Attached files

| file | filename |

|---|---|

| EX-24 - EXHIBIT 24 - CAMPBELL SOUP CO | cpb-822015xexh24.htm |

| EX-31.A - EXHIBIT 31.A - CAMPBELL SOUP CO | cpb-822015xexb31a.htm |

| EX-31.B - EXHIBIT 31.B - CAMPBELL SOUP CO | cpb-822015xexb31b.htm |

| EX-23 - EXHIBIT 23 - CAMPBELL SOUP CO | cpb-822015xexb23.htm |

| EX-32.A - EXHIBIT 32.A - CAMPBELL SOUP CO | cpb-822015xexb32a.htm |

| EX-21 - EXHIBIT 21 - CAMPBELL SOUP CO | cpb-822015xexb21.htm |

| EX-32.B - EXHIBIT 32.B - CAMPBELL SOUP CO | cpb-822015xexb32b.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

_______________________________________________________________________________

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended August 2, 2015 | Commission File Number 1-3822 |

CAMPBELL SOUP COMPANY

New Jersey | 21-0419870 |

State of Incorporation | I.R.S. Employer Identification No. |

1 Campbell Place

Camden, New Jersey 08103-1799

Principal Executive Offices

Telephone Number: (856) 342-4800

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Capital Stock, par value $.0375 | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. R Yes o No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. o Yes R No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. R Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). R Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes R No

As of January 30, 2015 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of capital stock held by non-affiliates of the registrant was approximately $8,888,874,209. There were 309,777,647 shares of capital stock outstanding as of September 15, 2015.

Portions of the Registrant’s Proxy Statement for the Annual Meeting of Shareholders to be held on November 18, 2015, are incorporated by reference into Part III.

TABLE OF CONTENTS

PART II | ||

PART III | ||

2

PART I

Item 1. Business

The Company

Unless otherwise stated, the terms "we," "us", "our" and the "company" refer to Campbell Soup Company and its consolidated subsidiaries.

We are a manufacturer and marketer of high-quality, branded convenience food products. We organized as a business corporation under the laws of New Jersey on November 23, 1922; however, through predecessor organizations, we trace our heritage in the food business back to 1869. Our principal executive offices are in Camden, New Jersey 08103-1799.

Background

Our long-term goal is to build shareholder value by driving sustainable, profitable net sales growth. Guided by our purpose - “Real Food That Matters For Life’s Moments,” we expect to deliver this goal by executing against a dual strategy of strengthening our core businesses while also expanding into faster-growing spaces. We have made a number of enterprise design and portfolio changes over the past several years in support of this strategy, including the following:

• | On January 29, 2015, we announced plans to implement a new enterprise design focused mainly on product categories. Under the new design, which we fully implemented at the beginning of 2016, our businesses are organized in the following divisions: Americas Simple Meals and Beverages, Global Biscuits and Snacks, and Campbell Fresh. |

• | In support of the new enterprise design, we designed and implemented a new Integrated Global Services (IGS) organization to deliver shared services across the company. IGS, which became effective at the beginning of 2016, is expected to reduce costs while increasing our efficiency and effectiveness. We are also pursuing other initiatives to reduce costs and increase effectiveness, such as streamlining our organizational structure and adopting zero-based budgeting over time. See "Management’s Discussion and Analysis of Financial Condition and Results of Operations" for additional information on these initiatives. |

• | In 2013, we acquired Bolthouse Farms and Plum. In 2014, we acquired Kelsen and divested our European simple meals business. Most recently, on June 29, 2015, we completed the acquisition of the assets of Garden Fresh Gourmet for approximately $230 million. Garden Fresh Gourmet is a provider of refrigerated salsa in North America, and it also produces hummus, dips and tortilla chips. We funded the Garden Fresh Gourmet acquisition through the issuance of commercial paper. See Note 3 to the Consolidated Financial Statements for additional information on our recent acquisitions, and Note 4 to the Consolidated Financial Statements for additional information on our divestiture of the European simple meals business. |

For additional information on our dual strategy of strengthening our core businesses while also expanding into faster-growing spaces, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

2015 Reportable Segments

Through the fourth quarter of 2015, we reported the results of our operations in the following reportable segments: U.S. Simple Meals; Global Baking and Snacking; International Simple Meals and Beverages; U.S. Beverages; and Bolthouse and Foodservice. During this period, we had 11 operating segments based on product type and geographic location, and we aggregated the operating segments into the appropriate reportable segment based on similar economic characteristics, products, production processes, types or classes of customers, distribution methods and regulatory environment. See also Note 7 to the Consolidated Financial Statements. The 2015 reportable segments are discussed in greater detail below.

U.S. Simple Meals

The U.S. Simple Meals segment includes the following products: Campbell’s condensed and ready-to-serve soups; Swanson broth and stocks; Prego pasta sauces; Pace Mexican sauces; Campbell’s gravies, pasta, beans and dinner sauces; Swanson canned poultry; and Plum food and snacks.

Global Baking and Snacking

The Global Baking and Snacking segment aggregates the following operating segments: Pepperidge Farm cookies, crackers, bakery and frozen products in U.S. retail; Arnott’s biscuits in Australia and Asia Pacific; and Kelsen cookies globally.

International Simple Meals and Beverages

The International Simple Meals and Beverages segment aggregates the following operating segments: the retail business in Canada and the simple meals and beverages business in Asia Pacific, Latin America and China. See “Background” and Note 4 to the Consolidated Financial Statements for information on the sale of the European simple meals business, which was historically

3

included in this segment. The results of operations of the European simple meals business have been reflected as discontinued operations.

U.S. Beverages

The U.S. Beverages segment represents the U.S. retail beverages business, including the following products: V8 juices and beverages, and Campbell’s tomato juice.

Bolthouse and Foodservice

Bolthouse and Foodservice comprises the Bolthouse Farms carrot products operating segment (Farms), including fresh carrots, juice concentrate and fiber; the Bolthouse Farms refrigerated beverages and refrigerated salad dressings operating segment (CPG); the North America Foodservice operating segment; and as of June 29, 2015, the Garden Fresh Gourmet operating segment. The North America Foodservice operating segment represents the distribution of products such as soup, specialty entrées, beverage products, other prepared foods and Pepperidge Farm products through various food service channels in the U.S. and Canada. None of these operating segments meets the criteria for aggregation nor the thresholds for separate disclosure.

New Reportable Segments in 2016

As discussed above, we recently announced plans to organize our businesses into three divisions: Americas Simple Meals and Beverages, Global Biscuits and Snacks, and Campbell Fresh. At the beginning of 2016, we implemented this new enterprise design, and we are now managing our operations under the design. Accordingly, we will modify our segment reporting as appropriate in future filings.

Ingredients and Packaging

The ingredient and packaging materials required for the manufacture of our food products are purchased from various suppliers. These items are subject to fluctuations in price attributable to a number of factors, including changes in crop size, cattle cycles, disease, product scarcity, demand for raw materials, commodity market speculation, energy costs, currency fluctuations, government-sponsored agricultural programs, import and export requirements, drought and other weather conditions (including the potential effects of climate change) during the growing and harvesting seasons. To help reduce some of this price volatility, we use a combination of purchase orders, short- and long-term contracts, inventory management practices and various commodity risk management tools for most of our ingredients and packaging. Ingredient inventories are at a peak during the late fall and decline during the winter and spring. Since many ingredients of suitable quality are available in sufficient quantities only at certain seasons, we make commitments for the purchase of such ingredients during their respective seasons. At this time, we do not anticipate any material restrictions on the availability of ingredients or packaging that would have a significant impact on our businesses. For information on the impact of inflation, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Customers

In most of our markets, sales and merchandising activities are conducted through our own sales force and our third-party broker and distributor partners. In the U.S., Canada and Latin America, our products are generally resold to consumers in retail food chains, mass discounters, mass merchandisers, club stores, convenience stores, drug stores, dollar stores and other retail, commercial and non-commercial establishments. In the Asia Pacific region, our products are generally resold to consumers through retail food chains, convenience stores and other retail, commercial and non-commercial establishments. We make shipments promptly after receipt and acceptance of orders.

