Attached files

| file | filename |

|---|---|

| EX-31.A - EXHIBIT 31.A - NEWMARKET CORP | neu-20161231xexhibit31a.htm |

| EX-32.B - EXHIBIT 32.B - NEWMARKET CORP | neu-20161231xexhibit32b.htm |

| EX-32.A - EXHIBIT 32.A - NEWMARKET CORP | neu-20161231xexhibit32a.htm |

| EX-31.B - EXHIBIT 31.B - NEWMARKET CORP | neu-20161231xexhibit31b.htm |

| EX-23 - EXHIBIT 23 - NEWMARKET CORP | neu-20161231xexhibit23cons.htm |

| EX-21 - EXHIBIT 21 - NEWMARKET CORP | neu-20161231xexhibit21subs.htm |

| EX-12 - EXHIBIT 12 - NEWMARKET CORP | neu-20161231xexhibit12rati.htm |

| EX-10.12 - EXHIBIT 10.12 - NEWMARKET CORP | neu-20161231xexhibit1012di.htm |

| EX-10.11 - EXHIBIT 10.11 - NEWMARKET CORP | neu-20161231xexhibit1011of.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-32190

NEWMARKET CORPORATION

Incorporated pursuant to the Laws of the Commonwealth of Virginia

Internal Revenue Service Employer Identification No. 20-0812170

330 South Fourth Street

Richmond, Virginia 23219-4350

804-788-5000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

COMMON STOCK, without par value | NEW YORK STOCK EXCHANGE | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | o | |

Non-accelerated filer | o | Smaller reporting company | o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

Aggregate market value of voting stock held by non-affiliates of the registrant as of June 30, 2016 (the last business day of the registrant’s most recently completed second fiscal quarter): $3,560,347,159*

Number of shares of Common Stock outstanding as of January 31, 2017: 11,852,697

DOCUMENTS INCORPORATED BY REFERENCE

Portions of NewMarket Corporation’s definitive Proxy Statement for its 2017 Annual Meeting of Shareholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A under the Securities Exchange Act of 1934 are incorporated by reference into Part III of this Annual Report on Form 10-K.

* | In determining this figure, an aggregate of 3,256,398 shares of Common Stock as beneficially owned by Bruce C. Gottwald and members of his immediate family have been excluded and treated as shares held by affiliates. See Item 12. The aggregate market value has been computed on the basis of the closing price on the New York Stock Exchange on June 30, 2016. |

Form 10-K

Table of Contents

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

Item 16. | ||

2

PART I

ITEM 1. | BUSINESS |

NewMarket Corporation (NewMarket) (NYSE: NEU) is a holding company and is the parent company of Afton Chemical Corporation (Afton), Ethyl Corporation (Ethyl), NewMarket Services Corporation (NewMarket Services), and NewMarket Development Corporation (NewMarket Development).

Each of our subsidiaries manages its own assets and liabilities. Afton manufactures and sells petroleum additives, while Ethyl represents the sale of tetraethyl lead (TEL) in North America and certain contracted manufacturing and services. NewMarket Development manages the property that we own in Virginia. NewMarket Services provides various administrative services to NewMarket, Afton, Ethyl, and NewMarket Development. NewMarket Services departmental expenses and other expenses are billed to each subsidiary pursuant to services agreements between the companies.

References in this Annual Report on Form 10-K to “we,” “us,” “our,” and “NewMarket” are to NewMarket Corporation and its consolidated subsidiaries, unless the context indicates otherwise.

As a specialty chemicals company, Afton develops and manufactures highly formulated lubricant and fuel additive packages and markets and sells these products worldwide. Afton is one of the largest lubricant and fuel additives companies in the world. Lubricant and fuel additives are necessary products for efficient and reliable operation of vehicles and machinery. From custom-formulated additive packages to market-general additives, we believe Afton provides customers with products and solutions that make engines run smoother, machines last longer, and fuels burn cleaner.

Through an open, flexible, and collaborative style, Afton works closely with its customers to understand their business and help them meet their goals. This style has allowed Afton to develop long-term relationships with its customers in every major region of the world, which Afton serves through eleven manufacturing facilities across the globe.

With more than 550 employees in research and development, Afton is dedicated to developing additive formulations that are tailored to our customers’ and the end-users’ specific needs. Afton’s portfolio of technologically-advanced, value-added products allows it to provide a full range of products, services, and solutions to its customers.

Ethyl provides contracted manufacturing and services to Afton and to third parties, and is a marketer of TEL in North America.

NewMarket Development manages the property that we own in Richmond, Virginia consisting of approximately 57 acres. Our corporate offices are included in this acreage, as well as a research and testing facility, and several acres dedicated to other uses. We are currently exploring various development opportunities for portions of the property as the demand warrants. This effort is ongoing in nature, as we have no specific timeline for any future developments.

We were incorporated in the Commonwealth of Virginia in 2004. Our principal executive offices are located at 330 South Fourth Street, Richmond, Virginia, and our telephone number is (804) 788-5000. We employed 1,998 people at the end of 2016.

Business Segments

Our business is composed of one segment, petroleum additives, which is primarily represented by Afton. The TEL business of Ethyl is reflected in the “All other” category. Each of these is discussed below.

Petroleum Additives—Petroleum additives are used in lubricating oils and fuels to enhance their performance in machinery, vehicles, and other equipment. We manufacture chemical components that are selected to perform one or more specific functions and combine those chemicals with other chemicals or components to form additive packages for use in specified end-user applications. The petroleum additives market is a global marketplace, with customers ranging from large, integrated oil companies to national and independent companies.

3

We believe our success in the petroleum additives market is largely due to our ability to deliver value to our customers through our products and our open, flexible, and collaborative working style. We accomplish this by understanding what our customers value and by applying our technical capabilities, formulation expertise, broadly differentiated product solutions, and global supply capabilities to satisfy the customers' needs. We invest significantly in research and development in order to meet our customers’ needs and to adapt to the rapidly changing environment for new and improved products and services.

We view the petroleum additives marketplace as being comprised of two broad product applications: lubricant additives and fuel additives. Lubricant additives are highly formulated chemical solutions that, when blended with base fluids, improve the efficiency, durability, performance, and functionality of mineral oils, synthetic oils, and biodegradable fluids, thereby enhancing the performance of machinery and engines. Fuel additives are chemical components that help oil refiners meet fuel specifications or formulated packages that improve the performance of gasoline, diesel, biofuels, and other fuels, resulting in lower operating costs, improved vehicle performance, and reduced tailpipe or smokestack emissions.

Lubricant Additives

Lubricant additives are essential ingredients for making lubricating oils. Lubricant additives are used in a wide variety of vehicle and industrial applications, including engine oils, transmission fluids, off-road powertrain and hydraulic systems, gear oils, hydraulic oils, turbine oils, metalworking fluids and virtually any other application where metal-to-metal moving parts are utilized. Lubricant additives are organic and synthetic chemical components that enhance wear protection, prevent deposits, and protect against the hostile operating environment of an engine, transmission, axle, hydraulic pump, or industrial machine.

