Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Starwood Waypoint Homes | d91120d8k.htm |

Exhibit 99.1

COLONYAMERICANHOMES Colony Starwood Homes Update Presentation October 2015

Forward-Looking Statements This presentation may include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements, which are based on current expectations, estimates and projections about the industry and markets in which Starwood Waypoint Residential Trust (“SWAY”) and Colony American Homes (“CAH”) operate and beliefs of and assumptions made by SWAY management and CAH management, involve uncertainties that could significantly affect the financial results of SWAY or CAH or the combined company (“Colony Starwood Homes” or the “Combined Company”). Words such as “may,” “will,” “should,” “might,” “could,” “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “potential,” “continue,” “predicts,” variations of such words, the negative of such words and similar expressions are intended to identify such forward-looking statements, which generally are not historical in nature. Such forward-looking statements include, but are not limited to, statements about the anticipated benefits of the business combination transaction involving SWAY and CAH, including future financial and operating results (such as core funds from operations, “Core FFO”), and the Combined Company’s plans, objectives, expectations and intentions. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future — including statements relating to expected synergies, improved liquidity and balance sheet strength — are forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Although we believe the expectations reflected in any forward-looking statements are based on reasonable assumptions, we can give no assurance that our expectations will be attained and therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements. Some of the factors that may affect outcomes and results include, but are not limited to: (i) national, regional and local economic climates, (ii) changes in financial markets and interest rates, or to the business or financial condition of either company or business, (iii) changes in market demand for rental single family homes and competitive pricing, (iv) risks associated with acquisitions, including the integration of the combined companies’ businesses, (v) maintenance of real estate investment trust (“REIT”) status, (vi) availability of financing and capital, (vii) risks associated with achieving expected revenue synergies or cost savings, (viii) risks associated with the companies’ ability to consummate the merger on the terms described or at all and the timing of the closing of the merger, and (ix) those additional risks and factors discussed in reports filed with the Securities and Exchange Commission (“SEC”) by SWAY from time to time, including those discussed under the heading “Risk Factors” in its most recently filed reports on Forms 10-K and 10-Q. There can be no assurance that the proposed combination will in fact be consummated. Neither SWAY, CAH nor any other person assumes responsibility for the accuracy or completeness of any of these forward-looking statements. You should not rely upon forward-looking statements as predictions of future events. The forward-looking statements speak only as of the date of this communication, and both SWAY and CAH anticipate that subsequent events and developments will cause their views to change. However, neither SWAY nor CAH undertakes any duty to update any forward-looking statements appearing in this presentation, nor to confirm SWAY or CAH’s prior statements to actual results or revised expectations, and neither SWAY nor CAH intend to do so.

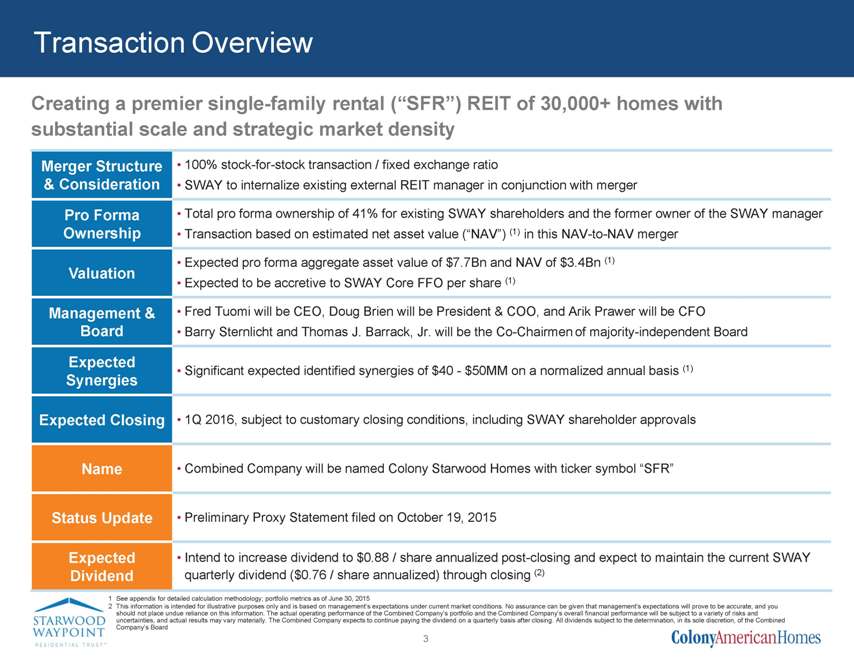

Transaction Overview Creating a premier single-family rental (“SFR”) REIT of 30,000+ homes with substantial scale and strategic market density Merger Structure • 100% stock-for-stock transaction / fixed exchange ratio & Consideration • SWAY to internalize existing external REIT manager in conjunction with merger Pro Forma • Total pro forma ownership of 41% for existing SWAY shareholders and the former owner of the SWAY manager Ownership • Transaction based on estimated net asset value (“NAV”) (1) in this NAV-to-NAV merger • Expected pro forma aggregate asset value of $7.7Bn and NAV of $3.4Bn (1) Valuation • Expected to be accretive to SWAY Core FFO per share (1) Management & • Fred Tuomi will be CEO, Doug Brien will be President & COO, and Arik Prawer will be CFO Board • Barry Sternlicht and Thomas J. Barrack, Jr. will be the Co-Chairmen of majority-independent Board Expected (1) • Significant expected identified synergies of $40—$50MM on a normalized annual basis Synergies Expected Closing • 1Q 2016, subject to customary closing conditions, including SWAY shareholder approvals Name • Combined Company will be named Colony Starwood Homes with ticker symbol “SFR” Status Update • Preliminary Proxy Statement filed on October 19, 2015 Expected • Intend to increase dividend to $0.88 / share annualized post-closing and expect to maintain the current SWAY Dividend • quarterly dividend ($0.76 / share annualized) through closing (2) 1 See appendix for detailed calculation methodology; portfolio metrics as of June 30, 2015 2 This information is intended for illustrative purposes only and is based on management’s expectations under current market conditions. No assurance can be given that management’s expectations will prove to be accurate, and you should not place undue reliance on this information. The actual operating performance of the Combined Company’s portfolio and the Combined Company’s overall financial performance will be subject to a variety of risks and uncertainties, and actual results may vary materially. The Combined Company expects to continue paying the dividend on a quarterly basis after closing. All dividends subject to the determination, in its sole discretion, of the Combined Company’s Board

