Attached files

| file | filename |

|---|---|

| EX-32.2 - CERTIFICATION - GL Brands, Inc. | freedomleaf_ex3202.htm |

| EX-32.1 - CERTIFICATION - GL Brands, Inc. | freedomleaf_ex3201.htm |

| EX-31.2 - CERTIFICATION - GL Brands, Inc. | freedomleaf_ex3102.htm |

| EX-31.1 - CERTIFICATION - GL Brands, Inc. | freedomleaf_ex3101.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_______________________________________________

FORM 10-K

_______________________________________________

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2017

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______.

Commission File Number: 000-55687

______________________________________________

![]()

FREEDOM LEAF INC.

(Exact name of registrant as specified in its charter)

_______________________________________________

| Nevada | 46-2093679 | |

|

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

|

3571 E. Sunset Road, Suite 420 Las Vegas, NV |

89120 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (702) 499-6022

____________________________________________

Securities registered under Section 12(b) of the Exchange Act:

None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, $0.001 Par Value

(Title of class)

____________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o |

| Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company x |

| Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes x No

On December 31, 2016, the last business day of the registrant’s most recently completed second quarter, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $4,595,945, based upon the closing price on that date of the common stock of the registrant on the OTC Bulletin Board system of $0.13. For purposes of this response, the registrant has assumed that its directors, executive officers and beneficial owners of 5% or more of its Common Stock are deemed affiliates of the registrant.

As of September 29, 2017, the registrant had 126,298,304 shares of its common stock, $0.001 par value, issued, issuable, and outstanding.

EXPLANATORY NOTE

This Annual Report on Form 10-K (the “Annual Report”) of Freedom Leaf Inc. (the “Company”) is being filed pursuant to the Order under Section 15B, Section 17A and Section 36 of The Securities Exchange Act of 1934 Granting Exemptions from Specified Provisions of the Exchange Act and Certain Rules Thereunder (the “Order”), dated September 28, 2017, of the Securities and Exchange Commission (available at https://www.sec.gov/rules/other/2017/34-81760.pdf), which extends the Company’s deadline to file this Annual Report. Pursuant to the Order, for companies affected by Hurricane Irma, all reports, schedules or forms must be filed on or before October 19, 2017.

The Company’s independent certifying accountant’s office is located in Tampa, Florida, and as a result of Hurricane Irma and its aftermath, was closed for about a week because it lost power and Internet access, which closure delayed the completion of the audit of the Company’s financial statements. As a result, the Company was not able to file this Annual Report by October 13, 2017, and the Company is therefore relying on the Order.

| 1 |

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Rule 175 of the Securities Act of 1933, as amended, and Rule 3b-6 of the Securities Act of 1934, as amended, that involve substantial risks and uncertainties. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about our industry, our beliefs and our assumptions. Words such as “anticipate,” “expects,” “intends,” “plans,” “believes,” “seeks” and “estimates” and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this Form 10-K. Investors should carefully consider all of such risks before making an investment decision with respect to the Company’s stock. The following discussion and analysis should be read in conjunction with our consolidated financial statements for Freedom Leaf Inc. Such discussion represents only the best present assessment from our Management.

| 2 |

General Overview

Freedom Leaf Inc. (“Freedom Leaf” and the “Company”) was incorporated in the State of Nevada on February 21, 2013, under the name of Arkadia International, Inc. The Company was originally engaged in the business of the acquisition of in demand equipment, cars, and goods with the intent to resell these in the U.S. territories or export to overseas countries.

On October 3, 2014, the Company experienced a change in control. Richard C. Cowan acquired a majority of the issued and outstanding common stock of the Company in accordance with stock purchase agreements by and between Mr. Cowan and Vladimir and Galina Shekhtman (“Sellers”). On the closing date, October 3, 2014, pursuant to the terms of the Stock Purchase Agreement, Cowan purchased from the Sellers 6,950,100 shares of the Company’s outstanding restricted common stock for $100,000, representing 93% of the total issued and outstanding at that time.

On November 6, 2014, the Company merged with Freedom Leaf Inc., a private Nevada corporation. The Company changed its name from Arkadia International, Inc., to Freedom Leaf Inc. As a result of the merger, the private company was dissolved, the sole officer, director and shareholder of the private company, Clifford J. Perry, became an officer and director of the Company, and Mr. Perry received approximately 48.1% of the Company’s common stock post-merger.

For financial reporting purposes, this merger was accounted for as a "reverse merger" rather than a business combination, and the private company was deemed to be the accounting acquirer in the transaction, with the Company deemed to be the acquired company for financial reporting purposes. Consequently, the assets and liabilities and the operations that have been reflected in the historical financial statements of the Company prior to the merger are those of the private company, and were be recorded at the historical cost basis of the private company, and the financial statements after completion of the merger include the combined assets and liabilities of the Company and the private company, the historical operations of the private company only, and the operations of both companies from the closing date of the merger.

We are currently devoting our efforts to the news, arts and entertainment niche, both in print and online publications, and to providing services to the cannabis/hemp industry. The Company generates revenue through paid advertising in publications, print and online, in the cannabis/hemp marketplace. The Company earns revenue from 1) providing consulting services to companies who are in our industry, 2) contracting with companies to brand, market, and sell their products and/or services, 3) providing seminars in this space, 4) selling branded products for the Company and others the Company represents, 5) selling licenses, both domestic and foreign, for the use of the Freedom Leaf brand that includes the Company’s products and services, and 6) pursuing mergers and/or acquisitions having instituted an accelerator that began working with one company starting during the year ended June 30, 2017.

Our corporate headquarters are located at 3571 E. Sunset Road, Suite 420, Las Vegas, Nevada, 89120. The Company’s primary web site is www.freedomleaf.com. This web site is not incorporated in this Form 10-K.

Overview

Freedom Leaf, The Marijuana Legalization Company, has now published and circulated hundreds of thousands of copies of our twenty-seven editions in thirty-eight states with the assistance of over 160 activist marketers. Freedom Leaf magazine, “The Good News in Marijuana Reform,” reports on arts, fashion, and lifestyle, all of the elements of the burgeoning cannabis movements. Freedom Leaf magazine provides activists, consumers, patients and entrepreneurs with a means to stay informed on the emerging industry's most cutting edge marijuana-related information, innovations and legislation. It is distributed nationally through chapters of the National Organization for the Reform of Marijuana Laws (NORML.org), Students for a Sensible Drug Policy (SSDP.org), and WomenGrow.com, as well as through participating medical and recreational dispensaries, smoke and vape shops, doctors and attorneys’ offices, and others in the marijuana industry. It is also available online at http://www.freedomleaf.com/freedom-leaf-ezines/ and on the Company’s free mobile app available on Apple iOS and the Google Play Store.

| 3 |

Freedom Leaf is also expanding its online presence. Freedom Leaf has an entire platform of content suited for every aspect of advertising and marketing to consumers from all businesses in the cannabis industry. These sites incorporate many aspects of the marijuana industry and movement. In May 2017, the Company acquired two Spanish domiciled websites: www.lamarihuana.com and www.marihuana-medicinal.com. This is another expansion of the Freedom Leaf Media Network. The www.lamarihuana.com website has 1.2 million Facebook likes and received in excess of 1 million visitors a month during the last six months, making this website one of the most popular Spanish speaking websites in the world. The content is automatically translated into the language of the country within which the viewer is residing.

The Industry

The following is a report on the industry, as published in ArcView Group’s State of Legal Marijuana Markets 5th Edition.

A Year Of Substantial Gains Across The Industry

The legal cannabis industry accelerated at a remarkable pace in 2016. North American consumers spent $6.7 billion on legal cannabis products, up 34% from 2015.