Lubricants are widely used in operating machinery from transportation vehicles to heavy industrial equipment. Lubricants provide a layer of protection between moving mechanical parts. Without this layer of protection, the normal functioning of machinery would not occur. Effective lubricants reduce downtime and increase efficiency. Specifically, lubricants serve the following main functions:

• | friction reduction—Friction is reduced by maintaining a thin film of lubricant between moving surfaces, preventing them from coming into direct contact with one another and reducing wear on moving machinery, thereby providing longer life and operational efficiency. |

• | heat removal—Lubricants act as coolants by removing heat resulting either from friction or through contact with other, higher temperature materials. |

• | containment of contaminants—Lubricants function by carrying contaminants away from the machinery and neutralizing the harmful impact of the by-products created by combustion. |

The functionality of lubricants is created through an exact balance between a base fluid and performance enhancing additives. This balance is the goal of effective formulations achieved by experienced research and development professionals. We offer a full line of lubricant additive packages, each of which is composed of component chemicals specially selected to perform desired functions. We manufacture most of the chemical components and blend these components to create formulated additives packages designed to meet industry and customer specifications. Lubricant additive components are generally classified based upon their intended functionality, including:

• | detergents, which clean moving parts of engines and machines, suspend oil contaminants and combustion by-products, and absorb acidic combustion products; |

• | dispersants, which serve to inhibit the formation of sludge and particulates; |

• | extreme pressure/antiwear agents, which reduce wear on moving engine and machinery parts; |

• | viscosity index modifiers, which improve the viscosity and temperature characteristics of lubricants and help the lubricant flow evenly to all parts of an engine or machine; and |

• | antioxidants, which prevent oil from degrading over time. |

4

We are one of the leading global suppliers of specially formulated lubricant additives that combine some or all of the components described above to develop our products. Our products are highly formulated, complex chemical compositions derived from extensive research and testing to ensure all additive components work together to provide the intended results. Our products are engineered to meet specifications prescribed by either the industry or a specific customer. Purchasers of lubricant additives tend to be integrated oil companies or independent compounders/blenders. We make no sales directly to end-users or to original equipment manufacturers (OEMs).

We view our participation in the lubricant marketplace in three primary areas: engine oil additives, driveline additives, and industrial additives. Our view is not necessarily the same way others view the market.

Engine Oil Additives—The largest submarket within the lubricant additives marketplace is engine oil additives which consists of additives designed for passenger cars, motorcycles, on and off-road heavy duty commercial equipment, locomotives, and large engines in ocean-going vessels. We estimate engine oil additives represent approximately 70% of the overall lubricant additives market volume.

The engine oil market’s primary customers include consumers, fleet owners, mining and construction companies, farmers, railroads, shipping companies, service dealers, and OEMs. The primary functions of engine oil additives are to reduce friction, prevent wear, control formation of sludge and oxidation, and prevent rust. Engine oil additives are typically sold to lubricant manufacturers who combine them with a base oil fluid to meet internal, industry, and OEM specifications.

Key drivers of engine oil additives demand are the total vehicle miles driven, fuel economy, number of vehicles on the road, the average age of vehicles on the road, drain intervals, engine and crankcase size, changes in engine design, and temperature and specification changes driven by the OEMs. The extension of drain intervals has generally offset increased demand due to higher vehicle population, new hardware, and more miles driven. Other key drivers include industrial production rates, agricultural output, mining and construction output, environmental regulations, and infrastructure investments of commercial companies. Afton offers products that enhance the performance of mineral, part-synthetic, and fully-synthetic engine oils.

Driveline Additives—The driveline additives submarket is comprised of additives designed for products such as transmission fluids, axle fluids, and off-road powertrain fluids. This submarket shares in the 30% of the market not covered by engine oil additives. Transmission fluids primarily serve as the power transmission and heat transfer medium in the area of the transmission where the torque of the drive shaft is transferred to the gears of the vehicle. Axle fluids lubricate gears and bearings in axles, and powertrain fluids are used in off-highway powertrain and hydraulic systems. Other products in this area include power steering fluids, shock absorber fluids, gear oils, and lubricants for heavy machinery. These products must conform to highly prescribed specifications developed by vehicle OEMs for specific models or designs. These additives are generally sold to oil companies for ultimate sale to vehicle OEMs for new vehicles (factory-fill), service dealers for aftermarket servicing (service-fill), retailers, and distributors.

Key drivers of the driveline additives marketplace are the number of vehicles manufactured, total number of vehicles in operation, drain intervals for transmission fluids and axle fluids, changes in engine and transmission design and temperatures, and specification changes driven by the OEMs.

Industrial Additives—The industrial additives submarket is comprised of additives designed for products for industrial applications such as hydraulic fluids, grease, industrial gear fluids, industrial specialty applications, such as turbine oils, and metalworking fluids. This submarket also shares in the 30% of the market not covered by engine oil additives. These products must conform to industry specifications, OEM requirements, and/or application and operating environment demands. Industrial additives are generally sold to oil companies, service dealers for after-market servicing, and distributors.

Key drivers of the industrial additives marketplace are gross domestic product levels and industrial production.

5

Fuel Additives

Fuel additives are chemical compounds that are used to improve both the oil refining process and the performance of gasoline, diesel, biofuels, and other fuels. Benefits of fuel additives in the oil refining process include reduced use of crude oil, lower processing costs, and improved fuel storage properties. Fuel performance additives enhance fuel economy, improve ignition and combustion efficiency, reduce emission particulates, maintain engine cleanliness, and protect against deposits in fuel injectors, intake valves, and the combustion chamber. Our fuel additives are extensively tested and designed to meet stringent industry, government, OEM, and individual customer requirements.

Many different types of additives are used in fuels. Their use is generally determined by customer, industry, OEM, and government specifications, and often differs from country to country. The types of fuel additives we offer include:

• | gasoline performance additives, which clean and maintain key elements of the fuel delivery systems, including fuel injectors and intake valves, in gasoline engines; |

• | diesel fuel performance additives, which perform similar cleaning functions in diesel engines; |

• | cetane improvers, which increase the cetane number (ignition quality) in diesel fuel by reducing the delay between injection and ignition; |

• | stabilizers, which reduce or eliminate oxidation in fuel; |

• | corrosion inhibitors, which minimize the corrosive effects of combustion by-products and prevent rust; |

• | lubricity additives, which restore lubricating properties lost in the refining process; |

• | cold flow improvers, which improve the pumping and flow of distillate and diesel fuels in cold temperatures; and |

• | octane enhancers, which increase octane ratings and decrease emissions. |

We offer a broad line of fuel additives worldwide and sell our products to major fuel marketers and refiners, as well as independent terminals and other fuel blenders.

Key drivers in the fuel additive marketplace include total vehicle miles driven, fuel economy, the introduction of new engine designs, regulations on emissions (both gasoline and diesel), quality of the crude oil slate and performance standards, and marketing programs of major oil companies.

Competition

We believe we are one of the four largest manufacturers and suppliers in the petroleum additives marketplace.

In the lubricant additives submarket of petroleum additives, our major competitors are The Lubrizol Corporation (a wholly-owned subsidiary of Berkshire Hathaway Inc.), Infineum (a joint venture between ExxonMobil Chemical and Royal Dutch Shell plc), and Chevron Oronite Company LLC. There are several other suppliers in the worldwide market who are competitors in their particular product areas.

