Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Rimini Street, Inc. | v468117_8k.htm |

Exhibit 99.1

1 Property of Rimini Street © 2017 1 Rimini Street, Inc. Investor Presentation May 31, 2017

Property of Rimini Street © 2017 2 “Rimini Street” is a registered trademark of Rimini Street, Inc., and Rimini Street, the Rimini Street logo, and combinations th ereof, and other marks marked by TM are trademarks of Rimini Street, Inc. ("Rimini“, the “Company”). All other trademarks remain the property of their respective owners, and unless otherwise specified, Rimini claims no affiliation, endo rse ment, or association with any such trademark holder or other companies referenced herein. Investor Presentation This communication is for informational purposes only and has been prepared to assist interested parties in making their own eva luation with respect to the proposed potential business combination between Rimini and GP Investments Acquisition Corp. (“GPIAC ”) and related transactions and for no other purpose. The information contained herein does not purport to be all - inclusive. The data contained herein is derived from various internal and external sources. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any project ion s, modelling or back - testing or any other information contained herein. Any data on past performance, modeling or back - testing contained herein is no indication as to future performance. Neither Rimini nor GPIAC assumes any obligation to update the information in this communication. Forward Looking Statements Certain statements included in this communication are not historical facts but are forward - looking statements for purposes of th e safe harbor provisions under The Private Securities Litigation Reform Act of 1995. Forward - looking statements generally are accompanied by words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect, ” “ should,” “would,” “plan,” “predict,” “potential,” “seem,” “seek,” “future,” “outlook,” and similar expressions are intended to identify forward - looking statements. These forward - looking statements include, but are not limited to, statements re garding 2017 and 2018 revenue estimates and forecasts of other financial and performance metrics, projections of customer savings, projections of market opportunity, and the expected benefits of the proposed business combination. These st ate ments are based on various assumptions and on the current expectations of GPIAC and Rimini management and are not predictions of actual performance. These forward - looking statements are subject to a number of risks and uncertainties, including adverse litigation developments; the inability to refinance existing debt on favorable terms; GPIAC’s and Rimini’s respective businesses and the proposed potential transaction; the loss of one or more members of GPIAC’s or Rimini’s management team; the inability of the parties to successfully or timely consummate the proposed potential transaction, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to unanti cip ated conditions that could adversely affect the combined company or the expected benefits of the proposed potential transaction or that the approval of the stockholders of GPIAC and/or the stockholders of Rimini for the transaction is not obtained; failure to realize the anticipated benefits of the pro po sed potential transaction, including as a result of a delay in consummating the proposed potential transaction or a delay or difficulty in integrating the businesses of GPIAC and Rimini; uncertainty as to the long - term value of GPIAC common stock; those discussed in GPIAC’s Annual Report on Form 10 - K for the year ended December 31, 2016 under the heading “Risk Factors,” as updated from time to time by GPIAC’s Quarterly Reports on Form 10 - Q and other documents of GPIAC on file or to be filed with the Securities and Exchange Commission (“SEC”). If the risks materialize or our assumptions prove incorrect, actual results could differ materially from the results im plied by these forward - looking statements. There may be additional risks that neither GPIAC nor Rimini presently know or that GPIAC and Rimini currently believe are immaterial that could also cause actual results to differ from those contained in the forwar d - looking statements. In addition, forward - looking statements provide GPIAC’s and Rimini’s expectations, plans or forecasts of future events and views as of the date of this communication. GPIAC and Rimini anticipate that subsequent events and developments will cause GPIAC’s and Rimini’s assessments to change. However, while GPIAC and Rimini may elect to update these forward - looking statements at some point in the future, GPIAC and Rimini specifically disclaim any obligation to do so. These forward - looking statements should not be relied upon as represe nting GPIAC’s and Rimini’s assessments as of any date subsequent to the date of this communication. No Offer or Solicitation This communication does not constitute an offer to sell or a solicitation of an offer to buy, or the solicitation of any vote or approval in any jurisdiction in connection with a proposed potential business combination between Rimini and GPIAC or any related transactions, nor shall there be any sale, issuance or transfer of securities in any jurisdiction where, or to an y p erson to whom, such offer, solicitation or sale may be unlawful. Legal Notice

Property of Rimini Street © 2017 3 Important Information for Investors and Stockholders In connection with the transactions referred to in this communication, GPIAC expects to file a registration statement on Form S - 4 w ith the SEC containing a preliminary joint proxy statement of GPIAC and Rimini Street that also constitutes a preliminary prospectus of GPIAC. After the registration statement is declared effective GPIAC and Rimini will mail a definiti ve joint proxy statement/prospectus to stockholders of GPIAC and stockholders of Rimini Street. This communication is not a substitute for the joint proxy statement/prospectus or registration statement or for any other document that GPIAC may file with the SEC and sen d t o GPIAC's stockholders and/or Rimini Street's stockholders in connection with the proposed transactions. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS AND OTHER DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain free copies of the joint proxy statement/prospectus (when available) and other documents filed with the SEC by GPIAC through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by GPIAC are avai lab le free of charge by contacting GPIAC at 150 E. 52nd Street, Suite 5003, New York, New York 10022, Attn: Investor Relations. Participants in the Solicitation GPIAC and Rimini Street and their respective directors and certain of their respective executive officers may be considered partici pan ts in the solicitation of proxies with respect to the proposed transactions under the rules of the SEC. Information about the directors and executive officers of GPIAC is set forth in its Annual Report on Form 10 - K for the year ende d December 31, 2016, which was filed with the SEC on March 16, 2017. Additional information regarding the participants in the proxy solicitations and a description of their direct and indirect interests, by security holdings or otherwise, will be included in the joint proxy statement/prospectus and other relevant materials to be filed with the SEC when they become available. These documents can be obtained free of charge from the sources indicated above. Non - GAAP Financial Measures This communication includes non - GAAP financial measures, including EBITDA and Adjusted EBITDA, which are supplemental measures o f performance that are neither required by, nor presented in accordance with, U.S. generally accepted accounting principles ("GAAP"). EBITDA is calculated as earnings before interest and taxes plus depreciation and amortizatio n. Adjusted EBITDA is calculated as EBITDA, excluding the impact of certain items that Rimini management does not consider representative of its ongoing operating performance. A reconciliation of such non - GAAP financial measures to GAAP fina ncial measures is included as an appendix hereto. Rimini and GPIAC believe that such non - GAAP financial measures provide useful supplemental information to their respective board of directors, management teams and investors regarding certain financial and business trends relating to Rimini's financial condition and results of operation. Rimini and GPIAC believe such measures, when viewed in conjunction with its consolidated financial statements, consistency and comparability w it h Rimini’s past financial performance, facilitate period - to - period comparisons of operating performance and may facilitate comparisons with other companies. Undue reliance should not be placed on these measures as Rimini's only measures of operating performance, nor should such measures be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP. N on - GAAP financial measures as used in respect of Rimini may not be comparable to similarly titled amounts used by other companies. Legal Notice (Continued)

Property of Rimini Street © 2017 4 Presenters Seth Ravin Founder, Chairman, & CEO Thomas Sabol SVP, CFO

