Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - NorthStar Realty Europe Corp. | nre12312015exhibit321.htm |

| EX-31.1 - EXHIBIT 31.1 - NorthStar Realty Europe Corp. | nre12312015exhibit311.htm |

| EX-21.1 - EXHIBIT 21.1 - NorthStar Realty Europe Corp. | nre12312015exhibit211.htm |

| EX-23.2 - EXHIBIT 23.2 - NorthStar Realty Europe Corp. | nre12312015exhibit232.htm |

| EX-23.1 - EXHIBIT 23.1 - NorthStar Realty Europe Corp. | nre12312015exhibit231.htm |

| EX-32.2 - EXHIBIT 32.2 - NorthStar Realty Europe Corp. | nre12312015exhibit322.htm |

| EX-31.2 - EXHIBIT 31.2 - NorthStar Realty Europe Corp. | nre12312015exhibit312.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One) | |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015 | |

or | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

Commission File Number: 001-37597

NORTHSTAR REALTY EUROPE CORP.

(Exact Name of Registrant as Specified in its Charter)

Maryland (State or Other Jurisdiction of Incorporation or Organization) | 32-0468861 (IRS Employer Identification No.) |

399 Park Avenue, 18th Floor, New York, NY 10022

(Address of Principal Executive Offices, Including Zip Code)

(212) 547-2600

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.01 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Annual Report on Form 10-K or any amendment to this Annual Report on Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | o | Accelerated filer | o | Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The registrant’s separation from NorthStar Realty Finance Corp. became effective on November 1, 2015. As a result, there was no aggregate market value of common stock held by non-affiliates of the registrant as of June 30, 2015, the last business day of the registrant’s most recently completed second fiscal quarter. As of March 24, 2016, the registrant had issued and outstanding 61,013,300 shares of common stock, $0.01 par value per share.

DOCUMENTS INCORPORATED BY REFERENCE

None.

NORTHSTAR REALTY EUROPE CORP.

FORM 10-K

TABLE OF CONTENTS

Index | Page | |

2

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Forward-looking statements are generally identifiable by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “seek,” “anticipate,” “estimate,” “believe,” “could,” “project,” “predict,” “continue,” “future” or other similar words or expressions. Forward-looking statements are not guarantees of performance and are based on certain assumptions, discuss future expectations, describe plans and strategies, contain projections of results of operations or of financial condition or state other forward-looking information. Such statements include, but are not limited to, those relating to the operating performance of our investments, our liquidity and financing needs, the effects of our current strategies and investment activities, our ability to grow our business, our expected leverage, our expected cost of capital, our ability to divest non-strategic properties, our management’s track record and our ability to raise and effectively deploy capital. Our ability to predict results or the actual effect of plans or strategies is inherently uncertain, particularly given the economic environment. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements and you should not unduly rely on these statements. These forward-looking statements involve risks, uncertainties and other factors that may cause our actual results in future periods to differ materially from those forward-looking statements. These factors include, but are not limited to:

• | the effect of economic conditions, particularly in Europe, on the valuation of our investments and on the tenants of the real property that we own; |

• | our rapid growth and relatively limited experience investing in Europe; |

• | a change in control of NorthStar Asset Management Group Inc., or NSAM; |

• | the ability of NSAM to scale its operations in Europe to effectively manage our company; |

• | our ability to qualify and remain qualified as a real estate investment trust, or REIT; |

• | adverse domestic or international economic conditions and the impact on the commercial real estate industry; |

• | volatility, disruption or uncertainty in the financial markets; |

• | access to debt and equity capital and our liquidity; |

• | our substantial use of leverage and our ability to comply with the terms of our borrowing arrangements; |

• | our ability to obtain mortgage financing on our real estate portfolio on favorable terms or at all; |

• | the unknown impact of the potential default and/or exit of one or more countries within the European Union; |

• | our ability to acquire attractive investment opportunities and the impact of competition for attractive investment opportunities; |

• | the effects of being an externally-managed company, including our reliance on NSAM and its affiliates and sub-advisors/co-venturers in providing management services to us, the payment of substantial base management and incentive fees to our manager, the allocation of investments by our manager among us and our manager’s other sponsored or managed companies and strategic vehicles and various conflicts of interest in our relationship with NSAM; |

• | the impact of adverse conditions affecting office properties; |

• | illiquidity of properties in our portfolio; |

• | our ability to realize current and expected return over the life of our investments; |

• | tenant defaults or bankruptcy; |

• | any failure in our due diligence to identify all relevant facts in our underwriting process or otherwise; |

• | the impact of terrorism or hostilities involving Europe; |

• | our ability to manage our costs in line with our expectations and the impact on our cash available for distribution, or CAD, and net operating income, or NOI, of our properties; |

• | environmental and regulatory requirements, compliance costs and liabilities relating to owning and operating properties in our portfolio and to our business in general; |

• | effect of regulatory actions, litigation and contractual claims against us and our affiliates, including the potential settlement and litigation of such claims; |

3

• | changes in European, international and domestic laws or regulations governing various aspects of our business; |

• | future changes in foreign, federal, state and local tax law that may have an adverse impact on the cash flow and value of our investments; |

• | our ability to effectively structure our investments in a tax efficient manner, including for foreign, federal, state and local tax purposes; |

• | the impact that a rise in future interest rates may have on our floating rate financing; |

• | potential devaluation of foreign currencies, predominately the Euro, relative to the U.S. dollar due to quantitative easing in Europe and/or other factors which could cause the U.S. dollar value of our investments to decline; |

• | general foreign exchange risk associated with properties located in European countries located outside of the Euro Area, including the United Kingdom and Sweden; |

• | the loss of our exemption from the definition of an “investment company” under the Investment Company Act of 1940, as amended; |

• | competition for qualified personnel and NSAM’s ability to hire and retain key personnel to manage us effectively; |

• | the lack of historical financial statements for properties we have acquired and may acquire in compliance with U.S. Securities and Exchange Commission, or SEC, requirements and U.S. generally accepted accounting principles, or U.S. GAAP, as well as the lack of familiarity of our tenants and third-party service providers with such requirements; |

• | the potential failure to maintain effective internal controls and disclosure controls and procedures; |

• | the historical combined consolidated financial statements included in this Annual Report on Form 10-K not providing an accurate indication of our performance in the future or reflecting what our financial position, results of operations or cash flow would have been had we operated as an independent public company during the periods presented; |

• | our status as an emerging growth company; and |

• | compliance with the rules governing REITs. |

The foregoing list of factors is not exhaustive. All forward-looking statements included in this Annual Report on Form 10-K are based on information available to us on the date hereof and we are under no duty to update any of the forward-looking statements after the date of this report to conform these statements to actual results.

Factors that could have a material adverse effect on our operations and future prospects are set forth in “Risk Factors” in this Annual Report on Form 10-K beginning on page 11. The risk factors set forth in our filings with the SEC could cause our actual results to differ significantly from those contained in any forward-looking statement contained in this report.

