Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________

FORM 10-K

___________________________________

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-11037

___________________________________

Praxair, Inc.

___________________________________

Praxair, Inc. | ||

10 Riverview Drive | State of incorporation: Delaware | |

Danbury, Connecticut 06810-5113 | IRS identification number: 06-124 9050 | |

Tel. (203) 837-2000 | ||

Securities registered pursuant to Section 12(b) of the Act:

Title of each class: | Registered on: | |

Common Stock ($0.01 par value) | New York Stock Exchange | |

1.50% Euro notes due 2020 | New York Stock Exchange | |

1.20% Euro notes due 2024 | New York Stock Exchange | |

1.625% Euro notes due 2025 | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

___________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ Accelerated filer ¨ Non- accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of the voting and non-voting common stock held by non-affiliates as of June 30, 2016, was approximately $32 billion (based on the closing sale price of the stock on that date as reported on the New York Stock Exchange).

At January 31, 2017, 285,071,181 shares of common stock of Praxair, Inc. were outstanding.

Documents incorporated by reference:

Portions of the Proxy Statement of Praxair, Inc., for its 2017 Annual Meeting of Shareholders, are incorporated in Part III of this report.

PRAXAIR, INC.

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended December 31, 2016

TABLE OF CONTENTS

Page | ||

Part I | ||

Item 1: | ||

Item 1A: | ||

Item 1B: | ||

Item 2: | ||

Item 3: | ||

Item 4: | ||

Part II | ||

Item 5: | ||

Item 6: | ||

Item 7: | ||

Item 7A: | ||

Item 8: | ||

Item 9: | ||

Item 9A: | ||

Item 9B: | ||

Part III | ||

Item 10: | ||

Item 11: | ||

Item 12: | ||

Item 13: | ||

Item 14: | ||

Part IV | ||

Item 15: | ||

2

Praxair, Inc. and Subsidiaries

PART I

ITEM 1. BUSINESS

General

Praxair, Inc. (Praxair or the company) was founded in 1907 and became an independent publicly traded company in 1992. Praxair was the first company in the United States to produce oxygen from air using a cryogenic process and continues to be a technological innovator in the industrial gases industry.

Praxair is a leading industrial gas company in North and South America and one of the largest worldwide. Praxair’s primary products in its industrial gases business are atmospheric gases (oxygen, nitrogen, argon, rare gases) and process gases (carbon dioxide, helium, hydrogen, electronic gases, specialty gases, acetylene). The company also designs, engineers, and builds equipment that produces industrial gases primarily for internal use. The company’s surface technologies segment, operated through Praxair Surface Technologies, Inc., supplies wear-resistant and high-temperature corrosion-resistant metallic and ceramic coatings and powders. Praxair’s sales were $10,534 million, $10,776 million, and $12,273 million for 2016, 2015, and 2014, respectively. Refer to Item 7, Management's Discussion and Analysis, for a discussion of consolidated sales and Note 18 to the consolidated financial statements for additional information related to Praxair’s reportable segments.

Praxair serves a diverse group of industries including healthcare, petroleum refining, manufacturing, food, beverage carbonation, fiber-optics, steel making, aerospace, chemicals and water treatment. In 2016, 94% of sales were generated in four geographic segments (North America, Europe, South America and Asia) primarily from the sale of industrial gases, with the balance generated from the surface technologies segment. Praxair provides a competitive advantage to its customers by continuously developing new products and applications, which allow them to improve their productivity, energy efficiency and environmental performance.

Industrial Gases Products and Manufacturing Processes

Atmospheric gases are the highest volume products produced by Praxair. Using air as its raw material, Praxair produces oxygen, nitrogen and argon through several air separation processes of which cryogenic air separation is the most prevalent. Rare gases, such as krypton, neon and xenon, are also produced through cryogenic air separation. As a pioneer in the industrial gases industry, Praxair is a leader in developing a wide range of proprietary and patented applications and supply systems technology. Praxair also led the development and commercialization of non-cryogenic air separation technologies for the production of industrial gases. These technologies open important new markets and optimize production capacity for the company by lowering the cost of supplying industrial gases. These technologies include proprietary vacuum pressure swing adsorption (“VPSA”) and membrane separation to produce gaseous oxygen and nitrogen, respectively. Praxair also manufactures precious metal and ceramic sputtering targets used primarily in the production of semiconductors.

Process gases, including carbon dioxide, hydrogen, carbon monoxide, helium, specialty gases and acetylene are produced by methods other than air separation. Most carbon dioxide is purchased from by-product sources, including chemical plants, refineries and industrial processes or is recovered from carbon dioxide wells. Carbon dioxide is processed in Praxair’s plants to produce commercial and food-grade carbon dioxide. Hydrogen and carbon monoxide can be produced by either steam methane reforming or auto-thermal reforming of natural gas or other feed streams such as naphtha. Hydrogen is also produced by purifying by-product sources obtained from the chemical and petrochemical industries. Most of the helium sold by Praxair is sourced from certain helium-rich natural gas streams in the United States, with additional supplies being acquired from outside the United States. Acetylene is primarily sourced as a chemical by-product, but may also be produced from calcium carbide and water.

Industrial Gases Distribution

There are three basic distribution methods for industrial gases: (i) on-site or tonnage; (ii) merchant or bulk liquid; and (iii) packaged or cylinder gases. These distribution methods are often integrated, with products from all three supply modes coming from the same plant. The method of supply is generally determined by the lowest cost means of meeting the customer’s needs, depending upon factors such as volume requirements, purity, pattern of usage, and the form in which the product is used (as a gas or as a cryogenic liquid).

On-site. Customers that require the largest volumes of product (typically oxygen, nitrogen and hydrogen) and that have a relatively constant demand pattern are supplied by cryogenic and process gas on-site plants. Praxair constructs plants on or adjacent to these customers’ sites and supplies the product directly to customers by pipeline. On-site product supply contracts generally are total requirement contracts with terms typically ranging from 10-20 years and containing

3

minimum purchase requirements and price escalation provisions. Many of the cryogenic on-site plants also produce liquid products for the merchant market. Therefore, plants are typically not dedicated to a single customer. Advanced air separation processes allow on-site delivery to customers with smaller volume requirements. Customers using these systems usually enter into requirement contracts with terms typically ranging from 5-15 years.

Merchant. The merchant business is generally associated with distributable liquid oxygen, nitrogen, argon, carbon dioxide, hydrogen and helium. The deliveries generally are made from Praxair’s plants by tanker trucks to storage containers at the customer's site which are owned and maintained by Praxair and leased to the customer. Due to distribution cost, merchant oxygen and nitrogen generally have a relatively small distribution radius from the plants at which they are produced. Merchant argon, hydrogen and helium can be shipped much longer distances. The customer agreements used in the merchant business are usually three-to seven-year requirement contracts.

Packaged Gases. Customers requiring small volumes are supplied products in metal containers called cylinders, under medium to high pressure. Packaged gases include atmospheric gases, carbon dioxide, hydrogen, helium, acetylene and related products. Praxair also produces and distributes in cylinders a wide range of specialty gases and mixtures. Cylinders may be delivered to the customer’s site or picked up by the customer at a packaging facility or retail store. Packaged gases are generally sold under one to three-year supply contracts and through purchase orders.

A substantial amount of the cylinder gases sold in the United States is distributed by independent distributors that buy merchant gases in liquid form and repackage the products in their facilities. Packaged gas distributors, including Praxair, also distribute hardgoods and welding equipment purchased from independent manufacturers. Over time, Praxair has acquired a number of independent industrial gases and welding products distributors at various locations in the United States and continues to sell merchant gases to other independent distributors. Between its own distribution business, joint ventures and sales to independent distributors, Praxair is represented in 48 states, the District of Columbia and Puerto Rico.

Surface Technologies

Praxair Surface Technologies is a leading worldwide supplier of coating services and thermal spray consumables to customers in the aircraft, energy, printing, primary metals, petrochemical, textile, and other industries. Its coatings are used to provide wear resistance, corrosion protection, thermal insulation, and many other surface-enhancing functions which serve to extend component life, enable optimal performance, and reduce operating costs. It also manufactures a complete line of electric arc, plasma and wire spray, and high-velocity oxy-fuel ("HVOF") equipment.

Inventories – Praxair carries inventories of merchant and cylinder gases, hardgoods and coatings materials to supply products to its customers on a reasonable delivery schedule. On-site plants and pipeline complexes have limited inventory. Inventory obsolescence is not material to Praxair’s business.

