Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - HV Bancorp, Inc. | d251878dex232.htm |

| EX-99.2 - EX-99.2 - HV Bancorp, Inc. | d251878dex992.htm |

| EX-99.1 - EX-99.1 - HV Bancorp, Inc. | d251878dex991.htm |

| EX-23.3 - EX-23.3 - HV Bancorp, Inc. | d251878dex233.htm |

| EX-21 - EX-21 - HV Bancorp, Inc. | d251878dex21.htm |

| EX-10.3 - EX-10.3 - HV Bancorp, Inc. | d251878dex103.htm |

| EX-10.2 - EX-10.2 - HV Bancorp, Inc. | d251878dex102.htm |

| EX-10.1 - EX-10.1 - HV Bancorp, Inc. | d251878dex101.htm |

| EX-8.2 - EX-8.2 - HV Bancorp, Inc. | d251878dex82.htm |

| EX-8.1 - EX-8.1 - HV Bancorp, Inc. | d251878dex81.htm |

| EX-5 - EX-5 - HV Bancorp, Inc. | d251878dex5.htm |

| EX-4 - EX-4 - HV Bancorp, Inc. | d251878dex4.htm |

| EX-3.2 - EX-3.2 - HV Bancorp, Inc. | d251878dex32.htm |

| EX-3.1 - EX-3.1 - HV Bancorp, Inc. | d251878dex31.htm |

| EX-2 - EX-2 - HV Bancorp, Inc. | d251878dex2.htm |

| EX-1.1 - EX-1.1 - HV Bancorp, Inc. | d251878dex11.htm |

| S-1 - S-1 - HV Bancorp, Inc. | d251878ds1.htm |

Exhibit 99.3

PRO FORMA VALUATION REPORT

STANDARD CONVERSION

HV Bancorp, Inc. | Huntingdon Valley, Pennsylvania

PROPOSED HOLDING COMPANY FOR:

Huntingdon Valley Bank | Huntingdon Valley, Pennsylvania

Dated as of August 5, 2016

1100 North Glebe Road Suite 600

Arlington, Virginia 22201

703.528.1700

rpfinancial.com

August 5, 2016

Board of Directors

HV Bancorp, Inc.

Board of Trustees

Huntingdon Valley Bank

3501 Masons Mill Road, Suite 401

Huntingdon Valley, Pennsylvania 19006

Members of the Board of Directors:

At your request, we have completed and hereby provide an independent appraisal (“Appraisal”) of the estimated pro forma market value of the common stock which is to be issued in connection with the mutual-to-stock conversion transaction described below.

This Appraisal is furnished pursuant to the requirements stipulated in the Code of Federal Regulations and has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” of the Office of Thrift Supervision (“OTS”) and accepted by the Federal Reserve Board (“FRB”), the Office of the Comptroller of the Currency (“OCC”), the Federal Deposit Insurance Corporation (“FDIC”) and the Pennsylvania Department of Banking and Securities (the “Department”), and applicable regulatory interpretations thereof.

Description of Plan of Conversion

The Board of Trustees of Huntingdon Valley Bank, Huntingdon Valley, Pennsylvania (““HV Bank” or the “Bank”) adopted the plan of conversion on July 20, 2016, incorporated herein by reference. Pursuant to the plan of conversion, the Bank will convert from a Pennsylvania-chartered mutual savings bank to a Pennsylvania-chartered stock savings bank and become a wholly-owned subsidiary of HV Bancorp, Inc. (“HV Bancorp” or the “Company”), a Pennsylvania corporation formed by HV Bank. HV Bancorp will offer 100% of its common stock to qualifying depositors of the Bank in a subscription offering to Eligible Account Holders, Tax-Qualified Employee Benefit Plans including HV Bank’s employee stock ownership plan (the “ESOP”), Supplemental Eligible Account Holders and Other Members, as such terms are defined for purposes of applicable federal regulatory guidelines governing mutual-to-stock conversions. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to the public at large in a community offering and/or a syndicated community offering. Going forward, HV Bancorp will own 100% of the Bank’s stock, and the Bank will initially be HV Bancorp’s sole subsidiary. A portion of the net proceeds received from the sale of common stock will be used to purchase all of the then to be issued and outstanding capital stock of the Bank and the balance of the net proceeds will be retained by the Company.

| Washington Headquarters | ||

| Three Ballston Plaza | Telephone: (703) 528-1700 | |

| 1100 North Glebe Road, Suite 600 | Fax No.: (703) 528-1788 | |

| Arlington, VA 22201 | Toll-Free No.: (866) 723-0594 | |

| www.rpfinancial.com | E-Mail: mail@rpfinancial.com |

Board of Directors

August 5, 2016

Page 2

At this time, no other activities are contemplated for the Company other than the ownership of the Bank, a loan to the newly-formed ESOP and reinvestment of the proceeds that are retained by the Company. In the future, HV Bancorp may acquire or organize other operating subsidiaries, diversify into other banking-related activities, pay dividends or repurchase its stock, although there are no specific plans to undertake such activities at the present time.

RP® Financial, LC.

RP® Financial, LC. (“RP Financial”) is a financial consulting firm serving the financial services industry nationwide that, among other things, specializes in financial valuations and analyses of business enterprises and securities, including the pro forma valuation for savings institutions converting from mutual-to-stock form. The background and experience of RP Financial is detailed in Exhibit V-1. For its appraisal services, RP Financial is being compensated on a fixed fee basis for the original appraisal and for any subsequent updates, and such fees are payable regardless of the valuation conclusion or the completion of the conversion offering transaction. We believe that we are independent of the Bank and the other parties engaged by HV Bank or the Company to assist in the stock conversion process.

Valuation Methodology

In preparing our Appraisal, we have reviewed the regulatory applications of the Bank and the Company, including the prospectus as filed with the FRB, the FDIC, the Department and the Securities and Exchange Commission (“SEC”). We have conducted a financial analysis of the Bank that has included a review of audited financial information for the fiscal years ended June 30, 2012 through June 30, 2016 and a review of various unaudited information and internal financial reports through June 30, 2016. We have also conducted due diligence related discussions with HV Bank’s management; BDO USA, LLP, HV Bank’s independent auditor; Luse Gorman, PC, HV Bank’s conversion counsel; and Sandler O’Neill & Partners, L.P., HV Bank’s financial and marketing advisor in connection with the stock offering. All assumptions and conclusions set forth in the Appraisal were reached independently from such discussions. In addition, where appropriate, we have considered information based on other available published sources that we believe are reliable. While we believe the information and data gathered from all these sources are reliable, we cannot guarantee the accuracy and completeness of such information.

We have investigated the competitive environment within which HV Bank operates and have assessed the Bank’s relative strengths and weaknesses. We have monitored all material regulatory and legislative actions affecting financial institutions generally and analyzed the potential impact of such developments on HV Bank and the industry as a whole to the extent we were aware of such matters. We have analyzed the potential effects of the stock conversion on the Bank’s operating characteristics and financial performance as they relate to the pro forma market value of HV Bank. We have reviewed the economy and demographic characteristics of the primary market area in which the Bank currently operates. We have compared HV Bank’s financial performance and condition with publicly-traded thrift institutions evaluated and selected in accordance with the Valuation Guidelines, as well as all publicly-traded thrifts and thrift holding companies. We have reviewed conditions in the securities markets in general and the market for thrifts and thrift holding companies, including the market for new issues.

Board of Directors

August 5, 2016

Page 3

The Appraisal is based on HV Bank’s representation that the information contained in the regulatory applications and additional information furnished to us by the Bank and its independent auditors, legal counsel, investment bankers and other authorized agents are truthful, accurate and complete. We did not independently verify the financial statements and other information provided by the Bank, or its independent auditors, legal counsel, investment bankers and other authorized agents nor did we independently value the assets or liabilities of HV Bank. The valuation considers HV Bank only as a going concern and should not be considered as an indication of the Bank’s liquidation value.

Our appraised value is predicated on a continuation of the current operating environment for the Bank and for all thrifts and their holding companies. Changes in the local and national economy, the federal and state legislative and regulatory environments for financial institutions, the stock market, interest rates, and other external forces (such as natural disasters or significant world events) may occur from time to time, often with great unpredictability, and may materially impact the value of thrift stocks as a whole or the Bank’s value alone. It is our understanding that HV Bank intends to remain an independent institution and there are no current plans for selling control of the Bank as a converted institution. To the extent that such factors can be foreseen, they have been factored into our analysis.

The estimated pro forma market value is defined as the price at which the Company’s stock, immediately upon completion of the offering, would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.