4

PART I

Item 1. Business

References to “we,” “us” or “our” refer to NorthStar Realty Europe Corp. and its subsidiaries unless the context specifically requires otherwise.

Overview

On October 31, 2015, NorthStar Realty Finance Corp., or NorthStar Realty, completed the spin-off of its European real estate business (excluding its European healthcare properties), or the Spin-off, into a newly-formed publicly-traded real estate investment trust, or REIT, NorthStar Realty Europe Corp., a Maryland corporation. We are a European focused commercial real estate company with predominantly prime office properties in key cities within Germany, the United Kingdom and France. Our objective is to provide our stockholders with stable and recurring cash flow supplemented by capital growth over time.

The European real estate business contributed by NorthStar Realty upon completion of the Spin-off is comprised of: (i) business activities related to the launch of the European real estate business and the acquisition of a multi-tenant office complex located in the United Kingdom, or the U.K. Complex on September 16, 2014, or Acquisition Date, referred to as the NorthStar Europe Predecessor; (ii) other European real estate acquisitions in 2015 primarily comprised of multi-tenant office properties, or the New European Investments; and (iii) certain other assets and liabilities related to NorthStar Realty’s European real estate business, herein collectively referred to as the European Real Estate Business.

On November 2, 2015, our common stock began trading on the New York Stock Exchange, or the NYSE, under the symbol “NRE.” We are externally managed and advised by an affiliate of NorthStar Asset Management Group Inc. (NYSE: NSAM), which together with its affiliates is referred to as NSAM. Substantially all of our assets, directly or indirectly, are held by, and we conduct our operations, directly or indirectly, through NorthStar Realty Europe Limited Partnership, a Delaware limited partnership and our operating partnership, or our Operating Partnership. We intend to conduct our operations so as to qualify as a REIT for U.S. federal income tax purposes.

Our Investments

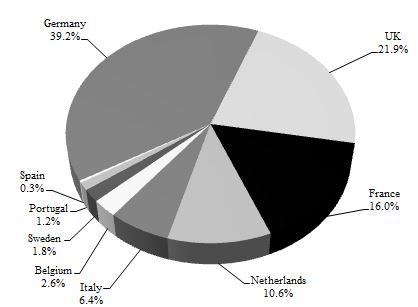

Our current portfolio of $2.5 billion, at cost, as of December 31, 2015, adjusted for sales through March 22, 2016 is comprised of 48 properties and a total of 495,588 square meters of rentable space, located in many key European markets, including Frankfurt, Hamburg, Berlin, London, Paris, Amsterdam, Milan, Brussels and Madrid. Our portfolios primarily comprises office properties that generated 96% of our in-place rental income as of December 31, 2015. We hold predominantly prime office properties in Germany, the United Kingdom and France that account for approximately 66% of our in-place rental income as of December 31, 2015. As of December 31, 2015, our overall portfolio was 87% occupied, had a weighted average remaining lease term of approximately six years and included high-quality tenants.

The following presents a summary of our portfolio and diversity across geographic location as of December 31, 2015, adjusted for sales through March 22, 2016:

Portfolio by Geographic Location | |||

Total portfolio, at cost(1) | $2.5 billion |  | |

Number of properties(2) | 48 | ||

Number of countries | 9 | ||

Total square meters(3) | 495,588 | ||

Weighted average occupancy | 87% | ||

Weighted average lease term | 6 years | ||

In-place rental income:(4) | |||

Office properties | 96% | ||

Other | 4% | ||

___________________________________

(1) | Amount includes transaction costs incurred, deferred financing costs and other assets assumed and is translated using exchange rates as of December 31, 2015. |

(2) | Excludes two assets in the Internos Portfolio and one asset in the Deka Portfolio that were sold in December 2015 and one asset in the Deka Portfolio that was sold in March 2016. |

(3) | Based on contractual rentable area. |

(4) | In-place rental income represents gross rent adjusted for vacancies based on the rent roll as of December 31, 2015. |

5

Our European Real Estate Business as of December 31, 2015, adjusted for sales through March 22, 2016, includes the following (dollars in millions):

Acquisition | Ownership | ||||||||||||||

Portfolio | Date | Primary Location(s) | Primary Description | Cost(1) | Properties | Interest | |||||||||

U.K. Complex | Sept-14 | United Kingdom | Multi-tenant office | $ | 90 | 1 | 93% | ||||||||

SEB Portfolio | Apr-15 | Germany, United Kingdom, France | Multi-tenant office | 1,309 | 11 | 95% | (2) | ||||||||

Internos Portfolio | Apr-15 | Germany, France, Portugal | Office/Hotel/Industrial/Retail | 199 | 10 | 95% | (2) | ||||||||

IVG Portfolio | Apr-15 | Germany, United Kingdom, France | Multi-tenant office | 247 | 15 | 95% | (2) | ||||||||

Deka Portfolio | Apr-15 | Germany | Multi-tenant office | 81 | 8 | 95% | (2) | ||||||||

Trianon Tower | Jul-15 | Germany | Multi-tenant office | 611 | 3 | 95% | (2) | ||||||||

Total | $ | 2,537 | 48 | ||||||||||||

__________________

(1) | Amount includes transaction costs incurred, deferred financing costs and other assets assumed and is translated using exchange rates as of December 31, 2015. |

(2) | We have an approximate 95% equity interest in certain subsidiaries that own these portfolios that are entitled to 100% of net income (loss) based on the allocation formula, as set forth in the governing documents. |

Financing Strategy

We seek to access a wide range of secured and unsecured debt and public and private equity capital sources to fund our investment activities. We predominantly use investment-level financing as part of our strategy to seek to prudently leverage our investments and deliver attractive risk-adjusted returns to our stockholders. We target overall leverage of 40% to 50% over time, although there is no assurance that this will be the case.

We pursue a variety of financing arrangements such as mortgage notes and bank loans available from the CMBS market, finance companies and banks. In addition, we may use corporate-level financing such as credit facilities and other term borrowings. We generally seek to limit our reliance on recourse borrowings. Borrowing levels for our investments may be dependent upon the nature of the investments and the related financing that is available.

In July 2015, we issued $340 million aggregate principal amount of 4.625% senior stock-settlable notes due December 2016, or the Senior Notes. We received aggregate net proceeds of $331 million, after deducting the underwriters’ discount and other expenses. Proceeds from the issuance of the Senior Notes were distributed to subsidiaries of NorthStar Realty, which used such amounts for general corporate purposes, including, among other things, the funding of acquisitions, including the Trianon Tower, and the repayment of NorthStar Realty’s borrowings. The Senior Notes are our senior unsubordinated and unsecured obligations. NorthStar Realty’s operating partnership continues to guarantee payments on the Senior Notes subsequent to the Spin-off. In February 2016, we repurchased approximately $150 million of the Senior Notes, at a slight discount to par value, through open market purchases.

