Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF KLJ & ASSOCIATES LLP - Peekay Boutiques, Inc. | pkay_ex231.htm |

As filed with the Securities and Exchange Commission on August 19, 2015

Registration No. 333-203870

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

____________________________

Amendment No. 2 to

FORM S-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

| PEEKAY BOUTIQUES, INC. |

| (Exact name of registrant as specified in its charter) |

| Nevada |

| 5990 |

| 46-4007972 |

| (State or other jurisdiction |

| (Primary Standard Industrial |

| (I.R.S. Employer |

901 West Main Street, Suite A, Auburn, WA 98001

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

____________________________

Vcorp Services, LLC

1811 Silverside Road

Wilmington, Delaware 19810

888-528-2677

(Names, addresses and telephone numbers of agents for service)

____________________________

Copies to:

Louis A. Bevilacqua, Esq.

BEVILACQUA PLLC

1629 K Street, NW, Suite 300

Washington, DC 20006

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

| (Do not check if a smaller reporting company) |

|

| |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

| Proposed Maximum Aggregate Offering Price (1) |

|

| Amount of Registration Fee (2)(5) |

| ||

| Common Stock, par value $0.001 per share (3) (4) |

| $ | 50,000,000 |

|

| $ | 5,810.00 |

|

| Underwriter's common stock purchase warrants(6) (7) |

|

| - |

|

|

| - |

|

| Common stock included in underwriter's common stock purchase warrants (3) (7) |

| $ | 1,725,000 |

|

| $ | 200.45 |

|

| Total |

| $ | 51,725,000 |

|

| $ | 6,010.45 |

|

(1) Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act.

(2) Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price.

(3) Pursuant to Rule 416 under the Securities Act, the shares of common stock registered hereby also include an indeterminate number of additional shares of common stock as may from time to time become issuable by reason of stock splits, stock dividends, recapitalizations or other similar transactions.

(4) Includes shares of common stock the underwriter has the option to purchase to cover over-allotments, if any.

(5) The Registrant previously paid $5,810.00 of the registration fee in connection with the initial filing of this registration statement.

(6) No fee required pursuant to Rule 457(g) under the Securities Act of 1933, as amended.

(7) Represents 3% of the shares to be sold in this offering, including shares that may be sold upon exercise of the underwriter's over-allotment option. The underwriter's warrants are exercisable at a per share price equal to 115% of the common stock public offering price .

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

| i |

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS

Subject to completion, dated , 2015

PEEKAY BOUTIQUES, INC.

SHARES OF COMMON STOCK

This is a firm commitment public offering of [___] shares of common stock by Peekay Boutiques, Inc. No public market currently exists for our common stock. We anticipate that the initial public offering price of our common stock will be between $[___] and $[___] per share.

We are an "emerging growth company" as defined in the Jumpstart Our Business Startups Act, or the JOBS Act.

INVESTING IN OUR SECURITIES INVOLVES A HIGH DEGREE OF RISK. YOU SHOULD CAREFULLY READ AND CONSIDER "RISK FACTORS" BEGINNING ON PAGE 10.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

| Per Share | Total | |||||||

| Public offering price | $ | $ | ||||||

| Underwriting discounts and commissions (1) | $ | $ | ||||||

| Proceeds, before expenses, to us | $ | $ | ||||||

(1) The underwriter will receive compensation in addition to the underwriting discount s and commissions described above, which compensation consists of (i) five-year compensation warrants entitling the underwriter to purchase 3.0% of the aggregate number of shares issued in this offering, including shares issued pursuant to the exercise of the over-allotment option, with an exercise price equal to 115% of the price per share of the common stock sold in this offering, and (ii) reasonable out-of-pocket expenses incurred by the underwriter (up to a maximum amount of $125,000 for all such expenses), including fees of the underwriter's legal counsel . See "Underwriting" beginning on page 75 of this prospectus for a description of compensation payable to the underwriter.

We have granted the underwriter a 45-day option to purchase up to [___] additional shares of common stock solely to cover over-allotments, if any. See "Underwriting" for a full description of compensation payable to the underwriter.

The underwriter expects to deliver the shares against payment therefor on or about , 2015

The date of this prospectus is , 2015.

| ii |

TABLE OF CONTENTS

| Prospectus Summary | 1 | |

| Risk Factors | 10 | |

| Special Note Regarding Forward-Looking Statements and Market Data | 29 | |

| Use of Proceeds | 31 | |

| Dividend Policy | 33 | |

| Determination of Offering Price | 33 | |

| Dilution | 33 | |

| Capitalization | 34 | |

| Market for Common Equity and Related Stockholder Matters | 35 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 36 | |

| Business | 44 | |

| Management | 55 | |

| Security Ownership of Certain Beneficial Owners and Management | 66 | |

| Certain Relationships and Related Transactions | 68 | |

| Description of Capital Stock | 69 | |

| Underwriting | 76 | |

| Legal Matters | 80 | |

| Experts | 80 | |

| Where You Can Find Additional Information | 80 | |

| Index To Financial Statements | F-1 |

You should rely only on the information contained in this prospectus. We have not, and the underwriter has not, authorized anyone to provide you with any information other than that contained in this prospectus. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus may only be used where it is legal to offer and sell our securities. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of our securities. Our business, financial condition, results of operations and prospects may have changed since that date. We are not, and the underwriter is not , making an offer of these securities in any jurisdiction where the offer is not permitted.

For investors outside the United States: We have not and the underwriter has not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of securities and the distribution of this prospectus outside the United States.

| iii |

SUMMARY

The items in the following summary are described in more detail later in this prospectus. This summary provides an overview of selected information and does not contain all the information you should consider. Therefore, you should also read the more detailed information set out in this prospectus, including the financial statements, the notes thereto and matters set forth under "Risk Factors."

Overview of Our Business

Based on our management's belief and experience in the industry, we believe we are a leading retailer of lingerie, sexual health and wellness products. Our company was founded in 1981 in Auburn, WA by a mother and daughter team with a focus on creating a comfortable and inviting store environment catering to women and couples. We are dedicated to creating both a place and attitude of acceptance and education for our customers. Today, our company is a leader in changing the perception of sexual wellness throughout the United States with 48 locations across six states.

Our stores offer a broad selection of lingerie, sexual health and wellness products and accessories. We offer over 5,000 stock keeping units, or SKUs. We strive to create a visually inspiring environment at our stores and employ highly trained, knowledgeable sales staff, which ensures that our customers leave our stores

enlightened by new information, great ideas and fun products.

Our mission is to provide a warm and welcoming retail environment for individuals and couples to explore sexual wellness.

Store Design and Operations

Our stores are designed and built to appeal to a mainstream customer base. Exterior signage is designed, constructed and installed by professional signage partners. Signage and logos are visible, well-lit and easy to read. The entrance to our stores typically consists of glass windows featuring high-end lingerie displays coordinated by our corporate visual merchandising department. Every detail of our stores is intended to convey a welcoming, open and friendly shopping environment.

We have engaged an architectural firm to develop a brand new retail store design. The all-female design team has decades of experience in retail store design and

execution. The new store layout is designed to flourish in the highest-end shopping centers with its fun, welcoming and open atmosphere. With an energetic color palette and dynamic lighting, the new store design is aligned with the shopping preferences of today's mainstream women and couples. Our new prototype has currently been rolled out at five locations in California, namely, North Hollywood, San Bernardino, Santa Monica, Palmdale and Northridge. In March 2015, we opened our newest store in Valencia, California.

