Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - THOR INDUSTRIES INC | v462138_8k.htm |

Exhibit 99.1

www.thorindustries.com Investor Presentation March 17, 2017

FORWARD LOOKING STATEMENTS This presentation includes certain statements that are “forward looking” statements within the meaning of the U . S . Private Securities Litigation Reform Act of 1995 , Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended . These forward looking statements are made based on management’s current expectations and beliefs regarding future and anticipated developments and their effects upon Thor Industries, Inc . , and inherently involve uncertainties and risks . These forward looking statements are not a guarantee of future performance . We cannot assure you that actual results will not differ from our expectations . Factors which could cause materially different results include, among others, raw material and commodity price fluctuations, raw material or chassis supply restrictions, legislative, regulatory and tax policy developments, the impact of rising interest rates on our operating results, the costs of compliance with increased governmental regulation, legal and compliance issues including those that may arise in conjunction with recent transactions, the potential impact of increased tax burdens on our dealers and retail consumers, lower consumer confidence and the level of discretionary consumer spending, interest rate fluctuations and the potential economic impact of rising interest rates on the general economy, restrictive lending practices, management changes, the success of new product introductions, the pace of obtaining and producing at new production facilities, the pace of acquisitions, the potential loss of existing customers of acquisitions, the integration of new acquisitions, our ability to retain key management personnel of acquired companies, the loss or reduction of sales to key dealers, the availability of delivery personnel, asset impairment charges, cost structure changes, competition, the impact of potential losses under repurchase agreements, the potential impact of the strengthening U . S . dollar on international demand, general economic, market and political conditions and the other risks and uncertainties discussed more fully in ITEM 1 A of our Annual Report on Form 10 - K for the year ended July 31 , 2016 and Part II, Item 1 A of our quarterly report on Form 10 - Q for the period ending January 31 , 2017 . We disclaim any obligation or undertaking to disseminate any updates or revisions to any forward looking statements contained in this presentation or to reflect any change in our expectations after the date of this presentation or any change in events, conditions or circumstances on which any statement is based, except as required by law . 2

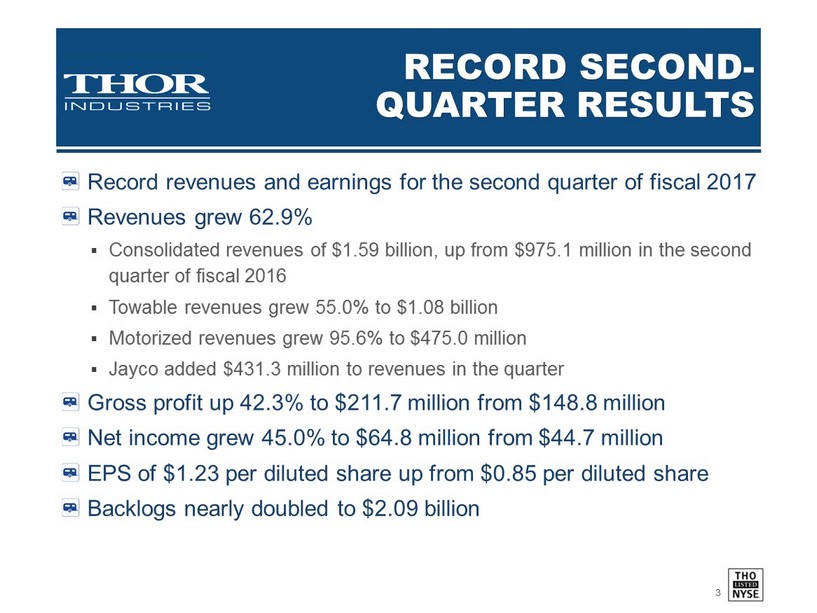

RECORD SECOND - QUARTER RESULTS Record revenues and earnings for the second quarter of fiscal 2017 Revenues grew 62.9% ▪ Consolidated revenues of $1.59 billion, up from $975.1 million in the second quarter of fiscal 2016 ▪ Towable revenues grew 55.0% to $1.08 billion ▪ Motorized revenues grew 95.6% to $475.0 million ▪ Jayco added $431.3 million to revenues in the quarter Gross profit up 42.3% to $211.7 million from $148.8 million Net income grew 45.0% to $64.8 million from $44.7 million EPS of $1.23 per diluted share up from $0.85 per diluted share Backlogs nearly doubled to $2.09 billion 3

