Attached files

| file | filename |

|---|---|

| EX-10.23 - CONSULTING AGREEMENT - Lifeway Foods, Inc. | exh10-23_17915.htm |

| EX-10.25 - STOCK PURCHASE AGREEMENT - Lifeway Foods, Inc. | exh10-25_17915.htm |

| EX-10.24 - ENDORSEMENT AGREEMENT - Lifeway Foods, Inc. | exh10-24_17915.htm |

| EX-31.2 - CERTIFICATION - Lifeway Foods, Inc. | exh31-2_17915.htm |

| EX-21 - SUBSIDIARIES OF LIFEWAY FOODS, INC. - Lifeway Foods, Inc. | exh21_17915.htm |

| EX-32.2 - CERTIFICATION - Lifeway Foods, Inc. | exh32-2_17915.htm |

| EX-32.1 - CERTIFICATION - Lifeway Foods, Inc. | exh32-1_17915.htm |

| EX-31.1 - CERTIFICATION - Lifeway Foods, Inc. | exh31-1_17915.htm |

| EX-99.1 - PRESS RELEASE - Lifeway Foods, Inc. | ex99-1_17915.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

Commission file number: 000-17363

LIFEWAY FOODS, INC.

(Name of registrant as specified in its charter)

Illinois | 36-3442829 |

(State or other jurisdiction of | (IRS Employer |

incorporation or organization) | Identification No.) |

6431 West Oakton St., Morton Grove, Illinois 60053

(Address of principal executive offices) (Zip Code)

(847) 967-1010

(Registrant's telephone number, including area code)

Securities registered under Section 12(b) of the Exchange Act:

Title of Each Class | Name of each exchange on which registered |

|

|

Common Stock, No Par Value | Nasdaq Global Market |

Securities registered under Section 12(g) of the Exchange Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T(§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer þ | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the stock was last sold as of June 30, 2015 ($19.19 per share as quoted on the Nasdaq Global Market) was $91,167,353.

As of March 1, 2016 16,188,376 shares of the registrant's common stock, no par value, were outstanding.

Portions of the Registrant's Proxy Statement for the Annual Meeting of Shareholders to be held on June 17, 2016, are incorporated by reference into Part III.

Table of Contents

Pagination to be updated

PART I | |||

Item 1. | Business | 4 | |

Item 1A. | Risk Factors | 8 | |

Item 1B. | Unresolved Staff Comments | 15 | |

Item 2. | Properties | 15 | |

Item 3. | Legal Proceedings | 15 | |

Item 4. | Mine Safety Disclosures | 15 | |

PART II | |||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 16 | |

Item 6. | Selected Financial Data | 18 | |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 19 | |

Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | 26 | |

Item 8. | Financial Statements and Supplementary Data | 27 | |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 47 | |

Item 9A. | Controls and Procedures | 48 | |

Item 9B. | Other Information | 50 | |

PART III | |||

Item 10. | Directors, Executive Officers and Corporate Governance | 51 | |

Item 11. | Executive Compensation | 51 | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 51 | |

Item 13. | Certain Relationships and Related Transactions and Director Independence | 51 | |

Item 14. | Principal Accountant Fees and Services | 51 | |

PART IV | |||

Item 15. | Exhibits, Financial Statement Schedules | 52 | |

Signatures | 56 | ||

Index of Exhibits | 57 | ||

| 2 |

FORWARD LOOKING STATEMENTS

In connection with the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995, readers of this document and any document incorporated by reference herein, are advised that this document and documents incorporated by reference into this document contain both statements of historical facts and forward looking statements. Forward looking statements are subject to certain risks and uncertainties, which could cause actual results to differ materially from those indicated by the forward looking statements. Examples of forward looking statements include, but are not limited to, (i) projections of revenues, income or loss, earnings or losses per share, capital expenditures, dividends, capital structure and other financial items, (ii) statements of Lifeway Foods, Inc.'s ("Lifeway" or the "Company") plans and objectives, including the introduction of new products, or estimates or predictions of actions by customers, suppliers, competitors or regulatory authorities, (iii) statements of future economic performance, and (iv) statements of assumptions underlying other statements and statements about Lifeway or its business.

This document and any documents incorporated by reference herein also identify important factors which could cause actual results to differ materially from those indicated by forward looking statements. These risks and uncertainties include

● | price competition; |

● | the decisions of customers or consumers; |

● | the actions of competitors; |

● | changes in the pricing of commodities; |

● | the effects of government regulation; |

● | possible delays in the introduction of new products; |

● | customer acceptance of products and services; and |

● | the other risks and uncertainties that are set forth in Item 1, "Business", Item 1A "Risk Factors" and Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations". |

These factors are not necessarily all of the important factors that could cause actual results to differ materially from those expressed in any of our forward-looking statements. Other unknown or unpredictable factors could also have material adverse effects on future results. Except as otherwise required to be disclosed in periodic reports required to be filed by public companies with the Securities and Exchange Commission ("SEC") pursuant to the SEC's rules, we have no duty to update these statements, and we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

| 3 |

PART I

ITEM 1 BUSINESS

OVERVIEW

Lifeway Foods, Inc. (the "Company" or "Lifeway") was co-founded in 1986 by Michael and Ludmila Smolyansky shortly after their emigration from Russia to the United States. Mr. and Mrs. Smolyansky were the first to successfully introduce Kefir to the U.S. consumer on a commercial scale, initially catering to ethnic consumers in the Chicago metropolitan area. In the thirty years that have followed, Lifeway has grown to become the largest producer and marketer of Kefir in the U.S. and an important player in the broader market spaces of probiotic-based products and natural, "better for you" foods.

PRODUCTS

Lifeway's primary product is drinkable kefir, a fermented dairy product. Kefir has a tart and tangy taste similar to yogurt and the consistency of a smoothie. Kefir also has a slightly effervescent quality all its own. Unlike yogurt though, Lifeway incorporates a unique blend of probiotic kefir cultures in the fermentation process. The probiotic feature, in concert with the base-line nutritional value of a staple beverage that is high in protein, calcium and vitamin D, and low in calories, presents a unique and differentiated taste profile that we believe appeals to a broad and growing demographic.

Because of its drinkable feature, kefir requires no spoon and is ideal for on-the-go consumption … straight from the bottle. Lifeway's Kefir is commonly consumed as part of a healthy breakfast or as an "any-time, better for you" snack in its native form or as a smoothie input. Kefir also serves as a base for lower-calorie dressings, dips, marinades, soups or sauces and as a basic ingredient in other healthy, home-prepared foods. Recipes are made available through the company's website.

In addition to the drinkable kefir that we broadly market to consumers of all ages, we also market and sell our ProBugs line of drinkable kefir which is delivered in our proprietary non-spill pouches (and in 3.5 oz. bottles) intended for children with caring, health-conscious parents. Our frozen kefir offers a nutritional profile similar to our drinkable kefir but in a frozen bar and pint size container conventionally thought of as an indulgent treat. In addition to kefir, Lifeway produces a variety of Kefir-based Eastern European style soft cheeses.