Merchandise

We employ a seven-member merchandising team responsible for product sourcing, vendor negotiations and relationship management, purchasing, planning and analysis, as well as visual merchandising. We utilize "trend-right" in-store displays, which are custom-made, feature tables designed to show elegant collections of seasonal merchandise. Our merchandising philosophy is focused on understanding our customers' needs.

| 1 |

We offer our customers a variety of wellness- and sexual health-related products. Products are designed for women and couples to enhance their sexual satisfaction and meet their broad range of expectations. We offer a variety of quality products ranging from entry-level price points to premium, high-end brands. We have over 5,000 SKUs available ranging from $1 condoms to $265 vibrators. Seasonally, new products represent 20-25% of our overall product assortment. In addition to our broad retail brand portfolio, we also provide SuteraTMprivate label merchandise. As part of our change in merchandising strategy to a "wellness" focus, we have minimized our visual category, which constitutes video sales (a lower-margin product not targeted at our key demographic).

During the fiscal year ended December 31, 2014, our breakdown of sales by product category was as follows:

| · | Sales of personal items constituted approximately 47% of our sales. These items include massagers, vibrators, personal care, and restraints, including brands such as Jimmy Jane, Pipedream, We Vibe and SuteraTM Toys. | |

| · | Sales of gift items constituted approximately 37% of our sales. These items include personal lubricants, apothecary, candles, condoms and sensitizers and desensitizers, including brands such as Crazy Girl, Kamasutra, Earthly Body and System Jo. | |

| · | Sales of lingerie constituted approximately 16% of our sales. Lingerie includes a broad range of sleepwear, bodystockings, clubwear, costumes, corsets, babydolls, hosiery and panties, including brands such as Dreamgirl, Coquette, Escante and Rene Rofe. |

Marketing and Advertising

We market our retail stores through a variety of channels, including billboards, direct mail, radio, interactive and social media and grassroots events. All new stores are allotted a special marketing budget dedicated to a grand opening event. We have an integrated marketing plan that extends from out-of-store to in-store elements, including posters, signage and displays created by a professional in-house design staff.

Store Locations

We select geographic areas and store sites on the basis of demographic information, the quality and nature of neighboring tenants, store visibility and location accessibility. We seek to locate stores primarily in or near centers with major national brands and regional brands such as Target, Walgreens, TJ Maxx, Sally Beauty Supply, Starbucks and others. Based on our management's belief and experience in the industry, our customer demographics also align well with those of Nordstrom, Macy's and other higher-end specialty retailers.

We balance our store expansion between new and existing marketplaces. In our existing marketplaces, we add stores as necessary to provide additional coverage. In new marketplaces, we generally seek to expand in geographically contiguous areas to leverage our experience. We believe that our knowledge of local marketplaces is an important part of our success.

| 2 |

The following table provides a history of our store count during the last two fiscal years:

| Fiscal Year Ended December 31, | ||||||||

| 2014 | 2013 | |||||||

| Stores open at beginning of period | 44 | 42 | ||||||

| Net store openings during period | 3 | 1 | ||||||

| Stores acquired during period | - | 1 | ||||||

| Stores open at end of period | 47 | 44 | ||||||

On March 23, 2015, we opened our newest retail store in Valencia, California.

Competition

Our major competitors for our lingerie, sexual health and wellness products include Adam & Eve, Ann Summers, Pure Romance, Pleasure Chest, Kiss & Tell and Romantix. For our lingerie products, we also compete with traditional department stores such as Macy's and Nordstrom and specialty stores such as Victoria's Secret. We also compete with the online businesses of the aforementioned retailers, as well as pure play e-commerce businesses such as Amazon. Our competitive advantages are the quality and assortment of our merchandise and services, our value proposition, the quality of our customers' shopping experience brought about as the result of our knowledgeable and welcoming sales personnel and the convenience of our stores and website as a one-stop destination for lingerie, sexual health and wellness products.

Customer Service

We strive to complement our extensive merchandise selection and innovative store design with superior customer service. We actively recruit individuals with significant knowledge and experience in the field of lingerie, sexual health and wellness products. We try to ensure that our customers walk out of our stores enlightened with new information, great ideas and fun products. We seek individuals with retail experience because we believe their general retail knowledge can be leveraged in the lingerie, sexual health and wellness products industry. We believe that employees' knowledge of the products and ability to explain the advantages of the products increases sales and that their prompt, knowledgeable service fosters the confidence and loyalty of customers and differentiates our business from other professional retailers of lingerie, sexual health and wellness products. Our employees are trained to foster a warm and welcoming retail environment for individuals and couples to explore sexual wellness. We believe that this attitude of acceptance and education for consumers sets us apart from our competitors.

We emphasize product knowledge during initial training as well as during ongoing training sessions, with programs intended to provide new associates and managers with significant training. The training programs encompass operational and product training and are designed to increase employee and store productivity. Store employees are also required to participate in training on an ongoing basis to keep up-to-date on new products and operational practices.

Most of our stores are staffed with a store manager, assistant store manager and two or three part-time associates. A district manager, who reports directly to the Vice President of Retail, supervises the operations of each store.

| 3 |

Our Competitive Strengths

Based on our management's belief and experience in the industry, the following competitive strengths enable us to compete effectively in and capitalize on the growing lingerie, sexual health and wellness products market.

| · | Niche dominance. Based on our management's experience in the industry, w e believe that we are the dominant brand in the lingerie and sexual health and wellness market, recognized for offering the highest quality products in a bright and comfortable store. | |

| · | Our unique customer experience. We combine top-of-the-line products, value and convenience with the distinctive environment and experience of a specialty retailer. Our well-trained sales personnel provide customized advice tailored to our customers' needs to ensure that customers walk out of our stores enlightened with new information, great ideas and fun products. We believe that our customer service strategy, convenient locations and attractive store design combine to create a unique shopping experience. | |

| · | Strong vendor relationships across product categories. We have strong, active relationships with over 70 vendors. We believe the scope of these relationships, which have taken years to develop, creates a significant impediment for other retailers to replicate our model. We work closely with our vendors to market both new and existing brands in a collaborative manner. | |

| · | Experienced Management Team. Our management team has over 150 years of combined experience in the retail market. |

Our Growth Strategy

We will strive to be a leading retailer of lingerie, sexual health and wellness products by pursuing the following growth strategies:

| ·

| Retail expansion strategy: In 2013, we re-engineered our new store design and layout to reflect our new retail concept, and in 2014 we began our new store expansion in earnest with the opening of five new stores. We have used these new stores to test and adjust the concept and new site selection criteria and process, and are now positioned to ramp up our new store buildout plans. We believe our new stores now feature d cor aligned with the shopping preference of today's modern women and couples. This foundation will allow us to scale our new store openings from five in 2014 to up to 50 or more stores on an annual basis in the future, if desired. As we increase our new store openings, we will need to add two additional headcount to our general and administrative expenses, to focus solely on site selection, store construction and maintenance, and will add one District Manager for every ten stores added.Each new store requires an initial cash outlay of approximately $260,000, for store buildout , fixture expenditures, initial inventory load-in and pre-opening expenses. | |

| ·

| Online retail expansion: We believe that the creation of a stronger online presence and more targeted focus on e-commerce and omni-channel retail will result in growth opportunities for our business. Increased focus on e-commerce will provide additional brand recognition and awareness for our brick and mortar stores. | |

| ·

| Expansion of private label business: We launched our SuteraTM Toys private label brand in 2012 and believe that it has been well-received by our customers. We plan to build brand recognition through SuteraTM print and online ads and to feature SuteraTM products in physical and online retail stores. | |

