Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - PITNEY BOWES INC /DE/ | pbi20161231ex322.htm |

| EX-32.1 - EXHIBIT 32.1 - PITNEY BOWES INC /DE/ | pbi20161231ex321.htm |

| EX-31.2 - EXHIBIT 31.2 - PITNEY BOWES INC /DE/ | pbi20161231ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - PITNEY BOWES INC /DE/ | pbi20161231ex311.htm |

| EX-23 - EXHIBIT 23 - PITNEY BOWES INC /DE/ | pbi20161231ex23.htm |

| EX-21 - EXHIBIT 21 - PITNEY BOWES INC /DE/ | pbi20161231ex21.htm |

| EX-12 - EXHIBIT 12 - PITNEY BOWES INC /DE/ | pbi20161231ex12.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016 Commission file number: 1-3579

PITNEY BOWES INC.

Incorporated in Delaware | I.R.S. Employer Identification No. 06-0495050 |

3001 Summer Street, Stamford, CT 06926 | |

(203) 356-5000 | |

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $1 par value per share | New York Stock Exchange | |

$2.12 Convertible Cumulative Preference Stock (no par value) | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: 4% Convertible Cumulative Preferred Stock ($50 par value)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check marks whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

As of June 30, 2016, the aggregate market value of the registrant's common stock held by non-affiliates of the registrant was $3.3 billion based on the closing sale price as reported on the New York Stock Exchange.

Number of shares of common stock, $1 par value, outstanding as of close of business on February 17, 2017: 186,399,332 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's proxy statement to be filed with the Securities and Exchange Commission (the Commission) no later than 120 days after our fiscal year end and to be delivered to stockholders in connection with the Annual Meeting of Stockholders to be held May 8, 2017, are incorporated by reference in Part III of this Form 10-K.

1

PITNEY BOWES INC.

TABLE OF CONTENTS

Page Number | ||

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

2

PART I

Forward-Looking Statements

This Annual Report on Form 10-K (Annual Report) contains statements that are forward-looking. We want to caution readers that any forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 may change based on various factors. These forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties and actual results could differ materially. Words such as "estimate," "target," "project," "plan," "believe," "expect," "anticipate," "intend" and similar expressions may identify such forward-looking statements. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Factors which could cause future financial performance to differ materially from the expectations as expressed in any forward-looking statement made by or on our behalf include, without limitation:

• | declining physical mail volumes |

• | competitive factors, including pricing pressures, technological developments and introduction of new products and services by competitors |

• | our ability to fully utilize the new enterprise business platform in the United States and successfully implement it internationally without significant disruptions to existing operations |

• | our success in developing new products and services, including digital-based products and services, obtaining regulatory approval if required, and the market’s acceptance of these new products and services |

• | the success of our investment in rebranding the company to build market awareness and create new demand for our products, services and solutions |

• | changes in postal or banking regulations |

• | macroeconomic factors, including global and regional business conditions that adversely impact customer demand and foreign currency exchange rates |

• | capital market disruptions or credit rating downgrades that adversely impact our ability to access capital markets at reasonable costs |

• | changes in interest rates and fuel prices |

• | the continued availability and security of key information systems and the cost to comply with information security requirements and privacy laws |

• | a breach of security, including a cyberattack or other comparable event |

• | third-party suppliers' ability to provide product components, assemblies or inventories |

• | our success at managing the relationships with our outsource providers, including the costs of outsourcing functions and operations not central to our business |

• | the loss of some of our larger clients in the Global Ecommerce segment |

• | integrating newly acquired businesses including operations and product and service offerings |

• | intellectual property infringement claims |

• | our success at managing customer credit risk |

• | significant changes in pension, health care and retiree medical costs |

• | income tax adjustments or other regulatory levies for prior audit years and changes in tax laws, rulings or regulations |

• | a disruption of our businesses due to changes in international or national political conditions, including the use of the mail for transmitting harmful biological agents or other terrorist attacks |

• | acts of nature |

Risks are more fully described under Item 1A. "Risk Factors" in this Annual Report.

ITEM 1. BUSINESS

General

Pitney Bowes Inc. (we, us, our, or the company), was incorporated in the state of Delaware in 1920. We are a global technology company offering innovative products and solutions that help our clients navigate the complex world of commerce. We offer customer information

3

management, location intelligence and customer engagement products and solutions to help our clients market to their customers, and shipping, mailing, and cross border ecommerce products and solutions that enable the sending of parcels and packages across the globe. Clients around the world rely on our products, solutions and services. For more information about us, our products, services and solutions, visit www.pb.com.

Our Strategy and Business Segments

Our business is organized around three distinct sets of solutions -- Small and Medium Business Solutions (SMB), Enterprise Business Solutions and Digital Commerce Solutions (DCS).

Small and Medium Business Solutions

We are a global leader in providing a full range of equipment, software, supplies and services that enable our clients to efficiently create physical and digital mail, evidence postage and print shipping labels for the sending of mail, flats and parcels. We segment the SMB Solutions group between our North America operations, comprising the U.S. and Canadian businesses, and our International operations, comprising all other SMB businesses globally. We are a leading provider of mailing systems globally with about 1.2 million meters installed worldwide. We are also continuing to expand our business to include online offerings without a hardware component. This business is characterized by a high level of recurring revenue driven by rental, lease and loan arrangements, contract support services and supplies sales.

Enterprise Business Solutions

Our Enterprise Business Solutions group includes equipment and services that enable large enterprises to process inbound and outbound mail. The Enterprise Business Solutions group includes our Production Mail operations and Presort Services operations.

Production Mail

Our product and service offerings enable clients to integrate all areas of print and mail into an end-to-end production environment from message creation to dispatch while realizing cost savings on postage. The core products within this segment include high-speed, high-volume inserting equipment, customized sortation products for mail and parcels and high-speed digital color printing systems that create high-value, relevant and timely communications targeted to our clients' customers. In 2017, we expect to expand our cloud connectivity solutions currently available for our inserter equipment into our print and sortation machines.

Presort Services

We are a national outsource provider of mail presort services for First-Class, Standard, flat and parcels in the U.S. and a workshare partner of the United States Postal Service (USPS). Our Presort Services network and fully-customized proprietary technology provides our clients with end-to-end solutions from pick up at their location to delivery into the postal system network. We process approximately 15 billion pieces of mail annually through our network of operating centers throughout the Unites States and are able to expedite mail delivery and optimize postage savings for our clients. In 2016, we began offering sortation services for parcel mail and expect to expand this offering in 2017.

Digital Commerce Solutions

Within the Digital Commerce Solutions group, we provide a broad range of solutions, including customer information management, location intelligence, customer engagement software and shipping management and cross border ecommerce solutions for businesses of all sizes. These solutions are delivered as traditional software licenses, enterprise platforms, software-as-a-service (SaaS) or on-demand applications. Our Digital Commerce Solutions group includes Software Solutions and Global Ecommerce.

Software Solutions

Customer information management solutions help businesses harness and develop a deep and broad understanding of their customers and their context, such as location, relationships, propensity, sentiment and influence. The trusted data and associated insights allow our clients to deliver a personalized customer experience across multiple channels, manage risk and compliance, and improve sales, marketing and service effectiveness. We are one of the market leaders in the data quality segment. Large corporations and government agencies rely on our products in complex, high-volume, transactional environments to support their business processes.

