Attached files

|

Ohio Valley Banc Corp

|

|

Annual Report 2016

|

|

Community

FIRST

|

|

A Message

from

Management

|

Dear Neighbors and Friends,

IMPACT!

The people of YOUR company strove to make a direct and positive impact on their communities in 2016. Together, we expanded our reach with the addition of John Jones and the Milton Banking Company Division. With the merger, we added an experienced crew of community bankers and two new market areas. The bank's assets as of end of year stand proud at approximately $950 million.

And as we grew, we kept loyal to our roots by donating more than $440,000 to local organizations. Fortunately, we weren't satisfied with just handing over checks. We rolled up our sleeves and pitched in with over 2,600 volunteer hours clocked. We did the things that make this place a little more special like building homes with Habitat for Humanity, cleaning and making repairs at Field of Hope, gathering supplies to help those displaced by the flooding in West Virginia, and brightening faces at local senior centers.

We think Donna Casey of Apple Grove said it best. "A bank that is friendly and helpful. OVB not only takes care of its customers, but helps in their communities..."

We think Donna Casey of Apple Grove said it best. "A bank that is friendly and helpful. OVB not only takes care of its customers, but helps in their communities..."

"Community First" isn't just something we say. We put community at the heart of all that we do. Now others are starting to take notice and join the call.

In March 2016, Brent Eastman joined our Board of Directors. Mr. Eastman is President and Co-Owner of Ohio Valley Supermarkets. You may recall that his father, Bob Eastman, dedicated many years to the very same board.

Our newest director brought with him the business knowledge that was passed to him by his father and enhances it with his own penchant for modern tactics in marketing and strategy. And while it's true that he is an outstanding local business leader, he also serves as a role model to our employees by example. His own devoted service to the Gallia County Agricultural Society and Gallia County Jr. Fair Board sets the bar for our bankers as they strive to do more for their hometowns.

As we close the books on 2016, join us in saying "Congratulations" to the friendly professionals at Loan Central who in 2016 celebrated 20 years in business. We also honor the bankers of the OVB Main Office on the office's 55th anniversary as well as the OVB Jackson Pike Office on their 40th anniversary and our OVB Jackson and OVB Waverly offices on their respective 25th anniversaries. Special mention goes out to OVB Barboursville and the OVB Athens Loan Office upon completion of their first full year.

We look forward to 2017, Ohio Valley Bank's 145th year in business. We also thank you, our shareholders, for your timeless support of this American success story.

Sincerely,

|

Jeffrey E. Smith

|

Thomas E. Wiseman

|

|

Chairman of the Board

|

President and CEO

|

|

Ohio Valley Banc Corp.

|

Ohio Valley Banc Corp.

|

1

Merger

A NEW PARTNER…

On Friday, August 5, 2016, the Milton Banking Company

merged with Ohio Valley Bank, becoming a new division

of OVB. Over the weekend, MBC accounts and loans

were converted to Ohio Valley Bank's computer systems.

Pictured above are a few of the 52 employees

who in just 3 days put in 755 hours to

make the switchover happen as seamlessly as

possible so that it was business as usual by

Monday morning.

To put that in perspective, if one person did

that work alone, he or she would have to

work full-time for 19 weeks (roughly five months)

to achieve what we did as a team in one weekend!

John Jones and Tom Wiseman (pictured right)

were interviewed by University of Rio Grande

President Dr. Michelle Johnston about the

experience. You can find the interview on

the Rio Grande Cable Access channel on YouTube.

2

...A CONTINUING MISSION

"Perhaps the biggest change is

that we will have access to the

resources of Ohio Valley Bank,

allowing us more time

for community service,

more options for lending, and

more internet banking

functionality,"

|

-John Jones to his customers

|

|

just prior to the merger

|

3

2016 Year in Review by the Numbers

|

$441,438

|

Dollars given to local charities, schools, and

organizations through donations and sponsorships.

|

|

|

|

|

2,625.5

|

Hours Ohio Valley Bank and Loan Central

employees actively volunteered in their communities during bank hours.

|

|

|

|

|

940,322

|

Transactions conducted at Ohio Valley Bank offices.

|

| $4,096,380.31 | Deposited via OVB Mobile Deposit with cell phones and tablets. |

|

|

|

| 154,735 | Secure statements and notices delivered electronically. |

| 5 | New, conveniently located offices as part of the Milton Banking Company Division. |

4

|

4,744

|

Times customers trusted

Loan Central with their tax needs.

|

|

|

|

|

$284,552.03

|

Paid in rewards to customers using their

OVB Credit Card for purchases.

|

|

|

|

|

$686,069.19

|

Cash back earned by OVB Rewards Checking

accountholders.

|

| 92,000 | Bills paid via free OVB Online Bill Pay |

|

|

|

| 20 | Locally themed debit cards that give back

to the community.

|

| 4 in every 5 |

Ohio Valley Bank customers say they are extremely likely to recommend

OVB to a friend, according to customer surveys.

|

5

|

OVBC DIRECTORS

Jeffrey E. Smith

Chairman, Ohio Valley Banc Corp. and Ohio Valley Bank

Thomas E. Wiseman

President & CEO, Ohio Valley Banc Corp. and Ohio Valley Bank

David W. Thomas, Lead Director

Former Chief Examiner, Ohio Division of Financial Institutions

bank supervision and regulation

Steven B. Chapman

Retired Certified Public Accountant

Anna P. Barnitz

Treasurer & CFO, Bob's Market & Greenhouses, Inc.

wholesale horticultural products and retail landscaping stores

Brent A. Saunders

Chairman of the Board, Holzer Health System

Attorney, Halliday, Sheets & Saunders

healthcare

Harold A. Howe

Self-employed, Real Estate Investment and Rental Property

Brent R. Eastman

President and Co-owner, Ohio Valley Supermarkets

Partner, Eastman Enterprises

John G. Jones

President, MBC, Ohio Valley Bank

Kimberly A. Canady, JD

Owner, Canady Farms, LLC

agricultural products and agronomy services

Edward J. Robbins

President & CEO, Ohio Valley Veneer, Inc.

wood harvesting, processing and manufacturing of dry lumber & flooring in Ohio, Kentucky, and Tennessee