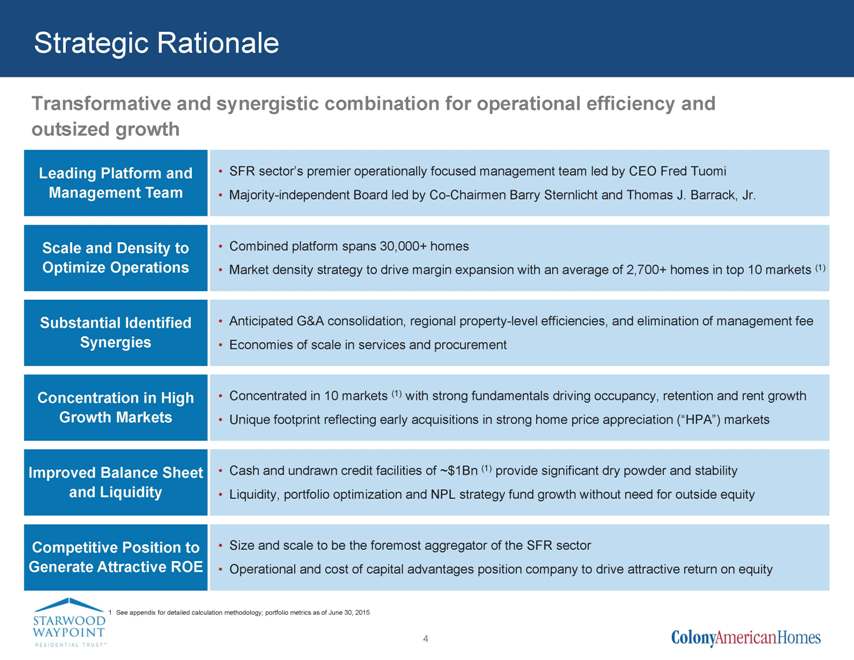

Strategic Rationale Transformative and synergistic combination for operational efficiency and outsized growth Leading Platform and • SFR sector’s premier operationally focused management team led by CEO Fred Tuomi Management Team • Majority-independent Board led by Co-Chairmen Barry Sternlicht and Thomas J. Barrack, Jr. Scale and Density to • Combined platform spans 30,000+ homes Optimize Operations • Market density strategy to drive margin expansion with an average of 2,700+ homes in top 10 markets (1) Substantial Identified • Anticipated G&A consolidation, regional property-level efficiencies, and elimination of management fee Synergies • Economies of scale in services and procurement Concentration in High • Concentrated in 10 markets (1) with strong fundamentals driving occupancy, retention and rent growth Growth Markets • Unique footprint reflecting early acquisitions in strong home price appreciation (“HPA”) markets Improved Balance Sheet • Cash and undrawn credit facilities of ~$1Bn (1) provide significant dry powder and stability and Liquidity • Liquidity, portfolio optimization and NPL strategy fund growth without need for outside equity Competitive Position to • Size and scale to be the foremost aggregator of the SFR sector Generate Attractive ROE • Operational and cost of capital advantages position company to drive attractive return on equity 1 See appendix for detailed calculation methodology; portfolio metrics as of June 30, 2015

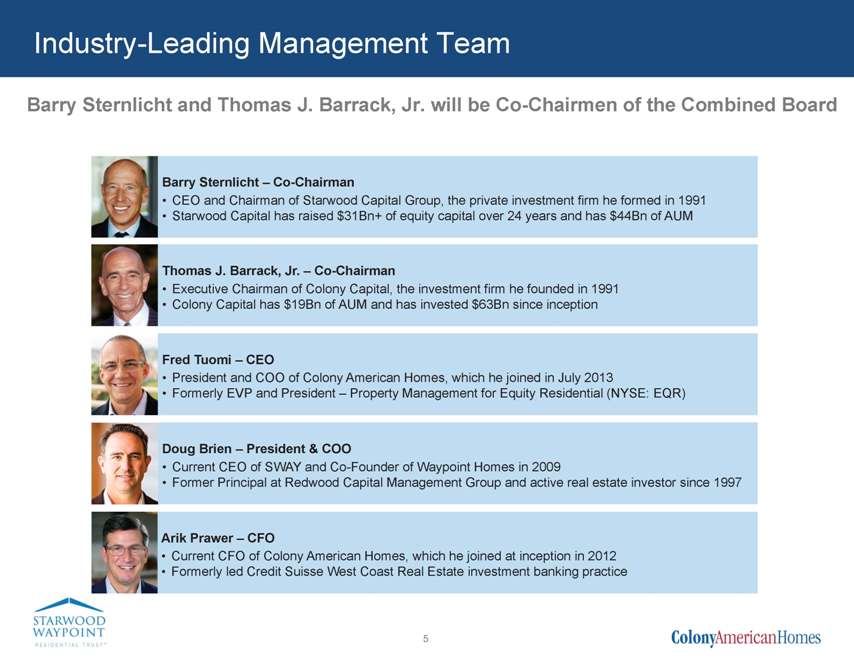

Industry-Leading Management Team Barry Sternlicht and Thomas J. Barrack, Jr. will be Co-Chairmen of the Combined Board Barry Sternlicht – Co-Chairman • CEO and Chairman of Starwood Capital Group, the private investment firm he formed in 1991 • Starwood Capital has raised $31Bn+ of equity capital over 24 years and has $44Bn of AUM Thomas J. Barrack, Jr. – Co-Chairman • Executive Chairman of Colony Capital, the investment firm he founded in 1991 • Colony Capital has $19Bn of AUM and has invested $63Bn since inception Fred Tuomi – CEO • President and COO of Colony American Homes, which he joined in July 2013 • Formerly EVP and President – Property Management for Equity Residential (NYSE: EQR) Doug Brien – President & COO • Current CEO of SWAY and Co-Founder of Waypoint Homes in 2009 • Former Principal at Redwood Capital Management Group and active real estate investor since 1997 Arik Prawer – CFO • Current CFO of Colony American Homes, which he joined at inception in 2012 • Formerly led Credit Suisse West Coast Real Estate investment banking practice