The fuel additives submarket is characterized by more competitors. While we participate in many facets of the fuel additives market, our competitors tend to be more narrowly focused. In the gasoline detergent market, we compete mainly against BASF, Chevron Oronite Company LLC, and The Lubrizol Corporation. In the diesel and refinery markets, we compete mainly against The Lubrizol Corporation, Infineum, BASF, Clariant Ltd., and Innospec Inc. We also compete against other regional competitors in the fuel additives marketplace.

The competition among the participants in these industries is characterized by the need to provide customers with cost effective, technologically-capable products that meet or exceed industry specifications. The need to continually increase technology performance and lower cost through formulation technology and cost improvement programs is vital for success in this environment.

6

All Other—The “All other” category includes the operations of the TEL business (primarily sales of TEL in North America), as well as certain contracted manufacturing and services performed by Ethyl. The Ethyl facility is located in Houston, Texas and is substantially dedicated to terminal operations related to TEL and other fuel additives. The financial results of the petroleum additives activities by Ethyl are reflected in the petroleum additives segment results. The “All other” category financial results include a service fee charged by Ethyl for its production services to Afton.

Raw Materials and Product Supply

We use a variety of raw materials and chemicals in our manufacturing and blending processes and believe the sources of these are adequate for our current operations. The primary raw materials for Afton are base oil, polyisobutylene, antioxidants, alcohols, solvents, sulfonates, friction modifiers, olefins, and copolymers.

As the performance requirements of our products become more complex, we often work with highly specialized suppliers. In some cases, we source from a single supplier. In cases where we decide to source from a single supplier, we manage our risk by maintaining safety stock of the raw material or qualifying alternate suppliers. The backup position could take additional time to implement, but we are confident we can ensure continued supply for our customers. We continue to monitor the raw material supply situation and continually adjust our procurement strategies as conditions require.

Research, Development, and Testing

Research, development, and testing (R&D) provides Afton with new performance-based solutions for our customers in the petroleum additives market. We develop products through a combination of chemical synthesis, formulation development, engineering design, and performance testing. In addition to developing new products, R&D provides our customers and OEMs with data to substantiate product differentiation and technical support to assure total customer satisfaction.

We are committed to providing the most advanced products, comprehensive testing programs, and superior technical solutions tailored to the needs of our customers and to OEMs worldwide. R&D expenditures, which totaled $157 million in 2016, $158 million in 2015, and $139 million in 2014, are expected to remain essentially flat in 2017. Afton continues to expand our internal testing, research, and customer support capabilities around the world in support of our goals of providing market-driven technical leadership and performance-based differentiation. In 2016, we invested in additional capability at our laboratories in Suzhou, China and Bracknell, United Kingdom.

Afton continues to develop new products and technology to meet the changing requirements of OEMs and to keep our customers well-positioned for the future. A significant portion of our R&D investment is dedicated to the development of products that are differentiated by their ability to deliver improved fuel efficiency in addition to robust performance in a wide range of new vehicle and industrial equipment designs. Afton’s state-of-the art testing capabilities are enabling customized research in all areas of performance needed by both OEMs and tier one suppliers. Our leading-edge capabilities and fundamental understanding in the areas of combustion, friction control, energy efficiency, and wear prevention are used to set the stage for next generation products in all areas.

In 2016, we successfully launched new technologies across all of our lubricant additive and fuel additive product areas. We developed new engine oil products for passenger cars and commercial trucks in support of our customers in all the major regions of the world in which we operate. Research in the engine oil area remained high as we developed and launched products in 2016 to meet new European and North America industry standards and as we prepare for the new engine oil specification in North America for passenger car motor oil, ILSACGF-6. This new specification is expected to go into effect in 2019.

Our industrial additives product line continued to expand with the development of new products in multiple application areas including hydraulic fluids, industrial gear oils, turbine oils, grease additives, and metalworking fluid additives. Research is focused on the development of technologies that will provide differentiation to our customers in multiple performance areas including equipment life and energy efficiency.

7

We continue to provide leading technology in the fuel additives area. In 2016, we developed and launched new products in all product lines including gasoline performance additives and diesel performance additives, as well as additives used in the refining and distribution of fuels. Research is focused on the development of new technologies that perform well in new, modern engine designs and changing fuel properties, as well as addressing the growing need for increased fuel economy and emissions reduction. In addition, we continue to maintain close interactions with regulatory, industry, and OEM leaders to guide our development of future fuel additive technologies based on well-defined market needs.

Research continued in our transmission fluid, axle oil, and tractor fluid product lines. This included the development of new OEM-specific additives used in factory fill fluids installed during automotive component and vehicle assembly in the United States, Germany, Japan, India, and China. In addition, we developed new products for the service-fill sector to provide our customers with the latest additive technology available to differentiate their offering to the retail market.

Intellectual Property

Our intellectual property, including our patents, licenses, and trademarks, is an important component of our business. We actively protect our inventions, new technologies, and product developments by filing patent applications and maintaining trade secrets. We currently own approximately 1,200 issued or pending United States and foreign patents. In addition, we have acquired the rights under patents and inventions of others through licenses or otherwise. We take care to respect the intellectual property rights of others and we believe our products do not infringe upon those rights. We vigorously participate in patent opposition proceedings around the world, where necessary, to secure a technology base free of infringement. We believe our patent position is strong, aggressively managed, and sufficient for the conduct of our business.

We also have several hundred trademark registrations throughout the world for our marks, including NewMarket®, Afton Chemical®, Ethyl®, mmt®, HiTEC®, TecGARD®, GREENBURN®, Passion for Solutions®, CleanStart®, Polartech®, BioTEC®, Microbotz®, and Axcel®, as well as a pending trademark application for DriveMoreTM.

Commitment to Environmental and Safety Excellence

Our commitment to the environment and safety excellence applies to every employee, contractor, and visitor every day, at every site. Safety and environmental responsibility are a way of life at NewMarket - enhancing operations, the way we work, and the relationships we maintain with our employees, customers, supply chain partners, and the communities in which we operate. Our objective is to establish a culture where our employees understand that good environmental and safety performance is good business and understand that environmental compliance and safety is their personal responsibility. Every employee at NewMarket is responsible for ensuring that our high standards in the area of health, safety (including process safety), environmental protection, and security are upheld at all times.

Our Global Responsible Care Policy Statement includes a commitment to conduct operations in a manner that protects our employees, communities, and the environment, to comply with all applicable laws and regulations, and to reduce our environmental impacts. Additionally, in pursuit of our vision of zero incidents, we work with our employees and other key stakeholders to establish appropriate goals, objectives and targets.

Both Afton and Ethyl have implemented Responsible Care Management Systems (RCMS® or RC14001®) at U.S. facilities. Our implementation of RCMS® is certified by an independent third-party auditing process. Additionally, Afton’s Feluy, Belgium; Suzhou, China; Hyderabad, India; and Manchester, England plants are certified to the environmental standard ISO 14001. Suzhou is also certified to OHSAS 18001, a global occupational health and safety standard. Afton’s Sauget, Illinois plant continues to be an OSHA VPP (Voluntary Protection Program) “Star” worksite.

In 2016, we continued to enhance our “Actively Caring” safety program, where people look out for the safety and welfare of others with courage and compassion, enabling the achievement of an injury-free environment. Our worldwide injury/illness recordable rate (which is the number of injuries per 200,000 hours worked) in 2016 was .52. Our performance is a demonstration of our safety-first culture and represents a focused effort by all of our employees. We are extremely proud of our accomplishments in this area. Both Afton and Ethyl continue to be top performers among their industry peers. While our safety performance is very strong, we strive for continual improvement with a vision of having zero injuries.