|

OVBC OFFICERS

EXECUTIVE OFFICERS

Jeffrey E. Smith, Chairman of the Board

Thomas E. Wiseman, President and Chief Executive Officer

Larry E. Miller, II, Chief Operating Officer and Secretary

Katrinka V. Hart-Harris, Senior Vice President

Scott W. Shockey, Senior Vice President & Chief Financial Officer

Bryan F. Stepp, Vice President

Mario P. Liberatore, Vice President

Cherie A. Elliott, Vice President

Jennifer L. Osborne, Vice President

Tom R. Shepherd, Vice President

Frank W. Davison, Vice President

Bryan W. Martin, Vice President

David K. Nadler, Vice President

Ryan J. Jones, Vice President

Paula W. Clay, Assistant Secretary

Cindy H. Johnston, Assistant Secretary

LOAN CENTRAL OFFICERS

Larry E. Miller, II Chairman of the Board Cherie A. Elliott President

Timothy R. Brumfield Vice President & Secretary

Manager, Gallipolis Office

John J. Holtzapfel Compliance Officer & Manager, Wheelersburg Office

T. Joe Wilson Manager, Waverly Office

Joseph I. Jones Manager, South Point Office

Deborah G. Moore Manager, Jackson Office

Gregory G. Kauffman Manager, Chillicothe Office

WEST VIRGINIA ADVISORY BOARD

Mario P. Liberatore Stephen L. Johnson

Richard L. Handley E. Allen Bell

Trenton M. Stover John A. Myers

|

|

OHIO VALLEY BANK DIRECTORS

Jeffrey E. Smith

Thomas E. Wiseman

David W. Thomas

Harold A. Howe

Steven B. Chapman

DIRECTORS EMERITUS

W. Lowell Call

James L. Dailey

Robert E. Daniel

Barney A. Molnar

|

Anna P. Barnitz

Brent A. Saunders

Brent R. Eastman

John G. Jones

Kimberly A. Canady, JD

Edward J. Robbins

C. Leon Saunders

Wendell B. Thomas

Lannes C. Williamson

|

6

|

OHIO VALLEY BANK OFFICERS

EXECUTIVE OFFICERS

Jeffrey E. Smith

Thomas E. Wiseman

Larry E. Miller, II

Katrinka V. Hart-Harris

Scott W. Shockey

Chief Financial Officer

Mario P. Liberatore

John G. Jones

SENIOR VICE PRESIDENTS

Jennifer L. Osborne

Tom R. Shepherd

Bryan F. Stepp

Frank W. Davison

Bryan W. Martin

David K. Nadler

Ryan J. Jones

VICE PRESIDENTS

Richard D. Scott

Patrick H. Tackett

Marilyn E. Kearns

Fred K. Mavis Business

Rick A. Swain

Bryna S. Butler

Tamela D. LeMaster

Christopher L. Preston

Gregory A. Phillips

Diana L. Parks

John A. Anderson

Kyla R. Carpenter

Allen W. Elliott

E. Kate Cox

Brian E. Hall

Daniel T. Roush

Gary L. Crabtree

Adam D. Massie

Shawn R. Siders

Jay D. Miller

|

Chairman of the Board

President and Chief Executive Officer

Chief Operating Officer and Secretary

Executive Vice President, Director of

WV Operations & Special Projects

Executive Vice President,

Chief Financial Officer

President, OVB West Virginia

President, MBC

SENIOR VICE PRESIDENTS

Retail Lending

Chief Deposit Officer

Chief Lending Officer

Financial Bank Group

Chief Administrative Officer

Chief Risk/Credit Officer

Chief Operating Officer - MBC

VICE PRESIDENTS

Trust

Corporate Banking

Director of Human Resources

Business Development Officer

Western Division Branch Manager

Corporate Communications

Branch Administration/CRM

Branch Administration

Business Development

Consumer Lending

Internal Audit Liaison

Loan Operations

Director of Marketing

Director of Customer Support

Director of Cultural Enhancement

Corporate Banking

Senior Compliance Officer

Lender/Business Development Officer

Lender/Business Development Officer

Senior Credit Officer

Business Development Officer

|

VICE PRESIDENTS

Melissa P. Wooten

Christopher S. Petro

Kimberly R. Williams

Paula W. Clay

Cindy H. Johnston

Joe J. Wyant

Brenda G. Henson

Gabriel U. Stewart

Randall L. Hammond

Barbara A. Patrick

Richard P. Speirs

Lori A. Edwards

Raymond G. Polcyn

Stephanie L. Stover

Brandon O. Huff

Anita M. Good

Angela S. Kinnaird

Laura F. Conger

Lonnie L. Hunt

Ruth R. Murphy

Terri M. Camden

Shelly N. Boothe

ASSISTANT CASHIERS

Lois J. Scherer

Linda K. Roe

Glen P. Arrowood, II

Michelle L. Hammond

Patricia G. Hapney

Anthony W. Staley

Jon C. Jones

Daniel F. Short

Pamela K. Smith

William F. Richards

|

Shareholder Relations Manager & Trust Officer

Comptroller

Systems Officer

Assistant Secretary

Assistant Secretary

Region Manager Jackson County

Manager Deposit Services

Chief Information Security Officer

Security Officer/Loss Prevention

BSA Officer/Loss Prevention

Facilities Manager

Secondary Market Manager

Manager of Loan Production Office

Retail Lending Operations Manager

Systems Administrator

Regional Branch Administrator

Customer Support Manager

Mortgage Loan Processing Clerk

Lender/Business Development Officer

Lender/Business Development Officer

Human Resources Officer

Business Development Officer

EFT Officer

Lead Cultural Engineer & Talent Development Specialist

Manager of Indirect Lending

Escrow Supervisor/Lead Mortgage Loan Documentation Clerk

Retail Lending & Personal Banker

Product Development Business Sales & Support

Western Cabell Region Manager

Meigs Region Manager

Eastern Cabell Region Manager

Advertising Manager

|

7

|

OHIO VALLEY BANK

Athens, Ohio

Loan Office - 2097 East State St. Suite C

Gallia County, Ohio

Main Office - 420 Third Ave.

Mini Bank - 437 Fourth Ave.

Inside Walmart - 2145 Eastern Ave.

Jackson Pike - 3035 State Route 160

Inside Holzer - 100 Jackson Pike

Loan Office - Walmart Plaza, 2145 Eastern Ave.

Rio Grande - 27 North College Ave.

Jackson County, Ohio

Upper Main - 740 East Main St.

Downtown - 400 East Main St.

Oak Hill - 116 Jackson St.

Wellston - 123 South Ohio Ave.

Mt. Sterling, Ohio

255 Yankeetown St.

New Holland, Ohio

25 North Main St.

Pomeroy, Ohio

Inside Save-a-Lot - 700 W. Main St.

Waverly, Ohio

507 West Emmitt Ave.

Barboursville, West Virginia

6431 East State Route 60

Milton, West Virginia

280 East Main St.

Point Pleasant, West Virginia

328 Viand St.

|

LOAN CENTRAL

Chillicothe, Ohio

1080 N. Bridge Street, Unit 43

Gallipolis, Ohio

2145 Eastern Avenue

Jackson, Ohio

345 Main Street

South Point, Ohio

348 County Road 410

Waverly, Ohio

505 West Emmitt Avenue

Wheelersburg, Ohio

326 Center Street

|

8

ohio valley banc corp.

annual report 2016

financials

SELECTED FINANCIAL DATA

|

|

Years Ended December 31

|

|||||||||||||||||||

|

|

2016

|

2015

|

2014

|

2013

|

2012

|

|||||||||||||||

|

(dollars in thousands, except share and per share data)

|

||||||||||||||||||||

|

|

||||||||||||||||||||

|

SUMMARY OF OPERATIONS:

|

||||||||||||||||||||

|

|

||||||||||||||||||||

|

Total interest income

|

$

|

39,348

|

$

|

36,334

|

$

|

36,355

|

$

|

35,958

|

$

|

39,001

|

||||||||||

|

Total interest expense

|

3,022

|

2,839

|

2,875

|

3,573

|

6,346

|

|||||||||||||||

|

Net interest income

|

36,326

|

33,495

|

33,480

|

32,385

|

32,655

|

|||||||||||||||

|

Provision for loan losses

|

2,826

|

1,090

|

2,787

|

477

|

1,583

|

|||||||||||||||

|

Total other income

|

8,239

|

8,597

|

9,793

|

8,518

|

8,483

|

|||||||||||||||

|

Total other expenses

|

32,899

|

29,619

|

29,293

|

29,375

|

29,741

|

|||||||||||||||

|

Income before income taxes

|

8,840

|

11,383

|

11,193

|

11,051

|

9,814

|

|||||||||||||||

|

Income taxes

|

1,920

|

2,809

|

3,120

|

2,939

|

2,762

|

|||||||||||||||

|

Net income

|

6,920

|

8,574

|

8,073

|

8,112

|

7,052

|

|||||||||||||||

|

|

||||||||||||||||||||

|

PER SHARE DATA:

