Attached files

| file | filename |

|---|---|

| EX-99.A - RESERVE AUDIT - ENERGEN CORP | egn123116ex99a.htm |

| EX-32 - ENERGEN CORPORATION 18 U.S.C. SECTION 1350 CERTIFICATION - ENERGEN CORP | egn12312016ex32.htm |

| EX-31.B - ENERGEN CORPORATION CERTIFICATION OF CFO - ENERGEN CORP | egn12312016ex31b.htm |

| EX-31.A - ENERGEN CORPORATION CERTIFICATION OF CEO - ENERGEN CORP | egn12312016ex31a.htm |

| EX-24 - POWER OF ATTORNEY - ENERGEN CORP | egn12312016ex24.htm |

| EX-23.B - CONSENT OF INDEPENDENT OIL AND GAS RESERVOIR ENGINEERS - ENERGEN CORP | egn12312016ex23b.htm |

| EX-23.A - CONSENT OF REGISTERED PUBLIC ACCOUNTING FIRM - ENERGEN CORP | egn12312016ex23a.htm |

| EX-21 - SUBSIDIARIES - ENERGEN CORP | egn12312016ex21.htm |

| EX-10.E - ENERGEN STOCK INCENTIVE PLAN - ENERGEN CORP | egn123116ex10e.htm |

| EX-10.D - SEVERANCE COMPENSATION AGREEMENT - ENERGEN CORP | egn123116ex10d.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE YEAR ENDED DECEMBER 31, 2016 |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM ___ TO ___ |

Commission file number 1-7810

Energen Corporation

(Exact name of registrant as specified in its charter)

Alabama | 63-0757759 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

605 Richard Arrington Jr. Boulevard North, Birmingham, Alabama | 35203-2707 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code

(205) 326-2700

Securities Registered Pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.01 par value | New York Stock Exchange | |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES x NO o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES o NO x

Indicate by a check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO o

Indicate by a check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer o Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO x

Aggregate market value of the voting stock held by non-affiliates of the registrant as of June 30, 2016: $4,616,230,556

Number of shares outstanding of the registrant’s common stock as of February 14, 2017: 97,187,767 shares

DOCUMENTS INCORPORATED BY REFERENCE

Energen Corporation Proxy Statement to be filed on or about March 22, 2017 (Part III, Item 10-14)

ENERGEN CORPORATION 2016 FORM 10-K ANNUAL REPORT | ||

TABLE OF CONTENTS | ||

Page | ||

Industry Glossary | ||

Cautionary Statement Regarding Forward-Looking Statements | ||

PART I | ||

Item 1. | Business | |

Item 1A. | Risk Factors | |

Item 1B. | Unresolved Staff Comments | |

Item 2. | Properties | |

Item 3. | Legal Proceedings | |

Item 4. | Mine Safety Disclosures | |

PART II | ||

Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer | |

Purchases of Equity Securities | ||

Item 6. | Selected Financial Data | |

Item 7. | Management’s Discussion and Analysis of Financial Condition and | |

Results of Operations | ||

Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | |

Item 8. | Financial Statements and Supplementary Data | |

Item 9. | Changes in and Disagreements with Accountants on Accounting and | |

Financial Disclosure | ||

Item 9A. | Controls and Procedures | |

PART III | ||

Item 10. | Directors, Executive Officers and Corporate Governance | |

Item 11. | Executive Compensation | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and | |

Related Stockholder Matters | ||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

Item 14. | Principal Accountant Fees and Services | |

PART IV | ||

Item 15. | Exhibits and Financial Statement Schedules | |

Signatures | ||

2

INDUSTRY GLOSSARY For a more complete definition of certain terms defined below, as well as other terms and concepts applicable to successful efforts accounting, please refer to Rule 4-10(a) of Regulation S-X, promulgated pursuant to the Securities Act of 1933 and the Securities Exchange Act of 1934, each as amended. | |

Basin | A large natural depression on the earth’s surface in which sediments accumulate. |

Basis | The difference between the futures price for a commodity and the corresponding cash spot price. This commonly is related to factors such as product quality, location and contract pricing. |

Basin Specific | A type of derivative contract whereby the contract’s settlement price is based on specific geographic basin indices. |

Bbl | A standard barrel containing 42 United States gallons. |

Bcf | One billion cubic feet of natural gas. |

BOE | One barrel of oil equivalent, a standard conversion used to express oil and natural gas volumes on a comparable oil equivalent basis. Natural gas equivalents are determined under the relative energy content method by using the ratio of six Mcf of natural gas to one barrel of oil. |

Collar | A contractual arrangement that effectively establishes a price range between a floor and a ceiling for the underlying commodity. The purchaser bears the risk of fluctuation between the minimum (or floor) price and the maximum (or ceiling) price. |

Completion | The process of treating a drilled well followed by the installation of permanent equipment for the production of oil or natural gas or, in the case of a dry hole, the reporting of abandonment to the appropriate agency. |

Development Costs | Costs necessary to gain access to, prepare and equip development wells in areas of proved reserves. |

Development Well | A well drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive. |

Downspacing | An increase in the number of available drilling locations as a result of a regulatory commission order. |

Dry Well | An exploratory or a development well found to be incapable of producing either oil or natural gas in sufficient quantities to justify completion as an oil or natural gas well. |

Exploration Expenses | Costs primarily associated with drilling unsuccessful exploratory wells in undeveloped properties or exploratory geological and geophysical activities. |

Exploratory Well | A well drilled to find and produce oil or natural gas in an unproved area, to find a new reservoir in a field previously found to be productive of oil or natural gas in another reservoir, or to extend a known reservoir. |

Field | An area consisting of a single reservoir or multiple reservoirs, all grouped on or related to the same individual geological structural feature and/or stratigraphic condition. |

Futures Contract | An exchange-traded contractual arrangement to buy or sell a standard quantity and quality of a commodity at a specified future date and price. Such contracts offer liquidity and minimal credit risk exposure but lack the flexibility of swap contracts. |

Hedging | The use of derivative commodity instruments such as futures, swaps, options and collars to help reduce financial exposure to commodity price volatility. |

Horizontal Drilling | A drilling technique used in certain formations where a well is drilled vertically to a certain depth and then drilled at a right angle with a specified interval. |

Hydraulic Fracturing | The process of creating and preserving a fracture or system of fractures in a reservoir rock typically by injecting a fluid under pressure through a wellbore and into the targeted formation. |

Gross Well or Acre | A well or acre in which a working interest is owned. |

LIBOR | London Interbank Offered Rate. |

MBbl | One thousand barrels of oil. |

MBOE | One thousand BOE. |

MBOE/d | One thousand BOE per day. |

Mcf | One thousand cubic feet of natural gas. |

MMBOE | One million BOE. |

3

MMcf | One million cubic feet of natural gas. |

MMcfe | One million cubic feet of natural gas equivalent. |

MMgal | One million gallons of natural gas liquids. |

Natural Gas Liquids (NGL) | Liquid hydrocarbons that are extracted and separated from the natural gas stream. NGL products include ethane, propane, butane, natural gasoline and other hydrocarbons. |

Net Well or Acre | A net well or acre is deemed to exist when the sum of fractional ownership working interests in gross wells or acres equals one. |

NYMEX | New York Mercantile Exchange. |

Operational Enhancement | Any action undertaken to improve production efficiency of oil and natural gas wells and/or reduce well costs. |

Operator | The company responsible for exploration, development and production activities for a specific project. |

Pay-Add | An operation within a currently producing wellbore that attempts to access and complete an additional pay zone(s) while maintaining production from the existing completed zone(s). |