8

As members of the American Chemistry Council (ACC), Afton and Ethyl provide data on twelve metrics used to track environmental impact, safety, energy use, community outreach and emergency preparedness, greenhouse gas intensity, and product stewardship performance of the ACC member companies. These can be viewed at http://responsiblecare.americanchemistry.com/Performance-Results. The information on this website is not, and shall not be deemed to be, a part of this Annual Report on Form 10-K or incorporated by reference in this Annual Report on Form 10-K or any other filings we make with the Securities and Exchange Commission (SEC).

Environmental

We believe that we comply, in all material respects, with laws, regulations, statutes, and ordinances protecting the environment, including those related to the management and stewardship of chemicals. We have policies and procedures in place establishing regular reviews of our compliance and stewardship, as well as monitoring any significant existing, potential or threatened environmental issues that could materially affect the company.

Our total accruals for environmental remediation, dismantling, and decontamination were approximately $16 million at December 31, 2016 and $17 million December 31, 2015.

As new technology becomes available, it may be possible to reduce accrued amounts. While we believe that we are currently fully accrued for known environmental issues, it is possible that unexpected future costs could have a significant financial impact on our financial position, results of operations, and cash flows.

We spent approximately $24 million in 2016, $22 million in 2015, and $22 million in 2014 for ongoing environmental operating and clean-up costs, excluding depreciation of previously capitalized expenditures. These environmental operating and clean-up expenses are primarily included in cost of goods sold.

For capital expenditures on pollution prevention and safety projects, we spent $14 million in 2016, $13 million in 2015, and $12 million in 2014. We expect expenditures in 2017 to be at a level similar to the previous three years.

The costs of complying with governmental pollution prevention and safety regulations are subject to:

• | potential changes in applicable statutes and regulations (or their enforcement and interpretation); |

• | uncertainty as to the success of anticipated solutions to pollution problems; |

• | uncertainty as to whether additional expense may prove necessary; and |

• | potential for emerging technology to affect remediation methods and reduce associated costs. |

We are subject to liabilities associated with the investigation and cleanup of hazardous substances, as well as personal injury, property damage, or natural resource damages arising from the release of, or exposure to, such hazardous substances. Further, we may have environmental liabilities imposed in many situations without regard to violations of laws or regulations. These liabilities may also be imposed jointly and severally (so that a responsible party may be held liable for more than its share of the losses involved, or even the entire loss) and may be imposed on many different entities with a relationship to the hazardous substances at issue, including, for example, entities that formerly owned or operated the property and entities that arranged for the disposal of the hazardous substances at an affected property. We are subject to many environmental laws, including the federal Comprehensive Environmental Response, Compensation and Liability Act, commonly known as CERCLA or Superfund, in the United States, and similar foreign and state laws.

Under CERCLA, we are currently considered a potentially responsible party (PRP), at several sites, ranging from a de minimis PRP or a minor PRP, to involvement considered greater than minor PRP involvement. At some of these sites, the remediation methodology, as well as the proportionate shares of each PRP, has been well established. Other sites are not as mature, which makes it more difficult to reasonably estimate our share of the future clean-up or remediation costs.

9

In 2000, the Environmental Protection Agency (EPA) named us as a PRP under Superfund law for the clean-up of soil and groundwater contamination at the five grouped disposal sites known as "Sauget Area 2 Sites" in Sauget, Illinois. Without admitting any fact, responsibility, fault, or liability in connection with this site, we are participating with other PRPs in site investigations and feasibility studies. In December 2013, the EPA issued its Record of Decision confirming its remedies for the selected Sauget Area 2 sites. We have accrued our estimated proportional share of the remedial costs and expenses addressed in the Record of Decision. We do not believe there is any additional information available as a basis for revision of the liability that we have established at December 31, 2016. The amount accrued for this site is not material. We also have several other sites where we are in the process of environmental remediation and monitoring. See Note 16 for further information.

Geographic Areas

We have operations in the United States, Europe, Asia Pacific, India, Latin America, Canada, and the Middle East. The economies are generally stable in the countries where we do most of our business, although many of those countries have experienced economic downturns in the past. In countries with more political or economic uncertainty, we generally minimize our risk of loss by utilizing U.S. Dollar-denominated transactions, letters of credit, and prepaid transactions. Our foreign customers consist of global, national, and independent oil companies, as well as financially viable state-owned organizations.

The tables below report net sales and long-lived assets by geographic area, as well as by country for those countries with significant net sales or long-lived assets. Since our foreign operations are significant to our overall business, we are also presenting net sales in the table below by the major regions in which we operate. NewMarket assigns net sales to geographic areas based on the location to which the product was shipped to a third party. Long-lived assets in the table below include property, plant, and equipment, net of depreciation. The change in net sales during the three-year period is discussed more fully in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Net sales to one customer of our petroleum additives segment exceeded 10% of consolidated net sales in 2014. Sales to Royal Dutch Shell plc and its affiliates (Shell) amounted to $261 million (11% of consolidated net sales) in 2014. These sales represented a wide range of products sold to multiple Shell affiliates around the world. No customer exceeded 10% of net sales in 2016 or 2015.

Geographic Areas

Years Ended December 31, | ||||||||||||

(in millions) | 2016 | 2015 | 2014 | |||||||||

Net sales | ||||||||||||

United States | $ | 701 | $ | 776 | $ | 811 | ||||||

Europe, Middle East, Africa, India | 653 | 669 | 784 | |||||||||

Asia Pacific | 471 | 436 | 471 | |||||||||

Other foreign | 224 | 260 | 269 | |||||||||

Net sales | $ | 2,049 | $ | 2,141 | $ | 2,335 | ||||||

December 31, | ||||||||

(in millions) | 2016 | 2015 | ||||||

Long-lived assets | ||||||||

United States | $ | 225 | $ | 198 | ||||

Singapore | 190 | 113 | ||||||

Other foreign | 89 | 91 | ||||||

Total long-lived assets | $ | 504 | $ | 402 | ||||

10

Availability of Reports Filed with the Securities and Exchange Commission and Corporate Governance Documents

Our internet website address is www.newmarket.com. We make available, free of charge through our website, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act), as soon as reasonably practicable after such documents are electronically filed with, or furnished to, the SEC. In addition, our Corporate Governance Guidelines, Code of Conduct, and the charters of our Audit, Compensation, and Nominating and Corporate Governance Committees are available on our website and are available in print, without charge, to any shareholder upon request by contacting our Corporate Secretary at NewMarket Corporation, 330 South Fourth Street, Richmond, Virginia 23219. The information on our website is not, and shall not be deemed to be, a part of this Annual Report on Form 10-K or incorporated by reference in this Annual Report on Form 10-K or any other filings we make with the SEC.

Executive Officers of the Registrant

The names and ages of all executive officers as of February 15, 2017 follow.