Gross sales of products by category were as follows for the years ended December 31:

| 2015 |

|

| 2014 |

|

| 2013 |

| ||||||||||||||||

In thousands |

| $ |

|

| % |

|

| $ |

|

| % |

|

| $ |

|

| % |

| ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Drinkable Kefir other than ProBugs |

|

| 118,090 |

|

|

| 86.0 | % |

|

| 110,297 |

|

|

| 84.7 | % |

|

| 90,441 |

|

|

| 83.0 | % |

ProBugs drinkable Kefir |

|

| 7,936 |

|

|

| 5.8 | % |

|

| 7,868 |

|

|

| 6.0 | % |

|

| 7,127 |

|

|

| 6.5 | % |

Lifeway cheese products |

|

| 9,725 |

|

|

| 7.1 | % |

|

| 10,266 |

|

|

| 7.9 | % |

|

| 9,388 |

|

|

| 8.6 | % |

Frozen Kefir |

|

| 1,493 |

|

|

| 1.1 | % |

|

| 1,785 |

|

|

| 1.4 | % |

|

| 2,010 |

|

|

| 1.9 | % |

Gross Sales |

|

| 137,244 |

|

|

| 100 | % |

|

| 130,216 |

|

|

| 100 | % |

|

| 108,966 |

|

|

| 100 | % |

Product innovation and new product development

The company is committed to maintaining its position as the leading producer of Kefir and routinely evaluates opportunities for new product flavors and formulations, improved package design, new product configurations and other forms of routine innovation. As of December 31, 2015 the company offered over 50 unique varieties of its Kefir product including more than 20 unique flavors delivered to consumers on three different milk platforms (fat- free, 1% and whole milk) as well as in both organic and conventional ingredient profiles. During 2015 our routine innovations led to the introduction of several new items, including our new 16 ounce protein enhanced Kefir aimed at the fitness-oriented consumer looking to incorporate more protein into their diets.

Beyond routine innovation, the company has an on-going effort to extend the strength of the Lifeway brand and leverage the capabilities of the Lifeway organization into categories outside of the dairy aisle including into non-food categories. Though we have not yet delivered a product to the market place that has clear commercial viability, our efforts will continue.

The company's innovation, research and development efforts are largely accomplished leveraging an intuitive entrepreneurial, unstructured approach; not a highly formalized, distinct "R&D" function commonly found with large food processors. Research and development costs are not significant.

| 4 |

Product Quality Assurance

The Company employs many skilled production managers across its three Kefir producing facilities who closely monitor our kefir-production process. The production managers have a complement of deep capabilities that spans from traditional dairy operations to the artisan, old-world practices first introduced by Michael and Ludmila Smolyansky at the inception of the Company. We conduct routine tests, tastings and evaluations to ensure that each batch of kefir conforms to the Company's product quality and safety standards. The Company leverages both on-site and third party quality control labs.

The Company includes a clearly legible "freshness" code on every Kefir product in order to ensure that our customers enjoy only the freshest products. To maintain the best of product freshness in the channel, we expect our channel customers (a) to ensure that our products are delivered directly to the retailer's dairy cooler and (b) to rotate such product in a routine and timely way. Due to the perishable nature of our products and the costs associated with moving product back through the channel, the Company does not offer return privileges to any of its channel customers; however, from time to time we do provide our customers with allowances for non-saleable product.

DISTRIBUTION

Lifeway's products reach the consumer through three primary "route-to-market" pathways:

- Direct store delivery ("DSD");

- Retail-direct; and,

- Distributor.

Under the direct store delivery (DSD) route to market, we distribute our products directly to the grocer's dairy cooler using a fleet of company-owned vehicles and a team of seasoned Lifeway merchandisers who engage face-to-face with store management to ensure optimal product assortments and presentation. We operate our DSD model in the Chicago metropolitan area only. Sales to our DSD customers represents less than10% of total company net sales.

Under the retail-direct channel, our products are sold to the retailer and shipped to that retailer's distribution center. In turn our retail customer then delivers the product to their respective stores within their chain. Customers in this route-to-market grouping include among others Kroger, Wal Mart and Costco. Under the retail direct model, optimal product merchandising, assortments and product presentation are attended to by the retailer with support from Lifeway's broker network. Sales to our retail-direct customers represents about 50% of total company net sales.

Under the distributor channel, our products are sold to distributors and shipped to that distributors designated warehouse. In turn, our distributor customers then sell the product to their retail customers and ship the products to their retail customers. Our distributors often use a DSD model of their own to make deliveries directly to individual stores but also make deliveries to the retailer's warehouse. Our distributor customers include among others United Natural Foods, Kehe Foods and C&S Wholesale. Optimal product merchandising, assortments and product presentation at the retail end of the channel are attended to by the distributor with support from Lifeway's broker network. Sales to our distributor customers represents about 40% of total company net sales.

Distribution outside of the U.S.

Substantially all of Lifeway's products are distributed within the United States; however, certain of our distributors sell our products to retailers in Mexico, Costa Rica, Dubai, Hong Kong, China, and the Caribbean. Additionally, the company's products reach a small number of consumers across Canada and in London, England under third party co-manufacturing agreements and in-country distributor arrangements.

5 |

Distribution arrangements

Beyond the customer's purchase order, we do not have written agreements with our distributors. Consequently we believe that our arrangements with distributors allow us the latitude to establish new relationships with distributors as the need arises. Lifeway does not offer exclusive territories to any of its distributors.

Distributors are provided Lifeway products at wholesale prices for distribution to their retail accounts. Lifeway believes that the price at which its products are sold to its distributors is competitive with the prices generally paid by distributors for similar products in the markets served. Each distributor carries a line of Lifeway's products on its trucks, checks the retail stores for space allocated to Lifeway's products, determines inventory requirements of the store and places Lifeway products directly into the retailers' dairy cases. Lifeway believes this method of distribution best serves the needs of each retail store, and is the best available means to ensure consistency and quality of product handling, quality control, flavor selection and favorable retail display.

MARKETING

The Company engages in an on-going and wide variety marketing and media campaigns - primarily digital and social media, print advertising in some newspapers and magazines and to a lesser extent television advertising. These marketing and media efforts are complemented by participation in sponsorships of cultural and community events, various festivals, industry-related trade shows and in-store promotional events. Our marketing efforts also include co-op advertising programs with our retail customers and various couponing campaigns.

Our marketing efforts are aimed at stimulating demand with our existing consumers and at driving trial with new consumers by elevating Kefir awareness. Our Kefir awareness marketing seeks to promote the verifiable nutritional profile, purity and good taste of our Kefir and to promote the common perception that our products may have a particular health benefit, such as promoting digestion.

COMPETITION

Lifeway competes with a limited number of other domestic kefir producers and consequently faces a small amount of direct competition for kefir products; however, Lifeway's kefir-based products compete with other dairy products, notably yogurt. Many producers of yogurt and other dairy products are well-established and have significantly greater financial resources than Lifeway to promote their products.

SUPPLIERS

We purchase our ingredients such as raw milk, cane and other forms of sugar and packaging materials from unaffiliated suppliers. Lifeway is not limited or contractually bound to any supplier beyond the terms of our purchase orders, which generally do not exceed our expected demand for periods more than one year. Lifeway has ready access to multiple suppliers for all of its ingredients and packaging requirements.

| 6 |

MAJOR CUSTOMERS

During the year ended December 31, 2015 one distributor, United Natural Foods, Inc., represented approximately 19% of the Company's total sales and one retail customer, Kroger, represented approximately 7% of the Company's total sales. These customers collectively accounted for approximately 19% of accounts receivable as of December 31, 2015.