Valuation Conclusion

It is our opinion that, as of August 5, 2016, the estimated aggregate pro forma market value of the shares to be issued immediately following the conversion equaled $16,500,000 at the midpoint, equal to 1,650,000 shares offered at a per share value of $10.00. Pursuant to conversion guidelines, the 15% offering range indicates a minimum value of $14,025,000 and a maximum value of $18,975,000. Based on the $10.00 per share offering price determined by the Board, this valuation range equates to total shares outstanding of 1,402,500 at the minimum and 1,897,500 at the maximum. In the event the appraised value is subject to an increase, the aggregate pro forma market value may be increased up to a super maximum value of $21,821,250 without a resolicitation. Based on the $10.00 per share offering price, the super maximum value would result in total shares outstanding of 2,182,250.

Limiting Factors and Considerations

The valuation is not intended, and must not be construed, as a recommendation of any kind as to the advisability of purchasing shares of the common stock. Moreover, because such valuation is determined in accordance with applicable regulatory guidelines and is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of common

Board of Directors

August 5, 2016

Page 4

stock in the conversion will thereafter be able to buy or sell such shares at prices related to the foregoing valuation of the estimated pro forma market value thereof. The appraisal reflects only a valuation range as of this date for the pro forma market value of HV Bancorp immediately upon issuance of the stock and does not take into account any trading activity with respect to the purchase and sale of common stock in the secondary market on the date of issuance of such securities or at anytime thereafter following the completion of the public stock offering.

The valuation prepared by RP Financial, in accordance with applicable regulatory guidelines, was based on the financial condition and operations of HV Bank as of June 30, 2016, the date of the financial data included in the prospectus.

RP Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by RP Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities. RP Financial maintains a policy which prohibits RP Financial, its principals or employees from purchasing stock of its financial institution clients.

The valuation will be updated as provided for in the conversion regulations and guidelines. These updates will consider, among other things, any developments or changes in the financial performance and condition of HV Bank, management policies, and current conditions in the equity markets for thrift stocks, both existing issues and new issues. These updates may also consider changes in other external factors which impact value including, but not limited to: various changes in the federal and state legislative and regulatory environments for financial institutions, the stock market in general, the market for thrift stocks and interest rates. Should any such new developments or changes be material, in our opinion, to the valuation of the shares, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in the update at the date of the release of the update.

| Respectfully submitted, |

| RP® FINANCIAL, LC. |

|

| Marcus Faust |

| Managing Director |

|

| Gregory E. Dunn |

| Director |

| RP® Financial, LC. | TABLE OF CONTENTS |

TABLE OF CONTENTS

HV Bancorp, Inc.

Huntingdon Valley Bank

Huntingdon Valley, Pennsylvania

| DESCRIPTION |

PAGE NUMBER |

|||||

| CHAPTER ONE | OVERVIEW AND FINANCIAL ANALYSIS | |||||

| Introduction |

I.1 | |||||

| Plan of Conversion |

I.1 | |||||

| Strategic Overview |

I.2 | |||||

| Balance Sheet Trends |

I.4 | |||||

| Income and Expense Trends |

I.7 | |||||

| Interest Rate Risk Management |

I.10 | |||||

| Lending Activities and Strategy |

I.11 | |||||

| Asset Quality |

I.14 | |||||

| Funding Composition and Strategy |

I.14 | |||||

| Legal Proceedings |

I.15 | |||||

| CHAPTER TWO |

MARKET AREA ANALYSIS | |||||

| Introduction |

II.1 | |||||

| National Economic Factors |

II.1 | |||||

| Market Area Demographics |

II.5 | |||||

| Regional Economy |

II.7 | |||||

| Unemployment Data |

II.11 | |||||

| Deposit Trends |

II.12 | |||||

| Competition |

II.13 | |||||

| CHAPTER THREE |

PEER GROUP ANALYSIS | |||||

| Peer Group Selection |

III.1 | |||||

| Financial Condition |

III.5 | |||||

| Income and Expense Components |

III.8 | |||||

| Loan Composition |

III.11 | |||||

| Interest Rate Risk |

III.13 | |||||

| Credit Rate Risk |

III.15 | |||||

| Summary |

III.17 | |||||

i

| RP® Financial, LC. | TABLE OF CONTENTS |

TABLE OF CONTENTS

HV Bancorp, Inc.

Huntingdon Valley Bank

Huntingdon Valley, Pennsylvania

(continued)

| DESCRIPTION |

PAGE NUMBER | |||

| CHAPTER FOUR | VALUATION ANALYSIS | |||

| Introduction |

IV.1 | |||

| Appraisal Guidelines |

IV.1 | |||

| RP Financial Approach to the Valuation |

IV.1 | |||

| Valuation Analysis |

IV.2 | |||

| 1. Financial Condition |

IV.2 | |||

| 2. Profitability, Growth and Viability of Earnings |

IV.4 | |||

| 3. Asset Growth |

IV.5 | |||

| 4. Primary Market Area |

IV.6 | |||

| 5. Dividends |

IV.7 | |||

| 6. Liquidity of the Shares |

IV.8 | |||

| 7. Marketing of the Issue |

IV.8 | |||

| A. The Public Market |

IV.8 | |||

| B. The New Issue Market |

IV.12 | |||

| C. The Acquisition Market |

IV.13 | |||

| 8. Management |

IV.16 | |||

| 9. Effect of Government Regulation and Regulatory Reform |

IV.16 | |||

| Summary of Adjustments |

IV.17 | |||

| Valuation Approach |

IV.17 | |||

| 1. Price-to-Earnings (“P/E”) |

IV.18 | |||

| 2. Price-to-Book (“P/B”) |

IV.19 | |||

| 3. Price-to-Assets (“P/A”) |

IV.21 | |||

| Comparison to Recent Offerings |

IV.21 | |||

| Valuation Conclusion |

IV.21 | |||

ii

| RP® Financial, LC. | LIST OF TABLES |

LIST OF TABLES

Huntingdon Valley Bancorp, Inc.

Huntingdon Valley Bank

Huntingdon Valley, Pennsylvania

| TABLE |

DESCRIPTION |

PAGE | ||

| 1.1 | Historical Balance Sheet Data |

I.5 | ||

| 1.2 | Historical Income Statements |

I.8 | ||

| 2.1 | Summary Demographic Data |

II.6 | ||

| 2.2 | Market Area Largest Employers – Greater Philadelphia |

II.9 | ||

| 2.3 | Market Area Largest Employers – Montgomery County |

II.11 | ||

| 2.4 | Unemployment Trends |

II.12 | ||

| 2.5 | Deposit Summary |

II.13 | ||

| 2.6 | Market Area Deposit Competitors |

II.14 | ||

| 3.1 | Peer Group of Publicly-Traded Thrifts |

III.3 | ||

| 3.2 | Balance Sheet Composition and Growth Rates |

III.6 | ||

| 3.3 | Income as a Pct. of Avg. Assets and Yields, Costs, Spreads |

III.9 | ||

| 3.4 | Loan Portfolio Composition and Related Information |

III.12 | ||

| 3.5 | Interest Rate Risk Measures and Net Interest Income Volatility |

III.14 | ||

| 3.6 | Credit Risk Measures and Related Information |

III.16 | ||

| 4.1 | Market Area Unemployment Rates |

IV.7 | ||

| 4.2 | Pricing Characteristics and After-Market Trends |

IV.14 | ||

| 4.3 | Market Pricing Comparatives |

IV.15 | ||

| 4.4 | Public Market Pricing Versus Peer Group |

IV.20 | ||

iii

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.1

I. OVERVIEW AND FINANCIAL ANALYSIS

Introduction

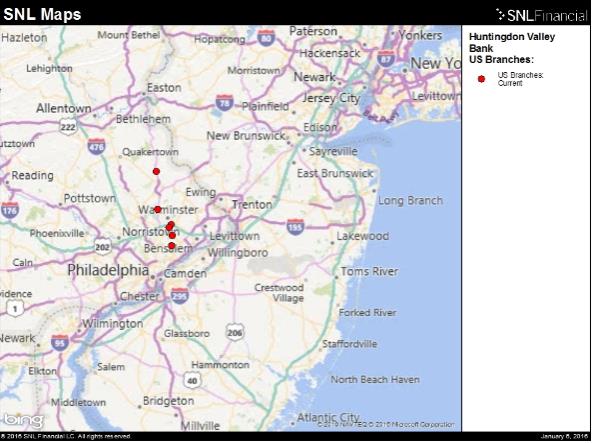

Huntingdon Valley Bank (“HV Bank” or the “Bank”), chartered in 1871, is a Pennsylvania-chartered mutual savings bank headquartered in Huntingdon Valley, Pennsylvania. HV Bank serves the Philadelphia metropolitan area through an administrative office, four full service branch offices, a limited service branch office, a mortgage center and a loan origination office. The Bank’s primary market area includes Montgomery, Bucks and Philadelphia counties in Pennsylvania. A map of the Bank’s office locations is provided in Exhibit I-1. HV Bank is a member of the Federal Home Loan Bank (“FHLB”) system and its deposits are insured up to the maximum allowable amount by the Federal Deposit Insurance Corporation (“FDIC”). As of June 30, 2016, HV Bank had total assets of $182.0 million, total deposits of $141.8 million and total equity of $13.0 million, equal to 7.13% of total assets. The Bank’s audited financial statements are incorporated by reference as Exhibit I-2.