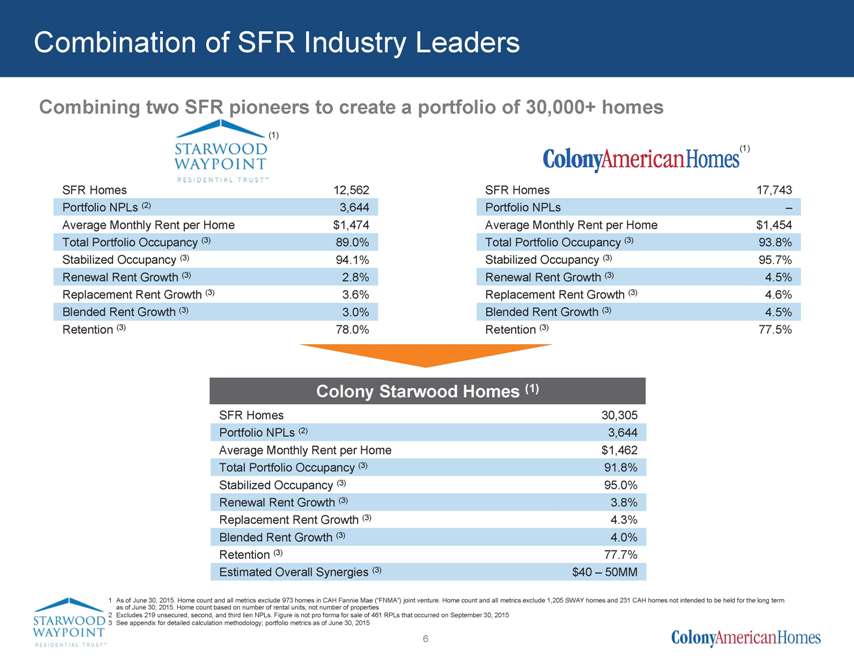

Combination of SFR Industry Leaders Combining two SFR pioneers to create a portfolio of 30,000+ homes SFR Homes 12,562 Portfolio NPLs (2) 3,644 Average Monthly Rent per Home $1,474 Total Portfolio Occupancy (3) 89.0% Stabilized Occupancy (3) 94.1% Renewal Rent Growth (3) 2.8% Replacement Rent Growth (3) 3.6% Blended Rent Growth (3) 3.0% Retention (3) 78.0% (1) SFR Homes 17,743 Portfolio NPLs –Average Monthly Rent per Home $1,454 Total Portfolio Occupancy (3) 93.8% Stabilized Occupancy (3) 95.7% Renewal Rent Growth (3) 4.5% Replacement Rent Growth (3) 4.6% Blended Rent Growth (3) 4.5% Retention (3) 77.5% Colony Starwood Homes (1) SFR Homes 30,305 Portfolio NPLs (2) 3,644 Average Monthly Rent per Home $1,462 Total Portfolio Occupancy (3) 91.8% Stabilized Occupancy (3) 95.0% Renewal Rent Growth (3) 3.8% Replacement Rent Growth (3) 4.3% Blended Rent Growth (3) 4.0% Retention (3) 77.7% Estimated Overall Synergies (3) $40 – 50MM 1 As of June 30, 2015. Home count and all metrics exclude 973 homes in CAH Fannie Mae (“FNMA”) joint venture. Home count and all metrics exclude 1,205 SWAY homes and 231 CAH homes not intended to be held for the long term as of June 30, 2015. Home count based on number of rental units, not number of properties 2 Excludes 219 unsecured, second, and third lien NPLs. Figure is not pro forma for sale of 461 RPLs that occurred on September 30, 2015 3 See appendix for detailed calculation methodology; portfolio metrics as of June 30, 2015

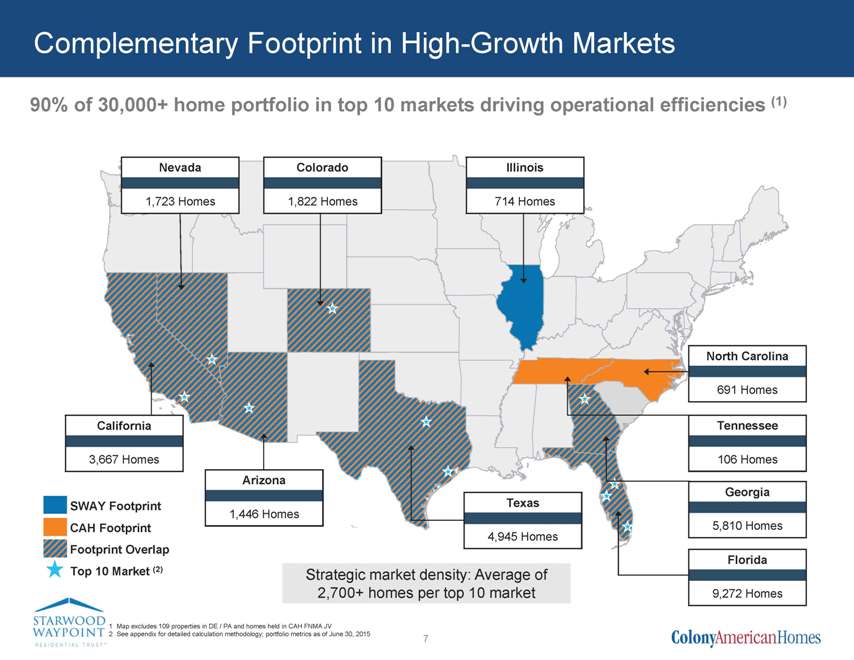

Complementary Footprint in High-Growth Markets 90% of 30,000+ home portfolio in top 10 markets driving operational efficiencies (1) Nevada Colorado Illinois 1,723 Homes 1,822 Homes 714 Homes North Carolina 691 Homes Tennessee 106 Homes Georgia 5,810 Homes Florida 9,272 Homes California 3,667 Homes Arizona SWAY Footprint 1,446 Homes Texas CAH Footprint 4,945 Homes Footprint Overlap Top 10 Market (2) Strategic market density: Average of 2,700+ homes per top 10 market 1 Map excludes 109 properties in DE / PA and homes held in CAH FNMA JV 2 See appendix for detailed calculation methodology; portfolio metrics as of June 30, 2015