|

||||||||||||||||||||

|

|

||||||||||||||||||||

|

Earnings per share

|

$

|

1.59

|

$

|

2.08

|

$

|

1.97

|

$

|

2.00

|

$

|

1.75

|

||||||||||

|

Cash dividends declared per share

|

$

|

0.82

|

$

|

0.89

|

$

|

0.84

|

$

|

0.73

|

$

|

1.09

|

||||||||||

|

Book value per share

|

$

|

22.40

|

$

|

21.97

|

$

|

20.94

|

$

|

19.62

|

$

|

18.66

|

||||||||||

|

Weighted average number of common shares outstanding

|

4,351,748

|

4,117,675

|

4,099,194

|

4,064,083

|

4,030,322

|

|||||||||||||||

|

|

||||||||||||||||||||

|

AVERAGE BALANCE SUMMARY:

|

||||||||||||||||||||

|

|

||||||||||||||||||||

|

Total loans

|

$

|

644,690

|

$

|

589,953

|

$

|

581,690

|

$

|

555,314

|

$

|

570,166

|

||||||||||

|

Securities(1)

|

196,389

|

188,754

|

170,314

|

175,809

|

202,413

|

|||||||||||||||

|

Deposits

|

749,054

|

694,218

|

673,410

|

664,061

|

705,111

|

|||||||||||||||

|

Other borrowed funds(2)

|

39,553

|

32,878

|

31,225

|

26,572

|

33,538

|

|||||||||||||||

|

Shareholders' equity

|

98,133

|

88,720

|

83,887

|

77,989

|

74,031

|

|||||||||||||||

|

Total assets

|

899,209

|

828,444

|

799,448

|

779,113

|

822,573

|

|||||||||||||||

|

|

||||||||||||||||||||

|

PERIOD END BALANCES:

|

||||||||||||||||||||

|

|

||||||||||||||||||||

|

Total loans

|

$

|

734,901

|

$

|

585,752

|

$

|

594,768

|

$

|

566,319

|

$

|

558,288

|

||||||||||

|

Securities(1)

|

151,985

|

155,900

|

137,274

|

133,173

|

159,791

|

|||||||||||||||

|

Deposits

|

790,452

|

660,746

|

646,830

|

628,877

|

655,064

|

|||||||||||||||

|

Shareholders' equity

|

104,528

|

90,470

|

86,216

|

80,419

|

75,820

|

|||||||||||||||

|

Total assets

|

954,640

|

796,285

|

778,668

|

747,368

|

769,223

|

|||||||||||||||

|

|

||||||||||||||||||||

|

KEY RATIOS:

|

||||||||||||||||||||

|

|

||||||||||||||||||||

|

Return on average assets

|

0.77

|

%

|

1.03

|

%

|

1.01

|

%

|

1.04

|

%

|

0.86

|

%

|

||||||||||

|

Return on average equity

|

7.05

|

%

|

9.66

|

%

|

9.62

|

%

|

10.40

|

%

|

9.53

|

%

|

||||||||||

|

Dividend payout ratio

|

51.79

|

%

|

42.74

|

%

|

42.62

|

%

|

36.56

|

%

|

62.29

|

%

|

||||||||||

|

Average equity to average assets

|

10.91

|

%

|

10.71

|

%

|

10.49

|

%

|

10.01

|

%

|

9.00

|

%

|

||||||||||

(1) Securities include interest-bearing deposits with banks and restricted investments in bank stocks.

(2) Other borrowed funds include subordinated debentures.

9

CONSOLIDATED STATEMENTS OF CONDITION

|

|

As of December 31

|

|||||||

|

|

2016

|

2015

|

||||||

|

(dollars in thousands, except share and per share data)

|

||||||||

|

|

||||||||

|

Assets

|

||||||||

|

|

||||||||

|

Cash and noninterest-bearing deposits with banks

|

$

|

12,512

|

$

|

9,475

|

||||

|

Interest-bearing deposits with banks

|

27,654

|

36,055

|

||||||

|

Total cash and cash equivalents

|

40,166

|

45,530

|

||||||

|

|

||||||||

|

Certificates of deposit in financial institutions

|

1,670

|

1,715

|

||||||

|

Securities available for sale

|

96,490

|

91,651

|

||||||

|

Securities held to maturity (estimated fair value: 2016 - $19,171; 2015 - $20,790)

|

18,665

|

19,903

|

||||||

|

Restricted investments in bank stocks

|

7,506

|

6,576

|

||||||

|

|

||||||||

|

Total loans

|

734,901

|

585,752

|

||||||

|

Less: Allowance for loan losses

|

(7,699

|

)

|

(6,648

|

)

|

||||

|

Net loans

|

727,202

|

579,104

|

||||||

|

|

||||||||

|

Premises and equipment, net

|

12,783

|

10,404

|

||||||

|

Other real estate owned

|

2,129

|

2,358

|

||||||

|

Accrued interest receivable

|

2,315

|

1,819

|

||||||

|

Goodwill

|

7,801

|

1,267

|

||||||

|

Other intangible assets, net

|

670

|

----

|

||||||

|

Bank owned life insurance and annuity assets

|

29,349

|

28,352

|

||||||

|

Other assets

|

7,894

|

7,606

|

||||||

|

Total assets

|

$

|

954,640

|

$

|

796,285

|

||||

|

|

||||||||

|

Liabilities

|

||||||||

|

|

||||||||

|

Noninterest-bearing deposits

|

$

|

209,576

|

$

|

176,499

|

||||

|

Interest-bearing deposits

|

580,876

|

484,247

|

||||||

|

Total deposits

|

790,452

|

660,746

|

||||||

|

|

||||||||

|

Other borrowed funds

|

37,085

|

23,946

|

||||||

|

Subordinated debentures

|

8,500

|

8,500

|

||||||

|

Accrued liabilities

|

14,075

|

12,623

|

||||||

|

Total liabilities

|

850,112

|

705,815

|

||||||

|

|

||||||||

|

Commitments and Contingent Liabilities (See Note L)

|

----

|

----

|

||||||

|

|

||||||||

|

Shareholders' Equity

|

||||||||

|

|

||||||||

|

Common stock ($1.00 stated value per share, 10,000,000 shares authorized;

2016 - 5,325,504 shares issued; 2015 - 4,777,414 shares issued

|

5,326

|

4,777

|

||||||

|

Additional paid-in capital

|

46,788

|

35,318

|

||||||

|

Retained earnings

|

69,117

|

65,782

|

||||||

|

Accumulated other comprehensive income (loss)

|

(991

|

)

|

305

|

|||||

|

Treasury stock, at cost (659,739 shares)

|

(15,712

|

)

|

(15,712

|

)

|

||||

|

Total shareholders' equity

|

104,528

|

90,470

|

||||||

|

Total liabilities and shareholders' equity

|

$

|

954,640

|

$

|

796,285

|

||||

See accompanying notes to consolidated financial statements

10

CONSOLIDATED STATEMENTS OF INCOME

|

For the years ended December 31

|

2016

|

2015

|

2014

|

|||||||||

|

(dollars in thousands, except per share data)

|

||||||||||||

|

|

||||||||||||

|

Interest and dividend income:

|

||||||||||||

|

Loans, including fees

|

$

|

36,266

|

$

|

33,481

|

$

|

33,635

|

||||||

|

Securities:

|

||||||||||||

|

Taxable

|

1,961

|

1,849

|

1,717

|

|||||||||

|

Tax exempt

|

445

|

526

|

555

|

|||||||||

|

Dividends

|

302

|

293

|

312

|

|||||||||

|

Other interest

|

374

|

185

|

136

|

|||||||||

|

|

39,348

|

36,334

|

36,355

|

|||||||||

|

Interest expense:

|

||||||||||||

|

Deposits

|

2,154

|

2,191

|

2,236

|

|||||||||

|

Other borrowed funds

|

664

|

478

|

474

|

|||||||||

|

Subordinated debentures

|

204

|

170

|

165

|

|||||||||

|

|

3,022

|

2,839

|

2,875

|

|||||||||

|

Net interest income

|

36,326

|

33,495

|

33,480

|

|||||||||

|

Provision for loan losses

|

2,826

|

1,090

|

2,787

|

|||||||||

|

Net interest income after provision for loan losses

|

33,500

|

32,405

|

30,693

|

|||||||||

|

|

||||||||||||

|

Noninterest income:

|

||||||||||||

|

Service charges on deposit accounts

|

1,977

|

1,573

|

1,627

|

|||||||||

|

Trust fees

|

227

|

221

|

223

|

|||||||||

|

Income from bank owned life insurance and annuity assets

|

725

|

681

|

672

|

|||||||||

|

Mortgage banking income

|

227

|

242

|

228

|

|||||||||

|

Electronic refund check / deposit fees

|

2,048

|

2,371

|

3,133

|

|||||||||

|

Debit / credit card interchange income

|

2,594

|

2,399

|

2,174

|

|||||||||

|

Gain (loss) on other real estate owned

|

(467

|

)

|

99

|

113

|

||||||||

|

Gain on sale of securities

|

----

|

163

|

----

|

|||||||||

|

Gain on sale of ProAlliance Corporation

|

----

|

----

|

810

|

|||||||||

|

Other

|

908

|

848

|

813

|

|||||||||

|

|

8,239

|

8,597

|

9,793

|

|||||||||

|

Noninterest expense:

|

||||||||||||

|

Salaries and employee benefits

|

18,874

|

17,498

|

17,878

|

|||||||||

|

Occupancy

|

1,846

|

1,599

|

1,585

|

|||||||||

|

Furniture and equipment

|

922

|

801

|

757

|

|||||||||

|

Professional fees

|

1,362

|

1,375

|

1,151

|

|||||||||

|

Marketing expense

|

915

|

860

|

1,004

|

|||||||||

|

FDIC insurance

|

455

|

583

|

483

|

|||||||||

|

Data processing

|

1,455

|

1,259

|

1,127

|

|||||||||

|

Software

|

1,316

|

1,123

|

1,014

|

|||||||||

|

Foreclosed assets

|

357

|

347

|

185

|

|||||||||

|

Amortization of intangibles

|

68

|

----

|

----

|

|||||||||

|

Merger related expenses

|

930

|

----

|

----

|

|||||||||

|

Other

|

4,399

|

4,174

|

4,109

|

|||||||||

|

|

32,899

|

29,619

|

29,293

|

|||||||||

|

Income before income taxes

|

8,840

|

11,383

|

11,193

|

|||||||||

|

Provision for income taxes

|

1,920

|

2,809

|

3,120

|

|||||||||

|

NET INCOME

|

$

|

6,920

|

$

|

8,574

|

$

|

8,073

|

||||||

|

Earnings per share

|

$

|

1.59

|

$

|

2.08

|

$

|

1.97

|

||||||

See accompanying notes to consolidated financial statements

11

CONSOLIDATED STATEMENTS OF

COMPREHENSIVE INCOME

|

For the years ended December 31

|

2016

|

2015

|

2014

|

|||||||||

|

(dollars in thousands)

|

||||||||||||

|

|

||||||||||||

|

NET INCOME

|

$

|

6,920

|

$

|

8,574

|

$

|

8,073

|

||||||

|

Other comprehensive income (loss):

|

||||||||||||

|

Change in unrealized gain (loss) on available for sale securities

|

(1,963

|

)

|

(830

|

)

|

1,077

|

|||||||

|

Reclassification adjustment for realized (gains)

|

----

|

(163

|

)

|

----

|

||||||||

|

(1,963

|

)

|

(993

|

)

|

1,077

|

||||||||

|

Related tax (expense) benefit

|

667

|

338

|

(366

|

)

|

||||||||

|

Total other comprehensive income (loss), net of tax

|

(1,296

|

)

|

(655

|

)

|

711

|

|||||||

|

Total comprehensive income

|

$

|

5,624

|

$

|

7,919

|

$

|

8,784

|

||||||

See accompanying notes to consolidated financial statements

12

Consolidated Statements of Changes in

Shareholders' Equity

|

For the years ended December 31, 2016, 2015, and 2014

|

||||||||||||||||||||||||

|

(dollars in thousands, except share and per share data)

|

||||||||||||||||||||||||

|

|

Common

Stock

|

Additional Paid-In Capital

|

Retained

Earnings

|

Accumulated Other Comprehensive Income

|

Treasury

Stock

|

Total Shareholders' Equity

|

||||||||||||||||||

|

Balances at January 1, 2014

|

$

|

4,758

|

$

|

34,883

|

$

|

56,241

|

$

|

249

|

$

|

(15,712

|

)

|

$

|

80,419

|

|||||||||||

|

Net income

|

----

|

----

|

8,073

|

----

|

----

|

8,073

|

||||||||||||||||||

|

Other comprehensive

income (loss), net

|

----

|

----

|

----

|

711

|

----

|

711

|

||||||||||||||||||

|

Common stock issued to ESOP,

14,618 shares

|

15

|

336

|

----

|

----

|

----

|

351

|

||||||||||||||||||

|

Common stock issued through

dividend reinvestment,

4,304 shares

|

4

|

99

|

----

|

----

|

----

|

103

|

||||||||||||||||||

|

Cash dividends, $.84 per share

|

----

|

----

|

(3,441

|

)

|

----

|

----

|

(3,441

|

)

|

||||||||||||||||

|

Balances at December 31, 2014

|

4,777

|

35,318

|

60,873

|

960

|

(15,712

|

)

|

86,216

|

|||||||||||||||||

|

Net income

|

----

|

----

|

8,574

|

----

|

----

|

8,574

|

||||||||||||||||||

|

Other comprehensive

income (loss), net

|

----

|

----

|

----

|

(655

|

)

|

----

|

(655

|

)

|

||||||||||||||||

|

Cash dividends, $.89 per share

|

----

|

----

|

(3,665

|

)

|

----

|

----

|

(3,665

|

)

|

||||||||||||||||

|

Balances at December 31, 2015

|

4,777

|

35,318

|

65,782

|

305

|

(15,712

|

)

|

90,470

|

|||||||||||||||||

|

Net income

|

----

|

----

|

6,920

|

----

|

----

|

6,920

|

||||||||||||||||||

|

Other comprehensive

income (loss), net

|

----

|

----

|

----

|

(1,296

|

)

|

----

|

(1,296

|

)

|

||||||||||||||||

|

Common stock issued to ESOP,

24,572 shares

|

25

|

550

|

----

|

----

|

----

|

575

|

||||||||||||||||||

|

Acquisition – Milton Bancorp, Inc.