Customers – Praxair is not dependent upon a single customer or a few customers.

International – Praxair is a global enterprise with approximately 56% of its 2016 sales outside of the United States. It conducts industrial gases business through consolidated companies in Argentina, Bahrain, Belgium, Bolivia, Brazil, Canada, Chile, China, Colombia, Costa Rica, Denmark, Dominican Republic, France, Germany, Ghana, India, Ireland, Italy, Japan, Mexico, the Netherlands, Norway, Panama, Paraguay, Peru, Portugal, Puerto Rico, Russia, South Korea, Spain, Sweden, Taiwan, Thailand, United Arab Emirates, the United Kingdom, and Uruguay. Societa Italiana Acetilene & Derivati S.p.A. ("S.I.A.D."), an Italian company accounted for as an equity company, also has established positions in Austria, Bosnia, Bulgaria, Croatia, the Czech Republic, Hungary, Romania, Russia, Serbia, Slovakia, Slovenia and Ukraine. Refrigeration and Oxygen Company Limited ("ROC"), a Middle Eastern company accounted for as an equity company, has operations in the United Arab Emirates, Kuwait and Qatar. Praxair’s surface technologies segment has operations in Brazil, Canada, China, France, Germany, India, Italy, Japan, Singapore, South Korea and the United Kingdom.

Praxair’s international business is subject to risks customarily encountered in foreign operations, including fluctuations in foreign currency exchange rates, import and export controls, and other economic, political and regulatory policies of local governments. Also, see Item 1A. “Risk Factors” and Item 7A. “Quantitative and Qualitative Disclosures About Market Risk.”

Seasonality – Praxair’s business is generally not subject to seasonal fluctuations to any significant extent.

Research and Development – Praxair’s research and development is directed toward developing new and improved methods for the production and distribution of industrial gases and the development of new markets and applications for these gases. This results in the development of new advanced air separation and hydrogen process technologies and the frequent introduction of new industrial gas applications. Research and development for industrial gases is principally conducted at Tonawanda, New York and Burr Ridge, Illinois.

4

Praxair conducts research and development for its surface technologies to improve the quality and durability of coatings and the use of specialty powders for new applications and industries. Surface technologies research is conducted at Indianapolis, Indiana.

Patents and Trademarks – Praxair owns or licenses a large number of United States and foreign patents that relate to a wide variety of products and processes. Praxair’s patents expire at various times over the next 20 years. While these patents and licenses are considered important to our individual businesses, Praxair does not consider its business as a whole to be materially dependent upon any one particular patent, or patent license, or family of patents. Praxair also owns a large number of valuable trademarks. Only the "Praxair" trademark is important to our business as a whole.

Raw Materials and Energy Costs – Energy is the single largest cost item in the production and distribution of industrial gases. Most of Praxair’s energy requirements are in the form of electricity, natural gas and diesel fuel for distribution.

The supply of energy has not been a significant issue in the geographic areas where the company conducts business. However, energy availability and price is unpredictable and may pose unforeseen future risks.

For carbon dioxide, carbon monoxide, helium, hydrogen, specialty gases and surface technologies, raw materials are largely purchased from outside sources. Praxair has contracts or commitments for, or readily available sources of, most of these raw materials; however, their long-term availability and prices are subject to market conditions.

Competition – Praxair operates within a highly competitive environment. Some of its competitors are larger in size and capital base than Praxair. Competition is based on price, product quality, delivery, reliability, technology and service to customers.

Major competitors in the industrial gases industry both in the United States and worldwide include Air Products and Chemicals, Inc., L’Air Liquide S.A., and Linde AG. Principal competitors for the surface technologies business are Chromalloy Gas Turbine LLC, a subsidiary of Sequa Corporation, Bodycote, PLC, and OC Oerlikon Corp AG. There are other industrial gas and surface coating competitors that compete on a local geography basis.

Employees and Labor Relations – As of December 31, 2016, Praxair had 26,498 employees worldwide. Of this number, 10,182 are employed in the United States. Praxair has collective bargaining agreements with unions at numerous locations throughout the world, which expire at various dates. Praxair considers relations with its employees to be good.

Environment – Information required by this item is incorporated herein by reference to the section captioned “Management’s Discussion and Analysis – Environmental Matters” in Item 7 of this 10-K.

Available Information – The company makes its periodic and current reports available, free of charge, on or through its website, www.praxair.com, as soon as practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission ("SEC"). Investors may also access from the company website other investor information such as press releases and presentations. Information on the company’s website is not incorporated by reference herein.

In addition, the public may read and copy any materials filed with the SEC at the SEC’s Public Reference Room located at 100 F Street NE, Washington, D.C. 20549. The public may also obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website, www.sec.gov, that contains reports, proxy information statements and other information regarding issuers that file electronically.

Executive Officers – The following Executive Officers have been elected by the Board of Directors and serve at the pleasure of the Board. It is expected that the Board will elect officers annually following each annual meeting of shareholders.

Stephen F. Angel, 61, is Chief Executive Officer of Praxair, Inc. since January 1, 2007, and Chairman since May 1, 2007. Before becoming the Chief Executive Officer, Mr. Angel served as President and Chief Operating Officer from March to December 2006, and as Executive Vice President from 2001 to March 2006. Prior to joining Praxair in 2001, Mr. Angel spent 22 years in a variety of management positions with General Electric. Mr. Angel is a director of PPG Industries, Inc. where he serves on the Officers-Directors Compensation Committee, and is the Chairman of the Technology and Environment Committee. He is also a member of the executive committee of The Business Council, co-chairs the U.S. - Brazil CEO Forum, a member of the Board of the U.S. - China Business Council and its Nominating Committee.

Guillermo Bichara, 42, was appointed Vice President, General Counsel and Corporate Secretary of Praxair, Inc. effective January 1, 2015. Prior to this, from 2013-2014, he was Associate General Counsel and Assistant Secretary. From 2011-2013, Mr. Bichara served as Associate General Counsel with responsibility for Praxair Europe, Praxair Mexico and corporate transactions. He was Vice President and General Counsel of Praxair Asia from 2007-2011, and joined Praxair in 2006 as director of legal affairs at Praxair Mexico. Prior to joining Praxair, Mr. Bichara served as corporate counsel at

5

CEMEX, Mexico's global leader in the building materials industry, and was a foreign associate and counsel, respectively, at the law firms of Skadden, Arps, Slate, Meagher & Flom and White & Case.

Kelcey E. Hoyt, 47, was named Vice President and Controller effective August 1, 2016. Prior to becoming Controller, she served as Praxair’s Director of Investor Relations since 2010. She joined Praxair in 2002 and served as Director of Corporate Accounting and SEC Reporting through 2008, and later served as Controller for various divisions within Praxair’s North American Industrial Gas business. Previously, she had five years of experience in audit at KPMG, LLP. She is a certified public accountant.

Eduardo F. Menezes, 53, was promoted to Executive Vice President from Senior Vice President effective March 1, 2012. He oversees Praxair’s businesses in Asia, Europe, Mexico, and South America. From 2010 to March 2011, he was a Vice President of Praxair with responsibility for the North American Industrial Gases business. From 2007 to 2010, he was President of Praxair Europe. He served as Managing Director of Praxair’s business in Mexico from 2004 to 2007, as Vice President and General Manager for Praxair Distribution, Inc. from 2003 to 2004 and as Vice President, U.S. West Region, for North American Industrial Gases, from 2000 to 2003.

Anne K. Roby, age 52, was named Senior Vice President on January 1, 2014, responsible for Global Supply Systems, R&D, Global Market Development, Global Operations Excellence, Global Procurement, Sustainability and Safety, Health and Environment. From 2011-2013, she served as President of Praxair Asia, responsible for Praxair’s industrial gases business in China, India, South Korea and Thailand as well as the electronics market globally. In 2010, Dr. Roby became President of Praxair Electronics, after having served as Vice President, Global Sales, for Praxair from 2009-2010. Prior to this, she was Vice President of the U.S. South Region from 2006-2009. Dr. Roby joined Praxair in 1991 as a development associate in the Company’s R&D organization and was promoted to other positions of increasing responsibility.