| ·

| Acquisition opportunities: Our market is primarily made up of small, regional players and represents a significant opportunity for expansion of store footprint through both greenfield store development in new markets and targeted acquisitions. Many regional and e-commerce companies exist both domestically and internationally. Acquisitions would allow us to quickly expand our geographic footprint into new and adjacent markets. |

| 4 |

Risks

Our business and our ability to execute our business strategy are subject to a number of risks of which you should be aware before you decide to buy our common stock. In particular, you should carefully consider the factors described in the section captioned "Risk Factors" beginning on page 10 of this prospectus and the following factors:

| · | the highly competitive nature of, and the increasing consolidation of, the lingerie, sexual health and wellness products industry; | |

| · | anticipating changes in consumer preferences and buying trends and managing our product lines and inventory; | |

| · | potential fluctuation in our same store sales and quarterly financial performance; | |

| · | our dependence upon manufacturers who may be unwilling or unable to continue to supply products to us; | |

| · | the possibility of material interruptions in the supply of products by our vendors or third-party distributors; | |

| · | products sold by us being found to be defective in labeling or content; | |

| · | compliance with laws and regulations or becoming subject to additional or more stringent laws and regulations; | |

| · | successfully identifying acquisition candidates and successfully completing desirable acquisitions; | |

| · | integrating acquired businesses; | |

| · | opening and operating new stores profitably; | |

| · | the impact of the health of the economy upon our business; | |

| · | protecting our intellectual property rights, particularly our trademarks; | |

| · | the risk that our products may infringe on the intellectual property rights of others; | |

| · | disruption in our information technology systems; | |

| · | the preparedness of our accounting and other management systems to meet financial reporting and other requirements and the upgrade of our existing financial reporting system; | |

| · | being a holding company, with no operations of our own, and depending on our subsidiaries for cash; | |

| · | after this offering, our executive officers, directors and principal stockholders, if they choose to act together, will continue to have the ability to control all matters submitted to stockholders for approval; |

| 5 |

| · | our substantial indebtedness; | |

| · | the possibility that we may incur substantial additional debt, including secured debt, in the future; | |

| · | restrictions and limitations in the agreements and instruments governing our debt; | |

| · | generating the significant amount of cash needed to service all of our debt and refinancing all or a portion of our indebtedness or obtaining additional financing; | |

| · | changes in interest rates increasing the cost of servicing our debt; | |

| · | the potential impact on us if the financial institutions we deal with become impaired; and | |

| · | the costs and effects of litigation. |

Our Corporate History and Background

We were incorporated in the State of Nevada on October 30, 2013 under the name Dico, Inc.

At the close of business on December 31, 2014, we entered into a securities exchange agreement, or the Exchange Agreement, with Christals Acquisition and its members, pursuant to which we acquired 100% of the issued and outstanding equity capital of Christals Acquisition in exchange for 2,524,870 shares of our common stock, par value $0.0001 per share, which constituted 70.5% of our issued and outstanding capital stock on a fully-diluted basis as of and immediately after the consummation of the transactions contemplated by the Exchange Agreement. In addition, at the closing of the share exchange, Christals paid us $350,000 in cash. This cash was immediately used for the following purposes (i) to pay down all of our outstanding liabilities, (ii) $308,436 of this cash was used as a partial payment toward the redemption of a total of 15,000,000 of our restricted shares from David Lazar, our former Chief Operating Officer and Secretary, pursuant to a redemption agreement that we entered into with Mr. Lazar on December 31, 2014, and (iii) to satisfy aggregate purchase price payable to holders of a total of 1,052,600 shares of our common stock, which shares were transferred to the members of Christals Acquisition as a condition to the closing of the exchange transaction. In addition to receiving the $308,436 payment for the redemption of his 15,000,000 shares of our common stock, we also transferred to Mr. Lazar our remaining inventory of loose diamonds pursuant to a bill of sale and assignment agreement as the balance of the consideration for the redemption of his shares. Immediately following the closing of the exchange transaction and the related transactions described above, the former members of Christals Acquisition and certain equity owners of such members who immediately received distributions of such securities, became the owners of 3,577,470 shares of our common stock, constituting 99.9% of our issued and outstanding common stock as of such closing. For accounting purposes, the exchange transaction with Christals Acquisition was treated as a reverse acquisition, with Christals Acquisition as the acquirer and Peekay Boutiques, Inc. as the acquired party.

As a result of our acquisition of Christals Acquisition, we now own all of the issued and outstanding equity capital of Christals Acquisition, a holding company, which in turn owns all of the equity capital of Peekay Acquisition and its several subsidiaries, which are engaged in the retail sale of lingerie, sexual health and wellness products.

Christals Acquisition was formed on January 3, 2012 for the purpose of acquiring all of the equity interests in each of the Christals Stores. The Christals Stores were comprised of several limited liability companies that operated as a retailer of lingerie, sexual health and wellness products. The acquisition of the Christals Stores was consummated on October 9, 2012. Thereafter, on December 31, 2012, Christals Acquisition, through its indirect subsidiary, Peekay SPA, acquired Peekay and ConRev, both of which operated as retailers of lingerie, sexual health and wellness products. Peekay was incorporated in the state of Washington on November 5, 1982. ConRev was incorporated in the state of Washington on December 29, 2004.

On January 23, 2015, we changed our name to Peekay Boutiques, Inc. to more accurately reflect our new business.

