Attached files

| file | filename |

|---|---|

| EX-31 - RULE 13A-14(A) CERTIFICATIONS - CSX CORP | csx12252015exhibit31certif.htm |

| EX-32 - SECTION 1350 CERTIFICATIONS - CSX CORP | csx12252015exhibit32certif.htm |

| EX-21 - SUBSIDIARIES OF THE REGISTRANT - CSX CORP | csx-12252015exhibit21subsi.htm |

| EX-24 - POWERS OF ATTORNEY - CSX CORP | csx-12252015exhibit24power.htm |

| EX-23 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - CSX CORP | csx12252015exhibit23consen.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(X) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 25, 2015

OR

( ) TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission File Number 1-8022 | ||||

CSX CORPORATION | ||||

(Exact name of registrant as specified in its charter) | ||||

Virginia | 62-1051971 | |||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

500 Water Street, 15th Floor, Jacksonville, FL | 32202 | (904) 359-3200 | ||

(Address of principal executive offices) | (Zip Code) | (Telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act: | ||||

Title of each class | Name of exchange on which registered | |||

Common Stock, $1 Par Value | Nasdaq Global Select Market | |||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes (X) No ( )

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ( ) No (X)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes (X) No ( )

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes (X) No ( )

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. (X)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. (as defined in Exchange Act Rule 12b-2).

Large Accelerated Filer (X) Accelerated Filer ( ) Non-accelerated Filer ( ) Smaller reporting company ( )

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2).

Yes ( ) No (X)

On June 26, 2015 (which is the last day of the second quarter and the required date to use), the aggregate market value of the Registrant’s voting stock held by non-affiliates was approximately $33 billion (based on the New York Stock Exchange closing price on such date).

There were 963,150,011 shares of Common Stock outstanding on January 22, 2016 (the latest practicable date that is closest to the filing date).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement (the “Proxy Statement”) to be filed no later than 120 days after the end of the fiscal year with respect to its annual meeting of shareholders scheduled to be held on May 11, 2016.

1

CSX CORPORATION | ||||

FORM 10-K | ||||

TABLE OF CONTENTS | ||||

Item No. | Page | |||

PART I | ||||

1. | ||||

2. | ||||

3. | ||||

4. | ||||

PART II | ||||

5. | ||||

6. | ||||

7. | ||||

· 2015 Highlights | ||||

· Critical Accounting Estimates | ||||

· Forward-Looking Statements | ||||

7A. | ||||

8. | ||||

9. | ||||

9A. | ||||

9B. | ||||

PART III | ||||

10. | Directors, Executive Officers of the Registrant and Corporate Governance | |||

11. | ||||

12. | ||||

13. | ||||

14. | ||||

PART IV | ||||

15. | ||||

2

CSX CORPORATION

PART I

Item 1. Business

CSX Corporation (“CSX”), and together with its subsidiaries (the “Company”), based in Jacksonville, Florida, is one of the nation's leading transportation companies. The Company provides rail-based transportation services including traditional rail service and the transport of intermodal containers and trailers.

The Company’s number of employees was approximately 29,000 as of December 2015, which includes approximately 24,000 union employees. Most of the Company’s employees provide or support transportation services.

CSX Transportation, Inc.

CSX’s principal operating subsidiary, CSX Transportation, Inc. (“CSXT”), provides an important link to the transportation supply chain through its approximately 21,000 route mile rail network, which serves major population centers in 23 states east of the Mississippi River, the District of Columbia and the Canadian provinces of Ontario and Quebec. It has access to over 70 ocean, river and lake port terminals along the Atlantic and Gulf Coasts, the Mississippi River, the Great Lakes and the St. Lawrence Seaway. The Company’s intermodal business links customers to railroads via trucks and terminals. CSXT also serves thousands of production and distribution facilities through track connections to approximately 240 short-line and regional railroads.

Lines of Business

During 2015, the Company services generated $11.8 billion of revenue and served three primary lines of business:

• | The merchandise business shipped nearly 2.9 million carloads and generated 62% of revenue and 42% of volume in 2015. The Company’s merchandise business is comprised of shipments in the following diverse markets: agricultural products, phosphates and fertilizers, food and consumer, chemicals, automotive, metals, forest products, minerals and waste and equipment. |

• | The coal business shipped about 1.1 million carloads and accounted for 19% of revenue and 16% of volume in 2015. The Company transports domestic coal, coke and iron ore to electricity-generating power plants, steel manufacturers and industrial plants as well as export coal to deep-water port facilities. Roughly one-third of export coal and the majority of the domestic coal that the Company transports is used for generating electricity. |

• | The intermodal business accounted for 15% of revenue and 42% of volume in 2015. The intermodal business combines the superior economics of rail transportation with the short-haul flexibility of trucks and offers a cost advantage over long-haul trucking. Through a network of more than 50 terminals, the intermodal business serves all major markets east of the Mississippi River and transports mainly manufactured consumer goods in containers, providing customers with truck-like service for longer shipments. |

Other revenue accounted for 4% of the Company’s total revenue in 2015. This category includes revenue from regional subsidiary railroads, demurrage, revenue for customer volume commitments not met, switching and other incidental charges. Revenue from regional railroads includes shipments by railroads that the Company does not directly operate. Demurrage represents charges assessed when freight cars are held beyond a specified period of time. Switching revenue is primarily generated when CSXT switches cars for a customer or another railroad.

3

CSX CORPORATION

PART I

Other Entities

In addition to CSXT, the Company’s subsidiaries include CSX Intermodal Terminals, Inc. (“CSX Intermodal Terminals”), Total Distribution Services, Inc. (“TDSI”), Transflo Terminal Services, Inc. (“Transflo”), CSX Technology, Inc. (“CSX Technology”) and other subsidiaries. CSX Intermodal Terminals owns and operates a system of intermodal terminals, predominantly in the eastern United States and also performs drayage services (the pickup and delivery of intermodal shipments) for certain customers and trucking dispatch operations. TDSI serves the automotive industry with distribution centers and storage locations. Transflo connects non-rail served customers to the many benefits of rail by transferring products from rail to trucks. The biggest Transflo markets are chemicals and agriculture, which includes shipments of plastics and ethanol. CSX Technology and other subsidiaries provide support services for the Company.

CSX’s other holdings include CSX Real Property, Inc., a subsidiary responsible for the Company’s operating and non-operating real estate sales, leasing, acquisition and management and development activities. These activities are classified in either operating income or other income - net depending upon the nature of the activity. Results of these activities fluctuate with the timing of real estate transactions.

Financial Information

See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for operating revenue, operating income and total assets for each of the last three fiscal years.

Company History

A leader in freight rail transportation for nearly 190 years, the Company’s heritage dates back to the early nineteenth century when The Baltimore and Ohio Railroad Company (“B&O”) – the nation’s first common carrier – was chartered in 1827. Since that time, the Company has built on this foundation to create a railroad that could safely and reliably service the ever-increasing demands of a growing nation.

Since its founding, numerous railroads have combined with the former B&O through merger and consolidation to create what has become CSX. Each of the railroads that combined into the CSX family brought new geographical reach to valuable markets, gateways, cities, ports and transportation corridors.

CSX was incorporated in 1978 under Virginia law. In 1980, the Company completed the merger of the Chessie System and Seaboard Coast Line Industries into CSX. The merger allowed the Company to connect northern population centers and Appalachian coal fields to growing southeastern markets. Later, the Company’s acquisition of key portions of Conrail, Inc. ("Conrail") allowed CSXT to link the northeast, including New England and the New York metropolitan area, with Chicago and midwestern markets as well as the growing areas in the Southeast already served by CSXT. This current rail network allows the Company to directly serve every major market in the eastern United States with safe, dependable, environmentally responsible and fuel efficient freight transportation and intermodal service.