Cannabis is now legally sold in state-of-the-art retail dispensaries with computer-based inventory and sales tracking, fully regulated and taxed by their state governments just like any other product category. Entrepreneurs are modernizing the product just as quickly. Many successful brands have launched extracts, edibles, topicals, and other types of products that are leading consumers to spend more and, in cutting-edge Colorado, they have reduced traditional dried flowers to less than 56% of the business. More states passed laws to open new markets and expand existing ones in 2016 than in any previous year. These new markets will drive sustained revenue growth in the years ahead.

The legislatures of Pennsylvania and Ohio legalized medical cannabis in those major swing states, while voters in California, Maine, Nevada, and Massachusetts North Dakota, Florida, and Montana voters passed medical cannabis laws. The blistering 34% compound annual growth rate (CAGR) from 2014 to 2016 was driven primarily by Colorado and Washington initiating adult-use sales. This rate of growth will subside somewhat in 2017 to 22%, as the eight states that voted to open or expand their cannabis markets on Election Day in November 2016 work to implement the new programs. But Arcview Market Research forecasts growth will reaccelerate beginning in 2018, as adult use sales ramp up in Canada, California, and Massachusetts along with medical sales in Florida. That will grow the $6.7-billion market of 2016 at a robust 27% CAGR to $22.6 billion in 2021.

| 4 |

Very few consumer industry categories reach $5 billion in annual spending and then post anything like 25% compound annual growth across the following five years. Cable television came close, growing 19% annually in the late 1980s as national networks like CNN and HBO proved to be wildly popular. Broadband internet subscription spending grew 29% per annum in the early 2000s as it became almost as much of a “must have” utility as electricity or television for the modern home. What became the ubiquitous home video business that birthed the great Blockbuster success story only grew at a 12% CAGR after reaching $5 billion in revenue in 1988.

That 20+% annual growth rate is likely to continue for many years past 2021 as more states and countries legalize cannabis. Arcview includes 30 states plus Canada with active legal markets by 2021 in its model, but in many of the largest markets, like New York and Florida, sales are expected to remain limited to medical-use. In the 2021-2026 period, however, many of these states will build robust legal adult-use markets, and all but a few states will make medical cannabis available legally.

It’s also likely that US federal prohibition will be repealed during that period, which would fuel explosive growth.

Canada and Mexico are included in Arcview’s North American market projections for the first time and analyzed throughout this 5th Edition of The State of Legal Marijuana Markets. The expected roll-out of Canada’s adult-use market is analyzed. The U.S. northern neighbor may be the world leader in moving toward a well-regulated legal cannabis industry. Countries around the world are already responding to the state-by-state dismantling of prohibition in America — the chief exporter of the “War on Drugs” for decades—by moving to allow medical use (as in Australia, Germany, and Colombia) or to outright legalization (as in Uruguay).

Robust growth through 2021 and beyond in the United States is predicted even if the US Justice Department opposes the cannabis industry. Chapter 2 provides a detailed analysis of why that kind of reversal in policy is unlikely, but a major one is the popularity of legal cannabis.

Polls show that 80% of Americans approve of legal access to medical cannabis and 60% approve of full adult use legalization. That level of agreement is rare on any policy issue and it’s allowing elected officials across the political spectrum to start to move past the stigma previously associated with this issue.

One key reason support for legalization is spreading so rapidly is that it is accomplishing a key goal: the illicit market is shrinking. The illicit market grew steadily throughout the last 40 years of the War on Drugs to what Arcview estimates was a North American total of $46.8 billion when adult-use sales first began in 2014 in Colorado and Washington. Illicit sales are now being rolled back at the fastest rates in those states with the most mature legal adult use markets (see graph, below). Most dramatically, what Arcview estimates was a $1-billion illicit market in Colorado is now less than $500 million, which represents just 27% of a $1.8-billion overall market.

| 5 |

Election Results

President Donald Trump said in 1991, “You have to legalize drugs to win that war.” He backed away from that position in his campaign for president but was remarkably consistent in his support for medical access to cannabis and his belief that cannabis policy should be up to the states. But once elected he appointed dedicated drug warrior Jeff Sessions for Attorney General. Sessions remarked “Good people don’t smoke marijuana” at a 2015 Congressional hearing. Despite conflicting signals from the new administration, investors and entrepreneurs have many other reasons to be hopeful:

• The newly elected Prime Minister of Canada, Justin Trudeau, took office in late 2015 and immediately started the formal process of legalizing adult use.

• In the US November elections, voters in eight of the nine states voting on cannabis measures approved them, bringing to 63% the portion of Americans living in medical use states and 21% those in adult-use states.

• For the first time, the Presidential nominees of both major U.S. political parties felt free to speak approvingly of the medical use of cannabis and the right of states to experiment with different cannabis policies.

• In December, the Mexican Senate voted overwhelmingly (98-7) to send a medical-use legalization bill to the Chamber of Deputies.

These developments were inconceivable just a few years ago. The biggest political win of the U.S. election came in California. California pioneered the modern cannabis policy reform movement in 1996 when voters passed Proposition 215, the Compassionate Care Act. Though voters failed to approve adult use in 2010, they voted overwhelmingly in 2016 to make adult use legal in a state that represents the world’s sixth-largest economy. Nevada also voted to legalize adult use, though a similar initiative failed narrowly in Arizona. Massachusetts and Maine also passed voter-generated initiatives to legalize the adult use of cannabis, joining District of Columbia voters in showing the continent-wide breadth of the movement.

The formalizing of medical-use rules in Montana, and the approval of medical cannabis sales in Arkansas, North Dakota, and Florida (where it garnered 71% of the vote) showed that cannabis policy reform is hugely popular, even in red and swing states that voted for Trump. Earlier in the year, big swing states Ohio and Pennsylvania saw medical legalization come to pass via legislative action.

The two most significant votes may have come in the smallest jurisdictions: citizens of Denver narrowly approved on-site usage in licensed clubs, and Pueblo, CO, voters rejected opponents’ efforts to pass what was essentially an industry shutdown. In both cases, cannabis supporters prevailed against the early betting. These votes show that experience with legalization can lead voters to pass even more open laws, and reject efforts to roll it back.

| 6 |

According to the England Journal of Medicine, 76% of clinicians polled worldwide believe that the medicinal benefits outweigh the risks and potential harms. Within the next five years, the legal cannabis industry is expected to out-earn the US film industry, the organic foods industry and more than triple the revenues of the NFL.

(Source: http://www.nejm.org/doi/full/10.1056/NEJMclde1305159)

53% of Americans support marijuana legalization according to Pew Research.

(Source: http://www.pewresearch.org/fact-tank/2015/04/14/6-facts-about-marijuana/)

Marketing Focus and Strategy

Our marketing is centered around the Freedom Leaf magazine and website. It is a two-fold strategy. First, the magazine draws businesses that are in the cannabis/hemp industry to speak to us either because they are interested in advertising in the magazine and/or for Freedom Leaf to publicize their business either through us writing an article about their company or for them to write an article about an aspect in the industry that relates to their business (content marketing). Second, Freedom Leaf will undertake cross promotion with operators of different expos, seminars and other public events that extend our reach to companies in the industry. Last of all, we also use the non-profit alliances that we have established to gain a prominent position in our Industry. This has provided Freedom Leaf with considerable credibility and the ability to attract deals with companies to either represent them accelerate them or acquire them.

