Attached files

| file | filename |

|---|---|

| EX-10.3 - EX-10.3 - CVR Refining, LP | cvrr201510-kxexhibit103.htm |

| EX-32.1 - EX-32.1 - CVR Refining, LP | cvrr201510-kxexhibit321.htm |

| EX-31.1 - EX-31.1 - CVR Refining, LP | cvrr201510-kxexhibit311.htm |

| EX-31.2 - EX-31.2 - CVR Refining, LP | cvrr201510-kxexhibit312.htm |

| EX-23.1 - EX-23.1 - CVR Refining, LP | cvrr201510-kxexhibit231.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________________________________________

Form 10-K

(Mark One) | |

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015 | |

OR | OR |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

Commission file number: 001-35781

_____________________________________________________________

CVR Refining, LP

(Exact name of registrant as specified in its charter)

Delaware (State or Other Jurisdiction of Incorporation or Organization) | 37-1702463 (I.R.S. Employer Identification No.) |

2277 Plaza Drive, Suite 500 Sugar Land, Texas (Address of Principal Executive Offices) | 77479 (Zip Code) |

Registrant's Telephone Number, including Area Code:

(281) 207-3200

_____________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered |

Common units representing limited partner interests | The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 or Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed based on the New York Stock Exchange closing price on June 30, 2015 (the last business day of the registrant’s second fiscal quarter) was $806,137,619. Common units of the registrant held by each executive officer and director and by each entity or person that, to the registrant’s knowledge, owned 10% or more of the registrant’s outstanding common units as of June 30, 2015 have been excluded from this number in that these persons may be deemed affiliates of the registrant. This determination of possible affiliate status is not necessarily a conclusive determination for other purposes.

Indicate the number of units outstanding of each of the registrant's classes of common units, as of the latest practicable date.

Class | Outstanding at February 16, 2016 |

Common units representing limited partner interests | 147,600,000 units |

TABLE OF CONTENTS

Page | ||

1

GLOSSARY OF SELECTED TERMS

The following are definitions of certain terms used in this Annual Report on Form 10-K for the year ended December 31, 2015 (this "Report").

2-1-1 crack spread — The approximate gross margin resulting from processing two barrels of crude oil to produce one barrel of gasoline and one barrel of distillate. The 2-1-1 crack spread is expressed in dollars per barrel.

backwardation market — Market situation in which futures prices are lower in succeeding delivery months. Also known as an inverted market. The opposite of contango market.

barrel — Common unit of measure in the oil industry which equates to 42 gallons.

blendstocks — Various compounds that are combined with gasoline or diesel from the crude oil refining process to make finished gasoline and diesel fuel; these may include natural gasoline, fluid catalytic cracking unit or FCCU gasoline, ethanol, reformate or butane, among others.

bpd — Abbreviation for barrels per day.

bpcd — Abbreviation for barrels per calendar day, which refers to the total number of barrels processed in a refinery within a year, divided by 365 days, thus reflecting all operational and logistical limitations.

bulk sales — Volume sales through third-party pipelines, in contrast to tanker truck quantity rack sales.

capacity — Capacity is defined as the throughput a process unit is capable of sustaining, either on a barrel per calendar or stream day basis. The throughput may be expressed in terms of maximum sustainable, nameplate or economic capacity. The maximum sustainable or nameplate capacities may not be the most economical. The economic capacity is the throughput that generally provides the greatest economic benefit based on considerations such as crude oil and other feedstock costs, product values and downstream unit constraints.

catalyst — A substance that alters, accelerates, or instigates chemical changes, but is neither produced, consumed nor altered in the process.

contango market — Market situation in which prices for future delivery are higher than the current or spot market price of the commodity. The opposite of backwardation market.

crack spread — A simplified calculation that measures the difference between the price for light products and crude oil. For example, the 2-1-1 crack spread is often referenced and represents the approximate gross margin resulting from processing two barrels of crude oil to produce one barrel of gasoline and one barrel of distillate.

CVR Energy — CVR Energy, Inc., a publicly traded company listed on the NYSE under the ticker symbol "CVI," which indirectly owns our general partner and a majority of our common units.

CVR Partners — CVR Partners, LP, a publicly traded limited partnership listed on the NYSE under the ticker symbol "UAN," which produces and markets nitrogen fertilizers in the form of urea ammonium nitrate ("UAN") and ammonia.

distillates — Primarily diesel fuel, kerosene and jet fuel.

ethanol — A clear, colorless, flammable oxygenated hydrocarbon. Ethanol is typically produced chemically from ethylene, or biologically from fermentation of various sugars from carbohydrates found in agricultural crops and cellulosic residues from crops or wood. It is used in the United States as a gasoline octane enhancer and oxygenate.

feedstocks — Petroleum products, such as crude oil and natural gas liquids, that are processed and blended into refined products, such as gasoline, diesel fuel and jet fuel during the refining process.

general partner — CVR Refining GP, LLC, our general partner, which is an indirect wholly-owned subsidiary of CVR Energy.

2

Group 3 — A geographic subset of the PADD II region comprising refineries in Oklahoma, Kansas, Missouri, Nebraska and Iowa. Current Group 3 refineries include our Coffeyville and Wynnewood refineries; the Valero Ardmore refinery in Ardmore, OK; HollyFrontier's Tulsa refinery in Tulsa, OK and El Dorado refinery in El Dorado, KS; Phillips 66's Ponca City refinery in Ponca City, OK; and CHS' refinery in McPherson, KS.

heavy crude oil — A relatively inexpensive crude oil characterized by high relative density and viscosity. Heavy crude oils require greater levels of processing to produce high value products such as gasoline and diesel fuel.

independent petroleum refiner — A refiner that does not have crude oil exploration or production operations. An independent refiner purchases the crude oil throughputs in its refinery operations from third parties.

Initial Public Offering — The initial public offering of 27,600,000 common units representing limited partner interests ("common units") of CVR Refining, LP, which closed on January 23, 2013 (which includes the underwriters' subsequently-exercised option to purchase additional common units).

light crude oil — A relatively expensive crude oil characterized by low relative density and viscosity. Light crude oils require lower levels of processing to produce high value products such as gasoline and diesel fuel.

Magellan — Magellan Midstream Partners L.P., a publicly traded company, whose business is the transportation, storage and distribution of refined petroleum products.

natural gas liquids — Natural gas liquids, often referred to as NGLs, are both feedstocks used in the manufacture of refined fuels and products of the refining process. Common NGLs used include propane, isobutane, normal butane and natural gasoline.

PADD II — Midwest Petroleum Area for Defense District which includes Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, Oklahoma, South Dakota, Tennessee, and Wisconsin.

petroleum coke (pet coke) — A coal-like substance that is produced during the refining process.

rack sales — Sales which are made at terminals into third-party tanker trucks.

refined products — Petroleum products, such as gasoline, diesel fuel and jet fuel, that are produced by a refinery.

Second Underwritten Offering — The second underwritten offering of 7,475,000 common units of CVR Refining, LP, which closed on June 30, 2014 (which includes the underwriters' subsequently-exercised option to purchase additional common units).

sour crude oil — A crude oil that is relatively high in sulfur content, requiring additional processing to remove the sulfur. Sour crude oil is typically less expensive than sweet crude oil.

spot market — A market in which commodities are bought and sold for cash and delivered immediately.

sweet crude oil — A crude oil that is relatively low in sulfur content, requiring less processing to remove the sulfur. Sweet crude oil is typically more expensive than sour crude oil.

throughput — The volume processed through a unit or a refinery or transported on a pipeline.

turnaround — A periodically required standard procedure to inspect, refurbish, repair and maintain our refineries. This process involves the shutdown and inspection of major processing units and occurs every four to five years.

Underwritten Offering —The underwritten offering of 13,209,236 common units of CVR Refining, LP, which closed

on May 20, 2013 (which includes the underwriters' subsequently-exercised option to purchase additional common units).