Attractive long-term, non-recourse, non-mark-to-market, financing continues to be available in the European markets. We predominately use floating rate financing and we seek to mitigate the risk of interest rates rising through hedging arrangements including interest rate swaps and caps.

Portfolio Management

NSAM performs portfolio management services on our behalf. In addition, we rely on the services of local third-party service providers. The comprehensive portfolio management process includes day-to-day oversight by the portfolio management team, regular management meetings and a quarterly investment review process. These processes are designed to enable management to evaluate and proactively identify investment-specific issues and trends on a portfolio-wide basis. Nevertheless, we cannot be certain that such review will identify all potential issues within our portfolio due to, among other things, adverse economic conditions or events adversely affecting specific investments; therefore, potential future losses may also stem from investments that are not identified during these investment reviews.

NSAM uses many methods to actively manage our risks to seek to preserve our income and capital, which includes our ability to manage our investments and our tenants in a manner that preserves cost and income and minimizes credit losses that could decrease income and portfolio value. Frequent re-underwriting, dialogue with tenants/partners and regular inspections of our properties have proven to be an effective process for identifying issues early. Monitoring tenant creditworthiness is an important component of our portfolio management process, which may include, to the extent available, a review of financial statements and operating statistics, delinquencies, third party ratings and market data. During the quarterly portfolio review, or more frequently as necessary, investments may be put on highly-monitored status and identified for possible asset impairment based upon several factors,

6

including missed or late contractual payments, tenant rating downgrades (where applicable) and other data that may indicate a potential issue in our ability to recover our invested capital from an investment.

We may need to make unplanned capital expenditures in connection with changes in laws and governmental regulations in relation to real estate. Where properties are being repositioned or refurbished, we may be exposed to unforeseen changes in scope to budgeted capital expenditures.

Regulation

We are subject, in certain circumstances, to supervision and regulation by international, federal, state and local governmental authorities and are subject to various laws and judicial and administrative decisions imposing various requirements and restrictions, which, among other things:

• regulate our public disclosures, reporting obligations and capital raising activity;

• require compliance with applicable REIT rules;

• regulate credit granting activities;

• require disclosures to customers;

• govern secured transactions;

• set collection, taking title to collateral, repossession and claims-handling procedures and other trade practices;

• regulate land use and zoning;

• regulate the foreign ownership or management of real property or mortgages;

• | regulate the ability of foreign persons or corporations to remove profits earned from activities within the country to the person’s or corporation’s country of origin; |

• regulate tax treatment and accounting standards; and

• | regulate use of derivative instruments and our ability to hedge our risks related to fluctuations in interest rates and exchange rates. |

We intend to elect and qualify to be taxed as a REIT under Sections 856 through 860 of the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code, beginning with the year ended December 31, 2015 upon filing our initial U.S. federal income tax. As a REIT, we must currently distribute, at a minimum, an amount equal to 90% of our taxable income. In addition, we must distribute 100% of our taxable income to avoid paying corporate U.S. federal income taxes. REITs are also subject to a number of organizational and operational requirements in order to elect and maintain REIT status. These requirements include specific share ownership tests and assets and gross income composition tests. If we fail to continue to qualify as a REIT in any taxable year, we will be subject to U.S. federal income tax (including any applicable alternative minimum tax) on our taxable income at regular corporate tax rates. Even if we qualify for taxation as a REIT, we may be subject to tax in foreign jurisdictions in which we operate or own property and state and local income taxes and to U.S. federal income tax and excise tax on our undistributed income.

We believe that we are not, and intend to conduct our operations so as not to become regulated as, an investment company under the Investment Company Act of 1940, as amended, or the Investment Company Act. We have relied, and intend to continue to rely on current interpretations of the staff of the Securities and Exchange Commission, or SEC, in an effort to continue to qualify for an exemption from registration under the Investment Company Act. For more information on the exemptions that we use refer to Item 1A. “Risk Factors - Risks Related to Regulatory Matters and Our REIT Tax Status.”

Real estate properties owned by us and the operations of such properties are subject to various international laws and regulations concerning the protection of the environment, including air and water quality, hazardous or toxic substances and health and safety. In addition, such properties are required to comply with applicable fire and safety regulations, building codes, legal or regulatory provisions regarding access to our properties for persons with disabilities and other land use regulations. For further information regarding environmental matters, refer to “Environmental Matters” below.

In addition, we currently own two hotels, leased to third-party operators, which are subject to various covenants, laws, ordinances and regulations, including regulations relating to common areas. We believe each of our hotels have the necessary permits and approvals to operate its business.

In the judgment of management, while we do incur significant expense complying with the various regulations to which we are subject, existing statutes and regulations have not had a material adverse effect on our business. However, it is not possible to

7

forecast the nature of future legislation, regulations, judicial decisions, orders or interpretations, nor their impact upon our future business, financial condition, results of operations or prospects.

Environmental Matters

A wide variety of environmental and occupational health and safety laws and regulations affect our properties. These complex laws, and their enforcement, involve a myriad of regulations, many of which involve strict liability on the part of the potential offender. Some of these laws may directly impact us. Under various local environmental laws, ordinances and regulations, an owner of real property, such as us, may be liable for the costs of removal or remediation of hazardous or toxic substances at, under or disposed of in connection with such property, as well as other potential costs relating to hazardous or toxic substances (including government fines and damages for injuries to persons and adjacent property). The cost of any required remediation, removal, fines or personal or property damages and the owner’s liability therefore could exceed or impair the value of the property, and/or the assets of the owner. In addition, the presence of such substances, or the failure to properly dispose of or remediate such substances, may adversely affect the owner’s ability to sell or rent such property or to borrow using such property as collateral which, in turn, could reduce our revenues.

Selected Regulations Regarding our Operations in Germany, the United Kingdom and France

Our commercial real estate investments are subject to a variety of laws and regulations in Europe. If we fail to comply with any of these laws and regulations, we may be subject to civil liability, administrative orders, fines or even criminal sanctions. The following provides a brief overview of selected regulations that are applicable to our business operations in Germany, the United Kingdom and France, where a majority of our properties in terms of contribution to rental income are located.

Germany

Land-use Regulations, Building Regulations and Tenancy Law for Commercial Properties

Land-use Regulations. There are several regulations regarding the use of land including German planning law and urban restructuring planning by communities.

Urban Restructuring Planning. Communities may designate certain areas as restructuring areas and undertake comprehensive modernization efforts regarding the infrastructure in such areas. While this may improve the value of properties located in restructuring areas, being located in a restructuring area also imposes certain limitations on the affected properties (e.g., the sale, encumbrance and leasing of such properties, as well as reconstruction and refurbishment measures, are generally subject to special consent by municipal authorities).