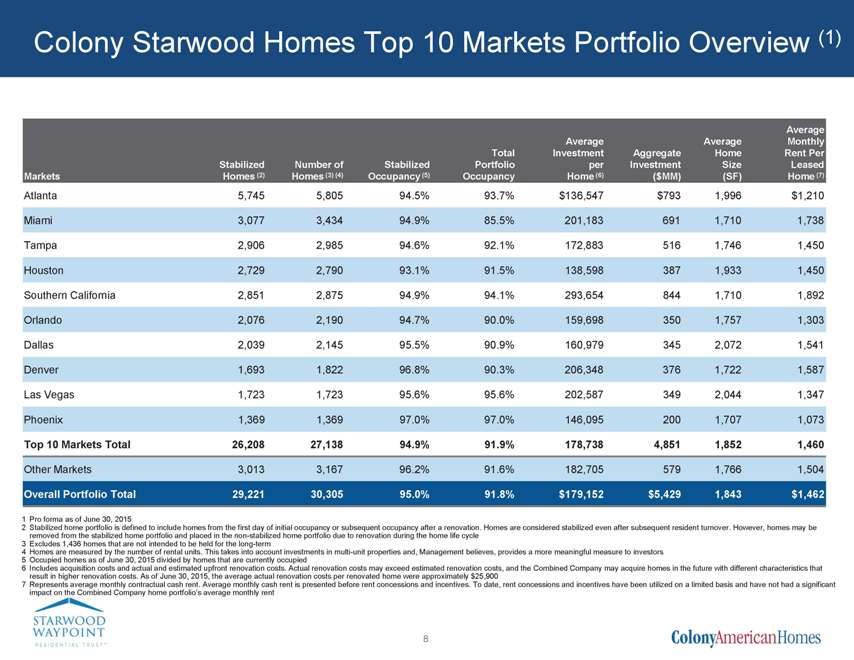

Colony Starwood Homes Top 10 Markets Portfolio Overview (1) Average Average Average Monthly Total Investment Aggregate Home Rent Per Stabilized Number of Stabilized Portfolio per Investment Size Leased Markets Homes (2) Homes (3) (4) Occupancy (5) Occupancy Home (6) ($MM) (SF) Home (7) Atlanta 5,745 5,805 94.5% 93.7% $136,547 $793 1,996 $1,210 Miami 3,077 3,434 94.9% 85.5% 201,183 691 1,710 1,738 Tampa 2,906 2,985 94.6% 92.1% 172,883 516 1,746 1,450 Houston 2,729 2,790 93.1% 91.5% 138,598 387 1,933 1,450 Southern California 2,851 2,875 94.9% 94.1% 293,654 844 1,710 1,892 Orlando 2,076 2,190 94.7% 90.0% 159,698 350 1,757 1,303 Dallas 2,039 2,145 95.5% 90.9% 160,979 345 2,072 1,541 Denver 1,693 1,822 96.8% 90.3% 206,348 376 1,722 1,587 Las Vegas 1,723 1,723 95.6% 95.6% 202,587 349 2,044 1,347 Phoenix 1,369 1,369 97.0% 97.0% 146,095 200 1,707 1,073 Top 10 Markets Total 26,208 27,138 94.9% 91.9% 178,738 4,851 1,852 1,460 Other Markets 3,013 3,167 96.2% 91.6% 182,705 579 1,766 1,504 Overall Portfolio Total 29,221 30,305 95.0% 91.8% $179,152 $5,429 1,843 $1,462 1 Pro forma as of June 30, 2015 2 Stabilized home portfolio is defined to include homes from the first day of initial occupancy or subsequent occupancy after a renovation. Homes are considered stabilized even after subsequent resident turnover. However, homes may be removed from the stabilized home portfolio and placed in the non-stabilized home portfolio due to renovation during the home life cycle 3 Excludes 1,436 homes that are not intended to be held for the long-term 4 Homes are measured by the number of rental units. This takes into account investments in multi-unit properties and, Management believes, provides a more meaningful measure to investors 5 Occupied homes as of June 30, 2015 divided by homes that are currently occupied 6 Includes acquisition costs and actual and estimated upfront renovation costs. Actual renovation costs may exceed estimated renovation costs, and the Combined Company may acquire homes in the future with different characteristics that result in higher renovation costs. As of June 30, 2015, the average actual renovation costs per renovated home were approximately $25,900 7 Represents average monthly contractual cash rent. Average monthly cash rent is presented before rent concessions and incentives. To date, rent concessions and incentives have been utilized on a limited basis and have not had a significant impact on the Combined Company home portfolio’s average monthly rent