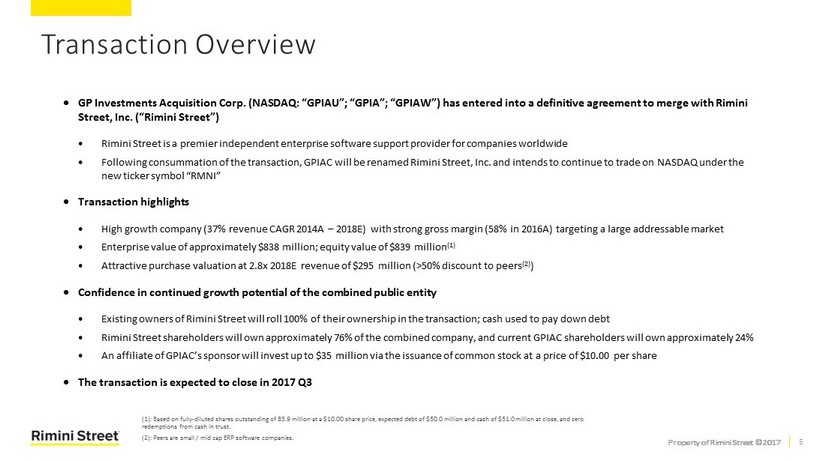

Property of Rimini Street © 2017 5 GP Investments Acquisition Corp. (NASDAQ: “GPIAU”; “GPIA”; “GPIAW”) has entered into a definitive agreement to merge with Rim ini Street, Inc. (“Rimini Street”) Rimini Street is a premier independent enterprise software support provider for companies worldwide Following consummation of the transaction, GPIAC will be renamed Rimini Street, Inc. and intends to continue to trade on NASDAQ under the new ticker symbol “ RMNI” Transaction highlights High growth company (37% revenue CAGR 2014A – 2018E) with strong gross margin (58% in 2016A) targeting a large addressable marke t Enterprise value of approximately $838 million; equity v alue of $839 million (1) Attractive purchase valuation at 2.8x 2018E revenue of $295 million (>50 % discount to peers (2) ) Confidence in continued growth potential of the combined public entity Existing owners of Rimini Street will roll 100% of their ownership in the transaction; cash used to pay down debt Rimini Street shareholders will own approximately 76% of the combined company, and current GPIAC shareholders will own approximately 24% An affiliate of GPIAC’s sponsor will invest up to $35 million via the issuance of common stock at a price of $10.00 per share The transaction is expected to close in 2017 Q3 Transaction Overview ( 1): Based on fully - diluted shares outstanding of 83.9 million at a $10.00 share price , expected debt of $50.0 million and cash of $51.0 million at close, and zero redemptions from cash in trust. (2): Peers are small / mid cap ERP software companies. 5

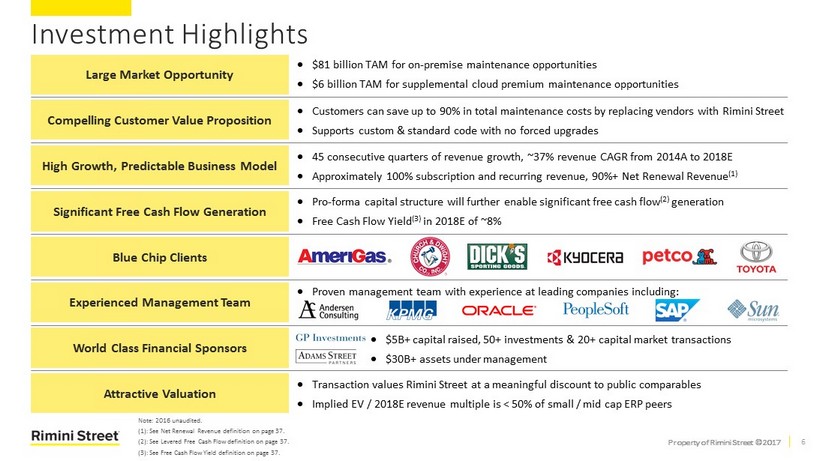

Property of Rimini Street © 2017 6 $ 5B+ capital raised, 50+ investments & 20+ capital market transactions $30B+ assets under management Investment Highlights Large Market Opportunity Compelling Customer Value Proposition High Growth, Predictable Business Model Significant Free Cash Flow Generation Blue Chip Clients Experienced Management Team World Class Financial Sponsors Attractive Valuation $81 billion TAM for on - premise maintenance opportunities $6 billion TAM for supplemental cloud premium maintenance opportunities Customers can save up to 90% in total maintenance costs by replacing vendors with Rimini Street Supports custom & standard code with no forced upgrades 45 consecutive quarters of revenue growth , ~37% revenue CAGR from 2014A to 2018E Approximately 100% subscription and recurring revenue, 90%+ Net R enewal R evenue (1) Pro - forma capital structure will further enable significant f ree cash flow (2 ) generation Free Cash F low Yield (3) in 2018E of ~ 8 % Proven management team with experience at leading companies including: Note: 2016 unaudited. (1): See Net Renewal Revenue definition on page 37. (2): See Levered Free Cash Flow definition on page 37. ( 3 ): See Free Cash Flow Yield definition on page 37. Transaction values Rimini Street at a meaningful discount to public comparables Implied EV / 2018E revenue multiple is < 50% of small / mid cap ERP peers

Property of Rimini Street © 2017 7 Company Overview

Property of Rimini Street © 2017 8 $85 $118 $160 $220 $295 0 50 100 150 200 250 300 $350 2014A 2015A 2016A 2017E 2018E Revenue (US$ in millions) Company Snapshot Founded: 2005 Global Headquarters: Las Vegas, NV Employees: 900+ Active Clients: 1,200+ Global Offices : Beijing, Bengaluru , Frankfurt, Hong Kong, Hyderabad, London, Melbourne, New York , Osaka, Paris, San Francisco Bay Area, São Paulo , Seoul , Singapore, Stockholm, Sydney, Tel Aviv and Tokyo Strong Growth Profile Multiple Products Supported Global Platform Rimini Street is a premier independent enterprise software support provider for companies worldwide Note: 2016 unaudited. Diversified Revenue Sources 36% 19% 14% 12% 10% 9% Manufacturing Services Healthcare & Retail Public Sector & Education TMT Distribution & Transportation 74% 15% 8% 3% North America Europe APAC LATAM By Industry (# Clients) By Geography ($ Value)

Property of Rimini Street © 2017 9 Highly - Experienced Management Team Thomas Shay SVP & CIO Seth Ravin Founder & CEO Daniel B. Winslow SVP & General Counsel David Rowe SVP & CMO Sebastian Grady President Kevin Maddock SVP, Global Sales Nancy Lyskawa SVP, Global Client Onboarding Thomas Sabol SVP, CFO Brian Slepko SVP , Global Service Delivery