Building Regulations. German building laws and regulations are quite comprehensive and address a number of issues, including, but not limited to, permissible types of buildings, building materials, proper workmanship, heating, fire safety, means of warning and escape in case of emergency, access and facilities for the fire department, hazardous and offensive substances, noise protection, ventilation and access and facilities for disabled people. Owners of erected buildings may be required to conduct alterations or improvements of the property if safety or health risks with respect to users of the building or the general public occur, including fire risks, traffic risks, risks of collapse and health risks from injurious building materials such as asbestos. To our knowledge, there are currently no official orders demanding any alterations to existing buildings owned by us.

Tenancy Law for Commercial Properties. German tenancy laws for commercial properties generally provide landlords and tenants with far-reaching discretion in how they structure lease agreements and use general terms and conditions. Certain legal restrictions apply with regard to the strict written form requirements regarding the lease agreement, transfer of operating costs and maintenance costs, cosmetic repairs and final decorative repairs. Lease agreements with a term of more than one year must be executed in writing or are deemed to have been concluded for an indefinite period with the consequence that they can be terminated at the end of one year after turning over the leased property to the lessee. Operating costs of commercial tenancies may be apportioned to the tenants if the lease agreement stipulates explicitly and specifically which operating costs shall be borne by the tenant. Responsibility for maintenance and repair costs may be transferred to tenants, except for the full cost transfer of maintenance and repair costs for roof, structures and areas used by several tenants in general terms and conditions. Expenses for cosmetic repairs (Schönheitsreparaturen) may, in principle, be allocated to tenants, provided that the obligation to carry out ongoing cosmetic repairs is not combined with an undertaking to perform initial and/or final decorative repairs.

Regulation Relating to Environmental Damage and Contamination

The portion of our commercial real estate portfolio located in Germany is subject to various rules and regulations relating to the remediation of environmental damage and contamination.

Soil Contamination. Pursuant to the German Federal Soil Protection Act, the responsibility for residual pollution and harmful changes to soil, or Contamination, lies with, among others, the perpetrator of the Contamination, such perpetrator’s universal successor, the current owner of the property, the party in actual control of the property and, if the title was transferred after March 1999, the previous owner of the property if such owner knew or should have known about the Contamination, or the Liable Persons.

8

The Liable Person that carried out the remediation work may claim indemnification on a pro rata basis from the other Liable Persons. Independently, from the aforementioned liability, civil law liability for Contaminations can arise from contractual warranty provisions or statutory law.

United Kingdom

For a discussion of the impact of regulations in the United Kingdom, refer to Item 1A. “Risk Factors — Risks Related to our Financing Strategy- “We are subject to risks associated with obtaining mortgage financing on our real estate, which could materially adversely affect our business, financial condition and results of operations and our ability to make distributions to stockholders.”

France

Participation in an Organismes de placement collectif en immobilier

We hold participations in Organismes de placement collectif en immobilier, or OPCIs, each of which takes the form of a Société de Placement à Prépondérance Immobilière à Capital Variable, or SPPICAV. Both the SPPICAV and its management company, Swiss Life Reim (France), are authorized and supervised by the French Autorité des marchés financiers.

Commercial Lease Regulation

The contractual conditions applying to commercial lease periods, renewal, rent and rent indexation are heavily regulated. The minimum duration of commercial leases is nine years. We cannot terminate the lease before such period, except in very specific cases (such as reconstructing or elevating an existing building). The tenant, on the other hand, has the power to terminate the lease at the end of each three-year period, subject to a six-month prior notice requirement. However, in leases of premises to be used exclusively as office spaces, such power of the tenant can be contractually removed.

The tenant has also a right of renewal of the lease at the end of its initial period and a right to a revision of the rent every three years. The rent variation is capped. Except in the case where the rental value considerably changes (increase by more than 10% in case of a revision upon a three-year period), the variation of the rent, in case of a revision upon a three-year period or in case of a renewal, cannot exceed the variation of the Commercial Rents Index (indice trimestriel des loyers commerciaux) or the Retail Rental Index (indice trimestriel des loyers des activités tertiaires). However, this provision does not apply in case of a renewal of a lease, the initial duration of which exceeded nine years or the effective duration of which exceeded twelve years. In addition, even in the case of a renewed or revised lease where the rental value has considerably changed, the rent increase cannot exceed 10% of the rent paid during the previous year.

Moreover, the tenant has a right of first refusal if the leased premises are offered for sale.

The legal distribution of charges between us and the tenant can be contractually determined. However, articles L. 145-40-2 and R. 145-35 of the French commercial code, which result from French law no. 2014-626 of June 18, 2014, make it mandatory for the property owner in leases entered into on or after November 3, 2014 to incur expenditures for major repairs, in particular those related to the obsolescence of the properties and those required to meet changing legal regulation. It also forces the property owner to incur certain taxes.

Bankruptcy Law

In France, a safeguarding (sauvegarde), judicial restructuring (redressement judiciaire) or judicial liquidation (liquidation) procedure commencement order against an insolvent tenant does not lead to the automatic termination of the lease. In such cases, we will not be able to get paid directly by the tenant any rent due before the commencement order. Furthermore, the tenant, via the insolvency court appointed receiver, will have the choice to continue or reject any unexpired lease. If the tenant chooses to continue an unexpired lease, but still fails to pay the rent in connection with the occupancy after the issue of the commencement order, we cannot legally request the termination of the lease before the end of a three-month period from the date of issue of the commencement order.

Environmental Law

In France, our investments are subject to regulations regarding the accessibility of buildings to persons with disabilities, public health and the environment, covering a number of areas, including the ownership and use of classified facilities, the use, storage, and handling of hazardous materials in building construction; inspections for asbestos, lead, and termites; inspection of gas and electricity facilities; assessments of energy efficiency; and assessments of technological and natural risks.

Emerging Growth Company Status

We are an “emerging growth company,” as defined in the Jumpstart Our Business Act, or JOBS Act and we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies.” These exemptions include not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports

9

and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

We have availed ourselves of some of the reduced regulatory and reporting requirements that are available to us as long as we qualify as an emerging growth company, except that we have irrevocably elected not to take advantage of the extension of time to comply with new or revised financial accounting standards available under Section 102(b) of the JOBS Act.

We will, in general, remain as an emerging growth company for up to five full fiscal years following December 31, 2015. We would cease to be an emerging growth company and, therefore, become ineligible to rely on the above exemptions, if we:

• | have more than $1 billion in annual revenue in a fiscal year; |

• | issue more than $1 billion of non-convertible debt during the preceding three-year period; or |

• | become a “large accelerated filer” as defined in Exchange Act Rule 12b-2, which would occur at the end of the fiscal year after: (i) we have filed at least one annual report pursuant to the Exchange Act; (ii) we have been an SEC-reporting company for at least 12 months; and (iii) the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter. |

Competition

We are subject to increased competition in seeking investments. We compete with many third parties engaged in real estate investment activities including publicly-traded REITs, non-traded REITS, insurance companies, commercial and investment banking firms, private equity funds, sovereign wealth funds and other investors. Some of these competitors, including other REITS and private real estate companies and funds, have substantially greater financial resources than we do. Such competitors may also enjoy significant competitive advantages that result from, among other things, a lower cost of capital and enhanced operating efficiencies.