Our Products

| · | Ads in magazine, on Freedom Leaf owned web sites, and in our email blasts |

| · | Events, education classes, expos and seminars |

| · | Marketing contracts with industry businesses |

| · | Branding contracts with industry businesses |

| · | Freedom Leaf branded products |

| · | Magazine subscriptions |

| · | Branded products and/or services companies that we represent |

| · | Concerts and musical festivals |

| · | Licensing the Freedom Leaf brand, products and services |

Sales Targets

Companies within the Cannabis/Hemp Industry for Advertising

We target companies in the cannabis/hemp industry to offer our advertising and related services. Some examples are: dispensaries in the 29 states, and Washington, D.C. (https://medicalmarijuana.procon.org/view.resource.php?resourceID=000881&print=true) that have legalized medical marijuana sales; locations that sell recreational marijuana in the 8 states that have legalized recreational marijuana use, companies that make edible food infused with marijuana and/or CBDs, vape manufacturers and wholesalers, websites that sell auxiliary products related to cannabis/hemp use, and other businesses that sell products and or services that wish to reach our market, such as clothing companies, concert organizers, and manufacturers or distributors of cell phones, headsets, soda, energy drinks, health products, etc.

| 7 |

Target Market

The State of Colorado completed a survey for the year 2014 which provides helpful information on the demographics related to our target markets:

Competitive Edge

Freedom Leaf’s credibility has been growing in the cannabis/hemp marketplace due to its support of non-profits in the space and for the excellent editorial and other content in our magazine.

At least 50% of our magazine distribution is through non-profit activists (to themselves and those they come in contact with) and we believe, industry activists are among the most loyal consumers any company can potentially have. All of the magazine issues are also available on our Web site in addition to other content for viewers.

Its digest size (5.5” x 8.5”) is perfect for people to carry around easily.

Competitors

We compete with companies of all sizes in a variety of geographies that offer solutions that compete with elements of our business plan, such as in print and online printing, advertising, etc. More specifically, however, the medical and recreational marijuana companies are a new, developing and nascent market, resulting in a highly fragmented and fractured marketplace. The federal state and municipal governments have varying degrees of legality that will affect business. Some of the companies we compete with are much larger than us, and such companies have significantly greater resources.

| 8 |

Most of our current and potential competitors have longer operating histories, larger customer or user bases, greater brand recognition and significantly greater financial, marketing and other resources than we do. Our competitors may be able to secure experienced employees, accommodate customers more efficiently and adopt more aggressive pricing policies than we can. Many of these current and potential competitors can devote substantially more resources to advertising, marketing and attracting experienced talent than we can. In addition, larger, more well-established and financed entities may acquire, invest in or form joint ventures with our competitors

Our competitors include:

Culture Magazine

www.ireadculture.com

Southern & Northern CA, Denver CO, Seattle WA, San Diego CA, Portland OR,

Started in Southern CA in 2009

High Times Magazine

www.hightimes.com

Started in 1974, monthly publication, oldest in industry but subscription base has reduced substantially, still the major national magazine.

Dope Magazine

www.dopemagazine.com

Approximately 10 months old in eastern Washington, 4 to 6 months in balance of locations (southern CA, northern CA, eastern WA, Portland, OR, Denver, CO)

Elevate Magazine

www.elavatenv.com

Local Las Vegas magazine (we have a strategic relationship with them)

Intellectual Property

Website

We assert common law copyright in the contents of our websites, www.FreedomLeaf.com, www.FreedomLeafInc.com, www.MyHempology.com, www.LaMarihuana.com, and www.CannaBizU.com, and common law trademark rights in our business name and related product labels, including “The Marijuana Legalization Company,” “Hemp Inspired,” “CannaBizU,” “CannaBiz,” and “BudFinder.” We have copyrights and trademarked some of our tradenames (see Trademarks section). We expect to copyright and/or trademark additional tradenames in the future, as we deem necessary to protect our business.

We plan to develop these other domains, which are owned by Freedom Leaf:

www.MarijuanaNews.com

www.LadyCannabis.com

www.CannabisSeminars.com

www.CannabisDebate.com

www.CannaSpa.com

www.Vegasterdam.com

| 9 |

| Other domains owned by Freedom Leaf: 420apps.com acjmg.com amstercamera.com amstercamera.nl bluegrasscbd.com budfindr.com budfindr.net campuscannabisdebate.com campuscannabisdebate.net campuscannabisdebates.com campuscannabisdebates.net canapoly.com cannabisarts.com cannabisbusinessservices.com cannabisbusinesssolutions.com cannabisbusinessuniversity.com cannabiscene.com cannabiscentury.com cannabisdebate.com cannabisfriendly.com cannabisgeriatrics.com cannabishempmuseum.com cannabishouse.com cannabisprogress.com cannabisseminars.com cannabistcafe.com cannabistjournal.com cannabistro.us cannabisvenues.com cannabiz.tv cannabizinc.com cannabizmapster.com cannabizmapster.net cannabizmuseum.com cannabizsolutions.com cannabizu.com cannabizu.net cannabizuniversity.com |

cannabizwire.com cannablunt.net cannacakefactory.com cannacalendar.com cannacouture.com cannadepot.us cannaderma.com cannado.com cannafactory.com cannagold.com cannagum.com cannahookah.com cannakitchen.com cannalatte.com cannalingo.com cannapachino.com cannapassion.com cannapoly.com cannarollup.com cannashisha.com cannaspa.com cannatreat.com cannavita.com cannawellness.com checkyourweed.com cliffsight.com dankdefenders.com dankdefenders.net fliagency.com freedomisnorml.com freedomleaf.com freedomleaf.guru freedomleaf.net freedomleaf.tv freedomleaf.vegas freedomleafaction.com freedomleafcares.com freedomleafcares.org |

| 10 |

| freedomleafinc.com freedomleafmagazine.com freedomleafmagazine.net freedomleafnetwork.com freedomleafnetwork.net freedomleafnetwork.tv freedomleafseniors.com freeedomleafinternational.com freeedomleafinternational.net freetheleaf.info freeleaf.com genuinetics.com healthyhips.org hempinspired.com hempinspired.net hempinspired.tv hempleaftoday.com hempology.co hempologyproducts.com highmilehigh.co highmilehigh.com highmilehigh.net highrollup.com iamwaycool.com iamwaycool.org jawpainsolution.com karmarijuana.com kingsofpotcomedy.com kingsofpotcomedytour.com kybluegrasscbd.com ladycanna.com ladycannabis.com ladycannabis.org |

ladyhempcbd.com ladyhempcbd.net ladyhempglobal.com lamarihuana.net lamarihuana.news lamarihuana.us lasvegasterdam.com lasvegasterdam.vegas lasweedas.com leafceutical.com leafvegas.com mangina.xxx marijuanalegalizationcompany.com marijuanalegalizationinc.com marijuananews.com marijuananews.tv marijuanarollup.com medicinalmarijuanauniversity.com myhempology.com naturaltmjcures.com normllegal.com nvnorml.com nvnorml.org otcfrlf.com passionhemp.com ponyboystuff.com primecommoditylogistics.com pufftuffstuff.vegas |

Trademarks

We have registered or filed for registration with the United States Trademark and Patent Office for the following trademarks: “Freedom Leaf,” “The Marijuana Legalization Company,” “Hemp Inspired,” “Hempology,” and with the State of Nevada “CannaBizU,” and “CannaBiz.” Internationally, we have filed for “Freedom Leaf” trademark protection in European Union, Columbia, China, Mexico, Jamaica and Uruguay.

Reports to Security Holders

We intend to furnish our shareholders annual reports containing consolidated financial statements audited by our independent registered public accounting firm and to make available quarterly reports containing unaudited consolidated financial statements for each of the first three quarters of each year. We file Quarterly Reports on Form 10-Q, Annual Reports on Form 10-K and Current Reports on Form 8-K with the Securities and Exchange Commission in order to meet our timely and continuous disclosure requirements. We may also file additional documents with the Commission if they become necessary in the course of our company's operations.

The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is www.sec.gov.

| 11 |

Government Regulations

We believe that we are and will continue to be in compliance in all material respects with applicable statutes and the regulations passed in the United States. There are no current orders or directions relating to our company with respect to the foregoing laws and regulations.