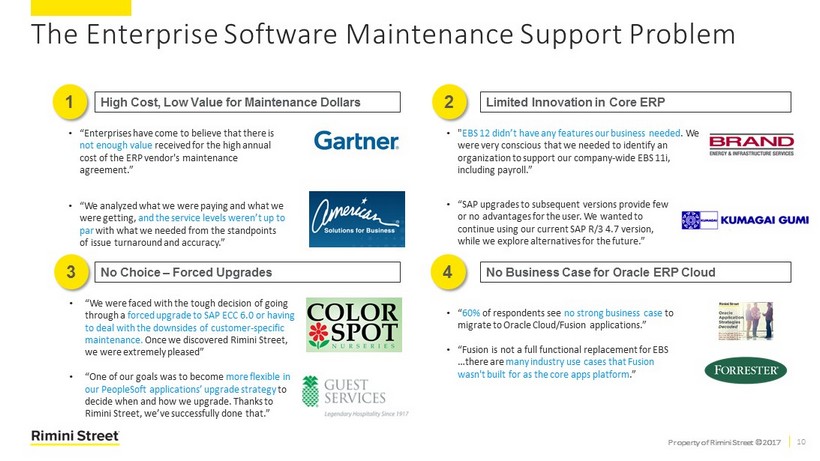

Property of Rimini Street © 2017 10 • “SAP upgrades to subsequent versions provide few or no advantages for the user. We wanted to continue using our current SAP R/3 4.7 version, while we explore alternatives for the future.” • “We were faced with the tough decision of going through a forced upgrade to SAP ECC 6.0 or having to deal with the downsides of customer - specific maintenance. Once we discovered Rimini Street, we were extremely pleased” • “One of our goals was to become more flexible in our PeopleSoft applications’ upgrade strategy to decide when and how we upgrade. Thanks to Rimini Street, we’ve successfully done that.” • “ 60% of respondents see no strong business case to migrate to Oracle Cloud/Fusion applications.” • “Fusion is not a full functional replacement for EBS …there are many industry use cases that Fusion wasn't built for as the core apps platform .” High Cost, Low Value for Maintenance Dollars Limited Innovation in Core ERP No Choice – Forced Upgrades No Business Case for Oracle ERP Cloud 1 • “Enterprises have come to believe that there is not enough value received for the high annual cost of the ERP vendor's maintenance agreement.” • “We analyzed what we were paying and what we were getting, and the service levels weren’t up to par with what we needed from the standpoints of issue turnaround and accuracy .” 2 3 4 • " EBS 12 didn’t have any features our business needed . We were very conscious that we needed to identify an organization to support our company - wide EBS 11i, including payroll.” The Enterprise Software Maintenance Support Problem

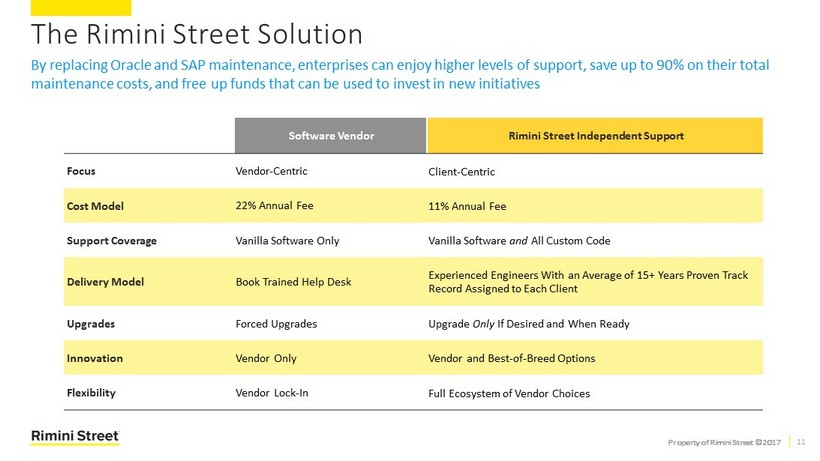

Property of Rimini Street © 2017 11 The Rimini Street Solution Software Vendor Rimini Street Independent Support Focus Vendor - Centric Client - Centric Cost Model 22% Annual Fee 11% Annual Fee Support Coverage Vanilla Software Only Vanilla Software and All Custom Code Delivery Model Book Trained Help Desk Experienced Engineers With an Average of 15+ Years Proven Track Record Assigned to Each Client Upgrades Forced Upgrades Upgrade Only If Desired and When Ready Innovation Vendor Only Vendor and Best - of - Breed Options Flexibility Vendor Lock - In Full Ecosystem of Vendor Choices By replacing Oracle and SAP maintenance, enterprises can enjoy higher levels of support, save up to 90% on their total maintenance costs, and free up funds that can be used to invest in new initiatives

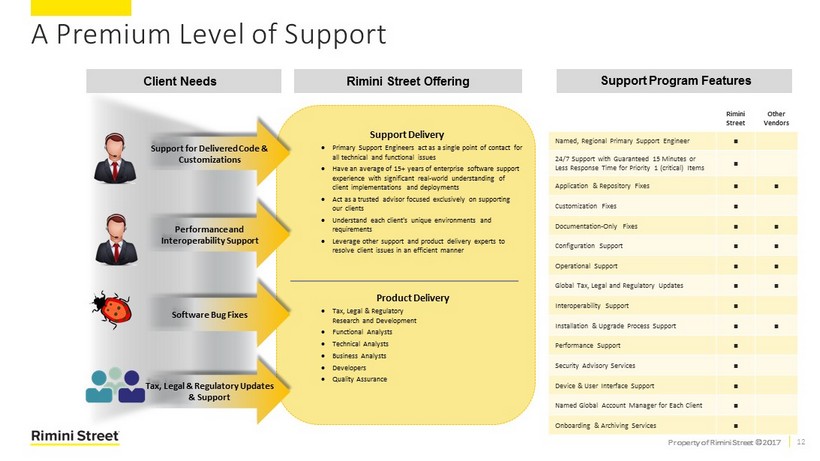

Property of Rimini Street © 2017 12 A Premium Level of Support Product Delivery Tax, Legal & Regulatory Research and Development Functional Analysts Technical Analysts Business Analysts Developers Quality Assurance Support Delivery Primary Support Engineers act as a single point of contact for all technical and functional issues Have an average of 15+ years of enterprise software support experience with significant real - world understanding of client implementations and deployments Act as a trusted advisor focused exclusively on supporting our clients Understand each client's unique environments and requirements Leverage other support and product delivery experts to resolve client issues in an efficient manner Support for Delivered Code & Customizations Tax, Legal & Regulatory Updates & Support Performance and Interoperability Support Rimini Street Offering Client Needs Software Bug Fixes Rimini Street Other Vendors Named, Regional Primary Support Engineer ■ 24/7 Support with Guaranteed 15 Minutes or Less Response Time for Priority 1 (critical) I tems ■ Application & Repository Fixes ■ ■ Customization Fixes ■ Documentation - Only Fixes ■ ■ Configuration Support ■ ■ Operational Support ■ ■ Global Tax, Legal and Regulatory Updates ■ ■ Interoperability Support ■ Installation & Upgrade Process Support ■ ■ Performance Support ■ Security Advisory Services ■ Device & User Interface Support ■ Named Global Account Manager for Each Client ■ Onboarding & Archiving Services ■ Support Program Features