Our five largest customers accounted for approximately 38% of our consolidated net sales from continuing operations in 2015, 35% in 2014 and 36% in 2013. Our largest customer, Wal-Mart Stores, Inc. and its affiliates, accounted for approximately 20% of our consolidated net sales in 2015 and 19% in 2014 and 2013. All of our reportable segments sold products to Wal-Mart Stores, Inc. or its affiliates. No other customer accounted for 10% or more of our consolidated net sales.

Trademarks and Technology

As of September 15, 2015, we owned over 3,700 trademark registrations and applications in over 160 countries. We believe our trademarks are of material importance to our business. Although the laws vary by jurisdiction, trademarks generally are valid as long as they are in use and/or their registrations are properly maintained and have not been found to have become generic. Trademark registrations generally can be renewed indefinitely as long as the trademarks are in use. We believe that our principal brands, including Arnott's, Bolthouse Farms, Campbell's, Garden Fresh Gourmet, Goldfish, Kjeldsens, Pace, Pepperidge Farm, Plum, Prego, Swanson, and V8, are protected by trademark law in the major markets where they are used. In addition, some of our products are sold under brands that have been licensed from third parties.

Although we own a number of valuable patents, we do not regard any segment of our business as being dependent upon any single patent or group of related patents. In addition, we own copyrights, both registered and unregistered, and proprietary trade secrets, technology, know-how, processes, and other intellectual property rights that are not registered.

4

Competition

We experience worldwide competition in all of our principal products. This competition arises from numerous competitors of varying sizes across multiple food and beverage categories, and includes producers of generic and private label products, as well as other branded food and beverage manufacturers. All of these competitors vie for trade merchandising support and consumer dollars. The number of competitors cannot be reliably estimated. The principal areas of competition are brand recognition, taste, quality, price, advertising, promotion, convenience and service.

Working Capital

For information relating to our cash and working capital items, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Capital Expenditures

During 2015, our aggregate capital expenditures were $380 million. We expect to spend approximately $350 million for capital projects in 2016. Major 2016 capital projects include an ongoing Bolthouse Farms beverage and salad dressing capacity expansion project, an ongoing North American warehouse capacity expansion project, a new Australian multi-pack biscuit capacity expansion project and a new refrigeration replacement project at our Virginia, Australia, plant.

Research and Development

During the last three fiscal years, our expenditures on research and development activities relating to new products and the improvement and maintenance of existing products were $113 million in 2015, $121 million in 2014, and $128 million in 2013. The decrease from 2014 to 2015 was primarily due to savings from cost reduction and restructuring initiatives. The decrease from 2013 to 2014 was primarily due to lower incentive compensation costs and cost savings from restructuring initiatives, partially offset by the impact of acquisitions.

Environmental Matters

We have requirements for the operation and design of our facilities that meet or exceed applicable environmental rules and regulations. Of our $380 million in capital expenditures made during 2015, approximately $12 million was for compliance with environmental laws and regulations in the U.S. We further estimate that approximately $10 million of the capital expenditures anticipated during 2016 will be for compliance with U.S. environmental laws and regulations. We believe that continued compliance with existing environmental laws and regulations (both within the U.S. and elsewhere) will not have a material effect on capital expenditures, earnings or our competitive position. In addition, we continue to monitor existing and pending environmental laws and regulations within the U.S. and elsewhere, including the recently-enacted regulations in the U.S. to limit carbon dioxide emissions from electric utilities, relating to climate change and greenhouse gas emissions. While the impact of these laws and regulations cannot be predicted with certainty, we do not believe that compliance with these laws and regulations will have a material effect on capital expenditures, earnings or our competitive position.

Seasonality

Demand for our products is somewhat seasonal, with the fall and winter months usually accounting for the highest sales volume due primarily to demand for our soup products. Sales of Kelsen products are also highest in the fall and winter months due primarily to holiday gift giving. Demand for our other products is generally evenly distributed throughout the year.

Employees

On August 2, 2015, we had approximately 18,600 employees.

Financial Information

Financial information for our reportable segments and geographic areas is found in Note 7 to the Consolidated Financial Statements. For risks attendant to our foreign operations, see “Risk Factors.”

Websites

Our primary corporate website can be found at www.campbellsoupcompany.com. We make available free of charge at this website (under the “Investor Center — Financial Information — SEC Filings” caption) all of our reports (including amendments) filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, including our annual report on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K. These reports are made available on the website as soon as reasonably practicable after their filing with, or furnishing to, the Securities and Exchange Commission.

All websites appearing in this Annual Report on Form 10-K are inactive textual references only, and the information in, or accessible through, such websites is not incorporated into this Annual Report on Form 10-K, or into any of our other filings with the Securities and Exchange Commission.

5

Item 1A. Risk Factors

In addition to the factors discussed elsewhere in this Report, the following risks and uncertainties could materially adversely affect our business, financial condition and results of operations. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations and financial condition.

We operate in a highly competitive industry

We operate in the highly competitive food industry and experience international competition in all of our principal products. The principal areas of competition are brand recognition, taste, quality, price, advertising, promotion, convenience and service. A number of our primary competitors have substantial financial, marketing and other resources. A strong competitive response from one or more of these competitors to our marketplace efforts, or a consumer shift towards private label offerings, could result in us reducing pricing, increasing marketing or other expenditures, and/or losing market share.

Our results are dependent on strengthening our core businesses while diversifying into faster-growing spaces

Our strategy is focused on strengthening our core businesses while diversifying our portfolio into faster-growing spaces. Our core businesses are concentrated in slower-growing center-store categories in traditional mass and grocery channels. Factors that may impact our success include:

•our ability to identify and capitalize on faster-growing spaces;

• | our ability to identify and capitalize on customer or consumer trends, including those related to new or improved products or packaging or to our existing products; |

•our ability to design and implement effective retail execution plans;

•our ability to design and implement effective advertising and marketing programs, including digital programs;

•our ability to secure or maintain sufficient shelf space at retailers; and

•changes in underlying growth rates of the categories in which we compete.

If we are not successful in addressing theses factors, our strategy may not be successful and/or our business or financial results may be negatively impacted.

We may not realize anticipated benefits from our cost reduction, organizational design or other initiatives

We recently implemented a new enterprise design focused mainly on product categories. We are also pursuing related initiatives to reduce costs and increase effectiveness, such as streamlining our organization and adopting zero-based budgeting over time. The success of these initiatives presents significant organizational challenges and in some cases may require extensive negotiations with third parties, such as suppliers and other business partners. As a result, we may not realize all or part of the anticipated cost savings or other benefits from the initiatives. Other events and circumstances, such as financial or strategic difficulties, delays or unexpected costs, may also adversely impact our ability to realize all or part of the anticipated cost savings or other benefits, or cause us not to realize the anticipated cost savings or other benefits on the expected timetable. If we are unable to realize the anticipated cost savings, our ability to fund other initiatives may be adversely affected. In addition, the initiatives may not advance our strategy as expected. Finally, the complexity of the initiatives will require a substantial amount of management and operational resources. Our management team must successfully execute the administrative and operational changes necessary to achieve the anticipated benefits of the initiatives. These and related demands on our resources may divert the organization’s attention from other business issues, have adverse effects on existing business relationships with suppliers and customers, and impact employee morale.

From time-to-time, we may also implement other supply chain, information technology or related initiatives. Our success is partly dependent upon properly executing, and realizing cost savings or other benefits from, these additional initiatives, which are often complex.

Any failure to implement our cost reduction, organizational design or other initiatives in accordance with our plans could adversely affect our business or financial results.