Pay Zone | The stratigraphic horizon from which oil and natural gas is produced. |

Production (Lifting) Costs | Costs incurred to operate and maintain wells. |

Productive Well | An exploratory or a development well that is not a dry well. |

Proved Developed Reserves | The portion of proved reserves which can be expected to be recovered through existing wells with existing equipment and operating methods. |

Proved Reserves | Estimated quantities of crude oil, natural gas and natural gas liquids that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions. |

Proved Reserves-to-Production Ratio | Ratio expressing years of supply determined by dividing the remaining recoverable proved reserves at year end by actual annual production volumes. The reserve-to-production ratio is a statistical indicator with certain limitations, including predictive value. The ratio varies over time as changes occur in production levels and remaining recoverable proved reserves. |

Proved Undeveloped Reserves (PUD) | The portion of proved reserves which can be expected to be recovered from new wells on undrilled proved acreage or from existing wells where a relatively major expenditure is required for completion. |

Recompletion | An operation within an existing wellbore whereby a completion in one pay zone is abandoned in order to attempt a completion in a different pay zone. |

Reservoir | A porous and permeable underground formation containing a natural accumulation of producible natural gas and/or oil that is confined by impermeable rock or water barriers and is separate from other reservoirs. |

SEC | The United States Securities and Exchange Commission. |

Service Well | A well employed for the introduction into an underground stratum of water, gas or other fluid under pressure or disposal of salt water produced with oil or other waste. |

Sidetrack Well | A new section of wellbore drilled from an existing well. |

Swap | A contractual arrangement in which two parties, called counterparties, effectively agree to exchange or “swap” variable and fixed rate payment streams based on a specified commodity volume. The contracts allow for flexible terms such as specific quantities, settlement dates and location but also expose the parties to counterparty credit risk. |

Undeveloped Acreage | Lease acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and natural gas regardless of whether such acreage contains proved reserves. |

Working Interest | Ownership interest in the oil and natural gas properties that is burdened with the cost of development and operation of the property. |

Workover | A major remedial operation on a completed well to restore, maintain, or improve the well’s production such as deepening the well or plugging back to produce from a shallow formation. |

4

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

All statements, other than statements of historical fact, appearing in this report constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are noted in Energen’s disclosure and analysis as permitted by the Private Securities Litigation Reform Act of 1995. These forward-looking statements include, among other things, statements about our expectations, beliefs, intentions or business strategies for the future, statements concerning our outlook with regard to the timing and amount of future production of oil, natural gas liquids and natural gas, price realizations, the nature and timing of capital expenditures for exploration and development, plans for funding operations and drilling program capital expenditures, the timing and success of specific projects, operating costs and other expenses, proved oil and natural gas reserves, liquidity and capital resources, outcomes and effects of litigation, claims and disputes and derivative activities. In particular, forward-looking statements may include words such as “anticipate”, “believe”, “could”, “estimate”, “expect”, “forecast”, “foresee”, “intend”, “may”, “plan”, “potential”, “predict”, “project”, “seek”, “will” or other words or expressions concerning matters that are not historical facts. These statements involve certain risks and uncertainties that may cause actual results to differ materially from expectations as of the date of this filing.

Factors that could cause actual results to differ materially from those expressed or implied by forward-looking statements include, but are not limited to, the following:

• | volatility of oil, natural gas liquids and natural gas prices; |

• | uncertainties about the estimates of our proved oil, natural gas liquids and natural gas reserves; |

• | drilling risks; |

• | risks associated with our concentration of operations in the Permian Basin of west Texas and New Mexico; |

• | competition in the oil and natural gas industry; |

• | the adequacy of our capital resources, access to financing and liquidity; |

• | operational risks including risks of personal injury, property damage and environmental damage; |

• | changes in the regulatory environment at the federal, state, or local level and our ability to comply with regulations promulgated by the various regulatory bodies; |

• | changes in and the effects of environmental and other governmental regulation that applies to our operations, including new legislation or regulation of hydraulic fracturing, water use and disposal, permitting, climate change and other legal requirements; |

• | instability in the domestic and global capital and credit markets; |

• | financial strength of the parties with whom we do business, including other working interest owners, providers of midstream services, providers of oilfield services, purchasers of our oil, natural gas liquids and natural gas and the counterparties to our derivative contracts; |

• | changes in domestic and global economic and business conditions that impact the demand for oil, natural gas liquids and natural gas; |

• | changes in domestic and global supplies of oil, natural gas and natural gas liquids arising from economic and business conditions (including actions by the Organization of the Petroleum Exporting Countries); |

• | uncertainties about our ability to successfully execute our business and financial plans and strategies, including but not limited to our ability to economically develop our proved oil, natural gas liquids and natural gas reserves and to replace those reserves as scheduled as well our ability to project future rates of production and the timing of development expenditures; |

• | risks associated with our ability to execute on property acquisitions and divestitures including market liquidity, price levels, timing and financing associated with such transactions; |

• | the effectiveness of and our ability to use derivative instruments as part of our risk management activities; |

• | the costs and effects of litigation; and |

• | acts of nature, sabotage, terrorism or other malicious intentional acts (including cyber-attacks), war and other similar acts that disrupt operations or cause damage greater than covered by insurance. |

5

See Item 1A, Risk Factors, for a discussion of risk factors that may affect Energen and cause material variances from forward-looking statement expectations. The Item 1A, Risk Factors, discussion is incorporated by reference into this forward-looking statement disclosure.

Except as otherwise disclosed, the forward-looking statements do not reflect the impact of possible or pending acquisitions, investments, divestitures or restructurings. The absence of errors in input data, calculations and formulas used in estimates, assumptions and forecasts cannot be guaranteed. We base our forward-looking statements on information currently available to us, and we undertake no obligation to update or revise any of these statements, whether as a result of changes in underlying factors, new information, future events or other developments.