| 6 |

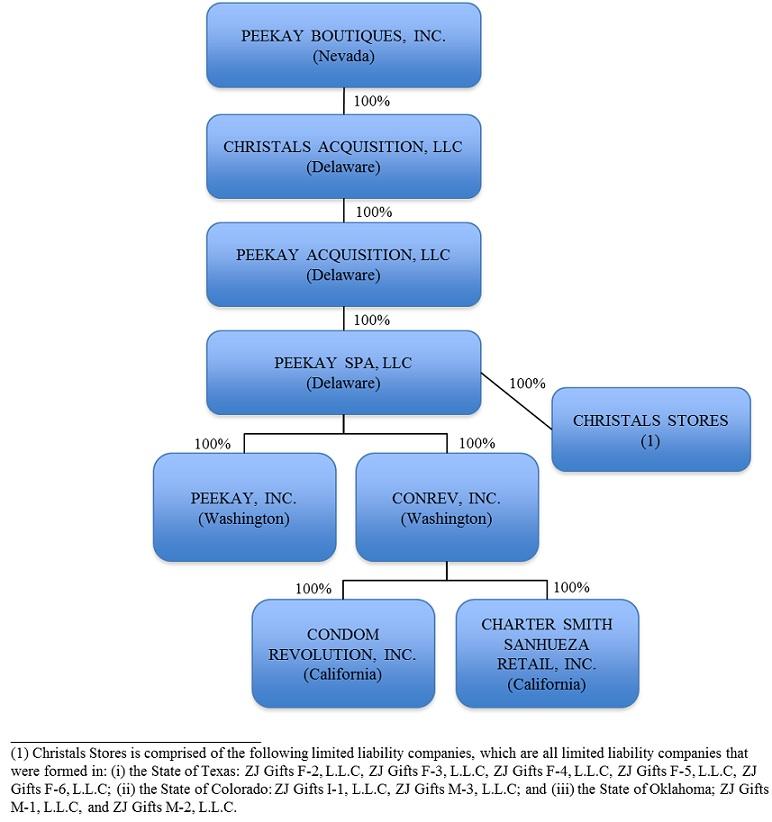

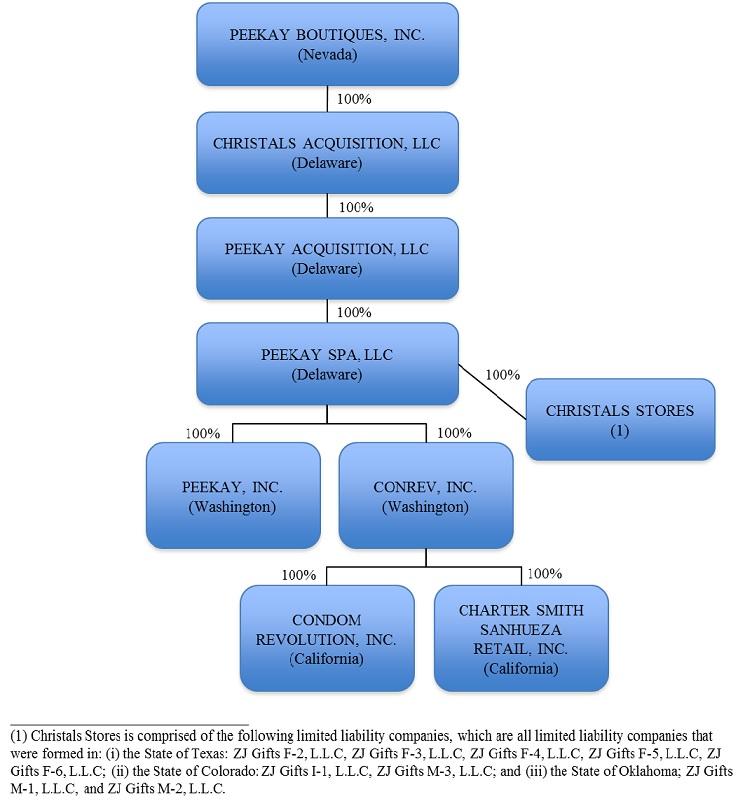

Our Corporate Structure

All of our business operations are conducted through our several operating subsidiaries. The chart below presents our corporate structure as of the date of this prospectus:

Our principal executive offices are located at 901 West Main Street, Suite A, Auburn, Washington 98001. The telephone number at our principal executive office is 1-800-447-2993.

| 7 |

THE OFFERING

| Common stock offered by us | [___] shares. |

| Common stock to be outstanding immediately after this offering | [___] shares. If the underwriter's over-allotment option is exercised in full, the total number of shares of common stock outstanding immediately after this offering would be [___]. |

| Over-allotment option | The underwriter has an option for a period of 45 days to purchase up to [___] additional shares of our common stock to cover over-allotments, if any. |

| Use of proceeds | We intend to use the net proceeds received from this offering for debt repayment, working capital and general corporate purposes. See "Use of Proceeds" on page 34. |

| Underwriter Compensation Warrants | We will issue to the underwriter, upon the closing of this offering, compensation warrants entitling the underwriter to purchase 3.0% of the aggregate number of shares of common stock issued in this offering, including shares issued pursuant to the exercise of the overallotment option. The underwriter warrants will have a term of five years and may be exercised commencing 12 months after the date of effectiveness of the Registration Statement on Form S-1 of which this prospectus forms a part. |

| Risk factors | See "Risk Factors" beginning on page 10 and the other information included in this prospectus for a discussion of factors you should carefully consider before investing in our securities. |

| No trading market | Our common stock is currently eligible to be quoted on the OTC Bulletin Board under the symbol "PKAY." However, there is currently no trading market for our common stock and there is no assurance that a regular trading market will ever develop. |

Unless we indicate otherwise, all information in this prospectus:

| · | is based on 3,582,470 shares of common stock issued and outstanding as of August 18, 2015; and | |

| · | assumes no exercise by the underwriter of its option to purchase up to an additional [___] shares of common stock to cover over-allotments, if any. |

See "Underwriting" for a full description of compensation payable to the underwriter.

Conventions Used in this Prospectus

Throughout this prospectus we use certain terms repeatedly. To assist you in reading and understanding the disclosure contained in this prospectus, please note the following frequently used terms, which, except as otherwise specified, have the meanings set forth below:

| ·

| "we," "us," "our," "our company," or the "Company" are to the combined business of Peekay Boutiques, Inc. (formerly Dico, Inc.) and its consolidated subsidiaries, Christals Acquisition, Peekay Acquisition, Peekay SPA, Peekay, Conrev, Condom Revolution, Charter Smith and the Christals Stores; | |

| · | "Christals Acquisition" are to Christals Acquisition, LLC, a Delaware limited liability company and a wholly-owned subsidiary of Peekay Boutiques, Inc.; | |

| · | "Peekay Acquisition" are to Peekay Acquisition, LLC, a Delaware limited liability company and wholly-owned subsidiary of Christals; | |

| · | "Peekay SPA" are to Peekay SPA, LLC, a Delaware limited liability company and the wholly-owned subsidiary of Peekay Acquisition; | |

| · | "Peekay" are to Peekay, Inc., a Washington corporation and wholly-owned subsidiary of Peekay SPA; | |

| · | "Conrev" are to Conrev, Inc., a Washington corporation and wholly-owned subsidiary of Peekay; | |

| · | "Condom Revolution" are to Condom Revolution, Inc., a California corporation and wholly-owned subsidiary of Conrev; | |

| · | "Charter Smith" are to Charter Smith Sanhueza Retail, Inc., a California corporation and wholly-owned subsidiary of Conrev; | |

| · | "Christals Stores" are to the following entities which each operate one store: ZJ Gifts F-2, L.L.C, ZJ Gifts F-3, L.L.C, ZJ Gifts F-4, L.L.C, ZJ Gifts F-5, L.L.C, ZJ Gifts F-6, L.L.C, ZJ Gifts I-1, L.L.C, ZJ Gifts M-1, L.L.C, ZJ Gifts M-2, L.L.C, and ZJ Gifts M-3, L.L.C.; | |

| · | "SEC" are to the Securities and Exchange Commission; | |

| · | "Exchange Act" are to the Securities Exchange Act of 1934, as amended; | |

| · | "Securities Act" re to the Securities Act of 1933, as amended; | |

| · | "U.S. dollars," "dollars" and "$" are to the legal currency of the United States. |

| 8 |

Summary Financial Data

The following table sets forth our summary statement of operations data for the fiscal years ended December 31, 2014 and 2013 derived from the audited financial statements of Christals Acquisition and the related notes included elsewhere in this prospectus. The summary financial data for the three months ended June 30, 2015 and 2014, and as of June 30, 2015, are derived from our unaudited financial statements appearing elsewhere in this prospectus and are not indicative of results to be expected for the full year. Our financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States. The results indicated below are not necessarily indicative of our future performance. You should read this information together with the sections entitled "Capitalization," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our financial statements and related notes included elsewhere in this prospectus.