Future competition from new market entrants may limit the number of suitable investment opportunities offered to us. It may also result in higher prices, lower yields and a narrower spread over our borrowing costs, making it more difficult for us to originate or acquire new investments on attractive terms.

Employees

We are externally managed by NSAM and do not have our own employees. As of December 31, 2015, NSAM had 276 employees.

Corporate Governance and Internet Address

We emphasize the importance of professional business conduct and ethics through our corporate governance initiatives. Our board of directors consists of a majority of independent directors; the audit, nominating and corporate governance and compensation committees of our board of directors are composed exclusively of independent directors. We have adopted corporate governance guidelines and a code of business conduct and ethics, which delineate our standards for our officers, directors and employees.

Our internet address is www.nrecorp.com. The information on our website is not incorporated by reference in this Annual Report on Form 10-K. We make available, free of charge through a link on our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to such reports, if any, as filed or furnished with the SEC, as soon as reasonably practicable after such filing or furnishing. We also post corporate presentations on our website from time-to-time. Our website further contains our code of business conduct and ethics, code of ethics for senior financial officers, corporate governance guidelines and the charters of our audit committee, nominating and corporate governance committee and compensation committee of our board of directors. Within the time period required by the rules of the SEC and the NYSE we will post on our website any amendment to our code of business conduct and ethics and our code of ethics for senior financial officers as defined in the code.

10

Item 1A. Risk Factors

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. Additional risks and uncertainties not presently known to us, that we currently deem immaterial or that generally apply to all businesses also may adversely impact our business. If any of the following risks occur, our business, financial condition, operating results, cash flow and liquidity could be materially adversely affected.

Risks Related to Our Business

The commercial real estate industry has been and may continue to be adversely affected by economic conditions and geopolitical events in Europe, the United States, China and elsewhere.

Our business and operations are dependent on the commercial real estate industry generally, which in turn is dependent upon global economic conditions in Europe, the United States, China and elsewhere. Recently, concerns over global economic conditions, energy and commodity prices, geopolitical events, acts of war and terrorism, deflation, Federal Reserve short term rate decisions, foreign exchange rates, the availability and cost of credit, the sovereign debt crisis, the Chinese economy, and weak consumer confidence in many markets, have contributed to increased economic uncertainty and diminished expectations for the global economy. These factors, combined with the volatile prices of oil and declining business and consumer confidence may precipitate an economic slowdown, as well as cause extreme volatility in security prices. Global economic and political headwinds, along with global market instability and the risk of maturing commercial real estate debt that may have difficulties being refinanced, may continue to cause periodic volatility in the commercial real estate market for some time. Adverse economic conditions in the commercial real estate industry, geopolitical events, acts of war or terrorism could harm our business and financial condition by, among other factors, reducing the value of our properties, limiting our access to debt and equity capital and otherwise negatively impacting our operations.

Challenging economic and financial market conditions could significantly reduce the value of our investments.

Challenging economic and financial market conditions may cause us to experience an increase in the number of investments that result in losses, including tenant defaults, a decrease in revenues and the value of our properties and delinquencies, all of which could adversely affect our results of operations. We may incur substantial losses and need to establish significant provision for losses or impairment.

Volatility, disruption or uncertainty in the financial markets may impair our ability to raise capital, obtain new financing or refinance existing obligations and fund real estate activities.

The global financial markets have experienced pervasive and fundamental disruptions. Market disruption, volatility or uncertainty could materially adversely impact our ability to raise capital, obtain new financing or refinance our existing obligations as they mature and fund real estate activities. In addition, market disruption, volatility or uncertainty may also expose us to increased litigation and shareholder activism. These conditions could materially disrupt our business, operations and ability to make distributions to our stockholders. Market volatility could also lead to significant uncertainty in the valuation of commercial real estate investments, which may result in a substantial decrease in the value of our properties. As a result, we may not be able to recover the carrying amount of such investments and the associated goodwill, if any, which may require us to recognize impairment charges in earnings.

Liquidity in the capital markets is essential to our business.

Liquidity is essential to our business. Our business may be adversely affected by disruptions in the debt and equity capital markets and institutional lending market, including a lack of access to capital or prohibitively high costs of obtaining or replacing capital, both domestically and abroad. We depend on external financing to fund the growth of our business mainly because one of the requirements of the Internal Revenue Code for a REIT is that we distribute 90% of our taxable income to our stockholders, including taxable income where we do not receive corresponding cash. Our access to equity or debt financing depends on the willingness of third parties to make equity and debt investments in us. It also depends on conditions in the capital markets generally. Companies in the real estate industry, including us, are currently experiencing, and have at times historically experienced, limited availability of capital and new capital sources may not be available on acceptable terms. Our ability to raise capital could be impaired if the capital markets have a negative perception of our long-term or short-term financial prospects or the prospects for REITs and the commercial real estate market generally. Sufficient funding or capital may not be available to us in the future on terms that are acceptable to us. If we cannot obtain sufficient funding on acceptable terms, we will not be able to grow our business and may have difficulty maintaining liquidity and making distributions to our stockholders, which would have a negative impact on the market price of our common stock. For information about our available sources of funds, refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources” in Item 7 of Part II of this Annual Report on Form 10-K and the notes to our combined consolidated financial statements in Item 8 of Part II of this Annual Report on Form 10-K.

11

We use significant leverage in connection with our investments, which increases the risk of loss associated with our investments and restricts our ability to engage in certain activities.

As of December 31, 2015, we had $1.8 billion of borrowings outstanding. We may also incur additional borrowings in the future to satisfy our capital and liquidity needs. Although the use of leverage may enhance returns and increase the number of investments that we can make, it may increase our risk of loss, impact our liquidity and restrict our ability to engage in certain activities. Our substantial borrowings, among other things, may:

• | require us to dedicate a large portion of our cash flow to pay principal and interest on our borrowings, which will reduce the availability of cash flow to fund working capital, capital expenditures and other business activities; |

• | require us to maintain minimum unrestricted cash; |

• | increase our vulnerability to general adverse economic and industry conditions; |

• | require us to post additional reserves and other additional collateral to support our financing arrangements, which could reduce our liquidity and limit our ability to leverage our assets; |

• | subject us to maintaining various debt, operating income, net worth, cash flow and other covenants and financial ratios; |

• | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

• | restrict our operating policies and ability to make strategic acquisitions, dispositions or exploit business opportunities; |

• | require us to maintain a borrowing base of assets; |

• | place us at a competitive disadvantage compared to our competitors that have fewer borrowings; |

• | put us in a position that necessitates raising equity capital at a time that is unfavorable to us and dilutive to our stockholders; |

• | limit our ability to borrow additional funds (even when necessary to maintain adequate liquidity), dispose of assets or make distributions to stockholders; and |

• | increase our cost of capital. |

If we fail to comply with the covenants in the instruments governing our borrowings or do not generate sufficient cash flow to service our borrowings, our liquidity may be materially and adversely affected. If we default or fail to meet certain coverage tests, we may be required to post additional collateral, subject our assets to foreclosure and/or require us to seek protection under bankruptcy laws. Further, to the extent we take certain actions prohibited by our borrowings, we may be required to repay outstanding obligations, together with penalties, prior to the stated maturity.

