Attached files

| file | filename |

|---|---|

| EX-4.18 - EXHIBIT 4.18 - Eloxx Pharmaceuticals, Inc. | v420584_ex4-18.htm |

| EX-31.1 - EXHIBIT 31.1 - Eloxx Pharmaceuticals, Inc. | v420584_ex31-1.htm |

| EX-32.1 - EXHIBIT 32.1 - Eloxx Pharmaceuticals, Inc. | v420584_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Eloxx Pharmaceuticals, Inc. | v420584_ex31-2.htm |

| EX-10.5 - EXHIBIT 10.5 - Eloxx Pharmaceuticals, Inc. | v420584_ex10-5.htm |

| EX-32.2 - EXHIBIT 32.2 - Eloxx Pharmaceuticals, Inc. | v420584_ex32-2.htm |

| EX-23.1 - EXHIBIT 23.1 - Eloxx Pharmaceuticals, Inc. | v420584_ex23-1.htm |

| EX-10.20 - EXHIBIT 10.20 - Eloxx Pharmaceuticals, Inc. | v420584_ex10-20.htm |

| EX-10.21 - EXHIBIT 10.21 - Eloxx Pharmaceuticals, Inc. | v420584_ex10-21.htm |

| EX-10.4 - EXHIBIT 10.4 - Eloxx Pharmaceuticals, Inc. | v420584_ex10-4.htm |

| EX-10.22 - EXHIBIT 10.22 - Eloxx Pharmaceuticals, Inc. | v420584_ex10-22.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the fiscal year ended June 30, 2015

OR

| ¨ | TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the transition period from ___________ to _____________ |

Commission file number: 001-31326

| SEVION THERAPEUTICS, INC. |

| (Exact name of registrant as specified in its charter) |

| Delaware | 84-1368850 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 4045 Sorrento Valley Boulevard, San Diego, CA | 92121 | |

| (Address of principal executive offices) | (Zip Code) |

| (858) 909-0749 |

| (Registrant’s telephone number, including area code) |

Securities registered under Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| None |

Securities registered under Section 12(g) of the Act:

Common Stock, $0.01 par value per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act . Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “accelerated filer”, “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer ¨ |

| Non-accelerated filer ¨ | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of December 31, 2014, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $9,102,633, based on the closing sales price as reported on the OTCQB Marketplace on that date.

The number of shares outstanding of each of the registrant's classes of common stock, as of September 15, 2015:

| Class | Number of Shares | ||

| Common Stock, $0.01 par value | 20,389,809 | ||

| Preferred Stock, $0.01 par value | 235,384 |

TABLE OF CONTENTS

- i -

PART I

| Item 1. | Business. |

Our Business

On September 29, 2014, we changed our name from Senesco Technologies, Inc. to Sevion Therapeutics, Inc.

The primary business of Sevion Therapeutics, Inc., a Delaware corporation incorporated in 1999, and its wholly-owned subsidiaries, Senesco, Inc., a New Jersey corporation incorporated in 1998, and Fabrus, Inc., a Delaware corporation incorporated in 2011, collectively referred to as “Sevion,” “we,” “us” or “our,” is to build and develop a portfolio of innovative therapeutics, from both internal discovery and acquisition, for the treatment of cancer and immunological diseases. The Company’s product candidates are derived from multiple key proprietary technology platforms, such as: cell-based arrayed antibody discovery, ultralong antibody scaffolds and Chimerasome nanocages.

Antibody Technology

Antibody Genes - We believe our antibody platforms have broad applicability to human health by allowing the discovery of unique monoclonal antibodies against difficult membrane targets in several therapeutic areas. Our antibody therapeutic candidates target the Kv1.3 ion channel, which is important in the pathogenesis of several autoimmune and inflammatory disorders. Other antibodies in our pipeline target important cell surface molecules involved in cancer progression.

Antibody Discovery Technology - Traditional antibody drug discovery methods, such as phage/yeast display or immunization, rely on competitive selection from a pool of antibodies to identify a lead therapeutic candidate. In these methods, a mixture of antibodies compete for binding to a purified target, and the antibody molecules that bind the strongest to the target, referred to as high affinity, are ultimately discovered. While these approaches have led to many successful antibody therapeutics, there are at least two drawbacks. First, the drug targets have been limited to only those proteins which can be easily purified. Many important target classes, including multispanning membrane proteins, cannot be easily purified in functional form. Secondly, when discovery is driven by selection based on competitive binding and affinity, the result is a significant limitation in the number of functional lead antibodies. However, the highest affinity antibody isn’t always the best therapeutic because lower affinity molecules may have unique activities or lower toxicities than the highest affinity binder. Thus, modulating a pathway more subtly to treat disease is often preferable to affecting it in a binary fashion through competition related to high-affinity binding. We believe the technology to identify (i) antibodies against unpurified targets, particularly multispanning membrane proteins like G Protein Coupled Receptors, or GPCR’s, and ion channels, and (ii) a range of antibodies with different affinities and activities will enable us to discover new antibody drug leads compared to existing technologies.

We have developed the world’s first “spatially addressed” antibody library with an expansive combinatorial collection of recombinant antibodies in which each well contains a single species of antibody of known concentration, composition and sequence. Our spatially addressed library allows us to evaluate the therapeutic potential of each antibody individually in a non-competitive way and allows direct discovery on the cell surface. This approach is more analogous to traditional small molecule drug discovery and allows us to screen antibodies for functional drug activity as opposed to simple binding properties. This next generation discovery system unlocks epitopes, targets, and functions that are only identifiable in the context of a living cell.

| 1 |

Modified Cow Antibodies - Despite the enormous diversity of the antibody repertoire, human antibodies all have a similar geometry, shape and binding mode. Our scientists have discovered and humanized a novel class of therapeutic antibodies derived from cows that have a highly unusual structure for binding targets. This unique ultralong Complementary Determining Region 3, or CDR3, structural domain found in cow antibodies is comprised of a knob on a stalk that protrudes far from the antibody surface, creating the potential for entirely new types of therapeutic functionality. Using both our humanized spatially addressed antibody library and direct engineering of the knob, we are exploring the ability of utilizing the knob and stalk structure to functionally interact with important therapeutic targets, including GPCRs, ion channels and other multispanning membrane therapeutic targets on the cell surface. Our lead antibody, SVN001, was derived from these efforts.

Antibody Drug Candidates – We have created functional antibodies that modulate GPCRs and ion channels, two classes of targets that have proven difficult to address using conventional antibody discovery approaches.

SVN001 is an ion channel blocking antibody that is potentially the first therapeutic antibody against this target class. SVN001 targets an ion channel, Kv1.3, which has been implicated in a number of different autoimmune disorders including rheumatoid arthritis, psoriasis and multiple sclerosis. By targeting a unique subset of immune cells, SVN001 is not believed to be broadly immunosuppressive, therefore potentially improving the safety profile compared to typical immunosuppressants.

SVN002 is a unique antibody against an oncology target that holds the potential to significantly impact highly metastatic tumors that are resistant to the class of drugs that target vascular endothelial growth factor, or VEGF. The target is highly expressed in clear cell renal carcinoma, where it is associated with poor prognosis.

