Attached files

| file | filename |

|---|---|

| EX-10.1 - EXHIBIT 10.1 - Clearway Energy, Inc. | yieldincex1012016q3.htm |

| EX-32 - EXHIBIT 32 - Clearway Energy, Inc. | yieldincex322016q3.htm |

| EX-31.3 - EXHIBIT 31.3 - Clearway Energy, Inc. | yieldincex3132016q3.htm |

| EX-31.2 - EXHIBIT 31.2 - Clearway Energy, Inc. | yieldincex3122016q3.htm |

| EX-31.1 - EXHIBIT 31.1 - Clearway Energy, Inc. | yieldincex3112016q3.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x | Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

For the Quarterly Period Ended: September 30, 2016 | ||

o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

Commission File Number: 001-36002

NRG Yield, Inc.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 46-1777204 (I.R.S. Employer Identification No.) | |

804 Carnegie Center, Princeton, New Jersey (Address of principal executive offices) | 08540 (Zip Code) | |

(609) 524-4500

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o | |||

(Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

As of October 31, 2016, there were 34,586,250 shares of Class A common stock outstanding, par value $0.01 per share, 42,738,750 shares of Class B common stock outstanding, par value $0.01 per share, 62,784,250 shares of Class C common stock outstanding, par value $0.01 per share, and 42,738,750 shares of Class D common stock outstanding, par value $0.01 per share.

TABLE OF CONTENTS

Index

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This Quarterly Report on Form 10-Q of NRG Yield, Inc., together with its consolidated subsidiaries, or the Company, includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. The words "believes," "projects," "anticipates," "plans," "expects," "intends," "estimates" and similar expressions are intended to identify forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company's actual results, performance and achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. These factors, risks and uncertainties include the factors described under Item 1A — Risk Factors in Part I, Item 1A of the Company's Annual Report on Form 10-K for the year ended December 31, 2015, and the following:

• | The Company's ability to maintain and grow its quarterly dividend; |

• | The Company's ability to successfully identify, evaluate and consummate acquisitions from third parties; |

• | The Company's ability to acquire assets from NRG; |

• | The Company's ability to raise additional capital due to its indebtedness, corporate structure, market conditions or otherwise; |

• | Hazards customary to the power production industry and power generation operations such as fuel and electricity price volatility, unusual weather conditions (including wind and solar conditions), catastrophic weather-related or other damage to facilities, unscheduled generation outages, maintenance or repairs, unanticipated changes to fuel supply costs or availability due to higher demand, shortages, transportation problems or other developments, environmental incidents, or electric transmission or gas pipeline system constraints and the possibility that the Company may not have adequate insurance to cover losses as a result of such hazards; |

• | The Company's ability to operate its businesses efficiently, manage maintenance capital expenditures and costs effectively, and generate earnings and cash flows from its asset-based businesses in relation to its debt and other obligations; |

• | The willingness and ability of counterparties to the Company's offtake agreements to fulfill their obligations under such agreements; |

• | The Company's ability to enter into contracts to sell power and procure fuel on acceptable terms and prices as current offtake agreements expire; |

• | Government regulation, including compliance with regulatory requirements and changes in market rules, rates, tariffs and environmental laws; |

• | Changes in law, including judicial decisions; |

• | Operating and financial restrictions placed on the Company that are contained in the project-level debt facilities and other agreements of certain subsidiaries and project-level subsidiaries generally, in the NRG Yield Operating LLC amended and restated revolving credit facility, in the indentures governing the Senior Notes and in the indentures governing the Company's convertible notes; and |

• | The Company's ability to borrow additional funds and access capital markets, as well as the Company's substantial indebtedness and the possibility that the Company may incur additional indebtedness going forward. |

Forward-looking statements speak only as of the date they were made, and the Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The foregoing review of factors that could cause the Company's actual results to differ materially from those contemplated in any forward-looking statements included in this Quarterly Report on Form 10-Q should not be construed as exhaustive.

3

GLOSSARY OF TERMS

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

2015 Form 10-K | NRG Yield, Inc.'s Annual Report on Form 10-K for the year ended December 31, 2015 | |

2019 Convertible Notes | $345 million aggregate principal amount of 3.50% convertible notes due 2019, issued by NRG Yield, Inc. | |

2020 Convertible Notes | $287.5 million aggregate principal amount of 3.25% convertible notes due 2020, issued by NRG Yield, Inc. | |

2024 Senior Notes | $500 million aggregate principal amount of 5.375% unsecured senior notes due 2024, issued by NRG Yield Operating LLC | |

2026 Senior Notes | $350 million aggregate principal amount of 5.00% unsecured senior notes due 2026, issued by NRG Yield Operating LLC | |

2037 Notes | $200 million aggregate principal amount of 4.68% senior secured notes due 2037, issued by CVSR Holdco | |

AOCL | Accumulated Other Comprehensive Loss | |

ARO | Asset Retirement Obligation | |

ASC | The FASB Accounting Standards Codification, which the FASB established as the source of authoritative GAAP | |

ASU | Accounting Standards Updates – updates to the ASC | |

ATM Program | At-The-Market Equity Offering Program | |

Buffalo Bear | Buffalo Bear, LLC, the operating subsidiary of Tapestry Wind LLC, which owns the Buffalo Bear project | |

CAFD | Cash Available For Distribution, which the Company defines as net income before interest expense, income taxes, depreciation and amortization, plus cash distributions from unconsolidated affiliates, less cash distributions to noncontrolling interests, maintenance capital expenditures, pro-rata EBITDA from unconsolidated affiliates, cash interest paid, income taxes paid, principal amortization of indebtedness and changes in other assets | |

Company | NRG Yield, Inc. together with its consolidated subsidiaries | |

CVSR | California Valley Solar Ranch | |

CVSR Drop Down | The Company's acquisition from NRG of the remaining 51.05% interest of CVSR Holdco | |

CVSR Holdco | CVSR Holdco LLC, the indirect owner of CVSR | |

DGPV Holdco 1 | NRG DGPV Holdco 1 LLC | |

DGPV Holdco 2 | NRG DGPV Holdco 2 LLC | |

Distributed Solar | Solar power projects, typically less than 20 MW in size, that primarily sell power produced to customers for usage on site, or are interconnected to sell power into the local distribution grid | |

Drop Down Assets | Collectively, the January 2015 Drop Down Assets, November 2015 Drop Down Assets, and CVSR Drop Down | |

Economic Gross Margin | Energy and capacity revenue less cost of fuels | |

EDA | Equity Distribution Agreement | |

El Segundo | NRG West Holdings LLC, the subsidiary of Natural Gas Repowering LLC, which owns the El Segundo Energy Center project | |

ERCOT | Electric Reliability Council of Texas, the ISO and the regional reliability coordinator of the various electricity systems within Texas | |

EWG | Exempt Wholesale Generator | |

Exchange Act | The Securities Exchange Act of 1934, as amended | |

FASB | Financial Accounting Standards Board | |

FERC | Federal Energy Regulatory Commission | |

GAAP | Accounting principles generally accepted in the U.S. | |

GenConn | GenConn Energy LLC | |

HLBV | Hypothetical Liquidation at Book Value | |

IASB | International Accounting Standards Board | |

ISO | Independent System Operator, also referred to as RTO | |

4

January 2015 Drop Down Assets | The Laredo Ridge, Tapestry and Walnut Creek projects, which were acquired by NRG Yield Operating LLC from NRG on January 2, 2015 | |

Kansas South | NRG Solar Kansas South LLC, the operating subsidiary of NRG Solar Kansas South Holdings LLC, which owns the Kansas South project | |

KPPH | 1,000 Pounds Per Hour | |

Laredo Ridge | Laredo Ridge Wind, LLC, the operating subsidiary of Mission Wind Laredo, LLC, which owns the Laredo Ridge project | |

LIBOR | London Inter-Bank Offered Rate | |

Marsh Landing | NRG Marsh Landing LLC, formerly GenOn Marsh Landing LLC | |

MMBtu | Million British Thermal Units | |

MW | Megawatts | |

MWh | Saleable megawatt hours, net of internal/parasitic load megawatt-hours | |

MWt | Megawatts Thermal Equivalent | |

NERC | North American Electric Reliability Corporation | |

Net Exposure | Counterparty credit exposure to NRG Yield, Inc. net of collateral | |

NOLs | Net Operating Losses | |

November 2015 Drop Down Assets | 75% of the Class B interests of NRG Wind TE Holdco, which owns a portfolio of 12 wind facilities totaling 814 net MW, which was acquired by NRG Yield Operating LLC from NRG on November 3, 2015 | |

NRG | NRG Energy, Inc. | |

NRG Wind TE Holdco | NRG Wind TE Holdco LLC | |

NRG Yield LLC | The holding company through which the projects are owned by NRG, the holder of Class B and Class D units, and NRG Yield, Inc., the holder of the Class A and Class C units | |

NRG Yield Operating LLC | The holder of the project assets that are owned by NRG Yield LLC | |

