Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - MEDICAL PROPERTIES TRUST INC | d286459dex991.htm |

| 8-K - FORM 8-K - MEDICAL PROPERTIES TRUST INC | d286459d8k.htm |

Exhibit 99.2

Medical Properties Trust

THIRD QUARTER 2016

Supplemental Information

MEDICALPROPERTIESTRUST.COM

TABLE OF CONTENTS

COMPANY OVERVIEW

Company Information 3

FINANCIAL INFORMATION

Reconciliation of Net Income to Funds from Operations 5

Debt Summary 6

Debt Maturity Schedule 7

Pro Forma Net Debt /Annualized EBITDA 8

PORTFOLIO INFORMATION

Lease and Mortgage Loan Maturity Schedule 9

Investments and Revenue by Asset Type, Operator,

State and Country 10

EBITDAR to Rent Coverage 13

Summary of Acquisitions and

Development Projects 14

FINANCIAL STATEMENTS

Consolidated Statements of

Income 15

Consolidated Balance Sheets 16

Other Income Generating Assets 17

FORWARD-LOOKING STATEMENT Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results of the

Company or future events to differ materially from those expressed in or underlying such forward-looking statements, including without limitation: Normalized FFO per share; expected payout ratio, the amount of acquisitions of healthcare real estate,

if any; estimated debt metrics, portfolio diversification, capital markets conditions, the repayment of debt arrangements; statements concerning the additional income to the Company as a result of ownership interests in certain hospital operations

and the timing of such income; the payment of future dividends, if any; completion of additional debt arrangement, and additional investments; national and international economic, business, real estate and other market conditions; the competitive

environment in which the Company operates; the execution of the Company’s business plan; financing risks; the Company’s ability to maintain its status as a REIT for income tax purposes; acquisition and development risks; potential

environmental and other liabilities; and other factors affecting the real estate industry generally or healthcare real estate in particular. For further discussion of the factors that could affect outcomes, please refer to the “Risk

Factors” section of the Company’s Annual Report on Form 10-K for the year ended December 31, 2015, and as updated by the Company’s subsequently filed Quarterly Reports on Form 10-Q and other SEC filings. Except as otherwise required

by the federal securities laws, the Company undertakes no obligation to update the information in this report.

On the Cover and Above: Saint Elizabeth’s

Medical Center (Steward Health Care) - Brighton, Massachusetts. Acquired in 2016.

Q3 2016 | SUPPLEMENTAL INFORMATION 2

MEDICALPROPERTIESTRUST.COM

COMPANY OVERVIEW

MPT

Medical Properties Trust, Inc. is a Birmingham, Alabama based

self-advised real estate investment trust formed to capitalize on the changing trends in healthcare delivery by acquiring and developing net-leased healthcare facilities. MPT’s financing model allows hospitals and other healthcare facilities to

unlock the value of their underlying real estate in order to fund facility improvements, technology upgrades, staff additions and new construction. Facilities include acute care hospitals, inpatient rehabilitation hospitals, long-term acute care

hospitals, and other medical and surgical facilities.

OFFICERS

Edward K.

Aldag, Jr. Chairman, President and Chief Executive Officer

R. Steven Hamner Executive Vice President and Chief Financial Officer

Emmett E. McLean Executive Vice President, Chief Operating Officer, Treasurer and Secretary

J.

Kevin Hanna Vice President, Controller and Chief Accounting Officer

BOARD OF DIRECTORS

Edward K. Aldag, Jr.

G. Steven Dawson

R. Steven Hamner

Robert. E. Holmes, Ph.D.

Sherry A. Kellett

William G. McKenzie

D. Paul Sparks, Jr.

Michael G. Stewart

C. Reynolds Thompson, III

CORPORATE HEADQUARTERS

Medical Properties Trust, Inc.

1000 Urban Center Drive, Suite 501

Birmingham, AL 35242

(205) 969-3755

(205) 969-3756 (fax)

www.medicalpropertiestrust.com

MPT Medical Properties

MPT Officers, from left: J. Kevin Hanna, Emmett E. McLean, Edward K.

Aldag, Jr., and R. Steven Hamner.

Q3 2016 | SUPPLEMENTAL INFORMATION 3

MEDICALPROPERTIESTRUST.COM

COMPANY

OVERVIEW(continued)

INVESTOR RELATIONS MPW CAPITAL MARKETS

Tim Berryman

LISTED Director - Investor Relations

Charles Lambert Managing Director - Capital Markets (205) 397-8897

(205) 397-8589

tberryman@medicalpropertiestrust.com

NYSE clambert@medicalpropertiestrust.com

TRANSFER AGENT

American Stock Transfer and Trust Company 6201 15th Avenue Brooklyn, NY 11219

STOCK EXCHANGE

LISTING AND TRADING SYMBOL

New York Stock Exchange (NYSE): MPW

SENIOR

UNSECURED

DEBT RATINGS

Moody’s – Ba1 Standard & Poor’s

– BBB-

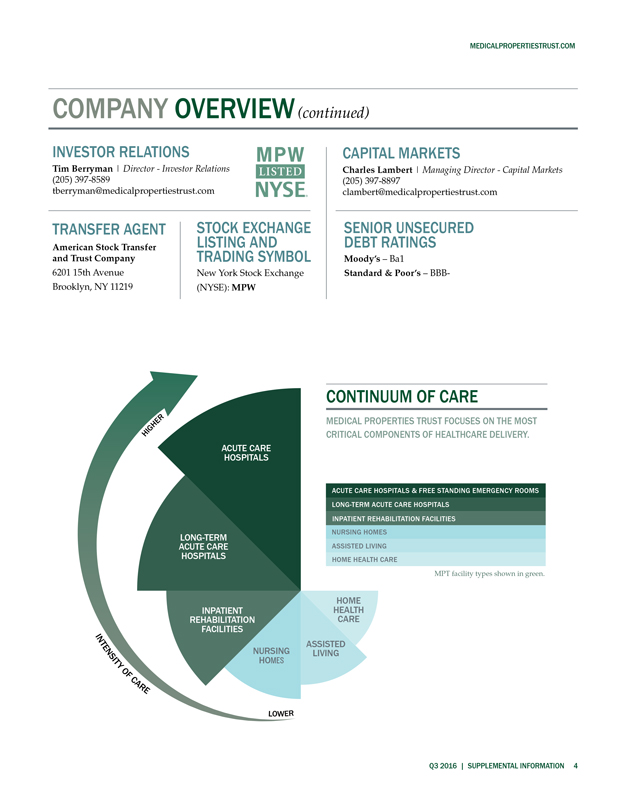

HIGHER

INTENSITY OF CARE

LOWER

ACUTE CARE HOSPITALS

LONG- TERM ACUTE CARE HOSPITALS

INPATIENT REHABILITATION FACILITIES

NURSING HOMES

ASSISTED LIVING

HOME HEALTH CARE

CONTINUUM OF CARE

MEDICAL PROPERTIES TRUST FOCUSES ON THE MOST CRITICAL COMPONENTS OF HEALTHCARE DELIVERY.

ACUTE CARE HOSPITALS & FREE STANDING EMERGENCY ROOMS

LONG-TERM ACUTE CARE

HOSPITALS

INPATIENT REHABILITATION FACILITIES

NURSING HOMES

ASSISTED LIVING

HOME HEALTH CARE

MPT facility types shown in green.