Plan of Conversion

On July 20, 2016, the Board of Trustees of the Bank adopted a plan of conversion, incorporated herein by reference, in which the Bank will convert from a Pennsylvania mutual savings bank to a Pennsylvania stock bank and become a wholly-owned subsidiary of HV Bancorp, Inc. (“HV Bancorp” or the “Company”), a newly formed Pennsylvania corporation.

HV Bancorp will offer its common stock in a subscription offering to Eligible Account Holders, Tax-Qualified Employee Stock Benefit Plans including HV Bank’s employee stock ownership plan (the “ESOP”), Supplemental Eligible Account Holders and Other Members, as such terms are defined for purposes of applicable federal regulatory guidelines governing mutual-to-stock conversions. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to members of the general public in a community offering and/or a syndicated community offering. A portion of the net proceeds received from the sale of the common stock will be used to purchase all of the then to be issued and outstanding capital stock of HV Bank and the balance of the net proceeds will be retained by the Company.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.2

At this time, no other activities are contemplated for the Company other than the ownership of the Bank, funding a loan to the newly-formed ESOP and reinvestment of the proceeds that are retained by the Company. In the future, HV Bancorp may acquire or organize other operating subsidiaries, diversify into other banking-related activities, pay dividends or repurchase its stock, although there are no specific plans to undertake such activities at the present time.

Strategic Overview

HV Bank maintains a local community banking emphasis, with a primary strategic objective of meeting the borrowing and savings needs of its local customer base. Mortgage banking, which is largely an off-balance sheet activity, constitutes a significant component of the Bank’s operations. Beyond its mortgage banking activities, HV Bank’s operating strategy has been fairly reflective of a traditional thrift operating strategy in which 1-4 family residential mortgage loans and retail deposits have constituted the principal components of the Bank’s assets and liabilities, respectively. Lending diversification by the Bank has emphasized the origination of commercial real estate loans and home equity loans and lines of credit. On a more limited basis, lending diversification by the Bank includes commercial business loans, construction loans and consumer loans. The Bank’s lending activities are supplemented with investments in securities, which comprise a less significant component of the Bank’s interest-earning asset composition. Mortgage-backed securities and municipal bonds comprise the largest components of the Bank’s current holdings of investment securities. Assets are primarily funded by retail deposits generated through the branch network, with supplemental funding provided by borrowings as an alternative funding source for purposes of funding loans held for sale, as well as for managing funding costs and interest rate risk.

The Bank’s lending markets were adversely impacted by the 2008 national recession and the resulting fallout from the financial crisis that occurred with the implosion of the housing market, pursuant to which the Bank experienced credit quality deterioration. Over the past five fiscal years, the Bank’s balance of non-performing assets peaked at $4.3 million or 2.74% of assets at fiscal yearend 2012. Since fiscal yearend 2012, the balance of non-performing assets has trended steadily lower to equal $1.3 million or 0.69% of assets at June 30, 2016.

Pursuant to the Bank’s mortgage banking activities, non-interest operating income and operating expenses are maintained at relatively high levels as a percent of assets and have a significant impact on the Bank’s earnings. Operating expenses and non-interest operating income have been increasing as a percent of average assets, which has been largely related to the growing

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.3

influence of the Bank’s mortgage banking activities on earnings. The Bank has maintained a relative stable net interest margin in recent years, in which the decline in the average yield on interest-earning assets has been fairly comparable to the decline in the average rate paid on interest-bearing liabilities. Overall, the Bank’s operating strategies have effectively reduced problem assets and improved core profitability. Growth in core earnings has been driven by the mortgage banking operation, which is viewed as a more volatile source of core earnings relative to earnings derived from the Bank’s retail and commercial banking operations.

The post-offering business plan of the Bank is expected to remain consistent with current strategic objectives. Specifically, HV Bank will continue to be an independent community-oriented financial institution with a commitment to local real estate financing with operations funded primarily by retail deposits. Growth strategies will continue to be implemented within the context of managing the Bank’s exposure to credit risk and interest rate risk.

The Bank’s Board of Directors has elected to complete a public stock offering to improve the competitive position of HV Bank. The capital realized from the stock offering will increase the Bank’s operating flexibility and allow for implementation of desired growth strategies. The additional funds realized from the stock offering will provide an alternative funding source to deposits and borrowings in meeting the Bank’s future funding needs, which may facilitate a reduction in HV Bank’s funding costs. Additionally, HV Bank’s higher equity-to-assets ratio will also better position the Bank to pursue expansion opportunities. Such expansion would most likely occur through the establishment or acquisition of additional banking offices. The Bank will also be in a better position to pursue growth through acquisition of other financial service providers following the stock offering, given its strengthened capital position and ability to offer its common stock as consideration .At this time, the Bank has no specific plans for expansion. The projected uses of proceeds are highlighted below.

| • | HV Bancorp, Inc. The Company is expected to retain up to 50% of the net offering proceeds. At present, funds at the Company level, net of the loan to the ESOP, are expected to be primarily invested initially into liquid funds held as a deposit at the Bank. Over time, the funds may be utilized for various corporate purposes, possibly including infusing additional equity into the Bank, repurchases of common stock and the payment of cash dividends. |

| • | HV Bank. Approximately 50% of the net stock proceeds will be infused into the Bank in exchange for all of the Bank’s stock. Cash proceeds (i.e., net proceeds less deposits withdrawn to fund stock purchases) infused into the Bank are anticipated to become part of general operating funds and are expected to be primarily utilized to fund loan growth over time. |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.4

Overall, it is the Bank’s objective to pursue growth that will serve to increase returns, while, at the same time, growth will not be pursued that could potentially compromise the overall risk associated with HV Bank’s operations.

Balance Sheet Trends

Table 1.1 shows the Bank’s historical balance sheet data for the past five fiscal years. From fiscal yearend 2012 through fiscal yearend 2016, HV Bank’s assets increased at a 3.95% annual rate. Asset growth during the period was largely due to loan growth, which was partially offset by a decline in investment securities. A combination of deposit growth and additional borrowings funded the Bank’s asset growth. A summary of HV Bank’s key operating ratios is presented in Exhibit I-3.

HV Bank’s loans receivable portfolio increased at a 7.64% annual rate from fiscal yearend 2012 through fiscal yearend 2016. The loans receivable portfolio showed a consistent upward trend since fiscal yearend 2012. The Bank’s higher loan growth rate compared to its asset growth rate provided for an increase in the loans-to-assets ratio from 44.65% at fiscal yearend 2012 to 51.34% at fiscal yearend 2016 Net loans receivable at June 30, 2016 totaled $93.5 million, versus $69.6 million at June 30, 2012. Additionally, loans held for sale, which consist of originations of 1-4 family permanent mortgage loans, fluctuated from a low of $9.3 million or 6.06% of assets at fiscal yearend 2013 to a high of $24.7 million or 13.56% of assets at fiscal yearend 2016.

Trends in the Bank’s loan portfolio composition over the past two fiscal years show that the concentration of residential mortgage loans comprising total loans receivable increased slightly from 75.70% at fiscal yearend 2015 to 76.75% at fiscal yearend 2016. The increase in the concentration of residential mortgage loans was primarily due to growth of the residential mortgage loan portfolio and, to a lesser extent, decreases in all other loan types with the exception of construction loans. Commercial real estate loans and home equity loans and lines of credit constitute the primary types of lending diversification for the Bank, with both of those areas of lending diversification showing a decline in loans outstanding during fiscal year 2016. From fiscal yearend 2015 to fiscal yearend 2016, commercial real estate loans decreased from 15.11% of total loans to 12.39% of total loans and home equity loans and lines of credit decreased from 7.95% of total loans to 6.87% of total loans. Other areas of lending diversification for the Bank have been fairly limited over the past five fiscal years, consisting of residential construction loans, commercial business loans and other consumer loans. As of June 30, 2016, construction loans equaled 3.39% of total loans, commercial business loans equaled 0.59% of total loans and other consumer loans equaled 0.01% of total loans.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.5

