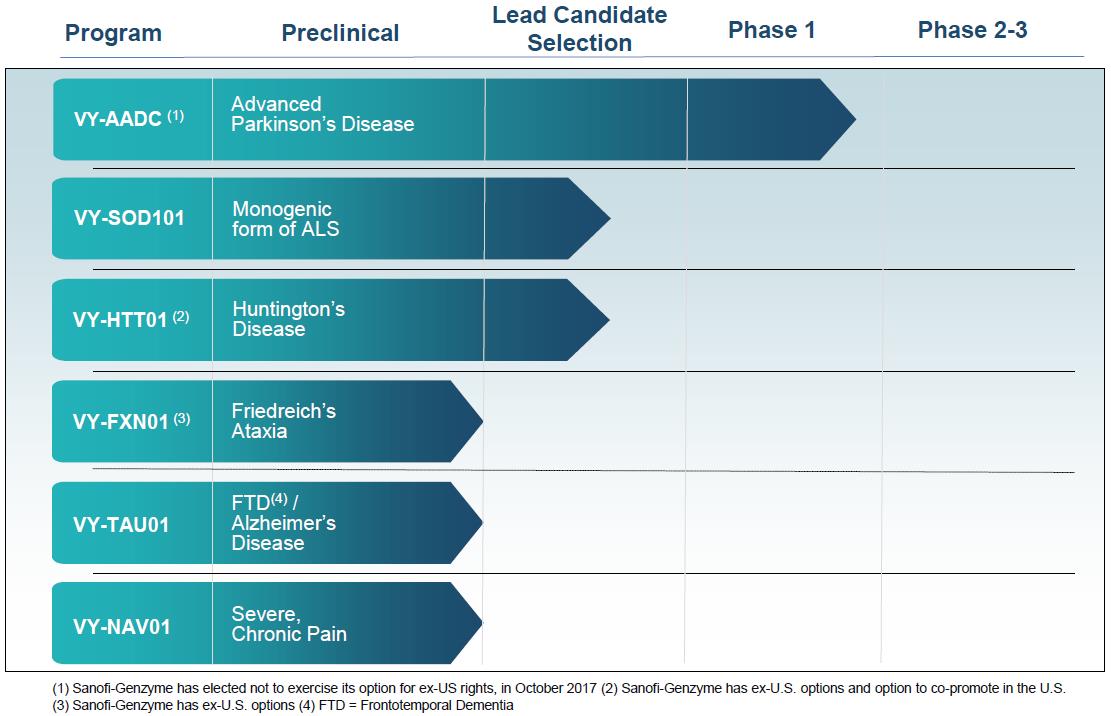

Voyager Therapeutics, Inc. (“the Company”) is a clinical-stage gene therapy company focused on developing life-changing treatments for patients suffering from severe neurological diseases. The Company focuses on neurological diseases where it believes an adeno associated virus (“AAV”) gene therapy approach that either increases or decreases the production of a specific protein can slow or reduce the symptoms experienced by patients, and therefore have a clinically meaningful impact. The Company has created a product engine that enables it to engineer, optimize, manufacture, and deliver its AAV-based gene therapies that have the potential to provide durable efficacy following a single administration. The Company’s pipeline consists of six programs including advanced Parkinson's disease; a monogenic form of amyotrophic lateral sclerosis; Huntington's disease; Friedreich's ataxia; frontotemporal dementia / Alzheimer’s disease; and severe, chronic pain. Additionally, the Company is working to identify and optimize novel AAV capsids.

The Company is devoting substantially all of its efforts to product research and development, activities related to its product engine, novel AAV capsid identification and optimization, and raising capital. The Company is subject to risks common to companies in the biotechnology and gene therapy industry, including but not limited to, risks of failure of pre-clinical studies and clinical trials, the need to obtain marketing approval for its drug product candidates, the need to successfully commercialize and gain market acceptance of its drug product candidates, dependence on key personnel, protection of proprietary technology, compliance with government regulations, development by competitors of technological innovations, and ability to transition from pilot scale manufacturing to large scale commercial production.

In February 2015, the Company entered into an agreement with Sanofi Genzyme (“Collaboration Agreement”), which included a non-refundable upfront payment of $65.0 million. In addition, contemporaneous with entering into the Collaboration Agreement, Sanofi Genzyme entered into a Series B Stock Purchase Agreement, under which Sanofi Genzyme purchased 10,000,000 shares of Series B Preferred Stock for $30.0 million.

Through September 30, 2017, the Company has raised capital primarily from sales of convertible preferred stock and common stock, including its initial public offering of its common stock (“IPO”), and proceeds from the Collaboration Agreement. The Company operates in a net loss position and has recorded a net loss of $58.9 million and $25.5 million for the nine months ended September 30, 2017 and 2016, respectively. As of September 30, 2017, the Company has recognized an accumulated deficit of $148.9 million. The Company believes that its cash, cash equivalents, and marketable debt securities of $125.6 million as of September 30, 2017 is sufficient to fund its current operating plan into 2019. There can be no assurance, however, that the current operating plan will be achieved in the timeframe anticipated by the Company or will not change, that its cash resources will fund the Company’s operating plan for the period anticipated by the Company, or that if the Company needs additional funding, such funding will be available on terms acceptable to the Company, or at all.

2. Summary of significant accounting policies and basis of presentation

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial reporting and as required by Regulation S-X, Rule 10-01. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. For further information, refer to the consolidated financial statements and footnotes included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2016 as filed with the Securities and Exchange Commission (“SEC”). These interim condensed consolidated financial statements, in the opinion of management, reflect all normal recurring adjustments necessary for a fair presentation of the Company’s financial position and results of operations for the periods presented. Any reference in these notes to applicable guidance is meant to refer to the authoritative United States generally accepted accounting

8

principles as found in the Accounting Standards Codification (“ASC”) and Accounting Standards Updates (“ASU”) of the Financial Accounting Standards Board (“FASB”).