Q3 2016 | SUPPLEMENTAL INFORMATION 4

MEDICALPROPERTIESTRUST.COM

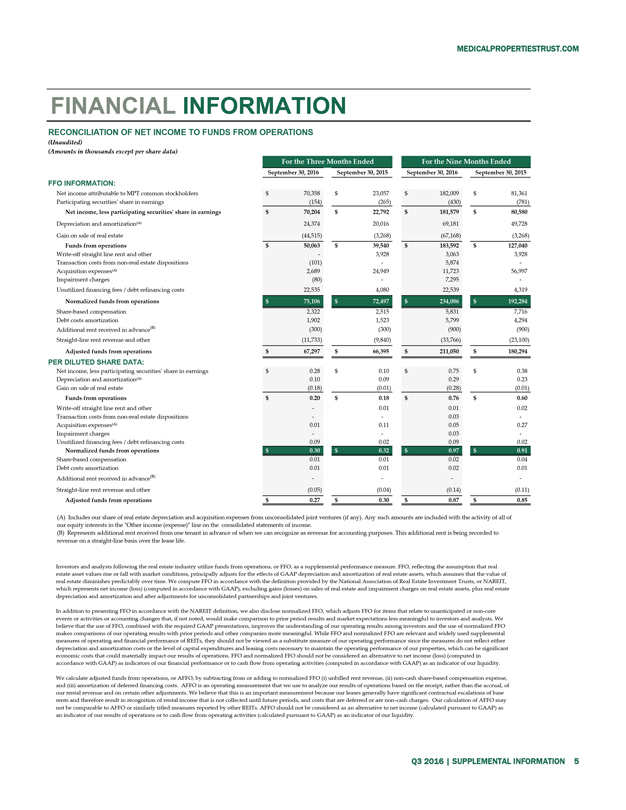

FINANCIAL

INFORMATION

RECONCILIATION OF NET INCOME TO FUNDS FROM OPERATIONS

(Unaudited)

(Amounts in thousands except per share data)

For the Three Months Ended For

the Nine Months Ended

September 30, 2016 September 30, 2015 September 30, 2016 September 30, 2015

FFO INFORMATION:

Net income attributable to MPT common stockholders $70,358 $23,057 $182,009

$81,361

Participating securities’ share in earnings (154) (265) (430) (781)

Net income, less participating securities’ share in earnings $70,204 $22,792 $181,579 $80,580

Depreciation and amortization(A) 24,374 20,016 69,181 49,728

Gain on sale of real estate

(44,515) (3,268) (67,168) (3,268)

Funds from operations $50,063 $39,540 $183,592 $127,040

Write-off straight line rent and other - 3,928 3,063 3,928

Transaction costs from non-real

estate dispositions (101) - 5,874 -

Acquisition expenses(A) 2,689 24,949 11,723 56,997

Impairment charges (80) - 7,295 -

Unutilized financing fees / debt refinancing costs 22,535

4,080 22,539 4,319

Normalized funds from operations $75,106 $72,497 $234,086 $192,284

Share-based compensation 2,322 2,515 5,831 7,716

Debt costs amortization 1,902 1,523 5,799

4,294

Additional rent received in advance(B) (300) (300) (900) (900)

Straight-line rent revenue and other (11,733) (9,840) (33,766) (23,100)

Adjusted funds from operations $67,297 $66,395 $211,050 $180,294

PER DILUTED

SHARE DATA:

Net income, less participating securities’ share in earnings $0.28 $0.10 $0.75 $0.38

Depreciation and amortization(A) 0.10 0.09 0.29 0.23

Gain on sale of real estate (0.18) (0.01)

(0.28) (0.01)

Funds from operations $0.20 $0.18 $0.76 $0.60

Write-off

straight line rent and other - 0.01 0.01 0.02

Transaction costs from non-real estate dispositions - - 0.03 -

Acquisition expenses(A) 0.01 0.11 0.05 0.27

Impairment charges - - 0.03 -

Unutilized financing fees / debt refinancing costs 0.09 0.02 0.09 0.02

Normalized funds from

operations $0.30 $0.32 $0.97 $0.91

Share-based compensation 0.01 0.01 0.02 0.04

Debt costs amortization 0.01 0.01 0.02 0.01

Additional rent received in

advance(B) - - - -

Straight-line rent revenue and other (0.05) (0.04) (0.14) (0.11)

Adjusted funds from operations $0.27 $0.30 $0.87 $0.85

(A) Includes our share of real

estate depreciation and acquisition expenses from unconsolidated joint ventures (if any). Any such amounts are included with the activity of all of our equity interests in the “Other income (expense)” line on the consolidated

statements of income.

(B) Represents additional rent received from one tenant in advance of when we can recognize as revenue for accounting purposes. This

additional rent is being recorded to revenue on a straight-line basis over the lease life.

Investors and analysts following the real estate industry utilize funds

from operations, or FFO, as a supplemental performance measure. FFO, reflecting the assumption that real estate asset values rise or fall with market conditions, principally adjusts for the effects of GAAP depreciation and amortization of real

estate assets, which assumes that the value of real estate diminishes predictably over time. We compute FFO in accordance with the definition provided by the National Association of Real Estate Investment Trusts, or NAREIT, which represents net

income (loss) (computed in accordance with GAAP), excluding gains (losses) on sales of real estate and impairment charges on real estate assets, plus real estate depreciation and amortization and after adjustments for unconsolidated partnerships and

joint ventures.

In addition to presenting FFO in accordance with the NAREIT definition, we also disclose normalized FFO, which adjusts FFO for items that relate to

unanticipated or non-core events or activities or accounting changes that, if not noted, would make comparison to prior period results and market expectations less meaningful to investors and analysts. We believe that the use of FFO, combined with

the required GAAP presentations, improves the understanding of our operating results among investors and the use of normalized FFO makes comparisons of our operating results with prior periods and other companies more meaningful. While FFO and

normalized FFO are relevant and widely used supplemental measures of operating and financial performance of REITs, they should not be viewed as a substitute measure of our operating performance since the measures do not reflect either depreciation

and amortization costs or the level of capital expenditures and leasing costs necessary to maintain the operating performance of our properties, which can be significant economic costs that could materially impact our results of operations. FFO and

normalized FFO should not be considered an alternative to net income (loss) (computed in accordance with GAAP) as indicators of our financial performance or to cash flow from operating activities (computed in accordance with GAAP) as an indicator of

our liquidity.

We calculate adjusted funds from operations, or AFFO, by subtracting from or adding to normalized FFO (i) unbilled rent revenue, (ii) non-cash

share-based compensation expense, and (iii) amortization of deferred financing costs. AFFO is an operating measurement that we use to analyze our results of operations based on the receipt, rather than the accrual, of our rental revenue and on

certain other adjustments. We believe that this is an important measurement because our leases generally have significant contractual escalations of base rents and therefore result in recognition of rental income that is not collected until future

periods, and costs that are deferred or are non-cash charges. Our calculation of AFFO may not be comparable to AFFO or similarly titled measures reported by other REITs. AFFO should not be considered as an alternative to net income (calculated

pursuant to GAAP) as an indicator of our results of operations or to cash flow from operating activities (calculated pursuant to GAAP) as an indicator of our liquidity.