Scott E. Telesz, 49, was promoted to Executive Vice President from Senior Vice President, effective March 1, 2012. He is responsible for Praxair’s U.S. atmospheric gases businesses, and it’s business in Canada, Praxair Distribution, Praxair Surface Technologies, and Helium-Rare Gases. Before joining Praxair in 2010, he was a Vice President from 2007 to 2010 of SABIC Innovative Plastics, a major division of Riyadh-based Saudi Basic Industries Corporation, a global manufacturer of chemicals, fertilizers, plastics and metals. From 1998 to 2007, he held a variety of general management positions with General Electric, and from 1989 to 1998, Mr. Telesz held several positions, including Engagement Manager, in the United States and Australia, with McKinsey & Company.

Matthew J. White, 44, was appointed Senior Vice President and Chief Financial Officer effective January 1, 2014. Prior to this, Mr. White was President of Praxair Canada from 2011-2014. Mr. White joined Praxair in 2004 as finance director of Praxair’s largest business unit, North American Industrial Gases. In 2008, he became Vice President and Controller of Praxair, then was named Vice President and Treasurer in 2010. Before joining Praxair, Mr. White was vice president, finance, at Fisher Scientific and before that he held various financial positions, including group controller, at GenTek, a manufacturing and performance chemicals company.

6

ITEM 1A. RISK FACTORS

Due to the size and geographic reach of the company’s operations, a wide range of factors, many of which are outside of the company’s control, could materially affect the company’s future operations and financial performance. Management believes the following risks may significantly impact the company:

General Economic Conditions – Weakening economic conditions in markets in which the company does business may adversely impact the company’s financial results and/or cash flows.

Praxair serves a diverse group of industries across more than 50 countries which generally leads to financial stability through various business cycles. However, a broad decline in general economic or business conditions in the industries served by its customers could adversely affect the demand for Praxair’s products and impair the ability of our customers to satisfy their obligations to the company, resulting in uncollected receivables and/or unanticipated contract terminations or project delays. In addition, many of the company’s customers are in businesses that are cyclical in nature, such as the chemicals, electronics, metals and energy industries. Downturns in these industries may adversely impact the company during these cycles. Additionally, such conditions could impact the utilization of the company’s manufacturing capacity which may require the company to recognize impairment losses on tangible assets such as property, plant and equipment as well as intangible assets such as goodwill, customer relationships or intellectual property.

Cost and Availability of Raw Materials and Energy – Increases in the cost of energy and raw materials and/or disruption in the supply of these materials could result in lost sales or reduced profitability.

Energy is the single largest cost item in the production and distribution of industrial gases. Most of Praxair’s energy requirements are in the form of electricity, natural gas and diesel fuel for distribution. Praxair attempts to minimize the financial impact of variability in these costs through the management of customer contracts and reducing demand through operational productivity and energy efficiency. Large customer contracts typically have escalation and pass-through clauses to recover energy and feedstock costs. Such attempts may not successfully mitigate cost variability which could negatively impact its financial condition or results of operations. The supply of energy has not been a significant issue in the geographic areas where it conducts business. However, regional energy conditions are unpredictable and may pose future risk.

For carbon dioxide, carbon monoxide, helium, hydrogen, specialty gases and surface technologies, raw materials are largely purchased from outside sources. Where feasible, Praxair sources several of these raw materials, including carbon dioxide, hydrogen and calcium carbide, as chemical or industrial byproducts. In addition, Praxair has contracts or commitments for, or readily available sources of, most of these raw materials; however, their long-term availability and prices are subject to market conditions. A disruption in supply of such raw materials could impact the company’s ability to meet contractual supply commitments.

International Events and Circumstances – The company’s international operations are subject to the risks of doing business abroad and international events and circumstances may adversely impact its business, financial condition or results of operations.

Praxair has substantial international operations which are subject to risks including devaluations in currency exchange rates, transportation delays and interruptions, political and economic instability and disruptions, restrictions on the transfer of funds, the imposition of duties and tariffs, import and export controls, changes in governmental policies, labor unrest, possible nationalization and/or expropriation of assets, domestic and international tax laws and compliance with governmental regulations. These events could have an adverse effect on international operations in the future by reducing the demand for its products, decreasing the prices at which it can sell its products, reducing the U.S. dollar value of revenue from international operations or otherwise having an adverse effect on its business.

The United Kingdom’s planned exit from the European Union has caused volatility in currency exchange rates as well as increased economic uncertainty. These factors could adversely affect our business and financial results primarily in Europe.

Global Financial Markets Conditions – Macroeconomic factors may impact the company’s ability to obtain financing or increase the cost of obtaining financing which may adversely impact the company’s financial results and/or cash flows.

Volatility and disruption in the U.S. and global credit and equity markets, from time to time, could make it more difficult for Praxair to obtain financing for its operations and/or could increase the cost of obtaining financing. In addition, the company’s borrowing costs can be affected by short and long-term debt ratings assigned by independent rating agencies which are based, in significant part, on the company’s performance as measured by certain criteria such as interest coverage and leverage ratios. A decrease in these debt ratings could increase the cost of borrowing or make it more difficult to obtain financing. While the impact of volatility in the global credit markets cannot be predicted with certainty, the

7

company believes that it has sufficient operating flexibility, cash reserves, and funding sources to maintain adequate amounts of liquidity to meet its business needs around the world.

Competitor Actions – The inability to effectively compete could adversely impact results of operations.

Praxair operates within a highly competitive environment worldwide. Competition is based on price, product quality, delivery, reliability, technology and service to customers. Competitors’ behavior related to these areas could potentially have significant impacts on the company’s financial results.

Governmental Regulations – The company is subject to a variety of United States and foreign government regulations. Changes in these regulations could have an adverse impact on the business, financial position and results of operations.

The company is subject to regulations in the following areas, among others:

• | Environmental protection including climate change; |

• | Domestic and international tax laws and currency controls; |

• | Safety; |

• | Securities laws (e.g., SEC and generally accepted accounting principles in the United States); |

• | Trade and import/ export restrictions; |

• | Antitrust matters; |

• | Global anti-bribery laws, including the U.S. Foreign Corrupt Practices Act; |

• | Healthcare regulations |

Changes in these or other regulatory areas may impact the company’s profitability, may require the company to spend additional resources to comply with the regulations, or may restrict the company’s ability to compete effectively in the marketplace. Noncompliance with such laws and regulations could result in penalties or sanctions that could have an adverse impact on the company’s financial results and/or reputation. Environmental protection is discussed further below.

Praxair is subject to various environmental and occupational health and safety laws and regulations, including those governing the discharge of pollutants into the air or water, the storage, handling and disposal of chemicals, hazardous substances and wastes, the remediation of contamination, the regulation of greenhouse gas emissions, and other potential climate change initiatives. Violations of these laws could result in substantial penalties, third party claims for property damage or personal injury, or sanctions. The company may also be subject to liability for the investigation and remediation of environmental contamination at properties that it owns or operates and at other properties where Praxair or its predecessors have operated or arranged for the disposal of hazardous wastes. Although management does not believe that any such liabilities will have a material adverse impact on its financial position and results of operations, management cannot provide assurance that such costs will not increase in the future or will not become material. See the section captioned “Management’s Discussion and Analysis – Environmental Matters” in Item 7 of this Form 10-K.

Catastrophic Events – Catastrophic events could disrupt the operations of the company and/or its customers and suppliers and may have a significant adverse impact on the results of operations.

The occurrence of catastrophic events or natural disasters such as extreme weather, including hurricanes and floods; health epidemics; acts of war or terrorism; could disrupt or delay the company’s ability to produce and distribute its products to customers and could potentially expose the company to third-party liability claims. In addition, such events could impact the company’s customers and suppliers resulting in temporary or long-term outages and/or the limitation of supply of energy and other raw materials used in normal business operations. To mitigate these risks, Praxair evaluates the direct and indirect business risks through business impact analysis and conducts regular reviews of these business risks with management. Subsequently, Praxair establishes policies and sets priorities; consults with vendors, insurance providers and industry experts; and makes investments in facilities with suitably resilient design and technology, in order to reduce such impact to the business. Despite these steps, however, these situations are outside the company’s control and may have a significant adverse impact on the company’s financial results.

Retaining Qualified Personnel – The inability to attract and retain qualified personnel may adversely impact the company’s business.

If Praxair fails to attract, hire and retain qualified personnel, the company may not be able to develop, market or sell its products or successfully manage its business. Praxair is dependent upon its highly skilled, experienced and efficient workforce to be successful. Much of Praxair’s competitive advantage is based on the expertise and experience of its key

8

personnel regarding its marketing, technology, manufacturing and distribution infrastructure, systems and products. The inability to attract and hire qualified individuals or the loss of key employees in very skilled areas could have a negative effect on the company’s financial results.