Principles of Consolidation

The unaudited interim consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries as disclosed in Note 2, Summary of Significant Accounting Policies, within the “Notes to Consolidated Financial Statements” accompanying its Annual Report on Form 10-K for the fiscal year ended December 31, 2016. Intercompany accounts and transactions have been eliminated.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. On an ongoing basis, the Company’s management evaluates its estimates, which include, but are not limited to, estimates related to revenue recognition, accrued expenses, stock‑based compensation expense, income taxes, and the fair value of common stock. The Company bases its estimates on historical experience and other market specific or other relevant assumptions that it believes to be reasonable under the circumstances. Actual results may differ from those estimates or assumptions.

Recent Accounting Pronouncements

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606) (“ASU 2014-09”). Subsequently, the FASB also issued ASU 2015-14, Revenue from Contracts with Customers (Topic 606), which adjusted the effective date of ASU 2014-09; ASU No. 2016-08, Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net), which amends the principal-versus-agent implementation guidance and illustrations in ASU 2014-09; ASU No. 2016-10, Revenue from Contracts with Customers (Topic 606): Identifying Performance Obligations and Licensing, which clarifies identifying performance obligation and licensing implementation guidance and illustrations in ASU 2014-09; and ASU No. 2016-12, Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements and Practical Expedients, which addresses implementation issues and is intended to reduce the cost and complexity of applying the new revenue standard in ASU 2014-09 (collectively, the “Revenue ASUs”).

The Revenue ASUs provide an accounting standard for a single comprehensive model for use in accounting for revenue arising from contracts with customers and supersedes most current revenue recognition guidance. The accounting standard is effective for interim and annual periods beginning after December 15, 2017, with an option to early adopt for interim and annual periods beginning after December 15, 2016. The guidance permits two methods of adoption: retrospectively to each prior reporting period presented (the full retrospective method), or retrospectively with the cumulative effect of initially applying the guidance recognized at the date of initial application (the modified retrospective method). The Company will adopt the Revenue ASUs effective January 1, 2018 and expects to utilize the modified retrospective methodology. As of September 30, 2017, revenue is generated exclusively from the Company’s collaboration arrangement with Sanofi Genzyme. The Company is currently evaluating the potential impact that the Revenue ASUs will have on its financial position and results of operations as it relates to this single arrangement. The adoption of the Revenue ASUs is expected to have a significant impact on the Company’s notes to consolidated financial statements and its internal controls over financial reporting.

In February 2016, the FASB issued ASU 2016-02, Leases (“ASC 842”), which sets out the principles for the recognition, measurement, presentation and disclosure of leases for both parties to a contract (i.e., lessees and lessors). The standard requires lessees to apply a dual approach, classifying leases as either finance or operating leases based on the principle of whether or not the lease is effectively a financed purchase by the lessee. This classification will determine whether lease expense is recognized based on an effective interest method or on a straight-line basis over the term of the lease. A lessee is also required to record a right-of-use asset and a lease liability for all leases with a term of greater than 12 months regardless of their classification. Leases with a term of 12 months or less will be accounted for similarly to existing guidance for operating leases today. ASC 842 supersedes the previous leases standard, ASC 840

9

Leases. The standard will be effective on January 1, 2019, with early adoption permitted. The Company is in the process of evaluating the impact that this new guidance will have on its consolidated financial statements.

In August 2016, the FASB issued ASU 2016-15, Statement of Cash Flows: Classification of Certain Cash Receipts and Cash Payments. The new standard clarifies certain aspects of the statement of cash flows, including the classification of contingent consideration payments made after a business combination and several other clarifications not currently applicable to the Company. The new standard also clarifies that an entity should determine each separately identifiable source or use within the cash receipts and cash payments on the basis of the nature of the underlying cash flows. In situations in which cash receipts and payments have aspects of more than one class of cash flows and cannot be separated by source or use, the appropriate classification should depend on the activity that is likely to be the predominant source or use of cash flows for the item. The new standard will be effective for the Company on January 1, 2018. The adoption of this standard is not expected to have a material impact on the Company’s consolidated statement of cash flows upon adoption.

In November 2016, the FASB issued ASU 2016-18, Statement of Cash Flows: Restricted Cash (“ASU 2016-18”). The amendments in this update require that amounts generally described as restricted cash and restricted cash equivalents be included within cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. ASU 2016-18 will be effective January 1, 2018, with early adoption permitted. The Company expects the adoption to impact its consolidated statement of cash flows as, upon adoption, it will include the Company’s restricted cash balance in the cash and cash equivalents reconciliation of operating, investing and financing activities.

3. Fair Value Measurements

Assets and liabilities measured at fair value on a recurring basis as of September 30, 2017 and December 31, 2016 are as follows:

|

|

|

|

|

|

Quoted Prices |

|

Significant |

|

|

|

|

||

|

|

|

|

|

|

in Active |

|

Other |

|

Significant |

|

|||

|

|

|

|

|

|

Markets for |

|

Observable |

|

Unobservable |

|

|||

|

|

|

|

|

|

Identical Assets |

|

Inputs |

|

Inputs |

|

|||

|

Assets |

|

Total |

|

(Level 1) |

|

(Level 2) |

|

(Level 3) |

|

||||

|

September 30, 2017 |

|

(in thousands) |

|

||||||||||

|

Money market funds included in cash and cash equivalents |

|

$ |

47,246 |

|

$ |

47,246 |

|

$ |

— |

|

$ |

— |

|

|

Marketable securities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

U.S. Treasury notes |

|

|

67,407 |

|

|

67,407 |

|

|

— |

|

|

— |

|

|

U.S. Government agency securities |

|

|

9,979 |

|

|

— |

|

|

9,979 |

|

|

— |

|

|

Equity securities |

|

|

960 |

|

|

960 |

|

|

— |

|

|

— |

|

|

Total marketable securities |

|

$ |

78,346 |

|

$ |

68,367 |

|

$ |

9,979 |

|

$ |

— |

|

|

Warrants to purchase equity securities |

|

|

472 |

|

|

— |

|

|

472 |

|

|

— |

|

|

Total |

|

$ |

126,064 |

|

$ |

115,613 |

|

$ |

10,451 |

|

$ |

— |

|

|

December 31, 2016 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Money market funds included in cash and cash equivalents |

|

$ |

36,003 |

|

$ |

36,003 |

|

$ |

— |

|

$ |

— |

|

|

Marketable securities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

U.S. Treasury notes |

|

|

130,173 |

|

|

130,173 |

|

|

— |

|

|

— |

|

|

U.S. Government agency securities |

|

|

7,604 |

|

|

— |

|

|

7,604 |

|

|

— |

|

|

Equity securities |

|

|

1,360 |

|

|

1,360 |

|

|

— |

|

|

— |

|

|

Total marketable securities |

|

$ |

139,137 |

|

$ |

131,533 |

|

$ |

7,604 |

|

$ |

— |

|

|

Warrants to purchase equity securities |

|

|

792 |

|

|

— |

|

|

792 |

|

|

— |

|

|

Total |

|

$ |

175,932 |

|

$ |

167,536 |

|

$ |

8,396 |

|

$ |

— |

|

10

The Company measures the fair value of money market funds, U.S. Treasury notes, and equity securities based on quoted prices in active markets for identical securities. The Level 2 debt securities include U.S. Government agency securities that are valued either based on recent trades of securities in inactive markets or based on quoted market prices of similar instruments and other significant inputs derived from or corroborated by observable market data. The Level 2 equity securities include warrants to purchase equity securities that are valued using the Black-Scholes model. The Black-Scholes option pricing model requires inputs based on certain assumptions, including (a) the expected stock price volatility, (b) the calculation of expected term of the awards, (c) the risk-free interest rate, and (d) expected dividends. The assumptions utilized to value the warrants to purchase equity securities as of September 30, 2017 and December 31, 2016 are as follows:

|

|

|

As of September 30, |

|

As of December 31, |

|

||

|

|

|

2017 |

|

2016 |

|

||

|

Risk-free interest rate |

|

1.8 |

% |

|

1.8 |

% |

|

|

Expected dividend yield |

|

— |

% |

|

— |

% |

|

|

Expected term (in years) |

|

3.9 |

|

|

4.7 |

|

|

|

Expected volatility |

|

100.1 |

% |

|

97.5 |

% |

|

The expected volatility is based on the historic volatility for the equity securities underlying the warrants and is calculated based on a period of time commensurate with the expected term assumption. The expected term is based on the remaining contractual life of the warrants on each measurement date. The risk-free interest rate is based on a treasury instrument whose term is consistent with the expected term of the warrants. The expected dividend yield is assumed to be zero as the entity that issued the warrants has never paid and has not indicated any intention to pay dividends.

4. Cash, Cash Equivalents, and Available for Sale Marketable Securities

Cash equivalents include all highly liquid investments maturing within 90 days from the date of purchase. Investments consist of securities with original maturities greater than 90 days when purchased. The Company classifies these investments as available-for-sale and records them at fair value in the accompanying condensed consolidated balance sheets. Unrealized gains or losses are included in accumulated other comprehensive income (loss). Premiums or discounts from par value are amortized to investment income over the life of the underlying investment.

The Company classifies marketable securities as available‑for‑sale. Marketable debt securities with a maturity date within the next year are classified as current assets. Marketable debt securities with a maturity date greater than one year and marketable equity securities are classified as non‑current where the Company has the intent and ability to hold these securities for at least the next 12 months. Available‑for‑sale debt securities are maintained by an investment manager and consist of U.S. Treasury notes and U.S. Government agency securities. During the third quarter in 2016, the Company invested in a supplier and received common stock and warrants to purchase common stock in that entity. The common stock is included in non-current marketable securities and the warrants are included in non-current assets.

All available‑for‑sale securities are carried at fair value with the unrealized gains and losses included in other comprehensive income (loss) as a component of stockholders’ equity until realized. Any premium or discount arising at purchase is amortized and/or accreted to interest income and/or expense. Realized gains and losses are determined using the specific identification method and are included in other income (expense). If any adjustment to fair value reflects a decline in value of the investment, the Company considers all available evidence to evaluate the extent to which the decline is “other‑than‑temporary” and, if so, recognizes the loss through a charge to the Company’s statement of operations and comprehensive loss. No other than temporary losses have been recognized.