WCS — Western Canadian Select crude oil, a medium to heavy, sour crude oil, characterized by an American Petroleum Institute gravity ("API gravity") of between 20 and 22 degrees and a sulfur content of approximately 3.3 weight percent.

WEC — Gary-Williams Energy Corporation, subsequently converted to Gary-Williams Energy Company, LLC and now known as Wynnewood Energy Company, LLC.

3

WRC — Wynnewood Refining Company, LLC, the owner of the Wynnewood, Oklahoma refinery and related assets with a rated capacity of 70,000 bpcd.

WTI — West Texas Intermediate crude oil, a light, sweet crude oil, characterized by an API gravity between 39 and 41 degrees and a sulfur content of approximately 0.4 weight percent that is used as a benchmark for other crude oils.

WTS — West Texas Sour crude oil, a relatively light, sour crude oil characterized by an API gravity of between 30 and 32 degrees and a sulfur content of approximately 2.0 weight percent.

Wynnewood Acquisition — The acquisition by CVR Energy of all the outstanding shares of WEC and its subsidiaries, which owned the Wynnewood, Oklahoma refinery with a rated capacity of 70,000 bpcd and 2.0 million barrels of storage tanks, on December 15, 2011. As of January 2013, WRC became a wholly-owned subsidiary of CVR Refining, LLC. It was previously a wholly-owned subsidiary of WEC.

yield — The percentage of refined products that is produced from crude oil and other feedstocks.

4

PART I

Item 1. Business

Overview

CVR Refining, LP and, unless the context otherwise requires, its subsidiaries ("CVR Refining," the "Partnership," "we," "us," or "our") is an independent downstream energy limited partnership with refining and related logistics assets that operates in the mid-continent region. Our common units are listed on the New York Stock Exchange ("NYSE") under the symbol "CVRR."

We are a petroleum refiner and own two of only seven refineries in Group 3 of the PADD II region of the United States. We own and operate a complex full coking medium-sour crude oil refinery in Coffeyville, Kansas with a rated capacity of 115,000 bpcd and a complex crude oil refinery in Wynnewood, Oklahoma with a rated capacity of 70,000 bpcd capable of processing 20,000 bpcd of light sour crude oils (within its rated capacity of 70,000 bpcd). The combined crude capacity represents approximately 22% of the region's refining capacity. In addition, we also control and operate supporting logistics assets including (i) approximately 336 miles of active owned and leased pipelines, (ii) approximately 150 crude oil transports, (iii) a network of strategically located crude oil gathering tank farms, (iv) approximately 7.0 million barrels of owned and leased crude oil storage, including 0.5 million barrels completed in October 2015, and (v) over 4.5 million barrels of combined refined products and feedstocks storage capacity. The strategic location of our refineries, combined with our supporting logistics assets, provide us with a significant crude oil cost advantage relative to our competitors. Furthermore, our Coffeyville refinery located in southeast Kansas and the Wynnewood refinery located 65 miles south of Oklahoma City, Oklahoma, are approximately 100 miles and 130 miles, respectively, from the crude oil hub at Cushing, Oklahoma, and have access to inland domestic and Canadian crude oils that are priced based on the price of WTI. During the year ended December 31, 2015, the crude oil consumed at the refineries was price advantaged to WTI.

Our refineries' complexity allows us to optimize the yields (the percentage of refined product that is produced from crude oil and other feedstocks) of higher value transportation fuels (gasoline and diesel). Complexity is a measure of a refinery's ability to process lower quality crude oil and feedstocks in an economic manner. Our two refineries' capacity weighted average complexity is 13.0. As a result of key investments in our refining assets and the addition of process units to comply with gasoline quality regulations, both of the refinery's complexities have increased. Our Coffeyville refinery's complexity score is 13.3, and our Wynnewood refinery's complexity score is 12.6. Our high complexity provides us the flexibility to increase our refining margin over comparable refiners with lower complexities. We have achieved significant increases in our refinery crude throughput rates over historical levels. As a result of the increasing complexities, we are capable of processing a variety of crudes, including WTS, WTI, sweet and sour Canadian, and locally gathered crudes.

For the year ended December 31, 2015, our Coffeyville refinery's product yield included gasoline (46%), diesel fuel (primarily ultra-low sulfur diesel) (43%), and pet coke and other refined products such as natural gas liquids ("NGLs") (propane and butane), slurry, sulfur and gas oil (11%). Our Wynnewood refinery's product yield included gasoline (52%), diesel fuel (primarily ultra-low sulfur diesel) (36%), asphalt (5%), jet fuel (4%) and other products (3%) (slurry, sulfur and gas oil, and specialty products such as propylene and solvents).

Our logistics assets have grown substantially since 2005. We have grown our crude oil gathering system capacity from 7,000 bpd in 2005 to over 65,000 bpd currently. The gathering system allows us to gather crude oil that is purchased from independent crude oil producers in Kansas, Nebraska, Oklahoma, Missouri, Colorado and Texas, which serves our two refineries. During 2015, we gathered approximately 69,000 bpd of price-advantaged crudes from our gathering area. The system has field offices in Bartlesville and Pauls Valley, Oklahoma and Plainville, Winfield and Iola, Kansas. Gathered crude oil provides an attractive and competitive base supply of crude oil for the Coffeyville and Wynnewood refineries. In aggregate, these crudes have been sourced at a discount to WTI because of our proximity to the sources of crude oil, existing logistics infrastructure and quality differences. We also have 35,000 bpd of contracted capacity on the Keystone and Spearhead pipelines that allow us to supply price-advantaged Canadian and Bakken crudes to our refineries. We also have contracted capacity on the Pony Express and White Cliffs pipelines, which both became in-service during 2015. Both the Pony Express and White Cliffs pipelines originate in Colorado and extend to Cushing, Oklahoma.

In addition to our gathering system, we own (i) a 170,000 bpd pipeline system that transports crude oil from our Broome Station facility to our Coffeyville refinery, (ii) approximately 1.5 million barrels of crude oil storage capacity that supports the gathering system and our Coffeyville refinery, (iii) approximately 0.9 million barrels of crude oil storage capacity at our Wynnewood refinery and (iv) approximately 1.5 million barrels of crude oil storage capacity in Cushing, Oklahoma. We also lease additional crude oil storage capacity of approximately (v) 2.8 million barrels in Cushing, (vi) 0.2 million barrels in

5

Duncan, Oklahoma and (vii) 0.1 million barrels at our Wynnewood refinery. The Duncan storage supports our Wynnewood refinery while the Cushing storage supports both our Wynnewood and Coffeyville refineries.

For the fiscal years ended December 31, 2015, 2014 and 2013, we generated net sales of $5.2 billion, $8.8 billion and $8.7 billion, respectively, and operating income of $361.7 million, $207.2 million and $603.0 million, respectively.

Our History

Our Coffeyville refining business was operated as a small component of Farmland Industries, Inc. ("Farmland") until March 3, 2004, the date on which Coffeyville Resources, LLC ("CRLLC") completed the acquisition of these assets and the adjacent nitrogen fertilizer plant now operated by CVR Partners, LP ("CVR Partners") through a bankruptcy court auction.

On June 24, 2005, our Coffeyville refinery and related businesses (as well as the adjacent nitrogen fertilizer plant now operated by CVR Partners), were acquired by Coffeyville Acquisition LLC ("CALLC").

On October 26, 2007, CVR Energy completed its initial public offering and its common stock was listed on the NYSE under the symbol "CVI." CVR Energy was formed as a wholly-owned subsidiary of CALLC in September 2006 in order to complete the initial public offering of the businesses acquired by CALLC. At the time of its initial public offering, CVR Energy operated our business and indirectly owned all of the limited partner interests in CVR Partners. In April 2011, CVR Partners completed its initial public offering. CVR Partners' common units are listed on the NYSE under the symbol "UAN." As of December 31, 2015, CVR Energy indirectly owns the general partner and approximately 53% of the outstanding common units of CVR Partners.