OCI/OCL | Other comprehensive income/loss | |

Pinnacle | Pinnacle Wind, LLC, the operating subsidiary of Tapestry Wind LLC, which owns the Pinnacle project | |

PML | NRG Power Marketing LLC | |

PPA | Power Purchase Agreement | |

PUCT | Public Utility Commission of Texas | |

QF | Qualifying Facility under the Public Utility Regulatory Policies Act of 1978 | |

Recapitalization | The adoption of the Company's Second Amended and Restated Certificate of Incorporation which authorized two new classes of common stock, Class C common stock and Class D common stock, and distributed shares of such new classes of common stock to holders of the Company’s outstanding Class A common stock and Class B common stock, respectively, through a stock split on May 14, 2015 | |

RPV Holdco | NRG RPV Holdco 1 LLC | |

RTO | Regional Transmission Organization | |

SEC | U.S. Securities and Exchange Commission | |

Senior Notes | Collectively, the 2024 Senior Notes and the 2026 Senior Notes | |

September 6, 2016 Form 8-K | NRG Yield, Inc.'s Current Report on Form 8-K filed on September 6, 2016 in connection with NRG Yield, Inc.'s acquisition of the remaining 51.05% interest in CVSR from NRG | |

TA High Desert | TA-High Desert LLC, the operating subsidiary of NRG Solar Mayfair LLC, which owns the TA High Desert project | |

Taloga | Taloga Wind, LLC, the operating subsidiary of Tapestry Wind LLC, which owns the Taloga project | |

Tapestry | Collection of the Pinnacle, Buffalo Bear and Taloga projects | |

Thermal Business | The Company's thermal business, which consists of thermal infrastructure assets that provide steam, hot water and/or chilled water, and in some instances electricity, to commercial businesses, universities, hospitals and governmental units | |

UPMC | University of Pittsburgh Medical Center | |

U.S. | United States of America | |

5

Utility Scale Solar | Solar power projects, typically 20 MW or greater in size (on an alternating current, or AC, basis), that are interconnected into the transmission or distribution grid to sell power at a wholesale level | |

VaR | Value at Risk | |

VIE | Variable Interest Entity | |

Walnut Creek | NRG Walnut Creek, LLC, the operating subsidiary of WCEP Holdings, LLC, which owns the Walnut Creek project | |

6

PART I - FINANCIAL INFORMATION

ITEM 1 — FINANCIAL STATEMENTS

NRG YIELD, INC.

CONSOLIDATED STATEMENTS OF INCOME

(Unaudited)

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

(In millions, except per share amounts) | 2016 | 2015 (a) | 2016 | 2015 (a) | |||||||||||

Operating Revenues | |||||||||||||||

Total operating revenues | $ | 272 | $ | 256 | $ | 789 | $ | 729 | |||||||

Operating Costs and Expenses | |||||||||||||||

Cost of operations | 76 | 82 | 238 | 246 | |||||||||||

Depreciation and amortization | 75 | 69 | 224 | 222 | |||||||||||

General and administrative | 4 | 3 | 10 | 9 | |||||||||||

Acquisition-related transaction and integration costs | — | 1 | — | 2 | |||||||||||

Total operating costs and expenses | 155 | 155 | 472 | 479 | |||||||||||

Operating Income | 117 | 101 | 317 | 250 | |||||||||||

Other Income (Expense) | |||||||||||||||

Equity in earnings of unconsolidated affiliates | 13 | 12 | 29 | 19 | |||||||||||

Other income, net | 1 | — | 3 | 2 | |||||||||||

Loss on debt extinguishment | — | (2 | ) | — | (9 | ) | |||||||||

Interest expense | (71 | ) | (71 | ) | (213 | ) | (201 | ) | |||||||

Total other expense, net | (57 | ) | (61 | ) | (181 | ) | (189 | ) | |||||||

Income Before Income Taxes | 60 | 40 | 136 | 61 | |||||||||||

Income tax expense | 13 | 8 | 25 | 8 | |||||||||||

Net Income | 47 | 32 | 111 | 53 | |||||||||||

Less: Pre-acquisition net income (loss) of Drop Down Assets | 6 | (2 | ) | 10 | (6 | ) | |||||||||

Net Income Excluding Pre-acquisition Net Income (Loss) of Drop Down Assets | 41 | 34 | 101 | 59 | |||||||||||

Less: Net income attributable to noncontrolling interests | 8 | 17 | 31 | 37 | |||||||||||

Net Income Attributable to NRG Yield, Inc. | $ | 33 | $ | 17 | $ | 70 | $ | 22 | |||||||

Earnings Per Share Attributable to NRG Yield, Inc. Class A and Class C Common Stockholders | |||||||||||||||

Weighted average number of Class A common shares outstanding - basic | 35 | 35 | 35 | 35 | |||||||||||

Weighted average number of Class A common shares outstanding - diluted | 49 | 35 | 49 | 35 | |||||||||||

Weighted average number of Class C common shares outstanding - basic | 63 | 63 | 63 | 44 | |||||||||||

Weighted average number of Class C common shares outstanding - diluted | 73 | 63 | 63 | 44 | |||||||||||

Earnings per Weighted Average Class A and Class C Common Share - Basic | $ | 0.34 | $ | 0.18 | $ | 0.72 | $ | 0.28 | |||||||

Earnings per Weighted Average Class A Common Share - Diluted | 0.30 | 0.18 | 0.68 | 0.28 | |||||||||||

Earnings per Weighted Average Class C Common Share - Diluted | 0.32 | 0.18 | 0.72 | 0.28 | |||||||||||

Dividends Per Class A Common Share | 0.24 | 0.21 | 0.695 | 0.80 | |||||||||||

Dividends Per Class C Common Share | $ | 0.24 | $ | 0.21 | $ | 0.695 | $ | 0.41 | |||||||

(a) Retrospectively adjusted as discussed in Note 1, Nature of Business.

See accompanying notes to consolidated financial statements.

7

NRG YIELD, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited)

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

(In millions) | 2016 | 2015 (a) | 2016 | 2015 (a) | |||||||||||

Net Income | $ | 47 | $ | 32 | $ | 111 | $ | 53 | |||||||

Other Comprehensive Income (Loss), net of tax | |||||||||||||||

Unrealized gain (loss) on derivatives, net of income tax benefit of $1, $9, $13 and $13 | 21 | (31 | ) | (36 | ) | (28 | ) | ||||||||

Other comprehensive income (loss) | 21 | (31 | ) | (36 | ) | (28 | ) | ||||||||

Comprehensive Income | 68 | 1 | 75 | 25 | |||||||||||

Less: Pre-acquisition net income (loss) of Drop Down Assets | 6 | (2 | ) | 10 | (6 | ) | |||||||||

Less: Comprehensive income attributable to noncontrolling interests | 30 | 2 | 16 | 32 | |||||||||||

Comprehensive Income (Loss) Attributable to NRG Yield, Inc. | $ | 32 | $ | 1 | $ | 49 | $ | (1 | ) | ||||||

(a) Retrospectively adjusted as discussed in Note 1, Nature of Business.

See accompanying notes to consolidated financial statements.

8

NRG YIELD, INC.

CONSOLIDATED BALANCE SHEETS

(In millions, except shares) | September 30, 2016 | December 31, 2015 | |||||

ASSETS | (unaudited) | ||||||

Current Assets | |||||||

Cash and cash equivalents | $ | 200 | $ | 111 | |||

Restricted cash | 138 | 131 | |||||

Accounts receivable — trade | 115 | 101 | |||||

Accounts receivable — affiliate | 2 | — | |||||

Inventory | 37 | 36 | |||||

Derivative instruments | 1 | — | |||||

Notes receivable | 17 | 17 | |||||

Prepayments and other current assets | 21 | 20 | |||||

Total current assets | 531 | 416 | |||||

Property, plant and equipment, net | 5,711 | 5,878 | |||||

Other Assets | |||||||

Equity investments in affiliates | 690 | 697 | |||||

Notes receivable | 18 | 30 | |||||

Intangible assets, net | 1,303 | 1,362 | |||||

Deferred income taxes | 182 | 170 | |||||

Other non-current assets | 47 | 136 | |||||

Total other assets | 2,240 | 2,395 | |||||

Total Assets | $ | 8,482 | $ | 8,689 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

Current Liabilities | |||||||

Current portion of long-term debt | $ | 281 | $ | 264 | |||

Accounts payable — trade | 23 | 23 | |||||

Accounts payable — affiliate | 29 | 86 | |||||

Derivative instruments | 32 | 39 | |||||

Accrued expenses and other current liabilities | 94 | 77 | |||||

Total current liabilities | 459 | 489 | |||||

Other Liabilities | |||||||

Long-term debt | 5,359 | 5,329 | |||||

Accounts payable — affiliate | 11 | — | |||||

Derivative instruments | 107 | 61 | |||||

Other non-current liabilities | 78 | 72 | |||||

Total non-current liabilities | 5,555 | 5,462 | |||||

Total Liabilities | 6,014 | 5,951 | |||||

Commitments and Contingencies | |||||||

Stockholders' Equity | |||||||

Preferred stock, $0.01 par value; 10,000,000 shares authorized; none issued | — | — | |||||

Class A, Class B, Class C and Class D common stock, $0.01 par value; 3,000,000,000 shares authorized (Class A 500,000,000, Class B 500,000,000, Class C 1,000,000,000, Class D 1,000,000,000); 182,848,000 shares issued and outstanding (Class A 34,586,250, Class B 42,738,750, Class C 62,784,250, Class D 42,738,750) at September 30, 2016, and December 31, 2015 | 1 | 1 | |||||

Additional paid-in capital | 1,858 | 1,855 | |||||

Retained earnings | 35 | 12 | |||||

Accumulated other comprehensive loss | (48 | ) | (27 | ) | |||

Noncontrolling interest | 622 | 897 | |||||

Total Stockholders' Equity | 2,468 | 2,738 | |||||

Total Liabilities and Stockholders' Equity | $ | 8,482 | $ | 8,689 | |||

See accompanying notes to consolidated financial statements.