Location intelligence solutions enable our clients to organize and understand the complex relationships between location, geographic and other forms of data to drive business decisions and customer experiences. Our location intelligence solutions use predictive analytics, location, geographic and socio-demographic characteristics, which enable our clients to harness the power of location to better serve their customers, solve business problems, deliver location-based services and ultimately drive business growth.

4

Customer engagement solutions provide clients with insight and understanding into customer behavior and interactions across the entire customer lifecycle, enabling them to orchestrate impactful, relevant and timely physical and digital interactions. When coupled with our inserting, sortation and digital print products, we are able to provide clients an all-inclusive solution that enables them to create, print and distribute wide-spread targeted customer communications. Our customer engagement solutions enable our clients to create connected experiences that positively influence future consumer behavior and generate business growth.

Global Ecommerce

Global Ecommerce includes our cross-border ecommerce solutions and retail and warehouse shipping management solutions. Global Ecommerce provides a full suite of domestic and cross-border solutions that help businesses of all sizes conduct commerce and participate in the parcel journey from “Anywhere to Everywhere™.” It is our technology, services and industry expertise that have made us an industry leader in global commerce. We offer a unified commerce platform of capabilities for cross-border, marketplaces and shipping that center around the consumer. With our proprietary technology, we are able to manage all aspects of the international shopping and shipping experience, including multi-currency pricing, payment processing, fraud management, calculation of fully landed costs by quoting duty, taxes and shipping at checkout, compliance with product restrictions, export complexities and documentation requirements for customs clearance and brokerage and global logistics services. Our cross-border ecommerce software platforms are currently utilized by direct merchants as well as a major online marketplace enabling millions of parcels to be shipped to countries and territories worldwide. Our platform also connects retailers to marketplaces around the world, opening new markets and expanding existing markets for their goods.

Our shipping management solutions enable clients to reduce transportation and logistics costs, to select the best carrier based on need and cost, to improve delivery times and to track packages in real-time. Our Shipping API technology, an integral part of the Pitney Bowes Commerce Cloud, provides easy access to shipping and tracking services that can be easily integrated into any web application such as online shopping carts or ecommerce sites. We also offer scalable shipping solutions that can be integrated into mail centers for the office market.

See Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations" and Note 2 to the Consolidated Financial Statements for additional segment and geographic information.

Client Service

We have a client care service organization that provides telephone, online and on-site support to diagnose and repair our increasingly complex mailing equipment, production printers and sophisticated software solutions. Most of our support services are provided under annual contracts.

Sales and Marketing

We market our products and services through a direct and inside sales force, direct mailings, telemarketing, independent dealers and distributors and web channels. We sell to a variety of business, governmental, institutional and other organizations, and in our Ecommerce business only, we also sell to consumers. We have a broad base of clients and are not dependent upon any one client or type of client for a significant part of our total revenue.

We have made, and are continuing to make significant investments in the rebranding of the company. These investments include marketing and advertising designed to build market awareness and client demand for our products and services, and enhance our operational and go-to-market changes, including how we sell to and service clients.

Competition

All of our businesses face competition from a number of companies. Our competitors range from large, multinational companies that compete against many of our businesses to smaller, more narrowly focused regional and local firms. We compete on the basis of technology and innovation; breadth of product offerings; our ability to design and tailor solutions to specific client needs; performance; client service and support; price; quality and brand.

We must continue to invest in our current technologies, products and solutions, and in the development of new technologies, products and solutions in order to maintain and improve our competitive position. We will encounter new competitors as we transition to higher value markets and offerings and enter new markets.

5

A summary of the competitive environment for each of our business segments is as follows:

North America Mailing and International Mailing

We face significant competition from other mail equipment and software companies, companies that offer products and services as alternative means of message communications and non-traditional competitors that offer shipping and mailing products and services through online solutions. The principal competitive factors include the composition of offerings between software and hardware solutions, pricing, available financing and payment offerings, product reliability, support services, industry knowledge and expertise and attractiveness of alternative communication methods. Our competitive advantage includes our breadth of physical and web-based digital offerings, customer service and our extensive knowledge of the shipping and mailing industry.

Through our wholly owned subsidiary, The Pitney Bowes Bank (the Bank), we offer a revolving credit solution to our clients in the United States that enables them to pay for postage, the rental of certain mailing equipment and purchase products, supplies and services. The Bank also provides an interest-bearing deposit solution to those clients in the United States who prefer to prepay postage. We also provide similar revolving credit solutions to our clients in Canada and the U.K. but do not offer these through the Bank. Our financing operations face competition, in varying degrees, from large, diversified financial institutions, including leasing companies, commercial finance companies and commercial banks, as well as small, specialized firms. Not all our competitors are able to offer these financing and payment solutions to their customers and we believe these solutions differentiate us from our competitors and are a source of competitive advantage. The Bank is chartered as an Industrial Bank under the laws of the State of Utah, and regulated by the Federal Deposit Insurance Corporation (FDIC) and the Utah Department of Financial Institutions.

Production Mail

We face competition from other companies that offer large production printers, inserters or sorters. We also face competition from the fact that some companies choose to outsource although those outsource providers can also be our customers. Our primary competitive advantage lies in our ability to offer all of these products and services and integrate them into an end-to-end solution. The principal competitive factors include functionality, reliability, productivity, price and support.

Presort Services

We face competition from regional and local presort providers and service bureaus that offer presort solutions as part of a larger bundle of outsourcing services, and large entities that have the capability to presort their own mailings in-house. The principal competitive factors include innovative service, delivery speed, industry expertise and economies of scale. Our competitive advantage includes our extensive network of presort facilities capable of processing significant volumes of mail and our innovative and proprietary technology that enables us to provide our clients with reliable and accurate services at maximum discounts.

Software Solutions

We operate in several highly competitive and rapidly evolving markets and face competition ranging from large global companies that offer a broad suite of solutions to smaller, more narrowly-focused companies that can design very targeted solutions. The principal competitive factors include reliability, functionality, ease of integration and use, scalability, innovation, support services and price. We compete based on the accuracy and processing speed of our solutions, particularly those used in our location intelligence solutions, the breadth and scalability of our products and solutions, our geocoding and reverse geocoding capabilities, and our ability to identify rapidly changing customer needs and develop technologies and solutions to meet these changing needs.

Global Ecommerce

The market for international ecommerce software and fulfillment services is highly fragmented and includes competitors of various sizes, including companies with greater financial resources than us. Some of these competitors specialize in point solutions or freight forwarding services, are full-service ecommerce business process outsourcers and online marketplaces with international logistic support, or major global delivery services companies. The principal competitive factors include reliability, functionality, ease of integration and use, scalability of our platform and our logistics services, innovation, support services and price. We compete based on the accuracy, reliability and scalability of our platform, and our ability to provide our clients and their customers a one-stop full-service cross border ecommerce experience. In our shipping solutions business, we compete with a wide range of technology providers who help make shipping easier and more cost-effective for the retailer, warehouse, or office shipper. There are established players in the marketplace who are set-up to compete against their client base. The remainder of the shipping market is very fragmented with many small companies offering negotiated carrier rates (primarily with the USPS). The principal competitive factors include technology stability and reliability, innovation, access to preferred shipping rates, and ease of integration with existing systems.

6

Financing Solutions

We offer a variety of finance and payment solutions to clients to finance their equipment and product purchases, rental and lease payments, postage replenishment and supplies purchases. As our other product and service offerings evolve, we continually evaluate whether there are appropriate financing solutions for us to offer our clients. We establish credit approval limits and procedures based on the credit quality of the client and the type of product or service provided to control risk in extending credit to clients. In addition, we utilize a systematic decision program for certain leases. This program is designed to facilitate low dollar transactions by utilizing historical payment patterns and losses realized for clients with common credit characteristics. The program defines the criteria under which we will accept a client without performing a more detailed credit investigation, such as maximum equipment cost, a client's time in business and payment experience.