Competition

The business environment in which the Company operates is highly competitive. Shippers typically select transportation providers that offer the most compelling combination of service and price. Service requirements, both in terms of transit time and reliability, vary by shipper and commodity. As a result, the Company’s primary competition varies by commodity, geographic location and mode of available transportation and includes other railroads, motor carriers that operate similar routes across its service area and, to a less significant extent, barges, ships and pipelines.

CSXT’s primary rail competitor is Norfolk Southern Railway, which operates throughout much of the Company’s territory. Other railroads also operate in parts of the Company’s territory. Depending on the specific market, competing railroads and deregulated motor carriers may exert pressure on price and service levels. For further discussion on the risk of competition to the Company, see Item 1A. Risk Factors.

4

CSX CORPORATION

PART I

Regulatory Environment

The Company's operations are subject to various federal, state, provincial (Canada) and local laws and regulations generally applicable to businesses operating in the United States and Canada. In the U.S., the railroad operations conducted by the Company's subsidiaries, including CSXT, are subject to the regulatory jurisdiction of the Surface Transportation Board (“STB”), the Federal Railroad Administration (“FRA”), and its sister agency within the U.S. Department of Transportation, the Pipeline and Hazardous Materials Safety Administration (“PHMSA”). Together, FRA and PHMSA have broad jurisdiction over railroad operating standards and practices, including track, freight cars, locomotives and hazardous materials requirements. In addition, the U.S. Environmental Protection Agency (“EPA”) has regulatory authority with respect to matters that impact the Company's properties and operations. The EPA is considering regulatory action directed towards the railroad industry governing the disposal of creosote cross-ties and seeking to increase air emission regulations that may impact our operations or increase costs. Similarly, the Transportation Security Administration (“TSA”), a component of the Department of Homeland Security, has broad authority over railroad operating practices that may have homeland security implications. In Canada, the railroad operations conducted by the Company’s subsidiaries, including CSXT, are subject to the regulatory jurisdiction of the Canadian Transportation Agency.

Although the Staggers Act of 1980 significantly deregulated the U.S. rail industry, the STB has broad jurisdiction over rail carriers. The STB regulates routes, fuel surcharges, conditions of service, rates for non-exempt traffic, acquisitions of control over rail common carriers and the transfer, extension or abandonment of rail lines, among other railroad activities.

Positive Train Control

In 2008, Congress enacted the Rail Safety Improvement Act (the “RSIA”). The legislation included a mandate that all Class I freight railroads implement an interoperable positive train control system (“PTC”) by December 31, 2015. Implementation of a PTC system is designed to prevent train-to-train collisions, over-speed derailments, incursions into established work-zone limits, and train diversions onto another set of tracks. On October 29, 2015, the President of the United States signed the Positive Train Control Enforcement and Implementation Act of 2015 into law extending the deadline. This Act requires the installation of all PTC hardware be completed by December 31, 2018, and, assuming certain conditions are met, requires that the PTC system be fully operational by December 31, 2020.

PTC must be installed on all main lines with passenger and commuter operations as well as most of those over which toxic-by-inhalation hazardous materials are transported. The Company expects to incur significant capital costs in connection with the implementation of PTC as well as related ongoing operating expenses. CSX currently estimates that the total multi-year cost of PTC implementation will be approximately $2.2 billion for the Company. Total PTC investment through 2015 was $1.5 billion.

STB Proceedings

In 2012, the STB announced it would accept comments on a proposal by the National Industrial Transportation League that would require Class I railroads to provide a form of "competitive access" to customers served solely by one railroad. Under this proposal, CSX would be required to allow a competing railroad to access certain customers that are currently solely served by CSX's network. In early 2013, shippers, railroads and other parties submitted comments on the proposal, and the STB held a hearing in March 2014 to receive further input from participating parties. Since the hearing, the STB has taken no further action in the proceeding.

In April 2014, the STB announced it would receive comments to explore its methodology for determining railroad revenue adequacy. The revenue adequacy standard represents the level of profitability for a healthy carrier. Shippers, railroads and other parties filed comments in late 2014. More recently, the STB held a hearing in July 2015 to receive further input from participating parties. Since the hearing, the STB has taken no further action in the proceeding.

5

CSX CORPORATION

PART I

New rules regarding competitive access or revenue adequacy could have a material adverse effect on the Company's financial condition, results of operations and liquidity as well as its ability to invest in enhancing and maintaining vital infrastructure. For further discussion on regulatory risks to the Company, see Item 1A. Risk Factors.

Other Information

CSX makes available on its website www.csx.com, free of charge, its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such reports are filed with or furnished to the Securities and Exchange Commission (“SEC”). The information on the CSX website is not part of this annual report on Form 10-K. Additionally, the Company has posted its code of ethics on its website, which is also available to any shareholder who requests it. This Form 10-K and other SEC filings made by CSX are also accessible through the SEC’s website at www.sec.gov.

CSX has included the certifications of its Chief Executive Officer (“CEO”) and the Chief Financial Officer (“CFO”) required by Section 302 of the Sarbanes-Oxley Act of 2002 (“the Act”) as Exhibit 31, as well as Section 906 of the Act as Exhibit 32 to this Form 10-K report.

The information set forth in Item 6. Selected Financial Data is incorporated herein by reference. For additional information concerning business conducted by the Company during 2015, see Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Item 1A. Risk Factors

The risks set forth in the following risk factors could have a materially adverse effect on the Company's financial condition, results of operations or liquidity, and could cause those results to differ materially from those expressed or implied in the Company's forward-looking statements. Additional risks and uncertainties not currently known to the Company or that the Company currently does not deem to be material also may materially impact the Company's financial condition, results of operations or liquidity.

New legislation or regulatory changes could impact the Company's earnings or restrict its ability to independently negotiate prices.

Legislation passed by Congress or new regulations issued by federal agencies can significantly affect the revenues, costs and profitability of the Company's business. For instance, several of the proposals under consideration by the STB could have a significant negative impact on the Company's ability to negotiate prices for the value of rail services provided and meet service standards, which could force a reduction in capital spending. In addition, statutes imposing price constraints or affecting rail-to-rail competition could adversely affect the Company's profitability.

Government regulation and compliance risks may adversely affect the Company's operations and financial results.

The Company is subject to the jurisdiction of various regulatory agencies, including the STB, FRA, PHMSA, TSA, EPA and other state, provincial and federal regulatory agencies for a variety of economic, health, safety, labor, environmental, tax, legal and other matters. New or modified rules or regulations by these agencies could increase the Company's operating costs or reduce operating efficiencies and impact service performance. For example, the RSIA mandates that the installation of PTC hardware be completed by December 31, 2018 and, assuming certain conditions are met, requires that the PTC system be fully operational by December 31, 2020 on main lines that carry certain hazardous materials and on lines that have commuter or passenger operations. Noncompliance with these and other applicable laws or regulations could erode public confidence in the Company and can subject the Company to fines, penalties and other legal or regulatory sanctions.

6

CSX CORPORATION

PART I

Climate change and other emissions-related legislation and regulation could adversely affect the Company's operations and financial results.

Climate change and other emissions-related legislation and regulation have been proposed and, in some cases adopted, on the federal, state, provincial and local levels. These final and proposed laws and regulations take the form of restrictions, caps, taxes or other controls on emissions. In particular, the EPA has issued various regulations and is expected to issue additional regulations targeting emissions, including rules and standards governing emissions from certain stationary sources and from vehicles.

Any of these pending or proposed laws or regulations could adversely affect the Company's operations and financial results by, among other things: (i) reducing coal-fired electricity generation due to mandated emission standards; (ii) reducing the consumption of coal as a viable energy resource in the United States and Canada; (iii) increasing the Company's fuel, capital and other operating costs and negatively affecting operating and fuel efficiencies; and (iv) making it difficult for the Company's customers in the U.S. and Canada to produce products in a cost competitive manner. Any of these factors could reduce the amount of shipments the Company handles and have a material adverse effect on the Company's financial condition, results of operations or liquidity.