Name | Age | Positions |

Thomas E. Gottwald | 56 | Chairman of the Board, President, and Chief Executive Officer (Principal Executive Officer) |

Brian D. Paliotti | 40 | Chief Financial Officer and Vice President (Principal Financial Officer) |

Bruce R. Hazelgrove, III | 56 | Executive Vice President and Chief Administrative Officer |

William J. Skrobacz | 57 | Controller (Principal Accounting Officer) |

Cameron D. Warner, Jr. | 58 | Treasurer |

M. Rudolph West | 63 | Vice President, General Counsel, and Secretary |

Robert A. Shama | 56 | President, Afton Chemical Corporation |

Our officers, at the discretion of the Board of Directors, hold office until the meeting of the Board of Directors following the next annual shareholders’ meeting. Mr. Gottwald, Mr. Hazelgrove, and Mr. Warner have served in their capacity for at least the last five years. Mr. Paliotti, Mr. West, Mr. Skrobacz, and Mr. Shama have served in their capacities for less than five years.

Mr. Paliotti has been employed by NewMarket or Afton since 2008. Prior to being named Chief Financial Officer and Vice President effective January 1, 2015, Mr. Paliotti was Vice President, Finance, of NewMarket Services since 2013, Senior Financial Officer of NewMarket Services since 2011, and Financial Officer of Afton since 2008. Mr. West was named Vice President, General Counsel, and Secretary effective January 1, 2016. Prior to that date, Mr. West served as Assistant General Counsel and Secretary for more than five years. Mr. Skrobacz joined NewMarket in May 2011 as Senior Manager, Business Assurance, and was appointed Controller Designate in September 2012. In May 2013, he was appointed Controller. Prior to joining NewMarket, Mr. Skrobacz served as Controller of UPS Freight, a wholly-owned subsidiary of United Parcel Service, Inc., since 2008. Mr. Shama has been employed by Afton for at least five years in various senior management capacities. Prior to being named President of Afton in 2013, he was Executive Vice President of Afton beginning in 2012 and Senior Vice President North America and Chief Marketing Officer in 2011. From 2008 to 2010, Mr. Shama was Vice President Sales and Marketing North America.

ITEM 1A. | RISK FACTORS |

Our business is subject to many factors that could have a material adverse effect on our future performance, results of operations, financial condition, or cash flows and could cause our actual results to differ materially from those expressed or implied by forward-looking statements made in this Annual Report on Form 10-K. Those risk factors are outlined below.

11

• | Lack of availability of raw materials, including sourcing from some single suppliers, could negatively impact our ability to meet customer demand. |

The chemical industry can experience limited supply of certain materials. In addition, in some cases, we choose to source from a single supplier. Any significant disruption in supply, for any reason, could adversely affect our ability to obtain raw materials, which in turn could adversely affect our ability to ensure continued supply for our customers and to meet customer demand.

• | A disruption in the availability or capacity of distribution systems could negatively impact our ability to meet our customers’ needs and affect our competitive position. |

We rely on a variety of modes of transportation to deliver products to our customers, including rail cars, cargo ships, and trucks. We depend upon the availability of a distribution infrastructure to deliver our products in a safe and timely manner. Any disruptions in this infrastructure network, whether caused by human error, accidents, deliberate acts of violence, limitations on capacity, repairs and improvements to infrastructure components, earthquakes, storms, or other natural disasters, could adversely affect our ability to meet customer demand.

• | A significant disruption or disaster at one of our production facilities, including those facilities which are sole producers of certain of our products, could result in our inability to meet production requirements and projected customer demand. This could potentially result in us incurring significant liabilities. |

We are dependent upon the continued safe operation of our production facilities. Several of the products we sell are produced only in one location. A prolonged disruption or disaster at one of our facilities could result in our inability to meet production requirements.

Our production facilities are subject to various hazards associated with the manufacturing, handling, storage, and transportation of chemical materials and products, some that are reactive, explosive, and flammable. Such hazards could include leaks, ruptures, chemical spills, explosions, or fires which result in the discharge or release of toxic or hazardous substances or gases; mechanical failures; unscheduled downtime; and environmental hazards. These sites may also experience significant disruptions in operations due to inclement weather, natural disasters, flooding, and levee breaches. Many of these hazards could cause a disruption in the production of our products and may diminish our ability to meet output goals. We cannot assure that our facilities will not experience these types of hazards and disruptions in the future or that these incidents will not result in production delays and affect our ability to meet production requirements. Any such disruptions or disasters at our facilities could result in us losing revenue or not being able to maintain our relationships with our customers.

Additionally, some of the hazards mentioned above could result in significant liabilities related to personal injury and loss of life; severe damage to, or destruction of, property and equipment; and environmental contamination.

• | Our research and development efforts are costly and may not succeed, which could impair our ability to meet our customers’ needs, affect our competitive position, and result in a loss of market share. |

The petroleum additives industry is subject to periodic technological change, changes in performance standards, and ongoing product improvements. Further, technological changes in some or all of our customers’ products or processes may make our products obsolete. As a result, the life cycle of our products is often hard to predict. In order to maintain our profits and remain competitive, we must effectively respond to technological changes in our industry and successfully develop, manufacture, and market new or improved products in a cost-effective and timely manner. As a result, we must commit substantial resources each year to research and development to maintain and enhance our technological capabilities and meet our customers’ changing needs. Ongoing investments in research and development for future products could result in higher costs without a proportional increase in profits. Additionally, for any new product program, there is a risk of technical or market failure in which case we may not be able to develop the new commercial products needed to maintain and enhance our competitive position, or we may need to commit additional resources to new product development programs. Moreover, new products may have lower margins than the products they replace.

12

• | Our failure to protect our intellectual property rights could harm our competitive position and could adversely affect our future performance and growth. |

Protection of our proprietary processes, methods, compounds, and other technologies is important to our business. We depend upon our ability to develop and protect our intellectual property rights to distinguish our products from those of our competitors. Failure to protect our existing intellectual property rights may result in the loss of valuable technologies or having to pay other companies for infringing on their intellectual property rights. The inability to continue using certain of our trademarks or service marks could result in the loss of brand recognition, and could require us to devote additional resources to advertise, rebrand our products, and market our brands. See Item 1, “Business-Intellectual Property.”

We rely on a combination of patent, trade secret, trademark, and copyright law, as well as judicial enforcement, to protect our intellectual property and technologies. We cannot assure that the measures taken by us to protect these assets and rights will provide meaningful protection or that adequate remedies will be available in the event of an unauthorized use or disclosure of our trade secrets or manufacturing expertise. We cannot assure that any of our intellectual property rights will not be challenged, invalidated, circumvented, or rendered unenforceable.

Furthermore, we cannot assure that any pending patent application filed by us will result in an issued patent, or if patents are issued to us, that those patents will provide meaningful protection against competitors or against competitive technologies. We could face patent infringement claims from our competitors or others alleging that our processes or products infringe on their proprietary technologies. If we were found to be infringing on the proprietary technology of others, we may be liable for damages, and we may be required to change our processes, to redesign our products partially or completely, to pay to use the technology of others, or to stop using certain technologies or producing the infringing product entirely. Even if we ultimately prevail in an infringement suit, the existence of the suit could prompt customers to switch to products that are not the subject of infringement suits. We may not prevail in any intellectual property litigation and such litigation may result in significant legal costs or otherwise impede our ability to produce and distribute key products.

We also rely on unpatented proprietary manufacturing expertise, continuing technological innovation and other trade secrets to develop and maintain our competitive position. While we generally enter into confidentiality agreements with our employees and third parties to protect our intellectual property, we cannot assure that our confidentiality agreements will not be breached, that they will provide meaningful protection for our trade secrets and proprietary manufacturing expertise, or that adequate remedies will be available in the event of an unauthorized use or disclosure of our trade secrets or manufacturing expertise.