Continued development of the marijuana industry is dependent upon continued legislative authorization of marijuana at the state level. Any number of factors could slow or halt progress in this area. Further, progress, while encouraging, is not assured. While there may be ample public support for legislative action, numerous factors impact the legislative process. Any one of these factors could slow or halt use of marijuana, which would negatively impact our proposed business.

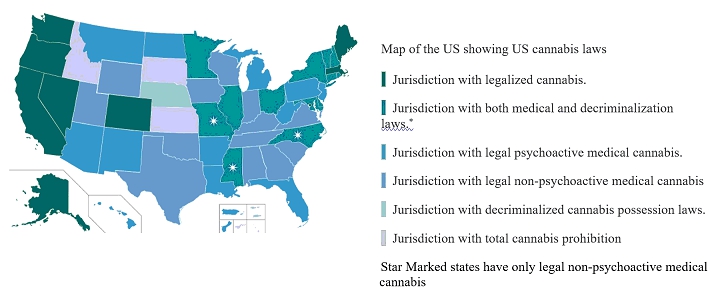

Marijuana is a Schedule-I controlled substance and is illegal under federal law. Even in those states in which the use of marijuana has been legalized, its use remains a violation of federal laws. There are currently 25 states and the District of Columbia allowing its citizens to use Medical Marijuana. Additionally, Alaska, Colorado, Oregon, Washington State, as well as Washington D.C., have voted to legalize cannabis for adult recreational use. The state laws are in conflict with the federal Controlled Substances Act, which makes marijuana use and possession illegal on a national level. The Obama administration effectively stated that it is not an efficient use of resources to direct law federal law enforcement agencies to prosecute those lawfully abiding by state-designated laws allowing the use and distribution of medical marijuana. However, the Trump administration has signaled that it may reverse Obama-era guidance, and the current administration may change the prior stated policy regarding the low-priority enforcement of federal marijuana laws. Active enforcement of the current federal regulatory position on cannabis may thus indirectly and adversely affect our revenues and profits. Any such change in the federal government’s enforcement of current federal laws could cause significant financial damage to us. While we do not intend to harvest, distribute or sell cannabis in the United States, we may be irreparably harmed by a change in enforcement by the federal government or state-level regulatory or legislative changes.

Environmental Regulations

We do not believe that we are or will become subject to any environmental laws or regulations of the United States. While our products and business activities do not currently violate any laws, any regulatory changes that impose additional restrictions or requirements on us or on our products or potential customers could adversely affect us by increasing our operating costs or decreasing demand for our products or services, which could have a material adverse effect on our results of operations.

Employees

As of June 30, 2017, we had a total of six full time employees. Our employees are not parties to any collective bargaining agreement. We believe our relationships with our employees are good.

Property

We lease approximately 2,800 square feet of office space in Las Vegas, Nevada, pursuant to a lease that will expire on April 15, 2019. This facility serves as our corporate headquarters.

Available Information

All reports of the Company filed with the SEC are available free of charge through the SEC’s website at www.sec.gov. In addition, the public may read and copy materials filed by the Company at the SEC’s Public Reference Room located at 100 F Street, N.E., Washington, D.C. 20549. The public may also obtain additional information on the operation of the Public Reference Room by calling the Commission at 1-800-SEC-0330.

As a smaller reporting company, we are not required to provide the information required by this item.

Item 1B. Unresolved Staff Comments.

None.

| 12 |

We lease approximately 2,800 square feet of office space in Las Vegas, Nevada, pursuant to a lease that will expire on April 15, 2019. This facility serves as our corporate headquarters.

From time to time, we may be involved in litigation relating to claims arising out of our operations in the normal course of business. As of September 30, 2017, there were no pending or threatened lawsuits that could reasonably be expected to have a material effect on the results of our operations.

Item 4. Mine Safety Disclosures.

Not applicable.

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market for Common Equity

Market Information

The Company’s common stock is quoted on OTC Markets Group’s OTCPink under the symbol “FRLF.” The symbol change from the predecessor company was effective February 24, 2015. As of June 30, 2017, the Company’s common stock was held by 45 shareholders of record, which does not include shareholders whose shares are held in street or nominee name.

The Company’s shares commenced trading on or about February 10, 2014 (for Arkadia International, Inc.). The following chart is indicative of the fluctuations in the stock prices for the fiscal years ended June 30, 2017 and 2016:

| For the Years Ended June 30, | ||||||||||||||||

| 2017 | 2016 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

| First Quarter | $ | 0.195 | $ | 0.09 | $ | 0.51 | $ | 0.10 | ||||||||

| Second Quarter | $ | 0.24 | $ | 0.0801 | $ | 0.51 | $ | 0.20 | ||||||||

| Third Quarter | $ | 0.1229 | $ | 0.0585 | $ | 0.35 | $ | 0.15 | ||||||||

| Fourth Quarter | $ | 0.0674 | $ | 0.033 | $ | 0.24 | $ | 0.17 | ||||||||

Source: OTC Markets

The Company’s transfer agent is Globex Transfer, LLC, at 780 Deltona Blvd., Suite 202, Deltona, FL 32725.

Dividend Distributions

We have not paid any cash dividends on our common stock and have no present intention of paying any dividends on the shares of our common stock for the foreseeable future. Our current policy is to retain earnings, if any, for use in our operations and in the development of our business. Our future dividend policy may be modified from time to time by our board of directors.

| 13 |

Securities authorized for issuance under equity compensation plans

The Company established a stock option plan on June 27, 2016.

Penny Stock

Our common stock is considered "penny stock" under the rules the Securities and Exchange Commission (the "SEC") under the Securities Exchange Act of 1934. The SEC has adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. Penny stocks are generally equity securities with a price of less than $5.00, other than securities registered on certain national securities exchanges or quoted on the NASDAQ Stock Market System, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or quotation system. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock, to deliver a standardized risk disclosure document prepared by the Commission, that:

| • | contains a description of the nature and level of risks in the market for penny stocks in both public offerings and secondary trading; |

| • | contains a description of the broker's or dealer's duties to the customer and of the rights and remedies available to the customer with respect to a violation to such duties or other requirements of Securities' laws; contains a brief, clear, narrative description of a dealer market, including bid and ask prices for penny stocks and the significance of the spread between the bid and ask price; |

| • | contains a toll-free telephone number for inquiries on disciplinary actions; |

| • | defines significant terms in the disclosure document or in the conduct of trading in penny stocks; and |

| • | contains such other information and is in such form, including language, type, size and format, as the Commission shall require by rule or regulation. |

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, the customer with:

| • | bid and offer quotations for the penny stock; |

| • | the compensation of the broker-dealer and its salesperson in the transaction; |

| • | the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the marker for such stock; and |

| • | monthly account statements showing the market value of each penny stock held in the customer's account. |

In addition, the penny stock rules that require that prior to a transaction in a penny stock not otherwise exempt from those rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written acknowledgement of the receipt of a risk disclosure statement, a written agreement to transactions involving penny stocks, and a signed and dated copy of a written suitably statement.

These disclosure requirements may have the effect of reducing the trading activity in the secondary market for our stock.

Related Stockholder Matters

None.

Purchase of Equity Securities

None.

Item 6. Selected Financial Data.

As the Company is a “smaller reporting company,” this item is inapplicable.

| 14 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation.

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Rule 175 of the Securities Act of 1933, as amended, and Rule 3b-6 of the Securities Act of 1934, as amended, that involve substantial risks and uncertainties. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about our industry, our beliefs and our assumptions. Words such as “anticipate,” “expects,” “intends,” “plans,” “believes,” “seeks” and “estimates” and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this Form 10-K. Investors should carefully consider all of such risks before making an investment decision with respect to the Company’s stock. The following discussion and analysis should be read in conjunction with our consolidated financial statements and summary of selected financial data for Freedom Leaf Inc. Such discussion represents only the best present assessment from our Management.