Capacity constraints could have a negative impact on service and operating efficiency.

CSXT may experience rail network difficulties related to: (i) increased volume; (ii) locomotive or crew shortages; (iii) extreme weather conditions; (iv) increased passenger activities, including high-speed rail; or (v) regulatory changes impacting where and how fast CSXT can transport freight or maintain routes, which could have a negative effect on CSXT's operational fluidity, leading to deterioration of service, asset utilization and overall efficiency.

Global economic conditions could negatively affect demand for commodities and other freight.

A decline or disruption in general domestic and global economic conditions that affects demand for the commodities and products the Company transports, including import and export volume, could reduce revenues or have other adverse effects on the Company's cost structure and profitability. For example, if the rate of economic growth in Asia slows or if European economies contract, U.S. export coal volume could be adversely impacted resulting in lower revenue for CSX. If the Company experiences significant declines in demand for its transportation services with respect to one or more commodities and products, the Company may experience reduced revenue and increased operating costs associated with the storage of locomotives, railcars and other equipment, workforce adjustments, and other related activities, which could have a material adverse effect on the Company's financial condition, results of operations and liquidity.

Changing dynamics in the U.S. and global energy markets could negatively impact profitability.

Over the past few years, production of natural gas in the U.S. has also increased dramatically, which has resulted in lower natural gas prices. As a result of sustained low natural gas prices, many coal-fired power plants have been displaced by natural gas-fired power generation facilities. If natural gas prices were to remain low, additional coal-fired plants could be displaced, which would likely further reduce the Company's domestic coal volumes and revenues.

Additionally, depressed crude oil prices due to increased supply or lower demand could result in a decrease in domestic crude oil production, which could have an adverse effect on crude oil volumes for CSX. In addition, new regulations related to the shipment of crude oil by rail, including proposed rail car safety standards, could increase costs for CSX, negatively impact network fluidity or have an adverse impact on customers.

7

CSX CORPORATION

PART I

CSXT, as a common carrier by rail, is required by law to transport hazardous materials, which could expose the Company to significant costs and claims.

A train accident involving the transport of hazardous materials could result in significant claims arising from personal injury, property or natural resource damage, environmental penalties and remediation obligations. Such claims, if insured, could exceed existing insurance coverage or insurance may not continue to be available at commercially reasonable rates. Under federal regulations, CSXT is required to transport hazardous materials under the legal duty referred to as the common carrier mandate.

CSXT is also required to comply with regulations regarding the handling of hazardous materials. In November 2008, the TSA issued final rules placing significant new security and safety requirements on passenger and freight railroad carriers, rail transit systems and facilities that ship hazardous materials by rail. Noncompliance with these rules can subject the Company to significant penalties and could be a factor in litigation arising out of a train accident. Finally, legislation preventing the transport of hazardous materials through certain cities could result in network congestion and increase the length of haul for hazardous substances, which could increase operating costs, reduce operating efficiency or increase the risk of an accident involving the transport of hazardous materials.

The Company is subject to environmental laws and regulations that may result in significant costs.

The Company is subject to wide-ranging federal, state, provincial and local environmental laws and regulations concerning, among other things, emissions into the air, ground and water; the handling, storage, use, generation, transportation and disposal of waste and other materials; the clean-up of hazardous material and petroleum releases and the health and safety of our employees. If the Company violates or fails to comply with these laws and regulations, CSX could be fined or otherwise sanctioned by regulators. The Company can also be held liable for consequences arising out of human exposure to any hazardous substances for which CSX is responsible. In certain circumstances, environmental liability can extend to formerly owned or operated properties, leased properties, adjacent properties and properties owned by third parties or Company predecessors, as well as to properties currently owned, leased or used by the Company.

The Company has been, and may in the future be, subject to allegations or findings to the effect that it has violated, or is strictly liable under, environmental laws or regulations, and such violations can result in the Company's incurring fines, penalties or costs relating to the clean-up of environmental contamination. Although the Company believes it has appropriately recorded current and long-term liabilities for known and reasonably estimable future environmental costs, it could incur significant costs that exceed reserves or require unanticipated cash expenditures as a result of any of the foregoing. The Company also may be required to incur significant expenses to investigate and remediate known, unknown or future environmental contamination.

The Company relies on the security, stability and availability of its technology systems to operate its business.

The Company relies on information technology in all aspects of its business. The performance and reliability of the Company's technology systems are critical to its ability to operate and compete safely and effectively. A cybersecurity attack, which is a deliberate theft of data or impairment of information technology systems, or other significant disruption or failure, could result in a service interruption, train accident, misappropriation of confidential information, process failure, security breach or other operational difficulties. Such an event could result in increased capital, insurance or operating costs, including increased security costs to protect the Company's infrastructure. A disruption or compromise of the Company's information technology systems, even for short periods of time, could have a material adverse effect on the Company.

8

CSX CORPORATION

PART I

Disruption of the supply chain could negatively affect operating efficiency and increase costs.

The capital intensive nature and sophistication of core rail equipment (including rolling stock equipment, locomotives, rail, and ties) limits the number of railroad equipment suppliers. If any of the current manufacturers stops production or experiences a supply shortage, CSXT could experience a significant cost increase or material shortage. In addition, a few critical railroad suppliers are foreign and, as such, adverse developments in international relations, new trade regulations, disruptions in international shipping or increases in global demand could make procurement of these supplies more difficult or increase CSXT's operating costs. Additionally, if a fuel supply shortage were to arise, whether due to production restrictions, lower refinery outputs, a disruption of oil imports, adverse political developments or otherwise, the Company would be negatively impacted.

Failure to complete negotiations on collective bargaining agreements could result in strikes and/or work stoppages.

Most of CSX's employees are represented by labor unions and are covered by collective bargaining agreements. Most of these agreements are bargained for nationally by the National Carriers Conference Committee and negotiated over the course of several years and previously have not resulted in any extended work stoppages. Under the Railway Labor Act's procedures (which include mediation, cooling-off periods and the possibility of an intervention of the U.S. President), during negotiations neither party may take action until the procedures are exhausted. If, however, CSX is unable to negotiate acceptable agreements, or if terms of existing agreements are disputed, the employees covered by the Railway Labor Act could strike, which could result in loss of business and increased operating costs as a result of higher wages or benefits paid to union members.

The Company faces competition from other transportation providers.

The Company experiences competition in pricing, service, reliability and other factors from various transportation providers including railroads and motor carriers that operate similar routes across its service area and, to a less significant extent, barges, ships and pipelines. Other transportation providers generally use public rights-of-way that are built and maintained by governmental entities, while CSXT and other railroads must build and maintain rail networks largely using internal resources. Any future improvements or expenditures materially increasing the quality or reducing the cost of alternative modes of transportation, or legislation providing for less stringent size or weight restrictions on trucks, could negatively impact the Company's competitive position. Additionally, any future consolidation in the rail industry could materially affect the regulatory and competitive environment in which the Company operates.

Future acts of terrorism, war or regulatory changes to combat the risk of terrorism may cause significant disruptions in the Company's operations.

Terrorist attacks, along with any government response to those attacks, may adversely affect the Company's financial condition, results of operations or liquidity. CSXT's rail lines, other key infrastructure and information technology systems may be direct targets or indirect casualties of acts of terror or war. This risk could cause significant business interruption and result in increased costs and liabilities and decreased revenues. In addition, premiums charged for some or all of the insurance coverage currently maintained by the Company could increase dramatically, or the coverage may no longer be available.

Furthermore, in response to the heightened risk of terrorism, federal, state and local governmental bodies are proposing and, in some cases, have adopted legislation and regulations relating to security issues that impact the transportation industry. For example, the Department of Homeland Security adopted regulations that require freight railroads to implement additional security protocols when transporting hazardous materials. Complying with these or future regulations could continue to increase the Company's operating costs and reduce operating efficiencies.