We closely monitor the portfolio by analyzing industry sectors and delinquency trends by product line, industry and client to ensure reserve levels and credit policies reflect current trends. Management continues to closely monitor credit lines and collection resources and revise credit policies as necessary to be more selective in managing the portfolio.

Research, Development and Intellectual Property

We invest in research and development programs to develop new products and solutions, enhance the effectiveness and functionality of existing products and solutions and deliver high value technology, innovative software and differentiated services in high value segments of the market. As a result of our research and development efforts, we have been awarded a number of patents with respect to several of our existing and planned products. The continued evolution of patent law and the nature of our innovation work may affect the number of patents we are able to receive for our internal development efforts. However, our businesses are not materially dependent on any one patent or license or group of related patents or licenses. Research and development expenditures were $121 million in 2016 and $110 million, in both 2015 and 2014.

Material Suppliers

We depend on third-party suppliers for a variety of services, components, supplies and a large portion of our product manufacturing. In certain instances, we rely on single-sourced or limited-sourced suppliers around the world because the relationship is advantageous due to quality, price, or there are no alternative sources. We have not historically experienced shortages in services, components or products and believe that our available sources for materials, components, services and supplies are adequate.

Regulatory Matters

We are subject to the regulations of postal authorities worldwide related to product specifications and business practices involving our postage meters. We are further subject to the regulations of the Utah Department of Financial Institutions and the FDIC with respect to the operations of the Bank and certain company affiliates that provide services to the Bank. We are also subject to the regulations of transportation, customs and other trade authorities worldwide related to the cross-border shipment of equipment, materials and parcels. In addition, we are subject to regulations worldwide concerning data privacy and security for our businesses that use, process and store certain personal, confidential or proprietary data.

Employees and Employee Relations

At December 31, 2016, we have approximately 14,200 employees worldwide. We believe that we maintain strong relationships with our employees. Management keeps employees informed of decisions and encourages and implements employee suggestions whenever practicable.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments thereto filed with, or furnished to, the Securities and Exchange Commission (the SEC), are available, free of charge, through the Investor Relations section of our website at www.pb.com/investorrelations or from the SEC's website at www.sec.gov, as soon as reasonably practicable after these reports are electronically filed with, or furnished to, the SEC. The other information found on our website is not part of this or any other report we file with or furnish to the SEC.

You may also read and copy any document we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549 or request copies of these documents by writing to the Office of Public Reference. Call the SEC at (800) 732-0330 for further information on the operations of the Public Reference Room and copying charges.

7

Executive Officers of the Registrant

Our executive officers are as follows:

Name | Age | Title | Executive Officer Since | |||

Marc B. Lautenbach | 55 | President and Chief Executive Officer | 2012 | |||

Daniel J. Goldstein | 55 | Executive Vice President and Chief Legal Officer and Corporate Secretary | 2010 | |||

Robert Guidotti | 59 | Executive Vice President and President, Software Solutions | 2016 | |||

Abby F. Kohnstamm | 63 | Executive Vice President and Chief Marketing Officer | 2013 | |||

Michael Monahan | 56 | Executive Vice President and Chief Operating Officer | 2005 | |||

Roger J. Pilc | 49 | Executive Vice President and Chief Innovation Officer | 2013 | |||

Mark L. Shearer | 60 | Executive Vice President and President, Pitney Bowes SMB Mailing Solutions | 2013 | |||

Lila Snyder | 44 | Executive Vice President and President, Global Ecommerce | 2016 | |||

Christoph Stehmann | 54 | Executive Vice President and President, Enterprise Solutions Group | 2016 | |||

Stanley J. Sutula III | 51 | Executive Vice President and Chief Financial Officer (1) | 2017 | |||

Johnna G. Torsone | 66 | Executive Vice President and Chief Human Resources Officer | 1993 | |||

(1) Effective February 1, 2017, Mr. Sutula assumed the responsibilities of Executive Vice President and Chief Financial Officer. Prior to that date, Mr. Monahan had the responsibilities of Chief Financial Officer.

There are no family relationships among the above officers. All of the officers have served in various executive positions with the company for at least the past five years except as described below:

Mr. Lautenbach was appointed President and Chief Executive Officer of the company in December 2012. Before joining Pitney Bowes, Mr. Lautenbach held numerous positions during his career at IBM, which he joined in 1985. His leadership roles at IBM included serving as Vice President Small and Medium Business in Asia Pacific from 1998-2000, General Manager of IBM Global Small and Medium Business from 2000-2005, General Manager of IBM North America from 2005-2010, and Managing Partner, North America, for IBM Global Business Services from 2010-2012.

Mr. Guidotti was appointed Executive Vice President and President, Software Solutions in January 2016. Before joining Pitney Bowes, Mr. Guidotti has been in the software industry for over 20 years and held a series of executive positions at IBM including General Manager, Software Sales where he was responsible for sales, technical sales, and channels for the $23 billion Software portfolio worldwide.

Ms. Kohnstamm joined the company as Executive Vice President and Chief Marketing Officer in June 2013. Before joining Pitney Bowes, Ms. Kohnstamm served as President of Abby F. Kohnstamm & Associates, Inc., a marketing and consulting firm.

Mr. Pilc joined the company as Executive Vice President and Chief Innovation Officer in June 2013. Before joining Pitney Bowes, Mr. Pilc served as General Manager at CA Technologies, where he was responsible for the company’s Industries, Solutions and Alliances unit.

Mr. Shearer joined the company as Executive Vice President and President, Pitney Bowes SMB Mailing Solutions in April 2013. Before joining Pitney Bowes, Mr. Shearer held numerous positions during his 30 year career at IBM, including general management, business and product strategy, and marketing. Before his retirement from IBM in 2010, he served as Vice President, Marketing and Strategy for IBM’s hardware business.

Ms. Snyder was elected to the office of Executive Vice President by the board of directors in January 2016. She joined the company in November 2013 as President, Document Messaging Technologies (DMT) and became President, Global Ecommerce in June 2015. Prior to joining Pitney Bowes, Ms. Snyder was a Partner at McKinsey & Company, Inc. In her 15 years at McKinsey, she focused on serving clients in the technology, media and communications sectors and was the leader of McKinsey's Stamford office.

8

Mr. Sutula joined the company as Executive Vice President and Chief Financial Officer in February 2017. Prior to joining the company, Mr. Sutula was employed at IBM for 28 years where he held several leadership positions in the United States and in Europe. Most recently, Mr. Sutula was Vice President and Controller.

ITEM 1A. RISK FACTORS

Our operations face certain risks that should be considered in evaluating our business. We manage and mitigate these risks on a proactive basis, including through the use of an enterprise risk management program. Nevertheless, the following risk factors, some of which may be beyond our control, could materially impact our business, financial condition, results of operations, brand and reputation, and may cause future results to be materially different than our current expectations. These risk factors are not intended to be all inclusive.

We are subject to postal regulations and processes, which could adversely affect our revenue and profitability.