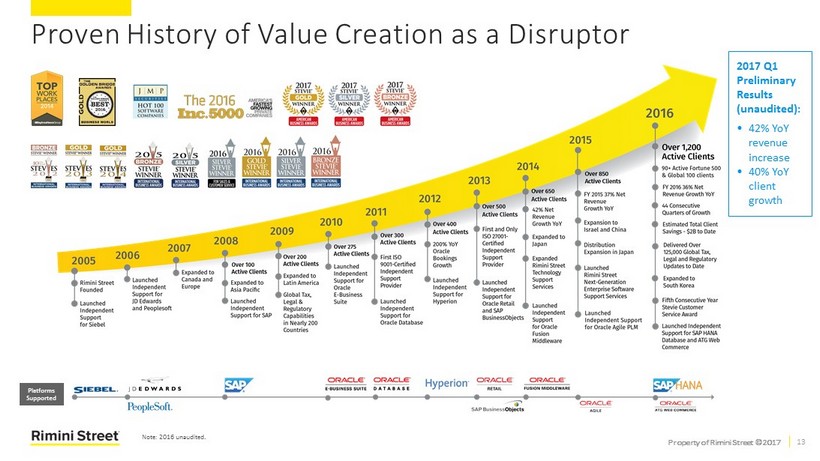

Property of Rimini Street © 2017 13 Proven History of Value Creation as a Disruptor 2017 Q1 Preliminary Results (unaudited): • 42% YoY revenue increase • 40% YoY client growth Platforms Suppor t e d Note: 2016 unaudited .

Property of Rimini Street © 2017 14 Diversified Blue - Chip Client Base Currently serving a large, growing, and diversified global client base (including many Fortune 500 & Global 100) Manufacturing & Transportation Services Public Sector & Education Healthcare & Retail Technology, Media, & Telecom ` ` ` `

Property of Rimini Street © 2017 15 • Upgrade Support & Best Practices • Engineers with 15 + Average Years Experience • Highly Compensated Engineers • Accelerate Globalization • Avoid Business Disruption • Capabilities for ~ 200 Countries • Expand License Rights • Purchase New Products • Mergers & Acquisitions • Invest in Systems of Engagement • Choose Best of Breed Solutions • Better Functionality, Lower Cost • Migrate HW/OS/MW/DB • Upgrade OS/DB/MW/Browsers • Add Mobile Devices Rimini Street: A Long - Term Partner for Clients Clients continue evolving, expanding and innovating their organizations and systems under Rimini Street Support Perform Upgrades Expand Capabilities Change Infrastructure Roll - Out Globally Innovate with Hybrid IT Over 150 Upgrades Support 120+ Countries Licenses and Products Run 15+ More Years Innovate Around Edges Use Cases for Growth with Clients

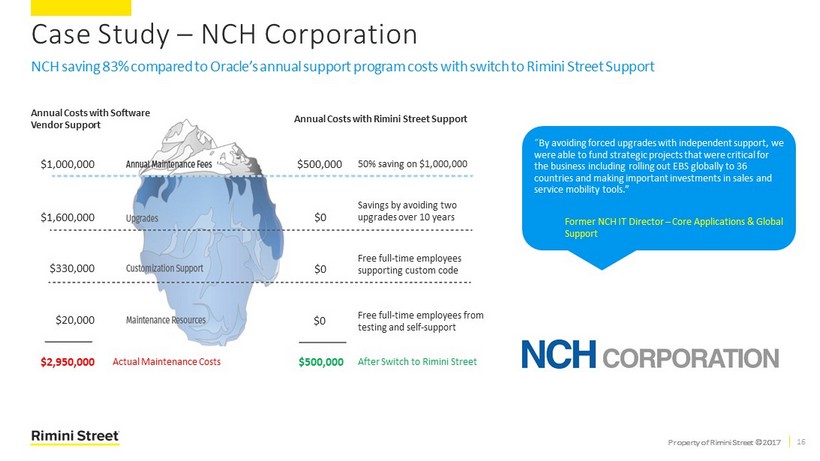

Property of Rimini Street © 2017 16 Case Study – NCH Corporation NCH saving 83% compared to Oracle’s annual support program costs with switch to Rimini Street Support $1,000,000 $1,600,000 $330,000 $20,000 $0 $0 $0 $500,000 $3,000,000 50% saving on $1,000,000 Savings by avoiding two upgrades over 10 years Free full - time employees supporting custom code Free full - time employees from testing and self - support Annual Costs with Rimini Street Support Annual Costs with Software Vendor Support “ By avoiding forced upgrades with independent support, we were able to fund strategic projects that were critical for the business including rolling out EBS globally to 36 countries and making important investments in sales and service mobility tools.” Former NCH IT Director – Core Applications & Global Support $2,950,000 $500,000 After Switch to Rimini Street Actual Maintenance Costs

Property of Rimini Street © 2017 17 Overview of Market Opportunity

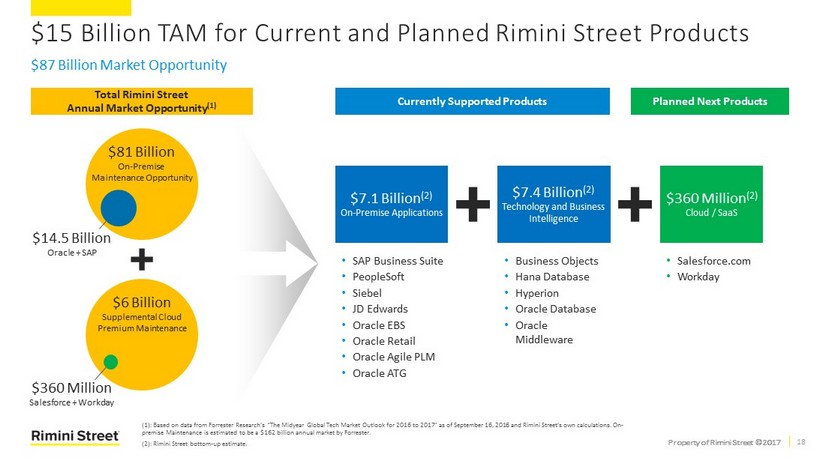

Property of Rimini Street © 2017 18 $ 87 Billion Market Opportunity $ 15 Billion TAM for Current and Planned Rimini Street Products $14.5 Billion Oracle + SAP Total Rimini Street Annual Market Opportunity (1) Currently Supported Products $360 Million (2) Cloud / SaaS • SAP Business Suite • PeopleSoft • Siebel • JD Edwards • Oracle EBS • Oracle Retail • Oracle Agile PLM • Oracle ATG • Business Objects • Hana Database • Hyperion • Oracle Database • Oracle Middleware • Salesforce.com • Workday Planned Next Products $360 Million Salesforce + Workday (1): Based on data from Forrester Research’s “The Midyear Global Tech Market Outlook for 2016 to 2017” as of September 16, 20 16 and Rimini Street’s own calculations. On - premise Maintenance is estimated to be a $162 billion annual market by Forrester. (2): Rimini Street bottom - up estimate. $7.1 Billion (2) On - Premise Applications $7.4 Billion (2) Technology and Business Intelligence $81 Billion On - Premise Maintenance Opportunity $6 Billion Supplemental Cloud Premium Maintenance