DESCRIPTION OF COMPANY

The Company was a startup company that was incorporated in Nevada under the name Arkadia International, Inc. on February 21, 2013.

On October 3, 2014, the Company experienced a change in control. Richard C. Cowan acquired a majority of the issued and outstanding common stock of the Company in accordance with stock purchase agreements by and between Mr. Cowan and Vladimir and Galina Shekhtman (“Sellers”). On the closing date, October 3, 2014, pursuant to the terms of the Stock Purchase Agreement, Cowan purchased from the Sellers 6,950,100 shares of the Company’s outstanding restricted common stock for $100,000, representing 93%.

On November 4, 2014, the Company's Board of Directors declared a twelve for one forward stock split of all outstanding shares of the Company’s common stock. As the stock split was approved by FINRA, the common share and per common share data in these consolidated financial statements and related notes hereto have been retroactively adjusted to account for the effect of the stock split. The total number of authorized common shares and the par value thereof was not changed by the split.

On November 6, 2014, we entered into a merger agreement (the “Merger Agreement”) with Freedom Leaf Inc., a Nevada corporation (“Private Company”), and the Company’s sole officer and director Clifford J. Perry (“Perry”), being the owners of record of all of the issued share capital of Freedom Leaf Inc. (the “FL Stock”). Pursuant to the Merger Agreement, the Shareholders received an aggregate of 83,401,200 shares (48.1%) our common stock (consisting of a new issuance of shares and Mr. Perry’s transfer of all of his shares), and Private Company was merged with and into us. As a result, Freedom Leaf Inc. became our Company whereas the operations of Arkadia International, Inc. ceased, and there was a change of control of the Company.

Prior to the merger, we were a startup company that originally intended to engage in the business of the acquisition of in demand equipment, cars, and goods with the intent to resell these in the in the U.S. territories or export to overseas countries.

We have had limited operations and have been issued a “going concern” opinion by our auditor, based upon our reliance on the sale of our common stock as the sole source of funds for our future operations.

We have been devoting substantially all of our efforts to migrate to the news, arts and entertainment niche, with both “in print” and online publications. The Company is generating revenue through paid advertising in publications, both print and online, in the cannabis/hemp marketplace. The Company will also earn revenue from providing consulting services to companies who are in our industry, contracting with companies to brand, market, and sell their products and/or services, provide seminars in this space, and sell branded products for the Company and others the Company represents. We have also started incubating other companies in the cannabis industry and have one company that we are currently incubating.

The following Management Discussion and Analysis should be read in conjunction with the consolidated financial statements and accompanying notes included in this Form 10-K.

| 15 |

COMPARISON OF THE YEAR ENDED JUNE 30, 2017 TO THE YEAR ENDED JUNE 30, 2016

Results of Operations

Revenue. For the year ended June 30, 2017, our revenue was $817,457, compared to $118,473 for the same period in 2016. This increase in revenue was attributable to increased sales related to increased magazine subscriptions and licensing fees.

Operating Expenses:

Direct costs of Revenue. For the year ended June 30, 2017, direct costs of revenue were $124,290 compared to $132,381 for the same period in 2016. As a percent of revenue, direct costs of revenue were 15.2% and 111.7%, respectively, for 2017 and 2016.

General and Administrative Expenses. For the year ended June 30, 2017, general and administrative expenses were $1,421,224 compared to $2,685,025 for the same period in 2016. The increase was due to the increase in operations and stock-based compensation ($750,990 compared to $2,258,863 for the years ended June 30, 2017 and 2016, respectively).

Net Loss. We generated net losses of $910,650 for the year ended June 30, 2017, compared to $3,011,220 for the same period in 2016.

Liquidity and Capital Resources

General. At June 30, 2017, we had cash and cash equivalents of $2,498. We have historically met our cash needs through a combination of cash flows from operating activities and proceeds from private placements of our securities and loans. Our cash requirements are generally for selling, general and administrative activities. We believe that our cash balance is not sufficient to finance our cash requirements for expected operational activities, capital improvements, and partial repayment of debt through the next 12 months.

Our operating activities used cash of $435,450 for the year ended June 30, 2017, and we used cash in operations of $50,831 during the same period in 2016. The principal elements of cash flow from operations for the year ended June 30, 2017, included a net loss of $910,650.

Cash used in investing activities during the year ended June 30, 2017, was $4,312 compared to $3,235 provided by investing activities during the same period in 2016.

Cash generated in our financing activities was $440,502 for the year ended June 30, 2017, compared to cash generated of $54,923 during the comparable period in 2016.

As of June 30, 2017, current assets exceeded current liabilities by 3.68 times. Current assets increased from $7,122 at June 30, 2016 to $641,915 at June 30, 2017, whereas current liabilities decreased from $176,310 at June 30, 2016, to $174,256 at June 30, 2017.

| For the years ended | ||||||||

| June 30, | ||||||||

| 2017 | 2016 | |||||||

| Cash used in operating activities | $ | 435,450 | $ | 50,831 | ||||

| Cash used in investing activities | 4,312 | 3,235 | ||||||

| Cash provided by financing activities | 440,502 | 54,923 | ||||||

| Net changes to cash | $ | 740 | $ | 857 | ||||

| 16 |

Going Concern

The accompanying consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company had sales of $817,457 and net losses of $910,650 for the year ended June 30, 2017, compared to sales of $118,473 and net losses of $3,011,220 for the year ended June 30, 2016. The Company had a working capital, stockholders’ equity, and accumulated deficit of $467,659, $187,818 and $4,920,988, respectively, at June 30, 2017. These factors raise substantial doubt about the ability of the Company to continue as a going concern for a reasonable period of time. The Company is highly dependent on its ability to continue to obtain investment capital from future funding opportunities to fund the current and planned operating levels. The consolidated financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts or the amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern. The Company’s continuation as a going concern is dependent upon its ability to bring in income generating activities and its ability to continue receiving investment capital from future funding opportunities. No assurance can be given that the Company will be successful in these efforts.

Critical Accounting Policies

Use of Estimates. The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates in the accompanying consolidated financial statements include the amortization period for intangible assets, valuation and impairment valuation of intangible assets, depreciable lives of the web site and property and equipment, valuation of warrant and beneficial conversion feature debt discounts, valuation of share-based payments and the valuation allowance on deferred tax assets.

Changes in Accounting Principles. No significant changes in accounting principles were adopted during fiscal 2017 and 2016.

Derivatives. The Company evaluates its convertible debt, options, warrants or other contracts to determine if those contracts or embedded components of those contracts qualify as derivatives to be separately accounted for. The result of this accounting treatment is that under certain circumstances the fair value of the derivative is marked-to-market each balance sheet date and recorded as a liability. In the event that the fair value is recorded as a liability, the change in fair value is recorded in the statement of operations as other income or expense. Upon conversion or exercise of a derivative instrument, the instrument is marked to fair value at the conversion date and then that fair value is reclassified to equity. Equity instruments that are initially classified as equity that become subject to reclassification under this accounting standard are reclassified to liability at the fair value of the instrument on the reclassification date.

Impairment of Long-Lived Assets. The Company accounts for long-lived assets in accordance with the provisions of Statement of Financial Accounting Standards ASC 360-10, “Accounting for the Impairment or Disposal of Long-Lived Assets”. This statement requires that long-lived assets and certain identifiable intangibles be reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to future undiscounted net cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amount of the assets exceeds the fair value of the assets. Assets to be disposed of are reported at the lower of the carrying amount or fair value less costs to sell.