Our results may be adversely affected by the failure to execute acquisitions and divestitures successfully

Our ability to meet our objectives with respect to the acquisition of new businesses or the divestiture of existing businesses may depend in part on our ability to identify suitable buyers and sellers, negotiate favorable financial terms and other contractual terms, and obtain all necessary regulatory approvals. Potential risks of acquisitions also include:

•the inability to integrate acquired businesses efficiently into our existing operations;

•diversion of management's attention from other business concerns;

•potential loss of key employees and/or customers of acquired businesses;

6

•potential assumption of unknown liabilities;

•the inability to implement promptly an effective control environment;

•potential impairment charges if purchase assumptions are not achieved or market conditions decline; and

•the risks inherent in entering markets or lines of business with which we have limited or no prior experience.

Acquisitions outside the U.S. may present unique challenges and increase our exposure to risks associated with foreign operations, including foreign currency risks and risks associated with local regulatory regimes. For divestitures, potential risks may also include the inability to separate divested businesses or business units from us effectively and efficiently and to reduce or eliminate associated overhead costs. Our business or financial results may be negatively affected if acquisitions or divestitures are not successfully implemented or completed.

Disruption to our supply chain could adversely affect our business

Our ability to manufacture and/or sell our products may be impaired by damage or disruption to our manufacturing or distribution capabilities, or to the capabilities of our suppliers or contract manufacturers, due to factors that are hard to predict or beyond our control, such as adverse weather conditions, natural disasters, fire, terrorism, pandemics, strikes or other events. Production of the agricultural commodities used in our business may also be adversely affected by drought, water scarcity, temperature extremes, scarcity of suitable agricultural land, crop disease and/or crop pests. Failure to take adequate steps to mitigate the likelihood or potential impact of such events, or to effectively manage such events if they occur, may adversely affect our business or financial results, particularly in circumstances where a product is sourced from a single supplier or location. Disputes with significant suppliers or contract manufacturers, including disputes regarding pricing or performance, may also adversely affect our ability to manufacture and/or sell our products, as well as our business or financial results.

Our non-U.S. operations pose additional risks to our business

In 2015, approximately 21% of our consolidated net sales from continuing operations were generated outside of the U.S. Sales outside the U.S. are expected to continue to represent a significant portion of consolidated net sales. Our business or financial performance may be adversely affected due to the risks of doing business in markets outside of the U.S., including but not limited to the following:

•unfavorable changes in tariffs, quotas, trade barriers or other export and import restrictions;

• | the difficulty and/or costs of complying with a wide variety of laws, treaties and regulations, including anti-corruption laws and regulations such as the U.S. Foreign Corrupt Practices Act; |

• | the difficulty and/or costs of designing and implementing an effective control environment across diverse regions and employee bases; |

• | the adverse impact of foreign tax treaties and policies; |

• | political or economic instability, including the possibility of civil unrest, armed hostilities or terrorist acts; |

• | the possible nationalization of operations; |

• | the difficulty of enforcing remedies and protecting intellectual property in various jurisdictions; and |

• | restrictions on the transfer of funds to and from countries outside of the U.S., including potentially negative tax consequences. |

In addition, we hold assets and incur liabilities, generate revenue, and pay expenses in a variety of currencies other than the U.S. dollar, primarily the Australian dollar and the Canadian dollar. Our consolidated financial statements are presented in U.S. dollars, and we must translate our assets, liabilities, sales and expenses into U.S. dollars for external reporting purposes. As a result, changes in the value of the U.S. dollar due to fluctuations in currency exchange rates or currency exchange controls may materially and negatively affect the value of these items in our consolidated financial statements, even if their value has not changed in their local currency.

We face risks related to recession, financial and credit market disruptions and other economic conditions

Customer and consumer demand for our products may be impacted by weak economic conditions, recession, equity market volatility or other negative economic factors in the U.S. or other nations. Similarly, disruptions in financial and/or credit markets may impact our ability to manage normal commercial relationships with our customers, suppliers and creditors. In addition, changes in tax or interest rates in the U.S. or other nations, whether due to recession, financial and credit market disruptions or other reasons, could impact us.

Increased regulation or regulatory-based claims could adversely affect our business or financial results

The manufacture and marketing of food products is extensively regulated. The primary areas of regulation include the processing, packaging, storage, distribution, marketing, advertising, labeling, quality and safety of our food products, as well as

7

the health and safety of our employees and the protection of the environment. In the U.S., we are subject to regulation by various government agencies, including the Food and Drug Administration, the U.S. Department of Agriculture, the Federal Trade Commission, the Occupational Safety and Health Administration and the Environmental Protection Agency, as well as various state and local agencies. We are also regulated by similar agencies outside the U.S. Changes in regulatory requirements (such as proposed labeling requirements), or evolving interpretations of existing regulatory requirements, may result in increased compliance cost, capital expenditures and other financial obligations that could adversely affect our business or financial results. In addition, the marketing of food products has come under increased scrutiny in recent years, and the food industry has been subject to an increasing number of legal proceedings and claims relating to alleged false or deceptive marketing under federal, state and foreign laws or regulations. Legal proceedings or claims related to our marketing could damage our reputation and/or could adversely affect our business or financial results.

Our results may be adversely impacted by increases in the price of raw and packaging materials

The raw and packaging materials used in our business include tomato paste, grains, beef, poultry, vegetables, steel, glass, paper and resin. Many of these materials are subject to price fluctuations from a number of factors, including crop size, cattle cycles, disease, product scarcity, demand for raw materials, commodity market speculation, energy costs, currency fluctuations, government-sponsored agricultural programs, import and export requirements, drought and other weather conditions (including the potential effects of climate change). To the extent any of these factors result in an increase in raw and packaging material prices, we may not be able to offset such increases through productivity or price increases or through our commodity hedging activity.

Adverse changes in the global climate or extreme weather conditions could adversely affect our business or operations

Our business or financial results could be adversely affected by changing global temperatures or weather patterns or by extreme or unusual weather conditions. Adverse changes in the global climate or extreme or unusual weather conditions could:

• | unfavorably impact the cost or availability of raw or packaging materials, especially if such events have a negative impact on agricultural productivity or on the supply of water; |

• | disrupt our ability, or the ability of our suppliers or contract manufacturers, to manufacture or distribute our products; |

• | disrupt the retail operations of our customers; or |

• | unfavorably impact the demand for, or the consumer's ability to purchase, our products. |

In addition, there is growing concern that the release of carbon dioxide and other greenhouse gases into the atmosphere may be impacting global temperatures and weather patterns and contributing to extreme or unusual weather conditions. This growing concern may result in more regional, federal, and/or global legal and regulatory requirements to reduce or mitigate the effects of greenhouse gases. Adoption of such additional regulation may result in increased compliance costs, capital expenditures, and other financial obligations that could adversely affect our business or financial results.

Price increases may not be sufficient to cover increased costs, or may result in declines in sales volume due to pricing elasticity in the marketplace

We intend to pass along to customers some or all cost increases in raw and packaging materials and other inputs through increases in the selling prices of, or decreases in the packaging sizes of, some of our products. Higher product prices or smaller packaging sizes may result in reductions in sales volume. To the extent the price increases or packaging size decreases are not sufficient to offset increased raw and packaging materials and other input costs, and/or if they result in significant decreases in sales volume, our business results and financial condition may be adversely affected.

We may be adversely impacted by a changing customer landscape and the increased significance of some of our customers

Our businesses are largely concentrated in the traditional retail grocery trade. In recent years, alternative retail grocery channels, such as dollar stores, drug stores, club stores and Internet-based retailers, have increased their market share. This trend towards alternative channels is expected to continue in the future. If we are not successful in pursuing our strategy to expand sales in alternative retail grocery channels, our business or financial results may be adversely impacted. In addition, consolidations in the traditional retail grocery trade have produced large, sophisticated customers with increased buying power and negotiating strength who may seek lower prices, increased promotional programs funded by their suppliers or more favorable terms. These customers may use more of their shelf space for their private label products. If we are unable to use our scale, marketing expertise, product innovation and category leadership positions to respond to these customer dynamics, our business or financial results could be negatively impacted.