6

PART I

ITEM 1. BUSINESS

General

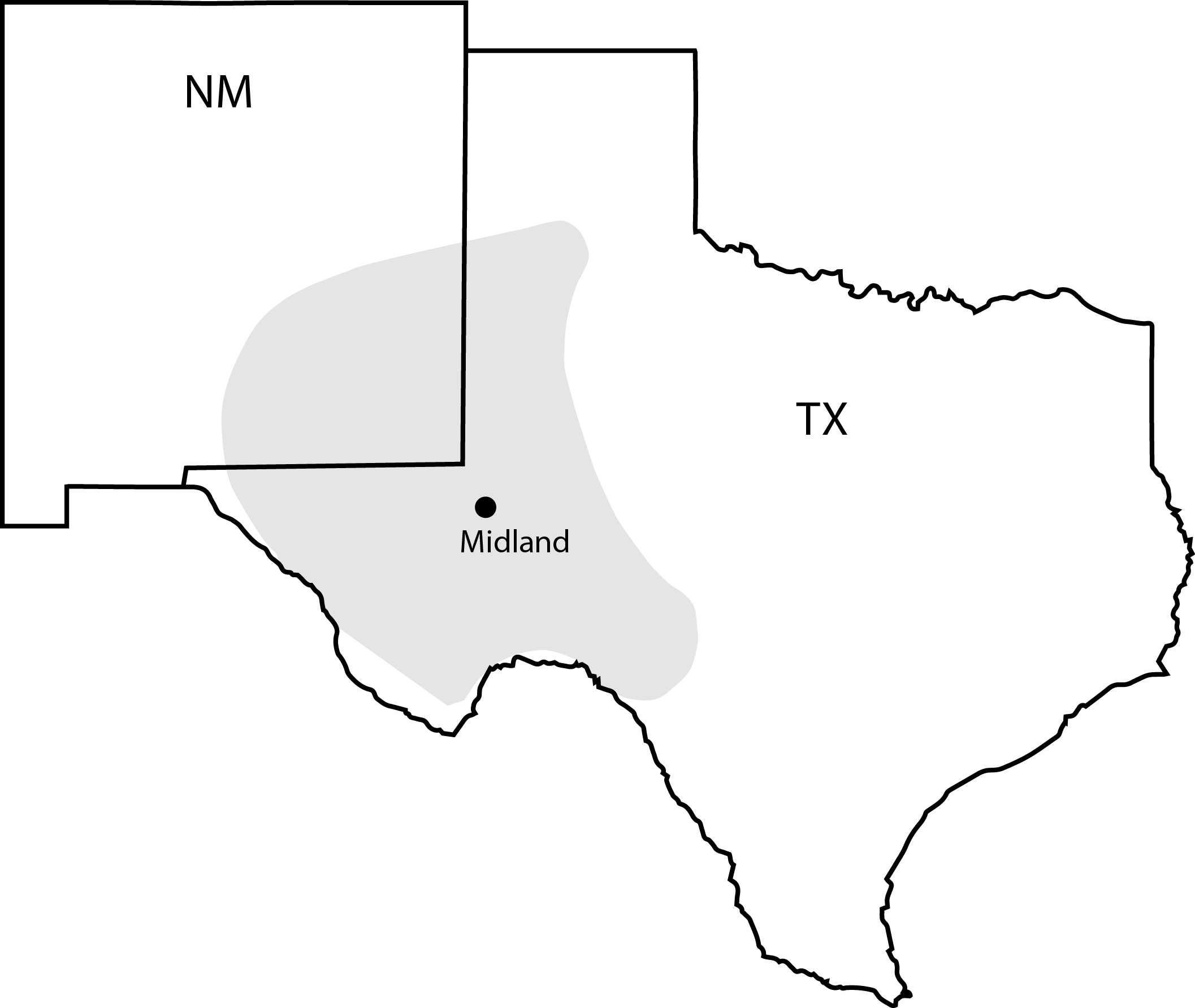

Energen Corporation (Energen or the Company) is an oil and natural gas exploration and production company engaged in the exploration, development and production of oil, natural gas liquids and natural gas. Our operations are conducted through our subsidiary, Energen Resources Corporation (Energen Resources) and primarily occur within the Midland Basin, the Delaware Basin and the Central Basin Platform areas of the Permian Basin in west Texas and New Mexico. Our corporate headquarters are located in Birmingham, Alabama.

Prior to September 2, 2014, Energen owned Alabama Gas Corporation (Alagasco), which was engaged in the purchase, distribution and sale of natural gas principally in central and north Alabama. On September 2, 2014, Energen completed the transaction to sell Alagasco to The Laclede Group, Inc. (Laclede) for $1.6 billion, less the assumption of $267 million in debt. The net pre-tax proceeds to Energen totaled approximately $1.32 billion resulting in a pre-tax gain of $726.5 million. This sale had an effective date of August 31, 2014. Energen used cash proceeds from the sale to reduce long-term and short-term indebtedness. During 2014, Energen classified Alagasco as held for sale and reflected the associated operating results in discontinued operations. See Note 16, Held for Sale Properties and Discontinued Operations, for further information regarding the sale of Alagasco.

Energen was incorporated in 1978 in connection with a corporate reorganization completed in 1979 which resulted in Energen becoming the parent company to Energen Resources, which was formed in 1971, and Alagasco. Alagasco was formed by merger in 1948. As noted above, Alagasco was sold in 2014 to Laclede.

Energen maintains a web site with the address www.energen.com. Information contained on this web site is not incorporated by reference into this report. Energen makes available free of charge through its web site the annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to these reports. Also, these reports are available in print upon shareholder request. These reports are available as soon as reasonably practicable after being electronically filed with or furnished to the Securities and Exchange Commission. Energen’s web site also includes its Business Conduct Guidelines, Corporate Governance Guidelines, Audit Committee Charter, Compensation Committee Charter and Governance and Nominations Committee Charter, each of which is available in print upon shareholder request.

Narrative Description of Business

• | Oil and Natural Gas Operations |

General: Energen’s operations focus on increasing production and adding proved reserves through the development of oil, natural gas liquids and natural gas properties. In addition, Energen explores for and develops new reservoirs, primarily in areas in which it has an operating presence. All oil, natural gas liquids and natural gas production is sold to third parties. Energen operates its properties for its own interest and that of its joint interest owners. This role includes overall project management and day-to-day decision-making relative to project operations.

At the end of 2016, Energen’s proved reserves totaled 316.3 MMBOE. Substantially all of these proved reserves are located in the Permian Basin in west Texas and New Mexico. Approximately 51 percent of Energen’s year-end proved reserves are proved developed reserves. Energen’s proved reserves are long-lived, with a year-end proved reserves-to-production ratio of 15 years. Oil, natural gas liquids and natural gas represent approximately 63 percent, 18 percent and 19 percent, respectively, of Energen’s proved reserves.

Property Acquisitions and Dispositions: During June, July and August of 2016, Energen completed a series of asset sales of certain non-core Permian Basin assets in the Delaware Basin in Texas and in the San Juan Basin in New Mexico for an aggregate purchase price of $552 million. These transactions had closing dates of June 3, 7, 30, July 15 and August 9 of 2016 with various effective dates ranging from March 1, 2016 to June 30, 2016. Minor portions of the assets were transferred to other parties upon the exercise of preferential purchase rights under pre-existing joint operating agreements in the ordinary course of business. Pre-tax proceeds to Energen were approximately $532.9 million after purchase price adjustments of approximately $19 million related to the operations of the properties subsequent to the effective dates and other one-time adjustments including transfer payments and certain amounts due the buyer, but before consideration of transaction costs of approximately $5 million. In the year ended December 31, 2016, Energen recognized pre-tax gains of $246.3 million on the sales. Energen used proceeds from the sale to fund ongoing operations.

7

In March 2015, Energen completed the sale of the majority of its natural gas assets in the San Juan Basin in New Mexico and Colorado (effective as of January 1, 2015) for an aggregate purchase price of $395 million. The sales proceeds were reduced by purchase price adjustments of approximately $11 million related to the operations of the San Juan Basin properties subsequent to December 31, 2014 and one-time adjustments related primarily to liabilities assumed by the buyer, which resulted in pre-tax proceeds to Energen of approximately $384 million before consideration of transaction costs of approximately $2.8 million. Energen recognized a pre-tax gain of $27.0 million on the sale. Energen used proceeds from the sale to reduce long-term indebtedness. At December 31, 2014, proved reserves associated with these San Juan Basin held for sale properties totaled 69,038 MBOE.

In March 2014, Energen completed the sale of its North Louisiana/East Texas natural gas and oil properties for $30.3 million. The sale had an effective date of December 1, 2013, and the proceeds from the sale were used to repay short-term obligations. During the third quarter of 2013, Energen classified these primarily natural gas properties as held for sale and reflected the associated operating results in discontinued operations.

Growth Strategy: Energen is focused on increasing its oil, natural gas liquids and natural gas production and proved reserves largely through active development and/or exploratory programs in the Permian Basin. The Company seeks to expand its footprint primarily through acquisitions of proved properties and unproved leasehold within areas of existing operations. Energen operated approximately 96 percent of its proved reserves at December 31, 2016.