Fair Value of Financial Instruments and Fair Value Measurements. The Company measures their financial assets and liabilities in accordance with generally accepted accounting principles. For certain of our financial instruments, including cash, accounts payable, accrued expenses escrow liability and short-term loans the carrying amounts approximate fair value due to their short maturities.

We have adopted accounting guidance for financial and non-financial assets and liabilities. The adoption did not have a material impact on our results of operations, financial position or liquidity. This standard defines fair value, provides guidance for measuring fair value and requires certain disclosures. This standard does not require any new fair value measurements, but rather applies to all other accounting pronouncements that require or permit fair value measurements. This guidance does not apply to measurements related to share-based payments. This guidance discusses valuation techniques, such as the market approach (comparable market prices), the income approach (present value of future income or cash flow), and the cost approach (cost to replace the service capacity of an asset or replacement cost). The guidance utilizes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value into three broad levels. The following is a brief description of those three levels:

| 17 |

Level 1: Observable inputs such as quoted prices (unadjusted) in active markets for identical assets or liabilities.

Level 2: Inputs other than quoted prices that are observable, either directly or indirectly. These include quoted prices for similar assets or liabilities in active markets and quoted prices for identical or similar assets or liabilities in markets that are not active.

Level 3: Unobservable inputs in which little or no market data exists, therefore developed using estimates and assumptions developed by us, which reflect those that a market participant would use.

Revenue Recognition. The Company recognizes revenue for our services in accordance with ASC 605-10, "Revenue Recognition in Financial Statements." Under these guidelines, revenue is recognized on transactions when all of the following exist: persuasive evidence of an arrangement did exist, delivery of service has occurred, the sales price to the buyer is fixed or determinable and collectability is reasonably assured. The Company has five primary revenue operating classes as follows:

| • | Consulting services. | |

| • | Advertising services. | |

| • | Branding, marketing and selling products for companies. | |

| • | Educational seminars. | |

| • | Selling branded products. |

Stock-Based Compensation. The Company accounts for stock-based instruments issued to employees in accordance with ASC Topic 718. ASC Topic 718 requires companies to recognize in the statement of operations the grant-date fair value of stock options and other equity based compensation issued to employees. The Company accounts for non-employee share-based awards in accordance with ASC Topic 505-50. The value of the portion of an award that is ultimately expected to vest is recognized as an expense over the requisite service periods using the straight-line attribution method. The Company estimates the fair value of each stock option at the grant date by using the Black-Scholes option-pricing model. The Company estimates the fair value of each stock option at the grant date by using the Black-Scholes option-pricing model.

NON-GAAP FINANCIAL MEASURES

Adjusted Net Earnings

In addition to reporting net loss from operations as defined under generally accepted accounting principles (“GAAP”), the Company presents adjusted net earnings from operations (adjusted net earnings), which is a non-GAAP performance measure. Adjusted net earnings consist of net loss from operations after adjustment for those items shown in the table below. Adjusted net earnings does not represent, and should not be considered an alternative to, GAAP measurements such as net loss from operations (its most comparable GAAP financial measure), and the Company’s calculations thereof may not be comparable to similarly titled measures reported by other companies. By eliminating the items shown below, the Company believes that the measure is useful to investors because similar measures are frequently used by securities analysts, investors, and other interested parties in their evaluation of companies. The Company’s management does not view adjusted net earnings in isolation and also uses other measurements, such as net loss from operation and revenues to measure operating performance. The following table provides a reconciliation of net loss from operations, the most directly comparable GAAP measure, to adjusted net earnings for the periods presented:

| Adjusted Net Loss | For the Years Ended | |||||||

| June 30, | ||||||||

| 2017 | 2016 | |||||||

| Net loss | $ | (910,650 | ) | $ | (3,011,220 | ) | ||

| Change in fair value of embedded conversion features | (21,506 | ) | – | |||||

| Beneficial conversion feature expense | (79,156 | ) | (290,174 | ) | ||||

| Adjusted net loss | $ | (809,988 | ) | $ | (2,721,046 | ) | ||

| Weighted average shares outstanding - basic and diluted | 100,294,433 | 171,858,687 | ||||||

| Adjusted basic and diluted net loss per share | $ | (0.01 | ) | $ | (0.02 | ) | ||

| 18 |

Adjusted EBITDA

In addition to reporting net loss from operations as defined under GAAP, the Company also presents adjusted net earnings before interest, income taxes, depreciation, depletion, and amortization from operations (adjusted EBITDA), which is a non-GAAP performance measure. Adjusted EBITDA consists of net loss from operations after adjustment for those items shown in the table below. Adjusted EBITDA does not represent, and should not be considered an alternative to, GAAP measurements such as net loss from operations (its most comparable GAAP financial measure), and the Company’s calculations thereof may not be comparable to similarly titled measures reported by other companies.

By eliminating the items shown below, the Company believes the measure is useful in evaluating its fundamental core operating performance. The Company also believes that adjusted EBITDA is useful to investors because similar measures are frequently used by securities analysts, investors, and other interested parties in their evaluation of companies. The Company’s management uses adjusted EBITDA to manage its business, including in preparing its annual operating budget and financial projections. The Company’s management does not view adjusted EBITDA in isolation and also uses other measurements, such as net loss from operations and revenues to measure operating performance. The following table provides a reconciliation of net loss from operations, the most directly comparable GAAP measure, to adjusted EBITDA for the periods presented:

| Adjusted EBITDA | For the Years Ended | |||||||

| June 30, | ||||||||

| 2017 | 2016 | |||||||

| Net loss from operations | $ | (910,650 | ) | $ | (3,011,220 | ) | ||

| Interest expense | (47,221 | ) | (3,779 | ) | ||||

| Interest income | 7,002 | – | ||||||

| Amortization | (741 | ) | (515 | ) | ||||

| Stock-based compensation | (750,990 | ) | (2,258,863 | ) | ||||

| Change in fair value of embedded conversion features | (21,506 | ) | – | |||||

| Beneficial conversion feature expense | (79,156 | ) | (290,174 | ) | ||||

| Adjusted EBITDA | $ | (18,038 | ) | $ | (457,889 | ) | ||

| Weighted average shares outstanding - basic and diluted | 100,294,433 | 171,858,687 | ||||||

| Adjusted basic and diluted net loss per share | $ | (0.00 | ) | $ | (0.00 | ) | ||

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

As the Company is a “smaller reporting company,” this item is inapplicable.

| 19 |

Item 8. Consolidated Financial Statements and Supplementary Data.

Freedom Leaf Inc.

Table of Contents

| 20 |

|

Green & Company, CPAs | |

| A PCAOB Registered Accounting Firm |

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of:

Freedom Leaf Inc.

We have audited the accompanying balance sheets of Freedom Leaf Inc. and subsidiaries as of June 30, 2017 and 2016, and the related statements of operations, changes in shareholders’ equity, and cash flows for the years then ended. These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the consolidated financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall consolidated financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Freedom Leaf Inc. as of June 30, 2017 and 2016, and the results of its operations and its cash flows for the years in the periods ended June 30, 2017 and 2016 in conformity with accounting principles generally accepted in the United States of America.

The accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern. As discussed in Note 3 to the consolidated financial statements, the Company reported a net loss of $910,650 in 2017, and used cash for operating activities of $435,450. At June 30, 2017, the Company had a working capital, shareholders’ equity and accumulated deficit of $467,659, $187,818 and $4,920,988, respectively. These matters raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans as to these matters are also described in Note 3. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ Green & Company CPAs, Inc.

Green & Company CPAs, Inc.