A significant portion of our revenue and profitability is directly or indirectly subject to regulation and oversight by postal authorities worldwide. We depend on a healthy postal sector in the geographic markets where we do business, which could be influenced positively or negatively by legislative or regulatory changes in those countries. Our revenue and profitability in a particular country could be affected by adverse changes in postal regulations, the business processes and practices of individual posts, the decision of a post to enter into particular markets in direct competition with us and the impact of any of these changes on postal competitors that do not use our products or services. These changes could affect product specifications, service offerings, client behavior and the overall mailing industry.

If we are not able to respond to the continuing decline in the volume of physical mail delivered via traditional postal services, our results of operations and profitability could be adversely impacted.

Declining mail volumes has had an adverse impact on our revenues and profitability and is expected to continue to influence our revenue and profitability in the future. We continue to employ strategies for stabilizing the mailing business which include new product and service offerings, transitioning our current products and services to more digital offerings and providing our clients broader access to products and services through online and direct sales channels. There is no guarantee that these offerings will be widely accepted in the marketplace, and they will likely face competition from existing and emerging alternative products and services.

Further, an accelerated or sudden decline in physical mail volumes could have an adverse effect on our mailing business. An accelerated or sudden decline could result from, among other things, changes in our clients' communication behavior, changes in communication technologies or legislation or regulations that mandate electronic substitution, prohibit certain types of mailings, increase the difficulty of using information or materials in the mail, or impose higher taxes or fees on mailing or postal services.

If we are not successful at meeting the continuing challenges faced in our mailing business, or if physical mail volumes were to experience an accelerated or sudden decline, our financial results could be negatively impacted.

If we are unable to protect our information technology systems against service interruptions, misappropriation of data, or breaches of security resulting from cyberattacks or other events, or we encounter other unforeseen difficulties in the operation of our information technology systems, our operations could be disrupted, our reputation may be harmed and we could be subject to legal liability or regulatory enforcement action.

We rely on the continuous and uninterrupted performance of our information technology systems to support numerous business processes and activities, to support and service our clients, to support consumer transactions and to support postal services. Several of our businesses use, process and store proprietary information and sensitive or confidential data relating to our businesses, our clients, consumers and our employees. Privacy laws and similar regulations in many jurisdictions where we do business require that we take significant steps to safeguard such information, and such legal requirements continue to evolve. In today's environment there are numerous risks to cybersecurity and privacy, including individual and groups of criminal hackers, industrial espionage, employee errors and/or malfeasance and technological errors. These cyber threats are constantly evolving, thereby increasing the difficulty of detecting and successfully defending against them. We have security systems and procedures in place designed to ensure the continuous and uninterrupted performance of our information technology systems and protect against unauthorized access to such information. However, there is no guarantee that these security measures will prevent or detect the unauthorized access by experienced computer programmers, hackers or others. Successful breaches could, among other things, result in the unauthorized disclosure, theft and misuse of company, client, consumer and employee sensitive and confidential information, disrupt the performance of our information technology systems and deny services to our clients. Additionally, we could be exposed to potential liability, litigation, governmental inquiries, investigations or regulatory enforcement actions, our brand and reputation damaged, and we could be subject to the payment of fines or other penalties, legal claims by our clients and significant remediation costs.

Our systems are also subject to adverse acts of nature, computer viruses, vandalism, power loss, computer or communications failures and other unexpected events. We have business continuity and disaster recovery plans in place to protect our business operations in case of such events; however, there can be no guarantee that these plans will function as designed. If our information technology systems are damaged or cease to function properly, we could be prevented from fulfilling orders and servicing clients and postal services. Also, we

9

may have to make a significant investment to repair or replace these systems, and could suffer loss of critical data and interruptions or delays in our operations.

We depend on third-party suppliers and outsource providers and our business could be adversely affected if we fail to manage these vendors effectively.

We depend on third-party suppliers and outsource providers for a variety of services, components and supplies, including a large portion of our product manufacturing, the hosting of our software-as-a-service offerings, as well as the logistics portion of our cross-border ecommerce business, and some non-core functions and operations. In certain instances, we rely on single-sourced or limited-sourced suppliers and outsourcing vendors around the world because doing so is advantageous due to quality, price or lack of alternative sources. If production or services were interrupted and we were not able to find alternate third-party suppliers, we could experience disruptions in manufacturing and operations including product shortages, higher freight costs and re-engineering costs. If outsourcing services were interrupted, not performed, or the performance was poor, our ability to process, record and report transactions with our clients, consumers and other constituents could be impacted. Such interruptions in the provision of supplies and/or services could impact our ability to meet client demand, damage our reputation and client relationships and adversely affect our revenue and profitability.

Capital market disruptions and credit rating downgrades could adversely affect our ability to provide competitive financing services to our clients and to fund various discretionary priorities.

Our financing activities include, among other things, providing competitive financing offerings to our clients and funding various discretionary priorities, such as business investments, strategic acquisitions, share repurchases and dividend payments. We fund these activities through a combination of cash generated from operations, deposits held in the Bank, commercial paper borrowings and long-term borrowings.

Our ability to fund these activities is dependent, in part, upon our ability to borrow and the cost of borrowing in U.S. capital markets. This ability and the cost, in turn, is dependent upon our credit ratings and is subject to capital market volatility. Credit rating downgrades, an increase in our credit default swap spread, material capital market disruptions, significant withdrawals by depositors at the Bank, adverse changes to our industrial loan charter or a significant decline in cash flow could impact our ability to provide competitive finance offerings to our clients and fund other financing activities, which in turn, could adversely affect our revenue, profitability and financial condition.

The international nature of our Global Ecommerce business subjects us to increased customs and regulatory risks from cross-border transactions, and fluctuations in foreign currency exchange rates. Further, the loss of any of our largest clients in our Global Ecommerce segment could have a material adverse effect on the segment.

International sales generated by our clients processing transactions through our platform are the primary source of both revenue and profit for the Global Ecommerce segment. Our Global Ecommerce segment is subject to significant trade regulations, taxes, and duties throughout the world. Any changes to these regulations could potentially impose increased documentation and delivery requirements, increase costs, delay delivery times, and subject us to additional liabilities, which could negatively impact our ability to compete in international markets and adversely impact our revenues and profitability.

The operating results of, and sales generated from, many of our clients’ internationally focused websites running on our platform are exposed to foreign exchange rate fluctuations. Currently, our platforms are located in the United States, the United Kingdom and Australia and a majority of consumers making purchases through these platforms are in a limited number of foreign countries. A strengthening of the U.S. Dollar or British Pound relative to currencies in the countries where we do the most business impacts our ability to compete internationally as the cost of similar international products improves relative to the cost of U.S. and U.K. retailers' products. A strong U.S. Dollar or British Pound would likely result in a decrease in international sales volumes, which would adversely affect the segment's revenue and profitability.

The Global Ecommerce segment is dependent on a relatively small number of significant clients and business partners for a large portion of its revenue. The loss of any of these larger clients or business partners, or a substantial reduction in their use of our products or services, could have a material adverse effect on the revenue and profitability of the segment. There can be no assurance that our larger clients and business partners will continue to utilize our products or services at current levels, or that we would be able to replace any of these clients or business partners with others who can generate revenue at current levels.

Our business, results of operations and financial condition may be negatively impacted by conditions abroad, including local economies, political environments and fluctuating foreign currencies.