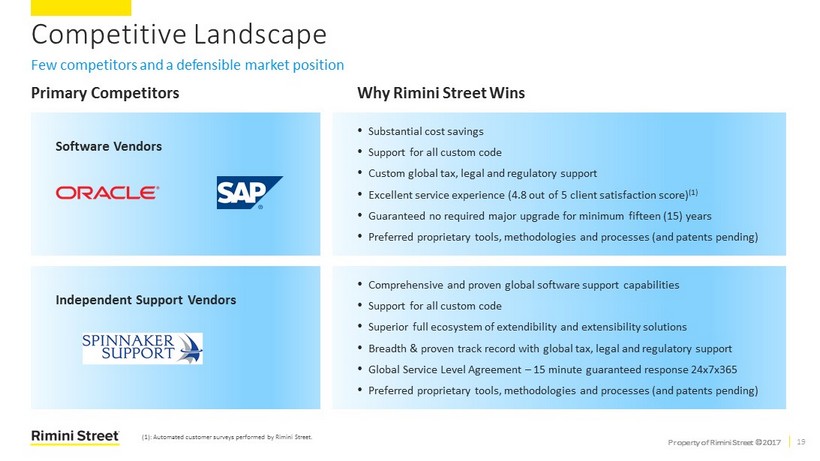

Property of Rimini Street © 2017 19 Competitive Landscape Independent Support Vendors Software Vendors Primary Competitors Few competitors and a defensible market position • Substantial cost savings • Support for all custom code • Custom global tax, legal and regulatory support • Excellent service experience (4.8 out of 5 client satisfaction score) (1 ) • Guaranteed no required major upgrade for minimum fifteen (15) years • Preferred proprietary tools, methodologies and processes (and patents pending ) • Comprehensive and proven global software support capabilities • Support for all custom code • Superior full ecosystem of extendibility and extensibility solutions • Breadth & proven track record with global tax, legal and regulatory support • Global Service Level Agreement – 15 minute guaranteed response 24x7x365 • Preferred proprietary tools, methodologies and processes (and patents pending ) Why Rimini Street Wins (1): Automated customer surveys performed by Rimini Street.

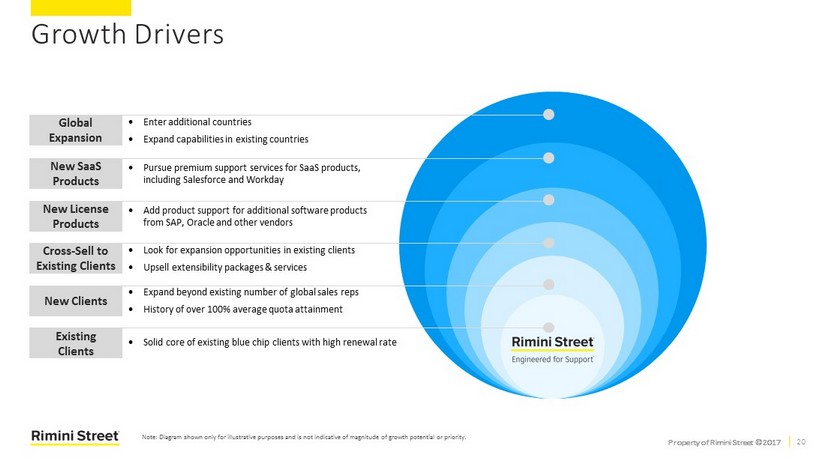

Property of Rimini Street © 2017 20 Growth Drivers Note: Diagram shown only for illustrative purposes and is not indicative of magnitude of growth potential or priority. Global Expansion New SaaS Products New License Products New Clients Existing Clients E nter additional countries Expand capabilities in existing countries Pursue premium support services for SaaS products, including Salesforce and Workday A dd product support for additional software products from SAP, Oracle and other vendors Expand beyond existing number of global sales reps History of over 100% average quota attainment Solid core of existing blue chip clients with high renewal rate Cross - Sell to Existing Clients Look for expansion opportunities in existing clients Upsell extensibility packages & services

Property of Rimini Street © 2017 21 Financial Overview

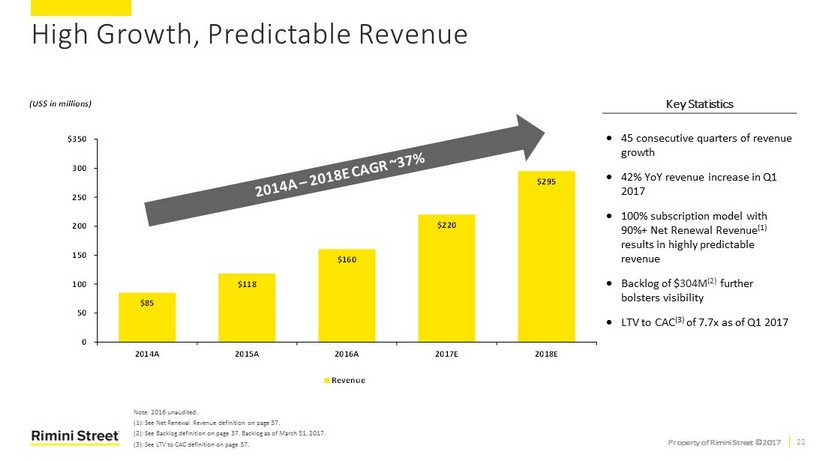

Property of Rimini Street © 2017 22 $85 $118 $160 $220 $295 0 50 100 150 200 250 300 $350 2014A 2015A 2016A 2017E 2018E Revenue (US$ in millions) High Growth, Predictable Revenue Note: 2016 unaudited . (1): See Net Renewal Revenue definition on page 37. (2): See Backlog definition on page 37. Backlog as of March 31, 2017. (3 ): See LTV to CAC definition on page 37. 45 consecutive quarters of revenue growth 42% YoY revenue increase in Q1 2017 100% subscription model with 90 %+ Net Renewal Revenue (1) results in highly predictable revenue Backlog of $ 304M (2) further bolsters visibility LTV to CAC (3) of 7.7x as of Q1 2017 Key Statistics

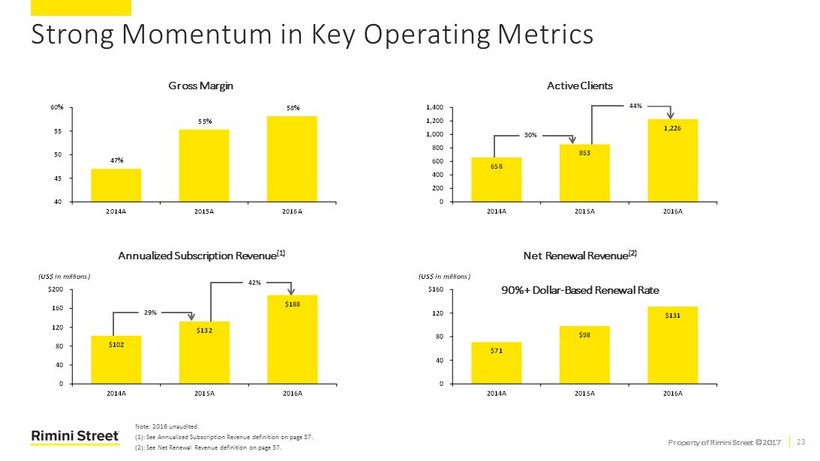

Property of Rimini Street © 2017 23 Strong Momentum in Key Operating Metrics Gross Margin Active Clients Net Renewal Revenue (2) 30% 44% Note: 2016 unaudited. ( 1 ): See Annualized Subscription Revenue definition on page 37. (2): See Net Renewal Revenue definition on page 37. 29% 42% Annualized Subscription Revenue (1) 90 %+ Dollar - Based Renewal Rate $71 $98 $131 0 40 80 120 $160 2014A 2015A 2016A (US$ in millions) $102 $132 $188 0 40 80 120 160 $200 2014A 2015A 2016A (US$ in millions) 47% 55% 58% 40 45 50 55 60% 2014A 2015A 2016A 658 853 1,226 0 200 400 600 800 1,000 1,200 1,400 2014A 2015A 2016A