Temple Terrace, Florida

October 19, 2017

| 10320 N 56 th Street, Suite 330 | Temple Terrace, FL 33617 | 813.606.4388 |

| F-1 |

FREEDOM LEAF, INC.

and Subsidiaries

June 30,

| 2017 | 2016 | |||||||||||

| ASSETS | ||||||||||||

| Current assets | ||||||||||||

| Cash | $ | 2,498 | $ | 1,758 | ||||||||

| Accounts receivable | – | 500 | ||||||||||

| Inventory | – | 2,465 | ||||||||||

| Prepaid expense | 1,600 | – | ||||||||||

| Other receivable, net of discount | 637,817 | 2,399 | ||||||||||

| Total current assets | 641,915 | 7,122 | ||||||||||

| Intangible assets, net | 10,820 | 7,464 | ||||||||||

| Other assets | 338,084 | 3,584 | ||||||||||

| Total assets | $ | 990,819 | $ | 18,170 | ||||||||

| LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) | ||||||||||||

| Current liabilities | ||||||||||||

| Convertible notes payable, net of discount | $ | 70,678 | $ | 44,521 | ||||||||

| Notes payable | 3,141 | – | ||||||||||

| Accounts payable | 15,789 | 46,936 | ||||||||||

| Accounts payable to related parties | – | 10,000 | ||||||||||

| Accrued expenses | 31,891 | 29,853 | ||||||||||

| Accrued expenses to related parties | – | 45,000 | ||||||||||

| Derivative liabilities | 52,757 | – | ||||||||||

| Total current liabilities | 174,256 | 176,310 | ||||||||||

| Non-current liabilities | ||||||||||||

| Other payables | 188,075 | – | ||||||||||

| Payable to related party | 290,670 | 126,250 | ||||||||||

| Total non-current liabilities | 478,745 | 126,250 | ||||||||||

| Total liabilities | 653,001 | 302,560 | ||||||||||

| Commitments and contingencies (Note 4) | 150,000 | – | ||||||||||

| Stockholders' equity (deficit) | ||||||||||||

| Preferred stock, $0.001

par value, 10,000,000 shares authorized Series A preferred stock, 1,000,000 shares authorized, 948,022 shares issued and outstanding at June 30, 2017 and 2016, respectively | 948 | 948 | ||||||||||

| Common stock, $0.001 par

value, 500,000,000 shares authorized, 111,101,795 and 94,438,650 shares issued, issuable, and outstanding at June 30, 2017 and 2016, respectively | 111,102 | 94,439 | ||||||||||

| Additional paid-in capital | 4,996,756 | 3,800,699 | ||||||||||

| Unearned stock compensation | – | (170,137 | ) | |||||||||

| Accumulated deficit | (4,920,988 | ) | (4,010,338 | ) | ||||||||

| Total stockholders' equity (deficit) | 187,818 | (284,390 | ) | |||||||||

| Total liabilities and stockholders' equity (deficit) | $ | 990,819 | $ | 18,170 | ||||||||

See accompanying notes to consolidated financial statements.

| F-2 |

FREEDOM LEAF, INC.

and Subsidiaries

Consolidated Statements of Operations

For the Years Ended June 30,

| 2017 | 2016 | |||||||

| Revenue, net | $ | 817,457 | $ | 118,473 | ||||

| Operating expenses | ||||||||

| Direct costs of revenue | 124,290 | 132,381 | ||||||

| General and administrative (includes stock-based compensation of $750,990 and $2,258,863 for the years ended June 30, 2017 and 2016, respectively.) | 1,421,224 | 2,685,025 | ||||||

| Marketing and selling | 41,712 | 18,335 | ||||||

| Operating loss | (769,769 | ) | (2,717,267 | ) | ||||

| Other income (expense) | ||||||||

| Interest expense | (47,221 | ) | (3,779 | ) | ||||

| Interest income | 7,002 | – | ||||||

| Change in fair value of embedded conversion features | (21,506 | ) | – | |||||

| Beneficial conversion feature | (79,156 | ) | (290,174 | ) | ||||

| Net loss | $ | (910,650 | ) | $ | (3,011,220 | ) | ||

| Net loss per share - basic and diluted | $ | (0.01 | ) | $ | (0.02 | ) | ||

| Weighted average number of shares outstanding - basic and diluted | 100,294,433 | 171,858,687 | ||||||

See accompanying notes to consolidated financial statements.

| F-3 |

FREEDOM LEAF, INC.

and Subsidiaries

Consolidated Statement of Shareholders' Deficit

June 30, 2017

| Unearned | ||||||||||||||||||||||||||||||||||||||||

| Common Stock | Stock | Additional | ||||||||||||||||||||||||||||||||||||||

| Preferred Stock | Issuable | Common Stock | Compen- | Paid In | Accumulated | |||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | sation | Capital | Deficit | Total | |||||||||||||||||||||||||||||||

| Balance at June 30, 2015 | – | $ | – | – | $ | – | 174,181,200 | $ | 174,181 | $ | – | $ | 594,130 | $ | (999,118 | ) | $ | (230,807 | ) | |||||||||||||||||||||

| Contributed capital | – | – | – | – | – | – | – | 12,000 | – | 12,000 | ||||||||||||||||||||||||||||||

| Capital contribution (services) | – | – | – | – | – | – | – | 58,500 | – | 58,500 | ||||||||||||||||||||||||||||||

| Beneficial conversion feature | – | – | – | – | – | – | – | 122,500 | – | 122,500 | ||||||||||||||||||||||||||||||

| Issuance of common stock for services | – | – | 960,000 | 960 | 8,685,000 | 8,685 | – | 1,919,355 | – | 1,929,000 | ||||||||||||||||||||||||||||||

| Unearned Stock Comp | – | – | – | – | – | – | (170,137 | ) | – | – | (170,137 | ) | ||||||||||||||||||||||||||||

| Warrants issued for services | – | – | – | – | – | – | – | 500,000 | – | 500,000 | ||||||||||||||||||||||||||||||

| Warrants exercised into common stock | – | – | 2,679,736 | 2,680 | – | – | – | 31,320 | – | 34,000 | ||||||||||||||||||||||||||||||

| Conversion of debt into common stock | – | – | 2,509,914 | 2,510 | 225,000 | 225 | – | 469,040 | – | 471,775 | ||||||||||||||||||||||||||||||

| Conversion of common stock into preferred stock | 948,022 | 948 | – | – | (94,802,200 | ) | (94,802 | ) | – | 93,854 | – | – | ||||||||||||||||||||||||||||

| Net loss for the period ended June 30, 2016 | – | – | – | – | – | – | – | – | (3,011,220 | ) | (3,011,220 | ) | ||||||||||||||||||||||||||||

| Balance at June 30, 2016 | 948,022 | $ | 948 | 6,149,650 | $ | 6,150 | 88,289,000 | $ | 88,289 | $ | (170,137 | ) | $ | 3,800,699 | $ | (4,010,338 | ) | $ | (284,390 | ) | ||||||||||||||||||||

| Contributed capital | – | – | – | – | – | – | – | 21,082 | – | 21,082 | ||||||||||||||||||||||||||||||

| Unearned stock compensation | – | – | – | – | – | – | 170,137 | – | – | 170,137 | ||||||||||||||||||||||||||||||

| Issuance of issuable common stock | – | – | (1,285,000 | ) | (1,285 | ) | 1,285,000 | 1,285 | – | – | – | – | ||||||||||||||||||||||||||||

| Cancellation of issuable shares | – | – | (5,014,650 | ) | (5,015 | ) | – | – | – | (229,842 | ) | – | (234,857 | ) | ||||||||||||||||||||||||||

| Sale of common stock | – | – | – | – | 3,112,501 | 3,113 | – | 146,887 | – | 150,000 | ||||||||||||||||||||||||||||||

| Issuance of common stock for services | – | – | 1,943,195 | 1,943 | 11,479,477 | 11,479 | – | 737,568 | – | 750,990 | ||||||||||||||||||||||||||||||