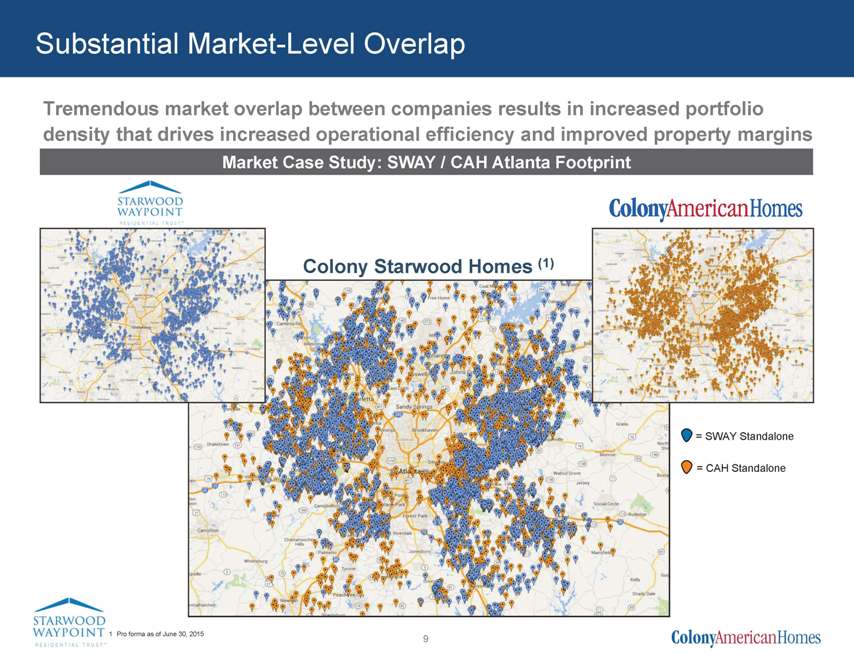

Substantial Market-Level Overlap Tremendous market overlap between companies results in increased portfolio density that drives increased operational efficiency and improved property margins Market Case Study: SWAY / CAH Atlanta Footprint SWAY Standalone CAH Standalone 1 Pro forma as of June 30, 2015

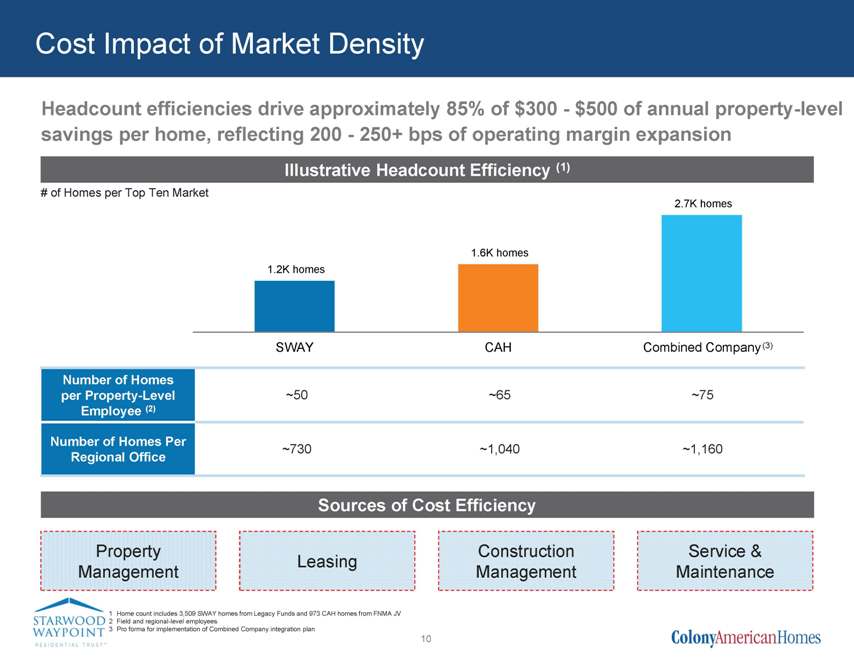

Cost Impact of Market Density Headcount efficiencies drive approximately 85% of $300—$500 of annual property-level savings per home, reflecting 200—250+ bps of operating margin expansion Illustrative Headcount Efficiency (1) # of Homes per Top Ten Market 2.7K homes Number of Homes per Property-Level ~50 ~65 ~75 Employee (2) Number of Homes Per ~730 ~1,040 ~1,160 Regional Office Property Construction Service & Leasing Management Management Maintenance 1 Home count includes 3,509 SWAY homes from Legacy Funds and 973 CAH homes from FNMA JV 2 Field and regional-level employees 3 Pro forma for implementation of Combined Company integration plan 10

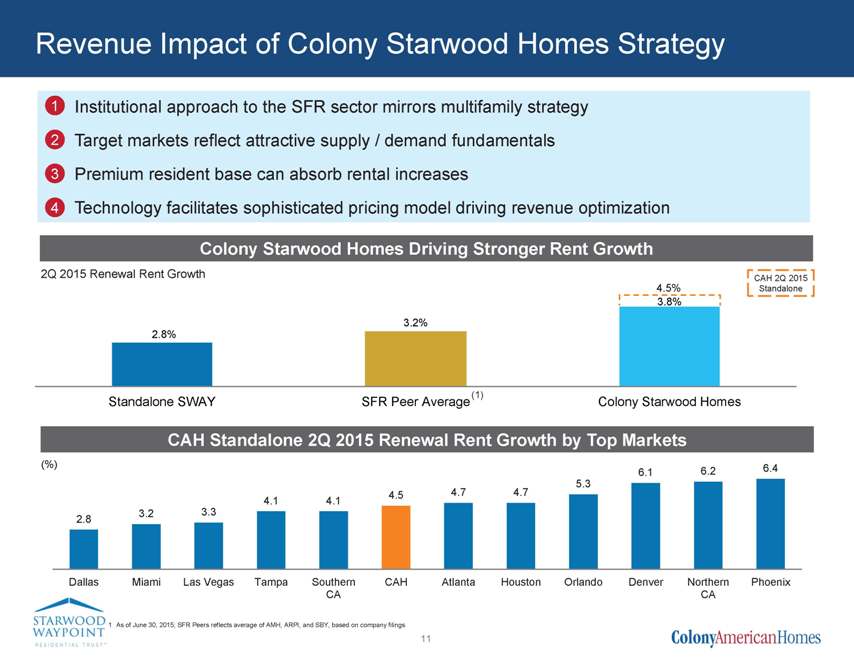

Revenue Impact of Colony Starwood Homes Strategy •1 Institutional approach to the SFR sector mirrors multifamily strategy •2 Target markets reflect attractive supply / demand fundamentals •3 Premium resident base can absorb rental increases •4 Technology facilitates sophisticated pricing model driving revenue optimization Colony Starwood Homes Driving Stronger Rent Growth 2Q 2015 Renewal Rent Growth CAH 2Q (1) Standalone SWAY SFR Peer Average Colony Starwood Homes CAH Standalone 2Q 2015 Renewal Rent Growth by Top Markets 6.1 6.2 6.4 1 As of June 30, 2015; SFR Peers reflects average of AMH, ARPI, and SBY, based on company filings

