Attached files

| file | filename |

|---|---|

| 8-K - INLAND REAL ESTATE INCOME TRUST, INC. - FORM 8-K - 3/24/16 - Inland Real Estate Income Trust, Inc. | ireit-8k.htm |

Exhibit 99.1

inland - investments.com 1 Inland Real Estate Income Trust, Inc. THIS IS NEITHER AN OFFER TO SELL NOR A SOLICITATION OF AN OFFER TO BUY THE SECURITIES DEPICTED HEREIN. THE OFFERING IS MADE ONLY BY THE PROSPECTUS. 2015 Q4 Results Webcast Thursday, March 24, 2016 • 1:00 pm CT Audio is available via webcast – dial in number not required. i nland - investments.com

inland - investments.com 2 Disclaimer This material is neither an offer to sell nor the solicitation of an offer to buy any security, which can be made only by the pros pec tus, which has been filed or registered with appropriate state and federal regulatory agencies, and sold only by broker dealers authoriz ed to do so. No regulatory agency has passed on or endorsed the merits of this offering. Any representation to the contrary is u nla wful. Past performance is not a guarantee of future results. When making an investment decision in Inland Real Estate Income Trust, Inc. (“Inland Income Trust”), investors should not rely on past performance of the real estate investment trusts (“REITs”) or re al estate programs sponsored by Inland Real Estate Investment Corporation (“Inland Investments”). An investment in Inland Income Trust wil l not entitle an investor to ownership in any other REIT or investment program sponsored by Inland Investments. Inland Income Trust is a part of The Inland Real Estate Group of Companies, Inc. The companies depicted in the logos in this presentation are tenants of Inland Income Trust. The companies depicted in the photographs and logos in this presentation may have proprietary interests in their trademarks and trade names and nothing her ein shall be considered an endorsement, authorization or approval of Inland Income Trust or its subsidiaries. The Inland name and logo are registered trademarks being used under license. This material has been distributed by Inland Securities Corporation, dealer manager for Inland Income Trust. Inland Securities Corporation, member FINRA/SIPC. Publication Date: 3/24/2016

inland - investments.com 3 Risk Factors Some of the risks related to investing in commercial real estate include, but are not limited to: market risks such as local pro perty supply and demand conditions; tenants’ inability to pay rent; tenant turnover; inflation and other increases in operating cos ts; adverse changes in laws and regulations; relative illiquidity of real estate investments; changing market demographics; acts of God s uch as earthquakes, floods or other uninsured losses; interest rate fluctuations; and availability of financing. An investment in Inland Income Trust’s shares involves significant risks. If Inland Income Trust is unable to effectively man age these risks, it may not meet its investment objectives and investors may lose some or all of their investment. Some of the risks re lat ed to investing in Inland Income Trust include, but are not limited to: the board of directors, rather than the trading market, det erm ines the offering price of shares; there is limited liquidity because shares are not bought and sold on an exchange; repurchase progra ms may be modified or terminated; a typical time horizon for an exit strategy may be longer than five years; there is no guarantee t hat a liquidity event will occur; distributions cannot be guaranteed and may be paid from sources other than cash flow from operati ons , including borrowings and net offering proceeds; and failure to continue to qualify as a REIT and thus being required to pay f ede ral, state and local taxes. Please consult Inland Income Trust’s most recent Annual Report on Form 10 - K and any subsequent Quarterly Reports on Form 10 - Q for more information on the specific risks.

inland - investments.com 4 Forward - Looking Statements In addition to historical information, this webcast contains "forward - looking statements" made under the "safe harbor" provision s of the Private Securities Litigation Reform Act of 1995. The statements may be identified by terminology such as "may," “can,” "would, " “will,” "expect," "intend," "estimate," "anticipate," "plan," "seek," "appear," or "believe." Such statements reflect the current view of Inland Income Trust with respect to future events and are subject to certain risks, uncertainties and assumptions related to certain fa ctors including, without limitation, the uncertainties related to general economic conditions, unforeseen events affecting the real es tate industry or particular markets, and other factors detailed under Risk Factors in our most recent Form 10 - K and subsequent Form 10 - Qs on file with the Securities and Exchange Commission. Although Inland Income Trust believes that the expectations reflected in such forward - looking statements are reasonable, it can give no assurance that such expectations will prove to be correct. You s hould exercise caution when considering forward - looking statements and not place undue reliance on them. Based upon changing conditions, should any one or more of these risks or uncertainties materialize, or should any underlying assumptions prove in cor rect, actual results may vary materially from those described herein. Except as required by federal securities laws, Inland Income Tr ust undertakes no obligation to publicly update or revise any written or oral forward - looking statements, whether as a result of new information, future events, changed circumstances or any other reason after the date of this webcast.