11

Cash, cash equivalents, and marketable securities included the following at September 30, 2017 and December 31, 2016:

|

|

|

Amortized |

|

Unrealized |

|

Unrealized |

|

Fair |

|

||||

|

|

|

Cost |

|

Gains |

|

Losses |

|

Value |

|

||||

|

|

|

(in thousands) |

|

||||||||||

|

As of September 30, 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Money market funds included in cash and cash equivalents |

|

$ |

47,246 |

|

$ |

— |

|

$ |

— |

|

$ |

47,246 |

|

|

Marketable securities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

U.S. Treasury notes |

|

|

67,421 |

|

|

— |

|

|

14 |

|

|

67,407 |

|

|

U.S. Government agency securities |

|

|

9,978 |

|

|

1 |

|

|

— |

|

|

9,979 |

|

|

Total debt securities |

|

$ |

77,399 |

|

$ |

1 |

|

$ |

14 |

|

$ |

77,386 |

|

|

Equity securities |

|

|

1,220 |

|

|

— |

|

|

260 |

|

|

960 |

|

|

Total marketable securities |

|

$ |

78,619 |

|

$ |

1 |

|

$ |

274 |

|

$ |

78,346 |

|

|

Total money market funds and marketable securities |

|

$ |

125,865 |

|

$ |

1 |

|

$ |

274 |

|

$ |

125,592 |

|

|

As of December 31, 2016 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Money market funds included in cash and cash equivalents |

|

$ |

36,003 |

|

$ |

— |

|

$ |

— |

|

$ |

36,003 |

|

|

Marketable securities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

U.S. Treasury notes |

|

|

130,237 |

|

|

2 |

|

|

66 |

|

|

130,173 |

|

|

U.S. Government agency securities |

|

|

7,604 |

|

|

— |

|

|

— |

|

|

7,604 |

|

|

Total debt securities |

|

$ |

137,841 |

|

$ |

2 |

|

$ |

66 |

|

$ |

137,777 |

|

|

Equity securities |

|

|

1,220 |

|

|

140 |

|

|

— |

|

|

1,360 |

|

|

Total marketable securities |

|

$ |

139,061 |

|

$ |

142 |

|

$ |

66 |

|

$ |

139,137 |

|

|

Total money market funds and marketable securities |

|

$ |

175,064 |

|

$ |

142 |

|

$ |

66 |

|

$ |

175,140 |

|

The estimated fair value of the Company’s debt securities balance at September 30, 2017, by contractual maturity, is as follows:

|

Due in one year or less |

|

$ |

77,386 |

|

5. Accrued Expenses

Accrued expenses as of September 30, 2017 and December 31, 2016 consist of the following:

|

|

|

As of September 30, |

|

As of December 31, |

|

||

|

|

|

2017 |

|

2016 |

|

||

|

|

|

(in thousands) |

|

||||

|

External research and development costs |

|

$ |

6,447 |

|

$ |

2,384 |

|

|

Employee compensation costs |

|

|

2,486 |

|

|

2,399 |

|

|

Professional services |

|

|

1,020 |

|

|

698 |

|

|

Accrued goods and services |

|

|

309 |

|

|

842 |

|

|

Patent costs |

|

|

180 |

|

|

89 |

|

|

Other |

|

|

51 |

|

|

76 |

|

|

Total |

|

$ |

10,493 |

|

$ |

6,488 |

|

6. Commitments and Contingencies

Operating Leases

During March 2014, the Company entered into an agreement to lease its facility located at 75 Sidney Street under a non-cancelable operating lease that would expire on December 15, 2019. The lease contains escalating rent clauses which require higher rent payments in future years. The Company expenses rent on a straight-line basis over the term of the lease, including any rent-free periods.

12

In December 2015, the Company executed an amendment to extend the 75 Sidney Street lease and executed an agreement to lease the 64 Sidney Street facility until December 31, 2024. The additional facility includes laboratory and office space, and was ready for occupancy in early 2017.

The Company received leasehold improvement incentives from the landlord totaling $1.3 million and $3.5 million for 75 Sidney Street and 64 Sidney Street, respectively. The Company recorded these incentives as a component of deferred rent and is amortizing these incentives as a reduction of rent expense over the life of the lease. The leasehold improvements have been recorded as fixed assets.

The following table summarizes the Company’s significant contractual obligations as of payment due date by period at September 30, 2017, related to the amended 75 Sidney Street lease and the 64 Sidney Street lease through December 2024:

|

|

|

Total Minimum |

|

|

|

|

|

Lease Payments |

|

|

|

|

|

(in thousands) |

|

|

|

2017 |

|

$ |

806 |

|

|

2018 |

|

|

3,290 |

|

|

2019 |

|

|

3,382 |

|

|

2020 |

|

|

3,762 |

|

|

2021 |

|

|

3,868 |

|

|

2022+ |

|

|

12,273 |

|

|

|

|

$ |

27,381 |

|

Significant Agreements

Sanofi Genzyme Collaboration Agreement

Summary of Agreement

In February 2015, the Company entered into the Collaboration Agreement with Sanofi Genzyme, which included a non‑refundable upfront payment of $65.0 million. In addition, contemporaneously with entering into the Collaboration Agreement, Sanofi Genzyme entered into a Series B Stock Purchase Agreement, under which Sanofi Genzyme purchased 10,000,000 shares of Series B Preferred Stock for $30.0 million. The fair value of the Series B Preferred Stock at the time of issuance was approximately $25.0 million. The $5.0 million premium over the fair value is accounted for as additional consideration under the Collaboration Agreement.

Under the Collaboration Agreement, the Company granted Sanofi Genzyme an exclusive option to license, develop and commercialize (i) ex‑U.S. rights to the following programs, which are referred to as Split Territory Programs; VY‑AADC (“Parkinson’s Program”), VY‑FXN01 (“Friedreich’s Ataxia Program”), a future program to be designated by Sanofi Genzyme (“Future Program”), and VY‑HTT01 (“Huntington’s Program”) with an incremental option to co‑commercialize VY‑HTT01 in the United States and (ii) worldwide rights to VY‑SMN101 (“Spinal Muscular Atrophy Program”). Sanofi Genzyme’s option for the Split Territory Programs and the Spinal Muscular Atrophy Program is triggered following the completion of the first proof of principle human clinical study (“POP Study”), on a program-by-program basis.