9

CSX CORPORATION

PART I

Severe weather or other natural occurrences could result in significant business interruptions and expenditures in excess of available insurance coverage.

The Company's operations may be affected by external factors such as severe weather and other natural occurrences, including floods, fires, hurricanes and earthquakes. As a result, the Company's rail network may be damaged, its workforce may be unavailable, fuel costs may rise and significant business interruptions could occur. In addition, the performance of locomotives and railcars could be adversely affected by extreme weather conditions. Insurance maintained by the Company to protect against loss of business and other related consequences resulting from these natural occurrences is subject to coverage limitations, depending on the nature of the risk insured. This insurance may not be sufficient to cover all of the Company's damages or damages to others, and this insurance may not continue to be available at commercially reasonable rates. Even with insurance, if any natural occurrence leads to a catastrophic interruption of service, the Company may not be able to restore service without a significant interruption in operations.

The Company may be subject to various claims and lawsuits that could result in significant expenditures.

As part of its railroad and other operations, the Company is subject to various claims and lawsuits related to disputes over commercial practices, labor and unemployment matters, occupational and personal injury claims, property damage, environmental and other matters. The Company may experience material judgments or incur significant costs to defend existing and future lawsuits. Although the Company establishes reserves and maintains insurance to cover these types of claims, final amounts determined to be due on any outstanding matters may differ materially from the recorded reserves and exceed the Company's insurance coverage. Additionally, the Company is subject to adverse developments not currently reflected in the Company's reserve estimates.

The unavailability of critical resources could adversely affect the Company’s operational efficiency and ability to meet demand.

Marketplace conditions for resources like locomotives as well as the availability of qualified personnel, particularly engineers and trainmen, could each have a negative impact on the Company’s ability to meet demand for rail service. Although the Company believes that it has adequate personnel for the current business environment, unpredictable increases in demand for rail services or extreme weather conditions may exacerbate such risks, which could have a negative impact on the Company’s operational efficiency and otherwise have a material adverse effect on the Company’s financial condition, results of operations, or liquidity in a particular period.

Weaknesses in the capital and credit markets could negatively impact the Company’s access to capital.

Due to the significant capital expenditures required to operate and maintain a safe and efficient railroad, the Company regularly relies on capital markets for the issuance of long-term debt instruments as well as on bank financing from time to time. Instability or disruptions of the capital markets, including credit markets, or the deterioration of the Company’s financial condition due to internal or external factors, could restrict or prohibit access and could increase the cost of financing sources. A significant deterioration of the Company’s financial condition could also reduce credit ratings and could limit or affect its access to external sources of capital and increase the costs of short and long-term debt financing.

Item 1B. Unresolved Staff Comments

None

10

CSX CORPORATION

PART I

Item 2. Properties

The Company’s properties primarily consist of track and its related infrastructure, locomotives and freight cars and equipment. These categories and the geography of the network are described below.

Track and Infrastructure

Serving 23 states, the District of Columbia, and the Canadian provinces of Ontario and Quebec, the CSXT rail network serves, among other markets, New York, Philadelphia and Boston in the Northeast and Mid-Atlantic, the southeast markets of Atlanta, Miami and New Orleans, and the midwestern cities of St. Louis, Memphis and Chicago.

CSXT’s track structure includes main thoroughfares, connecting terminals and yards (known as mainline track), track within terminals and switching yards, track adjacent to the mainlines used for passing trains, track connecting the mainline track to customer locations and track that diverts trains from one track to another known as turnouts. Total track miles are greater than CSXT’s approximately 21,000 route miles, which reflect the size of CSXT’s network that connects markets, customers and western railroads. At December 2015, the breakdown of track miles was as follows:

Track | ||

Miles | ||

Mainline track | 26,565 | |

Terminals and switching yards | 9,390 | |

Passing sidings and turnouts | 936 | |

Total | 36,891 | |

In addition to its physical track structure, CSXT operates numerous yards and terminals. These serve as hubs between CSXT and its local customers and as sorting facilities where railcars often are received, re-sorted and placed onto new outbound trains. The Company’s ten largest yards and terminals based on annual volume (number of railcars or intermodal containers processed) are listed in the table below.

Yards and Terminals | Annual Volume (number of units processed) | |

Chicago, IL | 1,072,809 | |

Waycross, GA | 672,801 | |

Selkirk, NY | 544,452 | |

Indianapolis, IN | 527,170 | |

Willard, OH | 517,891 | |

Nashville, TN | 497,371 | |

Cincinnati, OH | 485,105 | |

Hamlet, NC | 461,780 | |

Louisville, KY | 396,681 | |

Toledo, OH | 372,666 | |

11

CSX CORPORATION

PART I

Network Geography

CSXT’s operations are primarily focused on four major transportation networks and corridors which are defined geographically and by commodity flows below.

Interstate 90 (I-90) Corridor – This CSXT corridor links Chicago and the Midwest to metropolitan areas in New York and New England. This route, also known as the “waterlevel route,” has minimal hills and grades and nearly all of it has two main tracks (referred to as double track). These superior engineering attributes permit the corridor to support consistent, high-speed intermodal, automotive and merchandise service. This corridor is a primary route for import traffic coming from the far east through western ports moving eastward across the country, through Chicago and into the population centers in the Northeast. The I-90 Corridor is also a critical link between ports in New York, New Jersey, and Pennsylvania and consumption markets in the Midwest. This route carries consumer goods from all three of the Company’s major markets – merchandise, coal and intermodal.

Interstate 95 (I-95) Corridor – The CSXT I-95 Corridor connects Charleston, Jacksonville, Miami and many other cities throughout the Southeast with the heavily populated mid-Atlantic and northeastern cities of Baltimore, Philadelphia and New York. CSXT primarily transports food and consumer products, as well as metals and chemicals along this line. It is the only rail corridor along the eastern seaboard south of the District of Columbia, and provides access to major eastern ports.

Southeastern Corridor – This critical part of the network runs between CSXT’s western gateways of Chicago, St. Louis and Memphis through the cities of Nashville, Birmingham, and Atlanta and markets in the Southeast. The Southeastern Corridor is the premier rail route connecting these key cities, gateways, and markets and positions CSXT to efficiently handle projected traffic volumes of intermodal, automotive and general merchandise traffic. The corridor also provides direct rail service between the coal reserves of the southern Illinois basin and the demand for coal in the Southeast.

Coal Network – The CSXT coal network connects the coal mining operations in the Appalachian mountain region and Illinois basin with industrial areas in the Southeast, Northeast and Mid-Atlantic, as well as many river, lake, and deep water port facilities. CSXT’s coal network is well positioned to supply utility markets in both the Northeast and Southeast and to transport coal shipments for export outside of the U.S. Roughly one-third of the tons of export coal and the majority of the domestic coal that the Company transports is used for generating electricity.

See the following page for a map of the CSX Rail Network.

12

CSX CORPORATION

PART I

CSX Rail Network

13

CSX CORPORATION

PART I

Locomotives

CSXT owns and long-term leases nearly 4,500 locomotives, almost all of which are owned by CSXT. From time to time, the Company also short-term leases locomotives based on business needs. Freight locomotives are the power source used primarily to pull trains. Switching locomotives are used in yards to sort railcars so that the right railcar is attached to the right train in order to deliver it to its final destination. Auxiliary units are typically used to provide extra traction for heavy trains in hilly terrain. At December 2015, CSXT’s fleet of owned and long-term leased locomotives consisted of the following types of locomotives:

Locomotives | % | Average Age (years) | ||||||

Freight | 3,932 | 88 | % | 20 | ||||

Switching | 322 | 7 | % | 35 | ||||

Auxiliary Units | 209 | 5 | % | 23 | ||||

Total | 4,463 | 100 | % | 20 | ||||

Equipment

In 2015, the average daily fleet of cars on line consisted of approximately 206,000 cars. At any time, over half of the railcars on the CSXT system are not owned or leased by the Company. Examples of these non-CSXT railcars are as follows: railcars owned by other railroads (which are utilized by CSXT), shipper-furnished or private cars (which are generally used only in that shipper’s service) and multi-level railcars used to transport automobiles (which are shared among railroads).