In 2015, our five largest customers accounted for approximately 38% of our consolidated net sales, with the largest customer, Wal-Mart Stores, Inc. and its affiliates, accounting for approximately 20% of our consolidated net sales. Disruption of sales to any of these customers, or to any of our other large customers, for an extended period of time could adversely affect our business or financial results.

8

If our food products become adulterated or are mislabeled, we might need to recall those items, and we may experience product liability claims if consumers are injured

We may need to recall some of our products if they become adulterated or if they are mislabeled, and we may also be liable if the consumption of any of our products causes injury to consumers. A widespread product recall could result in significant losses due to the costs of a recall, the destruction of product inventory, and lost sales due to the unavailability of product for a period of time. We could also suffer losses from a significant adverse product liability judgment. A significant product recall or product liability claim could also result in adverse publicity, damage to our reputation, and a loss of consumer confidence in the safety and/or quality of our products, ingredients or packaging. Such a loss of confidence could occur even in the absence of a recall or a major product liability claim.

We may be adversely impacted by inadequacies in, or security breaches of, our information technology systems

Our information technology systems are critically important to our operations. We rely on our information technology systems (some of which are outsourced to third parties) to manage the data, communications and business processes for all of our functions, including our marketing, sales, manufacturing, logistics, customer service, accounting and administrative functions. If we do not allocate and effectively manage the resources necessary to build, sustain and protect an appropriate technology infrastructure, our business or financial results could be negatively impacted. Furthermore, our information technology systems may be vulnerable to material security breaches (including the access to or acquisition of customer, consumer or other confidential data), cyber-based attacks or other material system failures. If we are unable to prevent material failures, our operations may be impacted, and we may suffer other negative consequences such as reputational damage, litigation, remediation costs and/or penalties under various data privacy laws and regulations.

Our results may be negatively impacted if consumers do not maintain their favorable perception of our brands

We have a number of iconic brands with significant value. Maintaining and continually enhancing the value of these brands is critical to the success of our business. Brand value is based in large part on consumer perceptions. Success in promoting and enhancing brand value depends in large part on our ability to provide high-quality products. Brand value could diminish significantly due to a number of factors, including consumer perception that we have acted in an irresponsible manner, adverse publicity about our products, packaging and/or ingredients (whether or not valid), our failure to maintain the quality of our products, the failure of our products to deliver consistently positive consumer experiences, or the products becoming unavailable to consumers. The growing use of social and digital media by consumers increases the speed and extent that information and opinions can be shared. Negative posts or comments about us, our brands, products or packaging on social or digital media could seriously damage our brands and reputation. If we do not maintain the favorable perception of our brands, our results could be negatively impacted.

An impairment of the carrying value of goodwill or other indefinite-lived intangible assets could negatively affect our financial results and net worth

As of August 2, 2015, we had goodwill of $2.3 billion and other indefinite-lived intangible assets of $960 million. Goodwill and indefinite-lived intangible assets are initially recorded at fair value and not amortized, but are tested for impairment at least annually or more frequently if impairment indicators arise. We test goodwill at the reporting unit level by comparing the carrying value of the net assets of the reporting unit, including goodwill, to the unit's fair value. Similarly, we test indefinite-lived intangible assets by comparing the fair value of the assets to their carrying values. Fair value for both goodwill and other indefinite-lived intangible assets is determined based on a discounted cash flow analysis. If the carrying values of goodwill or indefinite-lived intangible assets exceed their fair value, the goodwill or indefinite-lived intangible assets are considered impaired and reduced to fair value. Factors that could result in an impairment include a change in revenue growth rates, operating margins, weighted average cost of capital, future economic and market conditions or assumed royalty rates. An impairment of the carrying value of goodwill or other indefinite-lived intangible assets could negatively affect our financial results and net worth.

We may be adversely impacted by legal proceedings or claims

We are party to a variety of legal proceedings and claims arising out of the normal course of business. Since litigation is inherently uncertain, there is no guarantee that we will be successful in defending ourselves against such proceedings or claims, or that our assessment of the materiality or immateriality of these matters, including any reserves taken in connection with such matters, will be consistent with the ultimate outcome of such proceedings or claims. In addition, our reputation could be damaged by allegations made in legal proceeding or claims (even if untrue). In the event we are unable to successfully defend ourselves against these proceedings or claims, or if our assessment of the materiality of these proceedings or claims proves inaccurate, our business or financial results may be adversely affected.

We may be adversely impacted by increased liabilities and costs related to our defined benefit pension plans

We sponsor a number of defined benefit pension plans for employees in the U.S. and various non-U.S. locations. The major defined benefit pension plans are funded with trust assets invested in a globally diversified portfolio of securities and other investments. Changes in regulatory requirements or the market value of plan assets, investment returns, interest rates and mortality rates may affect the funded status of our defined benefit pension plans and cause volatility in the net periodic benefit cost, future

9

funding requirements of the plans and the funded status as recorded on the balance sheet. A significant increase in our obligations or future funding requirements could have a material adverse effect on our financial results.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Our principal executive offices are company-owned and located in Camden, New Jersey. The following table sets forth our principal manufacturing facilities and the business segment that primarily uses each of the facilities:

Principal Manufacturing Facilities

Inside the U.S. | ||||

California | Michigan | Texas | ||

Bakersfield (BFS) | Ferndale (BFS) | Paris (USSM/USB/ISMB/BFS) | ||

Dixon (USSM/USB) | Grand Rapids (BFS) | Utah | ||

Stockton (USSM/USB) | New Jersey | Richmond (GBS) | ||

Connecticut | East Brunswick (GBS) | Washington | ||

Bloomfield (GBS) | North Carolina | Everett (BFS) | ||

Florida | Maxton (USSM/ISMB) | Prosser (BFS) | ||

Lakeland (GBS) | Ohio | Wisconsin | ||

Illinois | Napoleon (USSM/USB/BFS/ISMB) | Milwaukee (USSM) | ||

Downers Grove (GBS) | Willard (GBS) | |||

Pennsylvania | ||||

Denver (GBS) | ||||

Downingtown (GBS/BFS) | ||||

Outside the U.S. | ||||

Australia | Canada | Indonesia | ||

Huntingwood (GBS) | Toronto (USSM/ISMB/BFS) | Jawa Barat (GBS) | ||

Marleston (GBS) | Denmark | Malaysia | ||

Shepparton (ISMB) | Nørre Snede (GBS) | Selangor Darul Ehsan (ISMB) | ||

Virginia (GBS) | Ribe (GBS) | |||

____________________________________

USSM - U.S. Simple Meals

GBS - Global Baking and Snacking

ISMB - International Simple Meals and Beverages

USB - U.S. Beverages

BFS - Bolthouse and Foodservice

Each of the foregoing manufacturing facilities is company-owned, except the Selangor Darul Ehsan, Malaysia, and the East Brunswick, New Jersey, facilities, which are leased. We also maintain executive offices in Norwalk, Connecticut; Santa Monica, California; Emeryville, California; Toronto, Canada; Nørre Snede, Denmark; and North Strathfield, Australia.

We believe that our manufacturing and processing plants are well maintained and are generally adequate to support the current operations of the businesses.

Item 3. Legal Proceedings

None.

Item 4. Mine Safety Disclosures

Not applicable.