Prior to any option exercise by Sanofi Genzyme, the Company will collaborate with Sanofi Genzyme in the development of products under each Split Territory Program and the Spinal Muscular Atrophy Program pursuant to a written development plan and under the guidance of an Alliance Joint Steering Committee (“AJSC”), comprised of an equal number of employees from the Company and Sanofi Genzyme.

The Company is required to use commercially reasonable efforts to develop products under each Split Territory Program and the Spinal Muscular Atrophy Program through the completion of the applicable POP Study. During the development of these joint programs, the activities are guided by a Development Advisory Committee (“DAC”). The

13

DAC may elect to utilize certain Sanofi Genzyme technology relating to the Parkinson’s Program, the Huntington’s Program, or generally with the manufacture of Split Territory Program products.

The Company is solely responsible for all costs incurred in connection with the development of the Split Territory Programs and the Spinal Muscular Atrophy Program products prior to the exercise of an option by Sanofi Genzyme except that, at the Company’s request and upon mutual agreement, Sanofi Genzyme will provide “in‑kind” services valued at up to $5.0 million. As of September 30, 2017, the Company has received in-kind services from Sanofi Genzyme valued at $3.6 million.

Other than the Parkinson’s Program (for which a POP Study has already commenced), if the Company does not initiate a POP Study for a given Split Territory Program by December 31, 2026 (or for the Future Program by the tenth anniversary of the date the Future Program is nominated by Sanofi Genzyme), and Sanofi Genzyme has not terminated the Collaboration Agreement with respect to the collaboration program, then Sanofi Genzyme shall be entitled, as its sole and exclusive remedy, to a credit of $10.0 million for each such program against other milestone or royalty payments payable by Sanofi Genzyme under the Collaboration Agreement. However, if the POP Study is not initiated due to a regulatory delay or a force majeure event, such time period shall be extended for so long as such delay continues.

Under the Collaboration Agreement, Sanofi Genzyme is not required to pay an option exercise payment to exercise its option regarding the Parkinson’s Program. Sanofi Genzyme is required to pay $20.0 million for the exercise of each Split Territory Program option other than the Parkinson’s Program and $30.0 million for the exercise of the Spinal Muscular Atrophy Program option.

Upon Sanofi Genzyme’s exercise of its option to license a given product in a Split Territory Program (“Split Territory Licensed Product”), the Company will have sole responsibility for the development of such Split Territory Licensed Product in the United States and Sanofi Genzyme shall have sole responsibility for development of such Split Territory Licensed Product in the rest of the world. The Company and Sanofi Genzyme will have shared responsibility for execution of ongoing development of such Split Territory Licensed Product that is not specific to either territory, including costs associated therewith. The Company is responsible for all commercialization activities relating to Split Territory Licensed Products in the United States, including all of the associated costs. Sanofi Genzyme is responsible for all commercialization activities relating to the Split Territory Licensed Products in the rest of the world, including all of the associated costs. If Sanofi Genzyme exercises its co‑commercialization rights for the Huntington’s Program product (“Huntington’s Licensed Product”), Sanofi Genzyme will be the lead party responsible for all commercialization activities related to such product in the United States.

Upon exercise of the option, Sanofi Genzyme shall have the sole right to develop the licensed product from the Spinal Muscular Atrophy Program (“Spinal Muscular Atrophy Licensed Product”) worldwide. Sanofi Genzyme shall be responsible for all of the development costs that occur after the option exercise date for the Spinal Muscular Atrophy Program. Sanofi Genzyme is also responsible for commercialization activities relating to the Spinal Muscular Atrophy Licensed Product worldwide. In November 2016, the Company and Sanofi Genzyme elected to deprioritize the Spinal Muscular Atrophy Program due to, among other things, the progress made in other preclinical programs and the evolving competitive landscape.

Sanofi Genzyme is required to pay the Company for specified regulatory and commercial milestones, if achieved, up to $645.0 million across all programs. The regulatory approval milestones are payable upon either regulatory approval in the United States or regulatory and reimbursement approval in the European Union and range from $40.0 million to $50.0 million per milestone, with an aggregate total of $265.0 million. The commercial milestones are payable upon achievement of specified annual net sales in each program and range from $50.0 million to $100.0 million per milestone, with an aggregate total of $380.0 million.

In addition, to the extent any Split Territory Licensed Products or the Spinal Muscular Atrophy Licensed Product are commercialized, the Company is entitled to tiered royalty payments ranging from the mid‑single digits to mid‑teens based on a percentage of net sales by Sanofi Genzyme. Sanofi Genzyme is entitled to receive tiered royalty payments related to sales of Split Territory Licensed Product ranging from the low‑single digits to mid‑single digits based on a percentage of net sales by the Company depending on whether the Company uses Sanofi Genzyme technology in the Split Territory Licensed Product. If Sanofi Genzyme elects to co‑commercialize the Huntington’s

14

Licensed Product in the United States, the Company and Sanofi Genzyme will share in any profits or losses from sales of such product.

The Collaboration Agreement will continue in effect until the later of (i) the expiration of the last to expire of the option rights and (ii) the expiration of all payment obligations unless sooner terminated by the Company or Sanofi Genzyme. The Company and Sanofi Genzyme have customary termination rights including the right to terminate for an uncured material breach of the agreement committed by the other party and Sanofi Genzyme has the right to terminate for convenience.

In October 2017, the Company announced that Sanofi Genzyme decided not to exercise its option for the ex-U.S. rights to the Parkinson’s Program. Therefore, the Company now maintains global rights to VY-AADC. If the Company uses certain Sanofi Genzyme technology in VY-AADC, Sanofi Genzyme is entitled to receive low-single digit royalty payments based on a percentage of net sales by the Company and the Company may be obligated to make certain regulatory milestone payments to a third-party licensor. As a result of Sanofi Genzyme’s decision, the Company is no longer entitled to receive $45 million and $60 million of regulatory and commercial milestone payments, respectively, related to the Parkinson’s Program.