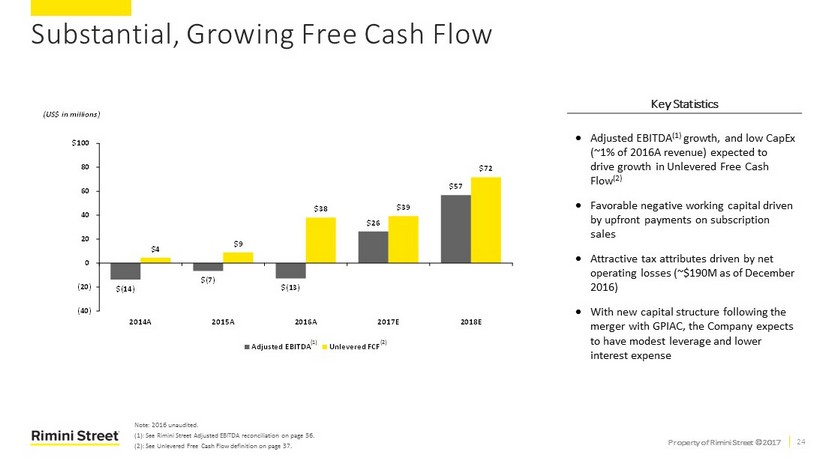

Property of Rimini Street © 2017 24 Substantial, Growing Free Cash Flow Note: 2016 unaudited . ( 1): See Rimini Street Adjusted EBITDA reconciliation on page 36. (2): See Unlevered Free Cash Flow definition on page 37. Adjusted EBITDA (1) growth, and low CapEx (~1% of 2016A revenue) expected to drive growth in Unlevered Free C ash Flow (2) Favorable negative working capital driven by upfront payments on subscription sales Attractive tax attributes driven by net operating losses (~$ 190M as of December 2016 ) With new capital structure following the merger with GPIAC, the Company expects to have modest leverage and lower interest expense Key Statistics (1) (2) $(14) $(7) $(13) $26 $57 $4 $9 $38 $39 $72 (40) (20) 0 20 40 60 80 $100 2014A 2015A 2016A 2017E 2018E Adjusted EBITDA Unlevered FCF (US$ in millions)

Property of Rimini Street © 2017 25 Business Combination Overview

Property of Rimini Street © 2017 26 ( 1): See LTV to CAC definition on page 37. 26 Rimini Street has the size, scale, and leading market position to become a compelling public company. GP has strong conviction in Rimini Street’s continued growth potential as it disrupts and redefines a very large established ERP software maintenance market ▪ Rimini Street’s growth and margin profile, and strong LTV to CAC (1) , are reflective of the Company’s meaningful customer value proposition Rimini Street currently has a debt facility that was utilized to fund a court judgment of $124.4M ▪ Judgment rendered against Rimini Street for verdict of “innocent infringement” and “violation of state computer access laws”; Co urt findings, being appealed, required service delivery process changes for some Rimini Street product lines in 2014 and payment of $124.4M to Or acl e in 2016 ▪ The verdict does not prohibit or restrict Rimini Street from providing support services to any client and the trial validated Rimini Street’s leg al right to offer independent maintenance services for enterprise software products (including Oracle products) ▪ Rimini Street has filed an appeal to overturn the judgment and is seeking return of the full $ 124.4M; expects the appeal to be resolved by the end of 2018 ▪ Rimini Street filed a lawsuit against Oracle in 2014, and Oracle has filed counter - claims. The case is in the “discovery” phase; If not settled or dismissed earlier, this litigation is expected to reach trial in 2020 or 2021 The combination of GPIAC and Rimini Street is expected to allow the Company to reduce debt and associated service costs, and eliminate restrictive covenants associated with the debt The transaction is expected to close in 2017 Q3 Transaction Background

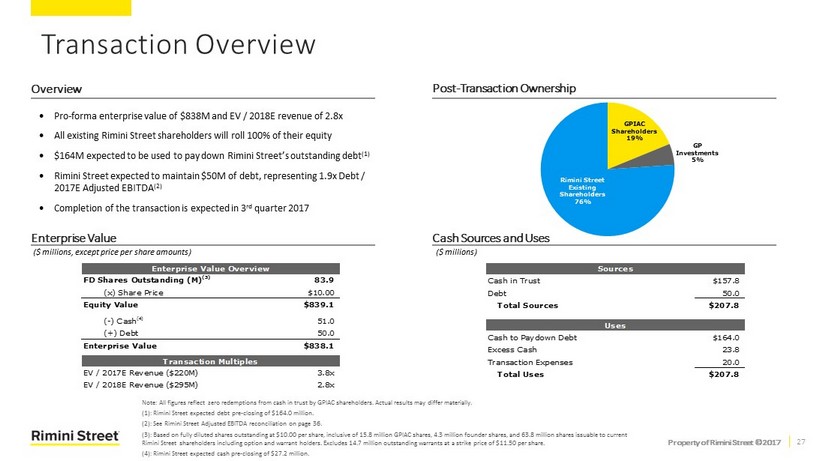

Property of Rimini Street © 2017 27 Pro - forma enterprise value of $ 838M and EV / 2018E revenue of 2.8x All existing Rimini Street shareholders will roll 100% of their equity $ 164M expected to be used to pay down Rimini Street’s outstanding debt (1) Rimini Street expected to maintain $50M of debt, representing 1.9x Debt / 2017E Adjusted EBITDA (2) Completion of the transaction is expected in 3 rd quarter 2017 Post - Transaction Ownership Enterprise Value Overview Cash Sources and Uses ($ millions, except price per share amounts) ($ millions) Note: All figures reflect zero redemptions from cash in trust by GPIAC shareholders . Actual results may differ materially. (1 ): Rimini Street expected debt pre - closing of $164.0 million . (2): See Rimini Street Adjusted EBITDA reconciliation on page 36 . ( 3): Based on fully diluted shares outstanding at $10.00 per share, inclusive of 15.8 million GPIAC shares, 4.3 million founder shares, and 63.8 million shares issuable to current Rimini Street shareholders including option and warrant holders. Excludes 14.7 million outstanding warrants at a strike price of $11.50 per share. (4): Rimini Street expected cash pre - closing of $27.2 million. Property of Rimini Street © 2017 27 Transaction Overview Enterprise Value Overview FD Shares Outstanding (M) (3) 83.9 (x) Share Price $10.00 Equity Value $839.1 (-) Cash (4) 51.0 (+) Debt 50.0 Enterprise Value $838.1 Transaction Multiples EV / 2017E Revenue ($220M) 3.8x EV / 2018E Revenue ($295M) 2.8x GPIAC Shareholders 19% GP Investments 5% Rimini Street Existing Shareholders 76% Sources Cash in Trust $157.8 Debt 50.0 Total Sources $207.8 Uses Cash to Paydown Debt $164.0 Excess Cash 23.8 Transaction Expenses 20.0 Total Uses $207.8