In addition, our trade secrets and know-how may be improperly obtained by other means, such as a breach of our information technology security systems or direct theft. Any unauthorized disclosure of our material know-how or trade secrets could adversely affect our business and results of operations.

• | In order to be successful, we must attract and retain a highly qualified workforce, including key employees in leadership positions. |

The success of our business is highly dependent on our ability to attract and retain highly qualified technical personnel to support our research and development efforts and our agility in effectively responding to technological changes in our industry. To the extent that the demand for skilled personnel exceeds supply, we could experience higher labor, recruiting, or training costs in order to attract and retain such a work force. We compete with other companies, both within and outside of our industry, for qualified technical and scientific personnel such as chemical and industrial engineers. To the extent that we lose experienced personnel through wage competition, normal attrition (including retirement), or other means, we must be able to attract qualified candidates to fill those positions and successfully manage the transfer of critical knowledge from those individuals leaving our company. Our inability to maintain a highly qualified technical workforce could adversely affect our competitive position and result in a loss of market share.

We also must manage leadership development and succession planning throughout our business. To the extent that we are unable to attract, develop, and retain leadership talent successfully, we could experience business disruptions and adversely affect our ability to grow our business.

13

• | Competitive pressures could adversely affect our margins and profitability. |

We face significant competition in all of the product lines and markets in which we compete. We expect that our competitors will develop and introduce new and enhanced products, which could cause a decline in the market acceptance of certain products we manufacture. In addition, as a result of price competition, we may be compelled to reduce the prices for some of our products, which could adversely affect our margins and profitability. Some of our competitors may also have greater financial, technological, and other resources than we have and may be able to maintain greater operating and financial flexibility than we are able to maintain. As a result, these competitors may be able to better withstand changes in conditions within our industry, changes in the prices for raw materials, and changes in general economic conditions.

• | Sudden or sharp changes in the prices of and/or demand for raw materials may adversely affect our profit margins. |

We utilize a variety of raw materials in the manufacture of our products, including base oil, polyisobutylene, antioxidants, alcohols, solvents, sulfonates, friction modifiers, olefins, and copolymers. We may also enter into contracts which commit us to purchase some of our more critical raw materials based on anticipated demand. Our profitability is sensitive to changes in the quantities of raw materials we may need and the costs of those materials which may be caused by changes in supply, demand or other market conditions, over which we have little or no control. Political and economic conditions globally have caused, and may continue to cause, our demand for and the cost of our raw materials to fluctuate. War, armed hostilities, terrorist acts, civil unrest, or other incidents may also cause a sudden or sharp change in our demand for and the cost of our raw materials. We cannot assure that we will be able to pass on to our customers any future increases in raw material costs in the form of price increases for our products. If our demand for raw materials were to decline such that we would not have need for the quantities required to be purchased under commitment agreements, we could incur additional charges that would affect our profitability.

• | We rely on a small number of significant customers concentrated in the lubricant and fuel industries. The loss of sales to any of these customers could significantly reduce our revenues and negatively affect our profitability. |

Our principal customers are multinational oil companies primarily in the lubricant and fuel industries. These industries are characterized by the concentration of a few large participants. This concentration of customers affects our overall risk profile, since our customers will be similarly affected by changes in economic, geopolitical, and industry conditions. Many factors affect the level of our customers’ spending on our products, including, among others, general business conditions, changes in technology, interest rates, gasoline prices, and consumer confidence in future economic conditions. A sudden or protracted downturn in these industries could adversely affect the buying power of, and purchases by, our customers. The loss of a significant customer or a material reduction in purchases by a significant customer could reduce our revenues and negatively affect our profitability.

• | The occurrence or threat of extraordinary events, including domestic and international terrorist attacks, may disrupt our operations, decrease demand for our products, and increase our expenses. |

Chemical-related assets may be at greater risk of future terrorist attacks than other possible targets in the United States and throughout the world. Federal legislation has imposed significant site security requirements, specifically on chemical manufacturing facilities. Federal regulations have also been enacted to increase the security of the transportation of hazardous chemicals in the United States. The enactment of further federal regulations to increase the security of the transportation of hazardous chemicals in the United States could result in additional costs.

The occurrence of extraordinary events, including future terrorist attacks and the outbreak or escalation of hostilities, cannot be predicted, but their occurrence can be expected to negatively affect the economy in general, and specifically the markets for our products. The damage from a direct attack on our assets or assets used by us could include loss of life, property damage, and production downtime. In addition, available insurance coverage may not be sufficient to cover all of the damage incurred or, if available, may be prohibitively expensive.

14

• | We face risks related to our foreign operations that may negatively affect our business. |

In 2016, sales to customers outside of the United States accounted for over 65% of consolidated net sales. We do business in all major regions of the world, some of which do not have stable economies or governments. In particular, we sell and market products in countries experiencing political and/or economic instability in the Middle East, Asia Pacific, Latin America, and Europe. Our international operations are subject to international business risks, including unsettled political conditions, expropriation, import and export restrictions, trade policies, increases in royalties, exchange controls, national and regional labor strikes, taxes, government royalties, inflationary or unstable economies, currency exchange rate fluctuations, and changes in laws and policies governing operations of foreign-based companies (such as restrictions on repatriation of earnings or proceeds from liquidated assets of foreign subsidiaries). The occurrence of any one or a combination of these factors may increase our costs or have other adverse effects on our business.

In addition, the United Kingdom's June 2016 vote to withdraw from the European Union has resulted in uncertainties in connection with the United Kingdom's relationship with the European Union and how it will withdraw from the European Union. Further, there are uncertainties as to what impact the United Kingdom's withdrawal from the European Union will have on our operations in both the United Kingdom and Europe and the resulting impact on our profitability.

• | A substantial amount of indebtedness could adversely impact our business and limit our operational and financial flexibility. |

We have incurred, and may in the future incur, significant amounts of indebtedness to support our operations. Our indebtedness could, among other things, require us to dedicate a substantial portion of our cash flow to repaying our indebtedness, thus reducing the amount of funds available for other general corporate purposes; limit our ability to borrow additional funds necessary for working capital, capital expenditures or other general corporate purposes; and limit our flexibility in planning for, or reacting to, changes in our business.

Our ability to make payments on or refinance our indebtedness will depend on our ability to generate cash from operations in the future. This, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory, and other factors that are beyond our control.

We cannot guarantee that our business will generate sufficient cash flow from operations or that future borrowings will be available to us under our credit facilities in an amount sufficient to enable us to repay our debt, service our indebtedness, or to fund other liquidity needs. Furthermore, substantially all of our business is conducted through our subsidiaries, and we cannot guarantee that our subsidiaries will be able to distribute funds to us for these purposes.

We may need to refinance all or a portion of our indebtedness on or before maturity. We cannot guarantee that we will be able to refinance any of our indebtedness on commercially reasonable terms or at all.

Additionally, our debt instruments contain restrictive covenants. These covenants may constrain our activities and limit our operational and financial flexibility. The failure to comply with these covenants could result in an event of default.