Table 1.1

Huntingdon Valley Bank

Historical Balance Sheet Data

| 6/30/12- 6/30/16 Annual. Growth Rate |

||||||||||||||||||||||||||||||||||||||||||||

| At June 30, | ||||||||||||||||||||||||||||||||||||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Pct | ||||||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | (%) | ||||||||||||||||||||||||||||||||||

| Total Amount of: |

||||||||||||||||||||||||||||||||||||||||||||

| Assets |

$ | 155,914 | 100.00 | % | $ | 153,373 | 100.00 | % | $ | 165,894 | 100.00 | % | $ | 167,298 | 100.00 | % | $ | 182,023 | 100.00 | % | 3.95 | % | ||||||||||||||||||||||

| Cash and cash equivalents |

11,261 | 7.22 | % | 7,073 | 4.61 | % | 15,309 | 9.23 | % | 15,596 | 9.32 | % | 15,427 | 8.48 | % | 8.19 | % | |||||||||||||||||||||||||||

| Investment securities |

48,860 | 31.34 | % | 51,807 | 33.78 | % | 43,425 | 26.18 | % | 42,832 | 25.60 | % | 39,106 | 21.48 | % | -5.41 | % | |||||||||||||||||||||||||||

| Loans held for sale |

16,393 | 10.51 | % | 9,293 | 6.06 | % | 16,375 | 9.87 | % | 16,261 | 9.72 | % | 24,676 | 13.56 | % | 10.77 | % | |||||||||||||||||||||||||||

| Loans receivable, net |

69,614 | 44.65 | % | 74,572 | 48.62 | % | 81,085 | 48.88 | % | 83,319 | 49.80 | % | 93,450 | 51.34 | % | 7.64 | % | |||||||||||||||||||||||||||

| FHLB stock |

761 | 0.49 | % | 779 | 0.51 | % | 871 | 0.53 | % | 627 | 0.37 | % | 1,108 | 0.61 | % | 9.85 | % | |||||||||||||||||||||||||||

| Bank-owned life insurance |

3,443 | 2.21 | % | 3,559 | 2.32 | % | 3,672 | 2.21 | % | 3,783 | 2.26 | % | 3,895 | 2.14 | % | 3.13 | % | |||||||||||||||||||||||||||

| Real estate owned |

1,824 | 1.17 | % | 2,199 | 1.43 | % | 431 | 0.26 | % | 574 | 0.34 | % | 115 | 0.06 | % | -49.89 | % | |||||||||||||||||||||||||||

| Deposits |

$ | 133,717 | 85.76 | % | $ | 133,540 | 87.07 | % | $ | 139,340 | 83.99 | % | $ | 142,877 | 85.40 | % | $ | 141,771 | 77.89 | % | 1.47 | % | ||||||||||||||||||||||

| Borrowings |

8,204 | 5.26 | % | 7,031 | 4.58 | % | 13,618 | 8.21 | % | 10,502 | 6.28 | % | 23,929 | 13.15 | % | 30.68 | % | |||||||||||||||||||||||||||

| Equity |

$ | 11,628 | 7.46 | % | $ | 10,566 | 6.89 | % | $ | 10,721 | 6.46 | % | $ | 11,456 | 6.85 | % | $ | 12,971 | 7.13 | % | 2.77 | % | ||||||||||||||||||||||

| Loans/Deposits |

52.06 | % | 55.84 | % | 58.19 | % | 58.32 | % | 65.92 | % | ||||||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of ending assets. |

Sources: HV Bank’s prospectus, audited financial statements and RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.6

The intent of the Bank’s investment policy is to provide adequate liquidity and to generate a favorable return within the context of supporting HV Bank’s overall credit and interest rate risk objectives. The Bank has maintained a higher level of cash and cash equivalents during the past three fiscal years for purposes of managing interest rate exposure, during a period when interest rates have been at historical lows. Over the past five fiscal years, the Bank’s level of cash and investment securities (inclusive of FHLB/ACBB stock) ranged from a low of 30.61% of assets at fiscal yearend 2015 to a high of 39.05% of assets at fiscal yearend 2012. The Bank maintained total cash and investments of $55.6 million or 30.56% of assets at June 30, 2016.

Mortgage-backed securities have comprised the largest concentration of the Bank’s investment holdings over the past five fiscal years and are generally purchased as a means to deploy excess liquidity at more favorable yields than other investment alternatives that are consistent with HV Bank’s investment philosophy. Mortgage-backed securities held by HV Bank consist of securities that are guaranteed or insured by government sponsored enterprises (“GSEs”). As of June 30, 2016, the mortgage-backed securities portfolio totaled $16.8 million and the entire portfolio was maintained as available for sale. Other investment securities held by the Bank at June 30, 2016 consisted of $9.4 million of municipal bonds, $1.5 million of U.S. Government agency securities, $8.3 million of corporate notes and $3.0 million of certificates of deposit (“CDs”) held in other financial institutions. With the exception of $5.8 million of municipal bonds, all investments were maintained as available for sale at June 30, 2016. As of June 30, 2016, investment securities maintained as available for sale had a net unrealized loss of $12,000. Exhibit I-4 provides detail of the Bank’s investment portfolio, as of fiscal yearend 2015 and fiscal yearend 2016. As of June 30, 2016, the Bank also held $1.1 million of FHLB/ACBB stock equal to 0.61% of assets and $15.4 million of cash and cash equivalents equal to 8.48% of assets.

The Bank also maintains an investment in bank-owned life insurance (“BOLI”) policies, which cover the lives of some of the Bank’s current and former officers. The purpose of the investment is to provide funding for the Bank’s benefit plans. As of June 30, 2016, the cash surrender value of the Bank’s BOLI equaled $3.9 million or 2.14% of assets.

Over the past five fiscal years, HV Bank’s funding needs have been addressed through a combination of deposits, borrowings and internal cash flows. From fiscal yearend 2012 through fiscal yearend 2016, the Bank’s deposits increased at a 1.47% annual rate. The Bank recorded

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.7

deposit growth in fiscal years 2014 and 2015, while deposits declined slightly during fiscal years 2013 and 2016. Overall, total deposits increased from $133.7 million or 85.76% of assets at fiscal yearend 2012 to $141.8 million or 77.89% of assets at fiscal yearend 2016. Transaction and savings account deposits constitute the largest concentration of the Bank’s deposits.

Borrowings serve as an alternative funding source for the Bank to address funding needs and to support management of deposit costs and interest rate risk. From fiscal yearend 2012 through fiscal yearend 2016, borrowings ranged from a low of $7.0 million or 4.58% of assets at fiscal yearend 2013 to a high of $23.9 million or 13.15% of assets at fiscal yearend 2016. Most of the increase in borrowings during fiscal year 2016 was related to funding an increase in the balance of loans held for sale at fiscal yearend 2016. As of June 30, 2016, borrowings held by the Bank consisted of $20.0 million of FHLB advances and $3.9 million of overnight repurchase agreements.

The Bank’s equity increased at a 2.77% annual rate from fiscal yearend 2012 through fiscal yearend 2016, which was mostly attributable to retention of earnings. A slightly lower rate of capital growth relative to asset growth provided for a slightly decline the Bank’s equity-to-assets ratio from 7.46% at fiscal yearend 2012 to 7.13% at fiscal yearend 2016. All of the Bank’s capital is tangible capital and HV Bank maintained capital surpluses relative to all of its regulatory capital requirements at June 30, 2016. The addition of stock proceeds will serve to strengthen the Bank’s capital position, as well as support growth opportunities. At the same time, HV Bank’s ROE will initially be depressed following its stock conversion as the Bank’s pro forma capital position will be significantly higher following the infusion of net stock proceeds into capital.