Q3 2016 | SUPPLEMENTAL INFORMATION 5

MEDICALPROPERTIESTRUST.COM

FINANCIAL

INFORMATION

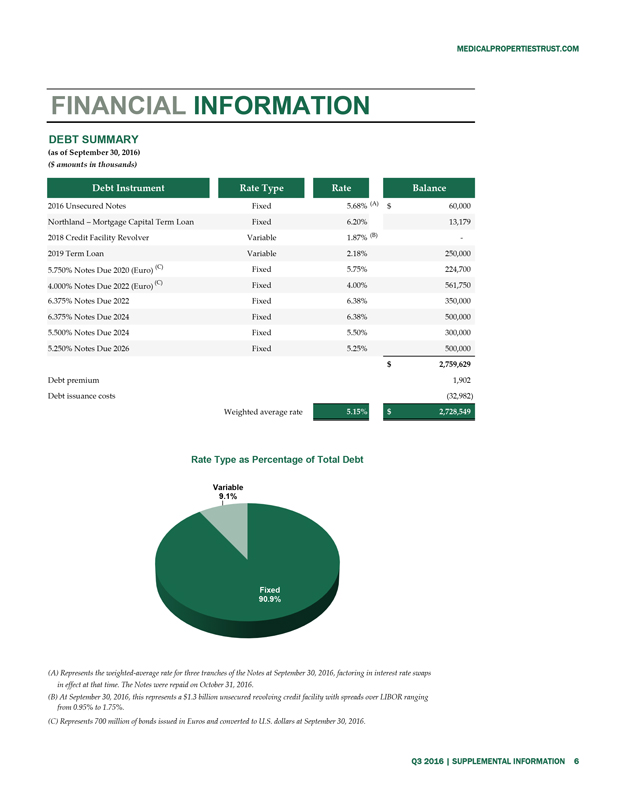

DEBT SUMMARY

(as of September 30, 2016)

($ amounts in thousands)

Debt Instrument Rate Type Rate Balance

2016 Unsecured Notes Fixed 5.68% (A) $60,000

Northland – Mortgage Capital Term Loan Fixed

6.20% 13,179

2018 Credit Facility Revolver Variable 1.87% (B) -

2019 Term

Loan Variable 2.18% 250,000

5.750% Notes Due 2020 (Euro) (C) Fixed 5.75% 224,700

4.000% Notes Due 2022 (Euro) (C) Fixed 4.00% 561,750

6.375% Notes Due 2022 Fixed 6.38% 350,000

6.375% Notes Due 2024 Fixed 6.38% 500,000

5.500% Notes Due 2024 Fixed 5.50%

300,000

5.250% Notes Due 2026 Fixed 5.25% 500,000

$2,759,629

Debt premium 1,902

Debt issuance costs (32,982)

Weighted average rate 5.15% $2,728,549

Rate Type as Percentage of Total Debt

Variable 9.1%

Fixed 90.9%

(A) Represents the weighted-average rate for three tranches of the Notes at September 30, 2016, factoring in interest rate swaps in effect at that time. The Notes were repaid on

October 31, 2016.

(B) At September 30, 2016, this represents a $1.3 billion unsecured revolving credit facility with spreads over LIBOR ranging from 0.95% to

1.75%.

(C) Represents 700 million of bonds issued in Euros and converted to U.S. dollars at September 30, 2016.

Q3 2016 | SUPPLEMENTAL INFORMATION 6

MEDICALPROPERTIESTRUST.COM

FINANCIAL

INFORMATION

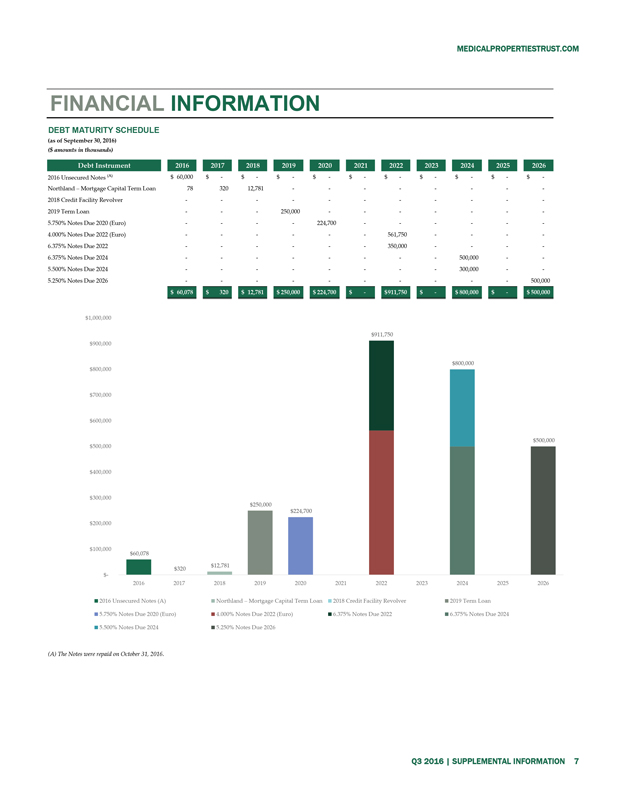

DEBT MATURITY SCHEDULE

(as of September 30, 2016)

($ amounts in thousands)

Debt Instrument 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

2026

2016 Unsecured Notes (A) $60,000 $- $- $- $- $- $- $- $- $- $-

Northland

– Mortgage Capital Term Loan 78 320 12,781 - - - - - - - -

2018 Credit Facility Revolver - - - - - - - - - - -

2019 Term Loan - - - 250,000 - - - - - - -

5.750% Notes Due 2020 (Euro) - - - - 224,700 - - -

- - -

4.000% Notes Due 2022 (Euro) - - - - - - 561,750 - - - -

6.375% Notes

Due 2022 - - - - - - 350,000 - - - -

6.375% Notes Due 2024 - - - - - - - - 500,000 - -

5.500% Notes Due 2024 - - - - - - - - 300,000 - -

5.250% Notes Due 2026 - - - - - - - - - -

500,000

$60,078 $320 $12,781 $250,000 $224,700 $- $911,750 $- $800,000 $- $500,000

$1,000,000 $900,000 $800,000 $700,000 $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $911,750

$- $60,078 $320 $12,781 $250,000 $224,700 $911,750 $800,000 $500,000

2016 2017 2018 2019 2020

2021 2022 2023 2024 2025 2026

2016 Unsecured Notes (A) Northland – Mortgage Capital Term Loan 2018 Credit Facility Revolver 2019 Term Loan

5.750% Notes Due 2020 (Euro) 4.000% Notes Due 2022 (Euro) 6.375% Notes Due 2022 6.375% Notes Due 2024

5.500% Notes Due 2024 5.250% Notes Due 2026

(A) The Notes were repaid on October 31, 2016.