9

NRG YIELD, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

Nine months ended September 30, | |||||||

2016 | 2015 (a) | ||||||

(In millions) | |||||||

Cash Flows from Operating Activities | |||||||

Net income | $ | 111 | $ | 53 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Equity in earnings of unconsolidated affiliates | (29 | ) | (19 | ) | |||

Distributions from unconsolidated affiliates | 39 | 40 | |||||

Depreciation, amortization and ARO accretion | 226 | 224 | |||||

Amortization of financing costs and debt discounts | 15 | 13 | |||||

Amortization of intangibles and out-of-market contracts | 57 | 41 | |||||

Adjustment for debt extinguishment | — | 9 | |||||

Changes in income taxes | 25 | 8 | |||||

Changes in derivative instruments | (5 | ) | (38 | ) | |||

Disposal of asset components | 5 | 2 | |||||

Changes in prepaid and accrued capacity payments | 2 | (1 | ) | ||||

Changes in other working capital | (7 | ) | (22 | ) | |||

Net Cash Provided by Operating Activities | 439 | 310 | |||||

Cash Flows from Investing Activities | |||||||

Acquisition of businesses, net of cash acquired | — | (37 | ) | ||||

Acquisition of Drop Down Assets, net of cash acquired | (77 | ) | (489 | ) | |||

Capital expenditures | (16 | ) | (17 | ) | |||

Increase in restricted cash | (7 | ) | (24 | ) | |||

Decrease in notes receivable | 11 | 13 | |||||

Proceeds from renewable energy grants | — | 22 | |||||

Return of investment from unconsolidated affiliates | 16 | 16 | |||||

Investments in unconsolidated affiliates | (69 | ) | (351 | ) | |||

Net Cash Used in Investing Activities | (142 | ) | (867 | ) | |||

Cash Flows from Financing Activities | |||||||

Net contributions from noncontrolling interests | 7 | 123 | |||||

Distributions to NRG for CVSR and NRG Wind TE Holdco | (122 | ) | (52 | ) | |||

Proceeds from the issuance of common stock | — | 599 | |||||

Payment of dividends and distributions to shareholders | (127 | ) | (99 | ) | |||

Payment of debt issuance costs | (6 | ) | (13 | ) | |||

Net (payments for) borrowings from the revolving credit facility | (306 | ) | 92 | ||||

Proceeds from the issuance of long-term debt | 550 | 292 | |||||

Payments for long-term debt | (204 | ) | (669 | ) | |||

Net Cash (Used in) Provided by Financing Activities | (208 | ) | 273 | ||||

Net Increase (Decrease) in Cash and Cash Equivalents | 89 | (284 | ) | ||||

Cash and Cash Equivalents at Beginning of Period | 111 | 429 | |||||

Cash and Cash Equivalents at End of Period | $ | 200 | $ | 145 | |||

(a) Retrospectively adjusted as discussed in Note 1, Nature of Business.

See accompanying notes to consolidated financial statements.

10

NRG YIELD, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Note 1 — Nature of Business

NRG Yield, Inc., together with its consolidated subsidiaries, or the Company, is a dividend growth-oriented company formed by NRG as a Delaware corporation on December 20, 2012, to serve as the primary vehicle through which NRG owns, operates and acquires contracted renewable and conventional generation and thermal infrastructure assets. NRG Yield, Inc. owns 100% of the Class A units and Class C units of NRG Yield LLC, including a controlling interest through its position as managing member. NRG Yield LLC, through its wholly owned subsidiary, NRG Yield Operating LLC, is the holder of a portfolio of renewable and conventional generation and thermal infrastructure assets, primarily located in the Northeast, Southwest and California regions of the U.S.

NRG Yield, Inc. consolidates the results of NRG Yield LLC through its controlling interest, with NRG's interest shown as noncontrolling interest in the financial statements. On May 14, 2015, NRG Yield, Inc. completed a stock split whereby each outstanding share of Class A common stock was split into one share of Class A common stock and one share of Class C common stock, and each outstanding share of Class B common stock was split into one share of Class B common stock and one share of Class D common stock. The stock split is referred to as the Recapitalization and all references to share or per share amounts in the accompanying consolidated financial statements and applicable disclosures have been retrospectively adjusted to reflect the Recapitalization. In addition, on June 29, 2015, NRG Yield, Inc. completed the issuance of 28,198,000 shares of Class C common stock for net proceeds of $599 million. The holders of NRG Yield, Inc.'s outstanding shares of Class A and Class C common stock are entitled to dividends as declared. NRG receives its distributions from NRG Yield LLC through its ownership of NRG Yield LLC Class B and Class D units.

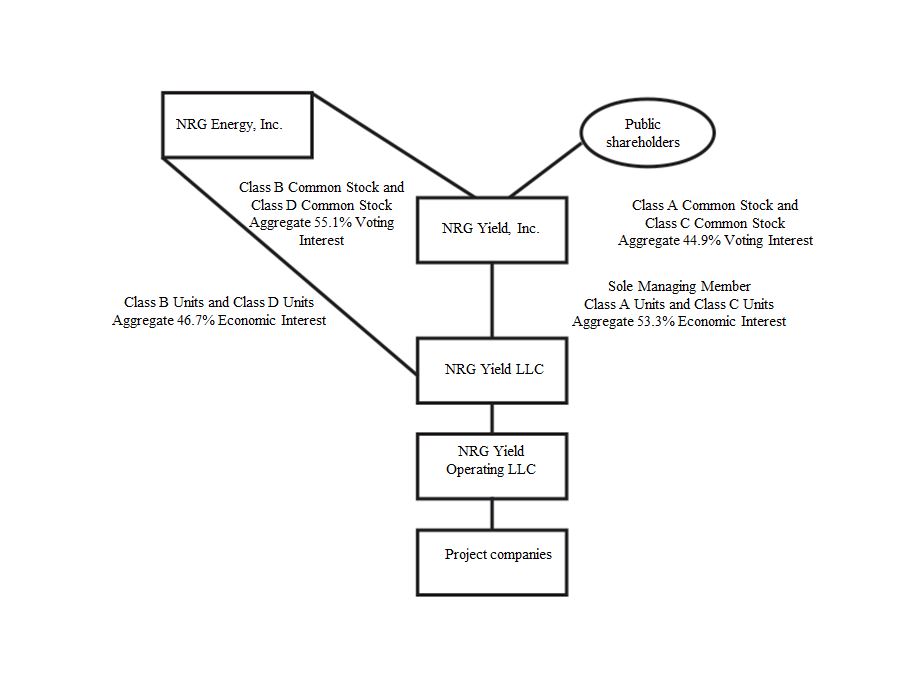

The following table represents the structure of the Company as of September 30, 2016:

11

As of September 30, 2016, the Company's operating assets are comprised of the following projects:

Projects | Percentage Ownership | Net Capacity (MW)(a) | Offtake Counterparty | Expiration | ||||||