Other Antibodies

We have discovered fully human antibodies against additional oncology targets, including ErbB2, ErbB3, CXCR4, and GLP1R which have been engineered to have activity in in vitro systems. These cell surface proteins are validated, therapeutically high value targets in the disease fields of oncology and diabetes. Additionally, we have early stage antibodies against other undisclosed targets which were derived from our addressed library platform.

Research Program

We were advancing SVN001 through preclinical development where it has demonstrated potent activity as well as advancing SVN002 through preclinical development. However, given the Company’s limited capital resources, in December 2014, we decided to temporarily reduce our research and development spending on our antibody program until we are able to consummate a strategic transaction or a financing transaction.

| 2 |

On December 18, 2014, we entered into a Collaboration Agreement with CNA Development, LLC, an affiliate of Janssen Pharmaceuticals, Inc., or Janssen, to discover antibodies using our spatially addressed library platform. The collaboration, facilitated by the Johnson & Johnson Innovation Center in California, will include discovery of antibodies against multiple targets in several therapeutic areas. We and Janssen will jointly conduct research on antibodies discovered by us, and Janssen will have an option to an exclusive license to develop, manufacture, and commercialize candidates resulting from the collaboration. Under the terms of the agreement, we will receive an up-front payment and research support payments for activities conducted in collaboration with Janssen. For candidates licensed by Janssen, we would be eligible to receive payments upon the achievement of certain development and commercial milestones potentially totaling up to $125 million as well as low single digit royalties on product sales.

In order to pursue the above research initiatives, as well as other research initiatives that may arise, we will use our cash reserves. However, it will be necessary for us to raise a significant amount of additional working capital in the future. If we are unable to raise the necessary funds, we may be required to significantly curtail the future development of some or all of our research initiatives and we will be unable to pursue other possible research initiatives.

We may further expand our research and development program beyond the initiatives listed above to include other diseases and research centers.

Intellectual Property

We continue to develop our intellectual property internally and by in-licensing certain intellectual property related to our antibody platforms and our chimerasome technology.

Prior to the fourth quarter of fiscal 2015, certain patent related costs were capitalized. We concluded, based on historical write offs of patent cost, that the future beneficial value of our patent assets were uncertain and as such made a change to our accounting policy. This change is considered a change in estimate for accounting purposes and is reflected on a prospective basis beginning in the fourth quarter of fiscal 2015.

Government Regulation

Our ongoing preclinical research with cell lines and lab animal models of human disease is not currently subject to the FDA requirements that govern clinical trials. Generally, the FDA must approve any drug or biologic product before it can be marketed in the United States. In addition, prior to being sold outside of the United States, any product candidates must be approved by the regulatory agencies of foreign governments. Prior to filing a new drug application or biologics license application with the FDA, we would have to perform extensive clinical trials, and prior to beginning any clinical trial, we need to perform extensive preclinical testing which could take several years and may require substantial expenditures.

Employees

We have nine (9) employees, three (3) of whom are executive officers and who are involved in our management and we also have five (5) consultants.

We may contract research to university laboratories or to other companies in order to advance the development of our technology.

| 3 |

Safe Harbor Statement

The statements contained in this Annual Report on Form 10-K that are not historical facts are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. Such forward-looking statements may be identified by, among other things, the use of forward-looking terminology such as “believes,” “expects,” “may,” “will,” “should,” or “anticipates” or the negative thereof or other variations thereon or comparable terminology, or by discussions of strategy that involve risks and uncertainties. In particular, our statements regarding the anticipated growth in the markets for our technologies, the continued advancement of our research, the approval of our patent applications, the successful implementation of our commercialization strategy, including the success of our product candidates, statements relating to our patent applications, the anticipated long term growth of our business, the results of our preclinical or clinical studies, if any, the quotation of the Company’s common stock on an over-the-counter securities market, and the timing of the projects and trends in future operating performance are examples of such forward-looking statements. The forward-looking statements include risks and uncertainties, including, but not limited to, our ability to continue as a going concern, our limited operating history, our need for additional capital to fund our operations until we are able to generate a profit, the current economic environment, our outsourcing of our research and development activities, our significant future capital needs, our dependence on our patents and proprietary rights and the enforcement of these rights, the potential for our competitors or third parties to allege that we are infringing upon their intellectual property rights, the potential that our security measures may not adequately protect our unpatented technology, potential difficulty in managing our growth and expanding our operations, our lack of marketing or sales history and dependence on third-party marketing partners, our potential future dependence on joint ventures and strategic alliances to develop and market our technology, the intense competition in the biotechnology industry, the various government regulations that our business is subject to, the potential that our preclinical studies of our product candidates may be unsuccessful, any inability to license from third parties their proprietary technologies or processes which we use in connection with the development of our technology, the length, expense and uncertainty associated with future clinical trials for our product candidates, the potential that, even if we receive regulatory approval, consumers may not accept products containing our technology, our dependence on key personnel, the potential that certain provisions of our charter, by-laws and Delaware law could make a takeover difficult, political and social turmoil, the potential that our management and other affiliates, due to their significant control of our common stock have the ability to significantly influence our actions, the potential that a significant portion of our total outstanding shares of common stock may be sold in the market in the near future, the limited trading market of our common stock, fluctuations in the market price of our common stock, our dividend policy and potential for our stockholders to be diluted.

| 4 |

| ITEM 1A: | Risk Factors |

The more prominent risks and uncertainties inherent in our business are described below. However, additional risks and uncertainties may also impair our business operations. If any of the following risks actually occur, our business, financial condition or results of operations may suffer.

Risks Related to Our Business

Recurring losses and negative cash flows from operations raise substantial doubt about our ability to continue as a going concern and we may not be able to continue as a going concern.

Our recurring losses from operations and negative cash flows from operations raise substantial doubt about our ability to continue as a going concern and as a result, our independent registered public accounting firm included an explanatory paragraph in its report on our consolidated financial statements for the fiscal year ended June 30, 2015. Substantial doubt about our ability to continue as a going concern may create negative reactions to the price of the common shares of our stock and we may have a more difficult time obtaining financing.

We have prepared our financial statements on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. The financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts or amounts of liabilities that might be necessary should we be unable to continue in existence.

Based on the cash on hand as of June 30, 2015 and the aggregate net proceeds from the issuance of preferred stock, common stock and warrants on July 27, 2015, we believe we have enough cash to fund operations through at least June 30, 2016.

We have a limited operating history and have incurred substantial losses and expect to incur future losses.

We are a development stage biotechnology company with a limited operating history and limited assets and capital. We have incurred losses each year since inception and had an accumulated deficit of $107,182,976 at June 30, 2015. We have generated minimal revenues by licensing our technology for certain crops to companies willing to share in our development costs. In addition, our technology may not be ready for commercialization for several years. We expect to continue to incur losses for the next several years because we anticipate that our expenditures on research and development and administrative activities will significantly exceed our revenues during that period. We cannot predict when, if ever, we will become profitable.

We will need additional capital to fund our operations until we are able to generate a profit.