| (In thousands of U.S. dollars, except for other operating data) |

| (Unaudited) Six Months Ended June 30, |

|

| Fiscal Year December 31, |

| ||||||||||

| Income Statement: |

| 2015 |

|

| 2014 |

|

| 2014 |

|

| 2013 |

| ||||

| Net revenue |

| $ | 21,203 |

|

| $ | 20,029 |

|

| $ | 39,625 |

|

| $ | 39,449 |

|

| Cost of goods sold |

|

| 7,595 |

|

|

| 6,834 |

|

|

| 13,740 |

|

|

| 13,640 |

|

| Gross profit |

|

| 13,608 |

|

|

| 13,195 |

|

|

| 25,885 |

|

|

| 25,809 |

|

| Selling, general & administrative expense |

|

| 10,993 |

|

|

| 10,349 |

|

|

| 20,964 |

|

|

| 19,570 |

|

| Depreciation and amortization |

|

| 1,546 |

|

|

| 979 |

|

|

| 2,199 |

|

|

| 1,902 |

|

| Operating income |

|

| 1,069 |

|

|

| 1,867 |

|

|

| 2,722 |

|

|

| 4,337 |

|

| Interest and other expense |

|

| 3,295 |

|

|

| 3,297 |

|

|

| 6,702 |

|

|

| 6,681 |

|

| Income tax expense |

|

| 47 |

|

|

| - |

|

|

| 202 |

|

|

| 233 |

|

| Net loss |

| $ | (2,273 | ) |

| $ | (1,430 | ) |

| $ | (4,182 | ) |

| $ | (2,577 | ) |

| Other operating data: | ||||||||

| Number of stores, beginning of period | 44 | 42 | ||||||

| Number of stores, end of period | 47 | 44 | ||||||

| Average selling square footage per store | 3,388 | 3,495 | ||||||

|

| As of June 30 , 2015 | |||||

|

| Actual |

|

| Pro Forma (1) (2) | ||

| Balance Sheet Data: |

|

|

|

|

| |

| Cash and cash equivalents |

| $ | 530 |

|

| $ |

| Total assets |

|

| 50,139 |

|

|

|

| Total liabilities |

|

| 58,446 |

|

|

|

| Total stockholders’ equity (deficit) |

|

| (8,306 | ) |

|

|

(1) Pro forma amounts give effect to the sale of the shares in this offering at the assumed initial public offering price of $[__] per share (the midpoint of the price range set forth on the cover page of this prospectus), and after deducting underwriting discounts and commissions and other estimated offering expenses payable by us.

A $1.00 increase (decrease) in the assumed initial public offering price of $[___] per share would increase (decrease) each of cash and cash equivalents, working capital, total assets, additional paid-in capital, and total stockholders' equity by $[___], assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same, and after deducting the estimated underwriting discounts and commissions.

(2) The pro forma data are illustrative only and will be adjusted based on the actual public offering price and other terms of this offering determined at pricing.

| 9 |

RISK FACTORS

An investment in our common stock involves a high degree of risk. You should carefully read and consider all of the risks described below, together with all of the other information contained or referred to in this prospectus, before making an investment decision with respect to our common shares or our company. If any of the following events occur, our financial condition, business and results of operations (including cash flows) may be materially adversely affected. In that event, the market price of our common shares could decline, and you could lose all or part of your investment.

RISKS RELATED TO OUR BUSINESS

Our auditor has raised substantial doubt about our ability to continue as a going concern. If we are unable to refinance our existing senior debt or otherwise raise capital, we may be forced to cease operations and liquidate.

Our financial statements have been prepared assuming that we will continue as a going concern, which contemplates the realization of assets and the liquidation of liabilities in the normal course of business. During 2013 and 2014, we incurred net losses of $2,577,263 and $4,181,890, respectively, largely as a result of interest expense on our outstanding debt of $6.6 million annually, which exceeds the operating profits generated through the operations of our business. Approximately $38.2 million in senior secured debt matures on December 31, 2015, and we do not have the resources necessary to pay this debt as it comes due. Our ability to continue our operations and execute our business plan is dependent on our ability to refinance this debt and/or to raise sufficient capital to pay this debt and other obligations as they come due (or are extended through a refinancing) and to provide sufficient capital to operate our business as contemplated. If we are unable to refinance our existing senior debt or raise equity capital we may have to cease operations and liquidate our assets and the holders of our equity may lose all or a significant portion of the value of their equity.

Our substantial indebtedness could adversely affect our financial condition.

We have a significant amount of indebtedness. As of December 31, 2014, our total debt was approximately $51 million.

Subject to the limits contained in our existing debt instruments, we may be able to incur substantial additional debt from time to time to finance working capital, capital expenditures, investments or acquisitions, or for other purposes. Due to the capital intensive nature of our business and our growth strategy, we expect that we will incur additional indebtedness in the future. If we do so, the risks related to our high level of debt could intensify. Specifically, our high level of debt could adversely affect our financial condition by, for example:

| · | making it more difficult for us to satisfy our obligations with respect to our existing debt; | |

| · | limiting our ability to obtain additional financing to fund future working capital, capital expenditures, acquisitions or other general corporate requirements; | |

| · | requiring a substantial portion of our cash flows to be dedicated to debt service payments instead of other purposes, thereby reducing the amount of cash flows available for working capital, capital expenditures, acquisitions and other general corporate purposes; | |

| · | increasing our vulnerability to general adverse economic and industry conditions; | |

| · | exposing us to the risk of increased interest rates as certain of our borrowings may be at variable rates of interest in the future; | |

| · | limiting our flexibility in planning for and reacting to changes in the industry in which we compete; | |

| · | placing us at a disadvantage compared to other, less leveraged competitors; and | |

| · | increasing our cost of borrowing. |

| 10 |

We may not be able to generate sufficient cash to service all of our indebtedness, and may be forced to take other actions to satisfy our obligations under our indebtedness, which may not be successful.

Our ability to make scheduled payments on or refinance our debt obligations, depends on our financial condition and operating performance, which are subject to prevailing economic and competitive conditions and to certain financial, business, legislative, regulatory and other factors beyond our control. We may be unable to maintain a level of cash flows from operating activities sufficient to permit us to pay the principal, premium, if any, and interest on our indebtedness.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we could face substantial liquidity problems and could be forced to reduce or delay investments and capital expenditures or to dispose of material assets or operations, seek additional debt or equity capital or restructure or refinance our indebtedness, including the notes. We may not be able to affect any such alternative measures, if necessary, on commercially reasonable terms or at all and, even if successful, those alternative actions may not allow us to meet our scheduled debt service obligations.

The terms of our existing debt contains certain restrictive covenants that could limit our operational flexibility, including our ability to open stores.

We have over $51 million total indebtedness, of which over $38 million is under a credit facility that has a term expiring in December 2015. Substantially all of our assets are pledged as collateral for outstanding borrowings under this credit facility. Outstanding borrowings under this facility and other unsecured notes bear interest at rates ranging from 9% to 15%. The credit facility agreement contains usual and customary restrictive covenants relating to our management and the operation of our business, including leverage and minimum cash covenants. Additional covenants limit our ability to grant liens on our assets, incur additional indebtedness, pay cash dividends and redeem our stock, enter into transactions with affiliates and merge or consolidate with another entity. These covenants could restrict our operational flexibility and any failure to comply with these covenants or our payment obligations would limit our ability to borrow under the credit facility and, in certain circumstances, may allow the lenders thereunder to require repayment.

We needed to obtain waivers from our secured lenders of our leverage ratio and minimum liquidity covenants and will likely require additional waivers of covenants in the future. If our secured lenders do not provide such waivers and if we are unable to refinance our secured debt on terms favorable to us, we could default on such debt, which would have potentially material adverse consequences.

During 2014, we obtained three covenant waivers through amendments to our financing agreements with our secured lenders, dated March 31, 2014, September 30, 2014 and December 31, 2014. These waivers cover covenant requirements through April 30, 2015. We expect that we will need additional covenant waivers in future periods. There can be no assurance that we will be able to obtain these or other waivers, or that we will continue to be in compliance with the terms and conditions of our debt agreements.