Q3 2016 | SUPPLEMENTAL INFORMATION 7

MEDICALPROPERTIESTRUST.COM

FINANCIAL

INFORMATION

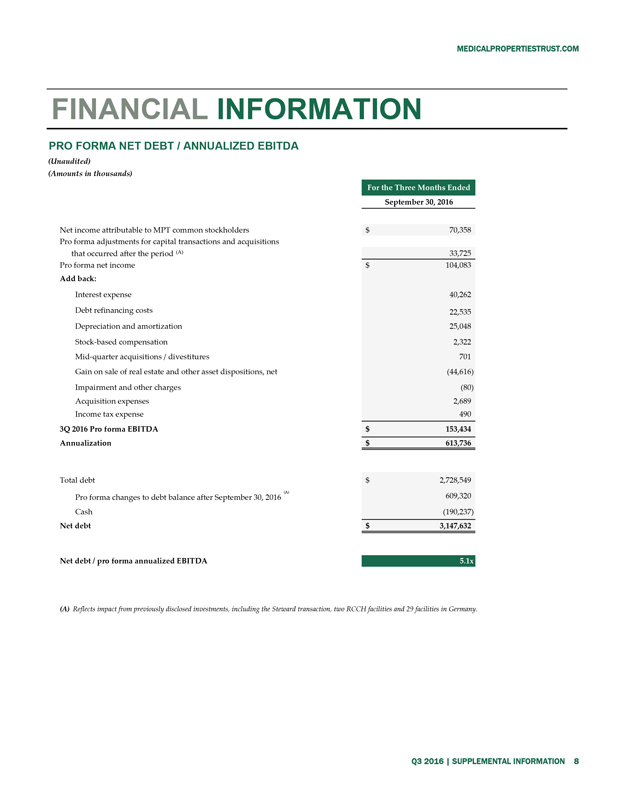

PRO FORMA NET DEBT / ANNUALIZED EBITDA

(Unaudited)

(Amounts in thousands) For the Three Months Ended

September 30, 2016

Net income attributable to MPT common stockholders $70,358

Pro forma adjustments for capital

transactions and acquisitions that occurred after the period (A) 33,725

Pro forma net income $104,083

Add back:

Interest expense 40,262

Debt refinancing costs 22,535

Depreciation and amortization 25,048

Stock-based compensation 2,322

Mid-quarter acquisitions / divestitures 701

Gain on sale of real estate and other asset dispositions, net (44,616)

Impairment and other

charges (80)

Acquisition expenses 2,689

Income tax expense 490

3Q 2016 Pro forma EBITDA $153,434

Annualization $613,736

Total debt $2,728,549

Pro forma changes to debt balance after September 30, 2016 (A) 609,320

Cash (190,237)

Net debt $3,147,632

Net debt / pro forma annualized EBITDA 5.1x

(A) Reflects impact from previously disclosed

investments, including the Steward transaction, two RCCH facilities and 29 facilities in Germany.

Q3 2016 | SUPPLEMENTAL INFORMATION 8

MEDICALPROPERTIESTRUST.COM

PORTFOLIO

INFORMATION

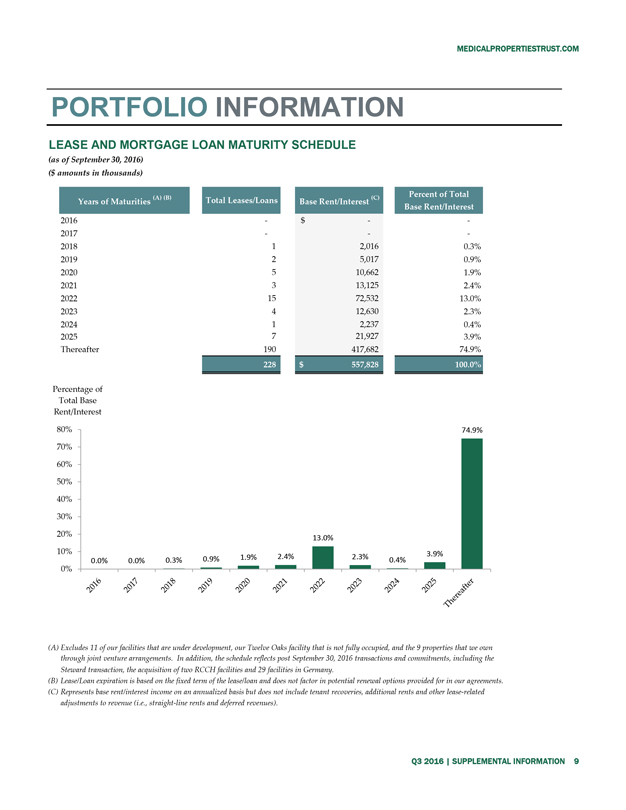

LEASE AND MORTGAGE LOAN MATURITY SCHEDULE

(as of September 30,

2016)

($ amounts in thousands)

Years of Maturities (A) (B) Total Leases/Loans

Base Rent/Interest (C) Percent of Total Base Rent/Interest

2016 - $- -

2017 -

- -

2018 1 2,016 0.3%

2019 2 5,017 0.9%

2020 5 10,662 1.9%

2021 3 13,125 2.4%

2022 15 72,532 13.0%

2023 4 12,630 2.3%

2024 1 2,237 0.4%

2025 7 21,927 3.9%

Thereafter 190 417,682

228 $557,828 100.0%

Percentage of Total Base Rent/Interest

80% 74.9%

70% 50% 40% 30% 20% 10% 0%

0.0% 0.0% 0.3% 0.9% 1.9% 2.4% 13.0% 2.3% 0.4% 3.9% 74.9%

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 Thereafter

(A) Excludes 11

of our facilities that are under development, our Twelve Oaks facility that is not fully occupied, and the 9 properties that we own through joint venture arrangements. In addition, the schedule reflects post September 30, 2016 transactions and

commitments, including the Steward transaction, the acquisition of two RCCH facilities and 29 facilities in Germany.

(B) Lease/Loan expiration is based on the

fixed term of the lease/loan and does not factor in potential renewal options provided for in our agreements.

(C) Represents base rent/interest income on an

annualized basis but does not include tenant recoveries, additional rents and other lease-related adjustments to revenue (i.e., straight-line rents and deferred revenues).

Q3 2016 | SUPPLEMENTAL INFORMATION 9

MEDICALPROPERTIESTRUST.COM

PORTFOLIO

INFORMATION

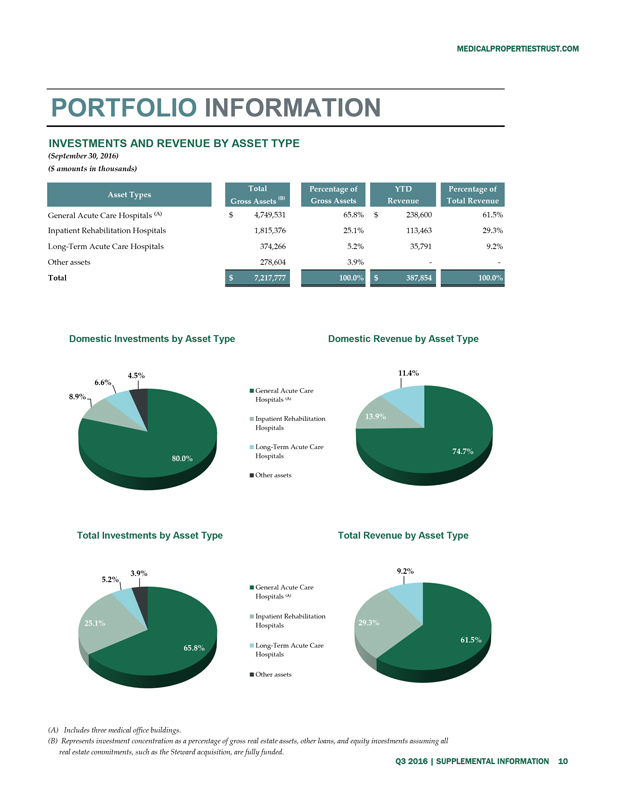

INVESTMENTS AND REVENUE BY ASSET TYPE

(September 30, 2016)