Conventional | ||||||||||

El Segundo | 100 | % | 550 | Southern California Edison | 2023 | |||||

GenConn Devon | 50 | % | 95 | Connecticut Light & Power | 2040 | |||||

GenConn Middletown | 50 | % | 95 | Connecticut Light & Power | 2041 | |||||

Marsh Landing | 100 | % | 720 | Pacific Gas and Electric | 2023 | |||||

Walnut Creek | 100 | % | 485 | Southern California Edison | 2023 | |||||

1,945 | ||||||||||

Utility Scale Solar | ||||||||||

Alpine | 100 | % | 66 | Pacific Gas and Electric | 2033 | |||||

Avenal | 50 | % | 23 | Pacific Gas and Electric | 2031 | |||||

Avra Valley | 100 | % | 26 | Tucson Electric Power | 2032 | |||||

Blythe | 100 | % | 21 | Southern California Edison | 2029 | |||||

Borrego | 100 | % | 26 | San Diego Gas and Electric | 2038 | |||||

CVSR | 100 | % | 250 | Pacific Gas and Electric | 2038 | |||||

Desert Sunlight 250 | 25 | % | 63 | Southern California Edison | 2035 | |||||

Desert Sunlight 300 | 25 | % | 75 | Pacific Gas and Electric | 2040 | |||||

Kansas South | 100 | % | 20 | Pacific Gas and Electric | 2033 | |||||

Roadrunner | 100 | % | 20 | El Paso Electric | 2031 | |||||

TA High Desert | 100 | % | 20 | Southern California Edison | 2033 | |||||

610 | ||||||||||

Distributed Solar | ||||||||||

AZ DG Solar Projects | 100 | % | 5 | Various | 2025 - 2033 | |||||

PFMG DG Solar Projects | 51 | % | 4 | Various | 2032 | |||||

9 | ||||||||||

Wind | ||||||||||

Alta I | 100 | % | 150 | Southern California Edison | 2035 | |||||

Alta II | 100 | % | 150 | Southern California Edison | 2035 | |||||

Alta III | 100 | % | 150 | Southern California Edison | 2035 | |||||

Alta IV | 100 | % | 102 | Southern California Edison | 2035 | |||||

Alta V | 100 | % | 168 | Southern California Edison | 2035 | |||||

Alta X (b) | 100 | % | 137 | Southern California Edison | 2038 | |||||

Alta XI (b) | 100 | % | 90 | Southern California Edison | 2038 | |||||

Buffalo Bear | 100 | % | 19 | Western Farmers Electric Co-operative | 2033 | |||||

Crosswinds | 74.3 | % | 16 | Corn Belt Power Cooperative | 2027 | |||||

Elbow Creek | 75 | % | 92 | NRG Power Marketing LLC | 2022 | |||||

Elkhorn Ridge | 50.3 | % | 41 | Nebraska Public Power District | 2029 | |||||

Forward | 75 | % | 22 | Constellation NewEnergy, Inc. | 2017 | |||||

Goat Wind | 74.9 | % | 113 | Dow Pipeline Company | 2025 | |||||

Hardin | 74.3 | % | 11 | Interstate Power and Light Company | 2027 | |||||

Laredo Ridge | 100 | % | 80 | Nebraska Public Power District | 2031 | |||||

Lookout | 75 | % | 29 | Southern Maryland Electric Cooperative | 2030 | |||||

Odin | 74.9 | % | 15 | Missouri River Energy Services | 2028 | |||||

Pinnacle | 100 | % | 55 | Maryland Department of General Services and University System of Maryland | 2031 | |||||

San Juan Mesa | 56.3 | % | 68 | Southwestern Public Service Company | 2025 | |||||

Sleeping Bear | 75 | % | 71 | Public Service Company of Oklahoma | 2032 | |||||

South Trent | 100 | % | 101 | AEP Energy Partners | 2029 | |||||

Spanish Fork | 75 | % | 14 | PacifiCorp | 2028 | |||||

Spring Canyon II (b) | 90.1 | % | 29 | Platte River Power Authority | 2039 | |||||

Spring Canyon III (b) | 90.1 | % | 25 | Platte River Power Authority | 2039 | |||||

Taloga | 100 | % | 130 | Oklahoma Gas & Electric | 2031 | |||||

Wildorado | 74.9 | % | 121 | Southwestern Public Service Company | 2027 | |||||

1,999 | ||||||||||

12

Projects | Percentage Ownership | Net Capacity (MW)(a) | Offtake Counterparty | Expiration | ||||||

Thermal | ||||||||||

Thermal equivalent MWt (c) | 100 | % | 1,315 | Various | Various | |||||

NRG Dover Energy Center LLC | 100 | % | 103 | NRG Power Marketing LLC | 2018 | |||||

Thermal generation | 100 | % | 20 | Various | Various | |||||

1,438 | ||||||||||

Total net capacity (excluding equivalent MWt)(d) | 4,686 | |||||||||

(a) Net capacity represents the maximum, or rated, generating capacity of the facility multiplied by the Company's percentage ownership in the facility as of September 30, 2016.

(b) Projects are part of tax equity arrangements.

(c) For thermal energy, net capacity represents MWt for steam or chilled water and excludes 134 MWt available under the right-to-use provisions contained in agreements between two of the Company's thermal facilities and certain of its customers.

(d) Total net capacity excludes 43 MW for RPV Holdco and 52 MW for DGPV Holdco 1 and DGPV Holdco 2 projects, of which the Company's net interests are 41 MW and 49, respectively, based on cash to be distributed. These projects are part of tax equity arrangements and are consolidated by NRG, as further described in Note 4, Variable Interest Entities, or VIEs.

Substantially all of the Company's generation assets are under long-term contractual arrangements for the output or capacity from these assets. The thermal assets are comprised of district energy systems and combined heat and power plants that produce steam, hot water and/or chilled water and in some instances, electricity, at a central plant. Three out of the fourteen district energy systems are subject to rate regulation by state public utility commissions while the other district energy systems have rates determined by negotiated bilateral contracts.

As described in Note 11, Related Party Transactions, the Company has a management services agreement with NRG for various services, including human resources, accounting, tax, legal, information systems, treasury, and risk management.

Stockholders' equity represents the equity associated with the Class A and Class C common stockholders, the equity associated with the Class B and Class D common stockholder, NRG, and the third-party interests under certain tax equity arrangements classified as noncontrolling interest.

As described in Note 3, Business Acquisitions, on September 1, 2016, the Company acquired the remaining 51.05% of CVSR, or the CVSR Drop Down, from NRG for cash consideration of $78.5 million plus an immaterial working capital adjustment. Prior to the transaction, the Company recorded its 48.95% interest in CVSR as an equity method investment. The acquisition of the CVSR Drop Down was accounted for as a transfer of entities under common control. The accounting guidance requires retrospective combination of the entities for all periods presented as if the combination has been in effect from the beginning of the financial statement period or from the date the entities were under common control (if later than the beginning of the financial statement period). Accordingly, in connection with the retrospective adjustment of prior periods, the Company removed the equity method investment from all prior periods and adjusted its financial statements to reflect its results of operations, financial position and cash flows as if it had consolidated CVSR from the beginning of the financial statement period.

Previously, on November 3, 2015, the Company acquired 75% of the Class B interests of NRG Wind TE Holdco, or the November 2015 Drop Down Assets, from NRG for cash consideration of $209 million. In February 2016, NRG made a final working capital payment of $2 million, reducing total cash consideration to $207 million. The Company has recorded all minority interests in NRG Wind TE Holdco as noncontrolling interest in the consolidated financial statements for all periods presented. On January 2, 2015, the Company acquired the Laredo Ridge, Tapestry, and Walnut Creek projects, or the January 2015 Drop Down Assets, for total cash consideration of $489 million, including $9 million for working capital.

The recast for the above transactions, referred to as Drop Down Assets, did not affect net income attributable to NRG Yield, Inc., weighted average number of shares outstanding, earnings per share or dividends.

The accompanying unaudited interim consolidated financial statements have been prepared in accordance with the SEC’s regulations for interim financial information and with the instructions to Form 10-Q. Accordingly, they do not include all of the information and notes required by GAAP for complete financial statements. The following notes should be read in conjunction with the accounting policies and other disclosures as set forth in the notes to the consolidated financial statements for the year ended December 31, 2015 included in the Company's September 6, 2016 Form 8-K. Interim results are not necessarily indicative of results for a full year.

13

In the opinion of management, the accompanying unaudited interim consolidated financial statements contain all material adjustments consisting of normal and recurring accruals necessary to present fairly the Company's consolidated financial position as of September 30, 2016, and the results of operations, comprehensive income (loss) and cash flows for the three and nine months ended September 30, 2016 and 2015.

Note 2 — Summary of Significant Accounting Policies

Use of Estimates

The preparation of consolidated financial statements in accordance with GAAP requires management to make estimates and assumptions. These estimates and assumptions impact the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities as of the date of the consolidated financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could be different from these estimates.

Accumulated Depreciation, Accumulated Amortization

The following table presents the accumulated depreciation included in the property, plant and equipment, net, and accumulated amortization included in intangible assets, net, respectively, as of September 30, 2016 and December 31, 2015:

September 30, 2016 | December 31, 2015 | ||||||

(In millions) | |||||||

Property, Plant and Equipment Accumulated Depreciation | $ | 1,002 | $ | 782 | |||

Intangible Assets Accumulated Amortization | 151 | 93 | |||||

Noncontrolling Interests

The following table reflects the changes in the Company's noncontrolling interest balance:

(In millions) | |||

Balance as of December 31, 2015 | $ | 897 | |

Capital contributions from tax equity investors, net of distributions | 7 | ||

November 2015 Drop Down Assets working capital payment | 2 | ||

Payment for CVSR Drop Down | (79 | ) | |

Pre-acquisition net income of Drop Down Assets | 10 | ||

Comprehensive income | 16 | ||

Distributions to NRG for Drop Down Assets | (172 | ) | |

Yield LLC distributions to NRG | (59 | ) | |

Balance as of September 30, 2016 | $ | 622 | |

Distributions to NRG for Drop Down Assets

Distributions to NRG for Drop Down Assets relate to NRG's 25% interest in the November 2015 Drop Down Assets as well as NRG's 51.05% interest in CVSR prior to its acquisition by the Company. This amount includes cash and non-cash distributions and includes portion of the proceeds from the senior notes issued under the CVSR Holdco Financing Arrangement on July 15, 2016, as described in Note 7, Long-term Debt.