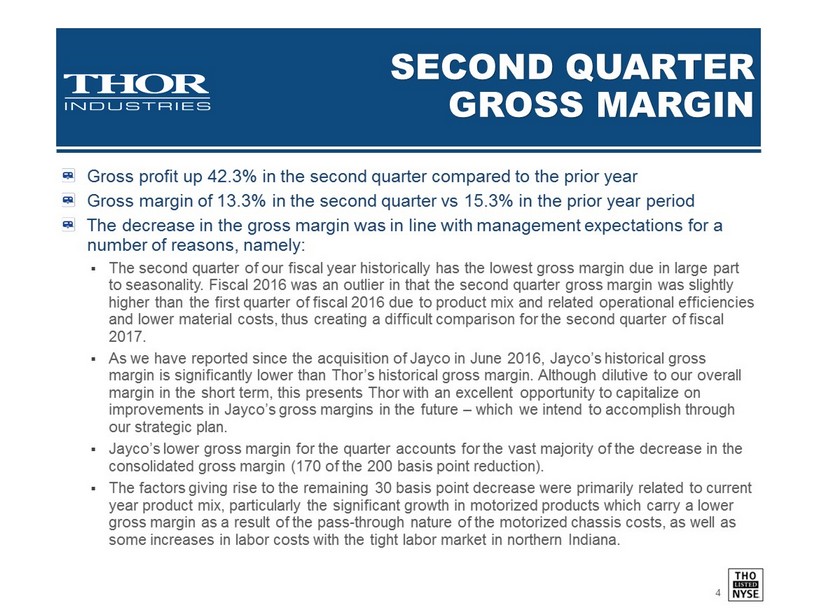

SECOND QUARTER GROSS MARGIN Gross profit up 42.3% in the second quarter compared to the prior year Gross margin of 13.3% in the second quarter vs 15.3% in the prior year period The decrease in the gross margin was in line with management expectations for a number of reasons, namely: ▪ The second quarter of our fiscal year historically has the lowest gross margin due in large part to seasonality. Fiscal 2016 was an outlier in that the second quarter gross margin was slightly higher than the first quarter of fiscal 2016 due to product mix and related operational efficiencies and lower material costs, thus creating a difficult comparison for the second quarter of fiscal 2017. ▪ As we have reported since the acquisition of Jayco in June 2016, Jayco’s historical gross margin is significantly lower than Thor’s historical gross margin. Although dilutive to our overall margin in the short term, this presents Thor with an excellent opportunity to capitalize on improvements in Jayco’s gross margins in the future – which we intend to accomplish through our strategic plan. ▪ Jayco’s lower gross margin for the quarter accounts for the vast majority of the decrease in the consolidated gross margin (170 of the 200 basis point reduction). ▪ The factors giving rise to the remaining 30 basis point decrease were primarily related to current year product mix, particularly the significant growth in motorized products which carry a lower gross margin as a result of the pass - through nature of the motorized chassis costs, as well as some increases in labor costs with the tight labor market in northern Indiana. 4

HEALTHY DEALER INVENTORY LEVELS The modest increase in dealer inventory as of January 31, which was up 12.6% excluding Jayco, is in line with management expectations and reflects the continued strong performance of Thor’s towable and motorized products in the market, particularly our growth in the current sweet spot of the market – affordably priced products in all major product categories. The modest increase in dealer inventory at January 31 is also an indicator of the growth dealers anticipated, and are now realizing, as a result of incredibly strong early season RV shows. Based on numerous dealer checks by various industry sources, dealer confidence is at record high levels and dealer inventory remains fresh, with little aged inventory and modestly improved inventory turnover rates compared to last year. 5

CURRENT CONDITIONS Retail demand remains very strong with many of the spring shows reporting record attendance along with strong sales activity – which is translating to continued strong backlog levels as dealers restock. Marcus Lemonis, CEO of Camping World, the largest RV dealer in America with 13% of the market and Thor’s largest customer, recently said, “…the industry feels as healthy as it ever has right now…” * New consumers, including younger families, are continuing to drive sales growth and the shift toward more affordable travel trailers and smaller motorhomes. We expect these trends will continue and are well positioned to take advantage of them. We also anticipate at least five more years of growth driven by retiring Baby Boomers. We anticipate little adverse impact on demand for RV’s from the recent interest rate hike. 6 * Source: Camping World Fourth Quarter Earnings Conference Call, March 8, 2017

OUTLOOK We are not seeing any signs indicating a peak has been reached nor are we seeing any signs of stress in the sales chain. We expect Jayco will continue to add meaningful growth to both sales and profits for the remainder of fiscal 2017, with additional incremental margin improvements expected in future periods. We anticipate strong top - line growth for the second half of the fiscal year, albeit total revenue growth will likely be lower than the 64.4% top - line growth achieved in the first half of the year due to the following: ▪ We typically have less available capacity in the seasonally strongest half of the year ▪ We will have only 5 incremental months of revenue from Jayco in the second half compared with 6 incremental months of revenues from Jayco in the first half. Our outlook, based on current conditions, dealer sentiment, demographic trends, availability of financing for dealers and consumers at historically low rates and strong retail demand continues to be optimistic. 7

www.thorindustries.com