10

Executive Officers of the Company

The following list of executive officers as of September 15, 2015, is included as an item in Part III of this Form 10-K:

Name | Present Title | Age | Year First Appointed Executive Officer |

Mark R. Alexander | Senior Vice President | 51 | 2009 |

Carlos J. Barroso | Senior Vice President | 56 | 2013 |

David B. Biegger | Senior Vice President | 56 | 2014 |

Ed Carolan | Senior Vice President | 46 | 2015 |

Adam G. Ciongoli | Senior Vice President and General Counsel | 47 | 2015 |

Anthony P. DiSilvestro | Senior Vice President - Chief Financial Officer | 56 | 2004 |

Jeffrey T. Dunn | Senior Vice President | 58 | 2015 |

Luca Mignini | Senior Vice President | 53 | 2013 |

Denise M. Morrison | President and Chief Executive Officer | 61 | 2003 |

Robert W. Morrissey | Senior Vice President and Chief Human Resources Officer | 57 | 2012 |

Michael P. Senackerib | Senior Vice President | 50 | 2012 |

Carlos J. Barroso served as President and Founder of CJB and Associates, LLC, an R&D consulting firm (2009 - 2013), and Senior Vice President of R&D, Pepsico Global Foods (2008 - 2009), of PepsiCo, Inc. prior to joining us in 2013. Adam G. Ciongoli served as Executive Vice President and General Counsel of Lincoln Financial Group (2012 - 2015) and Group General Counsel and Secretary of Willis Group Holdings, PLC (2007 - 2012) prior to joining us in 2015. Jeffrey T. Dunn served as President of Bolthouse Farms from 2008 until his promotion to Senior Vice President in 2015. Luca Mignini served as Chief Executive Officer of the Findus Italy division of IGLO Group (2010 - 2012) prior to joining us in 2013. Michael P. Senackerib served as Senior Vice President and Chief Marketing Officer of Hertz Global Holdings, Inc. and The Hertz Corporation (2008 - 2011) prior to joining us in 2012. We have employed Mark R. Alexander, David B. Biegger, Ed Carolan, Anthony P. DiSilvestro, Denise M. Morrison and Robert W. Morrissey in an executive or managerial capacity for at least five years.

Prior to Mr. Dunn's tenure with Bolthouse Farms, he was Chief Executive Officer of Ubiquity Brands, LLC. Ubiquity Brands was the parent company of Jay Foods, Inc., a maker of salty snack foods, that voluntarily filed for bankruptcy under Chapter 11 of the U.S. Bankruptcy Code in October 2007.

There is no family relationship among any of our executive officers or between any such officer and any director that is first cousin or closer. All of the executive officers were elected at the November 2014 meeting of the Board of Directors, except Ed Carolan was appointed an executive officer at the March 2015 meeting with the appointment effective as of April 1, 2015, Adam G. Ciongoli was appointed an executive officer at the June 2015 meeting with the appointment effective as of July 13, 2015, and Jeff Dunn was appointed an executive officer at the January 2015 meeting with the appointment effective as of February 1, 2015.

PART II

Item 5. | Market for Registrant’s Capital Stock, Related Shareholder Matters and Issuer Purchases of Equity Securities |

Market for Registrant’s Capital Stock

Our capital stock is listed and principally traded on the New York Stock Exchange. On September 15, 2015, there were 21,102 holders of record of our capital stock. Market price and dividend information with respect to our capital stock are set forth in Note 21 to the Consolidated Financial Statements. Future dividends will be dependent upon future earnings, financial requirements and other factors.

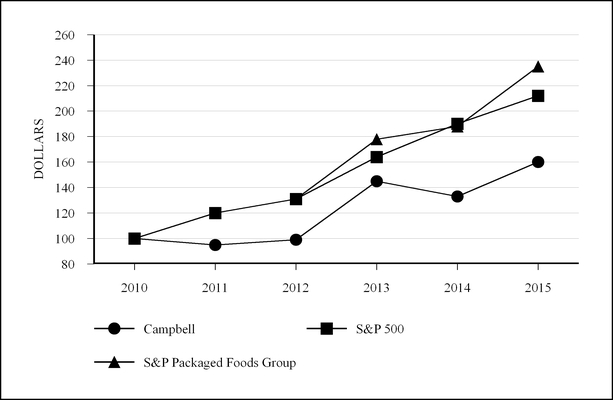

Return to Shareholders* Performance Graph

The following graph compares the cumulative total shareholder return (TSR) on our stock with the cumulative total return of the Standard & Poor’s 500 Stock Index (the S&P 500) and the Standard & Poor’s Packaged Foods Index (the S&P Packaged Foods Group). The graph assumes that $100 was invested on July 30, 2010, in each of our stock, the S&P 500 and the S&P Packaged Foods Group, and that all dividends were reinvested. The total cumulative dollar returns shown on the graph represent the value that such investments would have had on July 31, 2015.

11

* Stock appreciation plus dividend reinvestment.

2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |||||||

Campbell | 100 | 95 | 99 | 145 | 133 | 160 | ||||||

S&P 500 | 100 | 120 | 131 | 164 | 190 | 212 | ||||||

S&P Packaged Foods Group | 100 | 120 | 131 | 178 | 188 | 235 | ||||||

Issuer Purchases of Equity Securities

Period | Total Number of Shares Purchased (1) | Average Price Paid Per Share (2) | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (3) | Approximate Dollar Value of Shares that may yet be Purchased Under the Plans or Programs ($ in Millions) (3) | |||||

5/4/15 - 5/31/15 | 378,000 | $46.12 | 378,000 | $582 | |||||

6/1/15 - 6/30/15 | 380,000 | (4) | $47.63 | (4) | 350,000 | $565 | |||

7/1/15 - 8/2/15 | 335,300 | (5) | $47.51 | (5) | 325,300 | $550 | |||

Total | 1,093,300 | $47.07 | 1,053,300 | $550 | |||||

____________________________________

(1) | Includes 40,000 shares repurchased in open-market transactions to offset the dilutive impact to existing shareholders of issuances under stock compensation plans. |

(2) | Average price paid per share is calculated on a settlement basis and excludes commission. |

(3) | During the fourth quarter of 2015, we had a publicly announced strategic share repurchase program. Under this program, which was announced on June 23, 2011, our Board of Directors authorized the purchase of up to $1 billion of our stock. The program has no expiration date. We also expect to continue our longstanding practice, under separate authorization, of purchasing shares sufficient to offset shares issued under our incentive compensation plans. |

(4) | Includes 30,000 shares repurchased in open-market transactions at an average price of $47.63 to offset the dilutive impact to existing shareholders of issuances under stock compensation plans. |

(5) | Includes 10,000 shares repurchased in open-market transactions at an average price of $47.50 to offset the dilutive impact to existing shareholders of issuances under stock compensation plans. |

12

Item 6. Selected Financial Data

FIVE-YEAR REVIEW — CONSOLIDATED

Fiscal Year | 2015(1) | 2014(2) | 2013(3) | 2012(4) | 2011(5) | ||||||||||||||

(Millions, except per share amounts) | |||||||||||||||||||

Summary of Operations | |||||||||||||||||||

Net sales | $ | 8,082 | $ | 8,268 | $ | 8,052 | $ | 7,175 | $ | 7,143 | |||||||||

Earnings before interest and taxes | 1,095 | 1,192 | 1,080 | 1,155 | 1,212 | ||||||||||||||

Earnings before taxes | 990 | 1,073 | 955 | 1,049 | 1,100 | ||||||||||||||

Earnings from continuing operations | 691 | 726 | 680 | 724 | 749 | ||||||||||||||

Earnings (loss) from discontinued operations | — | 81 | (231 | ) | 40 | 53 | |||||||||||||

Net earnings | 691 | 807 | 449 | 764 | 802 | ||||||||||||||

Net earnings attributable to Campbell Soup Company | 691 | 818 | 458 | 774 | 805 | ||||||||||||||

Financial Position | |||||||||||||||||||

Plant assets - net | $ | 2,347 | $ | 2,318 | $ | 2,260 | $ | 2,127 | $ | 2,103 | |||||||||

Total assets | 8,089 | 8,113 | 8,323 | 6,530 | 6,862 | ||||||||||||||

Total debt | 4,095 | 4,015 | 4,453 | 2,790 | 3,084 | ||||||||||||||

Total equity | 1,376 | 1,603 | 1,210 | 898 | 1,096 | ||||||||||||||

Per Share Data | |||||||||||||||||||

Earnings from continuing operations attributable to Campbell Soup Company - basic | $ | 2.21 | $ | 2.35 | $ | 2.19 | $ | 2.30 | $ | 2.28 | |||||||||

Earnings from continuing operations attributable to Campbell Soup Company - assuming dilution | 2.21 | 2.33 | 2.17 | 2.29 | 2.26 | ||||||||||||||

Net earnings attributable to Campbell Soup Company - basic | 2.21 | 2.61 | 1.46 | 2.43 | 2.44 | ||||||||||||||

Net earnings attributable to Campbell Soup Company - assuming dilution | 2.21 | 2.59 | 1.44 | 2.41 | 2.42 | ||||||||||||||

Dividends declared | 1.248 | 1.248 | 1.16 | 1.16 | 1.145 | ||||||||||||||

Other Statistics | |||||||||||||||||||

Capital expenditures | $ | 380 | $ | 347 | $ | 336 | $ | 323 | $ | 272 | |||||||||

Weighted average shares outstanding - basic | 312 | 314 | 314 | 317 | 326 | ||||||||||||||

Weighted average shares outstanding - assuming dilution | 313 | 316 | 317 | 319 | 329 | ||||||||||||||

____________________________________

(All per share amounts below are on a diluted basis)

The 2014 fiscal year consisted of 53 weeks. All other periods had 52 weeks.