Energen’s capital spending plans for 2017 target an investment of approximately $790 million (excluding acquisitions and lease renewals), the bulk of which will focus on drilling and development activities on its existing properties, all targeting the liquids-rich Permian Basin. Energen may choose to allocate additional capital during the year for property acquisitions and/or increased drilling and development activities.

Energen’s development activities can result in the addition of new proved reserves and can serve to reclassify proved undeveloped reserves to proved developed reserves. Proved reserve disclosures are provided annually, although changes to reserve classifications occur throughout the year. Accordingly, additions of new proved reserves from development activities can occur throughout the year and may result from numerous factors including, but not limited to, regulatory approvals for drilling unit downspacing that increase the number of available drilling locations; changes in the economic or operating environments that allow previously uneconomic locations to be added; technological advances that make reserve locations available for development; successful development of existing proved undeveloped reserve locations that reclassify adjacent probable locations to proved undeveloped reserve locations; increased knowledge of field geology and engineering parameters relative to oil and natural gas reservoirs; and changes in management’s intent to develop certain opportunities.

During the three years ended December 31, 2016, Energen’s development and exploratory efforts have added 327 MMBOE of proved reserves. During the same period, we drilled 623 gross development, exploratory and service wells (including one sidetrack well) and 73 well recompletions and pay-adds. In 2016, Energen’s successful development and exploratory wells and other activities added approximately 64 MMBOE of proved reserves; Energen drilled 87 gross development, exploratory and service wells (including no sidetrack wells), performed some 6 well recompletions and pay-adds, and conducted other operational enhancements. Energen’s production from continuing operations totaled 21.6 MMBOE in 2016. In 2017, production is estimated to be 24 MMBOE, including approximately 16.9 MMBOE of estimated production from proved reserves owned at December 31, 2016. Production estimates do not include amounts for potential future acquisitions.

Drilling Activity: The following table sets forth the total number of net productive and dry exploratory and development wells drilled:

Years ended December 31, | 2016 | 2015 | 2014 | |||

Development: | ||||||

Productive | 18.5 | 50.8 | 80.2 | |||

Dry | — | — | — | |||

Total | 18.5 | 50.8 | 80.2 | |||

Exploratory: | ||||||

Productive | 53.2 | 98.5 | 109.4 | |||

Dry | — | 2.0 | 1.0 | |||

Total | 53.2 | 100.5 | 110.4 | |||

8

Included in the 2016 net wells drilled above are 42 gross (41 net) drilled but uncompleted wells in the Midland Basin and 17 gross (17 net) drilled but uncompleted wells in the Delaware Basin, all of which we plan to complete in 2017. Included in the 2015 net wells drilled above are 2 gross (2 net) drilled but uncompleted wells in the Midland Basin, which we also plan to complete in 2017. As of December 31, 2016, Energen was participating in the drilling of 2 gross (2 net) development and 16 gross (13 net) exploratory wells. In addition to the development wells drilled, Energen drilled 3.0, 12.9 and 22.5 net service wells during 2016, 2015 and 2014, respectively. Energen had 1 gross service well (1 net) in process as of December 31, 2016.

Productive Wells and Acreage: The following table sets forth the total gross and net productive gas and oil wells as of December 31, 2016, and developed and undeveloped acreage as of the latest practicable date prior to year end:

Gross | Net | |||

Oil wells | 5,128 | 3,384 | ||

Gas wells | 133 | 23 | ||

Developed acreage | 329,224 | 226,635 | ||

Undeveloped acreage | 51,572 | 26,505 | ||

There were no wells with multiple completions at December 31, 2016. All wells and acreage are located onshore in the United States, with the majority of the net undeveloped acreage located in Texas and New Mexico.

Concentration of Credit Risk: Revenues and related accounts receivable from oil and natural gas operations primarily are generated from the sale of produced oil, natural gas liquids and natural gas to energy marketing companies. Such sales are typically made on an unsecured credit basis with payment due the month following delivery. This concentration of sales to the energy marketing industry has the potential to affect Energen’s overall exposure to credit risk, either positively or negatively, in that our oil, natural gas liquids and natural gas purchasers may be affected similarly by changes in economic, industry or other conditions. Energen considers the credit quality of its purchasers and, in certain instances, may require credit assurances such as a deposit, letter of credit or parent guarantee. The two largest purchasers of Energen’s oil, natural gas liquids and natural gas, Plains Marketing, LP (Plains) and Shell Trading (US) Company (Shell), accounted for approximately 50 percent and 20 percent, respectively, of Energen’s accounts receivable for commodity sales as of December 31, 2016. Energen’s other purchasers each accounted for less than 7 percent of these accounts receivable as of December 31, 2016. During the year ended December 31, 2016, Plains and Shell accounted for approximately 52 percent and 12 percent, respectively, of total revenues from oil, natural gas liquids and natural gas sales. All other oil and natural gas purchasers each accounted for less than 10 percent of total revenues for the year ended December 31, 2016.

Risk Management: Energen attempts to lower the commodity price risk associated with its oil and natural gas business through the use of swaps and basis swaps. Energen has policies in place to limit hedging to not more than 80 percent of its estimated annual production; however, Energen’s credit facility contains a covenant that operates to limit hedging at a lower threshold in certain circumstances. Energen recognizes all derivatives on the balance sheet and measures all derivatives at fair value.

See the Cautionary Statement Regarding Forward-Looking Statements preceding Item 1, Business, and Item 1A, Risk Factors, for further discussion with respect to price and other risks.

• | Environmental Matters and Climate Change |

Various federal, state and local environmental laws and regulations apply to the operations of Energen. Historically, the cost of environmental compliance has not materially affected our financial position, results of operations or cash flows. New regulations, enforcement policies, claims for damages or other events could result in significant unanticipated costs.

Federal, state and local legislative bodies and agencies frequently exercise their respective authority to adopt new laws and regulations and to amend and interpret existing laws and regulations. Such law and regulation changes may occur with little prior notification, subject Energen to cost increases, and impose restrictions and limitations on our operations. Examples of law and regulatory changes with the potential to materially impact Energen include, but are not limited to, measures dealing with hydraulic fracturing, emission limits and reporting and the repeal of certain oil and natural gas tax incentives and deductions.

Energen regularly utilizes hydraulic fracturing in its drilling and completion activities. Energen’s first widespread use of hydraulic fracturing occurred during the 1980s in conjunction with the exploration and development of coalbed methane in Alabama’s Black Warrior Basin.

9

Hydraulic fracturing is a reservoir stimulation technique used throughout the oil and natural gas industry for more than 60 years. After a well has been drilled, hydraulic fracturing is used during the completion process to form small fractures in the target formation through which the oil and/or natural gas can flow. The fractures are created when a water-based fluid is pumped at a calculated rate and pressure into the crude oil- or natural gas-bearing rock. The fracture fluid is a mixture composed primarily of water and sand or inert ceramic, sand-like grains; it also contains a small percentage of special purpose chemical additives (which are highly diluted-typically less than one percent by volume) that can vary by project. The millimeter-thick cracks or fractures in the target formation are propped open by the sand, thereby allowing the crude oil or natural gas to flow from tight (low permeability) reservoirs into the well bore.

States in which we operate have adopted a variety of well construction, set back, and disclosure regulations limiting how drilling can be performed and requiring various degrees of chemical and water usage disclosure for operators that employ hydraulic fracturing. We are complying with these additional regulations as part of our routine operations and within the normal execution of our business plan. The adoption of additional federal or state regulations, however, could impose significant new costs and challenges. For example, adoption of new hydraulic fracturing permitting requirements could significantly delay or prevent new drilling. Adoption of new regulatory restrictions on the use of hydraulic fracturing could reduce the amount of oil and gas able to be recovered from our proved reserves. The degree to which additional oil and natural gas industry regulation may impact our future operations and results will depend on the extent to which we utilize the regulated activity and whether the geographic locations in which we operate are subject to the new regulation.