14

Yield LLC Distributions to NRG

The following table lists the distributions paid on NRG Yield LLC's Class B and D units during the nine months ended September 30, 2016:

Third Quarter 2016 | Second Quarter 2016 | First Quarter 2016 | ||||||||

Distributions per Class B Unit | 0.24 | $ | 0.23 | $ | 0.225 | |||||

Distributions per Class D Unit | 0.24 | $ | 0.23 | $ | 0.225 | |||||

On November 2, 2016, NRG Yield LLC declared a distribution on its units of $0.25 per unit payable on December 15, 2016 to unit holders of record as of December 1, 2016.

Reclassifications

Certain prior-year amounts have been reclassified for comparative purposes.

Recent Accounting Developments

ASU 2016-16 - In October 2016, the FASB issued ASU No. 2016-16, Income Taxes (Topic 740), Intra-Entity Transfers of Assets Other Than Inventory, or ASU No. 2016-16. The amendments of ASU No. 2016-16 were issued to improve the accounting for the income tax consequences of intra-entity transfers of assets other than inventory. Current GAAP prohibits the recognition of current and deferred income taxes for an intra-entity asset transfer until the asset has been sold to an outside party which has resulted in diversity in practice and increased complexity within financial reporting. The amendments of ASU No. 2016-16 would require an entity to recognize the income tax consequences of an intra-entity transfer of an asset other than inventory when the transfer occurs and do not require new disclosure requirements. The amendments of ASU No. 2016-16 are effective for annual reporting periods beginning after December 15, 2017, and interim periods within those annual periods. Early adoption is permitted and the adoption of ASU No. 2016-16 should be applied on a modified retrospective basis through a cumulative-effect adjustment directly to retained earnings as of the beginning of the period of adoption. The Company is currently evaluating the impact of the standard on the Company’s results of operations, cash flows and financial position.

ASU 2016-15 — In August 2016, the FASB issued ASU No. 2016-15, Statement of Cash Flows (Topic 230), Classification of Certain Cash Receipts and Cash Payments, or ASU No. 2016-15. The amendments of ASU No. 2016-15 were issued to address eight specific cash flow issues for which stakeholders have indicated to the FASB that a diversity in practice existed in how entities were presenting and classifying these items in the statement of cash flows. The issues addressed by ASU No. 2016-15 include but are not limited to the classification of debt prepayment and debt extinguishment costs, payments made for contingent consideration for a business combination, proceeds from the settlement of insurance proceeds, distributions received from equity method investees and separately identifiable cash flows and the application of the predominance principle. The amendments of ASU No. 2016-15 are effective for public entities for fiscal years beginning after December 15, 2017 and interim periods in those fiscal years. Early adoption is permitted, including adoption in an interim fiscal period with all amendments adopted in the same period. The adoption of ASU No. 2016-15 is required to be applied retrospectively. The Company is currently evaluating the impact of the standard on the Company's statement of cash flows.

ASU 2016-07 — In March 2016, the FASB issued ASU No. 2016-07, Investments - Equity Method and Joint Ventures (Topic 323), or ASU No. 2016-07. The amendments of ASU No. 2016-07 eliminate the requirement that when an investment qualifies for use of the equity method as a result of an increase in the level of ownership interest or degree of influence, an investor must adjust the investment, results of operations, and retained earnings retroactively on a step-by-step basis as if the equity method had been in effect during all previous periods that the investment had been held. The amendments require that the equity method investor add the cost of acquiring the additional interest in the investee to the current basis of the investor's previously held interest and adopt the equity method of accounting with no retroactive adjustment to the investment. In addition, ASU No. 2016-07 requires that an entity that has an available-for-sale equity security that becomes qualified for the equity method of accounting recognize through earnings the unrealized holding gain or loss in accumulated other comprehensive income at the date the investment becomes qualified for use of the equity method. The guidance in ASU No. 2016-07 is effective for fiscal years beginning after December 15, 2016, and interim periods within those annual periods. The adoption of ASU No. 2016-07 is required to be applied prospectively and early adoption is permitted. The Company does not expect the standard to have a material impact on its results of operations, cash flows and financial position.

15

ASU 2016-02 — In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842), or ASU No. 2016-02. The amendments of ASU No. 2016-02 complete the joint effort between the FASB and the International Accounting Standards Board, or IASB, to develop a common leasing standard for GAAP and International Financial Reporting Standards, or IFRS, with the objective to increase transparency and comparability among organizations by recognizing lease assets and lease liabilities on the balance sheet and to improve financial reporting. The guidance in ASU No. 2016-02 provides that a lessee that may have previously accounted for a lease as an operating lease under current GAAP should recognize the assets and liabilities that arise from a lease on the balance sheet. In addition, ASU No. 2016-02 expands the required quantitative and qualitative disclosures with regards to lease arrangements. The guidance in ASU No. 2016-02 is effective for fiscal years beginning after December 15, 2018, and interim periods within those annual periods. The adoption of ASU No. 2016-02 is required to be applied using a modified retrospective approach for the earliest period presented and early adoption is permitted. The Company is currently working through an adoption plan which includes the evaluation of lease contracts compared to the new standard and evaluating the impact of ASU No.2016-02 on the Company's results of operations, cash flows and financial position.

ASU 2016-01 — In January 2016, the FASB issued ASU No. 2016-01, Financial Instruments - Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities, or ASU No. 2016-01. The amendments of ASU No. 2016-01 eliminate available-for-sale classification of equity investments and require that equity investments (except those accounted for under the equity method of accounting, or those that result in consolidation of the investee) to be generally measured at fair value with changes in fair value recognized in net income. Further, the amendments require financial assets and financial liabilities to be presented separately in the notes to the financial statements, grouped by measurement category and form of financial asset. The guidance in ASU No. 2016-01 is effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within those annual periods. The Company is currently evaluating the impact of the standard on the Company's results of operations, cash flows and financial position.

ASU 2015-16 — In September 2015, the FASB issued ASU No. 2015-16, Business Combinations (Topic 805): Simplifying the Accounting for Measurement-Period Adjustments, or ASU No. 2015-16. The amendments of ASU No. 2015-16 require that an acquirer recognize measurement period adjustments to the provisional amounts recognized in a business combination in the reporting period during which the adjustments are determined. Additionally, the amendments of ASU No. 2015-16 require the acquirer to record in the same period's financial statements the effect on earnings of changes in depreciation, amortization or other income effects, if any, as a result of the measurement period adjustment, calculated as if the accounting had been completed at the acquisition date as well as disclosing on either the face of the income statement or in the notes the portion of the amount recorded in current period earnings that would have been recorded in previous reporting periods. The guidance in ASU No. 2015-16 is effective for financial statements issued for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. The amendments should be applied prospectively. The Company adopted this standard on January 1, 2016, and the adoption of this standard did not impact the Company's results of operations, cash flows or financial position.

ASU 2014-09 — In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606), or ASU No. 2014-09. The amendments of ASU No. 2014-09 complete the joint effort between the FASB and the IASB, to develop a common revenue standard for GAAP and IFRS, and to improve financial reporting. In addition to ASU No. 2014-09, the FASB has issued additional guidance which provides further clarification on Topic 606 including ASU No. 2016-08, ASU No. 2016-10, ASU No. 2016-12. The guidance under Topic 606 provides that an entity should recognize revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled to in exchange for the goods or services provided and establishes a four step process to be applied by an entity in evaluating its contracts with customers. In August 2015, the FASB issued ASU No. 2015-14, which formally deferred the effective date by one year to make the guidance of ASU No. 2014-09 effective for annual reporting periods beginning after December 15, 2017, including interim periods therein. Early adoption is permitted, but not prior to the original effective date, which was for annual reporting periods beginning after December 15, 2016. The Company is working through an adoption plan which includes the evaluation of revenue contracts compared to the new standard and evaluating the impact of Topic 606 on the Company' results of operations, cash flows and financial position.

Note 3 — Business Acquisitions

2016 Acquisitions

CVSR Drop Down— Prior to September 1, 2016, the Company had a 48.95% interest in CVSR, which was accounted for as an equity method investment. On September 1, 2016, the Company acquired from NRG the remaining 51.05% interest of CVSR Holdco LLC, which indirectly owns the CVSR solar facility, for total cash consideration of $78.5 million plus an immaterial working capital adjustment. The Company also assumed additional debt of $496 million, which represents 51.05% of the CVSR project level debt and 51.05% of the notes issued under the CVSR Holdco Financing Agreement, as further described in Note 7, Long-term Debt, as of the closing date. The acquisition was funded with cash on hand.