SEGMENTS

The Company has determined that it has one reportable segment based on how the Company's chief operating decision maker manages the business and in a manner consistent with the internal reporting provided to the chief operating decision maker. The chief operating decision maker, who is responsible for allocating resources and assessing company performance, has been identified collectively as the Chief Financial Officer, the Chief Executive Officer and Chairman of the board of directors. Substantially all of the consolidated revenues of the Company relate to the sale of fermented dairy products which are produced using the same processes and materials and are sold to consumers through a network of distributors and retailers in the United States.

GROUPE DANONE SA

Since October, 1999 Groupe Danone SA has been the beneficial owner of approximately 20% of the outstanding common stock of Lifeway. Lifeway and Danone are parties to a Stockholders' Agreement dated October 1, 1999, which as amended provides Danone the right to nominate one director, provides Danone with anti-dilutive rights relating to future offerings and grants Danone limited registration rights.

Danone's interest as of December 31, 2015 was approximately 21%.

PATENTS, TRADEMARKS, LICENSES, ROYALTY AGREEMENTS

The Company has obtained United States trademark registrations for over 20 trademarks, including ProBug Design 1, ProBug Design 2, Penelope ProBug Design, BA3APHBIII (a Stylized presentation of "bazarny" in Cyrillic characters), Bambino, Bazarny, Bio Kefir, Goo-Berry Pie, Helios Nutrition, Korovka, KPECTBRHCKNN (a Stylized presentation of "krestyanskiy" in Cyrillic characters-means "peasant"), Kwashenka, La Fruta, Lifeway, Orange Creamy Crawler, Phytoboost, Playgroup Pack, Pride of Main Street, PRO2O, ProBugs, Starfruit, Sublime Slime Lime and Sweet Kiss.

Lifeway also claims common law rights to, the following unregistered trademarks: "Elita," "Healthy Foods Today for a Better Life Tomorrow," "Milkshake Smoothie," "White Cheese," "Drink It to Be Beautiful Inside and Out," "Golden Zesta" and "Pride of Main Street."

The Company regards its Lifeway family of trademarks and other trademarks as having substantial value and as being an important factor in the marketing of its products. The Company is not aware of any trademark infringements that could materially affect its current business or any prior claim to the trademarks that would prevent the Company from using such trademarks in its business. The Company's policy is to pursue registration of its marks whenever appropriate and to vigorously oppose any infringements of its marks.

REGULATION

Lifeway is subject to regulation by federal, state and local governmental authorities regarding the distribution and sale of food products. Although Lifeway believes that it currently has all material government permits, licenses, qualifications and approvals for its operations, there can be no assurance that Lifeway will be able to maintain its existing licenses and permits or to obtain any future licenses, permits, qualifications or approvals which may be required for the operation of Lifeway's business.

Lifeway believes that it is currently in compliance with all applicable environmental laws and that the cost of such compliance was not material to the financial position of Lifeway.

SEASONALITY

The Company's business is not seasonal.

| 7 |

EMPLOYEES

As of December 31, 2015 the Company employed approximately 370 employees.

AVAILABLE INFORMATION

The Company maintains a corporate website for investors at www.lifeway.net and it makes available, free of charge, through this website its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports that the Company files with or furnishes to the Securities and Exchange Commission (the "SEC"), as soon as reasonably practicable after it electronically files such material with, or furnishes it to, the SEC.

ITEM 1A RISK FACTORS

In evaluating and understanding us and our business, you should carefully consider the risks described below, in conjunction with all of the other information included in this Annual Report on Form 10-K, including "Management's Discussion and Analysis of Financial Condition and Results of Operations" contained in Part II, Item 7 and "Quantitative and Qualitative Disclosures About Market Risk" contained in Part II, Item 7A. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may become important factors that adversely affect our business. If any of the events or circumstances described in the following risk factors actually occurs, our business, financial condition, results of operations, and future prospects could be materially and adversely affected.

Our product categories face a high level of competition, which could negatively impact our sales and results of operations.

We face significant competition in each of our product categories. Competition in our product categories is based on product innovation, product quality, price, brand recognition and loyalty, effectiveness of marketing, promotional activity, and our ability to identify and satisfy consumer tastes and preferences. We believe that our brands have benefited in many cases from being the first to introduce products in their categories, and their success has attracted competition from other food and beverage companies that produce branded products, as well as from private label competitors. Some of our competitors, such as Groupe Danone, General Mills, Inc., Dean Foods, WhiteWave Foods, Hain Celestial Group, and Nestle S.A., have substantial financial and marketing resources. These competitors and others may be able to introduce innovative products more quickly or market their products more successfully than we can, which could cause our growth rate to be slower than we anticipate and could cause sales to decline.

We also compete with producers of non-organic products, which have lower ingredient and production-related costs. As a result, these non-organic producers may be able to offer conventional products to customers at a lower price point. This could cause us to lower our prices, resulting in lower profitability or, in the alternative, cause us to lose market share if we fail to lower prices. Furthermore, private label competitors are generally able to sell their products at lower prices because private label products typically have lower marketing costs than their branded counterparts. If our products fail to compete successfully with other branded or private label offerings, demand for our products and our sales volumes could be negatively impacted.

Additionally, due to high levels of competition, certain of our key retailers may demand price concessions on our products or may become more resistant to price increases for our products. Increased price competition and resistance to price increases have had, and may continue to have, a negative effect on our results of operations.

We may not be able to successfully implement our growth strategy for our brands on a timely basis or at all.

We believe that our future success depends, in part, on our ability to implement our growth strategy of leveraging our existing brands and products to drive increased sales. Our ability to implement this strategy depends, among other things, on our ability to:

● | enter into distribution and other strategic arrangements with third-party retailers and other potential distributors of our products; |

● | compete successfully in the product categories in which we choose to operate; |

● | introduce new and appealing products and innovate successfully on our existing products; |

● | develop and maintain consumer interest in our brands; |

● | increase our brand recognition and loyalty; and |

● | enter into strategic arrangements with third-party growers and other providers to supply our necessary raw materials. |

| 8 |

We may not be able to implement this growth strategy successfully, and our sales and income growth rates may not be sustainable over time. Our sales and results of operations will be negatively affected if we fail to implement our growth strategy or if we invest resources in a growth strategy that ultimately proves unsuccessful.

If we fail to anticipate and respond to changes in consumer preferences, demand for our products could decline.

Consumer tastes and preferences are difficult to predict and they evolve over time. Demand for our products depends on our ability to identify and offer products that appeal to these shifting preferences. Factors that may affect consumer tastes and preferences include:

● | dietary trends and increased attention to nutritional values, such as the sugar, fat, protein, fiber or calorie content of different foods and beverages; |

● | concerns regarding the health effects of specific ingredients and nutrients, such as sugar, other sweeteners, dairy, soybeans, nuts, oils, vitamins, fiber and minerals; |

● | concerns regarding the public health consequences associated with obesity, particularly among young people; and |

● | increasing awareness of the environmental and social effects of food processing . |

If consumer demand for our products declines, our sales volumes and our business could be negatively affected.

We are subject to the risk of product contamination and product liability claims, which could harm our reputation, force us to recall products and incur substantial costs.

The sale of food products for human consumption involves the risk of injury to consumers. Such injuries may result from tampering by unauthorized third parties, misbranding, product contamination or spoilage including the presence of foreign objects, substances, chemicals, other agents, or residues introduced during the growing, storage, processing, handling or transportation phases. We also may be subject to liability if our products or production processes violate applicable laws or regulations, including environmental, health, and safety requirements, or in the event our products cause injury, illness, or death.