523,518 shares

|

524

|

10,920

|

----

|

----

|

----

|

11,444

|

||||||||||||||||||

|

Cash dividends, $.82 per share

|

----

|

----

|

(3,585

|

)

|

----

|

----

|

(3,585

|

)

|

||||||||||||||||

|

Balances at December 31, 2016

|

$

|

5,326

|

$

|

46,788

|

$

|

69,117

|

$

|

(991

|

)

|

$

|

(15,712

|

)

|

$

|

104,528

|

||||||||||

See accompanying notes to consolidated financial statements

13

Consolidated Statements of Cash Flows

|

For the years ended December 31

|

2016

|

2015

|

2014

|

|||||||||

|

(dollars in thousands)

|

||||||||||||

|

|

||||||||||||

|

Cash flows from operating activities:

|

||||||||||||

|

Net income

|

$

|

6,920

|

$

|

8,574

|

$

|

8,073

|

||||||

|

Adjustments to reconcile net income to net cash provided by operating activities:

|

||||||||||||

|

Depreciation of premises and equipment

|

1,126

|

872

|

795

|

|||||||||

|

Net (accretion) of purchase accounting adjustments

|

(255

|

)

|

----

|

----

|

||||||||

|

Net amortization of securities

|

407

|

432

|

732

|

|||||||||

|

Net realized (gain) on sale of securities

|

----

|

(163

|

)

|

----

|

||||||||

|

Proceeds from sale of loans in secondary market

|

6,455

|

6,746

|

4,286

|

|||||||||

|

Loans disbursed for sale in secondary market

|

(6,228

|

)

|

(6,504

|

)

|

(4,058

|

)

|

||||||

|

Amortization of mortgage servicing rights

|

79

|

93

|

77

|

|||||||||

|

Gain on sale of loans

|

(306

|

)

|

(335

|

)

|

(305

|

)

|

||||||

|

Amortization of intangible assets

|

68

|

----

|

----

|

|||||||||

|

Deferred tax (benefit) expense

|

(725

|

)

|

591

|

(517

|

)

|

|||||||

|

Provision for loan losses

|

2,826

|

1,090

|

2,787

|

|||||||||

|

Common stock issued to ESOP

|

575

|

----

|

351

|

|||||||||

|

Earnings on bank owned life insurance and annuity assets

|

(725

|

)

|

(681

|

)

|

(672

|

)

|

||||||

|

Gain on sale of ProAlliance Corporation

|

----

|

----

|

(810

|

)

|

||||||||

|

(Gain) loss on sale of other real estate owned

|

(22

|

)

|

(99

|

)

|

(25

|

)

|

||||||

|

(Appreciation) write-down of other real estate owned

|

489

|

----

|

(88

|

)

|

||||||||

|

Change in accrued interest receivable

|

(496

|

)

|

(13

|

)

|

95

|

|||||||

|

Change in accrued liabilities

|

1,461

|

473

|

1,326

|

|||||||||

|

Change in other assets

|

1,717

|

(678

|

)

|

(366

|

)

|

|||||||

|

Net cash provided by operating activities

|

13,366

|

10,398

|

11,681

|

|||||||||

|

|

||||||||||||

|

Cash flows from investing activities:

|

||||||||||||

|

Net cash acquired from Milton Bancorp, Inc. acquisition

|

1,770

|

----

|

----

|

|||||||||

|

Proceeds from sales of securities available for sale

|

----

|

10,550

|

----

|

|||||||||

|

Proceeds from maturities of securities available for sale

|

18,591

|

15,085

|

15,318

|

|||||||||

|

Purchases of securities available for sale

|

(20,256

|

)

|

(33,251

|

)

|

(16,077

|

)

|

||||||

|

Proceeds from maturities of securities held to maturity

|

3,089

|

3,482

|

827

|

|||||||||

|

Purchases of securities held to maturity

|

(1,528

|

)

|

(626

|

)

|

(885

|

)

|

||||||

|

Proceeds from maturities of certificates of deposit in financial institutions

|

490

|

245

|

----

|

|||||||||

|

Purchases of certificates of deposit in financial institutions

|

(445

|

)

|

(980

|

)

|

(980

|

)

|

||||||

|

Proceeds from restricted investments in bank stocks

|

----

|

----

|

1,200

|

|||||||||

|

Purchases of restricted investments in bank stocks

|

(566

|

)

|

----

|

----

|

||||||||

|

Net change in loans

|

(38,299

|

)

|

5,049

|

(29,936

|

)

|

|||||||

|

Proceeds from sale of other real estate owned

|

403

|

458

|

821

|

|||||||||

|

Proceeds from sale of ProAlliance Corporation

|

----

|

----

|

810

|

|||||||||

|

Purchases of premises and equipment

|

(1,683

|

)

|

(1,950

|

)

|

(985

|

)

|

||||||

|

Purchases of bank owned life insurance and annuity assets

|

----

|

(3,000

|

)

|

----

|

||||||||

|

Net cash (used in) investing activities

|

(38,434

|

)

|

(4,938

|

)

|

(29,887

|

)

|

||||||

|

|

||||||||||||

|

Cash flows from financing activities:

|

||||||||||||

|

Change in deposits

|

10,150

|

13,916

|

17,953

|

|||||||||

|

Proceeds from common stock through dividend reinvestment

|

----

|

----

|

103

|

|||||||||

|

Cash dividends

|

(3,585

|

)

|

(3,665

|

)

|

(3,441

|

)

|

||||||

|

Proceeds from Federal Home Loan Bank borrowings

|

11,102

|

400

|

7,575

|

|||||||||

|

Repayment of Federal Home Loan Bank borrowings

|

(1,883

|

)

|

(1,671

|

)

|

(1,612

|

)

|

||||||

|

Change in other long-term borrowings

|

3,899

|

----

|

----

|

|||||||||

|

Change in other short-term borrowings

|

21

|

113

|

261

|

|||||||||

|

Net cash provided by financing activities

|

19,704

|

9,093

|

20,839

|

|||||||||

|

|

||||||||||||

|

Cash and cash equivalents:

|

||||||||||||

|

Change in cash and cash equivalents

|

(5,364

|

)

|

14,553

|

2,633

|

||||||||

|

Cash and cash equivalents at beginning of year

|

45,530

|

30,977

|

28,344

|

|||||||||

|

Cash and cash equivalents at end of year

|

$

|

40,166

|

$

|

45,530

|

$

|

30,977

|

||||||

|

Supplemental disclosure:

|

||||||||||||

|

Cash paid for interest

|

$

|

2,930

|

$

|

2,784

|

$

|

3,274

|

||||||

|

Cash paid for income taxes

|

1,725

|

2,450

|

3,567

|

|||||||||

|

Transfers from loans to other real estate owned

|

957

|

1,381

|

879

|

|||||||||

|

Other real estate owned sales financed by The Ohio Valley Bank Company

|

316

|

189

|

390

|

|||||||||

|

Issuance of common stock for Milton Bancorp, Inc. acquisition

|

11,444

|

----

|

----

|

|||||||||

|

Net assets acquired from Milton Bancorp, Inc. acquisition, excluding cash and cash equivalents.

|

3,140

|

----

|

----

|

|||||||||

See accompanying notes to consolidated financial statements

14

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Amounts are in thousands, except share and per share data.

Note A - Summary of Significant Accounting Policies

Description of Business: Ohio Valley Banc Corp. ("Ohio Valley") is a financial holding company registered under the Bank Holding Company Act of 1956. Ohio Valley has one banking subsidiary, The Ohio Valley Bank Company (the "Bank"), an Ohio state-chartered bank that is a member of the Federal Reserve Bank and is regulated primarily by the Ohio Division of Financial Institutions and the Federal Reserve Board. Ohio Valley also has a subsidiary that engages in consumer lending to individuals with higher credit risk history, Loan Central, Inc.; a subsidiary insurance agency that facilitates the receipts of insurance commissions, Ohio Valley Financial Services Agency, LLC; and a limited purpose property and casualty insurance company, OVBC Captive, Inc. Ohio Valley and its subsidiaries are collectively referred to as the "Company."