The Company’s revenue generating equipment (either owned or long-term leased) consists of freight cars and containers as described below.

Gondolas – Support CSXT’s metals markets and provide transport for woodchips and other bulk commodities. Some gondolas are equipped with special hoods for protecting products like coil and sheet steel.

Open-top hoppers – Transport heavy dry bulk commodities such as coal, coke, stone, sand, ores and gravel that are resistant to weather conditions.

Box cars – Include a variety of tonnages, sizes, door configurations and heights to accommodate a wide range of finished products, including paper, auto parts, appliances and building materials. Insulated box cars deliver food products, canned goods, beer and wine.

Covered hoppers – Have a permanent roof and are segregated based upon commodity density. Lighter bulk commodities such as grain, fertilizer, flour, salt, sugar, clay and lime are shipped in large cars called jumbo covered hoppers. Heavier commodities like cement, ground limestone and sand are shipped in small cube covered hoppers.

Multi-level flat cars – Transport finished automobiles and are differentiated by the number of levels: bi-levels for large vehicles such as pickup trucks and SUVs and tri-levels for sedans and smaller automobiles.

Flat cars – Used for shipping intermodal containers and trailers or bulk and finished goods, such as lumber, pipe, plywood, drywall and pulpwood.

Containers – Weather-proof boxes used for bulk shipment of freight.

Other cars on the network consist primarily of refrigerated boxcars for transporting perishable items.

14

CSX CORPORATION

PART I

At December 2015, the Company’s owned and long-term leased equipment consisted of the following:

Equipment | Number of Units | % | |||

Gondolas | 24,844 | 37 | % | ||

Open-top hoppers | 11,161 | 17 | % | ||

Multi-level flat cars | 11,634 | 18 | % | ||

Covered hoppers | 10,308 | 16 | % | ||

Box cars | 7,386 | 11 | % | ||

Flat cars | 674 | 1 | % | ||

Other cars | 379 | — | % | ||

Subtotal freight cars | 66,386 | 100 | % | ||

Containers | 18,231 | ||||

Total equipment | 84,617 | ||||

Item 3. Legal Proceedings

For further details, please refer to Note 7. Commitments and Contingencies of this annual report on Form 10-K.

Item 4. Mine Safety Disclosure

Not Applicable

Executive Officers of the Registrant

Executive officers of the Company are elected by the CSX Board of Directors and generally hold office until the next annual election of officers. There are no family relationships or any arrangement or understanding between any officer and any other person pursuant to which such officer was elected. As of the date of this filing, the executive officers’ names, ages and business experience are:

Name and Age | Business Experience During Past Five Years |

Michael J. Ward, 65 Chairman and Chief Executive Officer | A 38-year veteran of the Company, Ward has served as Chairman and Chief Executive Officer of CSX since January 2003. Ward’s distinguished railroad career has included key executive positions in nearly all aspects of the Company’s business, including sales and marketing, operations and finance. |

Clarence W. Gooden, 64 President | Clarence Gooden was appointed President of CSX in September 2015 with responsibility for operations and sales and marketing. In this role, he is responsible for safe and reliable operations as well as a highly diversified market portfolio serving all facets of the North American economy. As an employee of the Company for 45 years, Gooden previously served as Executive Vice President and Chief Commercial Officer since 2004 where he was responsible for generating customer revenue, forecasting business trends and developing CSX's model for future revenue growth. Gooden has also held key executive positions in both operations and sales and marketing. |

15

CSX CORPORATION

PART I

Name and Age | Business Experience During Past Five Years |

Frank A. Lonegro, 47 Executive Vice President and Chief Financial Officer | Lonegro has served as Executive Vice President and Chief Financial Officer of CSX since September 2015. In this capacity, he directs all financial and strategic planning activities, including accounting, financial planning, tax, treasury and investor relations, and is also responsible for the management and oversight of the Company's technology assets and activities. During his 15-year tenure with the Company, Lonegro also served as Vice President Internal Audit, President of CSX Technology, Vice President-Mechanical and Vice President-Service Design. Additionally, he led development and implementation of Positive Train Control, an advanced train control system, to further enhance the Company’s safety performance. |

Cindy M. Sanborn, 51 Executive Vice President and Chief Operating Officer | Sanborn has served as Executive Vice President and Chief Operating Officer of CSXT since September 2015. In this capacity, she is responsible for all aspects of safe, reliable and cost-effective service delivery. She directs daily train operations, maintains the Company's locomotive and rail car fleet as well as maintains and upgrades the Company’s more than 21,000-route-mile network in the eastern United States and two Canadian provinces. Since joining the Company in 1987, she also served as Executive Vice President - Operations, Vice President and Chief Transportation Officer, Vice President of Operations for the Northern Region and various other key roles in network operations, locomotive management and division operations. |

Fredrik J. Eliasson, 45 Executive Vice President and Chief Sales and Marketing Officer | Eliasson has served as Executive Vice President and Chief Sales and Marketing Officer of CSX since September 2015. In this capacity, he directs all customer-facing aspects of the Company’s business, including market growth, forecasting business trends and development of strategic plans for revenue growth. During his 20-year tenure with the Company, he also served as Executive Vice President and Chief Financial Officer. Prior to becoming CFO, he led development of two of the Company’s major markets as Vice President of Chemicals and Fertilizer and Vice President of Emerging Markets. He also supported Sales and Marketing in a previous position as Vice President of Commercial Finance. |

Ellen M. Fitzsimmons, 55 Executive Vice President of Law and Public Affairs, General Counsel and Corporate Secretary | Fitzsimmons has been the Executive Vice President of Law and Public Affairs, General Counsel, and Corporate Secretary of CSX since December 2003. She serves as the Company’s Chief Legal Officer and oversees all government relations and public affairs activities as well as internal audit and other risk management functions. During her 24-year tenure with the Company, her broad responsibilities have included key roles in major risk and corporate governance-related areas. |

Lisa A. Mancini, 56 Senior Vice President and Chief Administrative Officer | Mancini has been Senior Vice President and Chief Administrative Officer of CSX since January 2009. She is responsible for employee compensation and benefits, labor relations, employee staffing and development activities, purchasing, real estate, and facilities management. She previously served as Vice President - Strategic Infrastructure Initiatives from 2007 to 2009 and, prior to that, Vice President - Labor Relations. Prior to joining CSX in 2003, Mancini served as Chief Operating Officer of the San Francisco Municipal Railway. |

Carolyn T. Sizemore, 53 Vice President and Controller | Sizemore has served as Vice President and Controller of CSX since April 2002. She is responsible for financial and regulatory reporting, freight billing and collections, payroll, accounts payable and various other accounting processes. Sizemore’s responsibilities during her 26-year tenure with the Company have included roles in finance and audit-related areas including a variety of positions in accounting, finance strategies, budgets and performance analysis. |

16

CSX CORPORATION

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

CSX’s common stock is listed on the Nasdaq Global Select Market, which is its principal trading market, and is traded over-the-counter and on exchanges nationwide. The official trading symbol is “CSX.”

Description of Common and Preferred Stock

A total of 1.8 billion shares of common stock are authorized, of which 965,513,559 shares were outstanding as of December 2015. Each share is entitled to one vote in all matters requiring a vote of shareholders. There are no pre-emptive rights, which are privileges extended to select shareholders that would allow them to purchase additional shares before other members of the general public in the event of an offering. At January 22, 2016, the latest practicable date that is closest to the filing date, there were 30,242 common stock shareholders of record. The weighted average of common shares outstanding, which was used in the calculation of diluted earnings per share, was 984 million as of December 25, 2015. (See Note 2, Earnings Per Share.) A total of 25 million shares of preferred stock is authorized, none of which is currently outstanding.