Technological Advances – If the company fails to keep pace with technological advances in the industry or if new technology initiatives do not become commercially accepted, customers may not continue to buy the company’s products and results of operations could be adversely affected.

Praxair’s research and development is directed toward developing new and improved methods for the production and distribution of industrial gases and the development of new markets and applications for the use of these gases. This results in the frequent introduction of new industrial gas applications and the development of new advanced air separation process technologies. The company also conducts research and development for its surface technologies to improve the quality and durability of coatings and the use of specialty powders for new applications and industries. As a result of these efforts, the company develops new and proprietary technologies and employs necessary measures to protect such technologies within the global geographies in which the company operates. These technologies help Praxair to create a competitive advantage and to provide a platform for the company to grow its business. If Praxair’s research and development activities do not keep pace with competitors or if it does not create new technologies that benefit customers, future results of operations could be adversely affected.

Litigation and Governmental Investigations – The outcomes of litigation and governmental investigations may affect the company’s financial results.

Praxair is subject to various lawsuits and governmental investigations arising out of the normal course of business that may result in adverse outcomes. These actions are based upon alleged environmental, tax, antitrust and personal injury claims, among others. Adverse outcomes in some or all of the claims pending may result in significant monetary damages or injunctive relief that could adversely affect its ability to conduct business. While management currently believes that resolving all of these matters, individually or in the aggregate, will not have a material adverse impact on the company’s financial position or liquidity, the litigation and other claims Praxair faces are subject to inherent uncertainties and management’s view of these matters may change in the future. There exists the possibility of a material adverse impact on the company’s results of operations for the period in which the effect of an unfavorable final outcome becomes probable and reasonably estimable.

Tax Liabilities – Potential tax liabilities could adversely impact the company’s financial position and results of operations.

Praxair is subject to income and other taxes in both the United States and numerous foreign jurisdictions. The determination of the company’s worldwide provision for income taxes and other tax liabilities requires judgment and is based on diverse legislative and regulatory structures that exist in the various jurisdictions where the company operates. Although management believes its estimates are reasonable, the ultimate tax outcome may differ from the amounts recorded in its financial statements and may materially affect the company’s financial results for the period when such determination is made. See Notes 5 and 17 to the consolidated financial statements of this Form 10-K.

Pension Liabilities – Risks related to our pension benefit plans may adversely impact our results of operations and cash flows.

Pension benefits represent significant financial obligations that will be ultimately settled in the future with employees who meet eligibility requirements. Because of the uncertainties involved in estimating the timing and amount of future payments and asset returns, significant estimates are required to calculate pension expense and liabilities related to the company’s plans. The company utilizes the services of independent actuaries, whose models are used to facilitate these calculations. Several key assumptions are used in the actuarial models to calculate pension expense and liability amounts recorded in the consolidated financial statements. In particular, significant changes in actual investment returns on pension assets, discount rates, or legislative or regulatory changes could impact future results of operations and required pension contributions. For information regarding the potential impacts regarding significant assumptions used to estimate pension expense, including discount rates and the expected long-term rates of return on plan assets. See “Critical Accounting Policies – Pension Benefits” included in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of this Form 10-K.

Operational Risks – Operational risks may adversely impact the company’s business or results of operations.

Praxair’s operating results are dependent on the continued operation of its production facilities and its ability to meet customer contract requirements and other needs. Insufficient or excess capacity threatens the company’s ability to generate competitive profit margins and may expose the company to liabilities related to contract commitments. Operating results are also dependent on the company’s ability to complete new construction projects on time, on budget and in accordance

9

with performance requirements. Failure to do so may expose the business to loss of revenue, potential litigation and loss of business reputation.

Also inherent in the management of the company’s production facilities and delivery systems, including storage, vehicle transportation and pipelines, are operational risks that require continuous training, oversight and control. Material operating failures at production, storage facilities or pipelines, including fire, toxic release and explosions, or the occurrence of vehicle transportation accidents could result in loss of life, damage to the environment, loss of production and/or extensive property damage, all of which may negatively impact the company’s financial results.

Information Technology Systems – The Company may be subject to information technology system ("IT") failures, network disruptions and breaches in data security.

Praxair relies on IT systems and networks for business and operational activities, and also stores and processes sensitive business and proprietary information in these systems and networks. These systems are susceptible to outages due to fire, flood, power loss, telecommunications failures, viruses, break-ins and similar events, or breaches of security. Management has taken steps to address these risks and concerns by implementing advanced security technologies, internal controls, network and data center resiliency and recovery process. Despite these steps, however, operational failures and breaches of security from increasingly sophisticated cyber threats could lead to the loss or disclosure of confidential information, result in regulatory actions and have a material adverse impact on Praxair's operations, reputation and financial results.

Acquisitions and Joint Ventures – The inability to effectively integrate acquisitions or collaborate with joint venture partners could adversely impact the company’s financial position and results of operations.

Praxair has evaluated, and expects to continue to evaluate, a wide array of potential strategic acquisitions and joint ventures. Many of these transactions, if consummated, could be material to its financial condition and results of operations. In addition, the process of integrating an acquired company, business or group of assets may create unforeseen operating difficulties and expenditures. Although historically the company has been successful with its acquisition strategy and execution, the areas where the company may face risks include:

• | The need to implement or remediate controls, procedures and policies appropriate for a larger public company at companies that prior to the acquisition lacked these controls, procedures and policies; |

• | Diversion of management time and focus from operating existing business to acquisition integration challenges; |

• | Cultural challenges associated with integrating employees from the acquired company into the existing organization; |

• | The need to integrate each company’s accounting, management information, human resource and other administrative systems to permit effective management; |

• | Difficulty with the assimilation of acquired operations and products; |

• | Failure to achieve targeted synergies; and |

• | Inability to retain key employees and business relationships of acquired companies. |

Foreign acquisitions and joint ventures involve unique risks in addition to those mentioned above, including those related to integration of operations across different cultures and languages, currency risks and the particular economic, political and regulatory risks associated with specific countries. Also, the anticipated benefit of the company’s acquisitions may not materialize. Future acquisitions or dispositions could result in potentially dilutive issuances of equity securities, the incurrence of debt, contingent liabilities or amortization expenses, or impairments of goodwill, any of which could adversely impact the company’s financial results.

Intended potential business combination with Linde - Risks in connection with the potential business combination may adversely impact Praxair’s business, financial condition and results of operations.

On December 20, 2016, Praxair and Linde AG (Linde) jointly issued a press release announcing that Praxair and Linde intend to combine in a merger of equals under a new holding company through an all-stock transaction (the business combination) and signed a non-binding term sheet. The potential business combination with Linde involves certain risks, which may adversely impact Praxair’s business, financial condition and results of operations, and the combined company may not realize all of the anticipated benefits of the intended potential business combination if and when the combination is completed. Risks in connection with the proposed business combination, which may result in significant costs and delays, include:

10

• | the expected timing and likelihood of the entry into or the completion of the proposed business combination, including the timing, receipt and terms and conditions of any required governmental and regulatory approvals of the proposed business combination that could reduce anticipated benefits or cause the parties not to enter into, or to abandon the transaction; |

• | if and when the parties enter into the proposed business combination agreement, the occurrence of any event, change or other circumstances that could give rise to the termination of the proposed business combination agreement; |

• | the ability to successfully complete the proposed business combination and the exchange offer, including regulatory or other limitations imposed as a result of the proposed business combination; |

• | the success of the combined company’s business following the proposed business combination, including the ability to successfully integrate the Praxair and Linde businesses; |

• | the possibility that Praxair stockholders may not approve the proposed business combination agreement or that the requisite number of Linde shares may not be tendered in the public offer; |

• | the risk that the parties may not be able to satisfy the conditions to closing of the proposed business combination in a timely manner or at all; |

• | the risk that the announcement or consummation of the proposed business combination could have adverse effects on the market price of Linde’s or Praxair’s common stock or the ability of Linde and Praxair to retain customers, retain or hire key personnel, maintain relationships with their respective suppliers and customers, and on their operating results and businesses generally; |

• | the risk that the combined company may be unable to achieve expected synergies or that it may take longer or be more costly than expected to achieve those synergies. |

11

ITEM 1B. UNRESOLVED STAFF COMMENTS

Praxair has received no written SEC staff comments regarding any of its Exchange Act reports which remain unresolved.