($ amounts in thousands)

| Asset Types General Acute Care Hospitals (A) Inpatient Rehabilitation Hospitals Long-Term Acute Care Hospitals Other assets Total | Total (B) Gross Assets $4,749,531 1,815,376 374,266 278,604 $7,217,777 | Percentage of Gross Assets 65.8% 25.1% 5.2% 3.9% 100.0% | YTD Revenue $238,600 113,463 35,791 — $387,854 | Percentage of Total Revenue 61.5% 29.3% 9.2% — 100.0% |

| Domestic Investments by Asset Type 4.5% 6.6% 8.9% 80.0% | General Acute Care Hospitals (A) Inpatient Rehabilitation Hospitals Long-Term Acute Care Hospitals Other assets | Domestic Revenue by Asset Type 11.4% 13.9% 74.7% |

| Total Investments by Asset Type 3.9% 5.2% 25.1% 65.8% | General Acute Care Hospitals (A) Inpatient Rehabilitation Hospitals Long-Term Acute Care Hospitals Other assets | Total Revenue by Asset Type 9.2% 29.3% 61.5% |

(A) Includes three medical office buildings.

(B)

Represents investment concentration as a percentage of gross real estate assets, other loans, and equity investments assuming all

real estate commitments, such as

the Steward acquisition, are fully funded.

Q3 2016 SUPPLEMENTAL INFORMATION 10

MEDICALPROPERTIESTRUST.COM

PORTFOLIO

INFORMATION

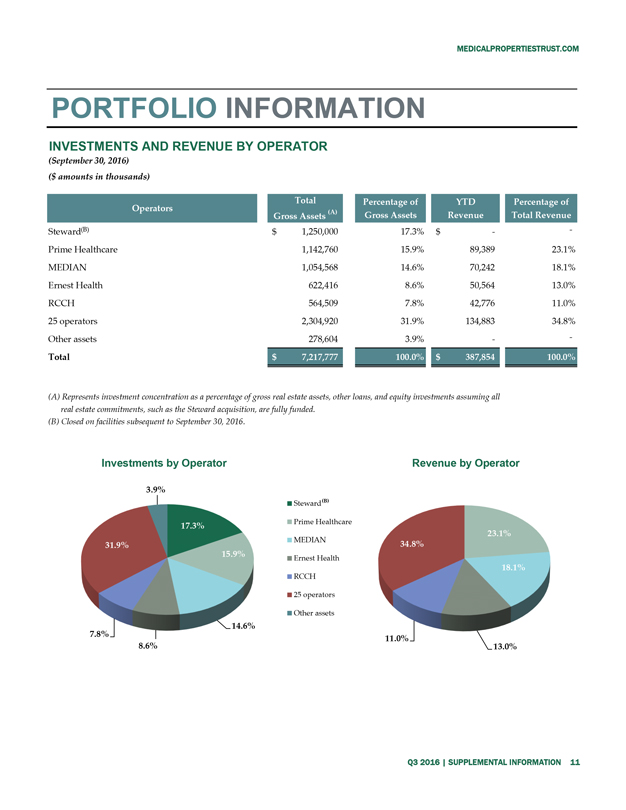

INVESTMENTS AND REVENUE BY OPERATOR

(September 30, 2016)

($ amounts in thousands)

| Operators Steward(B) Prime Healthcare MEDIAN Ernest Health RCCH 25 operators Other assets Total | Total (A) Gross Assets $1,250,000 1,142,760 1,054,568 622,416 564,509 2,304,920 278,604 $7,217,777 | Percentage of Gross Assets 17.3% 15.9% 14.6% 8.6% 7.8% 31.9% 3.9% 100.0% | YTD Revenue $— 89,389 70,242 50,564 42,776 134,883 — $387,854 | Percentage of Total Revenue — 23.1% 18.1% 13.0% 11.0% 34.8% — 100.0% |

(A) Represents investment concentration as a percentage of gross real estate assets, other loans, and equity investments assuming all real

estate commitments, such as the Steward acquisition, are fully funded.

(B) Closed on facilities subsequent to September 30, 2016.

| Investments by Operator 3.9% 17.3% 31.9% 15.9% 14.6% 7.8% 8.6% | Steward(B) Prime Healthcare MEDIAN Ernest Health RCCH 25 operators Other assets | Revenue by Operator 23.1% 34.8% 18.1% 11.0% 13.0% |

Q3 2016 | SUPPLEMENTAL INFORMATION 11

MEDICALPROPERTIESTRUST.COM

PORTFOLIO

INFORMATION

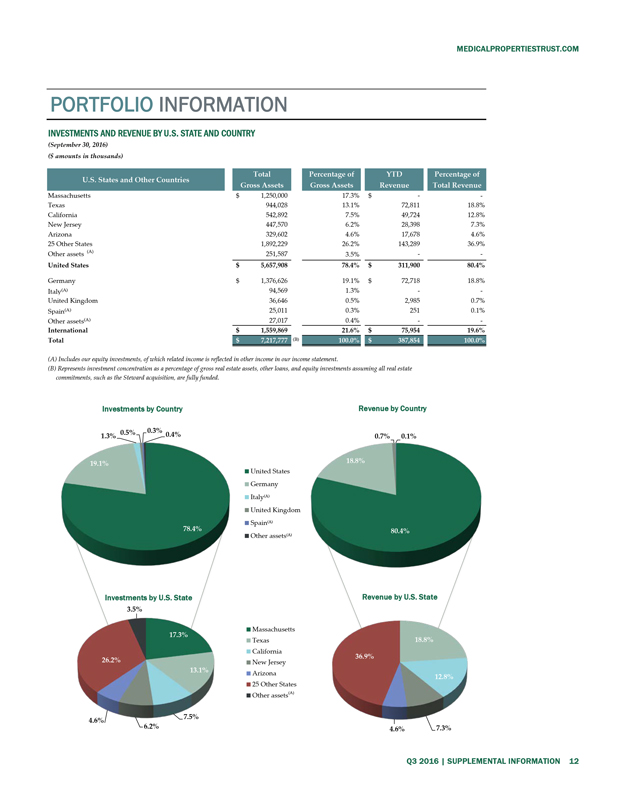

INVESTMENTS AND REVENUE BY U.S. STATE AND COUNTRY

(September 30,

2016)

($ amounts in thousands)

U.S. States and Other Countries Total Gross

Assets Percentage of Gross Assets YTD Revenue Percentage of Total Revenue

Massachusetts $ 1,250,000 17.3% $ — —

Texas 944,028 13.1% 72,811 18.8%

California 542,892 7.5% 49,724 12.8%

New Jersey 447,570 6.2% 28,398 7.3%

Arizona 329,602 4.6% 17,678 4.6%

25 Other States 1,892,229 26.2% 143,289 36.9%

Other assets (A) 251,587 3.5% — —

United States $ 5,657,908 78.4% $ 311,900 80.4%

Germany $ 1,376,626 19.1% $

72,718 18.8%

Italy(A) 94,569 1.3% — —

United Kingdom 36,646 0.5%

2,985 0.7%

Spain(A) 25,011 0.3% 251 0.1%

Other assets(A) 27,017 0.4% —

—

International $ 1,559,869 21.6% $ 75,954 19.6%

Total $ 7,217,777 (B)

100.0% $ 387,854 100.0%

(A) Includes our equity investments, of which related income is reflected in other income in our income statement.