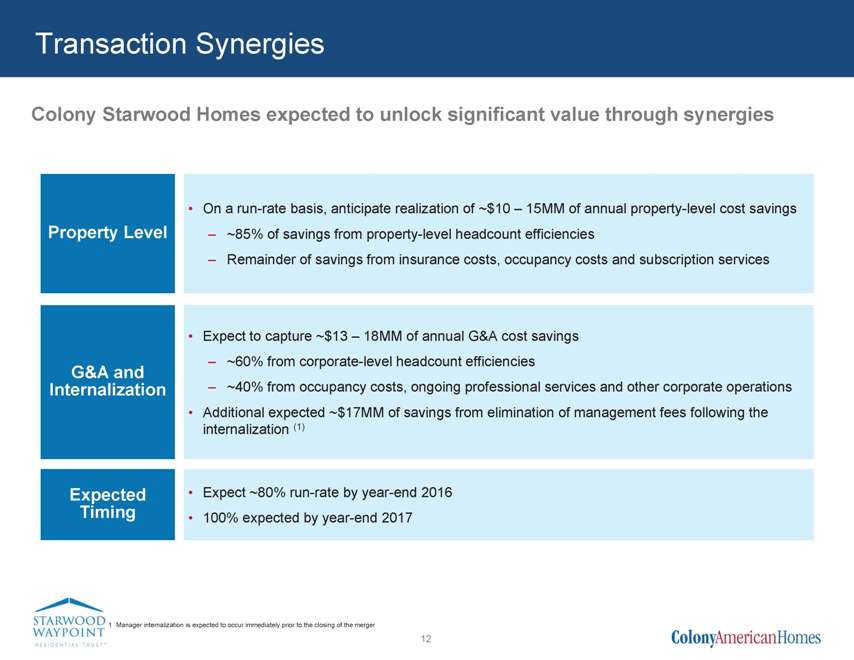

Transaction Synergies Colony Starwood Homes expected to unlock significant value through synergies • On a run-rate basis, anticipate realization of ~$10 – 15MM of annual property-level cost savings Property Level ? ~85% of savings from property-level headcount efficiencies ? Remainder of savings from insurance costs, occupancy costs and subscription services • Expect to capture ~$13 – 18MM of annual G&A cost savings ? ~60% from corporate-level headcount efficiencies G&A and Internalization ? ~40% from occupancy costs, ongoing professional services and other corporate operations • Additional expected ~$17MM of savings from elimination of management fees following the internalization (1) Expected • Expect ~80% run-rate by year-end 2016 Timing • 100% expected by year-end 2017