Our operations to date have required significant cash expenditures. Our future capital requirements will depend on the results of our research and development activities, preclinical and clinical studies, and competitive and technological advances.

| 5 |

We will need to obtain more funding in the future through collaborations or other arrangements with research institutions and corporate partners, or public and private offerings of our securities, including debt or equity financing. We may not be able to obtain adequate funds for our operations from these sources when needed or on acceptable terms. Future collaborations or similar arrangements may require us to license valuable intellectual property to, or to share substantial economic benefits with, our collaborators. If we raise additional capital by issuing additional equity or securities convertible into equity, our stockholders may experience dilution and our share price may decline. Any debt financing may result in restrictions on our spending.

If we are unable to raise additional funds, we will need to do one or more of the following:

| · | delay, scale-back or eliminate some or all of our research and product development programs; |

| · | provide licenses to third parties to develop and commercialize products or technologies that we would otherwise seek to develop and commercialize ourselves; |

| · | seek strategic alliances or business combinations; |

| · | attempt to sell our company; |

| · | cease operations; or |

| · | declare bankruptcy. |

Based on the cash on hand as of June 30, 2015 and the aggregate net proceeds from the issuance of preferred stock, common stock and warrants on July 27, 2015, we believe we have enough cash to fund operations through at least June 30, 2016.

We may be adversely affected by the current economic environment.

Our ability to obtain financing, invest in and grow our business, and meet our financial obligations depends on our operating and financial performance, which in turn is subject to numerous factors. In addition to factors specific to our business, prevailing economic conditions and financial, business and other factors beyond our control can also affect our business and ability to raise capital. We cannot anticipate all of the ways in which the current economic climate and financial market conditions could adversely impact our business.

Materials necessary to manufacture some of our compounds currently under development may not be available on commercially reasonable terms, or at all, which may delay our development and commercialization of these compounds.

Some of the materials necessary for the manufacture of our compounds under development may, from time to time, be available either in limited quantities, or from a limited number of manufacturers, or both. Our contract manufacturers need to obtain these materials for our preclinical and clinical trials and, potentially, for commercial distribution when and if we obtain marketing approval for these compounds. Suppliers may not sell us these materials at the time we need them or on commercially reasonable terms. If we are unable to obtain the materials needed to conduct our preclinical and clinical trials, product testing and potential regulatory approval could be delayed, adversely affecting our ability to develop the product candidates. Similarly, if we are unable to obtain critical manufacturing materials after regulatory approval has been obtained for a product candidate, the commercial launch of that product candidate could be delayed or there could be a shortage in supply, which could materially affect our ability to generate revenues from that product candidate. If suppliers increase the price of manufacturing materials, the price for one or more of our products may increase, which may make our products less competitive in the marketplace. If it becomes necessary to change suppliers for any of these materials or if any of our suppliers experience a shutdown or disruption at the facilities used to produce these materials, due to technical, regulatory or other reasons, it could harm our ability to manufacture our products.

| 6 |

We depend on a limited number of technologies and, if our technologies are not commercially successful, we will have no alternative source of revenue.

Our primary business is the development and licensing of technology to discover and engineer monoclonal antibodies. Our future revenue and profitability critically depend upon our ability, or our licensees’ ability, to successfully develop apoptosis and senescence gene technology and later license or market such technology. We have conducted certain preliminary cell-line and animal experiments, which have provided us with data upon which we have designed additional research programs. However, we cannot give any assurance that our technology will be commercially successful or economically viable for any therapeutic applications.

In addition, no assurance can be given that adverse consequences might not result from the use of our technology such as the development of negative effects on patients that receive our product candidates. Our failure to obtain market acceptance of our technology or the failure of our current or potential licensees to successfully commercialize such technology would have a material adverse effect on our business.

We outsource much of our research and development activities and, if we are unsuccessful in maintaining our alliances with these third parties, our research and development efforts may be delayed or curtailed.

We rely on third parties to perform much of our research and development activities. At this time, we have limited internal capabilities to perform our own research and development activities. Accordingly, the failure of third party research partners to perform under agreements entered into with us, or our failure to renew important research agreements with these third parties, may delay or curtail our research and development efforts.

We have significant future capital needs and may be unable to raise capital when needed, which could force us to delay or reduce our research and development efforts.

As of June 30, 2015, we had a cash balance of $3,334,626 and working capital of $2,951,210. Using our available reserves as of June 30, 2015, and the aggregate net proceeds from the issuance of preferred stock, common stock and warrants on July 27, 2015, we believe that we can operate according to our current business plan at least through June 30, 2016.

To date, we have generated minimal revenues and anticipate that our operating costs will exceed any revenues generated over the next several years. Therefore, we will be required to raise additional capital in the future in order to operate in accordance with our current business plan, and this funding may not be available on favorable terms, if at all. If we are unable to raise additional funds, we will need to do one or more of the following:

| · | delay, scale back or eliminate some or all of our research and development programs; |

| · | provide a license to third parties to develop and commercialize our technology that we would otherwise seek to develop and commercialize ourselves; |

| · | seek strategic alliances or business combinations; |

| · | attempt to sell our company; |

| · | cease operations; or |

| · | declare bankruptcy. |

| 7 |

Investors may experience dilution in their investment from future offerings of our common stock. For example, if we raise additional capital by issuing equity securities, such an issuance would reduce the percentage ownership of existing stockholders. In addition, assuming the exercise of all options and warrants outstanding and the conversion of the preferred stock into common stock, as of June 30, 2015, we had 461,262,961 shares of common stock authorized but unissued and unreserved, which may be issued from time to time by our board of directors. Furthermore, we may need to issue securities that have rights, preferences and privileges senior to our common stock. Failure to obtain financing on acceptable terms would have a material adverse effect on our liquidity.

Since our inception, we have financed all of our operations through equity and debt financings. Our future capital requirements depend on numerous factors, including:

| · | the scope of our research and development; |

| · | our ability to attract business partners willing to share in our development costs; |

| · | our ability to successfully commercialize our technology; |

| · | competing technological and market developments; |

| · | our ability to enter into collaborative arrangements for the development, regulatory approval and commercialization of other products; and |

| · | the cost of filing, prosecuting, defending and enforcing patent claims and other intellectual property rights. |

Our business depends upon our patents and proprietary rights and the enforcement of these rights. Our failure to obtain and maintain patent protection may increase competition and reduce demand for our technology.

As a result of the substantial length of time and expense associated with developing products and bringing them to the marketplace in the biotechnology industry, obtaining and maintaining patent and trade secret protection for technologies, products and processes is of vital importance. Our success will depend in part on several factors, including, without limitation:

| · | our ability to obtain patent protection for our technologies and processes; |

| · | our ability to preserve our trade secrets; and |

| · | our ability to operate without infringing the proprietary rights of other parties both in the United States and in foreign countries. |

Our success depends in part upon the grant of patents from our pending patent applications. In addition, we have licensed certain antibody technology from The Scripps Research Institute, or Scripps, pursuant to a license agreement dated August 8, 2014. If we are in breach of this license agreement, and Scripps elects to terminate the agreement, this termination could have a material adverse effect to our business in the future.

Although we believe that our technology is unique and that it will not violate or infringe upon the proprietary rights of any third party, we cannot assure you that these claims will not be made or if made, could be successfully defended against. If we do not obtain and maintain patent protection, we may face increased competition in the United States and internationally, which would have a material adverse effect on our business.