We obtained a fourth covenant waiver to the Financing Agreement under the Fourth Amendment to the Financing Agreement, dated June 30, 2015, for the period ending June 30, 2015.

Among other things, the Financing Agreement required:

(1) that we maintain a certain leverage ratio for each period of four fiscal quarters ending on June 30, 2015 and September 30, 2015; and (2) that we have liquidity of at least $1,500,000 at all times from June 30, 2015 through September 30, 2015 (the "Financial Covenants").

Pursuant to the Fourth Amendment, the lenders consented to, and waived any event of default relating to noncompliance with, the Financial Covenants, through September 30, 2015, subject to the following provisions:

| (1) | if any of our or other borrowers' or guarantors' Obligations (as defined in the Financing Agreement) remain outstanding as of November 15, 2015, then we and they must satisfy: |

| (i) | the original leverage ratio requirement under the Financing Agreement for the period of four fiscal quarters ending September 30, 2015 as set forth in Section 7.03(a) of the Financing Agreement, and | ||

| (ii) | the liquidity test at the end of the fiscal quarter ending September 30, 2015 as set forth in Section 7.03(b) of the Financing Agreement; and |

(2) we and the other borrowers and guarantors may not make certain Permitted Management Fee (as defined in the Financing Agreement) payments until the Financial Covenants have been satisfied and all Obligations of our Company and the other borrowers and guarantors and Commitments (as defined in the Financing Agreement) have been satisfied or terminated, but such Permitted Management Fees shall continue to accrue; and (3) we agreed to pay to the Administrative Agent (as defined in the Financing Agreement) an exit fee (the "Exit Fee"), for the account of each consenting lender, in an amount equal to the sum of 0.25% of the aggregate principal amount of the outstanding loans of such consenting lender, calculated on each of (i) the 15th day of July 2015 and the 15th day of each calendar month thereafter (if any Obligations remain outstanding on such day), and (ii) the last day of July and the last day of each calendar month thereafter (if any Obligations remain outstanding on such day). The Exit Fee is nonrefundable and deemed fully earned as of the 15th day and last day of each calendar month for the Exit Fee that accrues on such day and until paid shall constitute "Obligations" that are secured by "Collateral" (as defined in the Financing Agreement). The Exit Fee is due on the earlier to occur of (A) the Final Maturity Date (as defined in the Financing Agreement) and (B) the date which all of the other Obligations are repaid or required to be repaid in full in cash.

We expect that we will need additional covenant waivers in future periods.

There can be no assurance that we will be able to obtain additional waivers, or that we will continue to be in compliance with the terms and conditions of the agreements with our secured and other lenders. If we fail to obtain waivers or default on our secured debt, then our lenders may be able to accelerate such debt or take other action against us, which would have material adverse consequences on our financial condition and our ability to continue to operate.

We may need to raise additional funds to pursue our growth strategy, and we may be unable to raise capital when needed, which could have a material adverse effect on our business, financial condition, profitability and cash flows.

From time to time we may seek additional equity or debt financing to provide for capital expenditures and working capital consistent with our growth strategy. In addition, if general economic, financial or political conditions in our markets change, or if other circumstances arise that have a material effect on our cash flow, the anticipated cash needs of our business as well as our belief as to the adequacy of our available sources of capital could change significantly. Any of these events or circumstances could result in significant additional funding needs, requiring us to raise additional capital to meet those needs. If financing is not available on satisfactory terms or at all, we may be unable to execute our growth strategy as planned and our results of operations may suffer.

| 11 |

The health of the economy in the channels we serve may affect consumer purchases of discretionary items such lingerie, sexual health and wellness products, which could have a material adverse effect on our business, financial condition, profitability and cash flows. In addition, the recent global economic crisis and volatility in global economic conditions and the financial markets may adversely affect our business, financial condition, profitability, and cash flows.

Our results of operations may be materially affected by conditions in the global capital markets and the economy generally, both in the U.S. and internationally. Concerns over inflation, employment, tax laws, energy costs, healthcare costs, geopolitical issues, terrorism, the availability and cost of credit, the mortgage market, sovereign and private banking systems, sovereign deficits and increasing debt burdens and the real estate and other financial markets in the U.S. and Europe have contributed to increased volatility and diminished expectations for the U.S. and certain foreign economies. We appeal to a wide demographic consumer profile and offer an extensive selection of lingerie, sexual health and wellness products sold to retail consumers. Continued uncertainty in the economy could adversely impact consumer purchases of discretionary items across all of our product categories. Factors that could affect consumers' willingness to make such discretionary purchases include: general business conditions, levels of employment, interest rates, tax rates, the availability of consumer credit and consumer confidence in future economic conditions. In the event of a prolonged economic downturn or acute recession, consumer spending habits could be adversely affected and we could experience lower than expected net sales.

In addition, the recent global economic crisis and volatility and disruption to the capital and credit markets have had a significant, adverse impact on global economic conditions, resulting in recessionary pressures and declines in consumer confidence and economic growth. While these declines have moderated, the level of consumer spending is not where it was prior to the global recession, and economic conditions could lead to further declines in consumer spending in the future. Additionally, there can be no assurance that various governmental activities to stabilize the markets and stimulate the economy will restore consumer confidence or change spending habits. Reduced consumer spending could cause changes in customer order patterns and changes in the level of merchandise purchased by our customers, and may signify a reset of consumer spending habits, all of which may adversely affect our business, financial condition, profitability and cash flows.

Recent economic conditions have also resulted in a tightening of the credit markets, including lending by financial institutions, which is a source of capital for our borrowing and liquidity. This tightening of the credit markets has increased the cost of capital and reduced the availability of credit. Concern about the stability of the markets generally and the strength of counterparties specifically has led many lenders and institutional investors to reduce, and in some cases, cease to provide credit to businesses and consumers. These factors have led to a decrease in spending by businesses and consumers alike, and a corresponding decrease in global infrastructure spending. While global credit and financial markets appear to be recovering from extreme disruptions experienced over the past few years, uncertainty about continuing economic stability remains. It is difficult to predict how long the current economic and capital and credit market conditions will continue, the extent to which they will continue to recover, if at all, and which aspects of our products or business may be adversely affected. Current market and credit conditions could continue to make it more difficult for developers and landlords to obtain the necessary credit to build new retail centers. A significant decrease in new retail center development could limit our future growth opportunities as long as the aforementioned conditions exist.

Additionally, the general deterioration in economic conditions could adversely affect our commercial partners including our product vendors as well as the real estate developers and landlords who we rely on to construct and operate centers in which our stores are located. A bankruptcy or financial failure of a significant vendor or a number of significant real estate developers or shopping center landlords could have a material adverse effect on our business, financial condition, profitability, and cash flows.

We may be unable to compete effectively in our highly competitive markets.

The markets for lingerie, sexual health and wellness products are highly competitive with few barriers to entry even when economic conditions are favorable. We compete against a diverse group of retailers, both small and large, including regional and national department stores, specialty retailers, drug stores, mass merchandisers, Internet businesses, and catalog retailers. We believe the principal bases upon which we compete are the breadth of merchandise, our value proposition, the quality of our customers' shopping experience and the convenience of our stores as one-stop destinations for lingerie, sexual health and wellness products and services. Many of our competitors are, and many of our potential competitors may be, larger and have greater financial, marketing and other resources and therefore may be able to adapt to changes in customer requirements more quickly, devote greater resources to the marketing and sale of their products, generate greater national brand recognition or adopt more aggressive pricing policies than we can. As a result, we may lose market share, which could have a material adverse effect on our business, financial condition, profitability and cash flows.

| 12 |

If we are unable to stay abreast of trends in the lingerie, sexual health and wellness products market and react to changing consumer preferences in a timely manner, our sales will decrease.