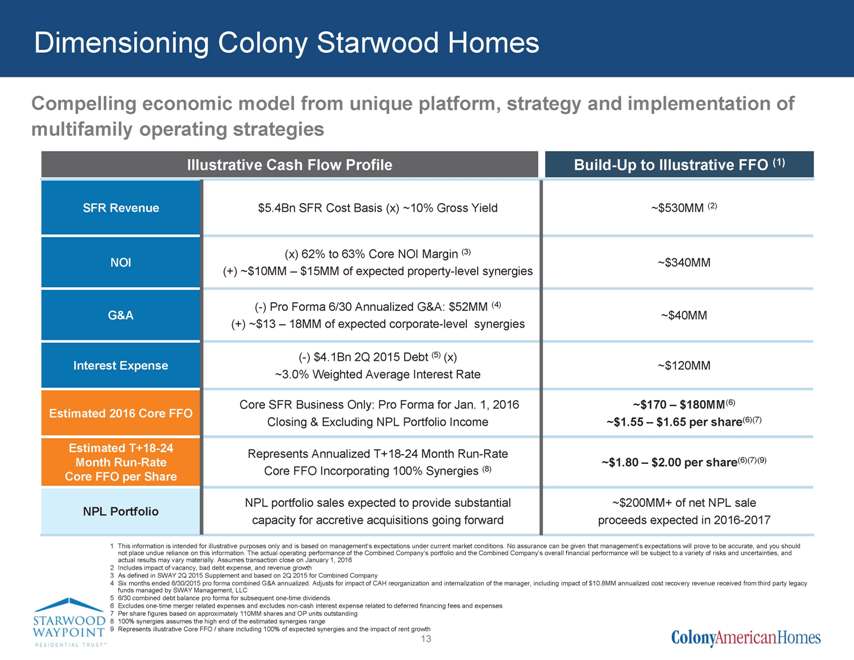

Dimensioning Colony Starwood Homes Compelling economic model from unique platform, strategy and implementation of multifamily operating strategies Illustrative Cash Flow Profile Build-Up to Illustrative FFO (1) SFR Revenue $5.4Bn SFR Cost Basis (x) ~10% Gross Yield ~$530MM (2) (x) 62% to 63% Core NOI Margin (3) NOI ~$340MM (+) ~$10MM – $15MM of expected property-level synergies (-) Pro Forma 6/30 Annualized G&A: $52MM (4) G&A ~$40MM (+) ~$13 – 18MM of expected corporate-level synergies (-) $4.1Bn 2Q 2015 Debt (5) (x) Interest Expense ~$120MM ~3.0% Weighted Average Interest Rate Core SFR Business Only: Pro Forma for Jan. 1, 2016 ~$170 – $180MM(6) Estimated 2016 Core FFO Closing & Excluding NPL Portfolio Income ~$1.55 – $1.65 per share(6)(7) Estimated T+18-24 Represents Annualized T+18-24 Month Run-Rate Month Run-Rate ~$1.80 – $2.00 per share(6)(7)(9) Core FFO Incorporating 100% Synergies (8) Core FFO per Share NPL portfolio sales expected to provide substantial ~$200MM+ of net NPL sale NPL Portfolio capacity for accretive acquisitions going forward proceeds expected in 2016-2017 1 This information is intended for illustrative purposes only and is based on management’s expectations under current market conditions. No assurance can be given that management’s expectations will prove to be accurate, and you should not place undue reliance on this information. The actual operating performance of the Combined Company’s portfolio and the Combined Company’s overall financial performance will be subject to a variety of risks and uncertainties, and actual results may vary materially. Assumes transaction close on January 1, 2016 2 Includes impact of vacancy, bad debt expense, and revenue growth 3 As defined in SWAY 2Q 2015 Supplement and based on 2Q 2015 for Combined Company 4 Six months ended 6/30/2015 pro forma combined G&A annualized. Adjusts for impact of CAH reorganization and internalization of the manager, including impact of $10.8MM annualized cost recovery revenue received from third party legacy funds managed by SWAY Management, LLC 5 6/30 combined debt balance pro forma for subsequent one-time dividends 6 Excludes one-time merger related expenses and excludes non-cash interest expense related to deferred financing fees and expenses 7 Per share figures based on approximately 110MM shares and OP units outstanding 8 100% synergies assumes the high end of the estimated synergies range 9 Represents illustrative Core FFO / share including 100% of expected synergies and the impact of rent growth 13

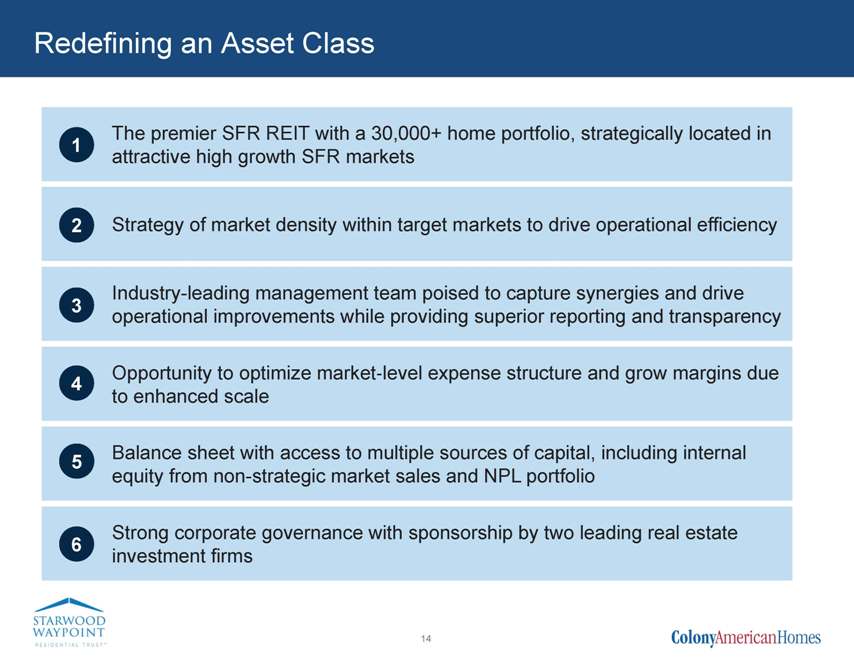

Redefining an Asset Class The premier SFR REIT with a 30,000+ home portfolio, strategically located in 1 attractive high growth SFR markets 2 Strategy of market density within target markets to drive operational efficiency Industry-leading management team poised to capture synergies and drive 3 operational improvements while providing superior reporting and transparency Opportunity to optimize market?level expense structure and grow margins due 4 to enhanced scale Balance sheet with access to multiple sources of capital, including internal 5 equity from non-strategic market sales and NPL portfolio Strong corporate governance with sponsorship by two leading real estate 6 investment firms