A portion of our revenue is generated from operations outside the United States. Our future revenues, costs and results of operations could be affected by changes in foreign currency exchange rates as well as by a number of other factors, including changes in economic conditions from country to country, changes in a country's political conditions, trade protection measures, licensing requirements, local tax issues, capitalization and other related legal matters. We generally hedge foreign currency denominated transactions primarily through the use of currency derivative contracts. The use of derivative contracts is intended to mitigate or reduce transactional level volatility in

10

the results of foreign operations, but does not completely eliminate volatility. We do not hedge the translation effect of international revenues and expenses, which are denominated in currencies other than our U.S. parent functional currency.

Our inability to obtain and protect our intellectual property and defend against claims of infringement by others may negatively impact our operating results.

Our business success depends in part upon protecting our intellectual property rights, including proprietary technology developed or obtained through acquisitions. We rely on copyrights, patents, trademarks and trade secrets and other intellectual property laws to establish and protect our proprietary rights. If we are unable to protect our intellectual property rights, our competitive position may suffer which could adversely affect our revenue and profitability. The continued evolution of patent law and the nature of our innovation work may affect the number of patents we are able to receive for our internal development efforts.

From time to time, third-parties may claim that we, our clients, or our suppliers, have infringed their intellectual property rights. These claims, if successful, may require us to redesign affected products, enter into costly settlement or license agreements, pay damage awards, or face a temporary or permanent injunction prohibiting us from marketing or selling certain products.

If we fail to comply with government contracting regulations, our operating results, brand name and reputation could suffer.

We have a significant number of contracts with governmental entities. Government contracts are subject to extensive and complex procurement laws and regulations, along with regular audits and investigations by government agencies. If one or more government agencies discovers instances of contractual noncompliance in the course of an audit or investigation, we may be subject to various civil or criminal penalties and administrative sanctions, which could include the termination of the contract, reimbursement of payments received, fines and debarment from doing business with one or more governments. Any of these events could not only affect us financially, but also adversely affect our brand and reputation.

We may not realize the anticipated benefits from our implementation of a new enterprise business platform, and the transition to the new enterprise business platform may not be uninterrupted or error-free.

We have made significant investments in the development and implementation of a new enterprise business platform that is expected to provide operating cost savings through the elimination of redundant systems and strategic efficiencies through the use of a standardized, integrated system. We implemented this platform for our Canadian operations in the fourth quarter of 2015, and completed the implementation of this system for our U.S. operations in the second quarter of 2016. We experienced temporary sales productivity and business disruptions from the implementations in Canada and the United States; however, material disruptions are not expected going forward.

We may not realize the anticipated benefits of strategic acquisitions and divestitures, which may harm our financial results.

As we look for opportunities to invest in strategic initiatives to drive revenue growth and market share gains while maintaining a leadership role in the mailing industry, we may make strategic acquisitions or divest certain businesses. These acquisitions and divestitures may involve significant risks and uncertainties, which could have an adverse effect on our operating results, including:

• | difficulties in achieving anticipated benefits or synergies from acquisitions and divestitures; |

• | difficulties in integrating newly acquired businesses and operations, including combining product and service offerings and entering new markets, or reducing fixed costs previously associated with divested businesses; |

• | the loss of key employees or clients of businesses acquired or divested; and |

• | significant charges to earnings for employee severance and other restructuring costs, goodwill and asset impairments and legal, accounting and financial advisory fees. |

Our investment in rebranding the company and enhancing marketing programs to build the market awareness necessary to create demand for our businesses may not result in increased revenue and could adversely affect our profitability.

Our brand strategy and identity are important to our global business transformation. Our phased roll-out of the new branding through advertising campaigns is integrated into the way we sell and service clients and acquire new clients, including sales collateral and the digital experience of getting information, service performance and transacting on our website. These factors are important to maintaining acceptance of our products and services by our existing clients and achieving increased acceptance with new clients. We expect continued spending in brand development and marketing promotion activities and if this increased spending does not result in increased revenue sufficient to offset these expenses, our profitability could be adversely affected.

Our operational costs could increase from changes in environmental regulations, or we could be subject to significant liabilities.

We are subject to various federal, state, local and foreign environmental protection laws and regulations around the world, including without limitation, those related to the manufacture, distribution, use, packaging, labeling, recycling or disposal of our products or the products of our clients for whom we perform services. Environmental rules concerning products and packaging can have a significant impact on the cost of operations or affect our ability to do business in certain countries. We are also subject to laws concerning use, discharge or disposal of materials. All of these laws are complex, change frequently and have tended to become more stringent over time.

11

If we are found to have violated these laws, we could be fined, criminally charged, otherwise sanctioned by regulators, or we could be subject to liability and clean-up costs. These risk can apply to both current and legacy operations and sites. From time to time, we may be involved in litigation over these issues. The amount and timing of costs under environmental laws are difficult to predict and there can be no assurance that these costs will not have an adverse effect our financial condition, results of operations or cash flows.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

We own or lease numerous facilities worldwide, which house general offices, including our corporate headquarters located in Stamford, Connecticut, sales offices, service locations, data centers and call centers. We conduct research and development, manufacturing and assembly, product management, information technology and many other activities at our Global Technology Center located in Danbury, Connecticut. Our other primary research and development facilities are located in Noida and Pune, India. Management believes that our facilities are well maintained, are in good operating condition and are suitable and adequate for our current business needs.

ITEM 3. LEGAL PROCEEDINGS

In the ordinary course of business, we are routinely defendants in, or party to, a number of pending and threatened legal actions. These may involve litigation by or against us relating to, among other things, contractual rights under vendor, insurance or other contracts; intellectual property or patent rights; equipment, service, payment or other disputes with clients; or disputes with employees. Some of these actions may be brought as a purported class action on behalf of a purported class of employees, clients or others.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR THE COMPANY'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is traded under the symbol "PBI" and is principally traded on the New York Stock Exchange (NYSE). At January 31, 2017, we had 16,276 common stockholders of record. The following table sets forth the high and low sales prices, as reported on the NYSE, and the cash dividends paid per share of common stock, for the periods indicated.

Stock Price | Dividend Per Share | ||||||||||

High | Low | ||||||||||

2016 | |||||||||||

First Quarter | $ | 21.60 | $ | 16.24 | $ | 0.1875 | |||||

Second Quarter | $ | 21.81 | $ | 16.28 | 0.1875 | ||||||

Third Quarter | $ | 19.33 | $ | 16.88 | 0.1875 | ||||||

Fourth Quarter | $ | 18.20 | $ | 14.22 | 0.1875 | ||||||

$ | 0.75 | ||||||||||

2015 | |||||||||||

First Quarter | $ | 24.60 | $ | 21.15 | $ | 0.1875 | |||||

Second Quarter | $ | 23.93 | $ | 20.79 | 0.1875 | ||||||

Third Quarter | $ | 21.64 | $ | 18.59 | 0.1875 | ||||||

Fourth Quarter | $ | 21.76 | $ | 19.12 | 0.1875 | ||||||

$ | 0.75 | ||||||||||

12

Share Repurchases

We may periodically repurchase shares of our common stock to manage the dilution created by shares issued under employee stock plans and for other purposes. For the full year 2016, we repurchased 10,454,835 shares of our common stock at an average share price of $18.51. During the fourth quarter of 2016 we did not repurchase any shares of our common stock. We have remaining Board authorization to repurchase up to $21 million of our common stock.