We believe our success depends in substantial part on our ability to:

| · | create a warm and welcoming retail environment for individuals and couples to explore sexual wellness; | |

| · | recognize and define trends in lingerie, sexual health and wellness products; | |

| · | anticipate, gauge and react to changing consumer demands in a timely manner; | |

| · | translate market trends into appropriate, saleable product and service offerings in our stores in advance of our competitors; | |

| · | source, develop and maintain vendor relationships that provide us access to the newest merchandise on reasonable terms; and | |

| · | distribute merchandise to our stores in an efficient and effective manner and maintain appropriate in-stock levels. |

If we are unable to anticipate and fulfill the merchandise needs of the regions in which we operate, our net sales may decrease and we may be forced to increase markdowns of slow-moving merchandise, either of which could have a material adverse effect on our business, financial condition, profitability and cash flows.

If we fail to retain our existing senior management team or attract qualified new personnel, such failure could have a material adverse effect on our business, financial condition, profitability and cash flows.

Our business requires disciplined execution at all levels of our organization. This execution requires an experienced and talented management team. Lisa Berman was appointed as our Chief Executive Officer upon the consummation of the reverse acquisition on December 31, 2014. Janet Mathews was appointed Chief Financial Officer of Christals Acquisition effective April 2014 and became our Chief Financial Officer upon the closing of the reverse acquisition, and Bob Patterson was appointed as the Chief Information Officer of Christals Acquisition effective January 2013, was promoted to Chief Operating Officer of Christals Acquisition in October 2014 and became our Chief Operating Officer upon the consummation of the reverse acquisition. If we were to lose the benefit of the experience, efforts and abilities of key executive personnel, it could have a material adverse effect on our business, financial condition, profitability and cash flows. Furthermore, our ability to manage our retail expansion will require us to continue to train, motivate and manage our associates. We will need to attract, motivate and retain additional qualified executive, managerial and merchandising personnel and store associates. Competition for this type of personnel is intense, and we may not be successful in attracting, assimilating and retaining the personnel required to grow and operate our business profitably.

| 13 |

Our comparable store sales and quarterly financial performance may fluctuate for a variety of reasons, which could result in a decline in the price of our common stock.

Our comparable store sales and quarterly results of operations have fluctuated in the past, and we expect them to continue to fluctuate in the future. A variety of factors affect our comparable store sales and quarterly financial performance, including:

| · | general U.S. economic conditions and, in particular, the retail sales environment; | |

| · | changes in our merchandising strategy or mix; | |

| · | performance of our new and remodeled stores; | |

| · | the effectiveness of our inventory management; | |

| · | timing and concentration of new store openings, including additional human resource requirements and related pre-opening and other start-up costs; | |

| · | cannibalization of existing store sales by new store openings; | |

| · | levels of pre-opening expenses associated with new stores; | |

| · | timing and effectiveness of our marketing activities; | |

| · | seasonal fluctuations due to weather conditions; and | |

| · | actions by our existing or new competitors. |

Accordingly, our results for any one fiscal quarter are not necessarily indicative of the results to be expected for any other quarter, and comparable store sales for any particular future period may decrease. In that event, the price of our common stock would likely decline. For more information on our quarterly results of operations, see "Management's Discussion and Analysis of Financial Condition and Results of Operations."

We may not be able to sustain our growth plans and successfully develop and implement our long-range strategic and financial plan, which could have a material adverse effect on our business, financial condition, profitability and cash flows. In addition, we intend to continue to open new stores, which could strain our resources and have a material adverse effect on our business, financial condition, profitability and cash flows.

Our continued and future growth largely depends on our ability to implement our long-range strategic and financial plan and successfully open and operate new stores on a profitable basis. Our senior management is currently evaluating our long-range strategic and financial plan to align and prioritize our growth strategies, as well as additional investments that will be needed to support continued and future growth. There can be no assurance that we will be successful in implementing our growth plan or long-range strategic initiatives, and our failure to do so could have a material adverse impact on our business, financial condition, profitability and cash flows. During fiscal 2013, we opened 2 new stores and in fiscal 2014, we have opened 5 new stores with a sixth store opening in March 2015. We intend to continue to grow our number of stores for the foreseeable future. During fiscal 2014, the average investment required to open a typical new store, including inventory, was approximately $250,000. Our continued expansion places increased demands on our financial, managerial, operational, supply-chain and administrative resources. For example, our planned expansion will require us to increase the number of people we employ as well as to monitor and upgrade our management information and other systems and our distribution infrastructure. These increased demands and operating complexities could cause us to operate our business less efficiently and could have a material adverse effect on our business, financial condition, profitability and cash flows.

| 14 |

A reduction in traffic to, or the closing of, the other destination retailers in the shopping areas where our stores are located could significantly reduce our sales and leave us with unsold inventory, which could have a material adverse effect on our business, financial condition, profitability and cash flows.

As a result of our real estate strategy, most of our stores are located in off-mall shopping areas known as strip centers and power centers. Power centers typically contain three to five big-box anchor stores along with a variety of smaller specialty tenants and a strip center has two to six retail co-tenants. As a consequence of most of our stores being located in such shopping areas, our sales are derived, in part, from the volume of traffic generated by the other destination retailers and the anchor stores in the retail areas and power centers where our stores are located. Customer traffic to these shopping areas may be adversely affected by the closing of destination retailers or anchor stores, or by a reduction in traffic to such stores resulting from a regional or global economic downturn, a general downturn in the local area where our store is located, or a decline in the desirability of the shopping environment of a particular retail area. Such a reduction in customer traffic would reduce our sales and leave us with excess inventory, which could have a material adverse effect on our business, financial condition and results of operations. We may respond by increasing markdowns or initiating marketing promotions to reduce excess inventory, which would further decrease our gross profits and net income. This risk is more pronounced during the recent economic downturn that has resulted in a number of national retailers filing for bankruptcy or closing stores due to depressed consumer spending levels.

We may acquire entities with significant leverage, increasing the entity's exposure to adverse economic factors.

Our future acquisitions could include entities whose capital structures may have significant leverage. Although we will seek to use leverage in a manner we believe is prudent, any leveraged capital structure of such investments will increase the exposure of the acquired entity to adverse economic factors such as rising interest rates, downturns in the economy or deteriorations in the condition of the relevant entity or their industries. If an entity cannot generate adequate cash flow to meet its debt obligations, we may suffer a partial or total loss of capital invested in such entity. To the extent there is not ample availability of financing for leveraged transactions (e.g., due to adverse changes in economic or financial market conditions or a decreased appetite for risk by lenders); our ability to consummate certain transactions could be impaired.

We may not be able to successfully identify acquisition candidates or successfully complete desirable acquisitions.

In the past several years, we have completed multiple acquisitions and we intend to pursue additional acquisitions in the future. We actively review acquisition prospects, which would complement our existing lines of business, increase the size and geographic scope of our operations or otherwise offer growth and operating efficiency opportunities. There can be no assurance that we will continue to identify suitable acquisition candidates.