Since patent applications in the United States are maintained in secrecy until patents are issued, and since publication of discoveries in the scientific and patent literature tend to lag behind actual discoveries by several months, we cannot be certain that we were the first creator of the inventions covered by our pending patent applications or that we were the first to file patent applications for these inventions.

| 8 |

In addition, among other things, we cannot assure you that:

| · | our patent applications will result in the issuance of patents; |

| · | any patents issued or licensed to us will be free from challenge and if challenged, would be held to be valid; |

| · | any patents issued or licensed to us will provide commercially significant protection for our technology, products and processes; |

| · | other companies will not independently develop substantially equivalent proprietary information which is not covered by our patent rights; |

| · | other companies will not obtain access to our know-how; |

| · | other companies will not be granted patents that may prevent the commercialization of our technology; or |

| · | we will not incur licensing fees and the payment of significant other fees or royalties to third parties for the use of their intellectual property in order to enable us to conduct our business. |

Our competitors may allege that we are infringing upon their intellectual property rights, forcing us to incur substantial costs and expenses in resulting litigation, the outcome of which would be uncertain.

Patent law is still evolving relative to the scope and enforceability of claims in the fields in which we operate. We are like most biotechnology companies in that our patent protection is highly uncertain and involves complex legal and technical questions for which legal principles are not yet firmly established. In addition, if issued, our patents may not contain claims sufficiently broad to protect us against third parties with similar technologies or products, or provide us with any competitive advantage.

The PTO and the courts have not established a consistent policy regarding the breadth of claims allowed in biotechnology patents. The allowance of broader claims may increase the incidence and cost of patent interference proceedings and the risk of infringement litigation. On the other hand, the allowance of narrower claims may limit the scope and value of our proprietary rights.

The laws of some foreign countries do not protect proprietary rights to the same extent as the laws of the United States, and many companies have encountered significant problems and costs in protecting their proprietary rights in these foreign countries.

We could become involved in infringement actions to enforce and/or protect our patents. Regardless of the outcome, patent litigation is expensive and time consuming and would distract our management from other activities. Some of our competitors may be able to sustain the costs of complex patent litigation more effectively than we could because they have substantially greater resources. Uncertainties resulting from the initiation and continuation of any patent litigation could limit our ability to continue our operations.

If our technology infringes the intellectual property of our competitors or other third parties, we may be required to pay license fees or damages.

If any relevant claims of third party patents that are adverse to us are upheld as valid and enforceable, we could be prevented from commercializing our technology or could be required to obtain licenses from the owners of such patents. We cannot assure you that such licenses would be available or, if available, would be on acceptable terms. Some licenses may be non-exclusive and, therefore, our competitors may have access to the same technology licensed to us. In addition, if any parties successfully claim that the creation or use of our technology infringes upon their intellectual property rights, we may be forced to pay damages, including treble damages.

| 9 |

Our security measures may not adequately protect our unpatented technology and, if we are unable to protect the confidentiality of our proprietary information and know-how, the value of our technology may be adversely affected.

Our success depends upon know-how, unpatentable trade secrets, and the skills, knowledge and experience of our scientific and technical personnel. We require all employees to disclose and assign to us the rights to their ideas, developments, discoveries and inventions. All of the current employees have also entered into Non-disclosure, Non-competition and Invention Assignment Agreements. We also attempt to enter into similar agreements with our consultants, advisors and research collaborators. We cannot assure you that adequate protection for our trade secrets, know-how or other proprietary information against unauthorized use or disclosure will be available.

We occasionally provide information to research collaborators in academic institutions and request that the collaborators conduct certain tests. We cannot assure you that the academic institutions will not assert intellectual property rights in the results of the tests conducted by the research collaborators, or that the academic institutions will grant licenses under such intellectual property rights to us on acceptable terms, if at all. If the assertion of intellectual property rights by an academic institution is substantiated, and the academic institution does not grant intellectual property rights to us, these events could limit our ability to commercialize our technology.

As we evolve from a company primarily involved in the research and development of our technology into one that is also involved in the commercialization of our technology, we may have difficulty managing our growth and expanding our operations.

As our business grows, we may need to add employees and enhance our management, systems and procedures. We may need to successfully integrate our internal operations with the operations of our marketing partners, manufacturers, distributors and suppliers to produce and market commercially viable products. We may also need to manage additional relationships with various collaborative partners, suppliers and other organizations. Expanding our business may place a significant burden on our management and operations. We may not be able to implement improvements to our management information and control systems in an efficient and timely manner and we may discover deficiencies in our existing systems and controls. Our failure to effectively respond to such changes may make it difficult for us to manage our growth and expand our operations.

We have no marketing or sales history and depend on third party marketing partners. Any failure of these parties to perform would delay or limit our commercialization efforts.

We have no history of marketing, distributing or selling biotechnology products, and we are relying on our ability to successfully establish marketing partners or other arrangements with third parties to market, distribute and sell a commercially viable product both here and abroad. Our business plan envisions creating strategic alliances to access needed commercialization and marketing expertise. We may not be able to attract qualified sub-licensees, distributors or marketing partners, and even if qualified, these marketing partners may not be able to successfully market agricultural products or human therapeutic applications developed with our technology. If our current or potential future marketing partners fail to provide adequate levels of sales, our commercialization efforts will be delayed or limited and we may not be able to generate revenue.

| 10 |

We will depend on joint ventures and strategic alliances to develop and market our technology and, if these arrangements are not successful, our technology may not be developed and the expenses to commercialize our technology will increase.

In its current state of development, our technology is not ready to be marketed to consumers. We intend to follow a multi-faceted commercialization strategy that involves the licensing of our technology to business partners for the purpose of further technological development, marketing and distribution. We have and are seeking business partners who will share the burden of our development costs while our technology is still being developed, and who will pay us royalties when they market and distribute products incorporating our technology upon commercialization. The establishment of joint ventures and strategic alliances may create future competitors, especially in certain regions abroad where we do not pursue patent protection. If we fail to establish beneficial business partners and strategic alliances, our growth will suffer and the continued development of our technology may be harmed.

Competition in the human therapeutic industry is intense and technology is changing rapidly. If our competitors market their technology faster than we do, we may not be able to generate revenues from the commercialization of our technology.

There are many large companies working in the therapeutic antibody field and similarly may develop technologies related to antibody discovery. These companies include Genentech, Inc., Amgen, Inc., Biogen Idec, Inc., Novartis AG, Janssen Biotech, Inc., Sanofi-aventis U.S. LLC, Regeneron Pharmaceuticals, Inc., Bristol-Myers Squibb Company, Teva Pharmaceutical Industries Ltd, Pfizer, Inc., Takeda Pharmaceutical Company Limited, Kyawa Hokko Kirin Pharma, Inc., Daiichi Sankyo Company Limited, Astellas Pharma, Inc., Merck & Co. Inc., AbbVie, Inc., Seattle Genetics, Inc., and Immunogen, Inc. Similarly, there are several small companies developing technologies for antibody discovery, including Adimab LLC, X-body Biosciences, Inc., Innovative Targeting Solutions, Inc., Heptares Therapeutics Ltd, Kymab Ltd., and Novimmune SA. Other companies are working on unique scaffolds, including Ablynx NV and ArGen-X N.V.