On December 15, 2011, CRLLC acquired all of the issued and outstanding shares of WEC. The assets acquired included a 70,000 bpcd rated capacity refinery in Wynnewood, Oklahoma and approximately 2.0 million barrels of storage tanks.

In May 2012, an affiliate of Icahn Enterprises L.P. ("IEP") acquired a majority of CVR Energy's common stock. As of December 31, 2015, IEP and its affiliates owned approximately 82% of CVR Energy's outstanding common stock.

We were formed by CVR Energy in September 2012 in order to own and operate petroleum and auxiliary businesses as a limited partnership. In preparation of the Initial Public Offering, CRLLC contributed its wholly-owned subsidiaries and logistics assets to CVR Refining, LLC ("Refining LLC") in October 2012, and CVR Refining Holdings, LLC ("CVR Refining Holdings"), a subsidiary of CRLLC and an indirect wholly-owned subsidiary of CVR Energy, contributed Refining LLC to us on December 31, 2012.

On January 23, 2013, we completed our Initial Public Offering of 24,000,000 common units to the public priced at $25.00 per unit, resulting in gross proceeds to us of $600.0 million. Of the common units issued, 4,000,000 units were purchased by an affiliate of IEP. Additionally, on January 30, 2013, the underwriters closed their option to purchase an additional 3,600,000 common units at a price of $25.00 per unit, resulting in gross proceeds to us of $90.0 million. The common units, which are listed on the NYSE, began trading on January 17, 2013 under the symbol "CVRR." In connection with the Initial Public Offering, we paid approximately $32.5 million in underwriting fees and incurred approximately $3.9 million of other offering costs.

We have two types of partnership interests outstanding:

• | common units representing limited partner interests, a portion of which we sold in the Initial Public Offering and which are listed on the NYSE; and |

• | a general partner interest, which is not entitled to any distributions, and which is held by our general partner. |

Immediately subsequent to the closing of the Initial Public Offering and through May 19, 2013, common units held by public security holders represented approximately 19% of all outstanding limited partner interests (this includes common units held by an affiliate of IEP, representing approximately 3% of all outstanding limited partner interests) and CVR Refining Holdings held common units approximating 81% of all outstanding limited partner interests.

On May 20, 2013, we completed an underwritten offering (the "Underwritten Offering") by selling 12,000,000 common units to the public at a price of $30.75 per unit. American Entertainment Properties Corporation ("AEPC"), an affiliate of IEP, also purchased an additional 2,000,000 common units at the public offering price in a privately negotiated transaction with a CVR Energy subsidiary, which was completed on May 29, 2013. In connection with the Underwritten Offering, on June 10,

6

2013, we sold an additional 1,209,236 common units to the public at a price of $30.75 per unit in connection with a partial exercise by the underwriters of their option to purchase additional common units. The transactions described in this paragraph are collectively referred to as the “Transactions.” In connection with the Transactions, we paid approximately $12.2 million in underwriting fees and approximately $0.4 million in offering costs.

We utilized net proceeds of approximately $394.0 million from the Underwritten Offering (including the underwriters' option) to redeem 13,209,236 common units from CVR Refining Holdings. We did not receive any of the proceeds from the sale of common units by a CVR Energy subsidiary to AEPC.

Immediately following the closing of the Transactions and prior to June 30, 2014, public security holders held approximately 29% of all outstanding limited partner interests (including common units held by affiliates of IEP, representing approximately 4% of all outstanding limited partner interests), and CVR Refining Holdings held approximating 71% of all outstanding limited partner interests.

On June 30, 2014, we completed a second underwritten offering (the "Second Underwritten Offering") by selling 6,500,000 common units to the public at a price of $26.07 per unit. We paid approximately $5.3 million in underwriting fees and approximately $0.5 million in offering costs. We utilized net proceeds of approximately $164.1 million from the Second Underwritten Offering to redeem 6,500,000 common units from CVR Refining Holdings. Immediately subsequent to the closing of the Second Underwritten Offering and through July 23, 2014, public security holders held approximately 33% of all outstanding limited partner interests, and CVR Refining Holdings held approximately 67% of all outstanding limited partner interests.

On July 24, 2014, we sold an additional 589,100 common units to the public at a price of $26.07 per unit in connection with the underwriters' exercise of their option to purchase additional common units. We utilized net proceeds of approximately $14.9 million from the underwriters' exercise of their option to purchase additional common units to redeem an equal amount of common units from CVR Refining Holdings. Additionally, on July 24, 2014, CVR Refining Holdings sold 385,900 common units to the public at a price of $26.07 per unit in connection with the underwriters' exercise of their remaining option to purchase additional common units. CVR Refining Holdings received net proceeds of $9.7 million.

Immediately subsequent to the closing of the underwriters' option for the Second Underwritten Offering and as of December 31, 2015, public security holders held approximately 34% of all outstanding limited partner interests (including common units owned by affiliates of IEP, representing approximately 4% of all outstanding limited partner interests), and CVR Refining Holdings held approximately 66% of all outstanding limited partner interests. In addition, CVR Refining Holdings owns 100% of the Partnership’s general partner, CVR Refining GP, LLC, which holds a non-economic general partner interest.

7

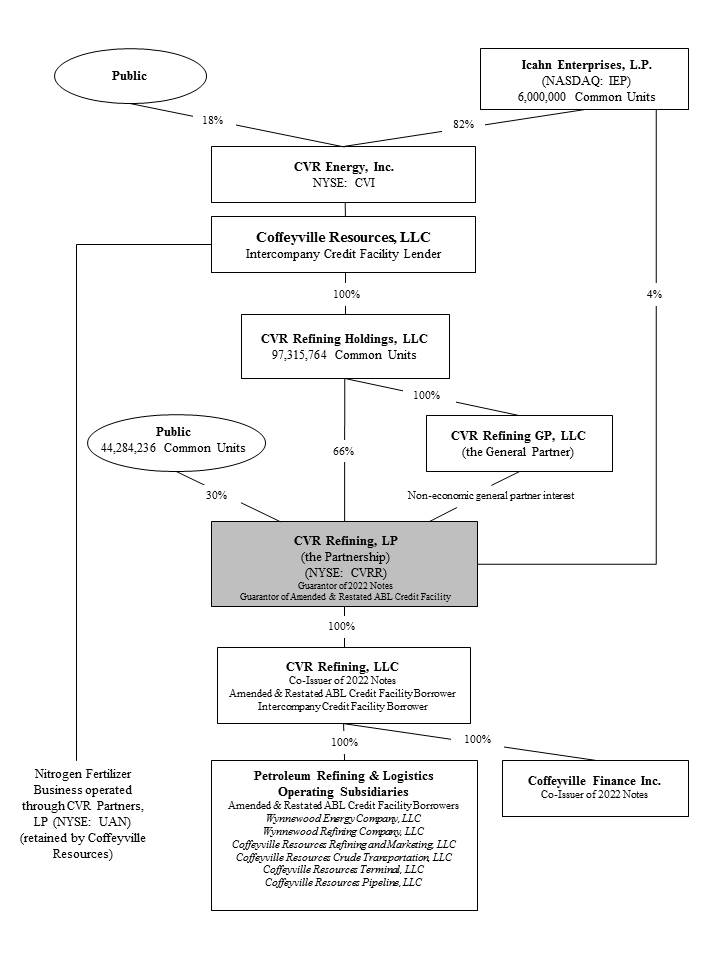

Organizational Structure and Related Ownership

The following chart illustrates our organizational structure as of the date of this Report.