| Issuance of common stock for debt | – | – | – | – | 1,004,701 | 1,005 | – | 56,182 | – | 57,187 | ||||||||||||||||||||||||||||||

| Issuance of 268,167 warrants | – | – | – | – | – | – | – | 3,319 | – | 3,319 | ||||||||||||||||||||||||||||||

| Beneficial conversion feature | – | – | – | – | – | – | – | 50,000 | – | 50,000 | ||||||||||||||||||||||||||||||

| Issuance of 1,150,000 warrants | – | – | – | – | – | – | – | 68,750 | – | 68,750 | ||||||||||||||||||||||||||||||

| Issuance of common stock for conversion of debt | – | – | – | – | 791,140 | 791 | – | 147,167 | – | 147,959 | ||||||||||||||||||||||||||||||

| Issuance of common stock for acquisition of intellectual property | 3,000,000 | 3,000 | 181,500 | 184,500 | ||||||||||||||||||||||||||||||||||||

| Issuance of common stock for settlement of debt | – | – | – | – | 346,781 | 347 | – | 13,444 | – | 13,791 | ||||||||||||||||||||||||||||||

| Net loss for the period ended June 30, 2017 | – | – | – | – | – | – | – | – | (910,650 | ) | (910,650 | ) | ||||||||||||||||||||||||||||

| Balance at June 30, 2017 | 948,022 | $ | 948 | 1,793,195 | $ | 1,793 | 109,308,600 | $ | 109,309 | $ | – | $ | 4,996,756 | $ | (4,920,988 | ) | $ | 187,818 | ||||||||||||||||||||||

See accompanying notes to consolidated financial statements.

| F-4 |

FREEDOM LEAF, INC.

and Subsidiaries

Consolidated Statements of Cash Flows

For the Years Ended June 30,

| 2017 | 2016 | |||||||

| Cash flows from operating activities: | ||||||||

| Net loss | $ | (910,650 | ) | $ | (3,011,220 | ) | ||

| Adjustments to reconcile net loss to net cash used in operations: | ||||||||

| Amortization of intellectual properties | 741 | 515 | ||||||

| Beneficial conversion feature | 79,156 | 290,174 | ||||||

| Issuance of common stock for services | 750,990 | 2,258,863 | ||||||

| Unearned stock compensation | 170,137 | (170,137 | ) | |||||

| Change in fair value of embedded conversion features | 21,506 | – | ||||||

| Bad debt expense | – | 5,000 | ||||||

| Issuance and amortization of warrants for services | 80,402 | 500,000 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | 500 | (3,020 | ) | |||||

| Inventory | 2,465 | (2,465 | ) | |||||

| Prepaid expense | (1,600 | ) | – | |||||

| Other receivable | (603,805 | ) | (399 | ) | ||||

| Accounts payable | (160,406 | ) | 42,225 | |||||

| Accounts payable to related parties | (10,000 | ) | (17,466 | ) | ||||

| Accrued expenses | 2,038 | 12,099 | ||||||

| Accrued expenses to related parties | 143,075 | 45,000 | ||||||

| Net cash used in operating activities | (435,450 | ) | (50,831 | ) | ||||

| Cash flows used in investing activities | ||||||||

| Intangible asset acquired | (4,312 | ) | (3,235 | ) | ||||

| Net cash used in investing activities | (4,312 | ) | (3,235 | ) | ||||

| Cash flows from financing activities: | ||||||||

| Proceeds from warrants exercised | – | 34,000 | ||||||

| Proceeds from capital contributed | 21,082 | – | ||||||

| Proceeds from related party | 164,420 | 136,815 | ||||||

| Proceeds from sale of common stock | 150,000 | – | ||||||

| Payments on notes payable | (25,000 | ) | ||||||

| Issuance of common stock on conversion of debt | – | (225,892 | ) | |||||

| Proceeds from notes payable | 130,000 | 110,000 | ||||||

| Net cash provided by financing activities | 440,502 | 54,923 | ||||||

| Net increase in cash | 740 | 857 | ||||||

| Cash at beginning of period | 1,758 | 901 | ||||||

| Cash at end of period | $ | 2,498 | $ | 1,758 | ||||

| Supplemental disclosure of cash flow information: | ||||||||

| Cash paid for interest | $ | 13,400 | $ | – | ||||

| Cash paid for taxes | $ | – | $ | – | ||||

| Non-cash investing and financing activities: | ||||||||

| Conversion of debt into common stock | $ | 239,026 | $ | 471,775 | ||||

| Conversion of common stock into licensing agreement | $ | (10,209 | ) | $ | – | |||

| Issuance of common stock for deposit on acquisition | $ | (184,500 | ) | $ | – | |||

| Contingent liability for deposit on acquisition | $ | (150,000 | ) | $ | – | |||

| Issuance of common stock in settlement of accounts payable | $ | 72,069 | $ | – | ||||

| Derivatives liability | $ | 286,504 | $ | – | ||||

See accompanying notes to consolidated financial statements.

| F-5 |

Freedom Leaf Inc.

and Subsidiaries

Notes to Consolidated Financial Statements

June 30, 2017

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Freedom Leaf Inc. (the “Company,” “we,” “us,” “our,” or “Freedom Leaf”) was incorporated in the State of Nevada on February 21, 2013, under the name of Arkadia International, Inc. The Company was originally engaged in the business of the acquisition of in demand equipment, cars, and goods with the intent to resale these in the U.S. territory or export to overseas countries.

On October 3, 2014, the Company experienced a change in control. Richard C. Cowan acquired a majority of the issued and outstanding common stock of the Company in accordance with stock purchase agreements by and between Mr. Cowan and Vladimir and Galina Shekhtman (“Sellers”). On the closing date, October 3, 2014, pursuant to the terms of the agreements with the Sellers, Cowan purchased from the Sellers 6,950,100 shares of the Company’s outstanding restricted common stock for $100,000, representing 93% of the then-outstanding common stock of the Company.

On November 6, 2014, the Company merged with Freedom Leaf Inc., a private Nevada corporation (“Private Company”). The Company changed its name from Arkadia International, Inc., to Freedom Leaf Inc. As a result of the merger, the Private Company was dissolved. See Note 2 for related discussion.

For financial reporting purposes, the acquisition of the Private Company via the merger transaction represents a "reverse merger" rather than a business combination, and Private Company is deemed to be the accounting acquirer in the transaction. The merger is being accounted for as a reverse-merger and recapitalization. Private Company is treated as the acquirer for financial reporting purposes, and the predecessor public company (Freedom Leaf Inc., f/k/a Arkadia International, Inc.) is treated as the acquired company. Consequently, the assets and liabilities and the operations that are reflected in the historical consolidated financial statements of the Company prior to the merger are those of the Private Company, and were recorded at the historical cost basis of the Private Company, and the consolidated financial statements after completion of the merger include the assets and liabilities of both the predecessor public company and Private Company, the historical operations of Private Company, and the operations of both companies from the date of the merger.

Cannabis Business Solutions Inc. (“Cannabis Business Solutions”), a Nevada corporation, was formed on February 5, 2014, and is a wholly-owned subsidiary of the Company. This subsidiary had no activity until the agreement with Valencia Web Technology S.L., B-97183354 (see Note 2).

Leafceuticals Inc. (“Leafceuticals”), formerly known as Cannabiz U, Inc., a Nevada corporation, was formed on February 13, 2014, and is a wholly-owned subsidiary of the Company. This subsidiary has had no activity to date.

Freedom Leaf Cares Inc. (“Freedom Leaf Cares”), a Nevada corporation, was formed on October 1, 2014, and is a wholly-owned subsidiary of the Company. Freedom Leaf Cares was dissolved in 2016. Until dissolution, this subsidiary had no activity.