(1) | The 2015 earnings from continuing operations attributable to Campbell Soup Company were impacted by a restructuring charge and administrative expenses of $78 million ($.25 per share) associated with restructuring and cost savings initiatives in 2015. |

(2) | The 2014 earnings from continuing operations attributable to Campbell Soup Company were impacted by the following: a restructuring charge and related costs of $36 million ($.11 per share) associated with restructuring initiatives in 2014 and 2013; pension settlement charges of $14 million ($.04 per share) associated with a U.S. pension plan; a loss of $6 million ($.02 per share) on foreign exchange forward contracts used to hedge the proceeds from the sale of the European simple meals business; $7 million ($.02 per share) tax expense associated with the sale of the European simple meals business; and the estimated impact of the additional week of $25 million ($.08 per share). Earnings from discontinued operations included a gain of $72 million ($.23 per share) on the sale of the European simple meals business. |

(3) | The 2013 earnings from continuing operations attributable to Campbell Soup Company were impacted by the following: a restructuring charge and related costs of $90 million ($.28 per share) associated with restructuring initiatives in 2013 and $7 million ($.02 per share) of transaction costs related to the acquisition of Bolthouse Farms. Earnings from discontinued operations were impacted by an impairment charge on the intangible assets of the simple meals business in Europe of $263 million ($.83 per share) and tax expense of $18 million ($.06 per share) representing taxes on the difference between the book value and tax basis of the business. |

(4) | The 2012 earnings from continuing operations attributable to Campbell Soup Company were impacted by the following: a restructuring charge of $4 million ($.01 per share) associated with the 2011 initiatives and $3 million ($.01 per share) of |

13

transaction costs related to the acquisition of Bolthouse Farms. Earnings from discontinued operations included a restructuring charge of $2 million ($.01 per share) associated with the 2011 initiatives.

(5) | The 2011 earnings from continuing operations attributable to Campbell Soup Company were impacted by a restructuring charge of $39 million ($.12 per share) associated with initiatives announced in June 2011. Earnings from discontinued operations included a restructuring charge of $2 million associated with the initiatives. |

Five-Year Review should be read in conjunction with the Notes to Consolidated Financial Statements.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

Description of the Company

Unless otherwise stated, the terms "we," "us","our" and the "company" refer to Campbell Soup Company and its consolidated subsidiaries.

We are a manufacturer and marketer of high-quality, branded convenience food products. Through 2015, we reported the results of operations in the following reportable segments: U.S. Simple Meals; Global Baking and Snacking; International Simple Meals and Beverages; U.S. Beverages; and Bolthouse and Foodservice.

In 2013, we acquired Bolthouse Farms and Plum. In 2014, we acquired Kelsen and divested our European simple meals business. Most recently, on June 29, 2015, we completed the acquisition of the assets of Garden Fresh Gourmet for $232 million, subject to post-closing adjustments. Garden Fresh Gourmet is a provider of refrigerated salsa in North America, and it also produces hummus, dips and tortilla chips. See Note 3 to the Consolidated Financial Statements for additional information on our recent acquisitions, and Note 4 to the Consolidated Financial Statements for additional information on our divestiture of the European simple meals business.

Key Strategies

Our long-term goal is to build shareholder value by driving sustainable, profitable net sales growth. Guided by our purpose - “Real Food That Matters For Life’s Moments,” we expect to deliver this goal by executing against a dual strategy of strengthening our core businesses while also expanding into faster-growing spaces.

New Enterprise Design

We recently implemented a new enterprise design that better aligns with our dual strategy. Under the new design, which we fully implemented at the beginning of 2016, our businesses are now organized in three divisions focused mainly on product categories. Each division also has a defined portfolio role. The new divisions and their portfolio roles are:

• | Americas Simple Meals and Beverages is our largest division. We expect to manage this division for moderate growth, consistent with the categories in which we operate, and for margin expansion. Americas Simple Meals and Beverages, which includes U.S. soup, will serve as a key economic engine for many years to come. |

• | Global Biscuits and Snacks is focused on expanding in developed and developing markets while improving margins. This division unifies our Pepperidge Farm, Arnott’s and Kelsen businesses around the world. |

• | Campbell Fresh includes Bolthouse Farms, Garden Fresh Gourmet and our refrigerated soup business. We plan to make focused investments in this division to accelerate sales growth and to expand into new categories in packaged fresh. |

In support of our new enterprise design, we designed and implemented a new Integrated Global Services (IGS) organization to deliver shared services across the company. IGS became effective at the beginning of 2016 and is a key element in our efforts to reduce costs while also increasing our efficiency and effectiveness. We are also pursuing other initiatives to reduce costs, such as streamlining our organizational structure and adopting zero-based budgeting over time. In total, we expect the new IGS organization and our other cost savings initiatives to generate approximately $250 million in annual cost savings by the end of fiscal 2018. These savings are above and beyond our existing enabler program. See "Restructuring Charges and Cost Savings Initiatives" for additional information on these initiatives.

Dual Strategy

With this new enterprise design in place, we plan to pursue our dual strategy by:

• | Providing greater transparency about the food we make; |

• | Further embracing digital marketing and e-commerce to connect with consumers and customers in new ways; |

• | Increasing our focus on health and wellbeing; and |

• | Expanding our presence in developing markets. |

14

Providing Greater Product Transparency

On our www.whatsinmyfood.com website, we are providing consumers with a wide range of detail about how some of our foods and beverages are made and the choices behind the ingredients we use in those products. Initially focused on some of our top U.S. products, such as Campbell’s Condensed Tomato and Chicken Noodle soups, we plan to expand this site to include all of our major products in the U.S. and Canada in 2016, with designs to expand globally over the next three fiscal years. We anticipate this enhanced transparency will lead to, or accelerate, changes in our products, including our continued efforts to remove many artificial ingredients where feasible.

Embracing Digital Marketing and E-Commerce

We plan to complement the growing consumer shift to digital and mobile technologies by focusing a larger percentage of our marketing efforts on digital marketing and e-commerce. For example, in 2016 we expect to spend a larger portion of our overall media budget on digital media, while reducing our spending on traditional television media. We also plan to continue our focus on e-commerce capabilities in 2016.

Increasing Focus on Health and Wellbeing

Capitalizing on recent consumer and retailer trends towards fresh and/or healthy products, we plan to increase our focus on our fresh and packaged fresh products. While other parts of our business will continue to provide shelf-stable products that are appealing to health-conscious consumers, our new Campbell Fresh division has a diverse portfolio of fresh and packaged fresh offerings that should help retailers attract these important customers. We expect the Campbell Fresh division to provide us with the needed scale to better compete in the growing perimeter of traditional retail outlets. The recent acquisition of Garden Fresh Gourmet, which provides refrigerated salsa, hummus and dips, as well as tortilla chips, compliments Campbell Fresh’s existing portfolio.