8

Crude and Feedstock Supply

Our Coffeyville refinery has the capability to process blends of a variety of crude oil ranging from heavy sour to light sweet crude oil. Currently, our Coffeyville refinery crude oil slate consists of a blend of mid-continent domestic grades and various Canadian medium and heavy sours, and it has recently introduced North Dakota Bakken and other similarly sourced crudes into its crude slate. While crude oil has constituted over 90% of our Coffeyville refinery's total throughput over the last five years, other feedstock inputs include normal butane, natural gasoline, alkylation feeds, naphtha, gas oil and vacuum tower bottoms.

Our Wynnewood refinery has the capability to process blends of a variety of crude oil ranging from medium sour to light sweet crude oil, although isobutane, gasoline components, and normal butane are also typically used. Historically most of the Wynnewood refinery's crude oil has been acquired domestically, mainly from Texas and Oklahoma, but it can also access and process various light and medium Canadian grades.

Crude oil is supplied to our refineries through our wholly-owned gathering system and by pipeline. We have continued to increase the number of barrels of crude oil supplied through our crude oil gathering system in 2015 and it now has the capacity of supplying over 65,000 bpd of crude oil to our refineries. For the year ended December 31, 2015, the gathering system supplied approximately 39% of both of the Coffeyville and Wynnewood refineries' crude oil demand. Locally produced crude oils are delivered to the refineries at a discount to WTI, and although sometimes slightly heavier and more sour, offer good economics to the refineries. These crude oils are light and sweet enough to allow us to blend higher percentages of lower cost crude oils such as heavy sour Canadian crude oil while maintaining our target medium sour blend with an API gravity of between 28 and 36 degrees and between 0.9% and 1.2% sulfur. Crude oils sourced outside of our proprietary gathering system are delivered to Cushing, Oklahoma by various pipelines, including the Keystone and Spearhead pipelines, and subsequently to our Broome Station facility via the Plains pipeline. In May 2015 and November 2015, our contracted capacity included the Pony Express and White Cliffs pipelines, respectively. From the Broome Station facility, crude oil is delivered to our Coffeyville refinery via our own 170,000 bpd pipeline system. Crude oils are delivered to the Wynnewood refinery by three separate pipelines, and received into storage tanks at terminals located at or near the refinery.

For the year ended December 31, 2015, our Coffeyville refinery's crude oil supply blend was comprised of approximately 85.4% light sweet crude oil, 12.8% heavy sour crude oil and 1.8% light/medium sour crude oil. For the year ended December 31, 2015, our Wynnewood refinery's crude oil supply blend was comprised of approximately 99.5% light sweet crude oil and approximately 0.5% light/medium sour crude oil. The light sweet crude oil supply blend includes our locally gathered crude oil.

The Coffeyville refinery is connected to the mid-continent natural gas liquids commercial hub of Conway, Kansas by the inbound Enterprise Pipeline Blue Line. Natural gas liquids feedstock supplies such as butanes and natural gasoline are sourced and delivered directly into the refinery. In addition, Coffeyville's proximity to Conway provides access to the natural gas liquid and liquid petroleum gas fractionation and storage capabilities as well as the commercial markets available at Conway.

Crude Oil Supply Agreement

On August 31, 2012, Coffeyville Resources Refining and Marketing, LLC ("CRRM") and Vitol Inc. ("Vitol") entered into an Amended and Restated Crude Oil Supply Agreement (as amended, the "Vitol Agreement"). Under the Vitol Agreement, Vitol supplies us with crude oil and intermediation logistics, which helps us to reduce our inventory position and mitigate crude oil pricing risk. The Vitol Agreement will automatically renew for successive one-year terms (each such term, a "Renewal Term") unless either party provides the other with notice of nonrenewal at least 180 days prior to expiration of any Renewal Term. The Vitol Agreement currently extends through December 31, 2016.

Refining Process

Coffeyville Refinery. Our Coffeyville refinery is a 115,000 bpcd rated capacity facility with operations including fractionation, catalytic cracking, hydrotreating, reforming, coking, isomerization, alkylation, sulfur recovery and propane and butane recovery. Our Coffeyville refinery benefits from significant refining unit redundancies, which include two crude oil distillation and vacuum towers, three sulfur recovery units and four hydrotreating units. These redundancies allow us to continue to receive and process crude oil even if one tower requires unplanned maintenance without having to shut down the entire refinery in the case of a major unit turnaround. In addition, our Coffeyville refinery has a redundant supply of hydrogen pursuant to our feedstock and shared services agreement with CVR Partners. Our Coffeyville refinery has the capability to process blends of a variety of crude oil ranging from heavy sour to light sweet crude oil into products such as gasoline, diesel, kerosene, propane, butane, sulfur, heavy oil and petroleum coke. During the year ended December 31, 2015, our Coffeyville

9

refinery processed approximately 113,300 bpd and 8,400 bpd of crude oil and feedstocks and blendstocks, respectively. These throughput rates for 2015 reflect the first phase of the major scheduled turnaround completed in mid-November 2015.

Wynnewood Refinery. Our Wynnewood refinery is a 70,000 bpcd rated capacity facility with operations including fractionation, cracking, hydrotreating, hydrocracking, reforming, solvent deasphalting, alkylation, sulfur recovery and propane and butane recovery. Similar to our Coffeyville refinery, our Wynnewood refinery benefits from unit redundancies, including two crude oil distillation and vacuum towers and four hydrotreating units. Our Wynnewood refinery has the capability to process blends of a variety of crude oil ranging from medium sour to light sweet crude oil (although isobutane, gasoline components, and normal butane are also typically used) into products such as gasoline, jet fuel, kerosene, propane, butane, propylene, sulfur, solvents, heavy oil and asphalt. During the year ended December 31, 2015, our Wynnewood refinery processed approximately 79,800 bpd and 3,300 bpd of crude oil and feedstocks and blendstocks, respectively.

Marketing and Distribution

We focus our Coffeyville petroleum product marketing efforts in the central mid-continent area, because of its relative proximity to the refinery and pipeline access. Coffeyville also has access to the Rocky Mountain area. Coffeyville engages in rack marketing, which is the supply of product through tanker trucks directly to customers located in close geographic proximity to the refinery and to customers at throughput terminals on the refined products distribution systems of Magellan and NuStar. Coffeyville also makes bulk sales (sales into third-party pipelines) into the mid-continent markets and other destinations utilizing the product pipeline networks owned by Magellan, Enterprise and NuStar. The outbound Enterprise Pipeline Red Line provides Coffeyville with access to the NuStar Refined Products Pipeline system. This allows gasoline and ULSD product sales from Kansas up into North Dakota.

The Wynnewood refinery ships its finished product via pipeline, railcar, and truck. It focuses its efforts in the southern portion of the Magellan system which covers all of Oklahoma, parts of Arkansas as well as eastern Missouri, and all other Magellan terminals. The pipeline system is also able to flow in the opposite direction, providing access to Texas markets as well as some adjoining states with pipeline connections. Wynnewood also sells jet fuel to the U.S. Department of Defense via its segregated truck rack and can offer asphalts, solvents and other specialty products via both truck and rail.

Customers

Customers for our refined products primarily include retailers, railroads and farm cooperatives and other refiners/marketers in Group 3 of the PADD II region because of their relative proximity to our refineries and pipeline access. We sell bulk products to long-standing customers at spot market prices based on a Group 3 basis differential to prices quoted on the New York Mercantile Exchange ("NYMEX"), which are reported by industry market-related indices such as Platts and Oil Price Information Service.

We also have a rack marketing business supplying product through tanker trucks directly to customers located in proximity to our Coffeyville and Wynnewood refineries, as well as to customers located at throughput terminals on refined products distribution systems run by Magellan and NuStar. Rack sales are at posted prices that are influenced by competitor pricing and Group 3 spot market differentials. Additionally, our Wynnewood refinery supplies jet fuel to the U.S. Department of Defense. In addition, our Coffeyville refinery sells a by-product of its refining operations, petroleum coke, to an affiliate, CVR Partners, pursuant to a multi-year agreement. For the year ended December 31, 2015, our two largest customers accounted for approximately 14% and 9% of our net sales while approximately 53% of our net sales were made to our ten largest customers.