Existing federal, state and local environmental laws and regulations also have the potential to increase costs, reduce liquidity, delay operations and otherwise alter business operations. These existing laws and regulations include, but are not limited to, the Clean Air Act; the Clean Water Act; Oil Pollution Prevention: Spill Prevention, Control, and Countermeasure regulations; Toxic Substances Control Act; Resource Conservation and Recovery Act; and the Federal Endangered Species Act. Compliance with these and other environmental laws and regulations is undertaken as part of Energen’s routine operations. Energen does not separately track costs associated with these routine compliance activities.

Climate change, whether arising through natural occurrences or human activities, may have a significant impact upon the operations of Energen. Volatile weather patterns and the resulting environmental impact may adversely affect our results of operations, financial position and cash flows. We are unable to predict the timing or manifestation of climate change or reliably estimate the impact to Energen. However, climate change could affect our operations as follows:

• | sustained increases or decreases to the supply and demand of oil, natural gas liquids and natural gas; |

• | potential disruption to third-party facilities to which Energen delivers. Such facilities include third-party oil and gas gathering, transportation, processing and storage facilities and are typically limited in number and geographically concentrated. |

During January 2014, Energen Resources responded to a General Notice and Information Request from the Environmental Protection Agency regarding the Reef Environmental Site in Sylacauga, Talladega County, Alabama. The letter identifies Energen Resources as a potentially responsible party under The Comprehensive Environmental Response, Compensation, and Liability Act for the cleanup of the Site. In 2008, Energen hired a third party to transport approximately 3,000 gallons of non-hazardous wastewater to Reef Environmental for wastewater treatment. Reef Environmental ceased operating its wastewater treatment system in 2010. Due to its one time use of Reef Environmental for a small volume of non-hazardous wastewater, Energen Resources has not accrued a liability for cleanup of the Site.

• | Employees |

The Company has approximately 390 employees. On January 22, 2016 and March 18, 2016, we reduced our workforce as part of an overall plan to reduce costs and better align our workforce with the needs of our business. Energen believes that its relations with employees are good.

10

ITEM 1A. RISK FACTORS

The future success and continued viability of our business, like any venture, is subject to many recognized and unrecognized risks and uncertainties. Such risks and uncertainties could cause actual results to differ materially from those contained in forward-looking statements made in this report and presented elsewhere by management. The following list identifies and briefly summarizes certain risk factors. The list should not be viewed as complete or comprehensive, as the risks below are not the only risks facing Energen. Energen could also be affected by other risks and uncertainties in addition to those described herein. If any of the following risks were to occur, our business, financial condition or results of operations could be materially adversely affected; and such events could impair our ability to implement business plans or complete development activities as scheduled. Further, the trading price of our shares could decline, and shareholders could lose part or all of their investment. In addition, such risks may prevent us from complying with our financial and non-financial covenants and may result in a default under our credit facility or other long-term debt.

We undertake no obligation to correct or update such risk factors whether as a result of new information, future events or otherwise. These risk factors should be read in conjunction with our disclosure specific to forward-looking statements made elsewhere in this report under the heading Cautionary Statement Regarding Forward-Looking Statements.

Risks Related to Our Business

Commodity prices for crude oil and natural gas are volatile, and a substantial reduction in commodity prices could adversely affect our financial condition and results of operations.

Our revenues, cash flows and earnings are influenced predominantly by the amount of oil, natural gas liquids and natural gas we produce, net of the effects of settlements on our derivative commodity instruments, and the prices we receive for production. Oil, natural gas liquids and natural gas are commodities and historical markets for oil, natural gas liquids and natural gas have been volatile and prices are subject to wide fluctuations in response to relatively minor changes in supply and demand. For example, during the year ended December 31, 2016, commodity prices changed significantly, with the settlement price for West Texas Intermediate (WTI) crude oil ranging from a high of approximately $54.06 per barrel to a low of approximately $26.21 per barrel and settlement prices for Henry Hub natural gas ranging from a high of approximately $3.93 per Mcf to a low of approximately $1.64 per Mcf.

In addition to reducing our revenue, cash flows and earnings, low prices for oil, natural gas liquids and natural gas may adversely affect us in a variety of ways. For example, some of our exploration and development projects could become uneconomic and we may also have to make significant downward adjustments to our estimated proved reserves and our estimates of the present value of those reserves. If these price effects occur, or if our estimates of production or economic factors change, accounting rules may require us to writedown, as a noncash impairment loss in our statements of income, the carrying value of our proved oil and natural gas properties. Lower commodity prices may also result in a reduction in the amount we are permitted to borrow under our credit facility and adversely impact our ability to meet financial ratios contained in our debt agreements, especially those calculated by reference to the value of our reserves, earnings or cash flows, which could reduce the amount we are permitted to borrow under our credit facility or result in an event of default. We could also be required to reduce our capital spending on exploration and development, which will adversely affect our ability to replace our reserves and could result in the loss of leasehold. As more fully disclosed in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations under the heading “Credit Facility and Working Capital”, the Company discusses its plans regarding liquidity and covenant compliance for 2017.

Approximately 63 percent of our December 31, 2016 proved reserves are oil. As a result, changes in oil prices have a greater impact on our business than changes of comparable magnitude in natural gas prices. Commodity prices for oil, natural gas liquids and natural gas are reflections of supply and demand and are subject to many factors that are beyond our control, including:

• | the domestic and foreign supply of oil, natural gas liquids and natural gas, including the ability of the members of the Organization of the Petroleum Exporting Countries and other exporting countries to agree on and maintain oil price and production controls; |

• | the level of consumer demand for oil, natural gas liquids and natural gas; |

• | global or regional oil and natural gas inventory levels; |

• | the availability, proximity and capacity of transportation facilities and processing facilities; |

• | global economic conditions; |

• | commodity price disparities between delivery points and applicable index prices; |

• | the supply, demand and pricing of alternative sources of energy or fuels and the effects of energy conservation efforts or technological advances in energy consumption; |

11

• | weather conditions; |

• | changes in political conditions in major oil and natural gas producing regions and |

• | domestic, local and foreign governmental regulations and taxes. |

Our oil and natural gas proved reserves are estimates, and actual future production may vary significantly and may also be negatively impacted by our inability to invest in production on planned timelines.

There are numerous uncertainties inherent in estimating quantities of proved oil and natural gas reserves and in projecting future rates of production and timing of development expenditures. Reserve estimation is a subjective process involving the estimation of volumes to be recovered from underground accumulations of oil and natural gas that are unable to be measured in an exact manner. The reserve estimation process is dependent upon and subject to multiple variables and assumptions, including:

• | oil, natural gas liquids and natural gas prices; |

• | timing of development expenditures; |

• | the quality, quantity and interpretation of available geological, geophysical and engineering data; |

• | the geologic characteristics of the reservoirs; |

• | future operating costs, property, severance, excise and other taxes and costs and |

• | the effects of compliance with regulatory and contractual requirements. |

Additionally, in the event we are unable to fully invest or must alter the timing of our planned investment expenditures, our future revenues, production and proved reserves could be negatively affected.

Drilling for and producing oil and natural gas are high-risk activities with many uncertainties that could impact our expenses or our production volumes.