Accounting Analysis

The Collaboration Agreement includes the following deliverables: (i) research and development services for each of the Split Territory License Programs and the Spinal Muscular Atrophy Program, (ii) participation in the AJSC, (iii) participation in the DAC and (iv) the option to obtain a development and commercial license in the Parkinson’s Program and related deliverables. The Company has determined that the option to obtain a development and commercial license in the Parkinson’s Program is not a substantive option for accounting purposes, primarily because there is no additional option exercise payment payable by Sanofi Genzyme at the time the option is exercised. Therefore, the option to obtain a license and other obligations of the Company that are contingent upon exercise of the option are considered deliverables at the inception of the arrangement. The options in the other Split Territory Programs and the Spinal Muscular Atrophy Program are considered substantive as there are substantial option exercise payments payable by Sanofi Genzyme upon exercise. In addition, as a result of the uncertainties related to the discovery, research, development and commercialization activities, the Company is at risk with regard to whether Sanofi Genzyme will exercise the options. Moreover, the substantive options are not priced at a significant incremental discount. Accordingly, the substantive options are not considered deliverables at the inception of the arrangement and the associated option exercise payments are not included in allocable arrangement consideration. The Company has also determined that any obligations which are contingent upon the exercise of a substantive option are not considered deliverables at the outset of the arrangement, as these deliverables are contingent upon the exercise of the options. In addition, any option exercise payments associated with the substantive options are not included in the allocable arrangement consideration.

The Company has concluded that each of the deliverables identified at the inception of the arrangement has standalone value from the other undelivered elements. Additionally, the Collaboration Agreement does not include return rights related to the initial collaboration term. Accordingly, each deliverable qualifies as a separate unit of accounting.

The Company identified $79.3 million of allocable arrangement consideration consisting of the $65.0 million upfront fee, the $5.0 million premium paid in excess of fair value of the Series B Preferred Stock and $9.3 million of Sanofi Genzyme “in‑kind” and other funding.

The Company has allocated the allocable arrangement consideration based on the relative selling price of each unit of accounting. For all units of accounting, the Company determined the selling price using the best estimate of selling price (“BESP”). The Company determined the BESP for the service related deliverable for the research and development activities based on internal estimates of the costs to perform the services, including expected internal expenses and expenses with third parties for services and supplies, marked up to include a reasonable profit margin and adjusted for the scope of the potential license. Significant inputs used to determine the total expense of the research and development activities include, the length of time required and the number and costs of various studies that will be performed to complete the applicable POP Study. The BESP for the AJSC and DAC have been estimated based on the costs incurred to participate in the committees, marked up to include a reasonable profit margin. The BESP for the

15

license option was determined based on the estimated value of the license and related deliverables adjusted for the estimated probability that the option would be exercised by Sanofi Genzyme.

Based on the relative selling price allocation, the allocable arrangement consideration was allocated as follows:

|

|

|

|

|

|

|

Unit of Accounting |

|

Amount |

|

|

|

|

|

(in thousands) |

|

|

|

Research and Development Services for: |

|

|

|

|

|

Huntington’s Program |

|

$ |

15,662 |

|

|

Parkinson’s Program |

|

|

6,648 |

|

|

Friedreich’s Ataxia Program |

|

|

16,315 |

|

|

Spinal Muscular Atrophy Program |

|

|

32,050 |

|

|

Future Program |

|

|

2,464 |

|

|

Committee Obligations: |

|

|

|

|

|

AJSC |

|

|

147 |

|

|

DAC |

|

|

227 |

|

|

License Option and related deliverables |

|

|

5,743 |

|

|

Total |

|

$ |

79,256 |

|

The Company recognizes the amounts associated with research and development services on a straight-line basis over the estimated period of service as there is no discernable pattern or objective measure of performance for the services. Similarly, the Company recognizes the amount associated with the committee obligations on a straight-line basis over the period of service consistent with the expected pattern of performance. The amount allocated to the license option is being deferred until the point in time in which Sanofi Genzyme is required to make a decision. In October 2017, Sanofi Genzyme elected not to exercise the option. The amount allocated to the Parkinson’s Program license option and related deliverables unit of accounting will be recognized as revenue at the time of the decision.

During 2016, the Company reassessed the estimated period of performance for each of its units of accounting and determined that the estimated period would be extended for two units of accounting. Additionally, the Company and Sanofi Genzyme agreed to deprioritize the development of the Spinal Muscular Atrophy Licensed Product and reduce the estimates related to the amount of “in-kind” services that would be provided by Sanofi Genzyme. These adjustments were made on a prospective basis and resulted in decreases in revenue recognized by $2.4 million per quarter.

During the first two quarters of 2017, the Company reassessed the estimated period of performance for each of its units of accounting and, based on the current facts and circumstances, determined that the estimated period would be extended for three units of accounting. These adjustments were made on a prospective basis and resulted in a decrease in revenue recognized by $0.5 million per quarter.

The Company has evaluated all of the milestones that may be received in connection with each Split Territory Licensed Product and the Spinal Muscular Atrophy Licensed Product. In evaluating if a milestone is substantive, the Company assesses whether: (i) the consideration is commensurate with either the Company’s performance to achieve the milestone or the enhancement of the value of the delivered item(s) as a result of a specific outcome resulting from the Company performance to achieve the milestone, (ii) the consideration relates solely to past performance and (iii) the consideration is reasonable relative to all of the deliverables and payment terms within the arrangement. All regulatory milestones are considered substantive on the basis of the contingent nature of the milestone, specifically reviewing factors such as the scientific, clinical, regulatory, and other risks that must be overcome to achieve the milestone as well as the level of effort and investment required. Accordingly, such amounts will be recognized as revenue in full in the period in which the associated milestone is achieved, assuming all other revenue recognition criteria are met. All commercial milestones will be accounted for in the same manner as royalties and recorded as revenue upon achievement of the milestone, assuming all other revenue recognition criteria are met.