ITEM 2. PROPERTIES

Praxair’s worldwide headquarters are located in owned office space in Danbury, Connecticut. Other principal administrative offices are owned in Tonawanda, New York, and leased in Rio de Janeiro, Brazil; Shanghai, China and Madrid, Spain.

Praxair designs, engineers, manufactures and operates facilities that produce and distribute industrial gases. These industrial gas production facilities and certain components are designed and/or manufactured at its facilities in Tonawanda, New York; Houston, Texas; Rio de Janeiro, Brazil; and Shanghai, China. Praxair’s Italian equity affiliate, S.I.A.D., also has such capacity.

Due to the nature of Praxair’s industrial gas products, it is generally uneconomical to transport them distances greater than a few hundred miles from the production facility. As a result, Praxair operates a significant number of production facilities spread globally throughout a number of geographic regions.

The following is a description of production facilities for Praxair by segment. No significant portion of these assets was leased at December 31, 2016. Generally, these facilities are fully utilized and are sufficient to meet our manufacturing needs.

North America

The North America segment operates production facilities in the U.S., Canada and Mexico, approximately 255 of which are cryogenic air separation plants, hydrogen plants and carbon dioxide plants. There are five major pipeline complexes in North America located in Northern Indiana, Houston, along the Gulf Coast of Texas, Detroit and Louisiana. Also located throughout North America are noncryogenic air separation plants, packaged gas facilities, specialty gas plants, helium plants and other smaller plant facilities.

Europe

The Europe segment has production facilities primarily in Italy, Spain, Germany, the Benelux region, the United Kingdom, Scandinavia and Russia which include approximately 70 cryogenic air separation plants and carbon dioxide plants. There are three major pipeline complexes in Europe located in Northern Spain and the Rhine and Saar regions of Germany. These pipeline complexes are primarily supplied by cryogenic air separation plants. Also located throughout Europe are noncryogenic air separation plants, packaged gas facilities and other smaller plant facilities.

South America

The South America segment operates more than 60 cryogenic air separation plants and carbon dioxide plants, primarily located in Brazil. Many of these plants support a major pipeline complex in Southern Brazil. Also located throughout South America are packaged gas facilities and other smaller plant facilities.

Asia

The Asia segment has production facilities located primarily in China, Korea, India and Thailand, approximately 60 of which are cryogenic air separation plants and carbon dioxide plants. Also located throughout Asia are noncryogenic air separation plants, hydrogen, packaged gas and other production facilities.

Surface Technologies

The Surface Technologies segment provides coating services and manufactures coating equipment at approximately 45 sites. The majority of these sites are located in the United States and Europe, with smaller operations in Asia, and Brazil.

ITEM 3. LEGAL PROCEEDINGS

Information required by this item is incorporated herein by reference to the section captioned “Notes to Consolidated Financial Statements – 17 Commitments and Contingencies” in Item 8 of this 10-K.

ITEM 4. MINE SAFETY DISCLOSURES

Not Applicable

12

PART II

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The principal market for the company’s common stock (ticker symbol: PX) is the New York Stock Exchange ("NYSE"). At December 31, 2016 there were 11,928 shareholders of record.

NYSE quarterly stock price and dividend information

Market Price | Trading High | Trading Low | Close | Dividend Per Share | |||||||||||

2016 | |||||||||||||||

First Quarter | $ | 115.32 | $ | 95.60 | $ | 114.45 | $ | 0.75 | |||||||

Second Quarter | $ | 120.04 | $ | 106.31 | $ | 112.39 | $ | 0.75 | |||||||

Third Quarter | $ | 125.00 | $ | 110.12 | $ | 120.83 | $ | 0.75 | |||||||

Fourth Quarter | $ | 124.48 | $ | 114.43 | $ | 117.19 | $ | 0.75 | |||||||

2015 | |||||||||||||||

First Quarter | $ | 130.38 | $ | 119.69 | $ | 120.74 | $ | 0.715 | |||||||

Second Quarter | $ | 124.99 | $ | 117.19 | $ | 119.55 | $ | 0.715 | |||||||

Third Quarter | $ | 120.51 | $ | 98.55 | $ | 101.86 | $ | 0.715 | |||||||

Fourth Quarter | $ | 118.58 | $ | 99.59 | $ | 102.40 | $ | 0.715 | |||||||

Praxair’s annual dividend on its common stock for 2016 was $3.00 per share. On January 26, 2017, Praxair’s Board of Directors declared a dividend of $0.7875 per share for the first quarter of 2017, or $3.15 per share annualized, which may be changed as Praxair’s earnings and business prospects warrant. The declaration of dividends is a business decision made by the Board of Directors based on Praxair’s earnings and financial condition and other factors the Board of Directors considers relevant.

Purchases of Equity Securities – Certain information regarding purchases made by or on behalf of the company or any affiliated purchaser (as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934, as amended) of its common stock during the three months ended December 31, 2016 is provided below:

Period | Total Number of Shares Purchased (Thousands) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Program (1) (Thousands) | Approximate Dollar Value of Shares that May Yet be Purchased Under the Program (2) (Millions) | |||||||||

October 2016 | 25 | $ | 117.44 | 25 | $ | 1,683 | |||||||

November 2016 | 369 | $ | 116.23 | 369 | $ | 1,640 | |||||||

December 2016 | 506 | $ | 117.36 | 506 | $ | 1,581 | |||||||

Fourth Quarter 2016 | 900 | $ | 116.90 | 900 | $ | 1,581 | |||||||

________________________

(1) | On January 28, 2014, the Company’s board of directors approved the repurchase of $1.5 billion of its common stock ("2014 program") which could take place from time to time on the open market (which could include the use of 10b5-1 trading plans) or through negotiated transactions, subject to market and business conditions. |

(2) | As of December 31, 2016, the Company had purchased $1,419 million of its common stock pursuant to the 2014 program, leaving an additional $81 million remaining authorized under the 2014 program. The 2014 program does not have any stated expiration date. In addition, on July 28, 2015, the Company's board of directors approved the repurchase of $1.5 billion of its common stock ("2015 program") which could take place from time to time on the open market (which could include the use of 10b5-1 trade plans) or through negotiated transactions, subject to market and business conditions. The 2015 program does not have any stated expiration date. The 2015 program is in addition to the 2014 program. |

13

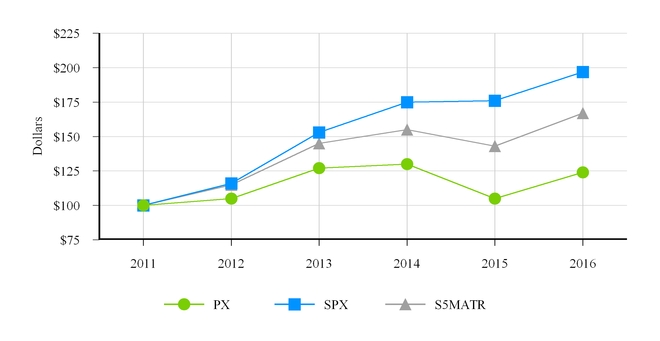

Peer Performance Table – The graph below compares the most recent five-year cumulative returns of Praxair’s common stock with those of the Standard & Poor’s 500 Index ("SPX") and the S5 Materials Index ("S5MATR") which covers 30 companies, including Praxair. The figures assume an initial investment of $100 on December 31, 2011 and that all dividends have been reinvested.