Income and Expense Trends

Table 1.2 shows the Bank’s historical income statements for the past five fiscal years. The Bank’s reported earnings over the past five fiscal years ranged from a net loss of $123,000 or 0.08% of average assets during fiscal 2014 to net income of $1.0 million or 0.62% of average assets during fiscal 2016. Currently, revenues derived from sources of non-interest operating income are a more significant contributor to the Bank’s earnings relative to net interest income, which is attributable to the revenues generated from the Bank’s mortgage banking operations. Also as the result of the significance of the significance of the Bank’s mortgage banking activities relative to its asset size, the Bank’s operating expense ratios as a percent of average assets have been maintained at relatively high levels as well. Loan loss provisions and non-operating income and losses have had a varied impact on the Bank’s earnings over the past five fiscal years.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.8

Table 1.2

Huntingdon Valley Bank

Historical Income Statements

| For the Fiscal Year Ended June 30, | ||||||||||||||||||||||||||||||||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | |||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | |||||||||||||||||||||||||||||||

| Interest income |

$ | 5,545 | 3.66 | % | $ | 4,994 | 3.21 | % | $ | 5,123 | 3.21 | % | $ | 5,057 | 3.02 | % | $ | 5,302 | 3.19 | % | ||||||||||||||||||||

| Interest expense |

(1,211 | ) | -0.80 | % | (982 | ) | -0.63 | % | (839 | ) | -0.53 | % | (785 | ) | -0.47 | % | (746 | ) | -0.45 | % | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net interest income |

$ | 4,334 | 2.86 | % | $ | 4,012 | 2.58 | % | $ | 4,284 | 2.68 | % | $ | 4,272 | 2.55 | % | $ | 4,556 | 2.74 | % | ||||||||||||||||||||

| Provision for loan losses |

(178 | ) | -0.12 | % | (120 | ) | -0.08 | % | (246 | ) | -0.15 | % | (79 | ) | -0.05 | % | (9 | ) | -0.01 | % | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net interest income after provisions |

$ | 4,156 | 2.74 | % | $ | 3,892 | 2.50 | % | $ | 4,038 | 2.53 | % | $ | 4,193 | 2.50 | % | $ | 4,547 | 2.73 | % | ||||||||||||||||||||

| Mortgage banking gains/Gain on sale of loans |

$ | 1,774 | 1.17 | % | $ | 1,686 | 1.08 | % | $ | 2,204 | 1.38 | % | $ | 4,519 | 2.70 | % | $ | 5,004 | 3.01 | % | ||||||||||||||||||||

| Other non-interest operating income |

417 | 0.28 | % | 409 | 0.26 | % | 333 | 0.21 | % | 381 | 0.23 | % | 333 | 0.20 | % | |||||||||||||||||||||||||

| Operating expense |

(6,073 | ) | -4.01 | % | (6,498 | ) | -4.17 | % | (6,616 | ) | -4.14 | % | (7,485 | ) | -4.47 | % | (8,354 | ) | -5.02 | % | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net operating income |

$ | 274 | 0.18 | % | ($ | 511 | ) | -0.33 | % | ($ | 41 | ) | -0.03 | % | $ | 1,608 | 0.96 | % | $ | 1,530 | 0.92 | % | ||||||||||||||||||

| Non-Operating Income/(Losses) |

||||||||||||||||||||||||||||||||||||||||

| Gain (loss) on sale of securities |

$ | 528 | 0.35 | % | $ | 592 | 0.38 | % | $ | 6 | 0.00 | % | $ | 9 | 0.01 | % | $ | 21 | 0.01 | % | ||||||||||||||||||||

| Merger and conversion costs |

— | 0.00 | % | — | 0.00 | % | (186 | ) | -0.12 | % | (854 | ) | -0.51 | % | — | 0.00 | % | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net non-operating income (loss) |

$ | 528 | 0.35 | % | $ | 592 | 0.38 | % | ($ | 180 | ) | -0.11 | % | ($ | 845 | ) | -0.50 | % | $ | 21 | 0.01 | % | ||||||||||||||||||

| Net income before tax |

$ | 802 | 0.53 | % | $ | 81 | 0.05 | % | ($ | 221 | ) | -0.14 | % | $ | 763 | 0.46 | % | $ | 1,551 | 0.93 | % | |||||||||||||||||||

| Income tax provision |

110 | 0.07 | % | 42 | 0.03 | % | 98 | 0.06 | % | (135 | ) | -0.08 | % | (525 | ) | -0.32 | % | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net income (loss) |

$ | 912 | 0.60 | % | $ | 123 | 0.08 | % | ($ | 123 | ) | -0.08 | % | $ | 628 | 0.38 | % | $ | 1,026 | 0.62 | % | |||||||||||||||||||

| Adjusted Earnings |

||||||||||||||||||||||||||||||||||||||||

| Net income |

$ | 912 | 0.60 | % | $ | 123 | 0.08 | % | ($ | 123 | ) | -0.08 | % | $ | 628 | 0.38 | % | $ | 1,026 | 0.62 | % | |||||||||||||||||||

| Add (Deduct): Non-operating income |

(528 | ) | -0.35 | % | (592 | ) | -0.38 | % | 180 | 0.11 | % | 845 | 0.50 | % | (21 | ) | -0.01 | % | ||||||||||||||||||||||

| Tax effect (2) |

211 | 0.14 | % | 237 | 0.15 | % | (72 | ) | -0.05 | % | (338 | ) | -0.20 | % | 8 | 0.01 | % | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Adjusted earnings |

$ | 595 | 0.39 | % | ($ | 232 | ) | -0.15 | % | ($ | 15 | ) | -0.01 | % | $ | 1,135 | 0.68 | % | $ | 1,013 | 0.61 | % | ||||||||||||||||||

| Expense Coverage Ratio (3) |

0.71 | x | 0.62 | x | 0.65 | x | 0.57 | x | 0.55 | x | ||||||||||||||||||||||||||||||

| Efficiency Ratio (4) |

93.04 | % | 106.38 | % | 96.96 | % | 81.57 | % | 84.37 | % | ||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of average assets. |

| (2) | Assumes a 40.0% effective tax rate. |

| (3) | Expense coverage ratio calculated as net interest income before provisions for loan losses divided by operating expenses. |

| (4) | Efficiency ratio calculated as operating expenses divided by the sum of net interest income before provisions for loan losses plus non-interest operating income. |

Sources: HV Bank’s prospectus, audited financial statements and RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.9

Over the past five fiscal years, the Bank’s net interest income to average assets ratio ranged from a low of 2.55% during fiscal 2015 to a high of 2.86% during fiscal 2012. For 2016, the Bank’s net interest income to average assets ratio equaled 2.74%. The decline in the Bank’s net interest income ratio since fiscal 2012 has been largely attributable to interest rate spread compression that has resulted from a more significant decrease in the yield earned on interest-earnings assets relative to the cost of interest-bearing liabilities. As the result of the prolonged low interest rate environment, the decline in yield earned on less rate sensitive interest-earning assets became more significant relative to the decline in rate paid on more rate sensitive liabilities. While the prolonged low interest rate environment and relatively flat yield curve has resulted in interest rate spread compress for financial institutions in general, a shift in the Bank’s interest-earning asset composition towards a higher concentration of loans has facilitated maintenance of a relatively stable net interest margin over the past five fiscal years. The increase in the Bank’s net interest income ratio during fiscal 2016 was attributable to a wider yield-cost spread, which increased from 2.65% during fiscal 2015 to 2.85% during fiscal 2016. An increase in yield earned on interest-earning assets drove the increase in the Bank’s yield-cost spread during fiscal 2016, as the concentration of loans comprising interest-earning assets increased during fiscal 2016. The Bank’s net interest rate spreads and yields and costs for the past two fiscal years are set forth in Exhibit I-3 and Exhibit I-5.

Non-interest operating income has been a significant and growing contributor to the Bank’s earnings, which has been largely driven by increases in gains on sales of loans and other mortgage banking related gains (gain from hedging instruments and change in fair value of loans held-for-sale). Beyond the mortgage banking related gains, revenues derived from sources of non-interest operating income have been somewhat of a limited contributor to the Bank’s earnings. Throughout the period shown in Table 1.2, sources of non-interest operating income ranged from a low of $2.1 million or 1.34% of average assets during fiscal 2013 to a high of $5.3 million or 3.21% of average assets during fiscal 2016. Mortgage banking related gains accounted for 93.8% of the Bank’s non-interest operating income during fiscal 2016. Other than mortgage banking related gains, customer service fees and earnings on BOLI constitute the largest sources of non-interest operating income for the Bank.

Operating expenses represent the other major component of the Bank’s earnings, ranging from a low of $6.1 million or 4.01% of average assets during fiscal 2012 to a high of $8.4 million or 5.02% of average assets during fiscal 2016. Consistent with the Bank’s relatively high levels of non-interest operating income, the Bank’s relatively high operating expense ratios are largely attributable to the significance of its mortgage banking operation relative to its asset size.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.10

Overall, the general trends in the Bank’s ratios for net interest income, non-interest operating income and operating expenses since fiscal 2012 reflect an increase in core earnings, as indicated by the Bank’s efficiency ratio efficiency ratio (operating expenses as a percent of the sum of net interest income and non-interest operating income). HV Bank’s efficiency ratio improved from 93.04% during fiscal 2012 to 84.37% during fiscal 2016. The improvement in the Bank’s efficiency ratio was the result of an increase in the non-interest operating income ratio, which was partially offset by a decrease in the net interest income ratio and an increase in the operating expense ratio.

During the period covered in Table 1.2, loan loss provisions had a varied impact on the Bank’s earnings with the amount of loan loss provisions established becoming a less significant earnings factor during recent periods. Over the past five fiscal years, loan loss provisions established by the Bank ranged from a low of $9,000 or 0.01% of average assets during fiscal 2016 to a high of $246,000 or 0.15% of average asset during fiscal 2014. As of June 30, 2016, the Bank maintained valuation allowances of $487,000, equal to 0.52% of loans receivable and 42.53% of non-accruing loans. Exhibit I-6 sets forth the Bank’s loan loss allowance activity for the past two fiscal years.