During the three and nine months ended September 30, 2017, the Company recognized $1.1 million and $3.8 million, respectively, of revenue associated with its collaboration with Sanofi Genzyme related to research and development services performed during the periods. As of September 30, 2017, there is $37.9 million of deferred

16

revenue related to the Collaboration Agreement, which is classified as either current or noncurrent in the accompanying consolidated balance sheet based on the period the consideration is expected to be recognized.

Costs incurred relating to the programs that Sanofi Genzyme has the option to license under the Collaboration Agreement consist of internal and external research and development costs, which primarily include: salaries and benefits, lab supplies and preclinical research studies. The Company does not separately track or segregate the amount of costs incurred under the Collaboration Agreement. These costs are included in research and development expenses in the Company’s statement of operations during the three and nine months ended September 30, 2017. The Company estimates that the majority of research and development expense during the period relate to programs for which Sanofi Genzyme has an option right.

MRI Interventions License and Securities Purchase Agreements

In September 2016, the Company entered into securities purchase and license agreements with MRI Interventions, Inc. (“MRIC”). MRIC is the primary supplier of the ClearPoint System, which is being used by the Company in ongoing development and clinical trials. Under a securities purchase agreement, the Company paid $2.0 million for shares of MRIC common stock and a warrant to purchase additional shares of MRIC common stock. The Company also entered into a license agreement with MRIC that provided for certain rights to MRIC technology and for MRIC to transfer the rights and know-how to manufacture the ClearPoint System to enable the Company to utilize an alternative supplier for the ClearPoint System for use in the Company’s development and clinical trials.

During the three months ended March 31, 2017, the Company terminated the license agreement with MRIC, and all prior and future commitments and obligations under such agreement became null and void. As of September 30, 2017 the Company continued to hold the common stock and warrants to purchase additional shares of common stock as an available-for-sale security and non-current asset, respectively.

Other Agreements

During September 2016, the Company entered into a research and development funding arrangement with a non-profit organization that provides up to $4.0 million in funding upon the achievement of clinical and development milestones. The agreement provides that the Company repay amounts received under certain circumstances including termination of the agreement, and to pay an amount up to 2.6 times the funding received upon successful development and commercialization of any products developed. During the three months ended March 31, 2017, the Company earned a milestone payment of $1.0 million. No milestone payments were earned in the three months ended September 30, 2017. The Company has evaluated the arrangement and has concluded that it represents a research and development financing arrangement as it is probable that the Company will repay amounts received under the arrangement. As a result, the $1.0 million earned through September 30, 2017 is recorded as a non-current liability in the accompanying balance sheet.

Litigation

The Company is not a party to any material legal matters and does not have contingency reserves established for any litigation liabilities as of September 30, 2017 or December 31, 2016.

7. Redeemable Convertible Preferred Stock

The Company has authorized preferred stock amounting to 5,000,000 shares as of September 30, 2017 and December 31, 2016. The authorized preferred stock was classified under stockholders’ equity at September 30, 2017 and December 31, 2016.

17

8. Stock‑Based Compensation

2015 Stock Option Plan

In October 2015, the Company’s board of directors and stockholders approved the 2015 Stock Option and Incentive Plan (“2015 Stock Option Plan”) which became effective upon the completion of the IPO. The 2015 Stock Option Plan provides the Company with the flexibility to use various equity-based incentive and other awards as compensation tools to motivate its workforce. These tools include stock options, stock appreciation rights, restricted stock, restricted stock units, unrestricted stock, performance share awards and cash-based awards. The 2015 Stock Option Plan replaced the Voyager Therapeutics, Inc. 2014 Stock Option and Grant Plan (“2014 Plan”). Any options or awards outstanding under the 2014 Plan remained outstanding and effective. The number of shares initially reserved for issuance under the 2015 Stock Option Plan is the sum of (i) 1,311,812 shares of common stock and (ii) the number of shares under the 2014 Plan that are not needed to fulfill the Company’s obligations for awards issued under the 2014 Plan as a result of forfeiture, expiration, cancellation, termination or net issuances of awards thereunder. The number of shares of common stock that may be issued under the 2015 Stock Option Plan is also subject to increase on the first day of each fiscal year by up to 4% of the Company’s issued and outstanding shares of common stock on the immediately preceding December 31.

Effective January 1, 2016 and 2017, an additional 1,069,971 and 1,070,635 shares, respectively, were added to the Company’s 2015 Stock Option Plan for future issuance. As of September 30, 2017, there were 1,628,505 shares of common stock available for future award grants under the 2015 Stock Option Plan. During the three and nine months ended September 30, 2017, the Company issued a total of 265,500 and 1,521,000 stock options, respectively, to employees and directors under the 2015 Stock Option Plan. During the three and nine months ended September 30, 2017, the Company issued a total of 20,000 stock options to non-employees under the 2015 Stock Option Plan.

The terms of stock awards agreements, including vesting requirements, are determined by the Board of Directors and are subject to the provisions of the 2015 Stock Option Plan.

2014 Stock Option and Grant Plan

In January 2014, the Company adopted the 2014 Plan, under which it may grant incentive stock options, non‑qualified stock options, restricted stock awards, unrestricted stock awards, or restricted stock units to purchase up to 823,529 shares of common stock to employees, officers, directors and consultants of the Company.