Competition

We compete primarily on the basis of price, reliability of supply, availability of multiple grades of products and location. The principal competitive factors affecting our refining operations are cost of crude oil and other feedstock costs, refinery complexity, refinery efficiency, refinery product mix and product distribution and transportation costs. The location of our refineries provides us with a reliable supply of crude oil and a transportation cost advantage over our competitors. We primarily compete against five refineries operated in the mid-continent region. In addition to these refineries, we compete against trading companies, as well as other refineries located outside the region that are linked to the mid-continent market through an extensive product pipeline system. These competitors include refineries located near the Gulf Coast and the Texas panhandle region. Our competition also includes branded, integrated and independent oil refining companies, such as Phillips 66, HollyFrontier, CHS, Valero and Flint Hills Resources.

10

Seasonality

Our business experiences seasonal effects as demand for gasoline products is generally higher during the summer months than during the winter months due to seasonal increases in highway traffic and road construction work. Demand for diesel fuel is higher during the planting and harvesting seasons. As a result, our results of operations for the first and fourth calendar quarters are generally lower compared to our results for the second and third calendar quarters. In addition, unseasonably cool weather in the summer months and/or unseasonably warm weather in the winter months in the markets in which we sell our petroleum products can impact the demand for gasoline and diesel fuel. The demand for asphalt is also seasonal and is generally higher during the months of March through October.

Environmental Matters

Our businesses are subject to extensive and frequently changing federal, state and local, environmental and health and safety laws and regulations governing the emission and release of hazardous substances into the environment, the treatment and discharge of waste water, the storage, handling, use and transportation of petroleum products, and the characteristics and composition of gasoline and diesel fuels. These laws and regulations, their underlying regulatory requirements and the enforcement thereof impact our business and operations by imposing:

• | restrictions on operations or the need to install enhanced or additional controls; |

• | the need to obtain and comply with permits, licenses and authorizations; |

• | requirements for the investigation and remediation of contaminated soil and groundwater at current and former facilities (if any) and liability for off-site waste disposal locations; and |

• | specifications for the products marketed by us, primarily gasoline and diesel fuel. |

Our operations require numerous permits, licenses and authorizations. Failure to comply with these permits or environmental laws and regulations could result in fines, penalties or other sanctions or a revocation of our permits. In addition, the laws and regulations to which we are subject are often evolving and many of them have become more stringent or have become subject to more stringent interpretation or enforcement by federal or state agencies. The ultimate impact on our business of complying with evolving laws and regulations is not always clearly known or determinable due in part to the fact that our operations may change over time and certain implementing regulations for laws, such as the federal Clean Air Act, have not yet been finalized, are under governmental or judicial review or are being revised. These laws and regulations could result in increased capital, operating and compliance costs.

The principal environmental risks associated with our businesses are outlined below with additional details included in Part I, Item 1A, Risk Factors and Part II, Item 8, Note 11 ("Commitments and Contingencies") of this Report.

The Federal Clean Air Act

The federal Clean Air Act and its implementing regulations, as well as the corresponding state laws and regulations that regulate emissions of pollutants into the air, affect our operations both directly and indirectly. Direct impacts may occur through the federal Clean Air Act's permitting requirements and/or emission control requirements relating to specific air pollutants, as well as the requirement to maintain a risk management program to help prevent accidental releases of certain regulated substances. The federal Clean Air Act indirectly affects our operations by extensively regulating the air emissions of sulfur dioxide ("SO2"), volatile organic compounds, nitrogen oxides and other substances, including those emitted by mobile sources, which are direct or indirect users of our products.

Some or all of the standards promulgated pursuant to the federal Clean Air Act, or any future promulgations of standards, may require the installation of controls or changes to our operations in order to comply. If new controls or changes to operations are needed, the costs could be material. These new requirements, other requirements of the federal Clean Air Act, or other presently existing or future environmental regulations could cause us to expend substantial amounts to comply and/or permit our facilities to produce products that meet applicable requirements.

The regulation of air emissions under the federal Clean Air Act requires that we obtain various construction and operating permits and incur capital expenditures for the installation of certain air pollution control devices at our petroleum operations when regulations change or we add new equipment or modify our existing equipment. Various regulations specific to our operations have been implemented, such as National Emission Standard for Hazardous Air Pollutants ("NESHAP"), New

11

Source Performance Standards ("NSPS") and New Source Review/Prevention of Significant Deterioration ("PSD"). We have incurred, and expect to continue to have to make substantial capital expenditures to attain or maintain compliance with these and other air emission regulations that have been promulgated or may be promulgated or revised in the future.

On September 12, 2012, the U.S. Environmental Protection Agency (the "EPA") published in the Federal Register final revisions to its NSPS for process heaters and flares at petroleum refineries. The EPA originally issued final standards in June 2008, but the portions of the rule relating to process heaters and flares were stayed pending reconsideration of certain provisions. The final standards regulate emissions of nitrogen oxide from process heaters and emissions of SO2 from flares, as well as require certain work practice and monitoring standards for flares. We do not believe that the costs of complying with the rule will be material.

On August 14, 2012, the EPA sent both the Wynnewood and Coffeyville refineries letters regarding the EPA's 2012 enforcement alert entitled EPA Enforcement Targets Flaring Efficiency Violations signaling the agency's intention to begin a national enforcement program to conduct compliance evaluations and take enforcement actions against petroleum refining companies that operate flares that are not in compliance with standards articulated in the Enforcement Alert. The Enforcement Alert identified new standards that refiners are required to meet for flaring combustion efficiency. The EPA entered into consent decrees with several refining companies. Because the EPA has not specifically told us that our operations are not in compliance, we cannot say with certainty whether or when we may become an enforcement target under this initiative.

Refer to Part II, Item 8, Note 11 ("Commitments and Contingencies") of this Report for further discussion of recent environmental matters related to the Clean Air Act including the "Flood, Crude Oil Discharge and Insurance" and certain "Environmental, Health and Safety ("EHS") Matters," such as the "Coffeyville Second Consent Decree," "Wynnewood Clean Air Act Compliance" and other compliance evaluations.

Our Coffeyville refinery's Clean Air Act Title V operating permit has expired, and has not yet been re-issued. Our Coffeyville refinery timely submitted an application for renewal, and therefore is authorized under the regulations to operate under the current permit until the permit is re-issued. The permit renewal process has begun, and capital costs or expenses, if any, related to changes to these permits are not known yet, but are not expected to be material.

The Federal Clean Water Act

The federal Clean Water Act ("CWA") and its implementing regulations, as well as the corresponding state laws and regulations that regulate the discharge of pollutants into the water, affect our operations. Direct impacts occur through the CWA's permitting requirements, which establish discharge limitations based on technology standards, water quality standards, and restrictions on the total maximum daily load of pollutants that may be released to a particular water body based on its use. In addition, water resources are becoming and in the future may become scarcer, and many refiners, including CRRM and Wynnewood Refining Company, LLC ("WRC"), are subject to restrictions on their ability to use water in the event of low availability conditions. Both CRRM and WRC have contracts in place to receive additional water during low-flow conditions, but these conditions could change over time if water becomes scarce.

The Wynnewood refinery's CWA permit ("OPDES permit") has expired. The refinery timely submitted their renewal application, and therefore is authorized to continue discharging under the expired permit until the Oklahoma Department of Environmental Quality ("ODEQ") re-issues the permit. The permit renewal process has begun, and capital costs or expenses related to changes to this permit, if any, are not expected to be material.