In addition, our product advertising could make us the target of claims relating to false or deceptive advertising under U.S. federal and state laws, including the consumer protection statutes of some states, or laws of other jurisdictions in which we operate. Lifeway is from time to time engaged in such litigation matters none of which presently is expected to have a material adverse effect on its business results or operations.

A significant product liability, consumer fraud, or other legal judgment against us or a widespread product recall would negatively impact our profitability. Moreover, claims or liabilities of this sort might not be covered by insurance or by any rights of indemnity or contribution that we may have against others. Even if a product liability, consumer fraud, or other claim is found to be without merit or is otherwise unsuccessful, the negative publicity surrounding such assertions regarding our products or processes could materially and adversely affect our reputation and brand image, particularly in categories that are promoted as having strong health and wellness credentials. Any loss of consumer confidence in our brand, our products and the ingredients we use or in the safety and quality of our products would be costly and might not be overcome.

The loss of any of our largest customers could negatively impact our sales and results of operations.

Two of our customers together accounted for 26% of our net sales in the fiscal year ended December 31, 2015. We do not generally enter into written agreements with our customers, and where such agreements exist, they are generally terminable at will by the customer. In addition, our customers sometimes award contracts based on competitive bidding, which could result in lower profits for contracts we win and the loss of business for contracts we lose. The loss of any large customer for an extended period of time could negatively affect our sales and results of operations.

| 9 |

We may not be able to successfully complete strategic acquisitions, establish joint ventures, or integrate brands that we acquire.

We intend to continue to grow our business in part through the acquisition of new brands and through the establishment of strategic alliances including potential joint ventures . We cannot be certain that we will successfully be able to:

● | identify suitable acquisition candidates or joint venture partners and accurately assess their value, growth potential, strengths, weaknesses, contingent and other liabilities, and potential profitability; |

● | secure regulatory clearance for our acquisitions and joint ventures; |

● | negotiate acquisitions and joint ventures on terms acceptable to us; or |

● | integrate any acquisitions that we complete. |

Acquired companies or brands may not achieve the level of sales or profitability that justify our investment in them, or an acquired company may have unidentified liabilities for which we, as a successor owner, may be responsible. These transactions typically involve a number of risks and present financial and other challenges, including the existence of unknown disputes, liabilities, or contingencies and changes in the industry, location, or regulatory or political environment in which these investments are located, that may arise after entering into such arrangements.

The success of any acquisitions we complete will depend on our ability to effectively integrate the acquired brands or products into our existing operations. We may experience difficulty entering new categories or geographies, integrating new products into our product mix, integrating an acquired brand's distribution channels and sales force, achieving anticipated cost savings, or retaining key personnel and customers of the acquired business. Integrating an acquired brand into our existing operations requires management resources and may divert management's attention from our day-to-day operations. If we are not successful in integrating the operations of acquired brands, or in executing strategies and business plans related to our joint ventures, our business could be negatively affected.

We may have to pay cash, incur debt, or issue equity, equity-linked, or debt securities to pay for any such acquisition, any of which could adversely affect our financial results.

Our continued success depends on our ability to innovate successfully and to innovate on a cost-effective basis.

A key element of our growth strategy is to introduce new and appealing products and to successfully innovate on our existing products. Success in product development is affected by our ability to anticipate consumer preferences, and to utilize our management's ability to launch new or improved products successfully and on a cost-effective basis. Furthermore, the development and introduction of new products requires substantial marketing expenditures, which we may not be able to finance or which we may be unable to recover if the new products do not achieve commercial success and gain widespread market acceptance. If we are unsuccessful in our product innovation efforts, our business could be negatively affected.

Reduced availability of raw materials and other inputs, as well as increased costs for our raw materials and other inputs, could adversely affect us.

Our business depends heavily on raw materials, such as conventional and organic raw milk, used in the production of our products. Our raw materials are generally sourced from third-party suppliers, and we are not assured of continued supply, pricing, or exclusive access to raw materials from any of these suppliers. In addition, a substantial portion of our raw materials are agricultural products, which are vulnerable to adverse weather conditions and natural disasters, such as floods, droughts, frost, earthquakes, and pestilence. Adverse weather conditions and natural disasters also can lower dairy and crop yields and reduce supplies of these ingredients or increase their prices. Other events that adversely affect our third-party suppliers and that are out of our control could also impair our ability to obtain the raw materials and other inputs that we need in the quantities and at the prices that we desire. Such events include problems with our suppliers' businesses, finances, labor relations, costs, production, insurance, and reputation.

The organic ingredients (including milk) we use in some of our products are less plentiful and available from a fewer number of suppliers than their conventional counterparts. Competition with other manufacturers in the procurement of organic product ingredients may increase in the future if consumer demand for organic products increases. In addition, the dairy industry continues to experience periodic imbalances between supply and demand for organic raw milk. Industry regulation and the costs of organic farming compared to costs of conventional farming can impact the supply of organic raw milk in the market. Oversupply levels of organic raw milk can increase competitive pressure on our products and pricing, while supply shortages can cause higher input costs and reduce our ability to deliver product to our customers. Cost increases in raw materials and other inputs could cause our profits to decrease significantly compared to prior periods, as we may be unable to increase our prices to offset the increased cost of these raw materials and other inputs. If we are unable to obtain raw materials and other inputs for our products or offset any increased costs for such raw materials and inputs, our business could be negatively affected.

| 10 |

Failure to maintain sufficient internal production capacity may result in our inability to meet customer demand and/or increase our operating costs and capital expenditures.

The success of our business depends, in part, on maintaining a strong production platform and we rely primarily on internal production resources to fulfill our manufacturing needs. Certain of our manufacturing plants are operating at high rates of utilization, and we may need to expand our production facilities or increase our reliance on third parties to provide manufacturing and supply services, commonly referred to as "co-packing" agreements, for a number of our products. A failure by any future co-packers to comply with food safety, environmental, or other laws and regulations may disrupt our supply of products. In addition, we have experienced, and expect to continue to experience, increased distribution and warehousing costs due to capacity constraints resulting from our growth.

If we need to enter into co-packing, warehousing or distribution agreements in the future, we can provide no assurance that we would be able to find acceptable third party providers or enter into agreements on satisfactory terms or at all. Our inability to maintain sufficient internal capacity or establish satisfactory co-packing, warehousing and distribution arrangements could limit our ability to operate our business or implement our strategic growth plan, and could negatively affect our sales volumes and results of operations.

In addition, our recent initiatives to expand our production platform and our productive capacity, could fail to achieve such objectives and in any case could increase our operating costs beyond our expectations and could require significant additional capital expenditures. If we cannot maintain sufficient production, warehousing and distribution capacity, either internally or through third party agreements, we may be unable to meet customer demand and/or our manufacturing, distribution and warehousing costs may increase, which could negatively affect our business.

Disruption of our supply or distribution chains could adversely affect our business.

Damage or disruption to our manufacturing or distribution capabilities due to weather, natural disaster, fire, environmental incident, terrorism, pandemic, strikes, the financial or operational instability of key suppliers, distributors, warehousing, and transportation providers, or other reasons could impair our ability to manufacture or distribute our products. In addition, most of our products are processed in a single facility, and damage or disruption to this facility could impair our ability to process and sell those products. If we are unable or it is not financially feasible to mitigate the likelihood or potential impact of such events, our business and results of operations could be negatively affected and additional resources could be required to restore our supply chain.

Our substantial debt and financial obligations could adversely affect our financial condition and ability to operate our business.