Drilling involves many risks, including the risk that no commercially productive oil or natural gas reservoirs will be located or economically developed. Our future drilling activities may not be successful and, if unsuccessful, such failure could have a material adverse effect on our future results of operations and financial condition. Anticipated drilling plans and capital expenditures may also be delayed, curtailed or canceled which could result in actual drilling and capital expenditures being substantially different than currently planned, due to:

• | delays resulting from compliance with regulatory or contractual requirements, which may include limitations on hydraulic |

fracturing or the emission of greenhouse gases;

• | unexpected or unusual pressure or irregularities in geological formations; |

• | unexpected drilling conditions; |

• | declines in oil, natural gas liquids or natural gas prices; |

• | adverse weather conditions, such as tornadoes, snow and ice storms; |

• | delays in, limited availability of, or cost to obtain personnel and equipment necessary to complete our drilling, completion and operating activities; |

• | equipment or facility failures and accidents or malfunctions resulting in blowouts, fires, explosions, uncontrollable flows of oil, natural gas or well fluids, surface cratering and other events; |

• | title related issues; |

• | fracture stimulation failures; |

• | restricted access to land for drilling; |

• | reductions in availability of financing at acceptable rates; |

• | strategic changes implemented by management and |

• | limitations in the market for oil, natural gas liquids and natural gas. |

While all drilling, whether developmental, extension or exploratory, involves these risks, exploratory and extension drilling involve greater risks of dry holes or failure to find and exploit commercially productive quantities of oil and natural gas. We expect to continue to experience exploration and abandonment expense in 2017 and future years.

12

Our concentration of producing properties in the Permian Basin of west Texas and New Mexico makes us vulnerable to risks associated with operating in limited geographic areas.

At December 31, 2016, primarily all of our total estimated proved reserves were attributable to properties located in the Permian Basin of west Texas and New Mexico. As a result of this geographic concentration, we may be disproportionately exposed to the impact of regional supply and demand factors, delays or interruptions of production from wells in these areas caused by:

• | local, state and federal governmental regulation; |

• | processing or transportation capacity constraints; |

• | market limitations; |

• | water shortages, including restrictions on water usage or other drought related conditions or |

• | interruption of the processing or transportation of oil, natural gas liquids or natural gas. |

Our industry is highly competitive which makes it challenging for us to acquire properties to replace our proved oil and natural gas reserves, market oil and natural gas and locate and secure qualified personnel.

We operate in a highly competitive environment for acquiring properties to replace our proved oil and natural gas reserves, marketing oil and natural gas and locating and securing qualified personnel. Many of our current and potential competitors may possess greater financial, technical and personnel resources than we do. Those competitors may be willing to pay more for exploratory prospects and productive oil and natural gas properties, as well as for trained personnel. Our ability to acquire properties and to find and develop proved reserves in the future will depend on our ability to evaluate and select suitable properties and to execute transactions in an intensely competitive environment. Our failure to acquire properties, market oil and natural gas and secure trained personnel could have a material adverse effect on our production, revenues and results of operations.

Our business is capital intensive, and we may not be able to obtain the needed capital, financing, or refinancing of our current indebtedness on satisfactory terms or at all.

Our exploration, development and acquisition activities are capital intensive and constitute the primary use of our capital resources. We make and expect to continue to make significant capital expenditures for the exploration, development and acquisition of oil, natural gas liquids and natural gas reserves. We have historically funded our capital expenditures through cash flows from operations, our credit facility or other borrowings, debt and equity markets and property sales. We expect that we will continue to fund a portion of our capital expenditures with borrowings under our credit facility, from the proceeds of debt and equity issuances and from proceeds from property sales. However, adverse changes in the commodity price environment or industry conditions may result in a lack of access to capital on attractive terms or at all. Thus, no assurance can be given that we will be able to access either the debt or equity capital markets, or be able to sell properties for attractive prices, to repay any such future borrowings.

If our borrowing capacity decreases, for any reason, we may have limited ability to obtain the capital necessary to support our future operations. If we are unable to obtain necessary financing with appropriate terms, we could experience a decline in our operations. Specifically, a failure to secure additional financing, or necessary refinancing, could result in a reduction of our operations relating to the development of future prospects, which in turn could lead to a decline in our proved oil and natural gas reserves and could adversely affect our future production, revenues and results of operations. Further, we could realize a loss of acreage through lease expirations, and we may not be able to complete acquisitions that may be favorable to us or finance the capital expenditures necessary to replace our reserves.

The terms of our credit facility limit the amount we can borrow to a borrowing base amount which is determined by our lenders in their sole discretion based on their valuation of our proved reserves and their internal criteria including commodity price outlook. The borrowing base amount is subject to redetermination semi-annually on April 1 and October 1 of each year and for event-driven unscheduled redeterminations. On April 13, 2016, the borrowing base and aggregate commitments were reduced to $1.05 billion in association with the semi-annual redetermination required under the agreement. On October 25, 2016, the borrowing base was reaffirmed with no changes. As of December 31, 2016, the Company had no outstanding amounts under its revolving credit facility. A lowering of our borrowing base could require us to immediately repay indebtedness in excess of the borrowing base, or we might need to further secure the lenders with additional collateral, if available. If our borrowing base decreases, we may have limited ability to obtain the capital necessary to sustain our operations at current levels. If additional capital is needed to fund our capital expenditures, our ability to access the capital markets may be limited by our financial condition at the time of any such financing or offering and the covenants in our existing debt agreements, as well as by adverse market conditions resulting from, among other things, general economic conditions and contingencies and uncertainties that are beyond our control.

13

We are also subject to financial and non-financial covenants under the terms of our credit facility. The financial covenants in our credit facility require Energen to maintain a ratio of total debt to consolidated income before interest expense, income taxes, depreciation, depletion, amortization, exploration expense and other noncash income and expenses (EBITDAX) less than or equal to 4.0 to 1.0. As of December 31, 2016, we were in compliance with our covenants and expect to maintain compliance during 2017. However, in future periods, factors including those outside of our control may prevent us from maintaining compliance with the financial and non-financial covenants, including our total debt to EBITDAX covenant. Such factors may include commodity price declines, lack of liquidity in property and capital markets and our continuing ability to execute on our business plan. In the event that we are unable to remain in compliance with our financial and non-financial covenants, we would seek covenant relief at a scheduled redetermination date or at an interim date, as appropriate. However, no assurances can be given with respect to such relief. If any such covenant violations are not waived by the lenders such violation would result in an event of default that could trigger acceleration of payment of the amounts outstanding under our credit facility and long term note agreements. Additionally, the lenders could refuse to make additional loans under the credit facility, take possession of any collateral, and exercise other remedies or rights that may be available to them, all of which could have a material adverse effect on the business and financial condition of the Company. As more fully disclosed in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations under the heading “Credit Facility and Working Capital”, the Company discusses its plans regarding liquidity and covenant compliance for 2017.

In 2016 we discontinued dividend payments and, therefore, only appreciation in the price of our common stock will provide a return to our stockholders.

Although we have paid cash dividends on our common stock in the past, in February 2016 our board of directors announced the discontinuance of dividend payments. We currently intend to retain future earnings and other cash resources, if any, for the operation and development of our business. Any payment of future dividends will be at the discretion of our board of directors and will depend on our results of operations, financial condition, contractual restrictions, cash requirements, future prospects and other considerations that our board of directors deems relevant.

The nature of our operations involves many operational risks including the risk of personal injury, property damage and environmental damage, and our insurance policies do not cover all such risks.