(B) Represents investment concentration as a percentage of gross real estate assets, other loans, and equity investments assuming all real estate commitments, such as the Steward

acquisition, are fully funded.

Investments by Country

1.3% 0.5% 0.3% 0.4%

19.1% 78.4%

Investments by U.S. State

3.5%

17.3%

26.2%

13.1%

4.6% 6.2% 7.5%

United States

Germany

Italy(A)

United Kingdom

Spain(A)

Other assets(A)

Massachusetts

Texas

California

New Jersey

Arizona

25 Other States

Other assets(A)

Revenue by Country

0.7% 0.1%

18.8%

80.4%

Revenue by U.S. State

18.8%

36.9%

12.8%

4.6% 7.3%

Q3 2016 | SUPPLEMENTAL INFORMATION 12

MEDICALPROPERTIESTRUST.COM

PORTFOLIO

INFORMATION

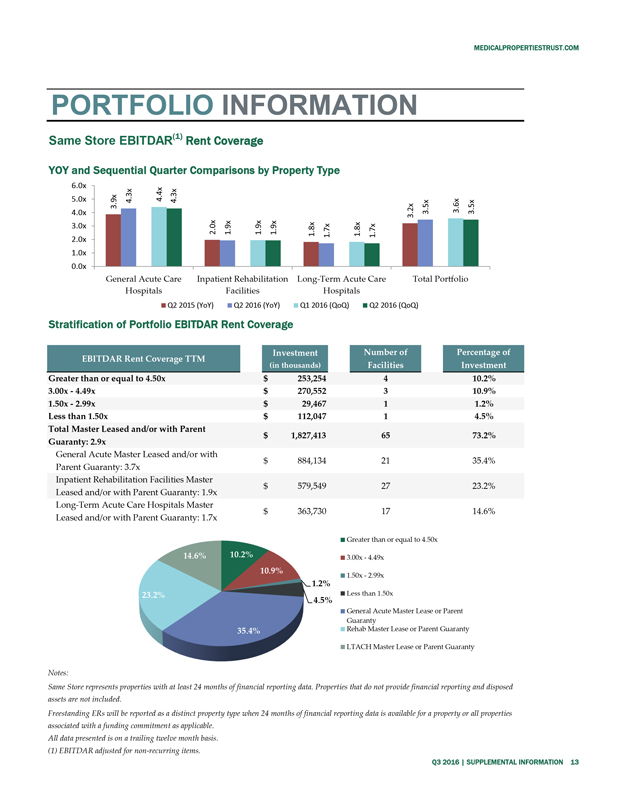

Same Store EBITDAR(1) Rent Coverage

YOY and Sequential Quarter

Comparisons by Property Type

| 6.0x 5.0x 4.0x 3.0x 2.0x 1.0x 0.0x | 3.9x 4.3x General Acute Care Hospitals | 4.4x 4.3x | 2.0x 1.9x Inpatient Rehabilitation Facilities | 1.9x 1.9x | 1.8x 1.7x Long-Term Acute Care Hospitals | 1.8x 1.7x | 3.2x 3.5x Total Portfolio | 3.6x 3.5x |

Q2 2015 (YoY) Q2 2016 (YoY) Q1 2016 (QoQ)Q2 2016 (QoQ)

Stratification of Portfolio EBITDAR Rent Coverage

| EBITDAR Rent Coverage TTM Greater than or equal to 4.50x 3.00x - 4.49x 1.50x - 2.99x Less than 1.50x Total Master Leased and/or with Parent Guaranty: 2.9x General Acute Master Leased and/or with Parent Guaranty: 3.7x Inpatient Rehabilitation Facilities Master Leased and/or with Parent Guaranty: 1.9x Long-Term Acute Care Hospitals Master Leased and/or with Parent Guaranty: 1.7x | Investment (in thousands) $253,254 $270,552 $29,467 $112,047 $1,827,413 $884,134 $579,549 $363,730 | Number of Facilities 4 3 1 1 65 21 27 17 | Percentage of Investment 10.2% 10.9% 1.2% 4.5% 73.2% 35.4% 23.2% 14.6% |

| 23.2% | 14.6% | 10.2% 10.9% 35.4% | 1.2% 4.5% | Greater than or equal to 4.50x 3.00x - 4.49x 1.50x - 2.99x Less than 1.50x General Acute Master Lease or Parent Guaranty Rehab Master Lease or Parent Guaranty LTACH Master Lease or Parent Guaranty |

Notes:

Same Store represents properties with at least

24 months of financial reporting data. Properties that do not provide financial reporting and disposed assets are not included.

Freestanding ERs will be reported

as a distinct property type when 24 months of financial reporting data is available for a property or all properties associated with a funding commitment as applicable.

All data presented is on a trailing twelve month basis.

(1) EBITDAR adjusted for non-recurring

items.

Q3 2016 SUPPLEMENTAL INFORMATION

13

MEDICALPROPERTIESTRUST.COM

PORTFOLIO

INFORMATION

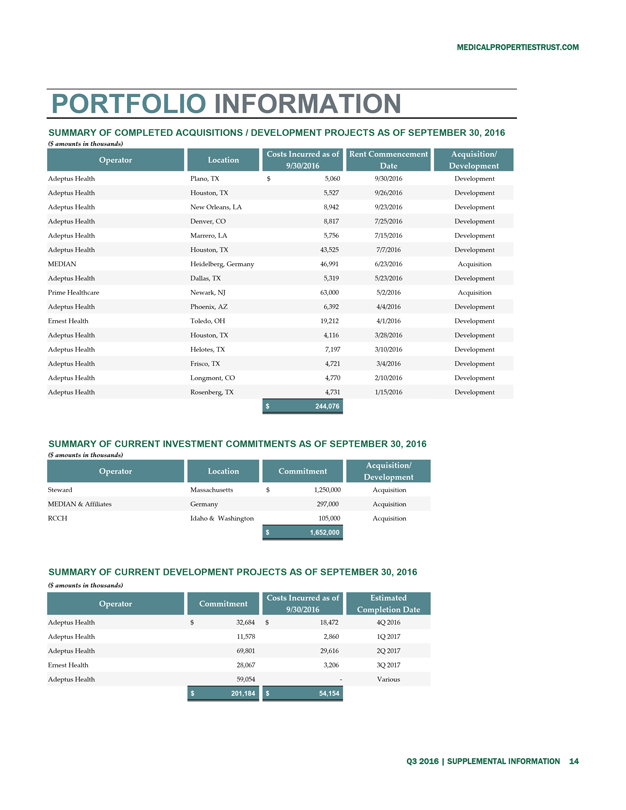

SUMMARY OF COMPLETED ACQUISITIONS / DEVELOPMENT PROJECTS AS OF SEPTEMBER 30, 2016

($ amounts in thousands)