2011 | 2012 | 2013 | 2014 | 2015 | 2016 | |

PX | $100 | $105 | $127 | $130 | $105 | $124 |

SPX | $100 | $116 | $153 | $175 | $176 | $197 |

S5MATR | $100 | $115 | $145 | $155 | $143 | $167 |

14

ITEM 6. SELECTED FINANCIAL DATA

FIVE-YEAR FINANCIAL SUMMARY

(Dollar amounts in millions, except per share data)

Year Ended December 31, | 2016(a) | 2015(a) | 2014(a) | 2013(a) | 2012(a) | ||||||||||||||

From the Consolidated Statements of Income | |||||||||||||||||||

Sales | $ | 10,534 | $ | 10,776 | $ | 12,273 | $ | 11,925 | $ | 11,224 | |||||||||

Cost of sales, exclusive of depreciation and amortization | 5,860 | 5,960 | 6,962 | 6,744 | 6,396 | ||||||||||||||

Selling, general and administrative | 1,145 | 1,152 | 1,308 | 1,349 | 1,270 | ||||||||||||||

Depreciation and amortization | 1,122 | 1,106 | 1,170 | 1,109 | 1,001 | ||||||||||||||

Research and development | 92 | 93 | 96 | 98 | 98 | ||||||||||||||

Cost reduction program and other charges – net | 100 | 172 | 138 | 32 | 65 | ||||||||||||||

Other income (expenses) – net | 23 | 28 | 9 | 32 | 43 | ||||||||||||||

Operating profit | 2,238 | 2,321 | 2,608 | 2,625 | 2,437 | ||||||||||||||

Interest expense – net | 190 | 161 | 213 | 178 | 141 | ||||||||||||||

Income before income taxes and equity investments | 2,048 | 2,160 | 2,395 | 2,447 | 2,296 | ||||||||||||||

Income taxes | 551 | 612 | 691 | 649 | 586 | ||||||||||||||

Income before equity investments | 1,497 | 1,548 | 1,704 | 1,798 | 1,710 | ||||||||||||||

Income from equity investments | 41 | 43 | 42 | 38 | 34 | ||||||||||||||

Net income (including noncontrolling interests) | 1,538 | 1,591 | 1,746 | 1,836 | 1,744 | ||||||||||||||

Noncontrolling interests | (38 | ) | (44 | ) | (52 | ) | (81 | ) | (52 | ) | |||||||||

Net income – Praxair, Inc. | $ | 1,500 | $ | 1,547 | $ | 1,694 | $ | 1,755 | $ | 1,692 | |||||||||

Per Share Data – Praxair, Inc. Shareholders | |||||||||||||||||||

Basic earnings per share | $ | 5.25 | $ | 5.39 | $ | 5.79 | $ | 5.94 | $ | 5.67 | |||||||||

Diluted earnings per share | $ | 5.21 | $ | 5.35 | $ | 5.73 | $ | 5.87 | $ | 5.61 | |||||||||

Cash dividends per share | $ | 3.00 | $ | 2.86 | $ | 2.60 | $ | 2.40 | $ | 2.20 | |||||||||

Weighted Average Shares Outstanding (000’s) | |||||||||||||||||||

Basic shares outstanding | 285,677 | 287,005 | 292,494 | 295,523 | 298,316 | ||||||||||||||

Diluted shares outstanding | 287,757 | 289,055 | 295,608 | 298,965 | 301,845 | ||||||||||||||

Other Information and Ratios | |||||||||||||||||||

Total assets | $ | 19,332 | $ | 18,319 | $ | 19,769 | $ | 20,223 | $ | 18,062 | |||||||||

Total debt | $ | 9,515 | $ | 9,231 | $ | 9,225 | $ | 8,779 | $ | 7,334 | |||||||||

Net debt (b) | $ | 8,991 | $ | 9,084 | $ | 9,099 | $ | 8,641 | $ | 7,177 | |||||||||

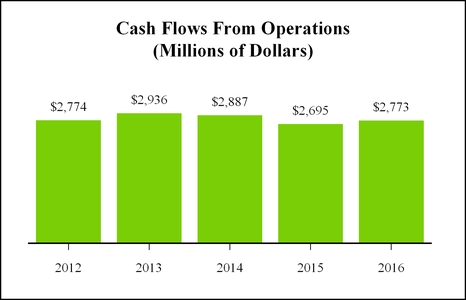

Cash flow from operations (c) | $ | 2,773 | $ | 2,695 | $ | 2,887 | $ | 2,936 | $ | 2,774 | |||||||||

Net cash used for investing activities | $ | (1,770 | ) | $ | (1,303 | ) | $ | (1,803 | ) | $ | (3,237 | ) | $ | (2,378 | ) | ||||

Net cash used for financing activities (c) | $ | (643 | ) | $ | (1,310 | ) | $ | (1,027 | ) | $ | 309 | $ | (325 | ) | |||||

Adjusted EBITDA (b) | $ | 3,501 | $ | 3,642 | $ | 3,958 | $ | 3,804 | $ | 3,537 | |||||||||

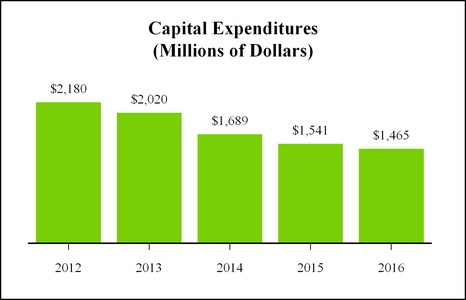

Capital expenditures | $ | 1,465 | $ | 1,541 | $ | 1,689 | $ | 2,020 | $ | 2,180 | |||||||||

Acquisitions, net of cash acquired | $ | 363 | $ | 82 | $ | 206 | $ | 1,323 | $ | 280 | |||||||||

After-tax return on capital (b) | 12.0 | % | 12.6 | % | 12.7 | % | 12.8 | % | 13.9 | % | |||||||||

Return on equity (b) | 31.9 | % | 34.6 | % | 28.7 | % | 28.6 | % | 28.9 | % | |||||||||

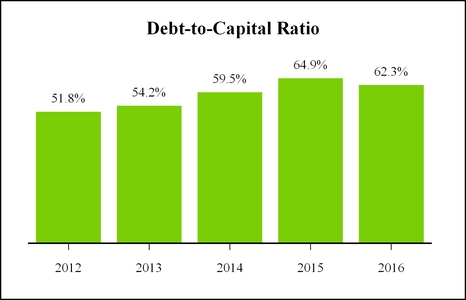

Debt-to-capital ratio (b) | 62.3 | % | 64.9 | % | 59.5 | % | 54.2 | % | 51.8 | % | |||||||||

Debt-to-adjusted EBITDA (b) | 2.6 | 2.5 | 2.3 | 2.2 | 1.9 | ||||||||||||||

Shares outstanding (000’s) | 284,901 | 284,879 | 289,262 | 294,134 | 296,229 | ||||||||||||||

Number of employees | 26,498 | 26,657 | 27,780 | 27,560 | 26,539 | ||||||||||||||

________________________

(a) | Amounts for 2016 include: (i) a $16 million charge to interest expense ($10 million after–tax, or $0.04 per diluted share) related to the redemption of the $325 million 5.20% notes due 2017, (ii) a pre–tax pension settlement charge of $4 million ($3 million after–tax, or $0.01 per diluted share) related to lump sum benefit payments made from the U.S. supplemental pension plan, and (iii) pre–tax charges of $96 million ($63 million after–tax and non–controlling interests, or $0.22 per diluted share) primarily related to cost reduction actions. |

15

Amounts for 2015 include: (i) a pre-tax charge of $165 million ($125 million after-tax, or $0.43 per diluted share) related to the cost reduction program and other charges; and (ii) a pre-tax charge of $7 million ($5 million after-tax, or $0.02 per diluted share) related to a pension settlement.

Amounts for 2014 include: (i) a pre-tax charge of $131 million ($131 million after-tax, or $0.45 per diluted share) related to the Venezuela currency devaluation, (ii) a pre-tax charge of $7 million ($5 million after-tax, or $0.02 per diluted share) related to pension settlements; and (iii) a pre-tax charge of $36 million ($22 million after-tax, or $0.07 per diluted share) related to a bond redemption.

Amounts for 2013 include: (i) a pre-tax charge of $23 million ($23 million after-tax, or $0.08 per diluted share) related to the Venezuela currency devaluation; (ii) a pre-tax charge of $9 million ($6 million after-tax, or $0.02 per diluted share) related to pension settlements; (iii) an income tax benefit of $40 million ($24 million net of noncontrolling interests, or $0.08 per diluted share) related to a realignment of the Italian legal structure; and (iv) a pre-tax charge of $18 million ($12 million after-tax, or $0.04 per diluted share) related to a bond redemption.

Amounts for 2012 include: (i) a pre-tax charge of $56 million, ($38 million after-tax and non-controlling interests, or $0.12 per diluted share) related to the 2012 cost reduction program; (ii) a pre-tax charge of $9 million ($6 million after-tax, or $0.02 per diluted share) related to pension settlement; and (iii) an income tax benefit of $55 million ($0.18 per diluted share) related to a loss on a liquidated subsidiary as a result of the divestiture of the U.S. Homecare business.

See Notes 2, 5, 11 and 16 to the consolidated financial statements.