We may be unable to compete successfully against our current and future competitors, which may result in price reductions, reduced margins and the inability to achieve market acceptance for products containing our technology. Many of these competitors have substantially greater financial, marketing, sales, distribution and technical resources than us and have more experience in research and development, clinical trials, regulatory matters, manufacturing and marketing. We anticipate increased competition in the future as new companies enter the market and new technologies become available. Our technology may be rendered obsolete or uneconomical by technological advances or entirely different approaches developed by one or more of our competitors, which will prevent or limit our ability to generate revenues from the commercialization of our technology.

| 11 |

Our business is subject to various government regulations and, if we or our licensees are unable to obtain regulatory approval, we may not be able to continue our operations.

Use of our technology, if developed for human therapeutic applications, is subject to FDA regulation. The FDA must approve any drug or biologic product before it can be marketed in the United States. In addition, prior to being sold outside of the United States, any of our product candidates must be approved by the regulatory agencies of foreign governments. Prior to filing a new drug application or biologics license application with the FDA, we would have to perform extensive clinical trials, and prior to beginning any clinical trial, we would need to perform extensive preclinical testing which could take several years and may require substantial expenditures.

We expect to perform clinical trials in connection with our product candidates, which are subject to FDA approval. Additionally, federal, state and foreign regulations relating to human therapeutic applications developed through biotechnology are subject to public concerns and political circumstances, and, as a result, regulations have changed and may change substantially in the future. Accordingly, we may become subject to governmental regulations or approvals or become subject to licensing requirements in connection with our research and development efforts. We may also be required to obtain such licensing or approval from the governmental regulatory agencies described above, or from state agencies, prior to the commercialization of our human therapeutic technology. If unfavorable governmental regulations are imposed on our technology or if we fail to obtain licenses or approvals in a timely manner, we may not be able to continue our operations.

Preclinical studies of our product candidates may be unsuccessful, which could delay or prevent regulatory approval.

Preclinical studies may reveal that one or more of our product candidates is ineffective or harmful, and/or may be unsuccessful in demonstrating efficacy and safety of our human therapeutic technology, which would significantly limit the possibility of obtaining regulatory approval for any drug or biologic product manufactured with our technology. The FDA requires submission of extensive preclinical, clinical and manufacturing data to assess the efficacy and safety of potential products. Any delay in receiving approval for any applicable IND from the FDA would result in a delay in the commencement of the related clinical trial. Additionally, we could be required to perform additional preclinical studies prior to the FDA approving any applicable IND. Furthermore, the success of preliminary studies does not ensure commercial success, and later-stage clinical trials may fail to confirm the results of the preliminary studies.

Our success will depend on the success of our clinical trials of our product candidates.

It may take several years to complete the clinical trials of a product, and failure of one or more of our clinical trials can occur at any stage of testing. We believe that the development of our product candidate involves significant risks at each stage of testing. If clinical trial difficulties and failures arise, our product candidate may never be approved for sale or become commercially viable.

There are a number of difficulties and risks associated with clinical trials. These difficulties and risks may result in the failure to receive regulatory approval to sell our product candidate or the inability to commercialize our product candidate. The possibility exists that:

| 12 |

| · | we may discover that the product candidate does not exhibit the expected therapeutic results in humans, may cause harmful side effects or have other unexpected characteristics that may delay or preclude regulatory approval or limit commercial use if approved; |

| · | the results from early clinical trials may not be statistically significant or predictive of results that will be obtained from expanded advanced clinical trials; |

| · | institutional review boards or regulators, including the FDA, may hold, suspend or terminate our clinical research or the clinical trials of our product candidate for various reasons, including noncompliance with regulatory requirements or if, in their opinion, the participating subjects are being exposed to unacceptable health risks; |

| · | subjects may drop out of our clinical trials; |

| · | our preclinical studies or clinical trials may produce negative, inconsistent or inconclusive results, and we may decide, or regulators may require us, to conduct additional preclinical studies or clinical trials; and |

| · | the cost of our clinical trials may be greater than we currently anticipate. |

Clinical trials for our product candidates will be lengthy and expensive and their outcome is uncertain.

Before obtaining regulatory approval for the commercial sales of any product containing our technology, we must demonstrate through clinical testing that our technology and any product containing our technology is safe and effective for use in humans. Conducting clinical trials is a time-consuming, expensive and uncertain process and typically requires years to complete. In our industry, the results from preclinical studies and early clinical trials often are not predictive of results obtained in later-stage clinical trials. Some products and technologies that have shown promising results in preclinical studies or early clinical trials subsequently fail to establish sufficient safety and efficacy data necessary to obtain regulatory approval. At any time during clinical trials, we or the FDA might delay or halt any clinical trial for various reasons, including:

| · | occurrence of unacceptable toxicities or side effects; |

| · | ineffectiveness of the product candidate; |

| · | negative or inconclusive results from the clinical trials, or results that necessitate additional studies or clinical trials; |

| · | delays in obtaining or maintaining required approvals from institutions, review boards or other reviewing entities at clinical sites; |

| · | delays in patient enrollment; or |

| · | insufficient funding or a reprioritization of financial or other resources. |

Any failure or substantial delay in successfully completing clinical trials and obtaining regulatory approval for our product candidates could severely harm our business.

| 13 |

If our clinical trials for our product candidates are delayed, we would be unable to commercialize our product candidates on a timely basis, which would materially harm our business.

Planned clinical trials may not begin on time or may need to be restructured after they have begun. Clinical trials can be delayed for a variety of reasons, including delays related to:

| · | obtaining an effective IND or regulatory approval to commence a clinical trial; |

| · | negotiating acceptable clinical trial agreement terms with prospective trial sites; |

| · | obtaining institutional review board approval to conduct a clinical trial at a prospective site; |

| · | recruiting qualified subjects to participate in clinical trials; |

| · | competition in recruiting clinical investigators; |

| · | shortage or lack of availability of supplies of drugs for clinical trials; |

| · | the need to repeat clinical trials as a result of inconclusive results or poorly executed testing; |

| · | the placement of a clinical hold on a study; |

| · | the failure of third parties conducting and overseeing the operations of our clinical trials to perform their contractual or regulatory obligations in a timely fashion; and |

| · | exposure of clinical trial subjects to unexpected and unacceptable health risks or noncompliance with regulatory requirements, which may result in suspension of the trial. |

We believe that our product candidates have significant milestones to reach, including the successful completion of clinical trials, before commercialization. If we have significant delays in or termination of clinical trials, our financial results and the commercial prospects for our product candidates or any other products that we may develop will be adversely impacted. In addition, our product development costs would increase and our ability to generate revenue could be impaired.

Any inability to license from third parties their proprietary technologies or processes which we use in connection with the development of our technology may impair our business.

Other companies, universities and research institutions have or may obtain patents that could limit our ability to use our technology in a product candidate or impair our competitive position. As a result, we would have to obtain licenses from other parties before we could continue using our technology in a product candidate. Any necessary licenses may not be available on commercially acceptable terms, if at all. If we do not obtain required licenses, we may not be able to develop our technology into a product candidate or we may encounter significant delays in development while we redesign methods that are found to infringe on the patents held by others.

| 14 |

We face potential product liability exposure far in excess of our limited insurance coverage.