Non-operating income and losses over the past five fiscal years have primarily consisted of gains on the sale of securities. Additionally, during fiscal years 2014 and 2015, the Bank recorded non-recurring losses related to the write-off of merger and conversion expenses. Overall, net non-operating income and losses ranged from a net loss of $845,000 or 0.50% of average assets during fiscal year 2015 to net non-operating income of $592,000 or 0.38% of average assets during fiscal year 2013. For fiscal year 2016 the Bank recorded non-operating income of $21,000 or 0.01% of average assets, which consisted entirely of gains on the sale of securities. Overall, the various items that comprise the Bank’s non-operating income and losses are not viewed to be part of the Bank’s core or recurring earnings base.

The Bank’s effective tax rate ranged from 33.85% during fiscal 2016 to a tax benefit of 51.85% during fiscal 2013. The Bank’s effective marginal tax rate on a fully taxable instrument approximates 40%.

Interest Rate Risk Management

The Bank’s balance sheet is liability-sensitive in the short-term (less than one year) and, thus, Economic Value of Equity (“EVE”) would decrease during periods of rising and higher interest rates. Comparatively, the Bank’s net interest income would increase during periods of rising interest

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.11

rates. As of June 30, 2016, an analysis of the Bank’s EVE and net interest income indicated that a 2.0% instantaneous and sustained parallel increase in the yield curve would result in an 11.99% decline in EVE and an 8.46% increase in net interest income over a one year period (see Exhibit I-7).

The Bank pursues a number of strategies to manage interest rate risk, particularly with respect to seeking to limit the repricing mismatch between interest rate sensitive assets and liabilities. The Bank manages interest rate risk from the asset side of the balance sheet through selling originations of 1-4 family fixed rate loans, retaining originations of ARM loans for its own portfolio, diversifying into other types of lending beyond 1-4 family permanent mortgage loans which consist primarily of shorter term fixed rate loans, maintaining most investments as available for sale and maintaining a relatively high level of liquidity in the prevailing low interest rate environment. As of June 30, 2016, of the Bank’s total loans due after June 30, 2017, ARM loans comprised 26.0% of those loans (see Exhibit I-8). The Bank also recently restructured the investment portfolio, in which the Bank invested in securities with shorter term maturities and durations. On the liability side of the balance sheet, management of interest rate risk has been pursued through increasing the concentration of lower cost and less interest rate sensitive transaction and savings account deposits comprising total deposits.

The infusion of stock proceeds will serve to further limit the Bank’s interest rate risk exposure, as most of the net proceeds will be redeployed into interest-earning assets and the increase in the Bank’s capital position will lessen the proportion of interest rate sensitive liabilities funding assets.

Lending Activities and Strategy

HV Bank’s lending activities have traditionally emphasized 1-4 family permanent mortgage loans and such loans continue to comprise the largest portion of the Bank’s loan portfolio. Beyond 1-4 family loans, lending diversification by the Bank has emphasized commercial real estate loans and home equity loans and lines of credit. Pursuant to the Bank’s strategic plan, the Bank is pursuing a diversified lending strategy emphasizing commercial real estate loans as the primary area of targeted loan growth. On a more limited basis, other areas of lending diversification for the Bank include commercial business loans, residential construction loans and other consumer loans. Exhibit I-9 provides historical detail of HV Bank’s loan portfolio composition for the past two fiscal years and Exhibit I-10 provides the contractual maturity of the Bank’s loan portfolio by loan type as of June 30, 2016.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.12

1-4 Family Residential Loans. HV Bank’s residential lending activities are conducted through its mortgage banking operations, in which the large majority of residential mortgage originations are sold to the secondary market on a servicing released basis. Fixed rate loans that do not meet secondary market standards and ARM loans are retained in the loans receivable portfolio. ARM loans generally have fixed rates for initial terms of five or seven years and adjust annually thereafter at a margin indexed to the one year LIBOR. The retained fixed rate loans generally do not have materially higher risk characteristics, but are not saleable for minor underwriting or loan characteristic reasons. The Bank generally limits the loan-to-value (“LTV”) ratio on 1-4 family residential without private mortgage insurance to 80%. As of June 30, 2016, the Bank’s outstanding balance of 1-4 family loans (excluding loans held for sale) equaled $72.0 million or 76.75% of total loans receivable.

Construction Loans. The Bank’s construction lending activities consist of financing for the purchase of developed lots and for the construction of single-family residences, which are extended to individuals for the construction and permanent financing of their personal residences. Construction loans to individuals are made on the same general terms as the Bank’s 1-4 family loans, but provide for the payment of interest only during the construction phase which is typically six months. At the end of the construction phase, the loan converts to a permanent mortgage loan. As of June 30, 2016, the Bank’s outstanding balance of construction loans equaled $3.2 million or 3.39% of total loans receivable.

Home Equity Loans and Lines of Credit. The Bank’s 1-4 family lending activities include home equity loans and lines of credit. Home equity loans are offered as fixed rate amortizing loans for terms of up to 20 years, while home equity lines of credit have a floating rate tied to the prime rate and generally have 30 year terms. The Bank will originate home equity loans and lines of credit up to a LTV ratio of 80% inclusive of other liens on the property. As of June 30, 2016, the Bank’s outstanding balance of home equity loans and lines of credit equaled $6.4 million or 6.87% of total loans receivable.

Commercial Real Estate Loans. The balance of the mortgage loan portfolio consists of commercial real estate loans, which are collateralized by properties in the Bank’s regional lending area. Commercial real estate loans are originated up to a LTV ratio of 80% and require a minimum debt-coverage ratio of 1.25 times. Commercial real estate loans are generally extended as five

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.13

year balloon loans with amortization terms of up to 25 years. The Bank’s commercial real estate loans are typically secured by medical, retail, industrial, warehouse, service, apartments or other commercial properties. The largest commercial real estate loan in the Bank’s loan portfolio at June 30, 2016 was a $1.3 million loan secured by a medical office, which was performing in accordance with its original terms at June 30, 2016. As of June 30, 2016, the Bank’s outstanding balance of commercial real estate loans totaled $11.6 million or 12.39% of total loans receivable.

Commercial real estate lending is a desired area of loan growth for the Bank, pursuant to which the Bank is seeking to become a full service community bank to its commercial loan customers through offering a full range of commercial loan products that can be packaged with lower cost commercial deposit products. The Bank’s plan is to focus on lending to small businesses located in its market area, targeting owner occupied businesses such as professional service providers. The Bank recently hired an experienced commercial loan officer with commercial lending relationships in the Bank’s market area to lead this initiative. The Bank intends to enter into a consulting agreement with another local financial institution in order to create a partnership where the Bank can sell to the other financial institution a participation interest in commercial real estate loans originated by the Bank so as to limit the Bank’s risk as it grows its portfolio of commercial real estate loans. The commercial real estate loans would have to comply with both the Bank’s and the other financial institution’s underwriting policies.

Commercial Business Loans. The commercial business loan portfolio is generated through extending loans to small businesses operating in the Bank’s local market area. Commercial business loans offered by the Bank consist of regular lines of credit and revolving lines of credit with terms up to twelve months to finance short-term working capital needs such as accounts receivable and inventory. As of December 31, 2016, the Bank’s outstanding balance of commercial business loans equaled $558,000 or 0.59% of total loans receivable.

Other Consumer Loans. Consumer loans other than home equity loans and line of credit is largely an inactive area of lending diversification for the Bank. As of June 30, 2016, the Bank held $10,000 of other consumer loans or 0.01% of total loans receivable.

Exhibit I-11 provides a summary of the Bank’s lending activities over the past two fiscal years. Total loans originated increased from $174.3 million during fiscal year 2015 to $190.1 million during fiscal year 2016. The increase in loans originated during fiscal year 2016 was substantially driven by an increase in originations of 1-family loans, with such originations increasing from $171.1 million during fiscal year 2015 to $183.0 million during fiscal year 2016. Other areas of lending

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.14

activity were comparatively modest during the past two fiscal years, consisting of originations of home equity loans and lines of credit, commercial real estate loans, construction loans and a nominal amount of consumer loans. Originations of loans other than 1-4 family loans increased from $3.2 million during fiscal year 2015 to $7.2 million during fiscal year 2016, which was due to increased originations of home equity loans and lines of credit and construction loans. Comparatively, commercial real estate loan originations declined during fiscal year 2016. Loans sold decreased from $159.5 million during fiscal year 2015 to $157.8 million during fiscal year 2016, while loan repayments increased from $13.0 million during fiscal year 2015 to $13.9 million during fiscal year 2016. Overall, total loans, including loans held for sale, increased by $18.4 million during fiscal year 2016 to total $118.5 million at June 30, 2016.