16

The assets and liabilities transferred to the Company relate to interests under common control by NRG and were recorded at historical cost in accordance with ASC 805-50, Business Combinations - Related Issues. The difference between the cash paid and historical value of the entities' equity was recorded as a distribution to NRG with the offset to noncontrolling interest. Because the transaction constituted a transfer of net assets under common control, the guidance requires retrospective combination of the entities for all periods presented as if the combination has been in effect since the inception of common control. In connection with the retrospective adjustment of prior periods, the Company has removed the equity method investment from all prior periods and adjusted its financial statements to reflect its results of operations, financial position and cash flows as if it had consolidated CVSR from the beginning of the financial statement period. As of June 30, 2016, the Company's recast consolidated balance sheet included a net receivable of $67 million related to current litigation with SunPower pursuant to indemnities in the project. The agreement between NRG and the Company for the CVSR Drop Down acquisition specified that all amounts related to the litigation with SunPower were excluded from the acquisition. Accordingly, prior to close of the transaction, the net receivable was transferred to NRG as a net reduction to its ownership interest in CVSR.

The following is the summary of historical net liabilities assumed in connection with the CVSR Drop Down as of September 1, 2016:

CVSR | |||

(In millions) | |||

Current assets | $ | 95 | |

Property, plant and equipment | 826 | ||

Non-current assets | 13 | ||

Total assets | 934 | ||

Debt (a) | 966 | ||

Other current and non-current liabilities | 12 | ||

Total liabilities | 978 | ||

Net liabilities assumed | (44 | ) | |

Accumulated Other Comprehensive Loss | (25 | ) | |

Historical Net Liabilities Assumed | $ | (19 | ) |

(a) Net of deferred financing costs of $5 million.

Since the acquisition date, CVSR has contributed $9 million in operating revenues and $4 million in net income to the Company.

2015 Acquisitions

November 2015 Drop Down Assets from NRG — On November 3, 2015, the Company acquired the November 2015 Drop Down Assets, a portfolio of 12 wind facilities totaling 814 net MW, from NRG for cash consideration of $209 million, subject to working capital adjustments. In February 2016, NRG made a final working capital payment of $2 million, reducing total cash consideration to $207 million. The Company is responsible for its pro-rata share of non-recourse project debt of $193 million and noncontrolling interest associated with a tax equity structure of $159 million (as of the acquisition date).

The Company funded the acquisition with borrowings from its revolving credit facility. The assets and liabilities transferred to the Company relate to interests under common control by NRG and were recorded at historical cost. The difference between the cash paid and historical value of the entities' equity was recorded as a distribution from NRG with the offset to noncontrolling interest.

The Class A interests of NRG Wind TE Holdco are owned by a tax equity investor, or TE Investor, who receives 99% of allocations of taxable income and other items until the flip point, which occurs when the TE Investor obtains a specified return on its initial investment, at which time the allocations to the TE Investor change to 8.53%. The Company generally receives 75% of CAFD until the flip point, at which time the allocations to the Company of CAFD change to 68.60%. If the flip point has not occurred by a specified date, 100% of CAFD is allocated to the TE Investor until the flip point occurs. NRG Wind TE Holdco is a VIE and the Company is the primary beneficiary, through its position as managing member, and consolidates NRG Wind TE Holdco.

17

Desert Sunlight — On June 29, 2015, the Company acquired 25% of the membership interest in Desert Sunlight Investment Holdings, LLC, which owns two solar photovoltaic facilities that total 550 MW, located in Desert Center, California from EFS Desert Sun, LLC, an affiliate of GE Energy Financial Services for a purchase price of $285 million. Power generated by the facilities is sold to Southern California Edison and Pacific Gas and Electric under long-term PPAs with approximately 20 years and 25 years of remaining contract life, respectively. The Company accounts for its 25% investment as an equity method investment.

Spring Canyon — On May 7, 2015, the Company acquired a 90.1% interest in Spring Canyon II, a 32 MW wind facility, and Spring Canyon III, a 28 MW wind facility, each located in Logan County, Colorado, from Invenergy Wind Global LLC. The purchase price was funded with cash on hand. Power generated by Spring Canyon II and Spring Canyon III is sold to Platte River Power Authority under long-term PPAs with approximately 24 years of remaining contract life.

University of Bridgeport Fuel Cell — On April 30, 2015, the Company completed the acquisition of the University of Bridgeport Fuel Cell project in Bridgeport, Connecticut from FuelCell Energy, Inc. The project added an additional 1.4 MW of thermal capacity to the Company's portfolio, with a 12-year contract, with the option for a 7-year extension. The acquisition is reflected in the Company's Thermal segment.

January 2015 Drop Down Assets from NRG — On January 2, 2015, the Company acquired the following projects from NRG: (i) Laredo Ridge, an 80 MW wind facility located in Petersburg, Nebraska, (ii) Tapestry, which includes Buffalo Bear, a 19 MW wind facility in Buffalo, Oklahoma; Taloga, a 130 MW wind facility in Putnam, Oklahoma; and Pinnacle, a 55 MW wind facility in Keyser, West Virginia, and (iii) Walnut Creek, a 485 MW natural gas facility located in City of Industry, California, for total cash consideration of $489 million, including $9 million for working capital, plus assumed project-level debt of $737 million. The Company funded the acquisition with cash on hand and drawings under its revolving credit facility. The assets and liabilities transferred to the Company relate to interests under common control by NRG and were recorded at historical cost. The difference between the cash paid and the historical value of the entities' equity of $61 million, as well as $23 million of AOCL, was recorded as a distribution to NRG and reduced the balance of its noncontrolling interest.

Note 4 — Variable Interest Entities, or VIEs

Entities that are Consolidated

The Company has a controlling financial interest in certain entities which have been identified as VIEs under ASC 810, Consolidations, or ASC 810. These arrangements are primarily related to tax equity arrangements entered into with third parties in order to monetize certain tax credits associated with wind facilities, as further described in Note 5, Investments Accounted for by the Equity Method and Variable Interest Entities, to the Company's consolidated financial statements included in the Company's September 6, 2016 Form 8-K.

Summarized financial information for the Company's consolidated VIEs consisted of the following as of September 30, 2016:

(In millions) | NRG Wind TE Holdco | Alta Wind TE Holdco | Spring Canyon | ||||||||

Other current and non-current assets | $ | 189 | $ | 19 | $ | 4 | |||||

Property, plant and equipment | 635 | 466 | 101 | ||||||||

Intangible assets | 2 | 278 | — | ||||||||

Total assets | 826 | 763 | 105 | ||||||||

Current and non-current liabilities | 225 | 9 | 6 | ||||||||

Total liabilities | 225 | 9 | 6 | ||||||||

Noncontrolling interest | 209 | 118 | 69 | ||||||||

Net assets less noncontrolling interests | $ | 392 | $ | 636 | $ | 30 | |||||

18

Entities that are not Consolidated

The Company has interests in entities that are considered VIEs under ASC 810, but for which it is not considered the primary beneficiary. The Company accounts for its interests in these entities under the equity method of accounting, as further described in Note 5, Investments Accounted for by the Equity Method and Variable Interest Entities, to the Company's consolidated financial statements included in the Company's September 6, 2016 Form 8-K.

NRG DGPV Holdco 1 LLC — The Company and NRG maintain a partnership, NRG DGPV Holdco 1 LLC, or DGPV Holdco 1, the purpose of which is to own or purchase solar power generation projects and other ancillary related assets from NRG Renew LLC or its subsidiaries via intermediate funds, including: (i) a tax equity-financed portfolio of 10 recently completed community solar projects representing approximately 8 MW with a weighted average remaining PPA term of 20 years; and (ii) a tax equity-financed portfolio of approximately 12 commercial photovoltaic systems representing approximately 37 MW with a weighted average remaining PPA term of 19 years. Both of these investments relate to the Company's $100 million commitment to distributed solar projects in partnership with NRG.

NRG DGPV Holdco 2 LLC — On February 29, 2016, the Company and NRG entered into an additional partnership by forming NRG DGPV Holdco 2 LLC, or DGPV Holdco 2, to own or purchase solar power generation projects representing approximately 7 MW with a weighted average remaining PPA term of 18 years as well as other ancillary related assets from NRG Renew LLC or its subsidiaries, via intermediate funds. Under this partnership, the Company committed to fund up to $50 million of capital.

The Company's maximum exposure to loss is limited to its equity investment in DGPV Holdco 1 and DGPV Holdco 2, which was $77 million on a combined basis as of September 30, 2016.