Continuing concerns regarding European debt, market perceptions concerning the instability of the Euro, recent volatility and price movements in the rate of exchange between the U.S. dollar and the Euro and the potential exit of the United Kingdom from the European Union could adversely affect our business, results of operations and financing.

Concerns persist regarding the debt burden of certain Euro Area countries and their potential inability to meet their future financial obligations, the overall stability of the Euro and the suitability of the Euro as a single currency, given the diverse economic and political circumstances in individual Euro Area countries and recent declines and volatility in the value of the Euro. These concerns could lead to the re-introduction of individual currencies in one or more Euro Area countries, or, in more extreme circumstances, the possible dissolution of the Euro currency entirely. Should the Euro dissolve entirely, the legal and contractual consequences for holders of Euro-denominated obligations would be uncertain. Such uncertainty would extend to, among other factors, whether obligations previously expressed to be owed and payable in Euros would be re-denominated in a new currency (with considerable uncertainty over the conversion rates), what laws would govern and which country’s courts would have jurisdiction. These potential developments, or market perceptions concerning these and related issues, could materially adversely affect the value of our Euro-denominated investments and obligations.

Furthermore, market concerns about economic growth in the Euro Area relative to the United States and speculation surrounding the potential impact on the Euro of a possible Greek or other country sovereign default and/or exit from the Euro Area may continue to exert downward pressure on the rate of exchange between the U.S. dollar and the Euro, which may adversely affect our results of operations and our ability to obtain financing. Additionally, the United Kingdom is currently seeking to negotiate changes to its membership in the European Union and has announced it intends to conduct a referendum in June 2016 as to whether the United Kingdom should exit the European Union. The exit of the United Kingdom, or the prospect of any exit, may create uncertainty within the United Kingdom and elsewhere regarding potential consequences of an exit. Any such uncertainty or adverse consequences of an exit could negatively impact liquidity of the commercial real estate market within the United Kingdom, which could have an adverse impact the values of our properties located within the United Kingdom. Further, the departure of the United

12

Kingdom from the European Union may cause instability within the union itself, which could lead to further departures, uncertainly and other adverse impacts, which could adversely impact the values of our properties located within the European Union.

Risks Related to Our Manager

Our ability to achieve our investment objectives and to pay distributions to our stockholders depends in substantial part upon the performance of our manager.

We rely upon NSAM to manage our day-to-day operations and our investments. Our ability to achieve our investment objectives and grow our business is dependent upon the performance of NSAM in the acquisition or disposition of investments, the determination of financing arrangements and the management of our investments and operation of our day-to-day activities under the supervision of, and subject to the policies and guidelines established by, our board of directors. If our manager performs poorly and as a result is unable to manage our investments successfully, we may be unable to achieve our investment objectives or to pay distributions to our stockholders.

Any adverse changes in NSAM’s financial health, the public perception of NSAM or our relationship with NSAM could hinder our operating performance and adversely affect our financial condition and results of operations.

Because NSAM is a publicly-traded company, any negative reaction by the stock market reflected in the price of its securities or deterioration in the public perception of NSAM could result in an adverse effect on our ability to manage our portfolio, including acquiring or disposing of assets and obtaining financing from third parties on favorable terms or at all. Recently, NSAM common stock has been highly volatile and NSAM is subject to an activist campaign, all of which could disrupt NSAM’s ability to perform services for us and potentially harm our business. In addition, NSAM depends upon the management and other fees and reimbursement of costs that it receives from us and NSAM’s other managed companies in connection with the acquisition, management and sale of properties to conduct its operations. Any adverse changes in the financial condition of NSAM or our relationship with NSAM could hinder NSAM’s ability to successfully support our business, which could have a material adverse effect on our financial condition and results of operations.

NSAM is seeking potential strategic alternatives, which could result in a change in the ownership of NSAM.

NSAM recently announced its exploration of strategic alternatives to seek to maximize stockholder value for NSAM’s stockholders. This exploration may not result in any transaction being announced or consummated. In addition, any value created for NSAM’s stockholders may not result in the creation of value for our stockholders.

If NSAM were to consummate a transaction that resulted in the transfer of a controlling block of securities of NSAM, this could result in a change to the management of our manager and its affiliates as well as a change to the board of directors at NSAM. Further, NSAM is currently the subject of activist efforts to change the board of directors, which may harm our relationship with NSAM. We could be managed by an entity and personnel that do not have the experience and track record that resides within NSAM and suitable alternatives may not be available. New board members, management and personnel could impair its performance of services to us. Any such fundamental change to NSAM could be disruptive to our business and operations.

Failure of NSAM to effectively perform its obligations to us, including under the management agreement, could have an adverse effect on our business and performance.

We have engaged NSAM to provide asset management and other services to us pursuant to a management agreement. Our ability to achieve our investment and business objectives and to make distributions to our stockholders depends in substantial part upon the performance of NSAM and its ability to provide us with asset management and other services. We are also dependent on other third party service providers to whom NSAM has delegated various responsibilities or engaged on our behalf. If for any reason NSAM or any other service provider is unable to perform such services at the level we require, our ability to replace NSAM or any other service providers is limited under the terms of our management agreement. Even if we were able to terminate our management agreement with NSAM, alternate service providers may not be readily available on acceptable terms or at all, which could adversely affect our performance and materially harm our ability to execute our business plan.

Our ability to terminate our management agreement with NSAM is limited.

Our management agreement with NSAM is only terminable by us for cause. We are unable to terminate our management agreement for any other reason, including if NSAM performs poorly or is unable to manage us successfully. The term “cause” is limited to specific circumstances set forth in the management agreement. Termination for unsatisfactory financial performance does not constitute “cause” under our management agreement. In addition, we are contractually committed to NSAM’s management for an initial term of approximately 20 years from October 2015, with automatic renewal terms thereafter. These provisions increase our risk that NSAM may not perform well and our business could suffer. If NSAM’s performance as our manager does not meet our or our stockholders’ expectations, and we are unable to terminate the management agreement, the market price of our common stock could suffer.

13

NSAM’s platform may not be as scalable as we anticipate and we could face difficulties managing our business without significant new investment in personnel and infrastructure by NSAM.

NSAM’s business has grown substantially over the course of the past several years, both in volume and in scope. This expansion has placed significant additional demands on management and other personnel, as well as our support infrastructure.