Asset Quality

Historically, the Bank’s lending emphasis on lending in local and familiar markets generally supported maintenance of relatively favorable credit quality measures. However, following the national recession and bursting of the housing bubble in 2008, the Bank experienced elevated levels of problems assets. Over the past two fiscal years, HV Bank’s balance of non-performing assets ranged from a high of $2.2 million or 1.33% of assets at fiscal yearend 2015 to a low of $1.3 million or 0.69% of assets at fiscal yearend 2016. As shown in Exhibit I-12, non-performing assets at June 30, 2016 consisted of $1.1 million of non-accruing loans and $115,000 of real estate owned. Non-accruing loans held by the Bank at June 30, 2106 were concentrated in 1-4 family permanent mortgage loans totaling $818,000.

To track the Bank’s asset quality and the adequacy of valuation allowances, the Bank has established detailed asset classification policies and procedures which are consistent with regulatory guidelines. Classified assets are reviewed monthly by senior management and quarterly by the Board. Pursuant to these procedures, when needed, the Bank establishes additional valuation allowances to cover anticipated losses in classified or non-classified assets. As of June 30, 2016, the Bank maintained loan loss allowances of $487,000, equal to 0.52% of total loans receivable and 42.53% of non-performing loans.

Funding Composition and Strategy

Deposits have consistently served as the Bank’s primary funding source and at June 30, 2016 deposits accounted for 85.56% of HV Bank’s combined balance of deposits and borrowings.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

I.15

Exhibit I-13 sets forth the Bank’s deposit composition for the past two fiscal years. Transaction and savings account deposits comprised 71.09%% of average total deposits during fiscal year 2016, as compared to 68.11% of average total deposits during fiscal year 2015. The increase in the concentration of core deposits comprising total deposits during fiscal year 2016 was realized through a decrease in CDs. Savings account deposits comprised the largest concentration of the Bank’s core deposits during fiscal year 2016, equaling 25.17% of average total deposits and 36.19% of average core deposits.

The balance of the Bank’s deposits consists of CDs, which equaled 28.91% of average total deposits during fiscal year 2016 compared to 31.89% of average total deposits during fiscal year 2015. As of June 30, 2016, jumbo CDs (CD accounts with balances of $100,000 or more) amounted to $18.5 million or 49.37% of total CDs and $12.3 million or 66.47% were scheduled to mature in one year or less. Exhibit I-14 sets forth the maturity schedule of the Bank’s jumbo CDs as of June 30, 2016. The Bank did not maintain any brokered CDs at June 30, 2016.

Borrowings serve as an alternative funding source for the Bank to facilitate management of funding costs and interest rate risk. Borrowings utilized by the Bank consist of FHLB advances and overnight repurchase agreements. As of June 30, 2016, the Bank’s borrowings consisted of $20.0 million of FHLB advances and $3.9 million of overnight repurchase agreements. The FHLB advances have scheduled maturities through June 2019. At June 30, 2016, the weighted average interest rate on the FHLB advances equaled 0.86% and the weighted average interest rate on the repurchase agreements equaled 0.08%. Exhibit I-15 provides further detail of the Bank’s borrowings during the past two fiscal years.

Legal Proceedings

The Bank is not currently party to any pending legal proceedings that the Bank’s management believes would have a material adverse effect on the Bank’s financial condition, results of operations or cash flows.

| RP® Financial, LC. | MARKET AREA ANALYSIS |

II.1

II. MARKET AREA ANALYSIS

Introduction

HV Bank serves the Philadelphia metropolitan area through four full service branches and a limited service branch, which serve the counties of Montgomery, Buck and Philadelphia. All of the branch offices, with the exception of the Philadelphia limited service branch, are located north of the city of Philadelphia. Exhibit II-1 provides information on the Bank’s office properties.

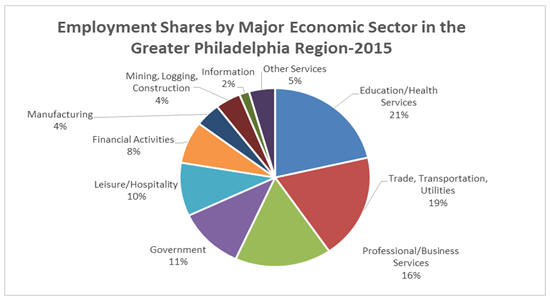

The Philadelphia MSA is the nation’s sixth largest metropolitan area in terms of total population, with a 2016 population of approximately 6.1 million. The three counties served by the Bank’s branches had a total population of approximately 3.0 million in 2016. The Greater Philadelphia area economy is typical of the cities in the northeast corridor, where the traditional manufacturing-based economy has diminished and the service sector has been the primary source of growth. Overall, the Philadelphia MSA maintains a fairly diversified economic base, as traditional employers in the manufacturing and financial services industry have been bolstered by growth in the life sciences and healthcare industries as well as the information technology and communication sectors.

Future growth opportunities for HV Bank depend on the future growth and stability of the local and regional economy, demographic growth trends, and the nature and intensity of the competitive environment. These factors have been briefly examined to help determine the growth potential that exists for the Bank, the relative economic health of the Bank’s market area, and the resultant impact on value.

National Economic Factors

The business potential of a financial institution is partially dependent on the future operating environment and growth opportunities for the banking industry and the economy as a whole. In assessing national economic trends over the past few quarters, manufacturing activity for January 2016 shrank for a fourth straight month with an index reading of 48.2. Comparatively, January service sector activity expanded at a slower rate with an index reading of 53.2. U.S. employers added 151,000 jobs in January, which was the weakest job growth since September 2015. However, the January unemployment rate fell to 4.9%. Retail sales increased 0.2% in January, while orders for durable goods surged 4.9% in January. Housing

| RP® Financial, LC. | MARKET AREA ANALYSIS |

II.2

data for January showed declines in housing starts and new home sales of 3.8% and 9.2%, respectively, while January existing home sales increased 0.4%. Pending home sales for January fell 2.5%, which was attributable to rising prices and lower inventory. Manufacturing activity for February contracted for a fifth straight month with an index reading of 49.5%, which was up slightly compared to January’s reading. February service sector activity expanded at a slightly higher rate with an index reading of 53.3. Job growth rebounded in February as U.S. employers added 242,000 jobs in February. The February unemployment rate held steady at 4.9%, although wages fell in February. February retail sales and orders for durable goods suggested a slowdown in the U.S. economy, based on respective declines of 0.1% and 2.8%. Comparatively, February housing data showed a pick-up in activity as housing starts rebounded with a 5.2% increase, new home sales rose 2.0% and pending home sales were up 3.5%. However, sales of existing homes dropped 7.1% in February. March job growth slowed slightly in March, as employers added 215,000 jobs in March. The March unemployment rate edged up to 5.0%, due to more Americans entering the labor force. Manufacturing activity for March expanded for the first time since August 2015, with an index reading of 51.8. Service sector activity for March also accelerated with an index reading of 54.5. March retail sales unexpectedly fell 0.3%, while durable-goods orders for March rose 0.8%. March housing data remained somewhat mixed, as existing and pending home sales rose 5.1% and 1.4%, respectively. Comparatively, new home sales dropped 1.5% in March. First quarter GDP increased at a 0.5% annual rate (subsequently revised up to 1.1%), which marked the economy’s worst performance in two years.

Manufacturing activity expanded for a second straight month in April 2016, but at a slightly slower pace with an index reading of 50.8%. April service sector activity recorded stronger growth, based on an index reading of 55.7. The U.S. economy added 160,000 jobs in April, which came in below expectations, and the April unemployment rate remained at 5.0%. Retail sales for April surged 1.3%, which was the highest level of retail sales in more than a year. Housing demand showed signs of firming up in April, as housing starts showed a healthy increase of 6.6%, existing home sales rose 1.7% and new home sales surged 16.6%. New home sales recorded for April was the strongest month since 2008 and the median home price for a new home rose to a record high of $321,000 in April. Other indications that the U.S. economy was gaining traction included a 1.0% increase in April consumer spending, which was the biggest one month jump since August 2009, and manufacturing activity expanded at a slightly faster pace in May with an index reading of 51.3. Comparatively, service sector activity

| RP® Financial, LC. | MARKET AREA ANALYSIS |

II.3

expanded a lower rate in May with an index reading of 52.9 and the May employment report suggested that the U.S. economy may be slowing. Employers added just 38,000 jobs in May, which was the fewest jobs added in more than five years. While the May unemployment rate dropped to 4.7%, which was the lowest unemployment rate since November 2007, the decrease was attributable to nearly a half-million jobless Americans stopped looking for work during May. Notwithstanding the weak job growth reported for May, retail sales showed a healthy increase of 0.5% in May. Housing starts declined 0.3% in May, suggesting the supply of new homes could have trouble keeping up with steady demand. Sales of new single-family homes declined 6.0% in May, versus a 1.8% increase in May existing home sales. Manufacturing activity expanded for a fourth consecutive month in June with a slightly higher index reading of 53.2. Service sector activity for June also accelerated in June with an index reading of 56.5, which was the highest reading since November 2015. June employment data eased fears about a downturn in the U.S. economy, as employers added a stronger-than-expected 287,000 jobs in June. The unemployment rate for June ticked up to 4.9%. June housing starts were up 4.8% compared to May. Home sales for June also pointed towards a healthy market for housing, with June existing and home sales showing increases of 1.1% and 3.5%, respectively. Second quarter GDP increased at a 1.2% annualized rate, which was less than forecasted and only slight above the first quarter growth rate of 0.8%. Manufacturing and service sector activity expanded at slightly lower rates in July 2016, with respective index readings of 52.6 and 55.5. The U.S. economy added a better-than-expected 255,000 jobs in July, while the July unemployment rate held steady at 4.9%.