As of December 31, 2015, we had outstanding borrowings of approximately $8 million substantially all of which consists of term loan borrowings. We also had additional borrowing capacity of approximately $5 million under our line of credit, of which none was outstanding as of December 31, 2015.

Our loan agreements contain certain restrictions and requirements that among other things:

● | require us to maintain a minimum fixed charged ratio and a tangible net worth thresholds; |

● | limit our ability to obtain additional financing in the future for working capital, capital expenditures and acquisitions, to fund growth or for general corporate purposes; |

● | limit our future ability to refinance our indebtedness on terms acceptable to us or at all; |

● | limit our flexibility in planning for or reacting to changes in our business and market conditions or in funding our strategic growth plan; and |

● | impose on us financial and operational restrictions. |

| 11 |

Our debt level and the terms of our financing arrangements could adversely affect our financial condition and limit our ability to successfully implement our growth strategy.

Our ability to meet our debt service obligations will depend on our future performance, which will be affected by the other risk factors described in this Annual Report on Form 10-K. If we do not generate enough cash flow to pay our debt service obligations, we may be required to refinance all or part of our existing debt, sell our assets, borrow more money or raise equity. There is no guarantee that we will be able to take any of these actions on a timely basis, on terms satisfactory to us, or at all.

Our notes bear interest at variable rates. If market interest rates increase, it will increase our debt service requirements, which could adversely affect our cash flow.

Our loan agreements also contain provisions that restrict our ability to:

● | borrow money or guarantee debt; |

● | create liens; |

● | make specified types of investments and acquisitions; |

● | pay dividends on or redeem or repurchase stock; |

● | enter into new lines of business; |

● | enter into transactions with affiliates; and |

● | sell assets or merge with other companies. |

These restrictions on the operation of our business could harm us by, among other things, limiting our ability to take advantage of financing, merger and acquisition opportunities, and other corporate opportunities. Various risks, uncertainties, and events beyond our control could affect our ability to comply with these covenants. Unless cured or waived, a default would permit lenders to accelerate the maturity of the debt under the credit agreement and to foreclose upon the collateral securing the debt.

We may need additional financing in the future, and we may not be able to obtain that financing.

From time to time, we may need additional financing to support our business and pursue our growth strategy, including strategic acquisitions. Our ability to obtain additional financing, if and when required, will depend on investor demand, our operating performance, the condition of the capital markets, and other factors. We cannot assure you that additional financing will be available to us on favorable terms when required, or at all. If we raise additional funds through the issuance of equity, equity-linked, or debt securities, those securities may have rights, preferences, or privileges senior to those of our common stock, and, in the case of equity and equity-linked securities, our existing stockholders may experience dilution.

Our international operations subject us to business risks that could cause our revenue and profitability to decline.

We intend to expand distribution of our products worldwide. Risks associated with our operations as we expand outside of the United States may include, among other things:

● | legal and regulatory requirements in multiple jurisdictions that differ from those in the United States and change from time to time, such as tax, labor, and trade laws, as well as laws that affect our ability to manufacture, market, or sell our products; |

● | foreign currency exposures; |

● | political and economic instability, such as the recent debt crisis in Europe; |

● | trade protection measures and price controls; and |

● | diminished protection of intellectual property in some countries. |

| 12 |

If one or more of these business risks occur, our business and results of operations could be negatively affected.

Loss of our key management or other personnel, or an inability to attract such management and other personnel, could negatively impact our business.

We depend on the skills, working relationships, and continued services of key personnel, including our experienced senior management team. We also depend on our ability to attract and retain qualified personnel to operate and expand our business. If we lose one or more members of our senior management team, or if we fail to attract talented new employees, our business and results of operations could be negatively affected.

Our workforce could become unionized in the future, which could materially and adversely affect the stability of our production and materially reduce our profitability.

Our employees have the right at any time under the National Labor Relations Act to form or affiliate with a union and certain of our employees have undertaken the process of forming a union. If our employees form or affiliate with a union and the terms of a union collective bargaining agreement are significantly different from our current compensation and job assignment arrangements with our employees, these arrangements could materially and adversely affect the stability of our operations and materially reduce our profitability.

Our intellectual property rights are valuable, and any inability to protect them could reduce the value of our products and brands.

We consider our intellectual property rights, particularly our trademarks, but also our trade secrets, copyrights, and licenses, to be a significant and valuable aspect of our business. We attempt to protect our intellectual property rights through a combination of trademark, copyright, and trade secret laws, as well as licensing agreements, third-party confidentiality, nondisclosure, and assignment agreements, and by policing third-party misuses of our intellectual property. Our failure to obtain or maintain adequate protection of our intellectual property rights, or any change in law or other changes that serve to lessen or remove the current legal protections of our intellectual property, may diminish our competitiveness and could materially harm our business.

We also face the risk of claims that we have infringed third parties' intellectual property rights. Any claims of intellectual property infringement, even those without merit, could be expensive and time consuming to defend, cause us to cease making, licensing, or using products that incorporate the challenged intellectual property, require us to redesign or rebrand our products or packaging, divert management's attention and resources, or require us to enter into royalty or licensing agreements to obtain the right to use a third party's intellectual property. Any royalty or licensing agreements, if required, may not be available to us on acceptable terms or at all. Additionally, a successful claim of infringement against us could result in our being required to pay significant damages, enter into costly license or royalty agreements, or stop the sale of certain products, any of which could have a negative effect on our results of operations.

Litigation or legal proceedings could expose us to significant liabilities and have a negative impact on our reputation.

We are party to various litigation claims and legal proceedings in the ordinary course of our business. In the opinion of management, the resolution of current litigation claims and legal proceedings will not have a material adverse effect on the Company's consolidated statements of financial condition. We evaluate these litigation claims and legal proceedings to assess the likelihood of unfavorable outcomes and to estimate, if possible, the amount of potential losses. Based on these assessments and estimates, we establish reserves or disclose the relevant litigation claims or legal proceedings, as appropriate. These assessments and estimates are based on the information available to management at the time and involve a significant amount of management judgment. Actual outcomes or losses may differ materially from our current assessments and estimates. If actual outcomes or losses differ materially from our current assessments and estimates or additional litigation or legal proceedings are initiated, we could be exposed to significant liabilities.

| 13 |

Our business is subject to various environmental and health and safety laws and regulations, which may increase our compliance costs or subject us to liabilities.

Our business operations are subject to numerous requirements in the United States relating to the protection of the environment and health and safety matters, including the Clean Air Act, the Clean Water Act, the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended, and the National Organic Standards of the U.S. Department of Agriculture, as well as similar state and local statutes and regulations in the United States and in each of the countries in which we do business in Europe. These laws and regulations govern, among other things, air emissions and the discharge of wastewater and other pollutants, the use of refrigerants, the handling and disposal of hazardous materials, and the cleanup of contamination in the environment.

We could incur significant costs, including fines, penalties and other sanctions, cleanup costs, and third-party claims for property damage or personal injury as a result of the failure to comply with, or liabilities under, environmental, health, and safety requirements. New legislation, as well as current federal and other state regulatory initiatives relating to these environmental matters, could require us to replace equipment, install additional pollution controls, purchase various emission allowances, or curtail operations. These costs could negatively affect our results of operations and financial condition.

Violations of laws or regulations related to the food industry, as well as new laws or regulations or changes to existing laws or regulations related to the food industry, could adversely affect our business.