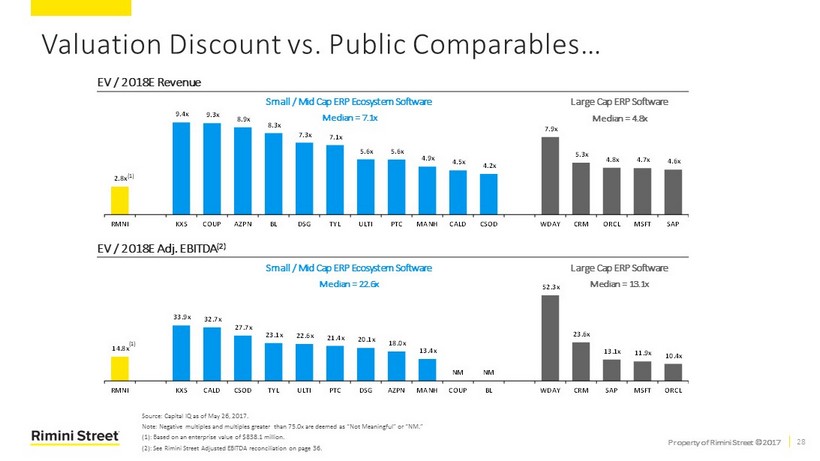

Property of Rimini Street © 2017 28 14.8x 33.9x 32.7x 27.7x 23.1x 22.6x 21.4x 20.1x 18.0x 13.4x NM NM 52.3x 23.6x 13.1x 11.9x 10.4x RMNI KXS CALD CSOD TYL ULTI PTC DSG AZPN MANH COUP BL WDAY CRM SAP MSFT ORCL 2.8x 9.4x 9.3x 8.9x 8.3x 7.3x 7.1x 5.6x 5.6x 4.9x 4.5x 4.2x 7.9x 5.3x 4.8x 4.7x 4.6x RMNI KXS COUP AZPN BL DSG TYL ULTI PTC MANH CALD CSOD WDAY CRM ORCL MSFT SAP Source: Capital IQ as of May 26, 2017. Note: Negative multiples and multiples greater than 75.0x are deemed as “Not Meaningful” or “NM.” (1): Based on an enterprise value of $ 838.1 million. ( 2 ): See Rimini Street Adjusted EBITDA reconciliation on page 36. Valuation Discount vs. Public Comparables … EV / 2018E Revenue EV / 2018E Adj. EBITDA (2) Large Cap ERP Software Small / Mid Cap ERP Ecosystem Software Median = 4.8x Median = 7.1x Large Cap ERP Software Median = 13.1x Median = 22.6x (1) (1) Small / Mid Cap ERP Ecosystem Software

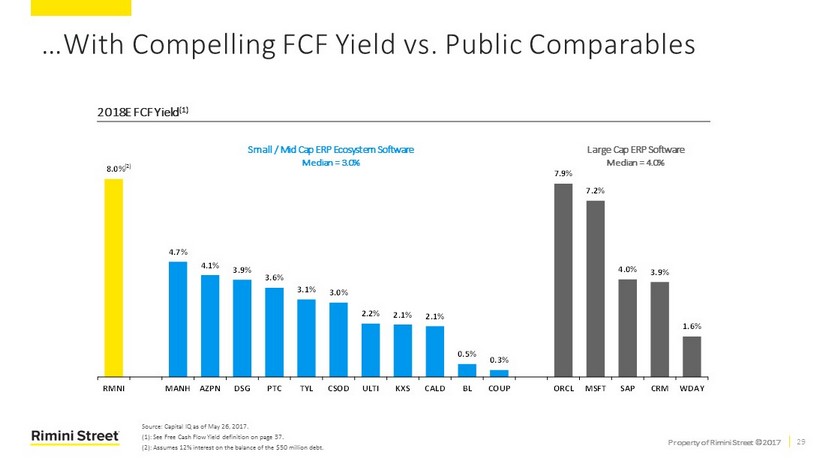

Property of Rimini Street © 2017 29 …With Compelling FCF Yield vs . Public Comparables 2018E FCF Yield (1) Large Cap ERP Software Median = 4.0% Median = 3.0% Source: Capital IQ as of May 26, 2017 . (1): See Free Cash Flow Yield definition on page 37. (2): Assumes 12% interest on the balance of the $50 million debt. Small / Mid Cap ERP Ecosystem Software ( 2) 8.0% 4.7% 4.1% 3.9% 3.6% 3.1% 3.0% 2.2% 2.1% 2.1% 0.5% 0.3% 7.9% 7.2% 4.0% 3.9% 1.6% RMNI MANH AZPN DSG PTC TYL CSOD ULTI KXS CALD BL COUP ORCL MSFT SAP CRM WDAY

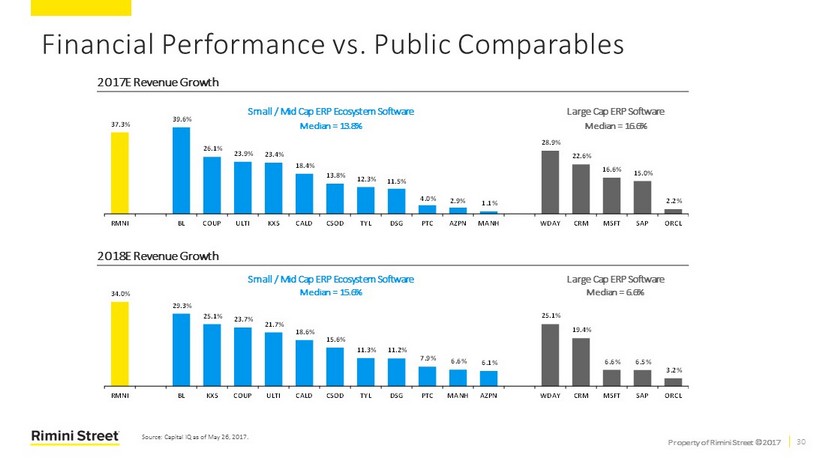

Property of Rimini Street © 2017 30 34.0% 29.3% 25.1% 23.7% 21.7% 18.6% 15.6% 11.3% 11.2% 7.9% 6.6% 6.1% 25.1% 19.4% 6.6% 6.5% 3.2% RMNI BL KXS COUP ULTI CALD CSOD TYL DSG PTC MANH AZPN WDAY CRM MSFT SAP ORCL Financial Performance vs. Public Comparables 2017E Revenue Growth 2018E Revenue Growth Large Cap ERP Software Median = 16.6% Median = 13.8% Large Cap ERP Software Median = 6.6% Median = 15.6% Source: Capital IQ as of May 26, 2017 . Small / Mid Cap ERP Ecosystem Software Small / Mid Cap ERP Ecosystem Software 37.3% 39.6% 26.1% 23.9% 23.4% 18.4% 13.8% 12.3% 11.5% 4.0% 2.9% 1.1% 28.9% 22.6% 16.6% 15.0% 2.2% RMNI BL COUP ULTI KXS CALD CSOD TYL DSG PTC AZPN MANH WDAY CRM MSFT SAP ORCL