We may be held liable if any product we or our collaborators develop causes injury or is found otherwise unsuitable during product testing, manufacturing, marketing or sale. Regardless of merit or eventual outcome, product liability claims could result in decreased demand for our product candidates, injury to our reputation, withdrawal of patients from our clinical trials, substantial monetary awards to trial participants and the inability to commercialize any products that we may develop. These claims might be made directly by consumers, health care providers, pharmaceutical companies or others selling or testing our products. We have obtained limited product liability insurance coverage for our clinical trials; however, our insurance may not reimburse us or may not be sufficient to reimburse us for expenses or losses we may suffer. Moreover, if insurance coverage becomes more expensive, we may not be able to maintain insurance coverage at a reasonable cost or in sufficient amounts to protect us against losses due to liability. If we obtain marketing approval for any of our product candidates, we intend to expand our insurance coverage to include the sale of commercial products, but we may be unable to obtain commercially reasonable product liability insurance for any products approved for marketing. On occasion, juries have awarded large judgments in class action lawsuits for claims based on drugs that had unanticipated side effects. In addition, the pharmaceutical and biotechnology industries, in general, have been subject to significant medical malpractice litigation. A successful product liability claim or series of claims brought against us could harm our reputation and business and would decrease our cash reserves.

We depend on our key personnel and, if we are not able to attract and retain qualified scientific and business personnel, we may not be able to grow our business or develop and commercialize our technology.

We are highly dependent on our scientific advisors, consultants and third-party research partners. Our success will also depend in part on the continued service of our key employees and our ability to identify, hire and retain additional qualified personnel in an intensely competitive market. Additionally, we do not have employment agreements with our key employees. We do not maintain key person life insurance on any member of management. The failure to attract and retain key personnel could limit our growth and hinder our research and development efforts.

If we are unable to successfully remediate the material weakness in our internal control over financial reporting, the accuracy and timing of our financial reporting may be adversely affected, which may adversely affect investor confidence in us and, as a result, the value of our common stock.

In connection with the audit of our fiscal year 2015 consolidated financial statements, our auditors noted a material weakness in our internal controls, principally relating to the review of the accounting and calculation surrounding our equity-linked financial instruments. A material weakness is a deficiency or combination of deficiencies in internal control over financial reporting that results in more than reasonable possibility that a material misstatement of annual or interim financial statements will not be prevented or detected on a timely basis. We cannot assure that any measures that we take to correct this material weakness will fully remediate the deficiencies or material weakness described above. We also cannot assure you that we have identified all of our existing significant deficiencies and material weaknesses, or that we will not in the future have additional significant deficiencies or material weaknesses.

Certain provisions of our charter, by-laws, Delaware law and stock plans could make a takeover difficult.

Certain provisions of our certificate of incorporation and by-laws could make it more difficult for a third party to acquire control of us, even if the change in control would be beneficial to stockholders. Our certificate of incorporation authorizes our board of directors to issue, without stockholder approval, 5,000,000 shares of preferred stock with voting, conversion and other rights and preferences that could adversely affect the voting power or other rights of the holders of our common stock.

| 15 |

In addition, we are subject to the Business Combination Act of the Delaware General Corporation Law which, subject to certain exceptions, restricts certain transactions and business combinations between a corporation and a stockholder owning 15% or more of the corporation’s outstanding voting stock for a period of three years from the date such stockholder becomes a 15% owner. These provisions may have the effect of delaying or preventing a change of control of us without action by our stockholders and, therefore, could adversely affect the value of our common stock.

Furthermore, in the event of our merger or consolidation with or into another corporation, or the sale of all or substantially all of our assets in which the successor corporation does not assume our outstanding equity awards or issue equivalent equity awards, our current equity plans require the accelerated vesting of such outstanding equity awards.

| 16 |

Risks Related to Our Common Stock

Penny stock regulations may impose certain restrictions on marketability of our securities.

The SEC has adopted regulations which generally define a “penny stock” to be any equity security that has a market price of less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. As a result, our common stock is subject to rules that impose additional sales practice requirements on broker dealers who sell such securities to persons other than established customers and accredited investors (generally those with assets in excess of $1,000,000 or annual income exceeding $200,000, or $300,000 together with their spouse). For transactions covered by such rules, the broker dealer must make a special suitability determination for the purchase of such securities and have received the purchaser’s written consent to the transaction prior to the purchase. Additionally, for any transaction involving a penny stock, unless exempt, the rules require the delivery, prior to the transaction, of a risk disclosure document mandated by the SEC relating to the penny stock market. The broker dealer must also disclose the commission payable to both the broker dealer and the registered representative, current quotations for the securities and, if the broker dealer is the sole market maker, the broker dealer must disclose this fact and the broker dealer’s presumed control over the market.

Finally, monthly statements must be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks. Broker-dealers must wait two business days after providing buyers with disclosure materials regarding a security before effecting a transaction in such security. Consequently, the “penny stock” rules restrict the ability of broker dealers to sell our securities and affect the ability of investors to sell our securities in the secondary market and the price at which such purchasers can sell any such securities, thereby affecting the liquidity of the market for our common stock.

Stockholders should be aware that, according to the SEC, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. Such patterns include:

| · | control of the market for the security by one or more broker-dealers that are often related to the promoter or issuer; |

| · | manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases; |

| · | “boiler room” practices involving high pressure sales tactics and unrealistic price projections by inexperienced sales persons; |

| · | excessive and undisclosed bid-ask differentials and markups by selling broker-dealers; and |

| · | the wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the inevitable collapse of those prices with consequent investor losses. |

Our management is aware of the abuses that have occurred historically in the penny stock market.

| 17 |

Our management and other affiliates have significant control of our common stock and could significantly influence our actions in a manner that conflicts with our interests and the interests of other stockholders.

As of June 30, 2015, our executive officers and directors together beneficially own approximately 21% of the outstanding shares of our common stock, assuming the exercise of options and warrants which are currently exercisable or will become exercisable within 60 days of June 30, 2015, held by these stockholders. Additionally, there are four shareholders that each beneficially own more than 5% of the outstanding shares of our common stock. As a result, these stockholders, acting together, will be able to exercise significant influence over matters requiring approval by our stockholders, including the election of directors, and may not always act in the best interests of other stockholders. Such a concentration of ownership may have the effect of delaying or preventing a change in control of us, including transactions in which our stockholders might otherwise receive a premium for their shares over then-current market prices.

A significant portion of our total outstanding shares of common stock may be sold in the market in the near future, which could cause the market price of our common stock to drop significantly.

As of June 30, 2015, we had 18,752,813 shares of our common stock issued and outstanding, 380 shares of Series A convertible preferred stock outstanding which can convert into 506,666 shares of common stock and 235,837 shares of Series C convertible preferred stock outstanding which can convert into 2,358,370 shares of common stock. As of June 30, 2015, all of our outstanding shares of common stock are registered pursuant to registration statements on Forms S-1 or S-3 or are either eligible to be sold under Rule 144 of the Securities Act of 1933, as amended, or are in the public float. In addition, we have registered 1,876,722 shares of our common stock underlying warrants previously issued and still outstanding and we registered 4,917,670 shares of our common stock underlying options granted or to be granted under our stock option plans. Consequently, sales of substantial amounts of our common stock in the public market, or the perception that such sales could occur, may have a material adverse effect on our stock price.