The following table sets forth, for the quarters indicated, the dividends declared and the high and low share prices of CSX common stock.

Quarter | |||||||||||||||||||

1st | 2nd | 3rd | 4th | Year | |||||||||||||||

2015 | |||||||||||||||||||

Dividends | $ | 0.16 | $ | 0.18 | $ | 0.18 | $ | 0.18 | $ | 0.70 | |||||||||

Common Stock Price | |||||||||||||||||||

High | $ | 36.96 | $ | 37.67 | $ | 33.63 | $ | 30.53 | $ | 37.67 | |||||||||

Low | $ | 32.71 | $ | 31.87 | $ | 24.47 | $ | 24.58 | $ | 24.47 | |||||||||

2014 | |||||||||||||||||||

Dividends | $ | 0.15 | $ | 0.16 | $ | 0.16 | $ | 0.16 | $ | 0.63 | |||||||||

Common Stock Price | |||||||||||||||||||

High | $ | 29.45 | $ | 31.09 | $ | 32.66 | $ | 37.99 | $ | 37.99 | |||||||||

Low | $ | 25.84 | $ | 27.14 | $ | 29.07 | $ | 29.75 | $ | 25.84 | |||||||||

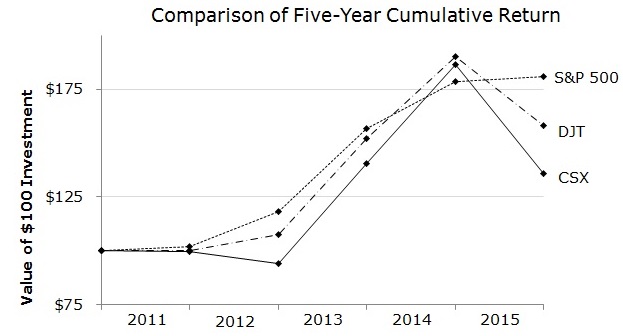

Stock Performance Graph

The cumulative shareholder returns, assuming reinvestment of dividends, on $100 invested at December 31, 2010 are illustrated on the graph below. The Company references the Standard & Poor 500 Stock Index (“S&P 500”), which is a registered trademark of the McGraw-Hill Companies, Inc., and the Dow Jones U.S. Transportation Average Index, which provide comparisons to a broad-based market index and other companies in the transportation industry.

17

CSX CORPORATION

PART II

CSX Purchases of Equity Securities

CSX is required to disclose any purchases of its own common stock for the most recent quarter. CSX purchases its own shares for two primary reasons: (1) to further its goals under its share repurchase program and (2) to fund the Company’s contribution required to be paid in CSX common stock under a 401(k) plan that covers certain union employees.

In April 2015, the Company announced a new $2 billion share repurchase program, which is expected to be completed by April 2017. Management's assessment of market conditions and other factors guide the timing and volume of repurchases. Future share repurchases are expected to be funded by cash on hand, cash generated from operations and debt issuances. During 2015, 2014, and 2013, CSX repurchased $804 million, or 26 million shares, $517 million, or 17 million shares, and $353 million, or 14 million shares, respectively, of common stock. In accordance with the Equity Topic in the Accounting Standards Codification ("ASC"), the excess of repurchase price over par value is recorded in retained earnings. Generally, retained earnings is only impacted by net earnings and dividends.

Share repurchase activity of $258 million for the fourth quarter 2015 was as follows:

CSX Purchases of Equity Securities for the Quarter | |||||||||||

Fourth Quarter (a) | Total Number of Shares Purchased (b) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs(b) | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs | |||||||

Beginning Balance | $ | 1,584,194,942 | |||||||||

October | 3,062,615 | $ | 27.38 | 3,037,000 | 1,501,038,454 | ||||||

November | 3,029,875 | 27.45 | 3,029,800 | 1,417,877,753 | |||||||

December | 3,401,200 | 26.89 | 3,401,200 | 1,326,402,817 | |||||||

Ending Balance | 9,493,690 | $ | 27.23 | 9,468,000 | $ | 1,326,402,817 | |||||

(a) Fourth quarter 2015 consisted of the following fiscal periods: October (September 26, 2015 - October 23, 2013), November (October 24, 2015 - November 20, 2015), and December (November 21, 2015 - December 25, 2015).

(b) The difference of 25,690 shares between the "Total Number of Shares Repurchase" and the "Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs" for the quarter represents shares purchased to fund the Company's contribution to a 401(k) plan that covers certain union employees.

18

CSX CORPORATION

PART II

Item 6. Selected Financial Data

Selected financial data related to the Company’s financial results for the last five fiscal years are listed below.

Fiscal Years | ||||||||||||||||||||

(Dollars and Shares in Millions, Except Per Share Amounts) | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||

Financial Performance | ||||||||||||||||||||

Revenue | $ | 11,811 | $ | 12,669 | $ | 12,026 | $ | 11,763 | $ | 11,795 | ||||||||||

Expense | 8,227 | 9,056 | 8,553 | 8,299 | 8,325 | |||||||||||||||

Operating Income | $ | 3,584 | $ | 3,613 | $ | 3,473 | $ | 3,464 | $ | 3,470 | ||||||||||

Net Earnings from Continuing Operations | 1,968 | 1,927 | 1,864 | 1,863 | 1,854 | |||||||||||||||

Operating Ratio | 69.7 | % | 71.5 | % | 71.1 | % | 70.6 | % | 70.6 | % | ||||||||||

Net Earnings Per Share: | ||||||||||||||||||||

From Continuing Operations, Basic | $ | 2.00 | $ | 1.93 | $ | 1.83 | $ | 1.80 | $ | 1.71 | ||||||||||

From Continuing Operations, Assuming Dilution | 2.00 | 1.92 | 1.83 | 1.79 | 1.70 | |||||||||||||||

Average Common Shares Outstanding | ||||||||||||||||||||

Basic | 983 | 1,001 | 1,019 | 1,038 | 1,083 | |||||||||||||||

Assuming Dilution | 984 | 1,002 | 1,019 | 1,040 | 1,089 | |||||||||||||||

Financial Position | ||||||||||||||||||||

Cash, Cash Equivalents and Short-term Investments | $ | 1,438 | $ | 961 | $ | 1,079 | $ | 1,371 | $ | 1,306 | ||||||||||

Total Assets | 35,039 | 33,053 | 31,782 | 30,723 | 29,491 | |||||||||||||||

Long-term Debt | 10,683 | 9,514 | 9,022 | 9,052 | 8,734 | |||||||||||||||

Shareholders' Equity | 11,668 | 11,176 | 10,504 | 9,136 | 8,598 | |||||||||||||||

Dividend Per Share | $ | 0.70 | $ | 0.63 | $ | 0.59 | $ | 0.54 | $ | 0.45 | ||||||||||

Additional Data | ||||||||||||||||||||

Capital Expenditures (a) | $ | 2,562 | $ | 2,449 | $ | 2,313 | $ | 2,341 | $ | 2,297 | ||||||||||

Employees -- Annual Averages (estimated) | 31,285 | 31,511 | 31,254 | 32,120 | 31,344 | |||||||||||||||

Employees -- Year-end Count (estimated) | 29,410 | 32,287 | 31,413 | 30,787 | 32,235 | |||||||||||||||

(a) | Capital expenditures include investments related to reimbursable public-private partnerships. These partnership investments of $14 million, $8 million, $40 million, $166 million and $102 million in 2015, 2014, 2013, 2012 and 2011, respectively, are projects that are partially or wholly reimbursed to CSX through either government grants or other funding sources such as cash received from a property sale. These reimbursements may not be fully received in a given year; therefore, the timing of receipts may differ from the timing of the investment. See the capital expenditures table on page 36 for additional information. |

19

CSX CORPORATION

PART II

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

STRATEGIC OVERVIEW

CSX provides rail-based freight transportation services including traditional rail service, the transport of intermodal containers and trailers as well as other transportation services such as rail-to-truck transfers and bulk commodity operations with its approximately 29,000 dedicated employees. The Company and the rail industry provide customers with access to an expansive and interconnected transportation network that plays a key role in North American commerce and is critical to the long-term economic success and improved global competitiveness of the United States. Low natural gas prices, increased foreign labor costs and supply chain factors have helped to improve competitiveness of CSX's customers over the long term.