The Company provides a full range of commercial and retail banking services from 25 offices located in southeastern Ohio and western West Virginia. It accepts deposits in checking, savings, time and money market accounts and makes personal, commercial, floor plan, student, construction and real estate loans. Substantially all loans are secured by specific items of collateral, including business assets, consumer assets, and commercial and residential real estate. Commercial loans are expected to be repaid from cash flow from business operations. The Company also offers safe deposit boxes, wire transfers and other standard banking products and services. The Bank's deposits are insured by the Federal Deposit Insurance Corporation. In addition to accepting deposits and making loans, the Bank invests in U. S. Government and agency obligations, interest-bearing deposits in other financial institutions and investments permitted by applicable law.

The Bank's trust department provides a wide variety of fiduciary services for trusts, estates and benefit plans and also provides investment and security services as an agent for its customers.

Principles of Consolidation: The consolidated financial statements include the accounts of Ohio Valley and its wholly-owned subsidiaries, the Bank, Loan Central, Inc., Ohio Valley Financial Services Agency, LLC, and OVBC Captive, Inc. All material intercompany accounts and transactions have been eliminated.

Industry Segment Information: Internal financial information is primarily reported and aggregated in two lines of business, banking and consumer finance.

Use of Estimates: To prepare financial statements in conformity with accounting principles generally accepted in the U.S., management makes estimates and assumptions based on available information. These estimates and assumptions affect the amounts reported in the financial statements and the disclosures provided, and actual results could differ.

Cash and Cash Equivalents: Cash and cash equivalents include cash on hand, noninterest-bearing deposits with banks, federal funds sold and interest-bearing deposits with banks with maturity terms of less than 90 days. Generally, federal funds are purchased and sold for one-day periods. The Company reports net cash flows for customer loan transactions, deposit transactions, short-term borrowings and interest-bearing deposits with other financial institutions.

Certificates of deposit in financial institutions: Certificates of deposit in financial institutions are carried at cost and have maturity terms of 90 days or greater. The longest maturity date is September 30,2019.

Securities: The Company classifies securities into held to maturity and available for sale categories. Held to maturity securities are those which the Company has the positive intent and ability to hold to maturity and are reported at amortized cost. Securities classified as available for sale include securities that could be sold for liquidity, investment management or similar reasons even if there is not a present intention of such a sale. Available for sale securities are reported at fair value, with unrealized gains or losses included in other comprehensive income, net of tax.

Premium amortization is deducted from, and discount accretion is added to, interest income on securities using the level yield method without anticipating prepayments, except for mortgage-backed securities where prepayments are anticipated. Gains and losses are recognized upon the sale of specific identified securities on the completed trade date.

15

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note A - Summary of Significant Accounting Policies (continued)

Other-Than-Temporary Impairments of Securities: In determining an other-than-temporary impairment ("OTTI"), management considers many factors, including: (1) the length of time and the extent to which the fair value has been less than cost, (2) the financial condition and near-term prospects of the issuer, (3) whether the market decline was affected by macroeconomic conditions, and (4) whether the Company has the intent to sell the debt security or more likely than not will be required to sell the debt security before its anticipated recovery. The assessment of whether an OTTI decline exists involves a high degree of subjectivity and judgment and is based on the information available to management at a point in time.

When an OTTI occurs, the amount of the OTTI recognized in earnings depends on whether an entity intends to sell the security or it is more likely than not it will be required to sell the security before recovery of its amortized cost basis, less any current-period credit loss. If an entity intends to sell or it is more likely than not it will be required to sell the security before recovery of its amortized cost basis, less any current-period credit loss, the OTTI shall be recognized in earnings equal to the entire difference between the investment's amortized cost basis and its fair value at the balance sheet date. If an entity does not intend to sell the security and it is not more likely than not that the entity will be required to sell the security before recovery of its amortized cost basis less any current-period loss, the OTTI shall be separated into the amount representing the credit loss and the amount related to all other factors. The amount of the total OTTI related to the credit loss is determined based on the present value of cash flows expected to be collected and is recognized in earnings. The amount of the total OTTI related to other factors is recognized in other comprehensive income, net of applicable taxes. The previous amortized cost basis less the OTTI recognized in earnings becomes the new amortized cost basis of the investment.

Restricted Investments in Bank Stocks: The Bank is a member of the Federal Home Loan Bank ("FHLB") system. Additionally, the Bank is a member of the Federal Reserve Bank ("FRB") system. Members are required to own a certain amount of stock based on their level of borrowings and other factors and may invest in additional amounts. FHLB stock and FRB stock are carried at cost, classified as restricted securities, and periodically evaluated for impairment based on ultimate recovery of par value. Both cash and stock dividends are reported as income. The Company has additional investments in other restricted bank stocks that are not material to the financial statements.

Loans: Loans that management has the intent and ability to hold for the foreseeable future or until maturity or payoff are reported at the principal balance outstanding, net of unearned interest, deferred loan fees and costs, and an allowance for loan losses. Interest income is reported on an accrual basis using the interest method and includes amortization of net deferred loan fees and costs over the loan term using the level yield method without anticipating prepayments. The amount of the Company's recorded investment is not materially different than the amount of unpaid principal balance for loans.

Interest income is discontinued and the loan moved to non-accrual status when full loan repayment is in doubt, typically when the loan is impaired or payments are past due 90 days or over unless the loan is well-secured or in process of collection. Past due status is based on the contractual terms of the loan. In all cases, loans are placed on nonaccrual or charged-off at an earlier date if collection of principal or interest is considered doubtful. Nonaccrual loans and loans past due 90 days or over and still accruing include both smaller balance homogeneous loans that are collectively evaluated for impairment and individually classified impaired loans.

All interest accrued but not received for loans placed on nonaccrual is reversed against interest income. Interest received on such loans is accounted for on the cash-basis method until qualifying for return to accrual. Loans are returned to accrual status when all the principal and interest amounts contractually due are brought current and future payments are reasonably assured.

Allowance for Loan Losses: The allowance for loan losses is a valuation allowance for probable incurred credit losses. Loan losses are charged against the allowance when management believes the uncollectibility of a loan balance is confirmed. Subsequent recoveries, if any, are credited to the allowance. Management estimates the allowance balance required using past loan loss experience, the nature and volume of the portfolio, information about specific borrower situations and estimated collateral values, economic conditions, and other factors. Allocations of the allowance may be made for specific loans, but the entire allowance is available for any loan that, in management's judgment, should be charged-off.

16

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note A - Summary of Significant Accounting Policies (continued)

The allowance consists of specific and general components. The specific component relates to loans that are individually classified as impaired. A loan is impaired when, based on current information and events, it is probable that the Company will be unable to collect all amounts due according to the contractual terms of the loan agreement. Loans for which the terms have been modified and for which the borrower is experiencing financial difficulties are considered troubled debt restructurings and classified as impaired.

Factors considered by management in determining impairment include payment status, collateral value, and the probability of collecting scheduled principal and interest payments when due. Loans that experience insignificant payment delays and payment shortfalls generally are not classified as impaired. Management determines the significance of payment delays and payment shortfalls on a case-by-case basis, taking into consideration all of the circumstances surrounding the loan and the borrower, including the length and reasons for the delay, the borrower's prior payment record, and the amount of shortfall in relation to the principal and interest owed.

Commercial and commercial real estate loans are individually evaluated for impairment. If a loan is impaired, a portion of the allowance is allocated so that the loan is reported, net, at the present value of estimated future cash flows using the loan's existing rate or at the fair value of collateral if repayment is expected solely from the collateral. Smaller balance homogeneous loans, such as consumer and most residential real estate, are collectively evaluated for impairment, and accordingly, they are not separately identified for impairment disclosure. Troubled debt restructurings are measured at the present value of estimated future cash flows using the loan's effective rate at inception. If a troubled debt restructuring is considered to be a collateral dependent loan, the loan is reported, net, at the fair value of the collateral. For troubled debt restructurings that subsequently default, the Company determines the amount of reserve in accordance with the accounting policy for the allowance for loan losses.