Stock Performance Graph

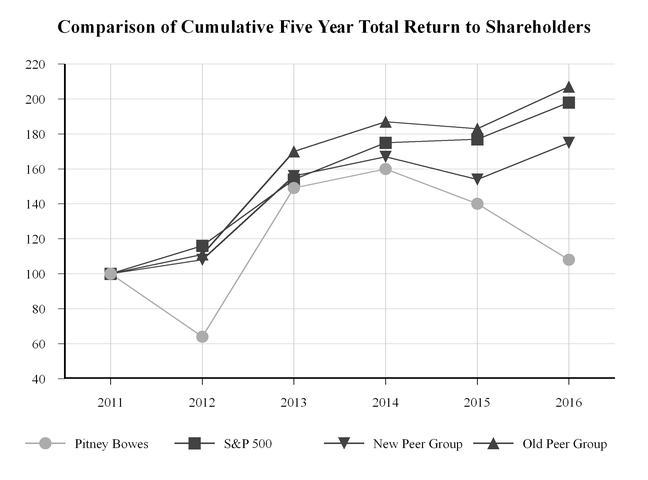

We revised our peer group from last year to exclude companies that were no longer a strong fit from a business perspective and included companies that are better aligned with our diverse business portfolio.

The new peer group is comprised of: Alliance Data Systems Corporation, Deluxe Corporation, Diebold, Incorporated, EchoStar Corp., Fidelity National Information Services, Inc., Fiserv, Inc., NCR Corp., NetApp Inc., Pitney Bowes Inc., R.R. Donnelley & Sons Company, Rockwell Automation Inc., Teradata Corp., Unisys Corporation, The Western Union Company and Xerox Corporation.

The old peer group was comprised of: Alliance Data Systems Corporation, Diebold, Incorporated, DST Systems Inc., EchoStar Corp., Fidelity National Information Services, Inc., Fiserv, Inc., Harris Corporation, Iron Mountain Inc., Lexmark International Inc., NCR Corp., Pitney Bowes Inc., R.R. Donnelley & Sons Company, Rockwell Automation Inc., Unisys Corporation, The Western Union Company and Xerox Corporation.

The accompanying graph shows the annual change in the value of a $100 investment in Pitney Bowes Inc., the Standard and Poor's (S&P) 500 Composite Index, the new peer group and the old peer group over a five-year period assuming the reinvestment of dividends. On a total return basis, a $100 investment on December 31, 2011 in Pitney Bowes Inc., the S&P 500 Composite Index, the old peer group and the new peer group would have been worth $108, $198, $207, and $175, respectively, on December 31, 2016.

All information is based upon data independently provided to us by Standard & Poor's Corporation and is derived from their official total return calculation. Total return for the S&P 500 Composite Index and each peer group is based on market capitalization, weighted for each year. The stock price performance is not necessarily indicative of future stock price performance.

13

14

ITEM 6. SELECTED FINANCIAL DATA

The following table of selected financial data should be read in conjunction with the more detailed consolidated financial statements and related notes thereto included in Item 8 of this Form 10-K.

Years Ended December 31, | |||||||||||||||||||

2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

Total revenue | $ | 3,406,575 | $ | 3,578,060 | $ | 3,821,504 | $ | 3,791,335 | $ | 3,823,713 | |||||||||

Amounts attributable to common stockholders: | |||||||||||||||||||

Net income from continuing operations | $ | 95,506 | $ | 402,672 | $ | 300,006 | $ | 287,612 | $ | 379,107 | |||||||||

(Loss) income from discontinued operations | (2,701 | ) | 5,271 | 33,749 | (144,777 | ) | 66,056 | ||||||||||||

Net income - Pitney Bowes Inc. | $ | 92,805 | $ | 407,943 | $ | 333,755 | $ | 142,835 | $ | 445,163 | |||||||||

Basic earnings per share attributable to common stockholders (1): | |||||||||||||||||||

Continuing operations | $ | 0.51 | $ | 2.01 | $ | 1.49 | $ | 1.43 | $ | 1.89 | |||||||||

Discontinued operations | (0.01 | ) | 0.03 | 0.17 | (0.72 | ) | 0.33 | ||||||||||||

Net income - Pitney Bowes Inc. | $ | 0.49 | $ | 2.04 | $ | 1.65 | $ | 0.71 | $ | 2.22 | |||||||||

Diluted earnings per share attributable to common stockholders (1): | |||||||||||||||||||

Continuing operations | $ | 0.51 | $ | 2.00 | $ | 1.47 | $ | 1.42 | $ | 1.88 | |||||||||

Discontinued operations | (0.01 | ) | 0.03 | 0.17 | (0.71 | ) | 0.33 | ||||||||||||

Net income - Pitney Bowes Inc. | $ | 0.49 | $ | 2.03 | $ | 1.64 | $ | 0.70 | $ | 2.21 | |||||||||

Cash dividends paid per share of common stock | $ | 0.75 | $ | 0.75 | $ | 0.75 | $ | 0.94 | $ | 1.50 | |||||||||

Balance sheet data: | |||||||||||||||||||

December 31, | |||||||||||||||||||

2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

Total assets (2) | $ | 5,837,133 | $ | 6,123,132 | $ | 6,476,599 | $ | 6,754,371 | $ | 7,846,867 | |||||||||

Long-term debt (2) | $ | 2,750,405 | $ | 2,489,583 | $ | 2,904,024 | $ | 3,323,231 | $ | 3,629,349 | |||||||||

Total debt (2) | $ | 3,364,890 | $ | 2,950,668 | $ | 3,228,903 | $ | 3,323,231 | $ | 4,004,349 | |||||||||

Noncontrolling interests (Preferred stockholders' equity in subsidiaries) | $ | — | $ | 296,370 | $ | 296,370 | $ | 296,370 | $ | 296,370 | |||||||||

(1) | The sum of earnings per share may not equal the totals due to rounding. |

(2) Certain prior year amounts have been revised to conform to current year presentation.

15

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

The following discussion and analysis should be read in conjunction with our consolidated financial statements and related notes. This discussion and analysis contains forward-looking statements based on management's current expectations, estimates and projections and involve risks and uncertainties. Our actual results may differ significantly from those currently expressed in our forward-looking statements as a result of various factors, including those factors described under "Forward-Looking Statements" and "Risk Factors" contained elsewhere in this Annual Report. All table amounts are presented in thousands of dollars, unless otherwise stated.

Overview

During 2016, we continued to execute on our strategic priorities to stabilize and reinvent our mail business, drive operational excellence and grow our business through digital commerce. We made acquisitions in our strategic businesses and exited certain markets (Market Exits) as part of our initiative to simplify our geographic footprint. We launched an advertising campaign to reintroduce the Pitney Bowes brand and continued to introduce new products including the Pitney Bowes Commerce Cloud, which helps our clients identify customers, locate new sales opportunities, communicate with their existing and prospective customers, power shipping globally and manage payments for mailing and shipping. Additionally, we continued to build our partner channels particularly in the software business.

During the year, we deployed our new enterprise business platform in the United States, which is one of the productivity initiatives to drive operational excellence. As a result of the conversion process and required sales and support training, we experienced reduced productivity and lost sales, which adversely impacted equipment sales and stream revenues.

Financial Highlights

Revenue -2016 compared to 2015

Revenue for 2016 decreased 5% to $3,407 million compared to $3,578 million in 2015. Of this decrease, 1% is attributable to foreign currency translation and 1% to Market Exits.