The food production and marketing industry is subject to a variety of federal, state, local, and foreign laws and regulations, including food safety requirements related to the ingredients, manufacture, processing, storage, marketing, advertising, labeling, and distribution of our products, as well as those related to worker health and workplace safety. Our activities, both in and outside of the United States, are subject to extensive regulation. We are regulated by, among other federal and state authorities, the U.S. FDA, the U.S. Federal Trade Commission ("FTC"), and the U.S. Departments of Agriculture, Commerce, and Labor, as well as by similar authorities abroad within the regulatory framework of the European Union and its members. Governmental regulations also affect taxes and levies, healthcare costs, energy usage, immigration, and other labor issues, all of which may have a direct or indirect effect on our business or those of our customers or suppliers.

In addition, the marketing and advertising of our products could make us the target of claims relating to alleged false or deceptive advertising under federal, state, and foreign laws and regulations, and we may be subject to initiatives that limit or prohibit the marketing and advertising of our products to children.

We are also subject to federal laws and regulations relating to our organic products and production. For example, as required by the National Organic Program ("NOP"), we rely on third parties to certify certain of our products and production locations as organic. Because the Organic Foods Production Act of 1990, which created the NOP, was so recently adopted, many regulations and informal positions taken by the NOP are subject to continued review and scrutiny.

Changes in these laws or regulations or the introduction of new laws or regulations could increase our compliance costs, increase other costs of doing business for us, our customers, or our suppliers, or restrict our actions, which could adversely affect our results of operations. In some cases, increased regulatory scrutiny could interrupt distribution of our products, as could be the case in the United States as the FDA enacts the Food Safety Modernization Act of 2011, or force changes in our production processes and our products. Further, if we are found to be in violation of applicable laws and regulations in these areas, we could be subject to civil remedies, including fines, injunctions, or recalls, as well as potential criminal sanctions, any of which could have a material adverse effect on our business.

Three of our directors and executive officers control a significant portion of our common stock and their interests may not align with the interests of our other shareholders.

Ludmila Smolyansky, the chairman of our board, Julie Smolyansky, our chief executive officer, president and director and Edward Smolyansky, our chief financial and accounting officer, chief operating officer, treasurer and secretary (together, the "Smolyansky Family") own approximately 49.6% of our issued and outstanding common stock. This significant concentration of share ownership may adversely affect the trading price of our common stock because investors often perceive a disadvantage in owning shares in a company with one or several controlling shareholders.

Furthermore, our directors and officers, as a group, which own in excess of 49.8% of our issued and outstanding common stock have the ability to significantly influence or control the outcome of all matters requiring shareholder approval, including the election of directors and approval of significant corporate transactions, such as mergers, consolidations or the sale of substantially all of our assets.

| 14 |

This concentration of ownership may have the effect of delaying or preventing a change in control of our company which could deprive our shareholders of an opportunity to receive a premium for their shares as part of a sale of our company and might reduce the price of our common stock. In addition, without the consent of the Smolyansky Family, we could be prevented from entering into transactions that could be beneficial to us. The Smolyansky Family may cause us to take actions that are opposed by other shareholders as their interests may differ from those of other shareholders.

We have identified material weaknesses in our internal control over financial reporting. Our failure to establish and maintain effective internal control over financial reporting could result in material misstatements in our financial statements, our failure to meet our reporting obligations and cause investors to lose confidence in our reported financial information, which in turn could cause the trading price of our securities to decline.

We have identified material weaknesses in our internal control over financial reporting. A description of the material weaknesses can be found in Item 9A of this report. As a result of such weaknesses, our management concluded that our disclosure controls and procedures and internal control over financial reporting were not effective as of December 31, 2015.

Unless and until these material weaknesses have been remediated, or should new material weaknesses arise or be discovered in the future material misstatements could occur and go undetected in the Company's interim or annual consolidated financial statements and we may be required to restate our financial statements. In addition, we may experience delays in satisfying our reporting obligations or to comply with SEC rules and regulations, which could result in investigations and sanctions by regulatory authorities. Any of these results could adversely affect our business and the value of our common stock.

ITEM 1B UNRESOLVED STAFF COMMENTS

None

ITEM 2 PROPERTIES

We operate the following facilities:

Location |

| Owned / Leased |

| Principal Use |

Morton Grove, Illinois |

| Owned |

| Production of kefir and cheese, principal executive offices |

Waukesha, Wisconsin |

| Owned |

| Production of kefir, administrative offices |

Niles, Illinois |

| Owned |

| Distribution center, administrative offices |

Philadelphia, Pennsylvania |

| Owned |

| Production of kefir and cheese, administrative offices |

Skokie, Illinois |

| Owned |

| Production of cheese |

Sauk Centre, Minnesota |

| Owned |

| Administrative offices |

|

|

|

|

The Company believes that its facilities are adequate for its current needs and that suitable additional space will be available on commercially acceptable terms as required. The Company believes that Lifeway has adequate insurance coverage for all of its properties.

ITEM 3 LEGAL PROCEEDINGS

From time to time we are engaged in litigation matters arising in the ordinary course of business none of which presently is reasonably likely to have a material adverse effect on our financial position or results of operations.

ITEM 4 MINE SAFETY DISCLOSURES

None

| 15 |

PART II

ITEM 5 MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is listed on The Nasdaq Global Market under the symbol "LWAY." Trading commenced on March 29, 1988.

As of February 29, 2016, there were approximately 65 holders of record of Lifeway's Common Stock. The Company has no information regarding beneficial owners whose shares are held in street name.

Common stock price

The following table shows the high and low sale prices per share of our common stock as reported on The Nasdaq Global Market for each quarter during the two most recent fiscal years is set forth in the following table:

Common Stock Price Range | ||

2014 | ||

Low | High | |

First Quarter | $ 13.35 | $ 15.99 |

Second Quarter | $ 12.59 | $ 15.50 |

Third Quarter | $ 12.34 | $ 14.78 |

Fourth Quarter | $ 15.00 | $ 20.33 |

2015 | ||

First Quarter | $ 16.79 | $ 22.38 |

Second Quarter | $ 17.20 | $ 21.90 |

Third Quarter | $ 10.16 | $ 20.00 |

Fourth Quarter | $ 9.88 | $ 12.56 |

Stock Performance Graph

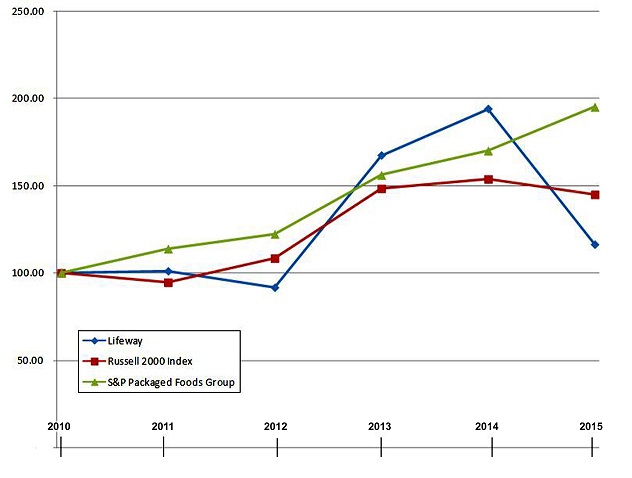

The following graph compares the cumulative total stockholder return on Lifeway's common stock over the last five fiscal years based on the market price of the common shares and assumes reinvestment of dividends, with the cumulative total return of companies in the Russell 2000 Stock Index and the S&P Packaged Foods group.