Inherent in our oil and natural gas production activities are a variety of hazards and operational risks, including but not limited to:

• | pipeline and storage leaks, ruptures and spills; |

• | equipment malfunctions and mechanical failures; |

• | fires and explosions; |

• | well blowouts, explosions and cratering; |

• | uncontrollable flows of oil, natural gas or well fluids; |

• | vandalism; |

• | pollution; |

• | releases of toxic gases; |

• | adverse weather conditions or natural disasters and |

• | soil, surface and water or groundwater contamination from petroleum constituents, hydraulic fracturing fluid, or produced water. |

Such events could result in loss of human life, significant damage to or destruction of property, environmental pollution or other damage, impairment or suspension of our operations, repair and remediation costs, regulatory investigations and penalties or lawsuits and other substantial financial losses. Furthermore, our oil and natural gas exploration and production activities are subject to all of the operating risks associated with drilling for and producing oil and natural gas, including those noted above. Additionally, the location of certain of our pipeline and storage facilities near populated areas, including residential areas, commercial business centers and industrial sites, could increase the level of damages resulting from these risks.

In accordance with customary industry practices, we maintain insurance against some, but not all, of these risks and losses; and the insurance coverages are subject to retention levels and coverage limits. We may elect not to obtain insurance if we believe the cost of available insurance is excessive relative to the risks presented. In addition, pollution and environmental risks generally are not fully insurable. Furthermore, we could be subject to the credit risk of our insurers if we make a claim under our insurance policies. There is no guarantee that we will be able to obtain or maintain our insurance in the future at rates we deem economical and that the insurance we may desire will be offered by insurers. Losses and liabilities arising from uninsured or under-insured events or insurer insolvency, in the event of a claim, could materially and adversely affect our business, financial condition or results of operations.

14

We are subject to extensive regulation, including numerous federal, state and local laws and regulations as well as legislation and regulations restricting the emissions of “greenhouse gases” that may require significant expenditures or impose significant restrictions on our operations.

We are subject to extensive federal, state and local regulation which significantly influences our operations. Federal, state and local legislative bodies and agencies frequently exercise their respective authority to adopt new laws and regulations and to amend, modify and interpret existing laws and regulations. Such changes can subject us to significant tax or increased expenditures and can impose significant restrictions and limitations on our operations. Noncompliance with these laws and regulations may subject us to administrative, civil or criminal penalties, remedial cleanups, and natural resource damages or other liabilities. Furthermore, we may incur significant costs to remain in compliance with or to return to compliance with applicable regulations if they are revised or reinterpreted or if governmental policies or laws change related to our operations.

If additional federal, state or local regulations or restrictions are adopted in the areas we operate or plan to operate, we may incur significant costs to comply with the requirements, experience delays or have to curtail our exploration, development, or production activities. Additionally, such restrictions could reduce the amount of oil and gas that we are able to recover from our proved reserves.

The subject of climate change continues to receive attention from many parties including legislators and governmental agencies.

If additional legislation or regulatory programs to reduce emissions of greenhouse gases are adopted, it could require us to incur increased operating costs, such as those for purchasing and operating emissions control systems, acquiring emissions allowances or complying with new regulatory or reporting requirements. Any such legislation or regulatory programs could also increase the cost of consuming and using oil and natural gas, and thereby negatively impact the demand for the oil, natural gas liquids and natural gas we produce. Consequently, legislation and regulatory programs related to greenhouse gases could adversely affect our production, revenues and results of operations.

Federal, state and local legislative and regulatory initiatives relating to hydraulic fracturing, as well as governmental reviews of such activities, could result in increased costs and additional operating restrictions or delays and adversely affect our production.

Energen regularly utilizes hydraulic fracturing in its drilling and completion activities, and hydraulic fracturing is a common practice that is used in the oil and gas industry to stimulate production of hydrocarbons from tight (low permeability) formations. After a well has been drilled, hydraulic fracturing is used during the completion process to form small fractures in the target formation through which the oil, natural gas liquids or natural gas can flow. The fractures are created when a water-based fluid is pumped at a calculated rate and pressure into the crude oil- or natural gas-bearing rock. The fracture fluid is a mixture composed primarily of water and sand or inert ceramic, sand-like grains; it also contains a small percentage of special purpose chemical additives (which are highly diluted-typically less than one percent by volume) that can vary by project. The millimeter-thick cracks or fractures in the target formation are propped open by the sand, thereby allowing the crude oil or natural gas to flow from tight reservoirs into the well bore.

The hydraulic fracturing process is typically regulated by state oil and gas commissions. However, under the Safe Drinking Water Act’s Underground Injection Control Program, the EPA has assumed regulatory authority of hydraulic fracturing involving diesel additives and issued revised permitting guidance in February 2014 requiring facilities to obtain permits to use diesel additives in hydraulic fracturing activities. Legislation intended to provide for federal regulation of hydraulic fracturing and require disclosure of the chemicals used has been introduced and considered by the U.S. Congress. In addition, Texas and New Mexico, two states in which we operate, have adopted, and other states have considered adopting, regulations that could impose new or stricter permitting, disclosure and well construction requirements on companies that perform hydraulic fracturing. Consideration and efforts to regulate hydraulic fracturing by local, state and federal authorities continue and local land use restrictions, such as county and city ordinances, may also restrict or prohibit any type of drilling or hydraulic fracturing. If additional federal, state or local restrictions are adopted in the areas we operate or plan to operate, we may incur significant costs to comply with the requirements, experience delays or have to curtail our exploration, development, or production activities. Additionally, such restrictions could reduce the amount of oil and gas that we are able to recover from our proved reserves.

Our operations are dependent on the availability, use and disposal of water; and restrictions on our ability to acquire or dispose of water could cause us to incur substantial costs in the acquisition, usage and disposal of water.

Water is a key component of both the drilling and hydraulic fracturing processes. Historically, we have been able to obtain water from various local sources for use in our operations. Texas has recently experienced periods of severe drought conditions that have persisted for several years. Local water districts may restrict the use of water subject to their jurisdiction for drilling and hydraulic fracturing in order to protect the local water supply during drought conditions. If we are unable to obtain water to use in our

15

operations from local sources, we may have to incur substantial costs to produce oil and natural gas and it may make it uneconomical to produce in that area. Our drilling procedures produce water of which we must dispose. We could be unable to dispose of our wastewater or face increased costs and procedures for disposal as a result of changes in federal or local legislation governing the disposal of drilling wastewater.

We periodically evaluate our proved and unproved oil and natural gas properties for impairment and could be required to recognize non-cash charges in our statements of income in future periods. If commodity prices for oil, natural gas liquids or natural gas decline or our drilling efforts are unsuccessful, we may be required to writedown the carrying values of certain oil and natural gas properties.

We periodically review the carrying value of our proved and unproved oil and natural gas properties for possible impairment on a field-by-field basis. We monitor our oil and natural gas properties as well as the market and business environments in which we operate and make assessments about events that could result in potential impairment issues, which include, but are not limited to, downward commodity price trends, unanticipated increased operating costs and lower than expected production performance. If a material event occurs, we perform an evaluation to determine whether the asset is impaired. If the undiscounted net future cash flows determined by such evaluations are insufficient to fully recover the cost invested in the respective project, we will record an impairment loss in our statements of income. We recorded $220.7 million and $1.3 billion of impairments during 2016 and 2015, respectively.

We are exposed to counterparty credit risk as a result of our concentrated customer base and to the risks associated with other companies with whom we do business experiencing financial distress.

Revenues and related accounts receivable from oil and natural gas operations primarily are generated from the sale of produced oil, natural gas liquids and natural gas to a small number of energy marketing companies. Such sales are typically made on an unsecured credit basis with payment due the month following delivery. This concentration of sales to a limited number of customers in the energy marketing industry has the potential to adversely affect our overall exposure to credit risk based on changes in economic, industry or other conditions specific to a single customer or to the energy marketing industry generally. We consider the credit quality of our customers and, in certain instances, may require credit assurances such as a deposit, letter of credit or parent company guarantee.