• | Equipment sales declined 3%, supplies revenues declined 9%, software revenue declined 10%, rentals revenue declined 7%, financing income declined 11% and support services revenue declined 8%. Business services revenue increased 3%, partially offsetting these declines. |

• | Within SMB, North America Mailing revenue was down 6% and International Mailing revenue was down 9%. In total, SMB revenue decreased 7% on a reported basis and 6% excluding the impacts of foreign currency translation and Market Exists. |

• | Within Enterprise Business Solutions, Production Mail revenue decreased 4% and Presort revenue was flat. In total, Enterprise Business Solutions revenue decreased 2% on a reported basis and was flat excluding the impacts of foreign currency translation and Market Exists. |

• | Within DCS, Global Ecommerce revenue increased 18%, but was partially offset by a 10% decrease in Software Solutions revenue. In total, DCS revenue increased 4% on a reported basis and 6% excluding the impacts of foreign currency translation. |

Net Income

Net income and diluted earnings per share from continuing operations for 2016 were $93 million and $0.49, respectively, compared to $408 million and $2.03, respectively, for 2015. The decrease in net income was primarily due to the $111 million gain on the sale of Imagitas in 2015, and a $171 million goodwill impairment charge related to our Software Solutions reporting unit, lower revenue and gross margin, and higher restructuring and asset impairment charges, partially offset by lower selling, general and administrative expenses in 2016.

16

Cash Flows

Cash and cash equivalents at December 31, 2016 increased $124 million compared to December 31, 2015. Sources and uses of cash include:

Sources:

• | Generated cash from operations of $491 million; |

• | Increased net long-term borrowings by $524 million; |

• | Cash from investment activities of $75 million; and |

• | Received $18 million for the sale of assets; |

Uses:

• | Redeemed preferred stock of subsidiary for $300 million; |

• | Spent $197 million to repurchase our common stock; |

• | Spent $161 million on capital expenditures; |

• | Paid dividends of $141 million to our common stockholders and $19 million to noncontrolling interests; |

• | Repaid $90 million of commercial paper borrowings; and |

• | Acquired Enroute and Maponics for an aggregate $38 million. |

Outlook

We anticipate that the introduction of new products and digital capabilities, the implementation of the new enterprise business platform, and incremental marketing will continue to provide long term benefits. We expect to see on-going cost-savings through the benefits of our restructuring actions and our new enterprise business platform. This will be offset, in part, by the normalization of variable compensation compared to 2016.

Within SMB Solutions, we anticipate that the introduction of new solutions and digital capabilities, particularly those included in the Pitney Bowes Commerce Cloud, will help further stabilize revenue over the long-term. In addition we plan to introduce technology upgrades to our meters later in 2017. We do not anticipate further significant disruption in sales productivity from the implementation of our enterprise platform, and expect to continue realizing the benefits from this platform. Internationally, we anticipate further stabilizing financial results from cost savings initiatives and rationalization of our geographic footprint.

Within Enterprise Business Solutions, we anticipate revenue and profitability growth in Presort Services due to network expansion and the January 2017 USPS rate change, which creates a greater incentive for high volume mailers to leverage our solutions. We expect that Production Mail revenue growth will continue to be challenged by consolidation and outsourcing pressures on services revenue.

Within DCS, we continue to build our partner channel in Software Solutions by adding new regional systems integrators and location intelligence partners. We continue to invest in expanding the indirect channel and training partner sales and technical resources. Although it takes time for a partner program to add significantly to our revenue, we do anticipate additional revenue from our partner channel in 2017. We continue to focus on improving direct sales effectiveness to grow the license revenue pipeline and have made changes to the sales organization structure to expedite this improvement. We anticipate continued growth in our ecommerce business with our existing marketplace sites (sites where multiple sellers sell) and individual retail clients, new client acquisition and expanded service offerings. A strong U.S. dollar could continue to affect demand for U.S. goods sold to customers in other countries, but such an impact could continue to be mitigated by the effects of a weakened British Pound on sales of U.K. goods to customers in other countries. We continue to expand and globalize our cross-border ecommerce offerings, including the successful launch of our cross-border platform for Australian retail clients, which diversifies the business and helps to mitigate foreign currency risk.

17

RESULTS OF OPERATIONS

Revenue by source and the related cost of revenue are shown in the following tables:

Revenue | % change | ||||||||||||||||||||||

Years Ended December 31, | Actual | Constant Currency | |||||||||||||||||||||

2016 | 2015 | 2014 | 2016 | 2015 | 2016 | 2015 | |||||||||||||||||

Equipment sales | $ | 675 | $ | 695 | $ | 770 | (3 | )% | (10 | )% | (2 | )% | (5 | )% | |||||||||

Supplies | 263 | 288 | 300 | (9 | )% | (4 | )% | (7 | )% | 2 | % | ||||||||||||

Software | 349 | 386 | 430 | (10 | )% | (10 | )% | (7 | )% | (5 | )% | ||||||||||||

Rentals | 413 | 442 | 485 | (7 | )% | (9 | )% | (6 | )% | (6 | )% | ||||||||||||

Financing | 366 | 410 | 433 | (11 | )% | (5 | )% | (10 | )% | (2 | )% | ||||||||||||

Support services | 513 | 555 | 625 | (8 | )% | (11 | )% | (7 | )% | (7 | )% | ||||||||||||

Business services | 828 | 802 | 779 | 3 | % | 3 | % | 4 | % | 3 | % | ||||||||||||

Total revenue | $ | 3,407 | $ | 3,578 | $ | 3,822 | (5 | )% | (6 | )% | (4 | )% | (3 | )% | |||||||||

Cost of Revenue | ||||||||||||||||||||

Years Ended December 31, | ||||||||||||||||||||

2016 | 2015 | 2014 | ||||||||||||||||||

$ | % of revenue | $ | % of revenue | $ | % of revenue | |||||||||||||||

Cost of equipment sales | $ | 332 | 49.1 | % | $ | 331 | 47.6 | % | $ | 366 | 47.5 | % | ||||||||

Cost of supplies | 81 | 31.0 | % | 89 | 30.8 | % | 94 | 31.2 | % | |||||||||||

Cost of software | 106 | 30.4 | % | 114 | 29.4 | % | 124 | 28.8 | % | |||||||||||

Cost of rentals | 76 | 18.4 | % | 84 | 19.1 | % | 97 | 20.1 | % | |||||||||||

Financing interest expense | 55 | 15.1 | % | 72 | 17.5 | % | 78 | 18.1 | % | |||||||||||

Cost of support services | 296 | 57.7 | % | 323 | 58.2 | % | 377 | 60.3 | % | |||||||||||

Cost of business services | 569 | 68.7 | % | 546 | 68.1 | % | 545 | 70.0 | % | |||||||||||

Total cost of revenue | $ | 1,515 | 44.5 | % | $ | 1,559 | 43.6 | % | $ | 1,681 | 44.0 | % | ||||||||

The discussion below refers to revenue growth on a constant currency basis to exclude the impact of changes in foreign currency exchange rates since the prior period under comparison. Constant currency measures are intended to help investors better understand the underlying revenue performance of the business excluding the impacts of shifts in currency exchange rates over the period. Constant currency is calculated by converting our current quarter reported revenue using the prior year’s exchange rate for the comparable quarter.

Equipment sales

Equipment sales decreased 3% in 2016 compared to 2015. On a constant currency basis, equipment sales decreased 2% primarily due to:

• | 3% from lower mailing equipment sales in North America, due in part to sales disruption during the second quarter from the platform cut-over; and |

• | 1% from Market Exits; partially offset by |

• | 2% from higher sales in our production mail business, primarily due to higher installations of sorter, inserter and print equipment. |

Cost of equipment sales as a percentage of equipment sales revenue increased to 49.1% compared to 47.5% in 2015 primarily due to product mix.