In April 2014, the Company amended the 2014 Plan to allow for the issuance of up to 1,411,764 shares of common stock. In August 2014, April 2015, August 2015, and October 2015, the Company further amended the 2014 Plan to allow for the issuance of up to 2,000,000, 2,047,058, 2,669,411, and 2,998,823 shares of common stock, respectively. During 2014 the Company issued only restricted stock awards under the 2014 Plan and during 2015 the Company only granted stock options.

Founder Awards

In January 2014, the Company issued 1,188,233 shares of restricted stock to its founders at an original issuance price of $0.0425 per share. Of the total restricted shares awarded to the founders, 835,292 shares generally vest over one to four years, based on each founder’s continued service to the Company in varying capacity as a Scientific Advisory Board member, consultant, director, officer or employee, as set forth in each grantee’s individual restricted stock purchase agreement. The remaining 352,941 of the shares issued begin vesting upon the achievement of certain performance objectives as well as continued service to the Company, as set forth in the agreements.

These performance conditions are tied to certain milestone events specific to the Company’s corporate goals, including but not limited to preclinical and clinical development milestones related to the Company’s product candidates. Stock‑based compensation expense associated with these performance‑based awards is recognized when the achievement of the performance condition is considered probable, using management’s best estimates. During 2016, management determined that the achievement of the performance milestone for one of the three performance‑based awards had become probable and began recognizing stock-based compensation accordingly. The Company recorded $0.6 million

18

and $1.5 million in stock-based compensation expense related to this award during the three and nine months ended September 30, 2017, respectively. The Company recorded $0.2 million and $1.0 million in stock-based compensation expense related to this award during the three and nine months ended September 30, 2016, respectively. No stock‑based compensation expense was recorded for the remaining two founders’ awards with performance-based vesting as of September 30, 2017 as the performance-based milestones related to these awards were not probable.

2015 Employee Stock Purchase Plan

In October 2015, the Company’s board of directors and stockholders approved the 2015 Employee Stock Purchase Plan (“2015 ESPP”). Under the 2015 ESPP, all full-time employees of the Company are eligible to purchase common stock of the Company twice per year, at the end of each six-month payment period. During each payment period, eligible employees who so elect, may authorize payroll deductions in an amount of 1% to 10% (whole percentages only) of the employee’s base pay for each payroll period. At the end of each payment period, the accumulated deductions are used to purchase shares of common stock from the Company at a discount. A total of 262,362 shares of common stock were initially authorized for issuance under this plan. The 2015 ESPP became effective upon the completion of the IPO. The number of shares of common stock that may be issued under the 2015 ESPP is also subject to increase on the first day of each fiscal year by up to 1% of the Company’s issued and outstanding shares of common stock on the immediately preceding December 31. The 2015 ESPP became effective upon the completion of the IPO. Effective January 1, 2016 and 2017, 267,492 and 267,658 shares of common stock, respectively, were added to the 2015 ESPP.

Stock‑Based Compensation Expense

Total compensation cost recognized for all stock‑based compensation awards in the statements of operations and comprehensive loss is as follows:

|

|

|

Three Months Ended |

|

Nine Months Ended |

|

||||||||

|

|

|

September 30, |

|

September 30, |

|

||||||||

|

|

|

2017 |

|

2016 |

|

2017 |

|

2016 |

|

||||

|

|

|

(in thousands) |

|

||||||||||

|

Research and development |

|

$ |

2,231 |

|

$ |

1,378 |

|

$ |

4,107 |

|

$ |

3,425 |

|

|

General and administrative |

|

|

1,010 |

|

|

411 |

|

|

2,838 |

|

|

1,103 |

|

|

Total stock compensation expense |

|

$ |

3,241 |

|

$ |

1,789 |

|

$ |

6,945 |

|

$ |

4,528 |

|

Restricted Stock

A summary of the status of and changes in unvested restricted stock unit activity under the Company’s equity award plan for the nine months ended September 30, 2017 was as follows:

|

|

|

|

|

Weighted |

|

|

|

|

|

|

|

Average |

|

|

|

|

|

|

|

Grant Date |

|

|

|

|

|

|

|

Fair Value |

|

|

|

|

|

Shares |

|

Per Share |

|

|

|

Unvested restricted common stock as of December 31, 2016 |

|

1,167,984 |

|

$ |

0.76 |

|

|

Issued |

|

— |

|

|

— |

|

|

Vested |

|

(455,634) |

|

$ |

0.76 |

|

|

Repurchased |

|

(36,202) |

|

$ |

0.67 |

|

|

Unvested restricted common stock as of September 30, 2017 |

|

676,148 |

|

$ |

0.72 |

|

The expense related to awards granted to employees and non-employees was $0.1 million and $1.6 million, respectively, for the three months ended September 30, 2017, and $0.4 million and $2.3 million for the nine months ended September 30, 2017, respectively. The expense related to awards granted to employees and non-employees was $0.1 million and $0.7 million, respectively, for the three months ended September 30, 2016, and $0.4 million and $1.9 million for the nine months ended September 30, 2016, respectively.

19

As of September 30, 2017, the Company had unrecognized stock-based compensation expense related to its unvested restricted stock unit awards of $8.1 million, which is expected to be recognized over the remaining average vesting period of 0.6 years.

Stock Options

The following is a summary of stock option activity for the nine months ended September 30, 2017:

|

|

|

|

|

Weighted |

|

Remaining |

|

Aggregate |

|

||

|

|

|

|

|

Average |

|

Contractual |

|

Intrinsic |

|

||

|

|

|

|

|

Exercise |

|

Life |

|

Value |

|

||

|

|

|

Shares |

|

Price |

|

(in years) |

|

(in thousands) |

|

||

|

Outstanding at December 31, 2016 |

|

1,871,237 |

|

$ |

10.21 |

|

|

|

|

|

|

|