In addition, we rely on other working interest owners in our wells to pay their proportionate share of costs and on oilfield service companies and midstream companies for services associated with the drilling and completion of wells and for certain midstream services. A decline in the commodity price environment may result in a material adverse impact on the liquidity and financial position of the companies with whom we do business, resulting in delays in payment of, or non-payment of, amounts owing to us and similar impacts. These events could have an adverse impact on our financial condition, results of operations and cash flows.

We are subject to financing and interest rate exposure risks. Volatility in global financial markets, negative operating results, certain strategic business decisions, or other matters resulting in a downgrade in, or a negative outlook with respect to, our credit ratings could negatively impact our cost of and our ability to access capital for future development and working capital needs.

We rely on access to credit markets, and turmoil or volatility in the global financial markets could lead to a contraction in credit availability and negatively impact our ability to finance our operations. Global financial market turmoil, as has been experienced in the last decade, could materially affect our operations, liquidity and financial condition through the adverse impacts such turmoil can have on the debt and equity capital markets. Market volatility and credit market disruption may severely limit credit availability, and issuer credit ratings can change rapidly. A significant reduction in cash flows from operations or the availability of credit could limit our ability to pursue acquisition opportunities or reduce cash flow used for drilling which could materially and adversely affect our ability to achieve our planned growth and operating results.

The availability and cost of credit market access is significantly influenced by market events and rating agency evaluations for lenders and Energen. In addition to operating results, business decisions relating to recapitalization, refinancing, restructuring, acquisition and disposition transactions involving Energen may negatively impact market and rating agency considerations regarding the credit of Energen.

16

Our derivative risk management activities may limit our potential gains and involve other risks that could result in financial losses.

Although we make use of futures, swaps, options, collars and fixed-price contracts to mitigate price risk, fluctuations in future oil, natural gas liquids and natural gas prices could materially affect our financial position, results of operations and cash flows. Furthermore, such risk mitigation activities may cause our financial position and results of operations to be materially different from results that would have been obtained had such risk mitigation activities not been implemented. The changes in the fair market value of our derivative contracts as reported in our consolidated statements of income may result in significant non-cash gains or losses.

The effectiveness of such risk mitigation assumes that counterparties maintain satisfactory credit quality and that actual sales volumes will generally meet or exceed the volumes subject to the futures, swaps, options, collars and fixed-price contracts. A substantial failure to meet sales volume targets, whether caused by miscalculations, weather events, natural disaster, accident, mechanical failure, criminal act or otherwise, could leave us financially exposed to our counterparties and result in material adverse financial consequences to Energen. The adverse effect could be increased if the adverse event was widespread enough to move market prices against our position.

Derivatives reform legislation which has been adopted by the U.S. Congress, or additions to or changes in the legislation, could negatively impact our ability to use derivative instruments as part of our risk management activities.

In July 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) was signed into law. Title VII of the Dodd-Frank Act establishes federal oversight and regulation of the over-the-counter derivatives markets and participants in such markets. The Commodities Futures Trading Commission (CFTC) and the SEC have adopted, or are in the process of adopting, rules and regulations covering, among other derivative transactions, transactions linked to crude oil and natural gas prices. We believe Energen’s derivative transactions qualify for the end-user exception which exempts them from certain Dodd-Frank Act swap clearing and exchange-trading requirements pursuant to final regulations adopted by the CFTC and SEC.

The CFTC has designated certain interest rate swaps and credit default swaps for mandatory clearing and the associated rules also may require Energen, in connection with covered derivative activities, to comply with certain clearing and trade-execution requirements or take steps to qualify for an exemption to such requirements, although the application of these provisions to us is uncertain at this time. Although we believe we qualify for the end-user exception from the mandatory clearing requirements for swaps entered to mitigate our commercial risks, the application of the mandatory clearing and trade execution requirements to other market participants, such as dealers, may change the cost and availability of our future derivative arrangements (including through requirements to post collateral which could adversely affect Energen’s available liquidity). The changes in the regulation of swaps may result in certain market participants deciding to curtail or stop engaging in derivative activities. If we reduce our use of derivatives as a result of the Dodd Frank Act and regulations, our results of operations may become more volatile and our cash flows may be less predictable, which could adversely affect our ability to plan for and fund capital expenditures and our results of operations. Our revenues could be adversely affected if, as a consequence of the Dodd-Frank Act and related regulations, commodity prices are lowered due to reduced trading in derivatives. Any of these consequences could have a material adverse effect on our financial condition and results of operations.

Our operations depend on the use of third-party facilities, and an interruption of our ability to utilize these facilities may adversely affect our financial condition and results of operations.

Energen delivers to third-party facilities. These facilities include third-party oil and natural gas gathering, transportation, processing and storage facilities. Energen relies on such facilities for access to market for our oil, natural gas liquids and natural gas production. Such facilities are typically limited in number and geographically concentrated. A lack of available capacity on these facilities could result in the shut-in of producing wells or the delay or discontinuance of development plans for properties for Energen. An extended interruption of access to or service from these facilities, whether caused by weather events, natural disaster, accident, mechanical failure, criminal act, maintenance or otherwise could have an adverse effect on our revenues and results of operations.

17

The success of our future operations is dependent on our future drilling activities and our ability to economically develop our oil, natural gas liquids and natural gas reserves; and our expectations regarding future drilling and development activities are subject to uncertainties that could significantly alter the occurrence or timing of such activities, as they are expected to be realized over multiple years.

We have identified drilling locations and prospects for future drilling, including development and exploratory drilling activities. Our ability to successfully and economically drill and develop these locations depends on a number of factors, including:

• | prices of oil, natural gas liquids and natural gas; |

• | current laws or regulations or changes in the laws or regulations in the identified and prospective locations; |

• | the availability and cost of capital; |

• | seasonal and other weather conditions; |

• | regulatory approvals; |

• | negotiation of agreements with third parties; |

• | access to and availability of required equipment, supplies and personnel and |

• | drilling results. |

Because of the factors noted above, we cannot provide any guarantee regarding the timing or success of future drilling activities; and our actual drilling activities may materially differ from our current expectations, including potential delays, curtailment or cancellation of anticipated drilling plans and capital expenditures.

Energen has limited control over activities on properties which we do not operate, which could reduce our production and revenues.

Energen operates in certain instances through joint ventures under joint operating agreements. Typically, the operator under a joint operating agreement enters into contracts, such as drilling contracts, for the benefit of all joint venture partners. Through the joint operating agreement, the non-operators reimburse, and in some cases advance, the funds necessary to meet the contractual obligations entered into by the operator. For properties we do not operate, we have limited ability to control the operation or future development of the properties or the amount of capital expenditures that we are required to fund with respect to them. An operator’s failure to adequately perform operations, an operator’s breach of the applicable agreements or an operator’s failure to act in our best interest could reduce our production and revenues. The success and timing of our drilling and development activities on properties operated by others is dependent on a number of factors, including the operator's timing and amount of capital expenditures, expertise and financial resources, inclusion of other participants in drilling wells and use of technology. Our dependence on the operator and other working interest owners for these projects and our limited ability to control the operation and future development of these properties could negatively affect the realization of our expected returns on capital in drilling or acquisition activities and could lead to unexpected costs in the future.

Our business could be negatively impacted by security threats, including cybersecurity threats and related disruptions.