In terms of interest rates trends over the past few quarters, long-term Treasury yields trended lower through the first three weeks of January 2016 with the yield on the 10-Treasury note approaching 2.0%. Data showing a slowing U.S. economy, falling commodity prices and investors moving into safe haven investments amid stock market volatility were factors contributing to long-term Treasury yields declining. The Federal Reserve held interest rates steady at its late-January meeting, expressing concerns about financial market turmoil and slow economic growth abroad. The decline in long-term Treasury yields accelerated in early-February, as investors moved into safe haven investments amid concern about the outlook for global economy that fueled a sell-off in global stock markets. Congressional testimony by the Federal Reserve Chairwoman signaling a cautious approach by the Federal Reserve for future interest rate increases pushed the 10-year Treasury yield to a one year low of 1.64% heading into mid-February. Long-term Treasury yields stabilized during the second half of February, as

| RP® Financial, LC. | MARKET AREA ANALYSIS |

II.4

investors took into consideration mixed data on the health of the U.S. economy. A rebound in February job growth pushed the 10-year Treasury yield higher at the start of March, as the 10-year Treasury yield approached 2.0% going into mid-March. Comments by the Federal Reserve Chairwoman that global economic and financial uncertainty justified a slower path for increasing interest rates contributed to long-term Treasury yields edging lower during the second half of March.

The 10-year Treasury yield hovered around 1.75% during the first half of April 2016, as minutes of the Federal Reserve’s March policy meeting signaled that an interest rate increase in April was unlikely. Long-term Treasury yields edged up slightly during the second half of April, with the Federal Reserve concluding its late-April policy meeting leaving interest rates unchanged and remaining ambiguous about raising interest rates in June. Weaker-than-expected job growth reflected in the April employment data contributed to the 10-year Treasury yield dipping back down to 1.75% through mid-May. Signals from the Federal Reserve that an interest rate hike at its June policy meeting was still in-play factored into long-term Treasury yields ticking up going into the second half of May. Investors bought Treasury bonds in early-June following the much-weaker-than-expected jobs report for May, as the anemic job growth reflected in the May employment data reduced expectations that the Federal Reserve would push up rates at its mid-June meeting. As expected, the Federal Reserve concluded it mid-June policy meeting holding short-term interest rates steady and lowered projections of how much they would raise rates in the coming years. Long-term Treasury yields stabilized heading into the second half of June, which was followed by a sharp decline in the 10-year Treasury yield in late-June as investors worried about the economic and political consequences of Britain’s vote to leave the European Union.

In early-July 2016, investors continued to sell risky assets in favor of safe haven investments, which drove the yield on the 10-year Treasury to a record low of 1.37%. Long-term Treasury yields rose going into mid-July, as investors moved back into riskier assets on the heels of the strong job growth reported for June. During the second half of July and into early-August, long-term Treasury yields remained fairly stable, as the Federal Reserve concluded its late-July policy meeting keeping its target interest rate unchanged as expected. As of August 5, 2016, the bond equivalent yields for U.S. Treasury bonds with terms of one and ten years equaled 0.56% and 1.59%, respectively, versus comparable year ago yields of 0.38% and 2.28%. Exhibit II-2 provides historical interest rate trends.

| RP® Financial, LC. | MARKET AREA ANALYSIS |

II.5

Based on the consensus outlook of economists surveyed by The Wall Street Journal in July 2016, GDP growth was projected to come in at 2.0% in 2016 and increase to 2.2% in 2017. The unemployment rate was forecasted to equal 4.7% in December 2016 and decrease slightly to 4.6% in June 2017. An average of 164,000 jobs were projected to be added per month during 2016. The majority of economists believed the next interest rate hike by the Federal Reserve would occur in December 2016 and, on average, the economists forecasted that the 10-year Treasury yield would increase to 1.78% by the end of 2016 and increase to 2.06% by June 2017. The surveyed economists also forecasted home prices would rise 5.2% in 2016 and increase an additional 4.3% in 2017. Housing starts were forecasted to increase slightly in 2016 and continue to trend higher in 2017.

The June 2016 mortgage finance forecast from the Mortgage Bankers Association (the “MBA”) was for 2016 existing home sales to increase by 5.0% and for 2016 new home sales to increase by 16.1%. The MBA forecast showed a 2.0% increase in the median sales price for existing homes in 2016 and a 0.8% decrease in the median sales price for new homes in 2016. Total mortgage production was forecasted to increase to $1.663 trillion in 2016, compared to $1.630 trillion in 2015. The forecasted increase in 2016 originations was based on a 10.4% increase in purchase volume, which was partially offset by a 7.9% decrease in refinancing volume. Purchase mortgage originations were forecasted to total $973 billion in 2016, versus refinancing volume totaling $690 billion. Housing starts for 2016 were projected to increase by 9.8% to total $1.217 billion.

Market Area Demographics

Table 2.1 presents information regarding the demographic and economic trends for the Bank’s market area from 2010 to 2016 and projected through 2021. Data for the nation, the state of Pennsylvania and the Philadelphia MSA are included for comparative purposes. The size and scope of the market area is evidenced by the demographic data, which shows that as of 2016 the total population of the state was 12.8 million, with 47.5% of the state’s population in the Philadelphia MSA. Between 2010 and 2016 the annualized population growth rates of the state and the MSA were 0.1% and 0.3%, respectively, which were less than the comparable national growth rate of 0.7%. Both Montgomery and Philadelphia Counties recorded an annualized population growth rate of 0.5%, while Bucks County no population growth for the same time period. Over the next projected five years, the state, MSA and all of the market area counties are expected to continue to experience similar population growth rates as recorded during the past six years.

| RP® Financial, LC. | MARKET AREA ANALYSIS |

II.6

Table 2.1

Huntingdon Valley Bank

Summary Demographic Data

| Year | Growth Rate | |||||||||||||||||||

| 2010 | 2016 | 2021 | 2010-2016 | 2016-2021 | ||||||||||||||||

| (%) | (%) | |||||||||||||||||||

| Population (000) |

||||||||||||||||||||

| USA |

308,746 | 322,431 | 334,342 | 0.7 | % | 0.7 | % | |||||||||||||

| Pennsylvania |

12,702 | 12,806 | 12,905 | 0.1 | % | 0.2 | % | |||||||||||||

| Philadelphia MSA |

5,965 | 6,077 | 6,177 | 0.3 | % | 0.3 | % | |||||||||||||

| Montgomery County |

800 | 822 | 839 | 0.5 | % | 0.4 | % | |||||||||||||

| Bucks County |

625 | 627 | 630 | 0.0 | % | 0.1 | % | |||||||||||||

| Philadelphia County |

1,526 | 1,569 | 1,600 | 0.5 | % | 0.4 | % | |||||||||||||

| Households (000) |

||||||||||||||||||||

| USA |

116,716 | 122,265 | 127,049 | 0.8 | % | 0.8 | % | |||||||||||||

| Pennsylvania |

5,019 | 5,087 | 5,143 | 0.2 | % | 0.2 | % | |||||||||||||

| Philadelphia MSA |

2,260 | 2,311 | 2,354 | 0.4 | % | 0.4 | % | |||||||||||||

| Montgomery County |

308 | 317 | 324 | 0.5 | % | 0.4 | % | |||||||||||||

| Bucks County |

235 | 238 | 240 | 0.2 | % | 0.2 | % | |||||||||||||

| Philadelphia County |

600 | 620 | 634 | 0.6 | % | 0.5 | % | |||||||||||||

| Median Household Income ($) |

||||||||||||||||||||