Release Reporting

The release of hazardous substances or extremely hazardous substances into the environment is subject to release reporting requirements under federal and state environmental laws. Our facilities periodically experience releases of hazardous substances and extremely hazardous substances. Our refineries periodically have excess emission events from flaring and other planned and unplanned start up, shutdown and malfunction events. From time to time, the EPA has conducted inspections and issued information requests to us with respect to our compliance with reporting requirements under the Comprehensive Environmental Response, Compensation and Liability Act ("CERCLA") and the Emergency Planning and Community Right-to-Know Act. If we fail to timely or properly report a release, or if the release violates the law or our permits, it could cause us to become the subject of a governmental enforcement action or third-party claims. Government enforcement or third-party claims relating to releases of hazardous or extremely hazardous substances could result in significant expenditures and liability.

12

Fuel Regulations

Tier 2, Low Sulfur Fuels. In February 2000, the EPA promulgated the Tier 2 Motor Vehicle Emission Standards Final Rule for all passenger vehicles, establishing standards for sulfur content in gasoline that were required to be met by 2006. In addition, in January 2001, the EPA promulgated its on-road diesel regulations, which required a 97% reduction in the sulfur content of diesel fuel sold for highway use by June 1, 2006, with full compliance by January 1, 2010. Our refineries are in compliance with the EPA's low sulfur gasoline and diesel fuel standards.

Tier 3. In April 2014, the EPA promulgated the Tier 3 Motor Vehicle Emission and Fuel Standards, which will require that gasoline contain no more than ten parts per million of sulfur on an annual average basis. Refineries must be in compliance with the more stringent emission standards by January 1, 2017; however, compliance with the rule is extended until January 1, 2020 for approved small volume refineries and small refiners. In March 2015, the EPA approved the Wynnewood refinery's application requesting "small volume refinery" status; therefore, its compliance deadline is January 1, 2020. It is not anticipated that the refineries will require additional controls or capital expenditures to meet the anticipated new standard.

Mobile Source Air Toxic II Emissions

In 2007, the EPA promulgated the Mobile Source Air Toxic II ("MSAT II") rule that requires the reduction of benzene in gasoline by 2011. The MSAT II projects for CRRM and WRC were completed within the compliance deadline of November 1, 2014. The projects were completed at a total cost of approximately $48.3 million and $89.0 million, excluding capitalized interest, by CRRM and WRC, respectively.

Renewable Fuel Standards

Refer to Part I, Item 1A, Risk Factors, If sufficient RINs are unavailable for purchase or if we have to pay a significantly higher price for RINs, or if we are otherwise unable to meet the EPA's Renewable Fuels Standard mandates, our business, financial condition and results of operations could be materially adversely affected, and Part II, Item 8, Note 11 ("Commitments and Contingencies"), "Environmental, Health and Safety ("EHS") Matters" of this Report for further discussion of the "Renewable Fuel Standards."

Greenhouse Gas Emissions

Refer to Part I, Item 1A, Risk Factors, Climate change laws and regulations could have a material adverse effect on our results of operations, financial condition and cash flows, of this Report for further discussion of the Greenhouse Gas ("GHG") Emissions regulations.

RCRA

Our operations are subject to the Resource Conservation and Recovery Act ("RCRA") requirements for the generation, transportation, treatment, storage and disposal of solid and hazardous wastes. When feasible, RCRA-regulated materials are recycled instead of being disposed of on-site or off-site. RCRA establishes standards for the management of solid and hazardous wastes. Besides governing current waste disposal practices, RCRA also addresses the environmental effects of certain past waste disposal practices, the recycling of wastes and the regulation of underground storage tanks containing regulated substances. Refer to Part II, Item 8, Note 11 ("Commitments and Contingencies"), "Environmental, Health and Safety ("EHS") Matters" for further discussion of "RCRA Compliance Matters."

Waste Management. There are two closed hazardous waste units at the Coffeyville refinery and eight other hazardous waste units in the process of being closed pending state agency approval. There is one closed hazardous waste unit and one active hazardous waste storage tank at the Wynnewood refinery. In addition, one closed interim status hazardous waste land farm located at the now-closed Phillipsburg terminal is under long-term post closure care.

Impacts of Past Manufacturing. The 2004 Consent Decree that CRRM signed with the EPA and the Kansas Department of Health and Environment (the "KDHE") required us to assume two RCRA corrective action orders issued to Farmland, the prior owner of the Coffeyville refinery. We are subject to a 1994 EPA administrative order related to investigation of possible past releases of hazardous materials to the environment at the Coffeyville refinery. In accordance with the order, we have documented existing soil and groundwater conditions, which require investigation or remediation projects. The now-closed Phillipsburg terminal is subject to a 1996 EPA administrative order related to investigation of releases of hazardous materials to the environment at the Phillipsburg terminal, which operated as a refinery until 1991. Remediation at both sites, if necessary, will be based on the results of the investigations. The Wynnewood refinery operates under a RCRA permit. A RCRA facility

13

investigation has been completed in accordance with the terms of the permit. Based on the facility investigation and other available information, ODEQ and WRC have entered into a Consent Order requiring further investigations of groundwater conditions and enhancements of existing remediation systems. Additional remediation, if necessary, will be based upon the results of the further investigation.

The anticipated investigation and remediation costs through 2019 were estimated, as of December 31, 2015, to be as follows:

Facility | Site Investigation Costs | Capital Costs | Total Operation & Maintenance Costs Through 2019 | Total Estimated Costs Through 2019 | |||||||||||

(in millions) | |||||||||||||||

Coffeyville Refinery | $ | 0.3 | $ | — | $ | 0.9 | $ | 1.2 | |||||||

Phillipsburg Terminal | 0.4 | — | 1.1 | 1.5 | |||||||||||

Wynnewood Refinery | 0.3 | — | 1.8 | 2.1 | |||||||||||

Total Estimated Costs | $ | 1.0 | $ | — | $ | 3.8 | $ | 4.8 | |||||||

These estimates are based on current information and could increase or decrease as additional information becomes available through our ongoing remediation and investigation activities. At this point, we have estimated that, over ten years starting in 2016, we will spend approximately $7.3 million to remedy impacts from past manufacturing activity at the Coffeyville refinery and to address existing soil and groundwater contamination at the now-closed Phillipsburg terminal and at the Wynnewood refinery. It is possible that additional costs will be required after this ten year period. We spent approximately $2.1 million in 2015 associated with related remediation.

Financial Assurance

We are required under the 2004 Consent Decree to establish financial assurance to secure the projected clean-up costs posed by the Coffeyville and the now-closed Phillipsburg facilities in the event we fail to fulfill our clean-up obligations. In accordance with the 2004 Consent Decree as modified by a 2010 agreement between CRRM, Coffeyville Resources Terminal, LLC, the EPA and the KDHE, this financial assurance is currently provided by a bond in the amount of $4.3 million for clean-up obligations at the Phillipsburg terminal and a letter of credit in the amount of $0.2 million for estimated costs to close regulated hazardous waste management units at the Coffeyville refinery. Additional self-funded financial assurance of approximately $4.9 million and $2.4 million is required by our post-closure care obligations and the 2004 Consent Decree for clean-up costs at the Coffeyville refinery and Phillipsburg terminal, respectively. The $4.3 million bond amount is reduced each year based on actual expenditures for corrective actions and the letter of credit and the self-funded mechanisms are re-evaluated and adjusted on an annual basis. Current RCRA financial assurance requirements for the Wynnewood refinery total $0.2 million for hazardous waste storage tank closure and post-closure monitoring of a closed storm water retention pond.

Environmental Remediation

Under the CERCLA, RCRA, and related state laws, certain persons may be liable for the release or threatened release of hazardous substances. These persons include the current owner or operator of property where a release or threatened release occurred, any persons who owned or operated the property when the release occurred, and any persons who disposed of, or arranged for the transportation or disposal of, hazardous substances at a contaminated property. Liability under CERCLA is strict, and under certain circumstances, joint and several, so that any responsible party may be held liable for the entire cost of investigating and remediating the release of hazardous substances. Similarly, the Oil Pollution Act of 1990 generally subjects owners and operators of facilities to strict, joint and several liability for all containment and clean-up costs, natural resource damages, and potential governmental oversight costs arising from oil spills into the waters of the United States, which has been broadly interpreted to include most water bodies including intermittent streams.