Our common stock has a limited trading market, which could limit your ability to resell your shares of common stock at or above your purchase price.

Our common stock is currently quoted on the OTCQB Marketplace, operated by the OTC Markets Group, or OTCQB, and our common stock currently has a limited trading market. We cannot assure you that an active trading market will develop or, if developed, will be maintained. As a result, our stockholders may find it difficult to dispose of shares of our common stock and, as a result, may suffer a loss of all or a substantial portion of their investment.

The market price of our common stock may fluctuate and may drop below the price you paid.

We cannot assure you that you will be able to resell the shares of our common stock at or above your purchase price. The market price of our common stock may fluctuate significantly in response to a number of factors, some of which are beyond our control. These factors include:

| · | quarterly variations in operating results; |

| 18 |

| · | the progress or perceived progress of our research and development efforts; |

| · | changes in accounting treatments or principles; |

| · | announcements by us or our competitors of new technology, product and service offerings, significant contracts, acquisitions or strategic relationships; |

| · | additions or departures of key personnel; |

| · | future offerings or resales of our common stock or other securities; |

| · | stock market price and volume fluctuations of publicly-traded companies in general and development companies in particular; and |

| · | general political, economic and market conditions. |

For example, during the fiscal year ended June 30, 2015, our common stock traded between $0.51 and $2.88 per share.

Because we do not intend to pay, and have not paid, any cash dividends on our shares of common stock, our stockholders will not be able to receive a return on their shares unless the value of our common stock appreciates and they sell their shares.

We have never paid or declared any cash dividends on our common stock, and we intend to retain any future earnings to finance the development and expansion of our business. We do not anticipate paying any cash dividends on our common stock in the foreseeable future. Therefore, our stockholders will not be able to receive a return on their investment unless the value of our common stock appreciates and they sell their shares.

Our stockholders may experience substantial dilution as a result of the conversion of convertible preferred stock, the exercise of options and warrants to purchase our common stock, or due to anti-dilution provisions relating to any on the foregoing.

As of June 30, 2015, we have outstanding 380 shares of Series A convertible preferred stock which may convert into 506,666 shares of common stock, 235,837 shares of Series C convertible preferred stock outstanding which can convert into 2,358,370 shares of common stock and warrants to purchase 7,332,776 shares of our common stock. In addition, as of June 30, 2015, we have reserved 4,917,670 shares of our common stock for issuance upon the exercise of options granted or available to be granted pursuant to our stock option plan, all of which may be granted in the future. Furthermore, in connection with the preferred stock agreements, we are required to reserve an additional 4,868,740 shares of common stock. The conversion of the convertible preferred stock and the exercise of these options and warrants will result in dilution to our existing stockholders and could have a material adverse effect on our stock price. The conversion price of the convertible preferred stock is also subject to certain anti-dilution adjustments.

| 19 |

| Item 1B. | Unresolved Staff Comments. |

None.

| Item 2. | Properties. |

Effective October 10, 2014, we lease office space in San Diego, California for a current monthly rental fee of $22,728. The lease expires on October 31, 2016. The office and laboratory space is in good condition, and we believe they will adequately serve as our headquarters and laboratory over the term of the lease. We also believe that the office and laboratory space is adequately insured by the lessors.

| Item 3. | Legal Proceedings. |

We are not currently a party to any legal proceedings; however, we may become involved in various claims and legal actions arising in the ordinary course of business.

| Item 4. | Mine Safety Disclosures. |

None.

| 20 |

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Our common stock currently trades on the OTCQB Marketplace under the symbol SVON.

The following table sets forth, for each of the quarters since the quarter ended September 30, 2013, the range of the high and low bid information for our common shares quoted on the OTCQB Marketplace. The prices in the table represent prices between dealers and do not include adjustments for retail mark-up, markdown or commission and may not represent actual transactions.

| Quarter Ended | Common Stock | |||||||

| High | Low | |||||||

| September 30, 2013 | $ | 7.00 | $ | 1.90 | ||||

| December 31, 2013 | $ | 6.35 | $ | 3.00 | ||||

| March 31, 2014 | $ | 6.09 | $ | 3.03 | ||||

| June 30, 2014 | $ | 3.69 | $ | 2.40 | ||||

| September 30, 2014 | $ | 2.88 | $ | 1.28 | ||||

| December 31, 2014 | $ | 1.60 | $ | 0.51 | ||||

| March 31, 2015 | $ | 0.90 | $ | 0.51 | ||||

| June 30, 2015 | $ | 1.57 | $ | 0.63 | ||||

As of September 15, 2015, the approximate number of holders of record of our common stock was 171. This number does not include “street name” or beneficial holders, whose shares are held of record by banks, brokers and other financial institutions.

We have neither paid nor declared dividends on our common stock since our inception, and we do not plan to pay dividends on our common stock in the foreseeable future. We expect that any earnings, which we may realize, will be retained to finance the growth of our company.

| 21 |

The following table provides information about the securities authorized for issuance under our equity compensation plans as of June 30, 2015.

EQUITY COMPENSATION PLAN INFORMATION

| Number of securities to be issued upon exercise of outstanding options, warrants and rights and restricted stock units | Weighted-average exercise price of outstanding options, warrants and rights and restricted stock units | Number of securities remaining available for future issuance under equity compensation plans | ||||||||||

| Equity compensation plans approved by security holders | 1,626,919 | (1) | $ | 4.45 | 3,290,751 | (2) | ||||||

| Equity compensation plans not approved by security holders | — | — | — | |||||||||

| Total | 1,626,919 | (1) | $ | 4.45 | 3,290,751 | (2) | ||||||

| (1) | Issued pursuant to our 1998 Stock Plan and 2008 Stock Plan. |

| (2) | Available for future issuance pursuant to our 2008 Stock Plan. |

RECENT SALES OF UNREGISTERED SECURITIES; USE OF PROCEEDS FROM REGISTERED SECURITIES

None, except as previously disclosed on our Quarterly Reports on Forms 10-Q and Current Reports on Forms 8-K.

| 22 |

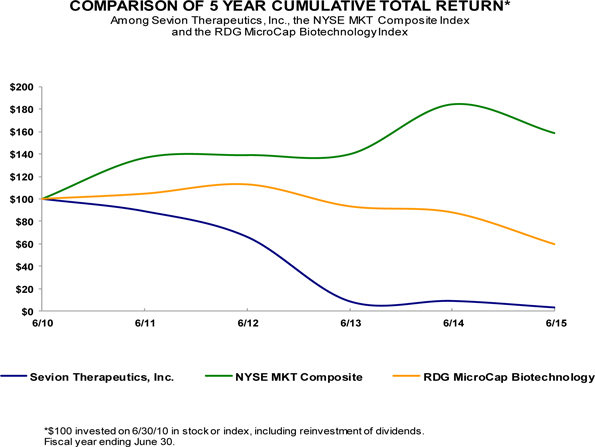

The graph below matches Sevion Therapeutics, Inc.'s cumulative 5-Year total shareholder return on common stock with the cumulative total returns of the NYSE MKT Composite index and the RDG MicroCap Biotechnology index. The graph tracks the performance of a $100 investment in our common stock and in each index (with the reinvestment of all dividends) from June 30, 2010 to June 30, 2015.