NRG RPV Holdco 1 LLC — The Company and NRG Residential Solar Solutions LLC, a subsidiary of NRG, maintain a partnership, NRG RPV Holdco 1 LLC, or RPV Holdco, that holds operating portfolios of residential solar assets developed by NRG's residential solar business, including: (i) an existing, unlevered portfolio of over 2,000 leases across nine states representing approximately 15 MW with a weighted average remaining lease term of approximately 17 years that was acquired outside of the partnership; and (ii) a tax equity-financed portfolio of approximately 5,400 leases representing approximately 28 MW, with an average lease term for the existing and new leases of approximately 17 to 20 years. In addition to the acquisition of the unlevered portfolio of leases, the Company had previously committed to fund up to $150 million of capital to invest in the tax equity financed portfolio, which was reduced to $100 million in February 2016. On August 5, 2016, the Company and NRG amended the RPV Holdco partnership to further reduce that capital commitment of $100 million to $60 million in connection with NRG’s change in business model approach in the residential solar business. As of September 30, 2016, the Company had contributed $57 million of this amount.

The Company's maximum exposure to loss is limited to its equity investment, which was $70 million as of September 30, 2016.

GenConn Energy LLC — The Company has a 50% interest in GCE Holding LLC, the owner of GenConn, which owns and operates two 190 MW peaking generation facilities in Connecticut at the Devon and Middletown sites. As of September 30, 2016, the Company's investment in GenConn was $106 million and its maximum exposure to loss is limited to its equity investment.

The following table presents summarized financial information for GCE Holding LLC:

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

(In millions) | 2016 | 2015 | 2016 | 2015 | |||||||||||

Income Statement Data: | |||||||||||||||

Operating revenues | $ | 18 | $ | 21 | $ | 54 | $ | 61 | |||||||

Operating income | 9 | 9 | 28 | 29 | |||||||||||

Net income | $ | 7 | $ | 6 | $ | 20 | $ | 20 | |||||||

September 30, 2016 | December 31, 2015 | ||||||

Balance Sheet Data: | (In millions) | ||||||

Current assets | $ | 29 | $ | 36 | |||

Non-current assets | 403 | 416 | |||||

Current liabilities | 12 | 16 | |||||

Non-current liabilities | $ | 208 | $ | 215 | |||

19

Note 5 — Fair Value of Financial Instruments

Fair Value Accounting under ASC 820

ASC 820 establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value into three levels as follows:

• | Level 1—quoted prices (unadjusted) in active markets for identical assets or liabilities that the Company has the ability to access as of the measurement date. |

• | Level 2—inputs other than quoted prices included within Level 1 that are directly observable for the asset or liability or indirectly observable through corroboration with observable market data. |

• | Level 3—unobservable inputs for the asset or liability only used when there is little, if any, market activity for the asset or liability at the measurement date. |

In accordance with ASC 820, the Company determines the level in the fair value hierarchy within which each fair value measurement in its entirety falls, based on the lowest level input that is significant to the fair value measurement.

For cash and cash equivalents, restricted cash, accounts receivable, accounts receivable — affiliate, accounts payable, accounts payable — affiliate, accrued expenses and other liabilities, the carrying amounts approximate fair value because of the short-term maturity of those instruments and are classified as Level 1 within the fair value hierarchy.

The estimated carrying amounts and fair values of the Company’s recorded financial instruments not carried at fair market value are as follows:

As of September 30, 2016 | As of December 31, 2015 | ||||||||||||||

Carrying Amount | Fair Value | Carrying Amount | Fair Value | ||||||||||||

(In millions) | |||||||||||||||

Assets: | |||||||||||||||

Notes receivable, including current portion | $ | 35 | $ | 35 | $ | 47 | $ | 47 | |||||||

Liabilities: | |||||||||||||||

Long-term debt, including current portion | $ | 5,704 | $ | 5,729 | $ | 5,656 | $ | 5,538 | |||||||

20

The fair value of the Company's publicly-traded long-term debt is based on quoted market prices and is classified as Level 2 within the fair value hierarchy. The fair value of debt securities, non-publicly traded long-term debt and certain notes receivable of the Company are based on expected future cash flows discounted at market interest rates, or current interest rates for similar instruments with equivalent credit quality and are classified as Level 3 within the fair value hierarchy. The following table presents the level within the fair value hierarchy for long-term debt, including current portion as of September 30, 2016 and December 31, 2015:

As of September 30, 2016 | As of December 31, 2015 | ||||||||||||||

Level 2 | Level 3 | Level 2 | Level 3 | ||||||||||||

(In millions) | |||||||||||||||

Long-term debt, including current portion | $ | 1,478 | $ | 4,251 | $ | 978 | $ | 4,560 | |||||||

Recurring Fair Value Measurements

The Company records its derivative assets and liabilities at fair value on its consolidated balance sheet. There were no derivative asset positions on the Company's consolidated balance sheet as of December 31, 2015. The following table presents assets and liabilities measured and recorded at fair value on the Company's consolidated balance sheets on a recurring basis and their level within the fair value hierarchy:

As of September 30, 2016 | As of December 31, 2015 | ||||||

Fair Value (a) | Fair Value (a) | ||||||

(In millions) | Level 2 | Level 2 | |||||

Derivative assets: | |||||||

Commodity contracts | $ | 1 | $ | — | |||

Total assets | 1 | — | |||||

Derivative liabilities: | |||||||

Commodity contracts | 1 | 2 | |||||

Interest rate contracts | 138 | 98 | |||||

Total liabilities | $ | 139 | $ | 100 | |||

(a) There were no derivative assets or liabilities classified as Level 1 or Level 3 as of September 30, 2016, and December 31, 2015.

Derivative Fair Value Measurements

The Company's contracts are non-exchange-traded and valued using prices provided by external sources. For the Company’s energy markets, management receives quotes from multiple sources. To the extent that multiple quotes are received, the prices reflect the average of the bid-ask mid-point prices obtained from all sources believed to provide the most liquid market for the commodity.

The fair value of each contract is discounted using a risk free interest rate. In addition, a credit reserve is applied to reflect credit risk, which is, for interest rate swaps, calculated based on credit default swaps using the bilateral method. For commodities, to the extent that the net exposure under a specific master agreement is an asset, the Company uses the counterparty’s default swap rate. If the net exposure under a specific master agreement is a liability, the Company uses NRG's default swap rate. For interest rate swaps and commodities, the credit reserve is added to the discounted fair value to reflect the exit price that a market participant would be willing to receive to assume the liabilities or that a market participant would be willing to pay for the assets. As of September 30, 2016, the credit reserve resulted in a $4 million increase in fair value, which was composed of a $3 million gain in OCI and $1 million reduction in interest expense. It is possible that future market prices could vary from those used in recording assets and liabilities and such variations could be material.

21

Concentration of Credit Risk

In addition to the credit risk discussion in Note 2, Summary of Significant Accounting Policies, to the Company's consolidated financial statements included in the Company's September 6, 2016 Form 8-K, the following is a discussion of the concentration of credit risk for the Company's financial instruments. Credit risk relates to the risk of loss resulting from non-performance or non-payment by counterparties pursuant to the terms of their contractual obligations. The Company monitors and manages credit risk through credit policies that include: (i) an established credit approval process; (ii) daily monitoring of counterparties' credit limits; (iii) the use of credit mitigation measures such as margin, collateral, prepayment arrangements, or volumetric limits; (iv) the use of payment netting agreements; and (v) the use of master netting agreements that allow for the netting of positive and negative exposures of various contracts associated with a single counterparty. Risks surrounding counterparty performance and credit could ultimately impact the amount and timing of expected cash flows. The Company seeks to mitigate counterparty risk by having a diversified portfolio of counterparties.

Counterparty credit exposure includes credit risk exposure under certain long-term agreements, including solar and other PPAs. As external sources or observable market quotes are not available to estimate such exposure, the Company estimates the exposure related to these contracts based on various techniques including, but not limited to, internal models based on a fundamental analysis of the market and extrapolation of observable market data with similar characteristics. Based on these valuation techniques, as of September 30, 2016, credit risk exposure to these counterparties attributable to the Company's ownership interests was approximately $2.6 billion for the next five years. The majority of these power contracts are with utilities with strong credit quality and public utility commission or other regulatory support, as further described in Note 12, Segment Reporting, to the Company's consolidated financial statements included in the Company's September 6, 2016 Form 8-K. However, such regulated utility counterparties can be impacted by changes in government regulations, which the Company is unable to predict.

Note 6 — Accounting for Derivative Instruments and Hedging Activities

This footnote should be read in conjunction with the complete description under Note 7, Accounting for Derivative Instruments and Hedging Activities, to the Company's consolidated financial statements included in the Company's September 6, 2016 Form 8-K.

Energy-Related Commodities

As of September 30, 2016, the Company had forward contracts for the purchase of fuel commodities relating to the forecasted usage of the Company’s district energy centers extending through 2018. At September 30, 2016, these contracts were not designated as cash flow or fair value hedges.

Interest Rate Swaps

As of September 30, 2016, the Company had interest rate derivative instruments on non-recourse debt extending through 2031, most of which are designated as cash flow hedges.