As is the case with all companies engaged in similar industries, we face potential exposure from future claims and lawsuits involving environmental matters, including soil and water contamination, personal injury or property damage allegedly caused by crude oil or hazardous substances that we manufactured, handled, used, stored, transported, spilled, disposed of or released. We cannot assure you that we will not become involved in future proceedings related to our release of hazardous or extremely hazardous substances or crude oil or that, if we were held responsible for damages in any existing or future proceedings, such costs would be covered by insurance or would not be material. Refer to Part II, Item 8, Note 11 ("Commitments and Contingencies"), "Flood, Crude Oil Discharge and Insurance" of this Report for discussion of the environmental remediation associated with the discharge of crude oil on July 1, 2007 at the Coffeyville refinery.

14

Environmental Insurance

We are covered by CVR Energy's site pollution legal liability insurance policy with an aggregate limit of $50.0 million per pollution condition, subject to a self-insured retention of $1.0 million. The policy includes business interruption coverage, subject to a 5-day waiting period deductible. This insurance expires on March 1, 2016 and is expected to be renewed without any material changes in terms. The policy insures any location owned, leased, rented or operated by CVR Refining, including the Coffeyville refinery and the Wynnewood refinery. The policy insures certain pollution conditions at or migrating from a covered location, certain waste transportation and disposal activities and business interruption.

In addition to the site pollution legal liability insurance policy, we benefit from umbrella and excess casualty insurance policies maintained by CVR Energy having an aggregate and occurrence limit of $200.0 million, subject to a self-insured retention of $2.0 million. This insurance provides coverage due to named perils for claims involving pollutants where the discharge is sudden and accidental and first commenced at a specific day and time during the policy period. The casualty insurance policies, including umbrella and excess policies, expire on March 1, 2016 and are expected to be renewed or replaced by insurance policies containing materially equivalent sudden and accidental pollution coverage with no reduction in limits.

The site pollution legal liability policy and the pollution coverage provided in the casualty insurance policies contains discovery requirements, reporting requirements, exclusions, definitions, conditions and limitations that could apply to a particular pollution claim, and there can be no assurance such claim will be adequately insured for all potential damages.

Safety, Health and Security Matters

We are subject to a number of federal and state laws and regulations related to safety, including the Occupational Safety and Health Act ("OSHA") and comparable state statutes, the purpose of which are to protect the health and safety of workers. We also are subject to OSHA Process Safety Management regulations, which are designed to prevent or minimize the consequences of catastrophic releases of toxic, reactive, flammable or explosive chemicals.

We operate a comprehensive safety, health and security program, with participation by employees at all levels of the organization. We have developed comprehensive safety programs aimed at preventing OSHA recordable incidents. Despite our efforts to achieve excellence in our safety and health performance, there can be no assurances that there will not be accidents resulting in injuries or even fatalities. We routinely audit our programs and consider improvements in our management systems.

The Wynnewood refinery has been the subject of a number of OSHA inspections since 2006. As a result of these inspections, the Wynnewood refinery entered into four OSHA settlement agreements in 2008, pursuant to which it has agreed to undertake certain studies, conduct abatement activities, and revise and enhance certain OSHA compliance programs. The remaining costs associated with implementing these studies, abatement activities and program revisions are not expected to exceed $1.0 million.

Refer to Part II, Item 8, Note 11 ("Commitments and Contingencies"), "Wynnewood Refinery Incident" of this Report for further discussion of OSHA matters related to the Wynnewood refinery boiler explosion.

Process Safety Management. We maintain a process safety management ("PSM") program. This program is designed to address all aspects of the OSHA guidelines for developing and maintaining a comprehensive PSM program. We will continue to audit our programs and consider improvements in our management systems and equipment.

Emergency Planning and Response. We have an emergency response plan that describes the organization, responsibilities and plans for responding to emergencies in our facilities. This plan is communicated to local regulatory and community groups. We have on-site warning siren systems and personal radios. We will continue to audit our programs and consider improvements in our management systems and equipment.

Employees

As of December 31, 2015, we employed 968 direct employees. These employees are covered by health insurance, disability and retirement plans established by CVR Energy. We believe that our relationship with our employees is good.

As of December 31, 2015, the Coffeyville refinery employed 610 of our employees, about 54% of whom were covered by a collective bargaining agreement. These employees are affiliated with five unions of the Metal Trades Department of the AFL-CIO ("Metal Trade Unions") and the United Steel, Paper and Forestry, Rubber, Manufacturing, Energy, Allied Industrial and

15

Service Workers International Union, AFL-CIO-CLC ("United Steelworkers"). We are a party to a collective bargaining agreement with the Metal Trade Unions covering union members who work directly at the Coffeyville refinery. The agreement expires in March 2019. In addition, a collective bargaining agreement with the United Steelworkers, which covers CVR Refining's unionized employees who work in crude transportation, expires in March 2017 and automatically renews on an annual basis thereafter unless a written notice is received sixty days in advance of the relevant expiration date.

As of December 31, 2015, the Wynnewood refinery employed 317 of our employees, about 59% of whom were represented by the International Union of Operating Engineers. The collective bargaining agreement with the International Union of Operating Engineers with respect to the Wynnewood refinery expires in June 2017.

We also rely on the services of employees of CVR Energy and its subsidiaries in the operation of our business pursuant to a services agreement among us, CVR Energy and our general partner. Additionally, the Partnership's general partner manages the Partnership's operations and activities as specified in the partnership agreement and had 11 employees as of December 31, 2015. For more information on these agreements, refer to Part II, Item 8, Note 14 ("Related Party Transactions") of this Report.

Available Information

Our website address is www.cvrrefining.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports, are available free of charge through our website under "Investor Relations," as soon as reasonably practicable after the electronic filing of these reports is made with the Securities and Exchange Commission (the "SEC"). In addition, our Corporate Governance Guidelines, Codes of Ethics and Charters of the Audit Committee and Compensation Committee of the Board of Directors of our general partner are available on our website. These guidelines, policies and charters are also available in print without charge to any unitholder requesting them. We do not intend for information contained in our website to be part of this Report.

Trademarks, Trade Names and Service Marks

This Report may include our and our affiliates' trademarks, including the CVR Energy logo, Coffeyville Resources, the Coffeyville Resources logo, the CVR Partners, LP logo and the CVR Refining, LP logo, each of which is registered or for which we are applying for federal registration with the United States Patent and Trademark Office. This Report may also contain trademarks, service marks, copyrights and trade names of other companies.

16

Item 1A. Risk Factors

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors together with all of the other information included in this Report.

If any of the following risks were to occur, our business, financial condition, results of operations and cash available for distribution could be materially adversely affected. In such cases, we might not be able to make distributions on our common units, the trading price of our common units could decline, and you could lose all or part of your investment.

Risks Inherent in Our Business

We may not have sufficient available cash to pay any quarterly distribution on our common units.

We may not have sufficient available cash (which is defined as Adjusted EBITDA reduced for cash needed for (i) debt service, (ii) reserves for environmental and maintenance capital expenditures, (iii) reserves for major scheduled turnaround expenses and, to the extent applicable, (iv) reserves for future operating or capital needs that the board of directors of our general partner deems necessary or appropriate) each quarter to enable us to pay any distributions to our common unitholders. Furthermore, our partnership agreement does not require us to pay distributions on a quarterly basis or otherwise. The board of directors of our general partner may at any time, for any reason, change our cash distribution policy or decide not to make any distribution. The amount of cash we will be able to distribute on our common units principally depends on the amount of cash we generate from our operations, which is directly dependent upon the margins we generate. Please see "— The price volatility of crude oil and other feedstocks, refined products and utility services may have a material adverse effect on our profitability and our ability to pay distributions to unitholders" below.