| Operator Adeptus Health Adeptus Health Adeptus Health Adeptus Health Adeptus Health Adeptus Health MEDIAN Adeptus Health Prime Healthcare Adeptus Health Ernest Health Adeptus Health Adeptus Health Adeptus Health Adeptus Health Adeptus Health | Location Plano, TX Houston, TX New Orleans, LA Denver, CO Marrero, LA Houston, TX Heidelberg, Germany Dallas, TX Newark, NJ Phoenix, AZ Toledo, OH Houston, TX Helotes, TX Frisco, TX Longmont, CO Rosenberg, TX | Costs Incurred as of 9/30/2016 $5,060 5,527 8,942 8,817 5,756 43,525 46,991 5,319 63,000 6,392 19,212 4,116 7,197 4,721 4,770 4,731 $244,076 | Rent Commencement Date 9/30/2016 9/26/2016 9/23/2016 7/25/2016 7/15/2016 7/7/2016 6/23/2016 5/23/2016 5/2/2016 4/4/2016 4/1/2016 3/28/2016 3/10/2016 3/4/2016 2/10/2016 1/15/2016 | Acquisition/ Development Development Development Development Development Development Development Acquisition Development Acquisition Development Development Development Development Development Development Development |

SUMMARY OF CURRENT INVESTMENT COMMITMENTS AS OF SEPTEMBER 30, 2016

($ amounts in thousands)

| Operator Steward MEDIAN & Affiliates RCCH | Location Massachusetts Germany Idaho & Washington | Commitment $1,250,000 297,000 105,000 $1,652,000 | Acquisition/ Development Acquisition Acquisition Acquisition |

SUMMARY OF CURRENT DEVELOPMENT PROJECTS AS OF SEPTEMBER 30, 2016

($ amounts in thousands)

| Operator Adeptus Health Adeptus Health Adeptus Health Ernest Health Adeptus Health | Commitment $32,684 11,578 69,801 28,067 59,054 $201,184 | Costs Incurred as of 9/30/2016 $18,472 2,860 29,616 3,206 $54,154 | Estimated Completion Date 4Q 2016 1Q 2017 2Q 2017 3Q 2017 - Various |

Q3 2016 | SUPPLEMENTAL INFORMATION 14

MEDICALPROPERTIESTRUST.COM

FINANCIAL

STATEMENTS

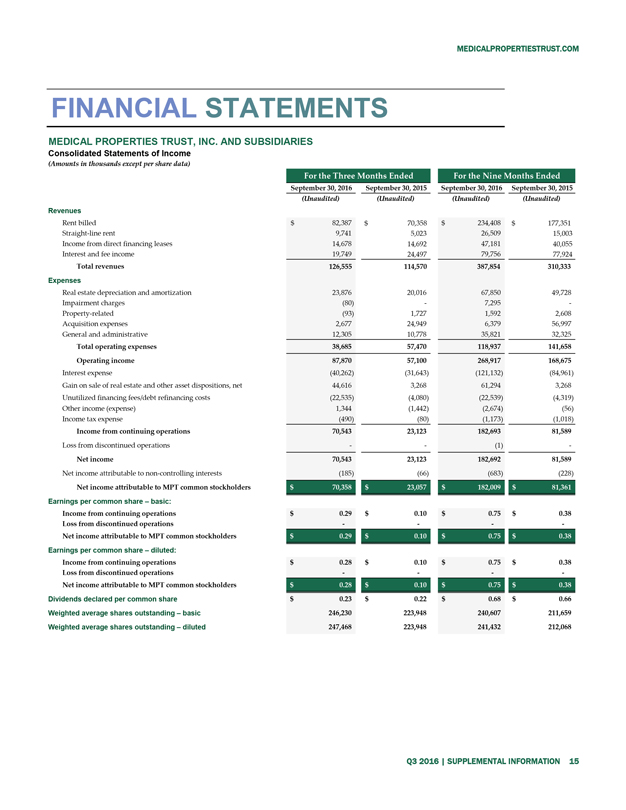

MEDICAL PROPERTIES TRUST, INC. AND SUBSIDIARIES

Consolidated

Statements of Income

(Amounts in thousands except per share data)

| Revenues Rent billed Straight-line rent Income from direct financing leases Interest and fee income Total revenues Expenses Real estate depreciation and amortization Impairment charges Property-related Acquisition expenses General and administrative Total operating expenses Operating income Interest expense Gain on sale of real estate and other asset dispositions, net Unutilized financing fees/debt refinancing costs Other income (expense) Income tax expense Income from continuing operations Loss from discontinued operations Net income Net income attributable to non-controlling interests Net income attributable to MPT common stockholders Earnings per common share – basic: Income from continuing operations Loss from discontinued operations Net income attributable to MPT common stockholders Earnings per common share – diluted: Income from continuing operations Loss from discontinued operations Net income attributable to MPT common stockholders Dividends declared per common share Weighted average shares outstanding – basic Weighted average shares outstanding – diluted | For the Three Months Ended September 30, 2016 September 30, 2015 (Unaudited) (Unaudited) $82,387 $70,358 9,741 5,023 14,678 14,692 19,749 24,497 126,555 114,570 23,876 20,016 (80) - (93) 1,727 2,677 24,949 12,305 10,778 38,685 57,470 87,870 57,100 (40,262) (31,643) 44,616 3,268 (22,535) (4,080) 1,344 (1,442) (490) (80) 70,543 23,123 - - 70,543 23,123 (185) (66) $70,358 $23,057 $0.29 $0.10 - - $0.29 $0.10 $0.28 $0.10 - - $0.28 $0.10 $0.23 $0.22 246,230 223,948 247,468 223,948 | For the Nine Months Ended September 30, 2016 September 30, 2015 (Unaudited) (Unaudited) $234,408 $177,351 26,509 15,003 47,181 40,055 79,756 77,924 387,854 310,333 67,850 49,728 7,295 - 1,592 2,608 6,379 56,997 35,821 32,325 118,937 141,658 268,917 168,675 (121,132) (84,961) 61,294 3,268 (22,539) (4,319) (2,674) (56) (1,173) (1,018) 182,693 81,589 (1) - 182,692 81,589 (683) (228) $182,009 $81,361 $0.75 $0.38 - - $0.75 $0.38 $0.75 $0.38 - - $0.75 $0.38 $0.68 $0.66 240,607 211,659 241,432 212,068 | ||||||