| 6/10 | 6/11 | 6/12 | 6/13 | 6/14 | 6/15 | |||||||||||||||||||

| Sevion Therapeutics, Inc. | 100.00 | 88.89 | 66.03 | 8.57 | 8.89 | 3.05 | ||||||||||||||||||

| NYSE MKT Composite | 100.00 | 136.56 | 139.01 | 139.81 | 184.33 | 158.66 | ||||||||||||||||||

| RDG MicroCap Biotechnology | 100.00 | 104.62 | 112.91 | 93.36 | 87.91 | 59.50 | ||||||||||||||||||

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

| 23 |

| Item 6. | Selected Financial Data. |

The following Selected Financial Data should be read in conjunction with “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Item 8. Financial Statements and Supplementary Data” included elsewhere in this Annual Report on Form 10-K.

SELECTED FINANCIAL DATA

| Fiscal Year Ended June 30, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| (In thousands, except per share data) | ||||||||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||

| Revenue | $ | 75 | $ | 100 | $ | - | $ | 200 | $ | - | ||||||||||

| Operating expenses: | ||||||||||||||||||||

| General and administrative | 3,170 | 3,683 | 2,500 | 2,724 | 2,610 | |||||||||||||||

| Research and development | 4,568 | 3,339 | 2,086 | 2,566 | 3,720 | |||||||||||||||

| Acquisition related costs | - | 545 | - | - | - | |||||||||||||||

| Impairment of Goodwill | 8,122 | - | - | - | - | |||||||||||||||

| Impairment and write-off of patents abandoned | 2,291 | 1,681 | 64 | 321 | 1,588 | |||||||||||||||

| Total operating expenses | 18,151 | 9,248 | 4,650 | 5,611 | 7,918 | |||||||||||||||

| Loss from operations | (18,076 | ) | (9,148 | ) | (4,650 | ) | (5,411 | ) | (7,918 | ) | ||||||||||

| Grant income | - | - | - | - | 244 | |||||||||||||||

| Fair value – stock right | 12 | - | - | - | - | |||||||||||||||

| Fair value – warrant liability | 3 | - | 371 | 472 | 609 | |||||||||||||||

| Other noncash expense | - | - | - | - | (116 | ) | ||||||||||||||

| Loss on extinguishment of debt | - | - | (1,725 | ) | - | - | ||||||||||||||

| Interest expense, net | (3 | ) | (77 | ) | (119 | ) | (127 | ) | (88 | ) | ||||||||||

| Net loss | (18,064 | ) | (9,225 | ) | (6,123 | ) | (5,066 | ) | (7,269 | ) | ||||||||||

| Preferred dividends | (839 | ) | (4,629 | ) | (863 | ) | (1,626 | ) | (2,638 | ) | ||||||||||

| Net loss available to common shares | $ | (18,903 | ) | $ | (13,854 | ) | $ | (6,986 | ) | $ | (6,692 | ) | $ | (9,907 | ) | |||||

| Basic and diluted net loss per common share | $ | (1.31 | ) | $ | (2.53 | ) | $ | (5.11 | ) | $ | (7.81 | ) | $ | (14.29 | ) | |||||

| Basic and diluted weighted average number of common shares outstanding | 14,417 | 5,477 | 1,366 | 857 | 693 | |||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 3,335 | $ | 6,111 | $ | 1,602 | $ | 2,001 | $ | 3,610 | ||||||||||

| Working capital | 2,951 | 5,399 | 310 | 387 | 1,788 | |||||||||||||||

| Total assets | 19,547 | 33,335 | 7,097 | 6,955 | 8,597 | |||||||||||||||

| Accumulated deficit | (107,183 | ) | (88,280 | ) | (74,426 | ) | (67,440 | ) | (60,748 | ) | ||||||||||

| Total stockholders’ equity | 12,225 | 27,490 | 3,786 | 3,453 | 4,517 | |||||||||||||||

| 24 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. |

The discussion in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contains trend analysis, estimates and other forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements include, without limitation, statements containing the words “believes,” “anticipates,” “expects,” “continue,” and other words of similar import or the negative of those terms or expressions. Such forward-looking statements are subject to known and unknown risks, uncertainties, estimates and other factors that may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Actual results could differ materially from those set forth in such forward-looking statements as a result of, but not limited to, the “Risk Factors” described in Part I, Item 1A. You should read the following discussion and analysis along with the “Selected Financial Data” and the financial statements and notes attached to those statements included elsewhere in this report.

Overview

We do not expect to generate significant revenues for several years, during which time we will engage in significant research and development efforts.

Our protein biologics technology comprises (i) a platform to discover and engineer human antibodies directly on the cell surface, (ii) antibodies derived from cows that contain ultralong binding regions that may be useful in binding certain therapeutic epitopes, and (iii) a chimerasome nanocage capable of encapsulating therapeutic payloads for drug delivery.

Our preclinical antibody development program comprises an antibody against the ion channel Kv1.3, which is an important molecule in regulating T-cell activation in a number of autoimmune diseases. We have performed experiments showing that this antibody potently blocks activation of human T-cells in vitro. Future development efforts will include a Phase I clinical trial.

Consistent with our commercialization strategy, we may license our technology as the opportunities may arise, that may result in additional license fees, revenues from contract research and other related revenues. Successful future operations will depend on our and our partners’ ability to transform our research and development activities into a commercially feasible technology.

| 25 |

Critical Accounting Policies and Estimates

Revenue Recognition

We record revenue under technology license and development agreements related to the following. Actual fees received may vary from the recorded estimated revenues.

| · | Nonrefundable upfront license fees that are received in exchange for the transfer of our technology to licensees, for which no further obligations to the licensee exist with respect to the basic technology transferred, are recognized as revenue on the earlier of when payments are received or collections are assured. |

| · | Nonrefundable upfront license fees that are received in connection with agreements that include time-based payments are, together with the time-based payments, deferred and amortized ratably over the estimated research period of the license. |

| · | Milestone payments, which are contingent upon the achievement of certain research goals, are recognized as revenue when the milestones, as defined in the particular agreement, are achieved. |

| · | Direct and indirect costs reimbursed are offset against R&D Costs. |

The effect of any change in revenues from technology license and development agreements would be reflected in revenues in the period such determination was made. Historically, no such adjustments have been made.

Estimates of Expenses

Our research and development agreements with third parties provide for an estimate of our expenses and costs, which are variable and are based on the actual services performed by the third party. We estimate the aggregate amount of the expenses based upon the projected amounts that are set forth in the agreements, and we accrue the expenses for which we have not yet been invoiced or prepay the expenses that have been invoiced but the services have not yet been performed. In estimating the expenses, we consider, among other things, the following factors:

| · | the existence of any prior relationship between us and the third party provider; |

| · | the past results of prior research and development services performed by the third party provider; and |

| · | the scope and timing of the research and development services set forth in the agreement with the third party provider. |