(b) Non-GAAP measures. See the “Non-GAAP Financial Measures” section in Item 7 for definitions and reconciliation to reported amounts.

(c) | During 2016, Praxair adopted the FASB's standard for Improvements to Employee Share-Based Payment Accounting. As a result of the standard, withholding tax payments related to stock compensation are required to be presented as financing versus operating cash flows on a retrospective basis (see Note 1 to the consolidated financial statements). |

16

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion of the company’s financial condition and results of operations should be read together with its consolidated financial statements and notes to the consolidated financial statements included in Item 8 of this Form 10-K.

Page | |

Business Overview | |

Executive Summary – Financial Results & Outlook | |

Consolidated Results and Other Information | |

Segment Discussion | |

Liquidity, Capital Resources and Other Financial Data | |

Contractual Obligations | |

Off-Balance Sheet Arrangements | |

Critical Accounting Policies | |

New Accounting Standards | |

Fair Value Measurements | |

Non-GAAP Financial Measures | |

Forward-Looking Statements | |

BUSINESS OVERVIEW

Praxair is a leading industrial gas company in North and South America and one of the largest worldwide. The Company's primary products in its industrial gases business are atmospheric gases (oxygen, nitrogen, argon, rare gases) and process gases (carbon dioxide, helium, hydrogen, electronic gases, specialty gases, acetylene). The company also designs, engineers, and builds equipment that produces industrial gases primarily for internal use. The company’s surface technologies segment supplies wear-resistant and high-temperature corrosion-resistant metallic and ceramic coatings and powders. Praxair Surface Technologies supplies high-performance coatings that protect metal parts from wear, corrosion and high heat. Praxair’s industrial gas operations are managed on a geographical basis and in 2016, 94% of sales were generated in four geographic segments (North America, Europe, South America, and Asia). The surface technologies segment generated the remaining 6% of sales.

Praxair serves a diverse group of industries including healthcare, petroleum refining, manufacturing, food, beverage carbonation, fiber-optics, steel making, aerospace, chemicals and water treatment. The diversity of end-markets creates financial stability for Praxair in varied business cycles.

Praxair generates most of its revenues and earnings in the following 12 core geographies where the company has its strongest market positions and where distribution and production operations allow the company to deliver the highest level of service to its customers at the lowest cost.

North America | South America | Europe | Asia | |||

United States | Brazil | Spain | China | |||

Canada | Italy | India | ||||

Mexico | Germany/Benelux | Korea | ||||

Scandinavia | Thailand | |||||

Praxair manufactures and distributes its products through networks of hundreds of production plants, pipeline complexes, distribution centers and delivery vehicles. Major pipeline complexes are located in the United States, Brazil, Spain and Germany. These networks are a competitive advantage, providing the foundation of reliable product supply to the company’s customer base. The majority of Praxair’s business is conducted through long-term contracts which provide stability in cash flow and the ability to pass through changes in energy and feedstock costs to customers. The company has growth opportunities in all major geographies and in diverse end-markets such as energy, chemicals, metals, healthcare, food and beverage, and aerospace.

17

EXECUTIVE SUMMARY – FINANCIAL RESULTS & OUTLOOK

2016 Year in review

Praxair delivered solid results for the full year of 2016 despite continued challenging global macro-economic trends and foreign currency headwinds. Volume growth from food and beverage and healthcare end-markets and new project start-ups largely in Asia, Europe and South America was offset by weaker volumes in North and South America, primarily manufacturing and up-stream energy end-markets. Excluding foreign currency headwinds, sales growth came from higher overall pricing and acquisitions. Operating cash flow was 3% higher than 2015 despite lower net income from currency and base volume headwinds.

• | Sales of $10,534 million were 2% below 2015 sales of $10,776 million. Excluding negative currency impacts which reduced sales by 3%, and lower cost pass-through, sales were 2% above the prior year due to growth from positive price, new project start-ups and acquisitions. These increases were partially offset by lower base volumes primarily in North America due to weaker upstream energy and manufacturing end-markets. |

• | Reported operating profit of $2,238 million was 4% below 2015. Adjusted operating profit of $2,338 million was 6% below adjusted operating profit in 2015, and 3% below the prior year excluding negative currency translation. Benefits from project start-ups, acquisitions net of divestitures, higher price, and cost reduction programs were more than offset by the impact of lower base volumes.* |

• | Reported net income – Praxair, Inc. of $1,500 million and diluted earnings per share of $5.21 decreased from $1,547 million and $5.35, respectively, in 2015. Adjusted net income – Praxair, Inc. of $1,576 million and adjusted diluted earnings per share of $5.48 were both 6% below 2015 adjusted amounts.* |

• | Cash flow from operations was a strong $2,773 million, 26% of sales. Capital expenditures were $1,465 million and acquisitions, net of cash acquired were $363 million primarily for investments in growth and density; dividends paid were $856 million; and net common stock purchases were $89 million. |

• | We announced a non-binding agreement in principle to merge with Linde AG. |

2017 Outlook

• | Diluted earnings per share are forecasted to be in the range of $5.45 to $5.80. 2017 EPS guidance does not include transaction costs related to the potential Linde merger. |

• | Effective tax rate of approximately 28%. |

• | Capital expenditures of approximately $1.4 billion. |

• | The company’s core business is to build, own, and operate industrial gas plants in order to supply atmospheric and process gases to customers. As such, Praxair believes that its project backlog is one indicator of future sales growth. At December 31, 2016, Praxair’s backlog of 16 large projects under construction was $1.5 billion. This represents the total estimated capital cost of large plants under construction. North America represents about 80 percent of the backlog, with the majority located in the U.S. Gulf Coast. The remaining backlog resides in Asia, Europe, and South America. These plants will supply customers in the energy, chemical, manufacturing, electronics and metals markets. |

* A reconciliation of the Adjusted amounts can be found in the "Non-GAAP Financial Measures" section in this MD&A. See Notes 2, 5, 11 and 16 to the consolidated financial statements.

The above guidance should be read in conjunction with the section entitled “Forward-Looking Statements.”

Praxair provides quarterly updates on operating results, material trends that may affect financial performance, and financial earnings guidance via earnings releases and investor teleconferences. These materials are available on the company’s website, www.praxair.com/investors but are not incorporated herein.

18

CONSOLIDATED RESULTS AND OTHER INFORMATION

The following table provides selected data for 2016, 2015, and 2014:

Variance | |||||||||||||||||

(Dollar amounts in millions, except per share data) Year Ended December 31, | 2016 | 2015 | 2014 | 2016 vs. 2015 | 2015 vs. 2014 | ||||||||||||

Reported Amounts: | |||||||||||||||||

Sales | $ | 10,534 | $ | 10,776 | $ | 12,273 | (2 | )% | (12 | )% | |||||||

Cost of sales, exclusive of depreciation and amortization | $ | 5,860 | $ | 5,960 | $ | 6,962 | (2 | )% | (14 | )% | |||||||

Gross margin (a) | $ | 4,674 | $ | 4,816 | $ | 5,311 | (3 | )% | (9 | )% | |||||||

As a percent of sales | 44.4 | % | 44.7 | % | 43.3 | % | |||||||||||

Selling, general and administrative | $ | 1,145 | $ | 1,152 | $ | 1,308 | (1 | )% | (12 | )% | |||||||

As a percent of sales | 10.9 | % | 10.7 | % | 10.7 | % | |||||||||||

Depreciation and amortization | $ | 1,122 | $ | 1,106 | $ | 1,170 | 1 | % | (5 | )% | |||||||

Cost reduction program and other charges (b) | $ | 100 | $ | 172 | $ | 138 | |||||||||||

Other income (expense) – net | $ | 23 | $ | 28 | $ | 9 | |||||||||||

Operating profit | $ | 2,238 | $ | 2,321 | $ | 2,608 | (4 | )% | (11 | )% | |||||||

Operating margin | 21.2 | % | 21.5 | % | 21.2 | % | |||||||||||

Interest expense – net | $ | 190 | $ | 161 | $ | 213 | 18 | % | (24 | )% | |||||||

Effective tax rate | 26.9 | % | 28.3 | % | 28.9 | % | |||||||||||

Income from equity investments | $ | 41 | $ | 43 | $ | 42 | (5 | )% | 2 | % | |||||||

Noncontrolling interests | $ | (38 | ) | $ | (44 | ) | $ | (52 | ) | (14 | )% | (15 | )% | ||||