The general component covers non-impaired loans and impaired loans that are not individually reviewed for impairment and is based on historical loss experience adjusted for current factors. The historical loss experience is determined by portfolio segment and is based on the actual loss history experienced by the Company over the most recent 3 years for the consumer and real estate portfolio segment and 5 years for the commercial portfolio segment. The total loan portfolio's actual loss experience is supplemented with other economic factors based on the risks present for each portfolio segment. These economic factors include consideration of the following: levels of and trends in delinquencies and impaired loans; levels of and trends in charge-offs and recoveries; trends in volume and terms of loans; effects of any changes in risk selection and underwriting standards; other changes in lending policies, procedures, and practices; experience, ability, and depth of lending management and other relevant staff; national and local economic trends and conditions; industry conditions; and effects of changes in credit concentrations. The following portfolio segments have been identified: Commercial and Industrial, Commercial Real Estate, Residential Real Estate, and Consumer.

Commercial and industrial loans consist of borrowings for commercial purposes to individuals, corporations, partnerships, sole proprietorships, and other business enterprises. Commercial and industrial loans are generally secured by business assets such as equipment, accounts receivable, inventory, or any other asset excluding real estate and generally made to finance capital expenditures or operations. The Company's risk exposure is related to deterioration in the value of collateral securing the loan should foreclosure become necessary. Generally, business assets used or produced in operations do not maintain their value upon foreclosure, which may require the Company to write down the value significantly to sell.

17

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note A - Summary of Significant Accounting Policies (continued)

Commercial real estate consists of nonfarm, nonresidential loans secured by owner-occupied and nonowner-occupied commercial real estate as well as commercial construction loans. An owner-occupied loan relates to a borrower purchased building or space for which the repayment of principal is dependent upon cash flows from the ongoing business operations conducted by the party, or an affiliate of the party, who owns the property. Owner-occupied loans that are dependent on cash flows from operations can be adversely affected by current market conditions for their product or service. A nonowner-occupied loan is a property loan for which the repayment of principal is dependent upon rental income associated with the property or the subsequent sale of the property. Nonowner-occupied loans that are dependent upon rental income are primarily impacted by local economic conditions which dictate occupancy rates and the amount of rent charged. Commercial construction loans consist of borrowings to purchase and develop raw land into 1-4 family residential properties. Construction loans are extended to individuals as well as corporations for the construction of an individual or multiple properties and are secured by raw land and the subsequent improvements. Repayment of the loans to real estate developers is dependent upon the sale of properties to third parties in a timely fashion upon completion. Should there be delays in construction or a downturn in the market for those properties, there may be significant erosion in value which may be absorbed by the Company.

Residential real estate loans consist of loans to individuals for the purchase of 1-4 family primary residences with repayment primarily through wage or other income sources of the individual borrower. The Company's loss exposure to these loans is dependent on local market conditions for residential properties as loan amounts are determined, in part, by the fair value of the property at origination.

Consumer loans are comprised of loans to individuals secured by automobiles, open-end home equity loans and other loans to individuals for household, family, and other personal expenditures, both secured and unsecured. These loans typically have maturities of 6 years or less with repayment dependent on individual wages and income. The risk of loss on consumer loans is elevated as the collateral securing these loans, if any, rapidly depreciate in value or may be worthless and/or difficult to locate if repossession is necessary. The Company has allocated the highest percentage of its allowance for loan losses as a percentage of loans to the other identified loan portfolio segments due to the larger dollar balances associated with such portfolios.

At December 31, 2016, there were no changes to the accounting policies or methodologies within any of the Company's loan portfolio segments from the prior period.

Concentrations of Credit Risk: The Company grants residential, consumer and commercial loans to customers located primarily in the southeastern Ohio and western West Virginia areas.

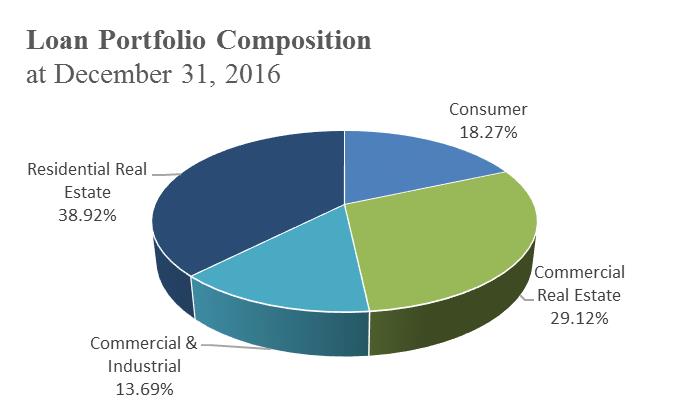

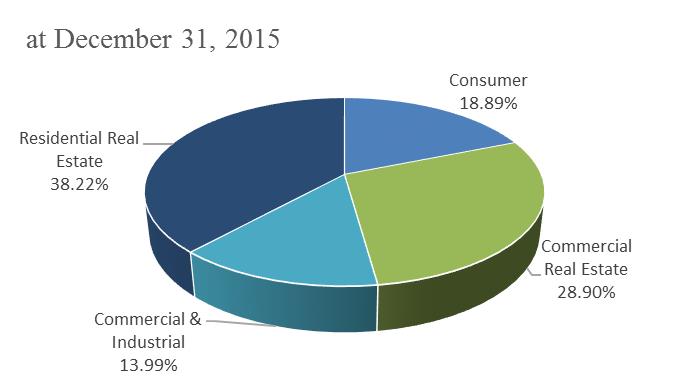

The following represents the composition of the Company's loan portfolio as of December 31:

|

% of Total Loans

|

||||||||

|

2016

|

2015

|

|||||||

|

Residential real estate loans

|

38.92

|

%

|

38.22

|

%

|

||||

|

Commercial real estate loans

|

29.12

|

%

|

28.90

|

%

|

||||

|

Consumer loans

|

18.27

|

%

|

18.89

|

%

|

||||

|

Commercial and industrial loans

|

13.69

|

%

|

13.99

|

%

|

||||

|

100.00

|

%

|

100.00

|

%

|

|||||

Approximately 5.61% of total loans were unsecured at December 31, 2016, down from 6.06% at December 31, 2015.

The Bank, in the normal course of its operations, conducts business with correspondent financial institutions. Balances in correspondent accounts, investments in federal funds, certificates of deposit and other short-term securities are closely monitored to ensure that prudent levels of credit and liquidity risks are maintained. At December 31, 2016, the Bank's primary correspondent balance was $26,422 on deposit at the Federal Reserve Bank, Cleveland, Ohio.

18

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note A - Summary of Significant Accounting Policies (continued)

Premises and Equipment: Land is carried at cost. Premises and equipment are stated at cost less accumulated depreciation, which is computed using the straight-line method over the estimated useful life of the owned asset and, for leasehold improvement, over the remaining term of the leased facility, whichever is shorter. The useful lives range from 3 to 8 years for equipment, furniture and fixtures and 7 to 39 years for buildings and improvements.