The table below assumes an investment of $100 on December 31, 2011 in our common stock, the Russell 2000 Index and the S&P Packaged Foods group.

| 16 |

2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

Lifeway | 100 | 101 | 92 | 167 | 194 | 116 |

Russell 2000 Index | 100 | 95 | 108 | 148 | 153 | 144 |

S&P Packaged Foods group | 100 | 114 | 122 | 156 | 170 | 195 |

Dividend Policy

Lifeway does not routinely declare and pay dividends. From time to time however our Board of Directors may declare and pay dividends depending on the Company's operating cash flow, financial condition, capital requirements and such other factors as the Board of Directors may deem relevant.

There were no dividends declared or paid in fiscal 2015 and 2014.

| 17 |

Issuer Purchases of Equity Securities

Period |

| Total number of shares purchased |

|

| Average price paid per share |

|

| Total number of shares purchased as part of a publicly announced program (a) |

|

| Approximate Dollar Value of Shares that may yet be Purchased Under the Plans or Programs ($ in thousands) |

| ||||

10/1/2015 to 10/31/2015 |

|

| 41,607 |

|

| $ | 11.56 |

|

|

| 41,607 |

|

| $ | 3,019 |

|

11/1/2015 to 11/302015 |

|

| 35,054 |

|

| $ | 10.63 |

|

|

| 35,054 |

|

| $ | 2,647 |

|

12/1/2015 to 12/31/2015 |

|

| 59,526 |

|

| $ | 11.56 |

|

|

| 59,526 | (b) |

| $ | 1,958 |

|

Total |

|

| 136,187 |

|

| $ | 11.32 |

|

|

| 136,187 |

|

| $ | 1,958 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (a) | During the fourth quarter of 2015, the company had a publicly announced share repurchase program. Under this program, which was announced on September 24, 2015, the company's Board of Directors authorized the purchase of up to $3.5 million of company stock. The program has no expiration date.

|

| (b) | Includes 30,000 shares purchased by the company in privately negotiated transactions, in accordance with all applicable securities laws and regulations. |

ITEM 6 SELECTED FINANCIAL DATA

The following table sets forth selected financial data for each of the fiscal years in the five-year period ended December 31, 2015:

Thousands except per share information |

| 2015 |

|

| 2014 |

|

| 2013 |

|

| 2012 |

|

| 2011 |

| |||||

Net Sales |

| $ | 118,587 |

|

| $ | 118,960 |

|

| $ | 97,524 |

|

| $ | 81,351 |

|

| $ | 69,970 |

|

Income from Operations |

|

| 4,403 |

|

|

| 4,235 |

|

|

| 8,031 |

|

|

| 8,845 |

|

|

| 5,076 |

|

Net Income |

|

| 1,972 |

|

|

| 1,956 |

|

|

| 4,990 |

|

|

| 5,620 |

|

|

| 2,855 |

|

Total assets |

|

| 64,918 |

|

|

| 63,424 |

|

|

| 63,674 |

|

|

| 53,507 |

|

|

| 51,473 |

|

Notes payable |

|

| 7,119 |

|

|

| 8,125 |

|

|

| 8,999 |

|

|

| 4,956 |

|

|

| 5,540 |

|

Total equity |

|

| 45,256 |

|

|

| 44,700 |

|

|

| 42,950 |

|

|

| 39,313 |

|

|

| 35,357 |

|

Basic and diluted earnings per common share |

|

| 0.12 |

|

|

| 0.12 |

|

|

| 0.31 |

|

|

| 0.34 |

|

|

| 0.17 |

|

Dividends per share |

|

| -- |

|

|

| -- |

|

|

| 0.08 |

|

|

| 0.07 |

|

|

| -- |

|

| 18 |

ITEM 7 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion of the financial condition and results of operations for the twelve-months ended December 31, 2015, 2014 and 2013 should be read in conjunction with the audited consolidated financial statements and the notes to those statements that are included elsewhere in this report on Form 10-K. In addition to historical information, the following discussion contains certain forward-looking statements within the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. These statements relate to our future plans, objectives, expectations and intentions. These statements may be identified by the use of words such as "may", "will", "could", "expect", "anticipate", "intend", "believe", "estimate", "plan", "predict", and similar terms or terminology, or the negative of such terms or other comparable terminology. Although we believe the expectations expressed in these forward-looking statements are based on reasonable assumptions within the bounds of our knowledge of our business, our actual results could differ materially from those discussed in these statements. Factors that could contribute to such differences include, but are not limited to, those discussed in the "Risk Factors" section in Part I, Item 1A. We undertake no obligation to update publicly any forward-looking statements for any reason even if new information becomes available or other events occur in the future.

Results of Operation

Comparison of Year Ended December 31, 2015 to Year Ended December 31, 2014

Net sales

The following table summarizes our net sales:

| Year ended December 31, |

|

| Change |

|

| |||||||||||

| 2015 |

|

| 2014 |

|

| $ |

|

| % |

| ||||||

Gross Sales |

| $ | 137,244 |

|

| $ | 130,216 |

|

| $ | 7,028 |

|

|

| 5.4 | % | |

Less: Discounts & promotional allowances |

|

| (18,657 | ) |

|

| (11,256 | ) |

|

| (7,401 | ) |

|

| 65.8 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Net Sales |

| $ | 118,587 |

|

| $ | 118,960 |

|

| $ | (373 | ) |

|

| -0.3 | % | |

Discounts & promotional allowances % |

|

| 13.6 | % |

|

| 8.6 | % |

|

|

|

|

|

|

|

| |

Net sales declined by $373 or 0.3% during the year ended December 31, 2015 from $118,960 during the same period in 2014. The decrease in net sales reflects a 5.4% increase in gross sales reflecting higher volumes of drinkable Kefir, higher cream sales, and increased private label sales offset by lower sales of cheese and frozen product and significantly higher discounts and promotional allowances given to customers.

Cost of goods sold & gross profit

The following table summarizes our cost of goods sold and gross profit:

| Year ended December 31, |

|

| Change |

|

| |||||||||||

| 2015 |

|

| 2014 |

|

| $ |

|

| % |

| ||||||

Purchases, net |

| $ | 51,776 |

|

| $ | 59,378 |

|

| $ | (7,602 | ) |

|

| -12.8 | % | |

Testing |

|

| 113 |

|

|

| 51 |

|

|

| 62 |

|

|

| 121.6 | % | |

Supplies |

|

| 2,026 |

|

|

| 1,414 |

|

|

| 612 |

|

|

| 43.3 | % | |

Salaries production |

|

| 12,078 |

|

|

| 9,465 |

|

|

| 2,613 |

|

|

| 27.6 | % | |

Contract work |

|

| 145 |

|

|

| 158 |

|

|

| (13 | ) |

|

| -8.2 | % | |

Freight |

|

| 13,206 |

|

|

| 12,790 |

|

|

| 416 |

|

|

| 3.3 | % | |

Labor and overhead |

|

| 5,229 |

|

|

| 4,305 |

|

|

| (924 | ) |

|

| -22.5 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Cost of Goods Sold, excluding depreciation |

|

| 84,573 |

|

|

| 87,561 |

|

|

| (2,988 | ) |

|

| -3.4 | % | |

Depreciation expense |

|

| 2,413 |

|

|

| 2,536 |

|

|

| (123 | ) |

|

| -4.9 | % | |

Cost of Goods Sold |

| $ | 86,986 |

|

| $ | 90,097 |

|

| $ | (3,111 | ) |

|

| -3.5 | % | |

Gross profit |

| $ | 31,601 |

|

| $ | 28,863 |

|

| $ | 2,738 |

|

|

| 9.5 | % | |

Gross Profit % to net sales |

|

| 26.6 | % |

|

| 24.3 | % |

|

|

|

|

|

|

|

| |

| 19 |

Gross profit as a percent of net sales increased to 26.6% during the year ended December 31, 2015 from 24.3% during the same period in 2014. The increase in the gross profit percent reflects lower input costs, primarily lower milk prices, partially offset by higher labor costs and the elevated level of promotional allowances and discounts given to customers.