inland - investments.com On Today’s Call 5 Mitchell Sabshon Chief Executive Officer JoAnn McGuinness President and Chief Operating Officer David Lichterman Vice President, Chief Accounting Officer & Treasurer

inland - investments.com 6 Inland Income Trust Highlights

inland - investments.com 7 Key Multi - Tenant Retail Attributes 1 Statista . Consumers’ weekly grocery shopping trips in the United States from 2006 to 2015 1

inland - investments.com 8 As of December 31 , 2015 Total Number of Properties: 54 Total Square Feet: 6,025,330 Number of States: 22 Economic Occupancy: 97.2% Physical Occupancy : 96.2% Number of Tenants: 668 Annualized Distribution Rate: 6.0% The 6 . 0 % annualized distribution rate is based on a $ 10 share price, is payable monthly and is not guaranteed and may be modified at any time . As of December 31 , 2015 , approximately 37 % of distributions paid to stockholders of record since inception ( 10 / 18 / 2012 ) were paid from the net proceeds of Inland Income Trust’s “best efforts” offering (return of capital), and approximately 63 % of distributions were paid from cash flow from operations (may be return of capital) and sponsor contributions . When Inland Income Trust makes cash distributions using offering or financing proceeds, it will have less proceeds to invest in properties, and this may lower its overall return potential . The Headline Numbers White City Shopping Center Shrewsbury, Massachusetts

inland - investments.com Top 10 Tenants 9 Top 10 Tenants as of December 31, 2015 Number of Leases % of ABR* Dick's Sporting Goods 5 3.4% Kroger 3 3.4% T.J.Maxx/HomeGoods/Marshalls 11 3.0% Petsmart 8 2.7% Albertsons/Jewel/Shaws 2 2.4% Ulta 9 2.3% Kohl’s 4 2.2% Ross Dress for Less 7 2.1% LA Fitness 2 2.1% Giant Eagle 1 2.1% *Annualized Base Rent

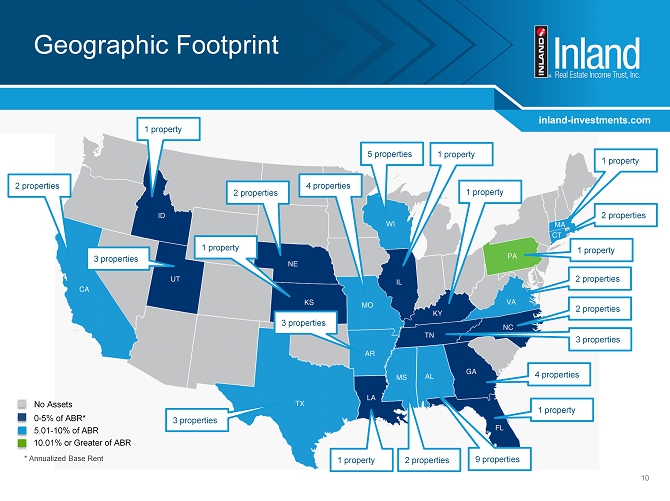

inland - investments.com 10 Geographic Footprint 3 properties 1 property 2 properties 4 properties 5 properties 1 property 1 property 3 properties 3 properties 3 properties 1 property 2 properties 1 property 1 property 1 property 2 properties 2 properties 4 properties 9 properties No Assets 0 - 5% of ABR* 5.01 - 10% of ABR 10.01% or Greater of ABR * Annualized Base Rent 1 property 2 properties 2 properties