Expanding Presence in Developing Markets

In 2016, we plan to continue to focus on expanding our presence in developing markets, especially our Global Biscuits and Snacks business in Asia. Our new enterprise design unifies all of our biscuit and snacks brands under a single integrated division - Global Biscuits and Snacks. We expect this new structure to help unlock the value of our biscuit and snack brands and to provide a platform to extend these brands across both faster growing developing markets, as well as our existing developed markets.

To support these four imperatives, we will continue to evaluate external development opportunities, ranging from acquisitions to strategic alliances such as joint ventures and other strategic partnerships.

Executive Summary

This Executive Summary provides significant highlights from the discussion and analysis that follows.

• | There were 53 weeks in 2014. There were 52 weeks in 2015 and 2013. |

• | Net sales decreased 2% in 2015 to $8.082 billion, primarily due to the impact of currency translation and one less week compared to the prior year, partly offset by higher selling prices. |

• | Gross profit, as a percent of sales, decreased to 34.7% from 35.1% a year ago. The decrease was primarily due to cost inflation and increased supply chain costs, partly offset by productivity improvements and higher selling prices. |

• | Administrative expenses increased 3% to $593 million from $573 million a year ago. The current year included $22 million of costs related to the implementation of the new organizational structure and cost reduction initiatives, and higher incentive compensation costs, partially offset by savings from cost reduction and restructuring initiatives. |

• | Earnings per share from continuing operations were $2.21 in 2015, compared to $2.33 a year ago. The current and prior year included expenses of $.25 and $.20 per share, respectively, from items impacting comparability as discussed below. The additional week contributed approximately $.08 per share to earnings from continuing operations in 2014. |

Earnings from continuing operations attributable to Campbell Soup Company - 2015 Compared with 2014

The following items impacted the comparability of earnings and earnings per share:

• | In 2015, we incurred charges associated with our initiatives to implement a new enterprise design, to reduce costs and to streamline our organizational structure. We recorded a pre-tax restructuring charge of $102 million related to these initiatives. We also incurred pre-tax charges of $22 million recorded in Administrative expenses related to the implementation of the new organizational structure and cost reduction initiatives (aggregate impact of $78 million after tax, or $.25 per share). See Note 8 to the Consolidated Financial Statements and "Restructuring Charges and Cost Savings Initiatives" for additional information; |

• | In 2014, we recognized pre-tax pension settlement charges in Cost of products sold of $22 million ($14 million after tax, or $.04 per share) associated with a U.S. pension plan. The settlements resulted from the level of lump sum distributions from the plan's assets in 2014, primarily due to the closure of the facility in Sacramento, California; |

15

• | On October 28, 2013, we completed the sale of our simple meals business in Europe. In 2014, we recorded a loss of $9 million ($6 million after tax, or $.02 per share) on foreign exchange forward contracts used to hedge the proceeds from the sale of our European simple meals business. The loss was included in Other expenses. In addition, we recorded tax expense of $7 million ($.02 per share) associated with the sale of the business; |

• | In 2014, we recorded a pre-tax restructuring charge of $54 million ($33 million after tax, or $.10 per share) associated with initiatives to streamline our salaried workforce in North America and our workforce in the Asia Pacific region; restructure manufacturing and streamline operations for our soup and broth business in China; improve supply chain efficiency in Australia; and reduce overhead across the organization. See Note 8 to the Consolidated Financial Statements and "Restructuring Charges and Cost Savings Initiatives" for additional information; and |

• | In 2013, we implemented several initiatives to improve our U.S. supply chain cost structure and increase asset utilization across our U.S. thermal plant network; expand access to manufacturing and distribution capabilities in Mexico; improve our Pepperidge Farm bakery supply chain cost structure; and reduce overhead in North America. In 2014, we recorded a pre-tax restructuring charge of $1 million and restructuring-related costs of $3 million in Cost of products sold (aggregate impact of $3 million after tax, or $.01 per share) related to the 2013 initiatives. See Note 8 to the Consolidated Financial Statements and "Restructuring Charges and Cost Savings Initiatives" for additional information. |

The items impacting comparability are summarized below:

2015 | 2014 | ||||||||||||||

(Millions, except per share amounts) | Earnings Impact | EPS Impact | Earnings Impact | EPS Impact | |||||||||||

Earnings from continuing operations attributable to Campbell Soup Company | $ | 691 | $ | 2.21 | $ | 737 | $ | 2.33 | |||||||

Restructuring charges and related costs/implementation costs | $ | (78 | ) | $ | (.25 | ) | $ | (36 | ) | $ | (.11 | ) | |||

Pension settlement charges | — | — | (14 | ) | (.04 | ) | |||||||||

Loss on foreign exchange forward contracts | — | — | (6 | ) | (.02 | ) | |||||||||

Tax expense associated with sale of business | — | — | (7 | ) | (.02 | ) | |||||||||

Impact of items on earnings from continuing operations(1) | $ | (78 | ) | $ | (.25 | ) | $ | (63 | ) | $ | (.20 | ) | |||

____________________________________

(1) | The sum of the individual per share amounts may not add due to rounding. |

Earnings from continuing operations were $691 million ($2.21 per share) in 2015, compared to $737 million ($2.33 per share) in 2014. The additional week contributed approximately $25 million ($.08 per share) to earnings from continuing operations in 2014. After adjusting for the 53rd week and other items impacting comparability, earnings decreased primarily due to a lower gross margin percentage and the impact of currency translation, partially offset by an increase in sales on a constant currency basis, lower marketing and selling expenses, lower interest expense and a lower effective tax rate. Currency translation had a negative impact of $.06 on earnings per share in the current year. Earnings per share benefited from a reduction in the weighted average diluted shares outstanding, primarily due to share repurchases under our strategic share repurchase program.

We sold our European simple meals business on October 28, 2013. See "Discontinued Operations" for additional information.

Earnings from continuing operations attributable to Campbell Soup Company - 2014 Compared with 2013

In addition to the 2014 items that impacted comparability of Earnings from continuing operations previously disclosed, the following items impacted the comparability of earnings and earnings per share:

• | In 2013, we implemented several initiatives to improve our U.S. supply chain cost structure and increase asset utilization across our U.S. thermal plant network; expand access to manufacturing and distribution capabilities in Mexico; improve our Pepperidge Farm bakery supply chain cost structure; and reduce overhead in North America. In 2013, we recorded a pre-tax restructuring charge of $51 million and restructuring-related costs of $91 million in Cost of products sold (aggregate impact of $90 million after tax, or $.28 per share) related to the 2013 initiatives. See Note 8 to the Consolidated Financial Statements and "Restructuring Charges and Cost Savings Initiatives" for additional information; and |

• | In 2013, we incurred pre-tax transaction costs of $10 million ($7 million after tax, or $.02 per share) associated with the acquisition of Bolthouse Farms, which closed on August 6, 2012. The costs were included in Other expenses. |

16

The items impacting comparability are summarized below:

2014 | 2013 | ||||||||||||||

(Millions, except per share amounts) | Earnings Impact | EPS Impact | Earnings Impact | EPS Impact | |||||||||||

Earnings from continuing operations attributable to Campbell Soup Company | $ | 737 | $ | 2.33 | $ | 689 | $ | 2.17 | |||||||

Restructuring charges and related costs | $ | (36 | ) | $ | (.11 | ) | $ | (90 | ) | $ | (.28 | ) | |||

Pension settlement charges | (14 | ) | (.04 | ) | — | — | |||||||||

Loss on foreign exchange forward contracts | (6 | ) | (.02 | ) | — | — | |||||||||

Tax expense associated with sale of business | (7 | ) | (.02 | ) | — | — | |||||||||

Acquisition transaction costs | — | — | (7 | ) | (.02 | ) | |||||||||

Impact of items on earnings from continuing operations(1) | $ | (63 | ) | $ | (.20 | ) | $ | (97 | ) | $ | (.31 | ) | |||

____________________________________

(1) | The sum of the individual per share amounts may not add due to rounding. |

Earnings from continuing operations were $737 million ($2.33 per share) in 2014, compared to $689 million ($2.17 per share) in 2013. After adjusting for items impacting comparability, earnings increased primarily due to lower administrative expenses, the benefit of the additional week and lower marketing expenses, partly offset by a lower gross margin percentage, lower sales (excluding the impact of acquisitions and the 53rd week), and a higher effective tax rate. The additional week contributed approximately $25 million ($.08 per share) to earnings from continuing operations in 2014.