Selling Expenses

The following table summarizes our selling expenses:

| Year ended December 31, |

|

| Change |

|

| |||||||||||

| 2015 |

|

| 2014 |

|

| $ |

|

| % |

| ||||||

Salesperson commissions |

| $ | 2,285 |

|

| $ | 2,259 |

|

| $ | 26 |

|

|

| 1.2 | % | |

Advertising |

|

| 5,006 |

|

|

| 3,875 |

|

|

| 1,131 |

|

|

| 29.2 | % | |

Salaries |

|

| 4,487 |

|

|

| 6,254 |

|

|

| (1,767 | ) |

|

| -28.3 | % | |

Other marketing & promotion costs |

|

| 216 |

|

|

| 403 |

|

|

| (187 | ) |

|

| -46.4 | % | |

Travel |

|

| 758 |

|

|

| 1,743 |

|

|

| (985 | ) |

|

| -56.5 | % | |

Selling expense |

| $ | 12,752 |

|

| $ | 14,534 |

|

| $ | (1,782 | ) |

|

| -12.3 | % | |

% to net sales |

|

| 10.8 | % |

|

| 12.2 | % |

|

|

|

|

|

|

|

| |

Selling expenses decreased by $1,782 or 12.3% to $12,752 during the year ended December 31, 2015 from $14,534 during the same period in 2014 reflecting an increase in advertising programs offset by lower salaries and travel related costs. The lower salaries reflects the reassignment of Company personnel in 2015 from principally selling responsibilities to broader general management responsibilities. Selling expenses as a percentage of sales were 10.8% for the year ended December 31, 2015 compared to 12.2% for the same period in 2014.

General and administrative expenses

The following table summarizes our general and administrative expenses:

| Year ended December 31, |

|

| Change |

|

| |||||||||||

| 2015 |

|

| 2014 |

|

| $ |

|

| % |

| ||||||

Salaries |

| $ | 5,811 |

|

| $ | 3,254 |

|

| $ | 2,557 |

|

|

| 78.6 | % | |

Rent |

|

| 265 |

|

|

| 298 |

|

|

| (33 | ) |

|

| -11.1 | % | |

Equipment lease |

|

| 12 |

|

|

| 8 |

|

|

| 4 |

|

|

| 50 | % | |

Auto expense |

|

| 135 |

|

|

| 93 |

|

|

| 42 |

|

|

| 45.2 | % | |

Office supplies |

|

| 167 |

|

|

| 325 |

|

|

| (158 | ) |

|

| -48.6 | % | |

Professional fees |

|

| 4,931 |

|

|

| 3,086 |

|

|

| 1,845 |

|

|

| 59.8 | % | |

Telephone expense |

|

| 165 |

|

|

| 99 |

|

|

| 66 |

|

|

| 66.7 | % | |

Facilities |

|

| 1,767 |

|

|

| 1,515 |

|

|

| 252 |

|

|

| 16.6 | % | |

Miscellaneous |

|

| 477 |

|

|

| 700 |

|

|

| (223 | ) |

|

| -31.8 | % | |

General & administrative expense |

| $ | 13,730 |

|

| $ | 9,378 |

|

| $ | 4,352 |

|

|

| 46.4 | % | |

% to net sales |

|

| 11.6 | % |

|

| 11.4 | % |

|

|

|

|

|

|

|

| |

General and administrative expenses increased $4,352 or 46.4% to $13,730 during the year ended December 31, 2015 from $9,378 during the same period in 2014. The increase is primarily a result of increases in salaries and professional fees. Salaries increased $2,557 or 78.6% to $5,811 during the year ended December 31, 2015 from $3,254 during the same period in 2014. The increase reflects the reassignment of Company personnel in 2015 from principally selling responsibilities to broader general management responsibilities and an increase in headcount, primarily in finance. Professional fees, which consists primarily of legal and accounting fees increased by $1,845 or 59.8% to $4,931 during the year ended December 31, 2015 from $3,086 during the same period in 2014. The higher professional fees primarily arise from our process improvement initiatives aimed at remediating internal control deficiencies, redundancies and inefficiencies associated with retaining a new audit firm, elevated legal fees associated the company's delayed SEC filings and related matters, and fees paid to executive search firms.

| 20 |

Income from operations and net income

The company reported income from operations of $4,403 during the year ended December 31, 2015, compared to $4,235 during the same period in 2014. The provision for income taxes was $2,020, or a 50.6% effective rate for the year ended December 31, 2015 compared to a provision for income taxes of $2,242 or a 53.4% effective tax rate during the same period in 2014. Income taxes are discussed in Note 10 to the Notes to the Consolidated Financial Statements.

Net income was $1,972 or $0.12 per basic and diluted common share for the year ended December 31, 2015 compared to $1,956 or $0.12 per basic and diluted common share in the same period in 2014.

Comparison of Year Ended December 31, 2014 to Year Ended December 31, 2013

Net sales

The following table summarizes our net sales:

| Year ended December 31, |

|

| Change |

|

| |||||||||||

| 2014 |

|

| 2013 |

|

| $ |

|

| % |

| ||||||

Gross Sales |

| $ | 130,216 |

|

| $ | 108,966 |

|

| $ | 21,250 |

|

|

| 19.5 | % | |

Less: Discounts & promotional allowances |

|

| (11,256 | ) |

|

| (11,442 | ) |

|

| 186 |

|

|

| -1.6 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Net Sales |

| $ | 118,960 |

|

| $ | 97,524 |

|

| $ | 21,436 |

|

|

| 22.0 | % | |

Discounts & promotional allowances % to gross sales |

|

| 8.6 | % |

|

| 10.5 | % |

|

|

|

|

|

|

|

| |

Total consolidated net sales increased by $21,436 (approximately 22%) to $118,960 during the year ended December 31, 2014 from $97,524 during the year ended December 31, 2013, primarily as a result of a $21,250 (approximately 19.5%) increase in total consolidated gross sales to $130,216 during the year ended December 31, 2014 from $108,966 during the year ended December 31, 2013, offset by a decrease in discounts and allowances in fiscal year 2014 as compared to fiscal year 2013. The increase in total consolidated gross sales resulted primarily from an increase in volume of products sold. The increase included $18,062 from an increase in volume of products sold and $3,188 from increases in prices of products sold.

Cost of goods sold & gross profit

The following table summarizes our cost of goods sold and gross profit:

| Year ended December 31, |

|

| Change |

| ||||||||||||

| 2014 |

|

| 2013 |

|

| $ |

|

| % |

| ||||||

Purchases, net |

| $ | 59,378 |

|

| $ | 47,145 |

|

| $ | 12,233 |

|

|

| 25.9 | % | |

Testing |

|

| 51 |

|

|

| 37 |

|

|

| 14 |

|

|

| 37.8 | % | |

Supplies |

|

| 1,414 |

|

|

| 780 |

|

|

| 634 |

|

|

| 81.3 | % | |