• | We are exposed to fluctuations in foreign exchange rates, which may adversely affect our results of operations. |

We conduct our business in the local currency of many of the countries in which we operate. The financial condition and results of operations of our foreign operating subsidiaries are reported in the relevant local currency and then translated to U.S. Dollars at the applicable currency exchange rate for inclusion in our consolidated financial statements. Changes in exchange rates between these foreign currencies and the U.S. Dollar will affect the recorded amounts of our assets and liabilities, as well as our revenues, costs, and operating margins. The primary foreign currencies in which we have exchange rate fluctuation exposure are the European Union Euro, British Pound Sterling, Japanese Yen, Chinese Renminbi, Indian Rupee, Singapore Dollar, Mexican Peso, Australian Dollar, and Canadian Dollar. Exchange rates between these currencies and the U.S. Dollar have fluctuated significantly in recent years and may do so in the future.

15

• | An information technology system failure may adversely affect our business. |

We rely on information technology systems to transact our business. An information technology system failure due to computer viruses, internal or external security breaches, cybersecurity attacks, power interruptions, hardware failures, fire, natural disasters, human error, or other causes could disrupt our operations and prevent us from being able to process transactions with our customers, operate our manufacturing facilities, and properly report transactions in a timely manner. A significant, protracted information technology system failure may adversely affect our results of operations, financial condition, or cash flows.

• | Our business could be adversely affected by current and future governmental regulation. |

We are subject to regulation by local, state, federal, and foreign governmental authorities. In some circumstances, before we may sell certain products, these authorities must approve these products, our manufacturing processes, and our facilities. We are also subject to ongoing reviews of our products, manufacturing processes, and facilities by governmental authorities. Any delay in obtaining, or any failure to obtain or maintain, these approvals would adversely affect our ability to introduce new products and to generate sales from those products.

New laws and regulations, including climate change regulations, may be introduced in the future that could result in additional compliance costs, seizures, confiscation, recall, or monetary fines, any of which could prevent or inhibit the development, distribution, and sale of our products. If we fail to comply with applicable laws and regulations, we may be subject to civil remedies, including fines, injunctions, and recalls or seizures.

We are subject to the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act, and similar anti-bribery laws in other jurisdictions which generally prohibit companies and their intermediaries from making improper payments to foreign officials for the purposes of obtaining or retaining business. We are also subject to export and import laws and regulations which restrict trading with embargoed or sanctioned countries and certain individuals. Although we have policies and procedures designed to facilitate compliance with these laws and regulations, our employees, contractors and agents may take actions in violation of our policies. Any such violation, even if prohibited by our policies, could adversely affect our business and/or our reputation.

• | Legal proceedings and other claims could impose substantial costs on us. |

We are involved in numerous administrative and legal proceedings that result from, and are incidental to, the conduct of our business. From time to time, these proceedings involve environmental, product liability, TEL, premises asbestos liability, and other matters. See Item 3, “Legal Proceedings.” There is no assurance that our available insurance will cover these claims, that our insurers will not challenge coverage for certain claims, or that final damage awards will not exceed our available insurance coverage.

At any given time, we are involved in claims, litigation, administrative proceedings, and investigations of various types in a number of jurisdictions involving potential environmental liabilities, including clean-up costs associated with waste disposal sites, natural resource damages, property damage, and personal injury. We cannot assure that the resolution of these environmental matters will not have an adverse effect on our results of operations, financial condition, or cash flows.

• | Environmental matters could have a substantial negative impact on our business. |

As a manufacturer and distributor of chemical products, we are generally subject to extensive local, state, federal, and foreign environmental, safety, and health laws and regulations concerning, among other things, emissions to the air; discharges to land and water; the generation, handling, treatment, and disposal of hazardous waste and other materials; and remediation of contaminated soil, as well as surface and ground water. Our operations entail the risk of violations of those laws and regulations, many of which provide for substantial fines and criminal sanctions for violations. We believe that we comply in all material respects with laws, regulations, statutes, and ordinances protecting the environment, including those related to the discharge of materials. However, we cannot assure that we have been or will be at all times in compliance with all of these requirements.

16

In addition, these requirements, and the enforcement or interpretation of these requirements, may become more stringent in the future. Although we cannot predict the ultimate cost of compliance with any such requirements, the costs could be material. Noncompliance could subject us to material liabilities, such as government fines, damages arising from third-party lawsuits, or the suspension and potential cessation of noncompliant operations. We may also be required to make significant site or operational modifications at substantial cost. Future developments could also restrict or eliminate the use of or require us to make modifications to our products.

There may be environmental problems associated with our properties of which we are unaware. The discovery of environmental liabilities attached to our properties could have an adverse effect on our business even if we did not create or cause the problem.

We may also face liability arising from current or future claims alleging personal injury, product liability, or property damage due to exposure to chemicals or other hazardous substances, such as premises asbestos, at or from our facilities. We may also face liability for personal injury, product liability, property damage, natural resource damage, or clean-up costs for the alleged migration of contaminants or hazardous substances from our facilities or for future accidents or spills.

In some cases, we have been identified, and in the future may be identified, as a PRP in connection with state and federal laws regarding environmental clean-up projects. As a PRP, we may be liable for a share of the costs associated with cleaning up hazardous waste sites, such as a landfill to which we may have sent waste.

The ultimate costs and timing of environmental liabilities are difficult to predict. Liability under environmental laws relating to contaminated sites can be imposed retroactively and on a joint and several basis. A liable party could be held responsible for all costs at a site, whether currently or formerly owned or operated, regardless of fault, knowledge, timing of the contamination, cause of the contamination, percentage of contribution to the contamination, or the legality of the original disposal. We could incur significant costs, including clean-up costs, natural resource damages, civil or criminal fines and sanctions, and third-party claims, as a result of past or future violations of, or liabilities under, environmental laws.

• | The insurance we maintain may not fully cover all potential exposures. |

We maintain property, business interruption, and casualty insurance, but such insurance may not cover all risks associated with the hazards of our business and is subject to limitations, including deductibles and maximum liabilities covered. We may incur losses beyond the limits, or outside the coverage, of our insurance policies, including liabilities for environmental remediation. In the future, we may not be able to obtain coverage at current levels, and our premiums may increase significantly on coverage that we maintain.

• | We may be unable to consummate a proposed acquisition transaction due to a lack of regulatory approval or the failure of one or more parties to satisfy conditions to close. In addition, we may not be able to realize the expected benefits from future acquisitions or from investments in our infrastructure, or it may take longer to realize those benefits than originally planned. The inability to achieve our objectives related to these activities could result in unanticipated expenses and losses. |

As part of our business growth strategy, we intend to continue pursuing acquisitions and investing in our infrastructure. Our ability to implement these components of our growth strategy will be limited by our ability to identify appropriate acquisition or joint venture candidates; our ability to consummate proposed transactions due to a lack of regulatory approval or the failure of one of the parties to a transaction to satisfy conditions required for closing; and the availability of financial resources, including cash and borrowing capacity. When we acquire new businesses or invest in infrastructure improvements (for example, building new plant facilities), we consider the benefits we expect to realize and time frames over which we will realize those benefits. The expenses incurred in completing these types of activities, the time it takes to integrate the activities into our ongoing business, or our failure to realize the expected benefits from the activities in the planned time frames could result in unanticipated expenses and losses. The process of integrating acquired operations into our existing operations may result in unforeseen operating difficulties and may require significant financial resources that would otherwise be available for the ongoing development or expansion of existing operations.