Net earnings (loss) attributable to noncontrolling interests

We own a 60% controlling interest in a joint venture formed with Swire Pacific Limited to support the development of our soup and broth business in China. The joint venture began operations on January 31, 2011. In 2014, together with our joint venture partner, we agreed to restructure manufacturing and streamline operations for our soup and broth business in China. The after-tax restructuring charge attributable to the noncontrolling interest was $5 million.

We also own a 70% controlling interest in a Malaysian food products manufacturing company.

The noncontrolling interests' share in the net earnings (loss) was included in Net earnings (loss) attributable to noncontrolling interests in the Consolidated Statements of Earnings.

DISCUSSION AND ANALYSIS

Sales

An analysis of net sales by reportable segment follows:

% Change | |||||||||||||||

(Millions) | 2015 | 2014 | 2013 | 2015/2014 | 2014/2013 | ||||||||||

U.S. Simple Meals | $ | 2,930 | $ | 2,944 | $ | 2,849 | —% | 3% | |||||||

Global Baking and Snacking | 2,375 | 2,440 | 2,273 | (3) | 7 | ||||||||||

International Simple Meals and Beverages | 700 | 780 | 869 | (10) | (10) | ||||||||||

U.S. Beverages | 689 | 723 | 742 | (5) | (3) | ||||||||||

Bolthouse and Foodservice | 1,388 | 1,381 | 1,319 | 1 | 5 | ||||||||||

$ | 8,082 | $ | 8,268 | $ | 8,052 | (2)% | 3% | ||||||||

17

An analysis of percent change of net sales by reportable segment follows:

2015 versus 2014 | U.S. Simple Meals | Global Baking and Snacking | International Simple Meals and Beverages (3) | U.S. Beverages | Bolthouse and Foodservice (3) | Total (3) | |||||

Volume and Mix | —% | 2% | 1% | (3)% | 2% | —% | |||||

Price and Sales Allowances | 1 | 1 | 1 | 1 | — | 1 | |||||

Increased Promotional Spending(1) | — | — | (1) | (1) | — | — | |||||

Currency | — | (4) | (9) | — | (1) | (2) | |||||

Net Accounting(2) | — | — | (1) | — | — | — | |||||

Acquisitions | — | — | — | — | 1 | — | |||||

Estimated Impact of 53rd week | (1) | (2) | (2) | (2) | (2) | (2) | |||||

—% | (3)% | (10)% | (5)% | 1% | (2)% | ||||||

2014 versus 2013 | U.S. Simple Meals | Global Baking and Snacking | International Simple Meals and Beverages | U.S. Beverages (3) | Bolthouse and Foodservice | Total | |||||

Volume and Mix | —% | 1% | (2)% | (5)% | 3% | —% | |||||

Price and Sales Allowances | 2 | 2 | (1) | — | — | 1 | |||||

Decreased/(Increased) Promotional Spending(1) | (2) | (3) | — | 1 | (1) | (2) | |||||

Currency | — | (3) | (6) | — | — | (1) | |||||

Net Accounting(2) | — | — | (3) | — | — | — | |||||

Acquisitions | 2 | 8 | — | — | 1 | 3 | |||||

Estimated Impact of 53rd week | 1 | 2 | 2 | 2 | 2 | 2 | |||||

3% | 7% | (10)% | (3)% | 5% | 3% | ||||||

__________________________________________

(1) | Represents revenue reductions from trade promotion and consumer coupon redemption programs. |

(2) | Beginning in 2014, revenue in Mexico is presented on a net accounting basis in connection with a new business model under which the cost of certain services provided by our suppliers is netted against revenue. |

(3) | Sum of the individual amounts does not add due to rounding. |

In 2015, U.S. Simple Meals sales were comparable to the year-ago period. U.S. soup sales declined 3%, with 1% due to the impact of the 53rdweek. Further details of U.S. soup include:

• | Sales of Campbell’s condensed soups decreased 3%, with declines in both eating and cooking varieties. Lower volumes were partially offset by higher selling prices and reduced promotional spending. |

• | Sales of ready-to-serve soups decreased 5%. |

• | Broth sales increased 3% due to gains in aseptically-packaged broth, partially offset by declines in canned broth. |

Sales of other simple meals increased 5%, primarily due to growth in Prego pasta sauces, Plum products and Campbell's dinner sauces, partially offset by lower sales in other simple meal products.

In 2014, U.S. Simple Meals sales increased 3%. U.S. soup sales decreased 1%. Excluding the benefit of the 53rd week, U.S. soup sales decreased 2%. Further details of U.S. soup, excluding the benefit of the 53rd week, include:

• | Sales of Campbell’s condensed soups decreased 3%, with declines in eating varieties partially offset by gains in cooking varieties. Lower volumes and increased promotional spending were partly offset by higher selling prices. |

• | Sales of ready-to-serve soups decreased 6%, primarily due to declines in canned and microwavable soup varieties. |

• | Broth sales increased 8%, primarily due to more effective marketing programs, innovation and distribution gains. |

Sales of other simple meals increased 15%, primarily due to the acquisition of Plum in June 2013, which contributed 9 points of growth. Excluding the impact of the acquisition and the benefit of the 53rd week, sales increased due to gains in Prego pasta sauces, which benefited from the launch of Alfredo sauces; and Campbell's dinner sauces, which benefited from the introduction in 2014 of Campbell's Slow Cooker Sauces; partially offset by declines in Campbell's canned gravy products.

18

In 2015, Global Baking and Snacking sales decreased 3%. In Arnott's, sales decreased due to the impact of currency translation. Excluding the impact of currency translation, sales of Arnott's products increased due to volume gains and higher selling prices in Australia and Indonesia. Pepperidge Farm sales declined primarily due to the impact of the 53rdweek. Excluding the impact of the 53rdweek, Pepperidge Farm sales increased due to gains in fresh bakery, and crackers and cookies, partially offset by declines in frozen products.

In 2014, Global Baking and Snacking sales increased 7%. The acquisition of Kelsen contributed $193 million to sales, or 8 points of growth. Excluding the impact of the acquisition and the benefit of the 53rd week, sales decreased primarily due to the impact of currency translation. Excluding the benefit of the 53rd week, Pepperidge Farm sales increased slightly with growth in fresh bakery and Goldfish crackers, partially offset by declines in adult cracker varieties and frozen products. In fresh bakery, sales increased due to gains in sandwich bread and rolls. In Arnott's, sales decreased primarily due to the impact of currency translation and sales declines in Australia in savory and chocolate varieties, partially offset by strong gains in Indonesia and the benefit of the 53rd week. In 2014, we increased trade spending in Arnott's and Pepperidge Farm to remain competitive.

In 2015, International Simple Meals and Beverages sales decreased 10%. In Canada, sales decreased due to the impact of currency translation and declines in beverages, partially offset by gains in baked snacks. In the Asia Pacific region, sales declined due to the impact of currency translation and the 53rd week. In Latin America, sales declined due in part to the impact of presenting revenue on a net basis and currency translation.

In 2014, International Simple Meals and Beverages sales decreased 10%. In Canada, sales decreased due to the impact of currency translation and declines in beverages, partly offset by gains in snacks. In Latin America, sales declined due to the impact of presenting revenue on a net basis and lower selling prices in Mexico. In the Asia Pacific region, sales decreased primarily due to the impact of currency translation and declines in Australia, primarily in soup, partially offset by gains in Malaysia.

In 2015, U.S. Beverages, sales decreased 5%, primarily due to declines in V8 V-Fusion beverages and V8 vegetable juice, partially offset by gains in V8 Splash beverages. U.S. Beverages continued to be under pressure from category weakness in shelf-stable juices, as well as from competition from specialty beverages and packaged fresh juices.