Foreclosed assets: Assets acquired through or instead of loan foreclosure are initially recorded at fair value less costs to sell when acquired, establishing a new cost basis. Physical possession of residential real estate property collateralizing a consumer mortgage loan occurs when legal title is obtained upon completion of foreclosure or when the borrower conveys all interest in the property to satisfy the loan through completion of a deed in lieu of foreclosure or through a similar legal agreement. These assets are subsequently accounted for at lower of cost or fair value less estimated costs to sell. If fair value declines subsequent to foreclosure, a valuation allowance is recorded through expense. Operating costs after acquisition are expensed. Foreclosed assets totaled $2,129 and $2,358 at December 31, 2016 and 2015.

Goodwill: Goodwill resulting from business combinations prior to January 1, 2009 represents the excess of the purchase price over the fair value of the net assets of businesses acquired. Goodwill resulting from business combinations after January 1, 2009, is generally determined as the excess of the fair value of the consideration transferred, plus the fair value of any noncontrolling interests in the acquiree, over the fair value of the net assets acquired and liabilities assumed as of the acquisition date. Goodwill acquired in a purchase business combination and determined to have an indefinite useful life are not amortized, but tested for impairment at least annually. Goodwill is the only intangible asset with an indefinite life on our balance sheet. The Company has selected December 31 as the date to perform its annual qualitative impairment test. Given that the Company has been profitable and had positive equity, the qualitative assessment indicated that it was more likely than not that the fair value of goodwill was more than the carrying amount, resulting in no impairment.

Long-term Assets: Premises and equipment and other long-term assets are reviewed for impairment when events indicate their carrying amount may not be recoverable from future undiscounted cash flows. If impaired, the assets are recorded at fair value.

Mortgage Servicing Rights: A mortgage servicing right ("MSR") is a contractual agreement where the right to service a mortgage loan is sold by the original lender to another party. When the Company sells mortgage loans to the secondary market, it retains the servicing rights to these loans. The Company's MSR is recognized separately when acquired through sales of loans and is initially recorded at fair value with the income statement effect recorded in mortgage banking income. Subsequently, the MSR is then amortized in proportion to and over the period of estimated future servicing income of the underlying loan. The MSR is then evaluated for impairment periodically based upon the fair value of the rights as compared to the carrying amount, with any impairment being recognized through a valuation allowance. Fair value of the MSR is based on market prices for comparable mortgage servicing contracts. Impairment is determined by stratifying rights into groupings based on predominant risk characteristics, such as interest rate, loan type and investor type. If the Company later determines that all or a portion of the impairment no longer exists for a particular grouping, a reduction of the allowance may be recorded as an increase to income. At December 31, 2016 and 2015, the Company's MSR assets were $387 and $429, respectively.

Earnings Per Share: Earnings per share is based on net income divided by the following weighted average number of common shares outstanding during the periods: 4,351,748 for 2016; 4,117,675 for 2015; 4,099,194 for 2014. Ohio Valley had no dilutive securities outstanding for any period presented.

Earnings Per Share: Earnings per share is based on net income divided by the following weighted average number of common shares outstanding during the periods: 4,351,748 for 2016; 4,117,675 for 2015; 4,099,194 for 2014. Ohio Valley had no dilutive securities outstanding for any period presented.

Income Taxes: Income tax expense is the sum of the current year income tax due or refundable and the change in deferred tax assets and liabilities. Deferred tax assets and liabilities are the expected future tax consequences of temporary differences between the carrying amounts and tax bases of assets and liabilities, computed using enacted tax rates. A valuation allowance, if needed, reduces deferred tax assets to the amount expected to be realized.

A tax position is recognized as a benefit only if it is "more likely than not" that the tax position would be sustained in a tax examination, with a tax examination being presumed to occur. The amount recognized is the largest amount of tax benefit that is greater than 50% likely of being realized on examination. For tax positions not meeting the "more likely than not" test, no tax benefit is recorded. The Company recognizes interest and/or penalties related to income tax matters in income tax expense.

19

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note A - Summary of Significant Accounting Policies (continued)

Comprehensive Income: Comprehensive income consists of net income and other comprehensive income. Other comprehensive income includes unrealized gains and losses on securities available for sale which are also recognized as separate components of equity, net of tax.

Loss Contingencies: Loss contingencies, including claims and legal actions arising in the ordinary course of business, are recorded as liabilities when the likelihood of loss is probable and an amount or range of loss can be reasonably estimated. Management does not believe there now are such matters that will have a material effect on the financial statements.

Bank Owned Life Insurance and Annuity Assets: The Company has purchased life insurance policies on certain key executives. Bank owned life insurance is recorded at the amount that can be realized under the insurance contract at the balance sheet date, which is the cash surrender value adjusted for other charges or other amounts due that are probable at settlement. The Company also purchased an annuity investment for a certain key executive that earns interest.

Employee Stock Ownership Plan: Compensation expense is based on the market price of shares as they are committed to be allocated to participant accounts.

Loan Commitments and Related Financial Instruments: Financial instruments include off-balance sheet credit instruments, such as commitments to make loans and commercial letters of credit, issued to meet customer financing needs. The face amount for these items represents the exposure to loss, before considering customer collateral or ability to repay. These financial instruments are recorded when they are funded. See Note L for more specific disclosure related to loan commitments.

Dividend Restrictions: Banking regulations require maintaining certain capital levels and may limit the dividends paid by the Bank to Ohio Valley or by Ohio Valley to its shareholders. See Note P for more specific disclosure related to dividend restrictions.

Restrictions on Cash: Cash on hand or on deposit with a third-party correspondent and the Federal Reserve Bank of $28,102 and $36,535 was required to meet regulatory reserve and clearing requirements at year-end 2016 and 2015. The balances on deposit with a third-party correspondent do not earn interest.

Derivatives: At the inception of a derivative contract, the Company designates the derivative as one of three types based on the Company's intentions and belief as to likely effectiveness as a hedge. These three types are (1) a hedge of the fair value of a recognized asset or liability or of an unrecognized firm commitment ("fair value hedge"), (2) a hedge of a forecasted transaction or the variability of cash flows to be received or paid related to a recognized asset or liability ("cash flow hedge"), or (3) an instrument with no hedging designation ("stand-alone derivative").

Net cash settlements on derivatives that qualify for hedge accounting are recorded in interest income or interest expense, based on the item being hedged. Net cash settlements on derivatives that do not qualify for hedge accounting are reported in noninterest income. Cash flows on hedges are classified in the cash flow statement the same as the cash flows of the items being hedged.

At December 31, 2016 and 2015, the Company's only derivatives on hand were interest rate swaps, which are classified as stand-alone derivatives. See Note H for more specific disclosures related to interest rate swaps.

Fair Value of Financial Instruments: Fair values of financial instruments are estimated using relevant market information and other assumptions, as more fully disclosed in Note O. Fair value estimates involve uncertainties and matters of significant judgment regarding interest rates, credit risk, prepayments, and other factors, especially in the absence of broad markets for particular items. Changes in assumptions or in market conditions could significantly affect the estimates.

Reclassifications: The consolidated financial statements for 2015 and 2014 have been reclassified to conform with the presentation for 2016. These reclassifications had no effect on the net results of operations or shareholders' equity.

20

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note A - Summary of Significant Accounting Policies (continued)

Adoption of New Accounting Standards: In May 2014, the FASB issued Accounting Standards Update ("ASU") 2014-09, "Revenue from Contracts with Customers (Topic 606)". The ASU creates a new topic, Topic 606, to provide guidance on revenue recognition for entities that enter into contracts with customers to transfer goods or services or enter into contracts for the transfer of nonfinancial assets. The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. Additional disclosures are required to provide quantitative and qualitative information regarding the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The new guidance is effective for annual reporting periods, and interim reporting periods within those annual periods, beginning after December 15, 2017, with early adoption permitted on January 1, 2017. The adoption of ASU 2014-09 is not expected to have a material effect on the Company's financial statements.