17

• | We could be required to make additional contributions to our pension plans, which may be underfunded due to any underperformance of the equities markets. |

Our pension plan asset allocation is predominantly weighted towards equities. Cash contribution requirements to our pension plans are sensitive to changes in our plans’ actual return on assets. Reductions in our plans’ return on assets due to poor performance of the equities markets could cause our pension plans to be underfunded and require us to make additional cash contributions.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

ITEM 2. | PROPERTIES |

Our principal operating properties are shown below. Unless indicated, we own the research, development, and testing facilities, as well as the manufacturing and distribution properties, which primarily support the petroleum additives business segment.

Research, Development, and Testing | Richmond, Virginia Bracknell, England Manchester, England Tsukuba, Japan Ashland, Virginia Suzhou, China | |

Manufacturing and Distribution | Bedford Park, Illinois (lubricant additives) Feluy, Belgium (lubricant additives) Houston, Texas (lubricant and fuel additives; also TEL storage and distribution) Hyderabad, India (lubricant additives) Jurong Island, Singapore (lubricant additives; leased land) Manchester, England (lubricant additives) Orangeburg, South Carolina (fuel additives; manufacturing equipment only) Port Arthur, Texas (lubricant additives) Rio de Janeiro, Brazil (petroleum additives storage and distribution; leased) Sauget, Illinois (lubricant and fuel additives) Suzhou, China (lubricant additives) | |

We own our corporate headquarters located in Richmond, Virginia, and generally lease our regional and sales offices located in a number of areas worldwide.

NewMarket Development manages the property we own in Richmond, Virginia consisting of approximately 57 acres. Our corporate offices are included in this acreage, as well as a research and testing facility and several acres dedicated to other uses. We are currently exploring various development opportunities for portions of the property as the demand warrants. This effort is ongoing in nature, and we have no specific timeline for any future developments.

Production Capacity

We believe our plants and supply agreements are sufficient to meet expected sales levels. Operating rates of the plants vary with product mix and normal sales swings. We believe that our facilities are well maintained and in good operating condition.

18

ITEM 3. | LEGAL PROCEEDINGS |

We are involved in legal proceedings that are incidental to our business and may include administrative or judicial actions. Some of these legal proceedings involve governmental authorities and relate to environmental matters. For further information, see “Environmental” in Part I, Item 1.

While it is not possible to predict or determine with certainty the outcome of any legal proceeding, we believe the outcome of any of these proceedings, or all of them combined, will not result in a material adverse effect on our consolidated results of operations, financial condition, or cash flows.

In late 2013, Afton initiated a voluntary self-audit of its compliance with certain sections of the Toxic Substances Control Act (TSCA) under the EPA’s audit policy (Audit Policy). If any potential TSCA violations are discovered during the audit, we would voluntarily disclose them to the EPA under the Audit Policy. In August 2014, the EPA staff began its own TSCA inspection of both Afton and Ethyl. While it is not possible to predict or determine with certainty the outcome, we do not believe that any findings identified as a result of our audit or the EPA’s TSCA inspection will have a material adverse effect on our consolidated results of operations, financial condition, or cash flows.

ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

19

PART II

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock, with no par value, has traded on the New York Stock Exchange (NYSE) under the symbol “NEU” since June 21, 2004 when we became the parent holding company of Ethyl, Afton, NewMarket Services, NewMarket Development, and their subsidiaries. We had 2,267 shareholders of record at January 31, 2017.

On October 21, 2015, our Board of Directors approved a share repurchase program authorizing management to repurchase up to $500 million of NewMarket's outstanding common stock until December 31, 2018, as market conditions warrant and covenants under our existing agreements permit. We may conduct the share repurchases in the open market and in privately negotiated transactions. The repurchase program does not require NewMarket to acquire any specific number of shares and may be terminated or suspended at any time. Approximately $447 million remained available under the 2015 authorization at December 31, 2016. No purchases were made during the fourth quarter of 2016 under this authorization.

As shown in the table below, cash dividends declared and paid totaled $6.40 per share for the year ended December 31, 2016 and $5.80 per share for the year ended December 31, 2015.

Year | Date Declared | Date Paid | Per Share Amount | ||||

2016 | February 25, 2016 | April 1, 2016 | $ | 1.60 | |||

April 28, 2016 | July 1, 2016 | 1.60 | |||||

August 11, 2016 | October 1, 2016 | 1.60 | |||||

October 27, 2016 | January 2, 2017 | 1.60 | |||||

2015 | February 26, 2015 | April 1, 2015 | 1.40 | ||||

April 23, 2015 | July 1, 2015 | 1.40 | |||||

August 6, 2015 | October 1, 2015 | 1.40 | |||||

October 21, 2015 | January 1, 2016 | 1.60 | |||||

The declaration and payment of dividends is subject to the discretion of our Board of Directors. Future dividends will depend on various factors, including our financial condition, earnings, cash requirements, legal requirements, restrictions in agreements governing our outstanding indebtedness, and other factors deemed relevant by our Board of Directors.

The following table shows the high and low prices of our common stock on the NYSE for each of the last eight quarters.

2016 | |||||||||||||||

First Quarter | Second Quarter | Third Quarter | Fourth Quarter | ||||||||||||

High | $ | 402.82 | $ | 415.74 | $ | 447.97 | $ | 435.03 | |||||||

Low | 322.54 | 385.66 | 399.91 | 386.90 | |||||||||||

2015 | |||||||||||||||

First Quarter | Second Quarter | Third Quarter | Fourth Quarter | ||||||||||||

High | $ | 482.31 | $ | 483.25 | $ | 461.24 | $ | 419.48 | |||||||

Low | 393.25 | 443.61 | 349.35 | 348.38 | |||||||||||

20

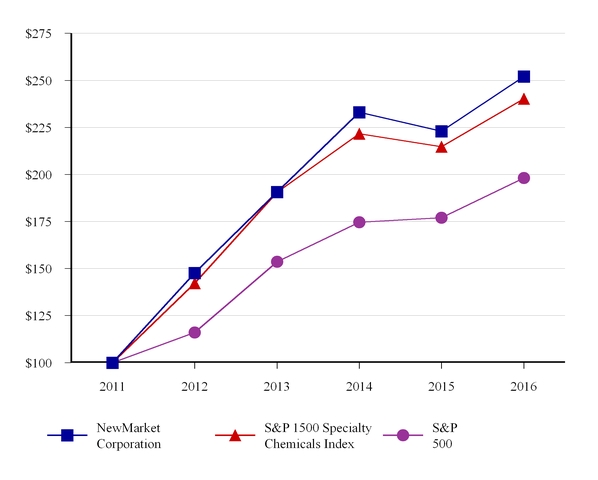

The performance graph showing the five-year cumulative total return on our common stock as compared to chemical companies in the S&P 1500 Specialty Chemicals Index and the S&P 500 is shown below. The graph assumes $100 invested on the last day of December 2011, and the reinvestment of all dividends. The graph is based on historical data, and is not intended to be a forecast or indication of future performance of our common stock.

Performance Graph

Comparison of Five-Year Cumulative Total Return

Performance Through December 31, 2016

December 31, | |||||||||||||||||||||||

2011 | 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||||

NewMarket Corporation | $ | 100.00 | $ | 147.61 | $ | 190.63 | $ | 233.02 | $ | 222.92 | $ | 252.10 | |||||||||||