Volumetric Underlying Derivative Transactions

The following table summarizes the net notional volume buy/(sell) of the Company's open derivative transactions broken out by commodity:

Total Volume | |||||||||

September 30, 2016 | December 31, 2015 | ||||||||

Commodity | Units | (In millions) | |||||||

Natural Gas | MMBtu | 3 | 4 | ||||||

Interest | Dollars | $ | 1,875 | $ | 1,991 | ||||

22

Fair Value of Derivative Instruments

There were no derivative asset positions on the balance sheet as of December 31, 2015. The following table summarizes the fair value within the derivative instrument valuation on the balance sheet:

Fair Value | |||||||||||

Derivative Assets | Derivative Liabilities | ||||||||||

September 30, 2016 | September 30, 2016 | December 31, 2015 | |||||||||

(In millions) | |||||||||||

Derivatives Designated as Cash Flow Hedges: | |||||||||||

Interest rate contracts current | $ | — | $ | 29 | $ | 34 | |||||

Interest rate contracts long-term | — | 94 | 56 | ||||||||

Total Derivatives Designated as Cash Flow Hedges | — | 123 | 90 | ||||||||

Derivatives Not Designated as Cash Flow Hedges: | |||||||||||

Interest rate contracts current | — | 2 | 3 | ||||||||

Interest rate contracts long-term | — | 13 | 5 | ||||||||

Commodity contracts current | 1 | 1 | 2 | ||||||||

Total Derivatives Not Designated as Cash Flow Hedges | 1 | 16 | 10 | ||||||||

Total Derivatives | $ | 1 | $ | 139 | $ | 100 | |||||

The Company has elected to present derivative assets and liabilities on the balance sheet on a trade-by-trade basis and does not offset amounts at the counterparty master agreement level. As of September 30, 2016 and December 31, 2015, there were no offsetting amounts at the counterparty master agreement level or outstanding collateral paid or received.

Accumulated Other Comprehensive Loss

The following table summarizes the effects on the Company’s accumulated OCL balance attributable to interest rate swaps designated as cash flow hedge derivatives, net of tax:

Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2016 | 2015 (a) | 2016 | 2015 (a) | ||||||||||||

(In millions) | |||||||||||||||

Accumulated OCL beginning balance | $ | (140 | ) | $ | (73 | ) | $ | (83 | ) | $ | (76 | ) | |||

Reclassified from accumulated OCL to income due to realization of previously deferred amounts | 4 | 5 | 10 | 12 | |||||||||||

Mark-to-market of cash flow hedge accounting contracts | 17 | (36 | ) | (46 | ) | (40 | ) | ||||||||

Accumulated OCL ending balance, net of income tax benefit of $29 and $19, respectively | (119 | ) | (104 | ) | (119 | ) | (104 | ) | |||||||

Accumulated OCL attributable to noncontrolling interests | (71 | ) | (72 | ) | (71 | ) | (72 | ) | |||||||

Accumulated OCL attributable to NRG Yield, Inc. | $ | (48 | ) | $ | (32 | ) | $ | (48 | ) | $ | (32 | ) | |||

Losses expected to be realized from OCL during the next 12 months, net of income tax benefit of $4 | $ | 16 | $ | 16 | |||||||||||

(a) Retrospectively adjusted as discussed in Note 1, Nature of Business.

Amounts reclassified from accumulated OCL into income and amounts recognized in income from the ineffective portion of cash flow hedges are recorded to interest expense. There was no ineffectiveness for the three and nine months ended September 30, 2016 and 2015.

Impact of Derivative Instruments on the Statements of Income

The Company has interest rate derivative instruments that are not designated as cash flow hedges. The effect of interest rate hedges is recorded to interest expense. For the three months ended September 30, 2016, and 2015, the impact to the consolidated statements of income was a gain of $2 million and a loss of $6 million, respectively. For the nine months ended September 30, 2016, and 2015, the impact to the consolidated statements of income was a loss of $7 million and a gain of $13 million, respectively.

23

A portion of the Company’s derivative commodity contracts relates to its Thermal Business for the purchase of fuel commodities based on the forecasted usage of the thermal district energy centers. Realized gains and losses on these contracts are reflected in the fuel costs that are permitted to be billed to customers through the related customer contracts or tariffs and, accordingly, no gains or losses are reflected in the consolidated statements of income for these contracts.

In 2015, certain NRG subsidiaries entered into commodity contracts with NRG Power Marketing and NRG Texas Power LLC. The purpose of these commodity contracts was to hedge the forecasted sale of power for Elbow Creek, Goat Wind, Alta X and Alta XI until the start of the PPAs. The effect of these commodity hedges was recorded to operating revenues, as described in Note 11, Related Party Transactions. For the three and nine months ended September 30, 2015, the impact to the consolidated statements of income was an unrealized loss of $2 million and an unrealized gain of $1 million, respectively.

See Note 5, Fair Value of Financial Instruments, for a discussion regarding concentration of credit risk.

24

Note 7 — Long-term Debt

This footnote should be read in conjunction with the complete description under Note 9, Long-term Debt, to the Company's consolidated financial statements included in the Company's September 6, 2016 Form 8-K. Long-term debt consisted of the following:

September 30, 2016 | December 31, 2015 | September 30, 2016, interest rate % (a) | Letters of Credit Outstanding at September 30, 2016 | |||||||||||

(In millions, except rates) | ||||||||||||||

2019 Convertible Notes (b) | $ | 334 | $ | 330 | 3.500 | |||||||||

2020 Convertible Notes (c) | 270 | 266 | 3.250 | |||||||||||

2024 Senior Notes | 500 | 500 | 5.375 | |||||||||||

2026 Senior Notes | 350 | — | 5.000 | |||||||||||

NRG Yield LLC and NRG Yield Operating LLC Revolving Credit Facility, due 2019 (d) | — | 306 | L+2.75 | $ | 64 | |||||||||

Project-level debt: | ||||||||||||||

Alpine, due 2022 | 147 | 154 | L+1.75 | 37 | ||||||||||

Alta Wind I, lease financing arrangement, due 2034 | 245 | 252 | 7.015 | 16 | ||||||||||

Alta Wind II, lease financing arrangement, due 2034 | 194 | 198 | 5.696 | 23 | ||||||||||

Alta Wind III, lease financing arrangement, due 2034 | 201 | 206 | 6.067 | 23 | ||||||||||

Alta Wind IV, lease financing arrangement, due 2034 | 130 | 133 | 5.938 | 16 | ||||||||||

Alta Wind V, lease financing arrangement, due 2035 | 208 | 213 | 6.071 | 26 | ||||||||||

Alta Realty Investments, due 2031 | 32 | 33 | 7.000 | — | ||||||||||

Alta Wind Asset Management, due 2031 | 18 | 19 | L+2.375 | — | ||||||||||

Avra Valley, due 2031 | 57 | 60 | L+1.75 | 3 | ||||||||||

Blythe, due 2028 | 20 | 21 | L+1.625 | 6 | ||||||||||

Borrego, due 2025 and 2038 | 70 | 72 | L+ 2.50/5.65 | 5 | ||||||||||

CVSR, due 2037 | 771 | 793 | 2.339 - 3.775 | — | ||||||||||

CVSR Holdco, due 2037 | 199 | — | 4.68 | 13 | ||||||||||

El Segundo Energy Center, due 2023 | 443 | 485 | L+1.625 - L+2.25 | 82 | ||||||||||

Energy Center Minneapolis, due 2017 and 2025 | 98 | 108 | 5.95 -7.25 | — | ||||||||||

Kansas South, due 2031 | 31 | 33 | L+2.00 | 4 | ||||||||||

Laredo Ridge, due 2028 | 101 | 104 | L+1.875 | 10 | ||||||||||

Marsh Landing, due 2017 and 2023 | 385 | 418 | L+1.75 - L+1.875 | 33 | ||||||||||

PFMG and related subsidiaries financing agreement, due 2030 | 28 | 29 | 6.000 | — | ||||||||||

Roadrunner, due 2031 | 37 | 40 | L+1.625 | 5 | ||||||||||

South Trent Wind, due 2020 | 58 | 62 | L+1.625 | 10 | ||||||||||

TA High Desert, due 2020 and 2032 | 51 | 52 | L+2.50/5.15 | 8 | ||||||||||

Tapestry, due 2021 | 175 | 181 | L+1.625 | 20 | ||||||||||

Viento, due 2023 | 183 | 189 | L+2.75 | 27 | ||||||||||

Walnut Creek, due 2023 | 322 | 351 | L+1.625 | 49 | ||||||||||

WCEP Holdings, due 2023 | 46 | 46 | L+3.00 | — | ||||||||||

Other | — | 2 | various | — | ||||||||||

Subtotal project-level debt: | 4,250 | 4,254 | ||||||||||||

Total debt | 5,704 | 5,656 | ||||||||||||

Less current maturities | 281 | 264 | ||||||||||||

Less deferred financing costs | 64 | 63 | ||||||||||||

Total long-term debt | $ | 5,359 | $ | 5,329 | ||||||||||