While we believe NSAM’s platform for operating our business is highly scalable and can support our recent significant growth without substantial new investment in personnel, expertise and infrastructure on a relative basis, we may be wrong in that assessment. It is possible that if the business of the other companies managed by NSAM, including companies sponsored by NSAM, continues to grow, NSAM will need to make significant investments in personnel, infrastructure and expertise to support that growth. In addition, service providers to whom NSAM may delegate certain asset management functions may also be strained by our growth or the growth of their other clients. NSAM, or its service providers, may be unable to make significant investments on a timely basis or at reasonable costs and its failure in this regard could disrupt our business and operations. Further, during periods of economic retraction, NSAM, or its service providers, may be incented to reduce its personnel and costs, which could have an adverse effect on us.

Substantially all of the fees payable to NSAM are payable regardless of the performance or size of our portfolio and may fail to appropriately incentivize NSAM when managing our portfolio.

We pay NSAM an annual base management fee regardless of the performance or size of our portfolio. Consequently, we may be required to pay NSAM significant base management fees despite certain dispositions of assets, repurchases of our common stock or experiencing a net loss or a decline in the value of our portfolio. This in turn could harm both our ability to make disruptions to our stockholders and the market price of our common stock.

NSAM’s entitlement to compensation regardless of our performance could reduce its incentive to devote its time and effort to seeking investments that provide attractive risk-adjusted returns for our portfolio, particularly if other management agreements to which NSAM is a party have a performance-based fee structure. In addition, NSAM has the ability to earn incentive fees each quarter based on our CAD, which may create an incentive for NSAM to invest in investments with higher yield potential, that are generally riskier or more speculative, or sell an investment prematurely for a gain and pay down borrowings, in an effort to increase our short-term net income and thereby increase the incentive fees to which it is entitled. Furthermore, the compensation payable to NSAM will increase as a result of future issuances of our equity securities, even if the issuances are dilutive to existing stockholders. If our interests and those of NSAM are not aligned, the execution of our business plan and our results of operations could be adversely affected, which could materially and adversely affect our ability to make distributions to our stockholders and the market price of our common stock.

The fees we pay to NSAM in connection with the acquisition and management of our investments pursuant to our management agreement were not determined on an arm’s length basis; therefore, we did not have the benefit of arm’s length negotiations of the type normally conducted between unrelated parties.

The fees we pay to NSAM for services it provides to us pursuant to the management agreement were not determined on an arm’s length basis. As a result, the fees are determined without the benefit of arm’s length negotiations of the type normally conducted between unrelated parties and may be in excess of amounts that we would otherwise pay to third parties for such services.

In addition to the management fees we pay to NSAM, we reimburse NSAM for costs and expenses incurred on our behalf, including indirect personnel and employment costs of NSAM and these costs and expenses may be substantial.

We pay NSAM substantial fees for the services it provides to us and we also have an obligation to reimburse NSAM for costs and expenses it may incur and pay on our behalf. Subject to certain limitations and exceptions, we reimburse NSAM for both direct expenses as well as indirect costs, including a portion of NSAM’s personnel and employment costs. The costs and expenses NSAM incurs on our behalf, including the compensatory costs incurred by NSAM and its affiliates, may be substantial. There are conflicts of interest that could arise when NSAM makes allocation determinations. Subsequent to the Spin-off through December 31, 2015, NSAM allocated $0.4 million of expense to us. In addition, we are required to issue equity awards to NSAM employees at NSAM’s request under the terms of our management agreement. For the year ended December 31, 2015, NSAM granted $0.8 million in the aggregate in our equity awards to its employees, including to employees who serve as our executive officers. NSAM could allocate costs and expenses to us in excess of what we anticipate and such costs and expenses could have an adverse effect on our financial performance and ability to make cash distributions to our stockholders.

There are conflicts of interest in our relationship with NSAM that could result in decisions that are not in the best interests of our stockholders.

We are subject to conflicts of interest arising out of our relationship with NSAM, its affiliates, managed entities and strategic ventures. In particular, we expect to compete for investment opportunities directly with other companies and/or accounts that NSAM or its strategic or joint venture partners manage. Certain of NSAM’s managed companies, along with companies, funds

14

and vehicles that are subject to a strategic relationship between NSAM and its strategic or joint venture partners (which we refer to collectively as strategic vehicles), may have investment mandates and objectives that target the same investments as us.

In addition, NSAM may have additional managed companies or strategic vehicles that will compete directly with us for investment opportunities in the future. We adopted an investment allocation policy with NSAM that is intended to ensure that investments are allocated fairly and appropriately among us and the other NSAM managed companies or strategic vehicles over time, but there is no assurance that NSAM will be successful in eliminating the conflicts arising from the allocation of investment opportunities. When determining the entity for which an investment opportunity would be the most suitable, the factors that NSAM may consider include, among other factors, the following:

• | investment objectives, strategy and criteria; |

• | cash requirements and amount of funds available; |

• | effect of the investment on the diversification of the portfolio, including by geography, size of investment, type of investment and risk of investment; |

• | leverage policy and the availability of financing for the investment by each entity; |

• | anticipated cash flow of the investment to be acquired; |

• | income tax effects of the purchase; |

• | the size of the investment; |

• | cost of capital; |

• | risk return profiles; |

• | targeted distribution rates; |

• | anticipated future pipeline of suitable investments; |

• | the expected holding period of the investment and the remaining term of the NSAM managed company, if applicable; |

• | affiliate and/or related party considerations; and |

• | whether a strategic vehicle has received a special allocation (as defined in the investment allocation policy). |

If, after consideration of the relevant factors, NSAM determines that an investment is equally suitable for us and one of its managed companies or strategic vehicles, the investment will be allocated among each of the applicable entities, including us, on a rotating basis. New NSAM clients, including us, will be initially added at the end of the rotation. If, after an investment has been allocated to us or any other entity, a subsequent event or development, such as delays in structuring or closing on the investment, makes it, in the opinion of NSAM, more appropriate for a different entity to fund the investment, NSAM may determine to place the investment with the more appropriate entity while still giving credit to the original allocation. In certain situations, NSAM may determine to allow more than one investment vehicle, including us, to co-invest in a particular investment.

There is no assurance this policy will remain in place during the entire period we are seeking investment opportunities. In addition, NSAM may sponsor additional managed companies or strategic vehicles in the future and, in connection with the creation of such managed companies or strategic vehicles, may revise these allocation procedures. The result of a revision to the allocation procedures may, among other things, be to increase the number of parties who have the right to participate in investment opportunities sourced by NSAM or us, thereby reducing the number of investment opportunities available to us.

In addition, under this policy, NSAM investment professionals may consider the investment objectives and anticipated pipeline of future investments of its managed companies or strategic vehicles. The decision of how any potential investment should be allocated among us and one of NSAM’s managed companies or strategic vehicles for which such investment may be suitable may, in many cases, be a matter of subjective judgment which will be made by NSAM. Pursuant to the investment allocation policy, NSAM may choose to allocate favorable investments to its other managed companies instead of to us. Our investment allocation policy with NSAM could produce unfavorable results for us that could harm our business.