The price volatility of crude oil and other feedstocks, refined products and utility services may have a material adverse effect on our earnings and our ability to pay distributions to unitholders.

Our financial results are primarily affected by the relationship, or margin, between refined product prices and the prices for crude oil and other feedstocks. When the margin between refined product prices and crude oil and other feedstock prices tightens, our earnings, profitability and cash flows are negatively affected. Refining margins historically have been volatile and are likely to continue to be volatile, as a result of a variety of factors including fluctuations in prices of crude oil, other feedstocks and refined products. Continued future volatility in refining industry margins may cause a decline in our results of operations, since the margin between refined product prices and crude oil and other feedstock prices may decrease below the amount needed for us to generate net cash flow sufficient for our needs. The effect of changes in crude oil prices on our results of operations therefore depends in part on how quickly and how fully refined product prices adjust to reflect these changes. A substantial or prolonged increase in crude oil prices without a corresponding increase in refined product prices, or a substantial or prolonged decrease in refined product prices without a corresponding decrease in crude oil prices, could have a significant negative impact on our earnings, results of operations and ability to pay distributions to unitholders.

Our profitability is also impacted by our ability to purchase crude oil at a discount to benchmark crude oils, such as WTI, as we do not produce any crude oil and must purchase all of the crude oil we refine. Crude oil differentials can fluctuate significantly based upon overall economic and crude oil market conditions. Adverse changes in crude oil differentials can adversely impact refining margins, earnings and cash flows. In addition, our purchases of crude oil, although based on WTI prices, have historically been at a discount to WTI because of our proximity to the sources, existing logistics infrastructure and quality differences. Any change in the sources of our crude oil, infrastructure or logistical improvements or quality differences could result in a reduction of our historical discount to WTI and may result in a reduction of our cost advantage.

Refining margins are also impacted by domestic and global refining capacity. Downturns in the economy reduce the demand for refined fuels and, in turn, generate excess capacity. In addition, the expansion and construction of refineries domestically and globally can increase refined fuel production capacity. Excess capacity can adversely impact refining margins, earnings and cash flows. The Arabian Gulf and Far East regions have added refining capacity in 2015 and 2016.

We are significantly affected by developments in the markets in which we operate. For example, numerous pipeline projects in 2014 expanded the connectivity of the Cushing and Permian Basin markets to the gulf coast, resulting in a decrease in the domestic crude advantage.

17

Volatile prices for natural gas and electricity also affect our manufacturing and operating costs. Natural gas and electricity prices have been, and will continue to be, affected by supply and demand for fuel and utility services in both local and regional markets.

The amount of cash we have available for distribution to unitholders depends primarily on our cash flow and not solely on profitability.

The amount of cash we have available for distribution depends primarily upon our cash flow and not solely on profitability, which may be affected by items that do not fully impact net income in a given quarter. We may have working capital changes as well as extraordinary capital expenditures and major maintenance expenses in the future. See "Management's Discussion and Analysis of Financial Condition and Results of Operation — Liquidity and Capital Resources — Capital Spending." While these items may not affect our profitability in a quarter, they would reduce the amount of cash available for distribution with respect to such quarter. As a result, we may make cash distributions during periods when we report losses and may not make cash distributions during periods when we report net income.

The amount of our quarterly cash distributions, if any, will vary significantly both quarterly and annually and will be directly dependent on the performance of our business which is volatile and seasonal.

Historically, our business performance has been volatile and seasonal. For instance, our results of operations for the second and third quarters are generally higher than our results of operations for the first and fourth quarters, as demand for gasoline products increases due to higher highway traffic and road construction work during the summer months, and demand for diesel fuel decreases somewhat due to decreased agricultural activity in the winter. We expect that our future business performance will be more volatile and seasonal, and that our cash flows will be less stable, than the business performance and cash flows of most publicly traded partnerships. Unlike most publicly traded partnerships, we do not have a minimum quarterly distribution or employ structures intended to consistently maintain or increase distributions over time. Because our quarterly distributions will significantly correlate to the cash we generate each quarter after payment of our fixed and variable expenses, future quarterly distributions paid to our unitholders will vary significantly from quarter to quarter and may be zero.

The board of directors of our general partner may modify or revoke our cash distribution policy at any time at its discretion, including in such a manner that would result in an elimination of cash distributions regardless of the amount of available cash we generate. Our partnership agreement does not require us to make any distributions at all.

Our general partner's current policy is to distribute an amount equal to all of the available cash we generate each quarter to unitholders of record on a pro rata basis. However, the board of directors of our general partner may change such policy at any time at its discretion and could elect not to make distributions for one or more quarters regardless of the amount of available cash we generate. Our partnership agreement does not require us to make any distributions at all. Any modification or revocation of our cash distribution policy could substantially reduce or eliminate the amounts of distributions to our unitholders.

Our refining business faces significant risks due to physical damage hazards, environmental liability risk exposure and unplanned or emergency partial or total plant shutdowns resulting in business interruptions. We could incur potentially significant costs to the extent there are unforeseen events which cause property damage and a material decline in production which are not fully insured. The commercial insurance industry engaged in underwriting energy industry risk is specialized and there is finite capacity; therefore, the industry may limit or curtail coverage, may modify the coverage provided or may substantially increase premiums in the future.

If any of our production plants, logistics assets, key pipeline operations serving our plants, or key suppliers sustains a catastrophic loss and operations are shutdown or significantly impaired, it would have a material adverse impact on our operations, financial condition and cash flows. Operations at either or both of the refineries could be curtailed, limited or completely shut down for an extended period of time as the result of one or more unforeseen events and circumstances, which may not be within our control, including:

• | major unplanned maintenance requirements; |

• | catastrophic events caused by mechanical breakdown, electrical injury, pressure vessel rupture, explosion, contamination, fire or natural disasters, including floods, windstorms and other similar events; |

• | labor supply shortages or labor contract disputes that result in a work stoppage or slowdown; |

18

• | cessation or suspension of a plant or specific operations dictated by environmental authorities; and |

• | an event or incident involving a large clean-up, decontamination, or the imposition of laws and ordinances regulating the cost and schedule of demolition or reconstruction, which can cause significant delays in restoring property to its pre-loss condition. |

We have sustained losses over the past ten-year period at our plants, which are illustrative of the types of risks and hazards that exist. These losses or events resulted in costs assumed by us that were not fully insured due to policy retentions or applicable exclusions. These events were as follows:

• | June 2007: Coffeyville refinery; flood |

• | December 2010: Coffeyville refinery; fluid catalytic cracking unit ("FCCU") fire |

• | December 2010: Wynnewood refinery; hydrocracker unit fire |

• | September 2012: Wynnewood refinery; boiler explosion |

• | July/August 2013: Coffeyville refinery; FCCU outage |

• | July 2014: Coffeyville refinery; isomerization unit fire |

Currently, we are insured under CVR Energy's casualty, environmental, property and business interruption insurance policies. The property and business interruption coverage has a combined policy limit of $1.25 billion. The property and business interruption insurance policies contain limits and sub-limits which insure all our assets as well as CVR Partners' assets. There is potential for a common occurrence to impact both the nitrogen fertilizer plant operated by CVR Partners and the Coffeyville refinery in which case the insurance limitations would apply to all damages combined. Under this insurance program, there is a $10.0 million property damage retention for all properties. For business interruption losses, the insurance program has a 45-day waiting period retention for any one occurrence. In addition, the insurance policies contain a schedule of sub-limits which apply to certain specific perils or areas of coverage. Sub-limits which may be of importance depending on the nature and extent of a particular insured occurrence are: flood, earthquake, contingent business interruption insuring key suppliers, pipelines and customers, debris removal, decontamination, demolition and increased cost of construction due to law and ordinance, and others. Such conditions, limits and sub-limits could materially impact insurance recoveries and potentially cause us to assume losses which could impair earnings.