inland - investments.com Fourth Quarter Acquisition Highlight 11 Marketplace at Tech Center Newport News, Virginia Marketplace at Tech Center Newport News, Virginia Transaction Date: December 24, 2015 Transaction Price: $72.5 Million Leasable Area: 210,584 SF Portfolio Sector: Retail Tenants: ▪ Whole Foods ▪ Stein Mart

inland - investments.com Additional Acquisitions 12 Property: Milford Marketplace Market: Milford, Connecticut Acquisition Date: October 1, 2015 Acquisition Price: $34.0 Million Leasable Area: 112,257 SF Tenants: Whole Foods, JoS. A. Bank, Ann Taylor’s Loft Property: Settlers Ridge Market: Pittsburgh, Pennsylvania Acquisition Date: October 1, 2015 Acquisition Price: $139.1 Million Leasable Area: 472,572 SF Tenants: Giant Eagle, Cinemark Theaters, REI Property: Marketplace at El Paseo Market: Fresno, California Acquisition Date: October 16, 2015 Acquisition Price: $70 Million Leasable Area: 224,683 SF Tenants: Marshalls, Burlington, Ross Dress for Less

inland - investments.com Capturing Value Through NOI Growth 13 2015 2016 2017 2018 Multi-Tenant Retail NOI Growth* 3.50% 3.20% 3.10% 2.70% CPI Forecast** 2.00% 2.10% 2.20% 2.40% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% Forecasted NOI Growth Rates, Multi - Tenant Retail *Source: Green Street Advisors **Source: Congressional Budget Office

inland - investments.com Consolidated Financial Highlights December 31, 2015 (in thousands) December 31,2014 (in thousands) Total Assets: $1,405,835 $571,486 Stockholders’ Equity: $690,844 $351,459 Distributions Paid: $42,537 $10,597 Cash Flow Provided by Operations: $27,080 $2,922 GAAP Net Loss : $(13,436) $(4,356 ) Funds from Operations (“FFO”) (1): $21,137 $3,323 Modified Funds from Operations (“MFFO”) (2) : $32,652 $8,089 For the year ended December 31, 2015, approximately 29% of the distributions paid to stockholders of record were paid from the net proceeds of Inland Income Trust’s “best efforts” offering (return of capital ), 7% from Sponsor contributions and approximately 64% were paid from cash flow from operations (may be return of capital). For the year ended December 31, 2014, approximately 66% of th e distributions paid to stockholders of record were paid from the net proceeds of Inland Income Trust’s “best efforts” offering (r eturn of capital), 6% from Sponsor contributions and approximately 28% were paid from cash flow from operations (may be return of capi tal ). When Inland Income Trust makes cash distributions using offering or financing proceeds it will have less proceeds to invest i n p roperties and this may lower its overall return potential. Year - Ended 12/31/15 (in thousands) Year - Ended 12 /31/14 (in thousands) GAAP Net loss $(13,436) $(4,356) Add: Depreciation and amortization related to investment properties 34,573 7,679 Funds from operations (FFO) $21,137 $3,323 Add: Acquisition related costs 13,903 5,139 Less: Amortization of acquired market lease intangibles, net (652) (59) Straight - line rental income (1,736) (314) Modified funds from operations (MFFO) $32,652 $8 ,089 Inland Real Estate Income Trust, Inc . FFO and MFFO for the years ended December 31 , 2015 and 2014 , calculated on page 45 of the Form 10 - K, is as follows : 1 – Funds from Operations (“FFO”) : A widely accepted and reported supplemental measure of REIT operating performance . As defined by the National Association of Real Estate Investment Trusts, FFO is equal to a REIT’s net income computed in accordance with U . S . GAAP, excluding gains or losses from sales of property, and adding back real estate depreciation and amortization, real estate impairment charges, and after adjustments for unconsolidated partnerships and joint ventures in which the REIT holds an interest . 2 – Modified Funds from Operations (“MFFO”) : An industry accepted and reported supplemental measure of publicly registered non - listed REIT’s operating performance . As defined by Investment Program Association, an industry trade group, MFFO is equal to a REIT’s FFO, further adjusted for the following items, as applicable, included in the determination of U . S . GAAP net income : acquisition fees and expenses ; amounts relating to deferred rent receivables and amortization of above and below market lease assets and liabilities, accretion of discounts and amortization of premiums on debt investments ; mark - to - market adjustments included in net income ; nonrecurring gains or losses included in net income from the extinguishment or sale of debt, hedges, foreign exchange, derivatives or securities holdings where trading of such holdings is not a fundamental attribute of the business plan, unrealized gains or losses resulting from consolidation from, or deconsolidation to, equity accounting, and after adjustments for consolidated and unconsolidated partnerships and joint ventures . 14