NSAM also has acquired and may in the future acquire additional interests in third parties, such as management firms that manage certain of our properties, which may cause its interests to differ from ours. NSAM may also encourage our use of third party service providers, including those in which NSAM owns an interest, for which we pay a fee. In addition, we may enter into principal transactions or cross transactions with NSAM’s other managed companies or strategic vehicles. For certain transactions, for which NSAM may receive a fee from the managed company. There is no guaranty that any such transactions will be favorable to us. Because our interests and NSAM’s interests may not be aligned, we may face conflicts of interest that result in action or inaction that is detrimental to us.

15

Further, there are conflicts of interest that arise when NSAM makes expense allocation determinations, as well as in connection with any fees payable between us and NSAM. These fees and allocation determinations are sometimes based on estimates or judgments, which may not be correct and could result in NSAM’s failure to allocate and pay certain fees and costs to us appropriately.

NSAM’s professionals who perform services for us face competing demands relating to their time and conflicts of interests relating to performing services on our behalf, which may cause our operations to suffer.

We rely on NSAM’s professionals to perform services related to the operation of our business. NSAM professionals performing services for us also perform services for NSAM’s other managed companies. As a result of their interests in NSAM, other managed companies and the fact that they engage in other business activities on behalf of others, these individuals may face conflicts of interest in allocating their time among us, NSAM and other managed companies and other business activities in which they are involved. In addition, certain management personnel performing services on behalf of NSAM own equity interests in NSAM or other managed companies and NSAM may grant additional equity interests in NSAM or other managed companies to such persons in connection with their continued services. These conflicts of interest, as well as the loyalties of these individuals to other entities and investors, could result in action or inaction that is detrimental to our business, which could harm the implementation of our business strategy and our investment opportunities. If we do not successfully implement our business strategy, we may be unable to generate the cash needed to make distributions to our stockholders or to maintain or increase the value of our investments.

Further, at times when there are turbulent conditions in the real estate markets or distress in the credit markets or other times when we will need focused support and assistance from NSAM, NSAM’s other managed companies may likewise require greater focus and attention, placing NSAM’s resources in high demand. In such situations, we may not receive the level of support and assistance that we may receive if we were internally managed or if NSAM did not act as a manager for other entities.

Our executive officers are employees of NSAM and face conflicts of interest related to their positions and interests in NSAM, which could hinder our ability to implement our business strategy.

Our executive officers are employees of NSAM and provide services to us solely in such capacity pursuant to NSAM’s obligations to us under the management agreement. We do not have employment agreements with any of our executive officers. If the management agreement with NSAM were to be terminated, we would lose the services of all our executive officers and other NSAM investment professionals acting on our behalf. Furthermore, if any of our executive officers ceased to be employed by NSAM, such individual would also no longer serve as one of our executive officers. NSAM is an independent contractor and controls the activities of its employees, including our executive officers. Our executive officers therefore owe duties to NSAM and its stockholders, which may from time-to-time conflict with the duties they owe to us and our stockholders. In addition, our executive officers may also own equity in NSAM or its other managed companies. As a result, the loyalties of these individuals to other entities and investors could result in action or inaction that is detrimental to our business, which could harm the implementation of our business strategy and our investment opportunities.

Both our board of directors and NSAM’s board of directors have adopted, and will likely in the future adopt, certain incentive plans to create incentives that will allow us and NSAM to retain and attract the services of key employees. These incentive plans may be tied to the performance of our common stock or NSAM’s common stock and a decline in stock price, like we have recently experienced, may result in us or NSAM being unable to motivate and retain our management and these other employees. Our inability to motivate and retain these individuals could also harm our business and our prospects. Additionally, competition for experienced real estate professionals could require NSAM or us to pay higher wages and provide additional benefits to attract qualified employees, which could result in higher compensation expenses to us.

We may not realize the anticipated benefits of our manager’s strategic partnerships and joint ventures.

NSAM may enter into strategic partnerships and joint ventures to further its own interests or the interests of its managed companies, including us. NSAM may not be able to realize the anticipated benefits of these strategic partnerships and joint ventures. These strategic partnerships and/or joint ventures may also subject NSAM and its managed companies, including us, to additional risks and uncertainties, as NSAM and its managed companies, including us, may be dependent upon, and subject to, liability, losses or reputational damage relating to systems, control and personnel that are not under NSAM’s control. In addition, where NSAM does not have a controlling interest, it may not be able to take actions that are in our best interests due to a lack of full control. Furthermore, to the extent that NSAM’s partners provide services to us, certain conflicts of interests may exist. Moreover, disagreements or disputes between NSAM and its partners could result in litigation, which could potentially distract NSAM from our business.

NSAM manages our portfolio pursuant to very broad investment guidelines and our board of directors does not approve each investment and financing decision made by NSAM unless required by our investment guidelines.

NSAM is authorized to follow very broad investment guidelines established by our board of directors. Our board of directors periodically reviews our investment guidelines and our investment portfolio but does not, and is not be required to, review all of our proposed investments, except in limited circumstances as set forth in our investment guidelines. Our board of directors may

16

also make modifications to our investment guidelines from time to time as it deems appropriate. In addition, in conducting periodic reviews or modifying our investment guidelines, our board of directors may rely primarily on information provided to them by NSAM. Furthermore, transactions entered into by NSAM on our behalf may be costly, difficult or impossible to unwind by the time they are reviewed by our board of directors. NSAM has flexibility within the broad parameters of our investment guidelines in determining the types and amounts of investments in which to invest on our behalf, including making investments that may result in returns that are substantially below expectations or result in losses, which could materially and adversely affect our business and results of operations, or may otherwise not be in the best interests of our stockholders.

NSAM’s liability is limited under the management agreement and we have agreed to indemnify NSAM against all liabilities incurred in accordance with and pursuant to the management agreement.

We have entered into a management agreement with NSAM, which governs our relationship with NSAM. Our manager maintains a fiduciary relationship with us. Under the terms of the management agreement, and subject to applicable law, NSAM, its directors, officers, employees, partners, managers, members, controlling persons, and any other person or entity affiliated with NSAM are not liable to us or our subsidiaries for acts taken or omitted to be taken in accordance with and pursuant to the management agreement, except those resulting from acts of willful misfeasance or bad faith in the performance of NSAM’s duties under the management agreement. In addition, subject to applicable law, we have agreed to indemnify NSAM and each of its directors, officers, employees, partners, managers, members, controlling persons and any other person or entity affiliated with NSAM from and against any claims or liabilities, including reasonable legal fees and other expenses reasonably incurred, arising out of or in connection with NSAM’s performance of its duties or obligations under the management agreement or otherwise as our manager, except where attributable to acts of willful misfeasance or bad faith in the performance of NSAM’s duties under the management agreement.

NSAM is subject to extensive regulation as an investment adviser in the United States and as a fund services business in the Bailiwick of Jersey and under the Business Investment Act of Bermuda, which could adversely affect its ability to manage our business.