The rail industry benefits from this long-term improved global competitiveness, continued economic growth and the shift towards more rail-based solutions. U.S. demand to move more goods by rail is expected to rise and freight railroads provide the most environmentally efficient and economical means to meet this growing demand. CSX can move a ton of freight about 475 miles on one gallon of diesel fuel, as trains are four times more fuel efficient than trucks on average. Shipping freight by rail also alleviates highway congestion, eases air pollution and saves energy.

CSX's network reaches nearly two-thirds of the U.S. population, which accounts for the majority of the nation's consumption of goods. Through this network, the Company transports a diverse portfolio of commodities and products to meet the country's needs. These products range from agricultural goods, such as grains, to chemicals, automobiles, metals, building materials, paper, consumer products, and energy sources like coal, ethanol and crude oil. The Company categorizes these products into three primary lines of business: merchandise, intermodal and coal. CSX's transportation solutions connect industries and population centers across the United States with each other and with global markets through access to over 70 port facilities whereby meeting the transportation needs of energy producers, manufacturers, industrial producers, construction companies, farmers and feed mills, wholesalers and retailers and the United States Armed Forces.

Operating Initiatives

To support long-term growth, CSX is focused on meeting or exceeding customers’ expectations while improving profitability. Several key operating initiatives have been implemented over the past several years that lay a foundation for meeting these objectives. The overall goal is sustained high customer service levels, which is in part achieved through a relentless focus on using advanced network modeling analytics and tools to create a disciplined, scheduled approach to designing and running CSX's network. The Company continues to identify the most efficient, cost-effective routes for CSXT customers' traffic while providing timely service with the fewest handlings and car miles possible.

Through the Service Excellence initiative, CSX is building a culture that engages all employees and focuses on the value delivered to customers through improved service. This initiative increases employee communication and dialogue to help identify and resolve customer issues at the lowest level, improving the customer experience and allowing CSX to grow the business. This process involves engagement from all operating employees, as well as collaboration with sales and marketing employees and, ultimately, with the Company’s customers. Higher levels of customer service and satisfaction support CSX’s ability to profitably grow the business by increasing customer retention, price sustainability and asset utilization.

20

CSX CORPORATION

PART II

In addition, Total Service Integration (“TSI”) is intended to align operating capabilities with customers' needs resulting in an efficient and effective service product. TSI was first implemented in the unit train network, where it successfully increased the average number of cars per train and improved asset utilization. CSX has been implementing TSI in the carload network over the past few years and has focused on improving the “first and last mile” service experience for carload customers, providing a more consistent and reliable service product. The carload network is connected to more than 5,000 customer facilities and has a high degree of variability each day. New tools and technology have allowed the Company to more effectively communicate with customers, not only providing the service the Company has promised to deliver but proactively notifying the customer of service status. Applying TSI to the carload network has improved local customer service satisfaction and local service performance.

Finally, Enterprise Asset Management (“EAM”) focuses on improving the utilization of the company’s most critical assets, namely, crews, locomotives, cars and track infrastructure. Projects are currently in place to deploy technology, improve processes and reduce unproductive time. Because the railroad is an asset intensive industry, EAM helps reduce the overall expense associated with asset ownership by monitoring the overall condition of equipment, helping proactively schedule maintenance, increasing utilization and also effectively managing the investment required for new or replacement assets. By improving asset utilization, CSX expects to sustain long-term operating efficiencies and reduce future capital expenditures associated with asset replacement.

In summary, these initiatives are designed to improve service levels in a cost effective manner and enhance the reliability of rail transportation. These improvements to operational processes, customer communication and service are better aligning CSX's operating capabilities with customers' needs and are enabling the Company to capitalize on the strategic opportunities described below.

Strategic Opportunities

Intermodal Growth

CSX’s intermodal business is a growth opportunity that provides an economical and environmentally friendly alternative to transporting freight on highways via truck. CSX’s intermodal network connects all major population centers east of the Mississippi River, and over 90% of intermodal traffic moves in double-stack (two containers high) service. This positions the Company to capture a significant share of the incremental domestic intermodal market opportunity, estimated at nine million truckloads in the eastern United States that move over 550 miles. The Company’s highway-to-rail initiatives assist in capturing this traffic and also help customers identify conversion opportunities for both domestic moves and the U.S. portion of international moves.

To further enhance the Company's intermodal offering and support future growth, CSX recently completed new or expanded terminal construction to increase network capacity and broaden its market presence in key growth areas. In 2015, CSX began construction on a new terminal near Pittsburgh, PA, enhancing the Company’s reach and supporting continued growth. Over the past several years, the Company also opened or expanded seven other terminals in Winter Haven, FL; Quebec, Canada; Columbus, OH; Louisville, KY; Atlanta, GA; and Worcester, MA; as well as the Company's Northwest Ohio terminal which is part of the National Gateway Initiative discussed below.

Illinois Basin Coal Shift

Energy markets have shifted over the past few years and continue to evolve. For instance, domestic utility coal demand decreased in 2015 relative to previous years. In the long term, downward pressure on domestic coal volumes will likely continue as the result of increasingly stringent existing and proposed environmental regulations and continued low natural gas prices. In addition, mining economics are causing a shift from Central Appalachian coal to thermal coal in the Illinois Basin and the Powder River Basin. CSX will capitalize on these shifts and address structural costs in the regions of declining volume.

21

CSX CORPORATION

PART II

Export Coal

CSX export coal volume and pricing is subject to a high degree of volatility as a result of changes in the global economy, competition from foreign coal producers and regulatory shifts. Over the past few years, CSX has capitalized on the global coal demand in both steel manufacturing and power generation. Currently, both global thermal and metallurgical coal prices are low due to oversupply, but CSX sees long-term growth in global demand as developing countries become more urbanized. The Company remains opportunistic based on the global markets and the resulting level of demand.

Energy Markets

Shale drilling for the extraction of oil and natural gas has created the opportunity for CSX to serve energy markets such as crude oil, liquefied petroleum gases (“LPG”), frac sand and other related materials, although energy market volume is volatile from year to year. For example, CSX is capitalizing on the opportunity to move the supply of crude oil from the domestic oil fields, particularly those located in the Bakken Shale region of North Dakota, to customers at eastern refineries. This service also provides greater flexibility in source locations as compared to pipelines. Volume, however, may vary depending upon oil prices and spreads.

CSX’s LPG market is also benefiting from drilling in Ohio, Pennsylvania and West Virginia within the Utica shale region. Midstream energy companies, which are involved in the transportation, storage and wholesale of refined petroleum products, are taking advantage of the abundance of inexpensive wet gas with newly constructed gas processing plants (or “fractionators”) in the region. Rail will also play a vital role in moving LPG products from the fractionators to the market.

Over the longer term, the energy supply outlook for the U.S. will create a sustainable competitive advantage for domestic chemical producers and generate additional growth opportunities for rail. Since natural gas is the primary component in the production of a wide range of petrochemicals, the supply growth and the resulting lower prices have now placed the U.S. amongst the lowest cost production regions in the world. This increased competitiveness is sparking significant investment in new U.S. chemical industry capacity for the first time in more than a decade. CSX is well-positioned to participate in this growing chemical business over the next several years.