If suitable candidates are identified, sufficient funds may not be available to make such acquisitions. We compete against many other companies, some of which have greater financial and other resources than we do. Increased competition for acquisition candidates could result in fewer acquisition opportunities and higher acquisition prices. In addition, we are highly leveraged and the agreements governing our indebtedness contain limits on our ability to incur additional debt to pay for acquisitions. Additionally, the amount of equity that we can issue to make acquisitions or raise additional capital is severely limited. We may be unable to finance acquisitions that would increase our growth or improve our financial and competitive position. To the extent that debt financing is available to finance acquisitions, our net indebtedness could increase as a result of any acquisitions.

| 15 |

If we acquire any businesses in the future, they could prove difficult to integrate, disrupt our business or have an adverse effect on our results of operations.

Any acquisitions that we do make may be difficult to integrate profitably into our business and may entail numerous risks, including:

| · | difficulties in assimilating acquired operations, stores or products, including the loss of key employees from acquired businesses; | |

| · | difficulties and costs associated with integrating and evaluating the distribution or information systems and/or internal control systems of acquired businesses; | |

| · | difficulties in competing with existing stores or business or diverting sales from existing stores or business; | |

| · | expenses associated with the amortization of identifiable intangible assets; | |

| · | problems retaining key technical, operational and administrative personnel; | |

| · | diversion of management's attention from our core business, including loss of management focus on marketplace developments; | |

| · | adverse effects on existing business relationships with suppliers and customers, including the potential loss of suppliers of the acquired businesses; | |

| · | operating inefficiencies and negative impact on profitability; | |

| · | entering geographic areas or channels in which we have limited or no prior experience; and | |

| · | those related to general economic and political conditions, including legal and other barriers to cross-border investment in general, or by U.S. companies in particular. |

In addition, during the acquisition process, we may fail or be unable to discover some of the liabilities of businesses that we acquire. These liabilities may result from a prior owner's noncompliance with applicable laws and regulations. Acquired businesses may also not perform as we expect or we may not be able to obtain the expected financial improvements in the acquired businesses.

If we are unable to profitably open and operate new stores, our business, financial condition and results of operations may be adversely affected.

Our future growth strategy depends in part on our ability to open and profitably operate new stores in existing and additional geographic areas. In the U.S., the capital requirements to open a new store, including inventory, average approximately $250,000. We may not be able to open all of the new stores we plan to open and any new stores we open may not be profitable, either of which could have a material adverse impact on our financial condition or results of operations. There are several factors that could affect our ability to open and profitably operate new stores, including:

| 16 |

| · | the inability to identify and acquire suitable sites or to negotiate acceptable leases for such sites; | |

| · | proximity to existing stores that may reduce the new store's sales or the sales of existing stores; | |

| · | difficulties in adapting our distribution and other operational and management systems to an expanded network of stores; | |

| · | the level of sales made through our internet channels and the potential that sales through our internet channels will divert sales from our stores; | |

| · | the potential inability to obtain adequate financing to fund expansion because of our high leverage and limitations on our ability to issue equity under our credit agreements, among other things; | |

| · | difficulties in obtaining any governmental and third-party consents, permits and licenses; | |

| · | limitations on capital expenditures which may be included in financing documents that we enter into; and | |

| · | difficulties in adapting existing operational and management systems to the requirements of national or regional laws and local ordinances. |

In addition, as we continue to open new stores, our management, as well as our financial, distribution and information systems, and other resources will be subject to greater demands. If our personnel and systems are unable to successfully manage this increased burden, our results of operations may be materially affected.

We have identified material weaknesses in our internal control over financial reporting. If we fail to develop or maintain an effective system of internal controls, we may not be able to accurately report our financial results and prevent fraud. As a result, current and potential stockholders could lose confidence in our financial statements, which would harm the trading price of our common stock.

Companies that file reports with the SEC, including us, are subject to the requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or SOX 404. SOX 404 requires management to establish and maintain a system of internal control over financial reporting and annual reports on Form 10-K filed under the Exchange Act to contain a report from management assessing the effectiveness of a company's internal control over financial reporting. Separately, under SOX 404, as amended by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, public companies that are large accelerated filers or accelerated filers must include in their annual reports on Form 10-K an attestation report of their regular auditors attesting to and reporting on management's assessment of internal control over financial reporting. Non-accelerated filers and smaller reporting companies, like us, are not required to include an attestation report of their auditors in annual reports.

| 17 |

A report of our management is included under Item 9A "Controls and Procedures" of our annual report on Form 10-K filed as Exhibit 99.1 to our current report on Form 8-K/A filed on April 23, 2015. We are a smaller reporting company and, consequently, are not required to include an attestation report of our auditor in our annual report. However, if and when we become subject to the auditor attestation requirements under SOX 404, we can provide no assurance that we will receive a positive attestation from our independent auditors.

During its evaluation of the effectiveness of internal control over financial reporting as of December 31, 2014, management identified material weaknesses. These material weaknesses were associated with separation of duties, internal control process documentation and testing of controls. We are undertaking remedial measures, which measures will take time to implement and test, to address this material weakness. There can be no assurance that such measures will be sufficient to remedy the material weakness identified or that additional material weaknesses or other control or significant deficiencies will not be identified in the future. If we continue to experience material weaknesses in our internal controls or fail to maintain or implement required new or improved controls, such circumstances could cause us to fail to meet our periodic reporting obligations or result in material misstatements in our financial statements, or adversely affect the results of periodic management evaluations and, if required, annual auditor attestation reports. Each of the foregoing results could cause investors to lose confidence in our reported financial information and lead to a decline in our stock price. See Item 9A "Controls and Procedures" of our annual report on Form 10-K filed as Exhibit 99.1 to our current report on Form 8-K/A filed on April 23, 2015 for more information.

We depend upon manufacturers who may be unable to provide products of adequate quality or who may be unwilling to continue to supply products to us.

We do not manufacture any products we sell, and instead purchase our products from manufacturers and private label fillers. Since we purchase products from many manufacturers and fillers under at-will contracts and contracts which can be terminated without cause upon 90 days' notice or less, or which expire without express rights of renewal, manufacturers and fillers could discontinue sales to us immediately or upon short notice. In lieu of termination, a manufacturer may also change the terms upon which it sells, for example, by raising prices or broadening distribution to third parties. For these and other reasons, we may not be able to acquire desired merchandise in sufficient quantities or on acceptable terms in the future.

Although we plan to mitigate the negative effects resulting from potential unfavorable changes in our relationships with suppliers, there can be no assurance that our efforts will partially or completely offset the loss of these distribution rights. Any significant interruption in the supply of products by manufacturers and fillers could disrupt our ability to deliver merchandise to our stores and customers in a timely manner, which could have a material adverse effect on our business, financial condition and results of operations.

Manufacturers and label fillers are subject to certain risks that could adversely impact their ability to provide us with their products on a timely basis, including inability to procure ingredients, industrial accidents, environmental events, strikes and other labor disputes, union organizing activity, disruptions in logistics or information systems, loss or impairment of key manufacturing sites, product quality control, safety, and licensing requirements and other regulatory issues, as well as natural disasters and other external factors over which neither they nor we have control. In addition, our operating results depend to some extent on the orderly operation of our receiving and distribution processes, which depend on manufacturers' adherence to shipping schedules and our effective management of our distribution facilities and capacity.

If a material interruption of supply occurs, or a significant manufacturer or filler ceases to supply us or materially decreases its supply to us, we may not be able to acquire products with similar quality as the products we currently sell or to acquire such products in sufficient quantities to meet our customers' demands or on favorable terms to our business, any of which could adversely impact our business, financial condition and results of operations.

| 18 |

If products sold by us are found to be defective in labeling or content, our credibility and that of the brands we sell may be harmed, marketplace acceptance of our products may decrease, and we may be exposed to liability in excess of our products liability insurance coverage and manufacturer indemnities.