inland - investments.com Mortgages and Credit Facility Payable 15 December 31, 2015 (in thousands) December 31, 2014 (in thousands) Mortgages Payable (excludes unamortized fair value adjustment related to assumed debt) : $484,995 $184,737 Credit Facility Payable: $100,000 - Ratio of Total Mortgages and Credit Facility Payable to Total Assets: 41.9% 32.3% Annual Weighted Average Interest Rate on Mortgages Payable: 3.77% 3.02% Annual Weighted Average Interest Rate on Credit Facility Payable: 1.65% - Scheduled Maturities of Mortgages and Credit Facility Payable As of December 31, 2015 (in thousands) 0 50,000 100,000 150,000 200,000 250,000 300,000 2016 2017 2018 2019 2020 Thereafter Mortgages Payable Credit Facility Payable

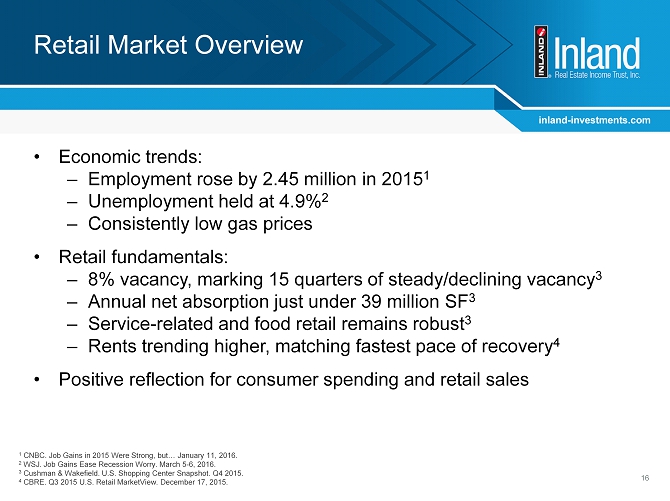

inland - investments.com Retail Market Overview 16 1 CNBC. Job Gains in 2015 Were Strong, but… January 11, 2016. 2 WSJ. Job Gains Ease Recession Worry. March 5 - 6, 2016. 3 Cushman & Wakefield. U.S. Shopping Center Snapshot. Q4 2015. 4 CBRE. Q3 2015 U.S. Retail MarketView. December 17, 2015. • Economic trends: – Employment rose by 2.45 million in 2015 1 – Unemployment held at 4.9% 2 – Consistently low gas prices • Retail fundamentals: – 8% vacancy, marking 15 quarters of steady/declining vacancy 3 – Annual net absorption just under 39 million SF 3 – Service - related and food retail remains robust 3 – Rents trending higher, matching fastest pace of recovery 4 • Positive reflection for consumer spending and retail sales

inland - investments.com Regulatory Changes 17 • Recent amendments to FINRA regulations will : – Require broker - dealers to provide per share estimated values on customer account statements earlier in lifecycle of nonlisted REITs – Provide greater consistency in per share estimated values – Enhance fee and expense transparency • Specific disclosures are required to be on customer statements in close proximity to the estimated per share values • Inland Income Trust, with the assistance of a nationally recognized, independent real estate advisory firm, will publish in 2Q 2016 a per share estimated value consistent in methodology and timing with the new FINRA regulation* * There is no assurance that the methodology will be acceptable to FINRA or under ERISA or the Internal Revenue Code for comp lia nce with reporting requirements.

inland - investments.com Benefits to Investors 18

inland - investments.com Questions?