Q3 2016 | SUPPLEMENTAL INFORMATION 15

MEDICALPROPERTIESTRUST.COM

FINANCIAL

STATEMENTS

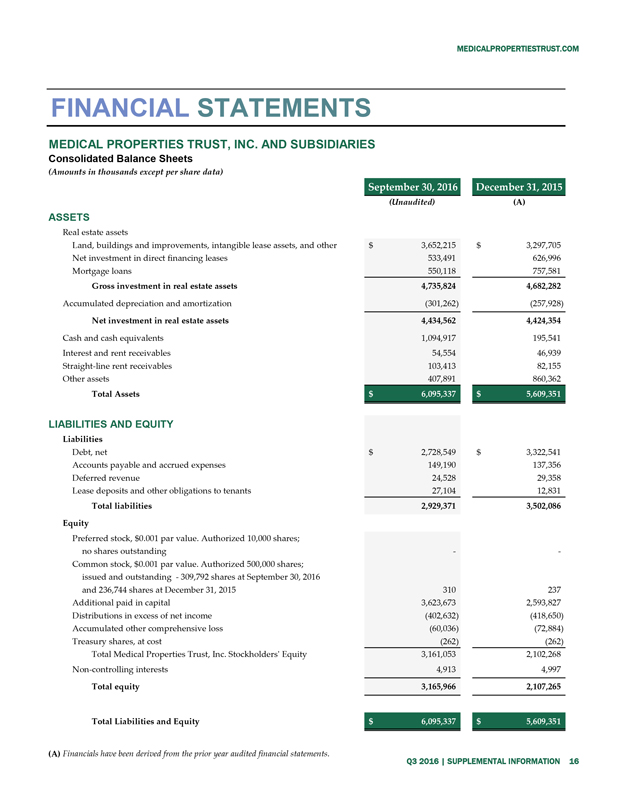

MEDICAL PROPERTIES TRUST, INC. AND SUBSIDIARIES

Consolidated

Balance Sheets

(Amounts in thousands except per share data)

| ASSETS Real estate assets Land, buildings and improvements, intangible lease assets, and other Net investment in direct financing leases Mortgage loans Gross investment in real estate assets Accumulated depreciation and amortization Net investment in real estate assets Cash and cash equivalents Interest and rent receivables Straight-line rent receivables Other assets Total Assets LIABILITIES AND EQUITY Liabilities Debt, net Accounts payable and accrued expenses Deferred revenue Lease deposits and other obligations to tenants Total liabilities Equity Preferred stock, $0.001 par value. Authorized 10,000 shares; no shares outstanding Common stock, $0.001 par value. Authorized 500,000 shares; issued and outstanding - 309,792 shares at September 30, 2016 and 236,744 shares at December 31, 2015 Additional paid in capital Distributions in excess of net income Accumulated other comprehensive loss Treasury shares, at cost Total Medical Properties Trust, Inc. Stockholders’ Equity Non-controlling interests Total equity Total Liabilities and Equity | September 30, 2016 (Unaudited) $3,652,215 533,491 550,118 4,735,824 (301,262) 4,434,562 1,094,917 54,554 103,413 407,891 $6,095,337 $2,728,549 149,190 24,528 27,104 2,929,371 - 310 3,623,673 (402,632) (60,036) (262) 3,161,053 4,913 3,165,966 $6,095,337 | December 31, 2015 (A) $3,297,705 626,996 757,581 4,682,282 (257,928) 4,424,354 195,541 46,939 82,155 860,362 $5,609,351 $3,322,541 137,356 29,358 12,831 3,502,086 - 237 2,593,827 (418,650) (72,884) (262) 2,102,268 4,997 2,107,265 $5,609,351 |

(A) Financials have been derived from the prior year audited financial statements.

Q3 2016 SUPPLEMENTAL INFORMATION 16

MEDICALPROPERTIESTRUST.COM

FINANCIAL

STATEMENTS

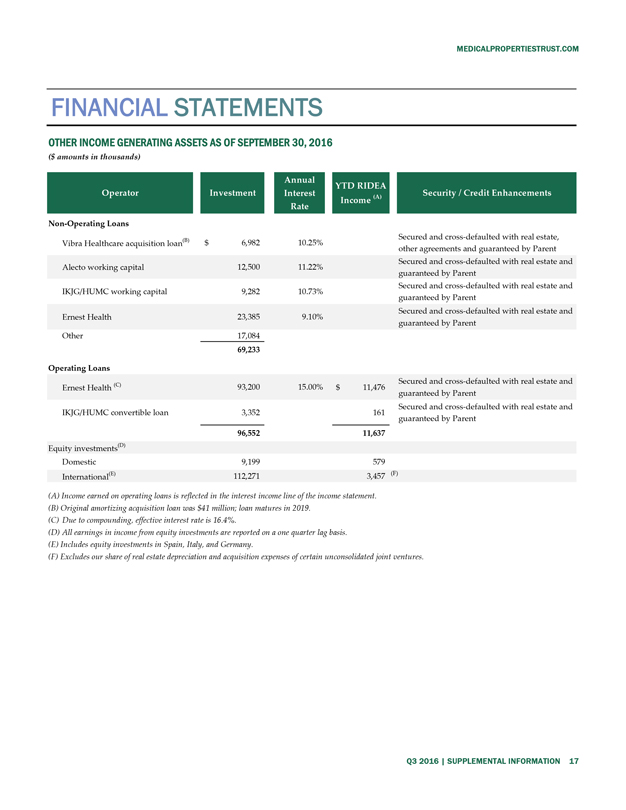

OTHER INCOME GENERATING ASSETS AS OF SEPTEMBER 30, 2016

($ amounts

in thousands)

Operator Investment Annual Interest Rate YTD RIDEA Income (A) Security / Credit Enhancements

Non-Operating Loans

Vibra Healthcare acquisition loan(B) $ 6,982 10.25%

Secured and cross-defaulted with real estate, other agreements and guaranteed by Parent

Alecto

working capital 12,500 11.22%

Secured and cross-defaulted with real estate and guaranteed by Parent

IKJG/HUMC working capital 9,282 10.73%

Secured and cross-defaulted with real estate and

guaranteed by Parent

Ernest Health 23,385 9.10%

Secured and cross-defaulted

with real estate and guaranteed by Parent

Other 17,084

69,233

Operating Loans

Ernest Health (C) 93,200 15.00% $ 11,476

Secured and cross-defaulted with real estate and guaranteed by Parent

IKJG/HUMC convertible

loan 3,352 161

Secured and cross-defaulted with real estate and guaranteed by Parent

96,552 11,637

Equity investments(D)

Domestic 9,199 579

International(E) 112,271 3,457 (F)

(A) Income earned on operating loans is reflected in the interest income line of the income statement.

(B) Original amortizing acquisition loan was $41 million; loan matures in 2019.

(C) Due to

compounding, effective interest rate is 16.4%.

(D) All earnings in income from equity investments are reported on a one quarter lag basis.

(E) Includes equity investments in Spain, Italy, and Germany.

(F) Excludes our share of real

estate depreciation and acquisition expenses of certain unconsolidated joint ventures.

Q3 2016 | SUPPLEMENTAL INFORMATION 17

MPT

Medical Properties Trust

1000 Urban Center Drive, Suite 501

Birmingham, AL 35242

(205) 969-3755 NYSE: MPW

www.medicalpropertiestrust.com

Contact:

Charles Lambert, Managing Director - Capital Markets

(205) 397-8897 or clambert@medicalpropertiestrust.com

or

Tim Berryman, Director - Investor Relations

(205) 397-8589 or

tberryman@medicalpropertiestrust.com

AT THE VERY HEART OF HEALTHCARE® .