Net income – Praxair, Inc. | $ | 1,500 | $ | 1,547 | $ | 1,694 | (3 | )% | (9 | )% | |||||||

Diluted earnings per share | $ | 5.21 | $ | 5.35 | $ | 5.73 | (3 | )% | (7 | )% | |||||||

Diluted shares outstanding | 287,757 | 289,055 | 295,608 | — | % | (2 | )% | ||||||||||

Number of employees | 26,498 | 26,657 | 27,780 | ||||||||||||||

Adjusted Amounts (c): | |||||||||||||||||

Operating profit | $ | 2,338 | $ | 2,493 | $ | 2,746 | (6 | )% | (9 | )% | |||||||

Operating margin | 22.2 | % | 23.1 | % | 22.4 | % | |||||||||||

Interest expense – net | $ | 174 | $ | 161 | $ | 177 | 8 | % | (9 | )% | |||||||

Effective tax rate | 27.1 | % | 28.0 | % | 27.5 | % | |||||||||||

Noncontrolling interests | $ | (43 | ) | $ | (45 | ) | $ | (52 | ) | (4 | )% | (13 | )% | ||||

Net income – Praxair, Inc. | $ | 1,576 | $ | 1,677 | $ | 1,852 | (6 | )% | (9 | )% | |||||||

Diluted earnings per share | $ | 5.48 | $ | 5.80 | $ | 6.27 | (6 | )% | (7 | )% | |||||||

________________________

(a) | Gross margin excludes depreciation and amortization expense. |

(b) | See Note 2 to the consolidated financial statements. |

(c) | Adjusted amounts are non-GAAP measures. A reconciliation of reported amounts to adjusted amounts can be found in the “Non-GAAP Financial Measures” section of this MD&A. See Notes 2, 5, 11 and 16 to the consolidated financial statements. |

19

Results of Operations

The following table provides a summary of changes in consolidated sales and adjusted operating profit:

2016 vs. 2015 | 2015 vs. 2014 | |||||||||||

% Change | % Change | |||||||||||

Sales | Operating Profit | Sales | Operating Profit | |||||||||

Factors Contributing to Changes | ||||||||||||

Volume | — | % | (5 | )% | (2 | )% | (5 | )% | ||||

Price/Mix | 1 | % | 3 | % | 1 | % | 6 | % | ||||

Cost pass-through | (1 | )% | — | % | (2 | )% | — | % | ||||

Currency | (3 | )% | (3 | )% | (10 | )% | (10 | )% | ||||

Acquisitions/Divestitures | 1 | % | — | % | 1 | % | — | % | ||||

Other | — | % | 1 | % | — | % | (2 | )% | ||||

Reported | (2 | )% | (4 | )% | (12 | )% | (11 | )% | ||||

Add: Cost reduction program and other charges and pension settlement | — | % | (2 | )% | — | % | 2 | % | ||||

Adjusted | (2 | )% | (6 | )% | (12 | )% | (9 | )% | ||||

The following tables provide consolidated sales by end-market and distribution method:

% of Sales | % Change* | ||||||||||||||

2016 | 2015 | 2014 | 2016 vs. 2015 | 2015 vs. 2014 | |||||||||||

Sales by End-Markets | |||||||||||||||

Manufacturing | 23 | % | 24 | % | 24 | % | (5 | )% | (4 | )% | |||||

Metals | 17 | % | 17 | % | 17 | % | 4 | % | (2 | )% | |||||

Energy | 12 | % | 13 | % | 14 | % | (6 | )% | (2 | )% | |||||

Chemicals | 10 | % | 10 | % | 10 | % | — | % | (3 | )% | |||||

Electronics | 8 | % | 8 | % | 7 | % | 2 | % | 5 | % | |||||

Healthcare | 8 | % | 8 | % | 8 | % | 6 | % | 4 | % | |||||

Food & Beverage | 9 | % | 9 | % | 8 | % | 7 | % | 7 | % | |||||

Aerospace | 3 | % | 3 | % | 3 | % | 2 | % | 3 | % | |||||

Other | 10 | % | 8 | % | 9 | % | 1 | % | (8 | )% | |||||

100 | % | 100 | % | 100 | % | ||||||||||

* Excludes impact of currency, natural gas/precious metals cost pass-through and acquisitions/divestitures.

% of Sales | |||||||||

2016 | 2015 | 2014 | |||||||

Sales by Distribution Method | |||||||||

On-Site | 29 | % | 29 | % | 29 | % | |||

Merchant | 35 | % | 34 | % | 34 | % | |||

Packaged Gas | 28 | % | 28 | % | 28 | % | |||

Other | 8 | % | 9 | % | 9 | % | |||

100 | % | 100 | % | 100 | % | ||||

20

2016 Compared With 2015

Sales decreased 2% to $10,534 million in 2016 compared to $10,776 million in 2015. The decrease is primarily due to negative currency translation impacts of 3% and lower cost pass-through which reduced sales by 1%. Excluding these impacts, sales increased 2% compared to prior year. Higher pricing, primarily in North and South America, and acquisitions, largely in Europe, each contributed 1% to sales.

Gross margin decreased $142 million, or 3%, versus 2015 primarily due to lower sales. Gross margin as a percentage of sales declined to 44.4% in 2016 from 44.7% in 2015.

Selling, general and administrative ("SG&A") expenses decreased $7 million or 1% in 2016 to $1,145 million, or 10.9% of sales, versus $1,152 million, or 10.7% of sales, for 2015. Currency impacts decreased SG&A by $31 million. Excluding currency impacts, SG&A increased $24 million driven by acquisitions, cost inflation and higher incentive compensation partially offset by benefits from cost reduction programs.

Depreciation and amortization expense increased $16 million versus 2015. This increase was primarily due to plant start ups and acquisitions partially offset by currency effects.

During the year ended December 31, 2016, Praxair recorded charges of $100 million related primarily to a cost reduction program. This program is expected to result in annualized pre-tax expense reductions and cash flows increases of approximately $45 million. During 2015, Praxair recorded charges of $146 million in the second quarter and $26 million in the third quarter also related primarily to a cost reduction program. The 2015 cost reduction actions are expected to result in annualized pre-tax expense reductions and cash flow increases of approximately $80 million. To date, the expected benefits of the 2015 and 2016 cost reduction programs have met expectations, excluding any currency translation impacts (refer to Note 2 to the consolidated financial statements).

Other income (expenses) – net in 2016 was a $23 million benefit versus a $28 million benefit in 2015 (see Note 7 to the consolidated financial statements for a summary of major components). Other income in 2016 is largely related to net gains on asset sales. Other income in 2015 includes a $28 million gain from the sale of a packaged gas business in the United States.

Reported operating profit of $2,238 million in 2016 was $83 million, or 4% lower than reported operating profit of $2,321 million in 2015. 2016 included charges of $96 million related to cost reduction actions and other charges and a $4 million charge related to a pension settlement. 2015 included a $165 million charge related to cost reduction actions and other charges and a $7 million charge related to a pension settlement. Refer to Note 2 of the consolidated financial statements for a further discussion of these items. Excluding the impact of these items, adjusted operating profit of $2,338 million in 2016 was $155 million, or 6% lower than adjusted operating profit of $2,493 million in 2015. Benefits from project start-ups, acquisitions net of divestitures, higher price, and cost reduction programs were more than offset by the impact of lower base volumes. A discussion of operating profit by segment is included in the segment discussion that follows.

Reported interest expense – net in 2016 increased $29 million, versus 2015. 2016 included charges of $16 million relating to the early redemption of notes (see Note 11 to the consolidated financial statements). Excluding this charge, adjusted interest expense increased $13 million largely attributable to higher average interest rates due primarily to extending debt maturities. See Note 7 to the consolidated financial statements for further information relating to interest expense.

The reported effective tax rate ("ETR") for 2016 was 26.9% versus 28.3% in 2015. The ETR for the 2016 period includes a $35 million tax benefit related to a pension settlement, bond redemption and cost reduction program and other charges. The 2015 period includes a $41 million tax benefit related to a pension settlement and cost reduction program and other charges (see Note 2 to the consolidated financial statements). Excluding these impacts, on an adjusted basis the ETR for the 2016 and 2015 periods was 27.1% and 28.0%, respectively. The decrease in the adjusted ETR is primarily due to a $20 million excess tax benefit on share–based compensation resulting from the adoption of a new accounting standard during 2016 (see Note 1 to the consolidated financial statements).