Public-Private Partnerships

Expanding capacity on U.S. rail networks provides substantial public benefits including job creation, increased business activity at U.S. ports, reduced highway congestion and lower air emissions. Therefore, CSX and its government partners are jointly working to invest in multi-year rail infrastructure projects such as the National Gateway. This initiative is a public-private partnership which will increase intermodal capacity and create substantial environmental and efficiency advantages by clearing key corridors between mid-Atlantic ports and the Midwest for double-stack intermodal trains.

As part of the National Gateway project, CSX broke ground on the modernization of the Virginia Avenue Tunnel in Washington, D.C. in 2015.This project will improve the flow of freight traffic through the District of Columbia and will eliminate a rail-traffic bottleneck that also impacts commuter and passenger trains in the region. The new structure will provide double-stack train clearances in Maryland, West Virginia and the District of Columbia. Going forward, CSX will continue to explore other opportunities to partner with the public sector to maximize the many public benefits of freight rail.

22

CSX CORPORATION

PART II

Balanced Approach to Cash Deployment

CSX remains highly committed to delivering value to shareholders through a balanced approach to deploying cash that includes investments in the business, dividend growth and share repurchases. In 2015, the Company invested $2.6 billion to further enhance the capacity, quality, safety and flexibility of its network. In addition, CSX continues to return value to its shareholders in the form of dividends and share repurchases. During 2015, the Company announced a 13 percent increase in the quarterly cash dividend to $0.18 per common share. The Company has increased its quarterly cash dividend 13 times over the last ten years which represents a 26 percent compounded annual growth rate. Also in 2015, CSX announced a new $2 billion share repurchase program, which is expected to be completed by April 2017 based on market and business decisions. CSX repurchased $804 million, or 26 million shares, during 2015 under this program. Since 2006, CSX has repurchased 520 million shares (adjusted for stock splits) for $9.6 billion, which represents about one-half of total shares currently outstanding. As part of this balanced approach, the Company is committed to maintaining a credit profile consistent with a BBB+ rating by Standard & Poor’s and a Baa1 rating by Moody’s Investment Services.

Summary

These operating initiatives, strategic areas, long-term investments and shareholder returns discussed above provide a foundation for volume growth, productivity improvement, enhanced customer service and continued advancements in the safety and reliability of operations. To continue these types of investments, the Company must be able to operate in an environment in which it can generate adequate returns and drive shareholder value. CSX will continue to advocate for a fair and balanced regulatory environment to ensure that the value of the Company's rail service would be reflected in any potential new legislation or policies.

23

CSX CORPORATION

PART II

2015 HIGHLIGHTS

• Revenue of $11.8 billion decreased $858 million or 7% versus the prior year.

• Expenses of $8.2 billion decreased $829 million or 9% year over year.

• Operating income of $3.6 billion decreased $29 million or 1% year over year.

• Operating ratio of 69.7%, the Company’s first sub-70 percent full-year operating ratio, improved 180 basis points from 71.5%.

• | Earnings per diluted share of $2.00 increased $0.08 or 4% year over year. |

Fiscal Years | |||||||||||

(in Thousands) | 2015 | 2014 | 2013 | ||||||||

Volume | 6,761 | 6,922 | 6,539 | ||||||||

(in Millions) | |||||||||||

Revenue | $ | 11,811 | $ | 12,669 | $ | 12,026 | |||||

Expense | 8,227 | 9,056 | 8,553 | ||||||||

Operating Income | $ | 3,584 | $ | 3,613 | $ | 3,473 | |||||

Operating Ratio | 69.7 | % | 71.5 | % | 71.1 | % | |||||

Earnings per diluted share | $ | 2.00 | $ | 1.92 | $ | 1.83 | |||||

For additional information, refer to Results of Operations discussed on pages 26 to 33. | ||||

24

CSX CORPORATION

PART II

Free Cash Flow (Non-GAAP Measure)

Free cash flow is considered a non-GAAP financial measure under SEC Regulation G, Disclosure of Non-GAAP Measures. Management believes that free cash flow is useful to investors as it is important in evaluating the Company’s financial performance. More specifically, free cash flow measures cash generated by the business after reinvestment. This measure represents cash available for both equity and bond investors to be used for dividends, share repurchases or principal reduction on outstanding debt. Free cash flow should be considered in addition to, rather than a substitute for, cash provided by operating activities. Free cash flow is calculated by using net cash from operations and adjusting for property additions and certain other investing activities. As described below, free cash flow before dividends increased $73 million year over year to $992 million. The primary reason for the increase in free cash flow from the prior year is primarily due to the following:

• | Higher proceeds from a property sale and other related income of $85 million |

• | Higher net sales of long-term marketable securities of $71 million |

• | Partially offsetting these increases were higher property additions of $113 million |

The following table reconciles cash provided by operating activities (GAAP measure) to free cash flow (non-GAAP measure).

Fiscal Years | |||||||||||

2015 | 2014 | 2013 | |||||||||

(Dollars in Millions) | |||||||||||

Net cash provided by operating activities | $ | 3,370 | $ | 3,343 | $ | 3,267 | |||||

Property additions (a) | (2,562 | ) | (2,449 | ) | (2,313 | ) | |||||

Proceeds from property dispositions | 147 | 62 | 53 | ||||||||

Other investing activities | 37 | (37 | ) | (112 | ) | ||||||

Free Cash Flow (before payment of dividends) | $ | 992 | $ | 919 | $ | 895 | |||||

(a) | Property additions include investments related to reimbursable public-private partnerships. These partnership investments of $14 million, $8 million and $40 million in 2015, 2014 and 2013, respectively, are projects that are partially or wholly reimbursed to CSX through either government grants or other funding sources such as cash received from a property sale. These reimbursements may not be fully received in a given year; therefore the timing of receipts may differ from the timing of the investment. |

25

CSX CORPORATION

PART II

RESULTS OF OPERATIONS

2015 vs. 2014 Results of Operations

Fiscal Years | |||||||||||||||

2015 | 2014 | $ Change | % Change | ||||||||||||

(Dollars in Millions) | |||||||||||||||

Revenue | $ | 11,811 | $ | 12,669 | $ | (858 | ) | (7 | )% | ||||||

Expense | |||||||||||||||

Labor and Fringe | 3,290 | 3,377 | 87 | 3 | |||||||||||

Materials, Supplies and Other | 2,336 | 2,484 | 148 | 6 | |||||||||||

Fuel | 957 | 1,616 | 659 | 41 | |||||||||||

Depreciation | 1,208 | 1,151 | (57 | ) | (5 | ) | |||||||||

Equipment and Other Rents | 436 | 428 | (8 | ) | (2 | ) | |||||||||

Total Expense | 8,227 | 9,056 | 829 | 9 | |||||||||||

Operating Income | 3,584 | 3,613 | (29 | ) | (1 | ) | |||||||||

Interest Expense | (544 | ) | (545 | ) | 1 | — | |||||||||

Other Income - Net | 98 | (24 | ) | 122 | (508 | ) | |||||||||

Income Tax Expense | (1,170 | ) | (1,117 | ) | (53 | ) | (5 | ) | |||||||

Net Earnings | $ | 1,968 | $ | 1,927 | $ | 41 | 2 | ||||||||

Earnings Per Diluted Share: | |||||||||||||||

Net Earnings | $ | 2.00 | $ | 1.92 | $ | 0.08 | 4 | % | |||||||

Operating Ratio | 69.7 | % | 71.5 | % | (180 | ) | bps | ||||||||

Volume and Revenue (Unaudited) | ||||||||||||||||||||||||||||||

Volume (Thousands of units); Revenue (Dollars in Millions); Revenue Per Unit (Dollars) | ||||||||||||||||||||||||||||||

Volume | Revenue | Revenue Per Unit | ||||||||||||||||||||||||||||