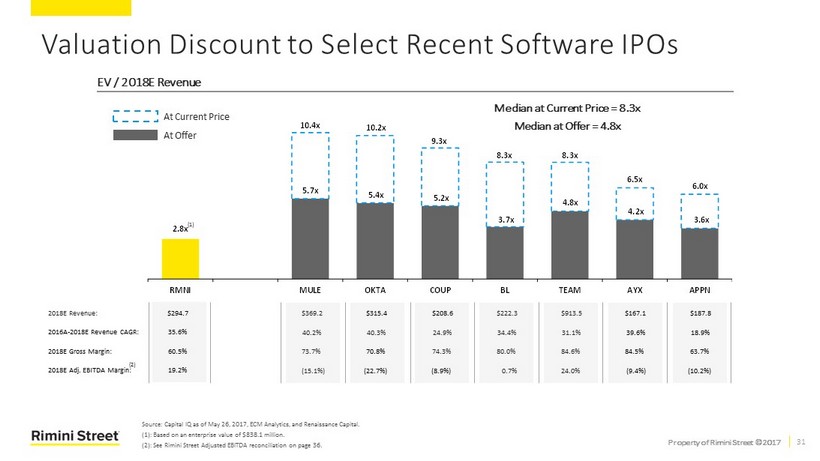

Property of Rimini Street © 2017 31 2.8x 5.7x 5.4x 5.2x 3.7x 4.8x 4.2x 3.6x 10.4x 10.2x 9.3x 8.3x 8.3x 6.5x 6.0x RMNI MULE OKTA COUP BL TEAM AYX APPN Source: Capital IQ as of May 26, 2017, ECM Analytics, and Renaissance Capital. (1): Based on an enterprise value of $ 838.1 million . (2): See Rimini Street Adjusted EBITDA reconciliation on page 36. Valuation Discount to Select Recent Software IPOs EV / 2018E Revenue Median at Offer = 4.8x (1) At Offer At Current Price Median at Current Price = 8.3x 2016A - 2018E Revenue CAGR: 2018E Gross Margin: 2018E Revenue: 2018E Adj. EBITDA Margin: 35.6% 19.2% 60.5% $ 294.7 (2) 40.2% (15.1%) 73.7% $369.2 40.3% (22.7%) 70.8% $ 315.4 24.9% (8.9%) 74.3% $208.6 34.4% 0.7% 80.0% $222.3 31.1% 24.0% 84.6% $913.5 39.6% (9.4%) 84.5% $ 167.1 18.9% (10.2%) 63.7% $187.8

Property of Rimini Street © 2017 32 Top Tier Sponsorship with Long Term Investment Horizons Leader in Alternative Investments Since its foundation in 1993, GP Investments has completed over 50 investments across multiple sectors and over 20 capital markets transactions Over $5 billion raised from investors worldwide and over $1 billion of proprietary capital invested alongside limited partners Long history of partnership with high growth companies and a successful track record in the technology space Focus on value creation through active management and an operationally - oriented approach Antonio Bonchristiano , CEO of GP Investments, was the Founder & CEO of Submarino which was acquired by B2W , one of the largest eCommerce companies in Latin America Private Equity Leadership in Technology S ingle largest shareholder in Rimini Street 45 + year history of private market investments across 30+ countries Currently managing $30+ billion of assets as a firm Adams Street Partners’ direct investment teams have partnered with over 220 entrepreneurs and have invested $1.5+ billion since 1972, intently focusing on the areas of technology and healthcare Adams Street Partners invested in Rimini Street in 2009 and has been a trusted advisor with Robin Murray serving on the Rimini Street board

Property of Rimini Street © 2017 33 Opportunity Summary • Strong and Mature Business with 45 Consecutive Quarters of Growth • Proven Management Team with Strong Execution History • TAM of more than $87 Billion, and Run - Rate Revenues of Nearly $200 Million • Transaction will Significantly Improve Balance Sheet, Reduce Leverage and Position the Company for Accelerated Growth • Transaction at a Meaningful Discount to Market Comparables While Company’s Growth Compares Favorably

Property of Rimini Street © 2017 34

Property of Rimini Street © 2017 35 Appendix

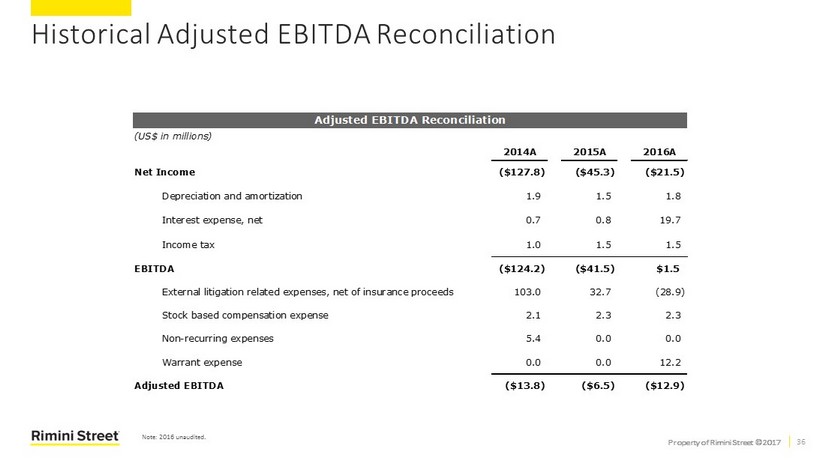

Property of Rimini Street © 2017 36 Historical Adjusted EBITDA Reconciliation Adjusted EBITDA Reconciliation (US$ in millions) 2014A 2015A 2016A Net Income ($127.8) ($45.3) ($21.5) Depreciation and amortization 1.9 1.5 1.8 Interest expense, net 0.7 0.8 19.7 Income tax 1.0 1.5 1.5 EBITDA ($124.2) ($41.5) $1.5 External litigation related expenses, net of insurance proceeds 103.0 32.7 (28.9) Stock based compensation expense 2.1 2.3 2.3 Non-recurring expenses 5.4 0.0 0.0 Warrant expense 0.0 0.0 12.2 Adjusted EBITDA ($13.8) ($6.5) ($12.9) Note: 2016 unaudited.

Property of Rimini Street © 2017 37 • Customer Lifetime Value (LTV): Equal to average gross margin over the forecast period per client multiplied by the average customer life • Customer Acquisition Costs (CAC): Equal to total sales and marketing costs (excludes Global C lient E ngagement expenses) in the TTM period divided by the new clients acquired in the same TTM period • LTV to CAC: Equal to LTV divided by CAC, shows the number of times company able to recover the acquisition costs over the lifetime of the customer • Backlog: Sum of billed ( deferred revenue on balance sheet) and non - cancellable (future revenue not on balance sheet ) • Unlevered Free Cash Flow: Equals Adjusted EBITDA – working capital changes – capital expenditures – cash taxes. Excludes balance sheet impact from debt and litigation • Levered Free Cash Flow: Calculated as Unlevered Free Cash Flow – net interest expense • Free Cash Flow ( FCF ) Yield: Calculated as Levered Free Cash Flow / equity value • Net Renewal Revenue: Calculated as revenue from current clients as of prior year end • Annualized Subscription Revenue: Equal to the annualized amount of 4th quarter revenue Glossary