Equipment sales decreased 10% in 2015 compared to 2014. On a constant currency basis, equipment sales decreased 5% primarily due to:

• | 3% from international mailing equipment sales primarily due to difficult economic circumstances and productivity disruptions caused by the implementation of our go-to-market strategy in Europe; |

• | 1% from lower sales of production mail equipment worldwide; and |

• | 1% from lower sales in North America due to the continuing trend of clients to extend existing leases rather than purchase new equipment. |

Cost of equipment sales as a percentage of equipment sales revenue of 47.6% was comparable from 2015 to 2014.

18

Supplies

Supplies sales decreased 9% in 2016 compared to 2015. On a constant currency basis, supplies revenue decreased 7% primarily due to:

• | 4% from lower North America mailing supplies sales; |

• | 1% from lower international mailing supplies, primarily in the U.K. and France; |

• | 1% from lower sales in our production mail business; and |

• | 1% from Market Exits. |

Cost of supplies as a percentage of supplies revenue increased slightly to 31.0% in 2016 compared to 30.8% in 2015 primarily due to lower revenue and sales productivity issues.

Supplies sales decreased 4% in 2015 compared to 2014, On a constant currency basis, supplies revenue increased 2% primarily due to:

• | 1% from our worldwide mailing businesses primarily due to productivity improvements and pricing actions; and |

• | 1% from higher sales of supplies for production printers. |

Cost of supplies as a percentage of supplies revenue improved to 30.8% in 2015 compared to 31.2% in 2014 primarily due to a greater mix of higher margin core supplies.

Software

Software revenue decreased 10% in 2016 compared to 2015. On a constant currency basis, software revenue decreased 7% primarily due to a worldwide decline in licensing revenue. License revenue from our Customer Engagement and our Location Intelligence software offerings declined but were partly offset by growth in the Customer Information Management software license revenue. Cost of software as a percentage of software revenue increased to 30.4% in 2016 compared to 29.4% in 2015 primarily due to the decline in high-margin licensing revenue.

Software revenue decreased 10% in 2015 compared to 2014. On a constant currency basis, software revenue decreased 5% in primarily due to:

• | 4% from more significant licensing deals in 2014 compared to 2015; and |

• | 1% from declines in maintenance, data and services revenue. |

Cost of software as a percentage of software revenue increased to 29.4% in 2015 compared to 28.8% in 2014 primarily due to declines in high-margin licensing revenue.

Rentals

Rentals revenue decreased 7% in 2016 compared to 2015 and 9% in 2015 compared to 2014. On a constant currency basis, rentals revenue decreased 6% in both periods. These decreases are primarily due to a reduction in the number of installed meters worldwide and the continuing shift by certain customers to less-featured, lower cost machines.

Cost of rentals as a percentage of rentals revenue improved from 20.1% in 2014 to 19.1% in 2015 and to 18.4% in 2016 primarily due to lower depreciation.

Financing

Financing revenue decreased 11% in 2016 compared to 2015. On a constant currency basis, financing revenue decreased 10% primarily due to lower mailing equipment sales in prior periods, a declining lease portfolio and lower financing fees as a result of proactive waivers to allow clients to adjust to new billing formats and timing of invoices being sent as a result of the platform cutover.

Financing revenue decreased 5% in 2015 compared to 2014. On a constant currency basis, financing revenue decreased 2% as a result of lower equipment sales in prior periods and a declining lease portfolio.

We allocate a portion of our total cost of borrowing to financing interest expense. In computing financing interest expense, we assume an 8:1 debt to equity leverage ratio (10:1 in 2015 and 2014) and apply our overall effective interest rate to the average outstanding finance receivables. Finance interest expense decreased 23% in 2016 compared to 2015 primarily due to a decline in our overall effective interest rate and lower average outstanding finance receivables. Finance interest expense decreased 9% in 2015 compared to 2014 primarily due to lower average outstanding finance receivables. Financing interest expense as a percentage of financing revenue was 15.1% in 2016, 17.5% in 2015 and 18.1% in 2014.

19

Support Services

Support services revenue decreased 8% in 2016 compared to 2015. On a constant currency basis, revenue decreased 7% primarily due to:

• | 2% from lower maintenance revenue on production mail equipment as some in-house mailers moved their mail processing to third-party service bureaus who service some of their own equipment; |

• | 2% from the worldwide decline in the number of mailing machines in service and shift to less-featured, lower cost machines; and |

• | 2% from Market Exits. |

Cost of support services as a percentage of support services revenue improved to 57.7% in 2016 compared to 58.2% in 2015 primarily due to expense reductions and productivity initiatives.

Support services revenue decreased 11% in 2015 compared to 2014. On a constant currency basis, revenue decreased 7%, primarily due to:

• | 5% from lower maintenance contracts on production mail equipment as some in-house mailers moved their mail processing to third-party service bureaus who service some of their own equipment; and |

• | 2% from Market Exits. |

Cost of support services as a percentage of support services revenue improved to 58.2% in 2015 compared to 60.3% in 2014 primarily due to expense reductions and productivity initiatives.

Business Services

Business services revenue increased 3% in 2016 compared to 2015. On a constant currency basis, revenue increased 4%; however, excluding the revenue in 2015 from our Imagitas business, which was sold in May 2015, business services revenue increased 11% in 2016 compared to 2015 primarily due to:

• | 10% from growth in our Ecommerce business from the expansion of our U.S. and U.K. cross-border marketplace business and retail network, including a full year of operations of Borderfree (acquired June 2015); and |

• | 1% from higher shipping solutions services. |

Cost of business services as a percentage of business services revenue increased to 68.7% in 2016 and compared to 68.1% in 2015, primarily due to higher mail processing costs in the presort business.

Business services revenue increased 3% in 2015 compared to 2014. On a constant currency basis, revenue increased 3%. Business Services revenue for 2015 was impacted by the sale of Imagitas in May 2015 and the acquisition of Borderfree in June 2015. Excluding the impacts of these transactions, business services revenue increased 5% primarily due to:

• | 4% from additional volumes of packages shipped from our U.K. outbound cross-border service facility; and |

• | 2% from higher volumes of mail processed in Presort Services. |

Cost of business services as a percentage of business services revenue improved to 68.1% in 2015 and compared to 70% in 2014, primarily due to operational efficiencies in Presort Services and higher revenue.

Selling, general and administrative (SG&A)

SG&A expense decreased 6% in 2016 compared to 2015 primarily due to lower salaries and benefits expense from our prior restructuring actions, lower annual variable compensation costs of $36 million, benefits from the new enterprise business platform of $28 million, loan forgiveness income of $10 million (see Note 11 to the Consolidated Financial Statements), a favorable sales tax adjustment of $5 million and other productivity and cost-saving initiatives. SG&A expense in 2015 also included a one-time compensation charge of $10 million related to the acquisition of Borderfree.

SG&A expense decreased 7% in 2015 compared to 2014 despite expenses of $13 million associated with implementation of our enterprise business platform, a one-time compensation charge of $10 million for the accelerated vesting and settlement of Borderfree stock-based compensation awards, additional amortization expense of $9 million related to the acquisition of Borderfree and costs of $5 million related to the exit of certain geographic markets during the fourth quarter of 2015. The overall decrease in SG&A expense is primarily due to our focus on operational excellence and the benefits of productivity and cost-cutting initiatives. Foreign currency translation also reduced SG&A expenses by 4% in 2015.

20

Restructuring charges and asset impairments, net