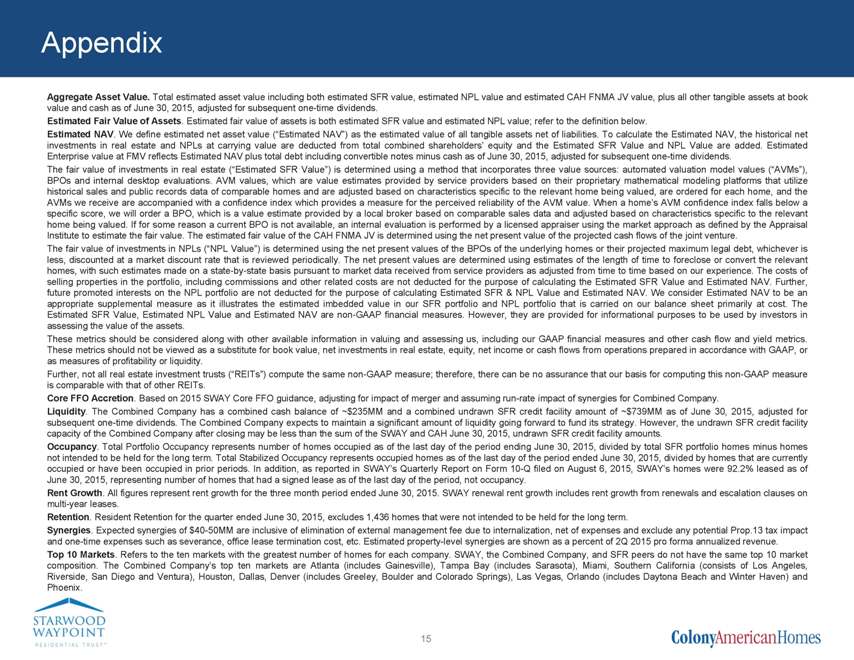

Appendix Aggregate Asset Value. Total estimated asset value including both estimated SFR value, estimated NPL value and estimated CAH FNMA JV value, plus all other tangible assets at book value and cash as of June 30, 2015, adjusted for subsequent one-time dividends. Estimated Fair Value of Assets. Estimated fair value of assets is both estimated SFR value and estimated NPL value; refer to the definition below. Estimated NAV. We define estimated net asset value (“Estimated NAV”) as the estimated value of all tangible assets net of liabilities. To calculate the Estimated NAV, the historical net investments in real estate and NPLs at carrying value are deducted from total combined shareholders’ equity and the Estimated SFR Value and NPL Value are added. Estimated Enterprise value at FMV reflects Estimated NAV plus total debt including convertible notes minus cash as of June 30, 2015, adjusted for subsequent one-time dividends. The fair value of investments in real estate (“Estimated SFR Value”) is determined using a method that incorporates three value sources: automated valuation model values (“AVMs”), BPOs and internal desktop evaluations. AVM values, which are value estimates provided by service providers based on their proprietary mathematical modeling platforms that utilize historical sales and public records data of comparable homes and are adjusted based on characteristics specific to the relevant home being valued, are ordered for each home, and the AVMs we receive are accompanied with a confidence index which provides a measure for the perceived reliability of the AVM value. When a home’s AVM confidence index falls below a specific score, we will order a BPO, which is a value estimate provided by a local broker based on comparable sales data and adjusted based on characteristics specific to the relevant home being valued. If for some reason a current BPO is not available, an internal evaluation is performed by a licensed appraiser using the market approach as defined by the Appraisal Institute to estimate the fair value. The estimated fair value of the CAH FNMA JV is determined using the net present value of the projected cash flows of the joint venture. The fair value of investments in NPLs (“NPL Value”) is determined using the net present values of the BPOs of the underlying homes or their projected maximum legal debt, whichever is less, discounted at a market discount rate that is reviewed periodically. The net present values are determined using estimates of the length of time to foreclose or convert the relevant homes, with such estimates made on a state?by?state basis pursuant to market data received from service providers as adjusted from time to time based on our experience. The costs of selling properties in the portfolio, including commissions and other related costs are not deducted for the purpose of calculating the Estimated SFR Value and Estimated NAV. Further, future promoted interests on the NPL portfolio are not deducted for the purpose of calculating Estimated SFR & NPL Value and Estimated NAV. We consider Estimated NAV to be an appropriate supplemental measure as it illustrates the estimated imbedded value in our SFR portfolio and NPL portfolio that is carried on our balance sheet primarily at cost. The Estimated SFR Value, Estimated NPL Value and Estimated NAV are non?GAAP financial measures. However, they are provided for informational purposes to be used by investors in assessing the value of the assets. These metrics should be considered along with other available information in valuing and assessing us, including our GAAP financial measures and other cash flow and yield metrics. These metrics should not be viewed as a substitute for book value, net investments in real estate, equity, net income or cash flows from operations prepared in accordance with GAAP, or as measures of profitability or liquidity. Further, not all real estate investment trusts (“REITs”) compute the same non?GAAP measure; therefore, there can be no assurance that our basis for computing this non?GAAP measure is comparable with that of other REITs. Core FFO Accretion. Based on 2015 SWAY Core FFO guidance, adjusting for impact of merger and assuming run-rate impact of synergies for Combined Company. Liquidity. The Combined Company has a combined cash balance of ~$235MM and a combined undrawn SFR credit facility amount of ~$739MM as of June 30, 2015, adjusted for subsequent one-time dividends. The Combined Company expects to maintain a significant amount of liquidity going forward to fund its strategy. However, the undrawn SFR credit facility capacity of the Combined Company after closing may be less than the sum of the SWAY and CAH June 30, 2015, undrawn SFR credit facility amounts. Occupancy. Total Portfolio Occupancy represents number of homes occupied as of the last day of the period ending June 30, 2015, divided by total SFR portfolio homes minus homes not intended to be held for the long term. Total Stabilized Occupancy represents occupied homes as of the last day of the period ended June 30, 2015, divided by homes that are currently occupied or have been occupied in prior periods. In addition, as reported in SWAY’s Quarterly Report on Form 10-Q filed on August 6, 2015, SWAY’s homes were 92.2% leased as of June 30, 2015, representing number of homes that had a signed lease as of the last day of the period, not occupancy. Rent Growth. All figures represent rent growth for the three month period ended June 30, 2015. SWAY renewal rent growth includes rent growth from renewals and escalation clauses on multi-year leases. Retention. Resident Retention for the quarter ended June 30, 2015, excludes 1,436 homes that were not intended to be held for the long term. Synergies. Expected synergies of $40-50MM are inclusive of elimination of external management fee due to internalization, net of expenses and exclude any potential Prop.13 tax impact and one-time expenses such as severance, office lease termination cost, etc. Estimated property-level synergies are shown as a percent of 2Q 2015 pro forma annualized revenue. Top 10 Markets. Refers to the ten markets with the greatest number of homes for each company. SWAY, the Combined Company, and SFR peers do not have the same top 10 market composition. The Combined Company’s top ten markets are Atlanta (includes Gainesville), Tampa Bay (includes Sarasota), Miami, Southern California (consists of Los Angeles, Riverside, San Diego and Ventura), Houston, Dallas, Denver (includes Greeley, Boulder and Colorado Springs), Las Vegas, Orlando (includes Daytona Beach and Winter Haven) and Phoenix. 15

Legal References In connection with the proposed transaction, SWAY expects to file a proxy statement with the SEC. SWAY also plans to file other relevant documents with the SEC regarding the proposed transaction. INVESTORS ARE URGED TO READ THE PROXY STATEMENT AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IF AND WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. You may obtain a free copy of the proxy statement (if and when it becomes available) and other relevant documents filed by SWAY with the SEC at the SEC’s website at www.sec.gov. Copies of the documents filed by SWAY with the SEC will be available free of charge on SWAY’s website at www.starwoodwaypoint.com or by contacting SWAY Investor Relations at 510-987-8308. SWAY and CAH and their respective trustees and executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. You can find information about SWAY’s executive officers and trustees in SWAY’s definitive annual proxy statement filed with the SEC on April 3, 2015. Additional information regarding the interests of such potential participants will be included in the proxy statement and other relevant documents filed with the SEC if and when they become available. You may obtain free copies of these documents from SWAY using the sources indicated above. This document shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended.